key trends in the global beer market - arena-international.com · 1 international beer strategies...

TRANSCRIPT

1

International Beer Strategies Conference London May 2018

Key Trends in the Global Beer Market

Kevin Baker, Global Research Director, Beer & Cider, GlobalData

2

It Was 20 Years Ago Today…

Canadean’s 1st International Beer Strategy Conference was held at the Langham Hotel in London

3

Also Launched in 1998

4

The World in 1998

5

The last 20 years have seen a lot of change….

6

These didn’t exist in 1998…

7

We have come a long way since 1998

8

GlobalData’s Platforms

Market intelligence service providing analysis, reports, data, survey findings and news on 40 global market sectors.

An insight and innovation portal focused on the key driver of change – the consumer.

Market and competitive intelligence on retail companies, brands, technologies, consumers and shoppers.

GlobalData Wisdom

The only empirical, consistent and robust research and analysis solution to provide in depth intelligence on global foodservice.

GlobalData Foodservice

GlobalData Retail

GlobalData Innovation

Forecasting

9

1,34

0,75

0

1,37

5,49

7

1,39

5,32

1

1,43

0,39

3

1,46

0,62

3

1,51

9,71

0

1,57

8,54

6

1,67

1,99

5

1,76

7,65

4

1,79

9,94

7

1,81

4,38

3

1,85

9,24

5

1,90

7,14

7

1,95

0,58

9

1,95

5,23

1

1,96

8,95

8

1,94

4,03

2

1,93

5,70

5

1,95

3,97

2

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

000's HL YoY Growth

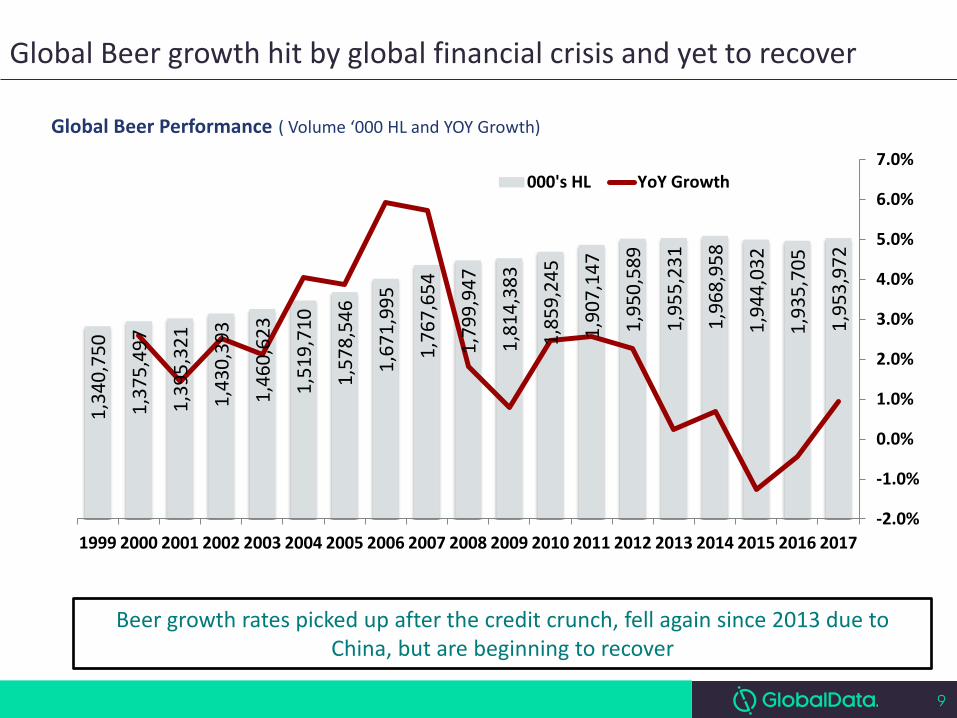

Global Beer growth hit by global financial crisis and yet to recover

Beer growth rates picked up after the credit crunch, fell again since 2013 due to China, but are beginning to recover

Global Beer Performance ( Volume ‘000 HL and YOY Growth)

10 10

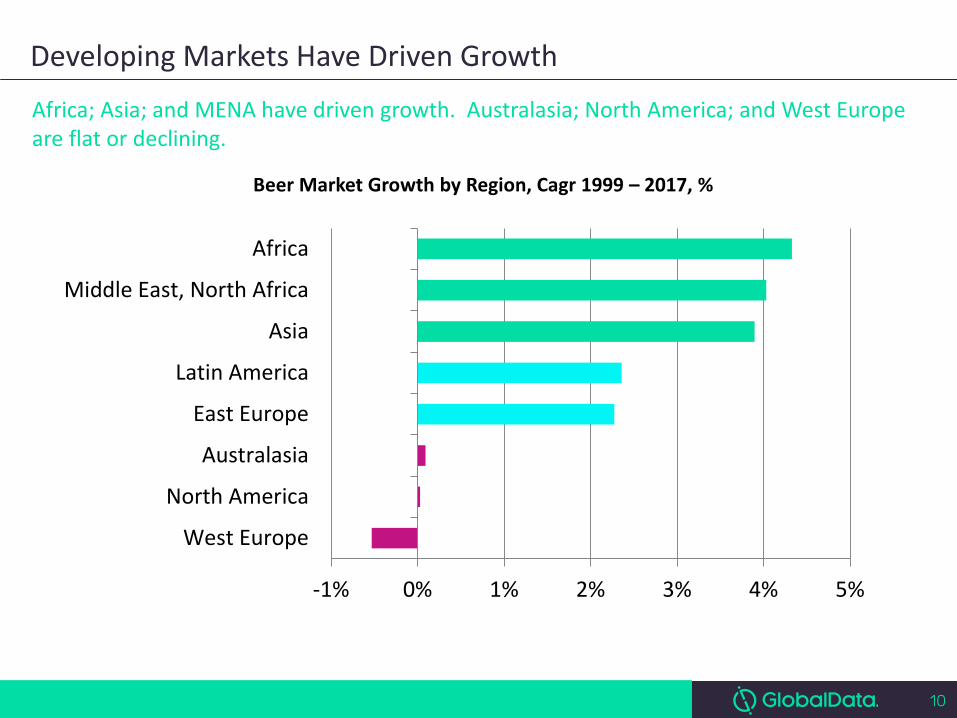

Developing Markets Have Driven Growth

Africa; Asia; and MENA have driven growth. Australasia; North America; and West Europe are flat or declining.

