investors’ seminar september 2011. disclaimer this is not advice. please see mark before...

Post on 20-Dec-2015

214 views

TRANSCRIPT

Investors’ Seminar

September 2011

Disclaimer

This is not Advice. Please see Mark before considering any changes. Mark will put any recommendations in writing

The information contained in this presentation has been prepared for general use only and does not take into

account your personal investment objectives, financial situation or particular needs. Before you make any decision

about whether to invest in a financial product, you should obtain and consider the Product Disclosure Statement of

the financial product.

The information provided by HFS has been done so in good faith and has been derived from sources believed to be

accurate at the time of compilation. Changes in circumstances, including unlawful interference and unauthorised

tampering, after the date of publication may impact on the accuracy of the information. Neither HFS d nor any

member of HFS accepts responsibility for any inaccuracy or for investment decisions or any other actions taken by

any person on the basis of the information included. Past performance is not a reliable indicator of future

performance.

Neither HFS nor any member of HFS guarantees the performance of the Funds, the repayment of capital or any

particular rate of return. The performance of any unit trust depends on the performance of its underlying investment

which can fall as well as rise and can result in both capital losses and gains. Consequently, due to market influences,

no assurance can be given that all stated objectives will be achieved.

Investors’ SeminarSeptember 2011

Will I achieve my goals?

Will we achieve our goals?

Realistic Goals

Structure/Strategy (Tax etc)

Super Fund Admin

Asset Mix 1 -Cash/TermDs needed

Asset Mix 2–Growth Section (LHS)

Stock-Picker Selection

The Boxes to Tick

Non – investment Matters

1. Goals – realistic cashflow needs

2. Structure & Strategy

Super & Pensions

Tax & Centrelink Matters

3. Super Fund Admin

SMSFs vs Wholesale/Retail/Industry etc

Investors’ SeminarSeptember 2011

The Current Environment

Governments have high debt levels

Governments have the financial burden of dealing with aging populations (ie pension liabilities)

Globally the Stimulus Funds have not been spent on productive assets or

infrastructure

Households over-leveraged from years of easy credit sourced from rising house prices

The Current Drivers

Fear prevails – affecting both the Market and the Economy

Consumers are restrained – becoming net savers

Inflation vs deflation – less topical now

6 farrelly’s

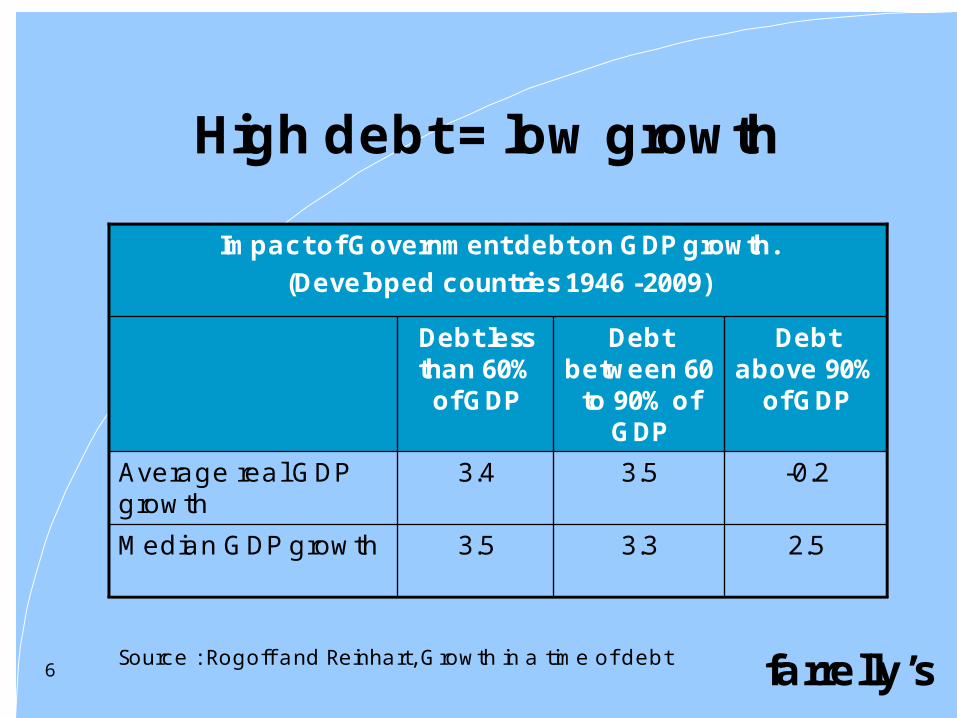

High debt = low growth

Impact of Government debt on GDP growth. (Developed countries 1946 -2009)

