“kredaqro” closed joint stock non … khojaly ave, az1025 ... and fair presentation of the...

TRANSCRIPT

“KREDAQRO” CLOSED JOINT STOCK NON-BANKING CREDIT ORGANIZATION The International Financial Reporting Standards Financial Statements and Independent Auditors’ Report For the Year Ended December 31, 2015

CONTENTS INDEPENDENT AUDITOR’S REPORT FINANCIAL STATEMENTS Statement of Financial Position ..................................................................................................................................... 3 Statement of Comprehensive Income ............................................................................................................................ 4 Statement of Changes in Equity .................................................................................................................................... 5 Statement of Cash Flows ............................................................................................................................................... 6 Notes to Financial Statements 1. INTRODUCTION.............................................................................................................................................. 7 2. STATEMENT OF COMPLIANCE ................................................................................................................... 7 3. OPERATING ENVIRONMENT OF THE ORGANISATION ......................................................................... 8 4. SIGNIFICANT ACCOUNTING POLICIES ..................................................................................................... 8 5. ADOPTION OF NEW OR REVISED STANDARDS AND INTREPRETATIONS ...................................... 17 6. CASH AND CASH EQUIVALENTS ............................................................................................................. 25 7. DUE FROM BANKS ....................................................................................................................................... 25 8. LOANS TO CUSTOMERS ............................................................................................................................. 25 9. PROPERTY AND EQUIPMENT .................................................................................................................... 31 10. INTANGIBLE ASSETS .................................................................................................................................. 32 11. OTHER ASSETS ............................................................................................................................................. 32 12. DERIVATIVE FINANCIAL INSTRUMENTS .............................................................................................. 33 13. NON-CURRENT ASSETS HELD FOR SALE............................................................................................... 33 14. INCOME TAX RECEIVABLE ....................................................................................................................... 33 15. DUE TO BANKS AND OTHER FINANCIAL INSTITUTIONS .................................................................. 33 16. OTHER LIABILITIES ..................................................................................................................................... 34 17. CHARTER CAPITAL ..................................................................................................................................... 34 18. CAPITAL RESERVES .................................................................................................................................... 34 19. NET INTEREST INCOME ............................................................................................................................. 35 20. PROVISION FOR IMPAIRMENT LOSSES ON INTEREST BEARING ASSETS ...................................... 35 21. IMPAIRMENT OF NON-CURRENT ASSETS HELD FOR SALE .............................................................. 36 22. NET LOSS ON FOREIGN EXCHANGE OPERATIONS .............................................................................. 36 23. FEE AND COMMISSION EXPENSE ............................................................................................................ 36 24. ADMINISTRATIVE AND OPERATING EXPENSES .................................................................................. 37 25. OTHER INCOME ............................................................................................................................................ 37 26. INCOME TAXES ............................................................................................................................................ 37 27. COMMITMENTS AND CONTINGENCIES ................................................................................................. 39 28. TRANSACTIONS WITH RELATED PARTIES ............................................................................................ 40 29. FAIR VALUE OF FINANCIAL INSTRUMENTS ......................................................................................... 41 30. RISK MANAGEMENT POLICIES ................................................................................................................ 41 31. EVENTS AFTER THE REPORTING DATE ................................................................................................. 49

.---RSf\JI

RSM Azerbaijan

Demirchi Tower 21st floor, 37 Khojaly ave, AZ1025,

Baku, Azerbaijan

T +994(12) 480 4571 F +994(12) 480 4563

www.rsm.az

INDEPENDENT AUDITOR'S REPORT

To the Shareholders and the Board of Directors of KredAqro Closed Joint Stock Non-Banking Credit Organ ization

Auditor's report on the Financial Statements

We have audited the accompanying financial statements of "KredAqro" CJS NBCO (hereinafter referred to as "the Organization") which comprise the statement of financial position as of 31 December 2015 and the statement of comprehensive income, statement of changes in equity and statement of cash flows for the year then ended and a summary of significant accounting policies and other explanatory information.

Management's Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with International Financial Reporting Standards, and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditor's Responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with International Standards on Auditing. Those Standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity's preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal contro!. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

THE POWER OF BEING UNDERSTOOD AUDIT ITAX ICONSULTING

-r RSM Azerbaijan is a member of the RSM network and trades as RSM, R5M is the trading name used by the members of the RSM network. Each member of the RSM network is an independent

accounting and consulting firm which pranlces In Its own right. The RSM network is not itself a separate legal entit y in any jurisdiction.

• RSI\A

Opinion

In our opinion, the accompanying financial statements present fairly, in all material respects, the financial position of the Organization as of 31 December 2015, and its financial performance and its cash flows for the year then ended in accordance with International Financial Reporting Standards.

Otlier Matter

The Organ ization has prepared a separate set of financial statements for the year ended December 31, ..015 in accordance with Accounting Principles Generally Accepted in the United States of America (US GAAP), on which we have issued a separate auditor's report to the shareholders of the Organization dated April 25, 2016.

Baku, Republic of Azerbaijan April 25, 2016

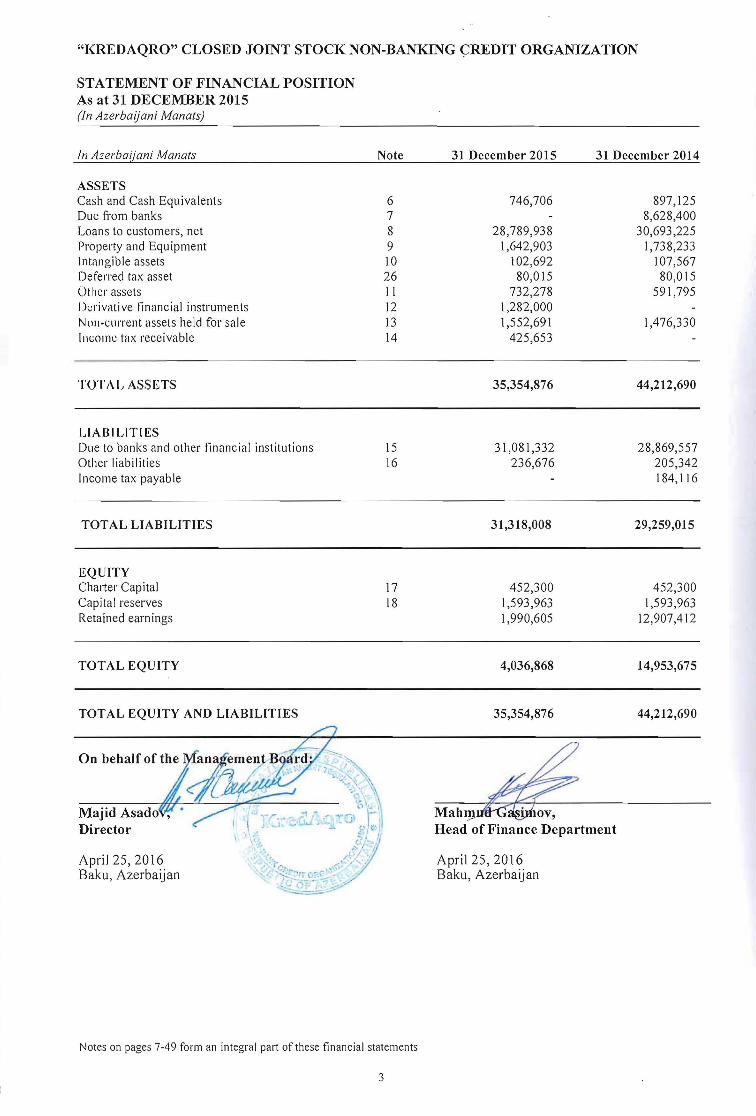

"KREDAQRO" CLOSED JOINT STOCK NON-BANKING CREDIT ORGANIZATION

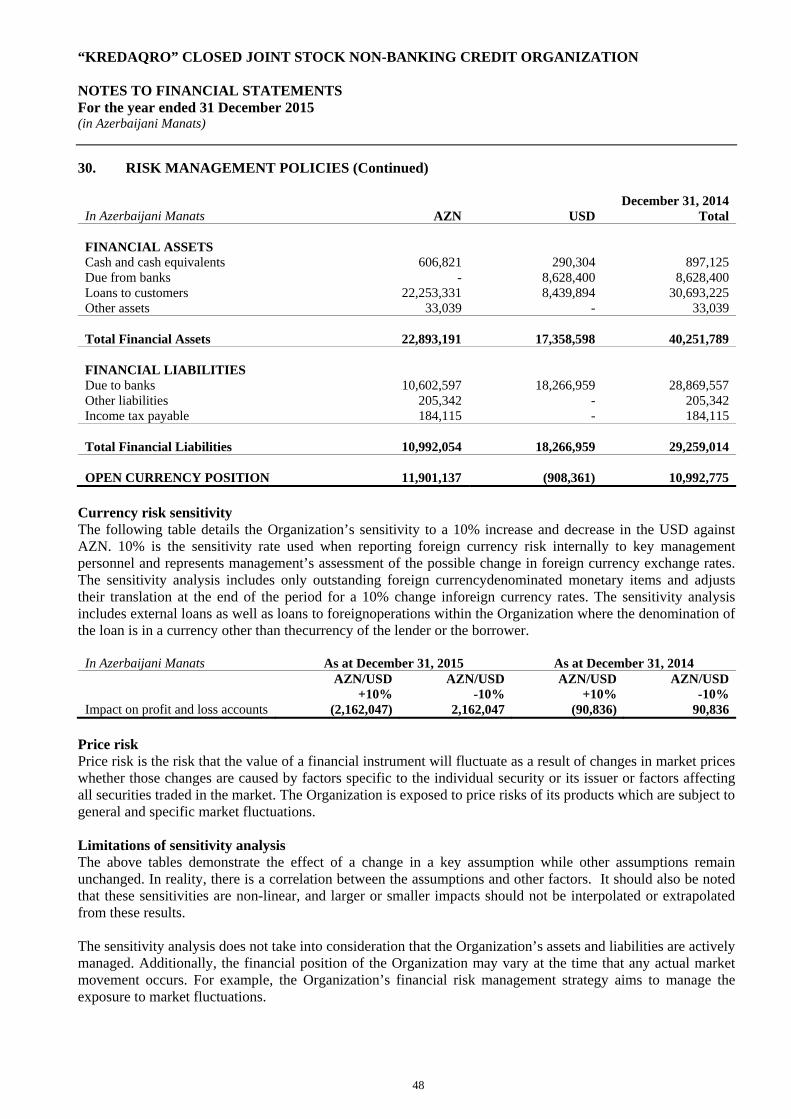

STATEMENT OF FINANCIAL POSITION As at 31 DECEMBER 2015 (In Azerbaijani Manats)

In Azerbaijani Manats Note 31 December 2015 31 December 2014

ASSETS Cash and Cash Equivalents Due from banks Loans to customers, net Property and Equipment Intangible assets Deferred tax asset Other assets I)cri vali ve financial instruments NOIl-clII'rellt assets held for sale Il\cOllle tax receivable

6 7 8 9 10 26 11 12 13 14

746,706

28,789,938 1,642,903

102,692 80,015

732,278 1,282,000 1,552,691

425,653

897,125 8,628,400

30,693,225 1,738,233

107,567 80,015

591,795

1,476,330

TOTAL ASSETS 35,354,876 44,212,690

LIABILITIES Due to banks and other financial institutions 15 31,081,332 28,869,557 Other liabilities 16 236,676 205,342 Income tax payable 184,116

TOTAL LIABILITIES 31,318,008 29,259,015

EQUITY Chal1er Capital 17 452,300 452,300 Capital reserves 18 1,593,963 1,593,963 Retained earnings 1,990,605 12,907,412

