karls thesis complete draft

TRANSCRIPT

THE FLINDERS UNIVERSITY OF SOUTH AUSTRALIA

FACULTY OF SOCIAL SCIENCES

SCHOOL OF POLITICAL AND INTERNATIONAL STUDIES

HONOURS PROGRAMME IN INTERNATIONAL RELATIONS

HAS REGIONAL TRADE HELPED OR HINDERED AUSTRALIA’S ECONOMIC DEVELOPMENT?

KARL COTLEANU

28 FEBRUARY 2002

THIS THESIS IS SUBMITTED IN PARTIAL FULFILMENT OF THE

REQUIREMENTS OF THE DEGREE OF

BACHELOR OF ARTS (HONOURS)

Table Of Contents

Synopsis iii

Acknowledgements iv

Abbreviations v

Introduction 1

Chapter

1 Early Influences Shaping Current Regional Trade Relationships

7

2 Liberalisation and the Consequences of International Exposure

19

3 The Importance of Regional Trade to Australia’s Future Growth

38

4 The Regional Financial Crisis, Consequences for Australia’s

Economic Development

47

5

6

APEC and the Development of New Regional Trade Regimes

The Forces Driving Australia into the New Millennium

55

70

Appendix

Bibliography

75

78

ii

iii

Synopsis

Australia’s economic development has been largely determined by its early

international trade relationships. While the importance of the US as a trading partner with

Australia is not in question, the relationship with the UK and Japan offers a significant

contrast. The thesis will explore both the differences and the similarities in their trading

relationship with Australia and the extent to which these relationships have determined the

distinctive commodity based focus of Australia’s regional trade.

Regional trade has seen the dominance of Australia’s primary resources in its

exports, marginalising secondary industry and reducing demands for research and

development that thrive on technical innovation and change derived from predominantly

manufacturing based industries.

The core argument of the thesis suggests that while regional trade has helped

Australia’s economic development, the region’s appetite for commodities in its own

industrial expansion has hindered this growth somewhat. This is particularly so in more

advanced, technological and innovative industries, which are now the leading growth

sectors in developed economies.

The Treasurer and later Australian Prime Minister Paul Keating advanced that

unless Australia reforms its industries it is in danger of becoming a banana republic. This

theme is addressed throughout the paper though the reforms suggested demand both

domestic structural changes, and the rethinking of trading modalities amidst the decline of

APEC as new regional trading forums emerge in the aftermath of the Asian financial crisis.

iv

Acknowledgments

I would like to thank Richard Leaver for his early direction and although my efforts

were not always forthcoming, his kind offers of assistance were always there. I would also

like to thank my dear friend William Mackay whose own tenacity became one of my

greatest strengths.

v

Abbreviations

AFTA ASEAN Free Trade Area

ANZUS Australia, New Zealand and United States Treaty

APEC Asia Pacific Economic Cooperation

ASEAN Association of South East Asian Nations

ASEAN + 3 ASEAN + China, Japan & South Korea

ASEAN 4 ASEAN + Indonesia, Malaysia, Thailand, Philippines

CER Closer Economic Relationship

EAEC East Asian Economic Caucus

EEC European Economic Community

ETM Elaborately Transformed Manufacture

EU European Union

FDI Foreign Direct Investment

FIRB Foreign Investment Review Board

FTA Free Trade Agreement

GATT General Agreement on Tariffs and Trade

GDP Gross Domestic Product

IMF International Monetary Fund

NAFTA North Atlantic Free Trade Agreement

OECD Organisation for Economic Co-operation and Development

OPEC Organisation of Petroleum Exporting Countries

R & D Research and Development

ROK Republic of Korea

RTA Regional Trade Arrangement

TCF Textiles, Clothing and Footwear

UK United Kingdom

UN United Nations

US United States

WB World Bank

WTO World Trade Organisation

WWI World War One

WWII World War Two

Introduction

Over the last decade Australia has been riding on a wave of economic success.

While global economic indicators have shown the world’s largest economies are

languishing, Australia has continued to reap the rewards from a booming economy. It has

grown to become one of the top-performing Organisations for Economic Co-operation and

Development (OECD) countries of the decade. Yet what is the driving force behind this

wave of growth, and what signposts (if any) did Australia use to direct the economy toward

its current path? What, also of the future should this wave of success lose its current

momentum?

These questions are particularly relevant now that the economic malaise in Japan

(brought to bear by the pressures of economic liberalisation), and the slowing in the

economies of the United States (US) and the European Union (EU) may well see a slowing

of the Australian economy. This situation demands the asking of fundamental questions

about the directions the economy took to reach its current stage of development, and where

this course is guiding Australia’s economy now. In keeping with the theme of this research,

the thesis sets out to establish the extent to which regional trade has helped or hindered

Australia’s economic development. Essentially, Australia’s relationship with the region

has, and will continue to have, a substantial influence over the extent to which this

economic development progresses.

However, before Australia’s current level of economic development can be

understood in its regional context, some consideration of certain historical points of

reference are needed, which to some extent have signposted the way Australia’s economy

has advanced. It is for these reason, chapter one of the thesis engages the idea that

Australia’s regional relationships are predicated by contrasting themes. These begin with

1

2

Australia’s relationship to the United Kingdom (UK) as a former colony, and the effects

this has had on Australia’s relationship with its subsequent major trading partner, Japan.

The change in the direction of Australia’s trade and the subsequent recomposition

of exports towards the region was brought about, as much by the UK’s hegemonic decline

as it was by changes in the global trading environment itself. This had to a considerable

extent set in train the way Australia perceives both itself, its place in the international

capitalist market, and the way it continues to conduct its regional trade relationships today.

Furthermore, chapter one addresses Australia’s overall bias towards commodity-

based export industries which, it is asserted, continues to undermine the general thrust of

economic development, retarding growth in the manufacturing sector of the economy. The

decline in manufacturing would be much worse, save for the fact that research and

development (R & D) in manufacturing accounts for a considerable amount of technical

innovation and change. This in turn has a considerable flow on effect to other sectors of the

domestic economy (see table 8).

Moreover, the real problems in Australia’s economic development are highlighted

by the gross domestic product (GDP), which has declined against many of Australia’s

regional competitors since the mid 1960’s. Australia’s population is considerably smaller

than that of Japan’s and some of its other trading partners in the region. While relative

output was comparable to these nations, for the size of the population, there has been a

continual decline of Australia’s GDP with its trading partners to the present day.

The thesis further asserts that industrial decline in Australia was largely the result

of sectoral disequilibrium, rather than, the simpler explanation of Japan’s dominance in the

nations commodities sector. Though, it was assisted considerably, by the insular inward-

looking industrial policies inherited from the UK.

3

In chapter two, the thesis acknowledges that Australia’s inwardness and the levels

of protection it maintained in response to the General Agreement on Tariffs and Trade

(GATT) bear the hallmarks of its relationship with the UK. In fact, the over emphasis on

commodity exports rather than an overall diversification of the economy also bears witness

to this imperial relationship. Thus was hailed in the Labor Party’s strategy in 1983 for the

liberalisation of the Australian economy to the full force of international competition as a

countermeasure to this somewhat isolationist, inward looking economy. In some quarters,

liberalisation was seen as essential to economic survival, while in others the consequences

of international exposure were considered more costly, especially in light of the uneven

nature of regional liberalisation. There was, however, a tendency for Australia’s economy

to revert to the pre-GATT protectionist measures of the inter-war years. This is to some

extent reflected in the automotive industries’ continual thrust for protection, which

indicates a decided lack of emphasis by the parent firms for expenditure on R & D in the

Australian economy.

While liberalisation of the Australian economy had freed up the financial sectors,

this offered a considerable contrast to industries still highly protected from international

competition, such as the textiles, clothing and footwear (TCF) industries. These industries

represent the continued protection of inefficient producers in changing market conditions,

which insulated the economy from international competition.

These issues hark back to chapter one and the stifling of manufacturing in

Australia’s domestic economy as the nation continued an over-reliance on commodity

exports at the expense of technological innovation and change. This underpins the

structural problems in Australia’s economic development, which Paul Keating had not

fully addressed in his banana republic statements concerning the need for the Australian

4

economy to change. In many ways, this points to a lack of investment in education as a

precursor to Australia’s current problems.

Chapters one and two have been interwoven by a common thread linking

Australia’s over-emphasis on commodity exports and a subsequent decline in

manufacturing with falls in the level of technical innovation and change. Yet, what

relationship does this have to the importance of regional trade to Australia’s future growth?

Chapter three attempts to draw the argument out of aspects of the past, focusing on

those, which are more relevant to Australia’s current trading environment. Here the

emphasis is upon the many differences that Australia faces in its relationship with the

region, as the demands of its geography determine an intrinsic requirement to be included

in regional trade arrangements (RTAs). This chapter highlights the difficulties of such

ventures not just in the differences between Australia and the region, but also the nature of

competing capitalisms and competing ethnic rivalries occurring between, and within, the

regional economies themselves.

