jl.mh. thamrin no.2 jakarta 10110 - indonesia :// · dollars, equivalent to 6.3 months of imports...

TRANSCRIPT

Jl.MH. Thamrin No.2 Jakarta 10110 - Indonesiahttp://www.bi.go.id

BANK INDONESIAFor further information. please contact:Economic Outlook & Policy DisseminationBureau of Monetary Policy Directorate of Economic Research and Monetary Policy

Telephone : +62 61 3818163 +62 21 3818206Fax. : +62 21 3452489E-mail : [email protected] : http://www.bi.go.id

i

MONETARY POLICY REPORTBANk INdONEsIA

Monetary Policy Report - Quarter I-2011

The Monetary Policy Report is published quarterly by Bank Indonesia after the Board of

Governors’ Meetings in December, April, July, and October. In addition to fulfilling the

mandate of article 58 of Act Number 23 of 1999 concerning Bank Indonesia, amended

by Act No. 3 of 2004 and Act No. 6 of 2009, the report has two main purposes: (i)

to function as a tangible product of a forward-looking working framework in which

formulation of monetary policy is based on economic and inflation forecasts; and (ii) as

a medium for the Board of Governors of Bank Indonesia to present to the public the

various policy considerations underlying its monetary policy decisions.

The Board of Governors

Darmin Nasution Governor

Hartadi A. Sarwono Deputy Governor

S. Budi Rochadi Deputy Governor

Muliaman D. Hadad Deputy Governor

Ardhayadi Mitroatmodjo Deputy Governor

Budi Mulya Deputy Governor

Halim Alamsyah Deputy Governor

MONETARY POLICY REPORTQUARTER I-2011

ii

MONETARY POLICY REPORTBANk INdONEsIA

Monetary Policy Report - Quarter I-2011

iii

MONETARY POLICY REPORTBANk INdONEsIA

Monetary Policy Report - Quarter I-2011

Monetary Policy Strategy

Underlying Principles

Under the ITF, the inflation target is established as the overriding objective and nominal anchor for monetary policy. In this regard, Bank Indonesia has adopted a forward looking strategy by guiding the present monetary policy response for achievement of a medium-term inflation target.

The application of the ITF does not mean that monetary policy disregards economic growth. The basic monetary policy paradigm of striking the optimum balance between inflation and economic growth is retained in both setting the inflation target and in the monetary policy response by focusing on achievement of low, stable inflation in the medium to long-term.

The Inflation Target

Government upon coordination with Bank Indonesia has set and announce an inflation target of CPI every year. Based on PMK No.143/PMK.011/2010 the inflation targets established by the Government for 2010 – 2012 are 5,0%, 5,0%, and 4,5% with ±1% deviation.

Monetary Instruments and Operations

The BI Rate is the published policy rate reflecting the monetary policy stance adopted by Bank Indonesia. The BI Rate is a signal for achieving the medium to long-term inflation target and is announced periodically by Bank Indonesia for a specific period. To strengthen the operational framework for monetary policy, Bank Indonesia changed from use of the 1-month SBI rate as the operational target to the overnight interbank rate with effect from 9 June 2008. In monetary operations, the BI Rate is implemented through liquidity management on the money market to achieve the monetary policy operational target, reflected in movement in the overnight interbank money market rate. To enhance the effectiveness of liquidity management on the market, a set of standing facilities in combination with an interest rate corridor is employed in day-to-day monetary operations.

Policymaking Process

The BI Rate is determined by the Board of Governors in the Monthly Board of Governors’ Meeting. In unforeseen circumstances, the monetary policy stance may be adjusted in advance of the Monthly Board of Governors’ Meeting in a weekly Board of Governors’ Meeting. Changes in the BI Rate essentially depict the Bank Indonesia monetary policy response for guiding the forecasted level of inflation within the limits of the established inflation target.

Transparency

Monetary policy is regularly communicated to the public through customary media for communication, such as statements to the press and market actors, website postings and publication of the Monetary Policy Report (MPR). This transparency is aimed at building improved understanding and shaping public expectations of the economic and inflation outlook and the monetary response taken by Bank Indonesia.

Coordination with the Government

For the purpose of coordination in inflation targeting, monitoring and control, the Government and Bank Indonesia have established a team of officials representing the various relevant agencies. The task of the Team is to deliberate and recommend the necessary policy actions for the Government and Bank Indonesia in managing inflationary pressures for achievement of the established inflation target.

Steps for Reinforcing Monetary Policy with the Overriding Objective of Price Stability (Inflation Targeting Framework)

In July 2005, Bank Indonesia launched a reinforced monetary policy framework consistent with the Inflation Targeting Framework (ITF), encompassing four key elements: (1) use of the BI Rate as the policy reference rate, (2) anticipatory monetary policymaking process, (3) more transparent communications strategy and (4) closer policy coordination with the Government. These measures are intended to strengthen monetary policy effectiveness and governance in order to achieve the overriding objective of price stability in support of sustainable economic growth and greater public prosperity.

Enhanced Monetary Policy Measures Under Inflation Targeting Framework

In July 2005, Bank Indonesia implemented and enhanced monetary policy measures within the Inflation Targeting Framework (ITF) which encompasses four main areas: the use of the BI rate as an operational target, enhanced decision making process, more transparent communications strategy, and strengthened policy coordination with the Government. The measures is intended to strengthen the effectiveness and to provide good governance to its monetary policy making to achieve the price stability needed to support sustainable economic growth and attain social welfare.

iv

MONETARY POLICY REPORTBANk INdONEsIA

Monetary Policy Report - Quarter I-2011

v

MONETARY POLICY REPORTBANk INdONEsIA

Monetary Policy Report - Quarter I-2011

Foreword

The global economic recovery is showing a steady, upward trend. Economies are regaining momentum in

almost all regions, from Asia’s emerging markets to Latin America and advanced economies such as the United States

and Europe. Economic recovery is marked by improving performance in manufacturing, which has benefited from

external sector performance and solid levels of household consumption. Despite this, progress in global economic

recovery remains daunted by a number of risks, including the debt crisis in some European nations. Global inflationary

pressures may also mount further, due to the soaring prices for oil and food commodities.

Domestic economic growth is on an upward trend. In 2011, economic growth is forecasted to reach 6.0%-

6.5% before mounting further to 6.1%-6.6% in 2012. Greater equilibrium is expected in the nation’s economic

growth, due to more robust growth in investment and exports. The expanding role of investment in the economy will

also pave the way for expansion of economic capacity. Exports are also predicted to maintain growth in line with the

ongoing global economic recovery. In analysis by sector, more robust economic activity is forecasted across a range

of sectors, led by transport and communications, trade, hotels and restaurants and the construction sector.

The ongoing improvement in external and domestic conditions underpins the outlook for continued robust

performance in Indonesia’s balance of payments. Throughout 2011, the balance of payments is projected to

chart a considerable surplus. While imports have mounted in keeping with strengthening domestic economic activity,

sustained growth in exports has enabled the current account to maintain a surplus, albeit less than in 2010. The

upbeat economic outlook and looming opportunity for Indonesia to achieve investment grade is expected to benefit

investment with stronger inflows of foreign direct investment (FDI) and portfolio capital, producing yet another hefty

surplus in the capital and financial account. The continued balance of payments surplus will further strengthen the

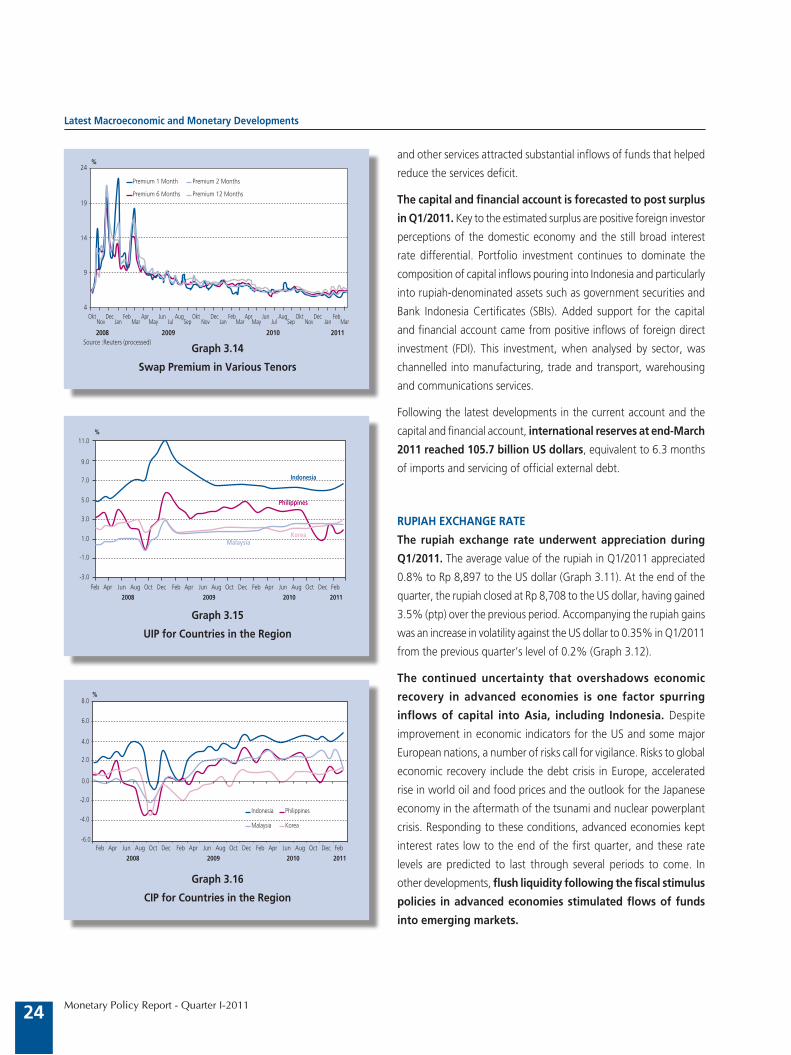

international reserves position. At the end of March 2011, international reserves were recorded at 105.7 billion US

dollars, equivalent to 6.3 months of imports and servicing of official foreign debt.

The rupiah exchange rate has charted further appreciation, bolstered by the improving condition of

Indonesia’s economic fundamentals and solid performance in the balance of payments. By the end of

Q1/2011, the rupiah had gained 3.47% to Rp 8,708 to the US dollar. The strengthening of the rupiah may assist in

The Governor of Bank Indonesia

vi

MONETARY POLICY REPORTBANk INdONEsIA

Monetary Policy Report - Quarter I-2011

easing inflationary pressures, in particular imported inflation related to increases in international commodity prices.

The rupiah has maintained adequate competitiveness to sustain export performance, given that rupiah appreciation

has kept pace with currency trends within the region.

Inflation is on a downward trend, although looming risks still call for vigilance. These risks have arisen from

developments in international commodity prices and steadily rising domestic demand. Inflation expectations also

remain high, necessitating comprehensive measures to curb inflation within the targeted range of 5%±1% in 2011

and 4.5%±1% in 2012. Bank Indonesia will keep a close watch on the risk of inflationary pressure. For this reason,

Bank Indonesia will reinforce the monetary and macroprudential policy mix and strengthen cooperation with the

Government in addressing supply issues.

Further improvement is visible in the bank intermediation function alongside prudently managed financial

system stability. Credit expansion reached 25.1% (yoy) in March 2011, with lending up in all categories including

MSME credit. Despite the brisk pace of credit expansion, credit quality has not deteriorated as reflected in the gross

ratio of non-performing loans (NPLs) that has held below 5%. Also attesting to the robust condition of the domestic

banking system is the capital adequacy ratio (CAR) at 18%.

A comprehensive assessment of the economic outlook with risks shifting towards equilibrium was carefully

considered in the decision in the Bank Indonesia Board of Governors’ Meeting on 12 April 2011 to hold the

BI Rate at 6.75%. Nevertheless, this decision did not alter the tight bias in the Bank Indonesia monetary policy stance

aimed at curbing the persistently high level of inflationary pressure. In addition, to minimise adverse impact from

short-term capital inflows on monetary and financial system stability, the Board of Governors decided to replace the

one-month holding period for Bank Indonesia Certificates (SBIs) with a six-month holding period. This new regulation

will come into force on 13 May 2011.