TOTAL EQUITY 4,036,868 14,953,675

TOTAL EQUITY AND LIABILITIES

Majid Asado Director

April 25, 2016 Baku, Azerbaijan

35,354,876 44,212,690

Mah~ Head of Finance Department

Apri125,2016 Baku, Azerbaijan

Notes on pages 7-49 form an integral part of these financial statements

3

"KREDAQRO" CLOSED JOINT STOCK NON-BANKING CREDIT ORGANIZATION

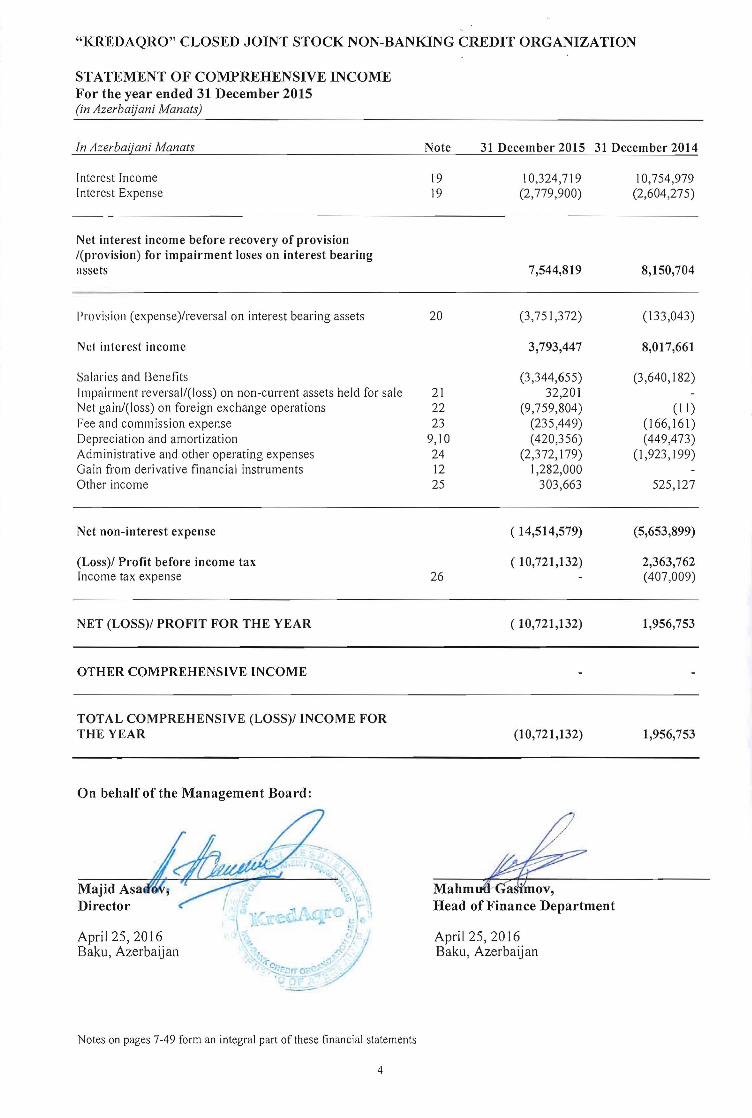

STATEMENT OF COMPREHENSIVE INCOME For the year ended 31 December 2015 (in Azerbaijani Manats)

In Azerbaijani Manats Note 31 December 2015 31 December 2014

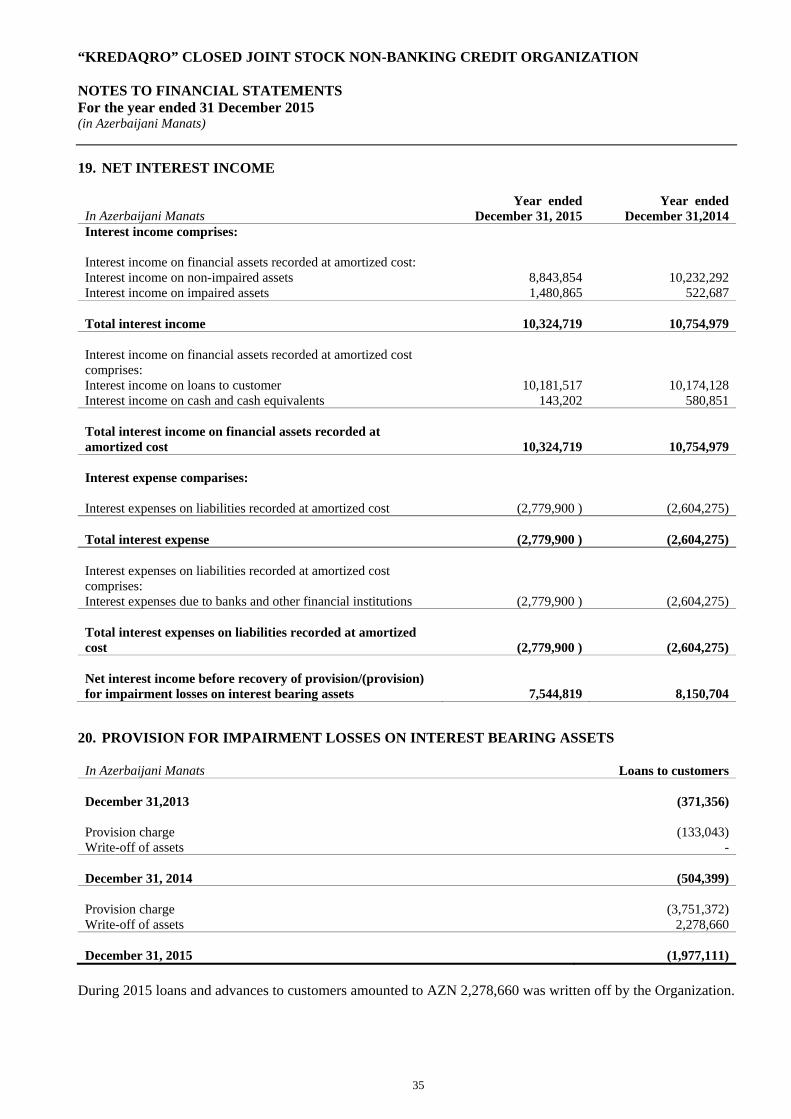

Interest Income 19 10,324,719 10,754,979 Interest Expense 19 (2,779,900) (2,604,275)

Net interest income before recovery of provision /(provision) for impairment loses on interest bearing lIssds 7,544,819 8,150,704

IJrovisioll (expense)/reversal on interest bearing assets 20 (3,751,372) (133,043)

Nl:I interest income 3,793,447 8,017,661

Salaries and Benefits Impairment reversal/(Ioss) on non-current assets held for sale Net gain/(loss) on foreign exchange operations Fee and commission expense Depreciation and amortization Administrative and other operating expenses Gain from derivative financial instruments Other income

21 22 23

9, I0 24 ]2 25

(3,344,655) 32,201

(9,759,804) (235,449) (420,356)

(2,372,179) 1,282,000

303,663

(3,640,182)

(II) (166,161) (449,473)

(I ,923, 199)

525, ]27

Net non-interest expense ( 14,514,579) (5,653,899)

(Loss)! Profit before income tax Income tax expense 26

( 10,721,132) 2,363,762 (407,009)

NET (LOSS)! PROFIT FOR THE YEAR ( 10,721,132) 1,956,753

OTHER COMPREHENSIVE INCOME

TOTAL COMPREHENSIVE (LOSS)! INCOME FOR THE YEAR (10,721,132) 1,956,753

On behalf of the Management Board:

Majid AsaE Director Head of Finance Department

April 25, 2016 April 25, 2016 Baku, Azerbaijan Baku, Azerbaijan

Notes on pages 7-49 form an integral part of these financial statements

4

"KREDAQRO" CLOSED JOINT STOCK NON-BANKING CREDIT ORGANIZATION

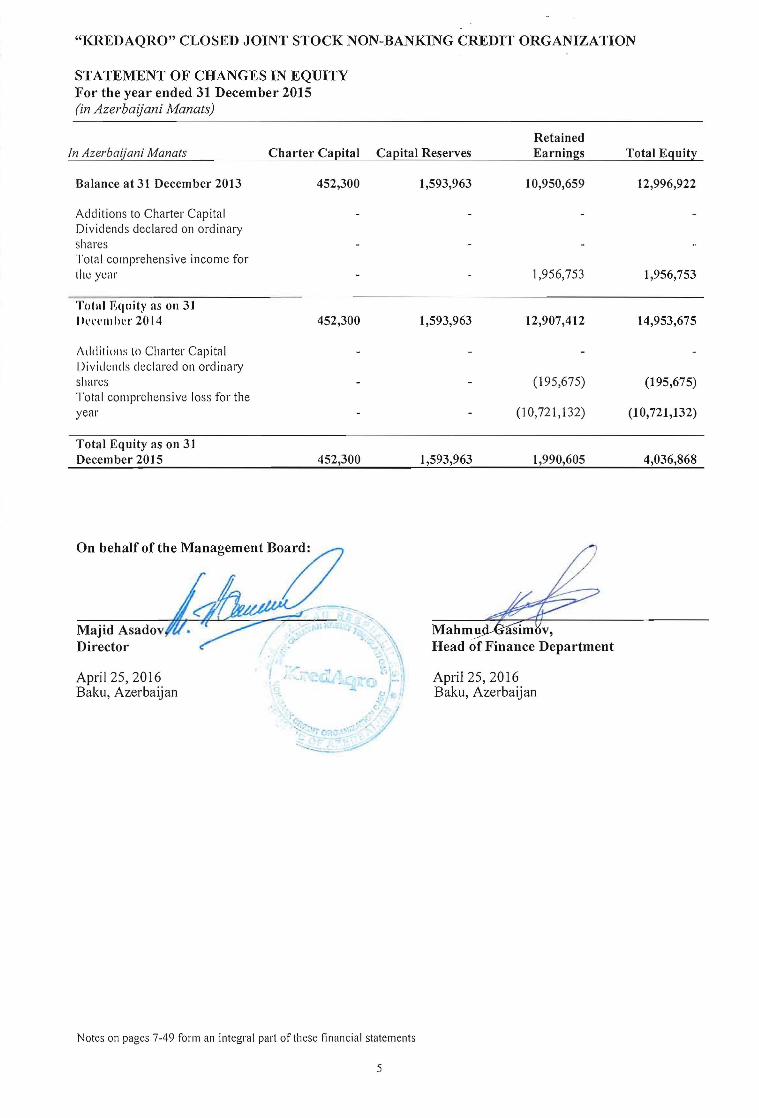

STATEMENT OF CHANGES IN EQUITY For the year ended 31 December 2015 (in Azerbaijani Manats)

In Azerbaijani Manats Charter Capital Capital Reserves Retained Earnings Total Equity

Balance at 31 December 2013 452,300 1,593,963 10,950,659 12,996,922

Additions to Charter Capital Dividends declared on ordinary shares Total comprehensive income for lh~: year 1,956,753 1,956,753

Tolal Equity ns on 31 Pt'\'\'mIH~r 2014 452,300 1,593,963 12,907,412 14,953,675

I\ddilillilS I() Charter Capital I)ividellcls cleclared on ordinary shares Total comprehensive loss for the year

(195,675)

(10,721,132)

(195,675)

(10,721,132)

Total Equity as on 31 December 2015 452,300 1,593,963 1,990,605 4,036,868

On behalf of the Management Board:

Majid Asadov Director

April 25, 2016 Baku, Azerbaijan

April 25, 2016 Baku, Azerbaijan

Notes on pages 7-49 form an integral part of these financial statements

5

I-"KREDAQRO" CLOSED JOINT STOCK NON-BANKING CREDIT ORGANIZATION

I

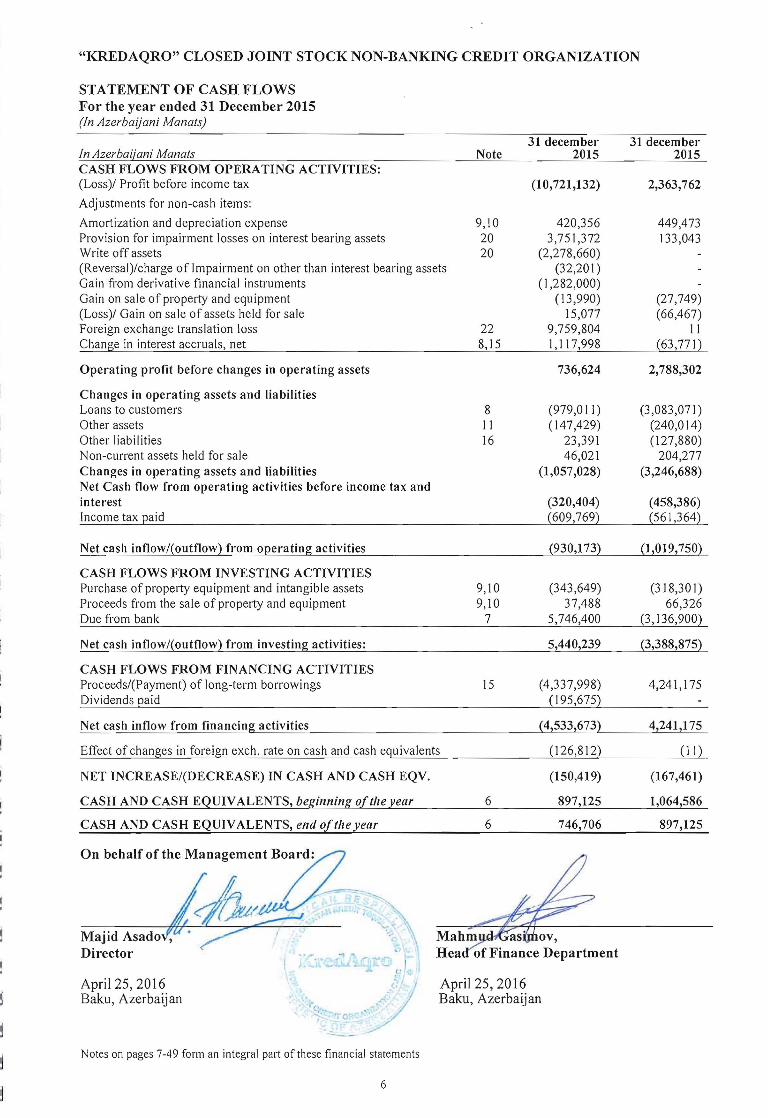

STATEMENT OF CASH FLOWS I For the year ended 31 December 2015

(In Azerbaijani Manats) I 31 december 31 december

In Azerbaijani Manats Note 2015 2015 CASH FLOWS FROM OPERATING ACTIVITIES: (Loss)! Profit before income tax (10,721,132) 2,363,762-

I Adjustments for non-cash items:

Amortization and depreciation expense 9,10 420,356 449,473 Provision for impairment losses on interest bearing assets 20 3,751,372 133,043 Write off assets 20 (2,278,660) (Reversal)/charge of Impairment on other than interest bearing assets (32,201) Gain from derivative financial instruments (1,282,000) Gain on sale of property and equipment (13,990) (27,749) (Loss)! Gain on sale of assets held for sale 15,077 (66,467) Foreign exchange translation loss 22 9,759,804 II Change in interest accruals, net 8,15 1,117,998 (63,771 )

Operating profit before changes in operating assets 736,624 2,788,302

Changes in operating assets and liabilities Loans to customers 8 (979,011) (3,083,071) Other assets I I (147,429) (240,014) Other liabilities 16 23,391 (127,880) Non-current assets held for sale 46,021 204,277 Changes in operating assets and liabilities (1,057,028) (3,246,688) Net Cash flow from operating activities before income tax and interest (320,404) (458,386) Income tax paid (609,769) (561,364)

I Net cash inflow/(outflow) from operating activities (930,173) (1,019,750)-- CASH FLOWS FROM INVESTING ACTIVITIES

I Purchase of property equipment and intangible assets 9,10 (343,649) (318,301) Proceeds from the sale of property and equipment 9,10 37,488 66,326 Due from bank 7 5,746,400 (3,136,900)

Net cash inflow/(outflow) from investing activities: 5,440,239 (3,388,875)-l CASH FLOWS FROM FINANCING ACTIVITIES Proceeds/(Payment) of long-term borrowings 15 (4,337,998) 4,241,175 Dividends paid (195,675)

Net cash inflow from financing activities (4,533,673) 4,241,175

Effect of changes in foreign exch. rate on cash and cash equivalents (126,812) (11 )

NET INCREASE/(DECREASE) IN CASH AND CASH EQV. (150,419) (167,461)

