jl.mh. thamrin no.2 jakarta 10110 - indonesia … monetary policy report bank indonesia downward...

TRANSCRIPT

Jl.MH. Thamrin No.2 Jakarta 10110 - Indonesiahttp://www.bi.go.id

BANK INDONESIAFor further information, please contact:Economic Outlook & Policy DisseminationBureau of Monetary Policy Directorate of Economic Research and Monetary Policy

Telephone : +62 61 3818163 +62 21 3818206Fax. : +62 21 3452489E-mail : [email protected] : http://www.bi.go.id

i

MONETARY POLICY REPORTBANk INdONEsIA

The Monetary Policy Report is published quarterly by Bank Indonesia after the Board of Governors’

Meetings in January, April, July, and October. In addition to fulfilling the mandate of article 58

of Act Number 23 of 1999 concerning Bank Indonesia, amended by Act No. 3 of 2004, the

report has two main purposes: (i) to function as a tangible product of a forward-looking working

framework in which formulation of monetary policy is based on economic and inflation forecasts;

and (ii) as a medium for the Board of Governors of Bank Indonesia to present to the public the

various policy considerations underlying its monetary policy decisions.

The Board of Governors

Boediono Governor

Miranda S. Goeltom Senior Deputy Governor

Hartadi A. Sarwono Deputy Governor

Siti Ch. Fadjrijah Deputy Governor

S. Budi Rochadi Deputy Governor

Muliaman D. Hadad Deputy Governor

Ardhayadi Mitroatmodjo Deputy Governor

Budi Mulya Deputy Governor

MONETARY POLICY REPORTQUARTER II-2009

ii

MONETARY POLICY REPORTBANk INdONEsIA

iii

MONETARY POLICY REPORTBANk INdONEsIA

Monetary Policy Strategy

Underlying Principles

Under the ITF, the inflation target is established as the overriding objective and nominal anchor for monetary policy. In this regard, Bank Indonesia has adopted a forward looking strategy by guiding the present monetary policy response for achievement of a medium-term inflation target.

The application of the ITF does not mean that monetary policy disregards economic growth. The basic monetary policy paradigm of striking the optimum balance between inflation and economic growth is retained in both setting the inflation target and in the monetary policy response by focusing on achievement of low, stable inflation in the medium to long-term.

The Inflation Target

After consultations with Bank Indonesia, the Government has determined and announced the CPI inflation target at 5%+1%, 4.5%+1% and 4%+1% for 2008, 2009 and 2010. The inflation target is consistent with the process of disinflation aimed at medium to long-term inflation competitive with other nations at about 3%.

Monetary Instruments and Operations

The BI Rate is the published policy rate reflecting the monetary policy stance adopted by Bank Indonesia. The BI Rate is a signal for achieving the medium to long-term inflation target and is announced periodically by Bank Indonesia for a specific period. To strengthen the operational framework for monetary policy, Bank Indonesia changed from use of the 1-month SBI rate as the operational target to the overnight interbank rate with effect from 9 June 2008. In monetary operations, the BI Rate is implemented through liquidity management on the money market to achieve the monetary policy operational target, reflected in movement in the overnight interbank money market rate. To enhance the effectiveness of liquidity management on the market, a set of standing facilities in combination with an interest rate corridor is employed in day-to-day monetary operations.

Policymaking Process

The BI Rate is determined by the Board of Governors in the Monthly Board of Governors’ Meeting. In unforeseen circumstances, the monetary policy stance may be adjusted in advance of the Monthly Board of Governors’ Meeting in a weekly Board of Governors’ Meeting. Changes in the BI Rate essentially depict the Bank Indonesia monetary policy response for guiding the forecasted level of inflation within the limits of the established inflation target.

Transparency

Monetary policy is regularly communicated to the public through customary media for communication, such as statements to the press and market actors, website postings and publication of the Monetary Policy Report (MPR). This transparency is aimed at building improved understanding and shaping public expectations of the economic and inflation outlook and the monetary response taken by Bank Indonesia.

Coordination with the Government

For the purpose of coordination in inflation targeting, monitoring and control, the Government and Bank Indonesia have established a team of officials representing the various relevant agencies. The task of the Team is to deliberate and recommend the necessary policy actions for the Government and Bank Indonesia in managing inflationary pressures for achievement of the established inflation target.

Steps for Reinforcing Monetary Policy with the Overriding Objective of Price Stability (Inflation Targeting Framework)

In July 2005, Bank Indonesia launched a reinforced monetary policy framework consistent with the Inflation Targeting Framework (ITF), encompassing four key elements: (1) use of the BI Rate as the policy reference rate, (2) anticipatory monetary policymaking process, (3) more transparent communications strategy and (4) closer policy coordination with the Government. These measures are intended to strengthen monetary policy effectiveness and governance in order to achieve the overriding objective of price stability in support of sustainable economic growth and greater public prosperity.

Enhanced Monetary Policy Measures Under Inflation Targeting Framework

In July 2005, Bank Indonesia implemented and enhanced monetary policy measures within the Inflation Targeting Framework (ITF) which encompasses four main areas: the use of the BI rate as an operational target, enhanced decision making process, more transparent communications strategy, and strengthened policy coordination with the Government. The measures is intended to strengthen the effectiveness and to provide good governance to its monetary policy making to achieve the price stability needed to support suistainable economic growth and attain social welfare.

iv

MONETARY POLICY REPORTBANk INdONEsIA

v

MONETARY POLICY REPORTBANk INdONEsIA

Foreword

The second quarter of 2009 was marked by initial signs of improvement in the world economy. Expectations

of recovery under way kindled positive sentiment on world financial markets. However, the improvement in the

economic outlook is not regarded sufficient to compensate for the global economic slowdown, which has its origin

mainly in advanced nations. Indonesia’s domestic economy has entered a period of slowdown, although not as

severe as originally projected. Externally, the balance of payments is performing ahead earlier forecasts, bolstered

by the improving outlook for the global economy, rising commodity prices and signs of renewed stability on global

financial markets.

Economic growth during Q2/2009 is estimated in the range of 3.7%-4.0%, below the 4.4% charted in

Q1/2009. Indonesia’s weaker economic growth is explained primarily by contraction in exports and slowing growth

in household consumption. Export performance is down considerably from the same period one year earlier as a

result of sluggish expansion in the world economy, including Indonesia’s major trading partners. Private consumption

expenditures have weakened in the absence of significant improvement in purchasing power. Nevertheless, spending

related to the presidential election and the payment of the 13th month salary to civil servants has helped keep private

consumption from steeper decline.

Indonesia’s balance of payments recorded an estimated second quarter surplus. Rising global commodity

prices and more vigorous demand from emerging markets, led by China and India, contributed to a surplus in the

current account. On the other hand, the capital and financial account posted a deficit. As a result of capital reversal

sustained briefly on domestic financial markets from mid-June 2009, portfolio investment in Q2/2009 fell short of

earlier predictions. International reserves reached USD57.58 billion, equivalent to 5.6 months of imports and servicing

of official debt.

Conditions in the domestic financial sector have improved in line with global developments and conducive

domestic macroeconomic indicators. During Q2/2009, the rupiah maintained an appreciating trend and yield on

Indonesian government securities with support from robust domestic fundamentals. At the end of the quarter, these

indicators sustained some correction due to the effect of unsettled global conditions.

Banking system liquidity is in more ample supply, as reflected in the growing placements of banking funds in

monetary instruments, increased volume of interbank money market transactions and fall in interbank rates. The

The Governor of Bank Indonesia

vi

MONETARY POLICY REPORTBANk INdONEsIA

downward interest rate response in the banking system is still limited to deposit rates. Lending rates have eased at a

slower pace, while credit expansion remains tight.

The downward inflationary trend continues. Inflationary pressure has eased in response to measures to safeguard

food supplies and exchange rate appreciation. Q2/2009 inflation was recorded at -0.15% (qtq), well below the historical

trend. Measured cumulatively, CPI inflation is at a very modest 0.21% (ytd), or 3.65% (yoy).

In 2009, the Indonesian economy has potential to chart higher than forecasted growth. GDP growth in 2009

is predicted in the 3.5%-4.0% range. At the same time, the outlook for CPI inflation is steady decline to about 5%

in 2009, with a substantial downward bias.

Bank Indonesia will stay the course with monetary policy conducive to domestic demand while remaining committed

to safeguarding economic stability in the medium to long-term. In the banking sector, Bank Indonesia will move

forward with the banking consolidation and intermediation programmes and strengthen the resilience of the banking

system amid the global economic turmoil. This concludes the overview of the Bank Indonesia progress report for

Q2/2009.

Jakarta, 2 July 2009

On behalf of

THE GOVERNOR OF BANK INDONESIA

Miranda S. Goeltom

Monetary Policy Report - Quarter I-2009Contents

MONETARY POLICY REPORTBANk INdONEsIA

vii

Contents

1. General Review ............................................................................ 1

2. Latest Macroeconomic Indicators ................................................ 5

Deveopments In The World Economy ............................................. 5

Economic Growth ........................................................................... 6

Balance of Payments ...................................................................... 13

3. Monetary Indicators and Policy, QII-2009 .............................................. 16

Rupiah Exchange Rate ................................................................................ 17

Inflation ..................................................................................................... 18

Monetary Policy ......................................................................................... 21

4. The Indonesian Economic Outlook......................................................... 26

Assumptions and Scenarios ....................................................................... 26

Economic Growth Outlook ........................................................................ 27

Inflation Forecast ............................................................................. 31

Risks................................................................................................ 32

5. Monetary Policy Response, QII-2009 ...................................................... 34

Statistics........................................................................................................ 35

General Review

1

1. General Review

Developments in the global economy suggest a gathering momentum in the recovery

process, although still daunted by risks. In developed nations, various indicators of

macroeconomic recovery have shown an improving trend. Government-sponsored stimulus

packages and financial sector stabilisation programmes have successfully bolstered public

confidence, and in turn strengthened consumption. Conditions on credit markets have also

begun to improve in an added development encouraging greater private consumption.

Despite this, stubbornly high levels of unemployment pose risks daunting the economic

recovery process in these nations. On the other hand, economic recovery is gaining

momentum in emerging market countries, led by China, India and Korea. Investment

activity in China, under way since the beginning of the year, is supported by a fiscal stimulus

through infrastructure spending and brisk credit expansion Resurgent domestic demand in

these Asian economies has stimulated improved economic performance in other countries

in the region. Despite this, the economic improvement in some emerging market countries

is not yet regarded sufficient to compensate for the slowdown in advanced economies. In

response to these developments, further contraction is predicted in the global economy,

although at a lesser pace.

