kelvin johnson and francisco canal vega - smith & … · kelvin johnson and francisco canal...

TRANSCRIPT

Emerging & International Markets organisations

Kelvin Johnson and Francisco Canal Vega

29 November 2012

Contents

Capital Markets Event, 28 - 30 November 2012

Emerging Markets

Introduction

International Markets

2

Economic balance – yesterday driven by rise of the US

(1) Source: Statistics on World Population, GDP, & Per Capita GDP 1 – 2008AD. Angus Maddison. University of Gronigen.

Capital Markets Event, 28 - 30 November 2012 3

Percentage of World GDP by PPP (1) (last 500 years)

Urbanisation - cities are expanding City Growth 2011 - 2025

4 Capital Markets Event, 28 - 30 November 2012 4

Source: UN DESA - http://esa.un.org/unup/Maps/maps_2011_2025.htm

Disease burden - extensive and growing

BURNS SICKLE CELL

OSTEOARTHRITIS

Death and DALY estimates for 2004 by cause for WHO Member States (Persons, all ages) (2009-11-12)

DALY = Disability adjusted life year

Capital Markets Event, 28 - 30 November 2012 5

OBESITY

http://en.wikipedia.org/wiki/File:Osteoarthritis_world_map_-_DALY_-_WHO2004.svg http://en.wikipedia.org/wiki/File:World_map_of_Male_Obesity,_2008.svg

http://en.wikipedia.org/wiki/File:Fires_world_map_-_DALY_-_WHO2004.svg http://www.ironhealthalliance.com/disease-states/sickle-cell-disease/epidemiology-and-pathophysiology.jsp

Market dynamics - tiers

High-

end

Low-end

Mid-

market

Capital Markets Event, 28 - 30 November 2012 6

• Key is knowing the local customer needs

S&N - progress and scale

A history of commitment

Since 1856: 156 years of ‘opportunistic

heritage’

2007: rigorous evaluation of potential and

clarity on strategic intent

2009: S&N “must win in China” priority

2011: “future growth driver”; expanded focus

and resource

Scale

• In 2007, EM/IM represented 6% of

S&N revenues, now 12% (2012

Q3 YTD)

• Revenue (EM/IM)

– 2011 revenue $454m

– 2012 Q3 YTD $350m

– contributing 43% of Group

growth

– EM/IM revenue split c ⅓ : ⅔

Capital Markets Event, 28 - 30 November 2012 7

Principles for success

• Where to consider – selecting the right markets

• Business model

– direct / indirect

• Ruthless focus – priority and unwavering concentration

• Product portfolio

– fit for market needs

Capital Markets Event, 28 - 30 November 2012 8

Contents

Capital Markets Event, 28 - 30 November 2012

Emerging Markets

International Markets

Introduction

9

International Markets traversing six regions

Capital Markets Event, 28 - 30 November 2012 10

Korea

ASEAN

IM CEE

Latin America

Africa

Puerto Rico

Singapore

Mexico *

*

*

*

*

*

*

MENAT

Dubai

Vienna

Seoul

Durban

San Juan Mexico City

$ profit “Drive"

• Maintain current momentum

• Continue to build presence

• Self funded growth, no incremental

investment

• Tough decisions and strong

prioritisation

“Develop" • Allocate small investment in medium/

longer term

• Establish business across franchises,

install infrastructure, grow sales

platforms

• Compromises in timing and scale of

investment

“Deliver" • Manage on an opportunistic basis

through 3rd parties or as lean

“scientific” sales office

• Higher expected ROI, shorter-term

• Cash generated used to drive

investments in EM and IM Level of maturity

Rigorous Portfolio Management

Capital Markets Event, 28 - 30 November 2012 11

Focusing our resources

Capital Markets Event, 28 - 30 November 2012

Addressing Diversity – illustrating the challenge

12

MENAT

Capital Markets Event, 28 - 30 November 2012 13

ASEAN

Capital Markets Event, 28 - 30 November 2012

Direct Sales

Distributor

Network

14

Summary

• Vast scope of our International Markets organisation requires focus and ability to make choices between countries and business areas

• Operational excellence is key to continue to deliver revenue growth and retain existing margins

• Continued success depends on the ability to address the unique needs of patients and customers in each market either through tailored business models and/or appropriate new products

Capital Markets Event, 28 - 30 November 2012 15

Contents

Capital Markets Event, 28 - 30 November 2012

International Markets

Emerging Markets

Introduction

16

Capital Markets Event, 28 - 30 November 2012

Agenda

1. Our Emerging Markets (EM) organisation and what drives growth

2. China: A success story and a strategic template

3. Maximizing the value in EM: mid-tier; innovation

4. Summary

17

Brazil

Russia

China

India

Drive the growth opportunity in the BRIC countries in a sustainable, profitable and capital efficient way.

