july 2013 update

DESCRIPTION

ÂTRANSCRIPT

Merritt’s Market Update

Monterey Peninsula

July, 2013

©2013 Merritt Ringer

Read, Seen, or Heard

A quant’s view of the Department of Motor Vehicles:

(this Venn diagram has many applications in modern life)

“There are two kinds of people, those who do the work

and those who take the credit. Try to be in the first

group; there is less competition there.”

- Indira Gandhi

Table of Contents

The Big Picture…………………….…….………... 3

More Big Picture…..……………….…….………... 4

Prices…………………………………….………… 5

Financing………………………………….……….. 6

Carmel………………………………...….….…… 7-8

Carmel Valley…………………………..….……… 9-10

Pebble Beach………………………...……….…… 10-11

Pacific Grove…………………………….…….…..12-13

Monterey…………………………………....….…..14-15

Monterey-Salinas Corridor………………...……. 16-17

Seaside & Marina ………………………...……… 18-19

An Agents Life …………………...….…...…….…..20

End Note …………………………………………....21

Caveat: I’m no economist (despite the performance of

most, this is not a boast). I also lack the gift of prophecy;

from the evidence, I’m not alone. But our real estate

market is buffeted and buoyed by all manner of larger

forces, so I do watch the horizons. I also dig into our

local market. The information here is as reliable as I can

make it, but nothing like comprehensive.

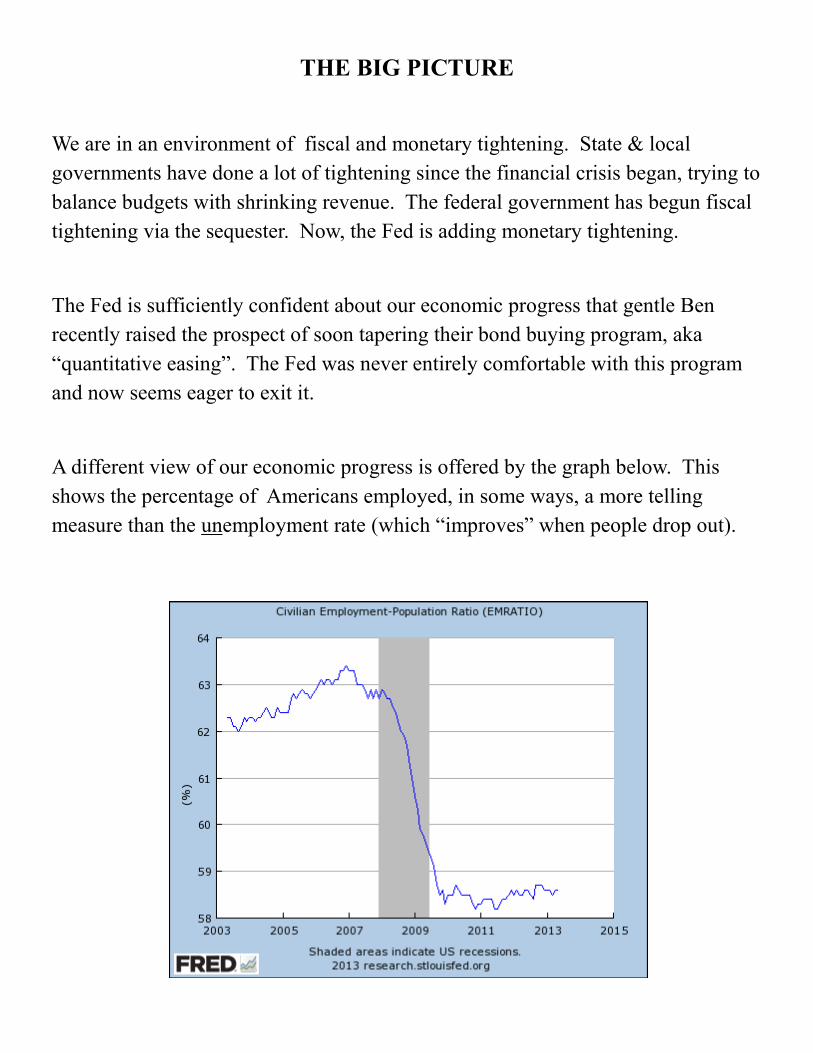

THE BIG PICTURE

We are in an environment of fiscal and monetary tightening. State & local

governments have done a lot of tightening since the financial crisis began, trying to

balance budgets with shrinking revenue. The federal government has begun fiscal

tightening via the sequester. Now, the Fed is adding monetary tightening.

The Fed is sufficiently confident about our economic progress that gentle Ben

recently raised the prospect of soon tapering their bond buying program, aka

“quantitative easing”. The Fed was never entirely comfortable with this program

and now seems eager to exit it.

A different view of our economic progress is offered by the graph below. This

shows the percentage of Americans employed, in some ways, a more telling

measure than the unemployment rate (which “improves” when people drop out).

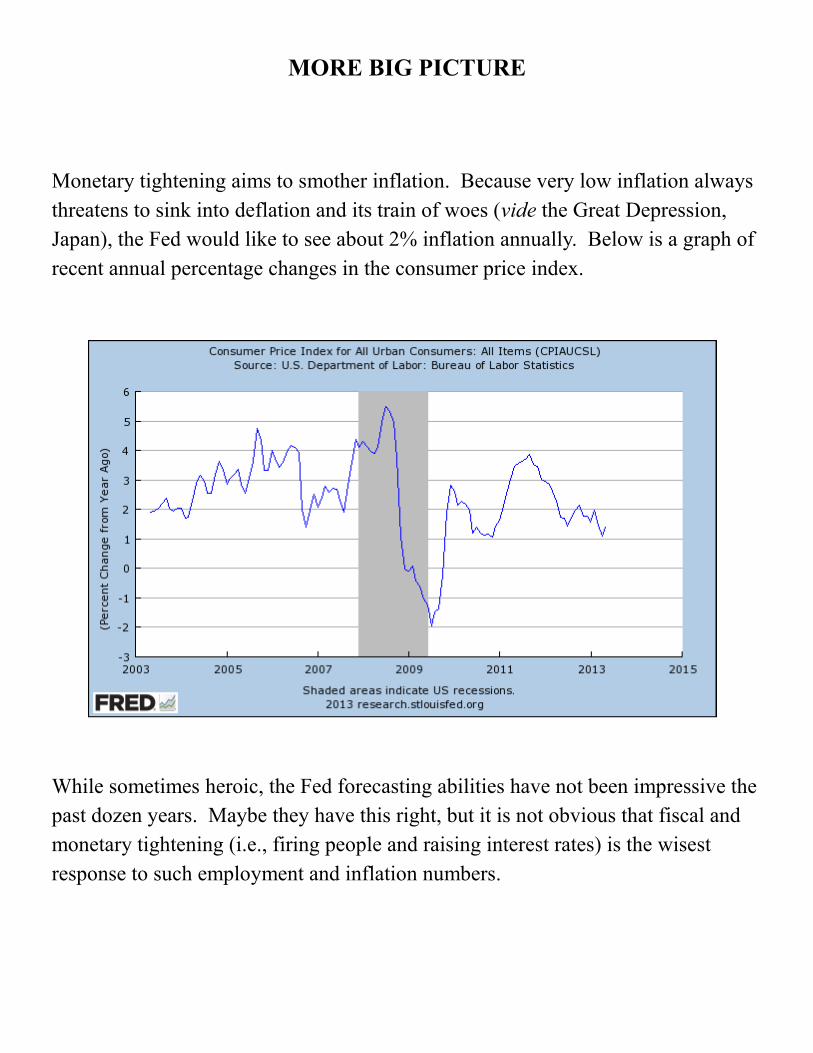

MORE BIG PICTURE

Monetary tightening aims to smother inflation. Because very low inflation always

threatens to sink into deflation and its train of woes (vide the Great Depression,

Japan), the Fed would like to see about 2% inflation annually. Below is a graph of

recent annual percentage changes in the consumer price index.

