kimberly clark corp -...

TRANSCRIPT

KIMBERLY CLARK CORP

FORM 10-K(Annual Report)

Filed 02/24/10 for the Period Ending 12/31/09

Address 351 PHELPS DRIVE

IRVING, TX 75038Telephone 9722811200

CIK 0000055785Symbol KMB

SIC Code 2670 - Converted Paper And Paperboard Products, ExceptIndustry Paper & Paper Products

Sector Basic MaterialsFiscal Year 12/31

http://www.edgar-online.com© Copyright 2010, EDGAR Online, Inc. All Rights Reserved.

Distribution and use of this document restricted under EDGAR Online, Inc. Terms of Use.

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549

FORM 10-K

(Mark One)

SECURITIES EXCHANGE ACT OF 1934

[X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

For the fiscal year ended December 31, 2009

OR

SECURITIES EXCHANGE ACT OF 1934

� � � � TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

For the transition period from to

Commission file number 1-225

KIMBERLY -CLARK CORPORATION (Exact name of registrant as specified in its charter)

Delaware 39-0394230 (State or other jurisdiction of

incorporation or organization) (I.R.S. Employer

Identification No.)

P. O. Box 619100, Dallas, Texas 75261-9100 (Address of principal executive offices) (Zip Code)

Registrant’s telephone number, including area code: (972) 281-1200

Securities registered pursuant to Section 12(b) of the Act:

Title of each class

Name of each exchange on which registered

Common Stock—$1.25 Par Value New York Stock Exchange

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes . No � .

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes � . No .

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes . No � .

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes . No � .

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer Accelerated filer � Non-accelerated filer � (Do not check if a smaller reporting company) Smaller reporting company �

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes � . No .

The aggregate market value of the registrant’s common stock held by non-affiliates on June 30, 2009 (based on the closing stock price on the New York Stock Exchange) on such date was approximately $21.7 billion.

As of February 12, 2010, there were 416,305,736 shares of the Corporation’s common stock outstanding.

Documents Incorporated By Reference

Certain information contained in the definitive Proxy Statement for the Corporation’s Annual Meeting of Stockholders to be held on April 29, 2010 is incorporated by reference into Part III hereof.

Table of Contents

KIMBERLY-CLARK CORPORATION

TABLE OF CONTENTS

Page

Part I

Item 1. Business 1 Item 1A. Risk Factors 4 Item 1B. Unresolved Staff Comments 9 Item 2. Properties 9 Item 3. Legal Proceedings 9 Item 4. Submission of Matters to a Vote of Security Holders 10

Part II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities 13 Item 6. Selected Financial Data 14 Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations 15 Item 7A. Quantitative and Qualitative Disclosures About Market Risk 34 Item 8. Financial Statements and Supplementary Data 36 Item 9. Changes in and Disagreements with Accountants on Accounting and Financial Disclosure 88 Item 9A. Controls and Procedures 88 Item 9B. Other Information 91

Part III

Item 10. Directors, Executive Officers and Corporate Governance 92 Item 11. Executive Compensation 92 Item 12. Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters 93 Item 13. Certain Relationships and Related Transactions, and Director Independence 94 Item 14. Principal Accountant Fees and Services 94

Part IV

Item 15. Exhibits, Financial Statement Schedules 95

Signatures 98

Table of Contents

PART I ITEM 1. BUSINESS

Kimberly-Clark Corporation was incorporated in Delaware in 1928. The Corporation is a global company focused on leading the world in essentials for a better life through product innovation and building its personal care, consumer tissue, K-C Professional & Other and health care brands. The Corporation is principally engaged in the manufacturing and marketing of a wide range of essential products to improve people’s lives around the world. Most of these products are made from natural or synthetic fibers using advanced technologies in fibers, nonwovens and absorbency. As used in Items 1, 1A, 2, 3, 6, 7, 7A, 8 and 9A of this Form 10-K, the term “Corporation” refers to Kimberly-Clark Corporation and its consolidated subsidiaries. In the remainder of this Form 10-K, the terms “Kimberly-Clark” or “Corporation” refer only to Kimberly-Clark Corporation. For financial information by business segment and geographic area, and information about principal products and markets of the Corporation, reference is made to Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and to Item 8, Note 20 to the Consolidated Financial Statements. Recent Developments

During the first quarter of 2009, the Corporation acquired the remaining approximate 31 percent interest in its Andean region subsidiary, Colombiana Kimberly Colpapel S.A. (“CKC”), for $289 million. During the second quarter of 2009, the Corporation acquired Jackson Products, Inc. (“Jackson”), a privately-held safety products company, for approximately $155 million, net of cash acquired. The acquisition of Jackson is consistent with the Corporation’s global business plan strategy to accelerate growth of high-margin workplace products sold by its Kimberly-Clark Professional business. During the fourth quarter of 2009, the Corporation acquired Baylis Medical Company’s pain management business (“Baylis”). The Corporation’s Health Care business has been the exclusive distributor of these pain management products in the U.S. since 2001. Also during the fourth quarter of 2009, the Corporation acquired I-Flow Corporation (“I-Flow”), a healthcare company that develops and markets drug delivery systems and products for post-surgical pain relief and surgical site care, for $262 million, net of cash acquired. The Baylis and I-Flow acquisitions are consistent with the Corporation’s global business plan strategy to invest in the higher-growth, higher-margin medical device market. See Item 8, Note 6 to the Consolidated Financial Statements for a discussion of the acquisitions.

In June 2009, the Corporation announced actions to reduce its worldwide salaried workforce by approximately 1,600 positions by the end of 2009. These actions resulted in cumulative pretax charges of approximately $128 million in 2009. See Item 8, Note 4 to the Consolidated Financial Statements for a discussion of the organization optimization initiative. Description of the Corporation

The Corporation is organized into operating segments based on product groupings. These operating segments have been aggregated into four reportable global business segments: Personal Care; Consumer Tissue; K-C Professional & Other; and Health Care. The reportable segments were determined in accordance with how the Corporation’s executive managers develop and execute the Corporation’s global strategies to drive growth and profitability of the Corporation’s worldwide Personal Care, Consumer Tissue, K-C Professional & Other and Health Care operations. These strategies include global plans for branding and product positioning, technology, research and development programs, cost reductions including supply chain management, and capacity and capital investments for each of these businesses.

The principal sources of revenue in each of our global business segments are described below. Revenue, profit and total assets of each reportable segment are shown in Item 8, Note 20 to the Consolidated Financial Statements.

1

Table of Contents

PART I (Continued)

The Personal Care segment manufactures and markets disposable diapers, training and youth pants, and swimpants; baby wipes; feminine and incontinence care products; and related products. Products in this segment are primarily for household use and are sold under a variety of brand names, including Huggies, Pull-Ups, Little Swimmers, GoodNites, Kotex, Lightdays, Depend, Poise and other brand names.

The Consumer Tissue segment manufactures and markets facial and bathroom tissue, paper towels, napkins and related products for household use. Products in this segment are sold under the Kleenex, Scott, Cottonelle, Viva, Andrex, Scottex, Hakle, Page and other brand names.

The K-C Professional & Other segment manufactures and markets facial and bathroom tissue, paper towels, napkins, wipers and a range of safety products for the away-from-home marketplace. Products in this segment are sold under the Kimberly-Clark, Kleenex, Scott, WypAll, Kimtech, KleenGuard, Kimcare and Jackson brand names.

The Health Care segment manufactures and markets disposable health care products such as surgical drapes and gowns, infection control products, face masks, exam gloves, respiratory products, pain management products and other disposable medical products. Products in this segment are sold under the Kimberly-Clark, Ballard, ON-Q and other brand names.

Products for household use are sold directly, and through wholesalers, to supermarkets, mass merchandisers, drugstores, warehouse clubs, variety and department stores and other retail outlets. Products for away-from-home use are sold through distributors and directly to manufacturing, lodging, office building, food service, health care establishments and high volume public facilities. In addition, certain products are sold to converters.

Net sales to Wal-Mart Stores, Inc. were approximately 13 percent in 2009, and 14 percent in 2008 and 2007. Patents and Trademarks

The Corporation owns various patents and trademarks registered domestically and in many foreign countries. The Corporation considers the patents and trademarks which it owns and the trademarks under which it sells certain of its products to be material to its business. Consequently, the Corporation seeks patent and trademark protection by all available means, including registration. Raw Materials

Cellulose fiber, in the form of kraft pulp or fiber recycled from recovered waste paper, is the primary raw material for the Corporation’s tissue products and is a component in disposable diapers, training pants, feminine pads and incontinence care products.