EM – the Mission

Dubai HQ

Capital Markets Event, 28 - 30 November 2012 18

Growth in the Emerging Markets: 4 key growth drivers

Aging Population Emerging Middle Class Life-style diseases Convergence of techs

performance =cost

capital efficiency

Diabetes comorbidities

Out-patient care

Access to Heath care

Disposable income

Doctor’s capability

Age related conditions

Genetic patterns

19

A clear set of operating principles

Above Market Growth

Organic Growth

– Leverage existing product portfolio

– Stream of new products

– Innovation

Sub-segments of “Mid-tier”

New business models

New therapies

– Sales force effectiveness

Supportive Acquisitions

Key Enablers /

Prerequisites for Growth Quality of Growth

Critical mass

People

Systems

Sustainable

Profitable

Capital efficient

Above market

Entrepreneurial

Consistent with S&N values

Compliance

Core Behaviours

Ambition: Transformation from “sales organisations” to “business organisations”

Capital Markets Event, 28 - 30 November 2012 20

S&N China: We have built a strong market foothold

Local

players

(unit

share)

S&N

position

Competitive

dynamics

Recon >40% Leading

player

Most MNC’s have

established competitive

positions

Trauma >55% Established

in premium

tier

Synthes strong in

premium tier

AWM

(Incl. AWD)

25% Strong

position

Different dynamics to

Established Markets (e.g

films)

Arthroscopy <2% Leader Capital plays an

important part as

infrastructure being

established Source: S&N Estimates

Market Recon Trauma AWM Arthroscopy

Size ($MM) 275 400 100 80

Growth (%) High

teens

High

teens 20+% 30+%

Revenue Share Market Dynamics 2012

Recon Market Procedures 2012

Estimated Total Procedures (2012) – 250,000

Local Hip

Imported Knee

Local Knee

Imported Hip

Capital Markets Event, 28 - 30 November 2012 21

S&N China: Strategic road-map

• Profitable, sustainable and capital efficient growth • Focus on revenue growth

2012 - ONWARDS 2008-11

Overall vision

• Business organisation • Sales organisation Organization

•Geographic expansion

•Growth in all product categories

• New product launches

•Operational excellence programs

• Local R&D and Local Manufacturing

• Capital deployment

• Sales/marketing headcount

• Coastal areas

Growth levers

•Market still growing at rapid pace

• Increased complexity & sophistication – Government; competition;

Health Care system

• Rapidly expanding market Market context

• Strategic account / External affairs

• Strategic marketing and Business Development

• Distributor management

•Market development

• Sales management

•Medical education Competencies

Capital Markets Event, 28 - 30 November 2012 22

GBU Country CN Description License NumberIssued Date_(YYYY-

MM-DD)

Final Expiration

Date_(YYYY-MM-

DD)