While such tensions are of paramount concern for transnational capital, which

searches for more stable environments for investment, the fact remains that the region is

still very important for Australia’s future growth. With this in mind, the chapter concludes

on aspects of increasing trade Australia is conducting with the region. There is much cause

to be wary here owing to the extent to which foreign direct investment (FDI), in terms of

both equity and levels of ownership, may well undermine new export industries for

Australia. This is primarily because much of Australia’s production is geared for domestic

consumption rather than export which require minimal input in terms of R & D

expenditure. Consequently, Australia’s economy is perceived as a commodity based, low

5

technology, branch economy in international money markets, with this perception leading,

in some part, to the nation’s insulation against the regional financial crisis of 1997.

In chapter four, the thesis qualifies why to some extent Australia may be considered

somewhat removed from the region, with many of these economies increasingly engaged

in technology related industries. These industries no longer require vast amounts of raw

materials in the manufacturing process as heavy industry did when the region began its

industrial expansion. This suggests that Australia’s trade diversion from the region to the

US and the EU during the Asian financial crisis was done with a view of trading with more

stable markets outside the region. This was evidenced by, growing strategic and economic

uncertainty in East Asia at the time. The argument further asserts that the ensuing currency

devaluation of Australia’s dollar as a direct result of the crisis was more favourable to extra

regional rather than intra regional trade. Combined with growing demands for regional

caucuses such as ASEAN + 3 which excluded nations such as Australia and the US, the

full impact of the crisis may yet unfold.

With this in mind, the chapter concludes on a more positive note assessing

Australia’s currency devaluation, financial market stability and openness as positive signs

for future investment. Much of this investment is tailored to the needs of large corporations

such as Holden and Ford, which already have a seemingly nationalised and established

brand name in Australia. Therefore, the opportunity of relocating to attractive markets,

where the consideration is not only cost competitiveness but also stable governments and

the availability of skilled workforces adds to the above considerations as worthy

inclusions.

In chapter five, the thesis raises concerns over APEC and the apparent failure of the

multilateral process, as regional economies rush to stamp their name on RTAs. The fact

6

that Australia has only been able to sign its name to one is disconcerting enough. Given

this consideration, there is some weight for an increasing bilateral relationship between the

US and Australia at a time when both western economies are feeling excluded from rising

regional caucuses. Whereas, the distant possibility of such a relationship is considered for

its merits and weaknesses, the ramifications for regional trade relationships suggest both

positive and negative effects for a small economy like Australia’s. By virtue of its linkages

with the world’s largest international economy, such a relationship could go some way in

according Australia recognition. Nonetheless, the possibility of inclusion in extra-regional

and intra-regional policy initiatives (not too distinct from arrangements under APEC), is no

guarantee of inclusion and could go the other way and see Australia excluded from these

very same arrangements.

7

CHAPTER 1

Early Influences Shaping Current Regional Trade Relationships

Traditionally, Australia’s export markets were dominated by the United Kingdom

and Europe (Figure 1).1 Australia’s colonial ties with the British Empire were the major

tenet for this trading relationship. As a relatively strong Imperial power, the UK had the

resources to service relationships with distant colonial outposts such as Australia, helping

to keeping this empire intact. Combined with a depressed Europe racked by two world

wars, this trading relationship saw Australia as a major producer of rural commodities

surge in demand.

Figure 1: Australia’s traditional export markets as a percentage of total trade

Source: Goldsworthy, D., Facing North, Vol. 1, Melbourne University Press, 2001, pp. 422-427.

1 Goldsworthy, D., Facing North, A Century of Australian Engagement with Asia, Vol. 1, Melbourne University Press, 2001, pp. 46-51.

8

By the 1950’s, rural exports composed 80 per cent of total export income, with

wool, wheat, and bovine products being the main export commodities, while

manufacturing and mining accounted for only 13 per cent of exports at this time.2

However, with the ever-increasing economic wellbeing of Europe, and the growing

unpopularity of Imperial powers (not to mention the cost of maintaining colonial outposts),

the UK began to offload its colonies in quick succession.

Moreover, severe protective measures adopted by the European Economic

Community (EEC) in 1958 and the UK’s subsequent entry in 1973 impacted harshly on

Australia’s total exports3. These factors, along with improvements in worldwide production

technology and the ensuing introduction of synthetics, saw the demand for Australia’s

primary resources, particularly wool, decline significantly.

By all accounts, this period represented a timely juncture in Australia’s economic

history. The increasing economic development of East Asia was owed mostly to US

expansion into the region. Furthermore, because of Australia’s diminishing continental

markets, the opening up of more lucrative markets closer to home have, initially bid well

for this fledgling nation.

This expansion took the form of economic assistance through US sponsored

organizations such as the International Monetary Fund (IMF) and the World Bank (WB) in

an effort to rebuild a shattered Japanese economy following its demise in World War Two

(WWII). Thus, a US economy flushed with funds in its war chest following its success in

WWII, and a Japan eager for economic superiority in light of its military demise, oversaw

what was to be the expansive development of East and South East Asia.

2 Howlett, M., 1990, Simplifying Senior Economics, Bernard Publishing, Pt Norlunga, p. 213.3 Howlett, p. 214.

9

It has been perceived that, owing to its geographical proximity to Asia and the

makeup of its already developed economy, Australia was in a prime position to take

advantage of regional expansion. Asia’s development saw a considerable demand for

Australia’s primary resources, particularly fuel and mineral exports, which were only 7 per

cent of total export income in 1953 and accounted for over 47 per cent of export income by

1989.4 These figures are impressive and so is much of the corresponding literature on

Australia’s trade with the region. However, what these figures fail to indicate are the terms

under which this trade was conducted.

Certainly, with the benefit of hindsight, it is much easier to be critical of

government and business initiatives, though the call to change the general dynamic of

Australia’s economic development has been a long-standing one. No more had this been

vindicated than by Australia’s former Treasurer (and later Prime Minister) Paul Keating.

When, in May of 1986 he boldly stated that unless Australia underwent some fundamental

changes in its economic structure it was in danger of becoming a “banana republic.”5

This is a pivotal focus for the research conducted in this paper, for the initiatives in

the economic development of Australia’s regional trade were congruent with keeping

Australia as very much a price taker in international markets.6 Instead of burgeoning

industries being developed and markets being established or a variety of productive

capacities being encouraged, the export of raw as opposed to processed materials has seen

this price taker attitude remain up until very recent times.

Moreover, the relative ease with which Australia traded its raw resources with the

region did little to help its economic development and did little to make it a regional

4 Howlett, p. 213.5 Broomhill, R. The Banana Republic? Left Book Club Co-op, NSW, 1991, p. 1.6 In economic theory the term price taker refers to competitors who cannot control the price in the market place. For more on this see Fischer, S. & Dornbusch, R. Economics, International Student Edition, McGraw-Hill Book Co-Singapore, 1983, pp. 220-224.

10

competitor. As can be seen in figure 2, the spikes and troughs indicate the volatile nature of

Australia’s exports that have occurred outside the boom-bust cycles experienced by the

world’s major economies. This highlights the impacts of an ongoing price taker attitude as

the Australian economy rises and falls at the apparent whim of international market forces.

The evolving price taker attitude has its roots in the mid 1960’s when American

global expansion into the region under Pax Americana had done much to fuel the region’s

demand for Australia’s raw mineral exports. As a result there has been a continual fall in

Australia’s commodity prices ever since. By the mid 1970’s the resultant worldwide price

inflation had seen a fourfold increase in the Organisation of Petroleum Exporting Countries

(OPEC) oil prices.7 While this resulted in higher prices for Australia’s fuel and commodity

exports, the inflationary effects generated eventually slowed demand and ended in a rapid

fall in commodity prices by 1979. The economic shocks this rapid expansion had initially

generated saw the global downturn bottom by 1984 with commodity prices left standing on

increasingly shaky ground.

A prima facie example of this is Australia’s coal industry, which had ridden the

fluctuating commodity wave since its inception in 1960. Having been kick-started by the

7 Calleo, D., The Atlantic Alliance and the World Economy, in Beyond American Hegemony, New York, Basic Books, 1987, p 93.

Source: AusStats, International Accounts & Trade, YearBook 1999. p. 2.

Figure 2: Ratio of exports to GDP

11

Japanese steel industry, the OPEC oil crisis itself generated huge demand for low quality

thermal coal, as nations heavily reliant on oil imports were forced to switch to less costly

equivalents. This pushed the price of low quality coal to new levels due to its significantly

increased demand by the 1970’s.8 However, excess capacity eventually saw these huge

price increases for coal eroded as oversupply generated a decline in demand, resulting in

changing price expectations.

In a bullish international market, the net gains for a commodity-based economy

such as Australia’s can be very high, and conversely when the market falls the erosion of

these net gains can occur rapidly. This highlights the volatility of commodities on world

markets, indicating how susceptible Australian production has been to these ever-

fluctuating market forces. Commodity prices have not stabilised in recent years either,

warranting at least some moves away from, or an overall diversification of, the national

industrial base.

Furthermore, it would appear that the composition of Australia’s trade has changed

markedly within a few short decades. Having gone from a strong primary base in rural and

agricultural production in the 1930’s, to a net exporter of fuel and mineral resources by the

mid 1950’s. Nonetheless, while these exports may seem to be a diversification of overall

commodities traded, what they represented was more of a horizontal shift in the base of

primary production itself.

