jkh-1hfy15 earnings note - sell - 07nov2014.pdf

TRANSCRIPT

8/10/2019 JKH-1HFY15 Earnings Note - SELL - 07Nov2014.pdf

http://slidepdf.com/reader/full/jkh-1hfy15-earnings-note-sell-07nov2014pdf 1/6

1

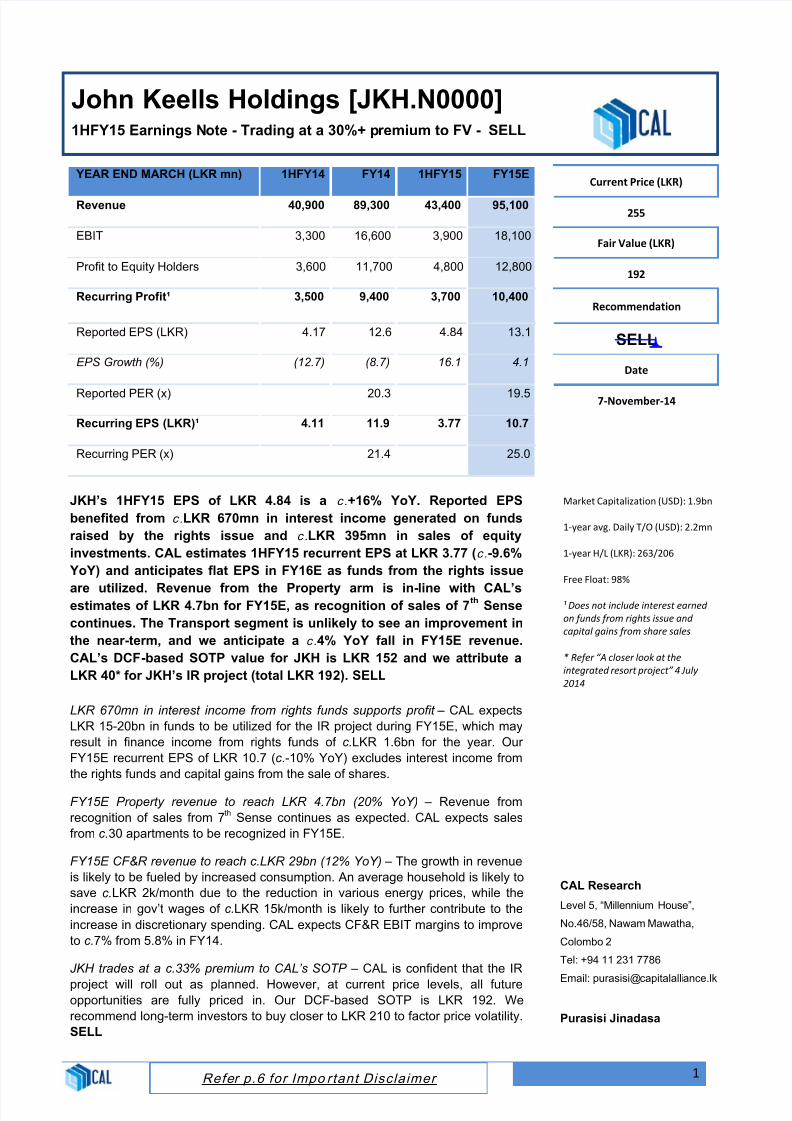

John Keells Holdings [JKH.N0000]1HFY15 Earnings Note - Trading at a 30%+ premium to FV - SELL

YEAR END MARCH (LKR mn) 1HFY14 FY14 1HFY15 FY15ECurrent Price (LKR)

Revenue 40,900 89,300 43,400 95,100255

EBIT 3,300 16,600 3,900 18,100Fair Value (LKR)

