joint ventures in business, part 1 & part 2 (60 minutes) · joint ventures in business, part 1...

TRANSCRIPT

JOINT VENTURES IN BUSINESS, PART 1 & PART 2

First Run Broadcast: December 17 & 18, 2013

Live Replay: March 26 & 27, 2014

1:00 p.m. E.T./12:00 p.m. C.T./11:00 a.m. M.T./10:00 a.m. P.T. (60 minutes)

Businesses frequently pool their resources – capital, expertise, marketing power – in joint

ventures to grow in existing or new markets, leveraging their strengths by partnering with

companies with complementary strengths. Joint ventures come in many varieties, including

contractual strategic alliances and formal entity-based ventures. Keys to long-term stability and

success in these ventures include understanding the current and future contributions of each

party, access to information and decision-making authority over time, dispute resolution and

transfers of interests in the JV. This program will provide you with a practical guide to planning

and drafting joint ventures, including financial and tax considerations, decision-making authority

and transfers of interests in the JV, ownership of jointly developed property and dispute

resolution.

Day 1 – March 26, 2014:

Joint ventures in business and real estate – planning and drafting considerations

Types of joint ventures – contractual strategic alliances v. shared entities

Framework of considerations – formality, capital, tax issues, management control, exits

Choice of entity – incorporated entities v. LPs and general partnerships v. LLCs

Decision-making, access to information, deadlocks and resolution

Day 2 – March 27, 2014:

Contributions – capital, marketing and distribution, expertise, intangible assets

Economics – allocation of profits and losses, and distribution policies

Transfers of JV interests – rights of first offer/refusal, restrictions on transfers, dissolution

Ownership – development of intellectual property and ownership of property

Speakers:

Joel R. Buckberg is of counsel in Nashville office of Baker, Donelson, Bearman, Caldwell &

Berkowitz, P.C., where he has more than 30 years’ experience in corporate and business

transactions. His practice focuses on corporate and asset transactions and operations, particularly

in hospitality, franchising and distribution. He also counsels clients on strategic planning,

financing, mergers and acquisitions, system policy and practice development, regulatory

compliance and contract system drafting. Prior to joining Baker Donelson, he was executive vice

president and deputy general counsel of Cendant Corporation. Mr. Buckberg received his B.S.

form Union College, his M.B.A. from Vanderbilt University, and his J.D. from Vanderbilt

University School of Law.

Peter J. Kinsella is a partner in the Denver office of Perkins Coie, LLP, where he has an

extensive practice advising businesses of every size on technology and commercial transactions,

and joint ventures. Prior to joining his firm, he worked for ten years in various legal capacities

with Qwest Communications International, Inc. and Honeywell, Inc. Mr. Kinsella has extensive

experience structuring and negotiating data sharing agreements, complex procurement

agreements, product distribution agreements, OEM agreements, marketing and advertising

agreements, corporate sponsorship agreements, and various types of patent, trademark and

copyright licenses. Mr. Kinsella received his B.S. from North Dakota State University and his

J.D. from the University of Minnesota Law School.

VT Bar Association Continuing Legal Education Registration Form

Please complete all of the requested information, print this application, and fax with credit info or mail it with payment to: Vermont Bar Association, PO Box 100, Montpelier, VT 05601-0100. Fax: (802) 223-1573 PLEASE USE ONE REGISTRATION FORM PER PERSON. First Name ________________________ Middle Initial____Last Name___________________________

Firm/Organization _____________________________________________________________________

Address ______________________________________________________________________________

City _________________________________ State ____________ ZIP Code ______________________

Phone # ____________________________Fax # ______________________

E-Mail Address ________________________________________________________________________

Joint Ventures in Business, Part 1

Teleseminar March 26, 2014 1:00PM – 2:00PM

1.0 MCLE GENERAL CREDITS

PAYMENT METHOD:

Check enclosed (made payable to Vermont Bar Association) Amount: _________ Credit Card (American Express, Discover, Visa or Mastercard) Credit Card # _______________________________________ Exp. Date _______________ Cardholder: __________________________________________________________________

VBA Members $75

Non-VBA Members $115

NO REFUNDS AFTER March 19, 2014

VT Bar Association Continuing Legal Education Registration Form

Please complete all of the requested information, print this application, and fax with credit info or mail it with payment to: Vermont Bar Association, PO Box 100, Montpelier, VT 05601-0100. Fax: (802) 223-1573 PLEASE USE ONE REGISTRATION FORM PER PERSON. First Name ________________________ Middle Initial____Last Name___________________________

Firm/Organization _____________________________________________________________________

Address ______________________________________________________________________________

City _________________________________ State ____________ ZIP Code ______________________

Phone # ____________________________Fax # ______________________

E-Mail Address ________________________________________________________________________

Joint Ventures in Business, Part 2

Teleseminar March 27, 2014 1:00PM – 2:00PM

1.0 MCLE GENERAL CREDITS

PAYMENT METHOD:

Check enclosed (made payable to Vermont Bar Association) Amount: _________ Credit Card (American Express, Discover, Visa or Mastercard) Credit Card # _______________________________________ Exp. Date _______________ Cardholder: __________________________________________________________________

VBA Members $75

Non-VBA Members $115

NO REFUNDS AFTER March 20, 2014

Vermont Bar Association

CERTIFICATE OF ATTENDANCE

Please note: This form is for your records in the event you are audited Sponsor: Vermont Bar Association Date: March 26, 2014 Seminar Title: Joint Ventures in Business, Part 1

Location: Teleseminar Credits: 1.0 MCLE General Credit Luncheon addresses, business meetings, receptions are not to be included in the computation of credit. This form denotes full attendance. If you arrive late or leave prior to the program ending time, it is your responsibility to adjust CLE hours accordingly.

Vermont Bar Association

CERTIFICATE OF ATTENDANCE

Please note: This form is for your records in the event you are audited Sponsor: Vermont Bar Association Date: March 27, 2014 Seminar Title: Joint Ventures in Business, Part 2

Location: Teleseminar Credits: 1.0 MCLE General Credit Luncheon addresses, business meetings, receptions are not to be included in the computation of credit. This form denotes full attendance. If you arrive late or leave prior to the program ending time, it is your responsibility to adjust CLE hours accordingly.

Joint Ventures in Business

Joel R. Buckberg

615 726-5639

Baker Donelson Bearman Caldwell & Berkowitz, P.C.

Nashville, Tennessee

2www.bakerdonelson.com© 2013 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

WHY A JOINT VENTURE?

• Definition - arrangement for 2 or more parties to execute a particularbusiness undertaking in which the parties share in the investment,control and profits and losses of the enterprise.

• Four basic elements establish a joint enterprise:

− (1) an agreement among the members of the group;

− (2) a common purpose;

− (3) a community of pecuniary interest; and

− (4) an equal right to control the enterprise.

• Joint Ventures take 2 distinct forms:

− a contractual joint venture, a general partnership under state lawformed for a specific purpose

Possibly a strategic alliance with a core set of agreements

− an entity joint venture, either a limited liability company orcorporation

3www.bakerdonelson.com© 2013 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

WHY A JOINT VENTURE?

• Until the advent of the LLC, contractual venture was common to avoiddouble taxation.

• Liability exposure covered with insurance, cross indemnities and corporateentities as the ownership of venture interests.

• As a general partnership, the venture partners were liable jointly andseverally for the debts and obligations of the venture.

• Contractual joint venture partner undertook risk it could not controlmanagerially.

• A complex operating agreement shaped rights and obligations

• In riskier activities, joint ventures needed liability shields to avoid unlimited,unmanaged risk.

• Venture partner balance sheet at risk for a venture liabilities

• Principle was severely tested in the product liability cases against DowCorning.