Superabsorbent materials are important components in disposable diapers, training and youth pants and incontinence care products. Polypropylene and other synthetics and chemicals are the primary raw materials for manufacturing nonwoven fabrics, which are used in disposable diapers, training and youth pants, wet wipes, feminine pads, incontinence and health care products, and away-from-home wipers.

Most recovered paper, synthetics, pulp and recycled fiber are purchased from third parties. The Corporation considers the supply of these raw materials to be adequate to meet the needs of its businesses. See Item 1A, “Risk Factors.”

2

Table of Contents

PART I (Continued) Competition

The Corporation has several major competitors in most of its markets, some of which are larger and more diversified than the Corporation. The principal methods and elements of competition include brand recognition and loyalty, product innovation, quality and performance, price, and marketing and distribution capabilities. For additional discussion of the competitive environment in which the Corporation conducts its business, see Item 1A, “Risk Factors.” Research and Development

Research and development expenditures are directed toward new or improved personal care, tissue, wiping, safety, and health care products and nonwoven materials. Consolidated research and development expense was $301 million in 2009, $297 million in 2008 and $277 million in 2007. Foreign Market Risks

The Corporation operates and markets its products globally, and its business strategy includes targeted growth in Asia, Latin America, the Middle East and Eastern Europe. See Item 1A, “Risk Factors” for a discussion of foreign market risks that may affect the Corporation’s financial results. Environmental Matters

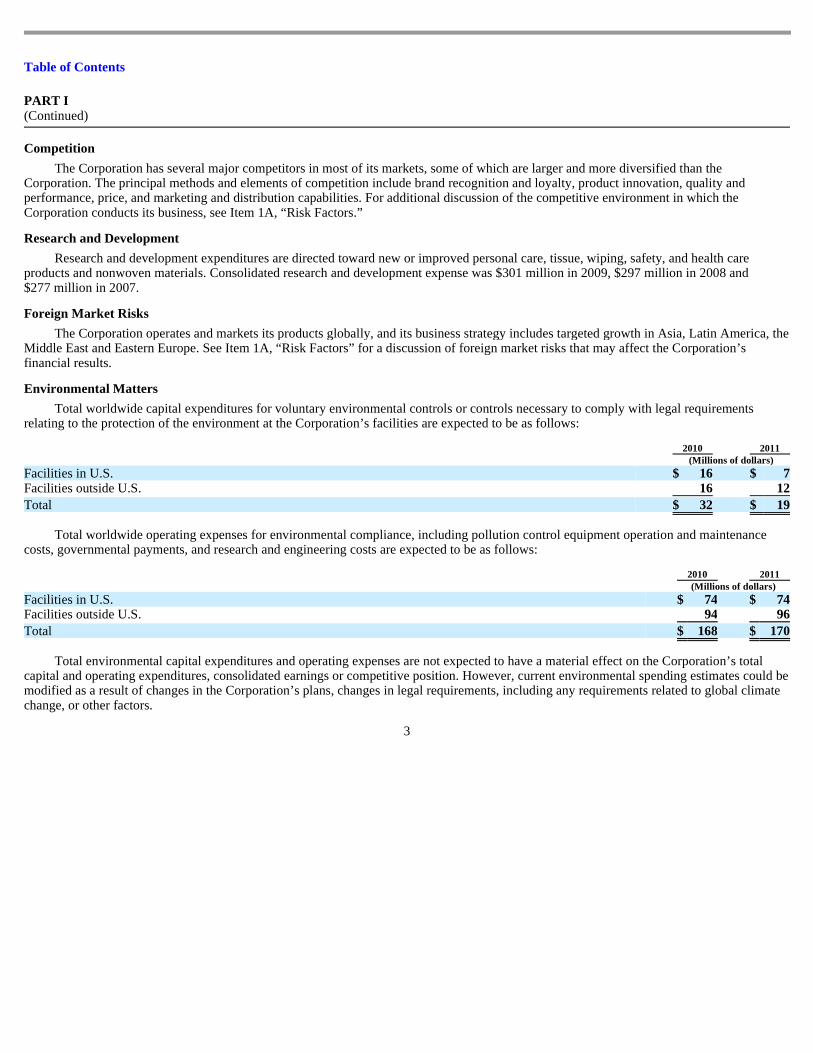

Total worldwide capital expenditures for voluntary environmental controls or controls necessary to comply with legal requirements relating to the protection of the environment at the Corporation’s facilities are expected to be as follows:

Total worldwide operating expenses for environmental compliance, including pollution control equipment operation and maintenance

costs, governmental payments, and research and engineering costs are expected to be as follows:

Total environmental capital expenditures and operating expenses are not expected to have a material effect on the Corporation’s total

capital and operating expenditures, consolidated earnings or competitive position. However, current environmental spending estimates could be modified as a result of changes in the Corporation’s plans, changes in legal requirements, including any requirements related to global climate change, or other factors.

3

2010 2011 (Millions of dollars)

Facilities in U.S. $ 16 $ 7 Facilities outside U.S. 16 12

Total $ 32 $ 19

2010 2011 (Millions of dollars)

Facilities in U.S. $ 74 $ 74 Facilities outside U.S. 94 96

Total $ 168 $ 170

Table of Contents

PART I (Continued) Employees

In its worldwide consolidated operations, the Corporation had approximately 56,000 employees as of December 31, 2009. Available Information

The Corporation makes available financial information, news releases and other information on the Corporation’s website at www.kimberly-clark.com . The Corporation’s annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and any amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 are available free of charge on this website as soon as reasonably practicable after the Corporation files these reports and amendments with, or furnishes them to, the Securities and Exchange Commission. Stockholders may also contact Stockholder Services, P.O. Box 612606, Dallas, Texas 75261-2606 or call 972-281-1522 to obtain a hard copy of these reports without charge. ITEM 1A. RISK FACTORS

The following factors, as well as factors described elsewhere in this Form 10-K, or in other filings by the Corporation with the Securities and Exchange Commission, could adversely affect the Corporation’s consolidated financial position, results of operations or cash flows. Other factors not presently known to us or that we presently believe are not material could also affect our business operations and financial results. Increased pricing pressure, intense competition for sales of the Corporation’s products and the inability to innovate effectively could have an adverse effect on the Corporation’s financial results.

The Corporation competes in intensely competitive markets against well-known, branded products and private label products both domestically and internationally. Inherent risks in the Corporation’s competitive strategy include uncertainties concerning trade and consumer acceptance, the effects of consolidation within retailer and distribution channels, and competitive reaction. Some of the Corporation’s major competitors have undergone consolidation, which could result in increased competition and alter the dynamics of the industry. This consolidation may give competitors greater financial resources and greater market penetration and enable competitors to offer a wider variety of products and services at more competitive prices, which could adversely affect the Corporation’s financial results. It may be necessary for the Corporation to lower prices on its products and increase spending on advertising and promotions, each of which could adversely affect the Corporation’s financial results.

In addition, the Corporation incurs substantial development and marketing costs in introducing new and improved products and technologies. The introduction of a new consumer product (whether improved or newly developed) usually requires substantial expenditures for advertising and marketing to gain recognition in the marketplace. If a product gains consumer acceptance, it normally requires continued advertising and promotional support to maintain its relative market position. Some of the Corporation’s competitors are larger and have greater financial resources than the Corporation. These competitors may be able to spend more aggressively on advertising and promotional activities, introduce competing products more quickly and respond more effectively to changing business and economic conditions than the Corporation. The Corporation’s ability to develop new products is affected by whether it can successfully anticipate consumer needs and preferences, develop and fund technological innovations, and receive and maintain necessary patent and trademark protection.

There is no guarantee that the Corporation will be successful in developing new and improved products and technologies necessary to compete successfully in the industry or that the Corporation will be successful in advertising, marketing, timely launching and selling its products.

4

Table of Contents

PART I (Continued) Changes in the policies of our retail trade customers and increasing dependence on key retailers in developed markets may adversely affect our business.

The Corporation’s products are sold in a highly competitive global marketplace, which is experiencing increased concentration and the growing presence of large-format retailers and discounters. With the consolidation of retail trade, especially in developed markets such as the U.S., Europe and Australia, the Corporation is increasingly dependent on key retailers, and some of these retailers, including large-format retailers, may have greater bargaining power than does the Corporation. They may use this leverage to demand higher trade discounts or allowances which could lead to reduced profitability. The Corporation may also be negatively affected by changes in the policies of its retail trade customers, such as inventory de-stocking, limitations on access to shelf space, delisting of our products; additional requirements related to safety, environmental, social and other sustainability issues; and other conditions. If the Corporation loses a significant customer or if sales of its products to a significant customer materially decrease, the Corporation’s business, financial condition and results of operations may be materially adversely affected. Significant increases in prices for raw materials, energy, transportation and other necessary supplies and services could adversely affect the Corporation’s financial results.