Profit to Equity Holders 3,600 11,700 4,800 12,800192

Recurring Profit¹ 3,500 9,400 3,700 10,400Recommendation

Reported EPS (LKR) 4.17 12.6 4.84 13.1SELL

EPS Growth (%) (12.7) (8.7) 16.1 4.1Date

Reported PER (x) 20.3 19.5 7-November-14

Recurring EPS (LKR)¹ 4.11 11.9 3.77 10.7

Recurring PER (x) 21.4 25.0

JKH’s 1HFY15 EPS of LKR 4.84 is a c .+16% YoY. Reported EPS

benefited from c .LKR 670mn in interest income generated on funds

raised by the rights issue and c .LKR 395mn in sales of equity

investments. CAL estimates 1HFY15 recurrent EPS at LKR 3.77 (c .-9.6%

YoY) and anticipates flat EPS in FY16E as funds from the rights issue

are utilized. Revenue from the Property arm is in-line with CAL’sestimates of LKR 4.7bn for FY15E, as recognition of sales of 7

th Sense

continues. The Transport segment is unlikely to see an improvement in

the near-term, and we anticipate a c .4% YoY fall in FY15E revenue.

CAL’s DCF-based SOTP value for JKH is LKR 152 and we attribute a

LKR 40* for JKH’s IR project (total LKR 192). SELL

LKR 670mn in interest income from rights funds supports profit – CAL expects

LKR 15-20bn in funds to be utilized for the IR project during FY15E, which may

result in finance income from rights funds of c.LKR 1.6bn for the year. Our

FY15E recurrent EPS of LKR 10.7 (c .-10% YoY) excludes interest income from

the rights funds and capital gains from the sale of shares.

FY15E Property revenue to reach LKR 4.7bn (20% YoY) – Revenue from

recognition of sales from 7th Sense continues as expected. CAL expects sales

from c.30 apartments to be recognized in FY15E.

FY15E CF&R revenue to reach c.LKR 29bn (12% YoY) – The growth in revenue

is likely to be fueled by increased consumption. An average household is likely to

save c.LKR 2k/month due to the reduction in various energy prices, while the

increase in gov’t wages of c.LKR 15k/month is likely to further contribute to the

increase in discretionary spending. CAL expects CF&R EBIT margins to improve

to c.7% from 5.8% in FY14.

JKH trades at a c.33% premium to CAL’s SOTP – CAL is confident that the IR

project will roll out as planned. However, at current price levels, all futureopportunities are fully priced in. Our DCF-based SOTP is LKR 192. We

recommend long-term investors to buy closer to LKR 210 to factor price volatility.

SELL

Refer p.6 for Impo rtant Disclaimer

CAL Research

Level 5, “Millennium House”,

No.46/58, Nawam Mawatha,

Colombo 2

Tel: +94 11 231 7786

Email: [email protected]

