international joint ventures handbook

TRANSCRIPT

A

International Joint Ventures Handbook

Law stated as of 1 September 2015 © Baker & McKenzie all rights reserved

InternationalJoint VenturesHandbook

THE LEADING CROSS-BORDER FIRM

International Joint Ventures Handbook

Baker & McKenzie and all contributors assert their rights under the Copyright, Designs and Patents Act 1988 to be identified as the authors of this work.

IMPORTANT DISCLAIMER: The materials in this handbook are of the nature of general comment only and are not intended to be a comprehensive exposition of the issues arising in the context of joint venture transactions, nor of the law(s) relating to such transactions. The contents of this handbook are not offered as advice on any particular matter and should not be taken as such. No reader should act or refrain from acting on the basis of any matter contained in this handbook without taking specific professional advice on the particular facts and circumstances at issue. Baker & McKenzie, the editors and the contributing authors expressly disclaim all and any liability to any person in respect of the consequences of anything done or permitted to be done or omitted to be done wholly or partly in reliance upon the whole or part of any of the content herein. This handbook may qualify as “Attorney Advertising” requiring notice in some jurisdictions. Save where otherwise indicated, law and practice are stated as of 1 September 2015.

Baker & McKenzie International is a Swiss Verein with member law firms around the world and reference to “Baker & McKenzie” includes Baker & McKenzie International and its member law firms.

© 2015 Baker & McKenziewww.bakermckenzie.comAll rights reserved

i

International Joint Ventures Handbook

Law stated as of 1 September 2015 © Baker & McKenzie all rights reserved

Editor’s Note

Editor’s Note

We are pleased to present the latest edition of Baker & McKenzie’s International Joint Ventures Handbook. Drawing on our unparalleled experience in all aspects of cross-border transactional work, this handbook is intended to help decision makers understand the breadth and depth of business and legal considerations associated with international joint venture transactions and suggests some ways to navigate the joint venture journey. This handbook is organized primarily in checklist, table and questionnaire format to assist users in gathering and assessing key information that impacts the various stages of joint venture planning. It is written primarily from the perspective of the foreign or “non-local” party entering into a new jurisdiction.

This handbook is not a comprehensive treatise. Its aim is to provide a framework for those contemplating a joint venture relationship, and it focuses on equity joint ventures where the parties participate through equity in a joint venture vehicle for the purpose of conducting business together. It does not attempt to provide a detailed discussion of the planning and execution of business acquisition and disposition transactions, even though many of those elements will be present in the joint venture context, particularly when one or both parties will be contributing an existing business to the venture.

This handbook is a product of numerous contributions from various practitioners around the world, to all of whom we would like to extend our profound thanks for their time, care and expertise.

Stuart Hopper, General EditorJennifer Ferguson, Editor

September 2015

ii

International Joint Ventures Handbook

Law stated as of 1 September 2015 © Baker & McKenzie all rights reserved

Table of Contents

Table of Contents

Section 1

Overview 1

Table 1(a) Transaction Continuum 21. Basic Considerations 22. Understanding the Different Approaches 4

Table 1(b) Transaction Matrix 5Table 1(c) Comparison of Typical Contractual Joint Venture, Equity Joint Venture and Establishment of Wholly Owned Subsidiary 6

Section 2

Diligence 9

1. Local Risk Assessment 92. Compatibility Assessment 9

Table 2(a) Local Risk Assessment Checklist 11Table 2(b) Compatibility Assessment Checklist 18

Section 3

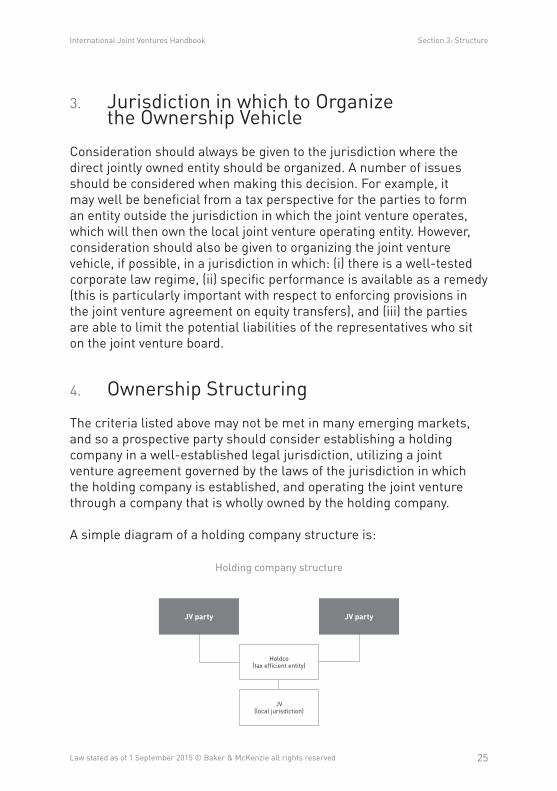

Structure 23

1. Tax Strategies 232. Structure of the Operating Vehicle 243. Jurisdiction in which to Organize the Ownership Vehicle 254. Ownership Structuring 255. Capital and Financial Interests 316. Equity Participation 387. Management Control 388. Director and Officer Liability 39

iii

International Joint Ventures Handbook

Law stated as of 1 September 2015 © Baker & McKenzie all rights reserved

Table of Contents

Table 3(a) Equity Participation Considerations 40Table 3(b) Management Control Considerations 41

Section 4

Exit and Termination 43

1. Transfer of Interests 442. Intellectual Property Considerations 463. Covenants Not to Compete 484. Other Transition Issues 49

Section 5

Other Key Considerations 51

1. Tax 512. Dispute Resolution 553. Methods for Contributing Assets 564. Covenants Not to Compete 585. Competition/Antitrust Law 596. Foreign Ownership Restrictions 637. Employee Transfers and Benefits 64

Section 6

Documentation 69

1. Confidentiality Agreement 692. Term Sheet 703. Joint Venture Agreement 704. Company Formation Documents 715. Ancillary Agreements 71

Table 6(a) Sample Term Sheet 72Supplement to Term Sheet Commentary and Alternative Provisions 77Table 6(b) Joint Venture Issues Checklist 96