2.53.33.5Median GDP growth

-0.23.53.4Average real GDP growth

Debt above 90%

of GDP

Debt between 60 to 90% of

GDP

Debt less than 60% of GDP

Source : Rogoff and Reinhart, Growth in a time of debt

Investors’ SeminarSeptember 2011

Historical Data

Forecasts

Hayden Asset Allocation Model

Specific Investment Selection

Bad case scenarios

Investors’ SeminarSeptember 2011

Historical Data

How far back to go?

Is old “data” relevant in today’s world?

Predictive Data

Theory; Reasoned Rational Approach

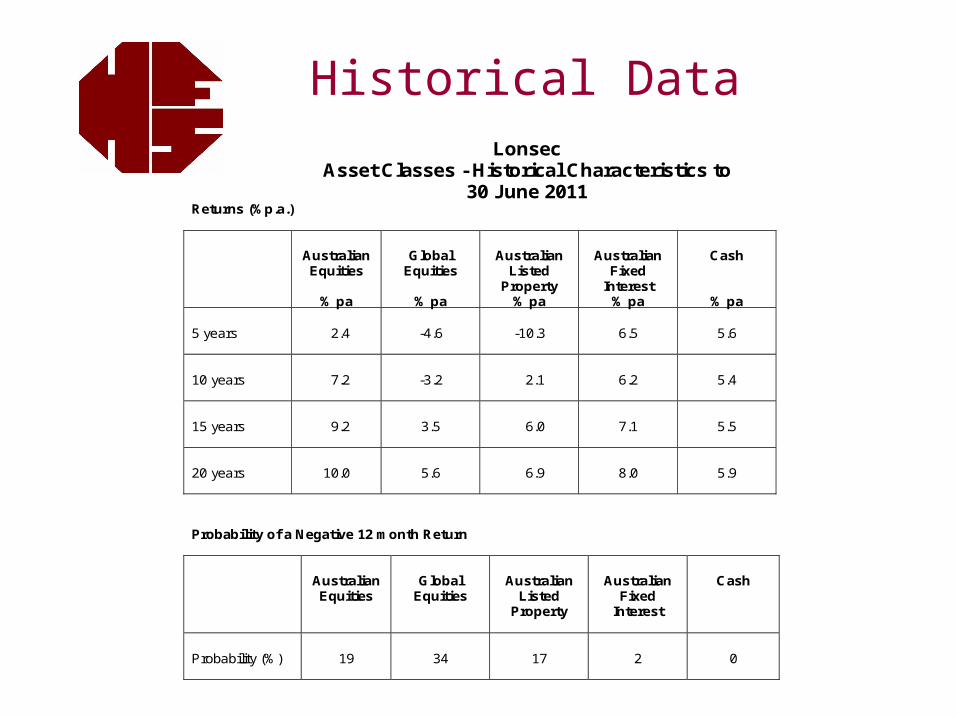

Historical DataLonsec

Asset Classes - Historical Characteristics to 30 June 2011

Returns (%p.a.)

Australian Equities

% pa

Global

Equities

% pa

Australian

Listed Property

% pa

Australian

Fixed Interest

% pa

Cash

% pa 5 years

2.4

-4.6

-10.3

6.5

5.6

10 years

7.2

-3.2

2.1

6.2

5.4

15 years

9.2

3.5

6.0

7.1

5.5

20 years

10.0

5.6

6.9

8.0

5.9

Probability of a Negative 12 month Return

Australian Equities

Global

Equities

Australian

Listed Property

Australian

Fixed Interest

Cash

Probability (%)