Increases in the cost of and availability of raw materials, including pulp and petroleum-based materials, the cost of energy, transportation and other necessary services, supplier constraints, an inability to maintain favorable supplier arrangements and relations or an inability to avoid disruptions in production output caused by events such as natural disasters, power outages, labor strikes, governmental regulatory requirements or nongovernmental voluntary actions in response to global climate change concerns, and the like could have an adverse effect on the Corporation’s financial results.

Cellulose fiber, in the form of kraft pulp or recycled fiber from recovered waste paper, is used extensively in the Corporation’s tissue products and is subject to significant price fluctuations due to the cyclical nature of these fiber markets. Recycled fiber accounts for approximately 32 percent of the Corporation and its equity companies’ overall fiber requirements.

Increases in pulp prices could adversely affect the Corporation’s earnings if selling prices for its finished products are not adjusted or if these adjustments significantly trail the increases in pulp prices. Derivative instruments have not been used to manage these risks. On a worldwide basis, the Corporation supplies approximately 8 percent of its virgin fiber needs from internal pulp manufacturing operations.

A number of the Corporation’s products, such as diapers, training and youth pants, incontinence care products, disposable wipes and various health care products, contain certain materials that are principally derived from petroleum. These materials are subject to price fluctuations based on changes in petroleum prices, availability and other factors. The Corporation purchases these materials from a number of suppliers. Significant increases in prices for these materials could adversely affect the Corporation’s earnings if selling prices for its finished products are not adjusted or if adjustments significantly trail the increases in prices for these materials. Derivative instruments have not been used to manage these risks.

Although the Corporation believes that the supplies of raw materials needed to manufacture its products are adequate, global economic conditions, supplier capacity constraints and other factors (including actions taken to address climate change and related market responses) could affect the availability of, or prices for, those raw materials.

The Corporation’s manufacturing operations utilize electricity, natural gas and petroleum-based fuels. To ensure that it uses all forms of energy cost-effectively, the Corporation maintains ongoing energy efficiency

5

Table of Contents

PART I (Continued) improvement programs at all of its manufacturing sites. The Corporation’s contracts with energy suppliers vary as to price, payment terms, quantities and duration. The Corporation’s energy costs are also affected by various market factors including the availability of supplies of particular forms of energy, energy prices and local and national regulatory decisions (including actions taken to address climate change and related market responses). There can be no assurance that the Corporation will be fully protected against substantial changes in the price or availability of energy sources. Derivative instruments are used to manage a portion of natural gas price risk in accordance with the Corporation’s risk management policy. Global economic conditions, including recessions or slow economic growth, and continuing credit market disruptions in the United States and certain foreign countries, could continue to adversely affect the Corporation’s business and financial results.

Unfavorable economic conditions, including the impact of recessions, slow economic growth and credit market disruptions in the United States and certain foreign countries, may continue to negatively affect the Corporation’s business and financial results. These economic conditions could negatively impact:

• consumer demand for our products, including shifting consumer purchasing patterns to lower-cost options such as private-label

products,

• demand by businesses for our products, including effects of increased unemployment and cost savings efforts of those customers,

• the mix of our products’ sales,

• our ability to collect accounts receivable on a timely basis from certain customers, and

Ongoing volatility in global commodity, currency and financial markets resulted in uncertainty in the business environment in 2009,

which is expected to continue into 2010. The Corporation relies on access to the credit markets, specifically the commercial paper and public bond markets, to provide supplemental funding for its operations. Although the Corporation has not experienced a disruption in its ability to access the credit markets, it is possible that the Corporation may have difficulty accessing the credit markets in the future, which may disrupt its businesses or further increase the Corporation’s cost of funding its operations.

Prolonged recessions, slow economic growth or credit market disruptions could result in decreased revenue, margins and earnings. The Corporation’s international operations are subject to foreign market risks, including foreign exchange risk and currency restrictions, which may adversely affect the Corporation’s financial results.

• the ability of certain suppliers to fill our orders for raw materials or other goods and services.

Because the Corporation and its equity companies have manufacturing facilities in 38 countries and their products are sold in more than 150 countries, the Corporation’s results may be substantially affected by foreign market risks. The Corporation is subject to the impact of economic and political instability in developing countries.

The Corporation faces increased risks in its international operations, including fluctuations in currency exchange rates, currency restrictions, adverse political and economic conditions, legal and regulatory constraints, tariffs and other trade barriers, risks of expropriation, difficulties in enforcing contractual and intellectual property rights, and potentially adverse tax consequences. Each of these factors could adversely affect the Corporation’s financial results. See Item 7, “Management’s Discussion and Analysis of Financial Condition and

6

Table of Contents

PART I (Continued) Results of Operations” and Item 8, Note 19 to the Consolidated Financial Statements, for information about the effects of currency restrictions, currency devaluation and inflation in Venezuela on the Corporation’s financial results in 2009 and 2010.

In addition, intense competition in European personal care and tissue markets, and the challenging economic, political and competitive environments in Latin America, Eastern Europe and Asia may slow the Corporation’s sales growth and earnings potential. See Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” The Corporation’s success internationally also depends on its ability to acquire or form successful business alliances, and there is no guarantee that the Corporation will be able to acquire or form these alliances. In addition, there can be no assurance that the Corporation’s products will be accepted in any particular market.

The Corporation is subject to the movement of various currencies against each other and versus the U.S. dollar. A portion of the exposures, arising from transactions and commitments denominated in non-local currencies, is systematically managed through foreign currency forward and swap contracts.

Translation exposure for the Corporation with respect to foreign operations generally is not hedged. Weaker foreign currency exchange rates increase the potential impact of forecasted increases in dollar-based input costs for operations outside the U.S. There can be no assurance that the Corporation will be protected against substantial foreign currency fluctuations. There is no guarantee that the Corporation’s ongoing efforts to reduce costs will be successful.

The Corporation continues to implement plans to improve its competitive position by achieving cost reductions in its operations. In addition, the Corporation expects ongoing cost savings from its organization optimization initiative and ongoing continuous improvement activities. The Corporation anticipates these continuing cost savings will result from previous reductions of its worldwide salaried workforce, reducing material costs and manufacturing waste and realizing productivity gains and distribution efficiencies in each of its business segments. See Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” If the Corporation cannot successfully implement its cost savings plans, the Corporation may not realize all anticipated benefits. Any negative impact these plans have on the Corporation’s relationships with employees or customers or any failure to generate the anticipated efficiencies and savings could adversely affect the Corporation’s financial results. The Corporation’s sales may not occur as estimated.

There is no guarantee that the Corporation will be able to anticipate consumer preferences, estimate sales of new products, estimate changes in population characteristics and the acceptance of the Corporation’s products in new markets or anticipate changes in technology and competitive responses. As a result, the Corporation may not be able to achieve anticipated sales. The Corporation may acquire new product lines or businesses and may have difficulties integrating future acquisitions or may not realize anticipated benefits of acquisitions.

The Corporation may pursue acquisitions of new product lines or businesses. Acquisitions involve numerous risks, including difficulties in the assimilation of the operations, technologies, services and products of the acquired product lines or businesses, personnel turnover and the diversion of management’s attention from other business concerns. We may be unable to identify suitable additional acquisition candidates or may be unable to successfully integrate and manage product lines or businesses that we have acquired or may acquire in the future. In addition, we may be unable to achieve anticipated benefits or cost savings from acquisitions in the timeframe we anticipate, or at all.

7

Table of Contents

PART I (Continued)

The inability to integrate and manage acquired product lines or businesses in a timely and efficient manner, the inability to achieve anticipated cost savings or other anticipated benefits from these acquisitions in the timeframe we anticipate or the unanticipated required increases in trade, promotional or capital spending from these acquisitions could adversely affect our business, consolidated financial condition, results of operations or liquidity.

Moreover, future acquisitions could result in substantial additional indebtedness, exposure to contingent liabilities or the impairment of goodwill or other intangible assets, all of which could adversely affect our financial condition, results of operations and liquidity. If we are unable to hire, develop or retain key employees or a skilled and diverse workforce, it could have an adverse effect on our business.

Our strategy includes a focus on hiring, developing and retaining our management team and a skilled and diverse international workforce. We compete to hire new employees and then seek to train them to develop their skills. Unplanned turnover or failure to develop an effective succession plan for our leadership positions, or to hire and retain a diverse, skilled workforce, could increase our operating costs and adversely affect our results of operations. There can be no assurance that we will be able to successfully recruit, develop and retain the key personnel that we need. Pending litigation, administrative actions and new legal requirements could have an adverse effect on the Corporation.

There is no guarantee that the Corporation will be successful in defending itself in legal and administrative actions or in asserting its rights under various laws, including intellectual property laws. In addition, the Corporation could incur substantial costs in defending itself or in asserting its rights in these actions.

