konstantinovetal_planningforcleanup.compressed

TRANSCRIPT

1

KALINGA JAGODA, B.SC, PH.D.

Bissett School of Business, Management 4825 Mount Royal Gate SW

Calgary, AB T3E 3R9, Canada [email protected]

CARLTON-JAMES OSAKWE, B.SC., MBA, PH.D.

Bissett School of Business, Financial Services

4825 Mount Royal Gate SW Calgary, AB T3E 3R9, Canada

NICHOLAS KONSTANTINOV, BBA

192 Ranch Estates Dr NW Calgary, AB T3G 1K6, Canada

2

Abstract

Like most physical investments, pipelines have limited lifespans; natural deterioration such as

corrosion could and often does result in unexpected explosions or leaks. Disasters and terrorism

are other examples that contribute to the high risk of their implementation. Furthermore, despite

the low incident over total pipeline supply ratio, a fraction of failure could yield devastating and

expensive consequences. As a compromise between environmental sustainability and economic

growth, a self-insurance fund has been proposed to relieve concerns and compensate spill clean-

up and remediation efforts. Ideally, this fund will generate an efficient response system that

would contain hazardous material in a timely manner to reduce costs. This paper has introduced

and demonstrated a self-insurance contribution payment scheme attributed to crude oil pipeline

operators. Our proposed model constructed a quarterly contribution payment scheme under risk-

neutral settings to develop a self-insurance fund to cover oil spill clean-up and remediation costs.

The payments are the product of company risk profiles (assessed oil spill incident arrival rates

based on historical performance) and the expected clean-up costs per hundreds of kilometres of

pipeline. Utilising crude oil pipeline spill records provided by the Pipeline and Hazardous

Materials Safety Administration, this paper has provided a practical demonstration of our model.

Keywords: Oil spills, self-insurance, pipelines, model

3

Planning for clean-up: Self-insurance model for managing risk in petroleum pipelines

Pipelines from around the world are proving to be integral in the transportation logistics

of oil products and natural gas. They require low operation costs and produce miniscule pollution

relative to alternative methods such as tankers, trains, or trucks. This strengthens the competitive

advantage amongst operators through cost-effective means in a commodity-based industry. They

are seen as ‘safe’ havens by many insurance specialists (Meckbach, 2013), and the right direction

for countries proactively reducing their carbon footprint (Bjørnmose, Hansen, Roca, & Turgot,

2009). In addition, pipelines dominate in transport efficiency as their consistent capacities satisfy

petroleum production output and demand.

In contrast, this system is also highly capital intensive, inflexible, and unsuitable for all

regions. The high initial costs and slow return on investment necessitates long-term goal

projections, which is unattractive for operators wishing to cross politically unstable zones. This

is a problem for oil-rich regions such as Eastern Europe and the former Soviet-states, where the

threat of terrorism is often put into consideration before such initiatives (Behzadian, Belaud,

Kennedy, Pirdashti, & Tavana, 2012). Most importantly, like most physical investments,

pipelines have limited lifespans; natural deterioration such as corrosion could and often does

result in unexpected explosions or leaks. Avalanches, storms, floods and other disasters are

anticipated and response plans must be structured accordingly (Kurtz, 2010). Despite the low

incident over total pipeline supply ratio, a fraction of failure could yield devastating

consequences.

Many recent attempts to develop the transport infrastructure necessary for expansion in

Canada have been met with severe opposition. TransCanada's Keystone XL extension and

4

Enbridge's Northern Gateway pipeline have encountered strong resistance and political

difficulties, from environmental activists, First Nations' representatives, and farmer and landlord

associations. The former faces the indecisiveness of the American President and much of the

backlash that is against the pipeline's pathway through Nebraskan water reserves (Kashi, 2013;

Wieners, 2013).

The Northern Gateway is in a similar situation, and is fuelled with Enbridge's continued

remediation struggles of its Line 6B Kalamazoo River oil spill in Michigan from July, 2010

(Forest Ethics, n.d.). The proposed pipeline, offering transportation from Bruderheim, Alberta, to

a marine terminal in Kitimat, British Columbia (Enbridge Inc., 2013), is planned to cut through

sensitive mountainous terrain, various water flows, and First Nations territory (Forest Ethics,

n.d.). Despite the relative low risk of pipelines compared with alternative transportation methods

such as trains and trucks, the plan has become a growing dilemma between economic growth and

environmental protection (Meckbach, 2013).

As a compromise, the Northern Gateway joint review panel imposed that the company

must “provide a total coverage of $950 million for the costs of liabilities for, without limitation,

clean-up, remediation and other damages emanating from project operations”. The conditions

also require Enbridge to maintain a core financial coverage of $600 million through means such

as third-party liability insurance.

However, Enbridge is not alone. New regulations will adjure operators of major crude oil

pipelines to supply similar financial capabilities to support the costs of incidents (Meckbach,

2013). As $950 million has historically proved to be more than necessary to cover the average

substantial costs of remediation efforts (Meckbach, 2013), the development of an industry-wide

5

self-insurance program to spread the costs among all operators has been suggested (Cryderman,

2013). Through quarterly contributions to this 'superfund', operators will have the means to cover

costs without relatively capital intensive policies.

This paper will analyse the suggested self-insurance framework through a model inspired

by the deposit-insurance valuation demonstration by Duffie, Jarrow, Purnanandam, & Yang

(2003). It will begin with a literature review of selected studies and reports, a case of Canada’s

current pipeline dilemma, and an overview of the adjusted model. Concluding will be an applied

analysis using the model and raw data extracted from Canadian and American sources, and a

discussion of the results.

