journal reinsurance - dla piper

TRANSCRIPT

Journalof

Reinsurance

Winter 2011 Vol. 18 No.1

Feature Articles

Troubled Horizon? The Insurance and ReinsuranceImplications of the Deepwater Horizon Oil Spill Disaster

The Once and Future New York Insurance Exchange

Follow the Fortunes: Decisions and Trends in 2010

Setoffs In Insurance Receiverships:Two Decades of Change

Board of theIntermediaries & Reinsurance Underwriters Association

Elizabeth GearyTransatlantic Reinsurance Company

Jodi MannG.J. Sullivan Co

Joan MartinoThomas E. Sears, Inc.

Virgil R. MaxwellAmerican Agricultural Insurance Co.

Robert MezzasalmaQBE Reinsurance Corp

Doug NuehringEMC Reinsurance Company

Brian QuinnOdyssey Re

Doug RarigArch Reinsurance

John ReinmanGuy Carpenter & Company LLC

Anne Marie RobertsBMS Intermediaries, Inc.

Matthew RoseAxiom Intermediaries, LLC

Sean RyanTrean Corporation

Michael SowaAspen Re

Joseph VaughanTowers Watson & Co.

Jeremy WallisMapfre Re

Michael WilliamsAxiom Intermediaries, LLC

PresidentFrank Bigley

Farmers Mutual Hail Co. of Iowa

Vice PresidentJames Brost

BMS Intermediaries, Inc.

Secretary/TreasurerJessica BongiornoArch Reinsurance

Immediate Past PresidentAnthony Joseph

Lloyd’s America Inc.

Directors

StaffAmy Barra

Executive Director

Elizabeth MarquezAdmistrative Assistant

CounselRobert CalinoffCalinoff & Katz

Intermediaries & Reinsurance Underwriters Association

Mission StatementTo promote professionalism and educational advancement, and toprovide a forum for the useful exchange of ideas among membercompanies.

PurposesThe purposes for which IRU, Inc. (Intermediaries & ReinsuranceUnderwriters Association) was formed are to foster and promote theinterests of those individuals, partnerships, firms, associations andcorporations who are engaged in the business of treaty reinsurance.

• To encourage an exchange of ideas among members,and to disseminate educational information for the benefit ofmembers and for the betterment of the reinsurance industry.• To promote professionalism among members.• To maintain liaison with other segments of theinsurance industry, for the discussion and debate of insuranceand reinsurance issues.• To develop and present programs on topics germane tothe fields of insurance and reinsurance.• To organize and conduct meetings for the members ofthe association.• To facilitate research into problems and issuessignificant to either the membership or the reinsuranceindustry.• To disseminate, through printed matter and otherappropriate means, general news and information concerningthe association and its members, the proceedings of theassociations meetings and programs.• To promote programs designed to increase awarenessand enhance positive image of the reinsurance industry.

Journal of ReinsuranceEditorial Board

Editor

Paul Walther, CPCU, AReReinsurance Directions, Inc.

Publications/Journal of Reinsurance Committee

Committee ChairmanJoseph Vaughan

Towers Watson & Co.

Committee MembersFrank Bigley

Farmers Mutual Hail Insurance Company of Iowa

Jerry WallisMapfre Re

General Information

The Journal of Reinsurance is an official publication of theIntermediaries & Reinsurance Underwriters Association. It ispublished quarterly in January, April, July, and October.

All opinions and views expressed in any material in theJournal of Reinsurance are those of the author(s) and do notnecessarily represent the views of the editor, the editorial staff, theIntermediaries & Reinsurance Underwriters Association or itsmembers.

Copyright © Intermediaries & Reinsurance Underwriters Association.All Rights Reserved. ISSN 1074-2948

SETOFFS IN INSURER RECEIVERSHIPS:Two Decades of Change

By

Debra J. HallStephen W. Schwab

Katherine C. Jahnke

Journal of Reinsurance/IRU

81

About the Authors: Debra J. Hall is an attorney and ARIAS-U.S. certified arbi-trator. She has also completed formal mediation training at the Strauss DisputeResolution Institute at Pepperdine Law School. Ms. Hall is the Principal ofGlobal Regulatory & Risk Consultants, providing expert witness testimony oninsurance, receivership and reinsurance matters, as well as training and regulato-ry consulting services for regulators, reinsurers, insurers and policymakers. Mostof Ms. Hall's 30-year legal career has been devoted to reinsurance, insurance andreceivership matters, involving a broad array of issues, including: collateral,setoff, claims estimation/acceleration, finite re, workers' compensation, sub-prime mortgage, property catastrophe, reinsurance contract wording and inter-pretations, and domestic and foreign regulatory matters. Ms. Hall's prior posi-tions include: Senior Vice President and General Counsel of the ReinsuranceAssociation of America (RAA); Senior Vice President and Senior RegulatoryCounsel for Swiss Re and General Counsel of the Illinois Office of the SpecialDeputy Receiver.Stephen W. Schwab is a partner in DLA Piper LLP (US) and co-chaired theFirm's Global Insurance Practice Steering Committee 2005-2010. He represents(re)insurance companies, brokers, trade organizations (and formerly regulatorsand receivers) in disputes, transactions and regulatory matters throughout theworld. Stephen has published extensively and spoken widely on a broad array of(re)insurance-related subjects. He is featured in the leading client and peerreviewed surveys of legal professionals, and is the exclusive winner of the ILOClient Choice Award 2010 in the U.S.A. Insurance & Reinsurance category.Stephen is an observer on behalf of the International Bar Association to theUniform Law Commission, Drafting Committee on the Uniform International

82

Setoffs In Insurer Receiverships: Two Decades of Change

TABLE OF CONTENTSI. INTRODUCTION 84II. SETOFFS IN THE UNITED STATES 85

A. Quick Review of the Basics 85B. Historical Foundation 87C. Two Decades of Statutory Setoff Developments in

the U.S. 88i. NAIC Adoption of Setoff Restrictions

88ii. Early Adoption of NAIC Amendments and

Alternatives 89D. Two Decades of Judicial Determinations - Issue by

Issue 94i. Acquired Setoffs 94ii. Affiliate Setoffs 95

Choice of Court Agreements Act (2009-present). He is also Past Chair (2006-07),American Bar Association, Excess, Surplus Lines and Reinsurance Committee.

Katherine Jahnke is a third year law student at Chicago-Kent College of Law.She was a 2010 summer associate in DLA Piper's Chicago office, working witha number of the firm's practice groups, including the insurance group. Ms.Jahnke serves as an Executive Articles Editor for the Chicago-Kent Law Reviewand Managing Editor for the Chicago-Kent Journal of International andComparative Law.

Abstract: Twenty years ago, the US was in the grips of a crisis in insurersolvency following a record number of insurer failures. Congress issued a reportblaming, in part, lax regulation of the business of reinsurance. Regulators andreceivers began restricting the exercise of setoffs. They changed the setoffprovisions in the NAIC model receivership law and state statutes, and deniedlegitimate assertions of setoffs by reinsurance counterparties. In 1991, two of theauthors published an article about what appeared to be a bona fide revolution inreceivership setoff law and practice. They return here to survey the results.

Journal of Reinsurance/IRU

83

iii. Arbitration: Arbitrability of Setoff Disputesand the Propriety of Setting Off Arbitration Awards 96

iv. Attorney Fees and Court Costs 98v. Contingent Claims 99vi. Contingent Commissions 100vii. Different Contracts 101viii. Guaranty Associations 101ix. Insolvency Clause 102x. Interest 103xi. Mutuality of Time 103xii. No Statute, No Setoff 104xiii. Oral Contract 105xiv. Pools and Fronting 105xv. Premium 106xvi. Principal-Agent 108xvii. Rehabilitation 109xviii. Salvage and Subrogation 110xix. Statutory Amendment and Limitation-

Retroactivity 110xx. Voidable Preference 111xxi. Waiver by Integration/Merger Clause

112III. CONCLUSION 112

84

Setoffs In Insurer Receiverships: Two Decades of Change

I. INTRODUCTION

The mere passage of time has not diminished the importanceof the question. The circumstances in which setoffs mayapply remains a critical issue for cedents, reinsurers andinsurance company runoff1 administrators and receivers.2

The issue is of particular importance to those charged witheither the runoff of companies that have discontinued activeunderwriting or the administration of receivership estates. Inthe case of runoff or of solvent rehabilitation receivership,setoffs deprive the company of funds that otherwise would beused for the payment of administrative expenses and interimclaims payments that are so necessary to avoid insolvency.For a company declared to be insolvent, setoffs deprive theestate of receivables that would be used to pay the insolvent'sinsureds or to reimburse state guaranty funds for paymentsadvanced to insureds and claimants. Setoffs are equallyimportant to active cedents and reinsurers who are eager tominimize the loss sustained from trading with a financiallytroubled partner, regardless whether that partner is in runoff,rehabilitation or liquidation. Given these conflicting interests,the proper application of setoffs is not an issue susceptible toeasy resolution.

Twenty years ago, insurance company regulators andreceivers were proposing changes in national model and statestatutes to delimit the application of set-offs. The authorsposited3 that the proposed changes amounted to a "revolu-tion." In the intervening years, the National Association ofInsurance Commissioners (NAIC) and numerous states went

Journal of Reinsurance/IRU

85

ahead and changed the codified law of setoff, while manycourts redrew or retraced the lines for its application. Thisarticle briefly traces the major developments in the UnitedStates, and assumes that the reader is sophisticated in thebusiness and law of insurer insolvency and reinsurancegenerally. Whether, in fact, a "revolution" occurred will beaddressed in a later piece that fully analyzes the changessurveyed here, and more. That issue aside, the developmentsmerit careful consideration because they reveal a continuedfocus on the policy implications of setoff as a driving force inthe evolution of setoff law.4

We begin with a quick review of setoff basics, chart the courseof significant legislative developments, and survey a numberof (but not all) judicial determinations on an issue-by-issuebasis.