iv

International Joint Ventures Handbook

Law stated as of 1 September 2015 © Baker & McKenzie all rights reserved

Table of Contents

Appendix A

Overview of D&O Duties and Liabilities in Foreign Entities 108

Appendix A1

Overview of Applicable US Laws Impacting D&O Liability 124

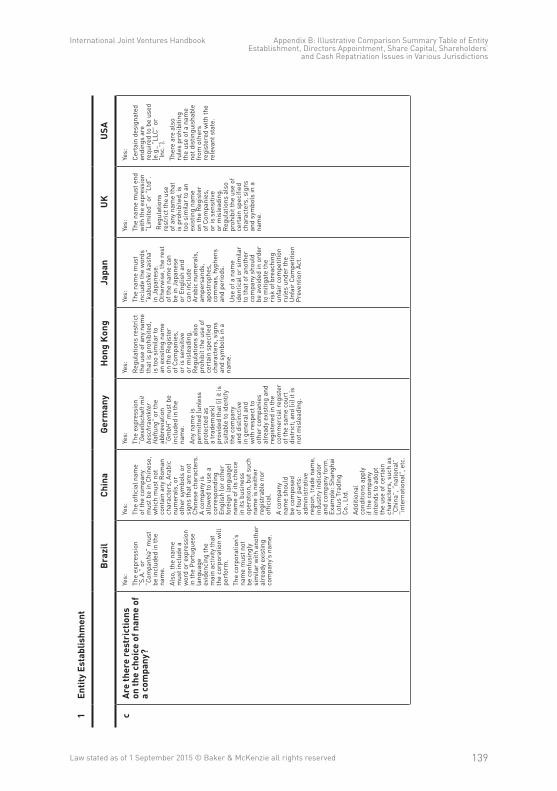

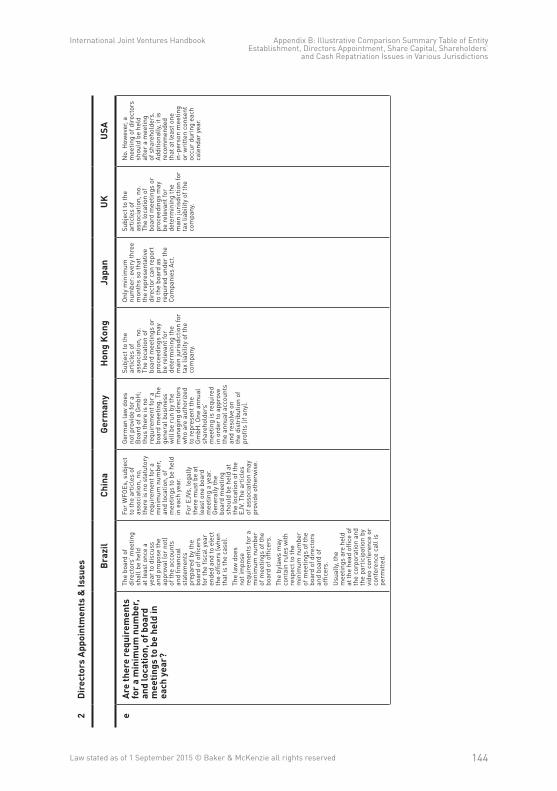

Appendix B

Illustrative Comparison Summary Table of Entity Establishment, Directors Appointment, Share Capital, Shareholders’ and Cash Repatriation Issues in Various Jurisdictions 137

Appendix C

Broad Principles of Information Exchange and ‘Gun-Jumping’ 151

Appendix C1

Overview of EU Merger Control Provisions 157

Appendix D

OECD Convention & Signatories, FCPA and UK Bribery Act 2010 Summaries 163

Appendix E

Baker & McKenzie Offices Worldwide 166

Section 1: Overview

1

International Joint Ventures Handbook

Law stated as of 1 September 2015 © Baker & McKenzie all rights reserved

Section 1

Overview

Today’s business leaders are exploring a wider range of strategic growth solutions across the whole continuum from acquisitions to alliances and joint ventures. According to a recent Baker & McKenzie report, joint ventures are one of the leading types of transactions that companies plan to pursue in the next 12 months.1 While a corporate alliance may take many forms—from a purely contractual relationship to a jointly owned entity—at its heart it is simply a commercial arrangement between two or more participants. What is agreed between those participants may involve transferring an existing business to the joint control of the parties or indirectly acquiring an existing business from another party, in which case organizing the venture will involve elements of a disposition or acquisition, or both. Alternatively, an alliance may only involve license agreements, joint marketing agreements, affiliate revenue sharing agreements or other types of agreements in which the parties agree to pursue a set of common goals.

This handbook focuses on “equity joint ventures” in which a foreign partner and a local partner participate through equity in a joint venture vehicle for the purpose of conducting business together in a particular jurisdiction.

Table 1(a) is a simplified overview of the range of typical corporate transactions to illustrate where joint ventures fit along the transaction continuum:

1 “Growing pains: Succeeding at business transformation in an increasingly complex world” Baker & McKenzie (2014)

Section 1: Overview

2

International Joint Ventures Handbook

Law stated as of 1 September 2015 © Baker & McKenzie all rights reserved

Table 1(a) Transaction Continuum

Licensing Supply,

Distribution

Non Controlling Acquisition

<50%

Controlling Acquisition

>50%

Resource Sharing

Equity Joint Venture

Full Acquisition

ContractServices

ContractualJoint Venture

Establishment ofWholly Owned Subsidary

Outsourcing Green FieldCorporate Alliance(Non-Equity)

Corporate Alliance(Equity) Traditional M&A

There are, however, endless ways in which a joint venture can be structured that defy the simple categories shown above. For example, even though the parties may set up an equity joint venture, substantial (if not all) contributions may be made via arm’s-length commercial agreements. Each opportunity thus will have its own characteristics which suggest a particular strategy, and rarely is there a single “right” or “wrong” approach.

This publication considers the different stages of the equity joint venture deal process, from evaluation of the initial opportunity and potential partner, through high level structure planning, evaluation of specific legal issues including exit and termination, and drafting the necessary transaction documents.

1. Basic Considerations

Some of the reasons commonly cited for entering into a joint venture are:2

• Fast entry into local markets;

• Low market entry costs;

2 See, for example, “Getting more value from joint ventures” Boston Consulting Group (December 2014); “A study of Joint Ventures: The challenging world of alliances” Deloitte (June 2010)

Section 1: Overview

3

International Joint Ventures Handbook

Law stated as of 1 September 2015 © Baker & McKenzie all rights reserved

• Strong local player (e.g., established customer base, market presence, production capacity, complimentary technology, employee base, distribution chain, and political savvy);

• Economical long-term resource commitment with shared risks;

• Diminished political risk (e.g., government interference, nationalization, political volatility); and

• No suitable acquisition targets or greenfield projects (e.g., establishment of wholly owned subsidiary) due to cost, local cultural resistance, foreign ownership restrictions, and other factors.

Potential downsides and risks include:

• Cultural differences between parties from different jurisdictions can lead to significant misunderstandings and inefficiencies;

• Misalignment or divergence of strategies can result in losses and a failure to achieve overall business objectives;

• Operational problems, whether the result of strategic differences, production issues, management control issues or otherwise, can limit the effectiveness of the venture;

• Lack of trust between the parties can limit cooperation;

• Decision-making and dispute resolution processes can be lengthy and costly, depending upon what mechanisms are agreed in the joint venture documentation and what practices have evolved during the life of the joint venture in this respect;

• Service and contribution agreements, which are often seen as ancillary to the relationship, can create a dependency of the joint venture on a particular party, even though an equity joint venture may be established with the overarching goal of giving the joint venture some measure of independence from the participants; and

Section 1: Overview

4

International Joint Ventures Handbook

Law stated as of 1 September 2015 © Baker & McKenzie all rights reserved

• Exit upon termination can be expensive or difficult.

That said, a joint venture may be the appropriate investment arrangement in the particular circumstances, and, like any investment arrangement, the potential downsides and risks can be identified and managed through careful diligence, thoughtful planning and appropriate documentation.

2. Understanding the Different Approaches

At the outset of any cooperative arrangement, the parties must determine the appropriate form to regulate their relationship in light of their respective goals and strategies. For example, in addition to the option of establishing an equity joint venture, the parties should consider whether any of the following types of arrangements would be appropriate in light of their respective commercial objectives:

• A supply agreement for goods or services;

• A distribution or agency agreement;

• A license or franchise agreement;

• A research and development or cooperation agreement;

• A 100% acquisition; or

• The establishment of a wholly owned subsidiary without participation from another party.

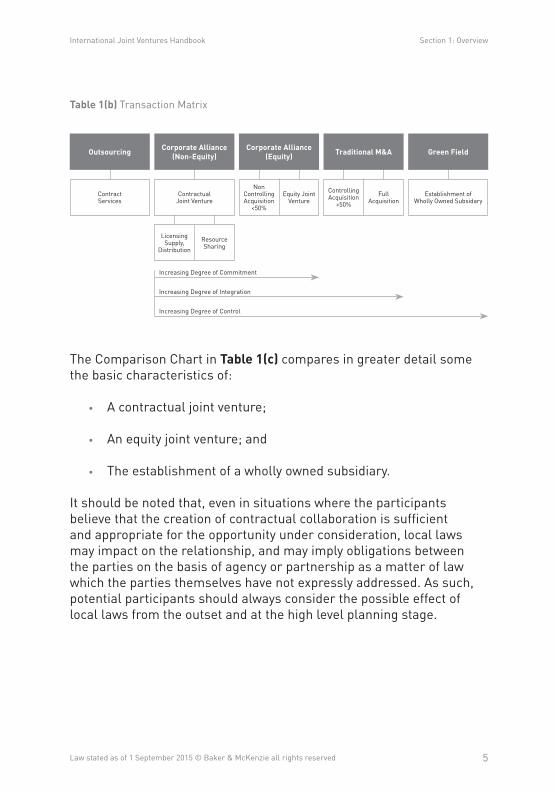

The Transaction Matrix in Table 1(b) uses the Transaction Continuum from Table 1(a) to depict broadly the levels of commitment, integration and control generally associated with these different types of relationships, and how transaction complexities can vary.