Jakarta, 12 April 2011

The Governor of Bank Indonesia

Dr. Darmin Nasution

vii

Contents

MONETARY POLICY REPORTBANk INdONEsIA

Monetary Policy Report - Quarter I-2011

Contents

1. Monetary Policy Response Quarter I-2011 ................................. 1

2. Economic Outlook and Risks Ahead ........................................... 3

Assumptions ................................................................................... 3

Economic Growth Outlook .............................................................. 4

Inflation Outlook ............................................................................ 11

Risks ............................................................................................... 12

3. Latest Macroeconomic and Monetary Developments ............... 14

Developments in the World Economy .............................................. 15

Economic Growth ........................................................................... 17

Balance of Payments (BOP) ............................................................. 23

Rupiah Exchange Rate ..................................................................... 24

Inflation .......................................................................................... 25

Dissaggregation of Inflation ............................................................ 26

Monetary Policy .............................................................................. 27

Statistics ............................................................................................ 32

viii

Contents

MONETARY POLICY REPORTBANk INdONEsIA

Monetary Policy Report - Quarter I-2011

1Monetary Policy Report - Quarter I-2011

Monetary Policy Response Quarter I-2011

1. Monetary Policy Response Quarter I-2011

In the Board of Governors’ Meeting convened on 12 April 2011, Bank Indonesia

decided to hold the BI Rate at 6.75%. This decision does not alter the tight bias in

the Bank Indonesia monetary policy stance aimed at curbing the persistently high

level of inflationary pressure in tandem with Government efforts to ease inflationary

pressure from volatile foods. In the opinion of the Board of Governors, rupiah appreciation

has worked effectively in mitigating pressure from imported inflation driven by rising prices

for internationally-traded commodities. Furthermore, to minimise negative impact from

short-term capital inflows on monetary and financial system stability, the Board of Governors

also decided to replace the one-month holding period for Bank Indonesia Certificates (SBIs)

with a six-month holding period, effective from 13 May 2011. Looking forward, Bank

Indonesia sees available headroom for adjustment in the BI Rate level to curb any further

rise in inflationary pressure. Bank Indonesia is confident that this mix of monetary and

macroprudential policies, with added support from strengthened policy coordination with the

Government, will safeguard macro stability and keep inflation on track with the established

target at 5%±1% in 2011 and 4.5%±1% in 2012.

The Board of Governors envisages further improvement in global economic

recovery, as evident in the upward revision of global economic growth projections

by various international agencies. This strengthening of global optimism will also bolster

growth in volume of world trade with positive impact on demand for exported products,

thus contributing to domestic economic growth. However, the global economic recovery

remains daunted by risks and uncertainty related to the debt crisis in some European nations

and potential disruption in manufacturing output in the aftermath of the earthquake in

Japan. In addition, further escalation is projected in world oil and food commodity prices,

generating added inflationary pressure in many advanced nations and emerging economies

including Indonesia.

On the domestic front, the Board of Governors forecasts Indonesia’s economic

growth to mount to 6.0%-6.5% in 2011 and 6.1%-6.6% in 2012. This performance will

be bolstered by greater equilibrium in the sources of growth, with investment forging ahead

alongside continued solid performance in exports. In Q2/2011, the economy is forecasted

to grow at a brisk 6.4%. Investment, led by FDI, is set for an expanded role in building the

capacity of the economy in keeping with buoyant domestic and external demand and the

upgrading of the sovereign credit rating. At the sectoral level, high growth is predicted in all

economic sectors, led by transport and communications, the trade, hotels and restaurants

sector and construction.

Indonesia’s balance of payments is expected to post another hefty surplus in 2011.

Key to this surplus will be performance in the current account and the capital and financial

account. Exports are forecasted to maintain vigorous growth. Foreign portfolio capital

2 Monetary Policy Report - Quarter I-2011

Monetary Policy Response Quarter I-2011

inflows are set to remain strong, while foreign direct investment (FDI) is on an upward

track. In response to these developments, the international reserves position at end-March

2011 reached 105.7 billion US dollars, equivalent to 6.3 months of imports and servicing

of official external debt.

The rupiah charted further appreciation during March 2011. While this can be

explained by the considerable surplus in the balance of payments and positive foreign

investor perceptions of the strength of Indonesia’s economic fundamentals, the rupiah gains

also formed part of the Bank Indonesia policy response for curbing pressure from imported

inflation. By the end of March 2011, the rupiah had strengthened 3.47% (ptp) to Rp 8,708

to the US dollar. So far, rupiah appreciation has not dented Indonesia’s competitiveness in

terms of the exchange rate, as reflected in the sustained high growth that marks Indonesia’s

non-oil and gas export performance.

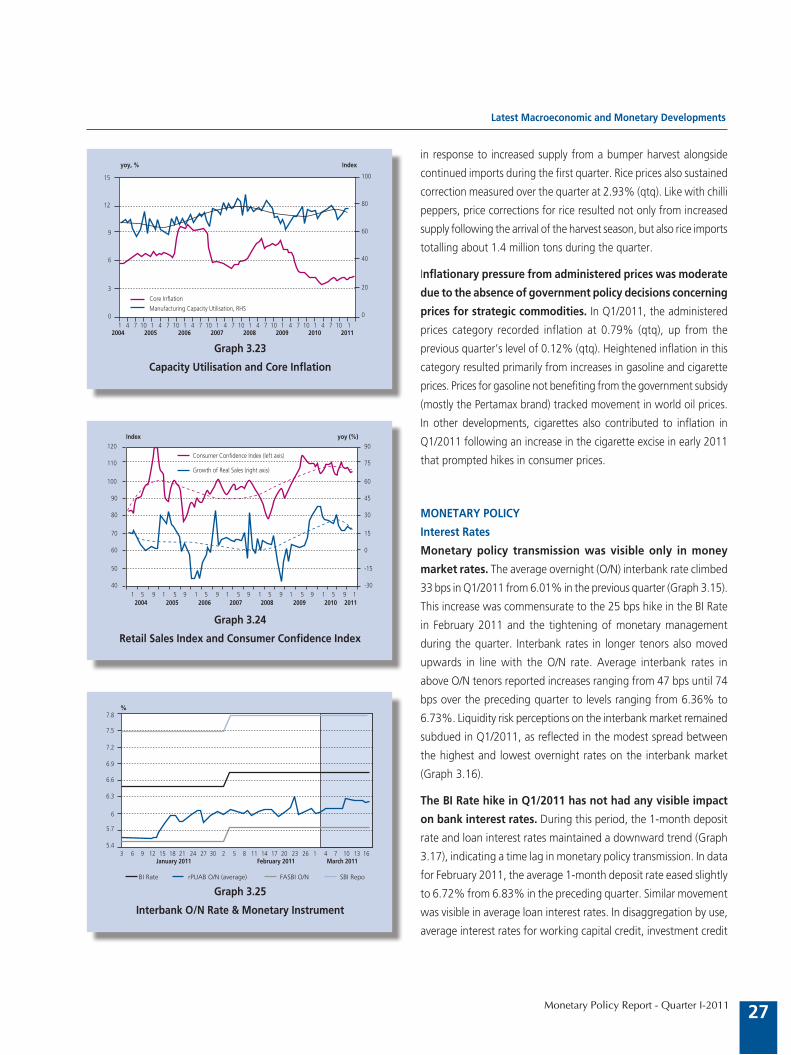

Regarding prices, while inflation has embarked on a downward trend, there is

considerable risk of high inflationary pressure looking forward. CPI inflation in March

2011 was recorded at 6.65% (yoy) following month-on-month deflation at 0.32% (mtm) in

line with correction in food stuffs inflation. Although still high, inflation in the volatile foods

category has shown a downward trend in line with Government actions to strengthen national

food resilience. Similarly, administered prices have experienced only moderate inflation, a

trend related to the minimum price increases announced by the Government. However,

core inflation is on the rise, having reached 4.45% (yoy) or 0.25% (mtm) in March 2011

as a result of secondary effects from high food prices and mounting inflation expectations.

Looking forward, risks of inflationary pressure continue to loom large, stoked by rising

international commodity prices, buoyant domestic demand and high inflation expectations.

Bank Indonesia will closely monitor the risk of inflationary pressure and reinforce the monetary

and macroprudential policy mix to keep inflation on track with the established target.

Financial system stability remained secure, accompanied by steady improvement in

the banking intermediation function and prudently managed banking liquidity. The

stable condition of the banking industry is marked by secure levels of capital and liquidity,

with the capital adequacy ratio (CAR) at a tall 18% and non-performing loans (NPLs) gross

managed at a comfortably safe level below 5%. Improvement in banking intermediation is

also reflected in rising credit growth, recorded in March 2011 at 25.1% (yoy) on the strength

of expansion in all categories of lending including credit to MSMEs.

Economic Outlook and Risk Ahead

3Monetary Policy Report - Quarter I-2011

2. Economic Outlook and Risks Ahead

The Indonesian economy is predicted to chart further improvement while building

greater equilibrium in sources of growth. Higher levels of economic growth will be driven

by a strengthening investment role and continued solid performance of exports. Economic

growth in 2011 is forecasted to reach 6.0%-6.5% and in 2012 to accelerate further to 6.1%-

6.6%. Investment will play an expanding role in economic growth as a result of positive factors

such as the outlook for robust economic growth, potential for achievement of investment

grade and improvements in the investment climate and bureaucratic reforms. Household

consumption is similarly forecasted to increase in line with improvement in wages, export

earnings and support from credit financing extended by banks. On the external side, exports

will maintain high growth to keep pace with escalating demand from trading partner nations

and rising export commodity prices. Analysed by line of business, future improvement in

growth will be supported mainly by manufacturing; the trade, hotels and restaurants sector;

and transport and communications.

Although inflationary pressure has embarked on a downward trend, there is

considerable risk of high inflationary pressure looking forward. Domestic factors

spurring inflation include growing demand, consistent with forecasts of increased economic

growth. Externally, inflationary pressure will come mainly from the upward trend in

international commodity prices. Nevertheless, headroom still exists for further appreciation in

the exchange rate and this is expected to mitigate rising inflationary

pressure from externals. While potential for inflationary pressure

remains strong, the outlook suggests that inflation can be managed

in line with the inflation target at 5%±1% for 2011 and 4.5%±1%

for 2012. Bank Indonesia and the Government will manage inflation

in line with the targeting range by strengthening the policy mix

and coordination.

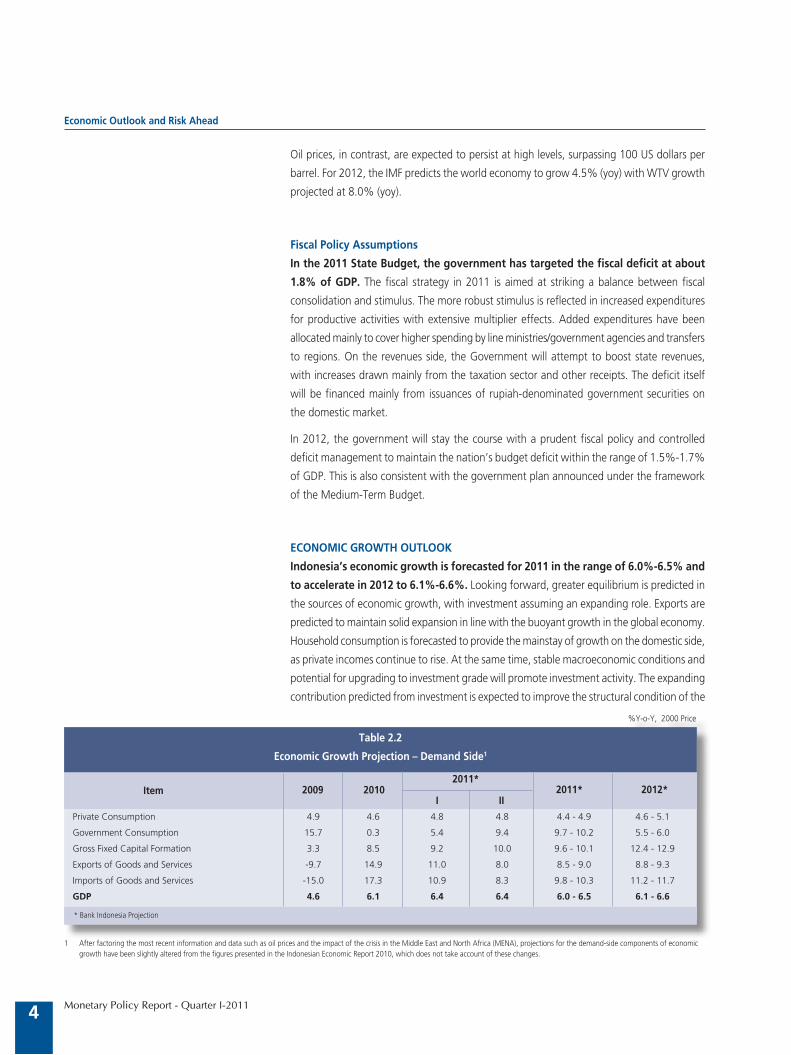

ASSUMPTIONS

Assumptions for the International Economy

Global economic recovery is moving forward albeit with

disparate trends in a multispeed recovery. Optimism for

future recovery in the global economy is evident in the IMF

forecast for world GDP growth in 2011, revised upwards to 4.4%

(Table 2.1). In keeping with the upward revision of global GDP,

the IMF publication projects 2011 growth in world trade volume

(WTV) to reach 7.1% (yoy). Meanwhile, slower increases are

predicted in prices for non-oil and gas commodities, with prices

in 2011 rising 13.4% (yoy).

