jpe industry

DESCRIPTION

JPE INDUSTRY REVIEW NIGHT Presented by: Hagop Tchamkertenian Manager, Industry & Commercial Policy Printing Industries Association of Australia. JPE INDUSTRY. REVIEW NIGHT. •. Developments in the. industry during financial. year 2002-2003 and. over recent years. •. Latest data from. - PowerPoint PPT PresentationTRANSCRIPT

JPE INDUSTRY REVIEW NIGHT

Presented by:Hagop Tchamkertenian

Manager, Industry &Commercial Policy

Printing IndustriesAssociation of Australia

JPE INDUSTRYREVIEW NIGHT

• Developments in theindustry during financialyear 2002-2003 andover recent years

• Latest data fromPrinting Industry TrendsReport and Industry Benchmarking study

• Industry Prospects for2004 and beyond

Compared to 2002 how was 2003? • Good • Average• Bad

Industry ConditionsHow good are

we doing?

Importance of Our Industry A Historical Context

A ranking of the 100 most influential persons in history shows:

• Ts’ai Lun inventor of paper at number 7

• Johann Gutenberg “father of printing” developer of movable type at number 8

• Gutenberg’s invention facilitated an easier exchange of ideas throughout Europe and helped spread the ideas of the Renaissance

Importance of Our Industry A Historical Context

• Printing has been the principal vehicle for the conveying of ideas during the past 500 years

• In Australia the printing industry was one of the earliest industries to emerge after white settlement

• Industry icon – John Sands was founded in 1837 and was the 2nd company to be registered in Australia after the Bank of NSW

Industry Significance Current Demographics

• 5,000 plus firms

• Employment of more than 115,000

• Turnover of more than $17 billion

• Industry value added of more than $8.5 billion

• Exports of nearly $600 million

• Average annual capital expenditure of $724 million

• Physical presence in every region

Economic Growth 1993-2003

-40.0 -30.0 -20.0 -10.0 0.0 10.0 20.0 30.0 40.0 50.0 60.0

Food, beverage and tobacco

Textile, clothing, footwear

Wood and paper products

Printing, publishing and recorded media

Petroleum, coal, chemical, etc

Non-metallic mineral products

Metal products

Machinery and equipment

Other manufacturing

Total Manufacturing

Australian economy

Percentage change

How fast did we grow?

ABS Data

Economic Growth 12 months to December 2003

-8.0 -6.0 -4.0 -2.0 0.0 2.0 4.0 6.0

Food, beverage and tobacco

Textile, clothing, footwear

Wood and paper products

Printing, publishing and recorded media

Petroleum, coal, chemical, etc

Non-metallic mineral products

Metal products

Machinery and equipment

Other manufacturing

Total Manufacturing

Australian economy

Percent

How fast are we growing now?

ABS Data

Fastest Growing Sectors - 1993 to 2003

0.0 20.0 40.0 60.0 80.0 100.0 120.0

Communication services

Property & business services

Personal services

Wholesale trade

Finance & insurance

Accomodation, cafes & restaurants

Mining

Retail trade

Health & community services

Construction

Printing

Transport

Australian economy

Percent

Tortoise or hare?

ABS Data

Economic Growth - Printing

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

Dec

.199

3

Jun

.199

4

Dec

.199

4

Jun

.199

5

Dec

.199

5

Jun

.199

6

Dec

.199

6

Jun

.199

7

Dec

.199

7

Jun

.199

8

Dec

.199

8

Jun

.199

9

Dec

.199

9

Jun

.200

0

Dec

.200

0

Jun

.200

1

Dec

.200

1

Jun

.200

2

Dec

.200

2

Jun

.200

3

Dec

.200

3

Per

cen

tag

e ch

ang

e

Trend

Recession… technically speaking

ABS Data

Capital Expenditure - Printing

-30.0

-25.0

-20.0

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

Dec

.199

3

Jun

.199

4

Dec

.199

4

Jun

.199

5

Dec

.199

5

Jun

.199

6

Dec

.199

6

Jun

.199

7

Dec

.199

7

Jun

.199

8

Dec

.199

8

Jun

.199

9

Dec

.199

9

Jun

.200

0

Dec

.200

0

Jun

.200

1

Dec

.200

1

Jun

.200

2

Dec

.200

2

Jun

.200

3

Dec

.200

3

Per

cen

tag

e ch

ang

e

Investment Trend Downward

ABS Data

Capital Expenditure

-30.0

-25.0

-20.0

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

Dec

.199

3

Jun.

