journal is a book of records where daily monetary transactions of a business is posted. though it...

TRANSCRIPT

LEDGER

JOURNAL-LEDGERJournal is a book of records where daily monetary

transactions of a business is posted. Though it brings all the transactions together, it creates

confusion between small and important expenses.

Thus, a ledger was introduced, where all the transactions are recorded under the individual

accounts.

WHAT IS A LEDGER:A ledger account can be defined as a summary statement of

all the transactions relating to a person, asset, expense or income which have taken place during a given period of time

and shows their net effect.

Thus, a group of accounts is known as ledger.

LEDGER: IN A NUTSHELL

Ledger contains same information as journal.It summarizes the transactions relating to person, asset, expense or income.It is a book of accounts as it helps in achieving the objective of accounts.It’s easier to understand and maintain than journal.

A ledger should answer:1. What are the total sales to an individual

customer?2. What are the total purchases from an

individual supplier?3. How much amount is owed by debtors?4. How much amount is owed to debtors?5. What is the amount of profit or loss made

during a particular period?6. What is the financial position of the firm on a

particular date?

TYPES OF LEDGER:GENERAL LEDGER• A collection of group of accounts

that supports the value items shown in the major financial statements

SUBSIDIARY LEDGER• Subset of general ledger

FORMAT OF LEDGER:

DATE

PARTICU-LARS

F. AMOUNT

DATE

PARTICU-LARS

F.

AMOUNT

To Name Of Credit Account

Rs. By Name Of Debit Account

Rs.

Dr. Cr.

ITEMS IN LEDGER:Each account in the ledger is divided into two equal parts by a vertical line.The left hand side is known as debit (Dr.) side.The right hand side is known as credit (Cr.) side.The two sides are further divided into four columns, date, particulars, folio and amount.‘F’ is the folio page number of the journal or subsidiary book.

LEDGER POSTING OF JOURNAL:

Every transaction is initially recorded in journal as journal entry. From the journal, it’s transferred to the respective accounts in the ledger.

This process of transferring from the journal to ledger is known as posting.

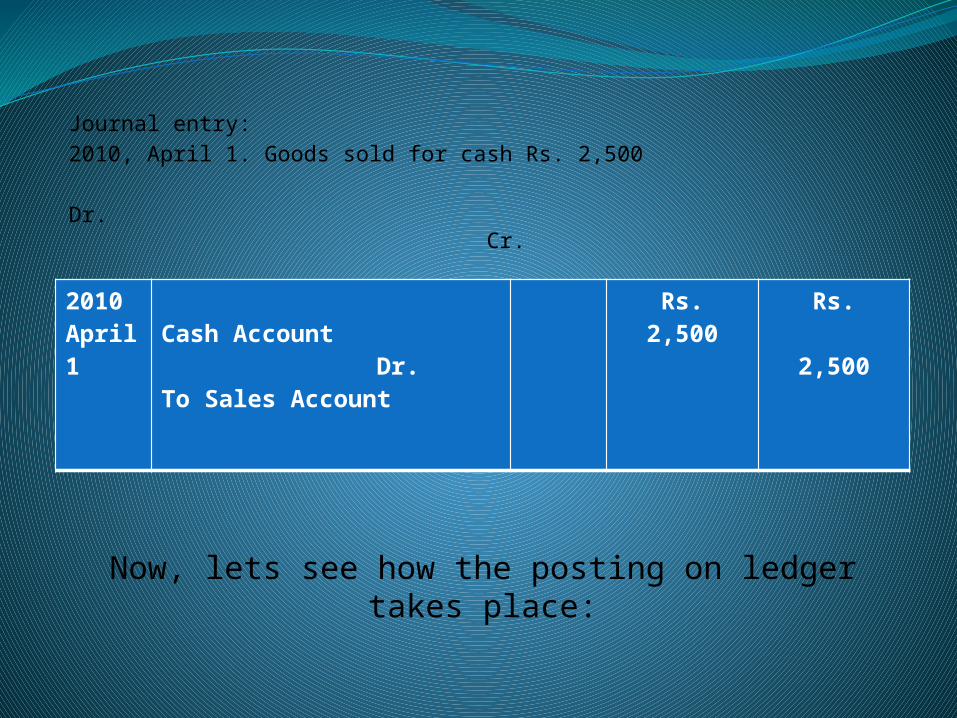

Lets see how do we post an entry from journal to ledger:

Journal entry:2010, April 1. Goods sold for cash Rs. 2,500

Dr. Cr.