Table 2.1

World Economic Outlook Projection (% yoy)

2011 2012 2009 2010

Projection

World GDP -0.6 5.0 4.4 4.5

Advanced Economies -3.4 3.0 2.5 2.5

United States -2.6 2.8 3.0 2.7

Euro Area -4.1 1.8 1.5 1.7

Japan -6.3 4.3 1.6 1.8

Other Advanced Economies -1.2 5.6 3.8 3.7

Developing Economies 2.6 7.1 6.5 6.5

Eastern and Central Europe -3.6 4.2 3.6 4.0

Commonwealth Countries -6.5 4.2 4.7 4.6

Developing ASia 7.0 9.3 8.4 8.4

China 9.2 10.3 9.6 9.5

India 5.7 9.7 8.4 8.0

ASEAN -5* 1.7 6.7 5.5 5.7

Latin America and Carribean -1.8 5.9 4.3 4.1

Middle East & North Africa 1.8 3.9 4.6 4.7

* Indonesia, Malaysia, Philippines, Thailand, and VietnamSource : IMF, World Economic Outlook, January 2011

Economic Outlook and Risk Ahead

4 Monetary Policy Report - Quarter I-2011

Oil prices, in contrast, are expected to persist at high levels, surpassing 100 US dollars per

barrel. For 2012, the IMF predicts the world economy to grow 4.5% (yoy) with WTV growth

projected at 8.0% (yoy).

Fiscal Policy Assumptions

In the 2011 State Budget, the government has targeted the fiscal deficit at about

1.8% of GDP. The fiscal strategy in 2011 is aimed at striking a balance between fiscal

consolidation and stimulus. The more robust stimulus is reflected in increased expenditures

for productive activities with extensive multiplier effects. Added expenditures have been

allocated mainly to cover higher spending by line ministries/government agencies and transfers

to regions. On the revenues side, the Government will attempt to boost state revenues,

with increases drawn mainly from the taxation sector and other receipts. The deficit itself

will be financed mainly from issuances of rupiah-denominated government securities on

the domestic market.

In 2012, the government will stay the course with a prudent fiscal policy and controlled

deficit management to maintain the nation’s budget deficit within the range of 1.5%-1.7%

of GDP. This is also consistent with the government plan announced under the framework

of the Medium-Term Budget.

ECONOMIC GROWTH OUTLOOK

Indonesia’s economic growth is forecasted for 2011 in the range of 6.0%-6.5% and

to accelerate in 2012 to 6.1%-6.6%. Looking forward, greater equilibrium is predicted in

the sources of economic growth, with investment assuming an expanding role. Exports are

predicted to maintain solid expansion in line with the buoyant growth in the global economy.

Household consumption is forecasted to provide the mainstay of growth on the domestic side,

as private incomes continue to rise. At the same time, stable macroeconomic conditions and

potential for upgrading to investment grade will promote investment activity. The expanding

contribution predicted from investment is expected to improve the structural condition of the

Item

Table 2.2

Economic Growth Projection – Demand Side1

* Bank Indonesia Projection

Private Consumption 4.9 4.6 4.8 4.8 4.4 - 4.9 4.6 - 5.1

Government Consumption 15.7 0.3 5.4 9.4 9.7 - 10.2 5.5 - 6.0

Gross Fixed Capital Formation 3.3 8.5 9.2 10.0 9.6 - 10.1 12.4 - 12.9

Exports of Goods and Services -9.7 14.9 11.0 8.0 8.5 - 9.0 8.8 - 9.3

Imports of Goods and Services -15.0 17.3 10.9 8.3 9.8 - 10.3 11.2 - 11.7

GDP 4.6 6.1 6.4 6.4 6.0 - 6.5 6.1 - 6.6

2009 2010I II

2011*2011* 2012*

%Y-o-Y, 2000 Price

1 After factoring the most recent information and data such as oil prices and the impact of the crisis in the Middle East and North Africa (MENA), projections for the demand-side components of economic growth have been slightly altered from the figures presented in the Indonesian Economic Report 2010, which does not take account of these changes.

Economic Outlook and Risk Ahead

5Monetary Policy Report - Quarter I-2011

economy. In analysis by line of business, the mainstay sectors of manufacturing, trade, hotels

and restaurants and transportation and communications are expected to carry forward as

the engines of economic growth. In view of these various factors, the Indonesian economy

has potential to grow beyond the forecasted range.

Outlook for Aggregate Demand

Vibrant growth is predicted for household consumption as incomes continue to

rise. Household consumption growth in Q2/2011 is forecasted at 4.8% and to stay within

the 4.4%-4.9% range for 2011 as a whole. In 2012, household consumption growth is

projected even higher in the range of 4.6%-5.1%. Income growth will be driven mainly by

increases in wages and salaries and export revenues.

In 2011, provincial minimum wage levels will rise by an average of 8.7%, ahead of the average

increase in 2010 reported at 8%. The stronger increase in provincial minimum wage levels in

2011 compared to 2010 will also boost private consumption. Besides the provincial minimum

wage, the 10%-15% rise in civil servant salaries and payment of a 13th month salary will

also strengthen household consumption. Civil servant incomes are also expected to benefit

from improved remuneration linked to administrative reforms in some line ministries and

government agencies. According to data held by the National Civil Servant Agency (BAKN),

the total number of civil servants in 2010 reached 4.6 million. Any increase in the purchasing

power of civil servants is therefore expected to provide a boost to household consumption.

Increased earnings will also strengthen expectations of even further improvement in incomes.

Reflecting this are the results of the Bank Indonesia consumer survey indicating an upward

trend in income expectations for the next six months (Graph 2.1).

After only modest expansion in 2010, positive growth forecasted in Government

consumption will deliver a larger contribution to the growth of the economy. In

Q2/2011, government consumption growth is projected to accelerate to 9.4% compared

to the Q1/2011 growth of 5.4% as procurement and other activity

gathers momentum. For 2011 as a whole, government consumption

growth is forecasted in the range of 9.7%-10.2%. Higher government

consumption in 2011 is associated mainly with larger budget

expenditure allocations for personnel, procurement and social aid.

In addition, expected increases in Government oil and natural gas

revenues will expand the available fiscal balance funds will be available

for the regions. Government revenues from oil and natural gas are

also forecasted to rise in response to movement in oil prices, recorded

in Q1/2011 at well over 100 US dollars per barrel.

The stable macroeconomic conditions and upbeat outlook for

the economy will stimulate investment activity in Indonesia. On

08 April 2011, the Standard & Poor’s rating agency raised Indonesia’s

sovereign credit rating to its highest ever level since the 1997 crisis.

Graph 2.1

Expectation of Income 6 months ahead

���

���

���

���

���

���

���

���

���

�����������������������

�����

���

���

���� ������������

Economic Outlook and Risk Ahead

6 Monetary Policy Report - Quarter I-2011

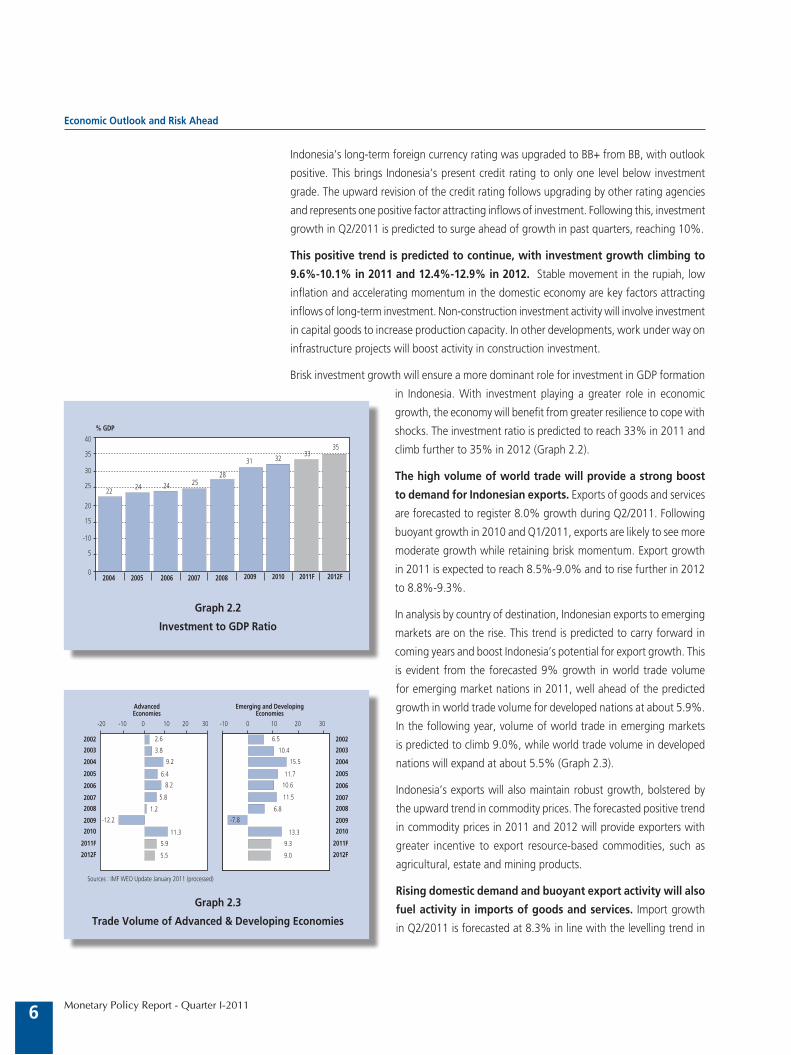

Graph 2.2

Investment to GDP Ratio

�������

����

��

��

��

��

��

���

�

�����

�������������

���� �� ��

��

�� ����

��

���� ���� ���� ���� ���� ����� �����

Graph 2.3

Trade Volume of Advanced & Developing Economies

Indonesia’s long-term foreign currency rating was upgraded to BB+ from BB, with outlook

positive. This brings Indonesia’s present credit rating to only one level below investment

grade. The upward revision of the credit rating follows upgrading by other rating agencies

and represents one positive factor attracting inflows of investment. Following this, investment

growth in Q2/2011 is predicted to surge ahead of growth in past quarters, reaching 10%.

This positive trend is predicted to continue, with investment growth climbing to

9.6%-10.1% in 2011 and 12.4%-12.9% in 2012. Stable movement in the rupiah, low

inflation and accelerating momentum in the domestic economy are key factors attracting

inflows of long-term investment. Non-construction investment activity will involve investment

in capital goods to increase production capacity. In other developments, work under way on

infrastructure projects will boost activity in construction investment.

Brisk investment growth will ensure a more dominant role for investment in GDP formation

in Indonesia. With investment playing a greater role in economic

growth, the economy will benefit from greater resilience to cope with

shocks. The investment ratio is predicted to reach 33% in 2011 and

climb further to 35% in 2012 (Graph 2.2).

The high volume of world trade will provide a strong boost

to demand for Indonesian exports. Exports of goods and services

are forecasted to register 8.0% growth during Q2/2011. Following

buoyant growth in 2010 and Q1/2011, exports are likely to see more

moderate growth while retaining brisk momentum. Export growth

in 2011 is expected to reach 8.5%-9.0% and to rise further in 2012

to 8.8%-9.3%.

In analysis by country of destination, Indonesian exports to emerging

markets are on the rise. This trend is predicted to carry forward in

coming years and boost Indonesia’s potential for export growth. This

is evident from the forecasted 9% growth in world trade volume

for emerging market nations in 2011, well ahead of the predicted

growth in world trade volume for developed nations at about 5.9%.

In the following year, volume of world trade in emerging markets

is predicted to climb 9.0%, while world trade volume in developed

nations will expand at about 5.5% (Graph 2.3).