− Economic substance of the joint venture and the reinvestment of profitsallowed partners to avoid liability for silicone breast implants

4www.bakerdonelson.com© 2013 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

WHY A JOINT VENTURE?

• Delaware corporation offers the benefit of a statutory deadlock

resolution procedure under Section 273 of the Delaware Corporation

Law for corporations with 2 stockholders owning 50% of stock

• Tax inefficiency of corporate form:

− double taxation

− dividend exclusion limited to 70%-80% of dividends

− losses trapped and not allocable to owners

• Joint venture co-investment format is a mutual decision to assert

executive management rights by committee instead of relying on

Board of Directors and chosen management

5www.bakerdonelson.com© 2013 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

Distinctions from other forms of business venture:

• Direct investment

• Lending Plus – non-bank loans coupled with enhanced governanceparticipation through covenants, board access; perhaps with equitykicker

• License – one party licenses asset to another in exchange forroyalty, upfront fee, with some retained control over use of licensedproperty

• Franchise – stronger form of license arrangement where assetowner imposes substantial control over operator’s management ofbusiness

• Commercial distribution or other contractual usage arrangement –asset packaged for commercialization by counterparty at itsdiscretion

WHY A JOINT VENTURE?

6www.bakerdonelson.com© 2013 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

WHY A JOINT VENTURE?

Key elements:

• Market potential and best means to exploit not clear at inception

• Parties bring different resources, skills, assets, that must mesh

• Cultures must be compatible or replaced with new common culture

− Think The Devil’s Brigade

• Common goals for venture, consistent with venturer goals

• Compatible investment horizons

• Balanced resource allocation

• Business plan congruity

• Shared vision of control and future growth

7www.bakerdonelson.com© 2013 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

CONTRIBUTIONS

Expertise:

• R&D

• Engineering/Technical

• Planning & Budgeting

• Process and Production

Marketing Power and Prowess

• Distribution Networks

• Define by customer or by product

• Competition restrictions and channel conflict

• The Third Sales Force/Delivery Force

8www.bakerdonelson.com© 2013 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

CONTRIBUTIONS

Intellectual Property Tangled Web

• Each party's own

• Enhancements to each other's IP

• Jointly developed – who owns, or does the venture own

• Mixed ownership – One from column A, one from column B

• Disengagement options

• Updating & Enhancing

• License back and perpetual use rights

• Royalty Trust and License Rights

9www.bakerdonelson.com© 2013 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

CONTRIBUTIONS

Property and Resources

• office & back office

• production/warehouse

• technical

• rolling stock

• Lease/sublease to venture – FMV or below?

− Difference is contribution of capital

10www.bakerdonelson.com© 2013 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

CONTRIBUTIONS

Human Capital

• Executive and managerial talent

• Secondment - the detachment of a person from their regular

organization for temporary assignment elsewhere

• Integration with contributing partners – cultures; facing the common

enemy

• Avoiding dead ends and duds – not a career killer to work for JV

• Benefits harmonization

• Training and Standardization

11www.bakerdonelson.com© 2013 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

GOVERNANCE & MANAGEMENT

Board(s)

• Grand Board – representatives of both sides in proportion toinvestment

• Operating Board – VP level board of operators focused onoperational issues and integration

• Super Board – Partner CEO's or COO's to oversee direction ofventure

• Independence – should venture have non-affiliated board members?

