kzn planning and dev comm book 1

DESCRIPTION

ÂTRANSCRIPT

THE NATURE OF THE INTERNATIONAL, NATIONAL AND KWAZULU-NATAL RETAIL

AND SHOPPING CENTRE INDUSTRY

KwaZulu-Natal Planning & Development Commission

THE NATURE OF THE INTERNATIONAL, NATIONAL AND KWAZULU-NATAL RETAIL AND SHOPPING CENTRE INDUSTRY

First Published in 2010 by

KwaZulu-Natal Planning and Development CommissionPrivate Bag X9038Pietermaritzburg3200

ISBN: 978-0-621-39201-2

PRICE: R50.00

This document is available from:

KwaZulu-Natal Planning and Development Commission12th Floor Natalia Building 330 Langalibalele StreetPietermaritzburg3201

OR

Private Bag X9038Pietermaritzburg3200

Tel: 033 395 3067Fax: 033 345 3647Email: [email protected]: www.kznpdc.gov.za

The reproduction of the contents of this document, whether in whole or in part, for publication is prohibited unless permission is fi rst obtained in writing from the KwaZulu-Natal Planning and Development Commis-sion, Private Bag X 9038, Pietermaritzburg, 3200, KwaZulu-Natal, South Africa.

The contents of this publication, whilst being the views of the author, do not necessarily represent the views of the KwaZulu-Natal Planning and Development Commission.

1THE NATURE OF THE INTERNATIONAL, NATIONAL AND KWAZULU-NATAL RETAIL AND SHOPPING CENTRE INDUSTRY

CONTENT PAGEFOREWORD 3ACKNOWLEDGEMENTS 4EXECUTIVE SUMMARY 5

1. Introduction and main objectives 52. Methodology 53. Retail trends - International to KZN examples 64. Situation analysis 65. Changes in demographic and shopping behaviour 66. South Africa retail and shopping centre industry 67. Retail demand and supply: KZN 78. Participation of planning and development 79. Site selection and different levels of analysis 810. Strategic development guidelines and actions for existing and new shopping centre facilities 811. Major retail types, classifi cation of hierarchy of retail facilities 912. Proposed interaction between town planners, retail centre developers and local authority 1313. Use of the guideline document 1314. Site selection checklist for retail development 1315. Conclusion 14

1. BACKGROUND 152. DEFINITION OF RETAIL AND THEORETICAL CLASSIFICATION MODELS 16

2.1 Defi nition of Retailing 162.2 Theoretical base 18

2.2.1 Central Place Theory (Christaller 1933) 182.2.2 Gravitation Model (Reilly, 1930s) 192.2.3 Probability Model - Huff (1963) 192.2.4 A classifi cation of urban commercial structure (Berry, 1967) 20

2.3 International Classifi cation of Retail Facilities 212.3.1 Retail Classifi cation (Dawson, 1983) 212.3.2 International Council of Shopping Centre Classifi cation 242.3.3 Australian Property Council 262.3.4 Pan-European Shopping Centre Standard 27

2.4 South African Classifi cation of Retail Facilities 282.4.1 Oosthuizen (1981) 282.4.2 Kahn (1988) 30

3. INTERNATIONAL SHOPPING CENTRE EXAMPLES AND TRENDS 324. SOUTH AFRICAN LANDSCAPE INFLUENCING RETAIL DEVELOPMENT 34

4.1 Macro South African Economic Conditions 344.1.1 Gross Domestic Product 344.1.2 Interest rates 354.1.3 Infl ation 364.1.4 Rand/Dollar exchange rate 364.1.5 Building plans passed and completed 374.1.6 Various confi dence indexes 384.1.7 Retail trade sales 394.1.8 Global infl uence 404.1.9 Property Economic Indicators: (2006-2009) 40

4.2 Political Conditions 424.3 Social Conditions 42

2 THE NATURE OF THE INTERNATIONAL, NATIONAL AND KWAZULU-NATAL RETAIL AND SHOPPING CENTRE INDUSTRY

5. CHANGES IN DEMOGRAPHICS AND SHOPPING BEHAVIOUR 435.1 Population Growth 435.2 Effect of Urbanisation 435.3 Socio-Economic Change 44

5.3.1 Living Standard Measurement (LSM) 445.4 Emerging Black Market and Changing Consumer Base 465.5 Township Areas, CBDs and Rural Shopping Centres 47

5.5.1 Retail in CBDs 475.5.2 Retail in township areas 485.5.3 Retail in rural areas 48

5.6 Changing Lifestyles 495.7 The Need for a Shopping Experience 505.8 The Youth Market 505.9 Trends towards Extended Shopping Hours 505.10 Growth in Homeware Stores and other New Retail Tenant Types 505.11 E-Commerce 515.12 Renewal of Centres 515.13 Cannibalisation 51

6. SOUTH AFRICAN RETAIL AND SHOPPING CENTRE INDUSTRY 526.1 Retail Supply in South Africa 52

7. RETAIL DEMAND AND SUPPLY IN KWAZULU NATAL 547.1 Main Characteristics of KwaZulu Natal Market 547.2 Economic Base of KZN in comparison to the RSA Economy 54

7.2.1 Gross Domestic Product per region for 2007 547.3 Retail demand in KZN: Demand drivers 57

7.3.1 Population Numbers, Growth and Projections 577.3.2 Additional population related information regarding KZN 587.3.3 Socio-Economic and demographic profi le of KZN households 58

7.4 Monthly Expenditure on Consumer Goods 647.5 Estimated annual retail expenditure for KZN 65

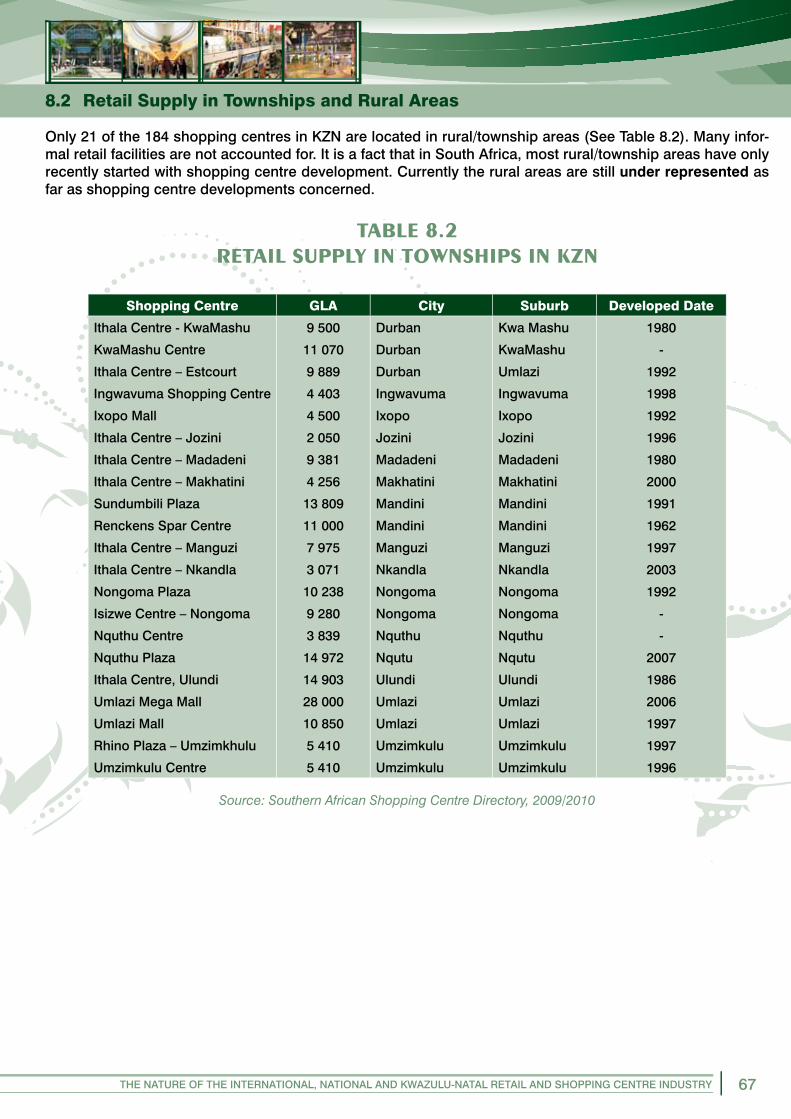

8. SUPPLY OF RETAIL SPACE IN KZN 668.1 Current Supply of Retail Space in KZN 668.2 Retail Supply in Townships and Rural Areas 678.3 Growth in Retail Supply in KZN (2003-2009) 688.4 Retail Development Potential in KZN 68

8.4.1 Retail apace per capita 698.4.2 Various other models 69

9. PARTICIPATION OF PLANNING AND DEVELOPMENT STAKEHOLDERS 709.1 Questionnaire Phase 709.2 Workshop 71

10. CONCLUSION 7311. TERMINOLOGY AND DEFINITIONS 7412. BIBLIOGRAPHY / REFERENCES 75

3THE NATURE OF THE INTERNATIONAL, NATIONAL AND KWAZULU-NATAL RETAIL AND SHOPPING CENTRE INDUSTRY

FOREWORDIn December 2008 the KwaZulu-Natal Planning and Development Commission (KZNPDC), appointed Urban Studies, to compile planning guidelines for shopping centre development in KwaZulu Natal. The project con-sisted of two components namely the understanding of retail development on an international, local and KZN level and to compile planning guidelines for future retail development.

Retail and shopping centre development forms part of one of the most dynamic urban markets and land uses. Shopping centres worldwide are continuously changing by trying to attract more shoppers to increase the drawcard and to increase the spending of their customers. There has been a substantial increase in planned shopping centres over the last 15 to 20 years, compared to the static situation as far as unplanned retail facili-ties are concerned.

A number of institutions like the International Council of Shopping Centres (ICSC) have published some guidelines for the classifi cation of shopping centres. Most of these publications are restricted to planned shopping centres only. In the case of this guideline report, the full spectrum of retail facilities ranging from metropolitan super regional centres to small rural village town squares, were included. There is a major need amongst town planners, developers, retailers and bankers to get a better understanding of the practical impli-cation of the classifi cation of shopping centres. This will streamline and regulate the development and control process of shopping centre development.

Shopping centres and retail markets in South Africa are all changing because of the growth in disposable income, the increase of the upper end of the market, the growth of the emerging market and the opening of a number of new retail facilities in township and rural areas. All role players (town planners, developers and retailers) need to understand these changes in order to have a better understanding as far as current and future shopping centre development is concerned.

All the different retail types ranging from planned metropolitan to unplanned rural facilities were discussed in detail in the guideline report. Each retail type was classifi ed according to its role and functions, market size and appropriate fl oor area. The locational criteria, a broad indication of the tenant mix and future trends and changes were incorporated for each retail type. Appropriate KwaZulu Natal examples were used in all cases.

The last part of the guideline document includes details regarding the interaction between town planners, shopping centre developers, and local authorities. These interaction guidelines were included to streamline the whole process of shopping centre development.

The dynamic nature of retail shopping centre development will always result in the provision of new retail types, the introduction of new types of retailers and the changing needs of shoppers. This will require an update of the guideline document on a regular basis to continuously obtain new information regarding the latest trends.