Indonesia’s exports will also maintain robust growth, bolstered by

the upward trend in commodity prices. The forecasted positive trend

in commodity prices in 2011 and 2012 will provide exporters with

greater incentive to export resource-based commodities, such as

agricultural, estate and mining products.

Rising domestic demand and buoyant export activity will also

fuel activity in imports of goods and services. Import growth

in Q2/2011 is forecasted at 8.3% in line with the levelling trend in

��� ��� � �� �� ��

�����������������

����

����

����

����

����

����

����

����

����

�����

�����

���

���

���

���

���

���

���

����

���

���

�����

��� � �� �� ��

��������������������������������

����

����

����

����

����

����

����

����

����

�����

�����

���

����

����

����

����

����

���

����

���

���

����

�������������������������������������������������

Economic Outlook and Risk Ahead

7Monetary Policy Report - Quarter I-2011

exports. For 2011 overall, imports are predicted to register 9.7%-10.3% growth, while

growth in 2012 will reach 11.2%-11.7%. Analysed by category of merchandise, import

growth will be driven mainly by imports of raw materials and capital goods, in line with

brisk investment activity.

Outlook for Aggregate Supply

Analysed by line of business, future improvement in growth will be supported

mainly by manufacturing; the trade, hotels and restaurants sector; and transport

and communications. Higher manufacturing growth will be driven primarily by rising

household consumption and investment, while also bolstered by continued solid performance

in exports. Performance in the trade, hotels and restaurants sector, while strengthened by

rising household consumption, is also related to high imports. Meanwhile, the transport and

communications sector is projected to maintain solid performance

commensurate with the mounting pace of economic activity.

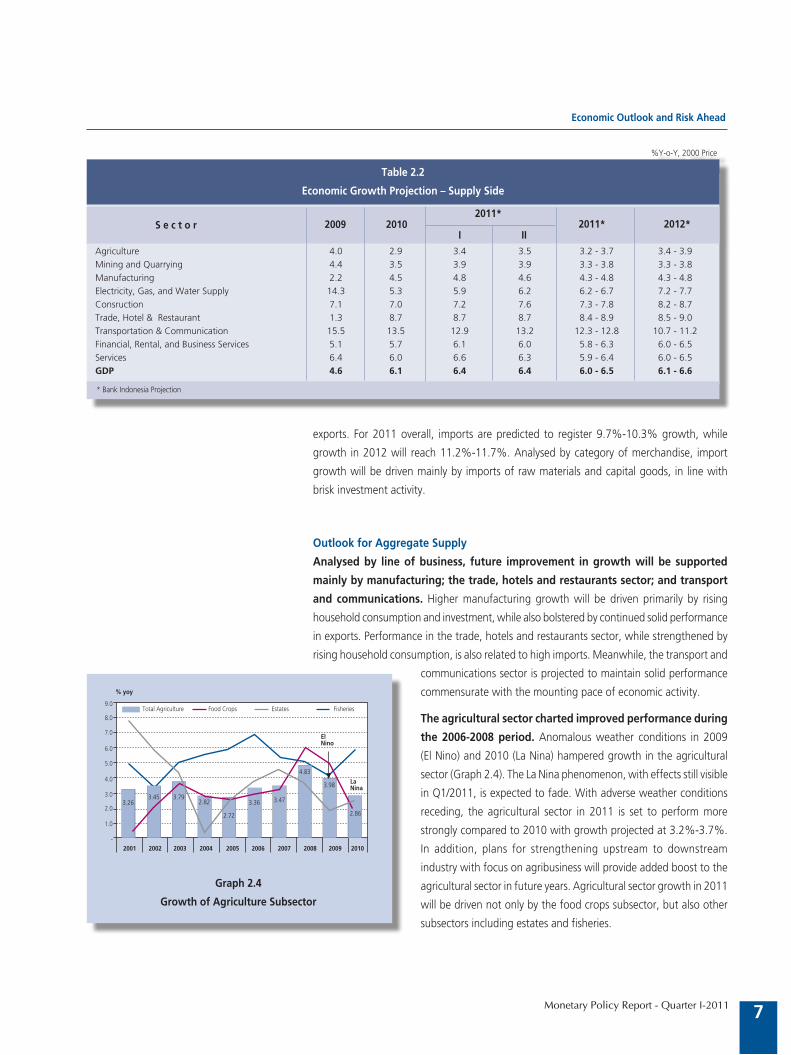

The agricultural sector charted improved performance during

the 2006-2008 period. Anomalous weather conditions in 2009

(El Nino) and 2010 (La Nina) hampered growth in the agricultural

sector (Graph 2.4). The La Nina phenomenon, with effects still visible

in Q1/2011, is expected to fade. With adverse weather conditions

receding, the agricultural sector in 2011 is set to perform more

strongly compared to 2010 with growth projected at 3.2%-3.7%.

In addition, plans for strengthening upstream to downstream

industry with focus on agribusiness will provide added boost to the

agricultural sector in future years. Agricultural sector growth in 2011

will be driven not only by the food crops subsector, but also other

subsectors including estates and fisheries.

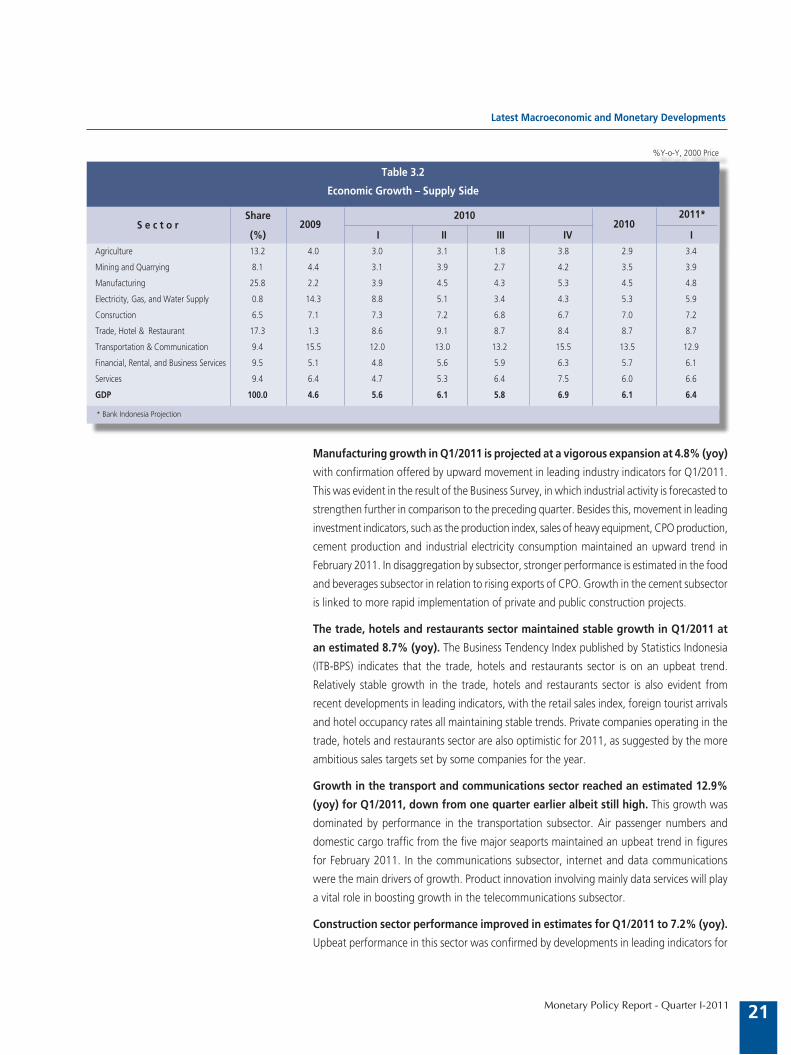

S e c t o r

Table 2.2

Economic Growth Projection – Supply Side

* Bank Indonesia Projection

Agriculture 4.0 2.9 3.4 3.5 3.2 - 3.7 3.4 - 3.9

Mining and Quarrying 4.4 3.5 3.9 3.9 3.3 - 3.8 3.3 - 3.8

Manufacturing 2.2 4.5 4.8 4.6 4.3 - 4.8 4.3 - 4.8

Electricity, Gas, and Water Supply 14.3 5.3 5.9 6.2 6.2 - 6.7 7.2 - 7.7

Consruction 7.1 7.0 7.2 7.6 7.3 - 7.8 8.2 - 8.7

Trade, Hotel & Restaurant 1.3 8.7 8.7 8.7 8.4 - 8.9 8.5 - 9.0

Transportation & Communication 15.5 13.5 12.9 13.2 12.3 - 12.8 10.7 - 11.2

Financial, Rental, and Business Services 5.1 5.7 6.1 6.0 5.8 - 6.3 6.0 - 6.5

Services 6.4 6.0 6.6 6.3 5.9 - 6.4 6.0 - 6.5

GDP 4.6 6.1 6.4 6.4 6.0 - 6.5 6.1 - 6.6

2009 2010I II

2011*2011* 2012*

%Y-o-Y, 2000 Price

Graph 2.4

Growth of Agriculture Subsector

�

���

���

���

���

���

���

���

���

���

���� ���� ���� ���� ���� ���� ���� ���� ���� ����

�����

����������������� ���������� ������� ���������

������

������

�������� ����

����

����

���� ����

����

����

����

Economic Outlook and Risk Ahead

8 Monetary Policy Report - Quarter I-2011

In addition to more favourable weather conditions, growth in the agricultural sector will

also benefit from programmes targeting increased agricultural production, with focus on

agricultural commodities. The food resilience programme is one focus of the Government

priority work programme in 2011-2012. Expansion of food crop cultivation in 2011 will

focus more closely on rice, corn, soy beans, sugar and beef. Food crop cultivation will be

promoted under the Integrated Crop Management (PTT) programme that encompasses use

of superior varieties, quality label seeds, regulation of the crop population and fertiliser use

and deployment of field laboratories. The government has established a target of building a

10 million ton surplus rice production under the Gerakan Surplus Beras programme, launched

in 2011. To this end, the Ministry of Agriculture is engaged in an aggressive drive to develop

special hybrid strains of rice.

Stronger performance is projected in the estates and fisheries subsectors during 2011. High

demand coupled with international market prices for estate commodities offer considerable

incentive for expansion in the estates subsector. Estate crop production

is predicted to rise in 2011, bolstered by Government programmes

for boosting productivity of cocoa, tea, sugar cane, coffee and oil

palm plantings. Looking forward, the estates subsector is expected to

show even further improvement in view of the investments planned

by some state enterprises operating in primary industry. During the

2011-2014 period, investment is slated for rubber, oil palm, sugar,

tea, coffee and cocoa cultivation in Sumatra, Java (including Jakarta),

Kalimantan, Sulawesi, the North Moluccas, Bali-Nusa Tenggara and

Papua-Moluccas. Stronger performance is also forecasted in the

fisheries subsector, driven in part by high demand for seaweed, eels,

silver catfish and smoked garfish.

Manufacturing has picked up with growth approaching levels

reached before the 2008 global economic crisis (Graph 2.5).

While manufacturing has been driven by rising domestic demand,

the improvement in global economic conditions will also benefit

export performance (Graph 2.6). The outlook for increasing demand

provides incentive for expansion in domestic and export-oriented

manufacturing. Among the indicators of expansion in the industrial

sector is growing activity in imports of raw materials and capital

goods as well as non-construction investment.

However, following the Japan earthquake, the upbeat performance

in manufacturing is overshadowed by looming risks in the

transportation equipment and oil and natural gas refining subsectors,

particularly during Q2/2011. The disaster in Japan has kindled fears

of disruption in supply of components and raw materials for vehicles

and heavy equipment. In other developments, the risk looming in

the oil and natural gas refining subsector is related to the burning

of raw material storage tanks owned by Pertamina in early April

Graph 2.5.

Growth of Manufacturing

Graph 2.6.

Growth of Export and Non Oil & Gas Industry

���� ���� ���� ���� ���� ���� ���� �������� ����

������

������ ������������������������

����

����

����

���

�

�����

������

������

���

���

���

���

���

���

���

���

�

�

���

���

���

���

���

���

���

���� ���� ���� ���� ���� ���� ���� ���� ���� ���� ����� �����

������

��������������������������������������������������������������������������������������

��� ���

���

��� ���

���

��� ��� ���

���

���

���

Economic Outlook and Risk Ahead

9Monetary Policy Report - Quarter I-2011

2011. Nevertheless, the fires at the Pertamina storage tanks in

Cilacap are expected to have minimum impact on fuel production.