Accounting & Reporting

• Annual Budget approved by parties

• Manage to variance

• Monthly reporting

• Separate audit

12www.bakerdonelson.com© 2013 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

GOVERNANCE & MANAGEMENT

Meetings –

• frequency

• location

• quorum

• agenda and preparation – anti-blindside rule

• participation & reports

• Real v. Show

13www.bakerdonelson.com© 2013 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

GOVERNANCE & MANAGEMENT

Supermajority/Consent of All Sides

• Amend charter or bylaws

• Capital Call

• Issue or redeem equity

• Borrow more than $x

• Capital leases

• Buy or sell real property

• Transactions with related parties

• Acquisitions

• Equity compensation to employees

• Grant indemnification

• Annual plan/budget

• tax elections

14www.bakerdonelson.com© 2013 Baker, Donelson, Bearman, Caldwell & Berkowitz, PC

GOVERNANCE & MANAGEMENT

Deadlock

• Super Board meeting

• Specialty arbitration

• Special Board Member Votes only on ties

• Mutual Buy/Sell

• Mandatory Sale

• Judicial intervention – Del. Corp. Law §273

Peter J. Kinsella 303-291-2300 2

Agenda

Day -1

Overview of IP issues arising from Entity and

Contractual JVs

Contributions

Day -2

IP Ownership

IP issues on Exit

The information provided in this presentation does not necessarily reflect the opinions of

Perkins Coie LLP, its clients or even the author.

Day 1

IP Issues Arising from Structure

Peter J. Kinsella

Peter J. Kinsella 303-291-2300

IP issues with Structure - 1

Contractual JV

One or more of the parties to the JV will need to own

the IP (either individually or jointly)

Joint ownership can cause problems when

enforcing the IP against third parties

Each party may grant a license (of a certain scope) to

the other

Entity JV

The JV can own IP, but should it?

4

Peter J. Kinsella 303-291-2300

IP issues with Structure - 2

Typical way to think about IP in a JV

Background IP – IP that exists prior to the formation

of the JV

May be licensed or assigned to the JV

Foreground IP – IP created by the JV

May be owned by the JV, if it is in entity

Will need to be owned by a party to the JV or

jointly

5

Day 1

Contributions

Peter J. Kinsella

Peter J. Kinsella 303-291-2300

Initial Contributions -1

The form of the contribution will differ depending onwhether the Joint Venture is merely a contractual JointVenture or is a legal entity

Contributions in a contractual joint venture willtypically be expressed as obligations to:

provide cash or certain rights or items to the otherparty; or

undertake certain obligations

Contributions to an entity typically take the form of anassignment, license or lease to the new entity

7

Peter J. Kinsella 303-291-2300

Initial Contributions -2

It is important to identify the form, amount and timing ofthe initial capital contributions

Cash

All at once or over time?

Intellectual property (patents, trademarks, know-how,

trade names)

Assignment or License?

Tangible property (real estate, equipment)

Assignment or Lease?

Services / Human Resources (management,

technical, marketing or administrative)

8

Peter J. Kinsella 303-291-2300

Common Issues Arising from Non-Cash Contributions

Valuation

Licenses

Permitted scope of intellectual property use

Transfer Pricing / Imputed Income Tax

Warranties concerning the contributions

Terms governing contributed services (service level,indemnification )

Export control issues

Some countries require minimum cash contributions

Tax goals may differ depending on nature of contribution

9

Peter J. Kinsella 303-291-2300

Subsequent contributions

Procedures for additional capital contributions?

Consequences of a failure to make additional capital

contributions?

partner priority loans?

Need to identify interest rate, maturity date,

security and priority entitlement to cash flow

dilution of ownership interest of a delinquent co-

venturer, and formula for calculating dilution

loss of voting rights for the delinquent co-venturer

10

Peter J. Kinsella 303-291-2300

Distributions -1 Generally, distributions are made at the discretion of the

JV's management

Some countries impose legal limitations on the

management's discretion

E.g., some countries do not permit distributions if

the JV is running at a loss or fails to maintain

minimum capital requirements

11

Peter J. Kinsella 303-291-2300

Distributions -2 Frequently, distributions are based on the current

percentage of ownership of the JV

Joint venture agreement can specify otherwise, including

by providing for:

mandatory distributions, such as

specified amounts if certain triggers are met

for pass-through entities, consider providing for

annual distributions sufficient to cover income taxes

that the parties must pay on the JV's profits.

priority of distributions (see next slide)

Consider distribution effects through ancillary documents

Consider effect of international withholding tax issues

12

Peter J. Kinsella 303-291-2300

Priority of Distributions

Consider effect of payment obligations under ancillary

agreements

Is there a priority return for initial or additional capital

contributions?