Purasisi Jinadasa

Market Capitalization (USD): 1.9bn

1-year avg. Daily T/O (USD): 2.2mn

1-year H/L (LKR): 263/206

Free Float: 98%

¹ Does not include interest earned

on funds from rights issue and

capital gains from share sales

* Refer “A closer look at the

integrated resort project” 4 July

2014

8/10/2019 JKH-1HFY15 Earnings Note - SELL - 07Nov2014.pdf

http://slidepdf.com/reader/full/jkh-1hfy15-earnings-note-sell-07nov2014pdf 2/6

2

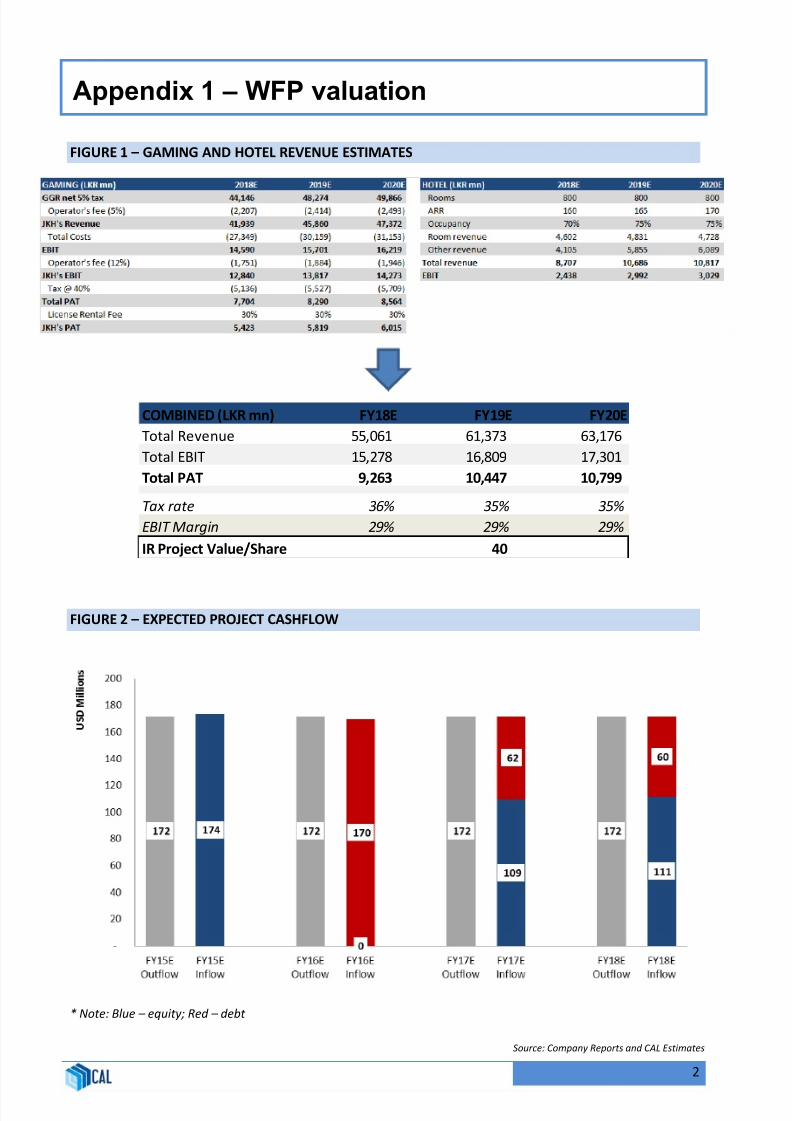

FIGURE 1 – GAMING AND HOTEL REVENUE ESTIMATES

FIGURE 2 – EXPECTED PROJECT CASHFLOW

* Note: Blue – equity; Red – debt

COMBINED (LKR mn) FY18E FY19E FY20E

Total Revenue 55,061 61,373 63,176

Total EBIT 15,278 16,809 17,301

Total PAT 9,263 10,447 10,799

Tax rate 36% 35% 35%

EBIT Margin 29% 29% 29%

IR Project Value/Share 40

Appendix 1 – WFP valuation

Source: Company Reports and CAL Estimates