CASH AND CASH EQUIVALENTS, beginning o[tlle year 6 897,125 1,064,586

CASH AND CASH EQUIVALENTS, end o(tlleyear 6 746,706 897,125

Majid Asado Director

...11·_""'..... ;tC-..i,·· '-J- r J

?JApril 25, 2016 Baku, Azerbaijan

April 25, 2016 Baku, Azerbaijan

Notes on pages 7-49 form an integral part of these financial statements

6

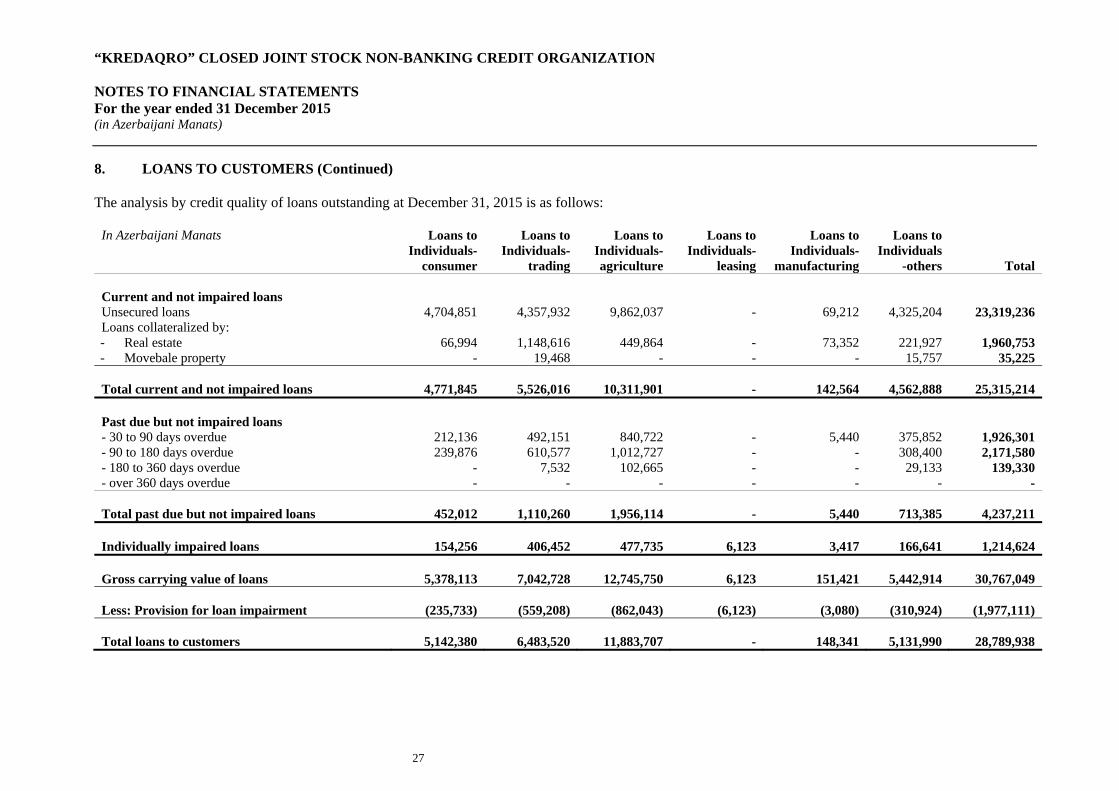

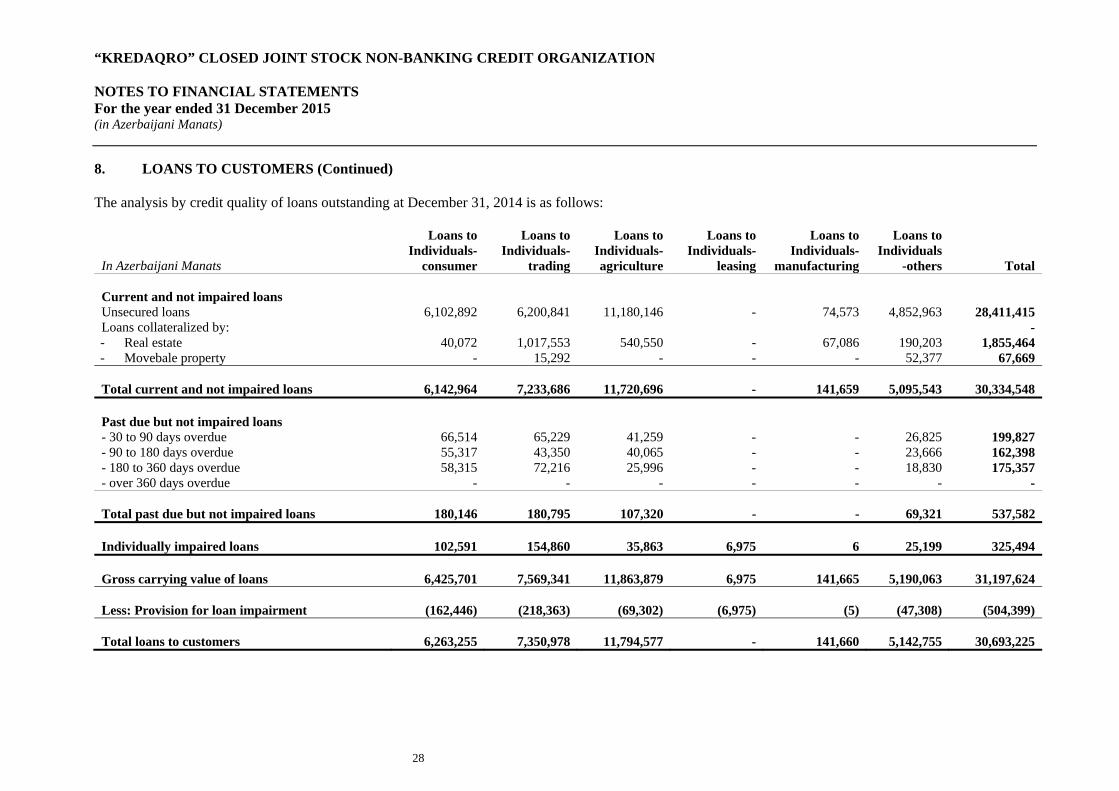

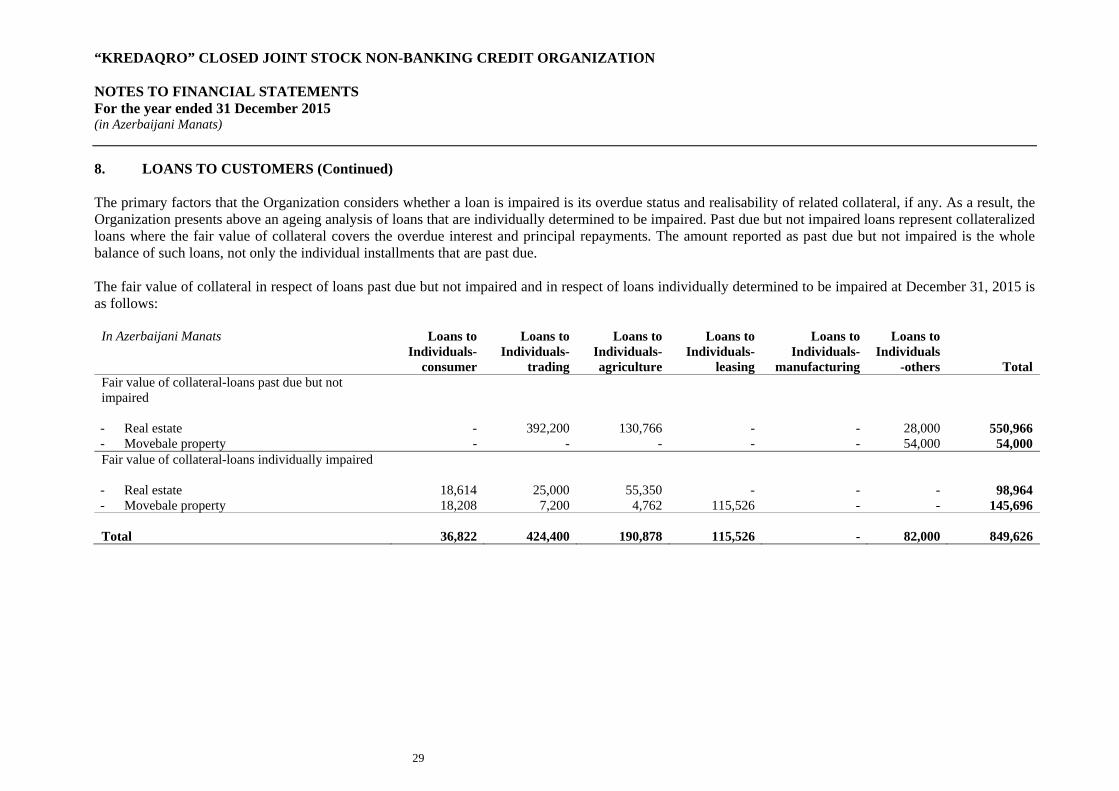

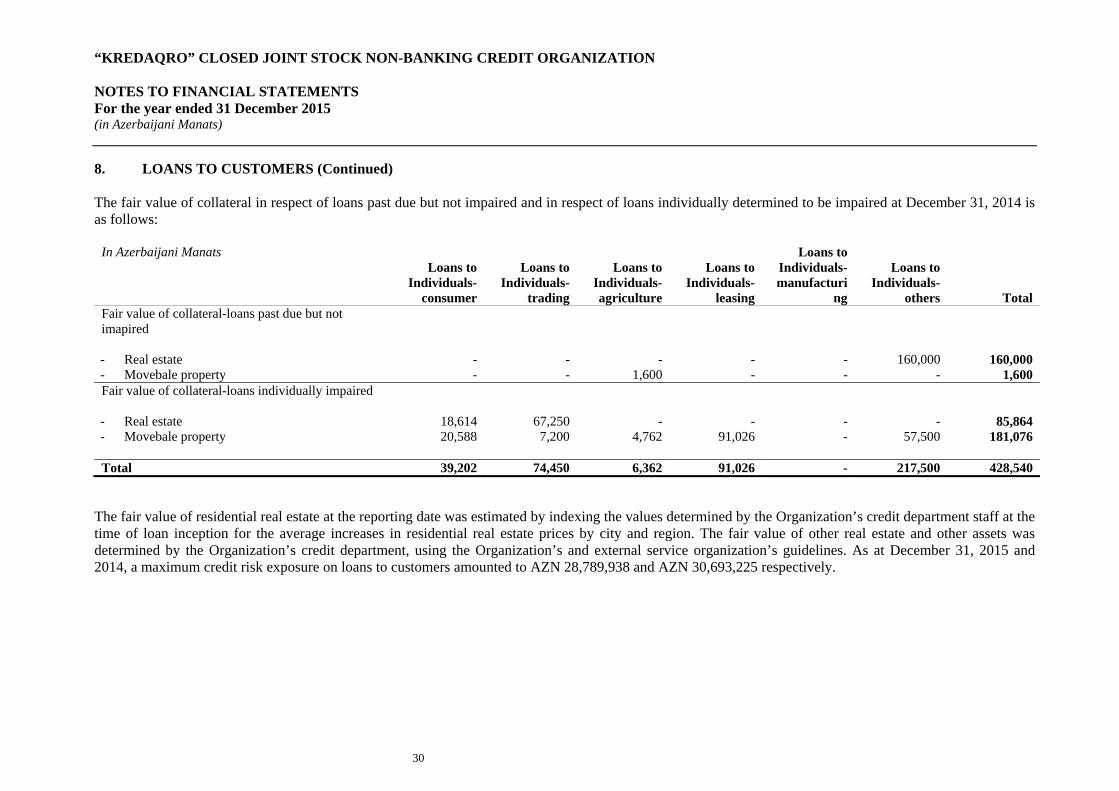

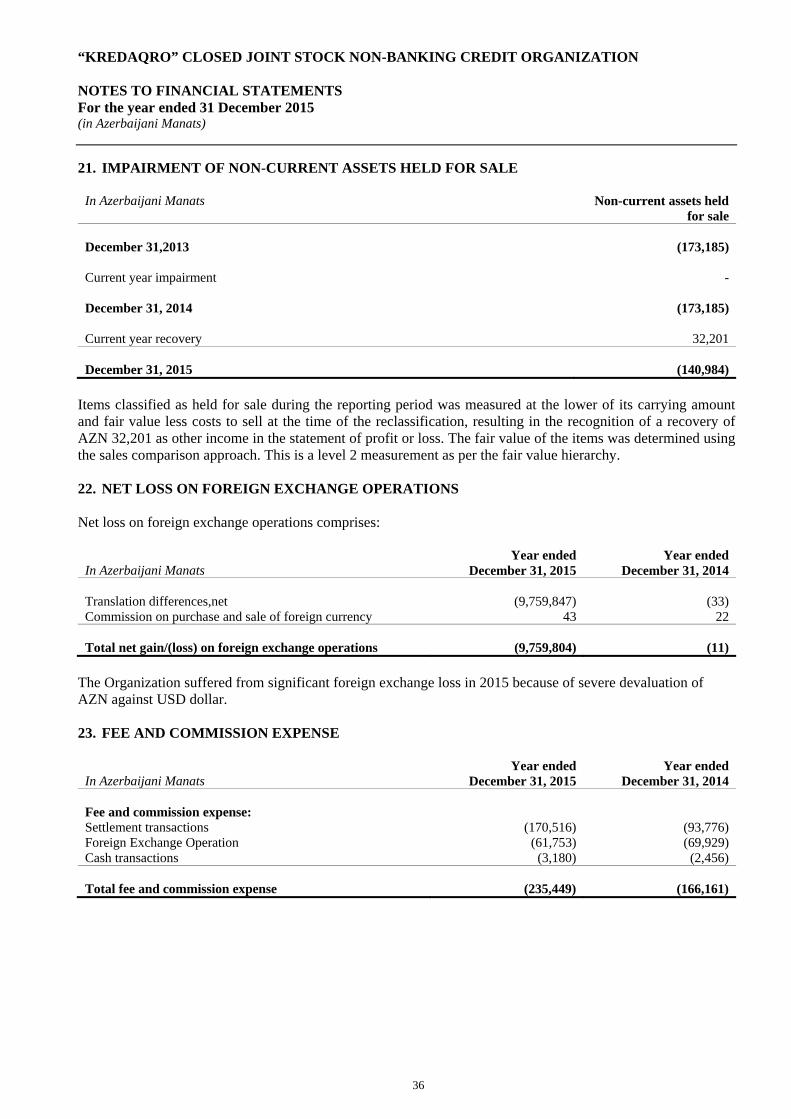

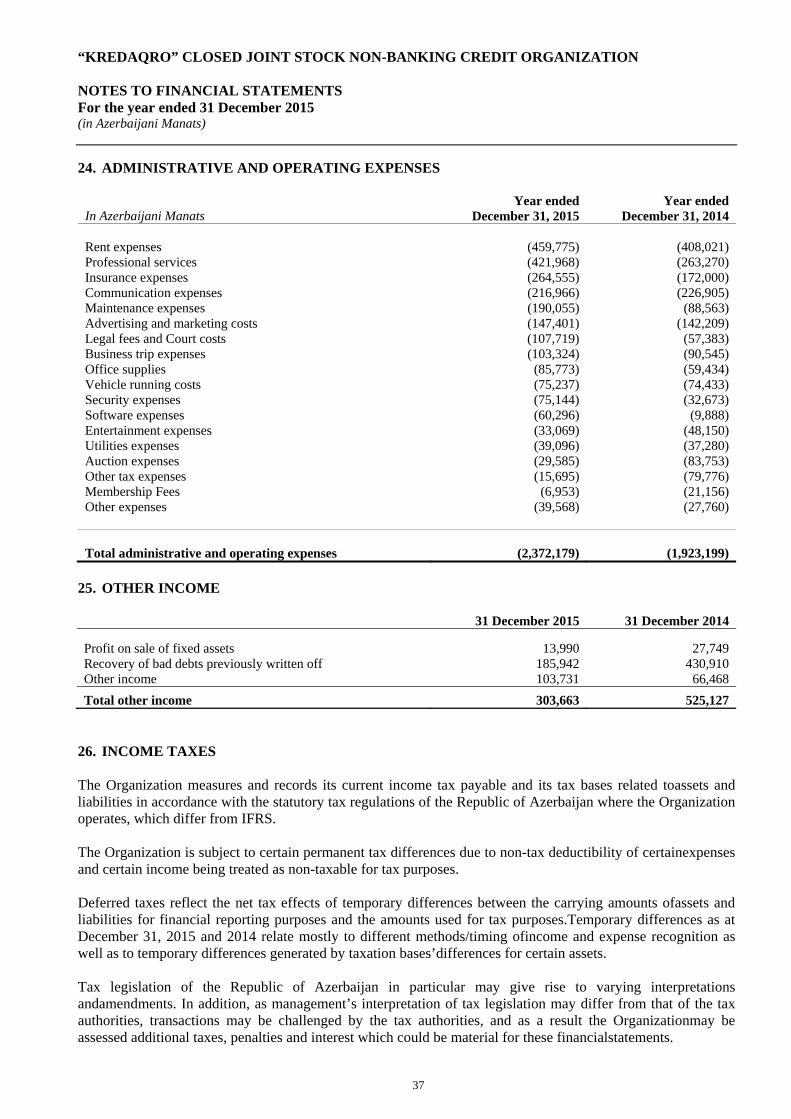

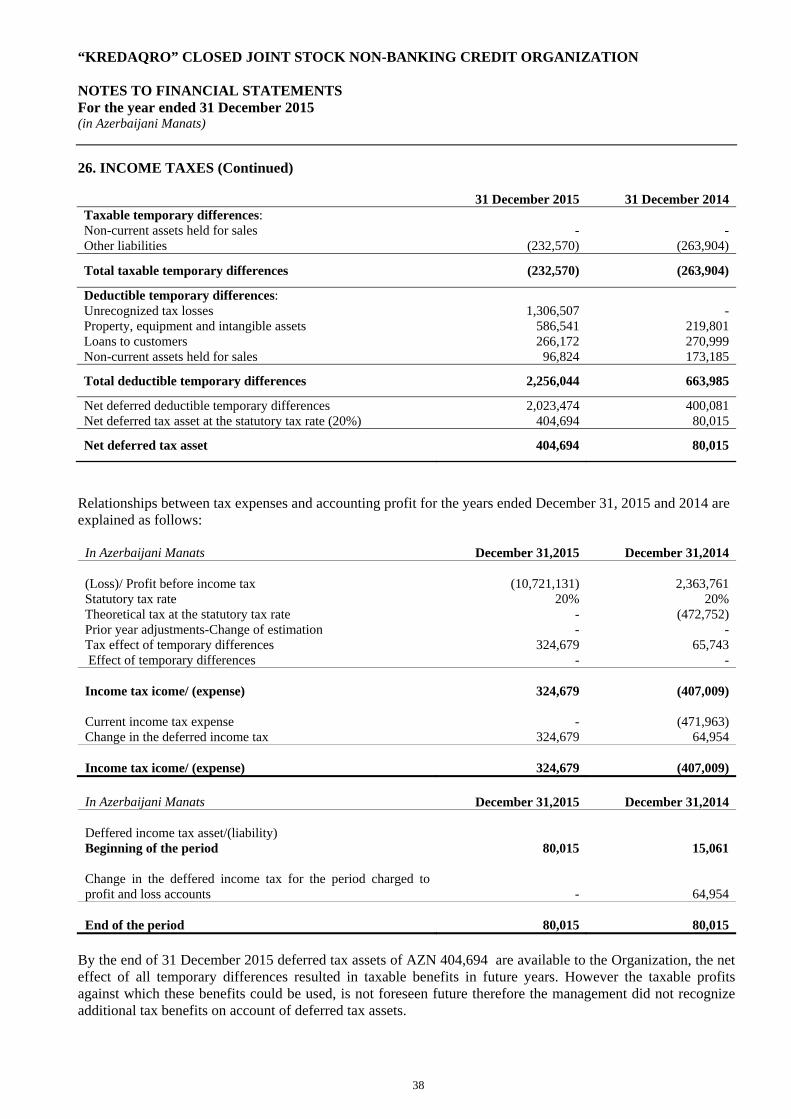

“KREDAQRO” CLOSED JOINT STOCK NON-BANKING CREDIT ORGANIZATION NOTES TO FINANCIAL STATEMENTS For the year ended 31 December 2015 (in Azerbaijani Manats)