Is there a priority based on operating cash flow or other

metric?

identify interest rate on partner loans

address tax distributions (optional, mandatory or none)

consider a “clawback” if a co-venturer receives excess

distributions.

13

Day 2

Who owns the JV IP?

Peter J. Kinsella

Peter J. Kinsella 303-291-230015

IP Overview

Type of Right Scope of Coverage Example

Patents Ideas - products,processes

Telephone

Trademarks Identities, Quality Coca-Cola®

Copyrights Expressions of Ideas Movies, Books

Trade Secrets ConfidentialInformation

Strategies,Lists

Peter J. Kinsella 303-291-2300

IP Ownership Rules - 1

With respect to intellectual property, the U.S. has

different types of rules for different types of property,

absent a written agreement to the contrary, typically:

Employees retain ownership of patent rights (while

the employer will have a non-transferable license

Employers will own copyrights created by employees

within the scope of their employment

Independent contractors will own everything they

create

Note: different rules may apply in different countries

16

Peter J. Kinsella 303-291-2300

IP Ownership Rules - 2

In the United States, absent a written agreement:

people who jointly contribute to a copyrighted work

will jointly own the work, but will have an obligation to

share profits derived from the use of that work

people who joint contribute to a patented invention

will jointly own the patent, and will have the right to

exercise the rights without an obligation to share

profits

Note: different rules may apply in different countries

17

Peter J. Kinsella 303-291-2300

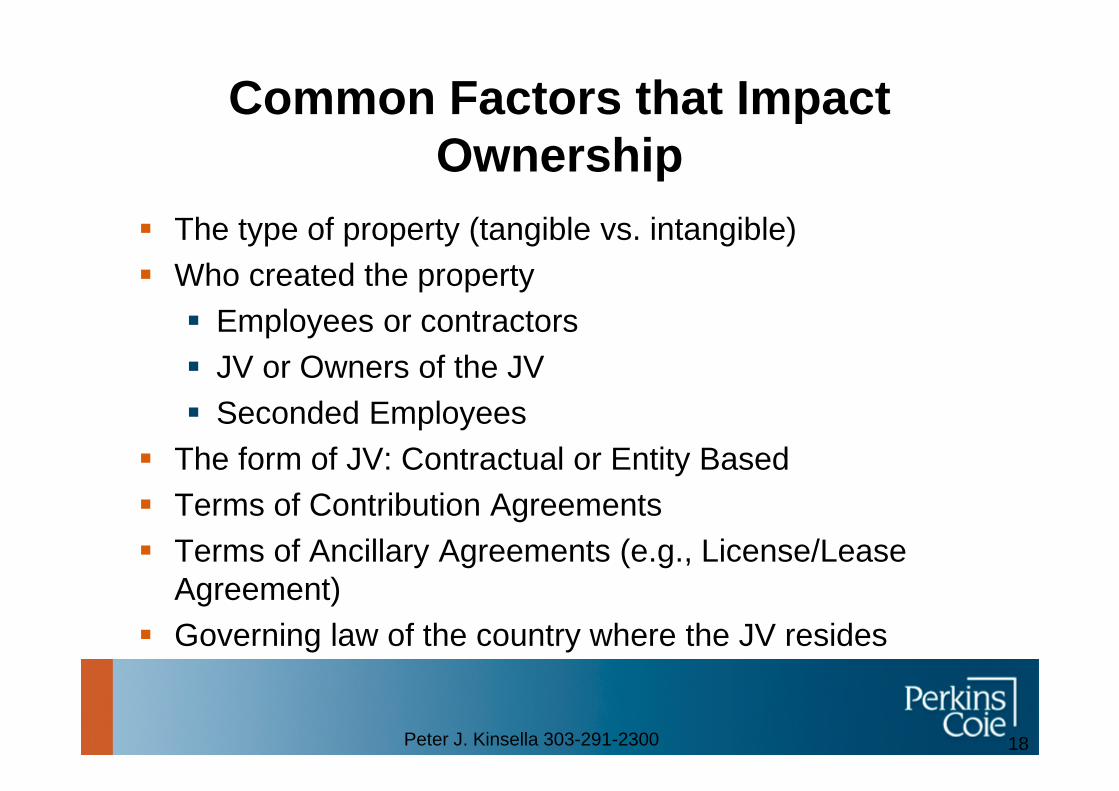

Common Factors that ImpactOwnership

The type of property (tangible vs. intangible)

Who created the property

Employees or contractors

JV or Owners of the JV

Seconded Employees

The form of JV: Contractual or Entity Based

Terms of Contribution Agreements

Terms of Ancillary Agreements (e.g., License/Lease

Agreement)

Governing law of the country where the JV resides

18

Peter J. Kinsella 303-291-2300

Issue 1: Trademark Selection

JV's often use the composite name of the co-venturer

This can create several issues:

Allowing the JV to own a composite trademark

could weaken the rights of each co-venturer in

their own trademarks

It may be difficult for the JV to obtain a trademark

registration in certain countries because each co-

venturer has independent trademark rights

19

Peter J. Kinsella 303-291-2300

Issue 2: JV needs to rely onBackground Technology

JV's often need to rely on background technology

developed by one or both of the co-venturers

Such technology is typically supplied in the form of:

a license agreement or

product supply agreement (for a key component)