1994

Dec

.199

4

Jun.

1995

Dec

.199

5

Jun.

1996

Dec

.199

6

Jun.

1997

Dec

.199

7

Jun.

1998

Dec

.199

8

Jun.

1999

Dec

.199

9

Jun.

2000

Dec

.200

0

Jun.

2001

Dec

.200

1

Jun.

2002

Dec

.200

2

Jun.

2003

Dec

.200

3

Per

cen

tag

e ch

nag

e

PrintingAll industries

Contrasting Trends

ABS Data

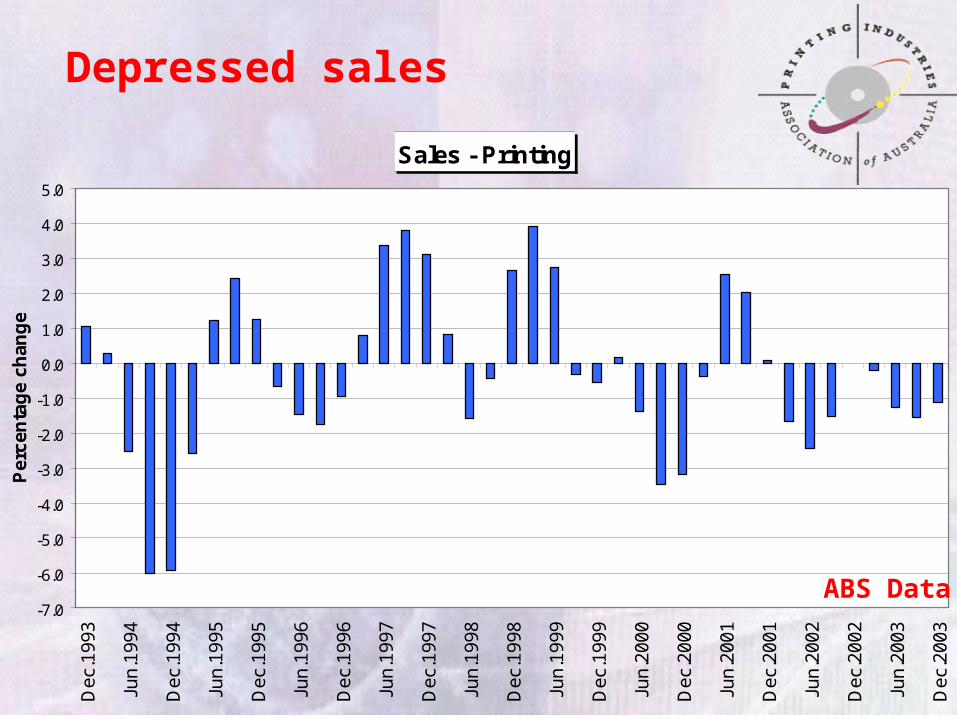

Sales - Printing

-7.0

-6.0

-5.0

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

Dec

.199

3

Jun

.199

4

Dec

.199

4

Jun

.199

5

Dec

.199

5

Jun

.199

6

Dec

.199

6

Jun

.199

7

Dec

.199

7

Jun

.199

8

Dec

.199

8

Jun

.199

9

Dec

.199

9

Jun

.200

0

Dec

.200

0

Jun

.200

1

Dec

.200

1

Jun

.200

2

Dec

.200

2

Jun

.200

3

Dec

.200

3

Per

cen

tag

e ch

ang

e

Depressed sales

ABS Data

Profits before tax - Printing

-14.0

-12.0

-10.0

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

Dec

.199

3

Jun

.199

4

Dec

.199

4

Jun

.199

5

Dec

.199

5

Jun

.199

6

Dec

.199

6

Jun

.199

7

Dec

.199

7

Jun

.199

8

Dec

.199

8

Jun

.199

9

Dec

.199

9

Jun

.200

0

Dec

.200

0

Jun

.200

1

Dec

.200

1

Jun

.200

2

Dec

.200

2

Jun

.200

3

Dec

.200

3

Per

cen

tag

e ch

ang

e

Booming profits? Read the fine print

ABS Data