-1% 0% 1% 2% 3% 4% 5%

West Europe

North America

Australasia

East Europe

Latin America

Asia

Middle East, North Africa

Africa

Beer Market Growth by Region, Cagr 1999 – 2017, %

11

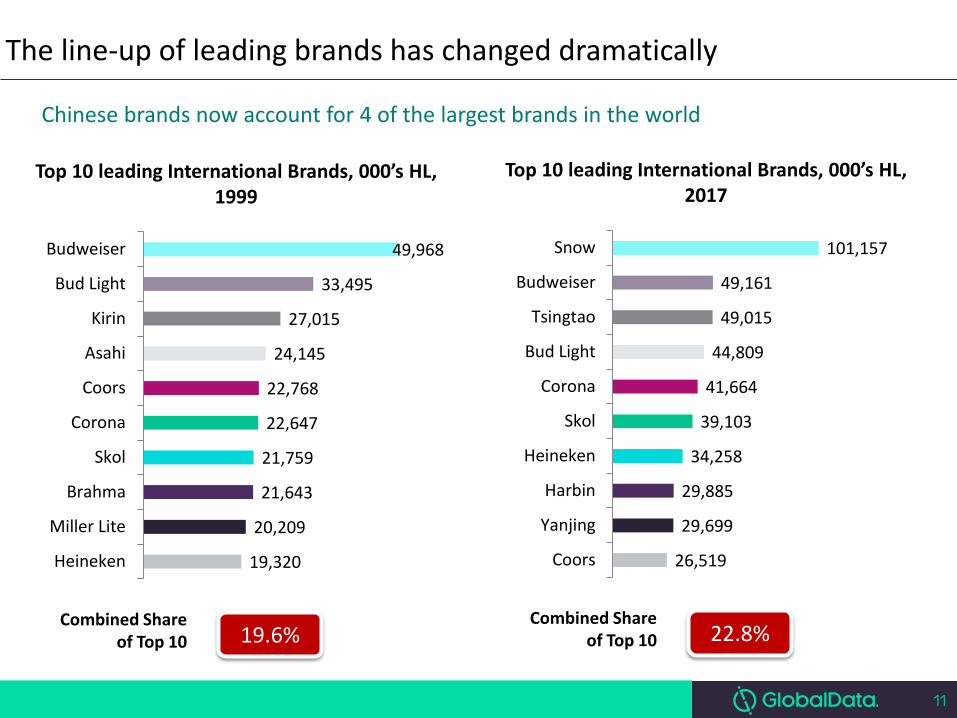

The line-up of leading brands has changed dramatically

Top 10 leading International Brands, 000’s HL, 1999

Performance

19,320

20,209

21,643

21,759

22,647

22,768

24,145

27,015

33,495

49,968

Heineken

Miller Lite

Brahma

Skol

Corona

Coors

Asahi

Kirin

Bud Light

Budweiser

Chinese brands now account for 4 of the largest brands in the world

19.6% Combined Share

of Top 10

Top 10 leading International Brands, 000’s HL, 2017

Performance

26,519

29,699

29,885

34,258

39,103

41,664

44,809

49,015

49,161

101,157

Coors

Yanjing

Harbin

Heineken

Skol

Corona

Bud Light

Tsingtao

Budweiser

Snow

22.8% Combined Share

of Top 10

12

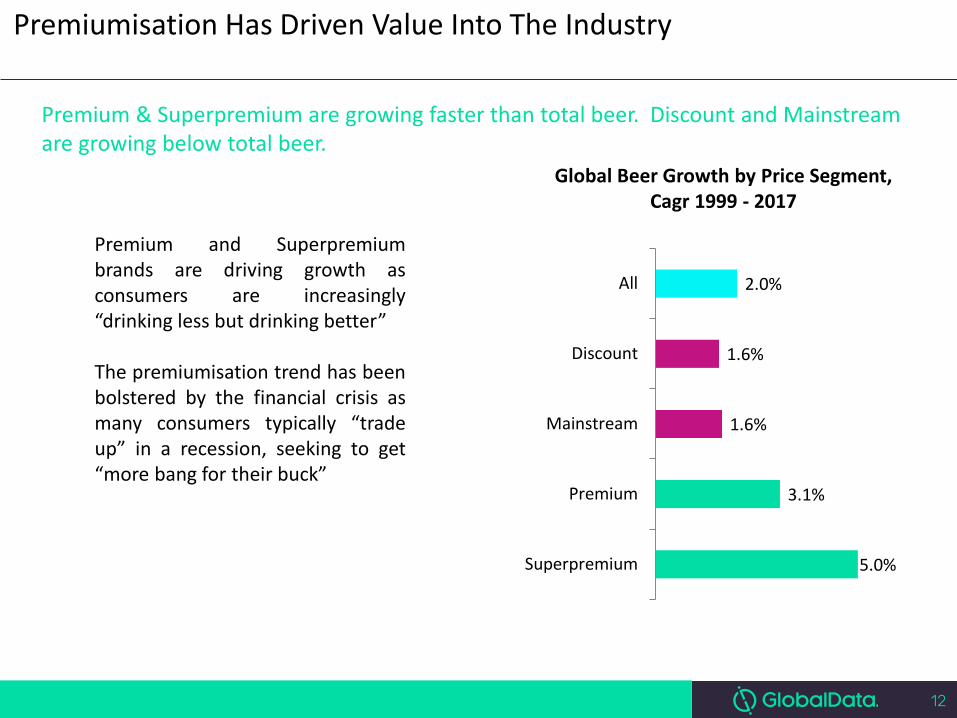

Premiumisation Has Driven Value Into The Industry

Global Beer Growth by Price Segment, Cagr 1999 - 2017

Performance

5.0%

3.1%

1.6%

1.6%

2.0%

Superpremium

Premium

Mainstream

Discount

All

Premium & Superpremium are growing faster than total beer. Discount and Mainstream are growing below total beer.

Premium and Superpremium brands are driving growth as consumers are increasingly “drinking less but drinking better” The premiumisation trend has been bolstered by the financial crisis as many consumers typically “trade up” in a recession, seeking to get “more bang for their buck”

