june 2, 2003

DESCRIPTION

June 2, 2003. Assessing the World Bank Contribution to the Development of Global Insurance Markets: A Market Perspective. Sean Mooney New York. Agenda. Introduction to Guy Carpenter What the “Market” wants What the World Bank is doing What the World Bank can do Case Study Conclusion. - PowerPoint PPT PresentationTRANSCRIPT

Sean Mooney New York

Assessing the World Bank Contribution to the Development of Global Insurance Markets: A Market Perspective

June 2, 2003

Guy Carpenter 2

Agenda

Introduction to Guy Carpenter

What the “Market” wants

What the World Bank is doing

What the World Bank can do

Case Study

Conclusion

Guy Carpenter 3

Guy Carpenter & Co., Inc.

The reinsurance intermediary subsidiary of Marsh & McLennan Companies

MMC is a global professional services firm with annual revenues exceeding $10B. Core businesses:

– Risk and insurance

– Investment management

– Consulting

MMC has approx. 59,000 employees who provide analysis, advice and transactional capabilities to clients in more than 100 countries.

Guy Carpenter 4

Guy Carpenter & Co., Inc.

49 offices in 22 countries - 2200 employees

Leading catastrophe risk reinsurance intermediary:

– Over $3B in catastrophe reinsurance premium

– Over $35B in Limits placed annually

Intermediary for numerous governmental catastrophe programs

Guy Carpenter 5

What the “Market” wants

Reinsurance is a global business

Reinsured natural disaster exposures are heavily concentrated - USA, Europe, Japan

Better diversification = better risk profile

Strong desire for additional diversifying risk

As such, the “Market” welcomes the development of new catastrophe insurance markets

Preference for market-based solutions

Guy Carpenter 6

What The World Bank is Doing

TCIP is the case study for Public/Private partnership:

– World Bank worked with Turkish Govt throughout

– Brought together the necessary resources and expertise.

Successful first effort

Enthusiasm for the efforts of the World Bank

Reinsurers support efforts in other countries

Guy Carpenter 7

What The World Bank Can Do

Reinsurers recognize that developing economies can benefit from external funding and expertise in:

– Risk mitigation

– Set up of catastrophe insurance programs

– Catastrophe risk transfer techniques Reinsurance Capital markets

Organization and funding required for these

– World Bank is well suited to this task

Guy Carpenter 8

What The World Bank Can Do

Reinsurers recognize that The World Bank is unique:

– Mission to help the World’s poor

– Expertise in large, complex project management

– Not profit motivated

– Can provide low-cost funding

– Important to developing countries

Private market natural disaster experts do not share all of these attributes

Guy Carpenter 9

What The World Bank Can Do

Reinsurers see key roles of World Bank:

– Impartial Interface with Government bodies

– Project management, if required

– Funding for studies: Mitigation Feasibility Insurance and risk transfer Low cost financing of “retained” risks -- e.g.

reinsurance program deductibles.

Guy Carpenter 10

What The World Bank Can Do

Reinsurers expect even smoother future projects:

– Benefits of experience

– All parties understand processes and approaches better e.g.:

Reinsurance broker and reinsurer interaction World Bank tender process

Reinsurers applaud and encourage World Bank efforts

Case Study:Taiwan Residential Earthquake Insurance Pool (TREIP)

Guy Carpenter 12

Case Study: Taiwan Residential Earthquake Insurance Pool (TREIP)

Formed April 1, 2002

Formed as a result of Chi-Chi Earthquake, 9/21/1999

Lack of Residential Earthquake Insurance cover

Vulnerability of Taiwan to Earthquakes

Guy Carpenter 13

Chi-Chi Earthquake

September 21, 1999, 1:47 am (local time)

Magnitude 7.3 -7.7

Central part of Taiwan

Guy Carpenter 14

Chi-Chi Earthquake

Over 2,400 lives were lost

More than 10,000 people were injured

Over 5,000 buildings collapsed

Taiwan’s worst disaster since the Shin-Chu Taichung earthquake of April 1935, magnitude 7.1, where 3,325 lives were lost.

Guy Carpenter 15

Vulnerability of Taiwan to Earthquakes

Taiwan is a seismically active region Affected by many earthquakes each year Taiwan is being compressed and forms a

transitional zone between two areas of subduction, as a result of the collision between the Philippine and Eurasian plates

Guy Carpenter 16

Guy Carpenter 17

Lack of Residential Earthquake Insurance cover

Prior to the Chi-Chi earthquake, only about 1% of the residences in Taiwan had earthquake insurance

Earthquake insurance was available as an endorsement to long term fire policies

Guy Carpenter 18

Taiwanese Government’s Main Goal

Availability of earthquake damage compensation to Taiwan residents

– Concern as to whether compensation would be available to most residents following an event

– Includes a quasi-mandatory purchase of earthquake cover

Guy Carpenter 19

Secondary Goals

Affordable Insurance

Minimize government budget exposure

– Ministry of Finance (MOF) required all insurance companies to provide coverage for residential earthquake risk

Public/Private cooperative solution

Guy Carpenter 20

Characteristics of Taiwan

Taiwan is a small island, but is one of the most densely populated countries in the world.

The earthquake risk is very high. Taiwan has numerous fault lines, and relatively high probabilities of activity along the fault lines.

