issue 2, february 2012 technology spotlight a few bytes ... · technology spotlight a few bytes...

TRANSCRIPT

Technology SpotlightA Few Bytes Away From Downloading the Converged Revenue Recognition Standard!

The Bottom Line

Issue 2, February 2012

In This Issue:• Background• KeyAccountingIssues• ChallengesforTechnology

Companies• ThinkingAhead• Appendix—KeyDifferences

BetweenASC985-605andtheFASB’sandIASB’sRevisedED

• OnNovember14,2011,theFASBandIASB(the“boards”)jointlyissuedtheirrevisedexposuredraft(ED)RevenueFromContractsWithCustomers.TherevisedEDproposesasinglecomprehensivemodelforentitiestouseinaccountingforrevenuearisingfromcontractswithcustomersandwouldsupersedemostcurrentrevenuerecognitionguidance.Inaddition,onJanuary4,2012,theFASBissuedacompanionproposedASUforpubliccommentthatwouldcodifytherevisedED’samendments.

• TherevisedEDwouldsupersedeASC985-6051(formerlySOP97-22)initsentirety.Theeliminationoftherequirementforvendor-specificobjectiveevidence(VSOE)offairvaluemaysignificantlymodifythetimingofrevenuerecognitionforsoftwareentities.

• Warrantiesthatprovideaserviceinadditiontosimpleassurancethataproductcomplieswithagreed-uponspecificationsmustbetreatedasseparateperformanceobligations,therebypotentiallydelayingtherecognitionofaportionofrevenueuntiltheobligationsaresatisfied.

• UndertherevisedED,thedeterminationofwhethervirtualgoodsandservicesaretransferredatapointintimeoroveraperiodoftimemaysignificantlyaffectrevenuerecognition.

• CommentsontherevisedEDandtheFASBcompanionproposedASUareduebyMarch13,2012.Afinalrevenuerecognitionstandardisnotexpectedtobeissueduntillaterin2012andwouldnotbeeffectiveearlierthanforannualperiodsbeginningonorafterJanuary1,2015.

The proposed revenue model requires management to use greater judgment in recognizing revenue and related costs and may change the timing of revenue recognition from current practice.

1 FortitlesofFASBAccountingStandardsCodification(ASC)references,seeDeloitte’s“TitlesofTopicsandSubtopicsinthe

FASBAccountingStandardsCodification.”2 AICPAStatementofPosition97-2,SoftwareRevenueRecognition.

2

ThisTechnologySpotlighthighlightstheframeworkoftheproposedrevenuerecognitionmodelandthepotentialimplicationsfortechnologycompanies.

BackgroundTherevisedEDstatesthatthegoaloftheboards’revenuerecognitionproject,whichbeganin2002,isto“clarifytheprinciplesforrecognizingrevenueandtodevelopacommonrevenuestandardforU.S.GAAPandIFRSs.”Afterreceivingnearly1,000commentlettersandredeliberatingalmosteveryaspectoftheirJune2010ED,theboardsmodifiedtheproposedguidanceanddevelopedtherevisedED(changesfromtheJune2010EDarediscussedindetailinDeloitte’sNovember15,2011,HeadsUp).TherevisedEDretainedtheoverallmodelthatwasoriginallyproposed,whichoutlinedfivesequentialstepstorecognizingrevenue:

1. “Identifythecontractwithacustomer.”

2. “Identifytheseparateperformanceobligationsinthecontract.”

3. “Determinethetransactionprice.”

4. “Allocatethetransactionpricetotheseparateperformanceobligationsinthecontract.”

5. “Recognizerevenuewhen(oras)theentitysatisfiesaperformanceobligation.”

TherevisedEDstatesthatthecoreprincipleforrevenuerecognitionisthatan“entityshallrecognizerevenuetodepictthetransferofpromisedgoodsorservicestocustomersinanamountthatreflectstheconsiderationtowhichtheentityexpectstobeentitledinexchangeforthosegoodsorservices.”Althoughtheboardsdidnotmodifythefivestepstoapplyingthisprinciple,theydidchangehoweachstepisappliedaswellasotheraspectsoftheproposedmodel.Forinstance,theproposalwouldrequirecapitalizationofcertaincostsofobtainingandfulfillingacontractandwouldmodifythecriteriaforrecognizinglossesoncertainonerousperformanceobligations.

Comparedwithcurrentrevenuerecognitionguidance,therevisedEDrequiressignificantlyexpandeddisclosuresaboutrevenuerecognition,includingbothquantitativeandqualitativeinformationabout(1)theamount,timing,anduncertaintyofrevenue(andrelatedcashflows)fromcontractswithcustomers;(2)thejudgment,andchangesinjudgment,exercisedinapplyingtheproposal’sprovisions;and(3)assetsrecognizedfromcoststoobtainorfulfillacontractwithacustomer.

Key Accounting IssuesTherevisedEDclarifiestherevenuerecognitionprinciplesandincludesadditionalguidanceoncertainrevenuetransactions.Althoughtheeffectoftheproposalsonsomeentitiesisexpectedtobelimited,hardwareandsoftwareentitiesoperatinginthetechnologyindustrymayfacesignificantaccountingandoperationalchallengesasaresultoftherevisedED,anumberofwhicharediscussedbelow.

SoftwareTherevisedEDeliminatesindustry-specificsoftwareguidance,requiringthatentitiesinallindustries,includingthesoftwareindustry,applya“one-size-fits-all”model.UndertherevisedED,goodsandservicesinasoftwarecontractaretreatedasseparateperformanceobligationsiftheyaredeemed“distinct.”TherevisedEDcontainscriteriafordeterminingwhethergoodsorservicesrepresentdistinctperformanceobligationsthatshouldbeaccountedforseparately.Revenueisallocatedtoeachseparateperformanceobligationonthebasisofitsrelativestand-alonesellingprice.Ifthestand-alonesellingpriceofaperformanceobligationisnotobservable,theentitymustuseoneofthemethods

The proposed model requires technology entities to reassess their accounting for various software and hardware products and services and determine whether accounting changes are necessary.

Beyond the Bottom Line

3

describedintherevisedEDtoestimateit.Revenueisthenrecognizedforeachseparateperformanceobligationastheobligationissatisfied(eitherovertimeoratapointintime),uptotheamounttowhichanentityisreasonablyassuredtobeentitled.

Softwarecompaniesmaybemostsignificantlyaffectedby(1)theeliminationoftherequirementthatVSOEoffairvaluemustexistforanentitytoseparateelementsinasoftwarearrangementand(2)thechangeinscopeoftheapplicationoftheresidualmethodforallocatingtheconsiderationtoeachelement.Theparagraphsbelowdiscusstheseitemsandafewotherdifferences.AlsoseetheappendixforadetailedcomparisonbetweenASC985-605(formerlySOP97-2)andtherevisedED.

Elimination of VSOE RequirementCurrently,ASC985-605providesindustry-specificguidanceonaccountingformultiple-elementsoftwarearrangements.Underthecurrentguidance,toseparateasoftwarearrangementthatincludesmultipleelements,avendormustestablishVSOEoffairvalue,whichASC985-605-25-6definesas:

a. Thepricechargedwhenthesameelementissoldseparately

b. Foranelementnotyetbeingsoldseparately,thepriceestablishedbymanagementhavingtherelevantauthority;itmustbeprobablethattheprice,onceestablished,willnotchangebeforetheseparateintroductionoftheelementintothemarketplace.

Theseparate-salecriterionforestablishingfairvalueismorerestrictivethanthatinanyexistingliteraturethatappliestomultiple-elementarrangements.WhetherVSOEoffairvaluecanbeestablishedforanelementmaydramaticallyaffecthowrevenueisrecognizedinamultiple-elementarrangement.Further,variationsinpricingfromcustomertocustomer,theuniqueandcustomer-specificnatureofmanysoftwareelements,andthelackofhistoricalsalesinformationfornewsoftwareproductscanoftenmakeitdifficultorimpossibletoestablishVSOEoffairvalue.

BecausetherevisedEDiseliminatingtheVSOErequirement,revenuerecognitioninsoftwarecontractswillnolongerbelimitedifVSOEoffairvalueisnotestablishedforcertaingoodsorservicesinacontract.However,whileentitieswillnolongerberequiredtoestablishandmaintainprocessesfordevelopingVSOEoffairvalueforgoodsorservicessoldinsoftwaretransactions,therevisedEDwillstillrequireentitiestodevelopsimilarprocessesfordeterminingthestand-alonesellingpriceofeachperformanceobligation.

EliminationoftheVSOErequirementmayhaveasignificantimpactonsoftwaretransactionsthatincludetechnology“roadmaps.”Mostsoftwarecompaniesdeveloproadmapstoarticulatebothshort-termandlong-termgoalsforthefuturedevelopmentofsoftwaresoldtoacustomer.Roadmapscanincludespecificupgradesorenhancementstothefunctionalityofsoftwaretobedeliveredataspecifictimeinthefuture.Becausesuchupgradesorenhancementstypicallyhavenotbeendevelopedorsoldseparatelyatcontractinception,VSOEoffairvalueoftendoesnotexistforsuchelements.Asdescribedabove,undercurrentguidance,ifaroadmapimpliesorexplicitlypromisesthedeliveryofspecifiedupgradesandVSOEoffairvaluedoesnotexistfortheupgraderights,revenuerelatedtootherelementsinthearrangementoftenmustbedeferreduntiltheupgradesaredeliveredorVSOEoffairvalueisestablished.Thislimitstheabilityofsoftwarecompaniestoincludedesiredcontentintheirproductroadmaps.ByreplacingtheseparationrequirementforVSOEoffairvaluewiththeconcept“distinct”goodsorservicesandrequiringallocationofrevenuetoseparateperformanceobligationsonthebasisofanestimateofstand-alonesellingprices,therevisedEDgivessoftwarecompaniesmoreflexibilitytoincludespecifiedupgraderightsintheirproductroadmaps.Inotherwords,revenuerecognitionincertainsoftwarearrangementsmaybeacceleratedasaresultoftherevisedED.

The elimination of VSOE and the allocation of revenue to each performance obligation on the basis of stand-alone selling prices may significantly change revenue recognition patterns in software arrangements.

4

Residual Allocation TechniquesMultiple-elementsoftwarearrangementsthatarenotwithinthescopeofASC985-605(e.g.,certaintypesofhostedsoftwareanddataarrangements)aretypicallyaccountedforunderASC605-25,whichdiscusseshowanentityshouldallocatethearrangementconsiderationtoseparateunitsofaccounting.Entitiesarerequired,attheinceptionofanarrangement,toestablishthe“sellingprice”foralldeliverablesthatqualifyforseparation.Themannerinwhich“sellingprice”isestablishedisbasedonahierarchyofevidencethatentitiesmustconsider;totalarrangementconsiderationisallocatedonthebasisofthedeliverables’relativesellingprices.The“residualmethod,”asdescribedinASC985-605,iscurrentlyprohibitedformultiple-elementarrangementsthatarewithinthescopeofASC605-25.

Intheabsenceofobservableseparatesales,therevisedEDrequiresentitiestouseestimatestodeterminethestand-alonesellingpriceofaseparateperformanceobligation.AlthoughtherevisedEDincludesthreeexamplesofsuitableestimationmethods,itdoesnotprescribeone.Instead,anentitywouldusejudgmentindetermininganestimationmethodthatmaximizestheuseofobservableinputs.TherevisedEDspecifiesthatwhenthestand-alonesellingpriceofaperformanceobligationishighlyvariableoruncertain,theapplicationofaresidualtechniquemaybeusedasanestimationmethod,regardlessofthetypeofgoodorservicebeingsold.

UndertherevisedED,anentityispermittedtoapplyaresidualallocationtechniqueinthecircumstancesdescribedaboveregardlessofwhethertheentityobtainsVSOEoffairvalueforallotherperformanceobligationsinthearrangement(asrequiredforarrangementsthatarecurrentlywithinthescopeofASC985-605).Thus,anentitymightnolongerneedtoperformorjustifycomplexestimationtechniquestodeterminetheestimateofstand-alonesellingpriceforhighlyuniquegoodsorservicesinmultiple-deliverablearrangements(forarrangementscurrentlywithinthescopeofASC605-25).Lastly,entitiesmaybeallowedgreaterflexibilityinallocatingrevenuetoperformanceobligations,dependingonthefactsandcircumstances.

Overall,entitiesthatcurrentlyfinditchallengingtomeettherequirementforVSOEoffairvaluewillmostlikelyhaveincreasedflexibilitytouseestimatestodemonstratestand-alonesellingpricesandwillthusbelesslikelytodeferrevenuewhenVSOEoffairvaluedoesnotexist.

Online Gaming / New Media

Sale of Virtual GoodsTraditionally,onlinegamingandnewmediacompanieshavechargedcustomersamonthlysubscriptionfeeorafeeforpremiumservicestogainaccesstoonlinecontentforaspecifiedperiod.Recently,the“free-to-play”businessmodelhasbecomemorepopularintheonlineindustry.Underthefree-to-playmodel,customersaregivenaccesstoonlinecontentfornochargebuthavetheoptiontopurchasevirtualgoods.Virtualgoodsareintangibleobjectspurchasedforuseinonlineplatforms(e.g.,virtualpets,avatars).

TherevisedEDspecifiesthatrevenueshouldberecognizedwhentheentitysatisfiesaperformanceobligationbytransferringagoodorservicetoacustomerandtheentityisreasonablyassuredtobeentitledtosuchrevenue.Agoodorserviceisdeemedtobetransferredwhenthecustomerobtainscontrolofthatgoodorservice,whichmaybeovertime(whencertaincriteriaaremet)oratapointintime.

The use of the residual technique may be permitted when the stand-alone selling price of a performance obligation is highly variably or uncertain.

5

Acustomergenerallycanexpectapurchasedvirtualgoodtobeavailableforuseatanytime.However,somecontractsspecifythemannerinwhichthecustomermayconsumethegood.Incertainsituations,controlofthevirtualgoodmaybetransferredtothecustomerinitsentiretyatthepointofsalesothatthecustomermayuseorconsumethevirtualgoodwithoutanyfurtherobligationonthepartofthesellertoprovideaccesstoit.Inthiscase,therevisedEDwouldmostlikelyrequirefullrevenuerecognitionforthesaleofthegoodatthepointofsaleiftheentityisreasonablyassuredtobeentitledtosuchrevenue.Incontrast,incertaincircumstances,acustomercouldberequiredtouseaseller’sonlineplatformorothermechanism,inwhichcasethesellerwouldbeobligatedtoprovidefurtherservicessothatthecustomercanuseorconsumethevirtualgood.Inthiscase,therevisedEDwouldmostlikelyrequirerevenuerecognitionasaccesstothevirtualgoodisprovidedanditsbenefitsareconsumedbythecustomer.