Section 1: Overview

5

International Joint Ventures Handbook

Law stated as of 1 September 2015 © Baker & McKenzie all rights reserved

Table 1(b) Transaction Matrix

Licensing Supply,

Distribution

Non Controlling Acquisition

<50%

Controlling Acquisition

>50%

Resource Sharing

Equity Joint Venture

Full Acquisition

Increasing Degree of Commitment

Increasing Degree of Integration

Increasing Degree of Control

ContractServices

ContractualJoint Venture

Establishment ofWholly Owned Subsidary

Outsourcing Green FieldCorporate Alliance(Non-Equity)

Corporate Alliance(Equity) Traditional M&A

The Comparison Chart in Table 1(c) compares in greater detail some the basic characteristics of:

• A contractual joint venture;

• An equity joint venture; and

• The establishment of a wholly owned subsidiary.

It should be noted that, even in situations where the participants believe that the creation of contractual collaboration is sufficient and appropriate for the opportunity under consideration, local laws may impact on the relationship, and may imply obligations between the parties on the basis of agency or partnership as a matter of law which the parties themselves have not expressly addressed. As such, potential participants should always consider the possible effect of local laws from the outset and at the high level planning stage.

Section 1: Overview

6

International Joint Ventures Handbook

Law stated as of 1 September 2015 © Baker & McKenzie all rights reserved

Tabl

e 1(

c) C

ompa

riso

n of

Typ

ical

Con

trac

tual

Joi

nt V

entu

re, E

quity

Joi

nt V

entu

re a

nd E

stab

lishm

ent o

f Who

lly O

wne

d Su

bsid

iary

Cont

ract

ual J

oint

Ven

ture

Equi

ty J

oint

Ven

ture

Who

lly O

wne

d Su

bsid

iary

Stru

ctur

e•

Cont

ract

bet

wee

n th

e pa

rtie

s.•

Sepa

rate

lega

l ent

ity, j

oint

ly o

wne

d by

fore

ign

part

y an

d lo

cal p

arty

.•

Sepa

rate

lega

l ent

ity, 1

00%

ow

ned

by fo

reig

n in

vest

or.

Entr

y in

to M

arke

t•

Fast

er.

• Fo

reig

n pa

rty

bene

fits

from

loca

l pa

rty’

s cu

stom

ers,

con

nect

ions

, kn

owle

dge

of c

ompe

titor

s, lo

cal

law

s an

d pr

actic

es.

• Fa

ster

.•

Fore

ign

part

y be

nefit

s fr

om lo

cal

part

y’s

cust

omer

s, c

onne

ctio

ns,

know

ledg

e of

com

petit

ors,

loca

l la

ws

and

prac

tices

.

• Sl

ower

.•

Fore

ign

inve

stor

has

to g

row

bu

sine

ss fr

om s

crat

ch (e

.g.,

hire

em

ploy

ees,

bui

ld d

eman

d, o

btai

n sa

les)

.

Star

t-up

cos

ts•

Low

er.

• Lo

wer

to m

oder

ate.

• Co

sts

of e

stab

lishi

ng a

nd

mai

ntai

ning

join

t ven

ture

veh

icle

ca

n be

sha

red.

• H

ighe

r.•

Cost

s of

est

ablis

hing

and

m

aint

aini

ng c

orpo

rate

ent

ity b

orne

so

lely

by

fore

ign

inve

stor

.

Res

ourc

e Co

mm

itmen

t•

Low

er.

• Fo

reig

n pa

rty

may

, e.g

., lic

ense

in

telle

ctua

l pro

pert

y or

sup

ply

good

s.•

Lice

nsee

/pur

chas

er p

ays

roya

lties

/ca

sh.

• Lo

wer

to m

oder

ate.

• Fo

reig

n pa

rty

ofte

n co

ntri

bute

s m

anag

emen

t exp

ertis

e,

inte

llect

ual p

rope

rty

and

know

-ho

w.

• Lo

cal p

arty

ofte

n co

ntri

bute

s em

ploy

ees,

cus

tom

ers,

pla

nt a

nd

faci

litie

s.

• H

ighe

r.•

Fore

ign

inve

stor

mus

t hir

e lo

cal

empl

oyee

s an

d/or

tran

sfer

ex

patr

iate

s, p

urch

ase

raw

goo

ds,

etc.

Inte

llect

ual P

rope

rty

Ris

k•

Hig

her.

• Po

tent

ially

sha

ring

or

givi

ng

away

IP to

oth

er p

arty

(i.e

., a

com

petit

or).

• H

ighe

r.•

Pote

ntia

lly s

hari

ng o

r gi

ving

aw

ay

IP to

loca

l par

ty (i

.e.,

a co

mpe

titor

).

• Lo

wer

.•

IP le

ss e

xpos

ed to

a c

ompe

titor

be

caus

e su

bsid

iary

is w

holly

ow

ned.

Section 1: Overview

7

International Joint Ventures Handbook

Law stated as of 1 September 2015 © Baker & McKenzie all rights reserved

Cont

ract

ual J

oint

Ven

ture

Equi

ty J

oint

Ven

ture

Who

lly O

wne

d Su

bsid

iary

Ret

urn

on In

vest

men

t•

Low

er.

• R

oyal

ties

gene

rally

yie

ld lo

wer

re

turn

s th

an e

quity

.

• M

oder

ate

to h

ighe

r.•

Equi

ty g

ener

ally

yie

lds

high

er

retu

rns

than

roya

lties

, but

retu

rns

are

shar

ed w

ith o

ther

join

t ven

ture

pa

rty.

• Fo

reig

n pa

rty

may

hav

e lic

ense

d in

telle

ctua

l pro

pert

y to

the

join

t ve

ntur

e ve

hicl

e in

exc

hang

e fo

r ro

yalty

pay

men

ts.

• H

ighe

r.•

Equi

ty g

ener

ally

yie

lds

high

er

retu

rns

than

roya

lties

.

Mar

ket P

rese

nce

• Lo

wer

.•

Fore

ign

part

y no

t pre

sent

in lo

cal

mar

ket e

xcep

t thr

ough

loca

l par

ty.

• M

oder

ate

to h

ighe

r.•

Fore

ign

part

y ha

s di

rect

acc

ess

to

loca

l mar

ket t

hrou

gh lo

cal p

arty

.

• H

ighe

r.•

Fore

ign

inve

stor

has

dir

ect

pres

ence

in lo

cal m

arke

t.

Polit

ical

Ris

k•

Low

er.

• Fo

reig

n pa

rty

(lice

nsor

) doe

s no

t be

ar r

isk

of e

ntry

into

vol

atile

m

arke

t.

• M

oder

ate.

• Fo

reig

n pa

rty

bear

s pa

rtia

l ris

k of

pol

itica

lly v

olat

ile m

arke

t, go

vern

men

t int

erfe

renc

e,

expr

opri

atio

n.

• H

ighe

r.•

Fore

ign

inve

stor

bea

rs fu

ll ri

sk

of p

oliti

cally

vol

atile

mar

ket,

gove

rnm

ent i

nter

fere

nce,

ex

prop

riat

ion.

Com

petit

ion

Law

Ris

k•

Mod

erat

e to

hig

her.

• Co

llabo

ratio

n of

com

petit

ors

may

tr

igge

r co

mpe

titio

n la

w o

blig

atio

ns

and

issu

es.

• M

oder

ate

to h

ighe

r.•

Part

icip

atio

n by

com

petit

ors

in

join

t ven

ture

veh

icle

may

trig

ger

com

petit

ion

law

issu

es.

• N

one.

• N

o co

llabo

ratio

n w

ith a

ano

ther

pa

rty,

ther

efor

e no

com

petit

ion

law

co

ncer

n.

Cont

rol o

ver

Stra

tegy

• Lo

wer

.•

Min

imal

inte

grat

ion

of fo

reig

n pa

rty

and

loca

l par

ty’s

glo

bal

stra

tegy

.

• M

oder

ate.

• Ce

rtai

n de

gree

of c

ontr

ol o

ver

join

t ve

ntur

e ve

hicl

e’s

glob

al s

trat

egy

• D

epen

dent

upo

n st

rate

gic

obje

ctiv

es o

f loc

al p

arty

and

abi

lity

of b

oth

part

ies

to a

dher

e to

agr

eed

stra

tegy

for

the

dura

tion

of th

e jo

int v

entu

re.