Aside from these factors, the potential for disruption in supply of

automotive components as a result of the Japan quake is seen as

only temporary.

Optimism for strengthening industry performance is also supported

by efforts by the Ministry of Industry to focus industrial development

in six priority areas of industry. These priority industries are labour

intensive and consist of textiles and textile products, small and

medium-scale industries, capital goods production and resource-

based, high growth and special priority industries. To promote

accelerated economic growth in Indonesia, the Ministry of Industry

has grouped industrial development into six economic corridors,

namely Sumatra, Kalimantan, Sulawesi and North Moluccas, Java, Bali

and Nusa Tenggara and Papua and the Moluccas. In other actions to

promote more rapid expansion in priority industries, the Government

will offer fiscal incentives including import duty exemptions on capital

goods and raw materials needed to support priority manufacturing

production in Indonesia.

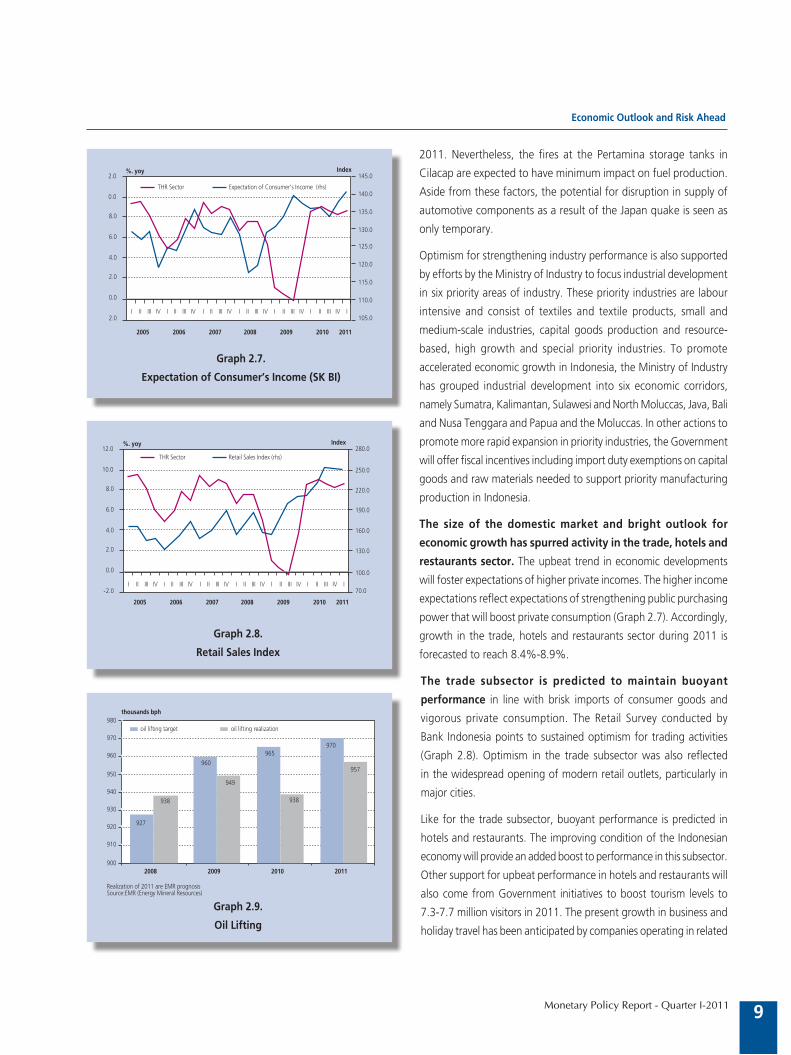

The size of the domestic market and bright outlook for

economic growth has spurred activity in the trade, hotels and

restaurants sector. The upbeat trend in economic developments

will foster expectations of higher private incomes. The higher income

expectations reflect expectations of strengthening public purchasing

power that will boost private consumption (Graph 2.7). Accordingly,

growth in the trade, hotels and restaurants sector during 2011 is

forecasted to reach 8.4%-8.9%.

The trade subsector is predicted to maintain buoyant

performance in line with brisk imports of consumer goods and

vigorous private consumption. The Retail Survey conducted by

Bank Indonesia points to sustained optimism for trading activities

(Graph 2.8). Optimism in the trade subsector was also reflected

in the widespread opening of modern retail outlets, particularly in

major cities.

Like for the trade subsector, buoyant performance is predicted in

hotels and restaurants. The improving condition of the Indonesian

economy will provide an added boost to performance in this subsector.

Other support for upbeat performance in hotels and restaurants will

also come from Government initiatives to boost tourism levels to

7.3-7.7 million visitors in 2011. The present growth in business and

holiday travel has been anticipated by companies operating in related

Graph 2.7.

Expectation of Consumer’s Income (SK BI)

�����

�����

�����

�����

�����

�����

�����

�����

�����

����

���

���

���

���

���

����

����

���� ���� ���� ���� ���� ���� ����

�����������

� �� ��� �� � �� ��� �� � �� ��� �� � �� ��� �� � �� ��� �� � �� ��� �� �

���������� ���������������������������������������

Graph 2.8.

Retail Sales Index

����

�����

�����

�����

�����

�����

�����

�����

����

���

���

���

���

���

����

����

���� ���� ���� ���� ���� ���� ����

�����������

����������� ������������������������

� �� ��� �� � �� ��� �� � �� ��� �� � �� ��� �� � �� ��� �� � �� ��� �� �

Graph 2.9.

Oil Lifting

���

���

���

���

���

���

���

���

���

���� ���� ���� ����

�������������

������������������ �����������������������

��������������������������������������������������������������������������

���

���

���

���

���

���

���

���

Economic Outlook and Risk Ahead

10 Monetary Policy Report - Quarter I-2011

lines of business, such as flights and accommodation. Some airlines

have responded to growing travel by expanding their aircraft fleets,

increasing flight frequency or opening new routes. Meanwhile, the

hospitality industry has seen a rush to build budget hotels, comprising

lower-priced 1 or 2 star accommodation. These hotels are being

developed to meet demand for short-term or transit accommodation,

currently a rapidly growing segment of the market.

The transport and communications sector is forecasted to

keep charting a respectable level of growth. The main engine of

growth in this sector, like before, is the communications subsector.

Service innovations are continually rolling out, particularly in

relation to development of data services infrastructure. Although

not dominant, the transportation subsector has also shown positive

growth. Performance in the transportation subsector is closely tied to

the dynamics of wider economic activity. The predicted expansion in

economic activity will also stimulate activity in freight and passenger

transportation. Bolstered by these developments, the transport and

communications sector is predicted to maintain vigorous growth at

12.3% in 2011.

Improved fortunes are predicted for the mining and quarrying

sector in 2011 compared to the year before. More favourable

weather conditions this year will pave the way for increased mining

activity compared to the past year. Production in the oil and gas

subsector is forecasted to rise (Graphs 2.9 and 2.10). In the non-oil

and gas subsector, coal offers bright prospects, given the steady

rise in domestic and foreign demand. Indonesian coal is not only in

demand in other countries in Asia, but also in Europe. At home, the

Government plans to expand the use of coal with the development

of coal bed methane (CBM) for power generation. Gas from CBM

project in the Sangatta field is targeted to come on stream for power

generation supplying the national grid before the end of 2011.

More rapid progress on infrastructure projects in 2011 is

expected to bolster performance in the construction sector. In

2011, the Government plans to develop infrastructure in a range of

sectors in support of national economic growth. A number of airport

expansion projects are targeted in the transportation infrastructure

development for 2011. Slated for expansion are the Achmad Yani

and Samarinda Baru airports, the Ngurah Rai international airport in

Bali, Sorong airport, airfields for pioneering routes in the Moluccas

and Papua, the Tampa Padang airport (Mamuju) and the Lombok

international airport. Aside from infrastructure development,

construction sector performance will also be driven by commercial

Graph 2.10.

Natural Gas Lifting

�����

�����

�����

�����

�����

�����

�����

���� ���� ���� ����

�����������������������

�������������������

��������������������������������������������������������������������������

�����

�����

�����

�����

Graph 2.11.

Oil Price and WPI Import

�

���

���

���

���

���

���

���

���

���

�

��

��

��

��

���

���

���

� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

���������������

����������

���������������

���� ���� ���� ���� ���� ���� ���� ����

Graph 2.12.

Manufacturing Production Capacity and Core Inflation

����

����

����

����

����

�����

�����

���

����

����

����

����

����

����

����

����

����

���� ���� ���� ���� ���� ����

� ����

���������������������������������������

��������������

� � � � � � � � � � � � � � � � � � � � �

Economic Outlook and Risk Ahead

11Monetary Policy Report - Quarter I-2011

property developments such as shopping centres, offices and

apartments.

INFLATION OUTLOOK

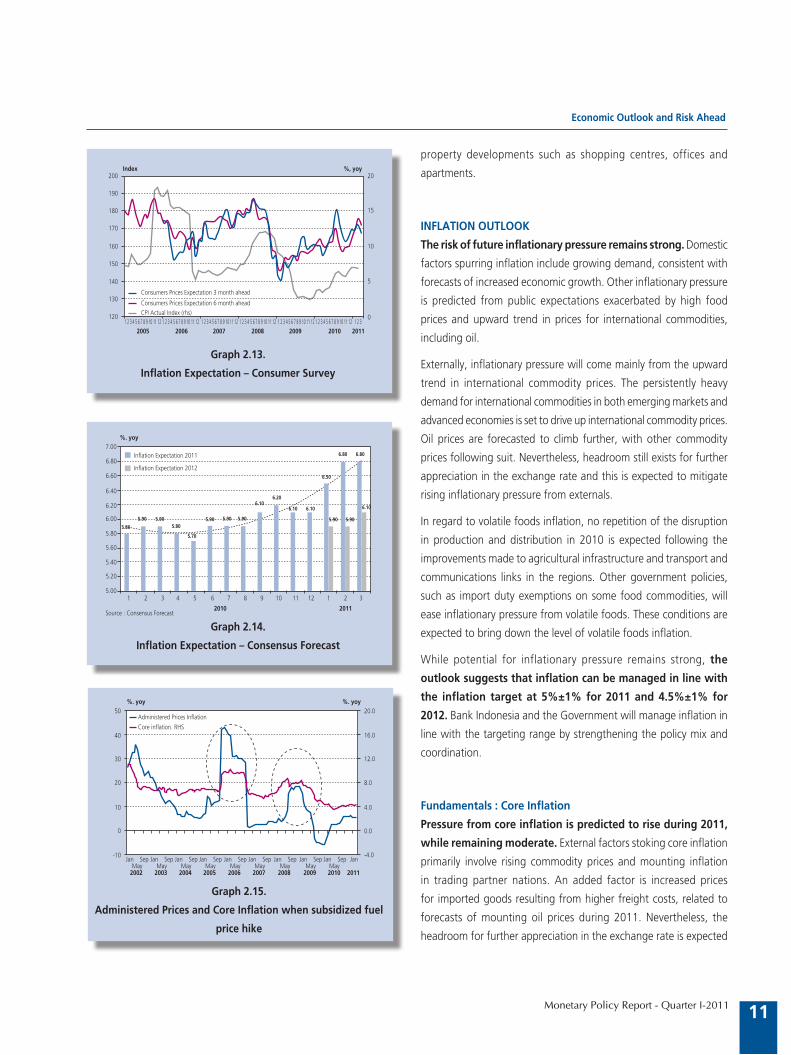

The risk of future inflationary pressure remains strong. Domestic

factors spurring inflation include growing demand, consistent with

forecasts of increased economic growth. Other inflationary pressure

is predicted from public expectations exacerbated by high food

prices and upward trend in prices for international commodities,

including oil.

Externally, inflationary pressure will come mainly from the upward

trend in international commodity prices. The persistently heavy

demand for international commodities in both emerging markets and

advanced economies is set to drive up international commodity prices.

Oil prices are forecasted to climb further, with other commodity

prices following suit. Nevertheless, headroom still exists for further

appreciation in the exchange rate and this is expected to mitigate

rising inflationary pressure from externals.

In regard to volatile foods inflation, no repetition of the disruption

in production and distribution in 2010 is expected following the

improvements made to agricultural infrastructure and transport and

communications links in the regions. Other government policies,

such as import duty exemptions on some food commodities, will

ease inflationary pressure from volatile foods. These conditions are

expected to bring down the level of volatile foods inflation.