Expectations of world economic recovery have fuelled positive developments

on global financial markets. Global financial sector performance showed steady gains

throughout Q2/2009. Stock markets in developed economies recorded index gains on the

back of positive sentiment linked to improvement in bank performance in the wake of the

stress tests, optimism for stabilisation of the financial sector and economic conditions and

positive performance reported in financial statements published by some world financial

institutions. Banking sector conditions have shown improvement, as reflected in a relaxation

of lending standards. These financial market developments in advanced nations have in turn

impacted financial markets in the region. Despite this, financial market developments took a

downturn near the end of the period, triggered by negative sentiment related to stubbornly

high levels of unemployment in the United States and Europe.

The improving trend in the global economy has had a positive impact on Indonesia’s

economic performance. The impact of strengthening demand in trading partners, led by

China and India, has boosted Indonesian exports of commodities such as CPO, coal and

copper,. Despite the steady improvement, the lack of recovery in the global economy means

that exports continue to suffer contraction. Concerning domestic demand, the flagging pace

of private consumption has been mitigated by the presidential election and the payout of

the 13th month salary to civil servants. Investment activity remains limited under the present

conditions of continued weak demand and low levels of capacity utilisation. In view of these

developments, economic growth in Q2/2009 is estimated at 3.7%-4.0%.

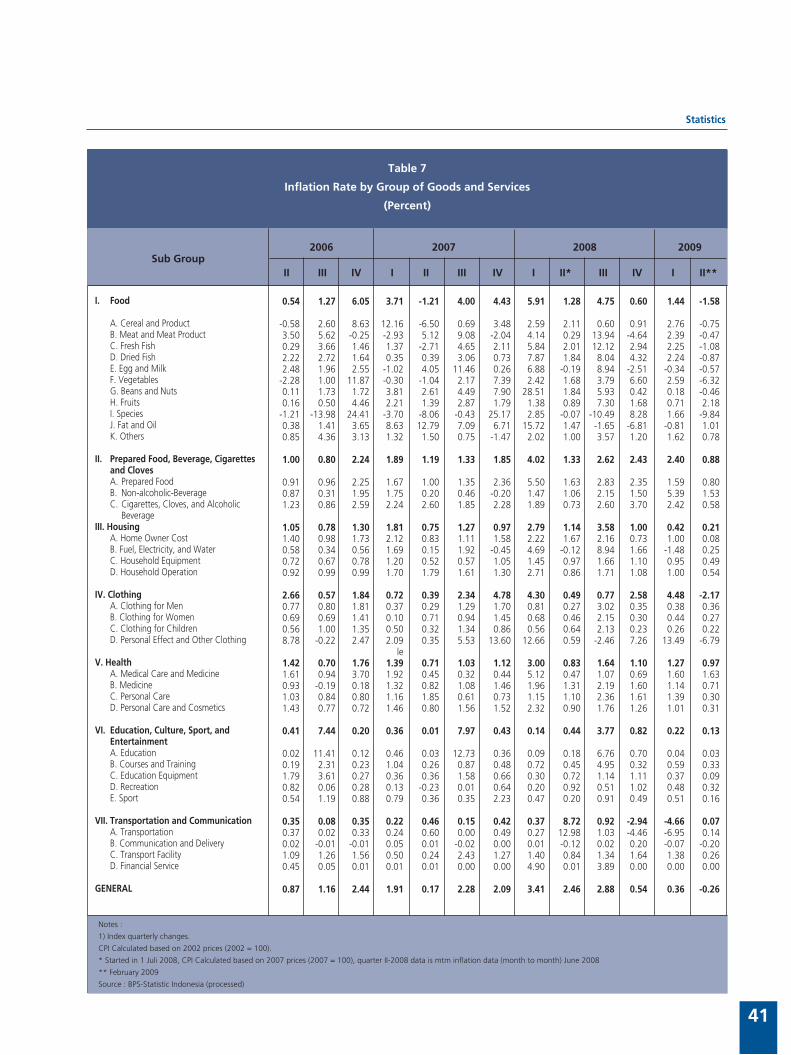

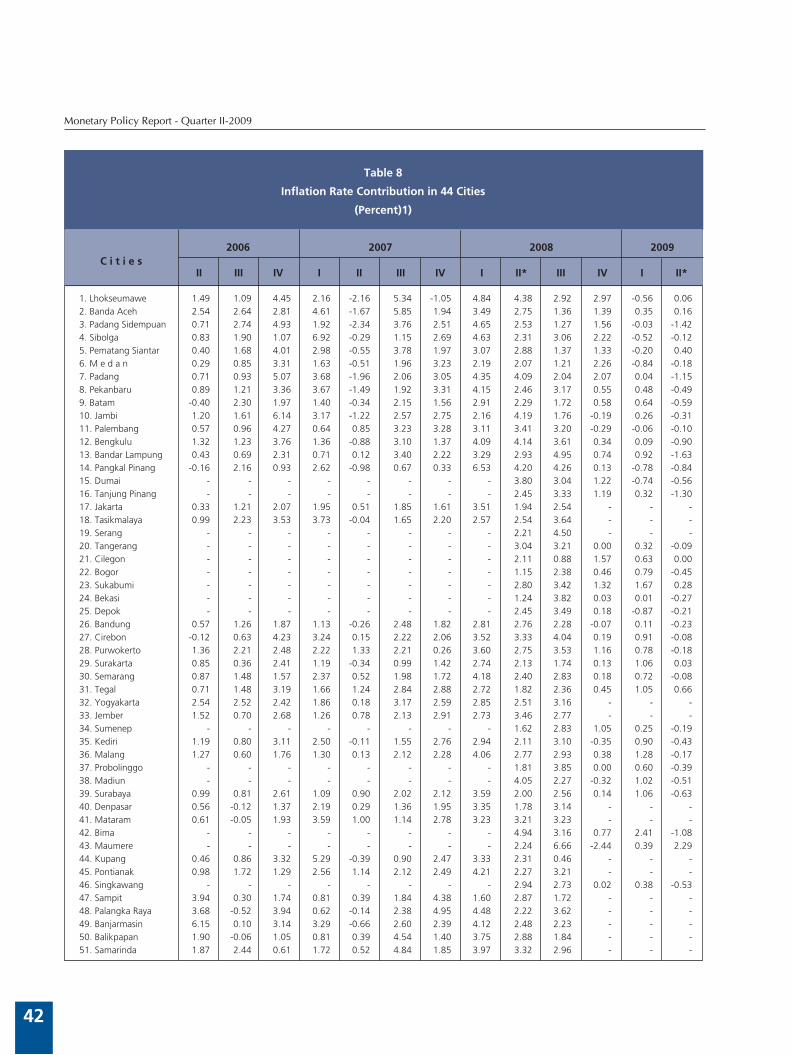

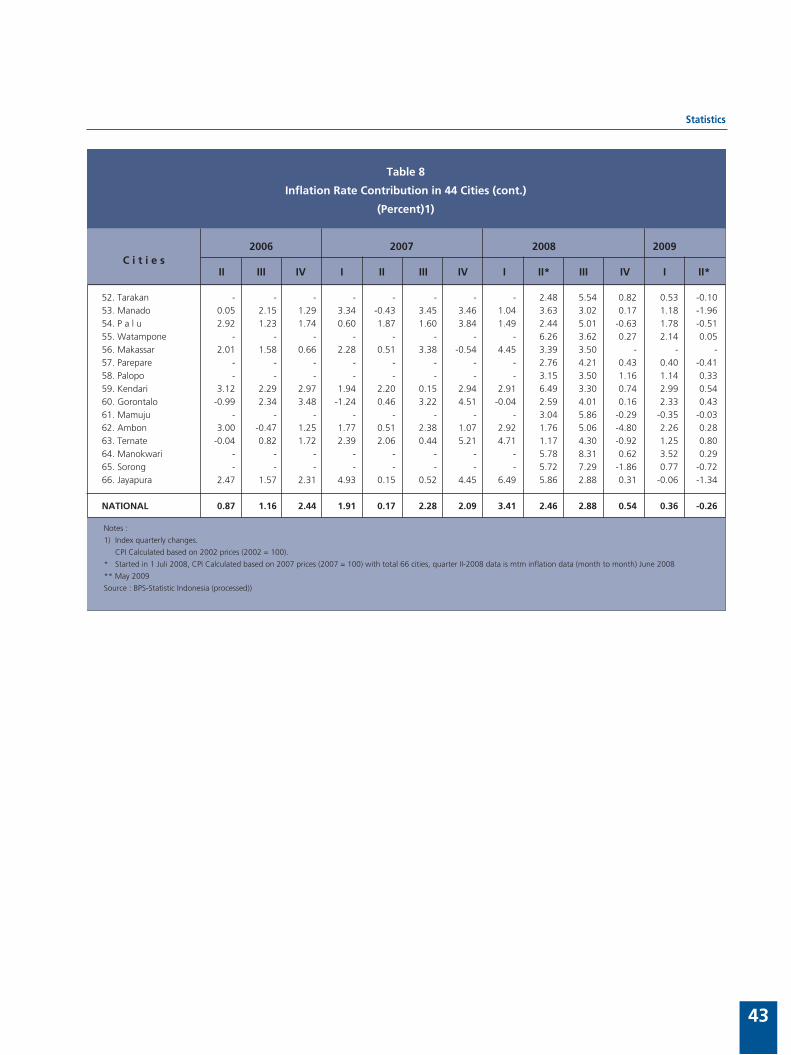

In regard to prices, the declining inflation trend is set to continue. During June 2009,

consumer goods prices recorded 0.11% inflation (mtm), considerably below the historical

level and earlier projections. Increases in some international food commodity prices were

Monetary Policy Report - Quarter II-2009

2

again offset by appreciation in the rupiah, thus keeping a lid on increases in domestic prices.

Besides the appreciation in the rupiah, improving expectations of inflation bolstered by

the accelerated pace of disinflation brought down the rate of core inflation. Measures to

safeguard adequate supplies of food staples also helped maintain low inflation in Q2/2009.

Taken together, cumulative inflation in the CPI measured 0.21% (ytd) or 3.65% (yoy).

Rising commodity prices and strengthening demand in emerging market countries

also bolstered the balance of payments, which is performing ahead of earlier

predictions. Balance of payments performance has strengthened on the back of a larger

than expected surplus in the current account. Non-oil and gas exports have received a boost

from rising global market commodity prices, led by mining commodities and crude palm

oil, and also from resurgent demand in emerging market nations and especially China and

India. In the capital and financial account, portfolio investments again recorded a surplus.