The Corporation’s sales and results of operations also may be adversely affected by new legal requirements, including proposed health care reform legislation and climate change and other environmental legislation and regulations. The costs and other effects of pending litigation and administrative actions against the Corporation and new legal requirements cannot be determined with certainty. For example, new legislation or regulations may result in increased costs to the Corporation, directly for its compliance or indirectly to the extent suppliers increase prices of goods and services because of increased compliance costs or reduced availability of raw materials.

Although management believes that none of these proceedings or requirements will have a material adverse effect on the Corporation, there can be no assurance that the outcome of these proceedings or effects of new legal requirements will be as expected. See Item 3, “Legal Proceedings”. The Corporation obtains certain manufactured products and administrative services from third parties. If the third-party providers fail to satisfactorily perform, our operations could be adversely impacted.

Third parties manufacture some of the Corporation’s products and provide certain administrative services. Disruptions or delays at the third-party manufacturers or service providers due to regional economic, business, environmental, or political events, or information technology system failures or military actions, or the failure of these manufacturers or service providers to otherwise satisfactorily perform, could adversely impact the Corporation’s operations, sales, payments to the Corporation’s vendors, employees, and others, and the Corporation’s ability to report financial and management information on a timely and accurate basis. Administrative functions transferred to third-party service providers include certain information technology;

8

Table of Contents

PART I (Continued) finance and accounting; sourcing and supply management; and human resources services. Although moving these administrative functions to third-party service providers has improved certain capabilities and lowered the Corporation’s cost of operations, the Corporation could experience disruptions in the quality and timeliness of the services. ITEM 1B. UNRESOLVED STAFF COMMENTS

None. ITEM 2. PROPERTIES

The Corporation owns or leases:

• its principal executive offices, located in the Dallas, Texas metropolitan area;

• five operating segment and geographic headquarters at two U.S. and three international locations; and

The locations of the Corporation’s and its equity affiliates’ principal production facilities by major geographic areas of the world are as

follows:

Many of these facilities produce multiple products. The types of products produced by these facilities are as follows:

Management believes that the Corporation’s and its equity affiliates’ facilities are suitable for their purpose, adequate to support their

businesses and well maintained. The extent of utilization of individual facilities varies, but they generally operate at or near capacity, except in certain instances such as when a new product or technology is being introduced. ITEM 3. LEGAL PROCEEDINGS

• five administrative centers at three U.S. and two international locations.

Geographic Area:

Number of

Facilities

United States (in 20 states) 27 Canada 1 Europe 20 Asia, Latin America and Other 64

Worldwide Total (in 38 countries) 112

Products Produced:

Number of

Facilities

Tissue, including consumer tissue and K-C Professional & Other products 66 Personal Care 50 Health Care 11

The Corporation is subject to federal, state and local environmental protection laws and regulations with respect to its business operations and is operating in compliance with, or taking action aimed at ensuring compliance with, these laws and regulations. The Corporation has been named a potentially responsible party under the provisions of the federal Comprehensive Environmental Response, Compensation and Liability Act, or

9

Table of Contents

PART I (Continued) analogous state statutes, at a number of waste disposal sites. In management’s opinion, none of the Corporation’s compliance obligations with environmental protection laws and regulations, individually or in the aggregate, is expected to have a material adverse effect on the Corporation’s business, financial condition, results of operations or liquidity.

In May 2007, a wholly-owned subsidiary of the Corporation was served a summons in Pennsylvania state court by the Delaware County Regional Water Quality Authority (“Delcora”). Also in May 2007, Delcora initiated an administrative action against the Corporation. Delcora is a public agency that operates a sewerage system and a wastewater treatment facility serving industrial and municipal customers, including Kimberly-Clark’s Chester Mill. Delcora also regulates the discharge of wastewater from the Chester Mill. Delcora has alleged in the summons and the administrative action that the Corporation underreported the quantity of effluent discharged to Delcora from the Chester Mill for several years due to an inaccurate effluent metering device and owes additional amounts. The Corporation’s action for declaratory judgment in the Federal District Court for the Eastern District of Pennsylvania was dismissed in December 2007 on grounds of abstention. The Corporation appealed this dismissal to the Third Circuit Court of Appeals. The Third Circuit directed the parties to mediation, which during the third quarter of 2008 resulted in a procedural agreement to appoint a neutral and qualified hearing officer. As a result of this arrangement with Delcora, the Corporation has dismissed its appeal to the Third Circuit. The Corporation continues to believe that Delcora’s allegations lack merit and is vigorously defending against Delcora’s actions. In management’s opinion, this matter is not expected to have a material adverse effect on the Corporation’s business, financial condition, results of operations or liquidity. ITEM 4. SUBMISSION OF MATTERS TO A VOTE OF SECUR ITY HOLDERS

No matters were submitted to a vote of security holders during the fourth quarter of 2009. EXECUTIVE OFFICERS OF THE REGISTRANT

The names and ages of the executive officers of the Corporation as of February 24, 2010, together with certain biographical information, are as follows:

Robert E. Abernathy , 55, was elected Group President—North Atlantic Consumer Products in 2008. He is responsible for the Corporation’s consumer business in North America and Europe and the related customer development and supply chain organizations. Mr. Abernathy joined the Corporation in 1982. His past responsibilities in the Corporation have included overseeing its businesses in Asia, Latin America, Eastern Europe, the Middle East and Africa, as well as operations and major project management in North America. He was appointed Vice President—North American Diaper Operations in 1992; Managing Director of Kimberly-Clark Australia Pty. Limited in 1994; Group President of the Corporation’s Business-to-Business segment in 1998 and Group President—Developing and Emerging Markets in 2004. He is a director of The Lubrizol Corporation.

Joanne B. Bauer , 54, was elected President—Global Health Care in 2006. She is responsible for the Corporation’s global health care business, which includes a variety of medical supplies and devices. Ms. Bauer joined the Corporation in 1981. Her past responsibilities have included various marketing and management positions in the Adult Care and Health Care businesses. She was appointed Vice President of KimFibers, Ltd. in 1996; Vice President of Global Marketing for Health Care in 1998; and President of Health Care in 2001.

Robert W. Black , 50, was elected Group President—K-C International in 2008. He is responsible for the Corporation’s businesses in Asia, Latin America, Eastern Europe, the Middle East and Africa. His past responsibilities have included overseeing the Corporation’s strategy, mergers and acquisitions, global

10

Table of Contents

PART I (Continued) competitiveness and innovation efforts. Prior to joining the Corporation in 2006 as Senior Vice President and Chief Strategy Officer, Mr. Black served as Chief Operating Officer of Sammons Enterprises, a multi-faceted conglomerate, from 2004 to 2005. From 1994 to 2004, Mr. Black held various senior leadership positions in marketing, strategy, corporate development and international management with Steelcase, Inc., a leading office furniture products and related services company. As President of Steelcase International from 2000 to 2004, he led operations in more than 130 countries.

Christian A. Brickman , 45, was elected Senior Vice President and Chief Strategy Officer in 2008. He is responsible for leading the development and monitoring of the Corporation’s strategic plans and processes to enhance the Corporation’s enterprise growth initiatives. Prior to joining the Corporation in 2008, Mr. Brickman served as a Principal of McKinsey & Company, Inc., a management consulting firm, from 2003 to 2008, and as an Associate Principal from 2001 to 2003.

Mark A. Buthman , 49, was elected Senior Vice President and Chief Financial Officer in 2003. Mr. Buthman joined the Corporation in 1982. He has held various positions of increasing responsibility in the operations, finance and strategic planning areas of the Corporation. Mr. Buthman was appointed Vice President of Strategic Planning and Analysis in 1997 and Vice President of Finance in 2002.

Thomas J. Falk , 51, was elected Chairman of the Board and Chief Executive Officer in 2003 and President and Chief Executive Officer in 2002. Prior to that, he served as President and Chief Operating Officer since 1999. Mr. Falk previously had been elected Group President—Global Tissue, Pulp and Paper in 1998, where he was responsible for the Corporation’s global tissue businesses. Earlier in his career, Mr. Falk had responsibility for the Corporation’s North American Infant Care, Child Care and Wet Wipes businesses. Mr. Falk joined the Corporation in 1983 and has held other senior management positions in the Corporation. He has been a director of the Corporation since 1999. He also serves on the board of directors of Catalyst Inc. and the University of Wisconsin Foundation, and serves as a governor of the Boys & Girls Clubs of America.