Giventhenumberofuniquearrangementsinthisindustry,onlinegamingandnewmediacompanieswillneedtoconsiderwhethertheircurrentrevenuerecognitionpracticesregardingthesaleofvirtualgoodsremainconsistentwiththerevisedED.

BreakageTherevisedED’sguidanceonbreakagemayaffecttheaccountingforrevenuerelatedtomicro-transactionsinthenewmediaandgamingindustries.“Micro-transactions”occurwhencustomerspurchasevirtualcurrencytoplaygames,purchasevirtualgoods,orpayforupgrades.“Breakage”referstotheamountofvirtualcurrencypurchasedbyacustomerthatwillneverbespent(i.e.,thevirtualcurrencyisneverredeemed).Incurrentpractice,amountsrelatedtobreakageoftenremainclassifiedasdeferredrevenueonthebalancesheetuntilitbecomeslikelythatthevirtualcurrencywillnotberedeemed.

TherevisedEDcontainsspecificimplementationguidanceonaccountingforacustomer’sunexercisedrights(i.e.,breakage).UndertherevisedED,whenanentityisreasonablyassuredofthebreakageamount,suchrevenueisrecognizedinproportiontothepatternofrightsexercisedbythecustomer.Iftheentityisnotreasonablyassuredofthebreakageamount,suchrevenuewouldbedeferreduntilthelikelihoodthatthecustomerwillredeemthevirtualcurrencyisremote.

TherevisedEDcouldmodifyrevenuerecognitionrelatedtobreakageformicro-transactions.Inparticular,therevenuerecognitionrelatedtomicro-transactionsmaybeaccelerated,providedthatentitieshavesufficienthistoricalinformationtoestimatethetimingandamountofbreakagesothattheycandeterminethattheyarereasonablyassuredofthebreakageamount.

HardwareCurrently,ASC605-20-25-1through25-6(formerlyFASBTechnicalBulletin90-13)provideguidanceonaccountingforanextendedwarrantythatispricedandsoldseparatelyfromthepurchasedproduct.Underthisguidance,theinvoicedamountthatispaidbyacustomerforaseparatelypricedwarrantyormaintenancecontractshouldberecognizedasrevenueonastraight-linebasisorinproportiontothecostsexpectedtobeincurredinperformingservicesoverthecontractterm.

UndertherevisedED,warrantieswouldbeaccountedforasfollows:

• Ifacustomerhastheoptiontopurchaseawarrantyseparatelyfromtheentity,theentitywouldaccountforthewarrantyasaseparateperformanceobligationandallocateaportionoftheoverallconsiderationtothewarrantyservice.

Entities that sell virtual goods and services may need to reconsider whether control of such goods or services is transferred at the point of sale or over a period of time.

3 FASBTechnicalBulletinNo.90-1,AccountingforSeparatelyPricedExtendedWarrantyandProductMaintenanceContracts.

6

• Ifacustomerdoesnothavetheoptiontopurchasethewarrantyseparatelyfromtheentity,theentitywoulduseacostaccrualmodeltoaccountforthewarranty,unlessthewarrantyprovidesaservicetothecustomerinadditiontoassurancethattheproductcomplieswithagreed-uponspecifications(inwhichcasetheentitywouldaccountfortheserviceasaseparateperformanceobligationandrevenuewouldbedeferred).

Hardwareentitiestypicallyprovidearangeofwarrantiesonsalesofproductstocustomers.UndertherevisedED,theaccountingformostwarranties(i.e.,generalwarrantiesthatareincludedaspartofthepurchaseofaparticularproductandthatassurethatthegoodorservicecomplieswithagreed-uponspecifications)underacostaccrualmodelwillnotchange.However,hardwareentitiesmaywishtoreassessalltheirwarrantiestoensurethattherearenoinstancesinwhichwarrantiesprovideanyservicesbeyondassuringthattheproductcomplieswithagreed-uponspecifications.

Hardwareentitieswillneedtoevaluatetheiraccountingforwarrantiesthatprovidemorethanassurancethataproductcomplieswiththeagreed-uponspecificationstodeterminewhetheraseparateperformanceobligationisembeddedinthewarranty.Insuchcircumstances,hardwareentitieswillneedtogatherthenecessaryinformationtoallocateaportionofthetransactionpricetotheseparateperformanceobligation,whichwillaffectthemannerinwhichrevenueisrecorded.Hardwareentitiesmayneedtofurtheranalyzewarrantiesofferingmultipleservices(oradditionalproducts)toidentifyeachseparateperformanceobligationinthearrangement.Therefore,hardwareentitiesshouldthoroughlyanalyzeallwarrantiesthatarenotseparatelypricedtodeterminewhethertheyshouldbeaccountedforunderthecostaccrualmethodorwhethertheyshouldbetreatedasseparateperformanceobligationsundertherevisedED.

Select Issues That Are Likely to Affect All Technology Companies

Contract CostsTherevisedEDrequirescapitalizationofcertaincostsassociatedwithobtainingacontractifthosecostsareincrementalandrecoverable.TherevisedEDalsorequirescapitalizationofcertaincostsoffulfillingacontractifallofthefollowingcriteriaaremetandthecostsarenotcoveredbyotherstandards:

1. “Thecostsrelatedirectlytoacontract(oraspecificanticipatedcontract).”

2. “Thecostsgenerateorenhanceresourcesoftheentitythatwillbeusedinsatisfyingperformanceobligationsinthefuture.”

3. “Thecostsareexpectedtoberecovered.”

Amortizationofcapitalizedcostswouldoccurinamannerconsistentwiththepatternoftransferofthegoodsorservicestowhichtheassetrelatesand,incertaincircumstances,mayextendbeyondtheoriginalcontracttermwiththecustomer(e.g.,whenfutureanticipatedcontractsorexpectedrenewalperiodsexist).Asapracticalexpedient,qualifyingcoststoobtainacontractcanbeexpensedasincurredwhentheamortizationperiodisoneyearorless.Allcapitalized-costassetswillbesubjecttoimpairmenttestingifanyindicatorsofimpairmentexist.

Dependingonhowanentitycurrentlyaccountsforrevenue-relatedcosts,theproposedguidancemayresultinsignificantchangesinpracticeandpotentiallyrequiretechnologyentitiestocapitalizecoststhattheymayhavepreviouslyexpensed.Entitiesmaywanttocloselyevaluatetheimpactofsuchguidanceontheircurrentaccountingpoliciesandconsidertheneedtodeterminetheiraccountingpolicyrelatedtocontractcostsforshort-termcontractswithadurationofoneyearorless.

Warranties that provide services beyond simple assurance that a product complies with agreed-upon specifications may give rise to additional performance obligations that may alter existing revenue recognition patterns.

7

The revised ED requires significantly more disclosures, including the judgments used in applying the guidance.

Presentation and DisclosuresTherevisedEDwouldrequiresignificantlymoreextensivedisclosuresthancurrentrevenuestandards,includingquantitativeandqualitativeinformationaboutcontractsandthesignificantjudgmentsusedinapplyingtheguidancetothosecontracts.Entitiesshouldconsiderhowdetailedtheirdisclosuresneedtobetomeettherequirementsandhowmuchemphasistoplaceoneachdisclosurerequirement.Therequireddisclosureswouldinclude:

• Adisaggregationofreportedrevenueinthe“primarycategoriesthatdepicthowthenature,amount,timing,anduncertaintyofrevenueandcashflowsareaffectedbyeconomicfactors.”

• Areconciliationofthebeginningandendingbalanceofcontractassetsandliabilities.

• Certaininformationaboutperformanceobligations(e.g.,typesofgoodsorservices,significantpaymentterms,typicaltimingofsatisfyingobligations,andotherprovisions).

• Informationaboutonerousobligations(extentandamountofsuchobligations,thereasonstheybecameonerous,theexpectedtimingtosatisfytheliability,andreconciliationofonerousbalances).

• Adescriptionofthesignificantjudgments,andchangesinthosejudgments,thataffecttheamountandtimingofrevenuerecognition.

• Informationaboutthemethods,inputs,andassumptionsusedtodeterminethetransactionpriceandallocateamountstoperformanceobligations.

• Informationaboutassetsrecognizedfromcoststoobtainorfulfillacontract,includingareconciliationofthebeginningandendingassets(bymaincategoryofasset).

OtherTherevisedEDprovidesguidanceonmanyothertopicsthatwerenothighlightedabove,includinglicensesandrightstouse,rightsofreturn,principal-versus-agentconsiderations,bill-and-holdarrangements,collectibility,onerouscontracts,andcustomeracceptance.Technologycompaniesshouldcarefullyanalyzesuchguidance,sinceitmaydifferfromcurrentpractice.Notethatsomeofthesetopicsarediscussedinrelationtosoftwarearrangementsintheattachedappendix.

Challenges for Technology Companies

Increased Use of JudgmentManagementwillneedtoexercisesignificantjudgmentinapplyingcertainoftherevisedED’srequirements,includingthoserelatedtotheidentificationofperformanceobligationsandallocationofrevenuetoeachperformanceobligation.ItisimportantforentitiestoconsiderhowtherevisedEDspecificallyappliestothemsothattheycanprepareforanychangesinrevenuerecognitionpatterns.

Retrospective Application TherevisedEDproposesretrospectiveapplication,withcertainoptionalpracticalexpedientsavailabletoentitiesattheirdiscretion.ThisaspectoftheproposalmayrequiretechnologyentitiestogatherdataandassesscontractsthatcommencedseveralyearsbeforetherevisedED’seffectivedate.Entitiesalsowillmostlikelyberequiredtoperformdualtrackingofrevenuebalancesduringthisretrospectiveperiod,giventhepotentialdifficultyassociatedwithretroactivelyrecalculatingrevenuebalancesatthetimethenewstandardbecomeseffective.

8

Entities will need to reevaluate existing systems, processes, and controls to ensure that they are able to produce the required information under the revised guidance.

Impact on ContractsManyorganizationshaveseveralbusinesscontractsthatarelinkedtofinancialperformanceorrevenuerecognitionspecifically,suchassalescompensationstructureagreements.Ifrevenuerecognitionchangesundertherevisedguidance,itemssuchascompensationplansmayalsoneedtobeevaluatedandadjustedaccordingly.

Systems, Processes and ControlsTherevisedEDproposesseveralnewpracticesanddisclosurerequirementsunderwhichtechnologyentitieswillhavetogatherandtrackinformationthattheymaynothavepreviouslymonitored.Thesystemsandprocessesassociatedwithsuchinformationmayneedtobemodifiedtosupportthecaptureofadditionaldataelementsthatmaynotcurrentlybesupportedbylegacysystems(e.g.,dataelementsneededtodetermineandallocatethetransactionpricebetweenseparateperformanceobligationsorelementsrelatedtocontractcoststhatmustbecapitalizedundertherevisedED).

Regardingtransactionprices,entitiesmayneedtodevelopanewmethodofestablishingastand-alonesellingpriceforeachperformanceobligation,takingintoaccount(1)variableconsideration,(2)thetimevalueofmoney,(3)noncashconsideration,and(4)considerationpayabletoacustomer.BecauseanentityhasnotpreviouslyconsideredmanyofthesefactorsinestablishingVSOEorestimatedsellingpricesunderthecurrentguidance,theentitywillneedtoupdateitscurrentpoliciesandprocedurestoestablishguidanceondeterminingtransactionprices.

Inaddition,toensuretheeffectivenessofinternalcontrolsoverfinancialreporting,managementwillneedtoassesswhetheradditionalcontrolsneedtobeimplemented.Technologyentitiesmayneedtobeginaggregatingessentialdatafromnewandexistingcontracts,sincemanyoftheirexistingcontractsmaybesubjecttotheproposedrulesgiventherequirementtoapplytherevisedEDretrospectively.

Income TaxesTaxdepartmentsneedtoassesschangesinbookrevenuerecognitionmethodstoprepareforthetaxeffects.Federalincometaxlawcontainsspecificrulesoncertaintypesofrevenue,suchasincomefromlong-termcontractsandadvancepaymentsforgoodsandservices.Thoserulesoftenoverlapwithataxpayer’sfinancialreportingpolicies,inwhichcasethetaxpayeroftenapplies,asitstaxmethod,therevenuerecognitionmethoditusesinmaintainingitsbooksandrecords.BecausetheproposedguidancemaychangetheamountandtimingofrevenuerecognitionforentitiesthatmaintaintheirbooksandrecordsunderU.S.GAAPorIFRSs,theaccountingproposedintherevisedEDmayhavecashtaximplicationsorgiverisetonewbook-taxdifferencesthatwillneedtobecaptured,calculated,andtrackedthroughtaxaccountingprocessesandsystems.

Ifachangeinataxaccountingmethodisadvantageousorexpedient,includingcircumstancesinwhichthebookmethodhashistoricallybeenused,thetaxpayerwillmostlikelyberequiredtoobtainapprovalfromthetaxauthorities.SimilarimplicationsmayariseinforeignjurisdictionsthatmaintainstatutoryaccountingrecordsunderU.S.GAAPorIFRSs.

Thinking AheadCommentsontherevisedEDandtheFASBcompanionproposedASUareduebyMarch13,2012.Afinalstandardisnotexpectedtobeissueduntillaterin2012andwouldbeeffectivenoearlierthanforannualperiodsbeginningonorafterJanuary1,2015(withaminimumofaone-yeardeferralfornonpublicentitiesapplyingU.S.GAAP).TechnologyentitiesshouldtakeadvantageofthistimetocarefullyexaminetherevisedED,providefeedbackontheproposedmodel,andbeginassessingtheimpactitmayhaveontheircurrentaccountingpolicies,procedures,systems,andprocesses.

9

Appendix — Key Differences Between ASC 985-605 and the FASB’s and IASB’s Revised ED ThetablebelowsummarizeskeydifferencesbetweenASC985-605andtheFASB’sandIASB’srevisedED.ItdoesnotaddressallpossiblefactpatternsandshouldbereadinconjunctionwithASC985-605,withtherevisedED,andwithotherrelevantguidance.ASC985-605statesthatifanarrangementcontainssoftwareaswellasservicesthatinvolvesignificantproduction,modification,orcustomizationofthesoftware,theservicescannotberecognizedseparatelyfromthesoftwareandthearrangementisthereforewithinthescopeofASC605-35.TherevisedEDwouldcompletelysupersedeASC985-605andASC605-35,amongmostothercurrentrevenuerecognitionguidanceinU.S.GAAP.ThetablefocusessolelyonthepotentialimpactstocontractscurrentlywithinthescopeofASC985-605anddoesnotaddressthepotentialchangestocontractswithinthescopeofASC605-35.AlthoughtherevisedEDalsoaddressesothertopicsthatarenotinASC985-605,suchasonerouscontracts,coststoobtainorfulfillacontract,financialstatementpresentation,anddisclosures,thetabledoesnotassessthepotentialimpactofthosetopics.