Literature Review

Piri (2013) focused on ex-post regulation of incident response and how to maximise

efficiency to reduce the impact of oil spills. The paper concluded that an effective regime is one

that holds the operator liable for all incurred costs, as the operator will perform in the less-costly

matter to secure full efficiency. In this case, the incident response must be supervised by

government official to satisfy environmental safety conditions. The company must prove that it

has the capability to perform adequate incident response actions prior to being issued a license,

and it must have a government approved emergency response plan preceding operations. This

strict liability regime is effective because the operator has self-interests to prevent or reduce

environmental damages due to the high sensitivity of impact toward profit.

Unlike vessel-source oil spills, pipeline spills have no international standards regarding

incident response. Policies vary in their quantification methods for assessing damages, and are

6

not required to include regulations either for the removal of oil, temporary storage of removed

oil, disposal of recovered oil, or environmental remediation. Nonetheless, responsibility is

generally classified in three ways: the operator is fully responsible for combating the oil spill; the

operator must conduct response actions as public authorities assist in the environmental

protection; and the public authorities must fully conduct the response actions (Piri, 2013).

Interference by the public authority is sometimes necessary, such as when the damage is

too great; however, this case leads to exponential costs due to additional administrative

functions. Therefore, it would be beneficial for the operator to avoid government efforts by

optimising the company’s response actions and preventative measures under a strict liability

regime (Piri, 2013).

Some regimes include insurance funds to cover incurred costs after a capped point.

Unfortunately, as contamination may take time to fully restore, operators could decline to

perform properly in due time as the moral hazard is dependent on the insurer. However, moral

hazard could be deterred due to the unpredictable nature of costs. If moral hazard could be

controlled, and if the liability regime covered all costs, then the operator will perform response

actions at the optimal level. If the costs exceed what is provided by the insurance, the incentives

to perform adequately are limited to how far the company could stretch its assets (Piri, 2013).

As an insurance to cover clean-up and remediation costs concerning oil spills, the US

authorised the Oil Spill Liability Trust Fund (OSLTF) through the Oil Pollution Act (OPA)

signed on 1990. This fund has a maximum limit of $1 billion, and functions toward: costs

incurred during clean-up and remediation for the coast guard and Environmental Protection

Agency (EPA), government access to perform remediation efforts and natural resource damage

7

assessments, payments of uncompensated removal costs, and research and development. It is

divided into two funds: the Emergency Fund, and the Principal Fund (United States Coast Guard,

2013).

The Emergency Fund is an annually recurring $50 million used by federal response

coordinators to initiate natural resource damage assessments. In addition, the Maritime

Transportation Security Act of 2002 enables officials to advance up to $100 million from the

Principal Fund in the case of insufficient capital (United States Coast Guard, 2013).

The Principal Fund is used to pay claims, compensate the administration and enforcement

of the OPA, and support research and development. Its revenue is gained through barrel tax,

which has been and is subject to continue increasing from 2009 until 2017, from 5 cents to 9

cents per barrel. Transfers from obsolete pollution funds have totalled $550 million, and U.S.

Treasury investments provide additional income. Those responsible for oil incidents are billed

for costs and damages which, along with fines and civil penalties, make up the remainder of the

Fund’s income (United States Coast Guard, 2013).

In banking, the United States was one of the first countries to implement a nationwide

deposit insurance program. Its deposit insurance is primarily governed by the Federal Deposit

Insurance Corporation (FDIC), an independent arm of the U.S. Congress. It was established in

1933 to provide assurance to depositors that they will be minimally impacted in the case of bank

failures. This is done through implementing a risk-based assessment system, managing the assets

of failed banks, liquidating troubled institutions, and monitoring banking organisations (Jickling

& Murphy, 2010).

8

Current policies enable banks to guarantee up to $250,000 per depositor in the case of a

failure. In circumstances of high systematic risk such as a recession, the FDIC may provide

additional alterations within emergency authority under the Federal Deposit Insurance

Corporation Improvement Act of 1991. For example in 2008, the FDIC declared guarantees on

newly issued senior unsecured debt of banking and trust organisations and on non-interest

deposit transaction accounts. Regulations require bank to draw up liquidation procedures, and

have strict minimum leverage capital requirements (3% and 4% for highly-rated and other

institutions, respectively) (Jickling & Murphy, 2010).

According to Wagster (2006), the application of deposit-insurance in Canada may have

reduced systematic risk in government organisations and increased non-systematic risk in

banking and trust organisations. Historically, high-risk institutions paid higher insurance

premiums than low-risk institutions. Therefore, the proposal of deposit insurance was viewed as

a poor choice by larger banks as it forced safe institutions to subsidise the actions of riskier

institutions through the flat-rate premium. In order to solve this problem, the safe institutions

increased their risk to match those of the riskier organisations.

The deposit insurance method aided this increase as the responsibility of monitoring was

realigned toward the Canadian Deposit Insurance Corporation (CDIC). Large-block shareholders

of banks, who were previously required to monitor each of their investments, were able to

diversify their portfolios without negatively affecting the institutions' share prices as expected

returns were increased (Wagster, 2006).

As suggested in the study, deposit insurance reduced the threat of loss to depositors

perhaps through the decrease in potential bank runs. The standard deviations of market returns

9

were shown to have decreased, therefore proving that systematic risk had been reduced. This

reduction in systematic risk justified the Government to absorb the non-systematic risk costs of

banks and trust companies without any significant increase in compensation (Wagster, 2006).