Lizanne C. Gottung , 53, was elected Senior Vice President and Chief Human Resources Officer in 2002. She is responsible for leading the design and implementation of all human capital strategies for the Corporation, including global compensation and benefits, talent management, diversity and inclusion, organizational effectiveness and corporate health services. Ms. Gottung joined the Corporation in 1981. She has held a variety of human resources, manufacturing and operational roles of increasing responsibility with the Corporation, including Vice President of Human Resources from 2001 to 2002. She is a director of Louisiana Pacific Corporation.

Thomas J. Mielke , 51, was elected Senior Vice President—Law and Government Affairs and Chief Compliance Officer in 2007. His responsibilities include the Corporation’s legal affairs, internal audit and government relations activities. Mr. Mielke joined the Corporation in 1988. He held various positions within the legal function and was appointed Vice President and Chief Patent Counsel in 2000, and Vice President and Chief Counsel – North Atlantic Consumer Products in 2004.

Anthony J. Palmer , 50, was elected Senior Vice President and Chief Marketing Officer in 2006. He also assumed leadership of the Corporation’s innovation organization in March 2008. He is responsible for leading the growth of enterprise-wide strategic marketing capabilities and the development of high-return marketing programs to support the Corporation’s business initiatives. Prior to joining the Corporation in 2006, he served in a number of senior marketing and general management roles at the Kellogg Company, a producer of cereal and convenience foods, from 2002 to 2006, including as managing director of Kellogg’s U.K. business.

Jan B. Spencer , 54, was elected President—Global K-C Professional in 2006. He is responsible for the Corporation’s global professional business, which includes commercial tissue and wipers, and skin care, safety

11

Table of Contents

PART I (Continued) and Do-It-Yourself products. Mr. Spencer joined the Corporation in 1979. His past responsibilities have included various sales and management positions in Europe and the U.S. He was appointed Vice President Research, Development & Engineering in the Away From Home sector in 1996; Vice President, Wiper Business in 1998; Vice President, European Operations, Engineering, Supply Chain in the K-C Professional sector in 2000; President, KCP Europe in 2002; President, KCP North America in 2003; and President—K-C Professional North Atlantic in 2004.

12

Table of Contents

PART II

ITEM 5. MARKET FOR REGISTRANT ’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND IS SUER PURCHASES OF EQUITY SECURITIES

The dividend and market price data included in Item 8, Note 22 to the Consolidated Financial Statements are incorporated in this Item 5 by reference.

Quarterly dividends have been paid continually since 1935. Dividends have been paid on or about the second business day of January, April, July and October. The dividend reinvestment service of Computershare Investor Services is available to Kimberly-Clark stockholders of record. This service makes it possible for Kimberly-Clark stockholders of record to have their dividends automatically reinvested in common stock and to make additional cash investments.

Kimberly-Clark common stock is listed on the New York Stock Exchange. The ticker symbol is KMB.

As of February 12, 2010, the Corporation had 28,633 holders of record of its common stock.

For information relating to securities authorized for issuance under equity compensation plans, see Part III, Item 12 of this Form 10-K.

The Corporation repurchases shares of Kimberly-Clark common stock from time to time pursuant to publicly announced share repurchase programs. The Corporation’s Board of Directors authorized a share repurchase program on July 23, 2007 that allows for the repurchase of 50 million shares in an amount not to exceed $5 billion. No shares were repurchased under this program during the fourth quarter of 2009. At December 31, 2009, there were 32 million shares remaining under this share authorization.

During October, November and December 2009, the Corporation purchased the following shares from current or former employees in connection with the exercise of employee stock options and other awards.

13

Month Shares Amount

October 2,387 $ 145,989 November 2,706 172,291 December — —

Table of Contents

PART II (Continued) ITEM 6. SELECTED FINANCIAL DATA

Year Ended December 31 2009 2008 2007 2006 2005 (Millions of dollars, except per share amounts)

Net Sales $ 19,115 $ 19,415 $ 18,266 $ 16,747 $ 15,903 Gross Profit 6,420 5,858 5,704 5,082 5,075 Operating Profit 2,825 2,547 2,616 2,102 2,311 Share of net income of equity companies 164 166 170 219 137 Income before extraordinary loss and cumulative effect of accounting

change 1,994 1,837 1,951 1,595 1,668 Extraordinary loss — (8 ) — — — Cumulative effect of accounting change — — — — (13 )

Net income 1,994 1,829 1,951 1,595 1,655 Net income attributable to noncontrolling interests (110 ) (139 ) (128 ) (95 ) (87 ) Net income attributable to Kimberly-Clark Corporation 1,884 1,690 1,823 1,500 1,568

Per share basis:

Basic

Income before extraordinary loss and cumulative effect of accounting change 4.53 4.06 4.11 3.26 3.33

Cumulative effect of accounting change — — — — (.03 ) Extraordinary loss — (.02 ) — — — Net income 4.53 4.04 4.11 3.26 3.30

Diluted

Income before extraordinary loss and cumulative effect of accounting change 4.52 4.05 4.08 3.24 3.31

Cumulative effect of accounting change — — — — (.03 ) Extraordinary loss — (.02 ) — — — Net income 4.52 4.03 4.08 3.24 3.28

Cash Dividends Per Share

Declared 2.40 2.32 2.12 1.96 1.80 Paid 2.38 2.27 2.08 1.92 1.75

Total Assets $ 19,209 $ 18,089 $ 18,440 $ 17,067 $ 16,303 Long-Term Debt 4,792 4,882 4,394 2,276 2,595 Total Stockholders’ Equity 5,690 4,261 5,687 6,502 5,936 (a) The Corporation recorded an extraordinary charge of $12 million ($8 million after tax) related to the consolidation of its monetization financing entities. See Item 8, Note 2 to the

Consolidated Financial Statements.

(b) The Corporation’s share of net income includes a gain of approximately $46 million from the sale by Kimberly-Clark de Mexico, S.A.B. de C.V. of its pulp and paper business.

(c) The Corporation recorded a pretax asset retirement obligation of $24 million at December 31, 2005. The cumulative effect of accounting change on income, net of related income tax effects, of recording the asset retirement obligation was $13 million, or $.03 per share.

(d) Effective January 1, 2009, the Corporation adopted new accounting requirements with respect to the classification of noncontrolling interests. Prior year results have been recast to conform to the current year presentation.

14

(e) The Corporation’s basic and diluted earnings per share amounts for 2005 to 2008 have been recast to include certain share-based payment awards as participating securities under the two-class method, as required by accounting requirements.

(a) (c)

(b)

(d)

(d)

(d)

(e)

(e)

(d)

Table of Contents

PART II (Continued)

ITEM 7. MANAGEMENT ’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AN D RESULTS OF OPERATIONS

Introduction

This management’s discussion and analysis of financial condition and results of operations (“MD&A”) is intended to provide investors with an understanding of the Corporation’s past performance, its financial condition and its prospects. The following will be discussed and analyzed:

• Overview of Business

• Overview of 2009 Results

• Results of Operations and Related Information

• Liquidity and Capital Resources

• Variable Interest Entities

• Critical Accounting Policies and Use of Estimates

• Legal Matters

• New Accounting Standards

• Business Outlook

Overview of Business

• Forward-Looking Statements

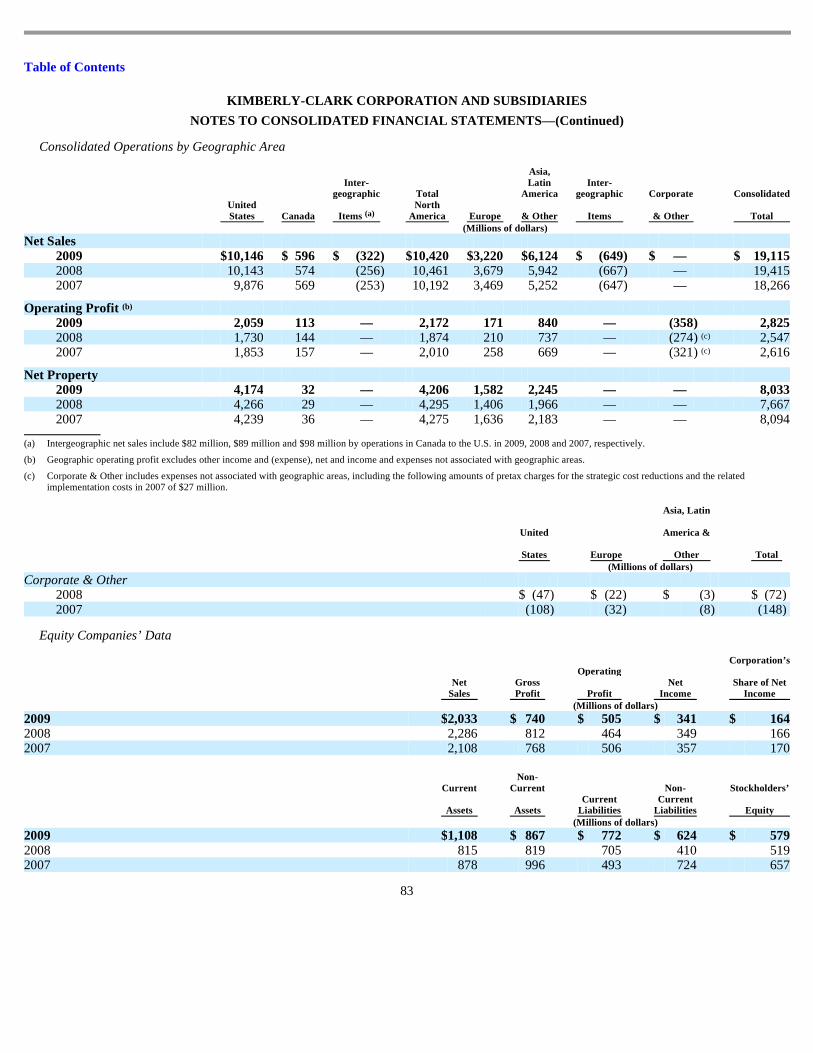

The Corporation is a global company focused on leading the world in essentials for a better life, with manufacturing facilities in 35 countries and products sold in more than 150 countries. The Corporation’s products are sold under such well-known brands as Kleenex, Scott, Huggies, Pull-Ups, Kotex and Depend. The Corporation has four reportable global business segments: Personal Care; Consumer Tissue; K-C Professional & Other; and Health Care. These global business segments are described in greater detail in Item 8, Note 20 to the Consolidated Financial Statements.

In managing its global business, the Corporation’s management believes that developing new and improved products, responding effectively to competitive challenges, obtaining and maintaining leading market shares, controlling costs, managing currency and commodity risks, and responding effectively to current and developing global economic environments are important to the long-term success of the Corporation. The discussion and analysis of results of operations and other related information will refer to these factors.

• Product innovation—Past results and future prospects depend in large part on product innovation. The Corporation relies on its ability to develop and introduce new or improved products to drive sales and volume growth and to achieve and/or maintain category leadership. In order to introduce new or improved products, the technology to support those products must be acquired or developed. Research and development expenditures are directed towards new or improved personal care, tissue, industrial wipers, safety and health care products and nonwoven materials.

15

• Competitive environment—Past results and future prospects are significantly affected by the competitive environment in which we operate. We experience intense competition for sales of our principal products in our major markets, both domestically and internationally. Our products compete with widely-advertised, well-known, branded products, as well as private label products, which are typically sold at lower prices. We have several major competitors in most of our markets, some of which

Table of Contents

PART II (Continued)

are larger and more diversified. The principal methods and elements of competition include brand recognition and loyalty, product innovation, quality and performance, price, and marketing and distribution capabilities. The Corporation increased promotional and strategic marketing spending in 2008 and 2009 to support new product introductions, further build brand equity and enable competitive pricing in order to protect the position of the Corporation’s products in the market. We expect competition to continue to be intense in 2010.

• Market shares—Achieving leading market shares in our principal products has been an important part of our past performance. We

hold number 1 or 2 share positions in more than 80 countries. Achieving and maintaining leading market shares is important because of ongoing consolidation of retailers and the trend of leading merchandisers seeking to stock only the top competitive brands.

• Cost controls—To maintain or improve our competitive position, we must control our manufacturing, distribution and other costs. We have achieved cost savings from reducing material costs and manufacturing waste, and realizing productivity gains and distribution efficiencies in our business segments. Our ability to control costs can be affected by changes in the price of pulp, oil and other commodities we consume in our manufacturing processes.

• Foreign currency and commodity risks—As a multinational enterprise, we are exposed to changes in foreign currency exchange

rates, and we are also exposed to changes in commodity prices. Our ability to effectively manage these risks can have a material impact on our results of operations.

Overview of 2009 Results

• Global economic environment—The Corporation’s business and financial results continue to be adversely affected by economic uncertainty in the United States and throughout the world and volatility in the global markets. Although it has become more challenging to predict our results in the near-term, we will continue to focus on executing our Global Business Plan strategies for the long-term health of our businesses.

• Net sales decreased 1.5 percent because of unfavorable currency effects and a decline in sales volumes, partially offset by higher net

selling prices.

• Operating profit increased 10.9 percent, and net income attributable to Kimberly-Clark and diluted earnings per share increased 11.5 percent and 12.2 percent, respectively. The benefits of higher net selling prices, cost savings and deflation in key cost components, were partially offset by unfavorable currency effects, organization optimization severance and related charges, increased pension expense, higher operating costs and increased strategic marketing spending.

Results of Operations and Related Information

• Cash flow from operations was $3.5 billion, an increase of 38 percent.

This section contains a discussion and analysis of net sales, operating profit and other information relevant to an understanding of 2009 results of operations. This discussion and analysis compares 2009 results to 2008, and 2008 results to 2007.

16

Table of Contents

PART II (Continued)

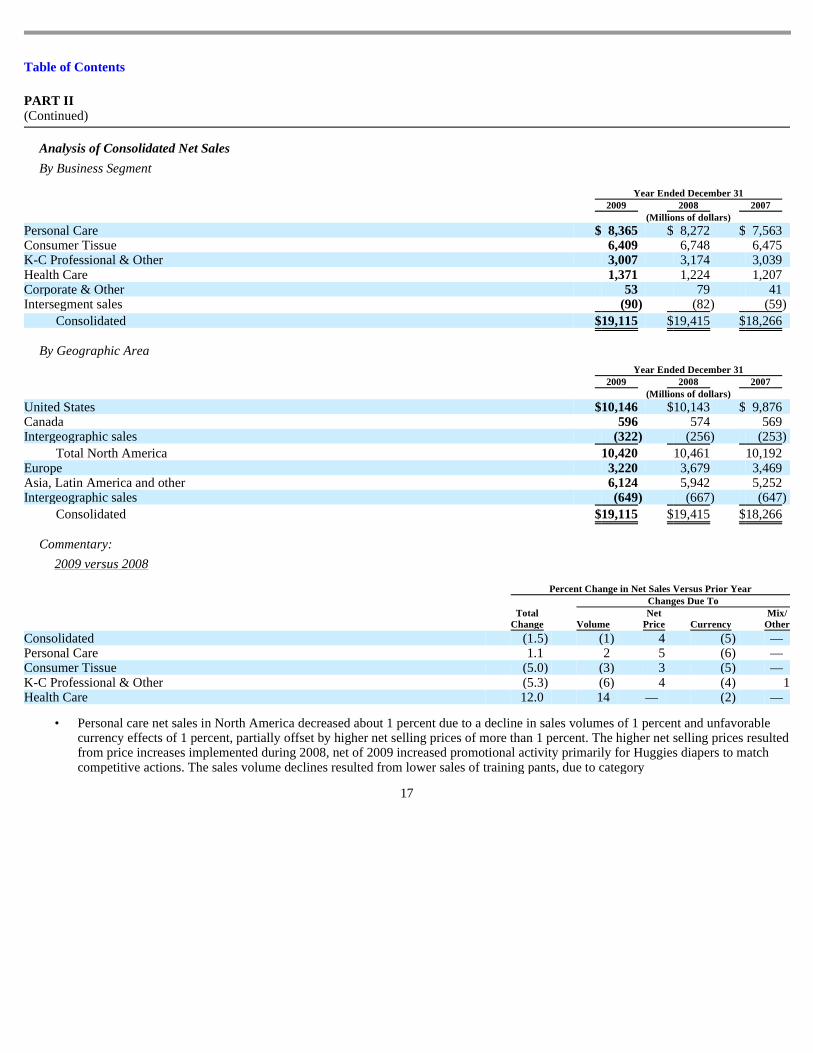

Analysis of Consolidated Net Sales

By Business Segment

By Geographic Area

Year Ended December 31 2009 2008 2007 (Millions of dollars)

Personal Care $ 8,365 $ 8,272 $ 7,563 Consumer Tissue 6,409 6,748 6,475 K-C Professional & Other 3,007 3,174 3,039 Health Care 1,371 1,224 1,207 Corporate & Other 53 79 41 Intersegment sales (90 ) (82 ) (59 )

Consolidated $ 19,115 $ 19,415 $ 18,266

Commentary:

Year Ended December 31 2009 2008 2007 (Millions of dollars)

United States $ 10,146 $ 10,143 $ 9,876 Canada 596 574 569 Intergeographic sales (322 ) (256 ) (253 )

Total North America 10,420 10,461 10,192 Europe 3,220 3,679 3,469 Asia, Latin America and other 6,124 5,942 5,252 Intergeographic sales (649 ) (667 ) (647 )