8/10/2019 JKH-1HFY15 Earnings Note - SELL - 07Nov2014.pdf

http://slidepdf.com/reader/full/jkh-1hfy15-earnings-note-sell-07nov2014pdf 3/6

3

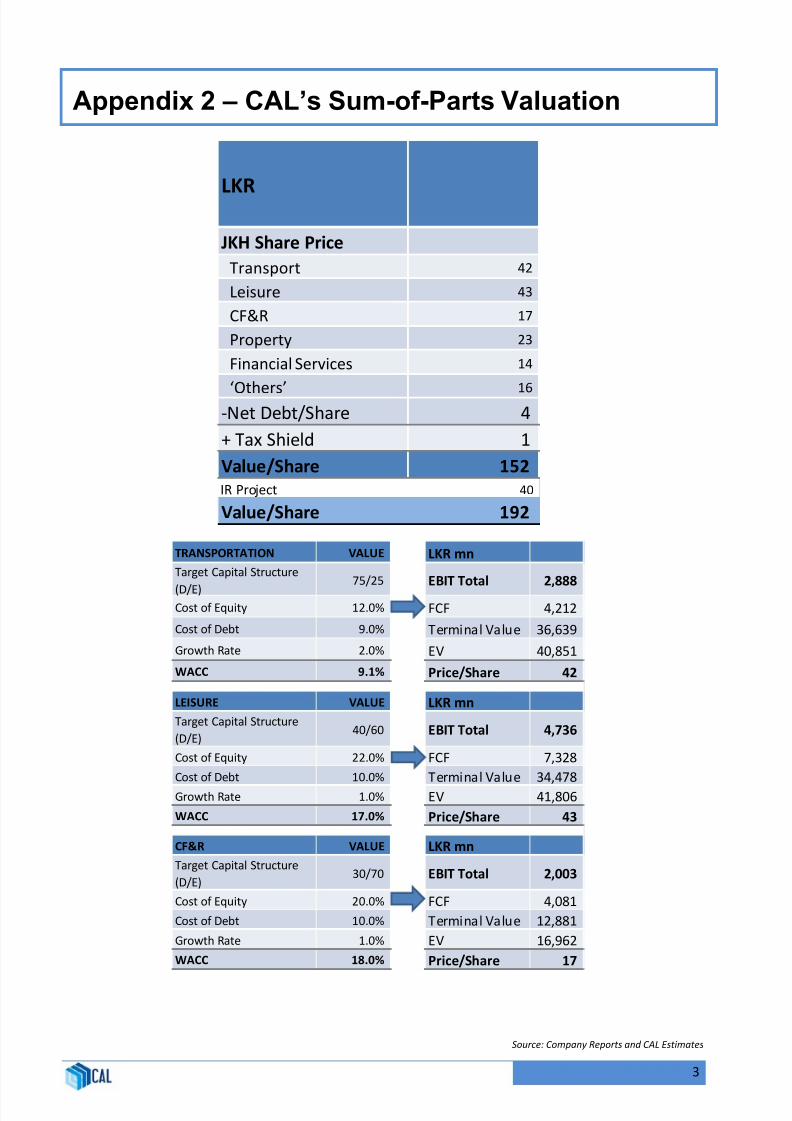

LKR

JKH Share Price

Transport 42

Leisure 43

CF&R 17

Property 23

Financial Services 14

‘Others’ 16 -Net Debt/Share 4

+ Tax Shield 1

Value/Share 152

IR Project 40

Value/Share 192

TRANSPORTATION VALUE LKR mn

Target Capital Structure

(D/E)75/25 EBIT Total 2,888

Cost of Equity 12.0% FCF 4,212

Cost of Debt 9.0% Terminal Value 36,639

Growth Rate 2.0% EV 40,851

WACC 9.1% Price/Share 42

LEISURE VALUE LKR mn

Target Capital Structure

(D/E)40/60 EBIT Total 4,736

Cost of Equity 22.0% FCF 7,328

Cost of Debt 10.0% Terminal Value 34,478

Growth Rate 1.0% EV 41,806

WACC 17.0% Price/Share 43

CF&R VALUE LKR mn

Target Capital Structure

(D/E)30/70 EBIT Total 2,003

Cost of Equity 20.0% FCF 4,081