13

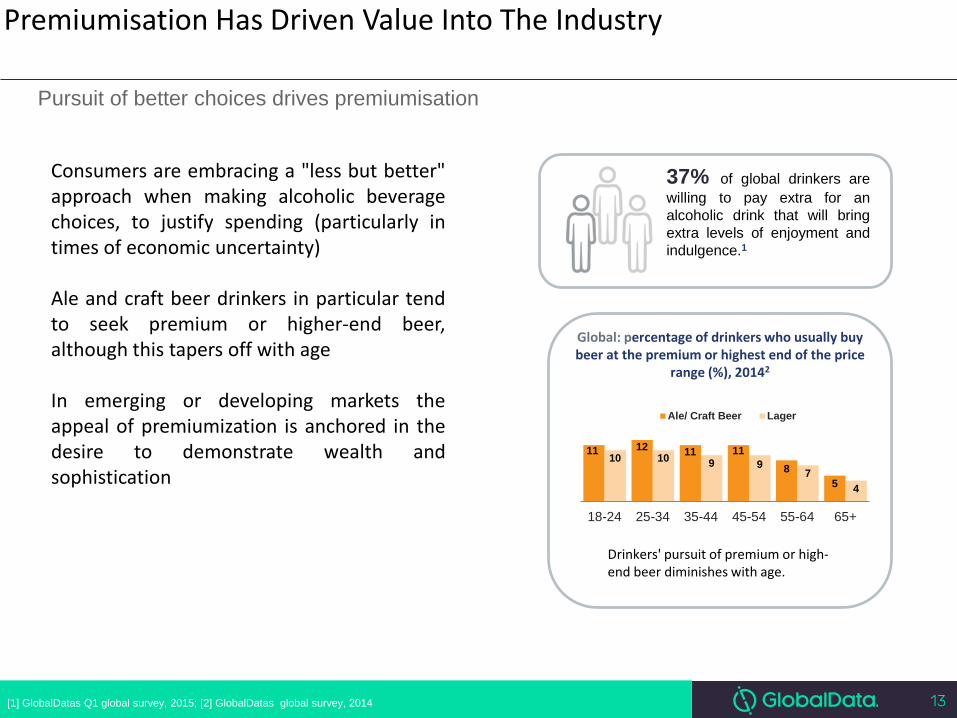

Pursuit of better choices drives premiumisation

[1] GlobalDatas Q1 global survey, 2015; [2] GlobalDatas global survey, 2014

Consumers are embracing a "less but better" approach when making alcoholic beverage choices, to justify spending (particularly in times of economic uncertainty) Ale and craft beer drinkers in particular tend to seek premium or higher-end beer, although this tapers off with age In emerging or developing markets the appeal of premiumization is anchored in the desire to demonstrate wealth and sophistication

37% of global drinkers are willing to pay extra for an alcoholic drink that will bring extra levels of enjoyment and indulgence.1

Global: percentage of drinkers who usually buy beer at the premium or highest end of the price

range (%), 20142

11 12 11 11 8

5

10 10 9 9 7

4

18-24 25-34 35-44 45-54 55-64 65+

Ale/ Craft Beer Lager

Drinkers' pursuit of premium or high-end beer diminishes with age.

Premiumisation Has Driven Value Into The Industry

14

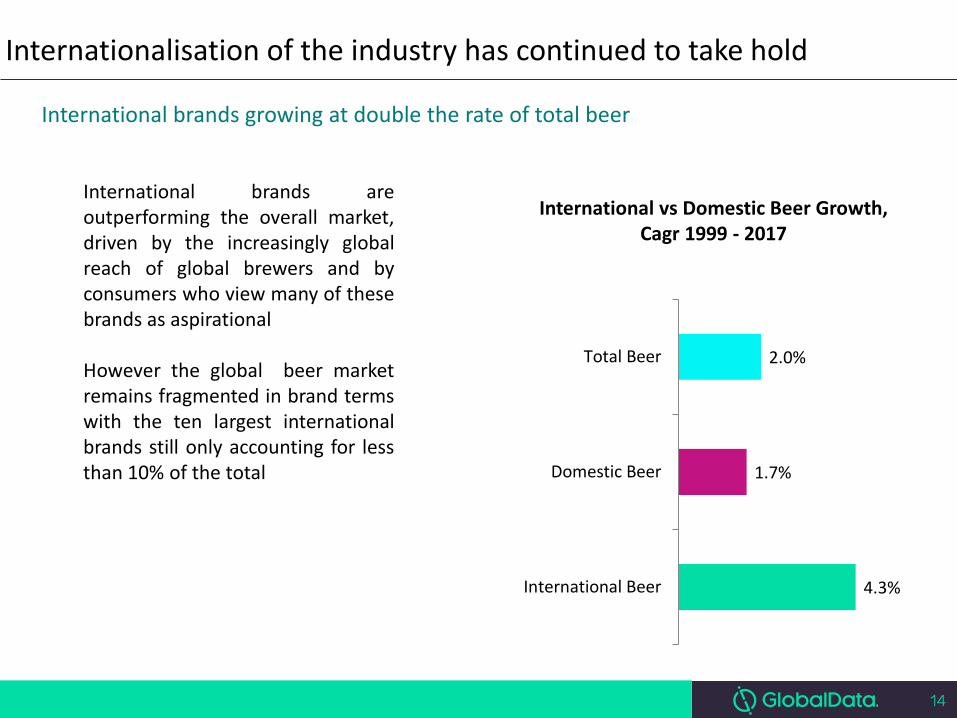

Internationalisation of the industry has continued to take hold

International vs Domestic Beer Growth, Cagr 1999 - 2017 Performance

4.3%

1.7%

2.0%

International Beer

Domestic Beer

Total Beer

International brands growing at double the rate of total beer

International brands are outperforming the overall market, driven by the increasingly global reach of global brewers and by consumers who view many of these brands as aspirational However the global beer market remains fragmented in brand terms with the ten largest international brands still only accounting for less than 10% of the total

