knowledge sharing forum on technology in … forum...the knowledge sharing forum on technology in...

TRANSCRIPT

Knowledge Sharing Forum on

Technology in Microinsurance

Summary Report

Alisa Hotel, Accra, Ghana

June 4-5, 2013

i

Summary Report: Knowledge Sharing Forum on the Impact of Health Microinsurance

The Knowledge Sharing Forum on Technology in Microinsurance was organized by the ILO

Microinsurance Innovation Facility, together with CGAP and MicroEnsure, as the Facility celebrates five

years of pushing the frontiers in microinsurance. To learn more about the celebration, visit our website

at www.ilo.org/microinsurance.

Table of Contents1 Forum Overview ......................................................................................................................................................... 1

Forum Theme ......................................................................................................................................................... 1

Forum Objectives ................................................................................................................................................... 1

Forum Agenda ........................................................................................................................................................ 1

Key Messages from the Forum .............................................................................................................................. 2

Introductions .............................................................................................................................................................. 3

Technological developments in microinsurance: An Overview ................................................................................. 3

Theme 1: Technology solutions for enrolment .......................................................................................................... 5

1.1 Smart card technology ................................................................................................................................. 5

1.2 Mobile phones ............................................................................................................................................. 6

Theme 2: Support technology for microinsurance .................................................................................................... 8

2.1 Technology for data management ............................................................................................................... 8

2.2 Technology for transaction processing ........................................................................................................ 9

2.3 Technology for process enhancement ......................................................................................................... 9

Theme 3: Technology for claims handling ............................................................................................................... 10

Wrap-up and closing ................................................................................................................................................ 12

Annex A. List of Forum Participants ......................................................................................................................... 14

1 The organizers would like to thank CENFRI for their contributions in producing this Summary Report.

1

Summary Report: Knowledge Sharing Forum on Technology in Microinsurance

Forum Overview

Forum Theme “Technology as an enabler for improving client value and sustainability in microinsurance”

Forum Objectives a) Provide a platform for sharing good and bad practices and lessons learned in the use of various

technological solutions to support the microinsurance value chain;

b) Take stock of and discuss specific technological solutions used by participating organizations in the

area of microinsurance; and

c) Explore next practices that can benefit the wider microinsurance sector.

Forum Agenda DAY 1: 4 June

09:00 – 09:30 Registration

09:30 – 10:30 Opening remarks and introductions (facilitator: ILO Microinsurance Innovation Facility)

10:30 –12:15 Technological developments in microinsurance: An overview (facilitator: CGAP

Technology and Business Model Innovation Team)

Camilo Tellez, CGAP, USA

Peter Zetterli, CGAP, Ghana

Michiel Berende, Microinsurance Network Technology Working Group, Netherlands

Anju Aggarwal, Leapfrog Investments, United Kingdom 12:15 – 13:30 Lunch

13:30 – 17:00 THEME 1: Technologies for enrolment (with webcast) (facilitator: ILO Microinsurance

Innovation Facility)

Pranav Prashad, ILO Microinsurance Innovation Facility, Switzerland

Sanjay Pande, Amicus Advisory Private Ltd, India

Eugene Adogla, MicroEnsure, Ghana

Camilo Tellez, CGAP, USA

Jasmin Suministrado, ILO Microinsurance Innovation Facility, Switzerland

17:00 – 17:30 Wrap-up of Day 1 (facilitator: ILO Microinsurance Innovation Facility)

19:00 Organized dinner and networking

DAY 2: 5 June

09:00 – 09:30 Recap of Day 1 (facilitator: ILO Microinsurance Innovation Facility)

09:30 – 12:30 THEME 2: Support technologies in microinsurance (facilitator: Berende Consulting)

Eugene Adogla, MicroEnsure, Ghana

Brenda Wandera, International Livestock Research Institute, Kenya

Devendra Shahapurkar, FINO Fintech, India

Michiel Berende, Microinsurance Network Technology Working Group, Netherlands

12:30 – 14:00 Lunch

2

Summary Report: Knowledge Sharing Forum on Technology in Microinsurance

14:00 – 17:00 THEME 3: Technologies for claims handling (facilitator: MicroEnsure)

Eugene Adogla, MicroEnsure, Ghana

Emeka Ajanwachuku, Uba Nwogu and Cees Hesp, PharmAccess / Hygeia, Nigeria/Netherlands

Alok Shukla, Tata AIG General Insurance Co., India

Sanjay Pande, Amicus Advisory Private Ltd, India

17:00 – 18:00 Forum wrap-up (facilitator: ILO Microinsurance Innovation Facility)

Key Messages from the Forum Attended by 42 participants from insurance companies, consulting companies, technology and solutions

providers, donors and investment companies, the Forum provided a platform to discuss the following key

messages:

Technology can play a vital role in enhancing the microinsurance processes across the value chain.