While sometimes heroic, the Fed forecasting abilities have not been impressive the

past dozen years. Maybe they have this right, but it is not obvious that fiscal and

monetary tightening (i.e., firing people and raising interest rates) is the wisest

response to such employment and inflation numbers.

PRICES

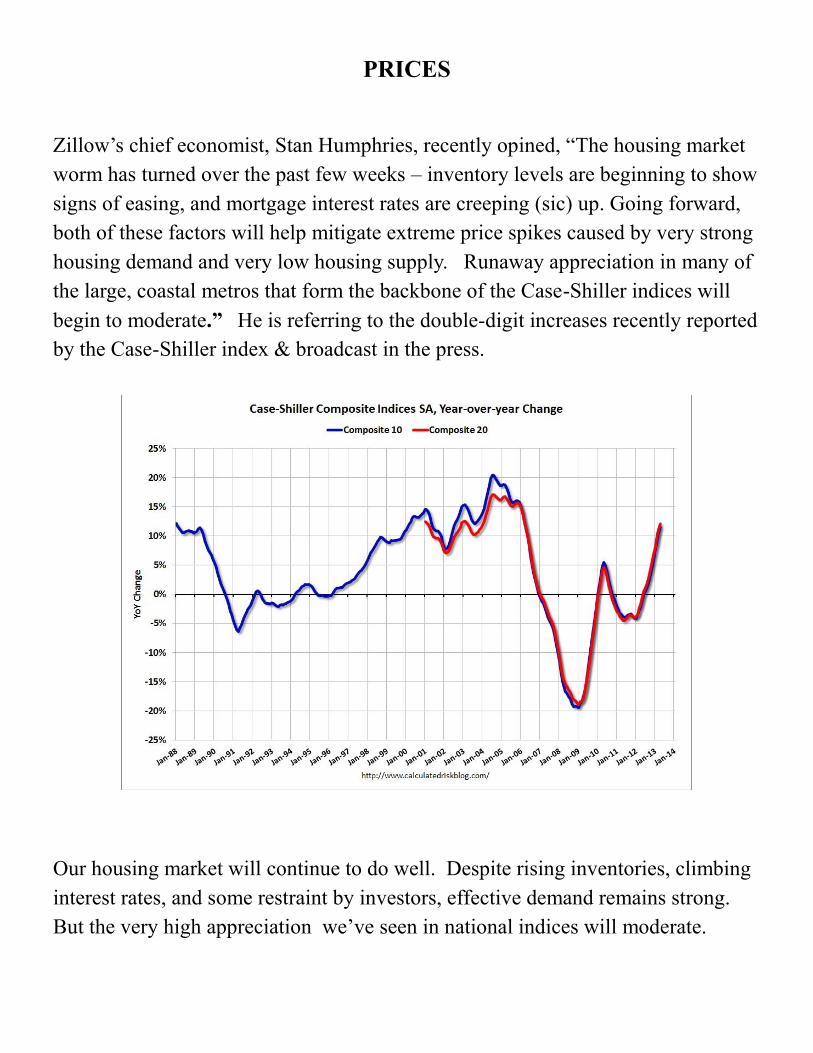

Zillow’s chief economist, Stan Humphries, recently opined, “The housing market

worm has turned over the past few weeks – inventory levels are beginning to show

signs of easing, and mortgage interest rates are creeping (sic) up. Going forward,

both of these factors will help mitigate extreme price spikes caused by very strong

housing demand and very low housing supply. Runaway appreciation in many of

the large, coastal metros that form the backbone of the Case-Shiller indices will

begin to moderate.” He is referring to the double-digit increases recently reported

by the Case-Shiller index & broadcast in the press.

Our housing market will continue to do well. Despite rising inventories, climbing

interest rates, and some restraint by investors, effective demand remains strong.

But the very high appreciation we’ve seen in national indices will moderate.

FINANCING

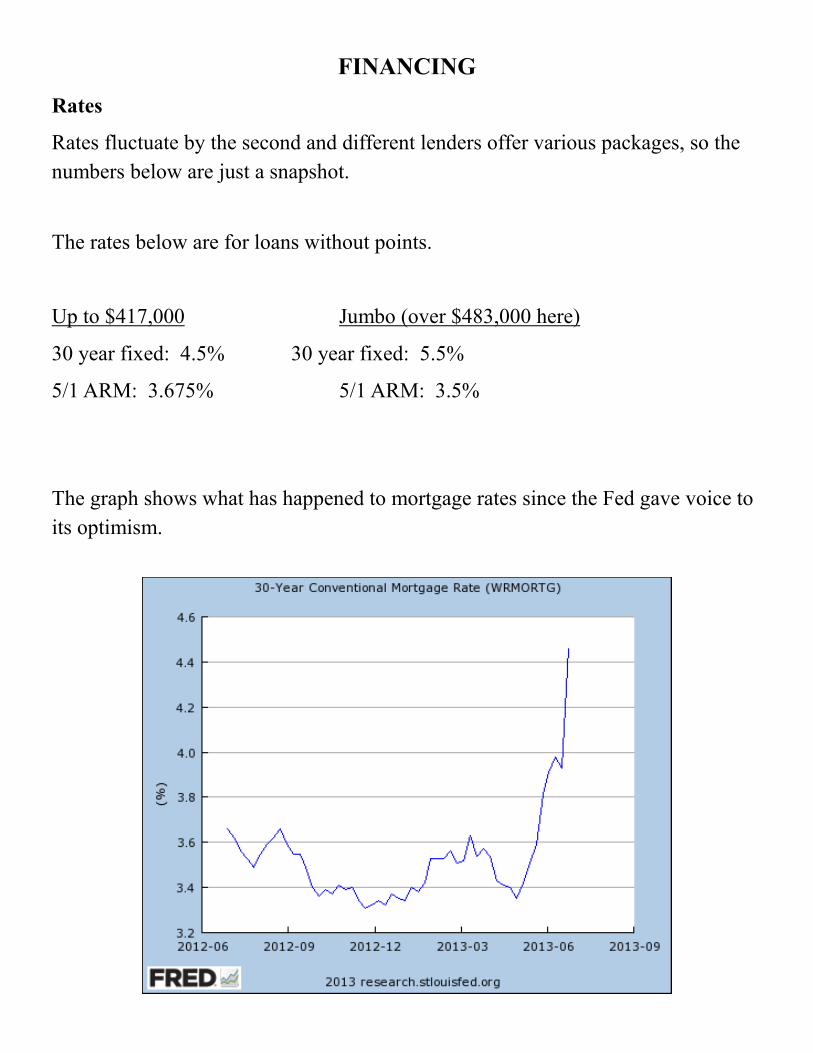

Rates

Rates fluctuate by the second and different lenders offer various packages, so the

numbers below are just a snapshot.

The rates below are for loans without points.

Up to $417,000 Jumbo (over $483,000 here)

30 year fixed: 4.5% 30 year fixed: 5.5%

5/1 ARM: 3.675% 5/1 ARM: 3.5%

The graph shows what has happened to mortgage rates since the Fed gave voice to

its optimism.