II. SETOFFS IN THE UNITED STATES

A. Quick Review of the Basics

The right to assert setoff in the United States arises by statute,common law, and contract. In its simplest form, setoff is theright between two parties to net their respective debts wheneach party owes the other an obligation.5 The general rule isthat "mutual" debts and credits6 between two parties may beset off, even though they arise from different contracts ortransactions. In other words, the debits and credits of amutual account constitute cross-demands and are deemed tocompensate each other.7 In litigation or arbitration, a setoff is

86

Setoffs In Insurer Receiverships: Two Decades of Change

used to reduce or extinguish a plaintiff's claim.8

Setoffs encourage equitable and economically efficientbusiness transactions. On the one hand, setoff is a proceduraldevice employed to avoid multiplicity of actions.9 On theother hand, it is a substantive right designed to avoid theinjustice of requiring an insolvent's debtor to pay the fullmeasure of his obligation while receiving only a portion of theamount owed to him. In the contemporary business world,setoff promotes economy of time and efficiency of method inresolving debt between parties. As a matter of common sense,a person should not be compelled to pay one moment what hewill be entitled to recover back the next. In sum, setoff can besaid to further the two public policies that are commonlyknown as fairness and commercial necessity.10

Whereas the allowance of setoffs furthers some publicpolicies, it may conflict with other public policies. In theunique context of insolvent insurer estates, these policiesinclude the prohibition of preferences (that is, the preferentialtreatment of one creditor over another), and the guarantee ofa pro rata distribution of estate assets. There is no questionthat in some circumstances, the application of setoffprinciples works to the advantage of one particular creditor, orclass of creditors, and to the disadvantage of others. Fornearly two thousand years, however, courts and legislatureshave resolved the tension between these competing publicpolicies in favor of setoffs.11 Today, setoff remains a specieof lawful preference.12 In economic terms, setoff is a form ofsecurity permitted by law.13

Journal of Reinsurance/IRU

87

Setoff is a ubiquitous concept. Our focus here is largely onexercise of the right of setoff between sophisticated insurersand reinsurers, and the effect that those rights have on partiesaffected by the discontinuation of business as usual. Whilethere is a well-developed body of law on setoff in other areasof insurance law, we do not address them here; e.g., setoffs inrespect of uninsured/underinsured motorist coverage.

B. Historical Foundation

American law has preserved setoff as a matter of policy fromthe earliest days because, inter alia, it helps curtail the multi-plicity of actions.14 This policy was first reflected in coloniallegislation enacted in 1645.15 American court-made law ofsetoff applicable to insurer insolvencies began to develop inthe late 1800s.16 The U.S. Supreme Court first recognized theright in insurer insolvencies in 1873.17

Congress incorporated the common law right of setoff in thefederal bankruptcy law beginning in 1800.18 Becauseinsurance companies have long been excluded from theoperation of federal bankruptcy laws, however, the applica-tion of setoffs in insurer insolvency proceedings developedlargely as a matter of state law.19 States began to enactprocedures for the dissolution of insurers in the nineteenthcentury,20 and statutory guarantees of the right of setoff insuch proceedings first appeared in 1909.21 Since then, stateshave codified many of the well-developed setoff rules thatexisted at common law into their insurer insolvencystatutes.22

88

Setoffs In Insurer Receiverships: Two Decades of Change

At the time of our prior article, all but seven U.S. states andterritories had codified the right of setoff in insurer insolven-cy proceedings.23 Today, every U.S. state and territory thatregulates the business of insurance has a statutory setoffprovision.24

C. Two Decades of Statutory Setoff Developments in theU.S.

The application of setoffs in insurer insolvencies remains acontroversial issue among both regulators/receivers and theinsurance industry.25 Twenty years ago, regulators andreceivers were struggling with a spate of massive insurerfailures and sought to enhance the assets in their estates byrestricting the application of setoffs in respect of reinsurancerecoverables. Such recoverables are often the largest asset ofan estate. When the courts held the line against suchadvances,26 these state actors moved their battle to the NAICand their domestic state legislative chambers.

i. NAIC Adoption of Setoff Restrictions

The NAIC first adopted a model insurer receivership law in1977.27 It contained a rather simple setoff provision in Section29. The section required setoff of mutual debts and credits,provided that the counterparty to the insolvent insurer (i) wasentitled to share in the estate's assets, (ii) had not purchasedthe right "with a view to its being used as a setoff," (iii) wasnot seeking to exercise an affiliate's right or a right against theinsurer's affiliate, (iv) was not seeking to set off against an

Journal of Reinsurance/IRU

89

assessment.

In April 1989, following three years of study and debate, asubgroup of the NAIC proposed amendments to Section 29.28

The Subgroup's amendments were the most comprehensive todate, including deletion of references to counterclaims,allowance of setoffs arising out of different contracts, anddenial of setoffs between affiliates. The Subgroup alsoproposed that the receivers provide reinsurers withaccountings of outstanding debts, and that only claims whicha cedent had paid could be set off. This proposal sparkedintense debate and spawned numerous counterproposals, bothfrom regulators/receivers and from the insurance industry.29

Despite the intense controversy, the NAIC adopted theseamendments to the Model Act in 1990.30

Among the more controversial amendments to the NAICmodel law is the "assumed/ceded" restriction. Adopted in1993,31 this provision prohibits setoff of obligations betweena debtor and the insolvent insurer that arise from businesswhich is "both ceded to and assumed from" the insolventinsurer.

ii. Early Adoption of NAIC Amendments andAlternatives

Even before the NAIC adopted the controversial amend-ments, three states (Missouri, North Dakota and Nebraska),whose commissioners were at the time in NAIC leadershippositions, rushed to enact the newly developed setoff

90

Setoffs In Insurer Receiverships: Two Decades of Change

restrictions.32 The Reinsurance Association of America(RAA) responded by working with the National Council ofInsurance Legislators (NCOIL) to adopt alternativerestrictions based on industry abuses, rather than a means tomaximize insolvent insurer estate assets.33 Until this time,most, if not all Model Act setoff restrictions tracked thecommon law with respect to mutuality. The assumed/cededrestriction was a major departure from the common lawdoctrine because the focus no longer was on the nature of theparties' respective obligations and their legal capacities, butinstead the relative fairness of a transaction (viewed retro-spectively).

Focusing on the abuses that regulators/receivers were decry-ing about setoffs, the RAA and NCOIL developed whatbecame known as the "circular assumed/ceded restriction" asan alternative to the NAIC restriction.34 Instead of denyingassumed/ceded setoff (and thereby altering the transfer of riskin the marketplace), the NCOIL language limited the restric-tion to "circular" transactions35 - where one party cedes risksor liabilities to the reinsurer and the reinsurer in turn cedesback the same business to the original insurer. The NCOILModel Setoff Provision thus provided:

(B) no setoff shall be allowed in favor of anyperson where:

(6) The obligations between the person and the insur-er arise from business where either the person or theinsurer has assumed risks and obligations from the

Journal of Reinsurance/IRU

91

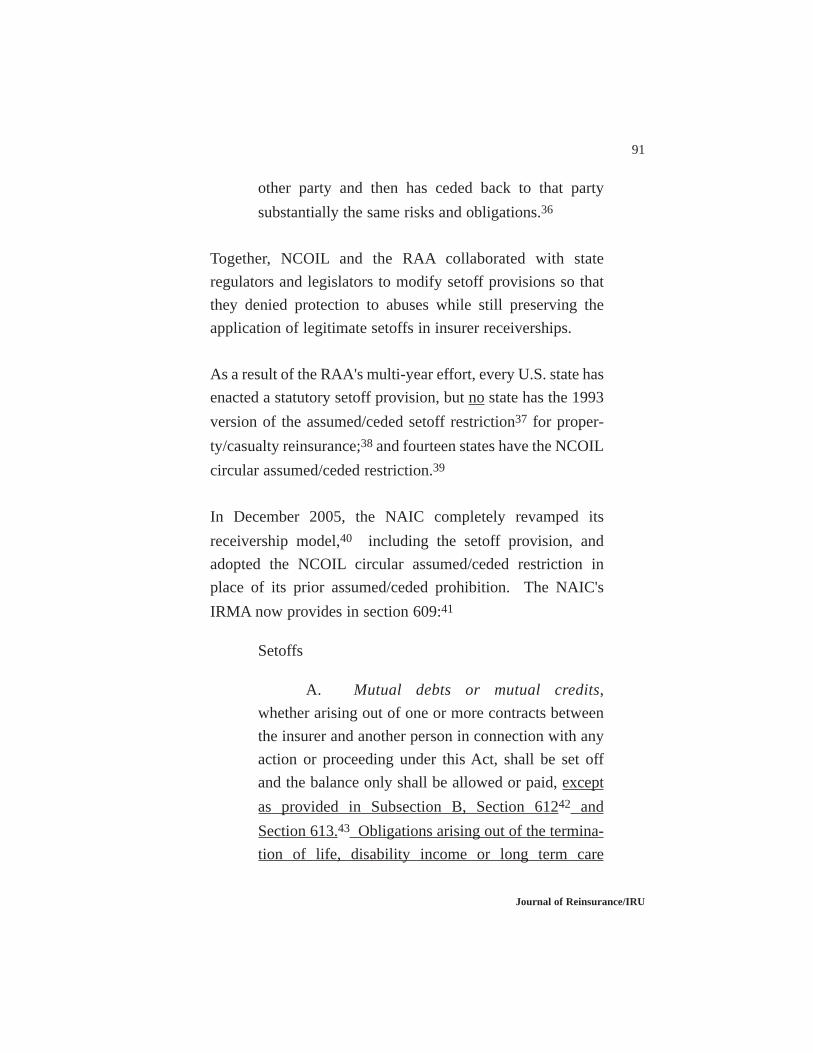

other party and then has ceded back to that partysubstantially the same risks and obligations.36

Together, NCOIL and the RAA collaborated with stateregulators and legislators to modify setoff provisions so thatthey denied protection to abuses while still preserving theapplication of legitimate setoffs in insurer receiverships.

As a result of the RAA's multi-year effort, every U.S. state hasenacted a statutory setoff provision, but no state has the 1993version of the assumed/ceded setoff restriction37 for proper-ty/casualty reinsurance;38 and fourteen states have the NCOILcircular assumed/ceded restriction.39

In December 2005, the NAIC completely revamped itsreceivership model,40 including the setoff provision, andadopted the NCOIL circular assumed/ceded restriction inplace of its prior assumed/ceded prohibition. The NAIC'sIRMA now provides in section 609:41