However, the introduction of technology has to be accompanied by a change in processes for

benefits to be realized. The choice of the technology should also be made in light of factors such as

its alignment with the objectives of the partners involved, the degree of market maturity and

readiness for the technology, and customer understanding of the product. (see “Overview Session”

on page 3)

Smart cards show promises in improving microinsurance operations – for instance, a reduction from

45-60 days to 25 minutes in a pilot project; an 8% increase in enrolment; reduction of fraud, and the

ability to carry out paperless transaction. Among the biggest challenges though are limited data

storage, client education, and limited availability of hardware suppliers. (see Section 1.1 on page 5)

Mobile phones-based microinsurance has grown significantly over the past three years, particularly

in Africa. It is still primarily used for life microinsurance, as it remains a challenge to offer more

complicated products such as health and agriculture products using mobile phones. And while

providing the microinsurance product for free seems to be a good starting point, experience suggests

the need to shift to paid products before it starts losing value for customers. (see Section 1.2 on page

6)

On technology for data management, it is important for data such as those generated using

satellites to be easily understood by customers, e.g., the presentation of vegetation data using color

codes. To ensure validity of data, government plays a key role. (see Section 2.1 on page 8)

Transaction processing technology requires standard codes and processes so that information

generated by different systems of partners can be seamlessly integrated. (see Section 2.2 on page 9)

Benefits can be derived from the use of certain technologies for process enhancements such as the

use of mobile phones for training the sales force. In this example, agents are kept up-to-date on the

products they sell, improving both their sales efforts and the ability to communicate value to their

clients. (see Section 2.3 on page 9)

The shift from a manual system to technology-enabled claims management can improve data

quality, reduce documentation requirements, hasten claims settlement, and reduce fraud. However,

some of the issues that should be addressed include connecting to legacy systems, high cost of

software development and training, ensuring clients understand the technology and the

accompanying processes, and low computer proficiency at healthcare facilities in the case of health

microinsurance. (see “Theme 3” on page 10)

3

Summary Report: Knowledge Sharing Forum on Technology in Microinsurance

Participants during the Introductions session

Resource persons in the Overview Session

Introductions

The Forum was opened with remarks from the

ILO Microinsurance Innovation Facility, and the

two co-organizers CGAP and MicroEnsure. All

organizers expressed their eagerness to

understand the variety of work being done

around the use of technology for different

products and across the microinsurance value

chain, as well as their excitement on the sharing

that will happen over the next two days.

A sociometric activity was used to introduce

participants and to set the interactive format of

the forum. Participants expressed their ideas

and insights on various questions including their

organization’s role in microinsurance, their

organization’s satisfaction with the technology

they use in microinsurance operations, and their expectations from the Forum. When asked to choose which

emoticon best represents their organization’s satisfaction with the technology they are using, majority of the

participants chose a thoughtful emoticon (as opposed to a smiling, grinning, or sad one), and explained that

while they are satisfied to a certain extent, they are eager to learn more about the actual benefits it delivers

and how to continuously improve. In terms of Forum expectations, participants see the forum as a venue to

learn from each other, share lessons, and find solutions to issues and challenges.

Technological developments in microinsurance: An Overview

The first session held on day one sought to provide an overview of technological developments in

microinsurance. Organized and moderated by Camilo Tellez from CGAP, the resource persons were Peter

Zetterli from CGAP, Michiel Berende from Berende Consulting representing the Technology Working Group

of the Microinsurance Network, and Anju Aggarwal from Leapfrog Investments. As the resource persons

proceeded with their sharing, a consensor tool was used to capture live feedback from the audience on

numerous polls about technology.

Peter Zetterli from CGAP started with a sharing of key

findings from a global market scan involving 63 mobile

phone-based microinsurance products to identify

patterns on how mobile phones are being used across

the microinsurance value chain over the past few years,

and explore where it is headed in the future. About 70%

of the products surveyed used mobile phones to initiate

registration, although less than half of these allow full

registration over phones. Around 85% use mobile

phones for premium payment, and almost 90% send out

policy information over the phone (though less

4

Summary Report: Knowledge Sharing Forum on Technology in Microinsurance

commonly for policy administration). In terms of geography, it has been observed that over half of mobile-

phone based insurance schemes operates in Sub-Saharan Africa, where 10 new products where launched in

2012 alone.

