katherine forrest - king and wood mallesons - a look at the legal and governance issues associated...

TRANSCRIPT

The Financial System Inquiry

24th Annual Credit Law Conference Katherine Forrest

11979868_2

King & Wood Mallesons / www.kwm.com

Background to the FSI

2

• Purpose of the FSI • Assess how well the financial system is working • Make recommendations to foster an efficient, competitive and flexible

system • The terms of reference were announced on 20 December 2013

including: • developments since the 1997 Financial System Inquiry and the GFC; • new technologies and market innovations; • consumer protection; • superannuation; • international integration; and • developments in the payment system.

King & Wood Mallesons / www.kwm.com

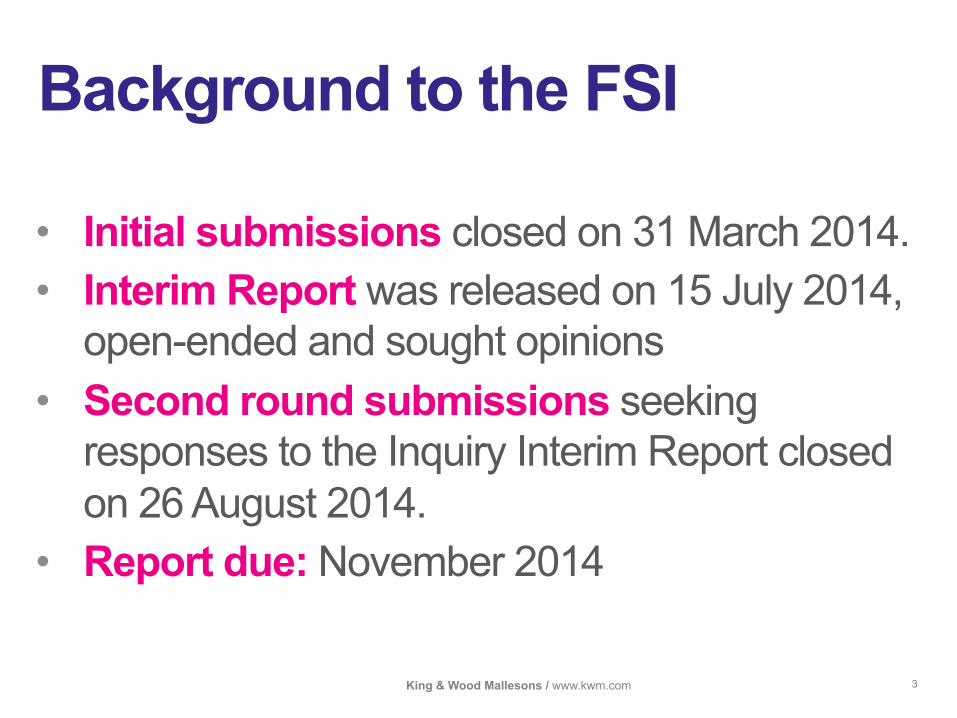

Background to the FSI

3

• Initial submissions closed on 31 March 2014. • Interim Report was released on 15 July 2014,

open-ended and sought opinions • Second round submissions seeking

responses to the Inquiry Interim Report closed on 26 August 2014.

• Report due: November 2014

King & Wood Mallesons / www.kwm.com

Initial Assessment

4

System has performed really well in meeting financial needs and facilitating productivity and growth.

However, future implications of: • future financial crises • fiscal pressures • productivity growth • technology change • international integration