Improving conditions on global financial markets and sustained positive perceptions of the

domestic economy have prompted renewed growth in portfolio capital inflows. However,

following the capital reversal that hit domestic financial markets in mid-June 2009, portfolio

investment levels for Q2/2009 were not as high as predicted. Inflows for direct investment

are also estimated to have climbed in response to growing exploration activity by oil and

natural gas companies. Furthermore, the confidence that has been maintained in the

domestic economic outlook and the freeing up of global financial markets has led to higher

than forecasted disbursements on private foreign debt. As a result, international reserves

reached US$57.58 billion at end-June/2009, equivalent to 5.6 months of imports and

servicing of official debt.

Improvement in the balance of payments and positive sentiment on the global

market have brought about exchange rate appreciation. Compared to other countries

in the region, the rupiah maintained the second highest rate of appreciation after the Korean

won. Averaged over Q2/2009, the rupiah gained 9.99% on the back of increased supply

of foreign currency in response to foreign capital inflows. Optimism for global economic

recovery alongside carefully managed domestic economic fundamentals, reflected in the

balance of payments surplus and attractive yields on rupiah instruments, has stimulated risk

appetite for financial assets in emerging markets, including Indonesia. Despite this, negative

sentiment over global economic developments prompted a slight drop in the value of the

rupiah at end-Q2/2009 compared to early June 2009.

In the financial sector, global developments and conducive domestic macroeconomic

indicators have had a positive effect on the domestic financial sector. The stock

market charted overall index gains during Q2/2009 despite temporary capital reversal near

the end of the quarter that prompted a dip in the stock index. Improvement in domestic

fundamentals and rising global commodity prices have paved the way for brisk share

buying activity by foreign and domestic investors. On the bond market, yield on Indonesian

government securities eased in line with the downward movement in the monetary policy

rate and resurgent interest among foreign investors. Despite this, Government Securities yield

in longer tenors (above 15 years) remains high, reflecting strong risk perceptions.

General Review

3

In the banking sector, the national banking system is in comparatively stable

condition despite the limited banking response to monetary easing. At the micro

level, conditions in the Indonesian banking system were again stable, as indicated by the

safe level of the capital adequacy ratio (CAR) at a high 17.3% in May 2009. Alongside this,

the gross non-performing loans (NPLs) ratio has been held below 5% with net NPLs less

than 2%. Banking liquidity, including liquidity on the interbank money market, is steadily

improving alongside growth in depositor funds. Despite this, bank interest rates again showed

only limited response. The base lending rate response to the 250 bps reduction in the BI

Rate from December 2008 to June 2009 measured no more than about 45 bps in figures

for May 2009. In a related development, bank loan disbursements for the position at May

2009 saw further contraction at 1.1% (ytd). Even so, liquidity in the economy was adequate.

Although the expansion in monetary aggregates (cash outside banks and M1) remains very

thin, calculations based on fundamentals indicate that the trend in monetary aggregates

is still commensurate to the needs of the economy. With loan interest rates declining at

a slower pace and the very limited rate of credit expansion, indications are emerging of a

more intensive shift under way in business towards non-bank financing alternatives, such

as bond issues.

Looking forward, the economic growth outlook is better than originally predicted.

In the short-term, economic projections will be strongly influenced by global developments.

The predicted contraction in exports for the year as a whole is expected to be offset by a

surge in private consumption from the national elections. Given the bigger than expected

impact from the election of parliamentary and local assembly candidates in Q1/2009, the

2009 presidential polls are predicted to contribute significantly to private consumption. While

purchasing power has yet to show significant improvement, private consumption is forecasted

to maintain brisk growth in 2009 from the knock-on effects of the national elections. Against

this background, the economy has potential to chart higher than projected growth for 2009

as a whole. Indonesia’s GDP is forecasted at 3.5%-4.0% growth by end-2009, with a bias

towards the upper limit of this band.

Indonesia’s balance of payments is predicted to chart a surplus for 2009 overall,

strengthened by improvement in global economic conditions, rising commodity prices and

ongoing stabilisation of global financial markets. Exports are predicted to improve in response

to the more evenly distributed improvement in the global economy across the world’s regions

since Q3/2008 and the ongoing rise in world commodity prices. In the capital and financial

account, foreign capital inflows in portfolio and direct investments are set to continue in line

with optimism for world economic recovery alongside more conducive conditions on global

financial markets. In addition, capital inflows in the public sector are expected to shore up

performance in the capital and financial account.

After factoring in these developments, the Bank Indonesia Board of Governors

Meeting on 03 July 2009 decided to lower the BI Rate by 25 bps from 7.0% to

6.75%. This decision is expected to bolster measures for sustaining optimism in domestic

economic growth.

Monetary Policy Report - Quarter II-2009

4

Looking ahead, monetary policy will seek to maintain a balance between bolstering the

domestic economy amid the persistent sluggishness of the global economy and maintaining

macroeconomic stability over the medium-term with the looming increase in inflationary

pressure in 2010. Accordingly, future monetary policy will pursue a more prudent

course in view of the progressively limited room for monetary relaxation.

Latest Macroeconomic Indicators

5

2. Latest Macroeconomic Indicators

Economic growth in Q2/2009 is estimated to have slowed to about 3.7-4.0% (y-o-y).

On the demand side, preliminary figures indicate that all GDP components maintained

a slowing trend. Although improvement in the global economy provided some

support for Indonesia’s exports during Q2/2009, the global economy itself remains

in contraction with the result that exports sustained further significant contraction

during Q2/2009. However, the economy was prevented from slowing further by

private consumption expenditures related to the first round of the presidential

election. Alongside this, investment growth is estimated lower in keeping with

weakening demand and lack of improvement in business sentiment. On the supply-

side, growth in some economic sectors is believed to have slowed during Q2/2009

due to weakening external and domestic demand. Some economic sectors are

nevertheless predicted to chart improved growth on the back of rising demand related

to the activities for holding the presidential election. This uplift is expected in the

transportation and telecommunications sector, the services sector and manufacturing,

with focus on the food and beverages, paper and printed products and the textile

industry subsectors.

DEVELOPMENTS IN THE WORLD ECONOMY

The global economic outlook has shown steady improvement. Key to the present

outlook is the stabilisation process in the financial sector, support from massive

fiscal stimulus packages, low interest rates and the onset of recovery in consumer

and business confidence. The various monetary easing and fiscal stimulus responses

pursued in almost all countries have reinvigorated market optimism for the global economic

outlook. The recovery trend in the world economy is reflected in the slowing rate of decline

in macroeconomic indicators, with many even convinced that the worst is over. Overall, the

world economy is estimated to have sustained further contraction in

Q2/2009, but this is thought to be more limited compared to the actual

drop in economic growth during Q1/2009. Improvement in the world

economy has been driven more by growth in developed economies,

while advanced nations remain in a trough.

The US economy is estimated to have declined further in Q2/2009.

This downward trend is the result of flagging economic activity triggered

mainly by falling private investment in non-residential business and

loss of exports caused by the collapse in world demand. On the other

hand, growth in US household consumption remains in positive territory

bolstered by the various cash aid policies launched by US government.

US household incomes in April were up from the preceding month, due

to the effect of social benefits provided by the US government (Graph

2.1). Despite this, concerns over the tight labour market and future

Graph 2.1

USA Household Income and Expenditure

������

����

����

����

���

���

���

���

����

����

����

���

���

���

���

���

������ ������ ������ ������ ������ ������ ������ ������ ������ ������

�����

�����������������

������������������

�����������

�

Monetary Policy Report - Quarter II-2009

6

uncertainties have prompted households to cut back consumption and

shift money to savings, as reflected in the surge in the savings rate to

a 14-year high. In the initial response to improvement in consumption

indicators, economic activity has picked up in the manufacturing sector.

Reflecting this is the falling inventory to sales ratio, improved purchasing

manager index (PMI) and slowing contraction in industrial production

(Graph 2.2).

Conditions in the global financial sector have seen steady

improvement. Tight liquidity conditions are easing in response to

liquidity flows and the quantitative easing policies adopted by some

central banks. Liquidity injections by central banks such as the Fed,

BOE, BOJ and ECB have eased tight conditions on credit markets, with

improvement reflected in the narrowing in the LIBOR-Overnight Index

Swap (OIS) spread to levels preceding the Lehman Brothers bankruptcy.

Improvement in the financial sector was also indicated by the results of stress tests by the

Fed. These tests concluded that the US banking system is adequately resilient to financial

turmoil, with shortfalls in the capital requirement not as great as originally suspected. In

more recent developments, some banks even plan to repay the TARP (Trouble Asset Relief

Programme) funding to the Government ahead of schedule and are able to comply with the

required capital adequacy without setting off financial market turmoil.

Indications of more vigorous economic growth in Q2/2009 are also visible in Asia.

Economic gains in China have boosted growth across the Asian region. This improvement

in the Chinese economy is reflected in the solid growth in fixed asset investments and high

rate of bank loan disbursements, added to which is the mega stimulus package worth 4

trillion yuan (586 billion US dollars).

World inflation remains on a downward trend due to slowing economic activity

and persistently low level of commodity prices compared to 2008. Some nations,

notably the US, Japan, China and India, even reported deflation in May 2009. Even so,

the improvement in the future economic outlook has been accompanied by escalation in

international oil prices that could drive up future inflation. These conditions have prompted

central banks around the world to pursue monetary relaxation with greater caution. For these

reasons, the improving developments in the global economy must be monitored closely in

view of the associated risks.

ECONOMIC GROWTH

Aggregate Demand

Within Indonesia, the improvement the global economy has resulted in a positive contribution

to export performance. However, in view of the ongoing global economic contraction, export

growth remains negative despite resistance to decline related to indications of improved

demand in developing countries. Import growth is also estimated in negative territory,

consistent with the declining intensity of economic activity (Table 2.1). At home, the domestic

Graph 2.2

USA Capacity Utilization and Industrial Production

����� �

���

����

����

��

��

��

��

��

��������������������

��������������������������

��� ��� ��� ��� ��� ��� ��� ������� ���� ����

Latest Macroeconomic Indicators

7

economic slowdown has been restrained to some extent by consumption expenditures in

advance of the first round of the presidential election. Alongside this, investment is also

predicted to slump further due to weakening economic activity. GDP

growth in Q2/2009 is estimated in the range of 3.7%-4.0% (yoy).

Confirming this slowing trend are leading GDP indicators suggesting

that economic growth will remain in a slowing phase for at least the

next 5 months (Graph 2.3).

Private consumption growth is estimated to have slackened in

Q2/2009. This slowdown is consistent with movement in the leading

indicators for private consumption, which suggest that growth will

continue to slow for at least two more quarters (Graph 2.4). With

companies still laying off workers, the downward pressure on public

purchasing power is forecasted to continue. Despite this, incomes from

the harvest at end-Q1/2009, payment of the 13th month salary for civil

servants and expenditures in advance of the presidential election offer

potential to keep private consumption from steeper decline. The arrest

in the decline of private consumption in Q2/2009 was also supported by

developments in early indicators, most of which showed gains in April

2009. In the overall analysis, household consumption recorded lower

estimated growth during Q2/2009 in the 3.8%-4.5% range (yoy).