In terms of composition, mobile phone based-insurance products remain heavily focused around life

products, which account for 70% of active products as opposed to roughly 8% for health. Products tend to

offer very simple benefits rather than tiered coverage, and they have largely been tied directly to a mobile

network operator. Peter cited the fact that 60% are paid products, while 33% are free products, which can

be further subdivided into passive loyalty where the product is provided by the mobile network operator

(MNO) in return for post-paid voice loyalty, and active loyalty products where insurance is offered to

incentivize various kinds of behaviours (e.g., more frequent use of mobile money, increase savings balance,

etc.). The presentation concluded with a look at the untapped market for future growth in mobile insurance

products, with the largest potential market in East Asia.

Following Peter’s informative presentation, Michiel Berende presented on his work with the Microinsurance

Network’s (MIN) Technology Working Group, which since 2008 has been working on the development of a

technology inventory for microinsurance, allowing practitioners and other interested parties to filter

technology solutions across a number of categories. Located on the MIN’s website

(http://www.microinsurancenetwork.org/Technology-Inventory/), the inventory currently houses

information on 26 technology solutions. The MIN Technology working group is also currently working on the

Microinsurance Open Source Initiative (MOSI), which will create and promote open source technology. The

presentation concluded with a debate on how to achieve scale in microinsurance with Michiel highlighting

the importance of standardization, harmonization, and interoperability.

Shifting gears, Anju Aggarwal shared on Leapfrog’s investments and portfolio management for seven

microinsurance players. She cited how mobile technology has improved customer service, distribution, and

transactions in microinsurance products. Posing the question “How should we focus on making customer

perspectives much more important on the development of technology innovations?”, the audience had a

lively debate with some questioning whether customers can accurately articulate their needs regarding

technology. Others argued that insurance products must innovate and then see whether the market accepts

it. It was largely agreed that those products which are built around customer needs are much more easily

accepted once they reach the market.

To close the session, Camilo led a brief question-and-answer session between the audience and the panel of

speakers. Peter commented on how MNOs have largely shaped the mobile phone based insurance space

and have in some cases become the largest insurers in certain countries. He further noted that failure of

mobile insurance products could have devastating effects on the industry. The discussion then shifted to

partnerships in mobile insurance products, with Anju sharing that each partner must have a distinct role and

Peter noting that the more partners you bring on board, the harder it is for a product to be viable. Camilo

closed the discussion citing the importance of alignment of all partners’ objectives.

In the final live poll, an overwhelming number of participants (84%) believed that an insurance company’s

technological roadmap should be one of the top five priority areas for its CEO. Although perhaps not

surprising at a technology forum, this conclusion illustrated the importance the participants gave to

technology, and paved the way for a number of very participatory and engaging sessions for the remainder

of the event.

5

Summary Report: Knowledge Sharing Forum on Technology in Microinsurance

Panelists in the webinar session on “Technology: Improving the enrolment experience”

Theme 1: Technology solutions for enrolment

The first thematic session of the event focused on how technology can be used in enrolment and included a

webinar for external audiences moderated by Jasmin Suministrado of the ILO’s Microinsurance Innovation

Facility with panellists Sanjay Pande, Director of Amicus Advisory Services in India, Eugene Adogla,

MicroEnsure Regional Operations Manager for Africa, Camilo Tellez of the CGAP Technology and Business

Model Innovation Team, and Pranav Prashad of the ILO’s Microinsurance Innovation Facility. To watch the

webinar recording, please visit: http://www.youtube.com/watch?v=4dexU97ymLM&feature=youtu.be. A

summary of the session is also provided below.

1.1 Smart card technology

After a discussion of main hurdles for enrolment

– on education and awareness; infrastructure;

and identification – facilitated by Pranav, Sanjay

presented on the smart card technology that

Amicus Advisory Services developed for the

RSBY National Health Insurance Scheme in India

and a pilot health microinsurance scheme in

2012. Sanjay explained that the Smart Card

technology was implemented to help identify

eligible participants for the two schemes and

reduce fraud. The scheme was suffering from

two types of fraud: (i) Identity fraud, i.e. saying

you are one person when you are really

another and (ii) collaborative fraud between

agents, beneficiaries and hospitals where they charge for higher operations that were administered and

pocketed the additional revenue.