BISHOP MM MAKHAYECHAIRMAN

4 THE NATURE OF THE INTERNATIONAL, NATIONAL AND KWAZULU-NATAL RETAIL AND SHOPPING CENTRE INDUSTRY

ACKNOWLEDGEMENTSRetail is one of the most dynamic urban land uses to be found in any human settlement. This is also the one land use that changes almost on a daily basis. New retail types are developed to attract more customers and to better service their needs. To understand the retail market and to prepare a set of town planning guidelines a number of people contributed to this project, which I sincerely want to thank.

The success of this document is based on the major contribution made by the Commissioners of the Steering Committee: Christine Platt, Dr D.S. Rajah and Prof Michael Kahn.

A special word of thanks to Prof Kahn for his input, his past experience in formulating comprehensive clas-sifi cations for shopping centres and his general knowledge of the KZN market, added additional value to this guideline report.

A word of thanks to the Research Programme Coordinators from the Planning and Development Commis-sion, Mr Hloniphani Ngcobo and Mrs Priscilla Shanmugam for managing the project.

Other representatives attending the meetings were Sibusiso Dlamini a representative from the Natal branch of the South African Planning Institute, Mr Mark Poval representative from the Provincial Planning Department, Me Dorcas Zondi from the Ingonyama Trust Board and the retailer representatives Amanda Stops of the South African Council of Shopping Centres and Mr Greg Azzopardi from the Mr Price Group.

A special word of thanks to all the different stakeholders who completed the questionnaire and attended the workshop. Your contributions were valuable to fully understand the specifi c needs from the different Town Planning Departments.

Lastly I would like to thank the staff from Urban Studies who all made a very large contribution in compiling this guideline document. Your commitment and dedication is well appreciated.

This Guideline Document will defi nitely assist all future users to contribute to a more successful development of shopping centres for all the people of KwaZulu-Natal and to improve the lives of many people.

5THE NATURE OF THE INTERNATIONAL, NATIONAL AND KWAZULU-NATAL RETAIL AND SHOPPING CENTRE INDUSTRY

EXECUTIVE SUMMARY1. Introduction and main objectives

The Provincial Planning and Development Commission (PPDC) identifi ed the need for planning guidelines for shopping centre development. The original research dated back to 1951, 1978 and 1981. There has been growth in the demand and supply of shopping centre development in all types of settlements. New demands and new types of shopping facilities require a good understanding of the latest development trends in retail-ing.

Urban Studies was commissioned to undertake this study with the following main objections:

• To describe, in general terms, the nature of the South African shopping centre environment;

• To update and explain the hierarchy of shopping centre typology, using current, local and international examples;

• To formulate a new set of guidelines that can be applicable for different types of shopping centre develop-ments in different types of settlements. This will then vary from metropolitan areas and small towns, includ-ing rural settlements;

• To link the guideline document to specifi c retail development strategies;

• To identify the implications of the guideline document in terms of the socio economic impact centre devel-opment will have on job creation, the tax base and the total multiplier effect it will have on a community.

• To highlight areas where the guideline document could be misused; and

• To recommend the way forward as far as retail shopping centre development is concerned.

2. Methodology

This study was mainly based on three research components namely:

• A desk survey where existing sources of information where used (see reference list);

• To understand the status quo as far as retail development in concerned;

• A questionnaire was sent to some of the planning and development stakeholders in KZN. It was expected that these stakeholders would comment and add to a list provided to them focusing on trade area analy-sis, types of retail facilities, guideline actions and strategies;

• To guide the development process in terms of pre-consultation between town planning offi cials and devel-opers;

• This was followed by a workshop attended by 22 people to provide their detailed input insofar as the con-tent of the guideline document is concerned.

All this information culminated in a good understanding of the retail environment and to direct guidelines for future retail developments and redevelopment of existing developments.

6 THE NATURE OF THE INTERNATIONAL, NATIONAL AND KWAZULU-NATAL RETAIL AND SHOPPING CENTRE INDUSTRY

3. Retail trends - International to KZN examples

A large number of different shopping centre classifi cation models are in existence. Most of these models only include planned shopping centres.

The current document is the South African Shopping Centre Classifi cation Standards, prepared for the South African Council of Shopping Centres. The project focuses on planned shopping centre development and a new guideline document for KZN covering the whole spectrum from metropolitan through to rural areas.

4. Situation analysis

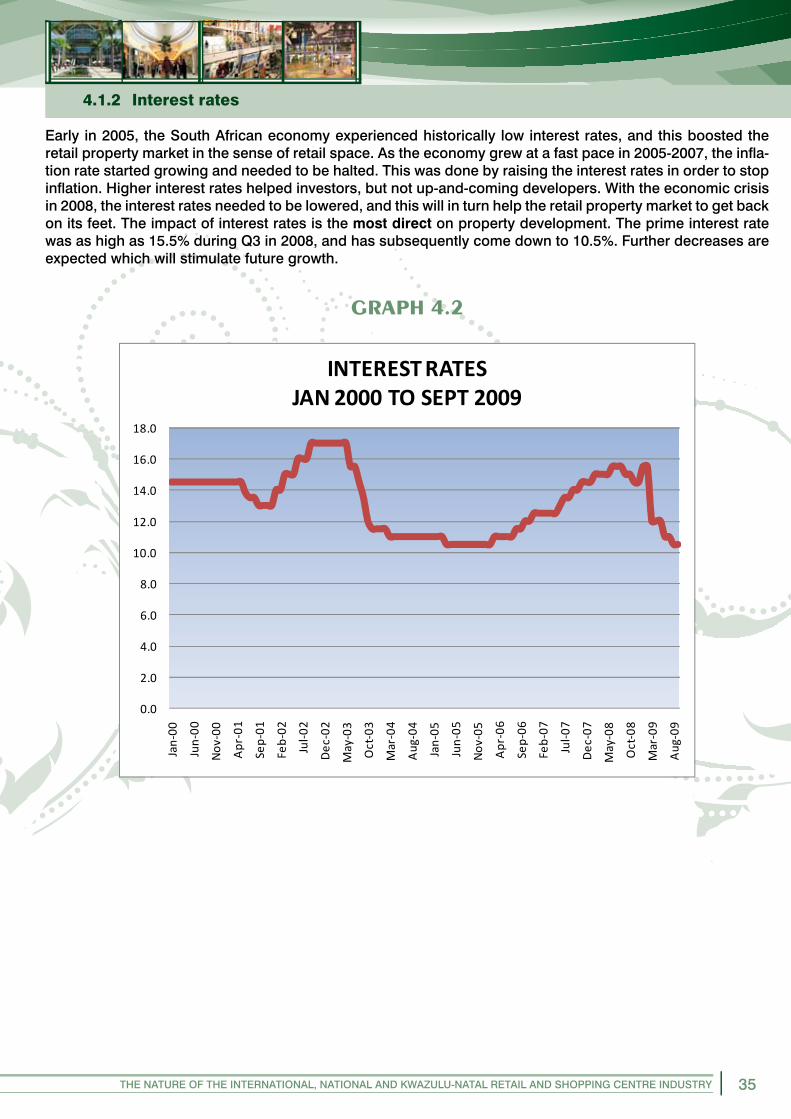

Retail development in the fi rst place, is infl uenced by macro economic conditions including aspects such as the gross domestic product (GDP) and interest rates. These two components of the economy has a major impact on property development, building plans passed and completed as well as retail trade sales. Macro economic conditions in South African have changed from very positive in 2006 to negative in 2008 with posi-tive changes in interest rates and infl ation during 2009.

5. Changes in demographic and shopping behaviour

The most important changes in the demographics of South Africa, which will infl uence retail “spend” and development, are:

• Population growth has slowed down to an annual increase of 1.5%, except that the number of foreigners living in South Africa is currently unknown;

• Increasing urbanisation will also increase the demand for retail facilities;

• Socio-economic changes, where especially the middle market as well as the upper end show major in-creases, with more disposable income to spend on retail products;

• The total “spend” by the different population groups clearly shows the increase in “spend” by the African market;

• CBD and Town Centre retail still focuses very strongly on the middle and lower LSM markets;

• The development of township shopping centres has shown tremendous growth since 2002;

• The growth in shopping centre development in rural areas is also substantial;

• Changes in lifestyle, the need for a shopping experience, the importance of the youth market, the open-ing of new retail format e-commerce and the renewal of shopping centres, all play a very important role to understand this dynamic and changing market.

6. South Africa retail and shopping centre industry

During the last 4 years South Africa and the world have experienced amongst the highest growth rates in re-cent decades. Shopping centre space has increased to 18 million m² representing ± 50% of all retail space in the country. This market has grown consistently with 8% during the last 15 years. The highest additional retail space has been added to the South African market in the four consecutive years since 2005.

7THE NATURE OF THE INTERNATIONAL, NATIONAL AND KWAZULU-NATAL RETAIL AND SHOPPING CENTRE INDUSTRY

7. Retail demand and supply: KZN

Retail demand and supply in KZN:

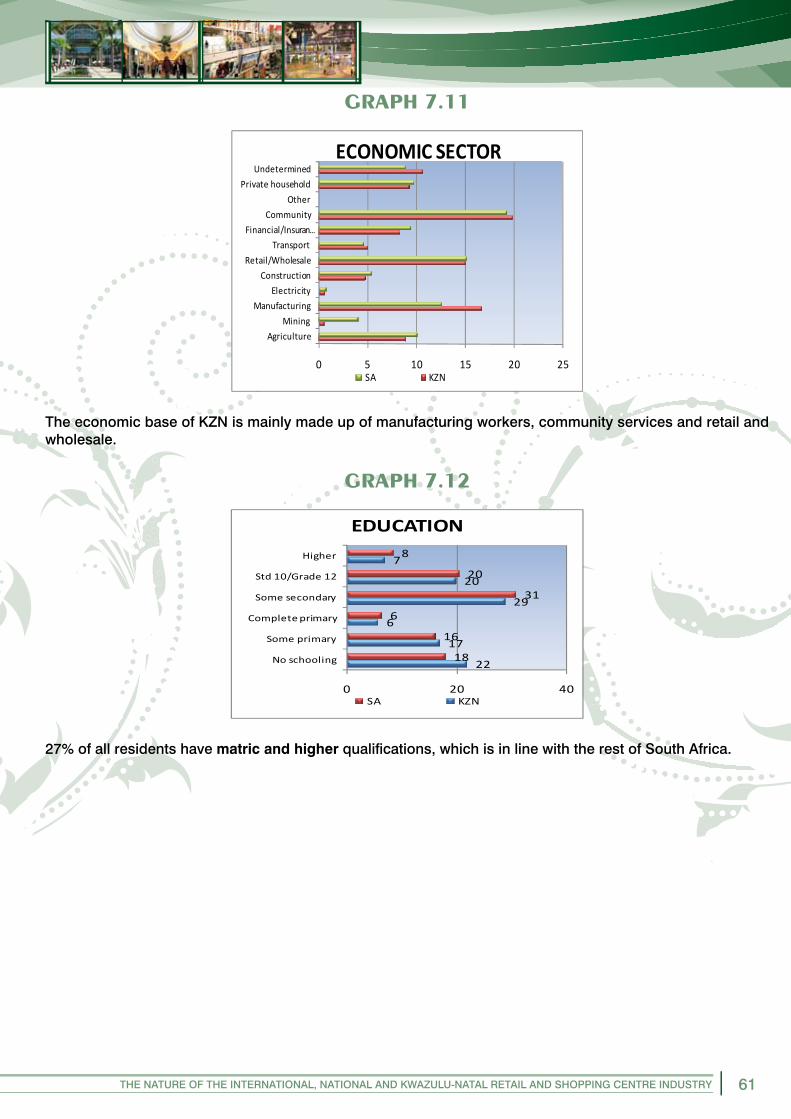

• The KZN GDP was growing over 5% per annum between 2003 and 2008;• KZN represents 16.2% of the total national GDP;• The contribution to KZN economy is mainly based on manufacturing, fi nance and real estates and whole-

sale and retail;• The latter clearly indicates how important retail development is for the province.