2010 April 1

Cash Account Dr.To Sales Account

Rs.2,500

Rs.

2,500

Now, lets see how the posting on ledger takes place:

DATE

PARTICU-LARS

F. AMOUNT

DATE

PARTICU-LARS

F.

AMOUNT

2010APRIL 1

To Sales Account

Rs.2,500

Rs.

DATE

PARTICU-LARS

F. AMOUNT

DATE

PARTICU-LARS

F.

AMOUNT

Rs. 2010April 1

By Cash Account

Rs.2,500

SALES ACCOUNT

CASH ACCOUNT

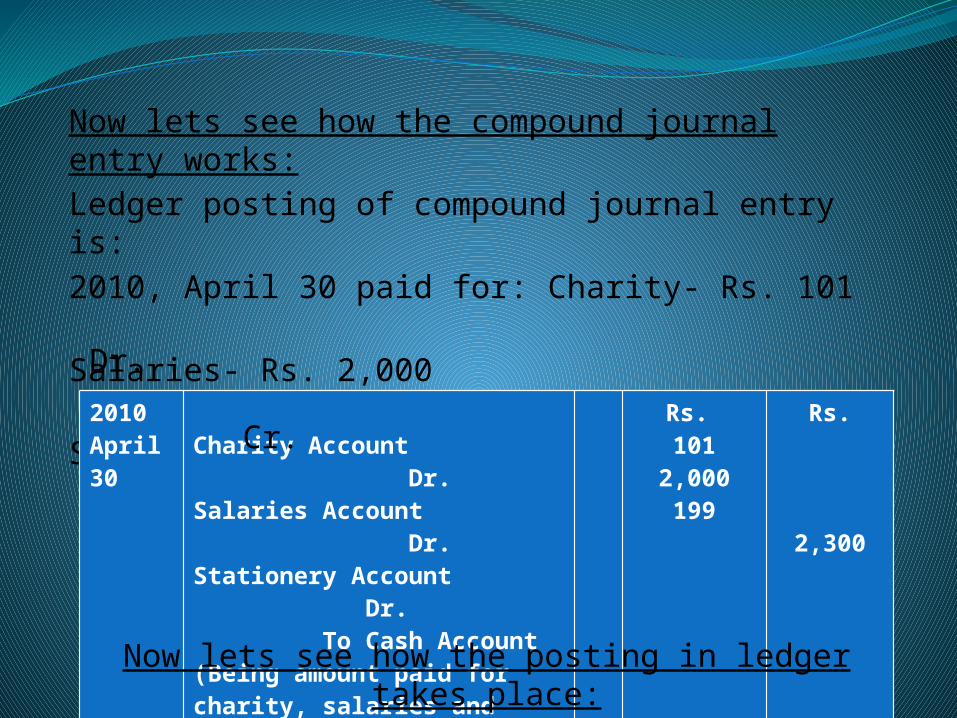

Now lets see how the compound journal entry works:Ledger posting of compound journal entry is:2010, April 30 paid for: Charity- Rs. 101 Salaries- Rs. 2,000 Stationery- Rs. 199

2010April 30

Charity Account Dr.Salaries Account Dr.Stationery Account Dr. To Cash Account(Being amount paid for charity, salaries and stationery)

Rs. 101

2,000199

Rs.

2,300

Dr. Cr.

Now lets see how the posting in ledger takes place:

DATE

PARTICU-LARS

F. AMOUNT

DATE

PARTICU-LARS

F.

AMOUNT

2010APRIL 30

To Cash Account

Rs.101

Rs.

DATE

PARTICU-LARS

F. AMOUNT

DATE

PARTICU-LARS

F.

AMOUNT

2010APRIL 30

To Cash Account

Rs.2,000

Rs.

CHARITY ACCOUNT

SALARIES ACCOUNT

DATE

PARTICU-LARS

F. AMOUNT

DATE

PARTICU-LARS

F.

AMOUNT

2010APRIL 1

To Sales Account

Rs.2,500

Rs.

STATIONERY ACCOUNT

DATE

PARTICU-LARS

F. AMOUNT

DATE

PARTICU-LARS

F.

AMOUNT

2010APRIL 1

To Sales Account

Rs.2,500

Rs.