CARMEL: NEW ESCROWS

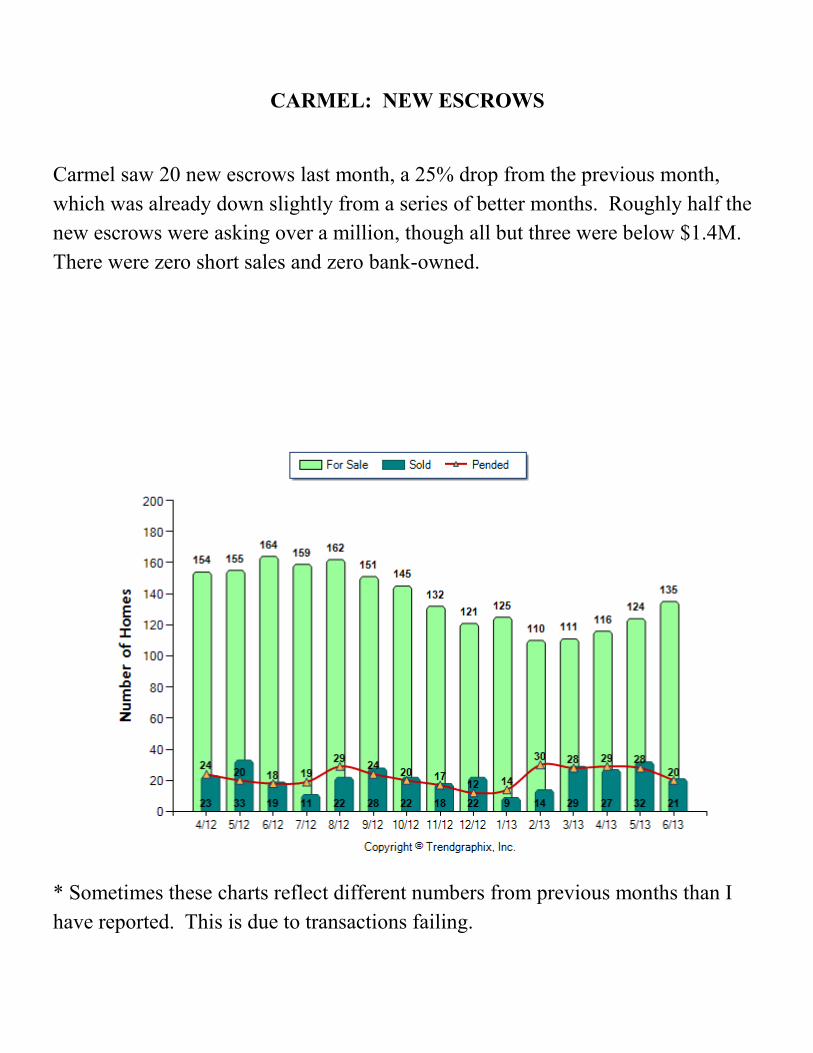

Carmel saw 20 new escrows last month, a 25% drop from the previous month,

which was already down slightly from a series of better months. Roughly half the

new escrows were asking over a million, though all but three were below $1.4M.

There were zero short sales and zero bank-owned.

* Sometimes these charts reflect different numbers from previous months than I

have reported. This is due to transactions failing.

CARMEL CLOSED HIGH & LOW

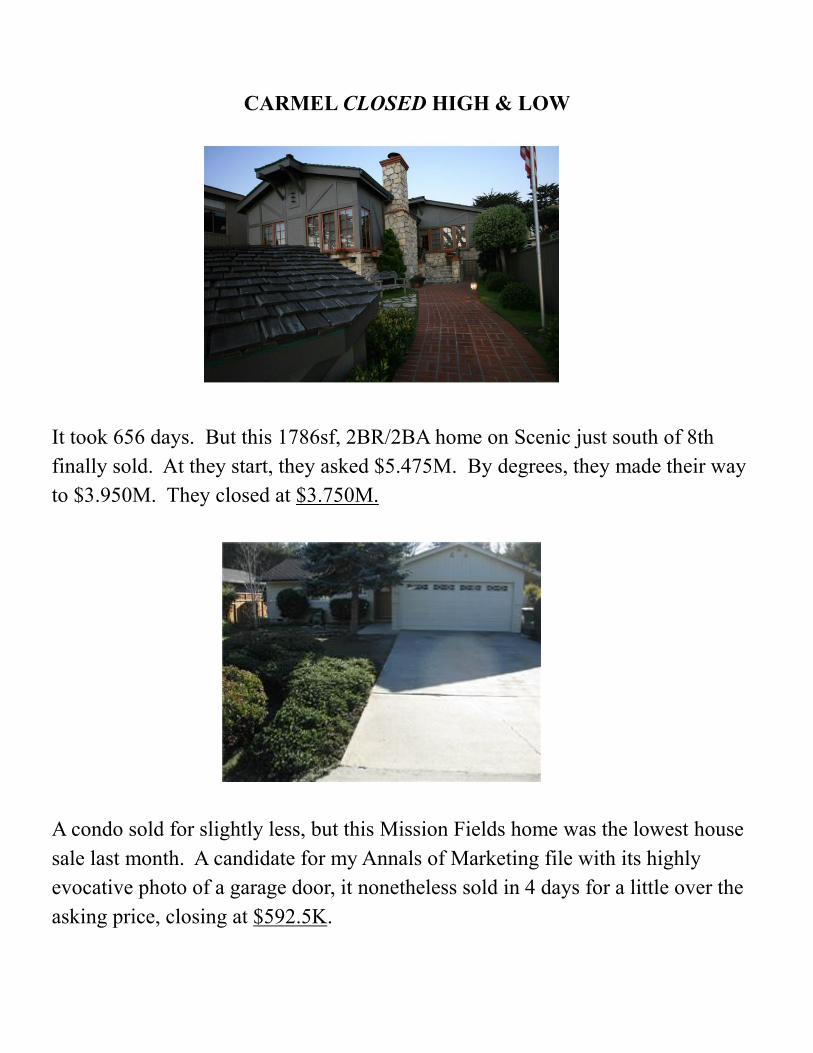

It took 656 days. But this 1786sf, 2BR/2BA home on Scenic just south of 8th

finally sold. At they start, they asked $5.475M. By degrees, they made their way

to $3.950M. They closed at $3.750M.

A condo sold for slightly less, but this Mission Fields home was the lowest house

sale last month. A candidate for my Annals of Marketing file with its highly

evocative photo of a garage door, it nonetheless sold in 4 days for a little over the

asking price, closing at $592.5K.