• H

ighe

r.•

Com

plet

e co

ntro

l ove

r w

holly

ow

ned

subs

idia

ry’s

glo

bal s

trat

egy.

Section 1: Overview

8

International Joint Ventures Handbook

Law stated as of 1 September 2015 © Baker & McKenzie all rights reserved

Cont

ract

ual J

oint

Ven

ture

Equi

ty J

oint

Ven

ture

Who

lly O

wne

d Su

bsid

iary

Com

plex

ity o

f Cor

pora

te

Gove

rnan

ce•

Low

er.

• N

o jo

int c

orpo

rate

con

trol

.•

Hig

her.

• Co

nflic

ting

stra

tegi

c vi

sion

s,

diffe

rent

man

agem

ent/

cultu

ral s

tyle

s, u

nequ

al c

apita

l in

vest

men

ts, a

nd o

ther

mat

eria

l di

ffere

nces

ofte

n re

quir

e co

mpl

ex c

orpo

rate

gov

erna

nce

mec

hani

sms.

• Lo

wer

.•

Fore

ign

inve

stor

can

exe

rcis

e fu

ll co

ntro

l ove

r w

holly

ow

ned

subs

idia

ry.

Mar

ket F

eedb

ack

• Lo

wer

.•

No

stan

d-al

one

entit

y fo

r cu

stom

ers

to id

entif

y w

ith.

• M

oder

ate

to h

ighe

r.•

Join

t ven

ture

veh

icle

may

pro

vide

a

dire

ct id

entit

y an

d pr

esen

ce in

th

e m

arke

t.

• M

oder

ate

to h

ighe

r.•

Who

lly o

wne

d su

bsid

iary

pro

vide

s di

rect

iden

tity

and

pres

ence

in th

e m

arke

t.

Form

ality

• M

oder

ate.

• N

eed

appr

opri

ate

cont

ract

s.•

No

need

to fo

rm a

n en

tity.

• H

ighe

r.•

Nee

d a

join

t ven

ture

agr

eem

ent

and

mus

t for

m jo

int v

entu

re e

ntity

.•

Poss

ible

anc

illar

y ag

reem

ents

(e

.g.,

inte

llect

ual p

rope

rty

licen

se, m

anag

emen

t ser

vice

s,

shar

ehol

der

righ

ts a

gree

men

t).

• M

oder

ate.

• N

eed

to e

stab

lish

who

lly o

wne

d su

bsid

iary

.

Com

plex

ity o

f D

ocum

enta

tion

• M

oder

ate

to h

ighe

r.•

Neg

otia

tion

of li

cens

e m

ay b

e co

mpl

ex.

• H

ighe

r.•

Neg

otia

tion

of p

rofit

-sha

ring,

m

anag

emen

t, et

c., m

ay b

e co

mpl

ex.

• Lo

wer

.•

No

coun

terp

arty

or

join

t ven

ture

pa

rtne

r.

Term

inat

ion

Ris

k•

Mod

erat

e to

hig

her.

• M

ay b

e di

fficu

lt to

obt

ain

mar

ket

inte

llige

nce

and

tran

sfer

join

tly-

deve

lope

d pr

oduc

ts o

ut o

f joi

nt

vent

ure

(i.e.

, cos

t and

ow

ners

hip

issu

es).

• M

oder

ate

to h

ighe

r.•

May

be

diffi

cult

to o

btai

n m

arke

t in

telli

genc

e an

d tr

ansf

er jo

intly

-de

velo

ped

prod

ucts

out

of j

oint

ve

ntur

e (i.

e., c

ost a

nd o

wne

rshi

p is

sues

).•

Pote

ntia

l for

con

flict

ove

r in

telle

ctua

l pro

pert

y de

velo

ped

duri

ng c

ours

e of

join

t ven

ture

.•

Buy-

out o

r ter

min

atio

n pr

oced

ures

can

be e

xpen

sive

and

tim

e-co

nsum

ing.

• Lo

wer

/non

e.•

Fore

ign

inve

stor

ow

ns 1

00%

of

subs

idia

ry a

nd, t

here

fore

, all

of it

s as

sets

.

Section 2: Diligence

9

International Joint Ventures Handbook

Law stated as of 1 September 2015 © Baker & McKenzie all rights reserved

Section 2

Diligence

1. Local Risk Assessment

An international joint venture implies an ongoing relationship in a market that may be unfamiliar to at least one of the parties. Especially where the joint venture will conduct business in an emerging market, the diligence exercise should thus include an assessment of the particular risks that are unique to that local market, including political, business, legal, and cultural risks. The Local Risk Assessment Checklist in Table 2(a) is designed to assist the analysis of these types of risks.

2. Compatibility Assessment

A joint venture also implies a degree of cooperation between the parties. An important aspect of the joint venture diligence exercise should be an evaluation of factors that may indicate compatibility between the prospective parties to assess the prospects of a successful joint venture. The Compatibility Assessment Checklist in Table 2(b) is intended to identify specific operational and non-operational areas for review in this regard. This checklist can also be used to help monitor the relationship throughout the life cycle of the joint venture.

Bear in mind, however, that:

• many of these factors can only be assessed through frank discussions between the parties;

• the parties may not be forthcoming until they know the transaction is likely to proceed; and

Section 2: Diligence

10

International Joint Ventures Handbook

Law stated as of 1 September 2015 © Baker & McKenzie all rights reserved

• cultural sensitivities may impact the level and nature of the diligence exercise,

and so a compatibility assessment is often easier said than done. Nevertheless, it is critical to include in the diligence process those individuals who will ultimately be involved in the management of the joint venture so they can begin to develop a working relationship and head off potential problems early in the joint venture’s life cycle.

The information and tools included in this section are not intended to be static, and the levels of importance of the individual factors will undoubtedly vary depending on the particulars of the party proposing to enter into the joint venture, and its objectives for the specific opportunity.

Section 2: Diligence

11

International Joint Ventures Handbook

Law stated as of 1 September 2015 © Baker & McKenzie all rights reserved

Tabl

e 2(

a) L

ocal

Ris

k As

sess

men

t Che

cklis

tPo

litic

al a

nd B

usin

ess

Ris

ks

Ris

kIs

sue

Poss

ible

Sol

utio

ns

Stab

ility

of L

ocal

Go

vern

men

t•

Be

clea

r as

to w

hat f

orm

of g

over

nmen

t is

in p

lace

an

d ho

w s

tabl

e it

is (e

.g.,

new

or

mat

ure

dem

ocra

cy/

olig

arch

y/di

ctat

orsh

ip/s

ingl

e pa

rty

stat

e/ab

solu

tist

mon

arch

y or

oth

er fo

rm o

f gov

ernm

ent,

sepa

ratio

n of

pow

ers,

civ

ilian

con

trol

s, fr

ee p

ress

, fre

edom

of

asso

ciat

ion/

cons

cien

ce, r

ecen

t his

tory

of i

nsta

bilit

y)?

• Co

nsid

er a

ny p

ossi

ble

repu

tatio

nal r

isks

(in

addi

tion

to fi

nanc

ial a

nd le

gal r

isks

) tha

t may

ari

se o

n en

teri

ng

into

bus

ines

s in

uns

tabl

e re

gion

s/w

ith u

nsav

ory

regi

mes

(see

Rep

utat

ion

Ris

k C

onsi

dera

tions

in

Tabl

e 2(

b) b

elow

).

• O

ne w

ay to

ass

ess

stab

ility

is to

exa

min

e co

untr

y st

udie

s pr

epar

ed b

y go

vern

men

t age

ncie

s, in

clud

ing

thos

e of

the

US

Dep

artm

ent o

f Sta

te, t

he C

IA W

orld

Fa

ct B

ook,

as

wel

l as

glob

al o

r lo

cal m

edia

suc

h as

th

e B

BC’

s Co

untr

y Pr

ofile

s, T

he E

cono

mis

t’s W

orld

in

Figu

res

and

loca

l new

spap

ers.

• M

inim

ize

capi

tal i

nves

tmen

t (re

serv

e) in

the

join

t ve

ntur

e en

tity.

• D

elay

unt

il st

abili

ty in

crea

ses.

Corr

uptio

n an

d An

ti-Co

rrup

tion

Reg

ulat

ion

• Is

cor

rupt

ion

com

mon

?•

If so

, can

the

join

t ven

ture

effe

ctiv

ely

oper

ate

its

busi

ness

with

out p

artic

ipat

ing

in c

orru

ptio

n?