Some early indicators in April 2009 point to improvement in

private consumption during the quarter under review, compared

to one quarter earlier. Concerning financing, the real M1 and real

consumption credit indicators suggest that support private consumption

financing is largely stable. Middle and upper class purchasing power is on

the rise, as indicated by the increased growth in shopping transactions

paid with debit/ATM cards and credit cards as of mid-Q2/2009 compared

to the average growth recorded for January-March 2009. Besides

this, positive indications are evident in private consumption growth,

especially for durable goods, as borne out in rising sales of electronic

Graph 2.3

Leading Indicators of GDP

��������� ����������������

����

����

����

�����

�����

�����

����

����

����

�����

�����

�����

� �� ��� �� � �� ��� �� � �� ��� �� � �� ��� �� � �� ��� �� � �� ��� �� � �� ��� �� � ������ ���� ���� ���� ���� ���� ���� ����

�������������������������������������� ����������������������������������������������������������� ��������������������������������������������������

��������������������������������������������������������������������������������������

����������������������������������������������������������������������������������������������

% Y-o-Y, Base Year 2000

II III IV I II III IV I II*I t e m

Table 2.1

Economic Growth - Demand Side

2007

* Bank Indonesia Projection Figures

Total Consumption 4.6 5.3 5.0 4.9 5.5 5.5 6.3 6.4 5.9 7.2 4 .9 - 5 .6

Private Consumption 4.7 5.1 5.5 5.0 5.7 5.5 5.3 4.8 5.3 5.8 3 .8 - 4 .5

Government Consumption 3.8 6.5 2.0 3.9 3.6 5.3 14.1 16.4 10.4 19.2 12.9 - 13.5

Gross Domestic Fixed Capital Formation 7.6 9.7 12.4 9.4 13.7 12.0 12.2 9.1 11.7 3.5 1 .9 - 2 .4

Export of Goods and Services 10.4 7.4 7.9 8.5 13.6 12.4 10.6 1.8 9.5 -19.1 (-17.4) - (-16.5)

Import of Goods and Services 6.5 7.0 13.9 9.0 18.0 16.1 11.0 -3.5 10.0 -24.1 (-21.3 - (-19.9)

GDP 6.6 6.6 5.8 6.3 6.2 6.4 6.4 5.2 6.1 4.4 3 .7 - 4 .0

20072008

20082009

Graph 2.4

Leading Indicators of Private Consumption

����

����

����

����

����

�����

�����

�����

�����

��

��

��

���

���

���

���

���

���

� �� ��� �� � �� ��� �� � �� ��� �� � �� ��� �� � �� ��� �� � �� ��� �� � �� ��� �� � �� ��� ��

���� ���� ���� ���� ���� ���� ���� ����

��������������������������������������

��������������������� ���������������������

Monetary Policy Report - Quarter II-2009

8

Graph 2.7

Construction and Non-Construction Investment Growth

������������� ����������������� �����������������������������

�

�

�

��

��

���

���

�

��

��

��

��

� �� ��� �� � �� ��� �� � ��

�������

���� ���� ����

products and motor vehicles, led by motorcycles. However, growth in

consumer goods imports has undergone steep decline. On the other

hand, consumer confidence is rising, buoyed by expectations of higher

incomes and greater availability of employment. The Bank Indonesia

Consumer Confidence Indicator (IKK-BI, Graph 2.5) shows improvement

mainly from strengthening consumer perceptions of current conditions,

which are comparatively stable in the aftermath of the presidential poll,

and of conditions 6 months forward due to mounting expectations of

better incomes bolstered by the payment of a 13th month salary to civil

servants at the end of the quarter under review. Alongside this, the real

retail sales index is moving upwards, particularly in the food and tobacco

category, in keeping with falling prices.

Purchasing power indicators in some regions confirm a levelling

out in the slowing consumption trend. Consumption credit has

maintained a stable trend across all regions alongside improvement

in public optimism indicated by a rise in the Consumer Confidence

Index in all regions. Added to this, the Farmer Terms of Trade have also

shown positive developments, most importantly in the Java-Bali-Nusa

Tenggara region.

Investment growth in Q2/2009 is predicted to ease due to

the present flagging levels of external demand and business

confidence. Leading indicators for investment until Q2/2009 suggest

that investment growth will remain in the contractionary stage of

the cycle for at least the next four months (Graph 2.6). The slowing

investment growth is explained primarily by falling non-construction

investment related to the low capacity for external absorption and lack of

improvement in global risks and uncertainties. Delays in the disbursement

of the fiscal stimulus and commencement of infrastructure projects have

weakened business tendencies, despite relative stable domestic conditions

leading up to the presidential polls. In addition, the establishment of two

agencies, the Infrastructure Fund and the Guarantee Fund, to accelerate

the process of infrastructure construction did not produce visible results

in Q2/2009. Accordingly, private consumption in Q2/2009 is estimated

to have charted 1.9%-2.2% growth (yoy), down from the preceding

quarter. Analysed in terms of distribution, preliminary figures suggest that

the investment growth share in Q2/2009 is still bolstered by construction

investment (Graph 2.7).

Slowing investment growth is also confirmed by developments

in a range of preliminary indicators. Growth in non-construction

investment is estimated to have declined in keeping with falling demand

for foreign machinery and equipment and flagging imports of capital

goods (Graph 2.8). On the other hand, construction investment growth

Graph 2.5

Consumer Confidence Index - BI Consumer Survey

��

��

��

��

���

���

���

� � � � � � � � � �� �� �� � � � � � � � � � �� �� �� � � � � � ������ ���� ����

������������������� ����������������������������� �������������������������

����������

����������

�����

Graph 2.6

Investment Leading Indicators

��

��

��

��

��

���

���

���

���

���

���

� �� ��� �� � �� ��� �� � �� ��� �� � �� ��� �� � �� ��� �� � �� ��� �� � �� ��� �� � ������ ���� ���� ���� ���� ���� ���� ����

����������������������������� ��������������

��������������������������������������������������������������������������

Latest Macroeconomic Indicators

9

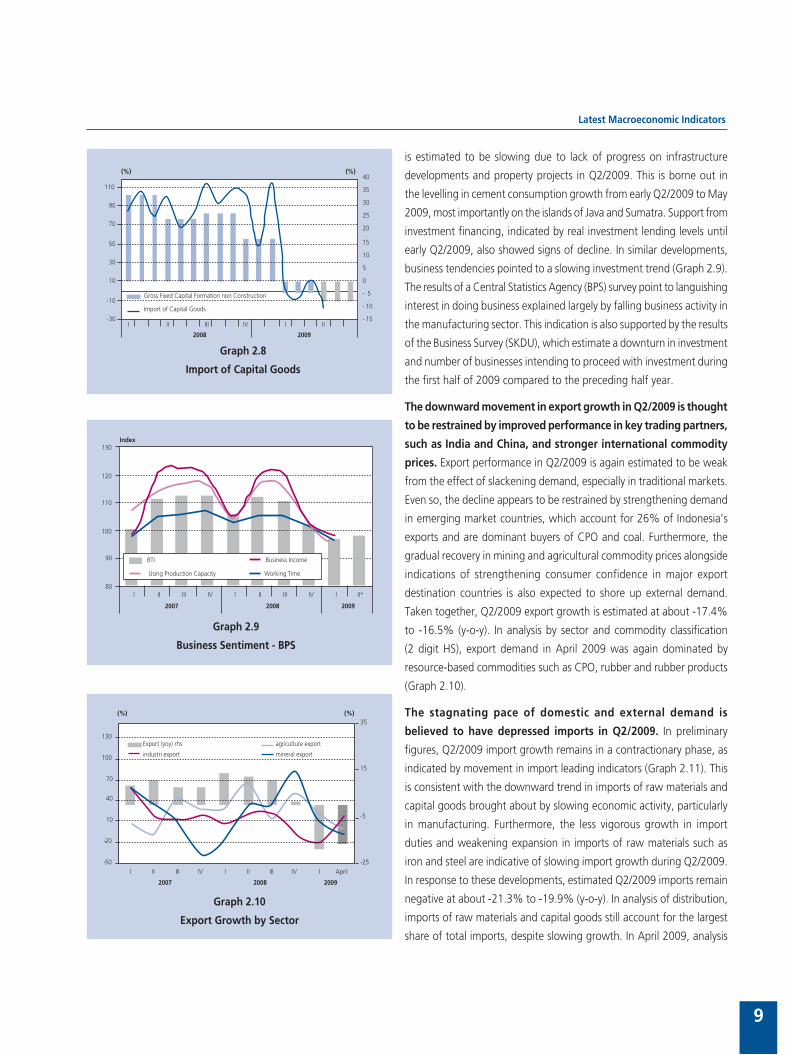

is estimated to be slowing due to lack of progress on infrastructure

developments and property projects in Q2/2009. This is borne out in

the levelling in cement consumption growth from early Q2/2009 to May

2009, most importantly on the islands of Java and Sumatra. Support from

investment financing, indicated by real investment lending levels until

early Q2/2009, also showed signs of decline. In similar developments,

business tendencies pointed to a slowing investment trend (Graph 2.9).

The results of a Central Statistics Agency (BPS) survey point to languishing

interest in doing business explained largely by falling business activity in

the manufacturing sector. This indication is also supported by the results

of the Business Survey (SKDU), which estimate a downturn in investment

and number of businesses intending to proceed with investment during

the first half of 2009 compared to the preceding half year.

The downward movement in export growth in Q2/2009 is thought

to be restrained by improved performance in key trading partners,

such as India and China, and stronger international commodity

prices. Export performance in Q2/2009 is again estimated to be weak

from the effect of slackening demand, especially in traditional markets.

Even so, the decline appears to be restrained by strengthening demand

in emerging market countries, which account for 26% of Indonesia’s

exports and are dominant buyers of CPO and coal. Furthermore, the

gradual recovery in mining and agricultural commodity prices alongside

indications of strengthening consumer confidence in major export

destination countries is also expected to shore up external demand.

Taken together, Q2/2009 export growth is estimated at about -17.4%

to -16.5% (y-o-y). In analysis by sector and commodity classification

(2 digit HS), export demand in April 2009 was again dominated by

resource-based commodities such as CPO, rubber and rubber products

(Graph 2.10).