Despite the decrease in systematic risk, many researchers have agreed that the deposit

insurance model should be reformed (Bodie & Merton, 1993). Bank runs occur because banks

tend to borrow with a short-term perspective, such as demand deposits, and loan in the long-

term, such as mortgages. This creates a balance sheet mismatch which breaks down when

depositors return in large groups to reclaim their funds (McCoy, 2007). Although deposit

insurance significantly reduces the risk of bank runs and stop runs, McCoy (2007) states that its

implementation could also lead to unstable bank crises through an increase in moral hazard to

take risks.

Under explicit deposit insurance banks could capture profits while governments absorb

losses, and lower the incentives for depositors and shareholders to monitor the banks. Therefore,

this model fuels risk-taking and develops a “too big to fail” mindset within the banking industry

(McCoy, 2007).

In contrast to private insurance schemes, deposit insurance schemes do not have coverage

conditions that define preventable, and thus unqualified, risks. It covers all types of failures,

which amplifies the need for risk-reducing features. This could be addressed through coverage

limits based on the types of institutions, the types of deposits, and the maximum amount of

deposits that is guaranteed by the state (McCoy, 2007).

10

Arping (2010) argues that fair pricing is optimal in transparent banking systems, as the

guarantee premia accurately reflects the banks' risk-taking initiatives. Banks under opaque

systems require excessive resources to accurately display their guarantee premia to ensure fair

pricing, therefore risk-taking is a burden.

Boyd & Chang (2002) have studied the interest elasticity of the deposits and the

perceived risk of the bank. In the general equilibrium framework, banks that are perceived as

relatively safe would see positive growth in deposits through interest adjustment. Banks on the

other end of the spectrum will not benefit in this scenario without an increase in their risk profile;

otherwise they will face costs.

Bodie & Merton (1993) maintain that the current system unintentionally encourages

misallocation of investment, redistribution of wealth and income, unnecessary risk-taking, and

maybe even fraud and abuse. Currently, commercial banks perform two functions: execute loans

and guarantees, and take deposits. The loans are made to businesses, households, and

governments, and require thorough, non-public information for risk assessment and valuation.

Therefore the loans are illiquid and strapped with excessive bid-ask spreads.

However, this is creates instability in regards to the second function: accepting deposits.

Banks take two types of deposits from customers: transactional deposits, and savings deposits.

The transactional deposits enable customers to make payments while the banks act as

intermediaries that assess the eligibility of each party to commit with the exchanges. Thus

transactional deposits should be completely default-free (Bodie & Merton, 1993).

11

In short, Bodie & Merton (1993) recommend that deposit insurance should be

collateralised with government securities (eg, U.S. Treasury Bills) or their equivalent to ensure

liquidity. If this is not possible, their second option is to include monitoring fees and risk-based

premiums to deposits backed by volatile assets.

Similarly, Martin (2006) suggests replacing the deposit insurance with liquidity provision

policies set at the central bank. He justifies this by stating that under deposit insurance banks

fully gain from their successful risk-taking, however only partially lose if their risks fail. This

creates the moral-hazard. However, if the central banks were to implement liquidity provision

policies, the banks would be unaware of the results of their investments until after they repay

their loans.

Canadian Predicament

On April 29, 2011, Plains Midstream Canada, a subsidiary of Plains All American

Pipeline, contacted the Energy Resources Conservation Board (ERCB) to report the pipeline

failure and the release of 4500m3 of sweet crude oil from its NPS 20 Rainbow Pipeline at

approximately 20 km from Little Buffalo, Alberta (Energy Resources Conservation Board,

2013).

In the previous evening at around 18:35, Plains' Supervisory Control and Data

Acquisition (SCADA) system detected abnormal behaviour along the pipeline. Alerts continued

until 03:00 the next morning, after the pipeline was shutdown ten minutes prior at 02:50. A

helicopter was dispatched at 07:30 to locate the spill, which was in a muskeg area with no active

water flow, and a Level-1 emergency response plan was initiated by Plains. Stopples were

12

installed upstream and downstream from the tainted pipeline region and efforts were made to halt

the flow (Energy Resources Conservation Board, 2013).

Once contacted, the ERCB downgraded the spill as an alert, based on its significant

distance from residential areas and flowing waterways. However, it was reinstated to a Level-1

emergency following an inspection at 19:00 due to the 8.3 hectare impact to wildlife and

standing water. Environment Canada, Occupational Health and Safety, First Nations and Inuit

Health, and other relevant organisations, including a third-party engineering review firm, were

later contacted. By May 6, over 25 officials from various groups and organisations toured or

supervised the site regularly (Energy Resources Conservation Board, 2013).

The pipeline was approved for operation by August 26, 2011. The total cleanup required

26 contracting firms and 8 equipment suppliers, and on average up to 200 personnel on-site

throughout the response. The investigation concluded that the spill was caused by a failure of

Type B repair sleeves applied in the 1980s by the previous owner, Imperial Oil, which were

notorious for causing problems. Because of previous incidents, the National Energy Board

(NEB) required thorough and regular inspections of the Type B repair sleeves as per license;

unfortunately, the NPS 20 Rainbow Pipeline was out of its jurisdiction and did not either know

or follow these instructions (Energy Resources Conservation Board, 2013).

Canadian pipeline administration is demarcated at provincial and federal jurisdictions. In

Alberta, a province where virtually all of the nation’s oil pipeline activity is located, all intra-

provincial pipelines are monitored by the Alberta Energy Regulator (AER; formerly the ERCB).

