joanna buickians narine mirzakhanyan narine mirzakhanyan econ 490 professor castillo microfinancing

TRANSCRIPT

Joanna BuickiansJoanna Buickians

Narine Mirzakhanyan Narine Mirzakhanyan

Econ 490

Professor Castillo

MICROFINANCINGMICROFINANCING

22

Key PointsKey Points

Muhammad YunusMuhammad Yunus Grameen BankGrameen Bank MicrofinancingMicrofinancing Micro-credit & MicrobanksMicro-credit & Microbanks Microfinancing ServicesMicrofinancing Services Women being targetedWomen being targeted Web Based MicrofinancingWeb Based Microfinancing Borrowers & LendersBorrowers & Lenders

3

Muhhamed Yunus

Yunus is the 1st Nobel Prize winner from Bangladesh

_________________________

Founder of Grameen (Rural) Bank in 1976

_________________________

Started microfinancing by giving out a loan of $27 to 42 women in a village in Bangladesh.

World’s Banker to the Poor

“If society was structured for self-employment, there would be no reason to fear being poor.” - Dr. Muhammad Yunus

4

Microfinancing• Supply of capital loans, consumer credit, savings, insurance & other basic financial services to low income households.

• People need to run their businesses, build assets, stabilize consumption & shield themselves against risks.

•It’s a service in which the poor people desire & are willing to pay for.

•Loans are typically less than $125 made to the rural poor who normally do not qualify for traditionally banking credit.

“say NO to poverty”

5

• Microfinancing is very beneficial; it is a combination of financial and non-financial education.

• Microfinancing used to be unknown, but it is now worldwide.

• World Bank estimates that there are 7,000 microfinance institutions worldwide.

Microfinancing (continued)

6

Micro-Credits & Micro-BanksCREDITS

• The Grameen transactions take place at the village level, usually in a local hall or temple.

• The borrowers will use a loan to buy tools and equipment to set up on their own.

BANKS

• Banks lend money to individual entrepreneurs in groups of five, each member being responsible for their own loans before any one individual can re-apply for the next level of funding.

• they use each other as collateral for their loans.

• This proven method has boasted over a 95% success rate in repayment and flourishing businesses.

7

Microfinancing Services

8

_______________________________________________________________________Why Targeting Women?

“One billion people in the world are illiterate and two thirds of those people are women.”

- Muhammed Yunus

9

• Microfinancing is a step towards uplifting women.• The Grameen Bank has lend $$$$ especially to women so that they can launch their own businesses.• Women gaining control over their lives. • Women achieving economic and political empowerment w/in their homes• About 90% of the people that are on micro-credit are women.• Women are more reliable in paying back the money.• Reducing domestic violence by giving women independence.

Why Targeting Women? (continued)

10

Web Based MicrofinancingCELLPHONES

• In poorer nations phones have help open up microfinancing.

• In Dev. Countries where bank branches and ATM are few/nonexistent,

cell phones make the financial services practical.

•Cell phones have the potential to take financial markets outside the urban

areas.

INTERNET

• With $$$$ transfer one can do anything to help the poor and support the economy.

11

Web Based Microfinancing (continued)

_______________________________________________________________________

KIVA.ORG

• “Connects people to make chance”

• San Francisco based nonprofit that has taken a step further w/just few clicks of the mouse, & now everyone can become a microfinancier.

• Includes photos of loan recipients & stories about borrowers, lenders can choose

aspiring small-business owner and make their own loans.

• Kiva has worked w/more than 20 microfinance institutions around the

world & enabled more than $1 million in loans for more than 2000 businesses.

12

Borrowers & Lenders• microfinance is provided by non-governmental organizations (NGOs), cooperatives, non-bank financial intermediaries and commercial banks.

• More than 10,000 microfinance institutions are in existence with a loan portfolio exceeding $7 billion.

• most of them are very small w/ client’s base of less than 2,500

• Some 1000 million people access microfinance services globally.

• Clients are typically self-employed and w/a relatively stable source of income.

• while most borrowers are women, studies indicated that many loans awarded to women and paid back by them are in fact used by men.

13

Global change through Microfinance Global change through Microfinance

Case Study #1:

Microloans in Iraq

•Al’laur Abd Mottar: microentrpreneur, Iraq

•Business: used $3,000 loan to start a scrap metal business

Case Study #2

MFI helps Dedan Ireri in Nairobi, Kenya

•Street begger, lost leg

•MFI gave him loan to start business with his friends, it failed

•Got a bicycle, worked as messenger for MFI

•Will be in 2008 Para Olympics

It works best “when there are middle-class entrepreneurs who have business savvy but do not have access to capital”—USAID Rep Gary Robbins

14

General InformationMicro-entrepreneurs: Don’t need collateral Small and shorter loans Group borrowing

Reputation and Peer pressure Some criticism

Microfinance Institution: Higher operating expenses

Rural costs are higher than urban costs

High transaction costs Because of the size of the loans

Higher interest ratesOverall: Improves employment

15

Different from traditional credit

http://www.microcapital.org/downloads/resourcepapers/IADB-VillagetoWallStreet.pdf

16

Example: “Financing urban structure Nepal”

http://www.idrc.ca/openebooks/216-3/

17

“Sustainable development continuum for organic microfarming”

http://www.idrc.ca/openebooks/216-3/

18

The larger picture: Improves Employment

Income-generation To start or expand micro enterprise

activity Helps entrepreneurs build assets and

sustain jobs Risk-management and reduction of

vulnerability Microfinance also plays a role for

vulnerable persons to cope with and mitigate risk.