Setoffs

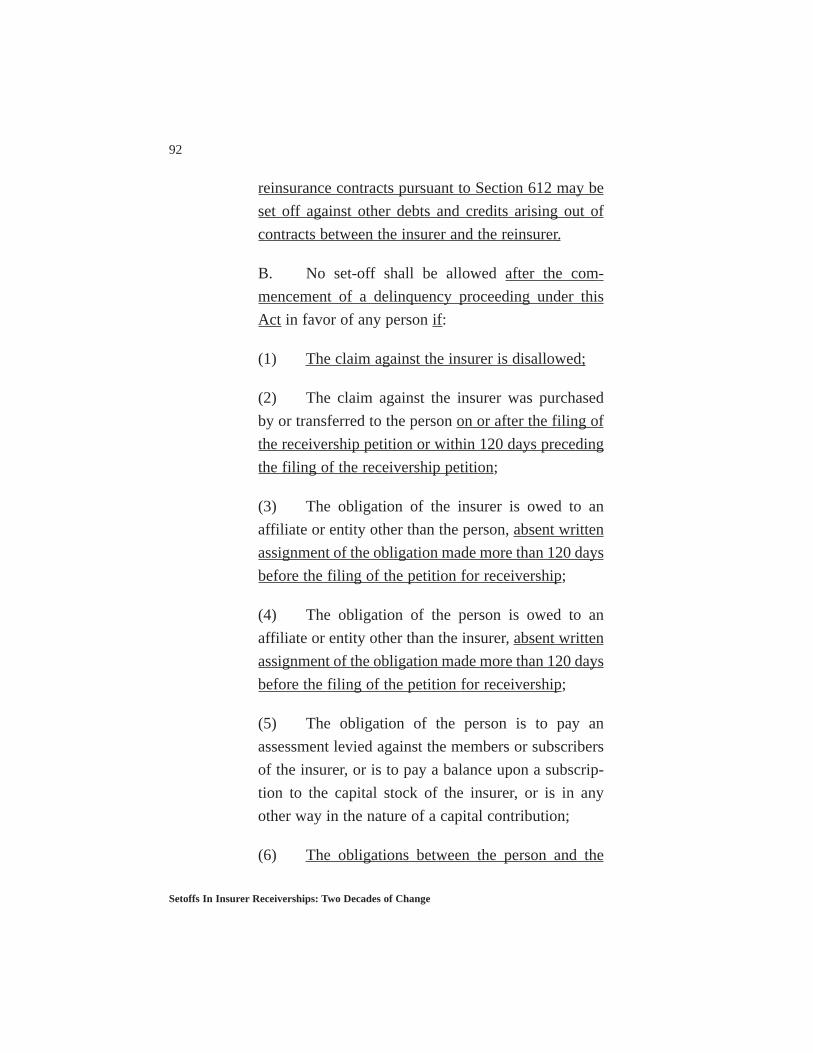

A. Mutual debts or mutual credits,whether arising out of one or more contracts betweenthe insurer and another person in connection with anyaction or proceeding under this Act, shall be set offand the balance only shall be allowed or paid, exceptas provided in Subsection B, Section 61242 andSection 613.43 Obligations arising out of the termina-tion of life, disability income or long term care

92

Setoffs In Insurer Receiverships: Two Decades of Change

reinsurance contracts pursuant to Section 612 may beset off against other debts and credits arising out ofcontracts between the insurer and the reinsurer.

B. No set-off shall be allowed after the com-mencement of a delinquency proceeding under thisAct in favor of any person if:

(1) The claim against the insurer is disallowed;

(2) The claim against the insurer was purchasedby or transferred to the person on or after the filing ofthe receivership petition or within 120 days precedingthe filing of the receivership petition;

(3) The obligation of the insurer is owed to anaffiliate or entity other than the person, absent writtenassignment of the obligation made more than 120 daysbefore the filing of the petition for receivership;

(4) The obligation of the person is owed to anaffiliate or entity other than the insurer, absent writtenassignment of the obligation made more than 120 daysbefore the filing of the petition for receivership;

(5) The obligation of the person is to pay anassessment levied against the members or subscribersof the insurer, or is to pay a balance upon a subscrip-tion to the capital stock of the insurer, or is in anyother way in the nature of a capital contribution;

(6) The obligations between the person and the

Journal of Reinsurance/IRU

93

insurer arise out of transactions by which either theperson or the insurer has assumed risks and obliga-tions from the other party and then has ceded back tothat party substantially the same risks and obligations.Notwithstanding the provisions of this subsection, thereceiver may permit setoffs if in his or her discretion asetoff is appropriate because of specific circumstancesrelating to a transaction;

(7) The obligation of the person arises out of anyavoidance action taken by the receiver; or

(8) The obligation of the insured is for the pay-ment of earned premiums or retrospectively ratedearned premiums in accordance with Section 613.

C. The receiver may avoid pursuant to Sections604,45 60546 and 606,47 and subject to defenses underthose sections any setoff that occurred prior to thecommencement of the delinquency proceeding underthis Act when the setoff would otherwise be disal-lowed pursuant to subsection B of this section.

A Drafting Note explains: "It is the intent of the drafters, withrespect to Subsections B(3) and B(4), to deny setoffs betweencompanies who are affiliated so as to not allow one companyto use setoffs of another affiliate. Contractual provisionscontrary to this intent would not be effective."48

94

Setoffs In Insurer Receiverships: Two Decades of Change

D. Two Decades of Judicial Determinations - Issue byIssue

During the legislative metamorphosis, the courts resolvedindividual setoff disputes between (re)insurance contractorsand their financially troubled counterparties. We addressbelow key issues that courts decided, organized in alphabeti-cal order by the name or type of setoff or issue in dispute.

i. Acquired Setoffs

Mergers and acquisitions are a common occurrence in the(re)insurance business community. May the acquirer assertthe setoff rights of its target as against their mutual counter-party?

The issue of acquired setoffs came before the VirginiaSupreme Court in 1997 during the Fidelity Bankers LifeInsurance Company receivership proceedings. Swiss Re LifeCompany America (Swiss Re) attempted to set off amounts itowed under a treaty it entered into with Fidelity againstamounts Fidelity owed to Swiss Re under integrated reinsur-ance treaties that had Fidelity as the indemnified party forsome of the policies.49 Swiss Re entered into the Fidelitytreaty in December 1990, Fidelity went into receivership inMay 1991, and Swiss Re acquired the integrated treaties inJune 1991.50 At that time, the Virginia Insurance Codeprohibited the setoff of debts "acquired for the purpose ofobtaining a set off."51 Because Swiss Re entered into theintegrated treaties after Fidelity was in receivership, the court

Journal of Reinsurance/IRU

95

denied the setoff. The court noted that the obligations weredifferent from those under the Fidelity treaty and so reasonedthat the treaties lacked mutuality.52 The court thus ignoredSwiss Re's "purpose" in obtaining the later integrated treaties.

ii. Affiliate Setoffs

May a reinsurance counterparty assert the setoff rights of anaffiliate against their common counterparty? In PrudentialReinsurance Co. v. Superior Court,53 the California SupremeCourt denied a setoff between Prudential's subsidiary,Gibralter, and the insolvent Mission Insurance Companies.Prudential reinsured five Mission entities and MissionInsurance Company or Mission National Insurance Companyreinsured Prudential and Gibraltar. Gibraltar was not a partyto or a principal under any of the contracts reinsuringMission.54 Similarly, three Mission companies were notprincipal reinsurers of Prudential. Finding a lack of mutuality"in the absence of an express mutual agreement that thesubsidiary would be deemed a mutual debtor-creditor of theparent."55 the court refused to allow a setoff between theprincipals and subsidiaries. Finding a lack of mutuality "inthe absence of an express mutual agreement that the sub-sidiary would be deemed a mutual debtor-creditor of the par-ent,"55 the court refused to allow a setoff between the princi-pals and subsidiaries. This portion of the court's opinionlies under the heading: "Mutuality of Identity andCapacity."56 The court thus recognized yet another form ofmutuality.

96

Setoffs In Insurer Receiverships: Two Decades of Change

Three years later, the California Court of Appeals againdenied affiliate setoffs in Mission Insurance Company v.Imperial Casualty and Indemnity Company,57 this timedespite language in the treaties referring to the parent andsubsidiaries collectively with regards to offsets. Missionreinsured Imperial and Imperial reinsured Mission and two ofits subsidiaries.58 During Mission's liquidation proceedings,Imperial sought to offset the amounts it owed the Missionsubsidiaries by the amount Mission owed it.59 The courtdenied the setoff, holding that "setoffs are limited to mutualdebts and credits between principal reinsurers."60 The debtowed to Mission's subsidiaries lacked mutuality with the debtowed by Mission; therefore, a setoff was prohibited.61

iii. Arbitration: Arbitrability of Setoff Disputesand the Propriety of Setting Off Arbitration Awards

Arbitration is often the chosen means of resolving reinsurancedisputes, but its enforceability against a party in receivershiphas received much attention in courts and commentary.62 Thecorollary setoff issues are whether setoff disputes between acompany in receivership and a counterparty are arbitrable,and whether awards entered in an arbitration may be set off inrespect of claims made against or by an insurer in receiver-ship.

The first issue was addressed in Selcke v. New EnglandReinsurance Company.63 The cedent, Centaur, was inrehabilitation and claimed that its reinsurer, New England Re(NERCO), owed it reinsurance indemnity payments. NERCO

Journal of Reinsurance/IRU

97

claimed that Centaur in turn owed NERCO and its affiliatesnearly ten times the amount. When Centaur sued, NERCOmoved to stay pending arbitration and the district court deniedthe motion. The Seventh Circuit Court of Appeals reversed,reasoning that the statutory setoff right was an implied term ofany agreement with an insolvent insurer and so covered by thearbitration clause in the parties' agreement, which coveredinterpretive disagreements. Recognizing that the source ofthe right was statutory, and acknowledging that claims whicharise out of the bankruptcy law are assumed to be not arbitra-ble,64 the court noted that no one had suggested that ajudicial determination would produce a result fairer to othercreditors and so the matter could not be arbitrated. As a result,the court held: "[a]ll things considered, we think the disputeover setoff is within the scope of the arbitration clause, thoughjust barely."65

The second issue was addressed when the California Court ofAppeal reached a contrary result on the first, in an unpub-lished decision in Garamendi v. California CompensationInsurance Company.66 The receivership court had entered aseries of orders in respect of the insolvent cedents. One orderdeclared that "no payment of any award or judgment obtainedagainst [the receiver] or against any of the companies them-selves, shall be paid in whole or in part out of any assets of theestates [without court approval]."67 Another order enjoinedall persons from "exercising any right of set-off" withoutleave of court.68 Thus, the court had deprived the arbitratorsof jurisdiction over the subject and remedy.69 Accordingly,the appellate court held that the arbitrators' award of attorneys

98

Setoffs In Insurer Receiverships: Two Decades of Change

fees and fraud damages in connection with a declaration ofrescission in favor of the reinsurers could not be set offagainst premium that otherwise would be due the cedents as aresult of the rescission. Accordingly, the appellate court heldthat the arbitrators' award of attorneys fees and fraud damagesin connection with a declaration of rescission in favor of thereinsurers could not be set off against premiums that other-wise would be due the cedents as a result of the rescission.

iv. Attorney Fees and Court Costs

Can an award of attorneys' fees and costs entered in favor ofa reinsurer in a post-liquidation proceeding be set off againstobligations otherwise owed to an insolvent cedent? InGaramendi, the court said "no," because the liability wasimposed by operation of law post-liquidation and no pre-liquidation debt could exist within the meaning of the setoffstatute; nor could the liability arise from the reinsuranceagreement itself.70 This is not to say, however, that a post-liquidation agreement between the parties would not dictate adifferent result, or that a court cannot permit setoff for reasonsaside from a statutory receivership provision.