Population numbers, growth and projection

The total KZN population has increased from 9.4million in 2001 to 10.1million in 2008. KZN is in a strong sec-ond position with 20.8% of the total number of people in South Africa (second after Gauteng). It is expected that this population will grow to between 10.6 million and 11million people by 2015.

Socio economic and demographic profi le of KZN households

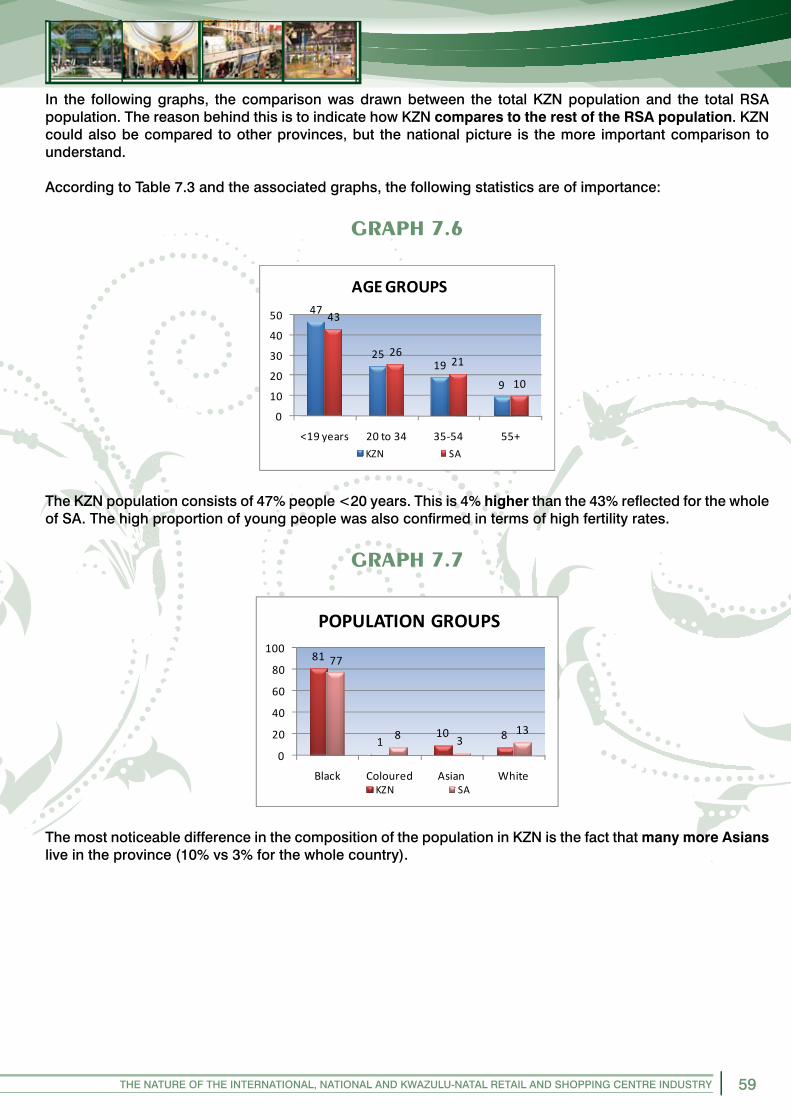

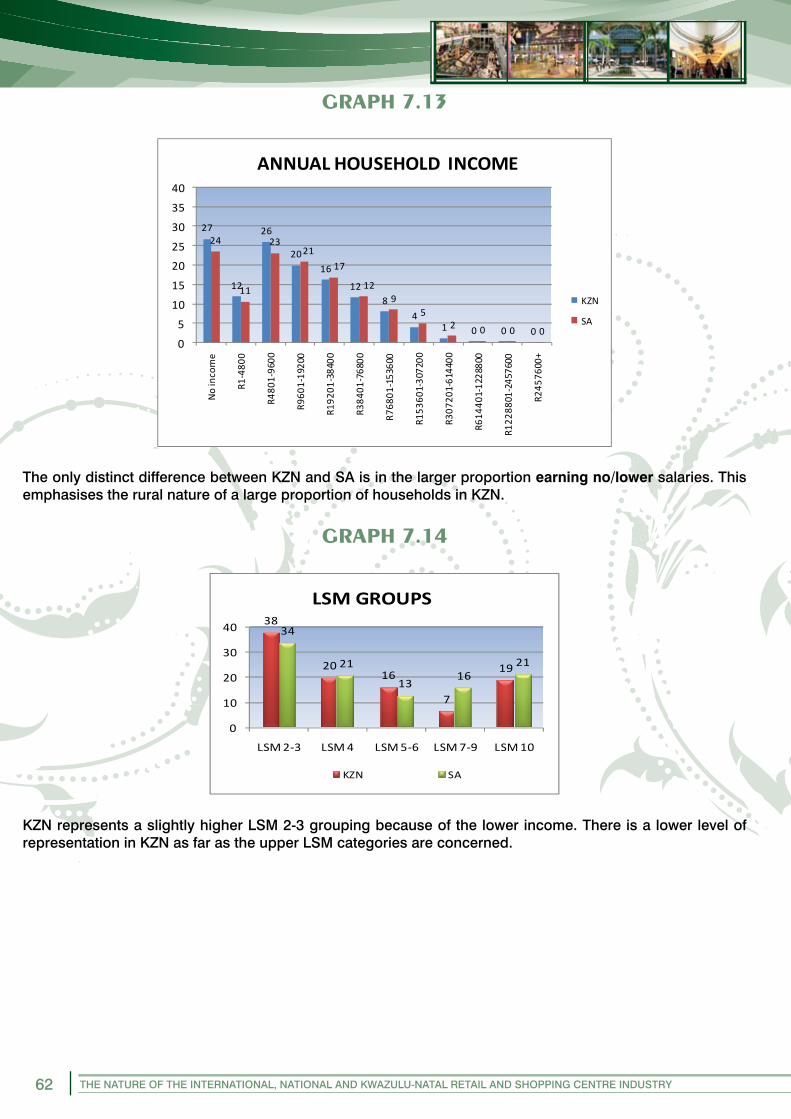

There are major resemblances between the KZN households and those of the South African Market. The major differences are a larger proportion of the younger cohorts in KZN, a strong rural character and fewer households in the upper LSM categories (LSM 7-10).

Estimated annual of retail expenditure for KZN

There are ±2.25mil households in KZN with a total spend on retail products of R79billion per annum. This represents 15% of the total retail spend which is in line with the GDP contribution of this province.

Retail supply in shopping centre facilities in the KZN is currently at 2.2mil m² and has increased annually by 9% since 2002. This clearly indicates the attractiveness of shopping centre development in the province. The total warranted retail fl oor space based on monthly expenditure for KZN is 5.2million m². This includes shop-ping centre space, unplanned retail space in metropolitan areas, small and medium sized towns, rural areas, as well as gaps that may exist in the market.

8. Participation of planning and development

This information was sent out to stake holders involved in a number of municipal and provincial planning departments. Specifi c comments were made to improve the guideline document.

A workshop was held during June 2009, and was attended by 22 people. Specifi c comments were made to fi ne tune the guidelines. All this was incorporated in the fi nal document.

8 THE NATURE OF THE INTERNATIONAL, NATIONAL AND KWAZULU-NATAL RETAIL AND SHOPPING CENTRE INDUSTRY

9. Site selection and different levels of analysis

The best approach to analyse different markets for retail development is from the macro to the micro loca-tions.

Area/Level Area Analysis/Key aspects to consider Main Objective

Macro

• Regions• Metropolitan areas, Cities, Towns and Rural areas• Population demographics• Competition• Growth

• Identify Gaps

Meso

• Primary trade areaEconomic growth rate of catchment areaTarget market of the centreExisting centres/competition

• Secondary trade area• Tertiary trade area• Demographic and socio-economic profi le of the area

• Identify Potential

Micro

Shopping Centre• Location• Pedestrian/traffi c fl ow• Accessibility• Visibility• Shape• Size• Topography• Utilities• Surrounding area

Specifi c Shop• Traffi c fl ow• Accessibility• Pedestrian volumes• Shop front• Parking• Competition

• Identify best location

10. Strategic development guidelines and actions for existing and new shopping centre facilities

The following broad action plans and guidelines for shopping centre development and re-development ex-ist.

Existing CBD/town centre retail

facilities

Existing suburban/township retail

facilities

Infi ll areasCBD/suburban/

township

Potential and new growth areas Greenfi elds

• Maintain• Upgrade• Redevelop/renew• Demolish• New-will become

more popular as existing facilities get older

• Maintain• Upgrade• Redevelop/renew• Expand• Demolish• Nodal/mixed use

• Develop new facilities

• Potential should be available

• Develop new facilities

• Potential must be noticeable/suffi cient

• ‘Follow the Roofs’

• ‘Follow the Roofs’

Time of implementation• Immediately• When necessary• Continuously• Suffi cient potential