Interprovincial or international pipeline activities, including tolls and tariffs, are subject to the

National Energy Board (NEB) (Cuschieri & Deyholos, 2013). Each pipeline proposal is

13

reviewed by the appropriate regulatory body and is subject to various socioeconomic and

environmental factors, including technological and financial feasibility. The regulators are

responsible for monitoring the planning, construction, and operation phases, and for ensuring

environmental protection throughout the lifespan of each project (Enbridge Inc., 2011).

In Canada, there are over 70,000 kilometers of pipeline running through the country and

across international borders to the United States, its main trading partner. It is estimated that

these pipelines transport around $127 billion of natural gas, natural gas liquids, crude oil, and

petroleum products each year. Canada is one of the only countries within the G-8 that has

considerable reserves of oil, and consumes about three quarters of its production levels. The

country is regarded as a net exporter of the product, most of which is transferred to its southern

neighbour (National Energy Board, 2013).

Unfortunately, a recent push in the production and mining of oil in the US has caused

great concern for Canadian policy makers and business owners. In addition to the increased

volatility and downward trend of prices, Canadian oil companies have to face discounted prices

when shipping to American states than otherwise if sent internationally (McCarthy &

Vanderklippe, 2012). With demand growing at high rate in non-OECD Asian countries such as

China, it could be a big opportunity for Canada to expand relationships with those regions

(National Energy Board, 2013).

The demand for petroleum products is increasing, yet its transportation involves an

indirect cost between the opposing forces of risk and reward. On the supposition that pipelines

are indeed the safest and the most cost-efficient out of all other petroleum transportation

methods, there must be compensation to mitigate the risk. One suggestion is a self-insurance

14

fund, provided by operators of pipelines, to assure adequate capital and coverage is available for

immediate response action and complete remediation.

Modelling using the Poisson Process

Consider relatively rare events occurring randomly and sporadically over a period of time

and/or space such as represented by the figure below:

Figure I

The events are called “relatively rare” because no two events will occur at exactly the

same moment in time or space. Examples of such rare events are the number of banks that go

bankrupt in a given month, the number of births of animals in a particular zoo during a year, the

number of calls to a telephone call-center in a one hour period, or the number of pipeline spills

over a three month period. The Poisson process is probably the most widely used random process

for modeling such rare events1.

1 For this process, time is generally expressed in years.

time 0 time t time s

occu

rren

ce

occu

rren

ce

occu

rren

ce

occu

rren

ce

15

Denote N(t) as the random number of occurrences observed within the time period [0, t].

Then, the formal definition of a Poisson process is that it is a non-decreasing stochastic counting

process N with the following properties:2

1) N(0) = 0

2) The process has stationary and independent increments. That is, for any two different

times s and t, let N(t) – N(s) denote the number of claims in the time interval [s, t]. Then

N(t) – N(s) is independent of N(t) – N(0) and the probability distribution of N(t) – N(s)

depends only on the length of the interval t – s

3) The number of occurrences N(t) in any interval [0, t] has a Poisson distribution with

mean λt. That is:

������ = �� = ����exp�−����!

The number λ is called the arrival rate or intensity of the Poisson process. That is, it is the

average number arrivals or occurrences per unit time which means that for any interval of size t,

λt is the expected number of occurrences in that interval. λ is sometimes called the hazard rate as

it also represents the instantaneous probability of the occurrence of an event at any point in time

(t), given no event has occurred prior to that time. In general, λ may be constant or be varying

over time and may also depend on a variety of factors.

2 Alternatively the Poisson process can be viewed as the arrival time or delays between any two occurrences with such a time

having an exponential distribution.

16

Estimating the Poisson arrival rate

Suppose we collect sample of n measured values ki with each value measured over the

same time period. We wish to estimate the value of the parameter λ of the Poisson population

from which the sample was drawn. To calculate the maximum likelihood value, we form the log-

likelihood function, the derivative of L with respect to λ and equate it to zero and solve for λ

yields the maximum-likelihood estimate of λ:

�� = 1�����

���

Thus, �� is just a sample average estimate the true mean arrival rate λ. From the sample,

percentiles or some other measure of position can also be estimated in the usual way to provide

additional descriptive statistics of λ.

Pricing deposit insurance

Duffie et al. (2003) demonstrated the use of a simple reduced form model of deposit

insurance where the default by a bank is the first occurrence of a Poisson process with a constant

arrival rate λ. Here λ is now called the default intensity and the (risk-neutral3) probability of the

bank surviving (not defaulting) up until time t is e–λt. The default intensity of different banks will

be different depending on the riskiness of their loan portfolios, their sensitivity to the state of the

economy, and so on.

3 The model is bases on the risk-neutral pricing approach (Harrison and Kreps, 1979) which uses adjusted probabilities so that the risk-free interest rate can be used as the discount rate. Duffie et al. (2003) demonstrate how to adjust the statistical estimates of the actual probability of default to get the risk neutral estimate.

17

If a bank defaults within the period (0, t), the level of losses that the insurance scheme

will have to pay bank depositors is denoted as L and depends on the dollar amount of assessed

insurable deposits less the percentage amount of these deposits that can be recovered from the

bank (the recovery rate) due to the bank’s level of capitalization. The figure below shows how

default rates and recovery rates have been changing over time. Although they appear to be

correlated, the simple model demonstrated by Duffie et al. (2003) assumes that for any particular

bank, both are constant and that across different banks, they are uncorrelated.