Whether a court retains the equitable power to permit a setoffof attorneys' fees and costs that is not provided for by statuteis a unique question that a UK court addressed in the contextof an ongoing reinsurance litigation. National Company forCo-operative Insurance v. St. Paul's Reinsurance Company,71

involved a dispute that arose outside the receivership context,but the court's decision may portend an exception in Americansetoff jurisprudence some time in the future. The cedent's

Journal of Reinsurance/IRU

99

reinsurers were wrongfully induced to settle a claim withoutthe cedent's knowledge through untruthful statements madeby the reinsurance broker, so that the cedent would settle withits insured. The cedent sued to compel payment andprevailed. When the reinsurers later prevailed in a courtaction focused on the broker's action, they sought to assert asetoff of their attorneys' fees and court costs incurred inprevailing as against moneys they owed under the settlement.The parties made various arguments based on this distinctionbetween legal and equitable setoff, but the court exercised its"inherent jurisdiction...to lay down the terms for set-off onsuch terms as it considers just and equitable" and allowed thesetoff.72 The key point here is the notion that a court retainsjurisdiction to permit a "judicial" or litigation costs setoff.

v. Contingent Claims

One of the "hot button" reinsurance issues in insurer receiver-ships over the last 20 years has been the "contingent claim"issue,73 and so it was only a question of time before thepropriety of asserting a contingent claim in setoff would beaddressed to in the courts.

An Illinois state appellate court decided the issue in Clark v.Cannon Steel Erection Company.74 Cannon Steel had becomea member of a group self-insured workers compensation fundand agreed to pay both premiums and assessments. When thefund was declared insolvent, the receiver pursued action tocollect from Cannon Steel. Cannon Steel sought to set off

100

Setoffs In Insurer Receiverships: Two Decades of Change

against its payment obligations its costs of defending pendingthird party claims and payments made in connection withpending workers compensation claims, as to both types ofwhich claims its liability had not been established. Thereceivership court denied the setoff and the appellate courtaffirmed, reasoning that setoff is available only where thedebts are mutual, mature and capable of being applied with-out intervention of a court to estimate them.75

A Canadian court weighed in on the issue three years later andreached a similar result. Section 73 of the Canadian Winding-Up and Restructuring Act "require[d] that there be a proceed-ing for the recovery of debts due or accruing due to acompany at the commencement of the winding up of thecompany."76 On that basis, the Ontario Superior Court denieda setoff between Swiss Re and Reliance Insurance (which wasplaced into liquidation in 2001), holding that Swiss Re failedto establish that there were any debts due to Reliance on thedate of the Reliance winding up application.77 Because thetreaties between the companies only "describe[d] a potentialliability," the debt was not due; therefore, Swiss Re's request-ed setoff was denied.78

vi. Contingent Commissions

Another calamitous issue that eventually spilled over into therealm of setoffs was the purported right of insurance brokersto receive "contingent commissions." The issue was mostrecently addressed in McRaith v. Burns & Wilcox, LTD.79 InMcRaith, the receiver of Legion Indemnity Company sued

Journal of Reinsurance/IRU

101

B&W to recover premiums that admittedly were both due andheld in a fiduciary capacity. The parties' agreement entitledB&W to payment of a "contingent commission" based uponloss experience, and contained a clause authorizing eitherparty to "offset" against B&W's "compensation" any claims"arising out of " the agreement.80 B&W claimed that it wasentitled to set off against the premium obligation amounts itwould be due for contingent commission. The court, howev-er, rejected the setoff because B&W could not sustain itsburden of proving that the commission was either "absolutelyowing but not presently due," or "accrued but as yetunliquidated" within the meaning of the Illinois insurerreceivership setoff provision.

vii. Different Contracts

The fact that debts and credits arise from different contractshas not prevented setoffs in many cases.81 This was a keyissue in the early 1990s, and landed in the highest courts ofNew York82 and California.83 The New York Court ofAppeals expressly rejected an insurer liquidator's argumentthat for debts and credits to be mutual they had to arise fromthe same contractual transaction. Although the New Yorkstatute did not expressly say whether debts and credits mustarise from the same transaction to be eligible for a setoff, thecourt looked at the legislative history that distinguished offsetfrom recoupment.84 Because the New York courts andlegislature recognized a distinction between recoupment andoffset, with debts arising out of separate transactions allowed

102

Setoffs In Insurer Receiverships: Two Decades of Change

to be setoff but not subject to recoupment, the court rejectedthe liquidator's "same transaction" rule.85

viii. Guaranty Associations

Guaranty associations administer funds to cover certainobligations of insolvent insurers.86 Do setoffs apply to reducethe amounts due from guaranty associations in respect ofcovered claims? The answer turns on the language of theindividual state guaranty association statute, but courts havereached different results when construing the same words.

In Ventulett v. Maine Insurance Guaranty Association,87 theSupreme Judicial Court of Maine held that a claimant mustoffset the workers compensation benefits he has receivedagainst what the guaranty association otherwise would pay ona tort claim for the same injuries brought by the claimantagainst the third party tortfeasor whose liability insurer hasbecome insolvent. The Maine statute provided that "[a]nyperson having a claim against an insurer under any provisionin an insurance policy, other than that of an insolvent insurer,shall be required to exhaust first the person's right under thepolicy."88 But in Alabama Insurance Guaranty Association v.Magic City Trucking Service, Inc.,89 the Alabama SupremeCourt addressed a state statute virtually identical to Maine'sand held that workers compensation benefits which paid aninjured party's medical expenses were not "insurancebenefits" available for the guaranty association to set offagainst the claim.

Journal of Reinsurance/IRU

103

ix. Insolvency Clause

In the 1990s, liquidators frequently argued that the statutorilyrequired contractual insolvency clause - providing thatreinsurance is payable "without diminution because of...insolvency" - precludes setoff.90 The courts most often reject-ed these arguments, holding that these clauses are intended to"provide the liquidator with the same rights and obligations ofthe insolvent insurer pursuant to the terms of the reinsurancecontract,"91 not to "destroy a reinsurer's right to offset."92

x. Interest

Most creditors do not receive any payment of interest on theirclaims against an insolvent insurer. Are there any circum-stances in which interest may be set off?

The Eighth Circuit allowed prejudgment interest in a disputedsetoff proceeding.93 Transit Casualty Company (Transit) andFortress Re, acting on behalf of Selective Insurance Company(Selective), entered into two sets of reinsurance contractsbefore Transit went into receivership.94 Under the contracts,Transit and Selective owed each other money.95 When theTransit receiver brought an action against Selective, Selectiveraised setoff as an affirmative defense.96 After upholdingSelective's affirmative defense, the court nevertheless upheldthe district court's award of prejudgment interest to Transit,payable from the date Transit made demand for paymentunder the contracts.97 The court found that Transit's claims

104

Setoffs In Insurer Receiverships: Two Decades of Change

were liquidated on the date of its demand, entitling it to pre-judgment interest under the Missouri Code.98

xi. Mutuality of Time

Another oft repeated argument of receivers in the 90s was thatsetoffs should be denied due to a lack of mutuality of time.99

In Prudential Reinsurance, the Liquidator also argued that the"debts owed by the reinsurers to Mission (namely, paymentson insured losses) are post-liquidation debts, while thoseowed to the reinsurers by Mission (namely, past-duepremiums) are pre-liquidation debts;"100 therefore, the claimslacked mutuality of time. The court rejected this argument,holding that "mutuality depends on whether the debts were inexistence before insolvency, not whether individual claimsarose before the date of insolvency."101 The debts forpayments on insured losses arose from contracts executedprior to liquidation and were therefore pre-liquidationdebts.102 As such, there was mutuality of time between thedebts, entitling them to setoff.103

xii. No Statute, No Setoff

What happens if a state's receivership code does not contain asetoff provision? Does the common law of setoff (equitableor legal) apply? In Bluewater Insurance Limited v.Balzano,104 the Colorado Supreme Court answered "no."After surveying reinsurance law and business practices, thecourt's decision turned on the statutory requirement that all

Journal of Reinsurance/IRU

105

reinsurance agreements be submitted to the state insurancecommissioner for review. As a result, the court held that thecommissioner had the power to regulate reinsurance contractsby particularly prohibiting the right to set off unremittedpremiums from the amount of proceeds due on reinsuredpolicies.105 In so doing, the court dispensed with argumentsby complaining reinsurers that this holding flew in the face ofthe insolvency clause, finding instead that the clause madereinsurance less a contract of indemnity and more a contractof liability enforcement.106

xiii. Oral Contract

Is an oral contract enforceable through setoff? In an unpub-lished decision rendered in Glogower v. Miller,107 theKentucky Court of Appeals said "yes," ruling that a trial courterred when it prohibited a former employee of an insolventinsurer from introducing evidence of an alleged oral agree-ment that he asserted as a setoff against amounts he owedunder certain promissory notes.

xiv. Pools and Fronting

One of the first major setoff decisions came from the SeventhCircuit Court of Appeals in 1990 in a case involving reinsur-ance pools.108 It was a harbinger, both for many of the latercourt decisions on setoff as well as the particularly trouble-some issues arising out of pools and fronting.

106

Setoffs In Insurer Receiverships: Two Decades of Change

In Stephens v. Federal Insurance Company, the court took afunctional approach to setoffs involving insurance pools,looking "through the transactions as they appeared on the sur-face" to "determine the real facts and the true intention of theparties."109 Federal Insurance Co. (Federal) reinsured DeltaAmerica Reinsurance Company (Delta Re).110 Delta Re rein-sured a group of insurers, called the "Chubb Pool," whichFederal was a member of.111 When Delta Re went intoliquidation, the Chubb Pool filed proof of claim forms, ofwhich Federal was entitled to fifty-six percent of theamount.112 Delta Re made a demand for payment fromFederal for amounts due under their reinsurance contract, towhich Federal raised the affirmative defense of setoff.113 Thecourt allowed the setoff, rejecting the Liquidator's argumentthat the debts were not mutual.114 Looking at the Chubb PoolTreaties, the court saw that although the treaties were enteredinto by an agent of the members, "one need not look farbeneath the surface...to get to the 'real fact' that Federal isindeed a party to the Chubb Pool Treaties;" therefore, therequired mutuality existed to allow Federal's setoffdefense.115

The Eighth Circuit likewise allowed a setoff between Transitas reinsurer and Selective as a pool member, despite the factthat Fortress was the signatory for the reinsurance poolcontracts.116 Fortress acted as Selective's agent, withSelective as a "partially disclosed principal."117 As such,Selective could bring a cause of action against Transit underthe contracts.118 Therefore, there was mutuality between

Journal of Reinsurance/IRU

107

Selective and Transit, allowing Selective to set off amounts itowed under the parties' retrocession contract against amountsTransit owed under the pool contracts.119

xv. Premium

Most states preclude set off by agents against premium theyare holding, and the courts agree due to a lack of mutuality ofcapacity. The agent typically holds the premium in a premi-um funds trust account, and so in a fiduciary capacity.