7

1. INTRODUCTION “Kredaqro” Closed Joint Stock Non-Banking Credit Organization (the “Organization”) is engaged inprovision of loans to different sectors of the economy in the Republic of Azerbaijan. The Organizationwas established in accordance with the laws and regulations of the Republic of Azerbaijan on August 28, 2000. The founder of the Organization is ACDI/VOCA, a company registered and existing under the laws of the United States of America, owning 100% of the Organization’s charter capital. The originalpurpose of the Organization was to provide small and micro loans to the individuals engaged in entrepreneurship in rural areas. The registered office of the Organization is 63 Hasan Aliyev Street, Baku, Republic of Azerbaijan. The Organization was established as a result of granting of 5,314,205 US Dollars (AZN 4,168,462) by the United States Agency for International Development (“USAID”) to ACDI/VOCA to providesupport for a program in Azerbaijani Rural Credit Project. The Organization is regulated by the Central Bank of the Republic of Azerbaijan (the “CBAR”) and conducts its business under a limitedlicense number 06/06-1891 dated August 28, 2006. The Organization’s business islendingactivities. The legal organizational structure and the name of the Organization were changed from “Credagro”LLC to “Kredaqro” Closed Joint Stock Non-Banking Credit Organization according to the decision ofACDI/VOCA made on April 15, 2010. On September 28, 2010 the updated charter of theOrganization was officially registered. 2. STATEMENT OF COMPLIANCE Statement of compliance These financial statements of the Organization have been prepared in accordance with International Financial Reporting Standards (“IFRS”) issued by the International Accounting Standards Board (“IASB”) and Interpretations issued by the International Financial Reporting Interpretations Committee (“IFRIC”). Operating environment of the organisation The Republic of Azerbaijan.As an oil exporting country the economy of Azerbaijan is heavily dependent on oil being the largest contributor to the state budget both in volume and value terms, therefore the price of oil is of critical importance for the economy and abrupt changes in the price of oil have wide ranging effects on the macro economic factors of the economy like depreciation in currency, slower economic and industrial expansions and instability of monetary ramifications. Since the global financial crisis of 2008-2009, recent fall of oil prices in international market is the biggest collapse for oil exporting countries. From the mid of June 2014 the oil prices are falling instantaneously and this sharp decline is directly impacting the oil producing countries i.e. Azerbaijan and their effects are robust resulting in decrease in revenue of oil industry, reduction in fiscal revenues, reduction in production of oil and shutting of their progressive operations. If low oil prices continue for a prolonged period of time, this could result in long-term reductions in economic expansion and negative impact to the allied industries like banks and real estate etc. The government of Azerbaijan is determined to use alternative sources to prevent the reduction of fiscal revenues to the state budget rather than reducing the state expenditures. For the Purposes of remaining competitive in international market the Central Bank of Azerbaijan change their foreign exchange policy

“KREDAQRO” CLOSED JOINT STOCK NON-BANKING CREDIT ORGANIZATION NOTES TO FINANCIAL STATEMENTS For the year ended 31 December 2015 (in Azerbaijani Manats)

8

2. STATEMENT OF COMPLIANCE (Continued) by depreciating Manat against US Dollar by 34% through a press release on February 21, 2015 and 48% on December 21, 2015. This intervention policy of Central Bank is a step to new equilibrium of the economy and the impact until the economy approaches its equilibrium level are uncertain till the signing of these financial statements. The oil crisis is significantly effecting the financial and liquidity position of companies in oil or energy sector and lending exposure to this sector may also be adversely affected by the financial and economic environment which could in turn impact their ability to repay the amounts owed. Deteriorating operating conditions for customers may also have an impact on management's cash flow forecasts and assessment of the impairment of financial and non-financial assets. To the extent that information is available, management has reflected revised estimates of expected future cash flows in their impairment assessments. Management is unable to reliably estimate the effects on the the Organization's operations due to the expected changes in macro-economic factors and response of corollary measure thereon. Management believes it is taking all the necessary measures to support the sustainability and development of the Organization's business in the current circumstances. Other basis of presentation criteria These financial statements are presented in Azerbaijani Manats (“AZN”), unless otherwise indicated. These financial statements have been prepared under the historical cost convention. 3. GOING CONCERN As described in Note 2 Operating Environment to these financial statements, the majority of the financial covenants with the Lenders, the non-compliance of which may constitute an event of default, were broken as at 31 December 2015. Considering these risks the Shareholder and Management held negotiations with the lenders and in respect of obtaining a waiver and restructuring of borrowings.

Deteriorating operating conditions for customers may also have an impact on management's cash flow forecasts and assessment of the impairment of financial and non-financial assets. To the extent that information is available, management has reflected revised estimates of expected future cash flows in their impairment assessments. Due to these factors the Management are planning a financial scenario for the period beginning from 2016 until 2018, which comprises:

Restructuring of the loan portfolio during 2016-2018;

Partial and quarterly repayment of the debts and postponement of some amounts beyond 2018.

As of 22 April 2016, Management has concluded a restructuring Memorandum Of Understanding (hereinafter referred to as “MOU”) with its Lenders which will be superceded by a definitive, binding and enforceable intercreditor agreement by the Parties no later than 30 June 2016. The Cooperating Lenders are willing to grant KredAqro the said time and other accomodations to scheduled payments with certain requirments from ACDI VOCA, the shareholder. According to the MOU, each of the Cooperating Lenders shall cease to accrue interest on the principal of its loan after 31 May 2016. The document also specifies rescheduled payments of of the principal amounts compatible with the current operations of the Organization. The Management believe that the lenders continues to provide financial restructuring to the Organization and they will be able to fully implement the scenario, therefore it is considered appropriate to prepare the financial statements on a going concern basis.

“KREDAQRO” CLOSED JOINT STOCK NON-BANKING CREDIT ORGANIZATION NOTES TO FINANCIAL STATEMENTS For the year ended 31 December 2015 (in Azerbaijani Manats)

9

4. SIGNIFICANT ACCOUNTING POLICIES Recognition of interest income and expense Interest income and expense are recognized on an accrual basis using the effective interest method. The effective interest method is a method of calculating the amortized cost of a financial asset or a financial liability (or group of financial assets or financial liabilities) and of allocating the interest income or interest expense over the relevant period. The effective interest rate is the rate that exactly discounts estimated future cash payments or receipts (including all fees on points paid or received that form an integral part of the effective interest rate, transaction costs and other premiums or discounts) through the expected life of the financial instrument or, when appropriate, a shorter period to the net carrying amount of the financial asset or financial liability. Once a financial asset or a group of similar financial assets has been written down (partly written down) as a result of an impairment loss, interest income is thereafter recognized using the rate of interest used to discount the future cash flows for the purpose of measuring the impairment loss. Interest earned on assets at fair value is classified within interest income. Recognition of fee and commission income and expense Loan origination fees are deferred, together with the related direct costs, and recognized as anadjustment to the effective interest rate of the loan. Where it is probable that a loan commitment willlead to a specific lending arrangement, the loan commitment fees are deferred, together with the relateddirect costs, and recognized as an adjustment to the effective interest rate of the resulting loan.Whereit is unlikely that a loan commitment will lead to a specific lending arrangement, the loan commitmentfees are recognized in the statement of income over the remaining period of the loan commitment. Where a loan commitment expires without resulting in a loan, the loan commitment fee is recognized in the statement of income on expiry. Loan servicing fees are recognized as revenue as the services are provided. All other commissions are recognized when services are provided. Financial instruments The Organization recognizes financial assets and liabilities in its statement of financial position when it becomes a party to the contractual obligations of the instrument. Regular way purchases and sales of financial assets and liabilities are recognized using settlement date accounting. Financial assets and financial liabilities are initially measured at fair value. Transaction costs that are directly attributable to the acquisition or issue of financial assets and financial liabilities (other than financial assets and financial liabilities at fair value through profit and loss accounts) are added to or deducted from the fair value of the financial assets or financial liabilities, as appropriate, on initial recognition. Transaction costs directly attributable to the acquisition of financial assets or financial liabilities at fair value through profit or loss are recognized immediately in profit and loss accounts. Financial assets Financial assets are classified into the following specified categories: financial assets “at fair valuethrough profit or loss” (FVTPL), “held-to-maturity” investments, “available-for-sale” (AFS)financial assets and “loans and receivables”. The classification depends on the nature and purpose ofthe financial assets and is determined at the time of initial recognition. Financial assets at FVTPL Financial assets classified as held for trading are included in the category “financial assets at fair value through profit or loss”. Financial assets are classified as held for trading if they are acquired for the purpose of selling in the near term. Derivatives are also classified as held for trading unless they are designated and effective hedging instruments. Gains or losses on financial assets held for trading are recognized in the profit and loss account.

“KREDAQRO” CLOSED JOINT STOCK NON-BANKING CREDIT ORGANIZATION NOTES TO FINANCIAL STATEMENTS For the year ended 31 December 2015 (in Azerbaijani Manats)

10

4. SIGNIFICANT ACCOUNTING POLICIES (Continued) Loans and receivables Loans and receivables are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market. They are not entered into with the intention of immediate or short-term resale and are not classified as trading securities or designated as investment securities available-for-sale. Such assets are carried at amortized cost using the effective interest method. Gains and losses are recognized in profit and loss accounts when the loans and receivables are derecognized or impaired, as well as through the amortization process. Determination of fair value The fair value for financial instruments traded in active market at the reporting date is based on their quoted market price or dealer price quotations (bid price for long positions and ask price for short positions), without any deduction for transaction costs. For all other financial instruments not listed in an active market, the fair value is determined by using appropriate valuation techniques. Valuation techniques include net present value techniques, comparison to similar instruments for which market observable prices exist, options pricing models and other relevant valuation models. Cash and cash equivalents Cash and cash equivalents are items which are readily convertible to known amounts of cash andwhich are subject to insignificant risk of changes in value. Amounts, which relate to funds that areof a restricted nature, are excluded from cash and cash equivalents. Cash and cash equivalents arecarried at amortized cost. Loans and advances to banks Loans and advances to banks are recorded when the Organization advances money to counterparty banks with no intention of trading the resulting unquoted non-derivative receivable due on fixed or determinable dates. Loans and advances to banks are carried at amortized costs. Loans to customers Loans to customers are non-derivative assets with fixed or determinable payments that are not quoted in an active market, other than those classified in other categories of financial assets. Loans granted by the Organization are initially recognized at a fair value plus related transactioncosts. Where the fair value of consideration given does not equal the fair value of the loan, for example where the loan is issued at lower than market rates, the difference between the fair value of consideration given and the fair value of the loan is recognized as a loss on initial recognition of the loan and included in the statement of comprehensive income according to nature of these losses. Subsequently, loans are carried at amortized cost using the effective interest method. Loans to customers are carried net of any allowance for impairment losses. Reclassification of financial assets If a non-derivative financial asset classified as held for trading is no longer held for the purpose of selling in the near term, it may be reclassified out of the fair value through profit or loss category in one of the following cases:

A financial asset that would have met the definition of loans and receivables above may be reclassified to loans and receivables category if the Organization has the intention and ability to hold it for the foreseeable future or until maturity;

Other financial assets may be reclassified to available-for-sale or held to maturity categories only in rare circumstances.

