key features of electricity spot market · pdf filekey features of electricity spot market...

TRANSCRIPT

The Lantau Group

Key Features of Electricity Spot Market Risk PowerGen Asia 2015

Sarah Fairhurst

The Lantau Group

Oranges and electricity spot markets

• Imagine you wish to buy an orange… …you choose your grocer or supermarket, enter,

pick up an orange, check it has no flaws, note the price, take it to the checkout and pay. Then

you take it home and eat it. Simple.

• But what if the orange was instead electricity purchased from an electricity spot market?

– No choice of shop – you have to go to the spot market

– You cannot just enter, first you have to meet a number of requirements, including prudentials which

require letters of credit or other financial guarantees

– The only electricity on offer is the one at the spot price…”quality” is defined by the market

– It’s all real time, you have to “consume” your electricity there and then, before you pay for it

– And the price of the electricity is changing all the time. By the time you “check out” it may be very

expensive… but you already consumed it!

Trading electricity in spot markets is a risky business

Fruit analogies, or indeed lessons from other industries, may be unhelpful in understanding the risks

1

The Lantau Group

Even stock exchanges are not much like electricity

markets… after all.. When was the last time you

absolutely HAD to buy a stock at 2:06pm irrespective of

its price?

Lesson 1: Electricity is unlike any other market or

trading arrangement.

Extrapolating from other industries without

understanding the details of the electricity market can

be very risky indeed

2

The Lantau Group

Key risks include

• The big risk is the price risk:

– The price at which electricity is bought and sold varies by the hour or half hour (in some markets every 5

minutes)

• But electricity markets are also “real time” and purchasers pay after they take the power

• The real-time nature of the market combines with the price risk to create other risks for market

participants

– Credit risks for generators if purchasers take electricity but do not pay the price

– Tariff risks for retailers if they cannot predict or manage the price of supply to consumers

• And for non participants

– Supply risks for consumers if the market does not incentivise enough generation or if the retailers cannot

manage purchasing

– Political risks for Governments if the market does not work and power does not flow

Management of risk is not just prudent, it’s essential for spot markets to operate in the long term. Markets where risk is

not managed will ultimately fail

3

The Lantau Group

Analysing electricity spot markets without their context

will miss some of the biggest risks market participants

face, particularly in developing countries

Lesson 2: There are the obvious large risks in

electricity markets…. And then there are the less

obvious, often even larger risks associated with all

the arrangements around the market and the political

and economic environment the market exists in

4

The Lantau Group

So – what is driving the prices and price risk?

• At its core, energy pricing is simple supply and demand

5

Singapore Merit Order

0

50

100

150

200

250

300

350

400

0 1,000 2,000 3,000 4,000 5,000 6,000 7,000 8,000 9,000

Capacity (MW)

Dis

pa

tch

Co

st

(S$

/MW

h)