For a particular bank, let its default intensity be λ and the (risk-neutral) mean loss per

dollar of insurable deposit be E*[L] at the end of one year. Then, the current fair market deposit

insurance premium per dollar of insured deposits is:

� = ��∗���

1 !

Here, r is the risk free rate of interest and E*[ ] is the expectation based on risk-neutral

probabilities.

Figure II: Default rates and recovery rates on defaulted banks

18

As an example, suppose for a particular bank, the risk neutral default intensity is 0.02

and, based on the banks capitalization, the FDIC expects to pay out 10 cents on every dollar of

insured deposits if default occurs. Then, the fair-market deposit insurance premium can be

quotes as 0.02×0.1 = 0.002 or 20 basis points per annum. Assuming a risk free rate of zero, if the

bank has 100 million dollars of insured deposits and pays its premiums quarterly, then its deposit

insurance premium would be 0.25×0.002×100,000,000 = $50,000.

Extending the deposit insurance model to pipeline spills

Because both are relatively rare occurrences, the model for deposit insurance can be

extended to determine the superfund contributions for pipeline companies. Let δ be the

annualized arrival rate of pipeline spills per 100 kilometers of pipeline, and C be the cost of

cleanup if a spill occurs. We assume that arrival rates have been estimated across the pipeline

industry and divided by quartiles or some other distributional spacing4. The cleanup cost C will

depend on several factors such as pipeline pressure, valve spacing location of the pipeline and so

on. Pipeline companies can thus be categorized according to their spill risk level and expected

cleanup costs as below:

δ1 (low

risk)

δ3 δ3 δ4 (high

risk)

Heavy cleanup costs

Moderate cleanup

costs

Mild cleanup costs Table I

4 For example the spacing could be in 0.5 standard deviation increments.

19

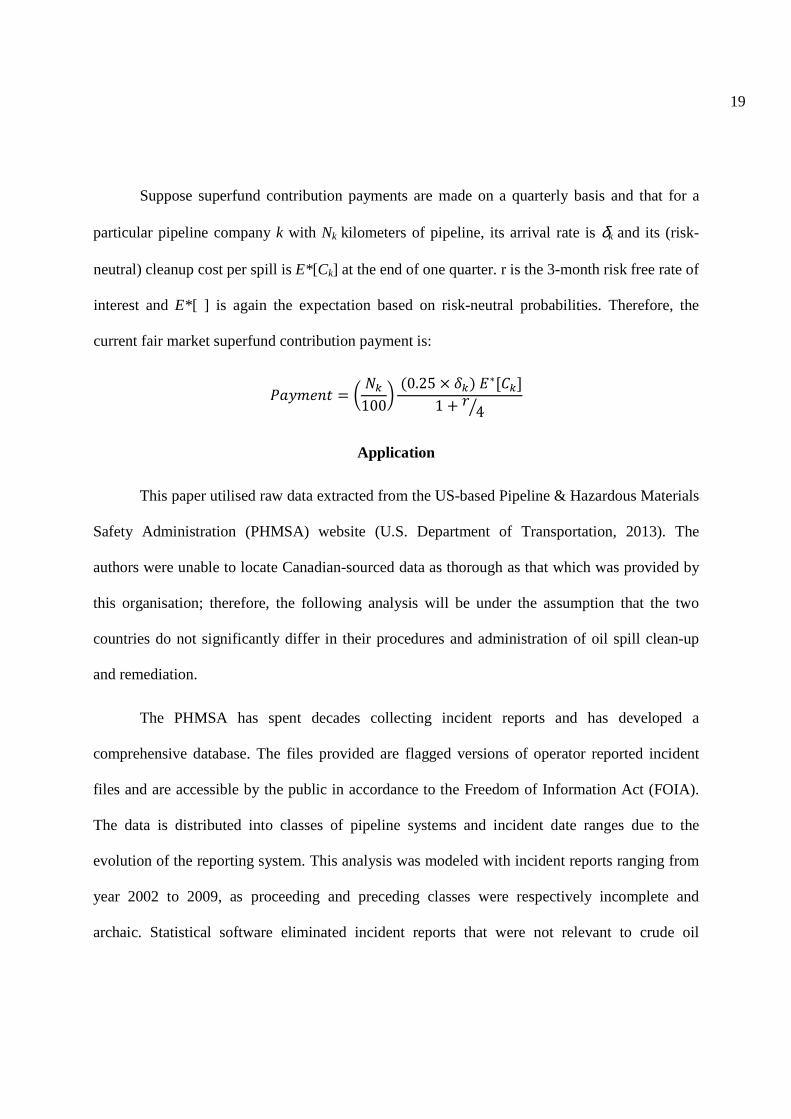

Suppose superfund contribution payments are made on a quarterly basis and that for a

particular pipeline company k with Nk kilometers of pipeline, its arrival rate is δk and its (risk-

neutral) cleanup cost per spill is E*[Ck] at the end of one quarter. r is the 3-month risk free rate of

interest and E*[ ] is again the expectation based on risk-neutral probabilities. Therefore, the

current fair market superfund contribution payment is:

�"#$%�� = & �'100)�0.25 × .'��∗[/']

1 + ! 41

Application

This paper utilised raw data extracted from the US-based Pipeline & Hazardous Materials

Safety Administration (PHMSA) website (U.S. Department of Transportation, 2013). The

authors were unable to locate Canadian-sourced data as thorough as that which was provided by

this organisation; therefore, the following analysis will be under the assumption that the two

countries do not significantly differ in their procedures and administration of oil spill clean-up

and remediation.