The biometric smart card supports identification for enrolment. It is a standard issue plastic card with a 64

MB chip that stores family details, finger prints and photos. Each family member has a distinctive number

that is encrypted in the card. The card can be used at almost all 10,000 hospitals that have been networked

to honour the cards. Each of the hospitals is equipped with the necessary hardware: (i) card reader (ii)

desktop computer to show the details of the card and (iii) biometric fingerprints to confirm the card.

To enrol for the card, the administrators of the government-sponsored schemes inform eligible participants

of where and when enrolment will take place. The administrator has the basic client information from the

Indian census that identifies who is below the national poverty line. Previous issues with fictitious data can

be picked up at enrolment (for example age, name, and gender) and amended on the spot with the smart

card.

The impact of the smart card technology has been impressive. Sanjay explained that in the pilot health

microinsurance project that was migrated from a manual system to a smart card system, they have observed

a reduction in waiting time for enrolment from 45-60 days to 25 minutes and an 8% increase in the

enrolment ratio. In addition to saving time, enrolment costs have been reduced by US$ 0.15 per client in the

pilot project. However, there are still challenges. The location and timing of the enrolment period is limited,

6

Summary Report: Knowledge Sharing Forum on Technology in Microinsurance

Break out discussion on smart cards hosted by Sanjay Pande of Amicus Advisory

potentially leaving many left out. On the technology side, participants are still intimated by technology and

operational constraints such as intermittent or lack of power supply and internet connectivity remain.

In the breakout discussions following the

webinar, one of the issues discussed was

the replicability of the smart card success.

Sanjay commented that while there may

be issues with replication given the unique

context of identification fraud in India,

companies encountering similar issues

that are operating in countries where

census data or a national identity scheme

is in place, can benefit significantly.

1.2 Mobile phones

Eugene Adogla from MicroEnsure and Camilo Tellez from CGAP presented their experience with using the

mobile phone in microinsurance enrolment and payment. Eugene started his presentation by highlighting

that microinsurance growth in Africa has been mobile. Microinsurance grew 200% from 2010-2012 with 8 of

9 markets outside of South Africa reaching 1 million insured lives through mobile insurance. Mobile phones

offer customer access, a financial transaction platform, a reputable and trusted brand and a cost-effective

information transfer source.

Camilo introduced the different business models and subsequent payment mechanisms for mobile insurance

that they have discovered in CGAP’s study of 63 mobile insurance products: (i) passive loyalty (ii) active

loyalty and (iii) the paid model. As explained in the previous section, passive loyalty schemes are those

products offered free of charge by MNOs in return for post-paid voice loyalty. Active loyalty is when a

product is offered to not just increase loyalty but to incentivize other kinds of behaviours such as buying

more airtime. CGAP’s research found that these two models make up about two thirds of the mobile

insurance offerings globally. The last model is the payment model which could be either a top-up of an

existing loyalty scheme, referred to as a freemium model, or a full premium model. Payments can be either

airtime based or mobile money based, with the former making up the majority of the market.

Eugene from MicroEnsure introduced the challenges with mobile insurance schemes for both the MNO and

the insurer. He highlighted that in certain markets it is important to offer free products for a certain period,

but once you’ve grown the pool of consumer through a free product (perhaps over a span of 18 to 24

months), there is a need to transition to a paid product. In the case of the Tigo Bima product in Ghana, a

“freemium” product combining the free product with a small premium payment was introduced to offer

better coverage.

Eugene concluded by introducing the challenges encountered in offering mobile insurance. Clients are often

illiterate and are not familiar with using the mobile phone for value added services beyond voice. In addition,

technologies are not fail-safe and there is the potential that an SMS is not delivered or the USSD server goes

down. He suggested that there is a need for good backups with either human agents or telecom service

centres.

7

Summary Report: Knowledge Sharing Forum on Technology in Microinsurance

Break out discussions on mobile phones for microinsurance hosted by Camilo Tellez and Peter Zetterli of CGAP (left) and by Eugene Adogla of MicroEnsure (right)

Small group discussions amongst participants after the webinar revolved around the following:

Free products are not necessarily loss making, but can lose value over time, making it difficult then to

reach new clients with a free model.

There are other schemes where mobile phone usage is coupled with other products or other benefits

to reach more clients. For example, Bradesco in Brazil uses a lottery ticket component to incentivize

potential clients to purchase insurance. M-PANI, also in Brazil, signs up a community to one telecom

service and the community is then provided water pipe benefits based on how much airtime they

use in a year.

Mobile phone technology is not an enrolment solution for every market. In India, regulation does not

allow the use of mobile phones for money transfers which inhibits collection of insurance premiums.