While potential for inflationary pressure remains strong, the

outlook suggests that inflation can be managed in line with

the inflation target at 5%±1% for 2011 and 4.5%±1% for

2012. Bank Indonesia and the Government will manage inflation in

line with the targeting range by strengthening the policy mix and

coordination.

Fundamentals : Core Inflation

Pressure from core inflation is predicted to rise during 2011,

while remaining moderate. External factors stoking core inflation

primarily involve rising commodity prices and mounting inflation

in trading partner nations. An added factor is increased prices

for imported goods resulting from higher freight costs, related to

forecasts of mounting oil prices during 2011. Nevertheless, the

headroom for further appreciation in the exchange rate is expected

Graph 2.13.

Inflation Expectation – Consumer Survey

��������

���

���

���

���

���

���

���

���

������������������������������������������

����������������������������������������������������������������

��

��

��

�

�

������

�������������������������� �������������������������� �������������������������� �������������������������� �������������������������� �������������������������� ��������� ���� ���� ���� ���� ���� ����

Graph 2.14.

Inflation Expectation – Consensus Forecast

����

����

����

����

����

����

����

����

����

����

����

����

���� ��������

����

���� ���� ����

��������

���� ����

����

���� ����

����

���� ����

� � � � � � � � � �� �� �� � � �

��������������������������

��������������������������

���� �������������������������������

������

Graph 2.15.

Administered Prices and Core Inflation when subsidized fuel

price hike

��

��

��

��

��

�

���

����

����

����

���

���

���

����

������������������������������������������������

������ ������

������

���

����

������

���

����

������

���

����

������

���

����

������

���

����

������

���

����

������

���

����

������

���

����

������

���

����

���

����

Economic Outlook and Risk Ahead

12 Monetary Policy Report - Quarter I-2011

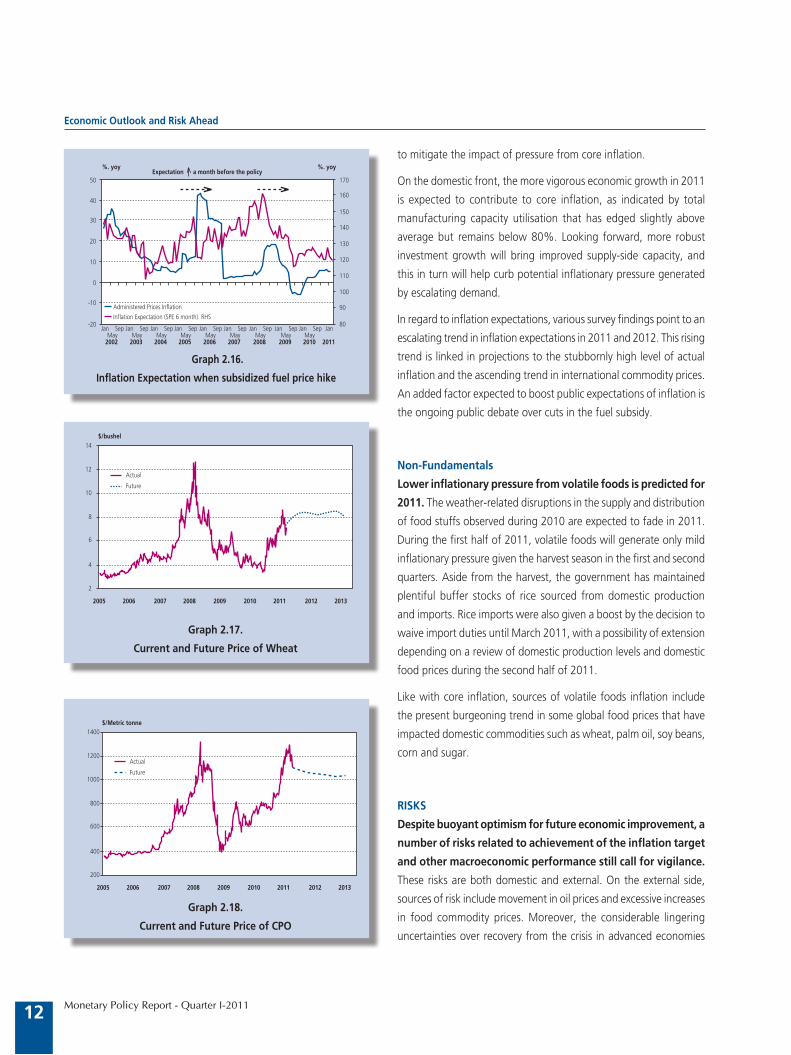

to mitigate the impact of pressure from core inflation.

On the domestic front, the more vigorous economic growth in 2011

is expected to contribute to core inflation, as indicated by total

manufacturing capacity utilisation that has edged slightly above

average but remains below 80%. Looking forward, more robust

investment growth will bring improved supply-side capacity, and

this in turn will help curb potential inflationary pressure generated

by escalating demand.

In regard to inflation expectations, various survey findings point to an

escalating trend in inflation expectations in 2011 and 2012. This rising

trend is linked in projections to the stubbornly high level of actual

inflation and the ascending trend in international commodity prices.

An added factor expected to boost public expectations of inflation is

the ongoing public debate over cuts in the fuel subsidy.

Non-Fundamentals

Lower inflationary pressure from volatile foods is predicted for

2011. The weather-related disruptions in the supply and distribution

of food stuffs observed during 2010 are expected to fade in 2011.

During the first half of 2011, volatile foods will generate only mild

inflationary pressure given the harvest season in the first and second

quarters. Aside from the harvest, the government has maintained

plentiful buffer stocks of rice sourced from domestic production

and imports. Rice imports were also given a boost by the decision to

waive import duties until March 2011, with a possibility of extension

depending on a review of domestic production levels and domestic

food prices during the second half of 2011.

Like with core inflation, sources of volatile foods inflation include

the present burgeoning trend in some global food prices that have

impacted domestic commodities such as wheat, palm oil, soy beans,

corn and sugar.

RISKS

Despite buoyant optimism for future economic improvement, a

number of risks related to achievement of the inflation target

and other macroeconomic performance still call for vigilance.

These risks are both domestic and external. On the external side,

sources of risk include movement in oil prices and excessive increases

in food commodity prices. Moreover, the considerable lingering

uncertainties over recovery from the crisis in advanced economies

Graph 2.16.

Inflation Expectation when subsidized fuel price hike

��

��

��

��

��

�

���

���

���

���

���

���

���

��

���������������������������������������������������������������������

������ ������

������

���

����

������

���

����

������

���

����

������

���

����

������

���

����

������

���

����

������

���

����

������

���

����

������

���

����

���

����

���

���

���

��

������������������������������������������

Graph 2.17.

Current and Future Price of Wheat

��

��

��

�

�

�

�

���� ���� ���� ���� ���� ���� ���� ���� ����

��������

������

������

Graph 2.18.

Current and Future Price of CPO

����

����

����

���

���

���

���

���� ���� ���� ���� ���� ���� ���� ���� ����

��������������

������

������

Economic Outlook and Risk Ahead

13Monetary Policy Report - Quarter I-2011

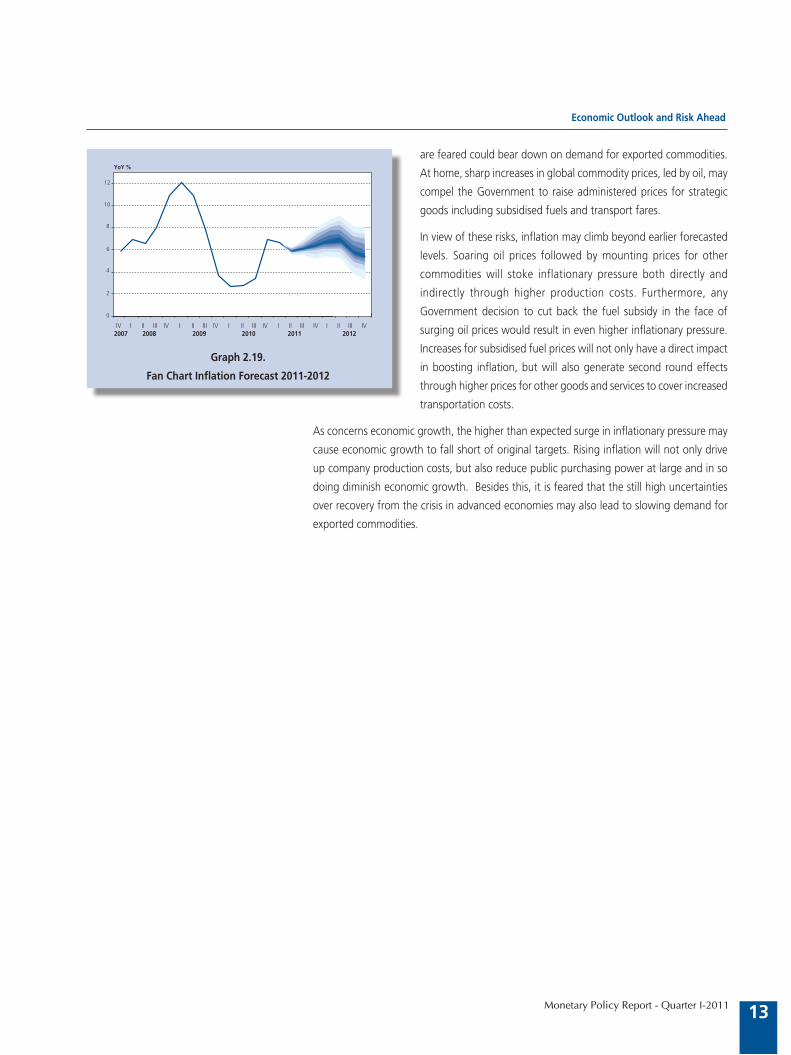

are feared could bear down on demand for exported commodities.

At home, sharp increases in global commodity prices, led by oil, may

compel the Government to raise administered prices for strategic

goods including subsidised fuels and transport fares.

In view of these risks, inflation may climb beyond earlier forecasted

levels. Soaring oil prices followed by mounting prices for other

commodities will stoke inflationary pressure both directly and

indirectly through higher production costs. Furthermore, any

Government decision to cut back the fuel subsidy in the face of

surging oil prices would result in even higher inflationary pressure.

Increases for subsidised fuel prices will not only have a direct impact

in boosting inflation, but will also generate second round effects

through higher prices for other goods and services to cover increased

transportation costs.

As concerns economic growth, the higher than expected surge in inflationary pressure may

cause economic growth to fall short of original targets. Rising inflation will not only drive

up company production costs, but also reduce public purchasing power at large and in so

doing diminish economic growth. Besides this, it is feared that the still high uncertainties

over recovery from the crisis in advanced economies may also lead to slowing demand for

exported commodities.

Graph 2.19.

Fan Chart Inflation Forecast 2011-2012

�

�

�

�

�

��

��

�����

�� ��� ��� �� ��� ��� �� ��� ��� ������ ���� ���� ����

���� ������

�� ���� �� ������

Monetary Policy Report - Quarter I-2011

3. Latest Macroeconomic and Monetary Developments

The ongoing global economic recovery has also strengthened the performance of the domestic

economy. During Q1/2011, the more vibrant economic recovery in emerging market nations

was buoyed by solid domestic consumption and improving performance in externals. These

conditions have had a positive impact on economic developments in Indonesia. Indonesia’s

economic growth for Q1/2011 is forecasted at 6.4%, driven mainly by exports and rising

investment. Exports are forecasted to maintain brisk growth in line with improvement in the

global economy and support from rising commodity prices. This combination of domestic

and external demand kept import volume running high during Q1/2011. On the supply-side,

stronger growth is predicted in the economic sectors of construction and electricity, gas and

water utilities. Manufacturing is also expected to chart significant growth.

Upbeat performance of the domestic economy, improvement in risk indicators and continued

attractiveness of yields on rupiah instruments all contributed to exchange rate appreciation.