15

Internationalisation of the industry has continued to take hold

Top 10 leading International Brands, 000’s HL, 1999

Performance

2,666

2,904

5,103

6,148

6,717

6,995

7,143

7,661

8,139

15,480

Tuborg

Coors

Stella Artois

Foster`s

Corona

Carlsberg

Guinness

Budweiser

Amstel

Heineken

International brands have increased their share of the market

5.2% Combined Share

of Top 10

Top 10 leading International Brands, 000’s HL, 2017

Performance

7,673

9,039

9,416

9,549

10,298

11,750

14,824

18,460

30,076

31,688

Amstel

Tiger

Modelo

Guinness

Stella Artois

Carlsberg

Tuborg

Corona

Budweiser

Heineken

7.8% Combined Share

of Top 10

16

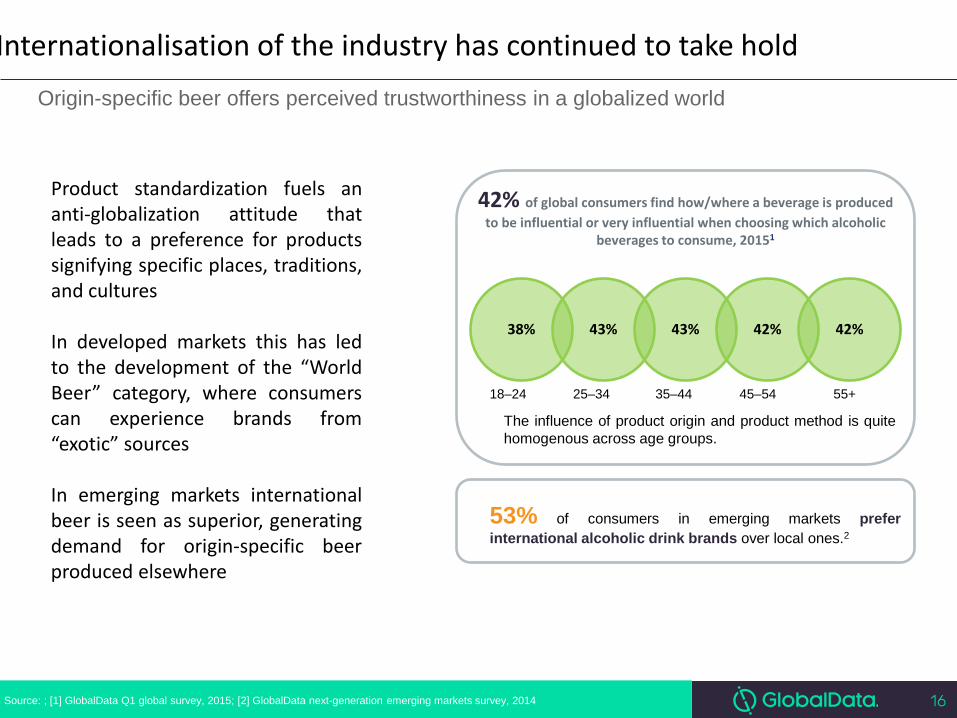

Origin-specific beer offers perceived trustworthiness in a globalized world

Source: ; [1] GlobalData Q1 global survey, 2015; [2] GlobalData next-generation emerging markets survey, 2014

Product standardization fuels an anti-globalization attitude that leads to a preference for products signifying specific places, traditions, and cultures In developed markets this has led to the development of the “World Beer” category, where consumers can experience brands from “exotic” sources In emerging markets international beer is seen as superior, generating demand for origin-specific beer produced elsewhere

42% of global consumers find how/where a beverage is produced to be influential or very influential when choosing which alcoholic

beverages to consume, 20151

53% of consumers in emerging markets prefer international alcoholic drink brands over local ones.2

38% 43% 43% 42% 42%

18–24 25–34 35–44 45–54 55+

The influence of product origin and product method is quite homogenous across age groups.

Internationalisation of the industry has continued to take hold

17

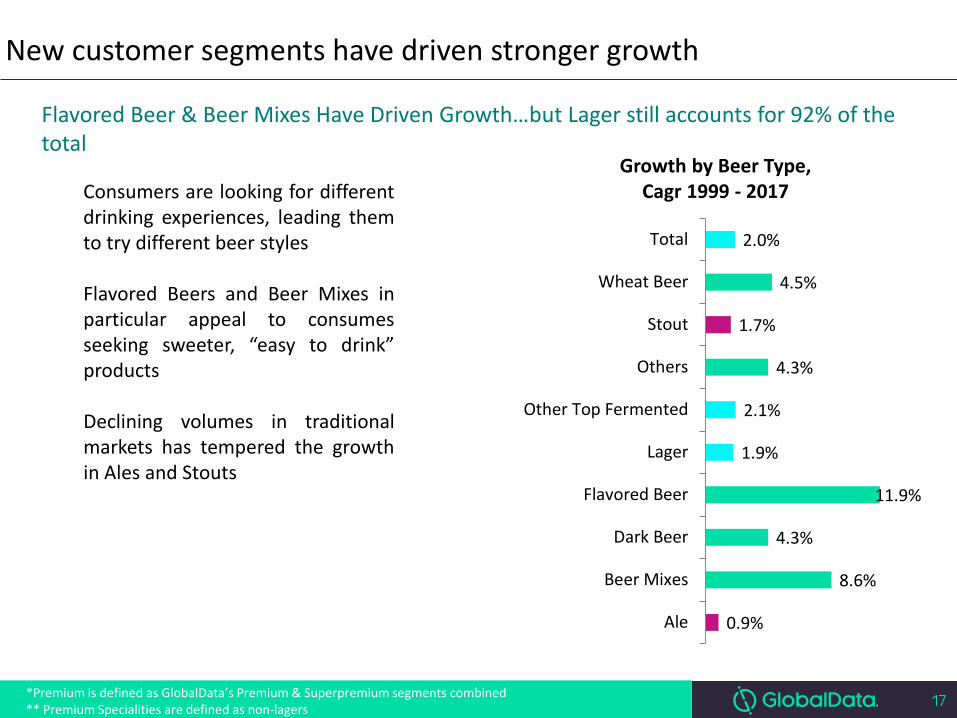

New customer segments have driven stronger growth

*Premium is defined as GlobalData’s Premium & Superpremium segments combined ** Premium Specialities are defined as non-lagers

Flavored Beer & Beer Mixes Have Driven Growth…but Lager still accounts for 92% of the total

Growth by Beer Type, Cagr 1999 - 2017 Performance

0.9%

8.6%

4.3%

11.9%

1.9%

2.1%

4.3%

1.7%

4.5%

2.0%

Ale

Beer Mixes

Dark Beer

Flavored Beer

Lager

Other Top Fermented

Others

Stout

Wheat Beer

Total

Consumers are looking for different drinking experiences, leading them to try different beer styles Flavored Beers and Beer Mixes in particular appeal to consumes seeking sweeter, “easy to drink” products Declining volumes in traditional markets has tempered the growth in Ales and Stouts

18

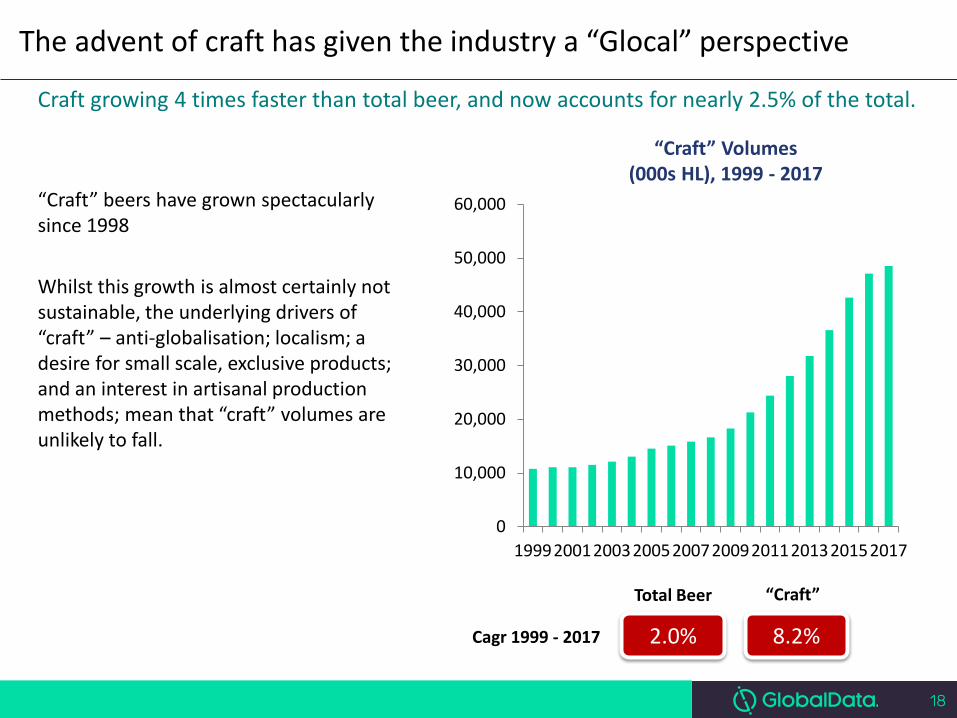

The advent of craft has given the industry a “Glocal” perspective

“Craft” Volumes (000s HL), 1999 - 2017

Total Beer “Craft”

2.0% 8.2% Cagr 1999 - 2017

Craft growing 4 times faster than total beer, and now accounts for nearly 2.5% of the total.