In Nigeria, mobile money can only be provided via third parties and not by MNOs, creating an

additional layer that lends itself to inefficiencies.

Limited technological infrastructure is a common characteristic among the developing countries,

providing challenges for sufficient mobile network coverage and internet connectivity. In India, such

limitations do not help in collecting data/premiums back from the microinsurance agents, who use

mobile phone platforms, especially when they operate in remote areas. There is still a gap between

the available technology solutions and the operational requirements, and infrastructure limitations

still hinder the wide use of different technological inventions in microinsurance enrolment.

In Nigeria, fraud was making it so challenging to offer hospitalization products. Eugene shared that

while mobile based insurance can contribute to scale, it may be challenging to verify each and every

case. Costs need to be considered while verifying claims for remote customers.

The session concluded with the understanding that technology can significantly improve the enrolment

efforts in microinsurance, but this must not be viewed as a stand-alone initiative. The need to support

enrolment technologies with not only education, but back-end processes is critical. Cooperation between

the various stakeholders is essential to make this happen, and they must align their incentives for greater

likelihood of success.

8

Summary Report: Knowledge Sharing Forum on Technology in Microinsurance

Fishbowl session to discuss support technology for microinsurance

Theme 2: Support technology for microinsurance

The second thematic session focused on support technologies in microinsurance. The session was moderated

by Michiel Berende of the Microinsuance Network Technology Working Group and panellists included

Eugene Adogla from MicroEnsure, Ghana who focused on transaction technology, Brenda Wandera from the

International Livestock Research Institute (ILRI), Kenya who focused on data management technology, and

Devendra Shahpurkar from FINO Paytech, India who focused on technology to enhance business processes.

The session allowed for a brief presentation of each type of support technology, and discussions were then

encouraged using a fishbowl method.

2.1 Technology for data management

Brenda kicked-off the presentations by introducing the work ILRI had done in developing an index-based

livestock insurance product in rural Kenya and Ethiopia. She explained that ILRI found livestock-related

deaths were one of the biggest problems for rural households in Kenya and identified microinsurance as

being a good solution. IRLI used satellite imagery combined with other available data to develop an index-

based livestock insurance product to meet the needs of the rural households. The parameters of index

insurance contract are based on climate levels that were correlated with livestock-related illness or death. In

Kenya, they use satellite data on vegetation trends for contracts. Claims are paid when forage scarcity is

predicted to cause livestock deaths in an area. In Ethiopia the index insurance contracts are based on the

deviation of availability of land for raising livestock from the long-run average.

Participants were interested in understanding how ILRI had overcome the challenge related to data accuracy.

Brenda explained that ILRI uses a trusted source in the NASA satellite data that is updated every 16 days, and

confirms the data with the community representatives. In addition, to address illiteracy concerns ILRI uses

colour codes to identify areas that would be paid out to the community. However, there are challenges with

complexity—the product is not very easy to understand and explaining community satellites to rural

communities in Kenya have been difficult. ILRI recognizes that it is important for communities to understand

what is being used to calculate their pay-outs and with continuous effort, education is starting to improve.

On the issue of sustainability, Brenda explained that for the scheme to be sustainable, the government or a

neutral third-party such as the national remote sensing unit needs to be involved. While it is a costly process,

9

Summary Report: Knowledge Sharing Forum on Technology in Microinsurance

it promotes data integrity that might be an issue if the technology resides with insurance companies. In this

set-up, data can simply be sold to insurance companies.

On the question of replicability, Brenda explained that as it is not in ILRI’s mandate to be a practitioner, it is

now creating a process manual that codifies the whole process that other people can take and use. They are

also busy mentoring institutions that can continue their work.

2.2 Technology for transaction processing

Eugene’s presentation focused on supporting the link between local back-end processes and central

administration technology. MicroEnsure has a global MIS team in Cheltenham, United Kingdom, that

manages data for all MicroEnsure’s clients using its proprietary ARK system. The MicroEnsure operations in

Ghana can access the central server through web-based interfaces and upload their data. MicroEnsure has

developed a new software that standardizes all the information to link up local servers (where these are

deployed) to the global system. He explained that they have codified and scheduled the process to increase

efficiency. It defines how and when the information will be shared to link the local server deployments with

the central server.

Eugene explained that sharing of information is scheduled upfront and the systems talk to each other

periodically to ensure that what is in the local server is in the global server. When the system is down, a red

flag is triggered and there is then a manual process to fix-it (though this can be done remotely over the

Internet). Also, necessary data exports can be sent through secure FTP transfer processes as a back-up. The

challenge MicroEnsure now faces is with on-boarding the old yet relevant client data onto the new platform.