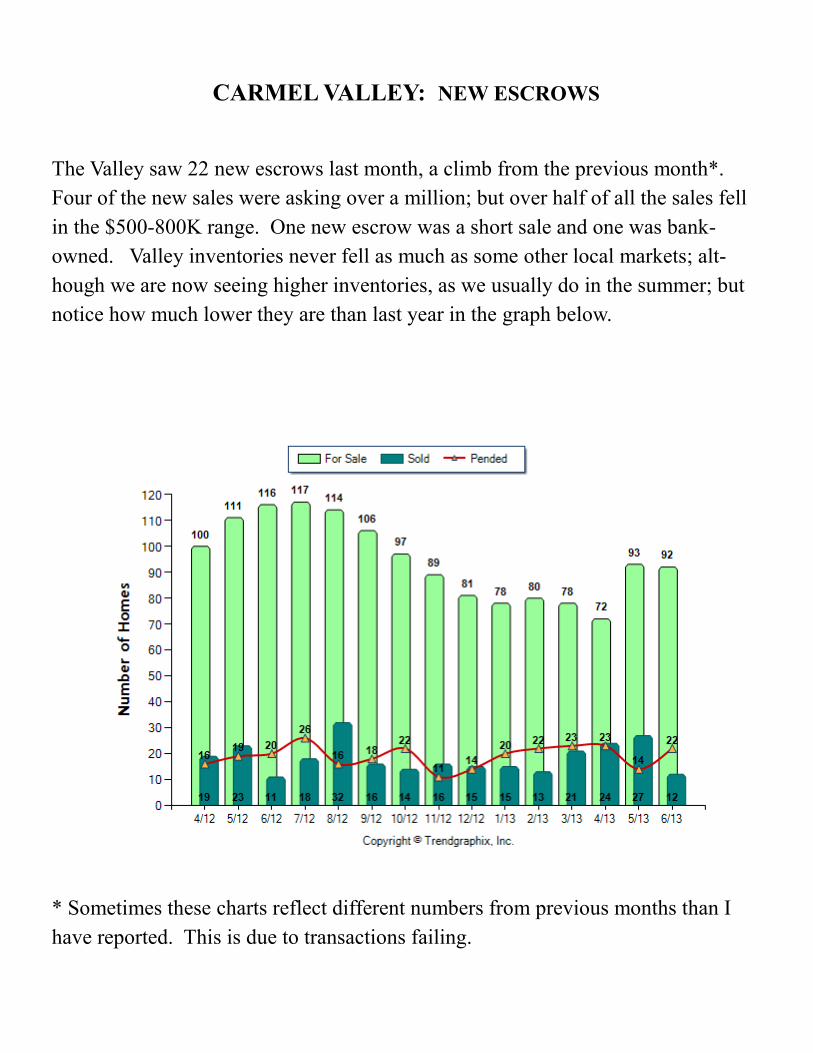

CARMEL VALLEY: NEW ESCROWS

The Valley saw 22 new escrows last month, a climb from the previous month*.

Four of the new sales were asking over a million; but over half of all the sales fell

in the $500-800K range. One new escrow was a short sale and one was bank-

owned. Valley inventories never fell as much as some other local markets; alt-

hough we are now seeing higher inventories, as we usually do in the summer; but

notice how much lower they are than last year in the graph below.

* Sometimes these charts reflect different numbers from previous months than I

have reported. This is due to transactions failing.

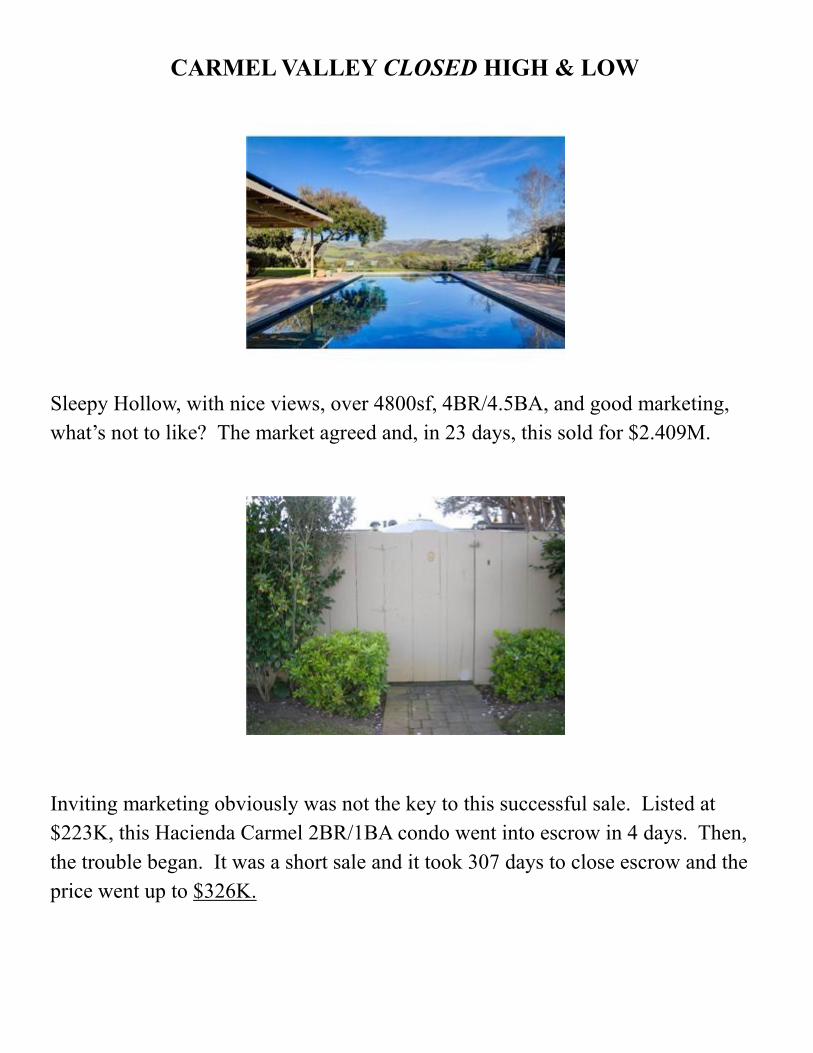

CARMEL VALLEY CLOSED HIGH & LOW

Sleepy Hollow, with nice views, over 4800sf, 4BR/4.5BA, and good marketing,

what’s not to like? The market agreed and, in 23 days, this sold for $2.409M.

Inviting marketing obviously was not the key to this successful sale. Listed at

$223K, this Hacienda Carmel 2BR/1BA condo went into escrow in 4 days. Then,

the trouble began. It was a short sale and it took 307 days to close escrow and the

price went up to $326K.

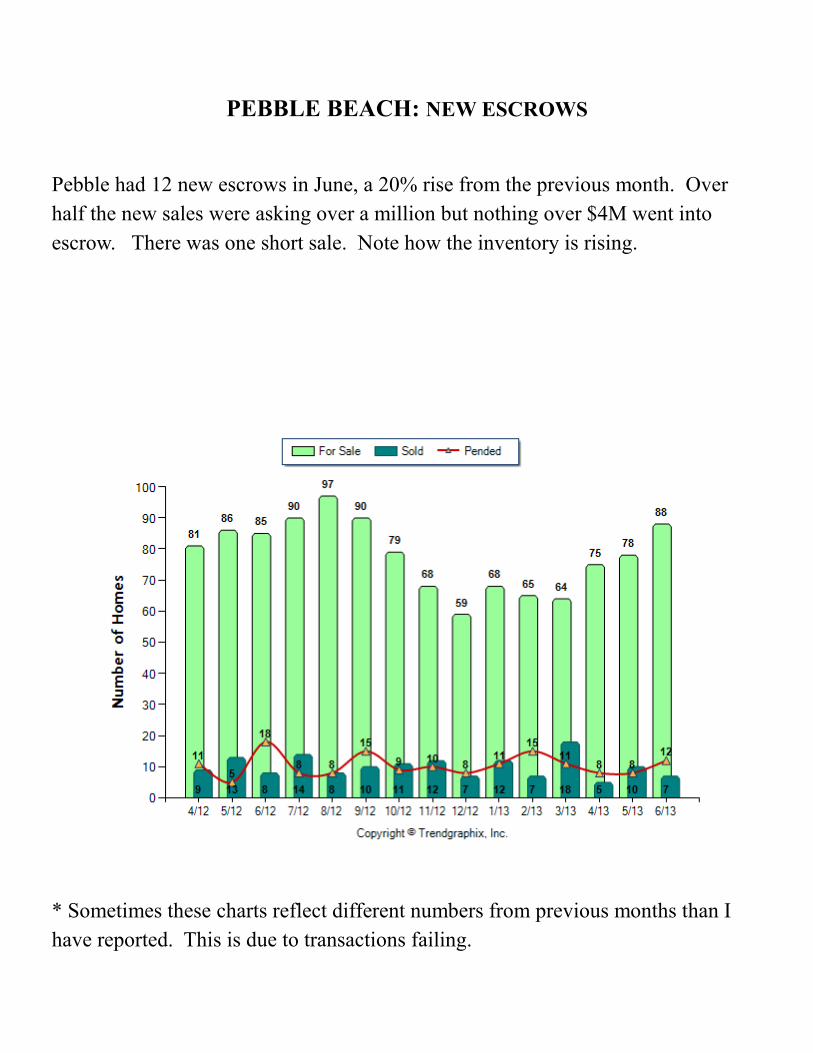

PEBBLE BEACH: NEW ESCROWS

Pebble had 12 new escrows in June, a 20% rise from the previous month. Over

half the new sales were asking over a million but nothing over $4M went into

escrow. There was one short sale. Note how the inventory is rising.