• A

good

sta

rtin

g po

int t

o as

sess

cou

ntry

cor

rupt

ion

is

to c

onsu

lt Tr

ansp

aren

cy In

tern

atio

nal’s

Cor

rupt

ion

Perc

eptio

n In

dex

(see

als

o Ap

pend

ix D

- O

ECD

Co

nven

tion

& S

igna

tori

es, F

CPA

and

UK

Bri

bery

Act

20

10 S

umm

arie

s fo

r ov

ervi

ews

of s

ome

of th

e ke

y an

ti-br

iber

y an

d co

rrup

tion

regi

mes

whi

ch h

ave

extr

a-te

rrito

rial

app

licab

ility

).•

Esta

blis

h an

d im

plem

ent a

mea

ning

ful c

ompl

ianc

e pr

ogra

m th

at c

onta

ins

stri

ct in

tern

al p

olic

ies

agai

nst c

orru

pt p

ract

ices

. Thi

s re

quir

es e

ffect

ive

com

mun

icat

ion

to th

e jo

int v

entu

re’s

em

ploy

ees,

as

wel

l as

on-g

oing

mon

itori

ng.

• In

clud

e ap

prop

riat

e re

pres

enta

tions

and

cov

enan

ts in

th

e jo

int v

entu

re a

gree

men

t and

impo

se p

enal

ties

that

al

ign

the

join

t ven

ture

par

ties

in th

e ou

tcom

e.•

Cond

uct p

riva

te in

vest

igat

ion

of th

e po

tent

ial p

artn

er

and

key

empl

oyee

s.

Section 2: Diligence

12

International Joint Ventures Handbook

Law stated as of 1 September 2015 © Baker & McKenzie all rights reserved

Ris

kIs

sue

Poss

ible

Sol

utio

ns

Curr

ency

Ris

k•

Is th

e lo

cal c

urre

ncy

conv

ertib

le?

• If

the

curr

ency

can

not b

e co

nver

ted

dire

ctly

, do

alte

rnat

ive

mea

ns o

f con

vers

ion

exis

t?•

Is th

e cu

rren

cy m

arke

t (or

cur

renc

y sy

stem

) sta

ble?

• D

o th

e ex

chan

ge c

ontr

ol/c

urre

ncy

law

s of

the

juri

sdic

tion

rest

rict

the

paym

ent o

f div

iden

ds o

r m

ovem

ent o

f cap

ital?

Doe

s th

e jo

int v

entu

re e

ntity

form

re

stri

ct th

e pa

ymen

t of d

ivid

ends

? Ar

e th

ere

any

way

s to

ove

rcom

e th

e re

stri

ctio

ns?

• H

edge

cur

renc

y ri

sk w

ith d

eriv

ativ

es.

• O

btai

n ex

empt

ions

as

a co

nditi

on to

inve

stm

ent.

• Co

nduc

t joi

nt v

entu

re in

con

vert

ible

cur

renc

y.

Loca

l Bus

ines

s R

isks

• D

oes

the

loca

l eco

nom

y ha

ve a

his

tory

of s

tabi

lity

or

vola

tility

? •

Coul

d m

anuf

actu

ring

and

/or

labo

r co

sts,

incr

ease

dr

astic

ally

?•

Are

labo

r un

ions

gen

eral

ly re

cogn

ized

in th

e ju

risd

ictio

n? If

yes

, how

pow

erfu

l are

they

?•

Is lo

cal c

onsu

mer

beh

avio

r/pr

efer

ence

sus

cept

ible

to

dras

tic c

hang

e?•

Are

ther

e ex

istin

g or

pot

entia

l loc

al c

ompe

titor

s to

who

m th

e lo

cal g

over

nmen

t can

giv

e sp

ecia

l pr

ivile

ges?

• B

uy in

sura

nce

polic

ies

for

coun

try

risk

s.•

Asse

ss lo

cal b

usin

ess

risk

s in

det

ail a

nd u

se re

alis

tic

or m

odes

t dis

coun

t rat

es.

• Ve

ntur

e w

ith p

oliti

cally

sav

vy lo

cal p

artn

er.

• W

ork

with

loca

l bus

ines

s, la

bor

and

polit

ical

lead

ers

to

obta

in in

vest

men

t and

oth

er lo

cal s

uppo

rt.

Section 2: Diligence

13

International Joint Ventures Handbook

Law stated as of 1 September 2015 © Baker & McKenzie all rights reserved

Lega

l Ris

ks

Ris

kIs

sue

Poss

ible

Sol

utio

ns

Rul

e of

Law

• D

oes

the

targ

et c

ount

ry h

ave

wel

l-es

tabl

ishe

d ru

les

of

law

in g

ener

al o

r do

offi

cial

s ha

ve s

igni

fican

t dis

cret

ion

with

resp

ect t

o in

terp

reta

tion

and

enfo

rcem

ent?

• Se

lect

gov

erni

ng la

w a

nd d

ispu

te re

solu

tion

foru

m o

f a

juri

sdic

tion

with

wel

l-de

velo

ped

and

flexi

ble

lega

l sy

stem

.

Enfo

rcea

bilit

y of

Con

trac

tual

Sa

fegu

ards

in J

oint

Ven

ture

D

ocum

ents

• Is

the

choi

ce o

f law

and

foru

m v

alid

and

enf

orce

able

?•

Are

pena

lty c

laus

es v

alid

and

enf

orce

able

?•

Is a

n in

junc

tion

orde

r to

enf

orce

con

trac

tual

rig

hts

avai

labl

e?•

Can

loca

l cou

rts

enfo

rce

spec

ific

perf

orm

ance

?•

Are

loca

l cou

rts

stri

ctly

impa

rtia

l or

do th

ey te

nd to

ex

hibi

t bia

s (to

war

ds lo

cal e

ntiti

es)?

• Ar

e ju

dgm

ents

of l

ocal

cou

rts

pred

icta

ble?

• H

ow lo

ng w

ill it

usu

ally

take

to o

btai

n an

d en

forc

e a

judg

men

t?•

Doe

s th

e lo

cal g

over

nmen

t hav

e st

rict

enf

orce

men

t pr

oced

ures

?•

Is th

e lo

cal c

ount

ry p

arty

to in

tern

atio

nal t

reat

ies

for

the

enfo

rcem

ent o

f for

eign

mon

ey ju

dgm

ents

and

arb

itral

aw

ards

?

• Pr

ovid

e fo

r ar

bitr

atio

n in

the

join

t ven

ture

agr

eem

ent.

• Se

lect

gov

erni

ng la

w a

nd fo

rum

of a

juri

sdic

tion

with

w

ell-

deve

lope

d an

d fle

xibl

e le

gal s

yste

m.

Section 2: Diligence

14

International Joint Ventures Handbook

Law stated as of 1 September 2015 © Baker & McKenzie all rights reserved

Ris

kIs

sue

Poss

ible

Sol

utio

ns

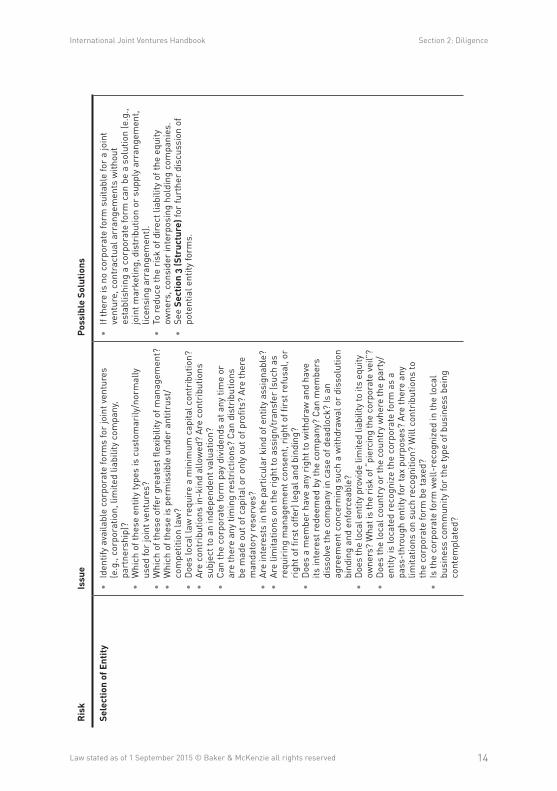

Sele

ctio

n of

Ent

ity•

Iden

tify

avai

labl

e co

rpor

ate

form

s fo

r jo

int v

entu

res

(e.g

., co

rpor

atio

n, li

mite

d lia

bilit

y co

mpa

ny,

part

ners

hip)

?•

Whi

ch o

f the

se e

ntity

type

s is

cus

tom

arily

/nor

mal

ly

used

for

join

t ven

ture

s?•

Whi

ch o

f the

se o

ffer

grea

test

flex

ibili

ty o

f man

agem

ent?