Time of implementation• When necessary• Continuously

Time of implementation• Warranted potential• When necessary

Time of implementation• Enough potential• Future potential

Growth

Time of implementation• Expected new

growth• Enough

potential to warrant retail

9THE NATURE OF THE INTERNATIONAL, NATIONAL AND KWAZULU-NATAL RETAIL AND SHOPPING CENTRE INDUSTRY

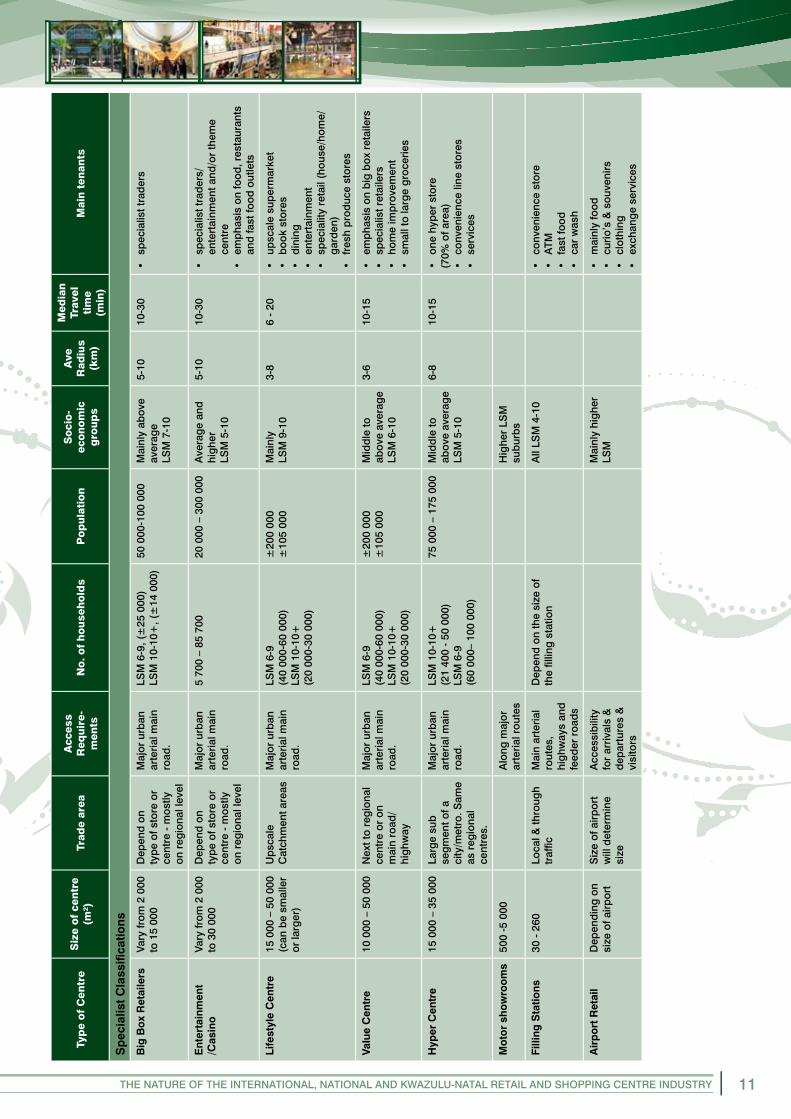

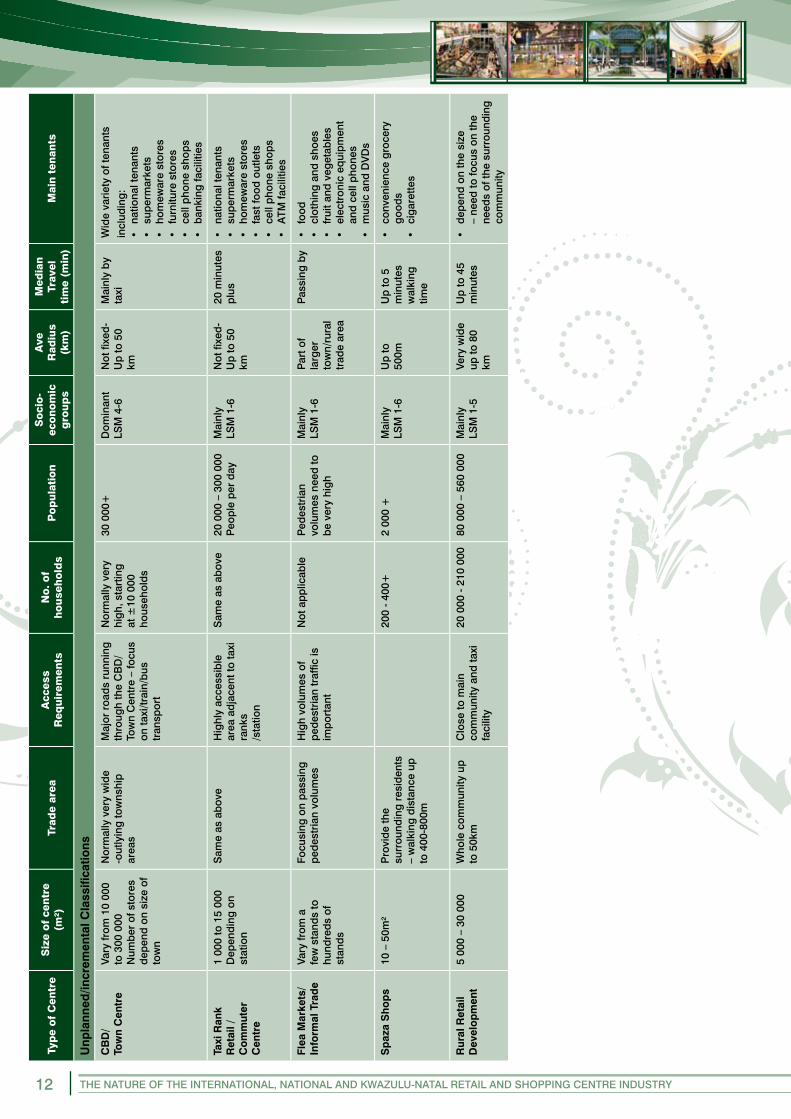

11. Major retail types, classifi cation of hierarchy of retail facilities

The whole spectrum of retail facilities consists of planned and unplanned retail types, each fulfi lling a specifi c role and function.

Planned Unplanned/Incremental Rural

Core Classifi cation• Small free standing-

convenience • Neighbourhood• Community• Small regional/large

community• Regional • Super Regional

Specialist• Big Box Retailers• Entertainment/casinos• Lifestyle• Value• Hyper• Motor showrooms and related facilities• Filling station stores• Airport

• CBD/town centre• Taxi rank retail/

commuter centre• Flea markets• Spaza shops• Fresh produce

markets• Informal trade

• Rural retail taxi orientated

• Town centres• Informal trade• Spaza shops• Planned

shopping centre

10 THE NATURE OF THE INTERNATIONAL, NATIONAL AND KWAZULU-NATAL RETAIL AND SHOPPING CENTRE INDUSTRY

SHO

PP

ING

CEN

TRE

CLA

SSIF

ICA

TIO

N

Typ

e o

f C

entr

eS

ize

of

cen

tre

(m²)

(GL

A)

Trad

e ar

eaA

cces

s R

equ

ire-

men

tsN

o. o

f h

ou

seh

old

sP

op

ula

tio

nS

oci

o-

eco

no

mic

g

rou

ps

Ave

Rad

ius

(km

)

Med

ian

Trav

el t

ime

(min

)M

ain

ten

ants

Co

re C

lass

ifi ca

tions

Sm

all f

ree

stan

din

g a

nd

conv

enie

nce

cent

re

500

– 5

000

5-25

sto

res

Ser

ves

par

t of a

su

bur

bs

Sub

urb

an s

tree

tLS

M 1

-5, (

<10

000

)LS

M 6

-9, (

<4

500)

LSM

10-

10+

, (<

2 00

0)

<40

000

<15

000

<7

000

All

LSM

g

roup

s1

– 1.

5<

3•

café

/Sup

eret

te•

few

con

veni

ence

sto

res

Nei

gh

bo

urh

oo

d

cent

re±

5 00

0-±

12 0

0025

-50

stor

esC

entr

ally

loca

ted

for

a g

roup

of s

ubur

bs

Maj

or c

olle

ctor

ro

ads

LSM

1-5

, (20

300

-47

000)

LSM

6-9

, (9

000-

20 1

00)

LSM

10-

10+

, (3

700-

8 60

0)

±13

5 00

0±

51 0

00±

18 5

00

All

LSM

4-1

02

4-9

• su

per

mar

ket

• co

nven

ienc

e•

som

e sm

all s

pec

ialis

ed s

tore

s

Co

mm

unity

ce

ntre

±12

000

-±25

000

50-1

00 s

tore

sS

trat

egic

ally

loca

ted

to

ser

ve a

sub

urb

an

com

mun

ity.

Maj

or a

rter

ial

road

LSM

1-5

, (44

000

-103

000

)LS

M 6

-9, (

20 0

00-4

6 00

0)

LSM

10-

10+

, (8

000-

19 0

00)

±29

5 00

0±

115

500

±41

000

All

LSM

4-1

03

6-14

• la

rge

sup

erm

arke

t•

conv

enie

nce

• sm

all n

atio

nal c

loth

ing

• re

stau

rant

s &

take

away

s•

serv

ices

Sm

all r

egio

nal/

Larg

e co

mm

unity

ce

ntre

±25

000

-±50

000

75-1

50 s

tore

sS

pec

ifi c

sub

-reg

ion

of c

ity (

can

be

larg

e se

lf co

ntai

ned

co

mm

unity

(i.e

. C

hats

wor

th)

Maj

or s

ubur

ban

ar

teria

l roa

d

linki

ng to

a

pro

vinc

ial

hig

hway

LSM

1-5

, (90

000

-209

000

)LS

M 6

-9, (

40 0

00-9

0 00

0)

LSM

10-

10+

(17

000

-38

000)

±60

0 00

0±

280

000

±83

000

All

LSM

4-1

05

10-1

6•

larg

e su

per

mar

ket

• 1

or 2

larg

e cl

othi

ng a

ncho

rs•

Str

ong

nat

iona

l ten

ant

com

par

ison

goo

ds

com

pon

ent

• b

outiq

ues

• re

stau

rant

s•

ente

rtai

nmen

t •

serv

ices

Reg

iona

l cen

tre

±50

000

-±10

0 00

015

0-25

0 st

ores

Larg

e re

gio

n of

city

/or

who

le c

ity/r

ural

to

wns

Maj

or a

rter

ial

road

usu

ally

a

Pro

vinc

ial m

ain

road

link

ing

to a

N

atio

nal r

oad

.

LSM

1-5

, (18

0 00

0-42

0 00

0)LS

M 6

-9, (

80 0

00-1

85 0

00)

LSM

10-

10+

(33

000-

76 0

00)

±1

200

000

±46

4 00

0±

165

000

All

LSM

4-1

08

14-2

0•

larg

e su

per

mar

ket (

even

2)/

or

hyp

er•

3 or

mor

e la

rge

clot

hing

• sm

all c

loth

ing

sto

res

and

b

outiq

ues

• en

tert

ainm

ent r

esta

uran

ts•

serv

ices

• co

nven

ienc

e

Sup

er r

egio

nal

cent

re>

100

000

Mor

e th

an 2

50

stor

es

Larg

e re

gio

n in

city

an

d s

urro

und

ing

ar

eas/

Tour

ists

Maj

or a

rter

ial

road

usu

ally

a

Pro

vinc

ial m

ain

road

, lin

king

to

a N

atio

nal r

oad

.

LSM

6-9

, (10

6 00

0-25

0 00

0)

LSM

10-

10+

(44

000-

101

000)

±62

3 00

0±

217

500

Ab

ove

aver

age

LSM

5-1

0

10+

24-3

0•

as a

t reg

iona

l but

mor

e em

pha

sis

on e

nter

tain

men

t and

va

riety

11THE NATURE OF THE INTERNATIONAL, NATIONAL AND KWAZULU-NATAL RETAIL AND SHOPPING CENTRE INDUSTRY

Typ

e o

f C

entr

eS

ize

of

cen

tre

(m²)

Trad

e ar

eaA

cces

sR

equ

ire-

men

tsN

o. o

f h

ou

seh

old

sP

op

ula

tio

nS

oci

o-

eco

no

mic

g

rou

ps

Ave

Rad

ius

(km

)

Med

ian

Trav

el

tim

e (m

in)

Mai

n t

enan

ts

Sp

ecia

list

Cla

ssifi

catio

ns

Big

Bo

x R

etai

lers

Vary

from

2 0

00

to 1

5 00

0D

epen

d o

n ty

pe

of s

tore

or

cent

re -

mos

tly

on r

egio

nal l

evel

Maj

or u

rban

ar

teria

l mai

n ro

ad.