19

34

17

2

0

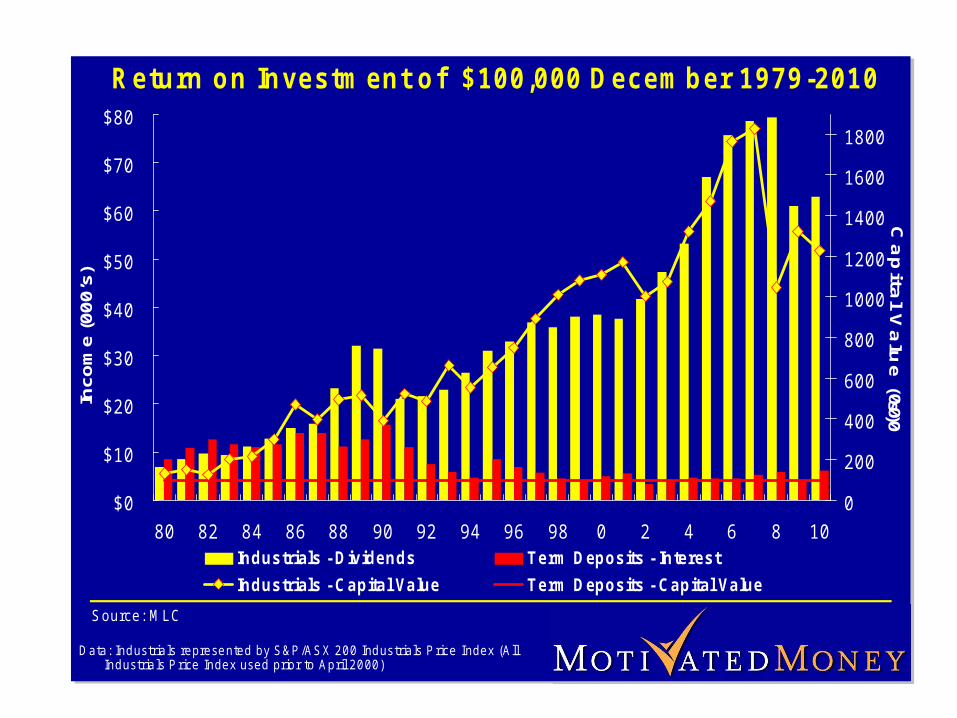

$0

$10

$20

$30

$40

$50

$60

$70

$80

80 82 84 86 88 90 92 94 96 98 0 2 4 6 8 10

0

200

400

600

800

1000

1200

1400

1600

1800

Industrials - D iv idends T erm D eposits - Interest

Industrials - C apita l Value T erm D eposits - Capital Value

R eturn o n In vestm en t o f $100 ,000 D ecem b er 1979 -2010In

com

e (0

00’s

)

S ource : M LC

D ata : Ind ustria ls re prese n ted by S & P /A S X 2 00 Ind us tr ia ls P rice Index (A ll Ind ustria ls P rice Index used prio r to A p ril 20 00 )

$0

$10

$20

$30

$40

$50

$60

$70

$80

80 82 84 86 88 90 92 94 96 98 0 2 4 6 8 10

0

200

400

600

800

1000

1200

1400

1600

1800

Industrials - D iv idends T erm D eposits - Interest

Industrials - C apita l Value T erm D eposits - Capital Value

R eturn o n In vestm en t o f $100 ,000 D ecem b er 1979 -2010In

com

e (0

00’s

)

S ource : M LC

D ata : Ind ustria ls re prese n ted by S & P /A S X 2 00 Ind us tr ia ls P rice Index (A ll Ind ustria ls P rice Index used prio r to A p ril 20 00 )