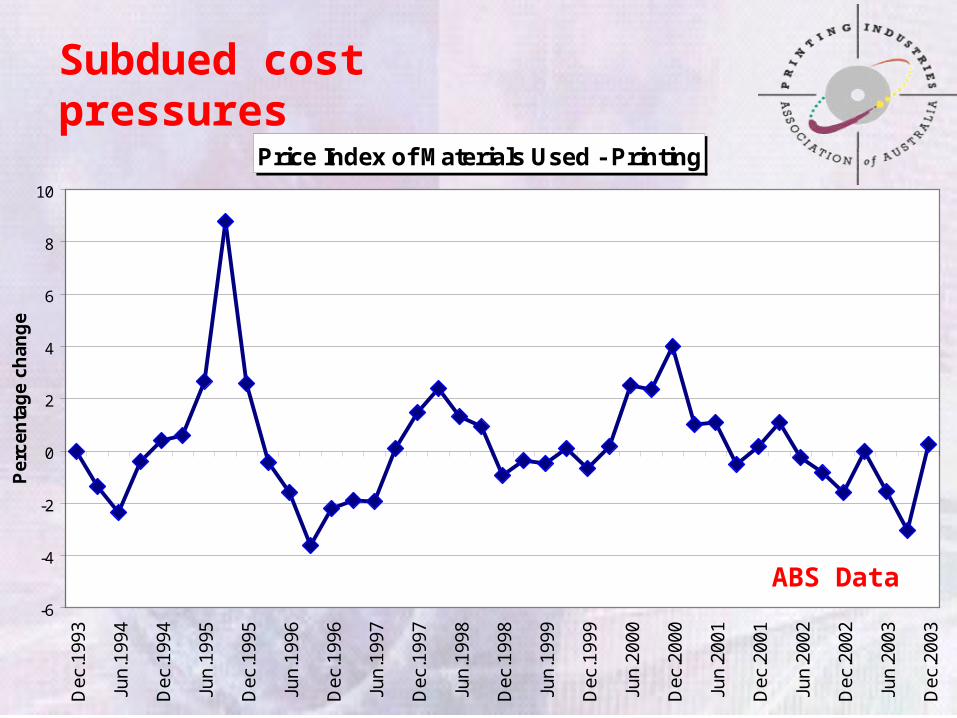

Price Index of Materials Used - Printing

-6

-4

-2

0

2

4

6

8

10

Dec

.199

3

Jun

.199

4

Dec

.199

4

Jun

.199

5

Dec

.199

5

Jun

.199

6

Dec

.199

6

Jun

.199

7

Dec

.199

7

Jun

.199

8

Dec

.199

8

Jun

.199

9

Dec

.199

9

Jun

.200

0

Dec

.200

0

Jun

.200

1

Dec

.200

1

Jun

.200

2

Dec

.200

2

Jun

.200

3

Dec

.200

3

Per

cen

tag

e ch

ang

e

Subdued cost pressures

ABS Data

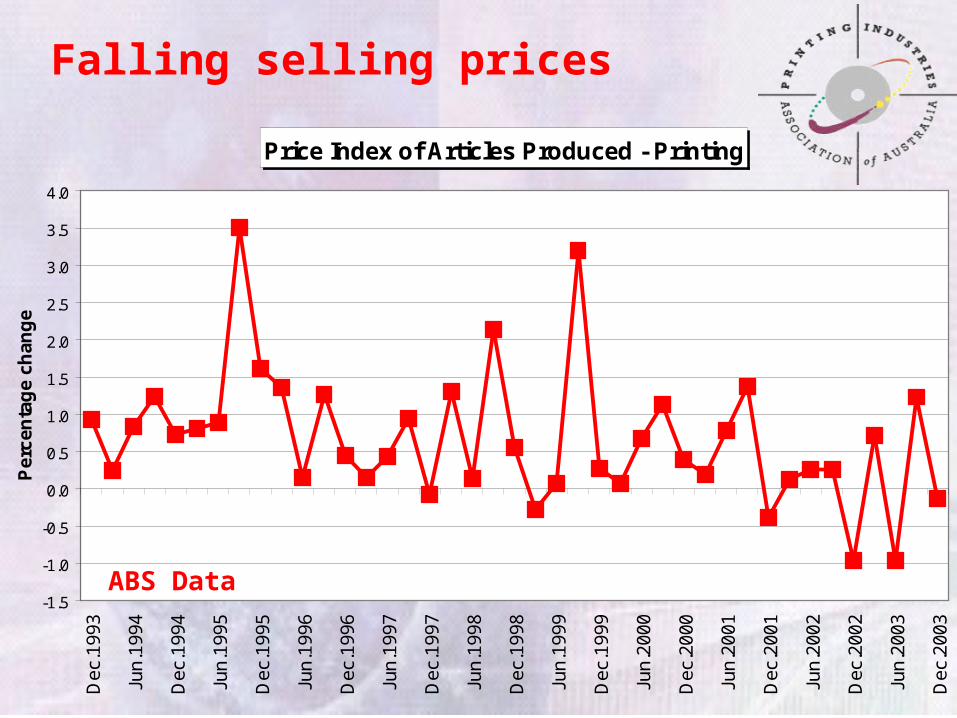

Price Index of Articles Produced - Printing

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Dec

.199

3

Jun

.199

4

Dec

.199

4

Jun

.199

5

Dec

.199

5

Jun

.199

6

Dec

.199

6

Jun

.199

7

Dec

.199

7

Jun

.199

8

Dec

.199

8

Jun

.199

9

Dec

.199

9

Jun

.200

0

Dec

.200

0

Jun

.200

1

Dec

.200

1

Jun

.200

2

Dec

.200

2

Jun

.200

3

Dec

.200

3

Per

cen

tag

e ch

ang

e

Falling selling prices

ABS Data

Price Index - Printing

-5.0

-3.0

-1.0

1.0

3.0

5.0

7.0

9.0

Dec

.199

3

Jun.

1994

Dec

.199

4

Jun.

1995

Dec

.199

5

Jun.

1996

Dec

.199

6

Jun.

1997

Dec

.199

7

Jun.

1998

Dec

.199

8

Jun.

1999

Dec

.199

9

Jun.

2000

Dec

.200

0

Jun.

2001

Dec

.200

1

Jun.

2002

Dec

.200

2

Jun.