LSM

6-9

, (±

25 0

00)

LSM

10-

10+

, (±

14 0

00)

50 0

00-1

00 0

00M

ainl

y ab

ove

aver

age

LSM

7-1

0

5-10

10-3

0•

spec

ialis

t tra

der

s

Ent

erta

inm

ent

/Cas

ino

Vary

from

2 0

00

to 3

0 00

0D

epen

d o

n ty

pe

of s

tore

or

cent

re -

mos

tly

on r

egio

nal l

evel

Maj

or u

rban

ar

teria

l mai

n ro

ad.

5 70

0 –

85 7

0020

000

– 3

00 0

00A

vera

ge

and

hi

ghe

rLS

M 5

-10

5-10

10-3

0•

spec

ialis

t tra

der

s/

ente

rtai

nmen

t and

/or

them

e ce

ntre

• em

pha

sis

on fo

od, r

esta

uran

ts

and

fast

food

out

lets

Life

styl

e C

entr

e15

000

– 5

0 00

0 (c

an b

e sm

alle

r or

larg

er)

Up

scal

eC

atch

men

t are

asM

ajor

urb

an

arte

rial m

ain

road

.

LSM

6-9

(40

000-

60 0

00)

LSM

10-

10+

(20

000-

30 0

00)

±20

0 00

0±

105

000

Mai

nly

LSM

9-1

03-

86

- 20

• up

scal

e su

per

mar

ket

• b

ook

stor

es•

din

ing

• en

tert

ainm

ent

• sp

ecia

lity

reta

il (h

ouse

/hom

e/g

ard

en)

• fr

esh

pro

duc

e st

ores

Valu

e C

entr

e10

000

– 5

0 00

0N

ext t

o re

gio

nal

cent

re o

r on

m

ain

road

/hi

ghw

ay

Maj

or u

rban

ar

teria

l mai

n ro

ad.

LSM

6-9

(40

000-

60 0

00)

LSM

10-

10+

(20

000-

30 0

00)

±20

0 00

0±

105

000

Mid

dle

to

abov

e av

erag

eLS

M 6

-10

3-6

10-1

5•

emp

hasi

s on

big

box

ret

aile

rs•

spec

ialis

t ret

aile

rs•

hom

e im

pro

vem

ent

• sm

all t

o la

rge

gro

cerie

s

Hyp

er C

entr

e15

000

– 3

5 00

0La

rge

sub

se

gm

ent o

f a

city

/met

ro. S

ame

as r

egio

nal

cent

res.

Maj

or u

rban

ar

teria

l mai

n ro

ad.

LSM

10-

10+

(21

400

- 50

000)

LSM

6-9

(60

000–

100

000

)

75 0

00 –

175

000

Mid

dle

to

abov

e av

erag

eLS

M 5

-10

6-8

10-1

5•

one

hyp

er s

tore

(7

0% o

f are

a)•

conv

enie

nce

line

stor

es•

serv

ices

Mo

tor

sho

wro

om

s50

0 -5

000

Alo

ng m

ajor

ar

teria

l rou

tes

Hig

her

LSM

su

bur

bs

Filli

ng S

tatio

ns30

- 26

0 Lo

cal &

thro

ugh

traf

fi cM

ain

arte

rial

rout

es,

hig

hway

s an

dfe

eder

roa

ds

Dep

end

on

the

size

of

the

fi llin

g s

tatio

nA

ll LS

M 4

-10

• co

nven

ienc

e st

ore

• A

TM•

fast

food

• ca

r w

ash

Air

po

rt R

etai

lD

epen

din

g o

n si

ze o

f airp

ort

Siz

e of

airp

ort

will

det

erm

ine

size

Acc

essi

bili

ty

for

arriv

als

&

dep

artu

res

&

visi

tors

Mai

nly

hig

her

LSM

• m

ainl

y fo

od•

curio

’s &

sou

veni

rs•

clot

hing

• ex

chan

ge

serv

ices

12 THE NATURE OF THE INTERNATIONAL, NATIONAL AND KWAZULU-NATAL RETAIL AND SHOPPING CENTRE INDUSTRY

Typ

e o

f C

entr

eS

ize

of

cen

tre

(m²)

Trad

e ar

eaA

cces

sR

equ

irem

ents

No

. of

ho

use

ho

lds

Po

pu

lati

on

So

cio

-ec

on

om

ic

gro

up

s

Ave

Rad

ius

(km

)

Med

ian

Trav

el

tim

e (m

in)

Mai

n t

enan

ts

Unp

lann

ed/in

crem

enta

l Cla

ssifi

catio

ns

CB

D/

Tow

n C

entr

eVa

ry fr

om 1

0 00

0 to

300

000

N

umb

er o

f sto

res

dep

end

on

size

of

tow

n

Nor

mal

ly v

ery

wid

e-o

utly

ing

tow

nshi

p

area

s

Maj

or r

oad

s ru

nnin

g

thro

ugh

the

CB

D/

Tow

n C

entr

e –

focu

s on

taxi

/tra

in/b

us

tran

spor

t

Nor

mal

ly v

ery

hig

h, s

tart

ing

at

±10

000

ho

useh

old

s

30 0

00+

Dom

inan

tLS

M 4

-6N

ot fi

xed

-U

p to

50

km

Mai

nly

by

taxi

Wid

e va

riety

of t

enan

ts

incl

udin

g:

• na

tiona

l ten

ants

• su

per

mar

kets

• ho

mew

are

stor

es•

furn

iture

sto

res

• ce

ll p

hone

sho

ps

• b

anki

ng fa

cilit

ies

Taxi

Ran

k R

etai

l /C

om

mut

er

Cen

tre

1 00

0 to

15

000

Dep

end

ing

on

stat

ion

Sam

e as

ab

ove

Hig

hly

acce

ssib

le

area

ad

jace

nt to

taxi

ra

nks

/sta

tion

Sam

e as

ab

ove

20 0

00 –

300

000

Peo

ple

per

day

Mai

nly

LSM

1-6

Not

fi xe

d-

Up

to 5

0 km

20 m

inut

es

plu

s•

natio

nal t

enan

ts•

sup

erm

arke

ts•

hom

ewar

e st

ores

• fa

st fo

od o

utle

ts•

cell

pho

ne s

hop

s•

ATM

faci

litie

s

Flea

Mar

kets

/In

form

al T

rad

eVa

ry fr

om a

fe

w s

tand

s to

hu

ndre

ds

of

stan

ds

Focu

sing

on

pas

sing

p

edes

tria

n vo

lum

esH

igh

volu

mes

of

ped

estr

ian

traf

fi c is

im

por

tant

Not

ap

plic

able

Ped

estr

ian

volu

mes

nee

d to

b

e ve

ry h

igh

Mai

nly

LSM

1-6

Par

t of

larg

er

tow

n/ru

ral

trad

e ar

ea

Pas

sing

by

• fo

od•

clot

hing

and

sho

es•

frui

t and

veg

etab

les

• el

ectr

onic

eq

uip

men

t an

d c

ell p

hone

s•

mus

ic a

nd D

VD

s

Sp

aza

Sh

op

s10

– 5

0m²

Pro

vid

e th

e su

rrou

ndin

g r

esid

ents

–

wal

king

dis

tanc

e up

to

400

-800

m

200

- 400

+2

000

+M

ainl

yLS

M 1

-6U

p to

50

0mU

p to

5

min

utes

w

alki

ng

time

• co

nven

ienc

e g

roce

ry

goo

ds

• ci

gar

ette

s

Rur

al R

etai

l D

evel

op

men

t5

000

– 30

000

Who

le c

omm

unity

up

to

50k

mC

lose

to m

ain

com

mun

ity a

nd ta

xi

faci

lity

20 0

00 -

210

000

80 0

00 –

560

000

Mai

nly

LSM

1-5

Very

wid

e up

to 8

0 km

Up

to 4

5 m

inut

es•

dep

end

on

the

size

–

need

to fo

cus

on th

e ne

eds

of th

e su

rrou

ndin

g

com

mun

ity

13THE NATURE OF THE INTERNATIONAL, NATIONAL AND KWAZULU-NATAL RETAIL AND SHOPPING CENTRE INDUSTRY

12. Proposed interaction between town planners, retail centre developers and local authority

The pre-application consultation should cover various aspects or issues such as:

• demographic and market study;• proven need and desirability;• traffi c impact assessment;• parking requirements;• provision for taxi rank and public transport facilities;• relevant land use zoning and development controls;• preliminary site development plan indicating aspects like ingress to and egress from the site, loading

zones, air-conditioning, signage, lighting, impact on adjacent properties and• the socio-economic impact of the development on the local community in terms of job creation, taxes and

the economic impact of such a development.

13. Use of the guideline document

The following 10 aspects are of critical importance:

• To understand the dynamic nature of a particular market;• The key aspect of retail facility viability remains a very good visible and accessible site;• Suffi cient people/households to warrant a specifi c size centre;• To make sure that most of the planned residential development for a new centre is occupied and that

households can spend money on retail products;• To be aware of cannibalisation of own stores;• To overestimate the potential, • To offer the right products to the target market;• To be aware of the size and strengths of competing facilities;• Not to over-build any centre ;and• To correctly time the project.

14. Site selection checklist for retail development

SITE SELECTION CHECKLIST FOR RETAIL DEVELOPMENT

Population Accessibility Competition

• Population size• Age profi le• Household size• Income levels• Disposable income per capita• Occupation classifi cations• Seasonal fl uctuations• Housing numbers• Housing age/type• Current shopping patterns• LSM Groups

• Pedestrian fl ow• Pedestrian entry routes• Public transport• Types of transport• Ease of use• Car ownership levels• Road network• Conditions and roads• Driving speeds• Congestion• Restrictions• Plans to upgrade• Parking facilities/requirements• Capacity- road• Convenience• Visibility

• Existing retail activity• Direct competitors• Indirect competitors• Anchor stores• Trade areas• Age of outlets• Competitive potential• Outlet expansion• Refurbishment• Vacant sites• Interception• Repositioning• Competitor policy• Cannibalisation

* Source: McGoldrich, 1990 (adjusted)

14 THE NATURE OF THE INTERNATIONAL, NATIONAL AND KWAZULU-NATAL RETAIL AND SHOPPING CENTRE INDUSTRY

15. Conclusion

Retailing is very dynamic, with changes on a regular basis. The above mentioned must be seen as broad guidelines which will answer most questions insofar as retail development is concerned.

Market and economic forces, as well as a good location, will in most cases, result in sustainable retail devel-opment and satisfying the needs of the customers.

15THE NATURE OF THE INTERNATIONAL, NATIONAL AND KWAZULU-NATAL RETAIL AND SHOPPING CENTRE INDUSTRY

THE NATURE OF THE INTERNATIONAL, NATIONAL AND KWAZULU NATAL RETAIL AND SHOPPING CENTRE

INDUSTRY1. BACKGROUND

The old marketplace has been replaced by shopping centres. The purpose of shopping centres is to satisfy the needs of customers through the provision of the required retail products. There are also other needs which become part of this ‘new marketplace’, such as entertainment, providing specifi c services, and allow-ing people to socialise.