In Albany Insurance Company v. Stephens,120 the issue waswhether the statutory proscription against premium setoffapplied to reinsurance premium that a cedent owed to itsinsolvent reinsurer Delta America Re. Noting that the statu-tory proscription applied to "the obligation of [a] person...topay premiums, whether earned or unearned, to the insurer,"121

the court quickly reasoned that as an insurer, the cedent was a"person" and that reinsurance is "insurance" that pays orindemnifies another. The court further reasoned that allowingsuch a setoff would prefer the cedent over other creditors, andthat denominating their claims as "recoupment" did not savethem. The fact that other jurisdictions might have ruledotherwise was of no moment to the court, in light of the"importance of viewing the set-off issue in the context of eachstate's particular statutory framework."122 Indeed, a commonlaw analysis would not lead to a different result.123

As demonstrated above, the wording of a state's statutory

108

Setoffs In Insurer Receiverships: Two Decades of Change

setoff provision most often controls the result, even when thelitigants are not in receivership. This fact is well illustrated inReliance Insurance Company v. Shriver, Inc.124 Shriver wasan intermediary that brokered insurance policies issued on thepaper of a fronting insurer for two Illinois trucking companyinsureds. Shriver held the premium in a statutorily requiredtrust account. When the insurer became financially troubled,Shriver cancelled the policies mid-term and replaced themwith Reliance paper. Shriver also exercised a contractualsetoff right and netted the unearned premium due back fromthe troubled insurer against the premium held in the trustaccount. Reliance demanded that Shriver replenish the trust.Although the first insurer was never placed into receivershipin Illinois, the trial court held that Shriver's setoff was properbecause the Illinois statutory receivership set-off provisionpermitted the exercise of contractual setoffs taken pre-receivership in respect of unearned premium due under poli-cies cancelled pre-receivership. The Seventh Circuit Court ofAppeals affirmed, based on the plain language of the statute,and rejected Reliance's lack of mutuality argument.

xvi. Principal-Agent

The mutuality issue notwithstanding, as indicated above, theEighth Circuit Court of Appeals held in Transit CasualtyCompany v. Selective Insurance Company of the Southeast125

that a "partially disclosed principal" may assert setoff under areinsurance agreement.

xvii. Rehabilitation

Journal of Reinsurance/IRU

109

Rehabilitation is fundamentally different from liquidation. Inone, the goal is the preservation of the insurer; the chief endof the other is distribution of all assets to allowed claimants,ending in the insurer's dissolution.126 Given this difference,are setoffs available in insurer rehabilitations and do theyoperate differently than in liquidations? These were the issuesin two seminal cases, one decided in Pennsylvania, the otherin Illinois.

American Mutual Reinsurance Company127 was placed intorehabilitation in February 1988. The Rehabilitator developeda plan which paid claims part in cash, part in "surplus note,"and administered claims on a quarterly basis, includingsetoffs: claims made in one quarter could be set off only toreduce the amount of recoverables due to the estate in thesame quarter. After the plan was adopted, a cedent/reinsurerchallenged the Rehabilitator's refusal to grant it the right toassert the amount of the note portion of payment received insetoff against recoverables due in the future. The receivershipcourt and the appellate court overruled the objection, reason-ing that the setoff provisions in the receivership article of thestate insurance code applied, but those provisions onlyindicated when setoff did not apply; they did not establishhow setoff should be applied in instances where it wasallowed.128

In Foster v. Mutual Fire, Marine & Inland InsuranceCompany,129 the receivership court approved a rehabilitation

110

Setoffs In Insurer Receiverships: Two Decades of Change

plan restricting set-off rights with respect to reinsurancerecoverables on claims settled and loss adjustment expensespaid post-receivership130; that is, only mature, liquidatedobligations could be set off. The Pennsylvania Supreme Courtdeclared that setoff is "an equitable remedy and accordingly,is permissive, not mandatory,"131 and upheld the plan.

Journal of Reinsurance/IRU

111

xviii. Salvage and Subrogation

The courts have denied setoff of salvage and subrogationfunds, as they are held in trust and therefore are not mutualwith debts and credits arising under reinsurance contracts.132

For example, in the Guardian Casualty Company (Guardian)liquidation proceedings, American Surety Company(American) attempted to setoff amounts it owed Guardianfrom salvage recoveries against amounts Guardian owedAmerican under reinsurance contracts.133 The court deniedthe setoff, holding that the claims between the parties lackedmutuality because they "were not held in the same right."134

xix. Statutory Amendment and Limitation-Retroactivity

What is the effect of a legislature's adoption of a setoff right?In Commissioner of Insurance v. Munich AmericanReinsurance Company, the Commissioner requested that thecourt not allow a setoff because the 1998 Massachusetts setoffamendment only applied prospectively and so could not applyto the 1989 contract between the insolvent and its reinsurer.135

The court did not apply the amendment retroactively, butinstead allowed the setoff under common law principles.136

Recognizing a long-standing common law principle of allow-ing setoffs in insurer insolvencies, the court held that the newstatute left these preexisting principles allowing setoffs toreinsurers intact.137

xx. Voidable Preference

112

Setoffs In Insurer Receiverships: Two Decades of Change

Receivers have often argued that allowing setoff prefers onecreditor over another, because the creditor who exercises thesetoff effectively recovers full dollars in respect of the claimsset off. The preference at issue in such arguments is"equitable preference," which derives from the priority ofdistribution scheme in state insurer receivership statutes. Butthere is another kind of preference which some receivers havealso asserted - "legal" preference, which results when acreditor receives payment on a debt from an insurer pre-receivership while other creditors receive less. In thosecircumstances, many state receivership codes permit thereceiver to avoid the preferential payment and recover backfrom the creditor post-receivership the payment they receivedpre-receivership. Whether the creditor may assert a setoffagainst the amount due back has also been addressed in thecourts.138

Resolution of this particular issue turns on the precise word-ing of the voidable preference statute. In Covington v.Airborne Express, Inc.,139 the state receivership statuteprovided that:

[i]f a creditor has been preferred, and afterward ingood faith gives the insurer further credit withoutsecurity of any kind, for property which becomes apart of the insurer's estate, the amount of the newcredit remaining unpaid at the time of the complaintmay be set off against the preference which wouldotherwise be recoverable from him.140

Journal of Reinsurance/IRU

113

Airborne Express provided the insolvent insurer with over$106,000 of airfreight services, and received over $97,000 inpayments.141 Airborne thereafter provided another $11,000 inservices, $4,000 pre-receivership and $7,000 post-receiver-ship.142 Airborne did not contest that the $97,000 constitutedpreferences,143 but argued that it was entitled to a setoff of thepreferences.144 In view of the plain language of the statute,the court held that Airborne was entitled only to set off the$4,000 against the $97,000.145

xxi. Waiver by Integration/Merger Clause

In Shapo v. Underwriters Management Corporation,146 theliquidator of Prestige Casualty Company sued the owner torecover under a promissory note. The owner sought a set offof moneys due him under a call option agreement. The courtheld that under both Illinois and New York law, no set offcould be taken because the note was separate from the callagreement and contained an integration clause.147 For what-ever reason, it does not appear that the court considered theIllinois receivership setoff statute.

III. CONCLUSION

In 1989, the authors observed that established rules of(re)insurance receivership setoff were teetering on the brinkof change. Regulators, receivers and legislative committeeswere challenging centuries old policies underlying setoffs andprecedent that previously had been regarded as fundamental.

114

Setoffs In Insurer Receiverships: Two Decades of Change

Endnotes:

1 "Runoff" is the term used to describe the circumstance under which aninsurer, inter alia, discontinues writing new and renewal premiums,refunds unearned premiums on in force policies and pays claims as theyare settled in the ordinary course. "Thus, a runoff of claims allows theinsurance company to conclude its business without the need of a moreexpensive and cumbersome court-ordered liquidation." Crowley v. Chait,NO. 85-2441(HAA), 2004 WL 5434953 at *2 n.2 (D.N.J. 2004). See, e.g.,215 ILCS 5/35A-30(c)(providing for a "run-off" under the supervision ofthe Illinois Director of Insurance).

2 See Stephen W. Schwab, Debra J. Anderson, Carolyn S. Reed & DavidE. Mendelsohn, Onset of An Offset Revolution: The Application of Set-Offsin Insurance Insolvencies, 95 DICK. L. REV. 449, 515 n.3 (1991) [here-inafter Offset Revolution](describing the types of receivership). The co-author of that article, Debra J. Anderson, is our co-author here, now knownas Debra J. Hall.

3 Id. at 453.

4 One measure of the continued importance of the issue is the attention iscontinues to receive from commentators. See, e.g., Robert M. Hall, DirectActions and Setoff: The Next Generation, 9-6 MEALEY'S LITIG. REP.INS. INSOLV. 9 (1997) and Setoff in Arbitration When One of the Partiesis Insolvent, 18-1 MEALEY'S LITIG. REP. INS. INSOLV. 11 (2006);Daniel P. Cunningham, United States of America, in SET-OFF LAW ANDPRACTICE 447-60 (William Johnston & Thomas Werlen, ed., 2006);Barry Ostrager & Mary Kay Vyskocil, MODERN REINSURANCE LAWAND PRACTICE 12-20, 35 (2d ed. 2000); Lia B. Royle, Reinsurers'Setoff Rights in the Insolvency Context: Recent Developments, 8-5MEALEY'S LITIG. REP. INS. INSOLV. 15 (1996); Stephen Schwartz,REINSURANCE LAW: AN ANALYTICAL APPROACH 15-20 -27(2009); Marcy B. Tanker & Stephen P. Chawaga, A Tale of Two Statutes:Application of Statutory Setoff Provisions in Insurance Insolvencies, 28

Journal of Reinsurance/IRU

115

TORT & INS. L.J. 854 (1993); Eugene Wollan, HANDBOOK OR REIN-SURANCE LAW §§ 4.11, 6.06[B], 7.04[A], [B] (2002); Special Report:Offset, 5-9 Mealey's Litig. Rep. Ins. Insolv. 8 (1993).

5 Offset Revolution, supra note 2, at 453 n.9 (citing R. Mabey, Setoff in aNon Insurance Commercial Setting 1 (unpublished manuscript 1989)).

6 See id. at 478-504.

7 Id. at 453 n.11 (citing Downey v. Humphreys, 102 Cal. App. 2d 323, 227P.2d 484 (1951)).

8 Id. n.12 (citing 4 COLLIER ON BANKRUPTCY 68.03 (J. Moore 14thed. 1978)).

9 Id. at 454 n.13 (citing William H. Loyd, The Development Of Set Off,64 U. PA. L. REV. 541, 569 (1916)).

10 Id. n.14 (citing R. Mabey, supra note 5, at 1).

11 Id. n.15 (citing P.R. Wood, ENGLISH AND INTERNATIONAL SET-OFF 271-72 (1989) [hereinafter P.R. WOOD], Scott v. Armstrong, 146U.S. 499, 511 (1892)).