2003

Dec

.200

3

Pec

ren

tag

e ch

ang

e

Articles producedMaterials used

Margins once again tighten

ABS Data

Business Expectations - Printing

-20

-10

0

10

20

30

40

50

60

D'9

3

J'94

D'9

4

J'95

D'9

5

J'96

D'9

6

J'97

D'9

7

J'98

D'9

8

J'99

D'9

9

J'00

D'0

0

J'01

D'0

1

J'02

D'0

2

J'03

D'0

3

Bal

ance

%

Business expectations remain positive

Printing Industry Trends data

Capital Expenditure Intentions - Printing

-15

-10

-5

0

5

10

15

20

25

30

D'9

3

J'94

D'9

4

J'95

D'9

5

J'96

D'9

6

J'97

D'9

7

J'98

D'9

8

J'99

D'9

9

J'00

D'0

0

J'01

D'0

1

J'02

D'0

2

J'03

D'0

3

Bal

ance

%

Investment intentions strengthen

Printing Industry Trends data

Capacity Utilisation Index

50

60

70

80

90

100

Dec

Q94

JunQ

95

Dec

Q95

JunQ

96

Dec

Q96

JunQ

97

Dec

Q97

JunQ

98

Dec

Q98

JunQ

99

Dec

Q99

June

Q00

Dec

Q00

JunQ

01

Dec

Q01

JunQ

02

Dec

Q02

JunQ

03

Dec

Q03

Per

cen

t

Utilisation rates improve

Printing Industry Trends data

Primary Barrier to Increased Production - Orders

40

45

50

55

60

65

70

75

80

85

90

95

100

D'9

3

J'94

D'9

4

J'95

D'9

5

J'96

D'9

6

J'97

D'9

7

J'98

D'9

8

J'99

D'9

9

J'00

D'0

0

J'01

D'0

1

J'02

D'0

2

J'03

D'0

3

Per

cen

t

Lack of orders less of a problem

Printing Industry Trends data

Level of Production

-50

-40

-30

-20

-10

0

10

20

30

40

50

60

D'00 M'01 J'01 S'01 D'01 M'02 J'02 S'02 D'02 M'03 J'03 S'03 D'03 M'04

Bal

ance

%

ActualExpected

Production improves

Printing Industry Trends data

Level of Sales

-50

-40

-30

-20

-10

0

10

20

30

40

50

D'00 M'01 J'01 S'01 D'01 M'02 J'02 S'02 D'02 M'03 J'03 S'03 D'03 M'04

Bal

ance

%

ActualExpected

So does sales

Printing Industry Trends data

Selling Prices

-40

-30

-20

-10

0

10

20

30

D'00 M'01 J'01 S'01 D'01 M'02 J'02 S'02 D'02 M'03 J'03 S'03 D'03 M'04

Bal

ance

%

ActualExpected

Selling prices fall

Printing Industry Trends data

Net Profits

-60

-50

-40

-30

-20

-10

0

10

20

30

40

D'00 M'01 J'01 S'01 D'01 M'02 J'02 S'02 D'02 M'03 J'03 S'03 D'03 M'04

Bal

ance

%

Actual Expected

Profits improve

Printing Industry Trends data

Number of Outstanding Debtors

0

5

10

15

20

25

30

35

40

D'00 M'01 J'01 S'01 D'01 M'02 J'02 S'02 D'02 M'03 J'03 S'03 D'03 M '04

Bal

ance

%

ActualExpected

Debtors profile worsens

Printing Industry Trends data

Profit Margin Index

12.6

8.5

3.3

-2.1

-7.4

13.0

7.9

2.4

-1.9

-8.6

11.7

7.5

3.5

0.2

-7.5

-10.0

-5.0

0.0

5.0

10.0

15.0

Highest 10% Highest 25% Median Lowest 25% Lowest 10%

Per

cen

t