Thelinksbelowcanbeusedtojumptogroupsoftopicsinthetable,whichconsistsofthefiveprimarystepsforrevenuerecognitionundertherevisedED(aswellasitsscope):

• Scope.

• Step1:IdentifytheContractWithaCustomer.

• Step2:IdentifytheSeparatePerformanceObligationsintheContract.

• Step3:DeterminetheTransactionPrice.

• Step4:AllocatingtheTransactionPricetotheSeparatePerformanceObligationsintheContract.

• Step5:RecognizeRevenueWhen(oras)theEntitySatisfiesaPerformanceObligation.

10

ASC 985-605 Revised ED Likely Impact4

SCOPE

Scope Thisguidancegenerallyappliestothefollowingtransactionsandactivities:

• “Licensing,selling,leasing,orotherwisemarketingcomputersoftware.”

• “Thesoftwareandsoftware-relatedelementsofarrangementsthatincludesoftwarethatismore-than-incidentaltotheproductsorservicesinthearrangementasawhole.”

• “More-than-insignificantdiscountsonfuturepurchasesthatareofferedbyavendorinasoftwarearrangement.”

• “Arrangementstodeliversoftwareorasoftwaresystem,eitheraloneortogetherwithotherproductsorservicesthatrequiresignificantproduction,modification,orcustomizationofsoftware.”(ASC985-605-15-3)

ASC985-605includesvariousscopeexceptions,whicharedescribedinfurtherdetailinthesectionsbelow.

Thisguidanceappliestoallcontractswithcustomersforthetransferofgoodsorservices.Certaincontracts,suchasleasecontracts,insurancecontracts,guarantees,nonmonetaryexchanges,andcertainothercontractualrightsandobligations(i.e.,mostASCfinancialinstrumentstopics)areoutsidethescopeoftherevisedED.(9)5

“Acontractwithacustomermaybepartiallywithinthescopeof[therevisedED]andpartiallywithinthescopeofother[ASCtopics].”Ifothertopicsspecifyhowtoseparateorinitiallymeasureanypartsofthecontract,anentityfirstappliesthoseseparationormeasurementrequirements.Iftheothertopicsdonotspecifyhowtoseparateorinitiallymeasureanypartsofthecontract,theentityappliestherevisedEDtoseparateorinitiallymeasurethosepartsofthecontract.(11)

ContractspreviouslyaccountedforunderASC985-605arewithinthescopeoftherevisedED.Entitieswillnolongerhavetoevaluatewhetheranarrangementiswithinthescopeofmultiplerevenuestandards(e.g.,ASC985-605,ASC605-35,andASC605-25).Theywilluseasingle,comprehensivemodeltoaccountforallarrangementswithinthescopeoftherevisedED,andthepriorguidancewillbesuperseded.

NonsoftwareDeliverablesinaSoftwareArrangement

ASC985-605doesnotprovideguidanceonseparatingnonsoftware-relateddeliverablesthatarewithinthescopeofotherliteraturefromsoftwareandsoftware-relateddeliverables.Therefore,entitiesgenerallyfirstapplytheseparationandallocationguidanceinASC605-25toanarrangementthatcontainsbothsoftwareandnonsoftwaredeliverables.

TheseparationofacontractintoseparateperformanceobligationsandtheallocationofthetransactionpriceareaddressedbytherevisedED.SeeSteps2and4ofthefive-stepmodel,below.

ContractspreviouslyaccountedforunderASC985-605arewithinthescopeoftherevisedED.Entitieswillnolongerhavetoevaluatewhetheranarrangementiswithinthescopeofmultiplerevenuestandards(e.g.,ASC985-605,ASC605-35,andASC605-25).Theywilluseasingle,comprehensivemodeltoaccountforallarrangementswithinthescopeoftherevisedED,andthepriorguidancewillbesuperseded.

4 LikelyimpactisbasedontherevisedEDascurrentlywrittenandfortypicalcontractterms.Itissubjecttointerpretationandmaynotapplytoallfactsandcircumstances.5 ReferencesaretoparagraphsoftherevisedED.

11

ASC 985-605 Revised ED Likely Impact

SoftwareComponentsExcludedFromtheScopeofASC985-605

Whenanarrangementcontainsbothnonsoftwarecomponentsoftangibleproductsandsoftwarecomponents,thenonsoftwarecomponentsareexcludedfromthescopeofASC985-605.Ifitisdeterminedthatthesoftwarecomponentsandtangibleproductsfunctiontogethertodeliverthetangibleproducts’essentialfunctionality,theessentialsoftwareandanyundeliveredelementsrelatedtothatessentialsoftwareareexcludedfromthescopeofASC985-605.(ASC985-605-15-4)

Allpromisedgoodsorservicesinacontractwithacustomer(e.g.,softwarecomponents,nonsoftwarecomponents,andtangibleproducts)thatdonotmeetanyofthescopeexceptions,arewithinthescopeoftherevisedED.

ContractspreviouslyaccountedforunderASC985-605arewithinthescopeoftherevisedED.Entitieswillnolongerhavetoevaluatewhetheranarrangementiswithinthescopeofmultiplerevenuestandards(e.g.,ASC985-605,ASC605-35,andASC605-25).Theywilluseasingle,comprehensivemodeltoaccountforallarrangementswithinthescopeoftherevisedED,andthepriorguidancewillbesuperseded.

ArrangementsIncludingLeasedSoftwareandTangibleProducts

UnderASC985-605,inarrangementsinvolvingaleaseofsoftwareandhardware(e.g.,property,plant,orequipment),revenueattributabletothehardwareisaccountedforinaccordancewithASC840,whilerevenueattributabletothesoftware,includingPCS,isaccountedforinaccordancewithASC985-605(providedthatthesoftwareismorethanincidentaltothearrangementbutnotessentialtothefunctionalityofthecombinedproduct).Ifthesoftwarefunctionstogetherwiththeleasedequipmenttodelivertheproduct’sessentialfunctionality,thehardware,software,andsoftware-relatedelementsareoutsidethescopeofASC985-605andsubjecttootherapplicableaccountingguidance(e.g.,ASC840,ASC605-25,orSABTopic13).

AcontractwithacustomermaybepartiallywithinthescopeoftherevisedEDandpartiallywithinthescopeofotherASCtopics.Ifothertopicsspecifyhowtoseparateorinitiallymeasureanypartsofthecontract,anentityfirstappliesthoseseparationormeasurementrequirements.Iftheothertopicsdonotspecifyhowtoseparateorinitiallymeasureanypartsofthecontract,theentityappliestherevisedEDtoseparateorinitiallymeasurethosepartsofthecontract.(11)

TheFASBandIASBarealsointheprocessofacompleteoverhaulofleaseaccounting.Ascurrentlyproposed,thetentativeleaseguidanceprovidesindicatorsforentitiestouseindeterminingwhetheranassetusedbyasupplierinthedeliveryofaserviceisseparablefromthearrangementasawhole(e.g.,whethertheassetissoldorleasedseparatelybythesupplierandwhetherthecustomercanusetheassetonitsownortogetherwithotherresourcesavailabletothecustomer).Insituationsinwhichasupplierdirectshowanassetisusedtoperformservicesforacustomer,thecustomerandsuppliermustassesswhethertheuseoftheassetisseparablefromtheservicesprovidedtothecustomer(e.g.,computerandserverequipmentwithoutsourcedinformationtechnologyservicesoracargoshipwithtimecharterservices).Iftheassetisseparable,thearrangementcouldcontainaleaseiftheassetiswithinthescopeofthetentativeleaseaccountingguidance(andthusisoutsidethescopeoftheproposedrevenueguidance).However,iftheuseofanassetisaninseparablepartoftheservicesrequestedbythecustomer,theentirearrangementwouldbewithinthescopeoftheproposedrevenueguidance.

ContractspreviouslyaccountedforunderASC985-605arewithinthescopeoftherevisedED.Entitieswillnolongerhavetoevaluatewhetheranarrangementiswithinthescopeofandcomplywithmultiplerevenuestandards(e.g.,ASC985-605,ASC605-35,andASC605-25).However,entitieswillstillberequiredtoseparateandallocatecontractconsiderationforgoodsandservicesthatarewithinthescopeofotherstandards.

12

ASC 985-605 Revised ED Likely Impact

HostingArrangements

AsoftwareelementinahostingarrangementisonlywithinthescopeofASC985-605ifthe“customerhasthecontractualrighttotakepossessionofthesoftwareatanytimeduringthehostingperiodwithoutsignificantpenalty[andit]isfeasibleforthecustomertoeitherrunthesoftwareonitsownhardwareorcontractwithanotherparty...tohostthesoftware.”Ifthearrangementdoesnotmeetthesetwocriteria,itwouldbeaccountedforasaservicecontractandwouldbeoutsidethescopeofASC985-605.(ASC985-605-55-121)

Dependingonthesubstanceofahostingarrangement,acustomermayobtaincontrolofthesoftwareitself,simplyhavetherighttouseitovertime,oracombinationofboth.(SeeStep4belowforadiscussionofthefactorsthatindicatewhethercontroltransfersoveraperiodoftimeoratapointintime.)Inotherinstances,thetangibleproductsusedtoprovidethehostingmightbewithinthescopeofthetentativeleaseaccountingguidance(seeArrangementsIncludingLeasedSoftwareandTangibleProductsabove).

Hostingarrangements,whetherhistoricallyaccountedforunderASC985-605orasaservicecontract,willbewithinthescopeoftherevisedED.Entitieswillhavetocloselyevaluatethesubstanceofthecontracttodeterminewhethertheentityis(1)performingaserviceforwhichcontrolistransferringovertimeor(2)insubstance,licensingsoftwareforwhichcontrolistransferredatapointintimeandprovidingaseparatehostingservice(whichmaybethecasewhenthecriteriainASC985-605-55-121aremet).WhileanentitywillmostlikelyconsiderfactorssimilartothescopingrulesinASC985-605todeterminethesubstanceofthearrangementandappropriateaccountinginaccordancewiththerevisedED,thesecriteriaarenotspecificallyincludedintherevisedEDandthusnotnecessarilydeterminativeoftheaccountingconclusion.Further,entitiesshouldcloselyevaluatethecontractualtermsofthehardwareasitmaymeetthedefinitionofalease.Ifitdoes,thecontractwouldneedtobeseparatedandinitiallymeasuredasdescribedinArrangementsIncludingLeasedSoftwareandTangibleProductsabove.

SoftwareRequiringSignificantProduction,Modification,orCustomization

Certainsoftwaresalesinvolvesignificantproduction,modification,orcustomizationofsoftware.AsstatedinASC985-605-25-88,thisarrangementisaccountedforunderASC605-35byusingtherelevantguidanceinASC985-605-25-88through25-107.

ContractscurrentlyaccountedforunderASC605-35arewithinthescopeoftherevisedED.

ContractspreviouslyaccountedforunderASC985-605orASC605-35arewithinthescopeoftherevisedED.Entitieswillnolongerhavetoevaluatewhetheranarrangementisinthescopeofmultiplerevenuestandards(e.g.,ASC985-605,ASC605-35,andASC605-25).Theywilluseasingle,comprehensivemodeltoaccountforallarrangementswithinthescopeoftherevisedED,andthepriorguidancewillbesuperseded.

13

ASC 985-605 Revised ED Likely Impact

STEP 1: IDENTIFY THE CONTRACT WITH A CUSTOMER

PersuasiveEvidenceofanArrangementExists

Practicevarieswithrespecttotheuseofwrittencontracts.Althoughanumberofsectorsoftheindustryrelyuponsignedcontractstodocumentarrangements,othersectorsoftheindustrythatlicensesoftware(notablythepackagedsoftwaresector)donot.

Ifthevendoroperatesinamannerthatdoesnotrelyonsignedcontractstodocumenttheelementsandobligationsofanarrangement,thevendorshouldhaveotherformsofevidencetodocumentthetransaction(e.g.,apurchaseorderfromathirdpartyoronlineauthorization).Ifthevendor’scustomarybusinesspracticeistousewrittencontracts,evidenceofthearrangementisprovidedonlywithacontractsignedbybothparties.

TherevisedEDdefinesacontractasanagreementbetweentwoormorepartiesthatcreatesenforceablerightsandobligations.Contractscanbewritten,oral,orimpliedbytheentity’scustomarybusinesspractices.(13)

Undertheproposedrevenuerequirements,acontractexistsonlyif:

• “Thecontracthascommercialsubstance.”

• “Thepartiestothecontracthaveapprovedthecontract”andarecommittedtosatisfying“theirrespectiveobligations.”

• “Theentitycanidentifyeachparty’srightsregardingthegoodsorservicestobetransferred.”

• “Theentitycanidentifythepaymenttermsforthegoodsorservicestobetransferred.”(14)

Inaddition,acontractdoesnotexistifeachparty“hastheunilateralenforceablerighttoterminateawhollyunperformedcontractwithoutcompensatingtheotherparty(parties).”(15)

ThedefinitionofacontractundertheproposedguidancediffersfromthedefinitionofpersuasiveevidenceofanarrangementunderASC985-605.Dependingonanentity’shistoricalpractice,thesedifferencesmayresultinaccountingchanges.

Inaddition,therequirementinASC985-605that“collectibilityisprobable”forrevenuetoberecognizedisnotanexplicitcriterionintherevisedED.However,intheBasisforConclusionsoftherevisedED,theboardsindicatedthatareasonableexpectationofcollectibilitywouldbenecessaryforacontracttohavecommercialsubstance.Therefore,whenanentitydoesnothaveareasonableexpectationofcollectibility,acontractmaynotexistundertherevisedED(andthus,revenuecannotberecognized).Somemayinterpretthecurrentrequirement(i.e.,thatcollectibilityisprobable)asadifferentthresholdthanthatintherevisedED(i.e.,thatthecontracthascommercialsubstanceandthereforeanentityhasareasonableexpectationofcollectibility).