The stagnating pace of domestic and external demand is

believed to have depressed imports in Q2/2009. In preliminary

figures, Q2/2009 import growth remains in a contractionary phase, as

indicated by movement in import leading indicators (Graph 2.11). This

is consistent with the downward trend in imports of raw materials and

capital goods brought about by slowing economic activity, particularly

in manufacturing. Furthermore, the less vigorous growth in import

duties and weakening expansion in imports of raw materials such as

iron and steel are indicative of slowing import growth during Q2/2009.

In response to these developments, estimated Q2/2009 imports remain

negative at about -21.3% to -19.9% (y-o-y). In analysis of distribution,

imports of raw materials and capital goods still account for the largest

share of total imports, despite slowing growth. In April 2009, analysis

Graph 2.8

Import of Capital Goods

� ��

� ��

� �

�

�

��

��

��

��

��

��

��

���

���

��

��

��

��

��

���

� �� ��� �� � ��

���� ����

����������������������������������������������

�����������������������

��� ���

Graph 2.9

Business Sentiment - BPS

��

��

���

���

���

���

� �� ��� �� � �� ��� �� � ���

���� ���� ����

�����

��� ���������������

������������������������� ������������

Graph 2.10

Export Growth by Sector

���������������� ������������������

��������������� ��������������

���

��

��

��

���

���

��

��

��

���

���

� �� ��� �� � �� ��� �� � �����

���� ���� ����

��� ���

Monetary Policy Report - Quarter II-2009

10

by HS2 digit commodity classification showed that imported growth

continued to rely on imports of raw material commodities and capital

goods in support of production, such as machinery/mechanical tools

and iron and steel.

Government Financial Operations

In April-May 2009, the state budget posted a Rp 5.8 trillion

surplus (0.1% of GDP), almost on par with performance in the

same period one year earlier, when the budget surplus reached

Rp 3.6 trillion (also 0.1% of GDP). Compared to the same period one

year before, estimated Government financial operations in Q2/2009

were down both in revenues and expenditures. Diminishing revenues

in January-May 2009 led to a reduced budget surplus compared to the

same period in 2008. Measured against the 2009 target, the outcome

in state revenues and grants was down from the same period one year

before, due to the flagging performance of the taxation sector. In contrast, absorption of

budget expenditures fared better during the quarter, with improvements recorded in central

government expenditures and transfers to the regions.

Taxation revenues were down in Q2/2009 in response to the slowdown in the

economy and the launching of stimulus measures involving tax cuts during 2009.

Nevertheless, this decline was offset to some degree by an increase in non-oil and gas income

taxes in April, related to tax payments on corporate earnings. Tax revenues were down mainly

in VAT and Export Tax due to the shrinking volume of international trade and the rescinding

of the CPO export tax in November 2008. In non-tax revenues, natural resource revenues on

oil and natural gas production mounted significantly in May in line with the renewed climb

in international oil prices.1 Growth tapered off further in major taxation sectors, such as

non-oil and gas income tax, not only from the effects of the economic slowdown, but also

from stimulus actions such as income tax cuts and the increased tax free income allowance

introduced this year. At the same time, the impact of the world economic slowdown was

starkly evident in the negative growth in VAT revenues at -.6.5% (yoy) during the first five

months of 2009, largely due to plunging import activity.

Improvements have been achieved in performance of state expenditures. Budget

expenditure activity during Q2/2009 was marked by significant payouts for the fuel and

electricity subsidies in May. The Government also made retroactive payments on wage

increases for civil servants, police and military personnel in April and the 13th month salary

payment was scheduled for June 2009. Looking at the year overall, budget expenditure

performance is up from the same period one year earlier, with increases in realised levels of

Central Government spending and transfers to the regions. The higher disbursement rate

of Central Government expenditures is driven by increased material and other expenditures.

In the area of transfer payments, the government expenditure portion for subsidy payments

improved against target in comparison to the January-May 2008 period. However, in nominal

terms, the subsidy expense was lower due to the effect of falling international oil prices.

1 In May 2009, the average Minas Crude price reached US$59.7 per barrel, up considerably from the Minas average of US$45.2 per barrel in January-April 2009.

Graph 2.11

Leading Import Indicators

����

����

����

����

����

�����

�����

�����

�����

�����

�����

��

��

��

��

��

���

���

���

���

���

���

� �� ��� �� � �� ��� �� � �� ��� �� � �� ��� �� � �� ��� �� � �� ��� �� � �� ��� �� � �� ��� ��

���� ���� ���� ���� ���� ���� ���� ����

����������������

����������������

�����

�������

����������

��������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������

Latest Macroeconomic Indicators

11

Under these conditions, the Central Government expenditure outcome came to 25.3% of the

Revised Budget, up from 21.8% of the Revised Budget in the same period one year earlier.

Transfers to the Regions also mounted despite the drop in Profit Sharing Funds related to the

fall in international market oil prices. The growing regional budget expenditures is explained

by technical factors with adjusted payment of General Allocations for January and February

paid out in January. In response to these developments, Transfers to the Regions came to

37.5% of the Revised Budget, representing improvement over the 33.0% of the Revised

Budget during the same period last year.

Aggregate Supply

Preliminary figures for economic sectors in Q2/2009 point to slowing economic

growth in keeping with demand-side developments (Table 2.2). This is related to

the persistently high level of global economic uncertainties that has resulted in business

postponing planned investments and business expansion. Indicating this are the findings of

the business survey, which point to decline in Q2/2009. The BPS Business Tendency Survey

identified deterioration in business expectations as of Q2/2009. Decline was reported in all

variables shaping the BPS business tendency index, such as capacity utilisation, business

revenues and hours of work. Indications of slowing supply-side performance were also

confirmed by the growing numbers of mass dismissals. Nevertheless, the holding of the

presidential election is believed to have positively impacted performance in some sectors

during Q2/2009. In looking back to the historical pattern in 2004, the presidential polls

provide a boost to growth in a number of sectors and especially in the corporate services

subsector. This is explained by the surge in advertising spending during the presidential

election compared to the previous legislative polls. At the same time, other sectors such as

communications and industry, notably the foods, textiles and printed goods subsectors, are

set to chart even lower growth compared to the previous legislative elections.

% Y-o-Y, Base Year 2000

II III IV I II III IV* I II*Sector

Table 2.2

Economic Growth - Supply Side

2007

* Bank Indonesia Projection Figures

Agriculture 5.6 7.7 2.0 3.4 6.3 4.8 3.4 4.7 4.8 4.8 4 . 0 - 4 . 3

Mining and Quarrying 3.2 1.0 -2.0 2.0 -1.7 -0.5 2.1 2.1 0.5 2.2 1 . 7 - 1 . 9

Manufacturing 5.1 4.5 3.8 4.7 4.3 4.2 4.3 1.8 3.7 1.6 1 . 3 - 1 . 6

Electricity, Gas and Water Supply 10.2 11.3 11.6 10.3 12.3 11.8 10.4 9.3 10.9 11.4 11.0 - 11.4

Construction 7.7 8.3 9.9 8.6 8.0 8.1 7.6 5.7 7.3 6.3 5 . 7 - 6 . 1

Trade, Hotels and Restaurants 7.8 8.0 8.6 8.4 6.9 8.1 8.4 5.6 7.2 0.6 0 . 3 - 0 . 6

Transportation and Communication 13.7 14.8 14.5 14.0 18.3 17.3 15.5 15.8 16.7 16.7 14.7 - 15.9

Financial, Rental and Business Services 7.6 7.6 8.6 8.0 8.3 8.7 8.6 7.4 8.2 6.3 4 . 6 - 4 . 6

Services 7.0 5.2 7.2 6.6 5.9 6.7 7.2 6.0 6.4 6.8 5 . 8 - 6 . 1

GDP 6.6 6.6 5.8 6.3 6.2 6.4 6.4 5.2 6.1 4.4 3 . 7 - 4 . 0

20072008

20082009

Monetary Policy Report - Quarter II-2009

12

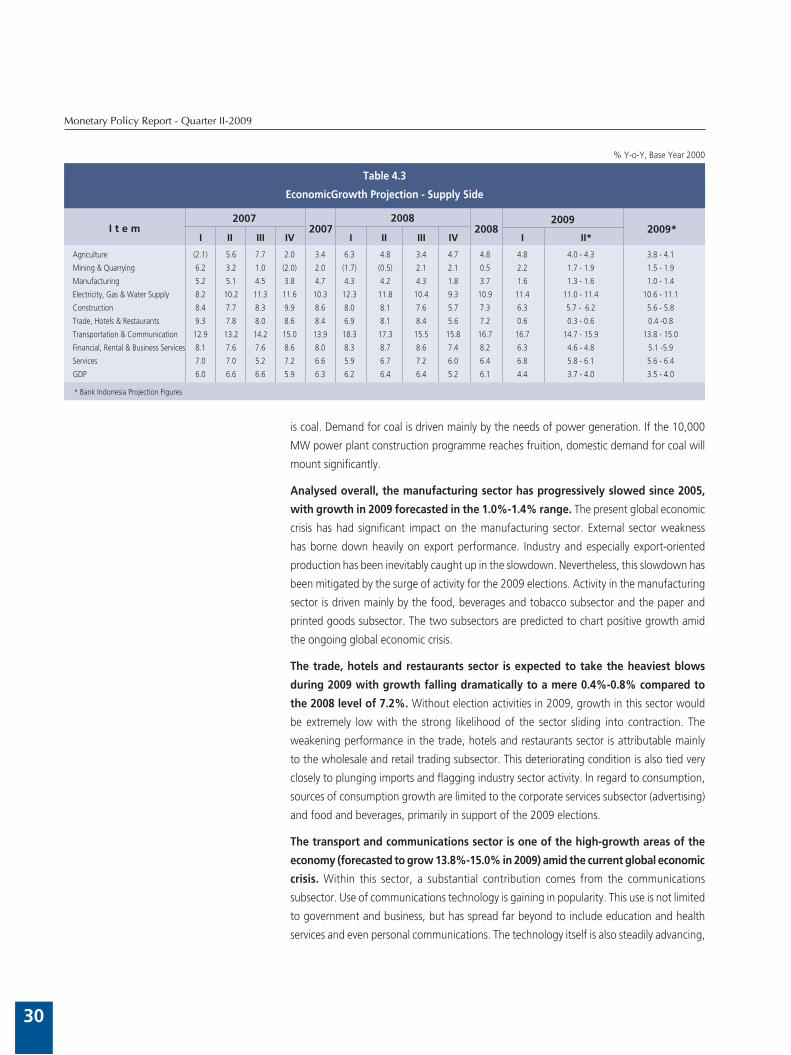

Manufacturing is estimated to have maintained a slowing trend in Q2/2009 with

growth at 1.3%-1.6% (yoy). The slowing performance is related primarily to lack of

improvement in demand, especially for exports. Besides impacting the utilisation of available

capacity, the weak demand has also prompted business to delay investments, as reflected in

the low rate of absorption of fiscal stimulus funding provided through import duty subsidies.