* Sometimes these charts reflect different numbers from previous months than I

have reported. This is due to transactions failing.

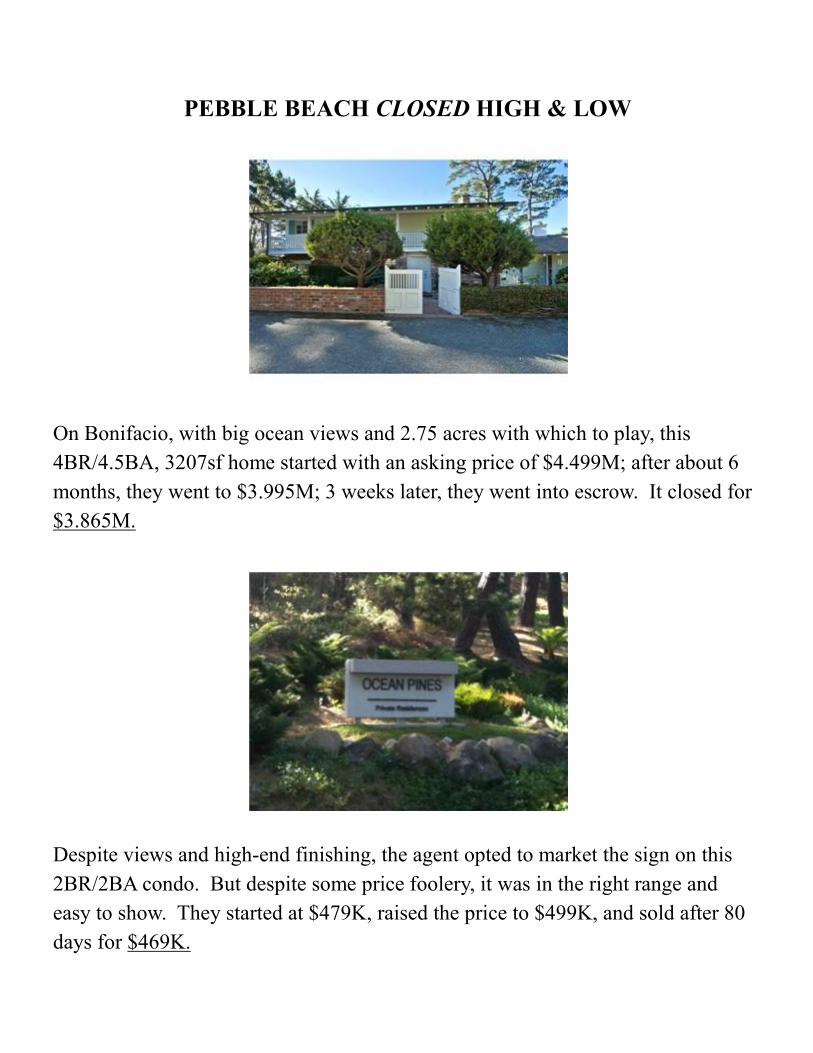

PEBBLE BEACH CLOSED HIGH & LOW

On Bonifacio, with big ocean views and 2.75 acres with which to play, this

4BR/4.5BA, 3207sf home started with an asking price of $4.499M; after about 6

months, they went to $3.995M; 3 weeks later, they went into escrow. It closed for

$3.865M.

Despite views and high-end finishing, the agent opted to market the sign on this

2BR/2BA condo. But despite some price foolery, it was in the right range and

easy to show. They started at $479K, raised the price to $499K, and sold after 80

days for $469K.

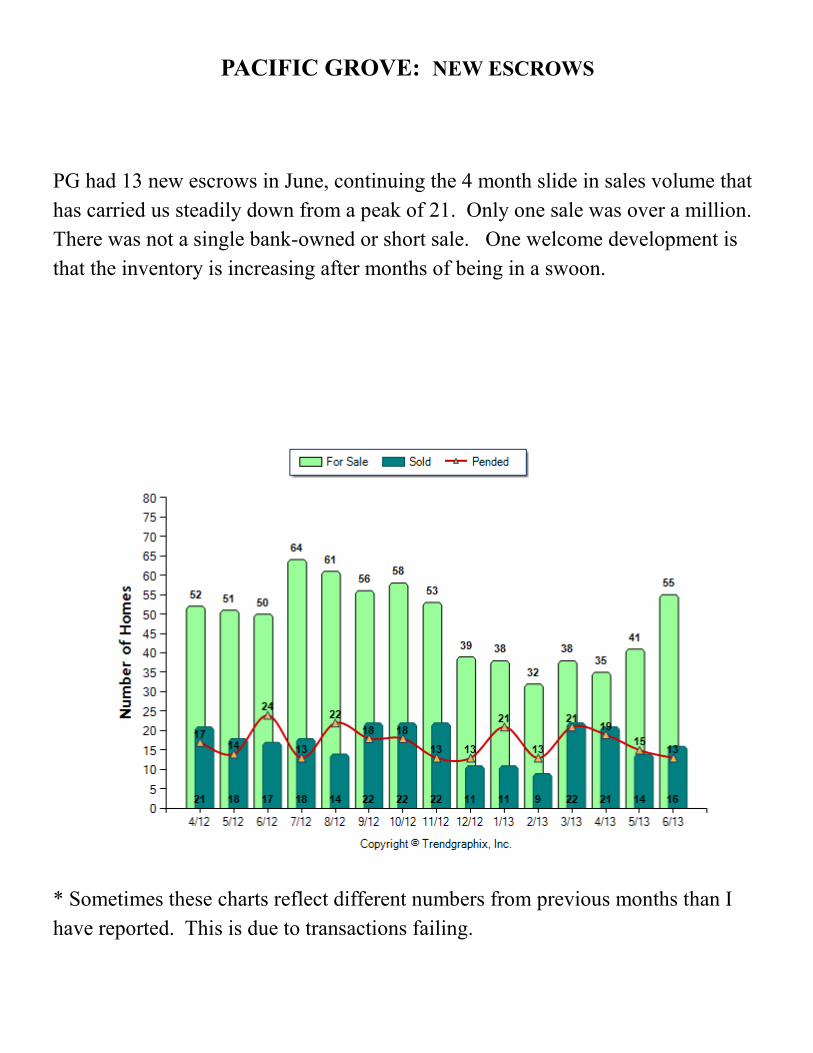

PACIFIC GROVE: NEW ESCROWS

PG had 13 new escrows in June, continuing the 4 month slide in sales volume that

has carried us steadily down from a peak of 21. Only one sale was over a million.

There was not a single bank-owned or short sale. One welcome development is

that the inventory is increasing after months of being in a swoon.

* Sometimes these charts reflect different numbers from previous months than I

have reported. This is due to transactions failing.