2.3 Technology for process enhancement

Devendra then discussed the use of mobile phones, in addition to in-person interaction, to train its agents.

He explained that by becoming a corporate agent for a non-life insurance company, FINO addresses possible

regulatory concerns on selling insurance products. It then keeps its on-field sales force updated and trained

through mobile phone.

To support their agents, FINO developed mIT, an

application for insurance training on mobile phones.

mIT is easy to access and free to download – there is

no login ID and password required. The module can

be used by any agent irrespective of the network

service provider. This helps keep agents up-to-date

on the products they are selling, improving both

their sales efforts and ability to communicate value

to their clients.

The use of mobile phones is something that ILRI had

also done to support its agents. ILRI initially tried to use point of sale (POS) devices with their agents to

collect payments from rural communities, but found it was too expensive with each POS device costing US$

12,500 on-average.

Subsequently, ILRI introduced a very basic java enabled phone that agents can buy as an investment into

their operations (costing less than US$100). However, the processes around collection of premium required

an agent to place a deposit with the insurer besides investment in the handset which limited the cash flow at

10

Summary Report: Knowledge Sharing Forum on Technology in Microinsurance

Resource persons on the use of technology solutions for claims management

the agent’s end. To overcome this, ILRI selected only trusted shopkeepers from whom no deposit was

required to collect the premium and sell to the community.

The session concluded with Michiel identifying challenges that still remain despite the improvements that

are resulting from the innovations discussed:

Insurance contracts based on data provided by satellites require funding and good understanding by

the target customers, both of which can be a challenge in the rural communities where

microinsurance is most needed.

It is important to have standardized processes when linking back-end processes through technology,

but having a back-up is important.

Finally, the mobile phone offers a great opportunity for efficient and improved agent management,

but it needs to be done in a cost-effective way and still be complemented with a human touch.

Theme 3: Technology for claims handling

In the third thematic session, the focused shifted

from enrolment and support technology to the use

of technology for claims handling. Eugene Adogla

from MicroEnsure facilitated the session, with

panelists Cees Hesp, Emeka Ajanwachuku and Uba

Nwogu from PharmAccess and Hygeia from the

Netherlands and Nigeria, respectively; Sanjay Pande

from Amicus Advisory in India, and Alok Shukla from

Tata AIG in India.

The session was kicked off with a mapping of

challenges in claims management, with claims

understood as the actual test of fulfilling the promise

of the microinsurance products. While this doesn’t

mean that all claims have to automatically be paid, it

is important that that the claims payment process be

transparent and fair. Challenges in claims recording,

claims approval, and claim settling were shared by

participants. Some of the common challenges that

arose included:

Trying to keep turnaround time as short as possible;

Controlling fraud;

The difficulty both in securing documentation and paying out claims for rural clients, and

Validating the coverage and the claim.

With the map of challenges setting the stage, presentations started with Cees Hesp from PharmAccess in the

Netherlands and Uba Nwogu from Hygeia Healthcare in Nigeria. PharmAccess has partnered with Hygeia to

subsidize health insurance, improve healthcare facilities, and ultimately determine how to extend greater

access to quality healthcare for Nigerians. Cees highlighted a number of challenges that the project has

experienced thus far such as the difficulties of managing communication and objectives when there are

11

Summary Report: Knowledge Sharing Forum on Technology in Microinsurance

Participants break out into smaller groups in a role play aimed at identifying solutions to claims handling challenges

many partners involved in a project. They also discussed how Hygeia handled claims initially with paper

forms and eventually shifted to a custom-built front office solution with adequate problem analysis. As

technologies like fingerprint identification were introduced, claims processing times have decreased. While

technology has improved data quality and processing, challenges still remain with trying to connect to legacy

systems and addressing low computer proficiency at healthcare facilities. Based on lessons learned with

Hygeia, PharmAccess is now establishing national and federal standards in Kenya, Tanzania, and 9 states in

Nigeria.

Following the presentation by PharmAccess, Alok Shukla from Tata AIG presented on how technology was

used to improve the provision of livestock insurance in India. Tata AIG partners with dairies, microfinance

institutions (MFIs), and non-government organizations to cover over 300,000 animals as of 2012. Given the

issues of high loss, high fraud, and vast geography, Tata introduced mobile technologies that translated to

several benefits – i.e., data to be relayed in real time from field to server, policy issuance time to decrease,

claims settlement to quicken, on-spot carcass verification, and decreased fraud. Even though challenges like

high cost of software development and training remain, Tata is showing that strong processes and field

controls can bring down fraud in a high-risk insurance field.