KeppelNEASembCorpTuasSenokoSerayaNew Entry Load

Market

Price

Supply

Curve

The Lantau Group

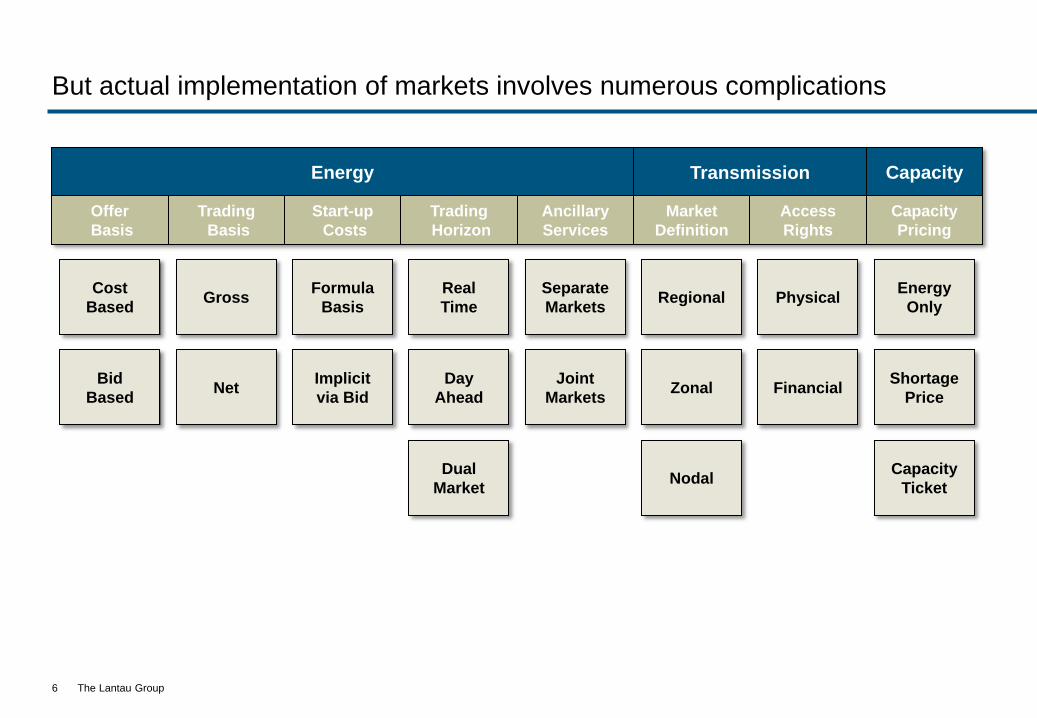

But actual implementation of markets involves numerous complications

6

Cost

Based

Bid

Based

Formula

Basis

Implicit

via Bid

Real

Time

Day

Ahead

Dual

Market

Separate

Markets

Joint

Markets

Regional

Zonal

Nodal

Energy

Only

Shortage

Price

Capacity

Ticket

Gross

Net

Physical

Financial

Energy Transmission Capacity

Offer

Basis

Start-up

Costs

Trading

Horizon

Ancillary

Services

Trading

Basis

Access

Rights

Market

Definition

Capacity

Pricing

The Lantau Group

Resulting in markets with many different designs

7

Component Element Singapore Philippines Korea Western

Australia

Eastern

Australia

New

Zealand

Energy Offer

Basis Bid-based Bid-based Cost-based Confused Bid-based Bid-based

Trading

Basis Gross Gross Gross Net Gross Gross

Start-Up

Costs Via bid Via bid Formula Via bid Via Bid Via Bid

Trading

Horizon Real-time Joint Day-ahead Day-ahead Real-time Real-time

Ancillary

Services Joint Separate Separate Confused Joint Joint

Transmission Market

Definition Nodal Nodal Zonal Regional

Regional

nodes Nodal

Access

Rights None None None

Access

Arrangement None Financial

Capacity Capacity

Pricing Energy-only Energy-only

Shortage

price

Fixed pricing

(originally) Energy-only Energy-only

The Lantau Group

The absolute size of price risk is a function of how high prices can go .. And

markets have very different price caps

Comparison of Selected Market Price Caps

USD/kWh (approx)

Due to increase

in 2015

0

2

4

6

8

10

12

14

WESM (2013) WESM (post 2013) Singapore NEMS Australian NEM US ERCOT

8

The Lantau Group

Even on the monthly average basis, the volatility in spot markets is apparent.

These high prices are necessary support investment

9

New Zealand historical monthly average final prices

2000-Current at 3 major nodes

Eastern Australia historical monthly average final prices

2000-Current at 3 major nodes

Without investment, price spikes get worse, the market fails, and huge value is destroyed

The Lantau Group

What drives price volatility in spot markets?

• Electricity spot price is set in each trading interval where the supply of electricity (offered by

generators) intersects with the demand for electricity (by customers)

• Thus factors which affect price are those which affect supply and demand

Supply

Demand

Price

10

The Lantau Group

Supply side price drivers

• The mix of plant (usually due to the mix of available fuels and policy choices in the past) drives

the shape of the supply curve

• A steeper supply curve tends to result in more volatile pricing

• Additional supply volatility may be caused by

– outages

– transmission constraints

– constrained fuels (e.g. hydro)

– intermittent generators (solar, wind)

11

The Lantau Group

Even relatively close markets can have quite different supply curves

0

25

50

75

100

125

150

175

0 5000 10000 15000 20000

Cumulative MW

Ind

ica

tiv

e M

arg

inal

Co

st

($/M

Wh

)

Approx. Peak Demand

(1999)Approx.Average Demand

(1999)

Cumulative MW 0 500 1000 1500 2000 2500 3000

Ind

icative C

ost ($

/MW

h)

Approx

Peak Demand

Marg

inal C

ost ($

/MW

h)

Market with very flat supply curve –

small changes in demand have very

little impact on prices

Market with steep supply curve –

small changes in demand have a

significant impact on prices

The example above is a historical snapshot of South Australia and Victoria, two adjacent sub-markets in Australia

But Luzon and Visayas, for example, also have quite different supply characteristics

12

The Lantau Group

Demand Side Price Drivers

• A steeper load duration curve tends to drive more volatility

– Steep load duration curves occur when some periods of time have much higher demand than others

• Fluctuations in demand cause by things such as:

– Weather fluctuations

– Seasonal weather (hot summers vs cold winters)

– Seasonal industries (Christmas or Chinese New Year shut downs)