The PHMSA has spent decades collecting incident reports and has developed a

comprehensive database. The files provided are flagged versions of operator reported incident

files and are accessible by the public in accordance to the Freedom of Information Act (FOIA).

The data is distributed into classes of pipeline systems and incident date ranges due to the

evolution of the reporting system. This analysis was modeled with incident reports ranging from

year 2002 to 2009, as proceeding and preceding classes were respectively incomplete and

archaic. Statistical software eliminated incident reports that were not relevant to crude oil

20

pipeline spills and that had no reported clean-up or remediation costs. This narrowed the sample

size to 314 reported incidents.

The data was further split into annual quarters, each containing the sum of incidents

within their designated date range. This was a crucial first step in the Poisson distribution

analysis; it further initiated the development of the categorisation of payments per hundreds of

kilometers of pipeline and risk profile. Annual mileage of crude oil pipelines across the USA

between the years 2004 to 2009 was extracted from the PHMSA website and split and converted

into hundreds of kilometers of pipeline per year. The numbers of incidents per quarter were each

divided by their respective annual hundreds of kilometers of crude oil pipeline (years 2002 and

2003 were subject to the data from 2004); this function produced each quarter's arrival rate, δ.

Descriptive statistics of the arrival rates and the total damage costs of each reported

incident were generated. Of the former's statistics, the first quartile, median, and third quartile

were used to represent low, medium, and high risk arrival rates, respectively. Heavy, moderate,

and mild clean-up costs were also designated according to their percentiles.

Finally, to emulate a risk-neutral estimation, each product was divided by one plus the

quarter of the 3-month Canadian Treasury Bill rate. At the time of this writing the 3-month T-

Bill return was at 0.90%.

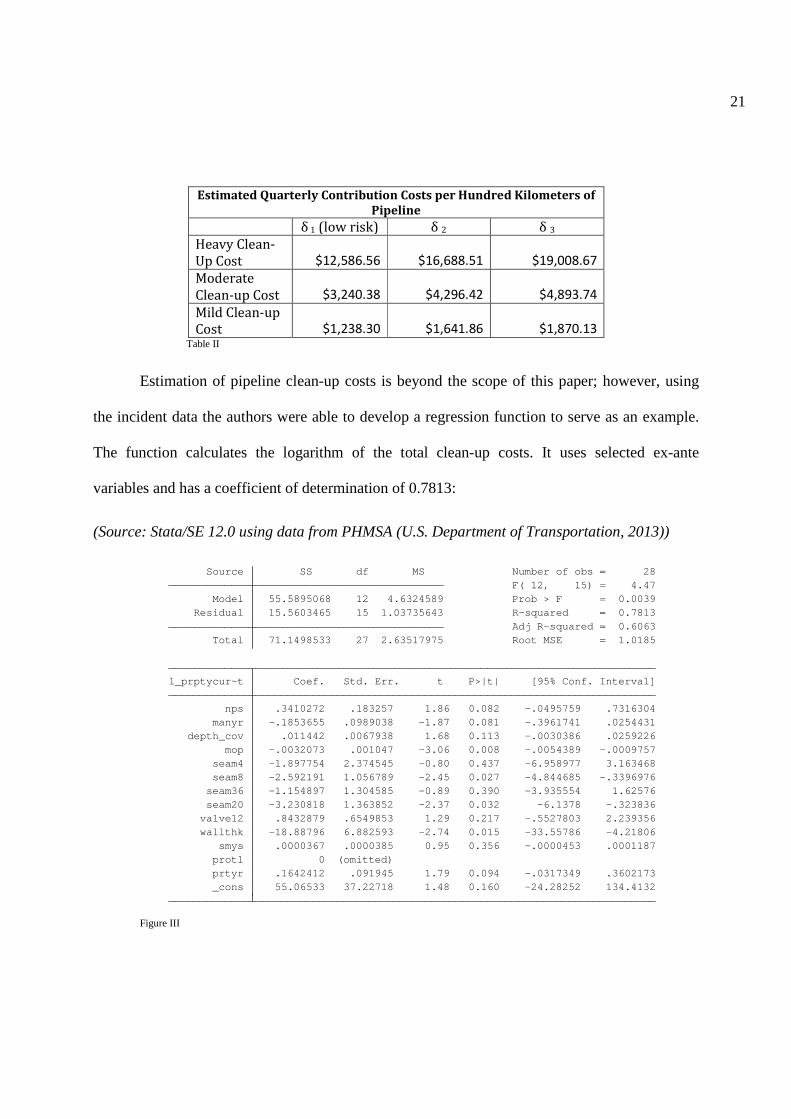

21

Estimated Quarterly Contribution Costs per Hundred Kilometers of

Pipeline

δ 1 (low risk) δ 2 δ 3 Heavy Clean-

Up Cost $12,586.56 $16,688.51 $19,008.67

Moderate

Clean-up Cost $3,240.38 $4,296.42 $4,893.74

Mild Clean-up

Cost $1,238.30 $1,641.86 $1,870.13 Table II

Estimation of pipeline clean-up costs is beyond the scope of this paper; however, using

the incident data the authors were able to develop a regression function to serve as an example.