“KREDAQRO” CLOSED JOINT STOCK NON-BANKING CREDIT ORGANIZATION NOTES TO FINANCIAL STATEMENTS For the year ended 31 December 2015 (in Azerbaijani Manats)

11

4. SIGNIFICANT ACCOUNTING POLICIES (Continued) A financial asset classified as available-for-sale that would have met the definition of loans andreceivables may be reclassified to loans and receivables category of the Organization has the intentionand ability to hold it for the foreseeable future or until maturity. Financial assets are reclassified at their fair value on the date of reclassification. Any gain or loss already recognized in profit and loss accounts is not reversed. The fair value of the financial asset onthe date of reclassification becomes its new cost or amortized cost, as applicable. Impairment of financial assets The Organization assesses at each reporting date whether there is any objective evidence that a financial asset or a group of financial assets is impaired. A financial asset or a group of financial assets is deemed to be impaired if, and only if, there is objective evidence of impairment as a result of one or more events that has occurred after the initial recognition of the asset (an incurred “loss event”) and that loss event (or events) has an impact on the estimated future cash flows of the financial asset or the group of financial assets that can be reliably estimated. Evidence of impairment may include indications that the borrower or a group of borrowers is experiencing significant financial difficulty, default or delinquency in interest or principal payments, the probability that they will enter bankruptcy or other financial reorganization and where observable data indicate that there is a measurable decrease in the estimated future cash flows, such as changes in arrears or economic conditions that correlate with defaults. Assets carried at amortized cost The Organization accounts for impairment losses of financial assets when there is objective evidence that a financial asset or a group of financial assets is impaired. Impairment losses are measured as the difference between carrying amounts and the present value of expected future cash flows, including amounts recoverable from guarantees and collateral, discounted at the financial asset’s original effective interest rate. Such impairment losses are not reversed, unless if in a subsequent period the amount of the impairment loss decreases and the decrease can be related objectively to an event occurring after the impairment was recognized, such as recoveries, in which case the previously recognized impairment loss is reversed by adjustment of an allowance account. For financial assets carried at cost, impairment losses are measured as the difference between the carrying amount of the financial asset and the present value of estimated future cash flows, discounted at the current market rate of return for a similar financial asset. Such impairment losses are not reversed. Write off of loans and advances Loans and advances are written off against the allowance for impairment losses when deemed uncollectible. Loans and advances are written off after management has exercised all possibilities available to collect amounts due to the Organization. Subsequent recoveries of amounts previously written off are reflected as an offset to the charge for impairment of financial assets in profit and loss accounts in the period of recovery. Derecognition of financial assets The Organization derecognizes a financial asset only when the contractual rights to the cash flowsfrom the asset expire, or when it transfers the financial asset and substantially all the risks andrewards of ownership of the asset to another entity. If the Organization neither transfers nor retainssubstantially all the risks and rewards of ownership and continues to control the transferred asset, theOrganization recognizes its retained interest in the asset and an associated liability for amounts itmay have to pay. If the Organization retains substantially all the risks and rewards of ownership of atransferred financial asset,

“KREDAQRO” CLOSED JOINT STOCK NON-BANKING CREDIT ORGANIZATION NOTES TO FINANCIAL STATEMENTS For the year ended 31 December 2015 (in Azerbaijani Manats)

12

4. SIGNIFICANT ACCOUNTING POLICIES (Continued) the Organization continues to recognize the financial asset and also recognizes a collateralized borrowing for the proceeds received. On derecognition of a financial asset in its entirety, the difference between the asset’s carrying amount and the sum of the consideration received and receivable and the cumulative gain or loss thathad been recognized in other comprehensive income and accumulated in equity is recognized inprofit and loss accounts. On derecognition of a financial asset other than in its entirety (for example when the Organizationretains an option to repurchase part of the transferred asset or retains a residual interest that does not result in the retention of substantially all the risks and rewards of ownership and the Organizationretains control), the Organization allocates the previous carrying amount of the financial assetbetween the part it continues to recognize under continuing involvement, and the part it no longer recognizes on the basis of the relative fair values of those parts on the date of the transfer. Thedifference between the carrying amount allocated to the part that is no longer recognized and the sumof the consideration received for the part no longer recognized and any cumulative gain or loss allocated to it that had been recognized in other comprehensive income is recognized in profit andloss accounts. A cumulative gain or loss that had beenrecognized in other comprehensive income isallocated between the part that continues to be recognized and the part that is no longer recognizedon the basis of the relative fair values of those parts. Financial liabilities Financial liabilities are classified as either financial liabilities “at FVTPL” or “other financial liabilities”. Other financial liabilities Other financial liabilities are initially measured at fair value, net of transaction costs. Other financial liabilities are subsequently measured at amortized cost using the effective interestmethod, with interest expense recognized on an effective yield basis. The effective interest method is a method of calculating the amortized cost of a financial liability andof allocating interest expense over the relevant period. The effective interest rate is the rate thatexactly discounts estimated future cash payments through the expected life of the financial liability,or (where appropriate) a shorter period, to the net carrying amount on initial recognition. Due to banks and other financial institutions Amounts due to banks and other financial institutions are recorded when money or other assets areadvanced to the Organization by counterparty banks and other financial institutions. The nonderivativeliability is carried at amortized cost. If the Organization purchases its own debt, it isremoved from the balance sheet and the difference between the carrying amount of the liability and theconsideration paid is included in gains or losses arising from early retirement of debt. Subordinated debt Subordinated debt includes long-term non-derivative liabilities and is carried at amortised cost. Debt isclassified as subordinated debt when its repayment ranks after all other creditors in case of liquidation. Derecognition of financial liabilities The Organization derecognizes financial liabilities when, and only when, the Organization’sobligationsare discharged, cancelled or they expire. The difference between the carrying amount ofthe financial liability derecognized and the consideration paid and payable is recognized in profit andloss accounts.

“KREDAQRO” CLOSED JOINT STOCK NON-BANKING CREDIT ORGANIZATION NOTES TO FINANCIAL STATEMENTS For the year ended 31 December 2015 (in Azerbaijani Manats)

13

4. SIGNIFICANT ACCOUNTING POLICIES (Continued) Offset of financial assets and liabilities Financial assets and liabilities are offset and reported net on the statement of financial position whenthe Organization has a legally enforceable right to set off the recognized amounts and the Organization intends either to settle on a net basis or to realize the asset and settle the liability simultaneously. In accounting for a transfer of a financial asset that does not qualify for derecognition,the Organization does not offset the transferred asset and the associated liability. Operating leases Operating lease payments are recognized as an expense on a straight-line basis over the lease term,except where another systematic basis is more representative of the time pattern in which economicbenefits from the leased asset are consumed. Contingent rentals arising under operating leases arerecognized as an expense in the period in which they are incurred. In the event that lease incentives are received to enter into operating leases, such incentives arerecognized as a liability. The aggregate benefit of incentives is recognised as a reduction of rentalexpense on a straight-line basis, except where another systematic basis is more representative of thetime pattern in which economic benefits from the leased asset are consumed. Property, equipment and intangible assets Property, equipment and intangible assets are carried at historical cost less accumulated depreciationand any recognized impairment loss, if any. Depreciation is charged on the carrying value of propertyand equipment and intangible assets and is designed to write off assets over their useful economiclives. It is calculated on a straight line basis at the following annual prescribed rates: Buildings 7% Furniture and fixtures 20% Computers and communication equipments 25% Vehicles 25% Intangible assets 10% Freehold land is not depreciated. Expenses related to repairs and renewals are charged when incurred and included in operatingexpenses unless they qualify for capitalization. Intangible assets with finite useful lives that are acquired separately are carried at cost lessaccumulated amortization and accumulated impairment losses. Amortization is recognized on astraight-line basis over their estimated useful lives. The estimated useful life and amortization methodare reviewed at the end of each reporting period, with the effect of any changes in estimate beingaccounted for on a prospective basis. Intangible assets with indefinite useful lives that are acquiredseparately are carried at cost less accumulated impairment losses. At the end of each reporting period, the Organization reviews the carrying amounts of its property,equipment and intangible assets to determine whether there is any indication that those assets havesuffered an impairment loss. An impairment loss will be recognised if the carrying amount of theassets is not recoverable and exceeds fair value. The carrying amount of the assets is considered notrecoverable if it exceeds the sum of the undiscounted cash flows expected to result from the use of the asset.

“KREDAQRO” CLOSED JOINT STOCK NON-BANKING CREDIT ORGANIZATION NOTES TO FINANCIAL STATEMENTS For the year ended 31 December 2015 (in Azerbaijani Manats)

14

4. SIGNIFICANT ACCOUNTING POLICIES (Continued) Assets held for sale.

The Organization classifies an asset as held for sale if its carrying amount will be recovered principally through a sale transaction rather than through continuing use. For this to be the case, the non-current asset must be available for immediate sale in its present condition subject only to terms that are usual and customary for sales of such assets and its sale must be highly probable.

The sale qualifies as highly probable if the Organization’s management is committed to a plan to sell the non-current asset and an active program to locate a buyer and complete the plan must have been initiated. Further, the non-current asset must have been actively marketed for a sale at price that is reasonable in relation to its current fair value and in addition the sale should be expected to qualify for recognition as a completed sale within one year from the date of classification of the non-current asset as held for sale.

The Organization measures an asset classified as held for sale at the lower of its carrying amount and fair value less costs to sell. The Organization recognizes an impairment loss for any initial or subsequent write-down of the asset to fair value less costs to sell if events or changes in circumstance indicate that their carrying amount may be impaired. Any subsequent increase in an asset’s fair value less costs to sell is recognized to the extent of the cumulative impairment loss that was previously recognized in relation to that specific asset. Taxation Income tax expense represents the sum of the current and deferred tax expense. The tax currently payable is based on taxable profit for the year. Taxable profit differs from net profit as reported in the statement of comprehensive income because it excludes items of income or expense that are taxable or deductible in other years and it further excludes items that are never taxable or deductible. The Organization’s current tax expense is calculated using tax rates that have been enacted or substantively enacted by the end of the reporting period. Deferred tax is the tax expected to be payable or recoverable on differences between the carrying amounts of assets and liabilities in the financial statements and the corresponding tax bases used in the computation of taxable profit, and is accounted for using the statement of financial position liability method. Deferred tax liabilities are generally recognized for all taxable temporary differences and deferred tax assets are recognized to the extent that it is probable that taxable profits will be available against which deductible temporary differences can be utilized. Such assets and liabilities are not recognized if the temporary difference arises from the initial recognition (other than in a business combination) of other assets and liabilities in a transaction that affects neither the tax profit nor the accounting profit. The carrying amount of deferred tax assets is reviewed at each reporting date and reduced to theextent that it is no longer probable that sufficient taxable profits will be available to allow all or part ofthe asset to be recovered. Deferred tax is calculated at the tax rates that are expected to apply in the period when the liability is settled or the asset is realized. Deferred tax is charged or credited in the statement of comprehensive income, except when it relates to items charged or credited directly to equity, in which case the deferred tax is also dealt with in equity. Deferred income tax assets and deferred income tax liabilities are offset and reported net on the statement of financial position if:

“KREDAQRO” CLOSED JOINT STOCK NON-BANKING CREDIT ORGANIZATION NOTES TO FINANCIAL STATEMENTS For the year ended 31 December 2015 (in Azerbaijani Manats)

15

4. SIGNIFICANT ACCOUNTING POLICIES (Continued)

The Organization has a legally enforceable right to set off current income tax assets against current income tax liabilities; and

Deferred income tax assets and the deferred income tax liabilities relate to income taxes levied by the same taxation authority on the same taxable entity.

The Republic of Azerbaijan also has various other taxes, which are assessed on the Organization’s activities. These taxes are included as a component of operating expenses in the statement of comprehensive income. Provisions Provisions are recognized when the Organization has a present legal or constructive obligation as aresult of past events, and it is probable that an outflow of resources embodying economic benefits willbe required to settle the obligation and a reliable estimate of the obligation can be made. The amount recognized as a provision is the best estimate of the consideration required to settle thepresent obligation at the end of the reporting period, taking into account the risks and uncertaintiessurrounding the obligation. When a provision is measured using the cash flows estimated tosettlethepresent obligation, its carrying amount is the present value of those cash flows (where the effect of thetime value of money is material). When some or all of the economic benefits required to settle a provision are expected to be recoveredfrom a third party, a receivable is recognized as an asset if it is virtually certain that reimbursementwill be received and the amount of the receivable can be measured reliably. Retirement and other benefit obligations In accordance with the requirements of the legislation of the Republic of Azerbaijan state pensionsystem provides for the calculation of current payments by the employer as a percentage of currenttotal payments to staff. This expense is charged in the period the related salaries are earned. Uponretirement all retirement benefit payments are made by pension funds selected by employees. The Organization does not have any pension arrangements separate from the state pension system of the Republic of Azerbaijan. In addition, the Organization has no post-retirement benefits or other significant compensated benefits requiring accrual. Contingencies Contingent liabilities are not recognized in the balance sheets but are disclosed unless the possibility ofany outflow in settlement is remote. A contingent asset is not recognized in the balance sheet butdisclosed when an inflow of economic benefits is probable. Charter capital Charter capital is the amount of capital contributed by all participants. The total number of shares willbe proportionate division between participants in charter capital of the Organization. The Organizationmay increase or decrease its charter capital with approval of the General Meeting of Participantsgranted in accordance with law. Foreign currency translation The functional currency of the Organization is the currency of the primary economic environment, inwhich the entity operates. The Organization’s functional currency is AZN.