CASH ACCOUNT

EXAMPLE:Question: Post the following transactions in the ledger of Imran:

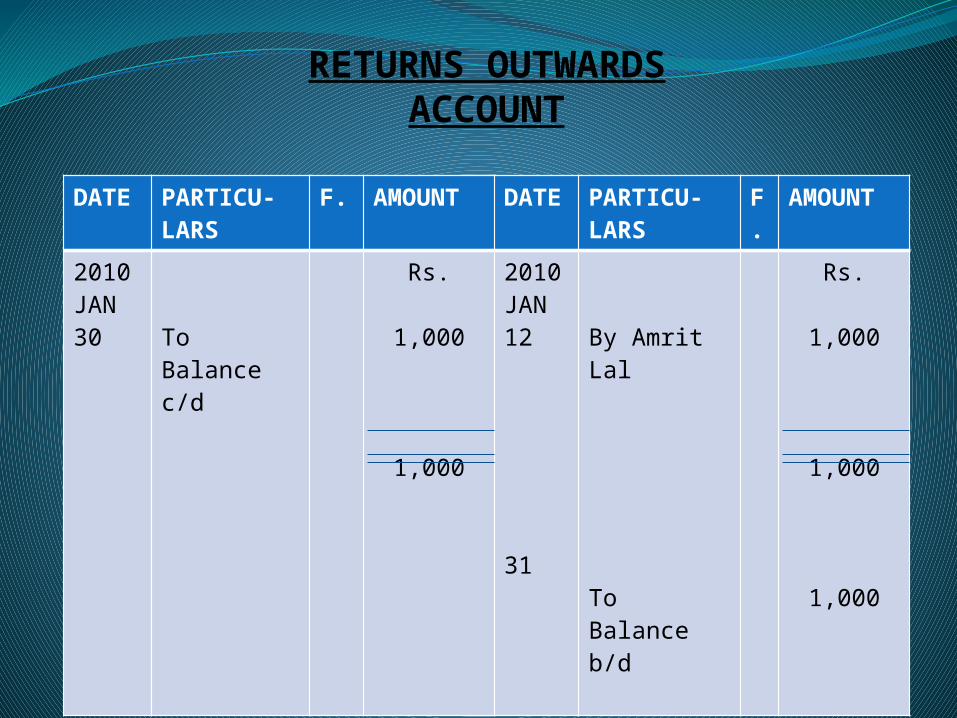

2010 Rs.Jan. 1 Started business with cash 45,000Jan. 2 Paid into bank 25,000Jan. 2 Goods purchased for cash 15, 000Jan. 3 Purchase of Furniture and payment by cheque 5,000Jan. 5 Sold goods for cash 8,500Jan. 8 Sold goods to Arvind Walia 4,000Jan. 10 Good purchased from Amrit Lal 7,000Jan. 12 Goods returned to Amrit Lal 1,000Jan. 15 Goods returned to Arvind Walia 200

Jan. 18 Cash received from Arvind Walia Rs. 3,760 and discount allowed to him 40Jan. 21 Withdrew from bank for private use 1,000 Withdrew from bank for use in the business 5,000Jan. 25 Paid telephone rent for one year 400Jan. 28 Cash paid to Amrit Lal in full settlement of his account 5,940Jan. 30 Paid for: Stationery 200 Rent 1,000 Salaries to staff 2,500

DATE

PARTICU-LARS

F. AMOUNT

DATE

PARTICU-LARS

F.

AMOUNT

2010JAN. 1

518

21

31

To Capital A/cTo Sales A/cTo Arvind WaliaTo Bank A/c

To Balance b/d

Rs.

45,000

8,5003,760

5,000

62,260

12,220

2010JAN.12

25

2830

3030

30

By Bank A/cBy Purchase A/cBy Telephone rent A/cBy Amrit LalBy Stationery A/cBy Rent A/cBy Salaries A/cBy Balances c/d

Rs.

25,000

15,000

4005,940

2001,000

2,500

12,22062,260

CASH ACCOUNT

DATE

PARTICU-LARS

F. AMOUNT

DATE

PARTICU-LARS

F.

AMOUNT

2010JAN 30

To Balance c/d

Rs.45,000

45,000

2010JAN1

DEC.1

By Cash A/c

By Balance b/d

Rs.45,000

45,000

45,000

CAPITAL ACCOUNT

DATE

PARTICU-LARS

F. AMOUNT

DATE

PARTICU-LARS

F.

AMOUNT

2010JAN 1

31

To Cash A/c

To Balance b/d

Rs.25,000

25,000

14,000

2010JAN3

21

2130

By Furniture A/cBy Drawings A/cBy Cash A/cBy Balance c/d

Rs.