The function calculates the logarithm of the total clean-up costs. It uses selected ex-ante

variables and has a coefficient of determination of 0.7813:

(Source: Stata/SE 12.0 using data from PHMSA (U.S. Department of Transportation, 2013))

Figure III

_cons 55.06533 37.22718 1.48 0.160 -24.28252 134.4132 prtyr .1642412 .091945 1.79 0.094 -.0317349 .3602173 prot1 0 (omitted) smys .0000367 .0000385 0.95 0.356 -.0000453 .0001187 wallthk -18.88796 6.882593 -2.74 0.015 -33.55786 -4.21806 valve12 .8432879 .6549853 1.29 0.217 -.5527803 2.239356 seam20 -3.230818 1.363852 -2.37 0.032 -6.1378 -.323836 seam36 -1.154897 1.304585 -0.89 0.390 -3.935554 1.62576 seam8 -2.592191 1.056789 -2.45 0.027 -4.844685 -.3396976 seam4 -1.897754 2.374545 -0.80 0.437 -6.958977 3.163468 mop -.0032073 .001047 -3.06 0.008 -.0054389 -.0009757 depth_cov .011442 .0067938 1.68 0.113 -.0030386 .0259226 manyr -.1853655 .0989038 -1.87 0.081 -.3961741 .0254431 nps .3410272 .183257 1.86 0.082 -.0495759 .7316304 l_prptycur~t Coef. Std. Err. t P>|t| [95% Conf. Interval]

Total 71.1498533 27 2.63517975 Root MSE = 1.0185 Adj R-squared = 0.6063 Residual 15.5603465 15 1.03735643 R-squared = 0.7813 Model 55.5895068 12 4.6324589 Prob > F = 0.0039 F( 12, 15) = 4.47 Source SS df MS Number of obs = 28

22

To clarify, the prediction function of l_prptycurrent (the logarithm of the total property

damage and remediation costs adjusted for inflation) utilises several selected variables listed

above. These variables were chosen based on their p-value (P>|t|) and their impact on the overall

function (R-Squared). Generally a p-value less than one is preferable, however there were some

exceptions made due to the effect on the coefficient of determination. The function below was

developed by extracting the coefficients (Coef.) of each variable:

2345657896:5: = 55.06533 .1642412�#%"!3=>3$?3�%��@�A�"22"�@3��+ .0000367�A?%>@=@%C$@�@$D$#@%2CA�!%�4�ℎ�− 18.88796�?@?%H"22�ℎ@>��%AA@�@�>ℎ%A�+ .8432879�CD$$#3=I"2I%�#?%12�− 3.230818�CD$$#3=A%"$�#?%20�− 1.154897�CD$$#3=A%"$�#?%36�− 2.592191�CD$$#3=A%"$�#?%8� − 1.897754�CD$$#3=A%"$�#?%4�− .0032073�$"�@$D$3?%!"�@�4?!%AAD!%�+ .011442�C%?�ℎ3=>3I%!@�@�>ℎ%A� − .1853655�#%"!>3$?3�%��$"�D=">�D!%C�+ .3410272��3$@�"2?@?%A@J%@�@�>ℎ%A�

As a takeaway: provided that there is enough information available, insurance specialists

would have no problem developing reliable estimations. The risk profile could be based on the

specified company and its historical incident arrival rate.

23

Therefore, a company with a low risk profile and a pipeline that is expecting moderate

clean-up costs should pay quarterly contributions at around $3,240.38 per hundreds of kilometers

of pipeline. For example, Company A owns roughly 20,000 km of pipelines; each pipeline has

approximately the same expected clean-up costs at mild levels, and the company has a medium

risk level. It was concluded Company A should contribute around $328,372.41 each quarter or

$1.3 Million per year.

Discussion

While the above calculations proved that it is possible to develop a system of contribution

payments toward the oil-spill superfund using Poisson distribution, there are still limitations that

require work beyond this paper. For instance, the processed data was a hybrid collection of both

American and Canadian sources. In order to be effective in the Canadian system, the data used

for the calculations of the arrival rate and average total costs must be provided by the pipeline

regulatory bodies. Whether in cooperation with the National Energy Board, the provincial

regulators, or another branch designed for the collection of oil spill data, information must be

congruent in order to optimise the accuracy of the payments.

Another setback is the calculation of the expected clean-up costs. The majority of

information provided by the operator incident files was ex-post, therefore unusable for predictor

functions. The remaining information suitable for predictions was not sufficient enough to create

a regression function that could effectively predict expected clean-up costs.

Finally, this paper merely examines the creation of the superfund through established

contribution payments based on risk profiles, estimated clean-up costs, and pipeline lengths.

24

Additional research is required in order to develop policies regarding the utilisation of the fund

to minimalize quality deficiencies, such as moral hazard. The absence of significant penalties

and fines and the realisation of sunk payments into an insurance fund may increase the risk-

taking of operators. This is a crucial problem and may be addressed through insurance caps,

clean-up deductibles, insurance coverage conditions, or fund reimbursement systems.

Conclusion

In conclusion, this paper adjusted the Duffie et al. (2003) valuation model of deposit

insurance using Poisson distribution and applied it toward a self-insurance method for oil

pipeline coverage. It included a literary review of relevant studies and reports, a case preview of

Canadian pipeline controversy, an overview of insurance modeling with Poisson distribution,

and an application and discussion of the model. While this is only a first step in pipeline self-

insurance, the authors are hopeful that this will inspire further research.

25

Reference List

Arping, S. (2010). The pricing of bank debt guarantees. Economics Letters, 108(2), 119-121.

Behzadian, M., Belaud, J., Kennedy, D. T., Pirdashti, M., & Tavana, M. (2012). A hybrid delphi-

SWOT paradigm for oil and gas pipeline strategic planning in Caspian Sea basin. Energy

Policy, 40, 345-360.