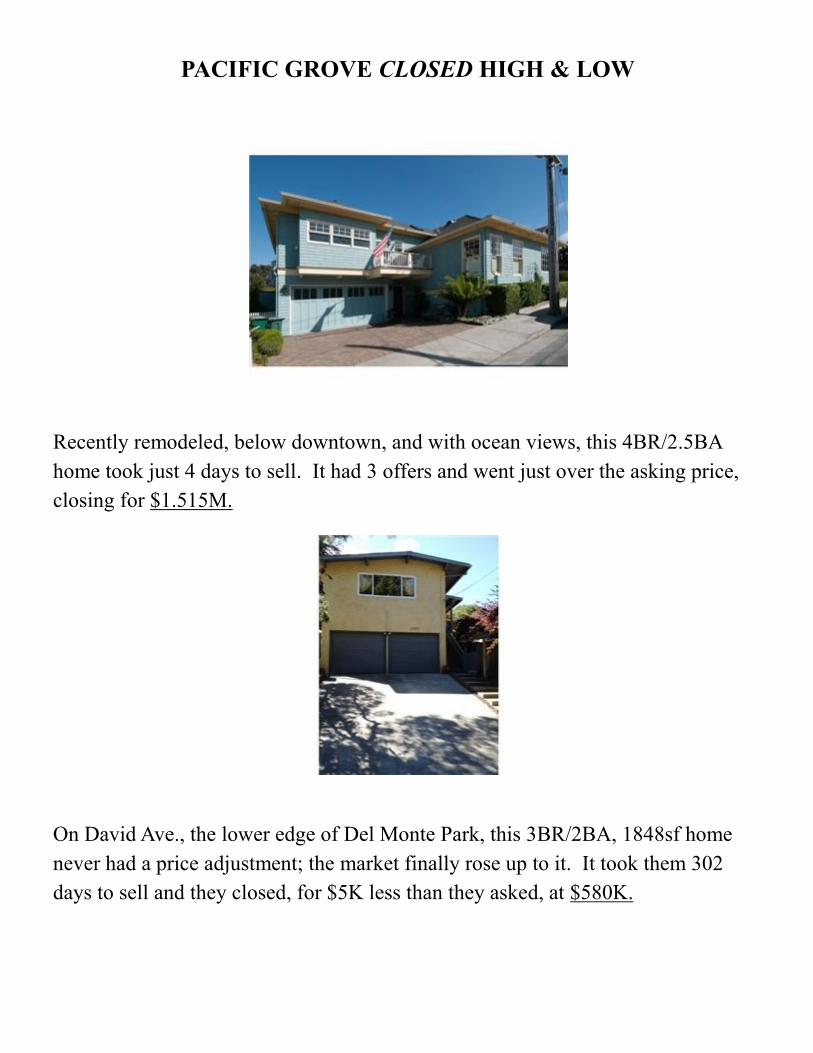

PACIFIC GROVE CLOSED HIGH & LOW

Recently remodeled, below downtown, and with ocean views, this 4BR/2.5BA

home took just 4 days to sell. It had 3 offers and went just over the asking price,

closing for $1.515M.

On David Ave., the lower edge of Del Monte Park, this 3BR/2BA, 1848sf home

never had a price adjustment; the market finally rose up to it. It took them 302

days to sell and they closed, for $5K less than they asked, at $580K.

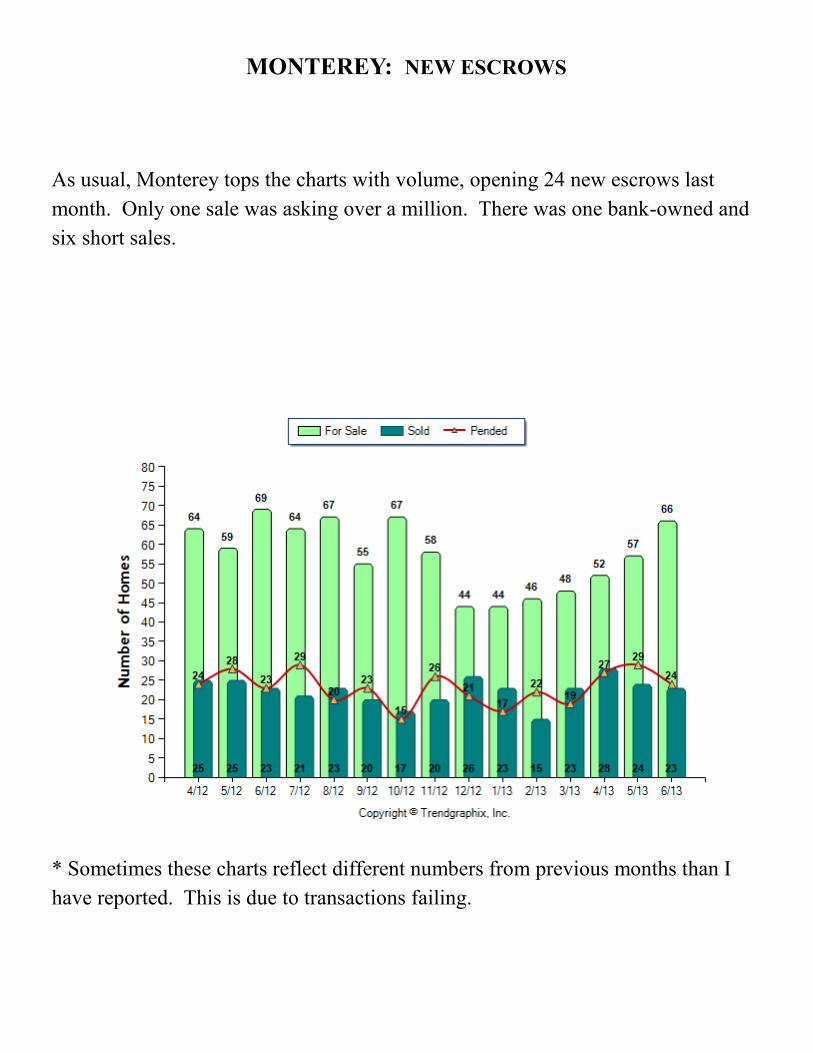

MONTEREY: NEW ESCROWS

As usual, Monterey tops the charts with volume, opening 24 new escrows last

month. Only one sale was asking over a million. There was one bank-owned and

six short sales.

* Sometimes these charts reflect different numbers from previous months than I

have reported. This is due to transactions failing.