• W

hich

of t

hese

is p

erm

issi

ble

unde

r an

titru

st/

com

petit

ion

law

?•

Doe

s lo

cal l

aw re

quir

e a

min

imum

cap

ital c

ontr

ibut

ion?

• Ar

e co

ntri

butio

ns in

-kin

d al

low

ed?

Are

cont

ribu

tions

su

bjec

t to

an in

depe

nden

t val

uatio

n?•

Can

the

corp

orat

e fo

rm p

ay d

ivid

ends

at a

ny ti

me

or

are

ther

e an

y tim

ing

rest

rict

ions

? Ca

n di

stri

butio

ns

be m

ade

out o

f cap

ital o

r on

ly o

ut o

f pro

fits?

Are

ther

e m

anda

tory

rese

rves

?•

Are

inte

rest

s in

the

part

icul

ar k

ind

of e

ntity

ass

igna

ble?

• Ar

e lim

itatio

ns o

n th

e ri

ght t

o as

sign

/tra

nsfe

r (s

uch

as

requ

irin

g m

anag

emen

t con

sent

, rig

ht o

f firs

t ref

usal

, or

righ

t of fi

rst o

ffer)

lega

l and

bin

ding

?•

Doe

s a

mem

ber

have

any

rig

ht to

with

draw

and

hav

e its

inte

rest

rede

emed

by

the

com

pany

? Ca

n m

embe

rs

diss

olve

the

com

pany

in c

ase

of d

eadl

ock?

Is a

n ag

reem

ent c

once

rnin

g su

ch a

with

draw

al o

r di

ssol

utio

n bi

ndin

g an

d en

forc

eabl

e?•

Doe

s th

e lo

cal e

ntity

pro

vide

lim

ited

liabi

lity

to it

s eq

uity

ow

ners

? W

hat i

s th

e ri

sk o

f “pi

erci

ng th

e co

rpor

ate

veil”

?•

Doe

s th

e lo

cal c

ount

ry o

r th

e co

untr

y w

here

the

part

y/en

tity

is lo

cate

d re

cogn

ize

the

corp

orat

e fo

rm a

s a

pass

-thr

ough

ent

ity fo

r ta

x pu

rpos

es?

Are

ther

e an

y lim

itatio

ns o

n su

ch re

cogn

ition

? W

ill c

ontr

ibut

ions

to

the

corp

orat

e fo

rm b

e ta

xed?

• Is

the

corp

orat

e fo

rm w

ell-

reco

gniz

ed in

the

loca

l bu

sine

ss c

omm

unity

for

the

type

of b

usin

ess

bein

g co

ntem

plat

ed?

• If

ther

e is

no

corp

orat

e fo

rm s

uita

ble

for

a jo

int

vent

ure,

con

trac

tual

arr

ange

men

ts w

ithou

t es

tabl

ishi

ng a

cor

pora

te fo

rm c

an b

e a

solu

tion

(e.g

., jo

int m

arke

ting,

dis

trib

utio

n or

sup

ply

arra

ngem

ent,

licen

sing

arr

ange

men

t).•

To re

duce

the

risk

of d

irec

t lia

bilit

y of

the

equi

ty

owne

rs, c

onsi

der

inte

rpos

ing

hold

ing

com

pani

es.

• Se

e Se

ctio

n 3

(Str

uctu

re) f

or fu

rthe

r di

scus

sion

of

pote

ntia

l ent

ity fo

rms.

Section 2: Diligence

15

International Joint Ventures Handbook

Law stated as of 1 September 2015 © Baker & McKenzie all rights reserved

Ris

kIs

sue

Poss

ible

Sol

utio

ns

Inte

llect

ual P

rope

rty

• D

oes

the

loca

l gov

ernm

ent h

ave

wel

l-es

tabl

ishe

d in

telle

ctua

l pro

pert

y la

ws

and

are

they

regu

larl

y en

forc

ed?

• Ar

e cr

oss-

bord

er tr

ansf

ers

of in

telle

ctua

l pro

pert

y by

as

sign

men

t or

licen

sing

sub

ject

to g

over

nmen

t rev

iew

/co

ntro

l?•

Wha

t are

the

man

dato

ry r

ules

rega

rdin

g em

ploy

ee

owne

rshi

p in

inve

ntio

ns (e

.g.,

in s

ome

coun

trie

s,

inve

ntor

s ar

e en

title

d to

a c

erta

in le

vel o

f com

pens

atio

n fo

r su

cces

sful

ly e

xplo

ited

inve

ntio

ns w

hich

may

in

crea

se in

telle

ctua

l pro

pert

y de

velo

pmen

t cos

ts)?

• D

oes

loca

l law

hav

e m

oral

rig

hts

for

auth

ors/

crea

tors

of

copy

righ

t wor

ks w

hich

can

not b

e w

aive

red

or a

ssig

ned?

3 •

Doe

s lo

cal l

aw p

rohi

bit o

r lim

it th

e ri

ght o

f a c

ontr

ibut

or

to re

ceiv

e an

aut

omat

ic a

ssig

nmen

t or

licen

se-b

ack

of im

prov

emen

ts m

ade

by a

lice

nsee

(i.e

., th

e jo

int

vent

ure)

?•

Doe

s lo

cal l

aw re

quir

e th

at in

telle

ctua

l pro

pert

y de

velo

ped

usin

g go

vern

men

tal f

unds

/spo

nsor

ship

re

mai

n un

der

the

owne

rshi

p of

a lo

cal e

ntity

? (T

his

coul

d im

pact

inte

llect

ual p

rope

rty

owne

rshi

p up

on

term

inat

ion

or e

xit).

• D

oes

loca

l law

requ

ire

that

a re

gist

ered

IP r

ight

, (su

ch

as tr

adem

arks

) can

onl

y be

regi

ster

ed b

y an

ent

ity

loca

ted

and/

or d

oing

bus

ines

s lo

cally

?

• Im

plem

ent a

bus

ines

s st

ruct

ure

whe

re p

ropr

ieta

ry

info

rmat

ion

will

not

be

disc

lose

d to

the

loca

l par

ty.

• Es

tabl

ish

and

impl

emen

t str

ict i

nter

nal c

onfid

entia

lity

polic

ies

for

the

join

t ven

ture

ent

ity.

• Fa

ctor

into

on-

goin

g co

ntri

butio

ns a

nd d

istr

ibut

ions

an

y re

quir

ed c

ompe

nsat

ion

aris

ing

as a

resu

lt of

em

ploy

ee-o

wne

d in

vent

ions

.•

Esta

blis

h th

e jo

int v

entu

re in

a ju

risd

ictio

n w

ith

favo

rabl

e in

telle

ctua

l pro

pert

y la

ws.

3 S

ome

juri

sdic

tions

(e.g

., th

e U

nite

d K

ingd

om) h

ave

mor

al r

ight

s fo

r th

e au

thor

s or

cre

ator

s of

cop

yrig

ht w

orks

(e.g

., to

be

reco

gniz

ed a

s th

e au

thor

) eve

n if

the

righ

t its

elf h

as b

een

assi

gned

to a

thir

d pa

rty.

Section 2: Diligence

16

International Joint Ventures Handbook

Law stated as of 1 September 2015 © Baker & McKenzie all rights reserved

Ris

kIs

sue

Poss

ible

Sol

utio

ns

Antit

rust

• W

hat a

re th

e ke

y pr

oduc

t/se

rvic

e se

ctor

s in

whi

ch th

e pa

rtie

s ar

e ac

tive?