There are different needs that should be satisfi ed and therefore different sizes and types of shopping cen-tres develop. Each type of store has its own threshold value, indicating the minimum number of people and disposable income required, to be viable. Some stores require fewer households, while others require a very large population to operate. This results in a defi nite hierarchy of shopping centres, which operates and func-tions according to the different environments.

Retail development in South Africa is strongly infl uenced by what is happening worldwide. Current worldwide economic conditions are also impacting on the retail sector in South Africa. It is therefore of utmost impor-tance to understand global economic trends, and the impact on retail development.

Retail development is also infl uenced by changes in demographics, income and shopping behaviour. The specifi c impact of all these aspects will also be highlighted to get a better understanding of the KZN situa-tion.

This report consists of two very clear sections:

1. A broad overview of the theoretical aspects associated with retail and shopping centre development locally and internationally, and

2. To focus on retail demand and supply in KZN.

Section 1 of the report focused on the following:

• The international and local understanding and classifi cation of retail and shopping centre facilities. This theoretical approach formed a broad based understanding of shopping centre development.

• To address international trends insofar as shopping centre development is concerned.

• To evaluate the broader environment in which retail in South Africa operates.

The latter will focus on the following:

- macro-economic conditions,

- the political situation,

- social changes and development.

- the retail market in South Africa with specifi c reference to the national supply and demand of shopping centre facilities, and

- The way in which changes in shopping behaviour infl uence the demand for shopping facilities.

16 THE NATURE OF THE INTERNATIONAL, NATIONAL AND KWAZULU-NATAL RETAIL AND SHOPPING CENTRE INDUSTRY

All this culminates in a good understanding of the macro environment, before focusing on KZN in particular.

The main objectives of the second section where the focus is on KZN, are:

• to get a clear understanding of the economic base of the province;• to indicate the current demand of all retail space as infl uenced by household numbers, socio-economic

profi les and disposable income;• to give an indication of the current supply of retail space in KZN with specifi c reference to shopping centre

space, and• to focus on the identifi cation of guideline parameters that would form the basis for the fi nal guideline

document. In this regard, input was received from a number of stake holders, as well as during a workshop held in Durban.

2. DEFINITION OF RETAIL AND THEORETICAL CLASSIFICATION MODELS

This section focuses on the following:

• a defi nition of retailing;

• a detailed understanding of the theoretical base for the existence of a hierarchy of shopping centres;

• to indicate historical and current international and local shopping centre classifi cation methods, and

• to give a brief description of shopping centre development trends in the rest of the world, with specifi c reference to Africa and other developing countries.

2.1 Defi nition of Retailing

The defi nition of retailing, as it will be used throughout this report, embraces the following:“All activities connected with the selling of goods and services to the end consumer”. Retail transactions, however, do not take place on business premises only. A clear differentiation will be drawn. The most impor-tant components of retail will include the following: (Diagram 2.1)

• type of ownership• the type of merchandise sold• type of business• the location• physical structures.

17THE NATURE OF THE INTERNATIONAL, NATIONAL AND KWAZULU-NATAL RETAIL AND SHOPPING CENTRE INDUSTRY

DIAGRAM 2.1DIFFERENT COMPONENTS OF RETAIL

Independent/Franchise

chain

Owned by manufacturer

Type of ownershipOwned by government

Owned by farmer

Owned by public company

Owned by consumer

Type of merchandise Variety

Motor dealers

Furniture & appliances

Clothing & accessories

Type of businessPharmacy & patent medicines

Eating and drinking places

Differentclassifi cations

Food stores

Service stations

General dealers

Service outlets

Entertainment

Distinguish: rural through to metropolitanCentral business district

LocationShopping centres

Individual centres/free standing(hierarchy of centres)

Strip/value

Mail orders

Non-store tradeElectronic in-house purchase

Telesales

Internet shopping

Source: Mason, et al., 1988:22 (adjusted for 2009).

18 THE NATURE OF THE INTERNATIONAL, NATIONAL AND KWAZULU-NATAL RETAIL AND SHOPPING CENTRE INDUSTRY

A large portion of the retail facilities in KZN is represented as part of a rural environment and therefore it is important from a geographical point of view to clearly distinguish between metropolitan and rural retail fa-cilities. The following characteristics are typical of rural areas:

• population numbers are in many instances small and spread over a very wide geographical area;• population densities are much lower, impacting on the size of the catchment area;• mainly part of the lower LSM*1 groups compared to the middle and upper income groups in the metropoli-

tan areas;• transport facilities comprise taxi versus private transport;• lower car ownership;• higher levels of unemployment;• no major other supporting employment facilities. In some cases trading activities would be a stimulus for

higher employment fi gures and higher household income.

2.2 Theoretical base

It is necessary to briefl y examine some of the theoretical models that were developed to explain the distribu-tion of retail facilities, and more specifi c shopping centres and their trade areas. A summary is given of the most important theoretical models that highlight and explain the existence of a hierarchy of shopping facili-ties.

2.2.1 Central Place Theory (Christaller 1933)

It is regarded that the central place theory is the basis for most of the classifi cations that have been developed in the western world, subsequent to the original study in 1933. There are many points of critique regarding this model, but there are a few important aspects that do apply in the evaluation of any shopping centre hierarchy.

The Central Place Theory is based on two very important fundamental concepts namely:

• Threshold population - this is the minimum population which is required to bring about the offering of certain goods for sale, or to sustain any service. In economic terms it means the minimum demand to make such an offering viable. A detailed discussion of this concept will be covered later in this document.

• Range of goods and service - this is the maximum distance which people will travel to purchase goods and derive a service offered at a central place.

All this resulted in a hierarchy of central places, each with its own appropriate size shopping facility.

The basic principle of a hierarchy of shopping opportunities is also applicable to an understanding of the hierarchy of retail centres within the city. The intra-urban hierarchy of shopping centres would range from the isolated street corner grocery store to the neighbourhood, community and super regional shopping centre.

1 * See Section 4.3.1 for a detailed explanation of the different LSM categories.

19THE NATURE OF THE INTERNATIONAL, NATIONAL AND KWAZULU-NATAL RETAIL AND SHOPPING CENTRE INDUSTRY

2.2.2 Gravitation Model (Reilly, 1930s)

The gravity model was based to a large extent on Newton’s Law of Gravitation where a force exists be-tween two bodies, and that force depends on the size (mass) of each of the bodies.

Reilly started to apply this model to measure the retail trade areas of cities in the 1930s. The main as-pects of his theory were as follows:

• population of and distance between two cities (centres) are the only variables used;

• cities of equal size would have a trade area boundary midway between them;

• if the centres are of unequal size the boundary would be nearer to the smaller city.

This model is very rigid, taking only two variables namely size and distance into account. It does how-ever provide an important base for any hierarchy to illustrate the forces that are active between certain shopping centres. The situation is however much more complex in reality.

2.2.3 Probability Model - Huff (1963)

The Huff model incorporates the conceptual framework of Reilly and other gravity models but focuses on the spatial behaviour of consumers. This model is based on two fundamentals:

• the size of a shopping centre• travel time to the centre.

The fundamental argument is as follows:

• the larger the centre, the more variety is offered and the greater the consumers’ expectation would be of a successful shopping trip;

• travel time is related to the utility of the shopping centre. The further the customer lives from the centre, the less likely the trip to the centre would be.

The unique feature of the Huff model is the generation of probability surface. Customers living close to the centre will have a high probability of supporting the centre. As distance increases from the centre, the probability decreases. This model can be used to delineate trade areas by determining equal prob-ability contours to two or more centres. A 50% or 60% contour is used to delineate a trade area.

An important notion of this model is the fact that the customer behaviour in urban areas is fl exible and complex, not rigid, and that shopping behaviour is governed by choice.

A shopper could thus support a variety of centres for goods and services offered at a particular centre if not available from another centre.

20 THE NATURE OF THE INTERNATIONAL, NATIONAL AND KWAZULU-NATAL RETAIL AND SHOPPING CENTRE INDUSTRY

2.2.4 A classifi cation of urban commercial structure (Berry, 1967)

This classifi cation forms the basis for our understanding of the different types and hierarchy of shop-ping centres.

Berry developed a broad classifi cation of retail facilities. He identifi ed three main components, namely: (see Diagram 2.1)

• centres• ribbons • specialised areas.

Shopping centres demonstrate a hierarchical arrangement with a 2low-order isolated convenience store (small grocery store) and a neighbourhood centre, both offering low order and a few 3higher-order facilities (variety of clothing and household stores). At the regional level the most specialised stores, as well as department stores are represented.

Ribbon developments incorporate those retail and service functions mainly orientated to vehicular traf-fi c, including fi lling stations, fast-food restaurants, motorcar dealers, tyre dealers, nurseries and other similar operations. These functions serve demand created by motorcar customers. Arterial streets with the highest vehicular traffi c volume are the most densely developed. The intersections of two or more major arterials have higher development intensity. Some commercial ribbon streets stretch for kilome-tres.

Large metropolitan areas also contain specialised function areas. These are characterised by motorcar showrooms and professional offi ce clusters (doctors, dentists and lawyers). Specialised function areas require good accessibility, because they draw customers from the entire metropolitan area.

This classifi cation remains the most suitable today to describe the retail landscape, and is especially appropriate to explain the hierarchy of shopping centres.

2 Low order facility refers to a product/store visited frequently for daily use/consumption3 A higher order facility refers to a product/store that needs a large number of people to warrant the existence of such a facility.

21THE NATURE OF THE INTERNATIONAL, NATIONAL AND KWAZULU-NATAL RETAIL AND SHOPPING CENTRE INDUSTRY

DIAGRAM 2.2

CENTRES RIBBONS SPECIALISED AREAS

Planned or Unplanned

Traditional Shopping Street Automobile Rows

Convenient

Urban Arterial Printing DistrictsNeighbourhood

Community New Suburban Ribbon Entertainment Districts

RegionalHighway Oriented

Planned or Unplanned Plaza

Exotic MarketsMetropolitan CBD

Furniture Districts

Medical CentresPlanned

Unplanned

Source: Berry, 1988

Note: Berry has not indicated any specifi c sizes for the different types of centres.

2.3 International Classifi cation of Retail Facilities

The main reason for including a variety of international classifi cation models is as follows:

• to indicate their approaches, trends and similarities; and• to learn from these classifi cations and to eventually indicate the difference as far as South Africa is con-

cerned.

2.3.1 Retail Classifi cation (Dawson, 1983)

Dawson developed his hierarchy (Table 2.1) which was an expansion of the traditional classifi cation of the neighbourhood, community and regional centre in 1983.

22 THE NATURE OF THE INTERNATIONAL, NATIONAL AND KWAZULU-NATAL RETAIL AND SHOPPING CENTRE INDUSTRY

TABLE 2.1SHOPPING CENTRE CLASSIFICATION

(DAWSON 1983)

The Structure of the Shopping Hierarchy

1. General Purpose of Free Standing Shopping Centres(or the 4 Suburban levels of the basic hierarchy) with subtypes of:• Local Convenience• Neighbourhood• Community• Regional • Super-Regional which may be added to the top of these sub-types

2. General Purpose of Renewal Centres (with three subtypes that occur within any of those in category 1, as well as the CBD):• Infi ll centre• Extension centre• Core replacement centreAlongside the general purpose shopping centres are the remaining categories, 3 - 6.