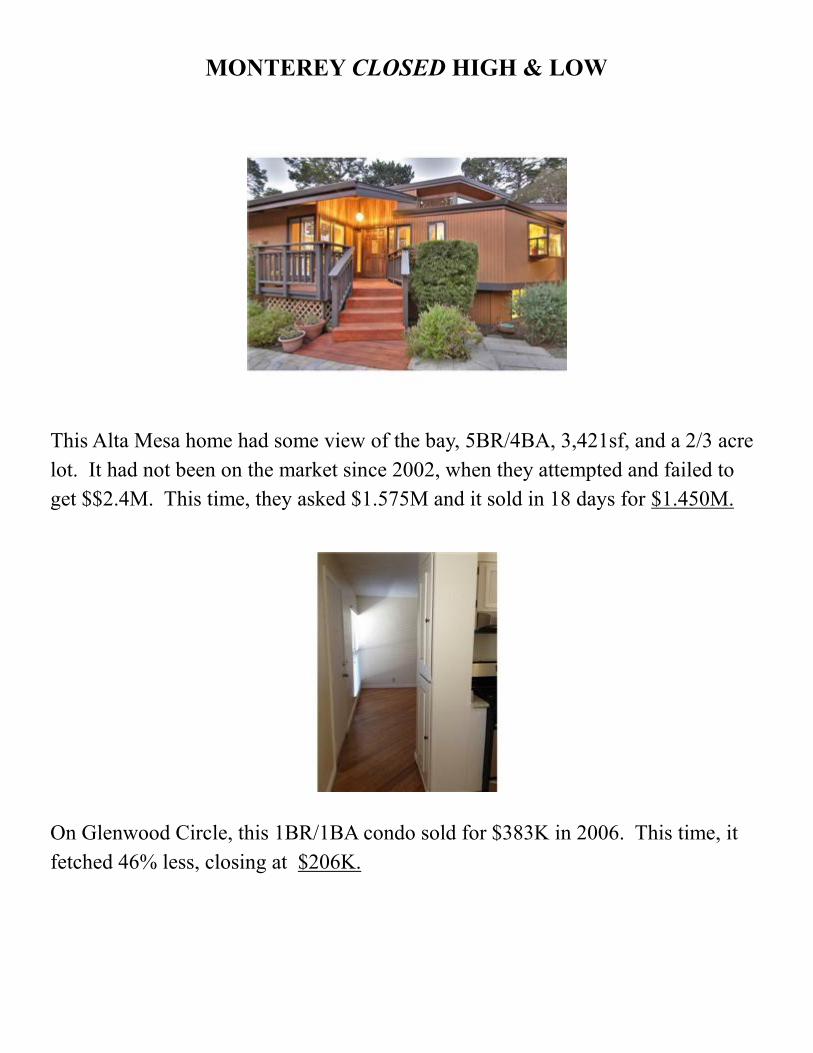

MONTEREY CLOSED HIGH & LOW

This Alta Mesa home had some view of the bay, 5BR/4BA, 3,421sf, and a 2/3 acre

lot. It had not been on the market since 2002, when they attempted and failed to

get $$2.4M. This time, they asked $1.575M and it sold in 18 days for $1.450M.

On Glenwood Circle, this 1BR/1BA condo sold for $383K in 2006. This time, it

fetched 46% less, closing at $206K.

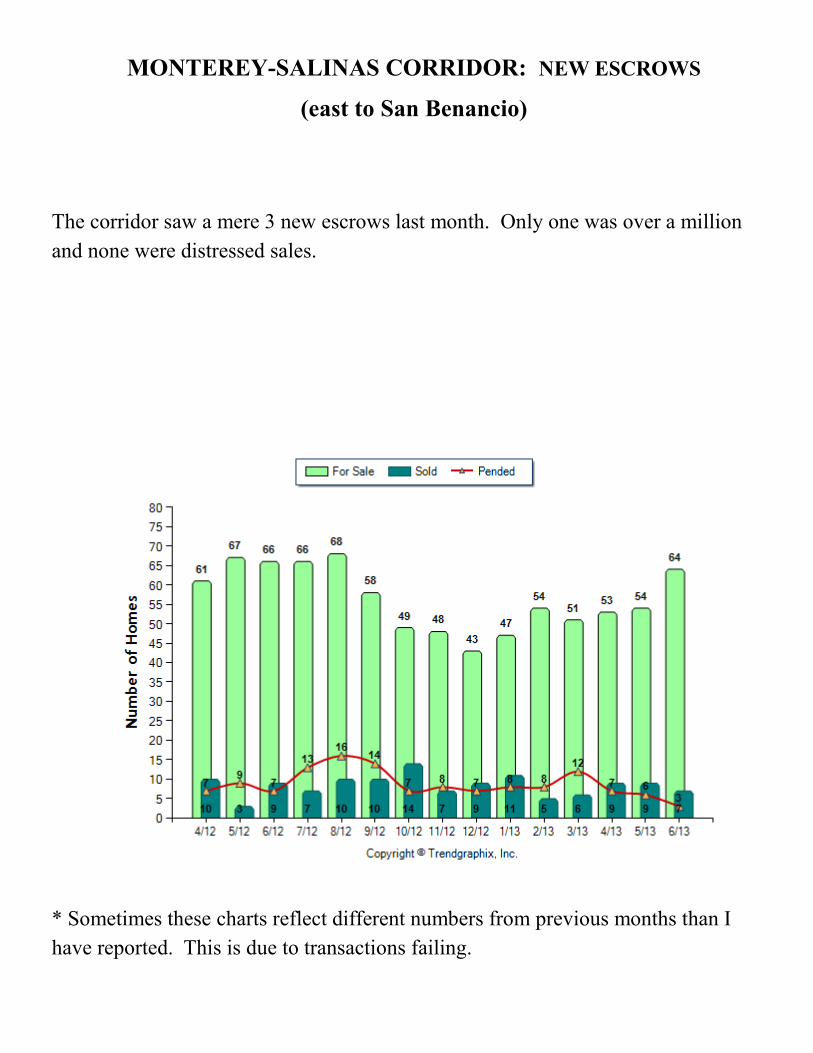

MONTEREY-SALINAS CORRIDOR: NEW ESCROWS

(east to San Benancio)

The corridor saw a mere 3 new escrows last month. Only one was over a million

and none were distressed sales.

* Sometimes these charts reflect different numbers from previous months than I

have reported. This is due to transactions failing.

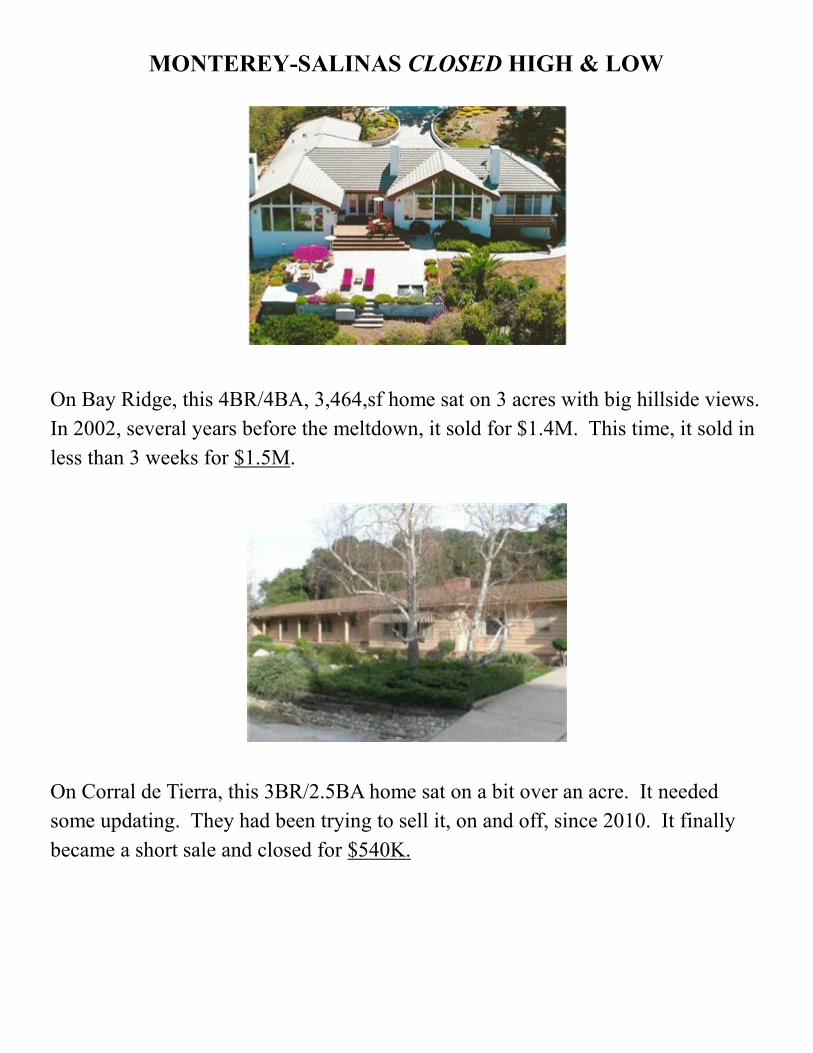

MONTEREY-SALINAS CLOSED HIGH & LOW

On Bay Ridge, this 4BR/4BA, 3,464,sf home sat on 3 acres with big hillside views.