“Craft” beers have grown spectacularly since 1998 Whilst this growth is almost certainly not sustainable, the underlying drivers of “craft” – anti-globalisation; localism; a desire for small scale, exclusive products; and an interest in artisanal production methods; mean that “craft” volumes are unlikely to fall.

0

10,000

20,000

30,000

40,000

50,000

60,000

1999200120032005200720092011201320152017

19 19

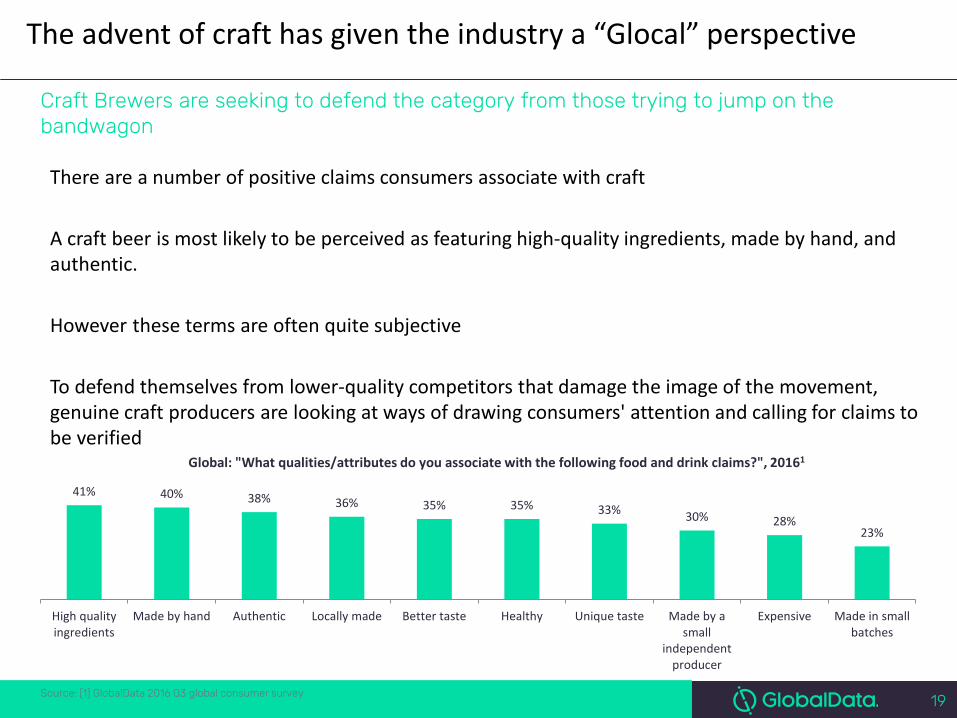

Craft Brewers are seeking to defend the category from those trying to jump on the bandwagon

Source: [1] GlobalData 2016 Q3 global consumer survey

There are a number of positive claims consumers associate with craft A craft beer is most likely to be perceived as featuring high-quality ingredients, made by hand, and authentic. However these terms are often quite subjective To defend themselves from lower-quality competitors that damage the image of the movement, genuine craft producers are looking at ways of drawing consumers' attention and calling for claims to be verified

41% 40% 38% 36% 35% 35% 33% 30% 28% 23%

High qualityingredients

Made by hand Authentic Locally made Better taste Healthy Unique taste Made by asmall

independentproducer

Expensive Made in smallbatches

Global: "What qualities/attributes do you associate with the following food and drink claims?", 20161

The advent of craft has given the industry a “Glocal” perspective

20 20

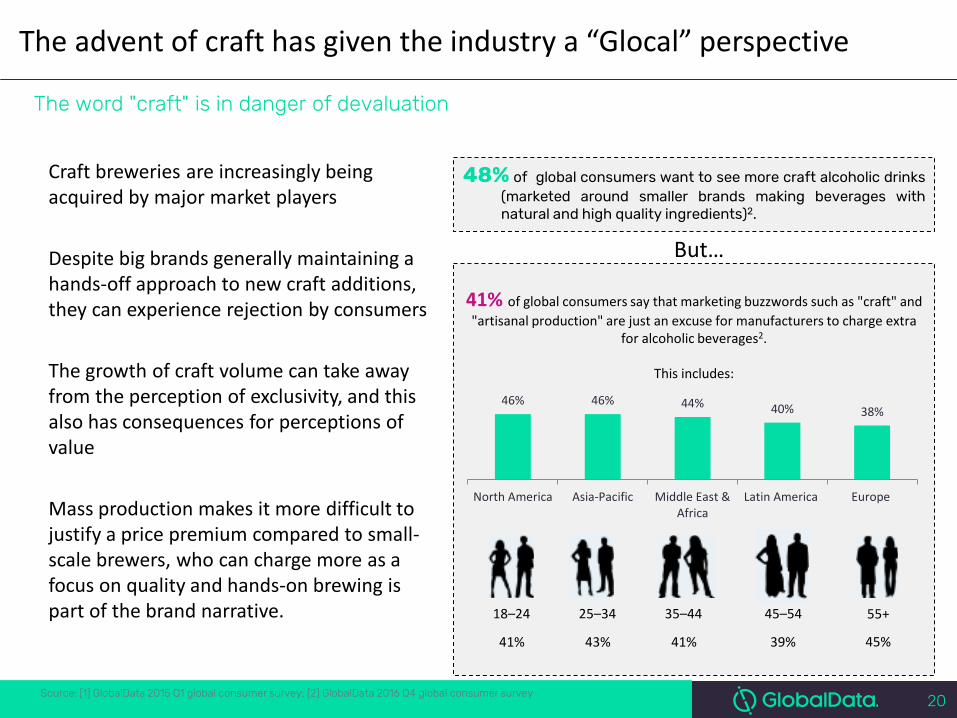

Craft breweries are increasingly being acquired by major market players Despite big brands generally maintaining a hands-off approach to new craft additions, they can experience rejection by consumers The growth of craft volume can take away from the perception of exclusivity, and this also has consequences for perceptions of value Mass production makes it more difficult to justify a price premium compared to small-scale brewers, who can charge more as a focus on quality and hands-on brewing is part of the brand narrative.