Despite this, the holding of the presidential election is expected to put some brake on decline

in manufacturing activity, particularly in the textile manufacturing, food, beverages and

tobacco production and the paper and printed goods subsectors. In analysis by structure,

manufacturing growth was distributed mostly among the transportation manufacturing,

machinery and tools, the food, beverages and tobacco and the chemical industry and rubber

products subsectors. Even so, the food, beverages and tobacco, chemicals and rubber goods

and paper and printed goods subsectors are the leading contributors to manufacturing

sector performance.

Slowing manufacturing performance is reflected in the downward trend in the

production capacity index generated in the BI Production Survey. When examined in

greater detail, a significant drop is visible in the transportation equipment, machinery and

machine tools and the basic metals subsectors. However, some election-related subsectors,

such as food and beverages, textile production and paper and printed goods, still charted

gains. Signs of slowing industry performance were also confirmed by developments in other

early indicators. As of mid-Q2/2009, growth in car and motorcycle production remained

on a downward trend. Similar movement was evident in the flagging levels of electricity

consumption by industrial users as of early Q2/2009. In contrast, the cement subsector

managed a modest turnaround indicated by an upswing in cement consumption in mid-

Q2/2009. Despite this, growth in cement consumption remains below that of the same

period one year before. In regard to financing, figures for early Q2/2009 indicate further

slowing in bank lending to manufacturing, which has been running below the average rate

of expansion for 2008.

The trade, hotels and restaurants sector charted reduced growth in Q2/2009 at

an estimated 0.3%-0.6% (yoy). This slowdown is primarily the result of sliding demand

in response to weakening public purchasing power as incomes decline and more workers

suffer layoffs. An added factor is slumping imports. Despite this, the activities surrounding

the presidential election are expected to prevent even worse decline, particularly in key

commodity categories such as food and tobacco and the clothing and accessories category.

Early indicators for the trade, hotels and restaurant sector, such as the retail sales index (SPE-

BI) also point to decline in mid-Q2/2009. Analysed in closer detail, almost all commodity

categories are marked by slowing trends, led by durable goods. Similar behaviour is visible

in performance indicators for the hotels subsector, with stagnating average occupancy rates

in Jakarta and Bali hotels in early Q2/2009. In regard to financing, figures for early Q2/2009

indicate further slowing in bank lending for the trade sector, which has similarly been running

below the average rate of expansion for 2008.

Preliminary Q2/2009 figures for agriculture sector growth indicate slowing

performance compared to one quarter earlier. This dip in growth is explained by the

Latest Macroeconomic Indicators

13

end of the main harvest season. In the Forecast I figures published by the Central Statistics

Agency (BPS), rice production and harvested land area will decline in the second sub-round

(May-August) in keeping with the end of the harvest season. When analysed by structure,

the food crops subsector accounts for the largest share of agricultural sector output. The

estates subsector also reported similar decline, except for oil palm cultivation. In regard to

financing, banks maintained stable levels of lending to agriculture in figures for mid-Q2/2009,

although below the average lending growth recorded in 2008.

The mining and quarrying sector recorded growth estimated at 1.7%-1.9% (yoy)

during Q2/2009. This stagnating performance in the mining sector is explained mainly by

subsiding demand for exported mining commodities, as visible in exports of metal ores, matte

and concentrates, nickel and aluminium. Despite this, the onset of price gains in some export

commodities is set to put some brake on the decline in the mining sector. In early Q2/2009,

significant contraction was also reported in lending to the mining sector.

Growth in the transport and communications is estimated stable in Q2/2009 in the

range of 14.7%-15.9% (yoy), as indicated by an upward trend in cellular subscribers.

The stable movement in this growth is reflected in the continued performance gains by

telecommunications enterprises such as Telkom. These gains are driven primary by the surge

in call traffic and calling time in advance of the legislative elections, with similar activity also

forecasted during the coming Presidential Election. At the same time, figures for early Q2/2009

indicate generally stable growth in bank lending to the transport and communications sector,

albeit still below the average growth in 2008.

The construction sector again charted stable estimated growth in Q2/2009. This is

borne out in indicators such as the comparatively stable growth in commercial property

construction in the BI Commercial Property Survey for Q2/2009. Also reflecting this are

developments in cement consumption, which at mid-Q2/2009 was still showing indications

of growth albeit below the growth levels of 2008. In regard to financing, bank lending to the

construction sector in early Q2/2009 remained below the average rate of credit expansion

in 2008. At the same time, the onset of decline in bank interest rates, and especially home

mortgage rates, is expected to have a positive impact on property sector growth.

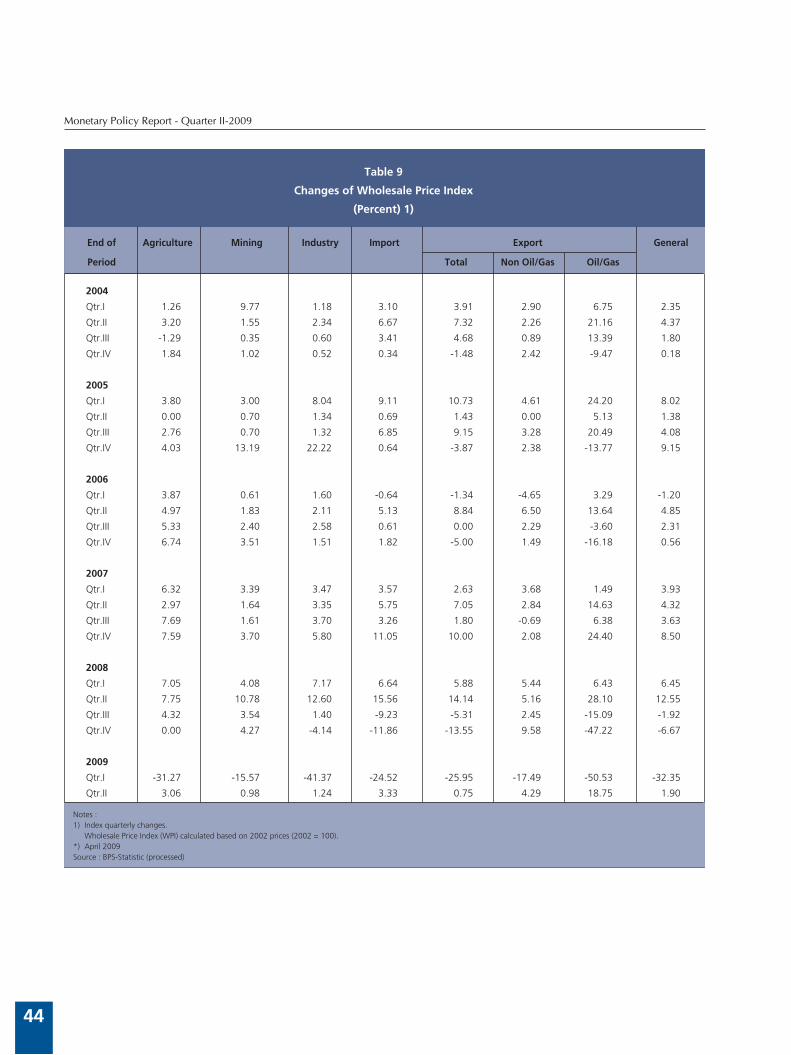

BALANCE OF PAYMENTS

Evaluation of the Q2/2009 balance of payments points toward future improvement

in Indonesia’s external performance, led by the current account. Key to this is the

improving outlook for the global economy and rising demand for Indonesia’s export

commodities. The halt in commodity price decline has also had a positive effect on Indonesia’s

balance of trade. In preliminary figures, imports contracted more steeply than exports,

resulting in an improved position in the current account for Q2/2009. In the capital and

financial account, the comparative stability on global financial markets and keen foreigner

interest in investment sustained positive momentum in foreign capital inflows for portfolio

investments. Foreign direct investment also appears to be moving in a positive direction

Monetary Policy Report - Quarter II-2009

14

in line with rising commodity prices and the continued positive outlook for the domestic

economy. The public sector role retains a dominant role in attracting inflows with the use of

Bank Indonesia Certificates (SBIs), Government Securities and the recent issuance of foreign

currency Sukuk (Islamic bonds) in Q2/2009. In the private sector, pressure from foreign

borrowing transactions mounted slightly due to an increase in corporate debt repayments.

Taken together, the Q2/2009 balance of payments is estimated to have achieved a surplus

The Current Account

The condition of the current account points to improvement in Indonesia’s external

performance, visible in the strengthening trade surplus as export mount a recovery.

The positive export performance was bolstered by rising demand for resource-based

commodities in some countries, led by China and other nations in non-Japan Asia. Demand

in these nations is expected to partially offset the slowdown in global demand originating

mainly from the US and Europe. The levelling off in the downward movement of commodity

prices has helped to shore up exports. Taken together, the balance of payments surplus was

sufficient to cover the deficits in the services, income and current account accounts.

Export performance received a positive boost from commodity price movements

during the January-June 2009 period. The downward movement in non-oil and gas

commodity prices dating back to Q3/2008 levelled out in Q1/2009, with prices recovering

in Q2/2009. With the combination of these commodity price developments and potential

for strengthening demand in trading partner nations, non-oil and gas exports in Q2/2009

are estimated to have surpassed original forecasts. In the import sector, the still struggling

domestic economy is maintaining a downward bias in actual imports of non-oil and gas

merchandise, In the oil and natural gas sector, the low oil consumption recorded in Q1/2009

is estimated to have carried forward into Q2/2009. In figures for March 2009, oil imports

were in progressive decline due to the effect of flagging domestic economic activity. Also

contributing to reduced oil imports was more modest consumption of oil-based fuels in

line with the progress in the kerosene to LPG conversion programme and diversification

of energy sources for power generation. The Q2/2009 deficit in the services, income and

current transfers account, as part of the overall balance of payments, is estimated above

earlier forecasts. The higher deficit is explained by the services account and especially

transportation, which recorded an increased deficit due to the effect of the recent climb in

international oil prices.