12 Id. n.16 (citing Barnett Bank of Jacksonville v. State ex rel. Dep't ofIns., 507 So. 2d 142 (Fla. Dist. Ct. App. 1987), Scott v. Armstrong, 146U.S. 499, 510 (1892), and Willing v. Binenstock, 302 U.S. 272, 276(1937)).

13 Id. n.17 (citing In re Elcona Homes Corp., 863 F.2d 483, 485 (7th Cir.1988), FLA. STAT. § 631.281(4) (Supp. 1990), P.R. WOOD, supra note11, at 17, 19.)

14 Id. at 458, n. 40 (citing Loyd, supra note 9, at 553-60).

15 Id. at 458, n.41 (citing February 17, 1644-5, I HENIG'S LAWS 294).

116

Setoffs In Insurer Receiverships: Two Decades of Change

16 Id. at 459

17 Id. (discussing Sawyer v. Hoag, 84 U.S.610 (1873)).

18 Id. n. 44.

19 Id. at 460, n.49 (citing Paul v. Virginia, 75 U.S. (8 Wall.) 168 (1868),United States v. South Eastern Underwriters Ass'n, 322 U.S. 533 (1944),and McCarran Ferguson Act, Pub. L. No. 20 15, 59 STAT. 33 (codified asamended at 15 U.S.C. §§ 1011 - 1015 (1983)).

20 Id. n.50 (citing LAWS of 1851, ch. 95, § 6, contained in DENIO &TRACY'S REVISED STATUTES OF THE STATE OF NEW YORK I:1288, § 30 (1852), ILL. REV. STAT. ch. 73, paras. 84 - 92 (1874), andKimball, History and Development of the Law of State InsurerDelinquency Proceedings: Another Look After 20 Years, 5 J. INS. REG.6, 12 (1986)).

21 Id. n.51 (citing N.Y. INS. LAW § 7427 (formerly § 538) (McKinney1985), CAL. INS. CODE § 1031 (West 1972), and Downey v. Humphreys,102 Cal. App. 2d 323, 227 P.2d 484, 492 (1951)).

22 Id. n.52 (citing Sawyer v. Hoag, 84 U.S. 610 (1873), and ILLINOISSTATE BAR ASSOCIATION, ILLINOIS INSURANCE CODE ANNO-TATED 377 - 80 (1939)).

23 Id. at 462 and Appendix A at 515-20.

24 See Appendix I, infra.

25 See, e.g., Joseph T. McCullough, IV, The Upset Over Offsets, 6/89REACTIONS 34 (1989); see also Offset Revolution at 504-13.

26 See, e.g., Mission Ins. Co. v. Imperial Cas. & Indem. Co., 41 Cal. App.4th 828, 48 Cal. Rptr. 2d 209 (Cal. Ct. App. 1995).

Journal of Reinsurance/IRU

117

27 Offset Revolution, supra note 2, at 460 (citing Report of the StudyGroup on Reinsurance Setoff, I NAT'L ASS'N INS. COMMISSIONERSPROCEEDINGS 238-75(1978) (hereinafter NAIC PROCEEDINGS).

28 For a discussion of the derivation of Section 29, see id. at 506-08 n.327-40 and accompanying text.

29 See Id. at 508-08 n 327-40 (citing II NAIC PROCEEDINGS 346, 351,and 357 (1989)).

30 Id. at 460 n.56.

31 II NAIC PROCEEDINGS 633, 661 (1993).

32 1991 MO. LAWS H.B. 385, 386, 387, 389, 390, & 451; 1991 N.D.LAWS Ch. 305; 1991 NEB. LAWS 236.

33 Co-author Debra Hall was RAA Senior V.P. and General Counsel at thetime and directly involved in these nationwide efforts.

34 Members of NCOIL committed substantial time to the RAA to learn thebusiness and market effects of the NAIC action. Although developed bythe RAA, the provision became known as the NCOIL approach. In order toencourage state legislators to support the alternative as a more efficient andrationale approach to perceived abuses, NCOIL passed a resolution ofsupport in 1991. See IV NAIC PROCEEDINGS 88, 130 (1991).

35 When done at the end of a cedent's financial year to mask the insurer'sfinancial position, this practice can indeed be abusive and leaves littlemeasure of real risk transfer. Consistently, the NAIC amended itsACCOUNTING PRACTICES AND PROCEDURES MANUAL torequire that any reinsurance transaction that is reported in a financial state-ment as a reduction of liabilities or an addition to assets must involve a truetransfer of "risk." See, e.g., id., Statement of Statutory AccountingPrinciple No. 62R ¶ 10 at 62R-5 (2010); see also ACCOUNTING &

118

Setoffs In Insurer Receiverships: Two Decades of Change

REPORTING FOR REINSURANCE OF SHORT-DURATION ANDLONG DURATION CONTRACTS, Fin. Accounting Standard No. 113, §9 (Fin. Accounting Standards Bd. 1992).

36 RAA, Setoffs in COMPENDIUM OF REINSURANCE LAWS ANDREGULATIONS 17 (2009).

37 Notably, none of the first three states that adopted the restriction hasretained it; Missouri and Nebraska eliminated their assumed/ceded restric-tion, see MO. REV. STAT. §375.1198 (WEST 2010), Nebraska, NEB.REV. STAT. § 44-4830 (West 2010), and North Dakota, N.D. CENT.CODE § 26.1-06.1-29 (West 2010), replaced their respectiveassumed/ceded restrictions with the NCOIL circular assumed/cededrestriction.

38 New Jersey has the assumed/ceded restriction for Life and Healthinsurance only and applies to contracts entered into after January 28, 1993.N.J. STAT. ANN. §17B:32-59 (West 2010).

39 These states are: California, Colorado, Connecticut, District ofColumbia, Kansas, Massachusetts, Michigan, Nebraska, North Carolina,North Dakota, Oklahoma, Rhode Island, Texas, and Utah. See AppendixI, infra.

40 NAIC, Insurer Receivership Model Act (hereinafter IRMA), IV NAICPROCEEDINGS 30, 32, 48-122 (2005).

41 The underlined provisions illustrate the extent of the changes made tothe old § 29.

42 Governing the assumption of life and health contracts by guarantyassociations and the application of related setoffs with reinsurers of thecontracts. IRMA §612.C (3) (c).

43 Governing the recovery of premiums owed and providing that "[c]red-

Journal of Reinsurance/IRU

119

its or setoffs or both shall not be allowed to an agent, broker, premiumfinance company or any other person for any amounts advanced to theinsurer by the person on behalf of, but in the absence of a payment by, theinsured, or for any other amount paid by the person to any other personafter the entry of the order of receivership." Id. §613 C.

44 Id.

45 Providing for the avoidance of voidable preferences and liens. Id.§604.

46 Providing that "[t]he receiver may avoid any transfer of an interest ofthe insurer in property, any reinsurance transaction or any obligationincurred by an insurer that was made or incurred on or within two (2)years before the date of the initial filing of a petition commencing delin-quency proceedings under this Act." Id. §605 A.

47 Deeming the receiver as a lien creditor for purposes of "pursuingclaims under the Uniform Fraudulent Transfer Act, the UniformFraudulent Conveyance Act or similar provisions of state or federal law."Id. §606.

48 Id.

49 Swiss Re Life Co. Am. v. Gross, 253 Va. 139, 479 S.E.2d 857, 859 (Va.1997).

50 Id.

51 VA. CODE ANN. § 38.2-1515 (emphasis added).

52 Swiss Re Life, 479 S.E.2d at 862.

53 3 Cal .4th 1118, 14 Cal. Rptr. 2d 749 (Cal. 1992).

120

Setoffs In Insurer Receiverships: Two Decades of Change

54 Id. at 1127.55 Id. at 1137.

56 Id. at 1136.

57 41 Cal. App. 4th 828 (1995).

58 Id. at 832.

59 Id. at 833.

60 Id. at 837 (emphasis in original).

61 Id.; see also John N. Gavin, Affiliates' Dealings with Troubled Insurers,19-12 MEALEY'S LITIG. REP. INS. INSOLV. 15 (2008)

62 See, e.g., Robert M. Hall, Setoff In Arbitration When One Of TheParties Is In Receivership, 18-1 MEALEY'S LITIG. REP. INS. INSOLV.11 (2006).

63 995 F.2d 688 (7th Cir. 1993).

64 Id. at 691 (citing Hays & Co. v. Merrill Lynch, Pierce, Fenner & Smith,Inc., 885 F.2d 1149, 1155 (3d Cir. 1989)).

65 995 F.2d at 691.

66 No. B177760, 2005 Cal. App. Unpub. LEXIS 11799 (Cal. Ct. App.2005)

67 Id. at *27.

68 Id. at *28.69 Id. at *29.

Journal of Reinsurance/IRU

121

70 Id. at *24-25.

71 [1998] NO. ER 1024, EWHC (Comm. Ct., Eng.).

72 Id.

73 See generally, Offset Revolution, supra note 2, at 499 - 503.

74 359 Ill.App.3d 739, 835 N.E.2d 394 (Ill. Ct. App. 2005).

75 Id. at 747, 835 N.E.2d at 402 (citing Bank of Chicago-Garfield Ridgev. Park Nat'l Bank, 606 N.E.2d 72 (Ill. Ct. App. 1992)).

76 In the Matter of Reliance Ins. Co., 2008 CanLII 8250, 35 (Can. ONS.C.).

77 Id. at 35

78 Id.

79 No. 06 C 4799, 2010 U.S. Dist. LEXIS 23419 (N.D. Ill. Mar. 11, 2010).

80 Id. at *3.

81 See Prudential Reins. Co. v. Superior Court, 3 Cal.4th 1118, 1125 (Cal.1992) (allowing setoff of different reinsurance contracts without discus-sion of the separate transactions); and Stamp v. Insurance Co. of N. Am.,908 F.2d 1375, 1380-81 (7th Cir. 1990) (allowing setoff among pool mem-bers without discussion of the separate transactions).

82 In re Midland Ins. Co., 79 N.Y.2d 253, 582 N.Y.S.2d 58 (1992).

83 Prudential Reins, Co., 3 Cal.4th 1118 (Cal. 1992).84 In re Midland, 79 N.Y.2d at 260; see also Offset Revolution supra note

122

Setoffs In Insurer Receiverships: Two Decades of Change

2 at 462-64.

85 In re Midland, supra n.81 79 N.Y.2d at 262. But see David Scott, Non-Accepting Names Must Pay The Equitas Premium, 8-2 MEALEY'S LITIG.REP. REINS. 11 (1997)

86 See generally Special Report: Guaranty Association Offset, 5-11MEALEY'S LITIG. REP. INS. INSOLV. 11 (1993)

87 583 A.2d 1022 (Me. 1990).

88 Id. at 1023 (quoting 24-a M.R.S.A. § 4443(1)).

89 547 So.2d 849 (Ala. 1989).