Consolidated $ 19,115 $ 19,415 $ 18,266

2009 versus 2008

17

Percent Change in Net Sales Versus Prior Year

Total Change

Changes Due To

Volume Net

Price Currency Mix/

Other

Consolidated (1.5 ) (1 ) 4 (5 ) — Personal Care 1.1 2 5 (6 ) — Consumer Tissue (5.0 ) (3 ) 3 (5 ) — K-C Professional & Other (5.3 ) (6 ) 4 (4 ) 1 Health Care 12.0 14 — (2 ) —

• Personal care net sales in North America decreased about 1 percent due to a decline in sales volumes of 1 percent and unfavorable currency effects of 1 percent, partially offset by higher net selling prices of more than 1 percent. The higher net selling prices resulted from price increases implemented during 2008, net of 2009 increased promotional activity primarily for Huggies diapers to match competitive actions. The sales volume declines resulted from lower sales of training pants, due to category

Table of Contents

PART II (Continued)

weakness, and modestly lower volumes for Huggies diapers. These declines were partially offset by higher volumes for K-C’s adult incontinence brands, including benefits from innovation of Depend products. In Europe, personal care net sales decreased about 10 percent as unfavorable currency effects of 12 percent and decreased net selling prices of 2 percent were partially offset by increased sales volumes of 4 percent. The volume increase was driven by growth of Huggies diapers in Central Europe and in the Corporation’s four core markets—the U.K., France, Italy and Spain.

In K-C’s international operations in Asia, Latin America, the Middle East, Eastern Europe and Africa, net sales increased about 5 percent driven by a more than 11 percent increase in net selling prices and 4 percent increase in sales volumes, partially offset by a 10 percent unfavorable currency effect. The growth in net selling prices was broad-based, with particular strength throughout Latin America and in South Korea, Russia, and South Africa. Unfavorable currency effects were primarily in South Korea, Russia, Australia and Latin America.

• Consumer tissue net sales in North America decreased 2 percent as an increase in net selling prices of 2 percent was offset by a sales volume decline of about 4 percent. The higher net selling prices were primarily attributable to price increases in all categories implemented during 2008, net of increased promotional activity to match competitive actions. Sales volumes were down low single-digits in facial tissue and double-digits in paper towels, primarily as a result of focusing on improving revenue realization and some consumer trade-down to lower-priced product offerings. In Europe, consumer tissue net sales decreased almost 14 percent due to unfavorable currency effects of 11 percent, a decrease in sales volumes of 2 percent and a decrease of net selling prices of 1 percent. The lower sales volumes were primarily because of reduced sales of bathroom tissue due to some consumer trade-down to lower-priced product offerings.

In K-C’s international operations in Asia, Latin America, the Middle East, Eastern Europe and Africa, consumer tissue net sales decreased 3 percent, as an increase in net selling prices of 7 percent and improvements in product mix of 1 percent were more than offset by unfavorable currency effects of 8 percent and lower sales volumes of 3 percent. The increase in net selling prices resulted from price increases implemented in most markets in 2008, net of current year increased promotional activity. Unfavorable currency effects were primarily attributable to South Korea, Russia, Australia and Latin America.

• Economic weakness and high unemployment levels in North America and Europe continued to affect K-C Professional’s categories in 2009. In North America, sales decreased 4 percent, due to a decrease in sales volumes of 6 percent (which is net of an approximate 4 percent benefit from the acquisition of Jackson in April 2009), partially offset by higher net selling prices of about 3 percent. In Europe, sales of K-C Professional products decreased 16 percent, due to a decrease in sales volumes of 9 percent (which is net of an approximate 1 percent benefit from the Jackson acquisition) and unfavorable currency effects of 9 percent, partially offset by higher net selling prices of 3 percent.

18

• The increased sales volumes for health care products were primarily due to broad-based growth across several categories including exam gloves and apparel and a 2 percent benefit from the acquisition of I-Flow in late November 2009. In addition, approximately 35 percent of the total gain in health care volume for the year was attributable to increased global demand for face masks, a result of the H1N1 influenza virus.

Table of Contents

PART II (Continued)

Commentary:

2008 versus 2007

Percent Change in Net Sales Versus Prior Year

Total Change

Changes Due To

Volume Net

Price Currency Mix/ Other

Consolidated 6.3 1 4 1 — Personal Care 9.4 5 3 1 — Consumer Tissue 4.2 (4 ) 6 1 1 K-C Professional & Other 4.4 (1 ) 4 1 — Health Care 1.4 4 (1 ) 1 (3 )

• Personal care net sales in North America increased about 5 percent due to more than 3 percent higher net selling prices and more than 1 percent higher sales volumes. The higher net selling prices resulted from increases implemented throughout 2008, net of increased promotional activity primarily for Huggies diapers to match competitive actions. Sales volume growth was dampened by the effects of the economic downturn in the fourth quarter of 2008 as customers adjusted inventory levels, child care category sales slowed and some consumers traded down to lower-priced product offerings. In Europe, personal care net sales were even with the prior year as favorable currency effects offset lower sales volumes and net selling prices. Sales volumes of Huggies diapers in the Corporation’s four core markets—the U.K., France, Italy and Spain—declined about 4 percent from the prior year.

In K-C’s international operations in Asia, Latin America, the Middle East, Eastern Europe and Africa, net sales increased almost 17 percent driven by a more than 10 percent increase in sales volumes. The growth in sales volumes was broad-based, with particular strength throughout Latin America and in South Korea, Russia, Turkey and China. Increased net selling prices and favorable product mix added about 4 percent and 2 percent, respectively, to the net sales increase. Unfavorable currency effects in South Korea were offset by favorable effects in other countries, primarily in Brazil and Israel.

• Consumer tissue net sales in North America were even with the prior year as increased net selling prices of more than 6 percent and improved product mix of nearly 1 percent were offset by a sales volume decline of about 7 percent. The higher net selling prices were primarily attributable to price increases for bathroom tissue and paper towels implemented during the first and third quarters in the U.S. List prices for facial tissue were raised late in the third quarter. Sales volumes were down mid-single digits in bathroom tissue and facial tissue and double-digits in paper towels, primarily as a result of focusing on improving revenue realization. A portion of the overall volume decline is also due to the Corporation’s decision in late 2007 to shed certain low-margin private label business. In Europe, consumer tissue net sales increased almost 4 percent on nearly 3 percent higher net selling prices, a 1 percent improvement in product mix and more than 2 percent favorable currency effects, tempered by a decline in sales volumes of about 2 percent. The lower sales volumes were primarily due to reduced sales of Andrex and Scottex bathroom tissue and Kleenex facial tissue in response to higher net selling prices and a slowdown in category sales, particularly in the U.K.

Consumer tissue net sales in K-C’s international operations in Asia, Latin America, the Middle East, Eastern Europe and Africa increased nearly 13 percent. During 2008, the Corporation raised prices in most markets to recover higher raw materials costs and drove improvements in mix with more differentiated, value-added products, strategies that resulted in higher net selling prices of about 10 percent and better product mix of more than 2 percent. Sales volumes were even with last year. For the year, currency effects were neutral as favorable effects earlier in the year were offset by the dramatic changes in currency rates in the fourth quarter of 2008.

19

Table of Contents

PART II (Continued)

• Economic weakness and rising unemployment levels in North America and Europe began to affect K-C Professional’s categories in the fourth quarter of 2008. For the year, net sales in North America increased nearly 3 percent as increased net selling prices of about 4 percent and improved product mix of over 1 percent were tempered by lower sales volumes. In Europe, net sales of K-C Professional products advanced about 9 percent as increased net selling prices and higher sales volumes contributed nearly 3 percent and 2 percent, respectively, to the improvement. Currency effects were about 4 percent favorable versus the prior year.

Analysis of Consolidated Operating Profit

• The increased sales volumes for health care products were primarily due to mid-single digit growth outside North America and a

similar advance for medical devices in North America. The price decline was mainly attributable to competitive conditions affecting surgical supplies in North America and Europe.

By Business Segment

By Geographic Area

Year Ended December 31 2009 2008 2007 (Millions of dollars)

Personal Care $ 1,739 $ 1,649 $ 1,562 Consumer Tissue 736 601 702 K-C Professional & Other 464 428 478 Health Care 244 143 195 Other income and (expense), net (97 ) (20 ) 18 Corporate & Other (261 ) (254 ) (339 )

Consolidated $ 2,825 $ 2,547 $ 2,616

Year Ended December 31 2009 2008 2007 (Millions of dollars)

United States $ 2,059 $ 1,730 $ 1,853 Canada 113 144 157 Europe 171 210 258 Asia, Latin America and other 840 737 669 Other income and (expense), net (97 ) (20 ) 18 Corporate & Other (261 ) (254 ) (339 )

Consolidated $ 2,825 $ 2,547 $ 2,616

20

Note: Corporate & Other and Other income and (expense), net, include the following amounts of pre-tax charges for the strategic cost reductions. In 2007, Corporate & Other also includes the related implementation costs.