• W

here

will

the

join

t ven

ture

mak

e sa

les

or p

rovi

de

serv

ices

? •

Wha

t is

the

stru

ctur

e of

the

mar

ket i

n w

hich

the

join

t ve

ntur

e w

ill o

pera

te?

• D

oes

the

join

t ven

ture

invo

lve

com

petit

ors?

If s

o, w

hat

are

thei

r m

arke

t sha

res?

• W

hat s

truc

ture

will

the

join

t ven

ture

util

ize?

• D

oes

the

loca

l gov

ernm

ent h

ave

wel

l-de

velo

ped

antit

rust

regu

latio

ns a

nd a

re th

ey re

gula

rly

enfo

rced

?

• Co

nsid

er e

arly

on

whe

ther

mer

ger

cont

rol

notifi

catio

ns w

ill b

e re

quir

ed/a

dvis

able

.•

If co

mpe

titor

s ar

e in

volv

ed, c

onsi

der

earl

y on

whe

ther

th

e m

arke

t sha

res

of th

e pa

rtie

s w

ill p

recl

ude

the

join

t ve

ntur

e.•

Choo

se a

join

t ven

ture

str

uctu

re th

at w

ill n

ot v

iola

te

appl

icab

le a

ntitr

ust l

aws.

Fore

ign

Inve

stm

ent L

aws

• D

o in

vest

men

ts b

y a

fore

ign

pers

on re

quire

pri

or

appr

oval

of a

ny g

over

nmen

tal a

utho

ritie

s? If

not

, is

ther

e an

opt

ion

to v

olun

tari

ly n

otify

, and

is th

is a

dvis

able

?•

Doe

s lo

cal l

aw a

llow

a fo

reig

n pe

rson

to o

wn

a m

ajor

ity

of th

e sh

ares

in a

com

pany

?

• Co

nsid

er e

arly

on

whe

ther

fore

ign

inve

stm

ent fi

lings

w

ill b

e re

quir

ed/a

dvis

able

. Eve

n a

min

ority

fore

ign

inve

stm

ent m

ay re

quir

e fo

reig

n in

vest

men

t law

ap

prov

al.

Reg

ulat

ion

(Lic

ensi

ng)

• Ar

e fo

reig

n co

mpa

nies

allo

wed

to h

ave

a lic

ense

to d

o bu

sine

ss w

ithou

t the

par

ticip

atio

n of

the

loca

l par

ty?

• If

the

maj

ority

of s

hare

s in

the

join

t ven

ture

are

ow

ned

by a

fore

ign

com

pany

, is

the

join

t ven

ture

allo

wed

to

have

suc

h a

licen

se?

• Co

nsid

er e

arly

on

whe

ther

par

ticip

atio

n of

loca

l par

ty

is re

quir

ed.

Acco

untin

g &

Com

plia

nce

• D

oes

loca

l cor

pora

te la

w s

peci

fy a

ccou

ntin

g ru

les

for

the

part

icul

ar e

ntity

type

s or

are

the

part

ies

free

to c

hoos

e?

Is th

ere

any

limita

tion

on th

e ab

ility

of t

he n

on-l

ocal

par

ty

to re

quire

the

use

of it

s ow

n ac

coun

ting

stan

dard

s?•

Are

any

spec

ific

com

plia

nce

requ

irem

ents

of t

he n

on-

loca

l par

ty a

ccep

tabl

e lo

cally

?•

Is th

e fin

anci

al re

port

ing

of th

e jo

int v

entu

re s

ubje

ct

to th

e re

quire

men

t tha

t one

or

both

par

ties

mai

ntai

n ad

equa

te in

tern

al c

ontr

ols?

• R

equi

re th

e jo

int v

entu

re e

ntity

to a

dopt

acc

ount

ing

stan

dard

s th

at a

re a

s cl

ose

as p

ossi

ble

to th

e no

n-lo

cal

part

y’s (e

.g.,

sam

e fis

cal y

ear)

.•

Req

uire

fina

ncia

l sta

tem

ents

to b

e pr

epar

ed in

ac

cord

ance

with

IFR

S, G

AAP

or o

ther

app

licab

le

acco

untin

g st

anda

rds.

• R

etai

n pe

rson

nel a

t the

join

t ven

ture

who

are

ver

sed

in

appl

icab

le s

ecur

ities

and

acc

ount

ing

requ

irem

ents

with

re

spec

t to

inte

rnal

con

trol

s ov

er fi

nanc

ial r

epor

ting.

Man

agem

ent

• Ar

e th

ere

spec

ific

lega

l ris

ks to

indi

vidu

als

in

man

agem

ent p

ositi

ons?

(See

App

endi

x A

- O

verv

iew

of

D&

O D

utie

s an

d Li

abili

ties

in F

orei

gn E

ntiti

es).

• B

uy D

&O

Insu

ranc

e.

Section 2: Diligence

17

International Joint Ventures Handbook

Law stated as of 1 September 2015 © Baker & McKenzie all rights reserved

Cultu

ral R

isks

Ris

kIs

sue

Poss

ible

Sol

utio

ns

Lang

uage

/Soc

iety

• W

hat i

s th

e pr

imar

y la

ngua

ge s

poke

n by

peo

ple

in th

e co

untr

y? H

ow p

reva

lent

is th

e us

e of

Eng

lish

as th

e la

ngua

ge o

f com

mer

ce a

nd b

usin

ess?

• W

hat i

s th

e pr

edom

inan

t rel

igio

n in

the

coun

try?

• Ar

e in

tera

ctio

ns b

etw

een

mem

bers

of s

ocie

ty b

ased

up

on w

ealth

? Cl

ass?

Eth

nici

ty?

Seni

ority

? Fa

mily

R

elat

ions

?

• Cu

ltura

l bri

efing

for

the

non-

loca

l par

ty

repr

esen

tativ

es n

egot

iatin

g th

e jo

int v

entu

re.

• Cu

ltura

l tra

inin

g pr

ogra

m fo

r ex

patr

iate

em

ploy

ees

of

the

non-

loca

l par

ty.

• Cu

ltura

l tra

inin

g pr

ogra

m (i

nclu

ding

com

mun

icat

ions

tr

aini

ng, p

robl

em-s

olvi

ng a

nd c

ultu

ral a

war

enes

s) fo

r lo

cal e

mpl

oyee

s.•

Hir

e lo

cal m

anag

er to

repr

esen

t the

non

-loc

al p

arty

in

the

join

t ven

ture

.•

Appo

int j

oint

ven

ture

team

repr

esen

tativ

es w

ho id

eally

sp

eak

the

loca

l lan

guag

e or

oth

erw

ise

are

loca

lly tr

aine

d.•

Reg

ular

trai

ning

pro

gram

s on

pra

ctic

es a

nd s

tand

ards

of

the

non-

loca

l par

ty.

• H

old

mee

tings

freq

uent

ly in

the

loca

l jur

isdi

ctio

n an

d in

th

e ho

me

juri

sdic

tion

of th

e no

n-lo

cal p

arty

(e.g

., bo

ard

mee

tings

, bus

ines

s m

eetin

gs, e

mpl

oyee

retr

eats

).

Bus

ines

s/Cu

ltur

alPr

actic

es•

Do

peop

le c

omm

unic

ate

with

eac

h ot

her

expl

icitl

y or

im

plic

itly?

• Is

the

cultu

re h

iera

rchi

cal o

r fla

t?•

Are

busi

ness

rela

tions

and

com

mun

icat

ions

com

mon

ly

adve

rsar

ial o

r co

llabo

rativ

e?•

Wha

t are

the

impo

rtan

t dos

and

don

’ts o

f doi

ng b

usin

ess

in th

e lo

cal j

uris

dict

ion?

Sha

king

han

ds?

Smili

ng?

Han

ding

out

bus

ines

s ca

rds?

Bei

ng e

arly

/late

? Tr

eatin

g m

en a

nd w

omen

diff

eren

tly?

Tipp

ing

for

serv

ice?

View

of F

orei

gn C

ount

ries

• Is

ther

e an

ant

i-for

eign

inve

stm

ent s

entim

ent i

n th

e co

untr

y?•

Has

suc

h a

sent

imen

t his

tori

cally

exi

sted

in th

e co

untr

y?•

Wha

t are

the

key

hist

oric

al e

vent

s of

the

coun

try

invo

lvin

g th

e no

n-lo

cal p

arty

’s h

ome

coun

try?