During Q1/2011, the rupiah exchange rate charted further gains. The robust GDP growth

outcome and strong performance in the balance of payments bolstered the exchange rate,

with the rupiah appreciating by an average of 0.8% to Rp 8,897 to the US dollar despite

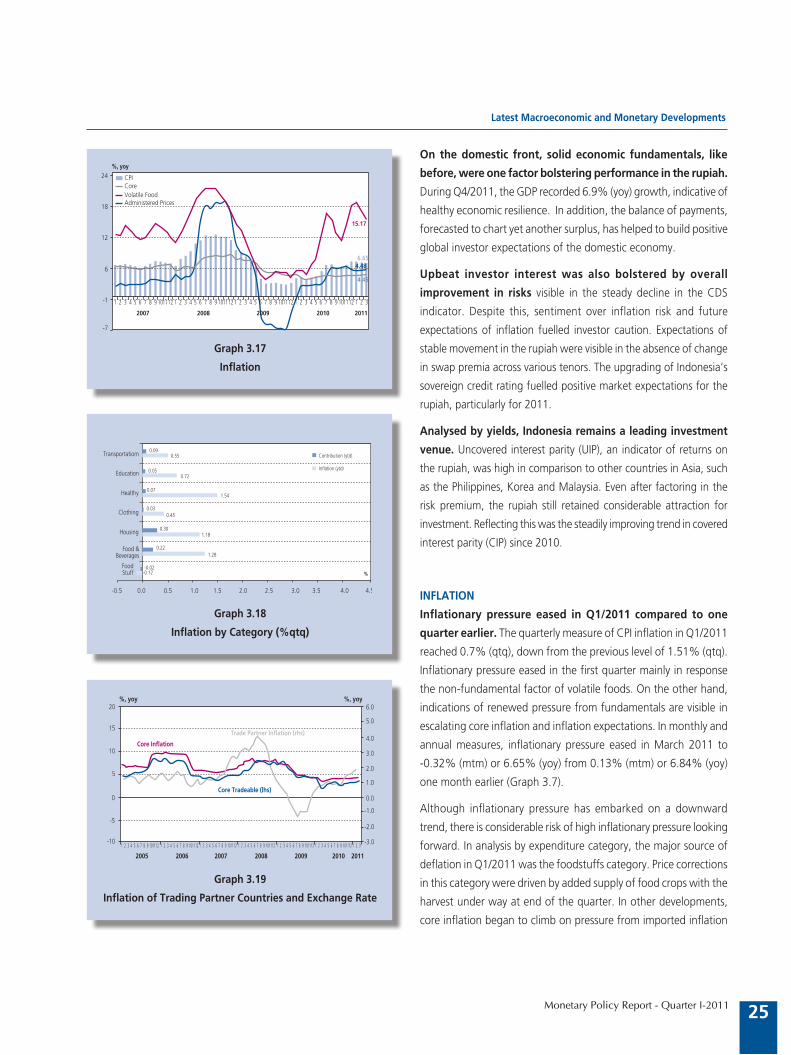

greater volatility than in the preceding quarter. In regard to prices, inflationary pressure eased

in Q1/2011 compared to one quarter earlier. Measured annually, CPI inflation in Q1/2011

eased to 6.65% (yoy) from the Q4/2010 level of 6.96% (yoy), primarily from correction

in volatile foods. In contrast, pressure from fundamentals, visible in core inflation, began

escalating in response to strengthening demand.

Monetary policy transmission showed mainly on the financial market, while transmission

through the banking sector was not yet evident due to the effect of monetary policy lag.

Short-term interest rates, reflected in the rates on the interbank market, remained at

conducive levels as indicated by stable movement in the overnight rate at about the BI Rate

level during Q1/2011. However, monetary policy lag was visible in the ongoing downward

movement in deposit and lending rates some time after the BI Rate increase. Monetary policy

transmission in the credit channel was marked by a rise in credit expansion to 25.1% (yoy), up

from the level reached one month before at 22.1% (yoy). Similarly, positive monetary policy

transmission was also observed on the capital market and markets for government securities

and mutual funds. On the stock market, Indonesia’s composite index - the JCI - mounted

steadily to a level of 3,678. Yields on the government securities market widened early in the

period under review, but eased again following the increase in the BI Rate. Performance of

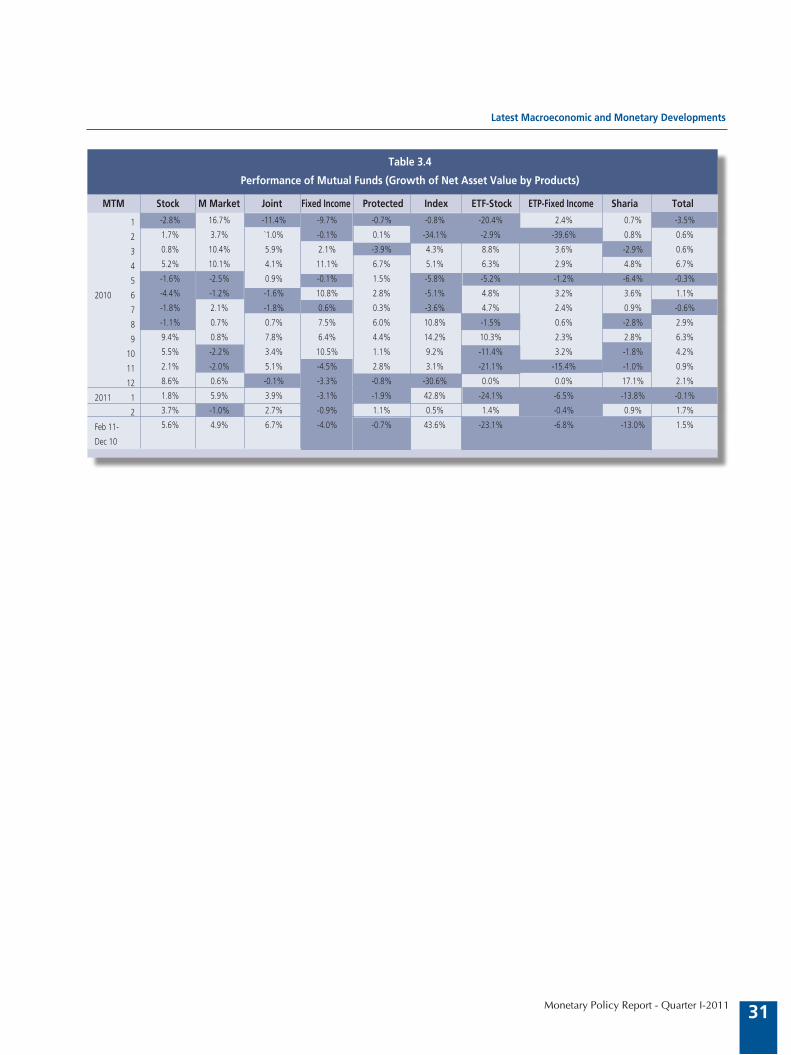

mutual funds was also up from the preceding quarter.

Latest Macroeconomic and Monetary Developments

14

Monetary Policy Report - Quarter I-2011

DEVELOPMENTS IN THE WORLD ECONOMY

Global economic recovery is predicted to carry forward on momentum generated by

emerging markets. Signs of this were visible in the higher than expected growth in 2010

that has contributed to more optimistic forecasts for growth for 2011. This is also consistent

with the upward revision in the 2011 growth projections by some international institutions.

The combination of ongoing recovery in the global economy with negative sentiment from

the geopolitical crisis in the Middle East and North Africa (MENA) and the natural disaster

in Japan has sent world commodity prices soaring with oil trading at over 100 US dollars

per barrel. The effect of this will be to stoke global inflationary pressure, with impact felt

in both emerging markets and advanced economies. As regards policy stance, emerging

markets have introduced further monetary tightening with interest rate increases, tighter

liquidity management and tolerance of currency appreciation. However, monetary policy in

advanced economies has maintained an accommodative stance although some countries and

also the European Central Bank (ECB) have begun raising their policy rates. Looking forward,

world economic growth faces various risks from the impact of the disaster in Japan, political

crisis in the MENA region, mounting world commodity prices, the debt and fiscal crisis in

the PIIGS nations and the global monetary policy response. On financial markets worldwide,

growth has been constrained by negative sentiment from the MENA geopolitical crisis and

the disaster in Japan. Besides this, the bearish condition of global financial markets has come

in response to monetary tightening in China and mounting tensions in the deft and fiscal

deficit crises in Europe. Global markets remain awash with liquidity, despite some liquidity

tightening in some nations including China, Europe and Japan.

US economic growth is again estimated in positive territory for Q1/2011, buoyed

by the industry sector. Confirmation of the solid gains in industry came from industry

indicators such as the Purchasing Manager Index, which remains on an upward trend. US

industrial growth in Q1/2011 is estimated at 5.3% (yoy), consistent with the strength of

external demand. Household consumption is predicted to remain stable, as indicated by

retail sales and household income and expenditure indicators moving into positive territory.

Despite this, household consumption remains daunted by high unemployment in the US,

recorded at 8.8%.

Sustained positive growth is also estimated for Eurozone economies in Q1/2011.

Positive economic growth in Europe was supported by economic expansion in Germany and

France with growth during the quarter running at 4.1% (yoy) and 1.7% (yoy). However, the

ability of Portugal, Ireland, Italy, Spain and Greece (the PIIGS nations) to promote economic

growth was constrained by the impact of fiscal tightening. From an overall perspective,

manufacturing remains the backbone of the European economy as nations respond to rising

external demand. Household consumption has maintained moderate growth, reflected in the

limited improvement in consumer confidence against the background of Europe’s persistently

high unemployment at 10%.

Asian economies are predicted to keep growing although at a more moderate

pace in line with the monetary tightening trend in Asia. Even so, still vibrant levels of

domestic demand and accommodative fiscal policies mean that Asian economies are set

Latest Macroeconomic and Monetary Developments

15

Monetary Policy Report - Quarter I-2011

to maintain expansion. Exports, the primary engine of growth in many Asian economies,

will return to normal in line with more modest economic expansion in China, the major

destination for exports from Asian countries. The moderation in China’s economic growth

will result from monetary tightening policies introduced by the nation’s authorities to curb

signs of overheating. Asian economies as a whole will keep forging ahead with expansion

despite the threat of rising inflationary pressure.

Commodity prices maintained upward movement during Q1/2011. According to

IMF projections as of February 2011, the commodity price index is on an ascending trend.

In monthly figures, the IMF commodity price index in January and February mounted by

6.6% and 4.4%. The rise in the index during February in particular was driven by increases

in fuel commodities and especially the price of oil. Oil prices have surged on fears of supply

disruptions triggered by escalating tensions in Egypt and Tunisia, which adds to the effect

on prices from the ongoing process of global economic recovery. Measured against the

preceding year, the commodity price index in January and February reported gains of

27.6% (yoy) and 26.0% (yoy). This surge in commodity prices also contributed in higher

world inflation during Q1/2011. Composite data on inflation outcomes in various countries

points to mounting global inflationary pressure in February 2011 compared to the previous

quarter. Inflation mounted to 3.7% (yoy) after being recorded at 3.3% (yoy) in Q4/2010

due to escalating world commodity prices.

Central banks in advanced economies continue to lean towards accommodative

monetary policy with renewed quantitative easing measures to boost their

economies. During Q1/2011, leading central banks, including the Fed, BoJ and ECB,

maintained low policy rates in a drive to promote domestic economic recovery. The Fed

held its policy rate in the 0%-0.25% range against a background of stubbornly high

unemployment and predictions of continued low inflation. The ECB followed suit by leaving

its rate unchanged at 1.0% to create a conducive climate for resolution of the European fiscal

crisis. Meanwhile, the BoJ responded the impact of the disaster in Japan that had triggered

bank liquidity shortages by injecting liquidity into the banking system. The Reserve Bank of

New Zealand lowered its policy rate by 50 bps to 2.50% in an effort to stimulate economic

recovery in the area struck by an earthquake in February 2011. In contrast, the Swedish

Riksbank opted for a different course through a policy of monetary tightening by raising its

policy rate to 1.50% in response to mounting inflationary pressure.

On the other hand, central banks in emerging markets are tightening monetary

policy through increases in interest rates in tandem with liquidity management

and macroprudential policies in the financial system. Some central banks in emerging

markets (Asia and Latin America) have embarked on monetary tightening to cope with

mounting inflationary pressure in these regions. Asian central banks announcing rate

increases included China (+25 bps), Philippines (+25 bps), India (+50 bps), Korea (+50 bps)

and Thailand (+50 bps). In Latin America, interest rates were raised by central banks in Brazil

(+100 bps), Chile (+75 bps), Colombia (+50 bps) and Peru (+75 bps). In addition to raising

interest rates, some central banks in emerging market economies also instituted non-interest

rate policies during Q1/2011. Monetary authorities in Singapore, Hong Kong and Taiwan

Latest Macroeconomic and Monetary Developments

16

Monetary Policy Report - Quarter I-2011

employed currency appreciation as a means to curb inflation. The central bank of Vietnam

raised its refinance rate and discount rate to 12%, while the policy rate remained unchanged.