41% of global consumers say that marketing buzzwords such as "craft" and "artisanal production" are just an excuse for manufacturers to charge extra

for alcoholic beverages2.

This includes:

18–24 25–34 35–44 45–54 55+

The word "craft" is in danger of devaluation

Source: [1] GlobalData 2015 Q1 global consumer survey; [2] GlobalData 2016 Q4 global consumer survey

48% of global consumers want to see more craft alcoholic drinks (marketed around smaller brands making beverages with natural and high quality ingredients)2.

But…

46% 46% 44% 40% 38%

North America Asia-Pacific Middle East &Africa

Latin America Europe

41% 43% 41% 39% 45%

The advent of craft has given the industry a “Glocal” perspective

21

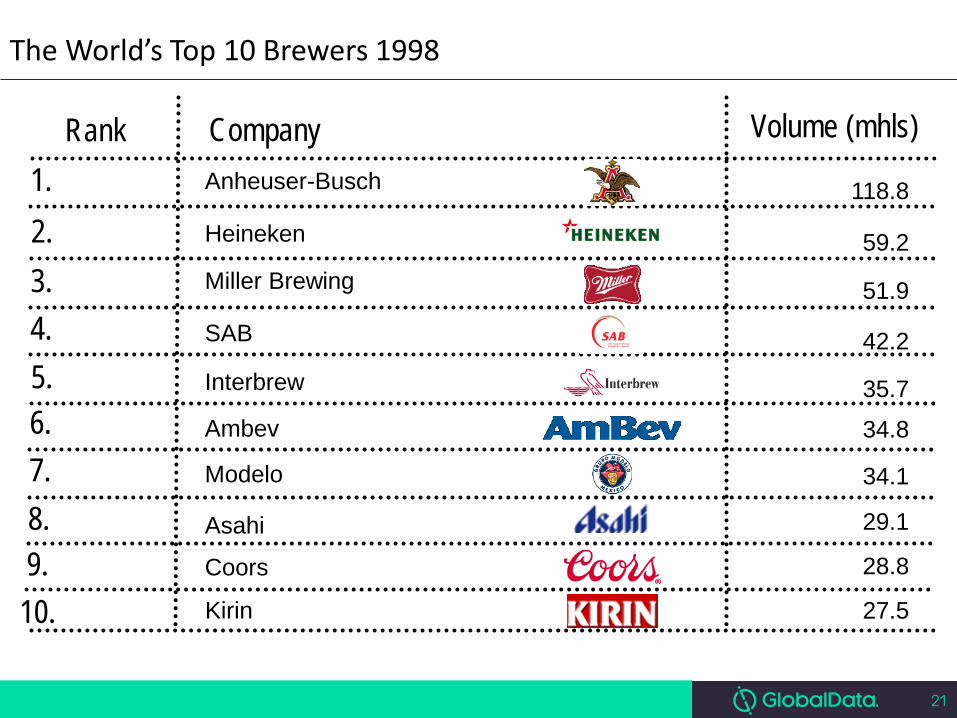

The World’s Top 10 Brewers 1998

1. Volume (mhls)

118.8 Anheuser-Busch

Company Rank

2. 59.2 Heineken

3. 4.

51.9 Miller Brewing

5. 42.2 SAB

6. 7.

35.7 Interbrew

8.

34.8

9. 29.1

Modelo

10. 28.8

Ambev

27.5

Coors

34.1

Asahi

Kirin

22

Based on 2016 volumes

The World’s Top 10 Brewers 2017 (Estimate)

1. Volume (mhls)

553.4 A-BInBev

Company Rank

2. 200.7 Heineken (inc. Schincariol)

3. 4.

118.3 Carlsberg

5. 117.3 China Resources (Snow) Brewery

6. 7.

91.6

Tsingtao

8.

79.8

9. 26.9

Yanjing

10.

60.6

Molson-Coors (incl. 100% of Miller Coors)

28.9

Asahi

45.1

Kirin (excl. Schincariol)

Castel

(incl. SABMiller; excl. all announced disposals)

(incl. Peroni, Grolsch & SABMiller’s East European breweries)

23

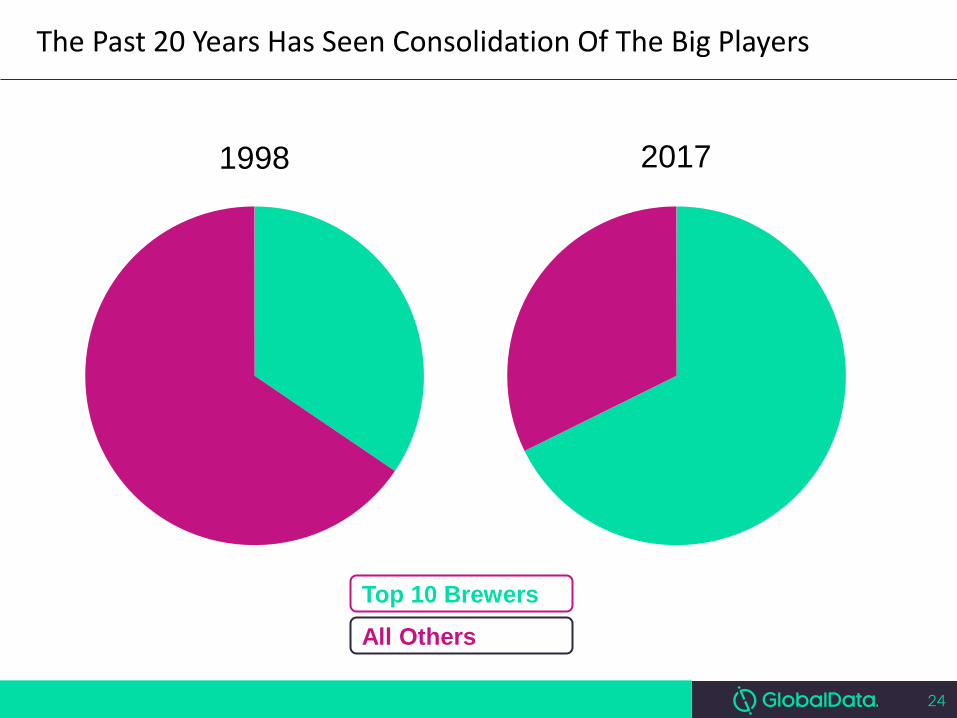

Major International Mergers & The Past 20 Years Has Seen Consolidation Of The Big Players