Horizontal shift refers to the side stepping or sideways movement, in this context,

of Australia’s primary industries. For a long time in both the private and particularly the

government sector there has been a great deal of celebration over the diversified content of

Australia’s exports. However, upon closer inspection this overall diversification is derived,

in fact, from a very narrow base of production in the primary sector.

8 Journal of Australian Political Economy, Number 44, December 1999, p. 92.

12

This overall bias towards primary industry had impacted quite dramatically on

other sectors of the Australian economy. The resulting marginalisation of secondary

industry had not seen manufacturing feature prominently in Australia’s export earnings

owing to a decided lack of comparative advantage, particularly with the region in terms of

the costs of labour and subsequently high production costs.

There have been recent improvements in this area due to the ongoing

implementation of tariff reductions (see table 5). However, this begs the question as to why

had Australia not taken advantage of its comparative advantage in many areas of

production sooner. The most significant reason for this may well have been the hollowing

out of manufacturing industry in Australia by external forces.9 This hollowing out process

is also referred to as the ‘Dutch Disease’, which was first coined after the discovery of

natural gas in the Netherlands.10 The discovery of these natural resources had artificially

increased the Dutch exchange rate, resulting in export industries being squeezed or

hollowed out which was followed by a decline in Dutch manufacturing industries.

One example of these external forces at work in an Australian context concerns the

vigorous pursuit by Japan of Australia’s raw materials, which were cheap by comparison to

those in other world markets. The aftermath of WWII had robbed the Japanese of the

mineral rich coal reserves in Manchuria and the burgeoning trade with the US went

asunder during the Suez Canal crisis of 1956. This had seen US coal shipments to Japan

stilted, resulting in the purchase of Australia’s cheaper coal, which fitted in with Japanese

plans to shop locally.11 Thus was hailed in the expansive development of raw material

9 Byrnes, M., Australia and the Asia Game, Allen and Unwin, NSW, 1994, pp. 50-51.10 Corden, W.M., ‘Booming Sector Dutch Disease Economics: A Survey’, Working Paper in Economics and Econometrics, No. 079, Research School of Social Sciences, ANU, November, 1982, p. 2.11 Byrnes, p. 68.

13

exports from Australia, which became a substitute for the possible development of more

lucrative manufacturing industries in this otherwise developed economy.

Many of the benefits of manufacturing are often derived by technological

innovation and changes in production and their associated techniques. These practises can

lead to the establishment of complimentary industries, not to mention the adding of

significant infrastructure and ongoing wealth and job creation within the domestic

economy.12

However, in light of this process of hollowing out, many of the above practices

were circumvented. This is because the short-term benefits of extracting and selling raw

materials in their cheapest form without significant, if any, value adding whatsoever were

not weighed up against the longer-term costs to local industry and the economy as a whole.

By longer-term costs the thesis is not simply referring to the way in which the economic or

financial gains are spent, but to the ‘equilibrium consequences’ occurring in other vital

sectors of the economy.13 This is an important distinction to make because as some

industries may decline in the face of new or significant growth industries others will

expand.14 Examples of this have occurred in Australia’s wool and agricultural industries

that declined as mining exports grew in the boom years of the 1960’s and 1970’s.

Moreover, the expansion of the services and financial industries in the 1990’s in the face of

a declining mining sector has seen a similar situation occur.

One means of measuring the longer-term costs of this shortsightedness is in GDP

growth trends. These measure an economy’s output over time, and can establish levels of

growth, particularly when measured next to regional economies with which trade has been

conducted over a comparable length of time. Indeed, by 1960 Australia was perhaps the

12 Byrnes, p. 68.13 Corden, p. 2.14 Corden, p. 2.

14

most developed regional economy in terms of its GDP when output was compared with the

relatively small size of its population. Meanwhile, many of the regional economies were

coming from an agrarian base, only beginning their entry into basic forms of

manufacturing such as textiles, footwear, and clothing industries. At this time, Australia

was already well advanced in more complex manufacturing techniques, however, the

exponential increase in the output of regional economies-particularly Japan, China, and

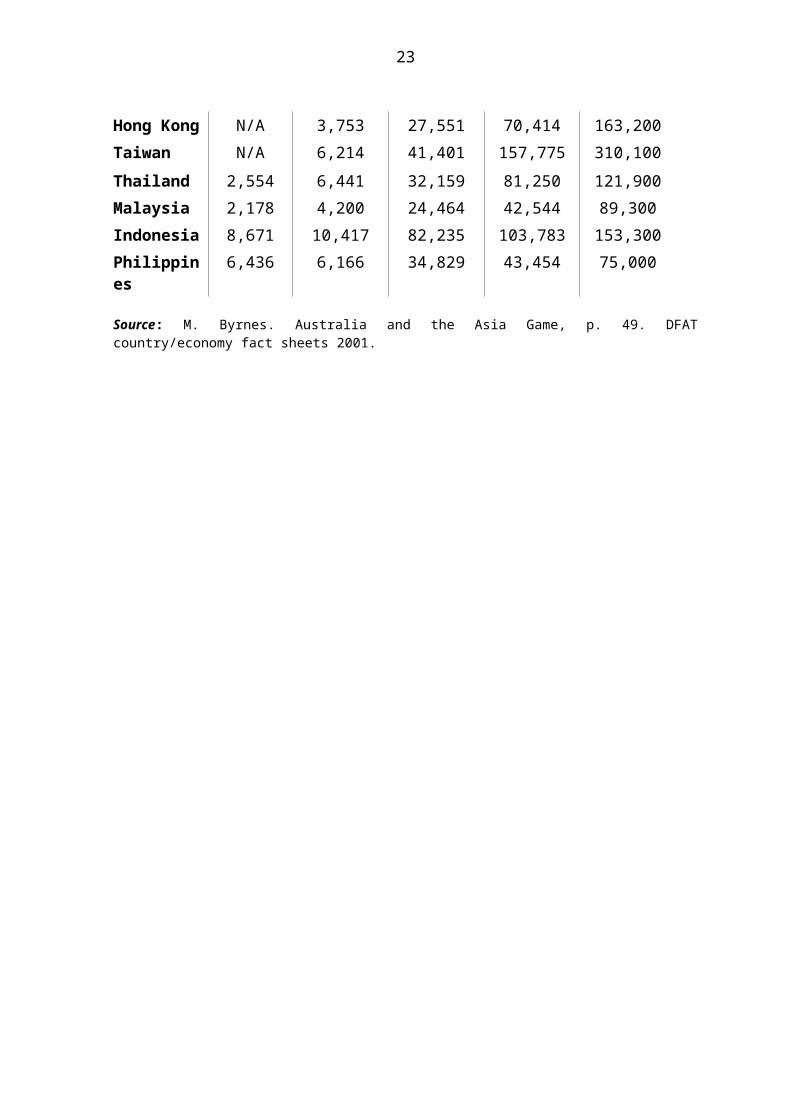

South Korea-very quickly accelerated beyond Australia’s output (Table 1).

Table 1 Gross Domestic Product, regional comparisons ($US billions).

Region 1960 1970 1980 1990 2000

Japan 44,439 203,301 1058,911 2964,055 4752,900China N/A 80,864 298,418 362,656 1099,800Australia 16,809 37,270 149,892 295,701 398,100South Korea N/A 11,744 62,627 239,773 457,000Singapore 0,707 1,870 11,947 35,430 91,000Hong Kong N/A 3,753 27,551 70,414 163,200Taiwan N/A 6,214 41,401 157,775 310,100

Thailand 2,554 6,441 32,159 81,250 121,900

Malaysia 2,178 4,200 24,464 42,544 89,300

Indonesia 8,671 10,417 82,235 103,783 153,300

Philippines 6,436 6,166 34,829 43,454 75,000

Source: M. Byrnes. Australia and the Asia Game, p. 49. DFAT country/economy fact sheets 2001.

15

Not only did the relationship with Japan incur this hollowing out process. To a

lesser extent, the relationship with the UK had a similar effect. In the 1940’s and 1950’s

Australia was said to have been “riding on the sheep’s back”, which is a euphemism for the

nation’s dependence on agricultural production. Again, this raw material export

represented a low value added product, as had later been the case with Japan in the export

of coal and later iron ore. Yet, this decline was not merely a symptom of Japan’s

expansion, so much as, colonial submission in the first instance under the banner of the

UK.

This is not to imply that Australia was merely an extractive colony as was Malaya

or Burma; clearly the penal colony gave way to free settler colonies and a considerable

degree of autonomy developed. However, what the argument suggests is that Australia’s

dependence on primary production, be it in the agricultural or mineral sector, resulted in

the stalling of manufacturing development, by curtailing investment in technological

innovation and change. Furthermore, this had come about, not as a deliberate attempt to

undermine these industries, but as a direct result of sectoral disequilibrium, which saw

mining overshadow the development of these other sectors in Australia’s economy.