“KREDAQRO” CLOSED JOINT STOCK NON-BANKING CREDIT ORGANIZATION NOTES TO FINANCIAL STATEMENTS For the year ended 31 December 2015 (in Azerbaijani Manats)

16

4. SIGNIFICANT ACCOUNTING POLICIES (Continued) Monetary assets and liabilities denominated in foreign currencies are translated into AZN at theappropriate spot rates of exchange of the CBAR ruling at the end of reporting date. Foreign currencytransactions are accounted for at the exchange rates prevailing at the date of the transaction. Profitsand losses arising from these translations are included in net gain/(loss) on foreign exchange operations. Rates of exchange The exchange rates at the year-end used by the Organization in the preparation of the financialstatements are as follows:

December 31,2015 December 31,2014 USD/AZN 1.5594 0.7844

Critical accounting judgments and key sources of estimation uncertainty The preparation of the Organization’s financial statements requires management to make estimates and judgments that affect the reported amounts of assets and liabilities at the reporting date and the reported amount of income and expenses during the period ended. Management evaluates its estimates and judgments on an ongoing basis. Management bases its estimates and judgments on historical experience and on various other factors that are believed to be reasonable under the circumstances. Actual results may differ from these estimates under different assumptions orconditions. The following estimates and judgments are considered important to the portrayal of theOrganization’s financial condition. Allowance for impairment of loans The Organization regularly reviews its loans to assess for impairment. The Organization’s loanimpairment provisions are established to recognize incurred impairment losses in its portfolio ofloans and receivables. The Organization considers accounting estimates related to allowance forimpairment of loans and receivables a key source of estimation uncertainty because (i) they arehighly susceptible to change from period to period as the assumptions about future default rates andvaluation of potential losses relating to impaired loans and receivables are based on recentperformance experience, and (ii) any significant difference between the Organization’s estimatedlosses and actual losses would require the Organization to record provisions which could have amaterial impact on its financial statements in future periods. The Organization uses management’s judgment to estimate the amount of any impairment loss incases where a borrower has financial difficulties and there are few available sources of historical datarelating to similar borrowers. Similarly, the Organization estimates changes in future cash flowsbased on past performance, past customer behavior, observable data indicating an adverse change inthe payment status of borrowers in a group, and national or local economic conditions that correlatewith defaults on assets in the group. Management uses estimates based on historical loss experiencefor assets with credit risk characteristics and objective evidence of impairment similar to those in thegroup of loans. The Organization uses management’s judgment to adjust observable data for a groupof loans to reflect current circumstances not reflected in historical data. The allowances for impairment of financial assets in the financial statements have been determinedon the basis of existing economic and political conditions. The Organization is not in a position topredict what changes in conditions will take place in the country and what effect such changes mighthave on the adequacy of the allowances for impairment of financial assets in future periods.

“KREDAQRO” CLOSED JOINT STOCK NON-BANKING CREDIT ORGANIZATION NOTES TO FINANCIAL STATEMENTS For the year ended 31 December 2015 (in Azerbaijani Manats)

17

5. ADOPTION OF NEW OR REVISED STANDARDS AND INTREPRETATIONS For the preparation of these financial statements, the following new, revised or amended pronouncements are mandatory for the first time for the financial year beginning 1 January 2015 (the list does not include information about new or amended requirements that affect interim financial reporting or first-time adopters of IFRS since they are not relevant to IFRS Statements Limited). IFRS 9 Financial Instruments (2009) (issued in November 2009 and amended in October 2010) - This standard introduces new requirements for classifying and measuring financial assets, as follows:

Debt instruments meeting both a 'business model' test and a 'cash flow characteristics' test are measured at amortized cost (the use of fair value is optional in some limited circumstances)

Investments in equity instruments can be designated as 'fair value through other comprehensive income' with only dividends being recognized in profit or loss

All other instruments (including all derivatives) are measured at fair value with changes recognized in the profit or loss

The concept of 'embedded derivatives' does not apply to financial assets within the scope of the Standard and the entire instrument must be classified and measured in accordance with the above guidelines. A revised version of IFRS 9 incorporating revised requirements for the classification and measurement of financial liabilities, and carrying over the existing derecognition requirements from IAS 39 Financial Instruments: Recognition and Measurement. The revised financial liability provisions maintain the existing amortized cost measurement basis for most liabilities. New requirements apply where an entity chooses to measure a liability at fair value through profit or loss – in these cases, the portion of the change in fair value related to changes in the entity's own credit risk is presented in other comprehensive income rather than within profit or loss. The most significant effect of IFRS 9 regarding the classification and measurement of financial liabilities relates to the accounting for changes in fair value of a financial liability that is designated as at fair value through profit or loss, attributable to changes in the credit risk of that liability. Specifically, under IFRS 9 for financial liabilities that are designated as at fair value through profit or loss, the amount of change in the fair value of the financial liability that is attributable to changes in the credit risk of that liability is recognized in other comprehensive income, unless the recognition of the effects of changes in the liability's credit risk in other comprehensive income would create or enlarge an accounting mismatch in profit or loss. Changes in fair value attributable to a financial liability's credit risk are not subsequently reclassified to profit or loss. Currently, under IAS 39, the entire amount of the change in the fair value of the financial liability designated as at fair value through profit or loss is recognized in profit or loss. Derecognition provisions are carried over almost unchanged from IAS 39. IFRS 9 is effective for annual periods beginning on or after 1 January 2015, by which time it will include requirements and guidance on impairment and hedge accounting. The Directors anticipate that IFRS 9 will be adopted in the Group's consolidated financial statements when it becomes mandatory and that the application of the new standard might have a significant impact on amounts reported in respect of the Companies’ financial assets and financial liabilities. However, it is not practicable to provide a reasonable estimate of that effect until a detailed review has been completed. New and revised pronouncements in issue but not yet effective The Company has not applied the following new, revised or amended pronouncements that have been issued by the IASB but are not yet effective for the financial year beginning 1 January 2015.The Directors anticipate that the new standards, amendments and interpretations will be adopted in the Company’s financial statements when they become effective. The Company has assessed, where practicable, the potential impact of all these new standards, amendments and interpretations that will be effective in future periods.

“KREDAQRO” CLOSED JOINT STOCK NON-BANKING CREDIT ORGANIZATION NOTES TO FINANCIAL STATEMENTS For the year ended 31 December 2015 (in Azerbaijani Manats)

18

5. ADOPTION OF NEW OR REVISED STANDARDS AND INTREPRETATIONS (Continued) IFRS 10 and IAS 28 Sale or Contribution of Assets between an Investor and its Associate or Joint Venture – Amendments to IFRS 10 and IAS 28 Effective for annual periods beginning on or after 1 January 2016. Key requirements The amendments address the conflict between IFRS 10 and IAS 28 in dealing with the loss of control of a subsidiary that is sold or contributed to an associate or joint venture. The amendments clarify that the gain or loss resulting from thesale or contribution of assets that constitute a business, as defined in IFRS 3 Business Combinations, between an investor and its associate or joint venture, is recognised in full. Any gain or loss resulting from the sale or contribution of assets that do not constitute a business, however, is recognised only to the extent of unrelated investors’ interests in the associate or joint venture. Transition The amendments must be applied prospectively. Early application is permitted and must be disclosed Impact The amendments will effectively eliminate diversity in practice and give preparers a consistent set of principles to apply or such transactions. However, the application of the definition of a business is judgemental and entities need to consider the definition carefully in such transactions. IFRS 10, IFRS 12 and IAS 28 Investment Entities: Applying the Consolidation Exception - Amendments to IFRS 10, IFRS 12 and IAS 28 Effective for annual periods beginning on or after 1 January 2016. Key requirements The amendments address issues that have arisen in applying the investment entities exception under IFRS 10. The amendments to IFRS 10 clarify that the exemption (in IFRS 10.4) from presenting consolidated financial statements applies to a parent entity that is a subsidiary of an investment entity, when the investment entity measures all of its subsidiaries at fair value. Furthermore, the amendments to IFRS 10 clarify that only a subsidiary of an investment entity that is not an investment entity itself and that provides support services to the investment entity is consolidated. All other subsidiaries of an investment entity are measured at fair value. The amendments to IAS 28 allow the investor, when applying the equity method, to retain the fair value measurement applied by the investment entity associate or joint venture to its interests in subsidiaries. Transition The amendments must be applied retrospectively. Early application is permitted and must be disclosed. Impact The amendments to IFRS 10 and IAS 28 provide helpful clarifications that will assist preparers in applying the standards more consistently. However, it may still be difficult to identify investment entities in practice when they are part of a multilayered group structure. IFRS 11 Accounting for Acquisitions of Interests inJoint Operations – Amendments to IFRS 11 Effective for annual periods beginning on or after 1 January 2016.

“KREDAQRO” CLOSED JOINT STOCK NON-BANKING CREDIT ORGANIZATION NOTES TO FINANCIAL STATEMENTS For the year ended 31 December 2015 (in Azerbaijani Manats)

19

5. ADOPTION OF NEW OR REVISED STANDARDS AND INTREPRETATIONS (Continued) Key requirements The amendments require an entity acquiring an interest in a joint operation in which the activity of the joint operation constitutes a business to apply, to the extent of its share, all of the principles in IFRS 3, and other IFRSs, that do not conflict with the requirements of IFRS 11. Furthermore, entities are required to disclose the information required in those IFRSs in relation to business combinations. The amendments also apply to an entity on the formation of a joint operation if, and only if, an existing business is contributedby the entity to the joint operation on its formation. Furthermore, the amendments clarify that for the acquisition of an additional interest in a joint operation in which the activity of the joint operation constitutes a business, previously held interests in the joint operation must not be remeasured if the joint operator retains joint control. Transition The amendments are applied prospectively. Early application is permitted and must be disclosed. Impact The amendments to IFRS 11 increase the scope of transactions that would need to be assessed to determine whether they represent the acquisition of a business or an asset, which would be highly judgemental. Entities need to consider the definition carefully and select the appropriate accounting method based on the specific facts and circumstances of the transaction. IFRS 14 Regulatory Deferral Accounts Effective for annual periods beginning on or after 1 January 2016. Key requirements IFRS 14 allows an entity, whose activities are subject to rate-regulation,to continue applying most of itsexistingaccountingpolicies for regulatory deferral account balances upon its first-timeadoption of IFRS. The standard does not apply to existing IFRS preparers. Also, an entity whose current GAAP does notallow the recognition of rate-regulated assets and liabilities,or that has not adopted such policy under its current GAAP,would not be allowed to recognise them on first-time applicationofIFRS.Entities that adopt IFRS 14 must present the regulatory deferralaccounts as separate line items on the statement of financialposition and present movements in these account balances asseparate line items in the statement of profit or loss and othercomprehensiveincome.The standard requires disclosures on the nature of, and risksassociated with, theentity’s rate regulation and the effects ofthat rate regulation on its financial statements. Transition Early application is permitted and must be disclosed. Impact IFRS 14 provides first-time adopters of IFRS with relief fromderecognising rate-regulated assets and liabilities until acomprehensive project on accounting for such assets andliabilities is completed by the IASB. The comprehensive rateregulatedactivities project is on the IASB’s active agenda. IAS 1 Disclosure Initiative – Amendments to IAS 1 Effective for annual periods beginning on or after 1 January 2016.

“KREDAQRO” CLOSED JOINT STOCK NON-BANKING CREDIT ORGANIZATION NOTES TO FINANCIAL STATEMENTS For the year ended 31 December 2015 (in Azerbaijani Manats)

20

5. ADOPTION OF NEW OR REVISED STANDARDS AND INTREPRETATIONS (Continued) Key requirements The amendments to IAS 1 Presentation of Financial Statementsclarify, rather than significantly change, existing IAS 1requirements. The amendments clarify • The materiality requirements in IAS 1 • That specific line items in the statement(s) of profit or lossand OCI and the statement of financial position may bedisaggregated • That entities have flexibility as to the order in which theypresent the notes to financial statements • That the share of OCI of associates and joint venturesaccounted for using the equity method must be presentedin aggregate as a single line item, and classified betweenthose items that will or will not be subsequently reclassifiedto profit or loss. Furthermore, the amendments clarify the requirements thatapply when additional subtotals are presented in the statement offinancial position and the statement(s) of profit or loss and othercomprehensive income. Transition Early application is permitted and entities do not need to disclosethat fact because the Board considers these amendments to beclarifications that do not affect an entity’s accounting policies oraccounting estimates. Impact These amendments are intended to assist entities in applyingjudgement when meeting the presentation and disclosurerequirements in IFRS, and do not affect recognition andmeasurement. IAS 16 and IAS 38 Clarification of Acceptable Methods of Depreciation and Amortisation –Amendments to IAS 16 and IAS 38 Effective for annual periods beginning on or after 1 January 2016. Key requirements The amendments clarify the principle in IAS 16 Property, Plantand Equipment and IAS 38 Intangible Assets that revenue reflectsa pattern of economic benefits that are generated from operatinga business (of which the asset is part) rather than the economicbenefits that are consumed through use of the asset. As a result,the ratio of revenue generated to total revenue expected to begenerated cannot be used to depreciate property, plant andequipment and may only be used in very limited circumstances toamortise intangible assets. Transition The amendments are effective prospectively. Early application is permitted and must be disclosed. Impact Entities currently using revenue-based amortisation methods forproperty, plant and equipment will need to change their currentamortisation approach to an acceptable method, such as thediminishing balance method, which would recognise increasedamortisation in the early part of the asset’s useful life. Revenuegenerated may be used to amortise an intangible asset only invery limited circumstances. IAS 16 and IAS 41 Agriculture: Bearer Plants –Amendments to IAS 16 and IAS 41 Effective for annual periods beginning on or after 1 January 2016.