•

Wha

t is

the

leve

l of i

nflue

nce

of fo

reig

n bu

sine

ss,

cultu

re, e

nter

tain

men

t, et

c., i

n th

e lo

cal c

ount

ry?

Section 2: Diligence

18

International Joint Ventures Handbook

Law stated as of 1 September 2015 © Baker & McKenzie all rights reserved

Tabl

e 2(

b) C

ompa

tibili

ty A

sses

smen

t Che

cklis

tO

pera

tiona

l Con

side

ratio

ns

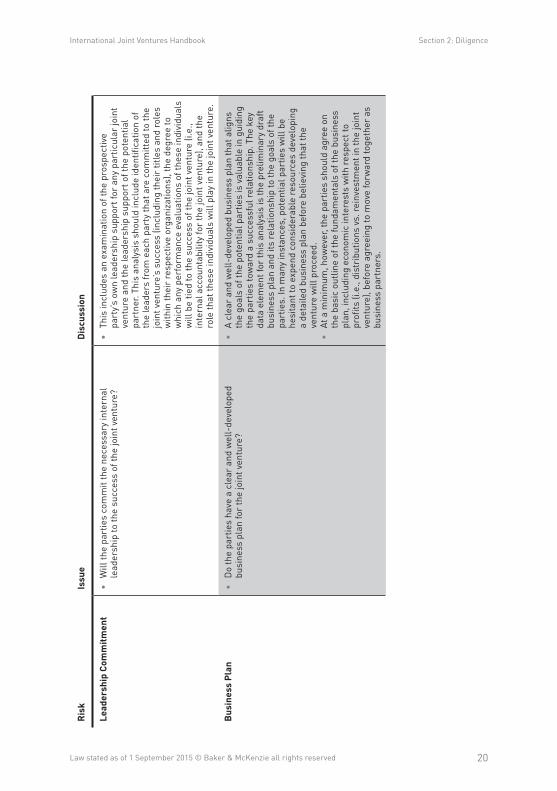

Ris

kIs

sue

Dis

cuss

ion

Alig

nmen

t of G

oals

• Ar

e th

e go

als

of th

e po

tent

ial j

oint

ven

ture

par

ties

com

plem

enta

ry a

nd a

ligne

d to

war

d th

e su

cces

s of

the

join

t ven

ture

?

• Th

is a

naly

sis

requ

ires

a c

lear

und

erst

andi

ng o

f th

e go

als

of e

ach

part

y, us

ually

obt

aine

d th

roug

h fr

ank

disc

ussi

ons

betw

een

the

part

ies.

The

se d

ata

mus

t the

n be

com

pare

d an

d ca

refu

lly c

onsi

dere

d.

In s

ome

inst

ance

s, g

oals

may

be

com

plem

enta

ry

and

a pr

ospe

ctiv

e jo

int v

entu

re p

arty

may

iden

tify

oppo

rtun

ities

for

alig

ning

goa

ls.

• In

oth

er c

ases

, a p

rosp

ectiv

e pa

rty

may

det

erm

ine

that

its

goa

ls a

nd th

e go

als

of th

e po

tent

ial p

artn

er a

re

sim

ply

not a

ligne

d.

Bus

ines

s Cu

ltur

es•

Are

the

busi

ness

cul

ture

s of

the

pote

ntia

l joi

nt v

entu

re

part

ies

com

patib

le?

Fact

ors

to c

onsi

der

incl

ude:

»ho

w d

oes

the

pote

ntia

l par

tner

mak

e de

cisi

ons

(e.g

., em

ploy

ee e

mpo

wer

men

t or

rigi

d to

p-do

wn

styl

e)?

»ho

w a

re re

sults

rew

arde

d? »

how

muc

h va

lue

does

the

pote

ntia

l par

tner

pla

ce

on li

fest

yle

(e.g

., va

luin

g em

ploy

ees

as p

eopl

e as

w

ell a

s w

orke

rs)?

• B

usin

ess

cultu

re c

an p

lay

a ke

y ro

le in

sev

eral

as

pect

s of

bus

ines

s pr

oces

s, in

clud

ing

fost

erin

g in

nova

tion,

dec

isio

n-m

akin

g an

d ri

sk-t

akin

g.

Info

rmat

ion

as to

a p

arty

’s b

usin

ess

cultu

re c

an b

e gl

eane

d fr

om fr

ank

disc

ussi

ons

not o

nly

betw

een

the

pros

pect

ive

man

ager

s of

the

join

t ven

ture

s,

but,

idea

lly, a

lso

with

the

rank

and

file

em

ploy

ees.

O

utsi

de c

onsu

ltant

s, in

clud

ing

hum

an re

sour

ce a

nd

othe

r bu

sine

ss c

onsu

ltant

s, m

ay b

e ab

le to

ass

ist

with

this

ass

essm

ent.

This

info

rmat

ion

may

then

be

com

pare

d to

the

non-

loca

l par

ty’s

bus

ines

s cu

lture

an

d fo

rmal

bus

ines

s pr

oces

ses

to d

eter

min

e th

e le

vel

of c

ompa

tibili

ty. T

he L

ocal

Ris

k As

sess

men

t Che

cklis

t in

Tab

le 2

(a) c

onta

ins

addi

tiona

l dis

cuss

ion

rega

rdin

g ge

nera

l cul

tura

l ris

ks th

at m

ay b

e pr

esen

t in

the

loca

l ju

risd

ictio

n th

at c

ould

impa

ct th

e su

cces

s of

the

join

t ve

ntur

e.

Section 2: Diligence

19

International Joint Ventures Handbook

Law stated as of 1 September 2015 © Baker & McKenzie all rights reserved

Ris

kIs

sue

Dis

cuss

ion

Fina

ncia

l Res

ourc

es•

Will

the

part

ies

be a

ble

to m

eet t

he fu

ndin

g ne

eds

of

the

join

t ven

ture

?•

Part

ies

that

are

not

str

ong

finan

cial

ly m

ay la

ck th

e re

sour

ces

to c

omm

it to

a s

ucce

ssfu

l joi

nt v

entu

re

oper

atio

n. F

inan

cial

ly s

tron

g pa

rtie

s m

ay b

e be

tter

abl

e to

mee

t the

ir fu

ndin

g an

d op

erat

iona

l com

mitm

ents

to

the

join

t ven

ture

. The

fina

ncia

l str

engt

h of

the

pote

ntia

l pa

rtne

r m

ay b

e de

term

ined

thro

ugh

publ

icly

ava

ilabl

e in

form

atio

n, c

redi

t che

cks

and

from

oth

er s

ourc

es

supp

lied

by th

e po

tent

ial p

artn

er. T

his

info

rmat

ion

shou

ld a

lso

be u

sed

to c

raft

app

ropr

iate

requ

irem

ents

an

d pr

otec

tions

with

resp

ect t

o on

-goi

ng c

apita

l co

ntri

butio

ns.

Ope

ratio

nal S

avvy

• D

oes

the

pote

ntia

l par

tner

hav

e th

e de

sire

d op

erat

iona

l an

d pe

rfor

man

ce c

apab

ilitie

s?•

Info

rmat

ion

abou

t ope

ratio

nal a

nd p

erfo

rman

ce

capa

bilit

ies

may

be

deri

ved

thro

ugh

revi

ews

of a

po

tent

ial p

artn

er’s

str

engt

h in

its

part

icul

ar m

arke

ts,

an a

naly

sis

of th

e pa

rtne

r’s p

oten

tial m

arke

t w

eakn

esse

s an

d th

e pa

rtne

r’s h

isto

rica

l ope

ratin

g an

d fin

anci

al p

erfo

rman

ce. T

his

info

rmat

ion

may

be

iden

tified

thro

ugh

inte

rvie

ws

and

disc

ussi

ons

with

ke

y m

anag

ers,

bus

ines

s cl

ient

s an

d as

soci

ates

of t

he

pote

ntia

l joi

nt v

entu

re p

artn

er. A

revi

ew o

f a p

oten

tial

part

ner’s

ope

ratio

nal s

avvy

sho

uld

also

take

into

co

nsid

erat

ion

the

com

petit

ive

envi

ronm

ent i

n th

e m

arke