It has often been suggested that Australia’s manufacturing industry was in better

condition than Japan’s when the Japanese started to nurture their interests in Australia’s

primary resources.15 This was owed largely to the fact that Australia was somewhat

insulated from Asia by virtue of its preferential trading relationship with the UK at the

time. By all appearances, this relationship gave the impression of Australia as largely self

sufficient in terms of its manufacturing and industrial capacities, as a result of this

preferential trade arrangement.16

15 Byrnes, p. 68.16 Byrnes, p. 68.

16

This had seen the development of manufacturing in Australia propelled along by

the exigencies of WWII, which had nurtured a thriving aircraft and automobile

manufacturing industry.17 The benefits of this had seen the establishment of

complementary industries in Australia supporting larger manufacturers. There was also a

burgeoning steel industry, of which the provision for Australia’s extensive coal reserves to

fuel the steel furnaces had established a potentially readymade domestic market.

However, the end of the war had seen many manufacturing industries fall into a

general state of decline. Instead of taking advantage of already existing technology and

infrastructure, and possibly developing them for domestic production and export, many of

these industries, particularly the aircraft industry, had practically collapsed by the end of

the 1960’s.18 This saw an extensive brain drain as local expertise either faded into oblivion

or went overseas to countries such as Canada or Brazil, whose governments supported the

development of domestic aircraft industries. Subsequently these countries are now ranked

among the biggest aircraft manufacturers in the world.19

This decline in manufacturing brought about from sectoral disequilibrium was,

perhaps largely assisted by Australia’s insular inward-looking industrial policies inherited

from the UK, where a government culture of “hands-off” relations with industry had seen

manufacturing develop along more pragmatic lines. Government support for potential

leading industries was decidedly lacking, and left manufacturing to fend largely for itself,

in a market dominated by, and largely catering to primary industry needs.20 The impacts of

maintaining these vibrant and innovative industries meant that Australia would have to

unleash itself onto the open trading system, which it was not inclined to do.

17 Aviation red tape just plane crazy, The Australian, Friday, 19 Oct 2001, p. 26.18 Aviation red tape, p. 26.19 Aviation red tape, p. 26.20 Journal of Australian Political Economy. Special Issue, Australia Reconstructed: Ten Years On, No. 39, June, 1997, pp. 17-18.

17

The establishment of an open trading system was a deliberate attempt by GATT to

reverse the protectionist stance derived during the inter–war years.21 In this way, it was

assumed that interdependence through trade would establish more harmonious relations

between states. Australia’s opposition to this stance was reflected in the high levels of tariff

protection it maintained in response to GATT, reflecting a need for insularity and certainty

in an increasingly destabilised world, or for that matter, the region.

Australia’s decline in manufacturing also coincided with Japan’s dominance

as Australia’s number one export market by the early 1970s. The UK was clearly

Australia’s key export market in 1960, and within a decade, Japan had overridden

the UK as the principal market for Australia’s exports (Table 2).

Table 2 Australian exports and imports ($Am)

1950-51 1960-61 1970-71 1980-81 1990-91 2000-01ExportsJapan 123.1 323.0 1,190.9 5,227.6 15,894.0 23,502.6UK 641.2 400.1 493.8 715.3 1,963.0 4,645.6US 297.7 144.9 519.4 2,147.0 6,136.0 11,675.3

ImportsJapan 31.2 130.9 573.6 3,629.3 9,526.0 15,370.6UK 713.8 681.1 887.2 1,584.5 3,532.0 6,321.3US 121.8 434.1 1,041.7 4,169.0 12,586.0 22,355.4

Source: M. Byrnes, Australia and the Asia Game, p. 51 & DFAT country/economy fact sheets 2001.

By 1980 this export share increased to a ratio of 7 to 1, although the Japanese

economy has been in a deep and prolonged recession since the early 1990’s. Moreover, its

share of Australia’s exports has still been a staggering ratio of 5 to 1, when compared to

the substantially reduced export share of the UK at this time.

21 Economic Papers, Economic Society of Australia, Vol 14, No. 1, March 1995, p. 1.

18

Therefore, it can be said that Australia’s exports to the UK had rapidly diminished

as international markets reprioritised their trading needs. This had seen Japan focus on

Australia’s extensive mineral reserves for its own, and the region’s, continued industrial

expansion. These events occurred at the expense of Australia’s manufacturing industries,

which continued to decline against a backdrop of easier profits gained in the resources

sector.

19

CHAPTER 2

Liberalisation and the Consequences of International Exposure

Australia has continued to reap the economic benefits of extracting its mineral

resources and exporting much of the raw materials to long established markets. While this

bade well for commodity industries undergoing rapid periods of growth owed by and large

to Japanese industrial requirements, when commodity prices began to fall in the mid

1970’s it distorted problems in Australia’s manufacturing industries. This made Australia’s

long-term inability to be an exporter of manufactured goods all the more obvious by

highlighting the distortions between local industry and the changing requirements of

international capital.22 Australia’s place in the international capital market was undermined

by its dependence on commodities for economic development. Initially this dependence

was underpinned by Australia’s relationship with the UK as a supplier of agricultural

produce, and then it switched over to Japan as a major supplier of mineral resources.

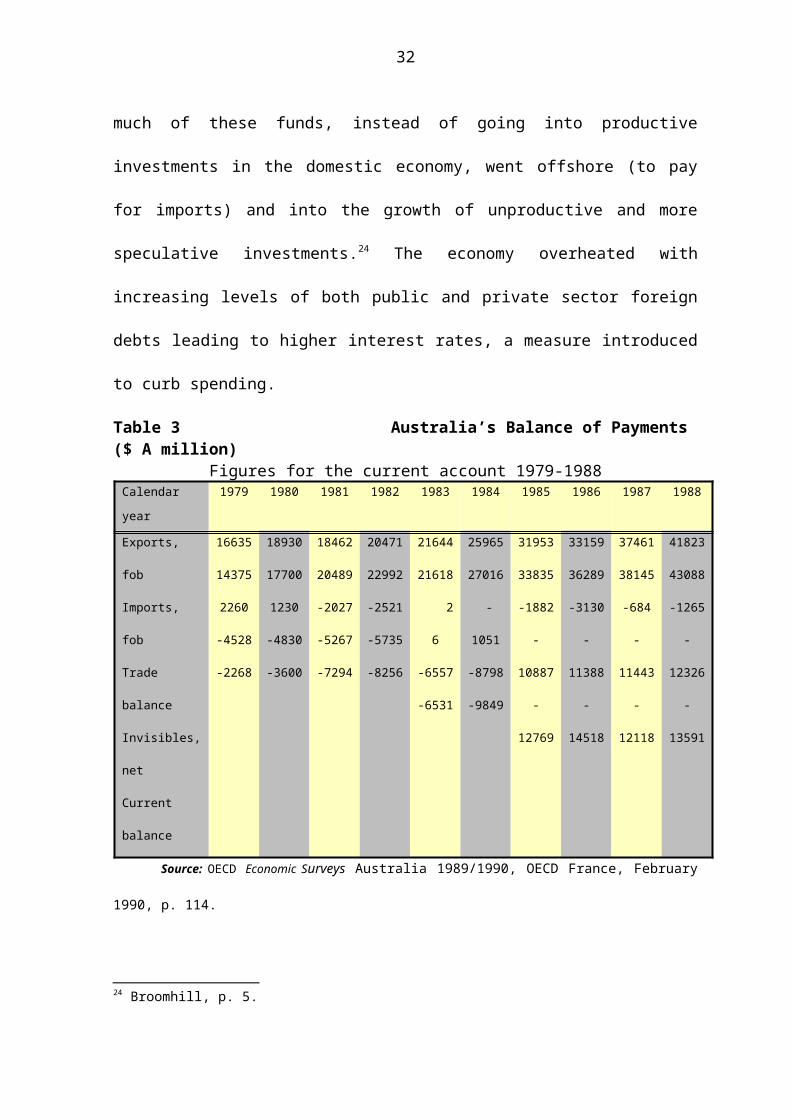

These factors, combined with the global downturn of the mid 1970’s, saw

Australia’s declining terms of trade and a rising current account deficit resulting in

significant balance of payment problems for the economy (Table 3). International money

markets responded to these concerns by displaying a loss of confidence in the Australian

economy, which were seen as being racked by ever increasing levels of foreign debt.23

All this came on top of substantial economic reform instigated by the Labor

government of the day, which began to open the Australian economy to the full force of

international competition in 1983. This liberalisation of the economy began with the

floating of the Australian dollar on the international market, and a wide range of

microeconomic reforms, particularly in the banking and financial sectors of the economy.

22 Broomhill, p. 2.23 Broomhill, p. 3.

20

Practices in these sectors were considered outmoded, inefficient and very much anti-

competitive.

Thus, liberalisation saw a rapid influx of foreign capital into Australia, making

access to funds, and therefore borrowing’s, much easier. The problem, of course, was that

much of these funds, instead of going into productive investments in the domestic

economy, went offshore (to pay for imports) and into the growth of unproductive and more

speculative investments.24 The economy overheated with increasing levels of both public

and private sector foreign debts leading to higher interest rates, a measure introduced to

curb spending.