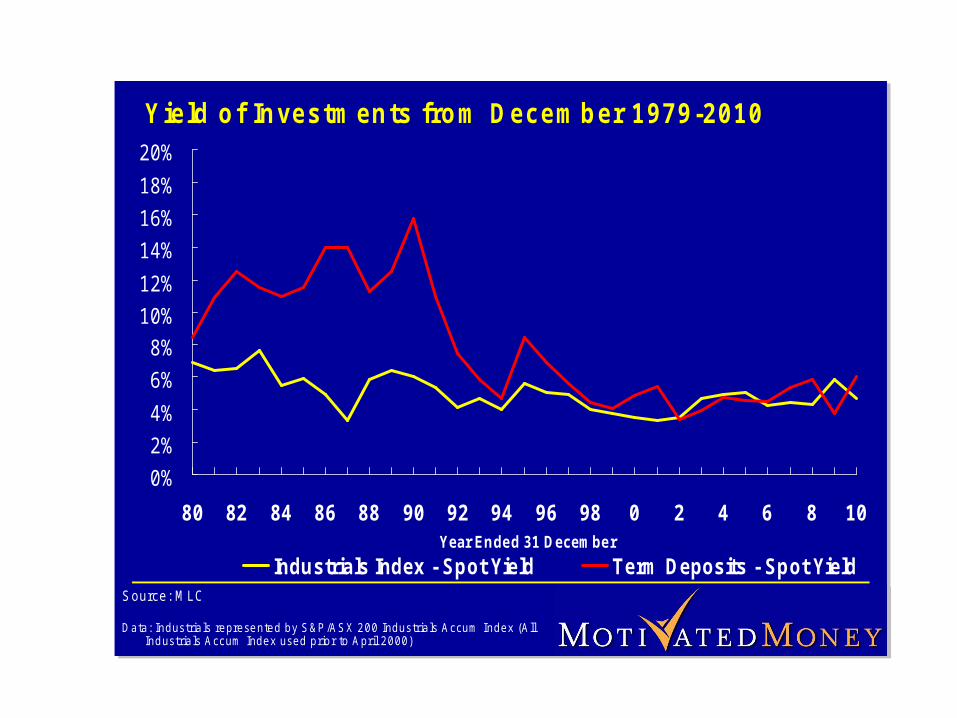

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

80 82 84 86 88 90 92 94 96 98 0 2 4 6 8 10Year Ended 31 December

Industrials Index - Spot Yield Term Deposits - Spot Yield

Y ie ld o f In ve s tm en ts fro m D e ce m b er 1 9 79 -2 01 0

S ourc e : M L C

D a ta : In d us tria ls re pre se n te d b y S & P /A S X 2 0 0 Ind us tr ia ls A ccu m In d e x (A ll In d us tria ls A cc um Ind e x use d p rio r to A pr il 2 0 0 0 )

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

80 82 84 86 88 90 92 94 96 98 0 2 4 6 8 10Year Ended 31 December

Industrials Index - Spot Yield Term Deposits - Spot Yield

Y ie ld o f In ve s tm en ts fro m D e ce m b er 1 9 79 -2 01 0

S ourc e : M L C

D a ta : In d us tria ls re pre se n te d b y S & P /A S X 2 0 0 Ind us tr ia ls A ccu m In d e x (A ll In d us tria ls A cc um Ind e x use d p rio r to A pr il 2 0 0 0 )

TD’s V Shares

Source: RBA, IRESS. Data as at 31 J uly 2011.