2008 2007 (Millions of dollars)

Corporate & Other $ (72 ) $ (148 ) Other income and (expense), net 12 14

Table of Contents

PART II (Continued)

Commentary:

2009 versus 2008

Percentage Change in Operating Profit Versus Prior Year

Total Change

Change Due To

Volume Net

Price Input

Costs

Production (Curtailment)/

Efficiencies Currency Other

Consolidated 10.9 (2 ) 29 26 (5 ) (14 ) (23 ) Personal Care 5.5 2 25 10 (2 ) (13 ) (17 ) Consumer Tissue 22.5 (12 ) 31 54 (12 ) (7 ) (32 ) K-C Professional & Other 8.4 (14 ) 33 32 (11 ) (4 ) (28 ) Health Care 70.6 45 (3 ) 36 19 (4 ) (22 ) (a) Includes raw materials deflation and energy and distribution variations.

(b) Includes organization optimization severance and related charges and cost savings.

Consolidated operating profit increased $278 million or 10.9 percent from the prior year. The benefits of higher net selling prices, cost

savings of about $240 million and deflation in key cost components totaling approximately $675 million, were partially offset by lower sales volumes, negative currency effects of about $355 million, severance and related costs of $128 million, increased pension expense of about $155 million, higher operating costs and increased strategic marketing spending. Operating profit as a percent of net sales increased to 14.8 percent from 13.1 percent last year. Charges in 2008 of $60 million for the strategic cost reductions, discussed later in this MD&A, are not included in the results of the business segments.

(c) Strategic cost reduction charges of $60 million were included in 2008.

• Operating profit for the personal care segment increased 5.5 percent as higher net selling prices, materials and other cost deflation, and cost savings, were partially offset by organization optimization severance charges, unfavorable currency effects, higher operating costs and increased marketing expense. In North America, operating profit increased due to higher net selling prices, materials and other cost deflation, and cost savings, tempered by organization optimization severance charges and increased marketing expenses. In Europe, operating profit declined as increased sales volumes were more than offset by lower net selling prices and organization optimization severance charges. Operating profit in K-C’s international operations in Asia, Latin America, the Middle East, Eastern Europe and Africa increased as higher net selling prices and the benefits of volume growth were only partially offset by unfavorable currency effects.

• Consumer tissue segment operating profit increased 22.5 percent. Materials and other cost deflation, higher net selling prices and cost savings were partially offset by lower sales volumes, increased selling and marketing spending, organization optimization severance charges and negative impacts of production down-time which occurred earlier in the year, in part to drive inventory reductions. Operating profit in North America increased due to the same factors that affected the overall segment. In Europe, operating profit increased as materials and other cost deflation were only partially offset by unfavorable currency effects, lower net selling prices, and lower sales volumes. Operating profit in K-C’s international operations in Asia, Latin America, the Middle East, Eastern Europe and Africa increased as higher net selling prices and materials and other cost deflation were partially offset by increased marketing expenses, unfavorable currency effects and lower sales volumes.

21

• Operating profit for K-C Professional & Other products increased 8.4 percent as higher net selling prices and materials and other cost

deflation were partially offset by organization optimization

(a) (b)

(c)

Table of Contents

PART II (Continued)

severance charges, lower sales volumes, negative impacts of production down-time, in part to drive reductions in inventory, increased general expense, partially as a result of the Jackson acquisition, and unfavorable currency effects.

Organization Optimization Initiative

• Operating profit for the health care segment increased 70.6 percent. The benefit of higher sales volumes, materials cost deflation,

manufacturing production efficiencies and cost savings were partially offset by higher selling expenses, as a result of the I-Flow acquisition, and lower net selling prices.

In June 2009, the Corporation announced actions to reduce its worldwide salaried workforce by approximately 1,600 positions by the end of 2009. These actions resulted in cumulative pretax charges of approximately $128 million in 2009. Related savings from this initiative were approximately $55 million in 2009. See Item 8, Note 4 to the Consolidated Financial Statements for detail on costs incurred for the initiative.

Other income and (expense), net

Other income and (expense), net for 2009 includes currency transaction losses of $110 million, an increase of $92 million over 2008, partially offset by additional favorable settlements of value-added tax matters in Latin America. Approximately $73 million of the currency transaction losses in 2009 related to operations in Venezuela.

Commentary:

2008 versus 2007

Percentage Change in Operating Profit Versus Prior Year

Total Change

Change Due To

Volume Net

Price

Raw Materials

Cost

Energy and

Distribution

Expense Currency Other

Consolidated (2.6 ) 3 29 (20 ) (8 ) — (7 ) Personal Care 5.6 9 15 (14 ) (3 ) — (1 ) Consumer Tissue (14.4 ) (9 ) 60 (27 ) (18 ) (1 ) (19 ) K-C Professional & Other (10.5 ) (2 ) 23 (18 ) (9 ) 2 (6 ) Health Care (26.7 ) 8 (8 ) (10 ) — 2 (19 ) (a) Includes higher marketing and general expenses net of the benefit of cost savings achieved.

Consolidated operating profit decreased $69 million or 2.6 percent from the prior year. Charges for the strategic cost reductions of $60

million for 2008 were $47 million lower than in the prior year. Charges for the strategic cost reductions are not included in the results of the business segments. The effect of higher net sales, primarily due to increased net selling prices, plus approximately $171 million in cost savings, were more than offset by significant inflation in key manufacturing cost inputs of more than $725 million, higher manufacturing costs, primarily related to production downtime, of nearly $100 million, increased strategic marketing spending of about $95 million and higher levels of selling and administrative expenses, mainly to support growth in K-C’s international operations in Asia, Latin America, the Middle East, Eastern Europe and Africa. Operating profit as a percent of net sales decreased to 13.1 percent from 14.3 percent last year.

22

(b) Charges for strategic cost reductions were $47 million lower in 2008 than in 2007.

(a)

(b)

Table of Contents

PART II (Continued)

• Operating profit for the personal care segment increased 5.6 percent as higher net sales and cost savings more than offset raw materials and other cost inflation. In North America, operating profit increased due to the higher net selling prices and cost savings, tempered by materials and other cost inflation, and increased marketing expenses. In Europe, operating profit declined as cost savings were more than offset by the lower net selling prices and materials inflation. Operating profit in K-C’s international operations in Asia, Latin America, the Middle East, Eastern Europe and Africa, increased because the higher net selling prices and sales volumes more than offset increased marketing and general expenses.

• Consumer tissue segment operating profit decreased 14.4 percent. Increased net selling prices and cost savings were more than offset by cost inflation, the lower sales volumes and higher manufacturing costs, including the effect of planned production downtime. Operating profit in North America decreased due to the same factors that affected the overall segment. In Europe, operating profit declined as higher net selling prices and cost savings were more than offset by cost inflation. Operating profit in K-C’s international operations in Asia, Latin America, the Middle East, Eastern Europe and Africa, was even with the prior year as higher net selling prices were offset by cost inflation, and increased marketing and general expenses to support growth in these regions.

• Operating profit for K-C Professional & Other products decreased 10.5 percent because higher net selling prices were more than

offset by cost inflation for both wastepaper and virgin fiber and other materials and increased manufacturing costs, including higher maintenance spending.

Strategic Cost Reduction Plan

• Operating profit for the health care segment decreased 26.7 percent. The benefit of higher sales volumes was more than offset by the

lower net selling prices and higher manufacturing cost. In addition to cost inflation, the segment absorbed manufacturing-related costs as part of a plan to reduce inventory and also experienced higher costs related to changes in its manufacturing footprint.

In July 2005, the Corporation authorized a multi-year plan to further improve its competitive position by accelerating investments in targeted growth opportunities and strategic cost reductions aimed at streamlining manufacturing and administrative operations, primarily in North America and Europe. The strategic cost reductions commenced in the third quarter of 2005 and were completed by December 31, 2008. The strategic cost reductions resulted in cumulative charges of $880 million before tax or $610 million after tax. Cumulative savings under the plan were $395 million, including $60 million in 2009 and $110 million in 2008.

Other income and (expense), net

Other income and (expense), net for 2008 includes costs for a legal judgment and the refinancing of dealer remarketable securities partially offset by favorable settlement of a value-added tax matter in Latin America. A gain of $16 million for the settlement of litigation related to prior years’ operations in Latin America is included in 2007. In addition, currency transaction losses included in this line item were about $5 million higher in 2008 than in 2007.

Additional Income Statement Commentary

2009 versus 2008