Table 3 Australia’s Balance of Payments ($ A million)Figures for the current account 1979-1988

Calendar year 1979 1980 1981 1982 1983 1984 1985 1986 1987 1988

Exports, fob

Imports, fob

Trade balance

Invisibles, net

Current balance

16635

14375

2260

-4528

-2268

18930

17700

1230

-4830

-3600

18462

20489

-2027

-5267

-7294

20471

22992

-2521

-5735

-8256

21644

21618

26

-6557

-6531

25965

27016

-1051

-8798

-9849

31953

33835

-1882

-10887

-12769

33159

36289

-3130

-11388

-14518

37461

38145

-684

-11443

-12118

41823

43088

-1265

-12326

-13591

Source: OECD Economic Surveys Australia 1989/1990, OECD France, February 1990, p. 114.

Moreover, it was the inefficient use of these borrowings and a seemingly scant

regard for Australia’s economic development that saw Paul Keating retort with scathing

sentiments in May of 1986. He said that unless Australia underwent some fundamental

changes, and “we started living within our means,” we were in danger of becoming a third

world country, or as the popularised phrase has been quoted, a “banana republic.”

Furthermore, Keating’s bombastic comments were directed at Australia’s

entrepreneurs and corporations who failed to capitalise on the increased availability of

capital, which by all accounts was seen as a means for increasing domestic investment, 24 Broomhill, p. 5.

21

furthering capital accumulation, and enhancing national wealth, and savings. It was not

intended as a free for all for corporate raiders such as Alan Bond, nor was it intended for

gambling on speculative investments, or investments offshore, which did little if anything

to enhance the national economy.

Having said this, Paul Keating’s entreaty had not taken into account that the

economy’s problems were essentially structural in origin, rather than the inability of the

polity to live within its means. Essentially, this is because in a country like Australia,

exports are primarily commodities and imports are mostly manufactured goods. The large

divergence in exports and imports results in greater terms of trade volatility than in

countries where exports and imports are similar.25 The global downturn in commodities

had peaked in Australia by 1986, with the current account deficit at $A3.13 billion, which

was down from its previous peak in 1982 of $A2.52 billion.26 Because of this, imports of

elaborately transformed manufactures (ETMs) and other manufactured goods required in

the restructuring of Australia’s economy left a significant shortfall. This occurred between

the prices generated from these falling commodity exports and the costs of importing

ETMs, resulting in the ever-escalating current account deficit. Evidence of this is clearly

indicated in OECD economic surveys, which state;

“… Slower aggregate labour productivity growth may have reflected the combined effect of a decline in real labour costs and a rise in the cost of capital as real interest rates rose…This factor may have lowered labour productivity growth by half of a percentage point per year (by one-third) during the period 1980 to 1988.”27

The tailing off of the overheated Australian economy came from the recessionary

impacts of this flurry of capital expenditure between 1983 and 1986, and culminated in

“the recession we had to have” (Paul Keating’s other famous comment from the period).

25 OECD Economic Surveys Australia 1989/1990, OECD France, February 1990, p. 46.26 OECD Australia, 1989/1990, p. 114.27 OECD Australia, 1989/1990, p. 55.

22

While this subsequent recession affected the domestic economy as monetary policy was

tightened, it had little impact on inward-bound foreign investment, which continued to

thrive with access to finance available from abroad.

The extent of this foreign investment is an important consideration when talking

about Australia’s economic development. Inflows of FDI after WWII impacted

significantly on patterns of ownership and the overall structure of firms themselves, which

in turn had a severe impact on Australia’s economic development. In 2001 foreign

investors owned more than one-quarter of the equity, and a controlling representation of

some 15 per cent in Australian firms. However, the level of foreign ownership has

remained steady at 28 per cent over the last three years.28

Australia’s federal government under its arm of the Foreign Investment Review

Board (FIRB) established in 1976 had regulated FDI in Australia. One substantial method

of control was the requirement for at least 50 per cent equity participation by Australian

firms in any national FDI. However, perhaps owing to large infrastructural costs in the

mining sector, this requirement was waived if the investment was not deemed detrimental

to national interests.29 Therefore, Australia had simply to reap the harvest while foreign

investors had to worry about the more complicated and costly tasks of infrastructural

expenditure and the conversion of primary goods into finished products.

In this way, Australia has become dependent on foreign capital for

manufacturing investment. This had hindered Australia’s economic

development by retarding R&D in crucial areas of production that may

otherwise have taken place, if value adding were high on the agenda for

the parent companies. Essentially, this strategy had the appearance of

28 Henderson, I. Foreign investors cooling their heels, The Australian, Monday, January 14, 2002, p. 5.29 Howlett, pp. 251-252.

23

an act of faith in the ability of foreign firms to deliver financial rewards

to successive Australian governments, rather than a seasoned plan for

Australia’s future economic development. This is particularly so in terms

of research conducted on the level of technological input for both

Australian and Foreign firms in 1993-94. It was established, to some

extent, that there was more interest by Australian firms in exports and R

& D expenditures than there was by foreign owned firms (Table 4).

Table 4 Foreign and Australian firms/manufacturing, by ownership and technology intensity. Sales, exports & R & D 1993 –94.

R & DIntensity

ForeignShare of Sales

Exports/Sales(%)

R & D/Sales(%)

Average Sales($Am)

Australia Foreign Australia Foreign Australia Foreign

High53.0 24.4 11.6 6.2 4.9 8.9 87.8

MediumHigh 65.4 12.6 12.7 2.5 1.6 7.4 119.3MediumLow 26.3 26.0 20.8 1.7 0.9 7.4 34.0

Low 25.6 16.4 14.0 1.0 0.6 12.0 69.6TotalManufac 36.7 18.7 14.3 1.6 1.4

Source: Sheehan, & Grewal., The Global Knowledge Economy & Regional Concentration of Manufacturing in Australia, CCSES, Victorian University of Technology, Working Paper No. 19. July 2000, p. 11.

The propensity for Australia’s firms to be involved in research was more so, in high

technology and R & D intensity areas. Here Australia’s share of exports/sales was more

than double that of foreign firms, while R & D commitment itself was also somewhat

larger. Average sales for these foreign firms were significantly greater than Australian

firms, and it is quite clear that much of the production was geared for the domestic

Australian market. As such this was seen to warrant little by way of R & D input. Judging

by the very high level of foreign share of sales (being well over fifty percent in the high

24

and medium high technology categories), this could significantly undermine the much

smaller Australian firms. This could affect the demands for production and ongoing

commitments to R & D itself.

Regardless of the arguments for and against foreign investment in Australia, it is

quite clear from these figures that significant levels of foreign ownership in Australian

firms invariably translates into significant influence by the parent company over its local

operations. Nowhere is this more clearly observed than in Australia’s automotive industry,

where handouts by the federal government in the form of industry grants do little to make

the industry more globally efficient or cost competitive.

Moreover, the pervasive threat by the foreign parent companies to bring about the

loss of thousands of jobs in the industry if assistance is not received has seen the doubling

of government handouts to the auto industry in the last two years alone. This has resulted

in a 2 billion-dollar industry pool funded directly by a freeze on car tariffs at 10 per cent

from 2000 to 2005.30

Conversely, these subsidies have won the parent a place in global trade and have

secured jobs in Australia. Yet, what will the long-term costs be if these industries cannot

remain competitive without industry assistance, while workers are not prepared for smarter

and more competitive jobs and industries themselves?

Mitsubishi in Adelaide has stated that it could only guarantee its plants remaining

open for production until 2004 - 5 provided they were profitable.31 This profitability comes

at the expense of higher import costs for motor vehicles, of which Mitsubishi itself is an

importer of small and medium-sized four wheel drives. This profitability also comes at the

expense of continued capital outflow to the parent company in the form of profits and

30 Marris, S., Handouts to car industry near double in two years. The Australian, Friday, December 21, 2001, p 2.31 Howard must just say no to Mitsubishi, Editorial et.al, The Australian, Thurs, December 13, 2001, p. 10.

25

dividends, resulting in the retarding of domestic industry, which maintains these inefficient

and anti-competitive practises.

Moreover, owing to the considerable distance to markets, and the overall size of the

economy, the fact remains that Australian auto firms are comparatively small by

international standards. For these reasons firms in Australia tend to be seen, and function

as branch offices with little scope, need or demand for R&D. 32 Clearly, this has proven to

be a hindrance to Australia’s economic development. While such attitudes may well be the

preserve of the foreign parent company, it is an attitude that can ill afford to prevail among

domestic industry elites and the federal government. Else, regional trade may not be in a

position to help drive Australia’s economic development.

It has long been the case that Australia has had an enormous comparative advantage

in terms of its natural resources, be they agricultural or mineral. While Asia conceded the

advantage of engagement with Australia to fuel its regional expansion in the 1960’s, this

comparative advantage went very much in reverse in the face of Asia’s subsequent cheap

manufacturing imports. Australia’s inability to compete with this flood of manufactured

goods saw the implementation of tariffs and other extensive barriers to protect home

industries.33 These tariffs, along with substantial levels of FDI, have impeded economic

development in Australia and threaten the development of future leading industries.