As the final speaker of the session, Sanjay Pande from Amicus spoke about his organization’s work with

smart cards on the RSBY National Health Insurance Scheme in India. In RSBY, smart cards created benefits for

all parties involved including hospitals, insurers, beneficiaries, and government. Essentially the smart cards

have resolved identification and verification problems (see Section 1.1 for more details), allowed for the shift

to cashless treatment, enabled real-time tracking of insurance policies, and permitted the availability of

medical history at multiple points. Nevertheless, challenges remain in the areas of data storage limitations,

stigma surrounding new technologies, and operational constraints like power and internet supplies. Despite

these, the experience of Amicus in India shows that technologies like smart cards can serve to increase

efficiencies and improve customer experience in large-scale insurance products.

Following the presentations, participants were challenged to come up with possible solutions to common

problems across four broad categories: documentation, validation, fraud control, and turnaround time. In

terms of documentation, participants suggested standardized templates and decentralized data collection to

ease the process clients must go through to submit claims. To improve claims validation and fraud control,

12

Summary Report: Knowledge Sharing Forum on Technology in Microinsurance

Insights shared by the participants at the end of the Forum

the group highlighted technologies that can audit and highlight suspicious claims. Similarly, the use of

biometric data and creating links to partner databases like MNOs or MFIs can help validate information.

Finally, to improve turn-around time in the claims process, participants suggested clearing out low-value

claims by quickly approving with less scrutiny, payment through distribution channels, and reducing

bureaucracy.

In conclusion, while technological solutions for claims management will vary by the type of product and the

environment in which it operates, the session illustrated the potential is there for technology to greatly

improve claims processing through increased efficiency, decreased fraud, and improved customer service.

Wrap-up and closing At the end of day 2, participants identified take away insights that they can explore in their work to improve

microinsurance both from the business and the client perspective. Some of the insights, classified according

to the three main themes of the Forum, are:

Insights related to enrolment technology solutions:

o Third party administrators should invest in standardized and flexible mobile-based enrolment (and claims management) software to facilitate the use of technology and maintain operational efficiency.

o Developing strategic partnerships with MNOs is a key factor in building scale of insurance

programs.

o Mobile payment platforms should be integrated with mobile insurance solutions to provide

end-to-end services, including claims settlement.

Insights related to support technology:

o It is important to standardize data collection processes.

o There is a need for marketing & sales support in awareness campaigns and data collection.

o Interoperability, the ability of partners’ systems to integrate seamlessly, is key.

Insights related to claims management technology:

o Mobile phones can be used to submit the claims form and dispatch the claim amount when

documents are complete.

o Technology helps in rethinking the claims process in terms of documents collection,

archiving, and claims payment.

13

Summary Report: Knowledge Sharing Forum on Technology in Microinsurance

For further comments on the Knowledge Sharing Forum on Technology in Microinsurance, please email us

at - [email protected].