Capital and Financial Account

A key development influencing the capital and financial account during Q2/2009 was

the decision by Moody’s to upgrade Indonesia’s credit rating outlook from stable

to positive. Moody’s emphasised a number of factors, including the strong outlook for

economic growth, an effective policy framework for mitigating the impact of turmoil and

sustaining economic resilience, domestic political stability, improving credit fundamentals

compared to peers reflected in the decline in the external debt ratio, a positive trade balance,

sustainability of external financing and adequate levels of banking liquidity backed by robust

Latest Macroeconomic Indicators

15

capital. Foreign portfolio capital transactions are estimated to have booked another surplus

in Q2/2009 on the back of subdued domestic macroeconomic conditions. During Q2/2009,

foreign investor interest in domestic commercial assets (SBIs, Government Securities and

stocks) remained positive. Nevertheless, portfolio transactions are predicted to fall short of

original forecasts in response to portfolio rebalancing by foreigners exiting the domestic

financial market, among others for profit taking purposes. This condition, which has persisted

since mid-June 2009, is expected to be temporary in view of the ongoing adjustments in the

global economy as it shifts towards a more positive direction.

International Reserves

Following the latest developments in the current account and the capital and financial account,

international reserves mounted to 57.58 billion US dollars at end-Q2/2009, a level

equivalent to 5.6 months of imports and servicing of official external debt.

Monetary Policy Report - Quarter II-2009

16

3. Monetary indicators and policy QII-2009

During Q2/2009, signs of improvement emerged in external conditions. The

ongoing process of global economic recovery has engendered positive sentiment

among market actors for resumption of investment activity in emerging markets.

This development has also imbued optimism for future improvement in the global

economy. The rupiah exchange rate registered appreciation during Q2/2009. This

performance was bolstered not only by external factors, but also the solid condition

of domestic factors. Indonesia’s balance of payments surplus, continued attractiveness

of rupiah yields and conducive socio-political conditions in the aftermath of the

national elections contributed to the strengthening of the rupiah. In Q2/2009, the

rupiah exchange rate averaged Rp 10,527 to the US dollar, having appreciated 9.99%

over Q1/2009. Concerning prices, inflationary pressure eased further in Q2/2009 with

an accelerated rate of decline. CPI inflation in Q2/2009 was recorded at 3.65% (yoy),

down from 7.92% (yoy) in the preceding quarter. The drop in inflation is explained

primarily by non-fundamentals, although pressure on the fundamentals side has also

begun to ease. The lower administered prices during Q2/2009 is explained by the

absence of government rulings on strategic items, while the decline in volatile foods

inflation was influenced mainly by the harvest season and measures safeguarding

domestic supply of foodstuffs. Inflationary pressure from fundamentals is also

estimated lower. The softening of external pressures from rupiah appreciation amid

conditions of sustained weak domestic demand has been a key factor bringing down

inflationary pressure.

In similar developments, monetary indicators show reduced expansion. The stagnating

growth in depositor funds is related to the drop in economic growth, while flagging

credit expansion is explained by heightened perceptions of risks in future economic

conditions. The bank interest rate response to BI Rate cuts is improving, as reflected

in the downward movement in interest rates across various tenors. On the stock

market, optimism in the global economic recovery process and the strength of

corporate micro fundamentals encouraged investors to return to the capital market.

During Q2/2009, the JSX composite index charted further gains, despite sustaining

brief correction at the end of the period under review. On the Government Securities

market, yield on all tenors eased in keeping with the lowering of the BI Rate alongside

improvement in perceptions of risk. This has encouraged renewed growth in foreign

investor placements on the Government Securities market. At the same time, Q2/2009

expansion in real sector financing came mainly from outside the banking sector.

Reflecting this were rights issues for some listed stocks and new corporate bond

issuances in contrast to the sharp drop in bank lending.

Monetary Indicators and Policy, QII-2009

17

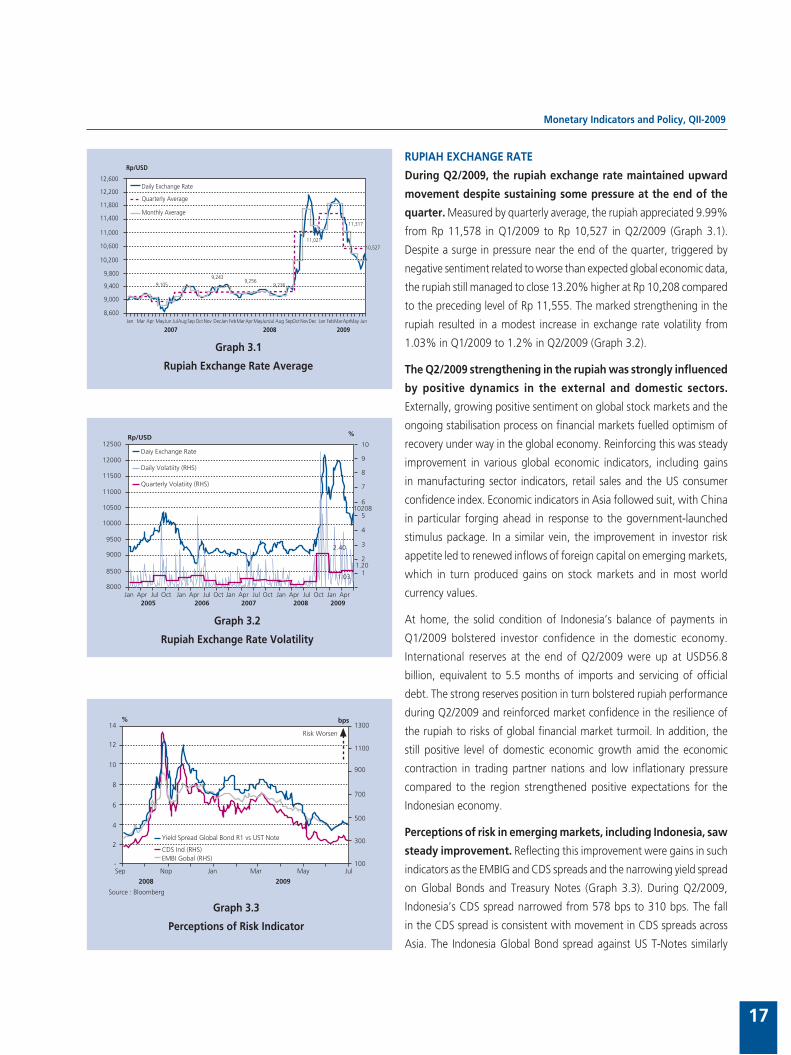

RUPIAH EXCHANGE RATE

During Q2/2009, the rupiah exchange rate maintained upward

movement despite sustaining some pressure at the end of the

quarter. Measured by quarterly average, the rupiah appreciated 9.99%

from Rp 11,578 in Q1/2009 to Rp 10,527 in Q2/2009 (Graph 3.1).

Despite a surge in pressure near the end of the quarter, triggered by

negative sentiment related to worse than expected global economic data,

the rupiah still managed to close 13.20% higher at Rp 10,208 compared

to the preceding level of Rp 11,555. The marked strengthening in the

rupiah resulted in a modest increase in exchange rate volatility from

1.03% in Q1/2009 to 1.2% in Q2/2009 (Graph 3.2).

The Q2/2009 strengthening in the rupiah was strongly influenced

by positive dynamics in the external and domestic sectors.

Externally, growing positive sentiment on global stock markets and the

ongoing stabilisation process on financial markets fuelled optimism of

recovery under way in the global economy. Reinforcing this was steady

improvement in various global economic indicators, including gains

in manufacturing sector indicators, retail sales and the US consumer

confidence index. Economic indicators in Asia followed suit, with China

in particular forging ahead in response to the government-launched

stimulus package. In a similar vein, the improvement in investor risk

appetite led to renewed inflows of foreign capital on emerging markets,

which in turn produced gains on stock markets and in most world

currency values.

At home, the solid condition of Indonesia’s balance of payments in

Q1/2009 bolstered investor confidence in the domestic economy.

International reserves at the end of Q2/2009 were up at USD56.8

billion, equivalent to 5.5 months of imports and servicing of official

debt. The strong reserves position in turn bolstered rupiah performance

during Q2/2009 and reinforced market confidence in the resilience of

the rupiah to risks of global financial market turmoil. In addition, the

still positive level of domestic economic growth amid the economic

contraction in trading partner nations and low inflationary pressure

compared to the region strengthened positive expectations for the

Indonesian economy.

Perceptions of risk in emerging markets, including Indonesia, saw

steady improvement. Reflecting this improvement were gains in such

indicators as the EMBIG and CDS spreads and the narrowing yield spread

on Global Bonds and Treasury Notes (Graph 3.3). During Q2/2009,

Indonesia’s CDS spread narrowed from 578 bps to 310 bps. The fall

in the CDS spread is consistent with movement in CDS spreads across

Asia. The Indonesia Global Bond spread against US T-Notes similarly

������

������

������

������

������

������

������

������

�����

�����

�����

�������� ��� ��� ������ ������ ��������� ������ ��������������� ��� ��������������� ��� ������������ ���

���� ���� ����

����������

����������

������

������

������

�����������������

�������������������

���������������

Graph 3.1

Rupiah Exchange Rate Average

Graph 3.2

Rupiah Exchange Rate Volatility

�����������

�����

�����

�����

�����

�����

����

����

����

������� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ���

���� ���� ���� ���� ����

�

��

�

�

�

�

�

�

�

�

�

�����

����

����

����

���������������������

�������������������������

������������������

Graph 3.3

Perceptions of Risk Indicator

���������������������������������������

�����������������������������

�����������

���

��

��

�

�

�

�

���� ��� ��� ��� ��� ���

���� ����

�������

����

���

���

���

���

���

������������������

Monetary Policy Report - Quarter II-2009

18

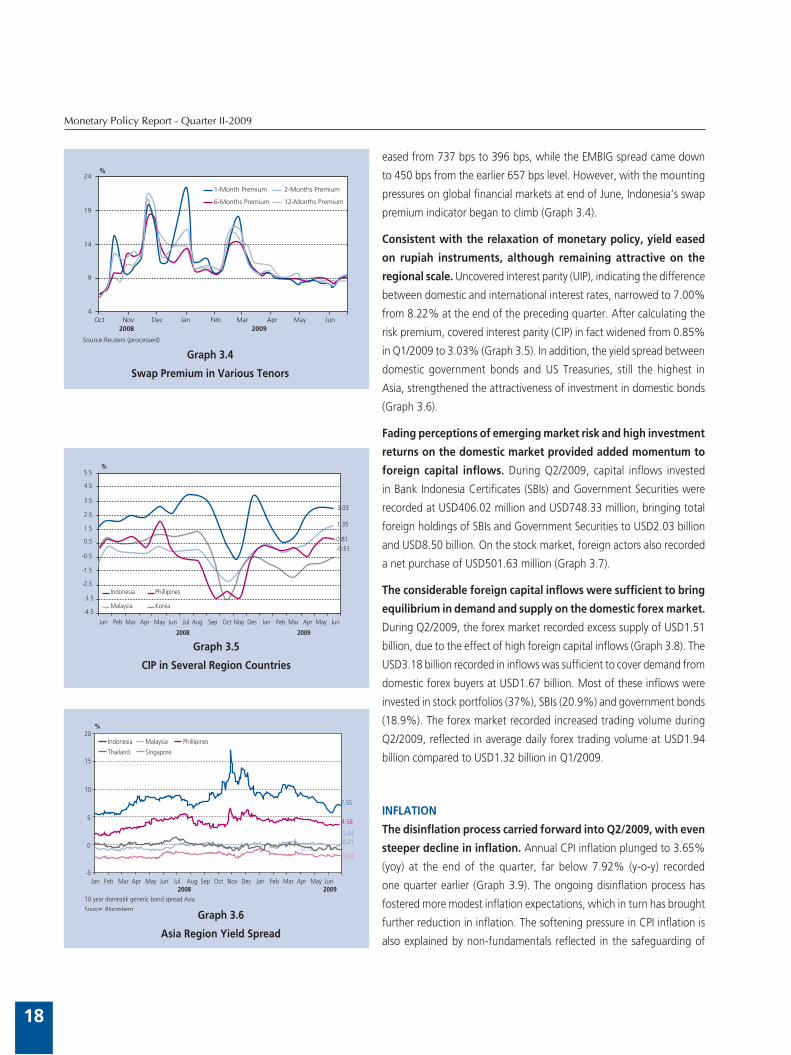

eased from 737 bps to 396 bps, while the EMBIG spread came down

to 450 bps from the earlier 657 bps level. However, with the mounting

pressures on global financial markets at end of June, Indonesia’s swap

premium indicator began to climb (Graph 3.4).