Moreover, these imperatives highlighted conflicting notions within the Australian

government bureaucracy, with the old guard clinging onto Cold War notions that the

region still posed a considerable threat to Australia. Ever since 1938, Australia had banned

the exports of iron ore, fearing these products may well come back as planes bombs and

32Sheehan, P. & Grewal., B. The Global Knowledge Economy and Regional Concentration of Manufacturing in Australia. Centre for Strategic Economic Studies (CCSES), Victorian University of Technology, Working Paper No. 19. July 2000. pp. 9-10.33 Switzer, T. Economic Nationalism: it’s Back to the Future, The Institute of Public Affairs Review, Vol 53, No 2, June 2001, p 7.

26

torpedoes.34 Indeed, with Japan importing iron ore from China and captured mines in

Manchuria, this fear may well have been founded at the time. This seeming foresight came

to pass after the shelling by the Japanese of Darwin, as they advanced to dominate the

region during WWII.

This threat was a consequence of strategic rather than economic considerations,

though the latter had been the original basis for the bans. In 1938 Australian Prime

Minister J.A. Lyons told the Japanese Consul-General that the embargo was not aimed at

them, but was in the interests of conserving Australia’s (then much smaller) reserves of

iron ore for domestic blast furnaces.35 With Japan’s production of iron ore hitting 20

million tonnes by 1960 and its appetite for the ore set to double within the next few years,

Australia eventually lifted its ban in December 1960.36 Perhaps the embargo would have

remained, if not for the fact, that between 1940 and 1959 Australia’s known reserves of

iron ore increased from around 260 million tons to some 370 million tons.37 The eventual

lifting of the ban may have been considered a step in the right direction for Australia’s

regional trade. Though the continuation of the White Australia Policy in the 1960’s was

still an ongoing reminder of apprehensions about an unknown quantity in the form of

Australia’s near neighbours, and unfounded fears of the regions links to communism.

However, these ongoing fears were encapsulated in the form of import protection

from the region’s cheaper imports, and did not come into play when selling Australia’s

exports to Asia. 38 The economic threat only came once exports had gone full circle to

become cheap imports, which threatened to undermine domestic manufacturing industries,

the assumed impact of which was to harm national wealth and jobs.

34 Byrnes. p. 89.35 Blainey, G., ‘The Cargo Cult in Mineral Policy’, Economic Record, Vol. 44, No. 108, 1968, p. 471.36 Byrnes, p. 89.37 Blainey, pp. 476-477.38 Switzer, p. 7.

27

It is a prevailing fallacy, which has influenced both public and private debate for

many decades, and does little except harm economic relations between Australia and the

region, as many of these issues are reported widely in regional media. The fact remains that

Hollowing Out and the Dutch Disease (in particular) offer a more accepted view of factors

which influence the B of P and structural change. Such influences are derived more from

the rapid growth in mineral exports than they are, from even very large tariff changes.39

This is primarily because the introduction of a tariff reduces the quantity of imports

purchased, moving the B of P into surplus, which then places downward pressure on the

price of traded goods. In other words the manufacturing sector, which must compete

strongly with imports, is forced into an equivalent position of a devaluation of the

exchange rate to restore equilibrium as a result the sector itself is not affected by the

changes. However, what is affected by the tariff change is income distribution, which is

effectively redistributed from the export sector towards the government sector receiving

the revenue from the tariff.

There is no better case in point for highlighting the negative effects on Australia’s

productivity than tariffs established in TCF Industries, which suffered the greatest impacts

from large tariff changes. Between 1968 and 1993 increasing tariffs were implemented,

which peaked in 1991. These gave TCF‘s the highest level of protection over all

manufactures in Australia; “… the levels in 1991/92 were 46% for textiles, 84% for

clothing and 91% for footwear, compared to 13% for all manufacturing.”40 While TCF

assistance has now almost halved from what it was in 1991/92, it is still comparatively

39 Gregory, R. G., ‘Some implications of the growth of the minerals sector’, Australian Journal of Agricultural Economics, 20(2), 1976, pp. 71-73.40 Economic Papers, Economic Society of Australia, Vol 20, No. 2, June 2001, p 2.

28

high when compared with all manufacturing assistance, which is lower than 5% in 2001

(Table 5).41

Table 5 TCF & Manufacturing levels of assistance, per industry, (in percent). Effective Rates of Assistance (ERA).

1960 1970 1980 1990 2000-01

All Manufactures N/A 34 24 13 5.0

Textiles N/A 50 55 46 17Clothing N/A 96 135 84 25Footwear N/A 107 161 91 25Motor Vehicles & Parts N/A 50 96 60 19

Source: Australian Parliamentary Library Research Paper 71999-2000.

These ongoing tariffs are the result of government intervention, which has

protected inefficient producers in changing international market conditions, leaving

domestic industry unresponsive to the changing climate. The resultant effects insulated the

economy in such a way that it:

“… Inhibited adaptation to changing circumstances arising from rapid advances in technology and increased globalisation. For example, government protection policy encouraged the Australian manufacturers to focus on import replacement, leaving a continued reliance on agriculture and minerals for export earnings.”42

In other words, Australia simply developed an over-reliance on commodity exports

and used any surpluses to acquire new technology from abroad rather than develop

technology locally to meet Australia’s own industrial requirements.

This seeming indolence or complacency shows a considerable weakness in

Australia’s fundamental policy initiatives. Instead of selling raw materials in the form of

coal and iron ore to Asia, Australia might have been better off building up competitiveness

in its domestic industries. In hindsight, this may have saved Australia from its current level

41 OECD Economic Surveys Australia, No. 14. August 2001, p. 83.42 The Australian Economic Review, Vol. 34, No. 2, June 2001, p. 126.

29

of exclusion, which the government seems to be facing, particularly in its trade

negotiations with ASEAN and other regional forums.

Moreover, Australia with a considerably more diversified economy, could have

enhanced its regional bargaining power and seen a much more fruitful and dynamic

relationship with its regional trading partners. Certainly, (as Blainey postulates) if

Australian governments had held the reigns and taken control (of the core) an earlier

development of mining industries may have heralded in better deals with the Japanese. The

likelihood of greater earnings in the 1950’s, an era of ‘brooding pessimism’ over

Australia’s B of P problems may have lifted economic attitudes and policies as a stimulus

to growth.43

Therefore, Australia’s inability to be more competitive with the region highlights

more a sense of insularity from externalities developed from its relationship with the UK.

This translates into apprehension of the Asian way of doing business, and a desire for

commercial linkages with those that have similar cultural affiliations such as the EU and

the US. Though Australia may be left wanting if it assumes such preferences will create the

pretence of a more even playing field. The imbalance or unevenness in the so-called

playing field is reflected in Australia’s technology needs, which are increasingly met

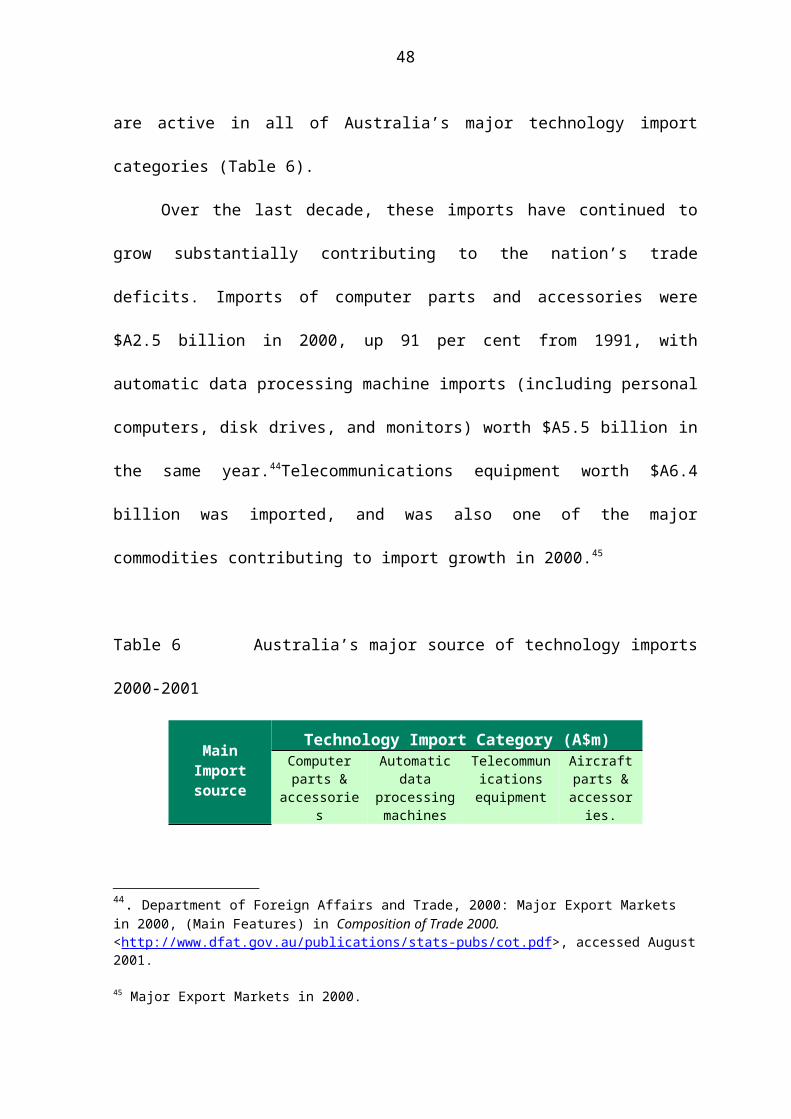

through imports from the US that are active in all of Australia’s major technology import

categories (Table 6).