“KREDAQRO” CLOSED JOINT STOCK NON-BANKING CREDIT ORGANIZATION NOTES TO FINANCIAL STATEMENTS For the year ended 31 December 2015 (in Azerbaijani Manats)

21

5. ADOPTION OF NEW OR REVISED STANDARDS AND INTREPRETATIONS (Continued) Key requirements The amendments to IAS 16 and IAS 41 Agriculture change thescope of IAS 16 to include biological assets that meet thedefinition of bearer plants (e.g., fruit trees). Agriculturalproduce growing on bearer plants (e.g., fruit growing on atree) will remain within the scope of IAS 41. As a result of theamendments, bearer plants will be subject to all the recognitionand measurement requirements in IAS 16 including the choicebetween the cost model and revaluation model for subsequentmeasurement.In addition, government grants relating to bearer plants will beaccounted for in accordance with IAS 20 Accounting for Government Grants and Disclosure of Government Assistance, instead of IAS 41. Transition Entities may apply the amendments on a fully retrospective basis.Alternatively, an entity may choose to measure a bearer plant atits fair value at the beginning of the earliest period presented.Earlier application is permitted and must be disclosed. Impact The requirements will not entirely eliminate the volatility in profitor loss as agricultural produce will still be measured at fair value.Furthermore, entities will need to determine appropriatemethodologies to measure the fair value of these assetsseparately from the bearer plants on which they are growing,which may increase the complexity and subjectivity of themeasurement. IAS 27 Equity Method in Separate FinancialStatements – Amendments to IAS 27 Effective for annual periods beginning on or after 1 January 2016. Key requirements The amendments to IAS 27 Separate Financial Statements allowan entity to use the equity method as described in IAS 28 toaccount for its investments in subsidiaries, joint ventures andassociates in its separate financial statements.Therefore, anentity must account for these investments either: • At cost • In accordance with IFRS 9 (or IAS 39) Or • Using the equity method The entity must apply the same accounting for each categoryof investments. A consequential amendment was also made to IFRS 1 First-timeAdoption of International Financial Reporting Standards. Theamendment to IFRS 1 allows a first-time adopter accounting forinvestments in the separate financial statements using the equitymethod, to apply the IFRS 1 exemption for past businesscombinations to the acquisition of the investment. Transition The amendments must be applied retrospectively. Earlyapplication is permitted and must be disclosed. Impact The amendments eliminate a GAAP difference for countries where regulations require entities to present separate financialstatements using the equity method to account for investmentsin subsidiaries, associates and joint ventures.

“KREDAQRO” CLOSED JOINT STOCK NON-BANKING CREDIT ORGANIZATION NOTES TO FINANCIAL STATEMENTS For the year ended 31 December 2015 (in Azerbaijani Manats)

22

5. ADOPTION OF NEW OR REVISED STANDARDS AND INTREPRETATIONS (Continued) IFRS 5 Non-Current Assets Held for Sale and Discontinued Operations Changes in methods of disposal • Assets (or disposal groups) are generally disposed of either through sale or distribution toowners. The amendment clarifies that changing from one of these disposal methods to theother would not be considered a new plan of disposal, rather it is a continuation of the original plan. There is, therefore, no interruption of the application of the requirements in IFRS 5. • The amendment must be applied prospectively. IFRS 7 Financial Instruments:DisclosuresServicing contracts • The amendment clarifies that a servicing contract that includes a fee can constitutecontinuing involvement in a financial asset. An entity must assess the nature of the fee andthe arrangement against the guidance for continuing involvement in IFRS 7.B30 andIFRS 7.42C in order to assess whether the disclosures are required. • The assessment of which servicing contracts constitute continuing involvement must bedone retrospectively. However, the required disclosures would not need to be providedfor any period beginning before the annual period in which the entity first applies theamendments. Applicability of the offsetting disclosures to condensed interim financial statements • The amendment clarifies that the offsetting disclosure requirements do not apply tocondensed interim financial statements, unless such disclosures provide a significantupdate to the information reported in the most recent annual report. • The amendment must be applied retrospectively. IFRS 15 Revenue from Contracts with Customers Effective for annual periods beginning on or after 1 January 2017. Key requirements IFRS 15 replaces all existing revenue requirements in IFRS (IAS 11 Construction Contracts, IAS 18 Revenue, IFRIC 13 Customer Loyalty Programmes, IFRIC 15 Agreements for the Construction of Real Estate, IFRIC 18 Transfers of Assets from Customers and SIC 31 Revenue – Barter Transactions Involving Advertising Services) and applies to all revenue arising from contracts with customers. It also provides a model for the recognition and measurement of disposal of certain non-financial assets including property, equipment and intangible assets. The standard outlines the principles an entity must apply to measure and recognise revenue. The core principle is that an entity will recognise revenue at an amount that reflects the consideration to which the entity expects to be entitled in exchange for transferring goods or services to a customer. The principles in IFRS 15 will be applied using a five-step model: 1. Identify the contract(s) with a customer 2. Identify the performance obligations in the contract 3. Determine the transaction price 4. Allocate the transaction price to the performance obligations in the contract 5. Recognise revenue when (or as) the entity satisfies a performance obligation The standard requires entities to exercise judgement, taking into consideration all of the relevant facts and circumstances when applying each step of the model to contracts with their customers. The standard also specifies how to account for the incremental costs of obtaining a contract and the costs directly related to

“KREDAQRO” CLOSED JOINT STOCK NON-BANKING CREDIT ORGANIZATION NOTES TO FINANCIAL STATEMENTS For the year ended 31 December 2015 (in Azerbaijani Manats)

23

5. ADOPTION OF NEW OR REVISED STANDARDS AND INTREPRETATIONS (Continued) fulfilling a contract. Application guidance is provided in IFRS 15 to assist entities in applying its requirements to certain common arrangements, including licences of intellectual property, warranties, rights of return, principal-versus-agent considerations, options for additional goods or services and breakage. Transition Entities can choose to apply the standard using either a full retrospective approach with some limited relief provided, or a modified retrospective approach. Early application is permitted and must be disclosed. Impact IFRS 15 is more prescriptive than current IFRS and provides more application guidance. The disclosure requirements are also more extensive. The standard will affect entities across all industries. Adoption will be a significant undertaking for most entities with potential changes to an entity’s current accounting, systems and processes. Therefore, it is important for entities to start assessing the impact early. In addition, as the IASB and FASB (together, the Boards) and the Joint Transition Resource Group for Revenue Recognition (TRG) continue to discuss implementation issues, it will be important for entities to monitor their discussions. IFRS 9 Financial Instruments Effective for annual periods beginning on or after 1 January 2018. Key requirements Classification and measurement of financial assets All financial assets are measured at fair value on initialrecognition, adjusted for transaction costs if the instrument isnot accounted for at fair value through profit or loss (FVTPL).Debt instruments aresubsequently measured at FVTPL,amortised cost or fair value through other comprehensive income(FVOCI), on the basis of their contractual cash flows and thebusiness model under which the debt instruments are held.There is a fair value option (FVO) that allows financial assets oninitial recognition to be designated as FVTPL if that eliminates orsignificantly reduces an accounting mismatch.Equity instruments are generally measured at FVTPL. However,entities have an irrevocable option on an instrument-by-instrumentbasis to present changes in the fair value of non-trading instrumentsin other comprehensive income (OCI) (without subsequentreclassification to profit or loss). Classification and measurement of financial liabilities For financial liabilities designated as FVTPL using the FVO, theamount of change in the fair value of such financial liabilities thatis attributable to changes in credit risk must be presented in OCI.The remainder of the change in fair value is presented in profit orloss, unless presentation of the fair value change in respect ofthe liability’s credit risk in OCI would create or enlarge anaccounting mismatch in profit or loss. All other IAS 39 Financial Instruments: Recognition andMeasurementclassification and measurement requirements forfinancial liabilities have been carried forward into IFRS 9,including the embedded derivative separation rules and thecriteria for using the FVO. Impairment The impairment requirements are based on an expected creditloss (ECL) model that replaces the IAS 39 incurred loss model.The ECL model applies to: debt instruments accounted for atamortised cost or at FVOCI; most loan commitments; financialguarantee contracts; contract assets under IFRS 15; and leasereceivables under IAS 17 Leases.Entities are generally required to recognise either 12-months’ orlifetime ECL, depending on whether there has been a significantincrease in credit risk since initial

“KREDAQRO” CLOSED JOINT STOCK NON-BANKING CREDIT ORGANIZATION NOTES TO FINANCIAL STATEMENTS For the year ended 31 December 2015 (in Azerbaijani Manats)

24

5. ADOPTION OF NEW OR REVISED STANDARDS AND INTREPRETATIONS (Continued) recognition (or when thecommitment or guarantee was entered into). For some tradereceivables, the simplified approach may be applied whereby thelifetime expected credit losses are always recognised. Transition Early application is permitted for reporting periodsbeginningafter 24 July 2014. The transition to IFRS 9 differsbyrequirements and is partly retrospective and partly prospective.Despite the requirement to apply IFRS 9 in its entirety, entitiesmay elect to apply early only the requirements for thepresentation of gains and losses on financial liabilities designatedas FVTPL without applying the other requirements in thestandard. Impact The application of IFRS 9 may change the measurement andpresentation of many financial instruments, depending on theircontractual cash flows and business model under which they are held.The impairment requirements will generally result in earlierrecognition of credit losses. The new hedging model may lead tomore economic hedging strategies meeting the requirements forhedge accounting. Unless otherwise described above, the new standards and interpretations are not expected to significantly affect the Company’s financial statements.

“KREDAQRO” CLOSED JOINT STOCK NON-BANKING CREDIT ORGANIZATION NOTES TO FINANCIAL STATEMENTS For the year ended 31 December 2015 (in Azerbaijani Manats)

25

6. CASH AND CASH EQUIVALENTS Cash and cash equivalents are comprised of the following:

In Azerbaijani Manats December 31, 2015 December 31, 2014 Cash in hand in national currency 9,315 6,037 Correspondent bank accounts in national currency 420,028 600,784 Correspondent bank accounts in foreign currency 317,363 290,304 Total cash and cash equivalents 746,706 897,125

7. DUE FROM BANKS This amount represents a deposit placed with a local bank USD 7,000,000 in December 2013, USD 2,000,000 in October 2014 and USD 2,000,000 in December 2014 for one year with interest rate 10% per annum. As at December 31, 2015 the amount of deposits was AZN 0 (2014: AZN 8,628,400). To avoid currency risk the Organisationhad placed deposits in the amount of USD 11,000,000 (AZN 8,628,400) and borrowed loans in the amount of AZN 8,197,645 with regard to mutual agreements signed with“Bank Technique” OJSC. Due to devaluation of Azerbaijani Manatthe Bank unilaterally cancelled the contract with the Organisationin 24 February 2015 and closed loan liabilities of the Organisationfrom those deposits with the rate of USD 0.7880/ AZN 1. The effect of this transaction on profit or loss is as follows:

Balance of deposit in USD Currrency Rate Balance of deposit in AZN

11,000,000 0.7880 8,668,000 11,000,000 1.0500 11,550,000

Effect on profit or loss (2,882,000) The foreign exchange loss of this transaction for the Organization is AZN 2,882,000.