14

ASC 985-605 Revised ED Likely Impact

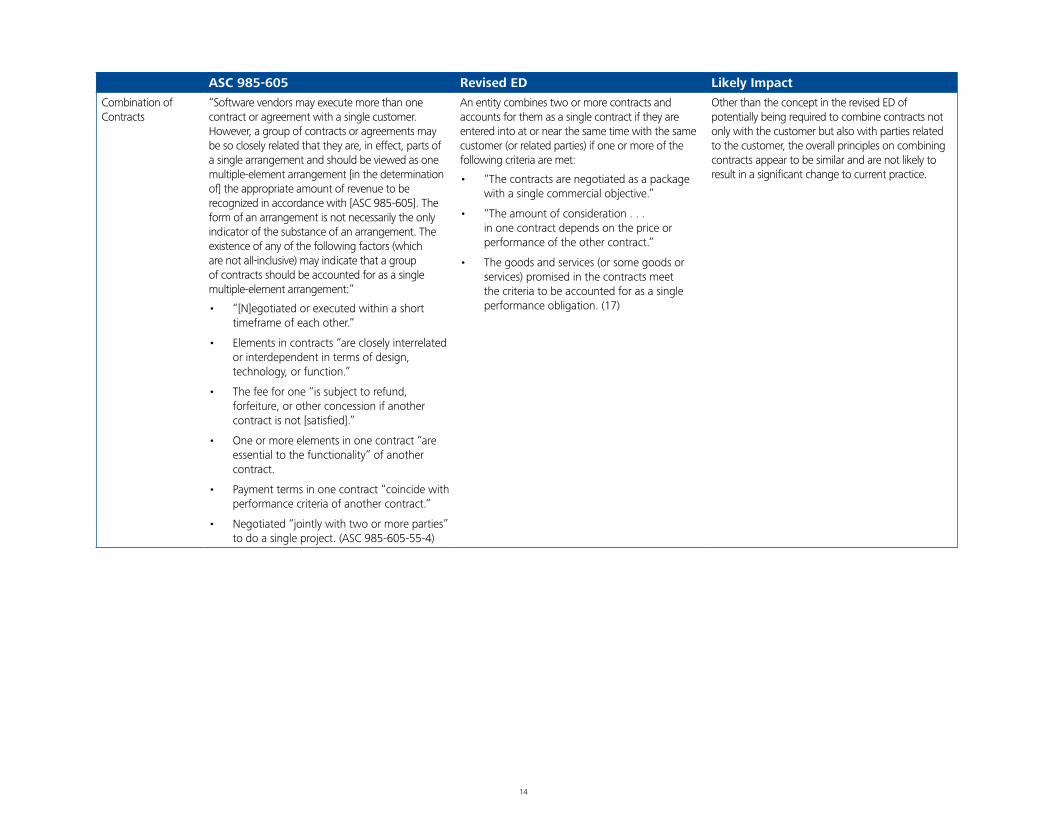

CombinationofContracts

“Softwarevendorsmayexecutemorethanonecontractoragreementwithasinglecustomer.However,agroupofcontractsoragreementsmaybesocloselyrelatedthattheyare,ineffect,partsofasinglearrangementandshouldbeviewedasonemultiple-elementarrangement[inthedeterminationof]theappropriateamountofrevenuetoberecognizedinaccordancewith[ASC985-605].Theformofanarrangementisnotnecessarilytheonlyindicatorofthesubstanceofanarrangement.Theexistenceofanyofthefollowingfactors(whicharenotall-inclusive)mayindicatethatagroupofcontractsshouldbeaccountedforasasinglemultiple-elementarrangement:”

• “[N]egotiatedorexecutedwithinashorttimeframeofeachother.”

• Elementsincontracts“arecloselyinterrelatedorinterdependentintermsofdesign,technology,orfunction.”

• Thefeeforone“issubjecttorefund,forfeiture,orotherconcessionifanothercontractisnot[satisfied].”

• Oneormoreelementsinonecontract“areessentialtothefunctionality”ofanothercontract.

• Paymenttermsinonecontract“coincidewithperformancecriteriaofanothercontract.”

• Negotiated“jointlywithtwoormoreparties”todoasingleproject.(ASC985-605-55-4)

Anentitycombinestwoormorecontractsandaccountsforthemasasinglecontractiftheyareenteredintoatornearthesametimewiththesamecustomer(orrelatedparties)ifoneormoreofthefollowingcriteriaaremet:

• “Thecontractsarenegotiatedasapackagewithasinglecommercialobjective.”

• “Theamountofconsideration...inonecontractdependsonthepriceorperformanceoftheothercontract.”

• Thegoodsandservices(orsomegoodsorservices)promisedinthecontractsmeetthecriteriatobeaccountedforasasingleperformanceobligation.(17)

OtherthantheconceptintherevisedEDofpotentiallybeingrequiredtocombinecontractsnotonlywiththecustomerbutalsowithpartiesrelatedtothecustomer,theoverallprinciplesoncombiningcontractsappeartobesimilarandarenotlikelytoresultinasignificantchangetocurrentpractice.

15

ASC 985-605 Revised ED Likely Impact

ModificationstoaSoftwareLicenseandSideAgreements

Otherthanrequiringthevendortoconsidertheimplicationsofconcessions,ASC985-605doesnotspecificallydiscussmodificationstosoftwarearrangements.Ifamodificationtoasoftwarearrangementisconsideredaconcession,thevendormayneedtoevaluatewhethertheoriginalfeewasfixedordeterminableandconsidertheimpactontheaccountingforfuturearrangements.Generally,previouslyrecognizedrevenueisnotaffectedandthevendordeterminestheimpactofamodificationprospectivelyonthebasisofthefactsandcircumstancesofthemodification.

Sideagreementsshouldbeevaluatedonacase-by-casebasistodeterminewhetherandhowtheyaffectthetermsofthearrangementandtherebyrevenuerecognition.Apracticeofenteringintosideagreementsraisesquestionsaboutwhatconstitutespersuasiveevidenceofanarrangementandwhen,infact,anarrangementhasbeenconsummated.

“Acontractmodificationexistswhenthepartiestoacontractapproveachangeinthescopeorpriceofacontract(orboth).”(18)IfthemodificationmeetsthecontractcriteriaundertherevisedED(discussedinPersuasiveEvidenceofanArrangementExistsabove),theaccountingtreatmentdependsonthenatureofthemodification.However,ifthepartieshaveapprovedachangeinthescopebutnottheprice,anentitywouldonlyaccountforthemodificationwhentheentityhasanexpectationthatthepriceofthemodificationwillbeapproved.

Acontractmodificationwouldbeaccountedforasaseparatecontractonlyifthemodificationresultsin(1)aseparateperformanceobligationand(2)additionalconsiderationthatreflectstheentity’sstand-alonesellingpriceofthatseparateperformanceobligation(whenappropriateadjustmentsforthecontract’sparticularcircumstancesaretakenintoaccount).Otherwise,anentitywouldevaluatethemodifiedcontractandallocatetheremainingtransactionpricetotheremainingperformanceobligations(prospectively)andupdateitsmeasureofprogresstowardcompletionforperformanceobligationsthataresatisfiedovertime(whichcouldresultinacumulativecatch-up).However,ifthemodificationtothecontractisonlyachangeinthetransactionprice,themodifiedtransactionpricewouldbereallocatedtoallperformanceobligationsinthecontract(seeStep4below).(19–22,78)

Althoughthereisnoexplicitguidance,entitieswithinthescopeofASC985-605generallyaccountforcontractmodificationsandsideagreementsprospectively.SincetherevisedEDspecificallyaddressesaccountingforcontractmodifications,itshouldimprovedisciplineandconsistencyinaccountingforcontractmodifications.TherevisedEDmayresultinacumulative-effectadjustmentwhenthemodificationisonlytothetransactionprice(becausethemodifiedtransactionpriceisreallocatedtotheseparateperformanceobligationsasifitexistedatcontractinception,potentiallyaffectingtheamountofrevenuepreviouslyrecognizedforsatisfiedperformanceobligations).

TherevisedEDdoesnotspecificallyaddresssideagreements,andentitieswillneedtoevaluatethemonacase-by-casebasistodeterminewhetherthey(1)representtermsintheoriginalcontract(andmeetthecontractcriteriaundertheproposedguidance,discussedabove)or(2)representacontractmodification(andshouldbeaccountedforunderthecontractmodificationguidancedescribedabove).

Ifasideagreementrepresentstermsthatexistedintheoriginalcontractandwerenotincludedintheoriginalaccountingforthatcontract,theentityshoulddeterminewhethertheadjustmentsfortheimpactofthesideagreementresultinanerrorunderASC250.

16

ASC 985-605 Revised ED Likely Impact

STEP 2: IDENTIFY THE SEPARATE PERFORMANCE OBLIGATIONS IN THE CONTRACT

Multiple-ElementArrangements

Softwarearrangementscommonlycomprisemultipleelementsordeliverables(i.e.,softwareandanycombinationofPCS,specifiedorunspecifiedsoftwareproductsorupgrades,additionallicenses,services,orothernonsoftwaredeliverables).Avendorshouldseparateamultiple-elementarrangementtoaccountforeachcomponentindividually(inaccordancewiththespecificguidanceprovidedinASC985-605).

Anentityidentifies“whichgoodsorservices(orwhichbundlesofgoodsorservices)aredistinct”andthereforeaccountedforasseparateperformanceobligations.(23)

TherevisedEDdefinesaperformanceobligationas“apromiseinacontractwithacustomertotransferagoodorservicetothecustomer.”Thisobligationmaybeexplicitinthecontractorimplied.(24)

TherevisedEDlistswhatmaybeconsideredagoodorserviceinacontract.(26).Entitiesevaluatethegoodsorservicestodeterminetheappropriateaccountingunits(i.e.,separateperformanceobligations).

SeeSeparatingtheArrangementbelowforadditionaldiscussionofhowtodeterminetheaccountingunitsinacontract.

Thepromisedgoodsorservicesinacontractaresimilartothecurrentconceptsofa“deliverable”or“element.”Onceanentitydeterminesthegoodsorservices(explicitorimplied)inthecontract,itthenmustseparatethosegoodsorservicesintoseparateunitsofaccounting.BecausetherevisedEDislessrestrictiveinthisarea,manyarrangementswillhavemoreunitsofaccountingthanunderASC985-605.ThiscouldresultinlessdeferralofrevenueinsituationsinwhichVSOEoffairvaluedoesnotexistforanundeliveredelementthatcouldmeettheseparationcriteriaundertherevisedED.ThismayrequireentitiestocloselyevaluatethegoodsorservicesdeliveredearlierinanarrangementthatmaynothavepreviouslybeengivenasmuchscrutinybecauserevenuewasbeingdeferredbecauseofanundeliveredelementnothavingVSOEoffairvalue(e.g.,PCS).

SeparatingtheArrangement

“Ifanarrangementincludesmultipleelements,thefee[is]allocatedtothevariouselements[VSOE]offairvalue,regardlessofanyseparatepricesstatedinthecontractforeachelement.[VSOE]offairvalueislimitedtothefollowing:”

• “Thepricechargedwhenthesameelementissoldseparately.”

• “Foranelementnotyetbeingsoldseparately,thepriceestablishedbymanagementhavingtherelevantauthority;itmustbeprobablethattheprice,onceestablished,willnotchangebeforetheseparateintroductionoftheelementintothemarketplace.”(ASC985-605-25-6)

Anentityaccountsforapromisetotransfermorethanonegoodorserviceasaseparateperformanceobligationifitisdistinct.Agoodorserviceis“distinct”iftheentityregularlysellsitseparatelyorthe“customercanbenefitfromthegoodorserviceeitheronitsownortogetherwithotherresourcesthatarereadilyavailable.”(27)

Further,theboardsdecidedthatanentitywouldaccountforabundleofgoodsorservicesasasingleperformanceobligationifthegoodsorservicesare(1)“highlyinterrelated”andtheentityprovides“asignificantserviceofintegrating”themintoacombineditemoritemsand(2)significantlymodifiedorcustomizedtofulfillthecontract.(28)

“Asapracticalexpedient,[when]twoormoredistinctgoodsorservices...havethesamepatternoftransfertothecustomer,”anentitymaycombinethemintooneseparateperformanceobligation.(30)

TherevisedEDreplacesthespecificrulesunderASC985-605withaprinciplethatislikelytoincreasethenumberofaccountingunitsbecauseofthelessrestrictiverequirementsintherevisedEDtoseparateperformanceobligations.Forexample,thefactthatVSOEoffairvaluedoesnotexistforanundeliveredelementwillnotdictatewhethergoodsorservicesinacontractcanbeseparated.The“distinct”criteriaprovidedintherevisedEDaregenerallyviewedasbeingconsistentwiththestand-alonevalueconceptinASC605-25.

UndertherevisedED,anentitymayneedtousesignificantjudgmentwhendeterminingwhetherthegoodsorservicesare“highlyinterrelated”and“significantlymodifiedorcustomized.”TheproposedASUincludesexamplestoillustratethisguidance;however,furtherclarificationmaybeneededtoensureconsistentapplication.