24

The Past 20 Years Has Seen Consolidation Of The Big Players

1998

Top 10 Brewers

All Others

2017

25 25

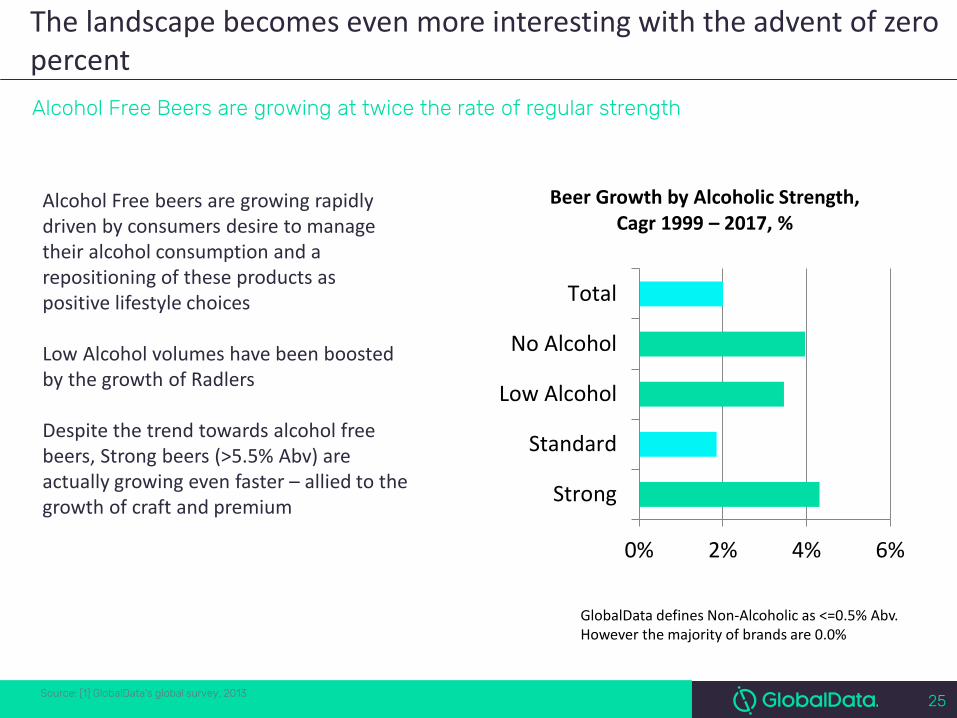

The landscape becomes even more interesting with the advent of zero percent Alcohol Free Beers are growing at twice the rate of regular strength

Source: [1] GlobalData's global survey, 2013

Strong

Standard

Low Alcohol

No Alcohol

Total

0% 2% 4% 6%

Beer Growth by Alcoholic Strength, Cagr 1999 – 2017, %

GlobalData defines Non-Alcoholic as <=0.5% Abv. However the majority of brands are 0.0%

Alcohol Free beers are growing rapidly driven by consumers desire to manage their alcohol consumption and a repositioning of these products as positive lifestyle choices Low Alcohol volumes have been boosted by the growth of Radlers Despite the trend towards alcohol free beers, Strong beers (>5.5% Abv) are actually growing even faster – allied to the growth of craft and premium

26 26

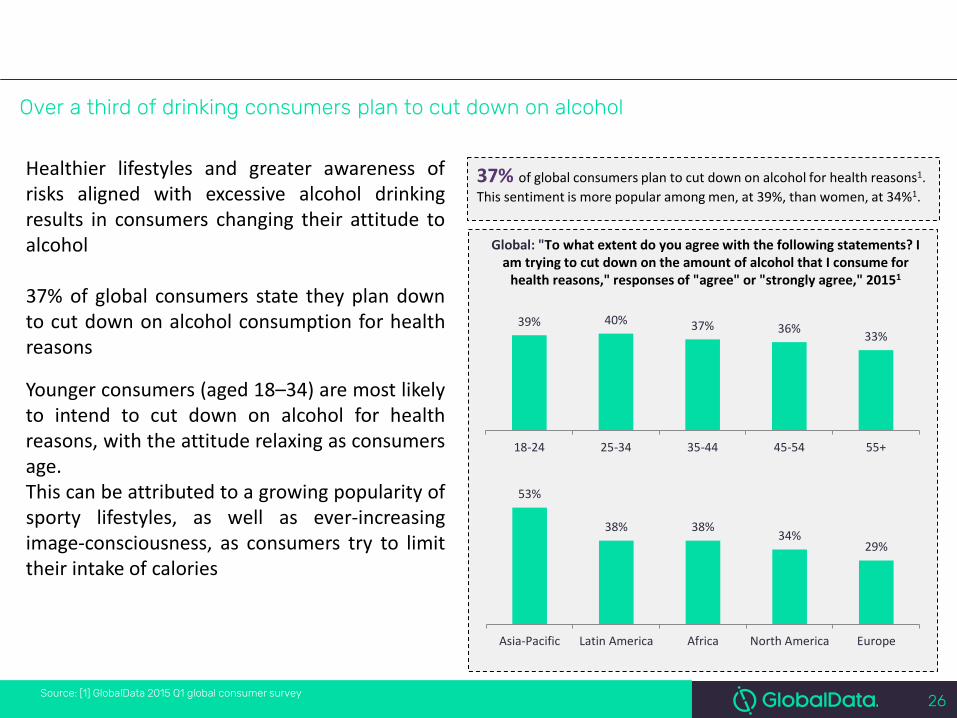

Over a third of drinking consumers plan to cut down on alcohol

Source: [1] GlobalData 2015 Q1 global consumer survey

Healthier lifestyles and greater awareness of risks aligned with excessive alcohol drinking results in consumers changing their attitude to alcohol 37% of global consumers state they plan down to cut down on alcohol consumption for health reasons

Younger consumers (aged 18–34) are most likely to intend to cut down on alcohol for health reasons, with the attitude relaxing as consumers age. This can be attributed to a growing popularity of sporty lifestyles, as well as ever-increasing image-consciousness, as consumers try to limit their intake of calories

39% 40% 37% 36% 33%

18-24 25-34 35-44 45-54 55+

Global: "To what extent do you agree with the following statements? I am trying to cut down on the amount of alcohol that I consume for

health reasons," responses of "agree" or "strongly agree," 20151

37% of global consumers plan to cut down on alcohol for health reasons1. This sentiment is more popular among men, at 39%, than women, at 34%1.