200020012002

Low margins

Benchmarking data

ROTA

20.8

14.9

5.5

1.2

-11.0

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

Highest 10% Highest 25% Median Lowest 25% Lowest 10%

Per

cen

t

For many printing ≠ good returns

Benchmarking data

Sales Index

0

20

40

60

80

100

120

140

160

Highest 10% Highest 25% Median Lowest 25% Lowest 10%

Per

cen

t

200020012002

Benchmarking data

Up for some, down for others

Value Added Component of Sales

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

Highest 10% Highest 25% Median Lowest 25% Lowest 10%

Per

cen

t

The key to profitability

Benchmarking data

Chargeable Proportion of Direct Labour Costs

0

10

20

30

40

50

60

70

80

90

100

Highest 10% Highest 25% Median Lowest 25% Lowest 10%

Per

cen

t

The higher the better

Benchmarking data

Effective Capacity Utilisation Rates

19

14

9

63

51

24

13

54

30

20

14

9

29

47

16

0

10

20

30

40

50

60

70

Highest 10% Highest 25% Median Lowest 25% Lowest 10%

Per

cen

t

pre-pressprintingbind/fin

Does idle capacity await you?

Benchmarking data

Cash flow gap – 26 days!

Cashflow Management

35

12

68

82

55

44

19

52

39

29

0

10

20

30

40

50

60

70

80

90

Highest 10% Highest 25% Median Lowest 25% Lowest 10%

Day

s

Average debtor daysAverage creditor days

Cas

h f

low

gap

Benchmarking data

INDUSTRY FORECASTSPaper and Paper Product Manufacturing

2004-2005 2005-2006

Employment -4.0 0.5

Production 0.0 2.6

Local Sales 0.1 0.9

Printing and Services to Printing

2004-2005 2005-2006

Employment 11.6 1.7

Production -0.7 1.9

Local Sales -0.6 1.8

Publishing

2004-2005 2005-2006

Employment 11.6 1.7

Production 2.5 5.2

Local Sales 2.4 4.7

Source: Econtech

• Improvements in printing industry economic conditions anticipated during 2004 • Pick up expected in advertising expenditure• 2004 is an election year• Further rationalisation and industry consolidation inevitable• Possible improvements in capacity utilisation rates• Possible reversal in labour force downsizing

Forecasts and Prospects

• Exports and import replacement efforts will remain at the mercy of currency movements• Currency probably has reached its peak and will begin to depreciate

•Capital expenditure likely to continue recent trend meaning it is unlikely to reach past peaks•Selling prices to continue to be driven down for traditional areas of printing • Targeted customisation campaigns to continue to overtake mass marketing campaigns• Benchmarking takes off!!!

Forecasts and Prospects

Compared to 2003 how will 2004 be?• Good• Average• Bad

Industry Expectations:How well are we going to do?