Cost of Debt 10.0% Terminal Value 12,881

Growth Rate 1.0% EV 16,962

WACC 18.0% Price/Share 17

Appendix 2 – CAL’s Sum-of-Parts Valuation

Source: Company Reports and CAL Estimates

8/10/2019 JKH-1HFY15 Earnings Note - SELL - 07Nov2014.pdf

http://slidepdf.com/reader/full/jkh-1hfy15-earnings-note-sell-07nov2014pdf 4/6

4

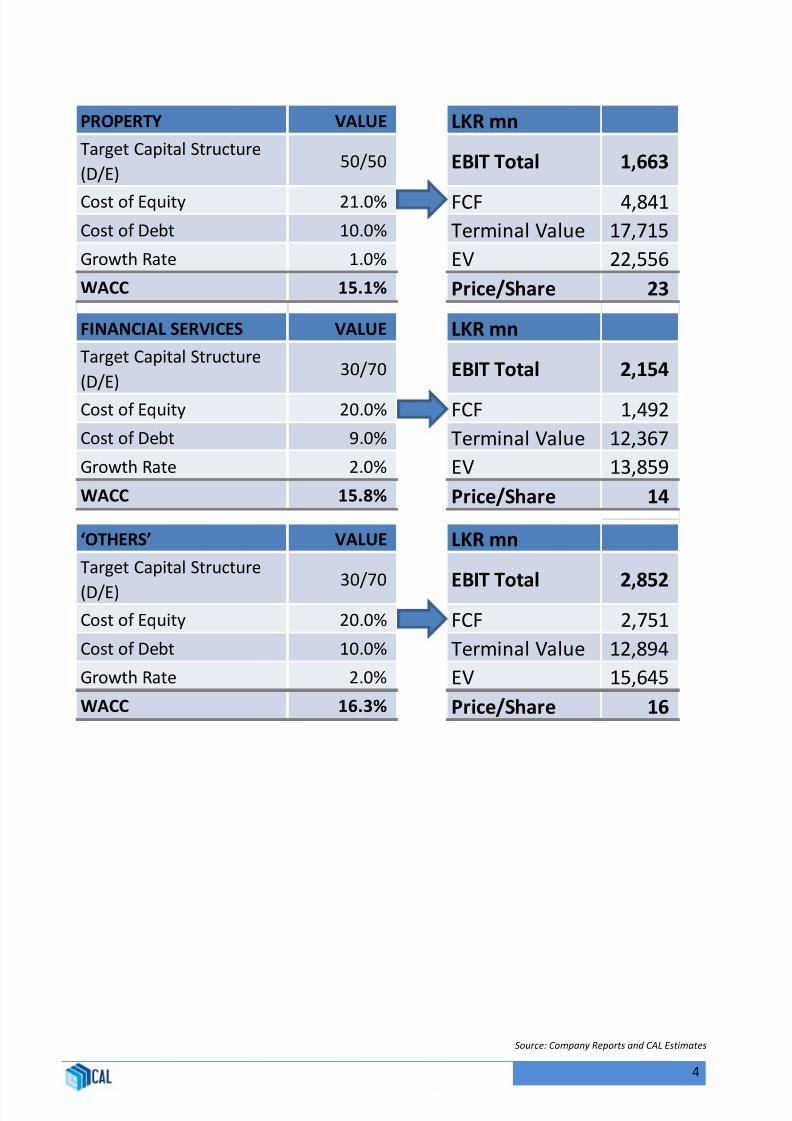

PROPERTY VALUE LKR mn

Target Capital Structure

(D/E)50/50 EBIT Total 1,663

Cost of Equity 21.0% FCF 4,841

Cost of Debt 10.0% Terminal Value 17,715

Growth Rate 1.0% EV 22,556

WACC 15.1% Price/Share 23

FINANCIAL SERVICES VALUE LKR mn

Target Capital Structure

(D/E)30/70 EBIT Total 2,154

Cost of Equity 20.0% FCF 1,492

Cost of Debt 9.0% Terminal Value 12,367

Growth Rate 2.0% EV 13,859

WACC 15.8% Price/Share 14

‘OTHERS’ VALUE LKR mn

Target Capital Structure

(D/E)30/70

EBIT Total 2,852Cost of Equity 20.0% FCF 2,751