Over the last decade, these imports have continued to grow substantially

contributing to the nation’s trade deficits. Imports of computer parts and accessories were

$A2.5 billion in 2000, up 91 per cent from 1991, with automatic data processing machine

imports (including personal computers, disk drives, and monitors) worth $A5.5 billion in

43 Blainey, p. 476.

30

the same year.44Telecommunications equipment worth $A6.4 billion was imported, and

was also one of the major commodities contributing to import growth in 2000.45

Table 6 Australia’s major source of technology imports 2000-2001

MainImport source

Technology Import Category (A$m)Computer

parts & accessories

Automatic data

processing machines

Telecommunications

equipment

Aircraft parts &

accessories.

USJapanChinaUKOther

715 429 169 544 636

901 635 359 3,345

1,400 622 554 3,473

1,700

687 513

Total 2,493 5,240 6,049 2,900 Source: DFAT country/economy fact sheets 2001 & Composition of trade 2000-01.

The $A17 billion combined for these technology imports represents some 15.6 per

cent of the commodity share of total Australian imports that year.46 Australia’s major

source of technology imports and the major exports highlight the differences in the types of

trade Australia is engaged in (Table 7). This divergence in trade illustrates the

predominantly primary base for exports and the overall dependence of the Australian

economy on technology imports to meet domestic industry needs.

Table 7 Major Australian exports and imports, 2000-2001 (A$m).

44. Department of Foreign Affairs and Trade, 2000: Major Export Markets in 2000, (Main Features) in Composition of Trade 2000. <h ttp://www.dfat.gov.au/publications/stats-pubs/cot.pdf >, accessed August 2001.

45 Major Export Markets in 2000.46 Department of Foreign Affairs and Trade, Feature article: Major commodities traded by Australia, 1991 to 2000, http//www.dfat.gov.au accessed July 2001.

31

Exports Imports

Coal

Crude petroleum

Non-monetary gold

Iron ore

Aluminium

10,818.5

7,607.1

5,110.2

4,911.2

4,734.4

Passenger motor vehicles

Crude petroleum

Telecommunications

Computers

Medicaments (inc. veterinary)

8,578.9

8,205.8

6,049.1

5,240.1

3,508.8

TOTAL 33,181.5 TOTAL 31,582.7

Source: DFAT country/economy fact sheets-Australia 2001.

These examples set the stage for the way in which the international community

views Australia today. Consequently, Australia continues to be seen as a bulk producer of

commodities, foreshadowing a lack of demand for full-scale manufacturing, let alone the

development of technology related industries here. Such a narrow export base may well be

viewed with scepticism by economies endowed with a greater diversification of national

production. This is no more so than in the telecommunications, computer and commercial

aircraft industries, which require a higher level of local expertise and ongoing technical

innovation and change to manufacture.

Current Australian government published trade statistics indicate little more than a

hint of any such marginalisation of secondary industry. Accordingly it is shown that

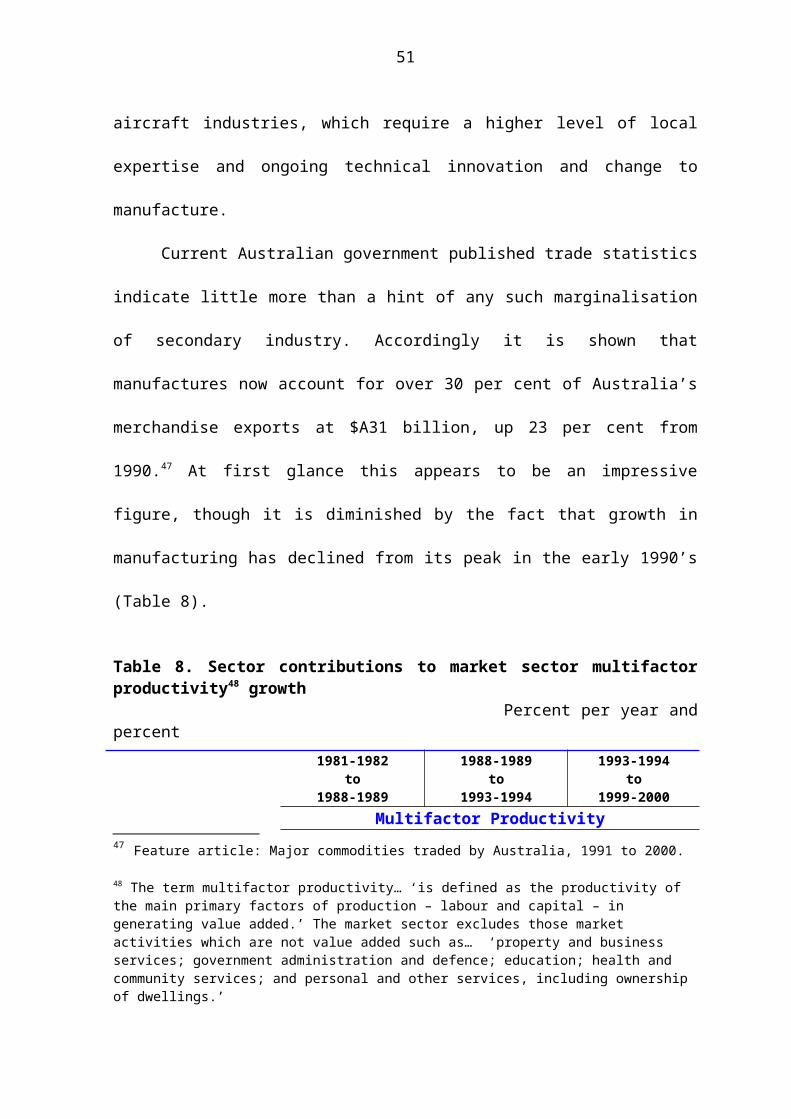

manufactures now account for over 30 per cent of Australia’s merchandise exports at $A31

billion, up 23 per cent from 1990.47 At first glance this appears to be an impressive figure,

though it is diminished by the fact that growth in manufacturing has declined from its peak

in the early 1990’s (Table 8).

Table 8. Sector contributions to market sector multifactor productivity48 growth47 Feature article: Major commodities traded by Australia, 1991 to 2000.

48 The term multifactor productivity… ‘is defined as the productivity of the main primary factors of production – labour and capital – in generating value added.’ The market sector excludes those market

32

Percent per year and percent 1981-1982

to1988-1989

1988-1989to

1993-1994

1993-1994to

1999-2000

Multifactor Productivity

Growth Contribution Growth Contribution Growth Contribution

Agriculture 1.1 10.7 4.3 25.8 2.5 9.0 Mining 3.9 30.9 1.9 13.7 0.8 3.5Manufacturing 1.6 78.2 1.8 53.9 0.5 7.0Electricity, gas and water 3.0 16.4 4.0 16.4 1.0 2.3Construction -0.8 -13.5 -0.4 -4.2 1.3 7.2Wholesale trade -0.9 -15.5 -2.1 -23.1 5.6 30.1Retail trade -0.7 -11.3 0.5 5.3 0.9 5.2Accommodation, cafes,And restaurants -2.7 -16.5

-2.0 -8.0 0.5 1.0

Transport and storage 1.0 16.1 0.6 6.9 2.1 12.8Communication 4.1 14.0 6.3 19.4 3.3 7.8Finance and insurance 0.2 2.9 0.0 -0.3 3.7 21.9Cultural and recreational services -2.6 -12.4 -1.7 -5.9 -4.1 -8.0

Market sector 0.6 100.0 0.6 100.0 1.7 100.0This is in part due to the prosperity of regional economies engaged in the

Competitive pressures from the liberalisation of manufacturing imports had initially

seen improvements in the sector. Although secondary industry exports have contributed to

Australia’s trade deficits in the last decade, while “… many of the positive effects of earlier

trade liberalisation on productivity growth had run their course.” 49 Astonishingly the

mainstay of Australia’s initial exporting foray into the region via the mining sector is now

one of the poorest performers. This highlights the ineffectiveness of raw resource

extraction and the decided lack of value adding associated with these industries.

activities which are not value added such as… ‘property and business services; government administration and defence; education; health and community services; and personal and other services, including ownership of dwellings.’ 49 OECD Economic Surveys, No. 14, August 2001, pp. 82-83.

Source: OECD Economic Surveys, Australia, August 2001, p. 82.

33

This is in part due to the prosperity of regional economies engaged in the

manufacture of semi conductors and other components for technology related industries,

which no longer use coal in the manufacturing process. Conversely service industries such

as those in finance and insurance, transportation and storage, wholesale trade and

communications are the new engines of productivity growth in the Australian economy

(Table 8).

When compared with other sectors of the Australian economy manufacturing,

mining and agriculture have come down from, what were very high levels of productivity

growth. Manufacturing itself now contributes, only about 7 percent to productivity growth,

down from previous high levels of 54 and 78 percent respectively. Yet, what is not overly

apparent is the extent to which manufacturing contributes to R & D in Australia.