Ortho Memphis, USA GⅡ胫骨高端部件 国食药监械(进)字2006第3461407号 2006/09/13 2012/12/31

Ortho Memphis, USA 骨科手术器械 国食药监械(进)字2007第1101624号 2007/09/06 2011/09/05

Endo Andover, USA 内窥镜摄像系统 国食药监械(进)字2007第1220419号 2007/03/14 2011/03/13

Endo Andover, USA 手术位置固定架系统 国食药监械(进)字2007第1660195号 2007/02/13 2011/02/12

Endo Andover, USA 内窥镜摄像系统 国食药监械(进)字2007第2221673号 2007/09/26 2011/09/25

Wound Hull, UK 透明防水敷料(商品名:安舒妥) 国食药监械(进)字2007第2641154号 2007/06/06 2011/06/05

Wound Hull, UK 手术薄膜(商品名:安舒妥) 国食药监械(进)字2007第2641155号 2007/06/06 2011/06/05

Wound Hull, UK 伤口愈合快示格胶贴(商品名:安舒妥) 国食药监械(进)字2007第2641163号 2007/06/06 2011/06/05

Wound Hull, UK 自粘性硅胶片(商品名:仙卡) 国食药监械(进)字2007第2660635号 2007/04/18 2011/04/17

Endo Andover, USA 带袢钢板 国食药监械(进)字2007第3460349号 2007/03/06 2011/03/05

Ortho Memphis, USA 股骨柄(商品名:SYNERGY) 国食药监械(进)字2007第3460384号 2007/03/06 2011/03/05

Ortho Memphis, USA 股骨柄(商品名:Echelon) 国食药监械(进)字2007第3460417号 2007/03/14 2011/03/13

Endo Andover, USA 双固定螺钉 国食药监械(进)字2007第3460490号 2007/03/28 2011/03/27

Ortho Memphis, USA 髋臼系统(商品名:Reflection) 国食药监械(进)字2007第3460491号 2007/03/28 2011/03/27

Endo Andover, USA 界面螺钉(商品名:SoftSilk) 国食药监械(进)字2007第3460884号 2007/05/21 2011/05/20

Ortho Memphis, USA 髋部螺钉系统(商品名:亚洲型) 国食药监械(进)字2007第3460919号 2007/05/28 2011/05/27

Ortho Memphis, USA 角度型钢板螺钉系统 国食药监械(进)字2007第3461237号 2007/06/13 2011/06/12

Ortho Memphis, USA 半髋关节假体组件(商品名:Tandem) 国食药监械(进)字2007第3461761号 2007/10/22 2011/10/21

Wound Hull, UK 洗必泰油纱(商品名:备替格) 国食药监械(进)字2007第3641695号 2007/09/28 2011/09/27

Ortho Memphis, USA 外固定支架(商品名:Jet-X) 国食药监械(进)字2008第1100870号 2008/04/12 2012/04/11

Commercial:

From sales to

business

Innovation:

Mid-tier

Operations:

Local & Export

Business hubs

Linhe BDA Suzhou Phase I and II

Complete Tailored options Local NPD

Targeted accounts Tracking procedures

S&N China: a continuous transformation

Registration of premium products

S&N China: Medical education a key differentiator

1. MAPPING OF HCP NEEDS 2. PROGRAMME DEFINITION

3. ALIGNED TO BUSINESS PRIORITIES 4. TRACKING SUCCESS

24

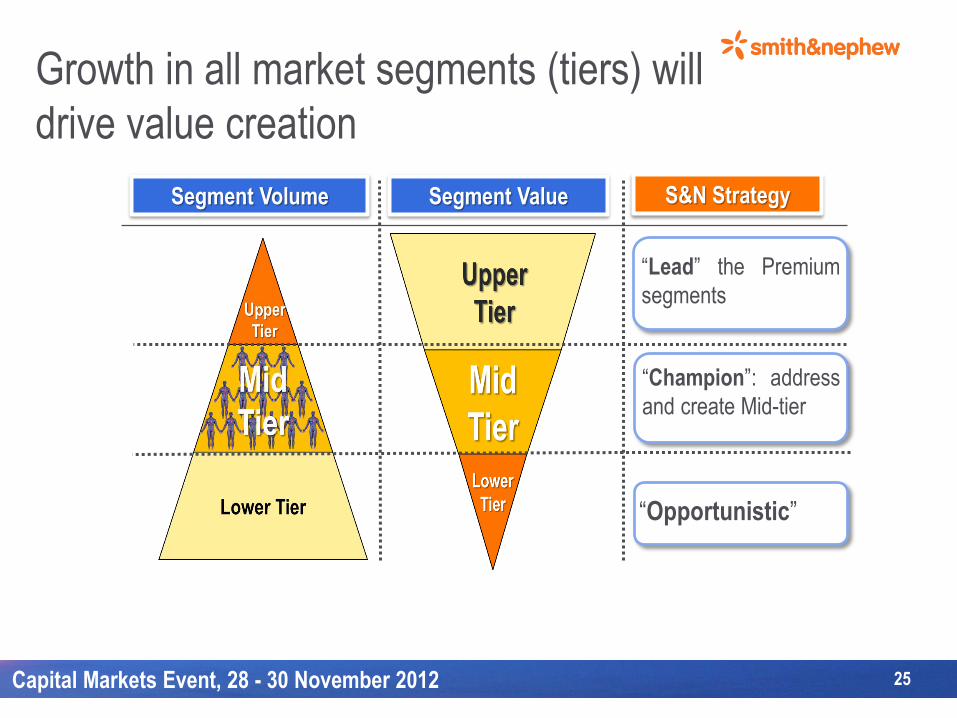

Segment Volume Segment Value S&N Strategy

“Lead” the Premium

segments

“Champion”: address

and create Mid-tier

“Opportunistic”