3. Multi-use Shopping Centres1

Here social, offi ce and other facilities are integrated with the shopping provision of the basic hierarchy.

4. Speciality, Theme or Festive Shopping Centres (with sub-types of the following):• High order comparison purpose-built speciality centres, such as fashion or tourist centres in high income

areas.• Speciality or theme centres developed in recycled buildings in central and specifi c locations, such as

centres in former markets or railway halls.• Festive shopping centres with specifi c leisure components developed in specialised locations such as

redeveloped waterfronts.

5. Entertainment Shopping Centres A shopping mall combined with substantial entertainment and amusement facilities, and includes food courts and cinemas.

6. Focused Shopping Centres (with two sub-types):• Superstore centres, in which a single large tenant dominates retail provision, such as in Hypermarket

centres or discount centres.• Specialised sales mall, in which all the outlets are orientated to the same product, such as auto malls, DIY

malls, etc.• Bargain centre, which refl ect the present trend of factory outlets to cluster.

7. Non-Residential Serving CentresThey provide retail fl oorspace that does not serve immediate resident populations. They comprise two subtypes:• Strip centres, which are on major transport routes and are interceptive to a large population, and• Ancillary Shopping Centres which provide shopping within structures (or landuse zones) developed

primarily for another function such as hotels, offi ces, industrial areas, or transport complexes.

It can thus be seen that there are innovative new shopping centres, which occur in addition to the traditional hierarchy.

Multi-use Shopping Centres4

4 This concept is lately (post - 2000) referred to as New Urbanism

23THE NATURE OF THE INTERNATIONAL, NATIONAL AND KWAZULU-NATAL RETAIL AND SHOPPING CENTRE INDUSTRY

Tab

le 2

.2 in

dic

ates

the

det

ail o

f the

cla

ssifi

catio

n of

Daw

son

with

som

e th

resh

old

val

ues

to r

adiu

s, p

opul

atio

n an

d s

ize

of c

entr

e.

TAB

LE 2

.2D

ETA

ILS

OF

THE

RET

AIL

CLA

SSIF

ICA

TIO

N (

DAW

SON

, 1

98

3)

BA

SIC

HIE

RA

RC

HY

RE

NE

WA

L C

EN

TR

ES

NO

N-R

ES

IDE

NT

IAL

SE

RV

ING

NE

W T

YP

ES

Loca

l C

onve

nien

ceC

lust

er

Nei

ghb

ourh

ood

Cen

tre

Com

mun

ityC

entr

eR

egio

nal

Cen

tre

Infi l

lC

entr

eE

xten

sion

Cen

tre

Cor

e R

epla

cem

ent

Mul

ti-us

eA

ncill

ary

Str

ipS

pec

ialit

y/Th

eme

Focu

sed

Hyp

er-

mar

ket

Cen

tre

Ent

erta

inm

ent

1M

ajor

func

tion

Con

veni

ence

g

ood

sC

onve

nien

ce

goo

ds

and

p

erso

nal s

ervi

ces

Sam

e, p

lus

com

par

ison

cl

othi

ng,

app

lianc

es,

etc.

Sam

e, p

lus

spec

ialit

y.Fu

rnitu

re,

qua

lity

clot

hes,

etc

.

Non

eC

omp

aris

on

shop

pin

gC

omp

aris

on

shop

pin

gC

omp

aris

on

shop

pin

g,

serv

ices

, ad

min

istr

ativ

e

Con

veni

ence

an

d s

ervi

ceB

asic

co

nven

ienc

e an

d

serv

ices

, or

sale

s ou

tlets

Hig

h or

der

im

pul

se

goo

ds

Dis

coun

ted

g

ood

s (li

mite

d

rang

e)

Con

veni

ence

g

ood

s an

d

rout

inel

y b

oug

ht

dur

able

s

Hig

h or

der

im

pul

se g

ood

s,

leis

ure

and

en

tert

ainm

ent

2Le

adin

g

tena

ntC

afé/

Gro

cer

Sup

erm

arke

t2-

3 sm

all

varie

ty a

nd/o

r d

epar

tmen

tal

stor

es

Thre

e or

m

ore

larg

e d

epar

tmen

t st

ores

Non

eVa

ried

Dep

artm

ent

stor

esD

epar

tmen

t st

ores

Non

eN

one

Ofte

n no

neM

ass

mer

chan

dis

erH

yper

mar

ket

Ran

ge

of

attr

actio

ns

2.a

Con

trol

of

tena

nt m

ixS

light

Som

eC

onsi

der

able

Con

sid

erab

leS

light

Som

eC

onsi

der

able

Con

sid

erab

leN

one

Non

eC

onsi

der

able

Con

sid

erab

leC

onsi

der

able

Con

sid

erab

le

3Lo

catio

nC

olle

ctor

ro

ads

with

in

resi

den

tial

area

Inte

rsec

tion

of

colle

ctor

and

ar

teria

l roa

ds

Inte

rsec

tion

of m

ajor

ar

teria

ls

Inte

rsec

tion

of fr

eew

ays

and

/or

maj

or

arte

rial

With

in e

xist

ing

d

evel

opm

ents

Clo

se to

co

re o

f sh

opp

ing

Cen

tre

of

shop

pin

gN

ew

com

mun

ityH

otel

, offi

ce

and

ind

ustr

yN

one

Hig

h in

com

e se

ctor

Junc

tion

on

maj

or r

oad

ne

twor

k

Inte

rsec

tion

of fr

eew

ays

and

/or

maj

or

arte

rial

Maj

or fo

cus

4R

adiu

s of

se

rvic

e ar

ea

With

in 5

m

ins.

Driv

ing

tim

e or

re

ason

able

w

alki

ng

dis

tanc

e

5-10

min

s.

driv

ing

tim

e5-

15 m

ins.

d

rivin

g ti

me

20 m

ins.

d

rivin

g ti

me

N/A

N/A

N/A

N/A

N/A

Inte

rcep

tory

lo

catio

nsN

/A20

-30

min

s.

driv

ing

tim

e20

min

s.

driv

ing

tim

e20

min

s. d

rivin

g

time

5M

inim

um

sup

por

t p

opul

atio

n

1 00

0 - 2

000

p

eop

le20

000

- 60

000

p

eop

le60

000

- 1

50 0

00

peo

ple

100

000

or

mor

e p

eop

leN

/AN

/AN

/A50

000

- 2

00 0

00

peo

ple

N/A

N/A

Reg

iona

lN

/A10

0 00

0 or

m

ore

peo

ple

Reg

iona

l

6S

ite a

rea

(Sho

pp

ing

ce

ntre

)

0,5

- 1,0

ha

1,5

- 3,0

ha

4,0

- 12,

0 ha

16,0

– 4

0,0

haN

/AN

/AN

/A5,

0 –

40,0

ha

0,5

- 3,0

ha

N/A

1,0

- 3,0

ha

N/A

10,0

– 2

0,0

haN

/A

7R

ang

e of

le

asab

le

area

(g

ross

)

300

– 1

200m

²7

000

- 12

000m

²15

000

- 30

000

m²

50 0

00 -

100

000m

²10

0 - 5

000

m²

5 00

0 -

20 0

00m

²10

000

- 75

000

m²

20 0

00 -

50 0

00m

²2

000

- 10

000

m²

200

- 3

000m

²5

000

- 10

000

m²

300

- 30

000

m²

18 0

00 -

30 0

00m

²N

/A

7aP

rese

nt

thre

shol

d

size

s

N/A

8 00

0 - 1

0 00

0m²

15 0

00 -

20 0

00m

²75

000

- 10

0 00

0m²

2 50

0m²

15 0

00m

²40

000

m²

20 0

00m

²(r

etai

l)3

000m

²Va

ried

6 00

0m²

10 0

00m

²15

000

- 18

000

m²

N/A

8N

umb

er o

f st

ores

5 –

1515

– 4

030

- 60

40 -

100

15 -

20Va

ried

Varie

dVa

ried

5 –

20Va

ried

Varie

d

(mos

tly s

mal

l un

its)

Dom

inan

t te

nant

(s)

Hyp

erm

arke

t p

lus

10-2

0 sh

ops

Varie

d o

utle

ts

24 THE NATURE OF THE INTERNATIONAL, NATIONAL AND KWAZULU-NATAL RETAIL AND SHOPPING CENTRE INDUSTRY

2.3.2 International Council of Shopping Centre Classifi cation

The classifi cation of retail space has always been complex. This is because there are so many different identities/categories to be linked to retail space. In the United States of America there have been prob-lems in classifying retail space into either standard categories or into some form of specialised type of centres. Table 2.3 is a list of the various categories:

TABLE 2.3CONFUSING TERMINOLOGY REGARDING

SHOPPING CENTRE DESCRIPTION AND TYPE OF CENTRES

General Descriptions/Standard Specialised Centres

Centres, commons, crossings, hybrids, lifestyle centres, malls, markets, marts, mega malls, mixed-use, outlets, parkways, places, plazas, promenades, shops, strips, squares, etc.

Convenience, entertainment, ethnicity, festival, lifestyle, luxury, tourist, urban and value.

In the United States of America, shopping centre development can be categorised into four distinct phases where different styles and approaches were followed:

• Phase 1

Shopping centres were classifi ed into several basic categories, this includes community centres, neighbourhood centres and strip centres. Early shopping centres also tended to be fairly uniform, de-signed to satisfy more of the mass merchandise demands, while offering the convenience of one-stop-shopping.

• Phase 2

The age of regional malls was born. The shift from urban to suburban shopping centres became the developing trend. Shopping centres were then mostly enclosed with a common corridor connecting tenants.

• Phase 3

Period of product differentiation, the two core categories were further subdivided. Super regional malls became more common, and even bigger mega malls started to develop. Developers started to recog-nise their niches and began to develop retail in the form of entertainment, festival, lifestyle, mixed-use, open-air, premium and tourist centres.

• Phase 4

The current wave is to build the so-called “lifestyle” centres, where it is all about the openness, the street-like atmosphere, and the creation of a unique shopping experience.

The main emphasis in each of the four phases discussed above was to offer something unique and to remain attractive in order to continuously draw support from the marketplace.

Table 2.4 below clearly indicates the latest classifi cation by the ICSC. Apart from the traditional malls, the classifi cation also distinguishes between open-air centres, including lifestyle centres, power cen-tres, theme/festival centres and outlet centres.

25THE NATURE OF THE INTERNATIONAL, NATIONAL AND KWAZULU-NATAL RETAIL AND SHOPPING CENTRE INDUSTRY

TABLE 2.4SUMMARY OF ICSC SHOPPING CENTRE CLASSIFICATIONS

Type Subtype Concept Size(m²)

Malls

Regional Centre General merchandise, fashion 40 000 - 80 000

Super Regional Centre Same as regional; more variety and assortment Over 80 000

Open-air centres

Neighbourhood Centre Convenience 3 000 - 15 000

Community Centre General merchandise; convenience 10 000 - 35 000

Lifestyle Centre Upscale; national, speciality; entertainment, outdoor 15 000 - 50 000

Power Centre Category-dominant anchors, few small tenants 25 000 - 60 000

Theme/Festival Centre Leisure; tourist-oriented; retail and service 8 000 - 25 000

Outlet Centre Manufacturer’s outlet stores 5 000 - 40 000

De Lisle, J. R, 2005, US Shopping Centre Classifi cation, volume 12, no 2. ICSC, Research Review, 2005.