53%

38% 38% 34%

29%

Asia-Pacific Latin America Africa North America Europe

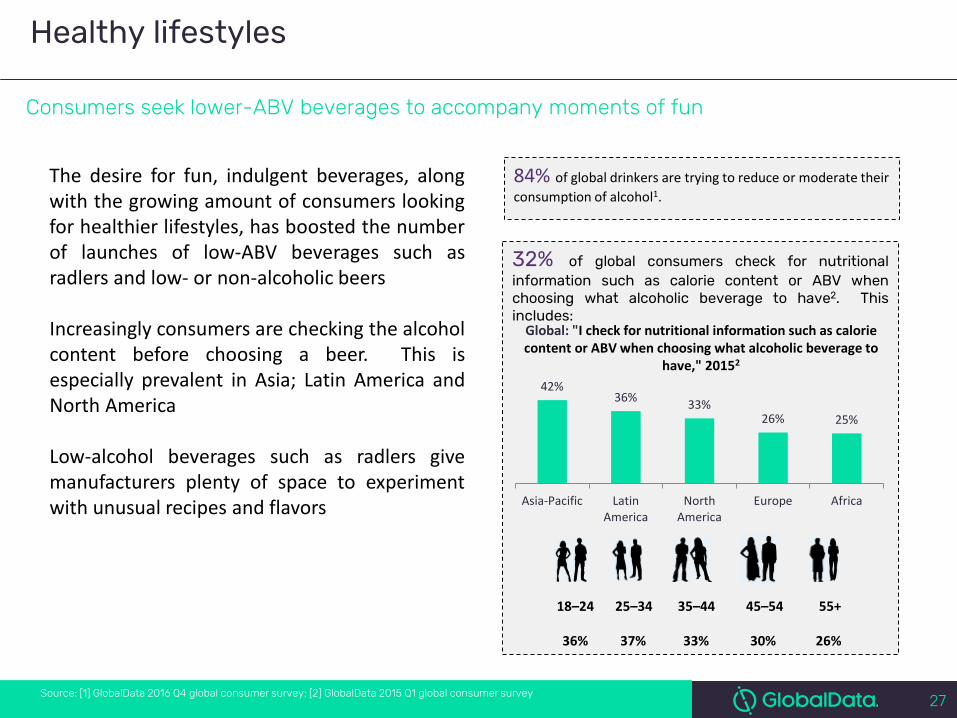

27 27

32% of global consumers check for nutritional information such as calorie content or ABV when choosing what alcoholic beverage to have2. This includes:

Consumers seek lower-ABV beverages to accompany moments of fun

Source: [1] GlobalData 2016 Q4 global consumer survey; [2] GlobalData 2015 Q1 global consumer survey

Healthy lifestyles

The desire for fun, indulgent beverages, along with the growing amount of consumers looking for healthier lifestyles, has boosted the number of launches of low-ABV beverages such as radlers and low- or non-alcoholic beers Increasingly consumers are checking the alcohol content before choosing a beer. This is especially prevalent in Asia; Latin America and North America Low-alcohol beverages such as radlers give manufacturers plenty of space to experiment with unusual recipes and flavors

84% of global drinkers are trying to reduce or moderate their consumption of alcohol1.

42% 36% 33%

26% 25%

Asia-Pacific LatinAmerica

NorthAmerica

Europe Africa

18–24 25–34 35–44 45–54 55+

36% 37% 33% 30% 26%

Global: "I check for nutritional information such as calorie content or ABV when choosing what alcoholic beverage to

have," 20152

28

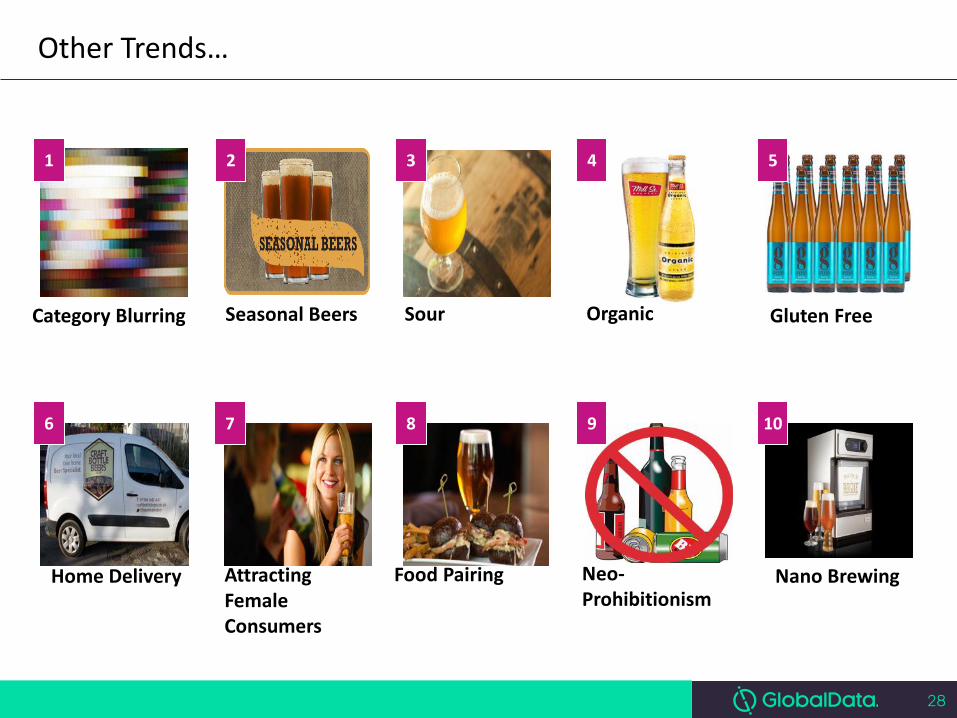

Other Trends…

Category Blurring

Attracting Female Consumers

Sour

Nano Brewing Neo-Prohibitionism

Food Pairing

Seasonal Beers

1

Gluten Free

2

Home Delivery

3 4 5

10 9 8 7 6

Organic

29

Conclusions

• The global beer market is unlikely to grow by more than 2% per annum for the foreseeable future

• However consumers are “drinking less, but drinking better”

• International premium brands are outperforming domestic mainstream

• Consumers are more experimental in their consumption habits and looking for new experiences and new beer styles

• Although the current momentum is unlikely to be maintained, “craft” is likely to continue to be a major issue

• The growth of craft and anti-globalisation/capitalism will see the emergence of more disruptors

• The industry has probably reached peak consolidation…but I said that in 2008!!

• Alcohol-Free beers are likely to grow in popularity and become mainstream choices

30

The next 20 years?

• Will beer return to the growth levels seen in the early 2000’s?

• Will the premiumisation trend continue?

• Will we see the emergence of truly “global” brands?

• Will we see new players from Asia join the acquisition trail?

• Will we see Spirits producers or Soft Drinks Companies enter the market, or will brewers acquire companies in those sectors?

• Has consolidation reached the endgame?

• Will Alcohol Free beers become a mainstream choice?

• See you in 2038!!

31

Thank You For more information please contact:

Kevin Baker, Global Research Director, Beer & Cider [email protected] 0044 7917 841 086