5,000

45,000

5,000

14,000

25,000

BANK ACCOUNT

DATE

PARTICU-LARS

F. AMOUNT

DATE

PARTICU-LARS

F.

AMOUNT

2010JAN 210

31

To Cash A/cTo Amrit Lal

To Balance b/d

Rs.

15,0007,000

22,000

14,000

2010JAN30 By Balance

c/d

Rs.

22,000

22,000

PURCHASES ACCOUNT

DATE

PARTICU-LARS

F. AMOUNT

DATE

PARTICU-LARS

F.

AMOUNT

2010JAN 3

31

To Bank A/c

To Balance b/d

Rs.

5,000

5,000

5,000

2010JAN30 By Balance

c/d

Rs.

5,000

5,000

FURNITURE ACCOUNT

DATE

PARTICU-LARS

F. AMOUNT

DATE

PARTICU-LARS

F.

AMOUNT

2010JAN 30

31

To Balance c/d

To Balance b/d

Rs.

12,500

12,500

14,000

2010JAN58

By Cash A/cBy Arvind Walia

Rs.

8,500

4,000

12,500

SALES ACCOUNT

DATE

PARTICU-LARS

F. AMOUNT

DATE

PARTICU-LARS

F.

AMOUNT

2010JAN 8 To Sales

A/c

Rs.

4,000

22,000

4,000

2010JAN15

1818

By Returns InwardsBy Cash A/cBy Discount A/c

Rs.

2003,760

40

4,000

ARVIND WALIA

DATE

PARTICU-LARS

F. AMOUNT

DATE

PARTICU-LARS

F.

AMOUNT

2010JAN 12

2828

To Returns OutwardsTo Cash A/cTo Discount A/c

Rs.

1,000

5,940

60

7,000

2010JAN10 By

Purchase A/c

Rs.

7,000

7,000

AMRIT LAL

DATE

PARTICU-LARS

F. AMOUNT

DATE

PARTICU-LARS

F.

AMOUNT

2010JAN 15

31

To Arvind Walia

To Balance b/d

Rs.

200

200

200

2010JAN30 By Balance

c/d

Rs.

200

200

RETURNS INWARDS ACCOUNT

DATE

PARTICU-LARS

F. AMOUNT

DATE

PARTICU-LARS

F.

AMOUNT

2010JAN 30 To Balance

c/d

Rs.

1,000

1,000

2010JAN12

31

By Amrit Lal

To Balance b/d

Rs.

1,000

1,000

1,000

RETURNS OUTWARDS ACCOUNT

DATE

PARTICU-LARS

F. AMOUNT

DATE

PARTICU-LARS

F.

AMOUNT

2010JAN 18

10

To Arvind WaliaTo Amrit Lal

Rs.

4020

60

2010JAN28

31

By Amrit Lal

By Balance b/d

Rs.

60

60

20

DISCOUNT ACCOUNT

DATE

PARTICU-LARS

F. AMOUNT

DATE

PARTICU-LARS

F.

AMOUNT

2010JAN 21

31

To Bank A/c

To Balance b/d

Rs.

1,000

1,000

1,000

2010JAN30 By Balance

c/d

Rs.

1,000

1,000

DRAWINGS ACCOUNT

DATE

PARTICU-LARS

F. AMOUNT

DATE

PARTICU-LARS

F.

AMOUNT

2010JAN 2510

31

To Cash A/cTo Amrit Lal

To Balance b/d

Rs.

15,0007,000

22,000

14,000

2010JAN30 By Balance

c/d

Rs.

22,000

22,000

TELEPHONE RENT ACCOUNT

DATE

PARTICU-LARS

F. AMOUNT

DATE

PARTICU-LARS

F.

AMOUNT

2010JAN 30

31

To Cash A/c

To Balance b/d

Rs.

200

200

200

2010JAN30 By Balance

c/d

Rs.

200

200

SALARY ACCOUNT

DATE

PARTICU-LARS

F. AMOUNT

DATE

PARTICU-LARS

F.

AMOUNT

2010JAN 30

31

To Cash A/c

To Balance b/d

Rs.

1,000

1,000

1,000

2010JAN30 By Balance

c/d

Rs.

1,000

1,000

RENT ACCOUNT

DATE

PARTICU-LARS

F. AMOUNT

DATE

PARTICU-LARS

F.

AMOUNT

2010JAN 30

31

To Cash A/c

To Balance b/d

Rs.

2,500

2,500

2,500

2010JAN30 By Balance

c/d

Rs.

2,500

2,500

SALARIES ACCOUNT

THANK YOU