13

The Lantau Group

Weather can have a significant impact in some markets – both within and

between years

7.0

7.5 2012

6.0

9.0

8.5

8.0

Jul Apr Mar Feb Jun May Jan Oct Aug Sep Nov Dec

6.5

5.5

2009

2008

2015

2010

2011

2013

2014

2007

+35%

GW

WESM Luzon grid monthly peak demand (2007-2015)

25

26

27

28

29

30

31

32

Feb Jan Mar Dec Nov Oct Sep Aug Jul Jun May Apr

Monthly average temperatures (Manila)

2015

2014

2013

2012

2011

2010

deg. Celsius

Relationship between hourly GDP-normalised*

demand and temperature in Luzon by time of day

(2006-2014)

Cooling and heating requirements throughout the year mean

that electricity demand is related to temperature.

Electricity is used for both cooling and heating, so weather

fluctuations cause significant impacts on demand

0

1

2

3

4

5

6

7

8

9

15 20 25 30 35 40

Shoulder

Peak

Off-peak

14

The Lantau Group

The shape of demand can vary significantly between different markets

On the one hand, very flat supply curves like

Singapore have relatively small daily

fluctuations in price

On the other hand, peaky markets like

those in the Philippines are much more

volatile

3,000

3,500

4,000

4,500

5,000

5,500

6,000

6,500

7,000

7,500

8,000

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

SingaporeWeekend Singapore

15

The Lantau Group

Behaviour of participants also drives price outcomes – some markets are more

concentrated than others but all are more concentrated than many other

industries

16

0%

20%

40%

60%

80%

100%

Other

NEM-QSL

CS

Energy

Stanwell

Intergen

Other

NEM-NSW

Macquarie

Origin

Other

WESM

Power

Seraya

SMC

PSALM

Aboitiz

Alinta

Tuas

Other

WEM

NewGen

Verve

NEM-SA

Other

Senoko

Snowy

Hydro

NEMS

Int’l

Power

Alinta

AGL

Energy

Other

Energy

Australia

First

Gen

Source: PEMC (2012 Annual Report); EMC (2012 Annual Report); AER (State of the Energy Market 2013); ERA (2013/14 capacity credits)

NEM

Generation company market share

Oligopoly market power exists in some degree in all energy markets, but so too does significant confusion between “bad”

market power (gaming) and the high prices that arise during periods of true economic scarcity

The Lantau Group

Analysing risk is specific to the market in question and

generic approaches are often unhelpful

Lesson 3: Understanding Market A does not

necessarily mean you understand Market B

17

The Lantau Group

Managing Electricity Spot Market risk depends on the market

• Firstly – understand what drives it: Example Philippines WESM

18

0

2

4

6

8

10

12

14

16

18

20

22

24

26

Jan-14 Jul-13 Jan-13 Jul-12 Jan-12 Jul-11 Jan-11 Jul-10 Jan-10 Jul-09 Jan-09 Jul-08 Jan-08 Jul-07 Jan-07

PhP/kWh

Low

hydro

Gas curtailments

and low hydro

Plant forced maintenance

outages and HVDC link

maintenance

Transformer breakdown and San

Jose substation congestion

Plant outages and

coal limitations

Plant outages

Gas curtailments

and plant outages

Average monthly WESM spot settlement price* (2007-14)

Gas scheduled outage

and plant outages

ERC-

regulated

price

reduction

The Lantau Group

Then decide what your objectives are, and how the risks might affect you

• A generator may wish to secure a minimum generation price and thus contract its output

– How does it manage the risk of being unavailable when the contract is called?

• A retailer may need to sell to franchise customers at a fixed tariff

– How does it ensure volatile spot prices do not result in purchase losses?

19

The Lantau Group

Understand what tools you have available to manage the risk – which also

varies by market

• Financial contracts are one of the most popular ways to manage spot market risk

• Australian NEM - deep and liquid derivative contract market, with a myriad type of contracts and

counterparties including exchange traded contracts that are settled through a clearing house

• Singapore - financial contract market exists but is much less liquid, fewer contract options.

Some hedging of fuel price as a proxy for electricity price

• Philippines - no financial contracts at all; physical bilaterals only and often for “whole of power

station” rather than flexible risk mitigation tools

20

The Lantau Group

Where contracts are not available, consider other mitigation mechanisms

• Vertical integration

– Generators entering into retailing and retailers building generation – is a physical way to mitigate spot

market risks

• Regulation

– In Philippines the regulation is effectively used as risk mitigation mechanism by retailers– gaining approval

for a contract allows fluctuating prices to be passed through to consumers

• Portfolio strategies

– Building a portfolio of supply options mitigates supply risks; having a portfolio of customers may assist in

managing demand side risks

• Customer management

– For contestable retailers choosing customers whose demand profile matches their supply available can be

very helpful (e.g. solar generators)