17

ASC 985-605 Revised ED Likely Impact

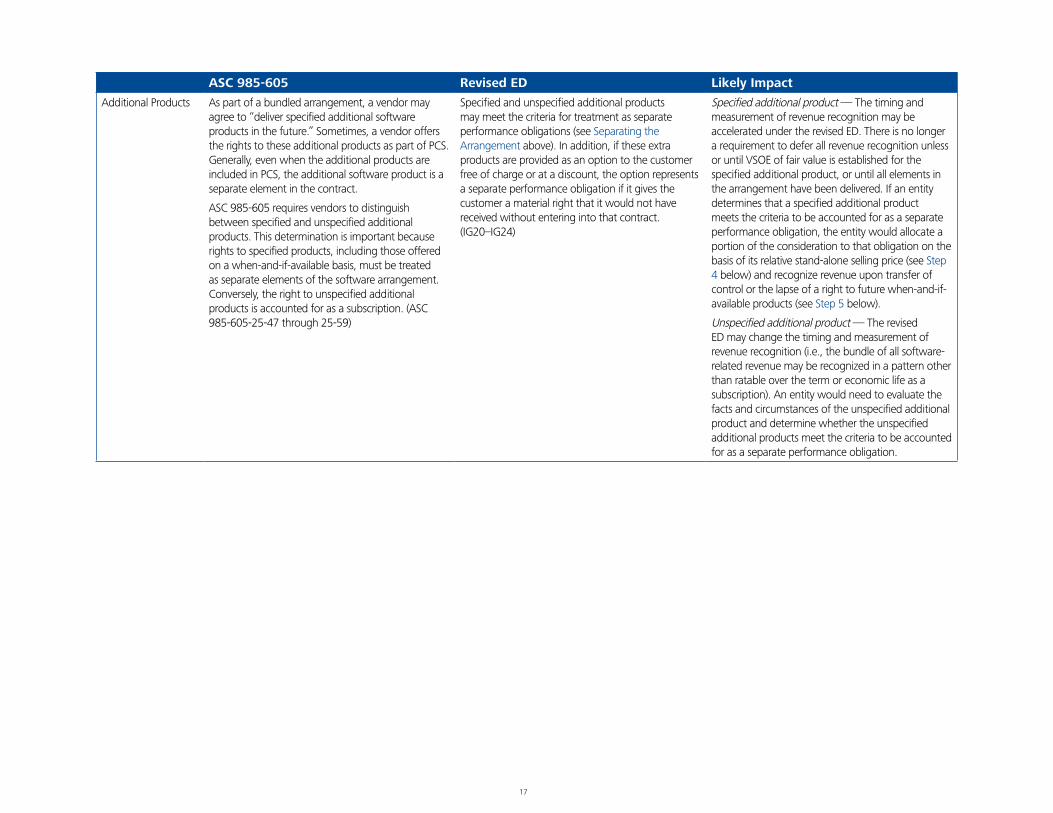

AdditionalProducts Aspartofabundledarrangement,avendormayagreeto“deliverspecifiedadditionalsoftwareproductsinthefuture.”Sometimes,avendorofferstherightstotheseadditionalproductsaspartofPCS.Generally,evenwhentheadditionalproductsareincludedinPCS,theadditionalsoftwareproductisaseparateelementinthecontract.

ASC985-605requiresvendorstodistinguishbetweenspecifiedandunspecifiedadditionalproducts.Thisdeterminationisimportantbecauserightstospecifiedproducts,includingthoseofferedonawhen-and-if-availablebasis,mustbetreatedasseparateelementsofthesoftwarearrangement.Conversely,therighttounspecifiedadditionalproductsisaccountedforasasubscription.(ASC985-605-25-47through25-59)

Specifiedandunspecifiedadditionalproductsmaymeetthecriteriafortreatmentasseparateperformanceobligations(seeSeparatingtheArrangementabove).Inaddition,iftheseextraproductsareprovidedasanoptiontothecustomerfreeofchargeoratadiscount,theoptionrepresentsaseparateperformanceobligationifitgivesthecustomeramaterialrightthatitwouldnothavereceivedwithoutenteringintothatcontract.(IG20–IG24)

Specifiedadditionalproduct—ThetimingandmeasurementofrevenuerecognitionmaybeacceleratedundertherevisedED.ThereisnolongerarequirementtodeferallrevenuerecognitionunlessoruntilVSOEoffairvalueisestablishedforthespecifiedadditionalproduct,oruntilallelementsinthearrangementhavebeendelivered.Ifanentitydeterminesthataspecifiedadditionalproductmeetsthecriteriatobeaccountedforasaseparateperformanceobligation,theentitywouldallocateaportionoftheconsiderationtothatobligationonthebasisofitsrelativestand-alonesellingprice(seeStep4below)andrecognizerevenueupontransferofcontrolorthelapseofarighttofuturewhen-and-if-availableproducts(seeStep5below).

Unspecifiedadditionalproduct—TherevisedEDmaychangethetimingandmeasurementofrevenuerecognition(i.e.,thebundleofallsoftware-relatedrevenuemayberecognizedinapatternotherthanratableoverthetermoreconomiclifeasasubscription).Anentitywouldneedtoevaluatethefactsandcircumstancesoftheunspecifiedadditionalproductanddeterminewhethertheunspecifiedadditionalproductsmeetthecriteriatobeaccountedforasaseparateperformanceobligation.

18

ASC 985-605 Revised ED Likely Impact

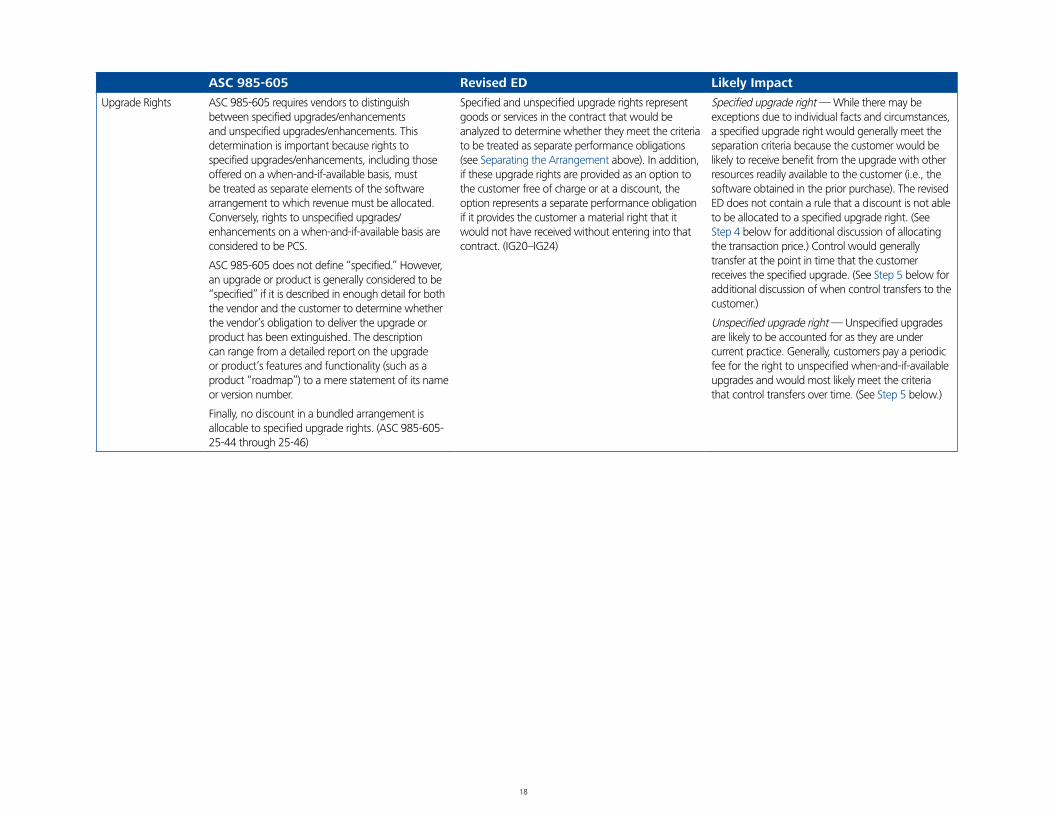

UpgradeRights ASC985-605requiresvendorstodistinguishbetweenspecifiedupgrades/enhancementsandunspecifiedupgrades/enhancements.Thisdeterminationisimportantbecauserightstospecifiedupgrades/enhancements,includingthoseofferedonawhen-and-if-availablebasis,mustbetreatedasseparateelementsofthesoftwarearrangementtowhichrevenuemustbeallocated.Conversely,rightstounspecifiedupgrades/enhancementsonawhen-and-if-availablebasisareconsideredtobePCS.

ASC985-605doesnotdefine“specified.”However,anupgradeorproductisgenerallyconsideredtobe“specified”ifitisdescribedinenoughdetailforboththevendorandthecustomertodeterminewhetherthevendor’sobligationtodelivertheupgradeorproducthasbeenextinguished.Thedescriptioncanrangefromadetailedreportontheupgradeorproduct’sfeaturesandfunctionality(suchasaproduct“roadmap”)toamerestatementofitsnameorversionnumber.

Finally,nodiscountinabundledarrangementisallocabletospecifiedupgraderights.(ASC985-605-25-44through25-46)

Specifiedandunspecifiedupgraderightsrepresentgoodsorservicesinthecontractthatwouldbeanalyzedtodeterminewhethertheymeetthecriteriatobetreatedasseparateperformanceobligations(seeSeparatingtheArrangementabove).Inaddition,iftheseupgraderightsareprovidedasanoptiontothecustomerfreeofchargeoratadiscount,theoptionrepresentsaseparateperformanceobligationifitprovidesthecustomeramaterialrightthatitwouldnothavereceivedwithoutenteringintothatcontract.(IG20–IG24)

Specifiedupgraderight—Whiletheremaybeexceptionsduetoindividualfactsandcircumstances,aspecifiedupgraderightwouldgenerallymeettheseparationcriteriabecausethecustomerwouldbelikelytoreceivebenefitfromtheupgradewithotherresourcesreadilyavailabletothecustomer(i.e.,thesoftwareobtainedinthepriorpurchase).TherevisedEDdoesnotcontainarulethatadiscountisnotabletobeallocatedtoaspecifiedupgraderight.(SeeStep4belowforadditionaldiscussionofallocatingthetransactionprice.)Controlwouldgenerallytransferatthepointintimethatthecustomerreceivesthespecifiedupgrade.(SeeStep5belowforadditionaldiscussionofwhencontroltransferstothecustomer.)

Unspecifiedupgraderight—Unspecifiedupgradesarelikelytobeaccountedforastheyareundercurrentpractice.Generally,customerspayaperiodicfeefortherighttounspecifiedwhen-and-if-availableupgradesandwouldmostlikelymeetthecriteriathatcontroltransfersovertime.(SeeStep5below.)