90 Prudential Reins. Co. v. Superior Court, 3 Cal.4th 1118, 1133 (Cal.1992).91 Prudential Reins, Co., 3 Cal.4th at 1135.

92 In re Midland Ins. Co., 79 N.Y.2d at 264. But see Bluewater Ins. Ltd.v. Balzano, 823 P.2d 1365 (Colo. 1992)(insolvency clause transformsindemnity aspect of reinsurance.

93 Transit Cas. Co. v. Selective Ins. Co., 137 F.3d 540, 546 (8th Cir.1998).

94 Id. at 542-43.

95 Id. at 543.

96 Id.

97 Id. at 546.98 Id.

Journal of Reinsurance/IRU

123

99 For a discussion of this type of mutuality, see Offset Revolution, supranote 2 at 494-504.

100 Prudential Reins. Co. v. Superior Court, 3 Cal.4th 1118, 1128 (Cal.1992).101 Id. at 1131 (emphasis in original).

102 Id.

103 Id. at 1132.

104 823 P.2d 1365 (Colo. 1992); but see Commissioner of Ins. v. MunichAm. Reins. Co., 706 N.E.2d 694, 696-97 (Mass 1999), infra text accom-panying notes 135-37 (rejecting the Bluewater court's argument thatallowing setoff would allow a reinsurer an improper preference and allow-ing setoff under common law principles).

105 Id. at 1373.

106 Id. at 1372.

107 2000 CA 002971-MR, 2001 CA 001576-MR, 2002 WL 31840798,14-15 MEALEY'S LITIG. REP. INS. INSOLV. 7 (2003) (Ky. Ct. App.2002) (unpublished), rehearing denied, 2001 CA 000022-MR, 2001 CA002368, 2002 WL 31840802 (Ky. Ct. App. 2003) (unpublished).

108 Stamp v. Insurance Co. of N. Am., 908 F.2d 1375 (7th Cir. 1990).

109 1995 WL 702385, *3 (S.D. N.Y. 1995), aff'd,113 F.3d 1230 (2d Cir.1997).

110 Id. at *1.

111 Id.

124

Setoffs In Insurer Receiverships: Two Decades of Change

112 Id.

113 Id.

114 Id. at *3.

115 Id. at *4.

116 Transit Cas. Co. v. Selective Ins. Co., 137 F.3d 540 (8th Cir. 1998).

117 Id. at 546. A " 'partially disclosed principal' is a party whose exis-tence, but not identity, is disclosed to the other parties to the contract." Id.(citing RESTATEMENT (SECOND) OF AGENCY § 4(2) (1958)).

118 Id.

119 Id.; see also Philip Hertz and David Steinberg, Waving or Drowning:Problems Arising When Pool Participants Go Under: The UK LegalPerspective, 12-2 MEALEY'S LITIG. REP. REINS. 10 (2001).

120 926 S.W.2d 460 (Ky. Ct. App. 1996).

121 Id. at 462 (quoting KRS 304.33-330).

122 Id.

123 Id.

124 224 F.3d641 (7th Cir. 2000).

125 137 F.3d 540 (8th Cir. 1998).

126 See, e.g., Offset Revolution, supra note 2 at 451-53 n. 3.127 In re the Rehabilitation of American Mut. Reins. Co., 606 N.E.2d 32

Journal of Reinsurance/IRU

125

(Ill. Ct. App. 1992).

128 Id. at 36; see also Selcke v. New Eng. Reins. Co., 995 F.2d 688 (7thCir. 1993) (assuming, without deciding, that setoff applies in rehabilita-tion).

129 531 Pa. 598, 614 A.2d 1086 (Penn. 1992).

130 Lia B. Royle, Reinsurers' Setoff Right in the Insolvency Context:Recent Developments, 8-5 MEALEY'S LITIG. REP. INS. INSOLV. 15(1996).

131 531 Pa. at 620, 614 A.2d at 1098.

132 Pink v. American Sur. Co., 28 N.E.2d 842 (N.Y. App. Ct. 1940).

133 Id. at 293-95.

134 Id. at 298.

135 429 Mass. 140, 706 N.E.2d 694 (Mass. 1999).

136 Id., 429 Mass. at 144, 706 N.E.2d at 697.

137 Id.

138 See, e.g., Stephen G. Schweller, Voidable Preferences in InsuranceCompany Liquidations, 21-2 MEALEY'S LITIG. REP. INS. INSOLV. 16(2009).

139 No. 03AP-733, 2004 Ohio App. LEXIS 6456 (Ohio App. Ct. 2004).

140 Id. at *9 (quoting R.C. 3903.28(I)).141 Id. at *2.

126

Setoffs In Insurer Receiverships: Two Decades of Change

142 Id.

143 Id. at *5.

144 Id. at *6. But see Covington v. University Hosp. of Cleveland, 149Ohio App. 3d 479, 778 N.E.2d 54 (Ohio Ct. App. 2002) (faced withcompeting setoff provisions - the general setoff section in the code and thesetoff provided in the voidable preference section of the code - the courtheld that the preference section's own setoff subsection should govern).

145 2004 Ohio App. LEXIS 6456 at *33.

146 No. 98 C 4084, 2002 WL 31155059 (N.D. Ill. 2002).

147 See also David Scott, Non-Accepting Names Must Pay The EquitasPremium, 8-2 MEALEY'S LITIG. REP. REINS. 11 (1997)(Lloyd's Namescould not assert setoff as against Equitas premium because contractexpressly obliged Names to pay the premium free and clear of any setoff).

EAST\43817784.2

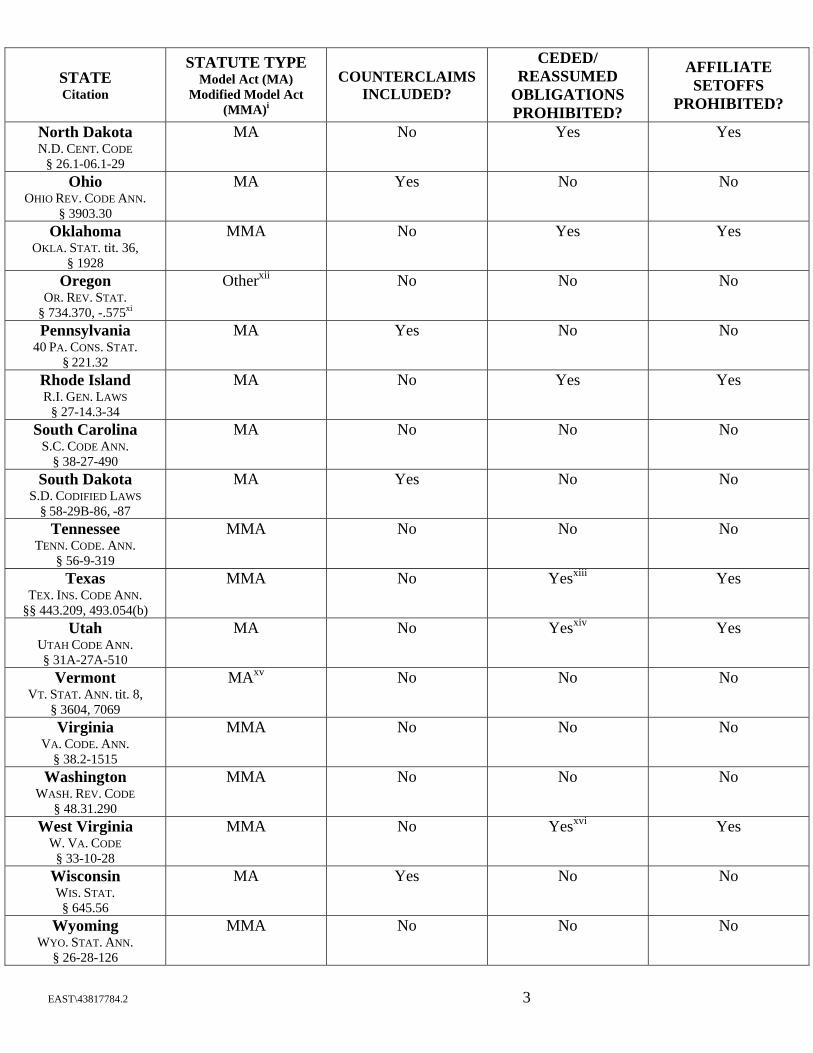

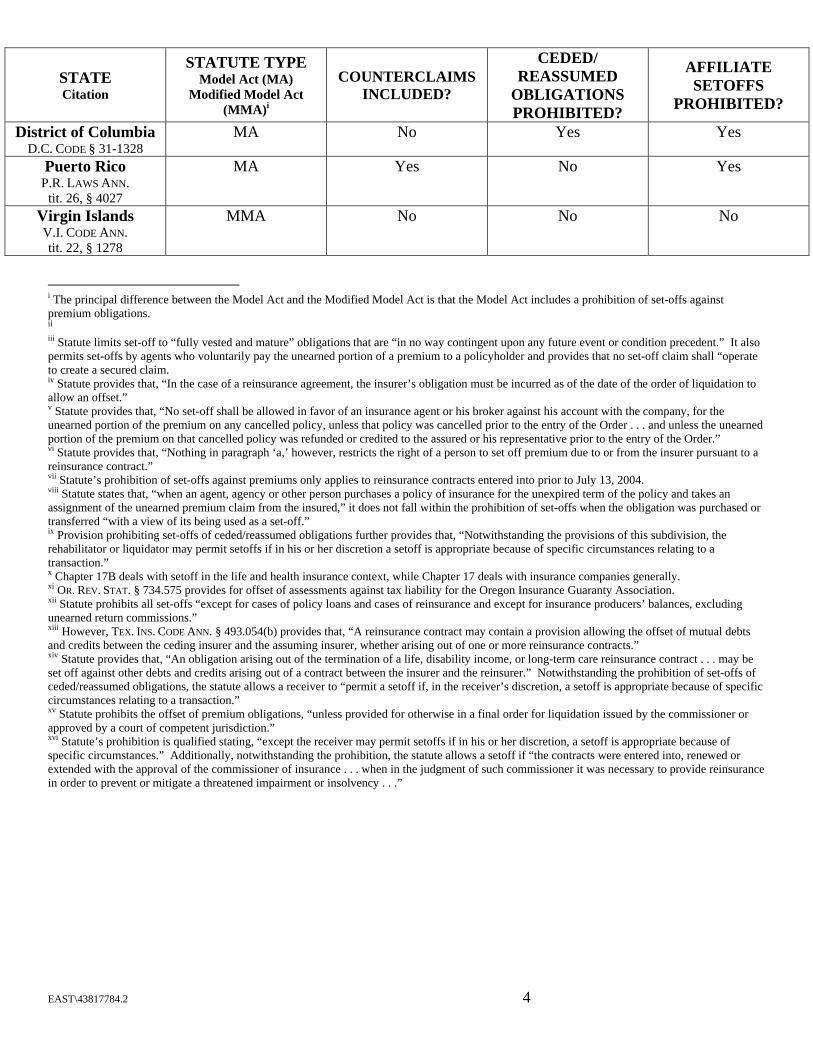

STATUTORY INSURER RECEIVERSHIP SETOFF PROVISIONS (2010 Update)

STATE Citation

STATUTE TYPE Model Act (MA)

Modified Model Act (MMA)i

COUNTERCLAIMS INCLUDED?