Note: If background IP is licensed to the JV, the

license agreement may be used to control ownership

and rights to improvements and related technology

20

Peter J. Kinsella 303-291-2300

Issue 3: JV Will Develop NewTechnology

Need to determine whether the JV will exclusively own

the new technology or whether it will license the new

technology to the co-venturers for certain purposes

Need to determine ownership and use rights if the JV

has a co-venturer create IP for the JV

Need to determine ownership strategy when the JV

utilizes third parties for IP development

Need to develop clear ownership guidelines if the JV is

using seconded employees of a co-venturer

21

Peter J. Kinsella 303-291-2300

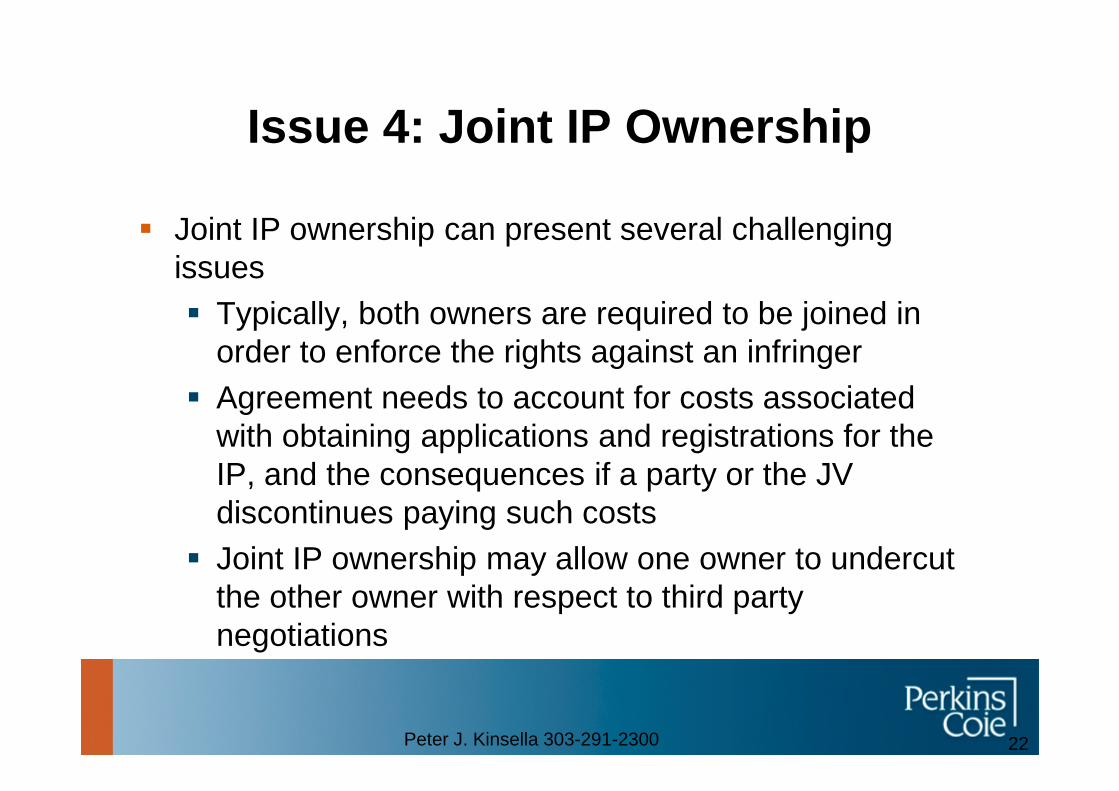

Issue 4: Joint IP Ownership

Joint IP ownership can present several challenging

issues

Typically, both owners are required to be joined in

order to enforce the rights against an infringer

Agreement needs to account for costs associated

with obtaining applications and registrations for the

IP, and the consequences if a party or the JV

discontinues paying such costs

Joint IP ownership may allow one owner to undercut

the other owner with respect to third party

negotiations

22

Peter J. Kinsella 303-291-2300

Issue 5: Exclusivity

Exclusivity issues can sometimes compliment and

overlap with the ownership provisions

Are the co-venturers restricted from engaging in any

particular activities?

Need to specifically define the activity

Need to specifically define the country

Need to specifically define the field

Need to be aware of potential anti-trust issues

23

Day 2

IP Exit Issues

Peter J. Kinsella

Peter J. Kinsella 303-291-2300

IP Exit Issues-1

Contractual JV

Termination of Cross Licenses ?

May not need to alter the ownership of the IP