19

ASC 985-605 Revised ED Likely Impact

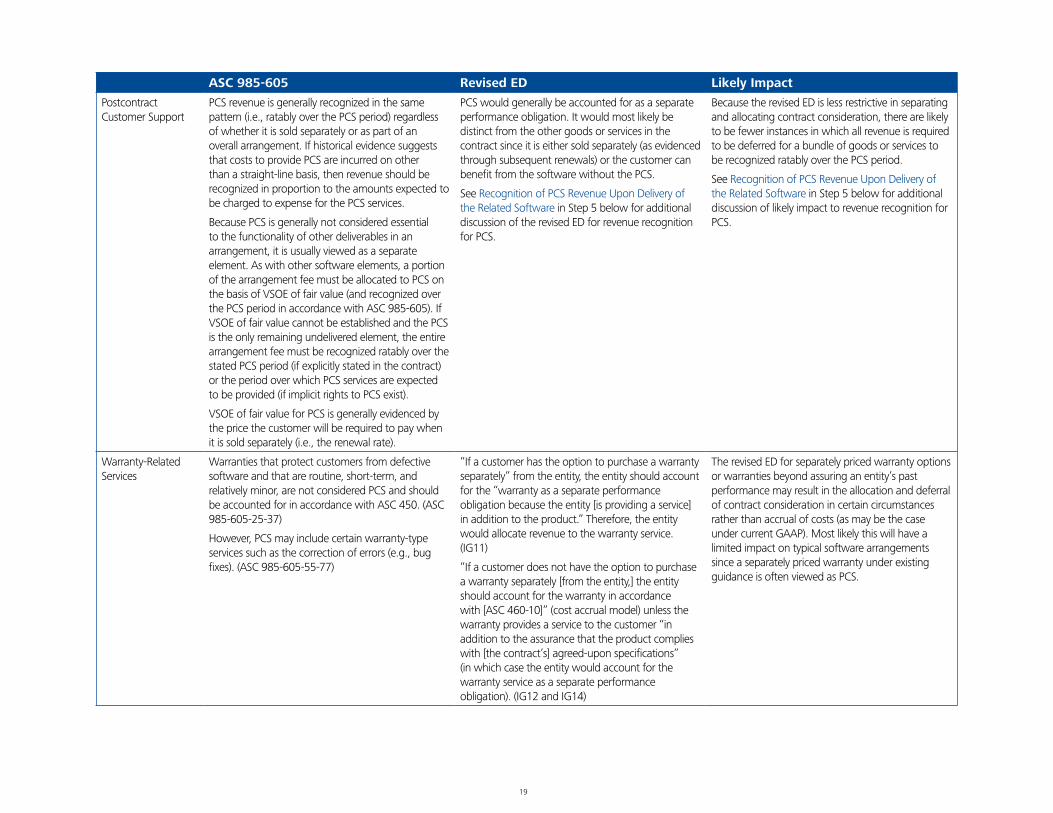

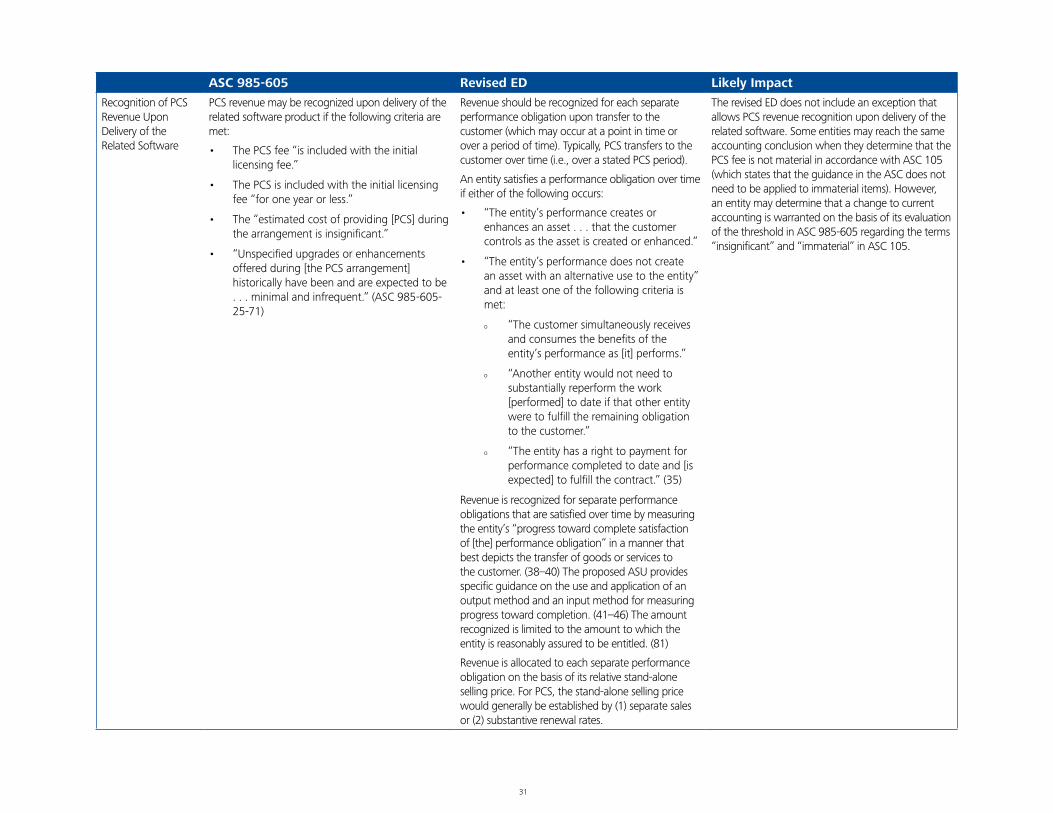

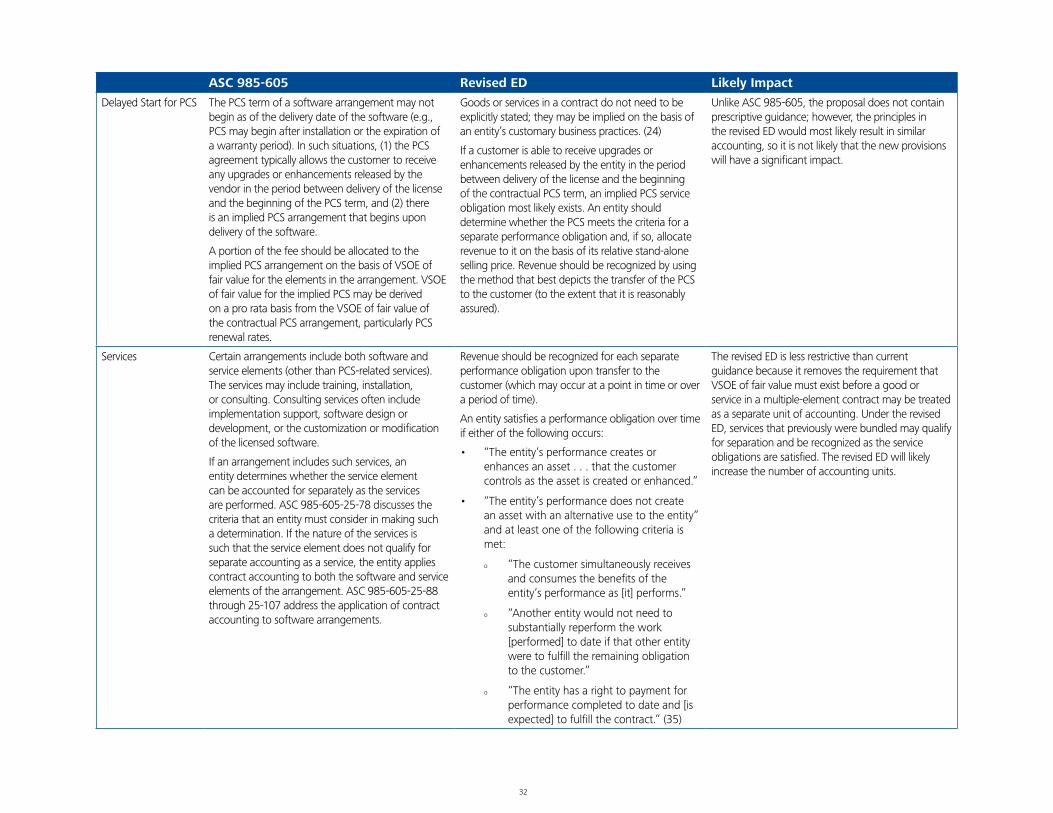

PostcontractCustomerSupport

PCSrevenueisgenerallyrecognizedinthesamepattern(i.e.,ratablyoverthePCSperiod)regardlessofwhetheritissoldseparatelyoraspartofanoverallarrangement.IfhistoricalevidencesuggeststhatcoststoprovidePCSareincurredonotherthanastraight-linebasis,thenrevenueshouldberecognizedinproportiontotheamountsexpectedtobechargedtoexpenseforthePCSservices.

BecausePCSisgenerallynotconsideredessentialtothefunctionalityofotherdeliverablesinanarrangement,itisusuallyviewedasaseparateelement.Aswithothersoftwareelements,aportionofthearrangementfeemustbeallocatedtoPCSonthebasisofVSOEoffairvalue(andrecognizedoverthePCSperiodinaccordancewithASC985-605).IfVSOEoffairvaluecannotbeestablishedandthePCSistheonlyremainingundeliveredelement,theentirearrangementfeemustberecognizedratablyoverthestatedPCSperiod(ifexplicitlystatedinthecontract)ortheperiodoverwhichPCSservicesareexpectedtobeprovided(ifimplicitrightstoPCSexist).

VSOEoffairvalueforPCSisgenerallyevidencedbythepricethecustomerwillberequiredtopaywhenitissoldseparately(i.e.,therenewalrate).

PCSwouldgenerallybeaccountedforasaseparateperformanceobligation.Itwouldmostlikelybedistinctfromtheothergoodsorservicesinthecontractsinceitiseithersoldseparately(asevidencedthroughsubsequentrenewals)orthecustomercanbenefitfromthesoftwarewithoutthePCS.

SeeRecognitionofPCSRevenueUponDeliveryoftheRelatedSoftwareinStep5belowforadditionaldiscussionoftherevisedEDforrevenuerecognitionforPCS.

BecausetherevisedEDislessrestrictiveinseparatingandallocatingcontractconsideration,therearelikelytobefewerinstancesinwhichallrevenueisrequiredtobedeferredforabundleofgoodsorservicestoberecognizedratablyoverthePCSperiod.

SeeRecognitionofPCSRevenueUponDeliveryoftheRelatedSoftwareinStep5belowforadditionaldiscussionoflikelyimpacttorevenuerecognitionforPCS.

Warranty-RelatedServices

Warrantiesthatprotectcustomersfromdefectivesoftwareandthatareroutine,short-term,andrelativelyminor,arenotconsideredPCSandshouldbeaccountedforinaccordancewithASC450.(ASC985-605-25-37)

However,PCSmayincludecertainwarranty-typeservicessuchasthecorrectionoferrors(e.g.,bugfixes).(ASC985-605-55-77)

“Ifacustomerhastheoptiontopurchaseawarrantyseparately”fromtheentity,theentityshouldaccountforthe“warrantyasaseparateperformanceobligationbecausetheentity[isprovidingaservice]inadditiontotheproduct.”Therefore,theentitywouldallocaterevenuetothewarrantyservice.(IG11)

“Ifacustomerdoesnothavetheoptiontopurchaseawarrantyseparately[fromtheentity,]theentityshouldaccountforthewarrantyinaccordancewith[ASC460-10]”(costaccrualmodel)unlessthewarrantyprovidesaservicetothecustomer“inadditiontotheassurancethattheproductcomplieswith[thecontract’s]agreed-uponspecifications”(inwhichcasetheentitywouldaccountforthewarrantyserviceasaseparateperformanceobligation).(IG12andIG14)

TherevisedEDforseparatelypricedwarrantyoptionsorwarrantiesbeyondassuringanentity’spastperformancemayresultintheallocationanddeferralofcontractconsiderationincertaincircumstancesratherthanaccrualofcosts(asmaybethecaseundercurrentGAAP).MostlikelythiswillhavealimitedimpactontypicalsoftwarearrangementssinceaseparatelypricedwarrantyunderexistingguidanceisoftenviewedasPCS.

20

ASC 985-605 Revised ED Likely Impact

PostdeliveryTelephoneSupport

ASC985-605requiresthatpostdeliverytelephonesupportthatisofferedoravailabletocustomersatnoadditionalchargebeaccountedforasPCS.Generally,thearrangementconsiderationallocatedtothetelephonesupportwouldhavetoberecognizedasrevenueovertheperiodduringwhichthetelephonesupportisexpectedtobeprovidedunlesstheASC985-605-25-71conditionsaremet,inwhichcasetherevenueallocabletotelephonesupportmayberecognizedtogetherwiththeinitiallicensingfeeondeliveryofthesoftware(substantiallyalltelephonesupportservicesareperformedwithinoneyearofthedateofsoftwaredelivery).

Postdeliverytelephonesupportismostlikelyaserviceinthecontractandanentitymustevaluateiftheservicerepresentsaseparateperformanceobligation.Ifitdoesnotmeettheseparationcriteria,theserviceshouldbecombinedwithanothergoodorserviceuntilthatbundleisdistinct.(27)

TherevisedEDdoesnotexplicitlyincludetheexceptionsthatwouldallowforpostdeliverytelephonesupporttoberecognizedupondeliveryofthesoftwarelicense.Rather,anentitywouldhavetoconcludethattheservicestobeprovidedarenotmaterialinaccordancewithASC105toconcludethattheseservicesdonotrequireallocationanddeferralofaportionoftheconsiderationinthearrangement.ASC105statesthattheguidanceintheASCdoesnotneedtobeappliedtoimmaterialitems.(BC66)

IndemnificationClauses

Thestandardsoftwarelicenseagreementofasoftwarevendoroftenincludesaclausethatprovidesforindemnificationforliabilitiesanddamagesarisingfromanyclaimsofpatent,copyright,trademark,ortradesecretinfringementbythesoftwarevendor’ssoftware.Thistypeofindemnificationisnotanelementthatcanbeseparatedfromthesoftware;rather,itisaninherentcomponentofthesoftwarelicenseitselfandissimilartoastandardwarranty.

“[A]nentity’spromisetoindemnifythecustomerforliabilitiesanddamagesarisingfromclaimsofpatent,copyright,trademark,orotherinfringementbytheentity’sproductsdoesnotgiverisetoaperformanceobligation.”TheentityaccountsforsuchobligationsinaccordancewiththeguidanceonlosscontingenciesinASC450-20.(IG15)

ItisnotlikelythatthiswillhaveasignificantimpactbecausetheprovisionsoftherevisedEDareconsistentwithcurrentpractice.

21

ASC 985-605 Revised ED Likely Impact

STEP 3: DETERMINE THE TRANSACTION PRICE

Vendor’sFeeIsFixedorDeterminable—ExtendedPaymentTerms

UnderASC985-605,anarrangementfeemustbefixedordeterminablebeforerevenuecanberecognized.Ifavendorcannotconcludethatthefeeisfixedordeterminableattheoutsetofanarrangement,revenuewouldberecognizedaspaymentsfromthecustomerbecomedue(providedthatallotherrequirementsforrevenuerecognitionaremet).

Inarrangementswithextendedpaymentterms,itmaybelesslikelythatthevendorwillcollectthefullpaymentstipulatedinthepaymenttermsandthearrangementfeemaynotmeetthefixed-or-determinablecriterion.ASC985-605-25-34specifiesthatanarrangementfeeispresumednottobefixedordeterminable“ifpaymentofasignificantportionofthesoftwarelicensingfeeisnotdueuntilafterexpirationofthelicenseormorethan12monthsafterdelivery.”

Anentity’sobjectivewhendeterminingthetransactionpriceistoestimatethetotalamountofconsiderationtowhichtheentityexpectstobeentitledunderthecontract.Tomeetthatobjective,anentityshoulduseeitherofthefollowingmethodstoestimatethetransactionprice,dependingonwhichmethodbetterpredictstheamountofconsiderationtowhichtheentitywillbeentitled:

• Theexpectedvalue(i.e.,probability-weightedamount).

• Thesinglemostlikelyamount.(55)

Anentityshouldadjustthepromisedamountofconsiderationtoreflectthetimevalueofmoneyifthecontractincludesasignificantfinancingcomponent.TherevisedEDcontainsfactorsforentitiestoconsiderindeterminingwhethertheeffectoffinancingissignificanttothecontract.Asapracticalexpedient,anentityshouldnotassesswhetheracontracthasasignificantfinancingcomponentifthe“periodbetweenpaymentbythecustomer[and]thetransferofthepromisedgoodsorservicestothecustomer[is]oneyearorless.”(58–62)

TherevisedEDmayrepresentasignificantchangefromcurrentpracticeforextendedpaymentterms.Thatis,extendedpaymenttermsmay(1)beindicatorsofasignificantfinancingcomponenttothecontract,(2)affectthecalculationoftheexpectedvalueormostlikelyamount,or(3)changetheuncertaintyregardingcollectibility(discussedinthenextsection).

Thisstepintheproposedmodelsimplycalculatestheamountofrevenuethatisexpectedtobereceivedfromthecontract.Whilemuchoftheguidanceinthesubheadingsunderthisstepmayaffectthetransactionpricecalculation,thetopicsinthesesubheadingsmayalsoaffecttheamountthattheentityisreasonablyassuredtobeentitledtointhedeterminationoftheamountofrevenuetoberecognized(seeStep5below).

Vendor’sFeeIsFixedorDeterminableandCollectabilityIsProbable

UnderASC985-605,theevaluationofcollectibilityfocusesbothonwhetherthecustomerhastheintentandabilitytopay(i.e.,creditworthiness)andonwhetherthefeeisdeemedfixedordeterminable.

TherevisedEDdoesnotincludeaspecificrecognitionthresholdrequiringthatcollectibilitybeprobable.Rather,implicitinthe“commercialsubstance”criterionforwhenacontractexistsisanotionthatrequiresareasonableexpectationofcollectability.(BC168–BC170)

Initialandsubsequentadjustmentsforcollectibility(i.e.,acustomer’screditriskorbad-debtexpense)areshownasareductionofrevenueinaseparatelineitem(i.e.,contrarevenuebelowgrossrevenue)andaremeasuredinaccordancewithASC310(69).

Somecouldinterpretthethresholdsof“collectibilityisprobable”and“reasonableexpectationofcollectibility”asbeingdifferent.Incertaincircumstances,thisdifferencecouldaffectthetimingandmeasurementofrevenuerecognition.Thepresentationofcollectibilityadjustmentsinaseparatelineitemisachangefromthecurrentpresentationrequirements.SeeadditionaldiscussioninPersuasiveEvidenceofanArrangementExistsabove.

22

ASC 985-605 Revised ED Likely Impact

Price-ProtectionClauses

Ifavendoroffersacustomeraprice-protectionclauseandcannotreasonablyestimatefuturepricechanges,orifthevendor’sabilitytomaintainitspriceisuncertain,thefeewouldnotbefixedanddeterminableandrevenueshouldbedeferreduntilthevendor’sliabilityundertheprice-protectionclausecanbereasonablyestimated(providedthatallotherrequirementsforrevenuerecognitionaremet).

Anentity’sobjectivewhendeterminingthetransactionpriceistoestimatethetotalamountofconsiderationtowhichtheentityexpectstobeentitledunderthecontract.Tomeetthatobjective,anentityshoulduseeitherofthefollowingmethodstoestimatethetransactionprice,dependingonwhichmethodbetterpredictstheamountofconsiderationtowhichtheentitywillbeentitled:

• Theexpectedvalue(i.e.,probability-weightedamount).