Consistent with the relaxation of monetary policy, yield eased

on rupiah instruments, although remaining attractive on the

regional scale. Uncovered interest parity (UIP), indicating the difference

between domestic and international interest rates, narrowed to 7.00%

from 8.22% at the end of the preceding quarter. After calculating the

risk premium, covered interest parity (CIP) in fact widened from 0.85%

in Q1/2009 to 3.03% (Graph 3.5). In addition, the yield spread between

domestic government bonds and US Treasuries, still the highest in

Asia, strengthened the attractiveness of investment in domestic bonds

(Graph 3.6).

Fading perceptions of emerging market risk and high investment

returns on the domestic market provided added momentum to

foreign capital inflows. During Q2/2009, capital inflows invested

in Bank Indonesia Certificates (SBIs) and Government Securities were

recorded at USD406.02 million and USD748.33 million, bringing total

foreign holdings of SBIs and Government Securities to USD2.03 billion

and USD8.50 billion. On the stock market, foreign actors also recorded

a net purchase of USD501.63 million (Graph 3.7).

The considerable foreign capital inflows were sufficient to bring

equilibrium in demand and supply on the domestic forex market.

During Q2/2009, the forex market recorded excess supply of USD1.51

billion, due to the effect of high foreign capital inflows (Graph 3.8). The

USD3.18 billion recorded in inflows was sufficient to cover demand from

domestic forex buyers at USD1.67 billion. Most of these inflows were

invested in stock portfolios (37%), SBIs (20.9%) and government bonds

(18.9%). The forex market recorded increased trading volume during

Q2/2009, reflected in average daily forex trading volume at USD1.94

billion compared to USD1.32 billion in Q1/2009.

INFLATION

The disinflation process carried forward into Q2/2009, with even

steeper decline in inflation. Annual CPI inflation plunged to 3.65%

(yoy) at the end of the quarter, far below 7.92% (y-o-y) recorded

one quarter earlier (Graph 3.9). The ongoing disinflation process has

fostered more modest inflation expectations, which in turn has brought

further reduction in inflation. The softening pressure in CPI inflation is

also explained by non-fundamentals reflected in the safeguarding of

��������������� ����������������

���������������� �����������������

���

��

��

�

���� ��� ��� ��� ��� ��� ��� ��� ���

���� ����

��������������������������

Graph 3.4

Swap Premium in Various Tenors

Graph 3.5

CIP in Several Region Countries

��������� �����������

�������� �����

����

����

���������

���

���

���

���

���

���

����

����

����

����

����

��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ���

���� ����

�

Graph 3.6

Asia Region Yield Spread

�����������������������������������������

�����������������

��������

�

��� ��� ��� ��� ��� ��� ��� ��� ���

����

��� ��� ������ ��� ��� ��� ��� ���

��������� �������� �����������

�������� ���������

��

�

�

��

��

��

����

����

����

���������

Monetary Indicators and Policy, QII-2009

19

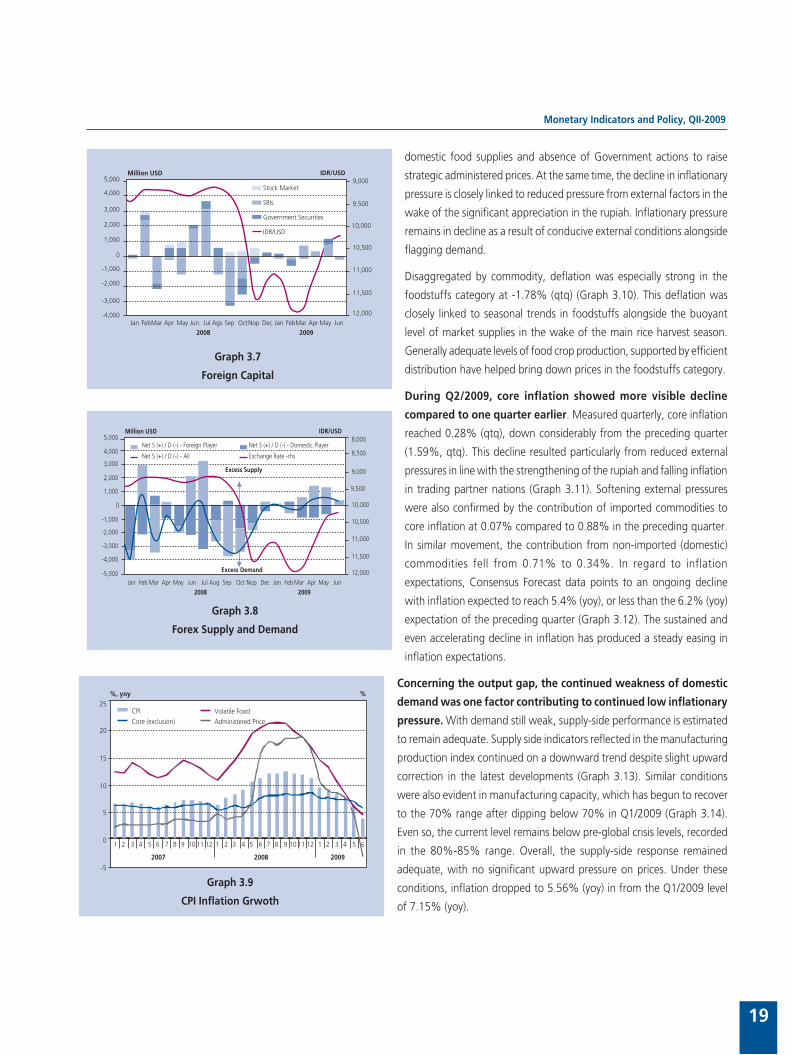

domestic food supplies and absence of Government actions to raise

strategic administered prices. At the same time, the decline in inflationary

pressure is closely linked to reduced pressure from external factors in the

wake of the significant appreciation in the rupiah. Inflationary pressure

remains in decline as a result of conducive external conditions alongside

flagging demand.

Disaggregated by commodity, deflation was especially strong in the

foodstuffs category at -1.78% (qtq) (Graph 3.10). This deflation was

closely linked to seasonal trends in foodstuffs alongside the buoyant

level of market supplies in the wake of the main rice harvest season.

Generally adequate levels of food crop production, supported by efficient

distribution have helped bring down prices in the foodstuffs category.

During Q2/2009, core inflation showed more visible decline

compared to one quarter earlier. Measured quarterly, core inflation

reached 0.28% (qtq), down considerably from the preceding quarter

(1.59%, qtq). This decline resulted particularly from reduced external

pressures in line with the strengthening of the rupiah and falling inflation

in trading partner nations (Graph 3.11). Softening external pressures

were also confirmed by the contribution of imported commodities to

core inflation at 0.07% compared to 0.88% in the preceding quarter.

In similar movement, the contribution from non-imported (domestic)

commodities fell from 0.71% to 0.34%. In regard to inflation

expectations, Consensus Forecast data points to an ongoing decline

with inflation expected to reach 5.4% (yoy), or less than the 6.2% (yoy)

expectation of the preceding quarter (Graph 3.12). The sustained and

even accelerating decline in inflation has produced a steady easing in

inflation expectations.

Concerning the output gap, the continued weakness of domestic

demand was one factor contributing to continued low inflationary

pressure. With demand still weak, supply-side performance is estimated

to remain adequate. Supply side indicators reflected in the manufacturing

production index continued on a downward trend despite slight upward

correction in the latest developments (Graph 3.13). Similar conditions

were also evident in manufacturing capacity, which has begun to recover

to the 70% range after dipping below 70% in Q1/2009 (Graph 3.14).

Even so, the current level remains below pre-global crisis levels, recorded

in the 80%-85% range. Overall, the supply-side response remained

adequate, with no significant upward pressure on prices. Under these

conditions, inflation dropped to 5.56% (yoy) in from the Q1/2009 level

of 7.15% (yoy).

Graph 3.7

Foreign Capital

������������

����

���������������������

�������

����������������

�����

�����

�����

�����

�

������

������

������

������

������������

�����

������

������

������

������

��������� ������ ��� ��� ��� ��� ��� ��� ������ ��� ��� ������ ��� ��� ���

���� ����

Graph 3.8

Forex Supply and Demand

����������������

�����

�����

�����

�����

�

������������

�����

�����

������

������

������

��������� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ���

���� ����

����������������������������������

�����������������������

�����������������������������������

������������������

�������������

�������������

������

������

������

������

������

������

�����

Graph 3.9

CPI Inflation Grwoth

��

�

�

��

��

��

��

� � � � � � � � � �� �� �� � � � � � � � � � �� �� �� � � � � � �

���� ���� ����

�������������������

�������������������������������

������ �

Monetary Policy Report - Quarter II-2009

20

Measured quarterly, volatile foods underwent deflation in

keeping with the abundant domestic market supply of foodstuffs

brought on by the arrival of the harvest. The volatile foods category

recorded -2.02% deflation (qtq) with rice deflation at about -1% (qtq).

Regarding seasonal factors, Q2/2009 was marked by the arrival of the

rice harvest, which led to deflation in rice commodity prices. Given

the considerable weighting of rice in the volatile food basket, the fall