21

The Lantau Group

And finally, don’t forget the “other” risks also need attention in some markets

• Regulatory management – in markets where regulatory decisions have a surprisingly large

impact on the spot market behaviours and even prices (E.g. Philippines)

• Government management – where policy decisions can change the lay of the land completely

(E.g. carbon in Australia)

• Media management – high electricity prices are big news; manage the story before it manages

your business

22

The Lantau Group

Example of external risks: The Australian electricity industry never saw the

impact of various renewable and energy efficiency policies coming

© AEMO 2011 Energy and demand projections 3-9

Figure 3-3 — Comparison of the NEM-wide medium growth energy projection (GWh)

3.2.2 Maximum demand

Table 3-5 and Table 3-6 present actual and projected summer and winter MDs for the NEM. The 90%, 50%, and

10% POE MD projections are shown for the medium, high, and low growth scenarios.

The summer 10% POE MD is projected to increase over the next 10 years at an annual average rate of:

2.6% under the medium growth scenario, and

3.3% and 2.1% under the high and low growth scenarios, respectively.

The winter 10% POE MD is projected to increase over the next 10 years at an annual average rate of:

2.4% under the medium growth scenario, and

3.3% and 1.8% under the high and low growth scenarios, respectively.

180,000

190,000

200,000

210,000

220,000

230,000

240,000

250,000

260,000

2011 ESOO projection 2010 ESOO projection Actual

Year

Yearl

y e

nerg

y (G

Wh

)

The 2011 Statement of Opportunities (the main

planning document for the market) highlighted the

changes in policy and forecast the this energy

demand projection, even while making the

following statement:

Fast forward a mere 4 years and the actual

energy consumption and forecasts are very

different. Per capital consumption, in particular,

has fallen dramatically.

NATIONAL ELECTRICITY FORECASTING REPORT OVERVIEW

1.2 Comparison to the 2014 NEFR

As shown in Figure 3 below, the medium forecast for operational consumption is higher than the

published 2014 NEFR medium forecast. It is, in fact, closer to the 2014 high consumption forecast.

The changes in the 2015 NEFR forecasts are due to:

A recovery in underlying consumption in the residential and commercial sector, driven by a fall in

electricity prices after the repeal of the carbon price. Per capita consumption is falling more slowly

than in the last two years, and more slowly than AEMO forecast in the 2014 NEFR:

In the 2014 NEFR, per capita consumption was forecast to decrease by 4.4% from 2014–15

to 2017–18, to 5.9 megawatt hours (MWh) per year.

The 2015 NEFR forecasts show a smaller decline, with per capita consumption reducing

by only 2% from 2014–15 to 2017–18, to 6.1 MWh/year.

A decrease in forecast rooftop PV, which increases consumption drawn from the grid. This update

is due to an overestimate of uptake over the last year, and separate modelling in the 2015 NEFR

of rooftop PV in the residential and commercial sectors.

Revisions to the estimated electricity used per terajoule of LNG produced, which have increased

forecast LNG consumption.9 (The estimated volume of exports remains the same.)

Recovery in industrial consumption in some sectors, due to factors including the fall in the

Australian dollar.

1.3 Overview of historical operational consumption

As shown in Figure 3, operational consumption has been declining in the NEM since 2008–09.

In the five years to 2014–15, operational consumption declined by 14,461 GWh to an estimated

180,390 GWh, an average annual decline of 1.5%.

Figure 3 NEM operational consumption forecasts to 2017–18

9 Converting raw gas to LNG requires energy across the supply chain. While the LNG projects source much of their electricity from embedded generators, they also consumer electricity from the grid. See Lewis Grey Advisory, Projections of Gas and Electricity Used in LNG, 15 April 2015 for more details.

5.50

5.70

5.90

6.10

6.30

6.50

6.70

6.90

7.10

7.30

7.50

0

50,000

100,000

150,000

200,000

250,000

2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16 2016-17 2017-18

Re

sid

en

tial a

nd

co

mm

erc

ial

co

nsu

mp

tion

pe

r ca

pita

(MW

h/y

ea

r)

Op

era

tio

na

l c

on

su

mp

tio

n (

GW

h)

2014 - Low 2014 - Medium 2014 - High Low

Medium High R+C/capita Actual

© AEMO 2015 8

23

The Lantau Group

Contact Details

For more information please contact us:

By email General Capabilities Inquiries

Direct Communications

By phone +852 2521 5501 (office)

By mail 4602-4606 Tower 1, Metroplaza

223 Hing Fong Road,

Kwai Fong, Hong Kong

Online www.lantaugroup.com

Rigour

Value

Insight

Networks Electricity Gas

24