• Thesinglemostlikelyamount.(55)

Anentitymustrecognizerevenuefromsatisfyingaperformanceobligationintheamounttowhichtheentityisreasonablyassuredtobeentitled.(81)(SeeStep5belowforadditionaldiscussionofconstrainingrecognizedrevenuetotheamountthatisreasonablyassured.)

Futurepricechangeswouldbeincludedintheentity’sestimateofthetransactionprice.Thisestimatewouldbeupdatedineachreportingperiodandwouldaffecttheamountofrevenuerecognized.However,thecumulativeamountrecognizedwouldbelimitedtotheamountthatisreasonablyassured(seeStep5belowforadditionaldiscussion).Unlikecurrentpractice,whichcouldrequiredeferraloftheentireamount,therevisedEDmayonlyrequiredeferralforalesseramount(i.e.,theamountthatisnotreasonablyassured).

CustomerCancellationPrivilegesandForfeitureorRefundClauses

Arrangementswithcustomercancellationprivilegesdonotmeetthefixedordeterminablefeerecognitioncriteriauntilthecancellationprivilegeslapse.Whenthecancellationprivilegesexpireratablyoverthelicenseperiod,thefeesbecomedeterminableandrevenueisrecognizedratablyoverthelicenseperiodastheprivilegeslapse.(ASC985-605-25-37)

Noportionofthefee(includingamountsotherwiseallocatedtodeliveredelements)meetsthecollectibilitycriterioniftheportionofthefeeallocabletodeliveredelementsissubjecttoforfeiture,refund,orotherconcessionifanyoftheundeliveredelementsarenotdelivered.

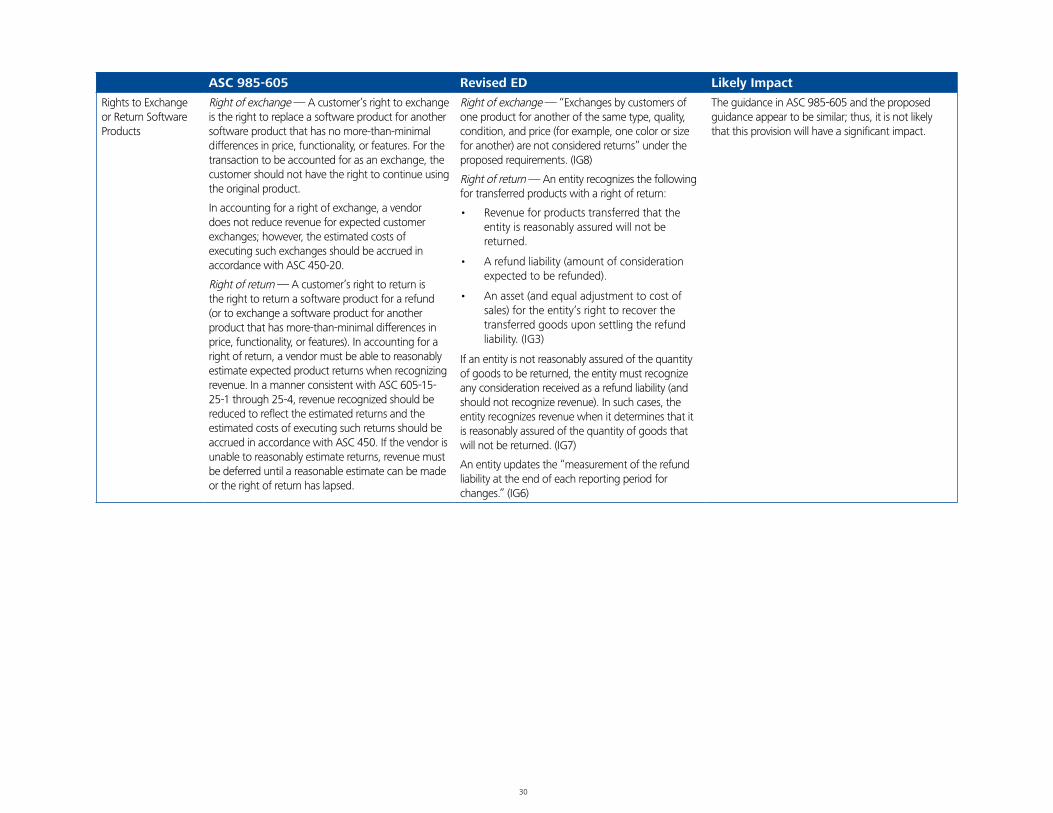

Customercancellationprivilegesandforfeitureorrefundclausesareaccountedforasarightofreturn.

Whenarightofreturnexists,anentityrecognizes(1)revenueforgoodsorservicesthathavebeentransferredtothecustomerandwhosereturnisnotreasonablyassured,(2)arefundliability,and(3)(ifapplicable)anasset(includinganadjustmenttocostofsales)fortherighttorecoverreturnedgoods.Ifanentityisnotreasonablyassuredoftheamountthatwillberefunded,revenueshouldnotberecognizeduntilsuchanamountisreasonablyassured(whichmaynotbeuntiltherightofreturnexpires).(IG2–IG9)

UndertherevisedED,whenanentityisreasonablyassuredtobeentitledtoconsiderationbeforetheexpirationofthecancellation,forfeiture,orrefundperiod,revenuemayberecognizedearlierthanitisundercurrentpractice.Thatis,revenuefromcontractsthatanentitydoesnotexpecttobecanceledmayberecognizedwhentheperformanceobligationsaresatisfied.

23

ASC 985-605 Revised ED Likely Impact

FiscalFundingClauses

Afiscalfundingclausewithacustomerotherthanagovernmentalunitthatisrequiredtoincludesuchaclausecreatesacontingencythatprecludesrevenuerecognitionuntiltherequirementsoftheclauseandallotherprovisionshavebeensatisfied.

Anentity’sobjectivewhendeterminingthetransactionpriceistoestimatethetotalamountofconsiderationtowhichtheentityexpectstobeentitledunderthecontract.Tomeetthatobjective,anentityshoulduseeitherofthefollowingmethodstoestimatethetransactionprice,dependingonwhichmethodbetterpredictstheamountofconsiderationtowhichtheentitywillbeentitled:

• Theexpectedvalue(i.e.,probability-weightedamount).

• Thesinglemostlikelyamount.(55)

Anentitymustrecognizerevenuefromsatisfyingaperformanceobligationintheamounttowhichtheentityisreasonablyassuredtobeentitled.(81)(SeeStep5belowforadditionaldiscussionofconstrainingrecognizedrevenuetotheamountthatisreasonablyassured.)

UndertherevisedED,whenanentityisreasonablyassuredtobeentitledtoconsiderationbeforetheresolutionofthecontingencycreatedbythefiscalfundingclause,revenuemayberecognizedearlierthanitisundercurrentpractice.Thatis,revenueintheamountthatanentityisreasonablyassuredwillnotbecanceledbythecustomerasaresultofthefiscalfundingclausemayberecognizedwhentheperformanceobligationsaresatisfied.

DeterminingtheamountthatisreasonablyassuredinaccordancewiththerevisedEDmayrequiresignificantjudgment.

Discounts Avendormayofferacustomerarighttoapricingdiscountonafuturepurchaseofaproductorservice.Ifthisdiscountismorethaninsignificant,therighttoitisconsideredanelementinthearrangement.(ASC985-605-15-3(d))

The“optiontoacquireadditionalgoodsorservicesatadiscount[representsa]performanceobligation[ifit]providesamaterialrighttothecustomer”thatwouldnototherwisehavebeenreceived.(IG20andIG21)

“Ifacustomerhastheoptiontoacquireanadditionalgoodorserviceataprice”thatiswithintherangeofpricestypicallychargedforthosegoodsorservices,“thatoptiondoesnotprovidethecustomerwithamaterialrighteveniftheoptioncanbeexercisedonlybecause[a]previouscontract”wasenteredinto.The“entityhasmerelymadeamarketingoffer.”(IG22)

TheguidanceinASC985-605andtherevisedEDappearsimilar;thus,itisnotlikelythattheproposedprovisionwillhaveasignificantimpact.

24

ASC 985-605 Revised ED Likely Impact

Fixed-FeeArrangementsBasedonaPriceperCopy

Whenafixed-feearrangementdoesnotspecifythemaximumnumberofcopiesallowed,theallocationofthearrangementfeetotheproductsisnotpossiblebecauseitdependsonthenumberofcopiesultimatelymadeofeachproduct.Revenueisrecognizedascopiesaredelivered.However,allunrecognizedrevenueinthearrangementisrecognizedwhenthevendorisnotobligatedtodeliveradditionalproductsandeither(1)deliveryofallproductsiscompleteor(2)totalrevenueresultingfromthecopiesproducedequalsthearrangement’sfixedfee.

If“anentitygrantsacustomertheoptiontoacquireadditionalgoodsorservices,thatoptiongivesrisetoaseparateperformanceobligationinthecontractonlyiftheoptionprovidesamaterialrighttothecustomerthatitwouldnotreceivewithoutenteringintothatcontract....Iftheoptionprovidesamaterialright,...thecustomerineffectpaystheentityinadvanceforfuturegoodsorservicesandtheentityrecognizesrevenuewhenthosefuturegoodsorservicesaretransferredorwhentheoptionexpires.”(IG20andIG21)

Regardlessofwhetherthearrangementspecifiesthemaximumnumberofcopiesallowed,theentitywouldallocatethefixedconsiderationamongtheseparateperformanceobligations(i.e.,expectednumberofcopiestobetransferredtothecustomeroverthelifeofthearrangement)andwouldrecognizerevenuewheneachcopyistransferredinamannerthatbestdepictsthetransferofcontrol.However,theentitywouldneedtoreevaluateitsperformanceinrelationtothenumberofcopiesexpectedtobedeliveredwhenitismeasuringitsperformancetodateineachperiod.

Therighttoreproduceorobtaincopiesofsoftwareproductsataspecifiedpricepercopywouldbeconsideredacustomeroptionforadditionalgoodsorservices.

Iftheright/optiontoreproduceorobtaincopiesofsoftwareproductswouldprovidethecustomerwithamaterialrightthatthecustomerwouldnotreceivewithoutenteringintothearrangement,eachadditionalcopyofthesoftwarewouldbeconsideredaseparateperformanceobligation.

Regardlessofwhetherthearrangementspecifiesthemaximumnumberofcopiesallowed,theentitywouldallocatethefixedfeeortransactionpriceamongtheseparateperformanceobligations(i.e.,expectednumberofcopiestobetransferredtothecustomeroverthelifeofthecontract)andwouldrecognizerevenuewhencontrolforeachperformanceobligationistransferred.

Platform-TransferRights

Forendusers,dependingonthetermsofthearrangement,platform-transferrightsshouldbeclassifiedasareturn,asanexchange(ifitisforthesameproductanddoesnotincreasethenumberofcopiesorconcurrentusersunderthelicenseagreement),orasanadditionalsoftwareproduct(ifthetermsallowthecustomertocontinueusingapreviouslydeliveredsoftwareproductinadditiontothesoftwarerelatedtothenewplatform).

Therearenospecificrequirementsforplatform-transferrights.Anentityshouldcloselyevaluatethetermsofthecontractandshoulddeterminewhetherthetransferrightsrepresentareturn,anexchange,oranadditionalsoftwareproduct.SeeRightstoExchangeorReturnSoftwareProductsinStep5belowandAdditionalSoftwareProductinStep2aboveforguidanceoneachtypeofcontract.

SeediscussioninStep5on“RightstoExchangeorReturnSoftwareProducts”andStep2on“AdditionalSoftwareProduct”forguidanceoneachtypeofcontract.

25

ASC 985-605 Revised ED Likely Impact

STEP 4: ALLOCATE THE TRANSACTION PRICE TO THE SEPARATE PERFORMANCE OBLIGATIONS IN THE CONTRACT

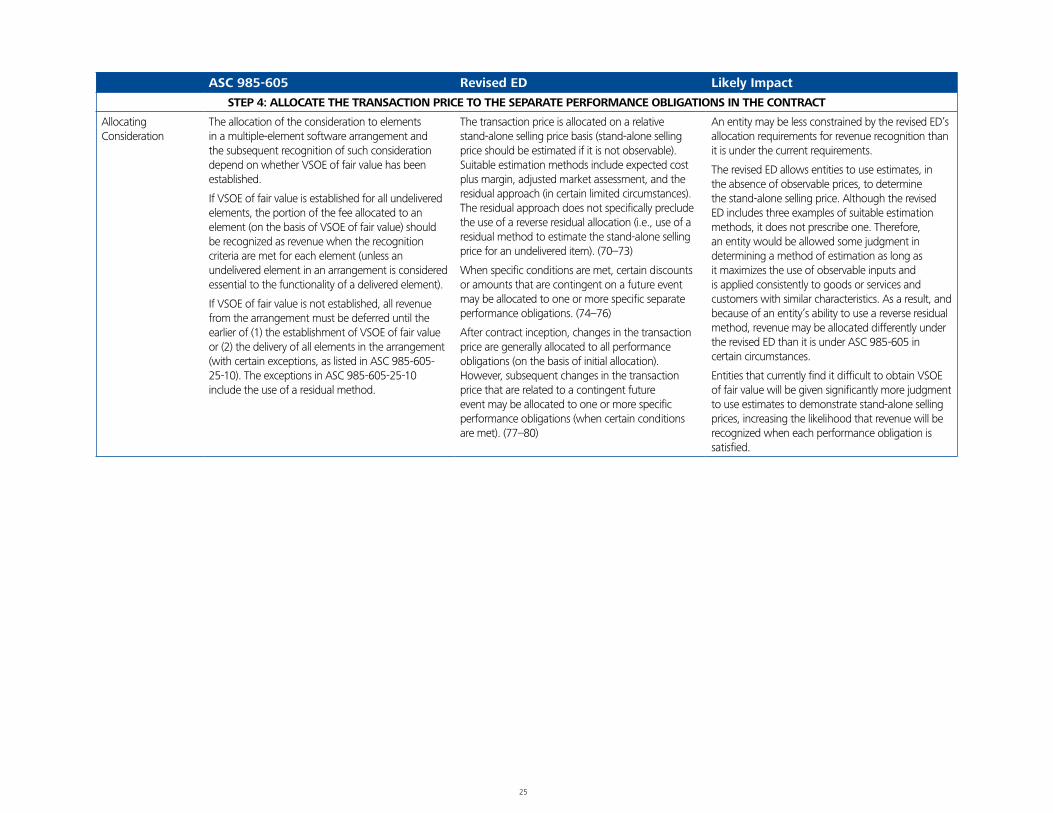

AllocatingConsideration

Theallocationoftheconsiderationtoelementsinamultiple-elementsoftwarearrangementandthesubsequentrecognitionofsuchconsiderationdependonwhetherVSOEoffairvaluehasbeenestablished.