Cost of Debt 10.0% Terminal Value 12,894

Growth Rate 2.0% EV 15,645

WACC 16.3% Price/Share 16

Source: Company Reports and CAL Estimates

8/10/2019 JKH-1HFY15 Earnings Note - SELL - 07Nov2014.pdf

http://slidepdf.com/reader/full/jkh-1hfy15-earnings-note-sell-07nov2014pdf 5/6

5

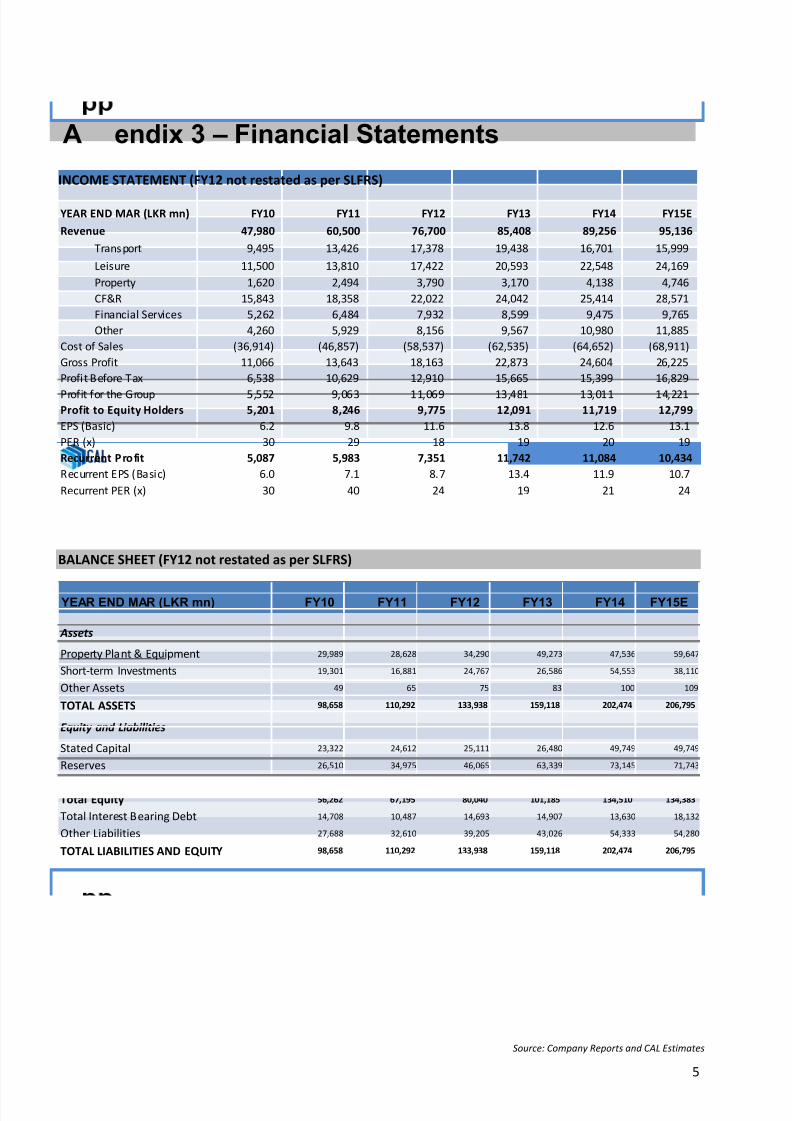

INCOME STATEMENT (FY12 not restated as per SLFRS)

BALANCE SHEET (FY12 not restated as per SLFRS)

YEAR END MAR (LKR mn) FY10 FY11 FY12 FY13 FY14 FY15E

Revenue 47,980 60,500 76,700 85,408 89,256 95,136

Transport 9,495 13,426 17,378 19,438 16,701 15,999

Leisure 11,500 13,810 17,422 20,593 22,548 24,169

Property 1,620 2,494 3,790 3,170 4,138 4,746

CF&R 15,843 18,358 22,022 24,042 25,414 28,571

Financial Services 5,262 6,484 7,932 8,599 9,475 9,765

Other 4,260 5,929 8,156 9,567 10,980 11,885

Cost of Sales (36,914) (46,857) (58,537) (62,535) (64,652) (68,911)