CEDED/ REASSUMED

OBLIGATIONS PROHIBITED?

AFFILIATE SETOFFS

PROHIBITED?

Alabama ALA. CODE § 27-32-29

MMA No No No

Alaska ALASKA STAT.

§ 21.78.270

MA Yes No No

Arizona ARIZ. REV. STAT.

§20-638

MMA No No No

Arkansas ARK. CODE. § 23-68-127

MMA No No No

California CAL. INS. CODE

§1031

MMA No Yes No

Colorado COL. REV. STAT. ANN. §

10-3-529

MA No Yes Yes

Connecticut CONN. GEN. STAT.

§38a-932

MA Yes Yes Yes

Delaware DEL. CODE ANN.

tit. 18, § 5927

MMA No No No

Florida FLA. STAT. § 631.281

MMAiiiii No Noiv No

Georgia GA. CODE ANN.

§ 33-37-29

MMA No No No

Hawaii HI. REV. STAT. § 431:15-319

MA Yes No No

Idaho ID. CODE ANN.

§ 41-3330

MA No No No

Illinois 215 ILL. COMP. STAT.

5/206

MAv Yes No No

Indiana IND. CODE § 27-9-3-28

MA Yes No No

Iowa IOWA CODE § 507C.30

MAvi No No Yes

Kansas KAN. STAT. ANN.

§ 40-3633

MMA No Yes Yes

EAST\43817784.2 2

STATE Citation

STATUTE TYPE Model Act (MA)

Modified Model Act (MMA)i

COUNTERCLAIMS INCLUDED?

CEDED/ REASSUMED

OBLIGATIONS PROHIBITED?

AFFILIATE SETOFFS

PROHIBITED?

Kentucky KY. REV. STAT. ANN.

§ 304.33-330

MMAvii Yes No No

Louisiana LA. REV. STAT. ANN. §

22:2026

MMAviii No No No

Maine ME. REV. STAT. tit. 24A, §

4381

MMA No No No

Maryland MD. CODE ANN., INS.

§ 9-229

MMA No No No

Massachusetts MASS. GEN. LAWS ANN.

ch. 175, § 180C

MMA No Yes Yes

Michigan MICH. COMP. LAWS

§ 500.8130

MA Yes Yes Yes

Minnesota MINN. STAT.

§ 60B.34

MA Yes No No

Mississippi MISS. CODE ANN.

§83-24-59

MA No No No

Missouri MO. REV. STAT.

§ 375.1198

MA No Yes Yes

Montana MONT. CODE ANN.

§ 33-2-1359

MA No No No

Nebraska NEB. REV. STAT.

§ 44-4830

MA No Yesix Yes

Nevada NEV. REV. STAT.

§ 696B.440

MMA No No No

New Hampshire N.H. REV. STAT. ANN.

§ 402-C:34

MMA No No No

New Jersey N.J. STAT. ANN.

§§ 17:30C-27, 17B:32-59x

MMA No No No

New Mexico N.M. STAT. ANN.

§ 59A-41-45

MA No No No

New York N.Y. INS. LAW

§ 7427

MMA No No No

North Carolina N.C. GEN. STAT.

§ 58-30-160

MA No Yes Yes

EAST\43817784.2 3

STATE Citation

STATUTE TYPE Model Act (MA)

Modified Model Act (MMA)i

COUNTERCLAIMS INCLUDED?

CEDED/ REASSUMED

OBLIGATIONS PROHIBITED?

AFFILIATE SETOFFS

PROHIBITED?

North Dakota N.D. CENT. CODE

§ 26.1-06.1-29

MA No Yes Yes

Ohio OHIO REV. CODE ANN.

§ 3903.30

MA Yes No No

Oklahoma OKLA. STAT. tit. 36,

§ 1928

MMA No Yes Yes

Oregon OR. REV. STAT.

§ 734.370, -.575xi

Otherxii No No No

Pennsylvania 40 PA. CONS. STAT.

§ 221.32

MA Yes No No

Rhode Island R.I. GEN. LAWS

§ 27-14.3-34

MA No Yes Yes

South Carolina S.C. CODE ANN.

§ 38-27-490

MA No No No

South Dakota S.D. CODIFIED LAWS

§ 58-29B-86, -87

MA Yes No No

Tennessee TENN. CODE. ANN.

§ 56-9-319

MMA No No No

Texas TEX. INS. CODE ANN.

§§ 443.209, 493.054(b)

MMA No Yesxiii Yes

Utah UTAH CODE ANN. § 31A-27A-510

MA No Yesxiv Yes

Vermont VT. STAT. ANN. tit. 8,

§ 3604, 7069

MAxv No No No

Virginia VA. CODE. ANN.

§ 38.2-1515

MMA No No No

Washington WASH. REV. CODE

§ 48.31.290

MMA No No No

West Virginia W. VA. CODE

§ 33-10-28

MMA No Yesxvi Yes

Wisconsin WIS. STAT. § 645.56

MA Yes No No

Wyoming WYO. STAT. ANN.

§ 26-28-126

MMA No No No

EAST\43817784.2 4

STATE Citation

STATUTE TYPE Model Act (MA)

Modified Model Act (MMA)i

COUNTERCLAIMS INCLUDED?

CEDED/ REASSUMED

OBLIGATIONS PROHIBITED?

AFFILIATE SETOFFS

PROHIBITED?

District of Columbia D.C. CODE § 31-1328

MA No Yes Yes

Puerto Rico P.R. LAWS ANN.

tit. 26, § 4027

MA Yes No Yes

Virgin Islands V.I. CODE ANN. tit. 22, § 1278

MMA No No No

i The principal difference between the Model Act and the Modified Model Act is that the Model Act includes a prohibition of set-offs against premium obligations. ii iii Statute limits set-off to “fully vested and mature” obligations that are “in no way contingent upon any future event or condition precedent.” It also permits set-offs by agents who voluntarily pay the unearned portion of a premium to a policyholder and provides that no set-off claim shall “operate to create a secured claim. iv Statute provides that, “In the case of a reinsurance agreement, the insurer’s obligation must be incurred as of the date of the order of liquidation to allow an offset.” v Statute provides that, “No set-off shall be allowed in favor of an insurance agent or his broker against his account with the company, for the unearned portion of the premium on any cancelled policy, unless that policy was cancelled prior to the entry of the Order . . . and unless the unearned portion of the premium on that cancelled policy was refunded or credited to the assured or his representative prior to the entry of the Order.” vi Statute provides that, “Nothing in paragraph ‘a,’ however, restricts the right of a person to set off premium due to or from the insurer pursuant to a reinsurance contract.” vii Statute’s prohibition of set-offs against premiums only applies to reinsurance contracts entered into prior to July 13, 2004. viii Statute states that, “when an agent, agency or other person purchases a policy of insurance for the unexpired term of the policy and takes an assignment of the unearned premium claim from the insured,” it does not fall within the prohibition of set-offs when the obligation was purchased or transferred “with a view of its being used as a set-off.” ix Provision prohibiting set-offs of ceded/reassumed obligations further provides that, “Notwithstanding the provisions of this subdivision, the rehabilitator or liquidator may permit setoffs if in his or her discretion a setoff is appropriate because of specific circumstances relating to a transaction.” x Chapter 17B deals with setoff in the life and health insurance context, while Chapter 17 deals with insurance companies generally. xi OR. REV. STAT. § 734.575 provides for offset of assessments against tax liability for the Oregon Insurance Guaranty Association. xii Statute prohibits all set-offs “except for cases of policy loans and cases of reinsurance and except for insurance producers’ balances, excluding unearned return commissions.” xiii However, TEX. INS. CODE ANN. § 493.054(b) provides that, “A reinsurance contract may contain a provision allowing the offset of mutual debts and credits between the ceding insurer and the assuming insurer, whether arising out of one or more reinsurance contracts.” xiv Statute provides that, “An obligation arising out of the termination of a life, disability income, or long-term care reinsurance contract . . . may be set off against other debts and credits arising out of a contract between the insurer and the reinsurer.” Notwithstanding the prohibition of set-offs of ceded/reassumed obligations, the statute allows a receiver to “permit a setoff if, in the receiver’s discretion, a setoff is appropriate because of specific circumstances relating to a transaction.” xv Statute prohibits the offset of premium obligations, “unless provided for otherwise in a final order for liquidation issued by the commissioner or approved by a court of competent jurisdiction.” xvi Statute’s prohibition is qualified stating, “except the receiver may permit setoffs if in his or her discretion, a setoff is appropriate because of specific circumstances.” Additionally, notwithstanding the prohibition, the statute allows a setoff if “the contracts were entered into, renewed or extended with the approval of the commissioner of insurance . . . when in the judgment of such commissioner it was necessary to provide reinsurance in order to prevent or mitigate a threatened impairment or insolvency . . .”

Important Subscription Information

For new orders, please allow 4-6 weeks for receipt of yourfirst issue.

Contact InformationMail: Journal of Reinsurance

Subscription Services971 Route 202 NorthBranchburg, NJ 08876

Telephone: 908-203-0211Fax: 908-203-0213Email: [email protected]

Subscription Rates

The Journal of Reinsurance is available at the followingsubscription rate:

1 year 2 years 3 years(4 issues) (8 issues) (12 iss.)$195.00 $350.00 $525.00

All prices are in U.S. dollars. We accept American Express,MasterCard, Visa, or check payable to Intermediaries &Reinsurance Underwriters Association.

Journal of ReinsuranceAdvertising Information

The Intermediaries & Reinsurance Underwriters Association is pleasedto announce the sale of advertisements in the Journal of Reinsurance,please respond promptly if you have an interest in reserving the frontinside or back inside covers.

About the Journal of ReinsuranceThe Journal of Reinsurance is an official publication of theIntermediaries & Reinsurance Underwriters Association. It is pub-lished quarterly in January, April and July, and October. Focused onissues confronting the reinsurance community in today's complexenvironment, the Journal of Reinsurance applies the best research andpractices to the strategic challenges and operating problems of today'senvironment. The Journal of Reinsurance is designed to keep reinsur-ance and insurance underwriters, insurance company executives, bro-kers, regulators, academicians and those interested in reinsuranceabreast of developments which will impact on reinsurers and the rein-surance market.

Advertising Deadlines (Volume 17)•Volume 17, No. 1, Winter 2010: December 15, 2009

•Volume 17, No. 2, Spring 2010: March 15, 2010•Volume 17, No. 3, Summer 2010: June 15, 2010