IfVSOEoffairvalueisestablishedforallundeliveredelements,theportionofthefeeallocatedtoanelement(onthebasisofVSOEoffairvalue)shouldberecognizedasrevenuewhentherecognitioncriteriaaremetforeachelement(unlessanundeliveredelementinanarrangementisconsideredessentialtothefunctionalityofadeliveredelement).

IfVSOEoffairvalueisnotestablished,allrevenuefromthearrangementmustbedeferreduntiltheearlierof(1)theestablishmentofVSOEoffairvalueor(2)thedeliveryofallelementsinthearrangement(withcertainexceptions,aslistedinASC985-605-25-10).TheexceptionsinASC985-605-25-10includetheuseofaresidualmethod.

Thetransactionpriceisallocatedonarelativestand-alonesellingpricebasis(stand-alonesellingpriceshouldbeestimatedifitisnotobservable).Suitableestimationmethodsincludeexpectedcostplusmargin,adjustedmarketassessment,andtheresidualapproach(incertainlimitedcircumstances).Theresidualapproachdoesnotspecificallyprecludetheuseofareverseresidualallocation(i.e.,useofaresidualmethodtoestimatethestand-alonesellingpriceforanundelivereditem).(70–73)

Whenspecificconditionsaremet,certaindiscountsoramountsthatarecontingentonafutureeventmaybeallocatedtooneormorespecificseparateperformanceobligations.(74–76)

Aftercontractinception,changesinthetransactionpricearegenerallyallocatedtoallperformanceobligations(onthebasisofinitialallocation).However,subsequentchangesinthetransactionpricethatarerelatedtoacontingentfutureeventmaybeallocatedtooneormorespecificperformanceobligations(whencertainconditionsaremet).(77–80)

AnentitymaybelessconstrainedbytherevisedED’sallocationrequirementsforrevenuerecognitionthanitisunderthecurrentrequirements.

TherevisedEDallowsentitiestouseestimates,intheabsenceofobservableprices,todeterminethestand-alonesellingprice.AlthoughtherevisedEDincludesthreeexamplesofsuitableestimationmethods,itdoesnotprescribeone.Therefore,anentitywouldbeallowedsomejudgmentindeterminingamethodofestimationaslongasitmaximizestheuseofobservableinputsandisappliedconsistentlytogoodsorservicesandcustomerswithsimilarcharacteristics.Asaresult,andbecauseofanentity’sabilitytouseareverseresidualmethod,revenuemaybeallocateddifferentlyundertherevisedEDthanitisunderASC985-605incertaincircumstances.

EntitiesthatcurrentlyfinditdifficulttoobtainVSOEoffairvaluewillbegivensignificantlymorejudgmenttouseestimatestodemonstratestand-alonesellingprices,increasingthelikelihoodthatrevenuewillberecognizedwheneachperformanceobligationissatisfied.

26

ASC 985-605 Revised ED Likely Impact

STEP 5: RECOGNIZE REVENUE WHEN (OR AS) THE ENTITY SATISFIES A PERFORMANCE OBLIGATION

DeliveryHasOccurred

ThesecondcriterioninASC985-605-25-3forrevenuerecognitionisdelivery.Theprincipleofnotrecognizingrevenuebeforedeliveryappliesregardlessofwhetherthecustomerisauserorreseller.Exceptforarrangementsinwhichthefeeisafunctionofthenumberofcopies,deliveryisconsideredtohaveoccurreduponthetransferoftheproductmasteror,iftheproductmasterisnottobedelivered,uponthetransferofthefirstcopy.Forsoftwarethatisdeliveredelectronically,thedeliverycriterioninthatparagraphisconsideredtohavebeenmetwheneitherofthefollowinghasoccurred:

• Thecustomerhastakenpossessionofthesoftwareviaadownload(i.e.,whenthecustomertakespossessionoftheelectronicdataonitshardware).

• Thecustomerhasbeenprovidedwithaccesscodesthatallowthecustomertotakeimmediatepossessionofthesoftwareonitshardwarepursuanttoanagreementorpurchaseorderforthesoftware.

Anentitysatisfiesaperformanceobligationwhencontrolofthegoodorserviceunderlyingtheobligationhasbeentransferredtothecustomer.Controlofagoodorservicecanbetransferredtoacustomer,andhenceanentitycansatisfyaperformanceobligation,atapointintimeorovertime.

Anentitysatisfiesaperformanceobligationovertimeifeitherofthefollowingoccurs:

• “Theentity’sperformancecreatesorenhancesanasset...thatthecustomercontrolsastheassetiscreatedorenhanced.”

• “Theentity’sperformancedoesnotcreateanassetwithanalternativeusetotheentity”andatleastoneofthefollowingismet:

o “Thecustomersimultaneouslyreceivesandconsumesthebenefitsoftheentity’sperformanceas[it]performs.”

o “Anotherentitywouldnotneedtosubstantiallyreperformthework[performed]todateifthatotherentityweretofulfilltheremainingobligationtothecustomer.”

o “Theentityhasarighttopaymentforperformancecompletedtodateand[isexpected]tofulfillthecontract.”(35)

Revenueisrecognizedforseparateperformanceobligationsthataresatisfiedovertimebymeasuringtheentity’s“progresstowardcompletesatisfactionof[the]performanceobligation”inamannerthatbestdepictsthetransferofgoodsorservicestothecustomer.(38–40)TheproposedASUprovidesspecificguidanceontheuseandapplicationofanoutputmethodandaninputmethodformeasuringprogresstowardcompletion.(41–46)Theamountrecognizedislimitedtotheamounttowhichtheentityisreasonablyassuredtobeentitled.(81)

Thecriteriaforwhenacustomerobtainscontrolofagoodorserviceatapointintimearegenerallyconsistentwiththetypesofitemsconsideredintheassessmentofwhetherandwhendeliveryhasoccurred.

Undertheproposedmodel,serviceswillgenerallybeunbundledandrecognizedovertimeastheserviceobligationsaresatisfied(assumingthattheseparationcriteriainStep2aremet).

Seeadditionaldiscussionbelowforguidanceonaccountingforagoodorservicesatisfiedovertime.

27

ASC 985-605 Revised ED Likely Impact

DeliveryHasOccurred(continued)

Ifaperformanceobligationdoesnotmeetthecriteriaforsatisfactionovertime,itissatisfiedatapointintime.TheproposedASUstatesthatindicatorsthatcontrolofanassethasbeentransferredtoacustomeratapointintimeinclude,butarenotlimitedto,thefollowing:

• “Theentityhasapresentrighttopayment.”

• “Thecustomerhaslegaltitle.”

• “Theentityhastransferredphysicalpossession.”

• “Thecustomerhasthesignificantrisksandrewardsofownership.”

• “Thecustomerhasacceptedtheasset.”(37)

CustomerAcceptance

Softwarearrangementsoftenincludespecificcustomeracceptanceprovisions;ASC985-605indicatesthatifthecustomer’sacceptanceofthesoftwareisuncertain,revenueshouldnotberecognizeduntilacceptanceoccurs.Further,ifpaymentforthesoftwareistiedtocustomeracceptance,theacceptanceprovisionwouldbepresumedsubstantive.Therefore,providedthatallotherrequirementsforrevenuerecognitionhavebeenmet,revenuerecognitionwouldbeprecludeduntilpaymentismadeordueunlessthatpresumptionisovercome.

Customeracceptanceisoneoftheindicatorsthatanentitymustconsiderindeterminingthepointintimeatwhichcontrolistransferredforagoodorserviceprovidedtoacustomer.(37e)Theeffectoftheacceptanceclausesondeterminingwhetheracustomerhasobtainedcontrolofapromisedgoodorservicedependsonwhetheranentitycanobjectivelydeterminethatagoodorservicehasbeentransferredtothecustomerinaccordancewiththeagreed-uponspecificationsinthecontract.“Ifanentitycanobjectivelydeterminethatcontrolofagoodorservicehasbeentransferredtothecustomerinaccordancewiththeagreed-uponspecifications,”thecustomeracceptanceprovisionswouldnotaffectthedeterminationofcontroltransfer.Ifanentitycannotobjectivelymakethisdetermination,itwouldnotbeabletoconcludethatithasobtainedcontroluntilitreceivesthecustomer’sacceptance.(IG55–IG58)

ItisnotlikelythattheseprovisionsoftherevisedEDwillhaveasignificantimpactsincetheyareconsistentwithcurrentpractice.However,therevisedEDdoesnotincludeapresumptionthatthecustomer’sacceptanceprovisionsaresubstantiveiftheyaretiedtopayment,whichcouldaffectthetimingofrevenuerecognition.

28

ASC 985-605 Revised ED Likely Impact

KeysorAuthorizationCodes

Insoftwarearrangementsinvolvingtheuseofkeys,avendorisnotnecessarilyrequiredtodeliverakeytofulfillitsdeliveryresponsibility.Thesoftwarevendorrecognizesrevenueondeliveryofthesoftwareifallofthefollowingconditionsaremet(providedthatallotherrequirementsforrevenuerecognitioninASC985-605aremet):

• “Thecustomerhaslicensedthesoftwareandthevendorhasdeliveredaversionofthesoftwarethatisfullyfunctionalexceptforthepermanentkeyortheadditionalkeys(ifadditionalkeysareusedtocontrolthereproductionofthesoftware).”

• “Thecustomer’sobligationtopayforthesoftwareandthetermsofpayment,includingthetimingofpayment,arenotcontingentondeliveryofthepermanentkeyoradditionalkeys(ifadditionalkeysareusedtocontrolthereproductionofthesoftware).”

• “Thevendorwillenforceanddoesnothaveahistoryoffailingtoenforceitsrighttocollectpaymentunderthetermsoftheoriginalarrangement.”(ASC985-605-25-28)

Acustomerobtainscontrolofagoodorservicewhenthecustomerhastheabilitytodirecttheuseof,andreceivethebenefitfrom,thegoodorservice.Whenaperformanceobligationdoesnotmeetthecriteriatobesatisfiedovertime,itissatisfiedatapointintime.TheproposedASUstatesthatindicatorsthatcontrolofanassethasbeentransferredtoacustomeratapointintimeinclude,butarenotlimitedto,thefollowing:

• “Theentityhasapresentrighttopayment.”

• “Thecustomerhaslegaltitle.”

• “Theentityhastransferredphysicalpossession.”

• “Thecustomerhasthesignificantrisksandrewardsofownership.”

• “Thecustomerhasacceptedtheasset.”(37)

Inthesecircumstances,anentityneedstoevaluatewhetherthecustomerhastheabilitytodirecttheuseof,andreceivebenefitfrom,thegoodorserviceundertheproposedstandard.Ifthesoftwaredoesnotfunctionwithoutthekeysorcodes,thetreatmentwouldbesimilar.

Anentitywillalsoneedtoevaluatethespecificfactsandcircumstancesassociatedwiththeuseofkeysandhowtheyaffecttheevaluationofwhetherthecustomerhasobtainedcontrolofthegoodorservice.Forexample,ifthekeyisusedsolelytoprotectagainstthecustomer’sfailuretocomplywiththetermsofthecontract,controlmaystillhavebeentransferred;however,ifthekeyisusedtocontroltheuseforatrialperiodorfordemonstrationpurposes,thencontrolmaynothavebeentransferredtothecustomer.

29

ASC 985-605 Revised ED Likely Impact

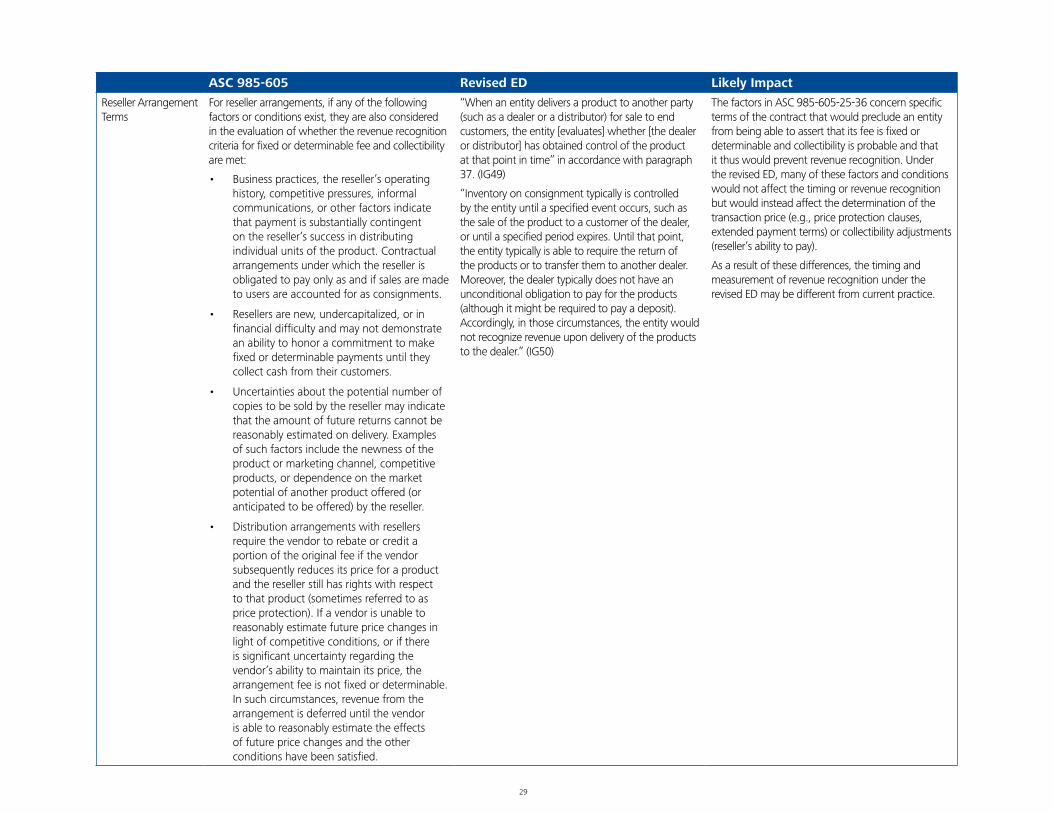

ResellerArrangementTerms