King & Wood Mallesons / www.kwm.com

Competition and funding

5

• Credit reporting • Product switching • LMI • Small business lending

King & Wood Mallesons / www.kwm.com

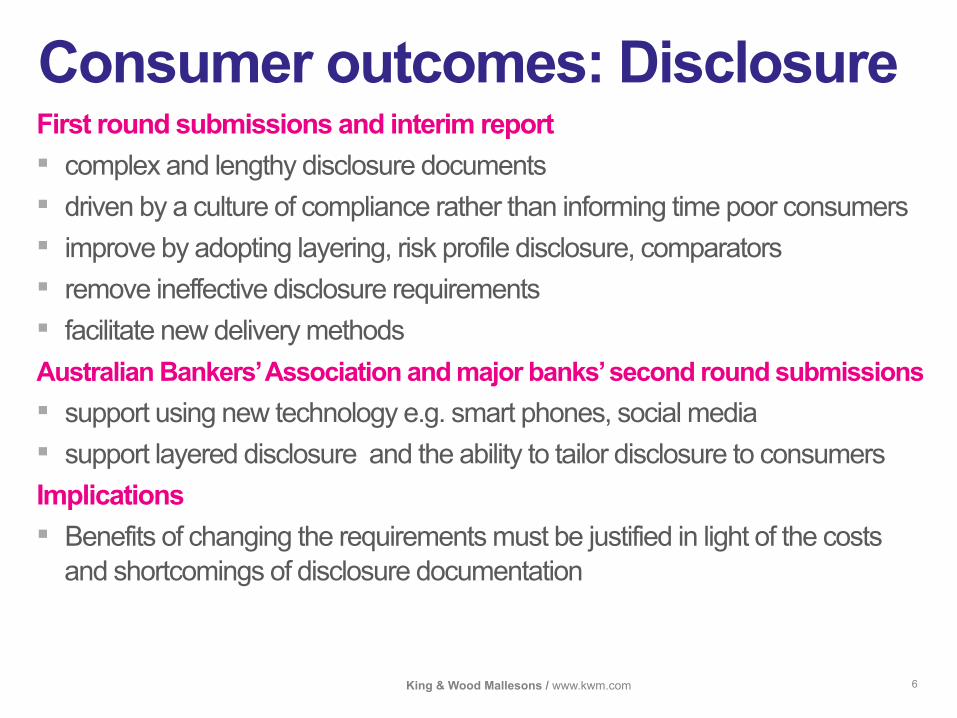

Consumer outcomes: Disclosure

6

First round submissions and interim report ▪ complex and lengthy disclosure documents ▪ driven by a culture of compliance rather than informing time poor consumers ▪ improve by adopting layering, risk profile disclosure, comparators ▪ remove ineffective disclosure requirements ▪ facilitate new delivery methods Australian Bankers’ Association and major banks’ second round submissions ▪ support using new technology e.g. smart phones, social media ▪ support layered disclosure and the ability to tailor disclosure to consumers Implications ▪ Benefits of changing the requirements must be justified in light of the costs

and shortcomings of disclosure documentation

King & Wood Mallesons / www.kwm.com

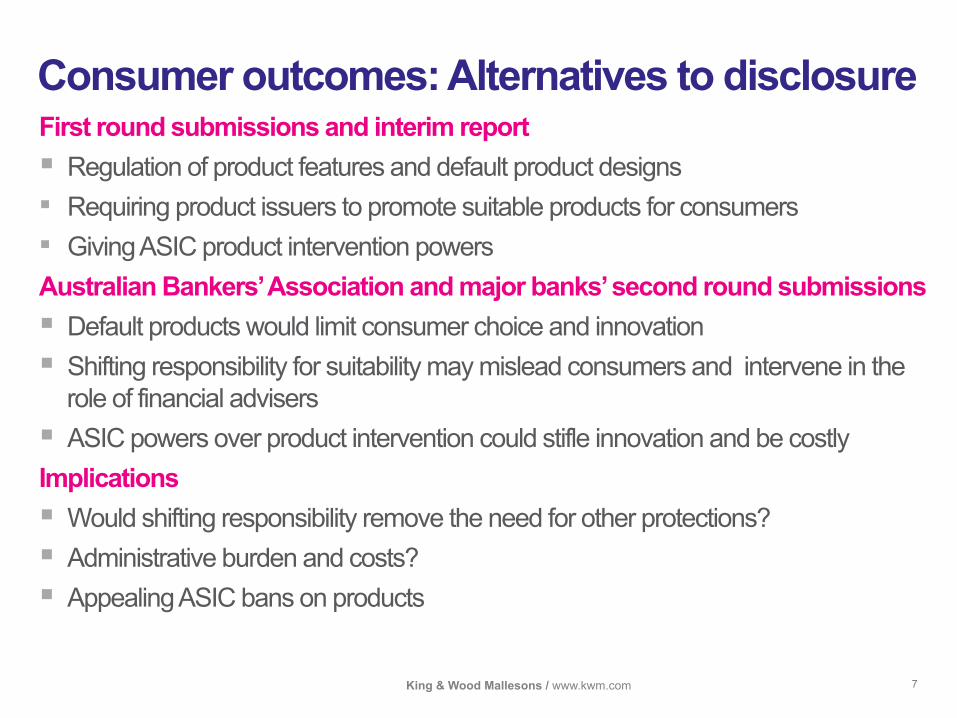

Consumer outcomes: Alternatives to disclosure

7

First round submissions and interim report § Regulation of product features and default product designs ▪ Requiring product issuers to promote suitable products for consumers ▪ Giving ASIC product intervention powers Australian Bankers’ Association and major banks’ second round submissions § Default products would limit consumer choice and innovation § Shifting responsibility for suitability may mislead consumers and intervene in the

role of financial advisers § ASIC powers over product intervention could stifle innovation and be costly Implications § Would shifting responsibility remove the need for other protections? § Administrative burden and costs? § Appealing ASIC bans on products

King & Wood Mallesons / www.kwm.com

Consumer outcomes: Advice

8

First round submissions and interim report • There is a need for higher quality financial advice and affordable advice. • Education, complementary and enhanced register of advisers • Wider banning powers • Differential labelling (sales v advice, independent v aligned) Australian Bankers’ Association and major banks’ second round submissions • Support better accreditation and continuing education and a public register • Support other elements of professionalisation e.g. best practices, professional

bodies • Support more clearly labelling 'General Advice' as ‘General Financial Information,’

and explicitly limiting who can hold themselves out to be a ‘financial adviser’. Implications ▪ Ability of regulators, banks to monitor and keep records of financial advisers ▪ Are different labels for financial advice helpful or simply another layer?