In 2002, several years before the meltdown, it sold for $1.4M. This time, it sold in

less than 3 weeks for $1.5M.

On Corral de Tierra, this 3BR/2.5BA home sat on a bit over an acre. It needed

some updating. They had been trying to sell it, on and off, since 2010. It finally

became a short sale and closed for $540K.

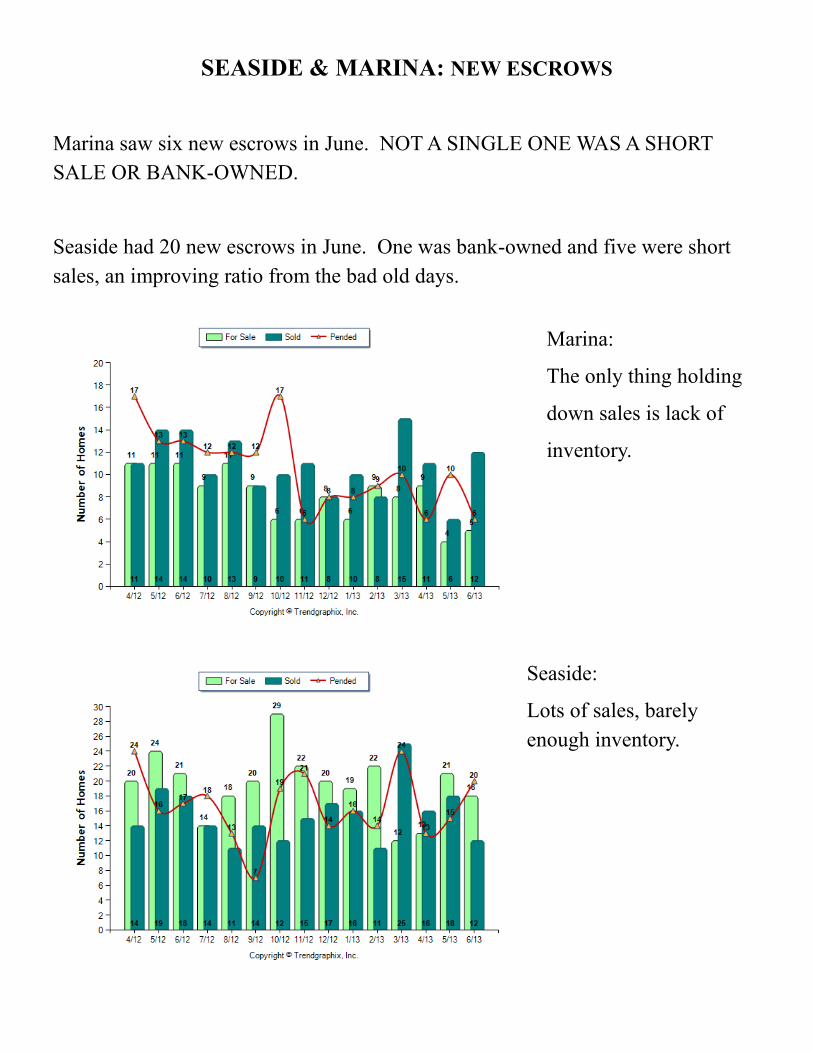

SEASIDE & MARINA: NEW ESCROWS

Marina saw six new escrows in June. NOT A SINGLE ONE WAS A SHORT

SALE OR BANK-OWNED.

Seaside had 20 new escrows in June. One was bank-owned and five were short

sales, an improving ratio from the bad old days.

Marina:

The only thing holding

down sales is lack of

inventory.

Seaside:

Lots of sales, barely

enough inventory.

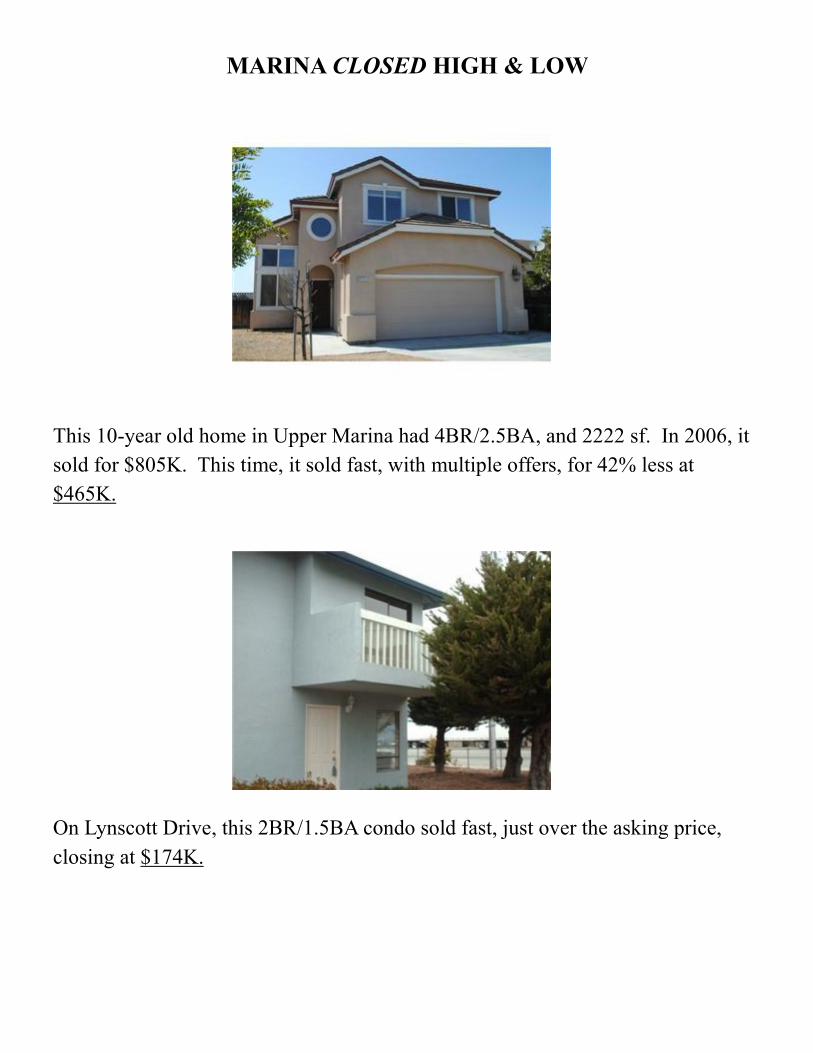

This 10-year old home in Upper Marina had 4BR/2.5BA, and 2222 sf. In 2006, it

sold for $805K. This time, it sold fast, with multiple offers, for 42% less at

$465K.

On Lynscott Drive, this 2BR/1.5BA condo sold fast, just over the asking price,

closing at $174K.

MARINA CLOSED HIGH & LOW

An Agent’s Life

A foggy July in Carmel before the sun got up.

We are seeing more all-cash transactions. I had buyers,

with great credit, who offered the highest price for a

home, 71% down, an 18-day close . . . & lost to an all-

cash, 7-day close offer. Fortunately, we found another

home and are in now escrow.

Thank your for taking a few minutes with my e-magazine. Your

comments & questions are welcome. Let me know about issues you’d

like to see addressed here or stories and facts you’d like others to know.

Know anyone thinking of buying or selling, someone who would benefit

from informed & straight counsel? Please keep me in mind. Referrals

like yours are the heart of my practice.

© Merritt Ringer 2013

Merritt’s Market Update

©2013 Merritt Ringer