Traditionally residents are reluctant to purchase property insurance. This is a global trait, but appears to be relatively higher in Taiwan.

Guy Carpenter 21

Characteristics of Taiwan (Continued)

Until TREIP, residential insurance policies in the main were purchased for the life of the mortgage.

Single family western-style residences are rare (seven percent of all households).

Guy Carpenter 22

Insurance Policy

Fixed Premium per Household: NT$ 1,459

Building, maximum sum insured amount: NT$1.2 million

Contingent Living Expenses (CLE): NT$180,000

No cover for contents

Flat Rate (no variation by location or type of structure)

Guy Carpenter 23

Goals How Achieved

AvailabilityQuasi-mandatory, Links earthquake insurance to fire and mortgage policies, resulting in relatively high penetration into market place

AffordabilityLow cost CTL Feature, No contents cover, Limit of NT$ 1.2 million max. insured amount

Minimize government budget exposure

Insurance companies participate at high frequency layer. Program capped, Reinsurance purchased from international market

Public / PrivateNational earthquake scheme - creating risk sharing partnership

Guy Carpenter 24

FundingStructure of TREIP

Excess NT$ 50 Billion: Pro Rata

NT$ 10 Billion xs. NT$ 40 Billion: Government

NT$ 20 Billion xs. NT$ 20 Billion: International Reinsurers

NT$ 18 Billion xs. NT$ 2 Billion: Government Foundation

NT$ 2 Billion: Private Insurers

Pro Rata

Layer 4

Layer 3

Layer 2

Layer 1

Guy Carpenter 25

Program Administration

TREIP managed by Central Reinsurance Corporation (CRC)

– Part owned by the Government

– Long time reinsurer of Taiwanese and international risks

– Professional/ well established expertise in reinsurance

Guy Carpenter 26

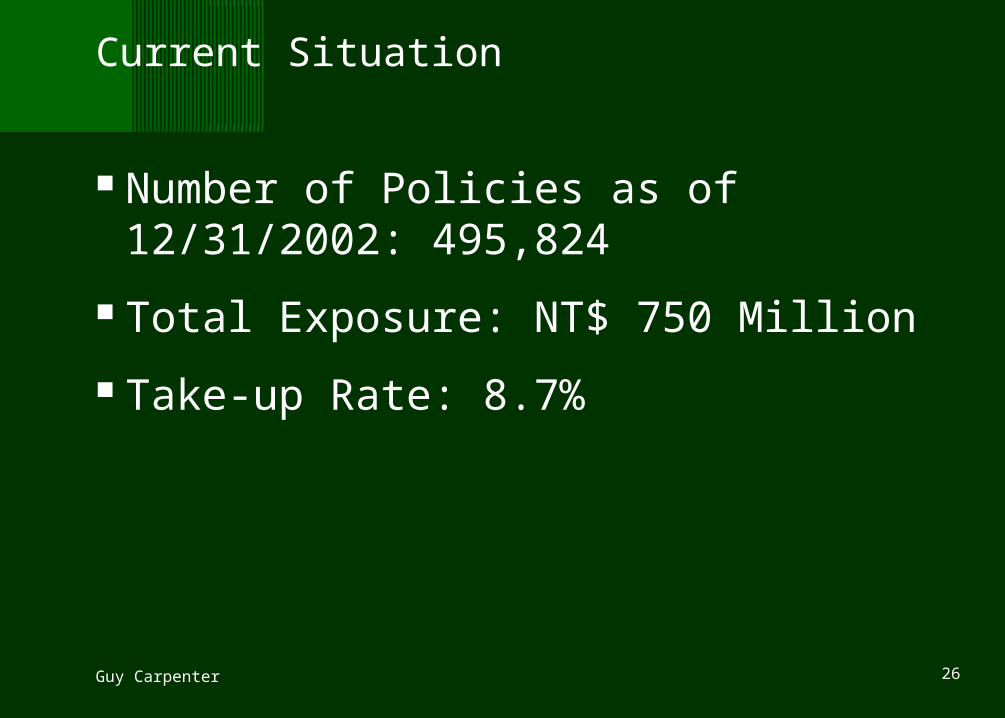

Current Situation

Number of Policies as of 12/31/2002: 495,824

Total Exposure: NT$ 750 Million

Take-up Rate: 8.7%

Guy Carpenter 27

Summary

TREIP successfully launched

Stable financial support

– Excellent public/private partnership

– Strong reinsurance support

Achieving key goal of availability

Guy Carpenter 28

Achieving Strong Support from Reinsurers: Lessons Learned

Professional Management of TREIP

High Quality Data

Adequate original pricing

Legal structures in place to manage disputes

Defined claims settlement process

Guy Carpenter 29

Role for the World Bank?

Taiwan is a relatively wealthy economy with substantial resources thus able to:

– Fund Feasibility studies Earthquake risk assessment (modeling)

– Domestically retained substantial risk

Other economies not in the same position:

– World Bank can provide the foregoing for less developed economies

Guy Carpenter 30

Conclusion

World Bank should continue its efforts:

– Improve economies of developing nations

– Simultaneously, help the international risk transfer markets function more efficiently

Sean MooneyNew York

Assessing the World Bank Contribution to the Development of Global Insurance Markets: A Market Perspective

June 2, 2003