King & Wood Mallesons / www.kwm.com

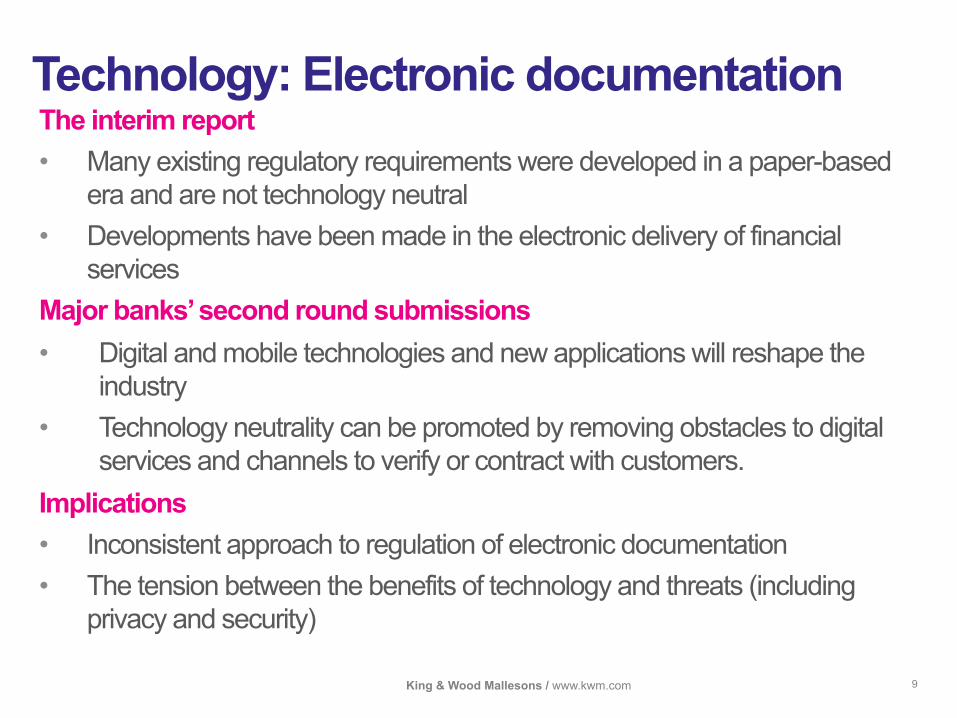

Technology: Electronic documentation

9

The interim report • Many existing regulatory requirements were developed in a paper-based

era and are not technology neutral • Developments have been made in the electronic delivery of financial

services Major banks’ second round submissions • Digital and mobile technologies and new applications will reshape the

industry • Technology neutrality can be promoted by removing obstacles to digital

services and channels to verify or contract with customers. Implications • Inconsistent approach to regulation of electronic documentation • The tension between the benefits of technology and threats (including

privacy and security)

King & Wood Mallesons / www.kwm.com

Payments products

10

The interim report • Lowering or removing interchange fee caps and capping merchant service fees • Regulation of payment products may be wound back e.g. purchased payment

facilities Second round submissions include • If interchange fees are lowered or banned, banks would need to adjust their business

models, as well as product fees and charges, to ensure cost recovery. • Banks support a narrower interchange range so merchants cannot justify

surcharging • Visa and MasterCard support capping fees and regulation by the RBA Implications • New payment systems that may be created by smaller and newer players • Should regulation be based on the risk of the institution, or should like products be

treated in the same way? • Regulators shaping the industry by explicit pricing controls

King & Wood Mallesons / www.kwm.com

Other issues

11

Stability and the major banks ▪ The risk posed by financial institutions that are “too big to fail” ▪ Will FSI will recommend more equity and less leverage? Superannuation ▪ Including fees, liquidity of assets, portability to allow rollovers, products for post-

retirement ▪ Leverage The corporate bond market ▪ How regulatory changes e.g. to disclosure can develop this market International integration ▪ How Australia can better integrate with ASIA e.g. through RMB internationalisation Role and Power of Regulators ▪ Independence, performance, higher penalties