Malaysia pursued similar action when the nation’s central bank raised the statutory reserve

requirement ratio to 2% without any change in the policy rate. The People’s Bank of China

also announced an increase in the reserve requirement for major banks to 20%, effective

from 25 March 2011.

The brisk advancement on global financial market abruptly slowed due to negative

geopolitical sentiment from the MENA region and natural disaster that hit Japan.

Global financial markets plunged significantly in response to mounting geopolitical turmoil

in the MENA region, despite the release of economic data pointing to further recovery in the

world economy. The disaster in Japan put even greater pressure on global financial markets

and disrupted activity in the nation’s economy. The bearish condition of global financial

markets is also explained by the fallout from the debt and fiscal deficit crises in Europe

after decisions by the Moody’s and Fitch rating agencies to downgrade credit ratings for

Greece, Spain and Portugal. This has prompted investors to switch to risk averse behaviour

by shunning higher-risk assets, including those in emerging market economies. Meanwhile,

the flush condition of global liquidity is predicted to continue. The accommodate interest

rate policies adopted under the quantitative easing by central banks in advanced economies

have created the present conditions of flush liquidity. However, indications of a liquidity

crunch are emerging in some nations, including Europe, China and Japan, as reflected in

higher rate quotations on the interbank market (LIBOR).

ECONOMIC GROWTH

Aggregate Demand

Indonesia’s economic growth is forecasted for Q1/2011 at 6.4%, bolstered mainly

by exports and investment (Table 3.1). Investment is predicted to accelerate further on

momentum from positive developments in infrastructure projects, appreciation in the rupiah,

regulatory improvements and performance of the capital market. Household consumption is

also forecasted to rise in keeping with strengthening purchasing power and buoyant levels

I t e m

Table 3.1

Economic Growth – Demand Side

* Bank Indonesia Projection

Private Consumption 4.9 3.9 5.0 5.2 4.4 4.6 4.8

Government Consumption 15.7 (-7.6) (-7.3) 4.8 7.3 0.3 5.4

Gross Fixed Capital Formation 3.3 8.0 8.0 9.2 8.7 8.5 9.2

Exports of Goods and Services -9.7 20.0 14.6 9.6 16.1 14.9 11.0

Imports of Goods and Services -15.0 22.6 18.4 12.2 16.9 17.3 10.9

GDP 4.6 5.6 6.1 5.8 6.9 6.1 6.4

20092010

I III III IV2010

2011*

%Y-o-Y, 2000 Price

Latest Macroeconomic and Monetary Developments

17

Monetary Policy Report - Quarter I-2011

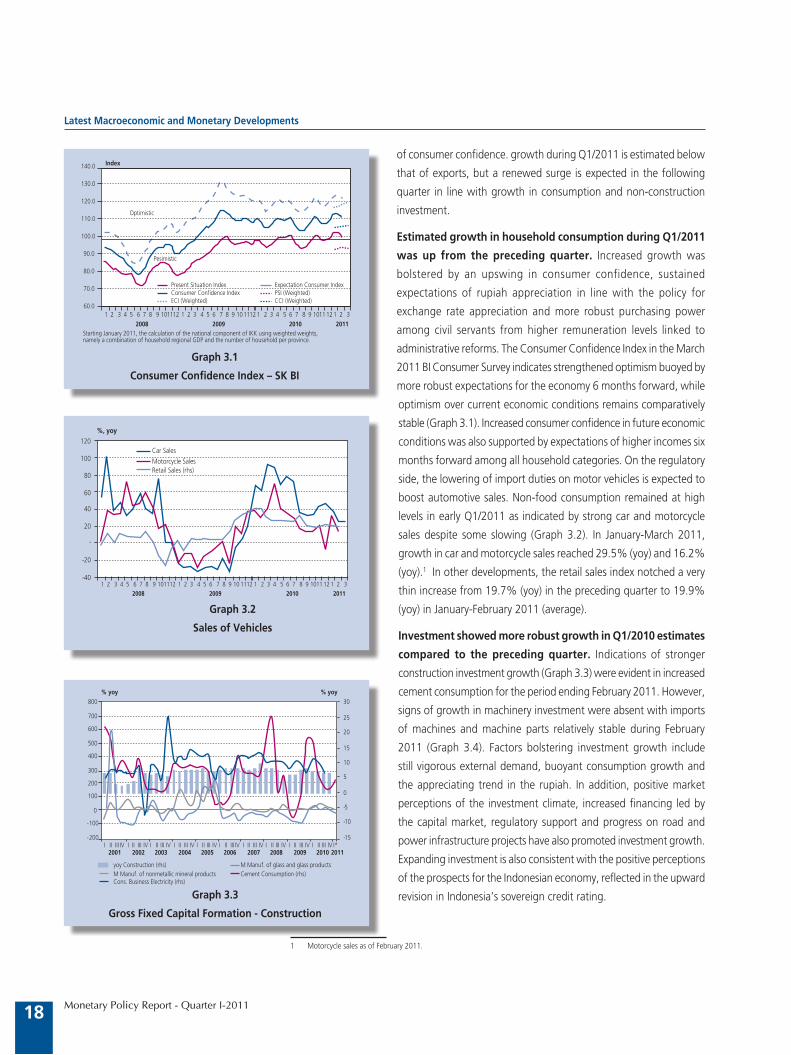

of consumer confidence. growth during Q1/2011 is estimated below

that of exports, but a renewed surge is expected in the following

quarter in line with growth in consumption and non-construction

investment.

Estimated growth in household consumption during Q1/2011

was up from the preceding quarter. Increased growth was

bolstered by an upswing in consumer confidence, sustained

expectations of rupiah appreciation in line with the policy for

exchange rate appreciation and more robust purchasing power

among civil servants from higher remuneration levels linked to

administrative reforms. The Consumer Confidence Index in the March

2011 BI Consumer Survey indicates strengthened optimism buoyed by

more robust expectations for the economy 6 months forward, while

optimism over current economic conditions remains comparatively

stable (Graph 3.1). Increased consumer confidence in future economic

conditions was also supported by expectations of higher incomes six

months forward among all household categories. On the regulatory

side, the lowering of import duties on motor vehicles is expected to

boost automotive sales. Non-food consumption remained at high

levels in early Q1/2011 as indicated by strong car and motorcycle

sales despite some slowing (Graph 3.2). In January-March 2011,

growth in car and motorcycle sales reached 29.5% (yoy) and 16.2%

(yoy).1 In other developments, the retail sales index notched a very

thin increase from 19.7% (yoy) in the preceding quarter to 19.9%

(yoy) in January-February 2011 (average).

Investment showed more robust growth in Q1/2010 estimates

compared to the preceding quarter. Indications of stronger

construction investment growth (Graph 3.3) were evident in increased

cement consumption for the period ending February 2011. However,

signs of growth in machinery investment were absent with imports

of machines and machine parts relatively stable during February

2011 (Graph 3.4). Factors bolstering investment growth include

still vigorous external demand, buoyant consumption growth and

the appreciating trend in the rupiah. In addition, positive market

perceptions of the investment climate, increased financing led by

the capital market, regulatory support and progress on road and

power infrastructure projects have also promoted investment growth.

Expanding investment is also consistent with the positive perceptions

of the prospects for the Indonesian economy, reflected in the upward

revision in Indonesia’s sovereign credit rating.

1 Motorcycle sales as of February 2011.

Graph 3.1

Consumer Confidence Index – SK BI

Graph 3.2

Sales of Vehicles

����

����

����

����

�����

�����

�����

�����

����� �����

����������������������� ��������������������������������������������������� ���������������������������� ��������������

����������

����������

� � � � � � � � � ������ � � � � � � � � � ������� � � � � � � � � ������� � ����� ���� ���� ����

���������������������������������������������������������������������������������������������������������������������������������������������������������������������������������������

� � � � � � � � � ������ � � � � � � � � � �� ���� � � � � � � � � � ���� �� � � ����� ���� ���� ����

���

���

��

��

��

��

�

���

���

�������������������������������������������

������

Graph 3.3

Gross Fixed Capital Formation - Construction

���

���

��

�

�

��

��

��

��

��

����

����

�

���

���

���

���

���

���

���

���

���������������������� ���������������������������������������������������������������������������� ��������������������������������������������������������

����� �����

� �� ��� �� � �� ��� �� � �� ��� �� � �� ��� �� � �� ��� �� � �� ��� �� � �� ��� �� � �� ��� �� � �� ��� �� � �� ��� �� ������ ���� ���� ���� ���� ���� ���� ���� ���� ���� ����

Latest Macroeconomic and Monetary Developments

18

Monetary Policy Report - Quarter I-2011

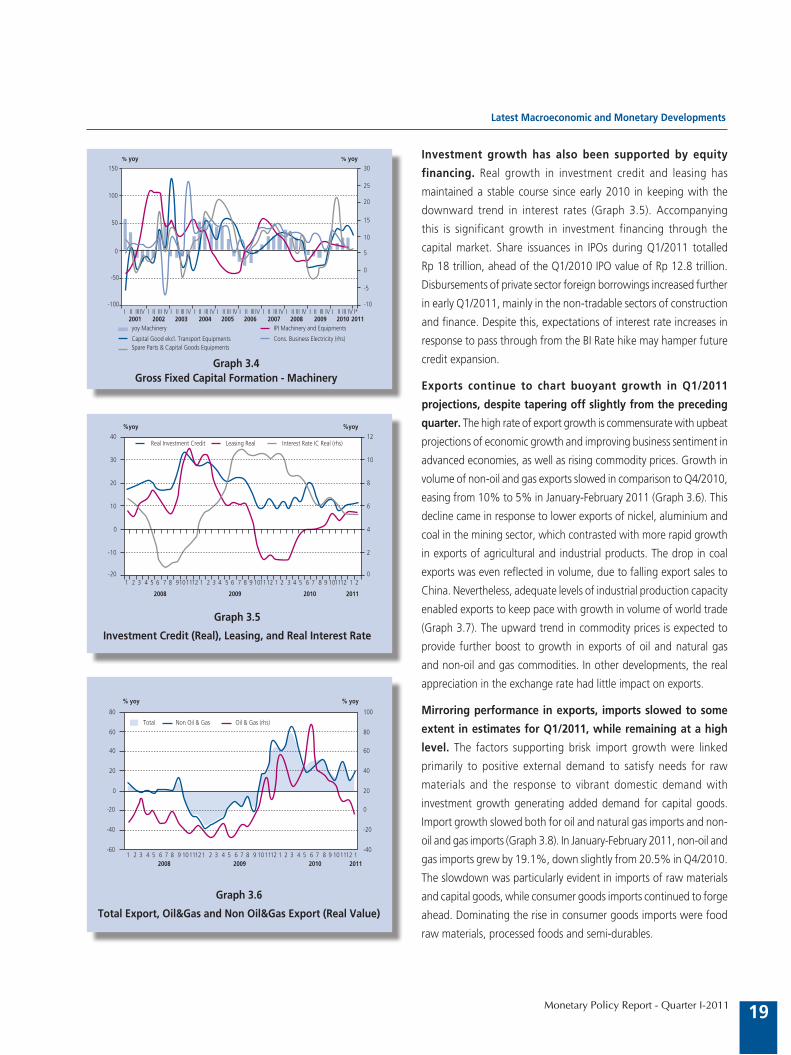

Graph 3.6

Total Export, Oil&Gas and Non Oil&Gas Export (Real Value)

Investment growth has also been supported by equity

financing. Real growth in investment credit and leasing has

maintained a stable course since early 2010 in keeping with the

downward trend in interest rates (Graph 3.5). Accompanying

this is significant growth in investment financing through the

capital market. Share issuances in IPOs during Q1/2011 totalled

Rp 18 trillion, ahead of the Q1/2010 IPO value of Rp 12.8 trillion.

Disbursements of private sector foreign borrowings increased further

in early Q1/2011, mainly in the non-tradable sectors of construction

and finance. Despite this, expectations of interest rate increases in

response to pass through from the BI Rate hike may hamper future

credit expansion.

Exports continue to chart buoyant growth in Q1/2011

projections, despite tapering off slightly from the preceding

quarter. The high rate of export growth is commensurate with upbeat

projections of economic growth and improving business sentiment in

advanced economies, as well as rising commodity prices. Growth in

volume of non-oil and gas exports slowed in comparison to Q4/2010,

easing from 10% to 5% in January-February 2011 (Graph 3.6). This