Bjørnmose, J., Hansen, D. S., Roca, F., & Turgot, T. (2009, August). An assessment of the gas

and oil pipelines in Europe. Retrieved from

http://www.europarl.europa.eu/RegData/etudes/note/join/2009/416239/IPOL-

ITRE_NT(2009)416239_EN.pdf

Bodie, Z., & Merton, R. C. (1993). Deposit insurance reform: A functional approach. Carnegie-

Rochester Conference Series on Public Policy, 38, 1-34.

Boyd, J. H., & Chang, C. (2002). Deposit insurance: A reconsideration. Journal of Monetary

Economics, 49(6), 1235-1260.

Cryderman, K. (2013, June 18). Enbridge proposes spill fund to ease pipeline fears. The Globe

and Mail. Retrieved from http://www.theglobeandmail.com/report-on-business/industry-

news/energy-and-resources/enbridge-proposes-spill-fund-to-ease-pipeline-

fears/article12620689/

Cuschieri, D., & Deyholos, R. (2013, January). Oil & gas: A comparative guide to the regulation

of oil and gas projects. The European Lawyer. Retrieved from

http://www.torys.com/Publications/Publications/AR2013-1.pdf

Duffie, D., Jarrow, R., Purnanandam, A., & Yang, W. (2003). Market pricing of deposit

insurance. Journal of Financial Services Research, 24(2/3), 93-119.

26

Enbridge Inc. (2011). Pipeline regulations: Canada. Retrieved from

http://www.northerngateway.ca/assets/pdf/General%20Project%20-

%20Regulatory/NGP-FS-01-007_Pipeline%20Regulations%20Canada.pdf

Enbridge Inc. (2013). Route map – Northern Gateway. Retrieved from

http://www.northerngateway.ca/project-details/route-map/

Energy Resources Conservation Board. (2013, February 26). ERCB investigation report: Plains

Midstream Canada ULC, NPS 20 Rainbow pipeline failure, April 28, 2011. Retrieved

from http://www.aer.ca/documents/reports/IR_20130226-PlainsMidstream.pdf

Forest Ethics. (n.d.). The issue – Enbridge’s proposed Northern Gateway pipeline and tanker

project threatens North America. Retrieved from http://forestethics.org/enbridge-issue

Harrison, J., Kreps, D. (1979). Martingales and arbitrage in multiperiod securities markets.

Journal of Economic Theory, 20(3), 381-408.

Jickling, M., & Murphy, E. V. (2010). Who regulates whom? An overview of U.S. financial

supervision. Congressional Research Service. Retrieved from

https://owl.english.purdue.edu/owl/resource/560/10/

Kashi, D. (2013, November 15). Environmental groups' latest weapon against Keystone XL:

How a pipeline explosion is helping the fight against Keystone. International Business

Times. Retrieved from http://www.ibtimes.com/environmental-groups-latest-weapon-

against-keystone-xl-how-pipeline-explosion-helping-fight-against

Kurtz, R. S. (2010). Oil pipeline regulation, culture, and integrity. Public Integrity, 13(1), 25-40.

Martin, A. (2006). Liquidity provision vs. deposit insurance: Preventing bank panics without

moral hazard. Economic Theory, 28(1), 197-211.

27

McCarthy, S., & Vanderklippe, N. (2012, November 12). Canada sees risk in U.S. oil boom. The

Globe and Mail. Retrieved from http://www.theglobeandmail.com/report-on-

business/industry-news/energy-and-resources/canada-sees-risk-in-us-oil-

boom/article5188639/

McCoy, P. A. (2007, February 18). The moral hazard implications of deposit insurance: Theory

and evidence. Retrieved from

http://www.imf.org/external/np/seminars/eng/2006/mfl/pam.pdf

Meckbach, G. (2013). Down the pipe. Canadian Underwriter, 80(8), 28-31.

National Energy Board. (2013). Canadian pipeline transportation system – Transportation

assessment. Retrieved from http://www.neb-one.gc.ca/clf-

nsi/rnrgynfmtn/nrgyrprt/trnsprttn/trnsprttnssssmnt2009/trnsprttnssssmnt2009-eng.html

Natural Resources Canada. (2009). Frequently asked questions. Retrieved from

http://www.nrcan.gc.ca/energy/sources/crude/1287

Piri, M. (2013). Responsibility for response to oil pipeline accidents and its co-relation to the

liability; what would be an effective regime? Retrieved from

https://www.genevaassociation.org/media/623348/ga_15th_eale_seminar_piri.pdf

Polzin, P. E. (2012). Transportation systems key to Montana's energy future. Montana Business

Quarterly, 50(2), 8-11.

Shaffer, E. H. (2006). Canada's oil and imperialism. International Journal of Political Economy,

35(2), 54-71.

United States Coast Guard. (2013). The Oil Spill Liability Trust Fund. Retrieved from

http://www.uscg.mil/npfc/About_NPFC/osltf.asp

28

U.S. Department of Transportation. (2013). Pipeline incidents and mileage reports. Retrieved

from http://primis.phmsa.dot.gov/comm/reports/safety/psi.html

Wagster, J. D. (2006, January 13). Wealth and risk effects of adopting deposit insurance in

Canada: Evidence of risk shifting by banks and trust companies. Retrieved from

http://www.efmaefm.org/efma2006/papers/393153_full.pdf

Wieners, B. (2013, November 13). Have Keystone XL opponents found their best weapon?

Bloomberg Business Week. Retrieved from http://www.businessweek.com/articles/2013-

11-13/have-keystone-xl-opponents-found-their-best-weapon