established during the term of the JV

Consider whether a broader license (or IP

assignment obligation) is triggered by certain

termination events

25

Peter J. Kinsella 303-291-2300

IP Exit Issues-2

Entity JV

Any IP that is owned by the JV needs to be assigned

prior to dissolution

Common Dissolution Structures

Assign Joint Ownership to the members

Assign Ownership to one party – grant broad

“ownership like” license to the other

Consider transferability of background licenses

26

Peter J. Kinsella 303-291-230027

BiographyPeter Kinsella is a partner in the firm's Licensing and Technology and

Intellectual Property Practice groups. His practice is focused on advising

start-up, emerging and large companies on licensing and technology

transaction matters. Prior to joining the firm in 2010, Pete was a partner

with Faegre & Benson. Prior to that, he worked in various legal capacities

with Qwest Communications International, Inc. (formerly U S WEST, Inc.)

in Denver and Honeywell, Inc. in Minneapolis.

Pete offers extensive experience structuring and negotiating domestic and

international agreements in the areas of: outsourcing, product

development, software development, technology transfer, consulting

services, e-commerce, telecommunications, hosting, data sharing,

complex procurement arrangements, product distribution and sales,

contract manufacturing, OEM and ODM arrangements, marketing and

advertising services, content creation and distribution, corporate

sponsorships, hardware acquisition and various types of patent, trademark

and copyright licenses. The value of several of these transactions has

exceeded one billion dollars. He also has significant international

experience, including, joint venture, holding company, transfer pricing,

export control, and international distribution issues.