Manufacturing industry contributions have a direct spin-off to other sectors within the

Australian economy. This contributes a great deal indirectly to the overall multifactor

productivity gains in these new growth sectors (Table 9).

Table 9 Australia’s R & D expenditures x industry, 1996-97.

Industry Expenditure($A millions)

Percentage of Total

MiningManufacturingWholesale & retailFinance & insuranceProperty, business servicesScientific researchOther

546243420194514152183

13.259.04.92.312.53.74.4

TOTAL ALL INDUSTRIES 4124 100.0Source: Journal of Australian Political Economy, No. 45, June 2000, p. 23.

Moreover, although R & D expenditure in manufacturing contributes positively to

the development of other industries in the Australian economy, the fact remains that

34

Australia is still viewed as a bulk producer of commodities. Previously high levels of FDI

and ownership in Australian equity and the decided lack of R & D input by these same

firms, is countenanced by the relatively small R & D input of Australian firms. Though,

this is not enough to counter-balance negative sentiments about Australia’s global

economic position.

Clearly, this is evident in Australia’s dollar value on overseas markets where the

currency is considered greatly under valued, falling as low as $US 0.49 cents in recent

months. The consensus of Australia as a commodity-based economy is reflected in this low

price and could see it fall even further.50 The need to meet the challenges of moving

Australia’s industries into more technology related areas echoes Paul Keating’s call that

the nation may very well succumb to the vicissitudes of a banana republic if it fails to

advance.

While Keating’s concerns led to structural reform in Australia’s industries, this had

to some extent seen education put on the backburner. Moreover, this had been the case ever

since Barry Jones was minister for Science and Technology in the mid 1980’s, and now

more recently, as the Knowledge nation Taskforce Chair in 2001. Jones continues to

stipulate the importance of gearing the nation towards more value added, and innovative

industries, of which education is very much the precursor.51 While Keating’s statement had

become a central issue in political and economic debate of the times, Jones’s call to arms

was considered more academic than an immediate requirement.

Nonetheless, one of the main items on the agenda for Australia’s recently held

federal election, which coincidentally the opposition party had pinned its election hopes

50 Australian Broadcasting Commission, 2001, Cortis, K. Goldman-Sachs Asia. Interview, Compare Tony Jones, ABC’s Lateline, <http://www.abc.net.au/lateline/s323755.htm>, accessed September 2001.

51 National Australian Labor Party, Home Page, Barry Jones – Launch of the report of the ‘Knowledge Nation’ taskforce, < http: www.alp.org.au/kn/kn_report_ 020701.html> accessed July 2001.

35

upon, was “Knowledge Nation”. Alternatively, to use the incumbent government’s terms

of reference this also became known as “Backing Australia’s Ability”, which was launched

in January 2001.52 The urgency with which both major Australian political parties

addressed this agenda and labelled it their own initiative highlights the necessity for such a

strategy and its implementation.

Moreover, the main agenda it underscored was the need for the reallocation of

resources to meet changing national interests, which among other needs, included

encouraging educational investment in information technology and associated industries.

With growth in these imports significantly outpacing those of Australia’s major exports in

recent years, enhancement of national wealth and job creation has proven a considerable

incentive for advocating this investment strategy, albeit better later than never. As an

election promise, such a proposal is commendable, though it may be difficult to rise above

the rhetoric and achieve any noteworthy outcome.

Barry Jones, in his role as Science and Technology minister some 15 years ago,

insisted on the need for such a program; however 15 years on, his fears have not been

allayed. This is primarily because federal politics in Australia has a tendency towards

pragmatism rather than vision. Government policies that have no immediate impact

therefore go largely unnoticed by the Australian public.

Allbeit the case, Australia’s dilemma of inefficient, uncompetitive industries,

overall market decline in manufacturing as a share of GDP, and increasing levels of

technology imports, attests to the requirements established by Barry Jones and others that

the nation must change its emphasis to enhance Australia’s economic development. This

52 OECD Economic Surveys, No. 14, August 2001, p. 184.

36

view is further reinforced by OECD statistics, which show Australia’s R & D to GDP ratio

at 1.5 per cent, having slipped significantly below the OECD average of 2.2 per cent.53

Australia’s historical origins and past relationships have shaped and moulded the

economy into its current position. For many commentators it was Keating’s influence over

the economy as Federal Treasurer in 1983 and the subsequent opening up of the economy

to international competition that heralded in the watershed years. These years had seen

Australia basking in the success of its resources boom with Asia until the price, food, and

fuel shocks of the mid 1970’s. As a consequence of this, changes were needed to revamp

the nation’s structural malaise, which had exposed a weak manufacturing sector.

Yet, while Australia’s problems were inherently structural they were also

institutional in origin, with the weaknesses in the manufacturing sector resulting from a

poorly developed entrepreneurial class. In Australia, the dominant capitalist class had

always existed more or less in the shape of those who owned the primary resources, rather

than as an indigenous crop of local capitalists who were manufacturers.54 This has

influenced the extent to which Australian industry has been involved in R & D and the

ongoing level of participation in technical innovation and change.

This presents significant ramifications for regional trade, with which Australia must

compete in order to extend its global reach. If Australia is to advance within regional

trading arrangements and fortify complementarity within these groups, it must address

these structural, and in particular the institutional problems, or else it may well see itself

largely excluded from inter-regional trade.

Therefore, the outcomes of Australia’s early trade relationships have consequences,

not just affecting past relationships, but also affecting those in the future. Not the least of

53 OECD Economic Surveys, No. 14, p. 107.54Broomhill, P. 41.

37

which concerns the extent of Australia’s ongoing interaction with the region, and the

overall importance of regional trade to Australia’s future growth.

38

CHAPTER 3

The Importance of Regional Trade to Australia’s Future Growth

An important consideration in any argument about economic development concerns

the nature and type of development that is taking place. The neo-classical, and more

recently, liberal models of economic development predicate Australia’s relationship with

the EU and the US, which are characterised by predominantly western societies. However,

if we are talking about Australia’s relationship with East Asia (particularly Southeast Asia)

then we are talking about economic development that has occurred along somewhat

dissimilar lines. Here, ostensibly authoritarian regimes headed by military dictators have

attempted to obtain legitimacy by shrugging off their military uniforms and entering the

public arena, while maintaining close links with the military.

In many ways, what managed to sustain dynamic regional growth had been the

complicity of foreign capital, transnational corporations, and foreign governments with the

ruling elites of the region who acted in cooperation with powerful domestic cartels.55 Such

relationships provided regional stability because the ruling elites also controlled, or in large

part acted in cooperation with, the defence establishments and their leaders. Australia’s

relationship to foreign capital has been predicated by stability incurred through “… stable

institutions and sound conventions within a tried and tested constitutional system.“ 56

For these reasons, the Australian economy may be perceived as a somewhat safer

haven for investment than that of its regional neighbours. Moreover, Australia and the

region differ in terms of the origins of internal stability, and as such their attractiveness to

foreign capital and investment. There are also considerable differences in terms of their

orientation towards R & D and the varying levels of technical innovation and change that

55 Jayasuriya, K. The crisis of open regionalism and the new political economy of the Asia-Pacific, in Policy, Organisation & Society, Vol. 20, No. 1, 2001, p. 90.56 Flint, D. Opinion, The Australian, Wednesday January 9, 2002, p. 11.

39

have taken place. As discussed in the previous chapter, the input of foreign investment into

R & D is significantly less than that of domestic industry. This has caused some concern

because of the high levels of foreign ownership, particularly in the resources sector of the

Australian economy. However, in the region, particularly Southeast Asia, much of the

technical innovation and change has occurred through technical transfer (often called the

flying geese model of development). This has come from Japanese industries outsourcing

technology to take advantage of cheaper labour and infrastructural costs in the region. In

effect, this created a situation where the region did not have an indigenous crop of local

capitalists who were manufacturers, and neither did Australia for that matter. Moreover

like Australia, the region may well suffer from a drought in technical innovation and

change by virtue of the R & D sector not containing an indigenous crop of capitalists

motivated by any economic need to develop leading domestic industries. Again, the

outsourcing of R & D by foreign organizations with little input from the host economies

has seen this situation prevail in Australia and the region.

However, what many fail to consider in an argument such as this is the variety of

competing capitalisms in the region. Take for example the Diaspora of Chinese capitalism

throughout Southeast Asia; it has been argued that their relative successes have not simply

been the result of imitation or copying of the west, but may be considered a desirable

alternative model.57 However, this Diaspora, while quite large, occurs throughout the

region in small units when compared to the extensive corporations of the Japanese

overseas. This often meets with hostility from host nations as the Chinese concentration of

economic power is much maligned by indigenous populations.

57 Tracy, C.L. & Tracy, N. The Dragon and the Rising Sun: Market Integration and Economic Rivalry in East and Southeast Asia, Flinders University, 1994, pp. 3-7.

40

With competing capitalisms, differing models of economic development and

strategic instability the region may be considered highly volatile. This in itself creates a

somewhat uncertain investment environment for Australian firms, who would be more

inclined to trade outside the region (with the EU and the US) because of confusion over the

regional environment. Therefore, the idea that regional trade has enhanced Australia’s

economic development and the overall importance of the region to Australia’s future