Growth in all market segments (tiers) will

drive value creation

Capital Markets Event, 28 - 30 November 2012 25

Access to HC, infrastructure and funding

is specific to each market

Brazil India China Russia USA

Macro

Indicators (1)

Avg. GDP Growth

(2007-12) 4% 7% 10% 3% 1%

Est. GDP Growth

(2012-17) 4% 6% 8% 4% 3%

2012 Population (m) 197m 1,223m 1,354m 142m 314m

Healthcare

Indicators (2)

$ HC spend per

capita $990 $54 $221 $525 $8,362

Out-of-Pocket 31% 61% 37% 31% 12%

Insurance coverage3 69% 39% 63% 69% 88%

Source(1) IMF World Economic Outlook database October 2012 – www.imf.org (2) World bank databank – 2010 data – www.databank.worldbank.org/ddp/

(3) Includes public and private insurance;

Capital Markets Event, 28 - 30 November 2012 26

“Mid-tier” is many segments, e.g: AWM India

Place of

Treatment

Mid-Tier

Patients

Upper Mid-Tier

and

Corp. Ins.

Lower Mid-Tier Bottom of the pyramid

Insured Out-of-pocket /

Outpatient

Gov’t Or Fund

Co-pay Out-of-pocket

Private

Hospitals

/ Clinics

DFU /

Pressure Ulcers

Surgery,

Minor

Burns

Large

chains

Small

hospitals

& clinics

Severe

Burn Clinic

Public

Hospitals

General

Military

Price

Insensitive

Limited Means Subsistence Patients in Public

Hospitals

Daily Wage

Earning

Daily Wage

Earners in

Public and

Small Private

Hospitals

10m ppl

55m ppl 1100m ppl

High Worth for AWM

Middle aged & elderly diabetes

sufferers

ICU & elderly bed ridden patients

Burns sufferers

30m ppl

Professionals

Industrial

Workers

1

2

3

4

5

6

Ppl = est. total population

Military

Active and retired personnel, and relatives

7

6m ppl

AWM

market

size

Popular care AWM

offering will grow

archetypes

Existing AWM products

cater to upper tier and

mid-tier archetypes

Time

1 2 3 4 7

5 6

27 Source: S&N Estimates

Innovation to address the Mid-tier:

lower cost; lower capital needs; ease of use

What

- Address/create Mid-tier

- Reduce cost of product

- Reduce delivered cost

- Simplify procedures (out-patient)

- Reduce capital demands

- Address unmet needs

How

- Keep S&N Quality

- Leveraging established market innovations

- Succeed in EM/IM R&D model

- Partnership and external vendors

- License and purchase agreements

Achieve one

offering

comprehensive

enough for 80% of

patients/practitioners

Capital Markets Event, 28 - 30 November 2012 28

The Diabetic Foot – addressing an

increased need in diabetic care Limb Salvage

TAYLOR SPATIAL FRAME Skin Care

SECURA

Surgical Debridement – Hydrocision

VERSAJET II

Debridement – Cadexomer Iodine

IODOSORB

Highly portable NPWT

PICO

Exudate Management & Protection

ALLEVYN LIFE

Capital Markets Event, 28 - 30 November 2012 Capital Markets Event, 28 - 30 November 2012 29 29

Distributor (D)

D+Rep Office (RO)

D+S&N legal entity

Sales Org Biz Organization

India

Brazil

Russia

China

Cri

tica

l Mas

s -

Gro

wth

Po

ten

tial

“Export”

“Export”

Admin support

Sales support

MedEd

Marketing

Commercial Org

MedEd

Supply Chain

HR/Finance

RAQA

Compliance Office

Commercial Org

Strategic Marketing; MedEd

Business Development

Support Functions

Government Affairs

Distributor Management

Legal

Key Account Management

Local Manufacturing and R&D

Ambition - transformation from

“sales organisations” to “business organisations”

30

Executive Summary

• Lead in the high-end while creating/expanding in the mid-tier

• NPD/Innovation

• Build critical mass/ Build capability (country; central)

• Operational excellence

• Acquisitions being pursued to accelerate growth and capabilities

Clear routes to accelerate growth in each specific market

31 Capital Markets Event, 28 - 30 November 2012 31