Gross Profit 11,066 13,643 18,163 22,873 24,604 26,225

Profit Before Tax 6,538 10,629 12,910 15,665 15,399 16,829

Profit for the Group 5,552 9,063 11,069 13,481 13,011 14,221Profit to Equity Holders 5,201 8,246 9,775 12,091 11,719 12,799

EPS (Basic) 6.2 9.8 11.6 13.8 12.6 13.1

PER (x) 30 29 18 19 20 19

Recurrent Profit 5,087 5,983 7,351 11,742 11,084 10,434

Recurrent EPS (Basic) 6.0 7.1 8.7 13.4 11.9 10.7

Recurrent PER (x) 30 40 24 19 21 24

YEAR END MAR (LKR mn) FY10 FY11 FY12 FY13 FY14 FY15E

Assets

Property Plant & Equipment 29,989 28,628 34,290 49,273 47,536 59,647

Short-term Investments 19,301 16,881 24,767 26,586 54,553 38,110

Other Assets 49 65 75 83 100 109

TOTAL ASSETS 98,658 110,292 133,938 159,118 202,474 206,795

Equity and Liabilities

Stated Capital 23,322 24,612 25,111 26,480 49,749 49,749

Reserves 26,510 34,975 46,065 63,339 73,145 71,743

Minority Interest 6,430 7,608 8,865 11,366 11,616 12,891

Total Equity 56,262 67,195 80,040 101,185 134,510 134,383

Total Interest Bearing Debt 14,708 10,487 14,693 14,907 13,630 18,132

Other Liabilities 27,688 32,610 39,205 43,026 54,333 54,280

TOTAL LIABILITIES AND EQUITY 98,658 110,292 133,938 159,118 202,474 206,795

A endix 3 – Financial Statements

Source: Company Reports and CAL Estimates

8/10/2019 JKH-1HFY15 Earnings Note - SELL - 07Nov2014.pdf

http://slidepdf.com/reader/full/jkh-1hfy15-earnings-note-sell-07nov2014pdf 6/6

6

Research TeamTel No: +94 11 231 7777 (General)

E-mail: [email protected]

Head of ResearchPurasisi Jinadasa Udeeshan JonasTel No: +94 11 231 7786 Tel No: +94 11 231 7746E-mail: [email protected] E-mail: [email protected]

Thushani de Silva Christeen SilvaTel No: +94 11 231 7777 (Ext: 7815) E-mail: [email protected]: [email protected]

Teresh AmaratungaE-mail: [email protected]

This document has been prepared and issued on the basis of publicly available information, internallydeveloped data and other sources, believed to be reliable. Capital Alliance Securities (Private) Limitedhowever does not warrant its completeness or accuracy. Opinions and estimates given constitute a judgment as of the date of the material and are subject to change without notice. This report is not intendedas an offer or solicitation for the purchase or sale of any financial instrument. The recipient of this reportmust make their own independent decision regarding any securities, investments or financial instrumentsmentioned herein. Securities or financial instruments mentioned may not be suitable to all investors. Capital Alliance Securities (Private) Limited it’s directors, officers, consultants, employees, outsourced research providers associates or business partner, will not be responsible, for any claims damages, compensation,

suits, damages, loss, costs, charges, expenses, outgoing or payments including attorney’s fees whichrecipients of the reports suffers or incurs directly or indirectly arising out actions taken as a result of thisreport. This report is for the use of the intended recipient only. Access, disclosure, copying, distribution orreliance on any of it by anyone else is prohibited and may be a criminal offence.

Definition of rating distribution for long-term investment opportunities

CAL Research uses the following rating system:

STRONG BUY Strong upside. Total return (incl. dividends) is expected to be above 20%within the next 12 months.

BUY Good upside. Total return (incl. dividends) is expected to be between 15% to

20% within the next 12 months.

HOLD For existing shareholders. Total return (incl. dividends) is expected to bebetween 5% to 15% within the next 12 months.

SELL Strong downside. Total return (incl. dividends) is expected to be below 5%within the next 12 months.

Disclaimer

Contacts