The outstanding aspects regarding this classifi cation are the following:

• not much additional information about the threshold values, driving times and other requirements is provided; and

• the open-air centres consist of a broad variety/mix of different retail types;

The current ICSC classifi cation is used by institutional investors, real estate investment trusts, research institutions, valuers, lenders and city planners. Potential users include city marketers, development agencies and retail developers.

26 THE NATURE OF THE INTERNATIONAL, NATIONAL AND KWAZULU-NATAL RETAIL AND SHOPPING CENTRE INDUSTRY

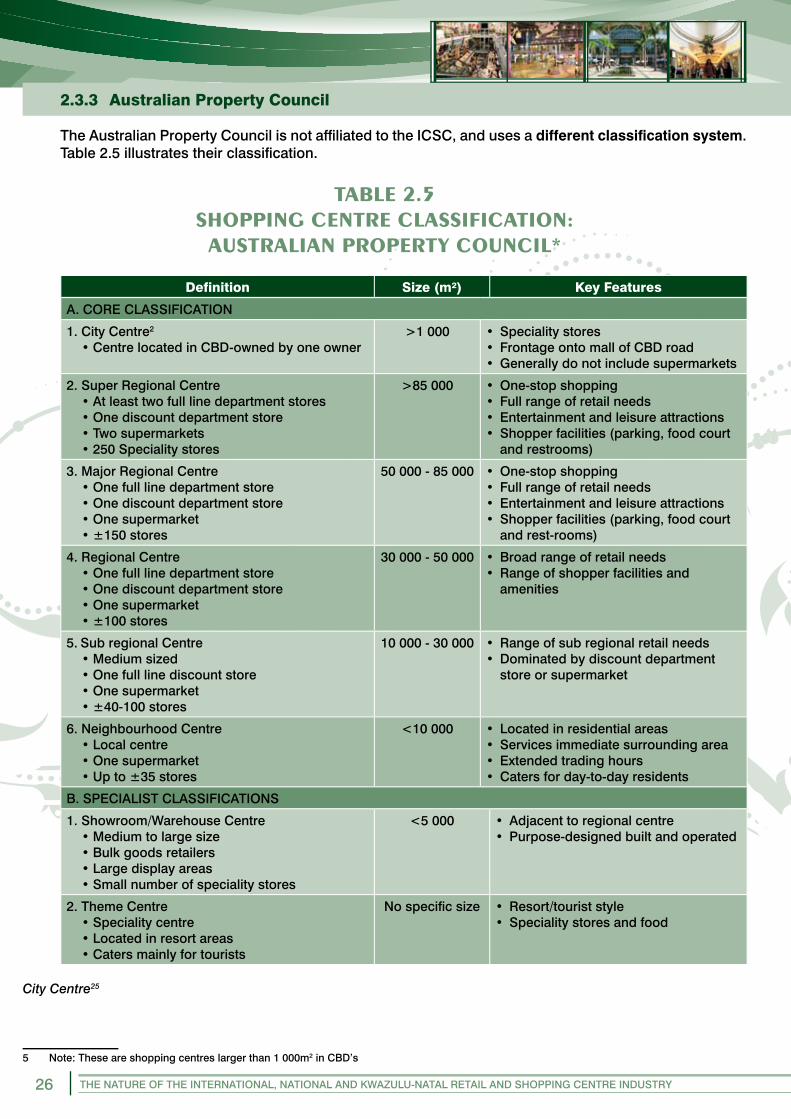

2.3.3 Australian Property Council

The Australian Property Council is not affi liated to the ICSC, and uses a different classifi cation system. Table 2.5 illustrates their classifi cation.

TABLE 2.5SHOPPING CENTRE CLASSIFICATION:AUSTRALIAN PROPERTY COUNCIL*

Defi nition Size (m²) Key Features

A. CORE CLASSIFICATION

1. City Centre2

• Centre located in CBD-owned by one owner>1 000 • Speciality stores

• Frontage onto mall of CBD road• Generally do not include supermarkets

2. Super Regional Centre• At least two full line department stores• One discount department store• Two supermarkets• 250 Speciality stores

>85 000 • One-stop shopping• Full range of retail needs• Entertainment and leisure attractions• Shopper facilities (parking, food court

and restrooms)

3. Major Regional Centre• One full line department store• One discount department store• One supermarket• ±150 stores

50 000 - 85 000 • One-stop shopping• Full range of retail needs• Entertainment and leisure attractions• Shopper facilities (parking, food court

and rest-rooms)

4. Regional Centre• One full line department store• One discount department store• One supermarket• ±100 stores

30 000 - 50 000 • Broad range of retail needs• Range of shopper facilities and

amenities

5. Sub regional Centre• Medium sized• One full line discount store• One supermarket• ±40-100 stores

10 000 - 30 000 • Range of sub regional retail needs• Dominated by discount department

store or supermarket

6. Neighbourhood Centre• Local centre• One supermarket• Up to ±35 stores

<10 000 • Located in residential areas• Services immediate surrounding area• Extended trading hours• Caters for day-to-day residents

B. SPECIALIST CLASSIFICATIONS

1. Showroom/Warehouse Centre• Medium to large size• Bulk goods retailers• Large display areas• Small number of speciality stores

<5 000 • Adjacent to regional centre• Purpose-designed built and operated

2. Theme Centre• Speciality centre• Located in resort areas• Caters mainly for tourists

No specifi c size • Resort/tourist style• Speciality stores and food

City Centre25

5 Note: These are shopping centres larger than 1 000m2 in CBD’s

27THE NATURE OF THE INTERNATIONAL, NATIONAL AND KWAZULU-NATAL RETAIL AND SHOPPING CENTRE INDUSTRY

Defi nition Size (m²) Key Features

3. Market• At least 50 stalls or outlets• Operates permanently or irregularly• Dominated by food retailing

<5 000

Source: Australia Property Council 2004

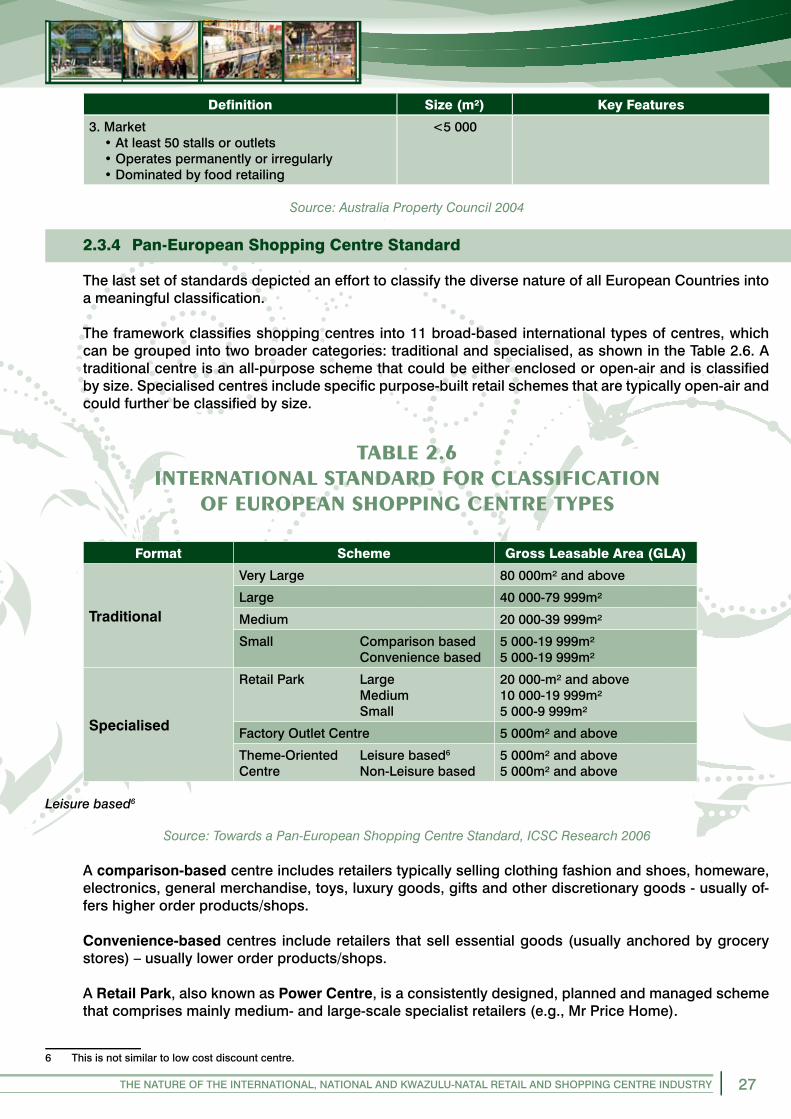

2.3.4 Pan-European Shopping Centre Standard

The last set of standards depicted an effort to classify the diverse nature of all European Countries into a meaningful classifi cation.

The framework classifi es shopping centres into 11 broad-based international types of centres, which can be grouped into two broader categories: traditional and specialised, as shown in the Table 2.6. A traditional centre is an all-purpose scheme that could be either enclosed or open-air and is classifi ed by size. Specialised centres include specifi c purpose-built retail schemes that are typically open-air and could further be classifi ed by size.

TABLE 2.6INTERNATIONAL STANDARD FOR CLASSIFICATION

OF EUROPEAN SHOPPING CENTRE TYPES

Format Scheme Gross Leasable Area (GLA)

Traditional

Very Large 80 000m² and above

Large 40 000-79 999m²

Medium 20 000-39 999m²

Small Comparison based Convenience based

5 000-19 999m²5 000-19 999m²

Specialised

Retail Park Large Medium Small

20 000-m² and above10 000-19 999m²5 000-9 999m²

Factory Outlet Centre 5 000m² and above

Theme-Oriented Leisure based6

Centre Non-Leisure based5 000m² and above5 000m² and above

Leisure based6

Source: Towards a Pan-European Shopping Centre Standard, ICSC Research 2006

A comparison-based centre includes retailers typically selling clothing fashion and shoes, homeware, electronics, general merchandise, toys, luxury goods, gifts and other discretionary goods - usually of-fers higher order products/shops.

Convenience-based centres include retailers that sell essential goods (usually anchored by grocery stores) – usually lower order products/shops.

A Retail Park, also known as Power Centre, is a consistently designed, planned and managed scheme that comprises mainly medium- and large-scale specialist retailers (e.g., Mr Price Home).

6 This is not similar to low cost discount centre.

28 THE NATURE OF THE INTERNATIONAL, NATIONAL AND KWAZULU-NATAL RETAIL AND SHOPPING CENTRE INDUSTRY

A Factory Outlet is where manufacturers and retailers sell merchandise at discounted prices (that may be surplus stock, prior-season stock or slow selling merchandise).

A Theme-oriented centre is either leisure based or non-leisure based. It consists of a narrow, but deep selection of merchandise within a specifi c retail category.