Building up emergency loans for unpredictable expenses and income droughts.

Empowerment: Mobilizing savings enables people to take

financial responsibility for their lives

As business income rises, businesses expand affecting the entire community through employment and contribution to the economy

http://moderato.files.wordpress.com/2007/06/diego.jpg

19

Job Creation

MFI’s do increase jobs in agriculture and transportation, however they decrease construction and manufacturing

http://www.dallasfed.org/research/swe/2006/images/0605b_c1.gif

20

Some negative results…

Depend on microcrediting for subsistence

Engage in "copycat" behavior Thus leads to more sellers saturating

the market as more microcredit is made available.

low "barriers to entry."

Largely, subsistence activities with no prospect of comparative advantage.

Child Labor Child labor increases current income

but reduces future income

21

“The enterprise…What enterprise?”

For the Lender: The client‘s decision may diverge from

the agreed purpose. Lending to people closer to the poverty

line is riskyFor the Borrower: Risk aversion restrains the propensity to

invest in new production technologies, which would boost employment.

Is this true? Researchers find limited technological

innovation and increased labor productivity as a result of micro loans.

Credit and financing does not directly lead to employment.

22

MFI’s are successful Increase profits and social prosperity

Decrease risks, thereby increase loans and the number of investors

Number of lenders growing at 25% per year

Is the future bright?

23

24

http://www.sinapiaba.com/links/arreas.html

25

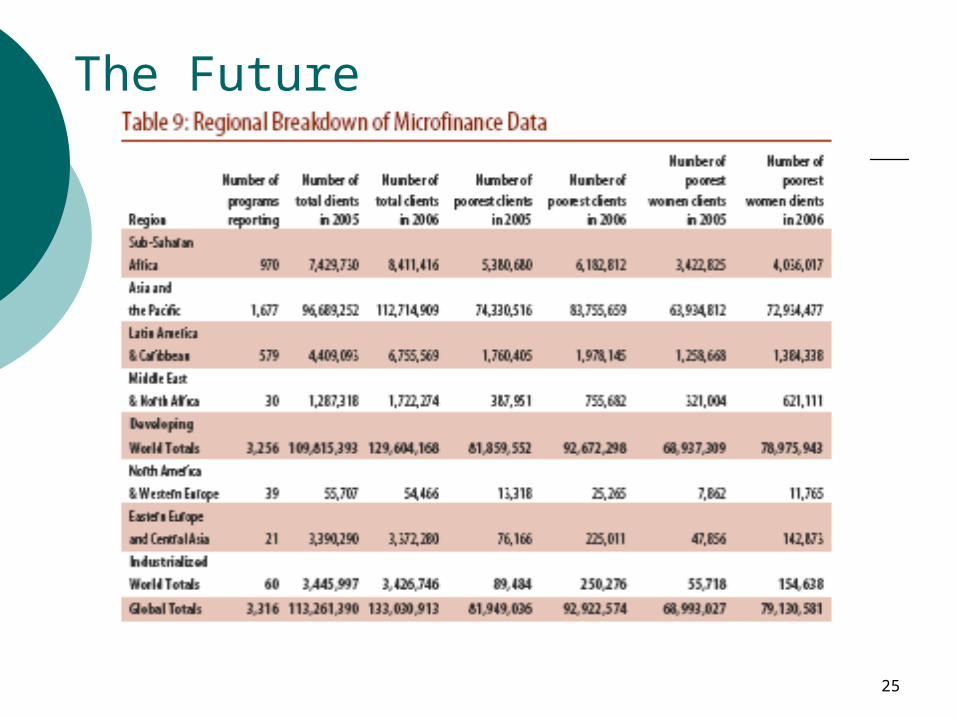

The Future

Source: http://www.microcreditsummit.org/pubs/reports/socr/EngSOCR2007.pdf

26

Sources

http://www.microcreditsummit.org/papers/Assocsession/Balkenhol.pdf http://www.cgap.org/docs/DonorBrief_06.pdf http://pdf.dec.org/pdf_docs/Pnacl633.pdf http://www.nytimes.com/2007/11/18/weekinreview/18deparle.html?

_r=1&scp=12&sq=microfinance&st=nyt&oref=slogin http://www.economist.com/world/la/displaystory.cfm?

story_id=10650663&CFID=15558859&CFTOKEN=3526b3b503e0171b-859DC346-B27C-BB00-012713530EF5EF4C

http://www.ft.com/cms/s/0/0d21e542-e8c4-11dc-913a-0000779fd2ac.html http://www.ft.com/cms/s/0/f39adbe2-dc02-11dc-bc82-0000779fd2ac.html

2727

QUESTIONS