14

Summary Report: Knowledge Sharing Forum on Technology in Microinsurance

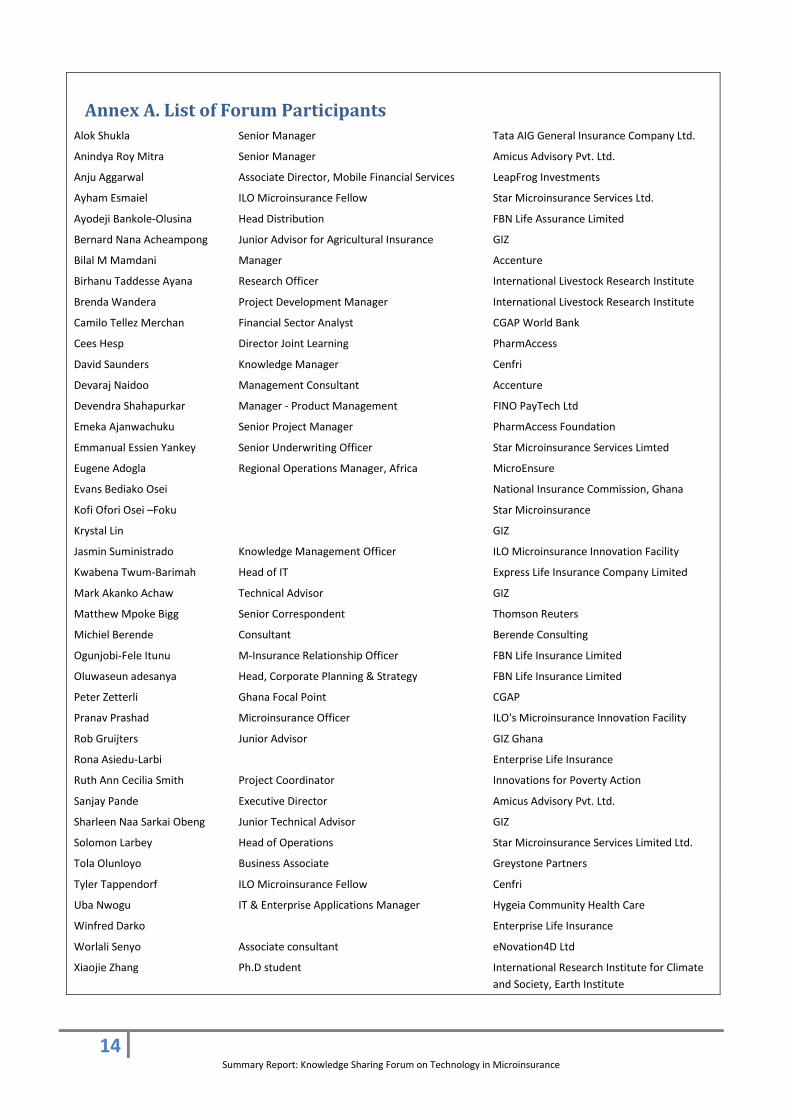

Annex A. List of Forum Participants

Alok Shukla Senior Manager Tata AIG General Insurance Company Ltd.

Anindya Roy Mitra Senior Manager Amicus Advisory Pvt. Ltd.

Anju Aggarwal Associate Director, Mobile Financial Services LeapFrog Investments

Ayham Esmaiel ILO Microinsurance Fellow Star Microinsurance Services Ltd.

Ayodeji Bankole-Olusina Head Distribution FBN Life Assurance Limited

Bernard Nana Acheampong Junior Advisor for Agricultural Insurance GIZ

Bilal M Mamdani Manager Accenture

Birhanu Taddesse Ayana Research Officer International Livestock Research Institute

Brenda Wandera Project Development Manager International Livestock Research Institute

Camilo Tellez Merchan Financial Sector Analyst CGAP World Bank

Cees Hesp Director Joint Learning PharmAccess

David Saunders Knowledge Manager Cenfri

Devaraj Naidoo Management Consultant Accenture

Devendra Shahapurkar Manager - Product Management FINO PayTech Ltd

Emeka Ajanwachuku Senior Project Manager PharmAccess Foundation

Emmanual Essien Yankey Senior Underwriting Officer Star Microinsurance Services Limted

Eugene Adogla Regional Operations Manager, Africa MicroEnsure

Evans Bediako Osei National Insurance Commission, Ghana

Kofi Ofori Osei –Foku Star Microinsurance

Krystal Lin GIZ

Jasmin Suministrado Knowledge Management Officer ILO Microinsurance Innovation Facility

Kwabena Twum-Barimah Head of IT Express Life Insurance Company Limited

Mark Akanko Achaw Technical Advisor GIZ

Matthew Mpoke Bigg Senior Correspondent Thomson Reuters

Michiel Berende Consultant Berende Consulting

Ogunjobi-Fele Itunu M-Insurance Relationship Officer FBN Life Insurance Limited

Oluwaseun adesanya Head, Corporate Planning & Strategy FBN Life Insurance Limited

Peter Zetterli Ghana Focal Point CGAP

Pranav Prashad Microinsurance Officer ILO's Microinsurance Innovation Facility

Rob Gruijters Junior Advisor GIZ Ghana

Rona Asiedu-Larbi Enterprise Life Insurance

Ruth Ann Cecilia Smith Project Coordinator Innovations for Poverty Action

Sanjay Pande Executive Director Amicus Advisory Pvt. Ltd.

Sharleen Naa Sarkai Obeng Junior Technical Advisor GIZ

Solomon Larbey Head of Operations Star Microinsurance Services Limited Ltd.

Tola Olunloyo Business Associate Greystone Partners

Tyler Tappendorf ILO Microinsurance Fellow Cenfri

Uba Nwogu IT & Enterprise Applications Manager Hygeia Community Health Care

Winfred Darko Enterprise Life Insurance

Worlali Senyo Associate consultant eNovation4D Ltd

Xiaojie Zhang Ph.D student International Research Institute for Climate

and Society, Earth Institute