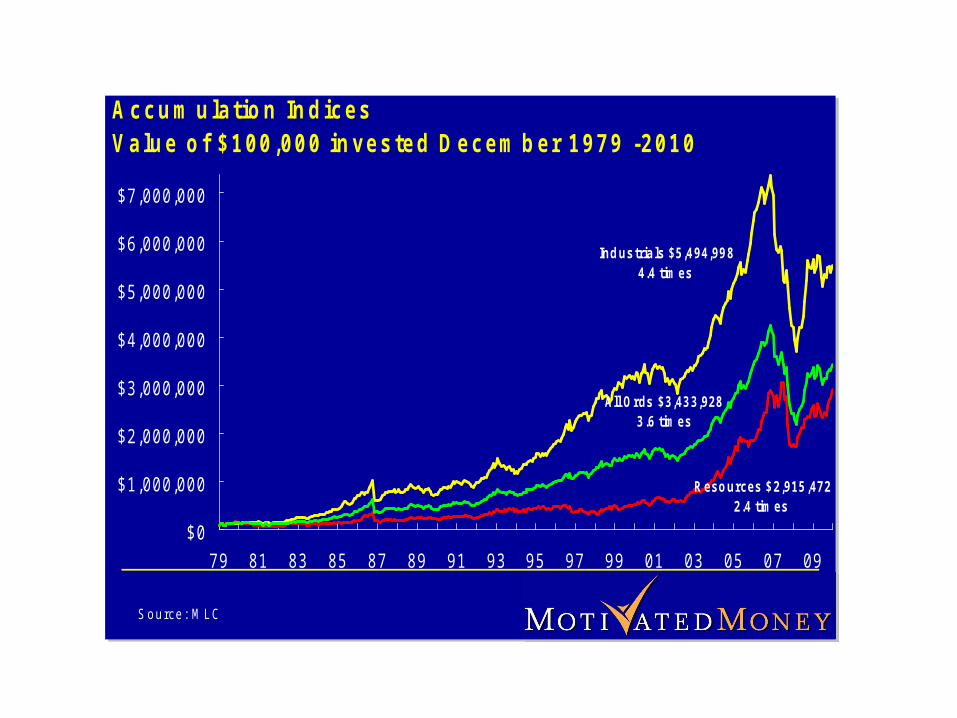

Ind us tria ls $5 ,4 94 ,99 84.4 tim es

R eso urces $ 2 ,915 ,4722.4 tim es

All O rds $3 ,43 3 ,9283 .6 tim es

$ 0

$ 1 ,0 0 0 ,0 0 0

$ 2 ,0 0 0 ,0 0 0

$ 3 ,0 0 0 ,0 0 0

$ 4 ,0 0 0 ,0 0 0

$ 5 ,0 0 0 ,0 0 0

$ 6 ,0 0 0 ,0 0 0

$ 7 ,0 0 0 ,0 0 0

7 9 8 1 8 3 8 5 8 7 8 9 9 1 9 3 9 5 9 7 9 9 0 1 0 3 0 5 0 7 0 9

A c c u m u la t io n In d ic e s V a lu e o f $ 1 0 0 ,0 0 0 in v e s te d D e c e m b e r 1 9 7 9 -2 0 1 0

S o u rc e : M L C

Ind us tria ls $5 ,4 94 ,99 84.4 tim es

R eso urces $ 2 ,915 ,4722.4 tim es

All O rds $3 ,43 3 ,9283 .6 tim es

$ 0

$ 1 ,0 0 0 ,0 0 0

$ 2 ,0 0 0 ,0 0 0

$ 3 ,0 0 0 ,0 0 0

$ 4 ,0 0 0 ,0 0 0

$ 5 ,0 0 0 ,0 0 0

$ 6 ,0 0 0 ,0 0 0

$ 7 ,0 0 0 ,0 0 0

7 9 8 1 8 3 8 5 8 7 8 9 9 1 9 3 9 5 9 7 9 9 0 1 0 3 0 5 0 7 0 9

A c c u m u la t io n In d ic e s V a lu e o f $ 1 0 0 ,0 0 0 in v e s te d D e c e m b e r 1 9 7 9 -2 0 1 0

S o u rc e : M L C

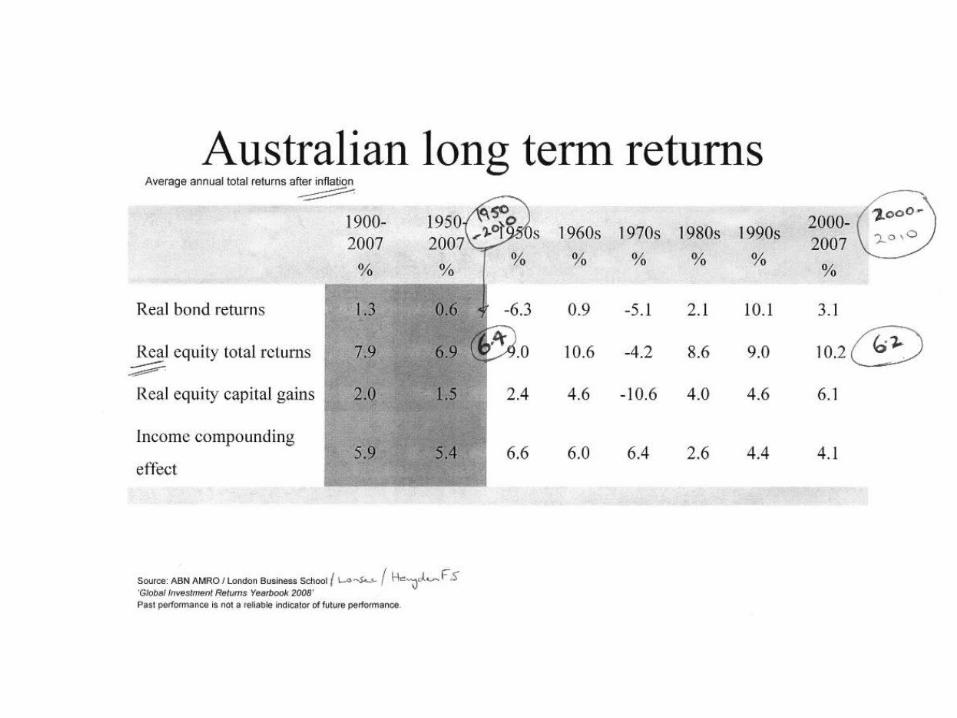

Average annual total returns after inflation

Australian long term returns

4.14.42.66.46.06.65.45.9Income compounding

effect

4.6

9.0

10.1

1990s

%

2.4

9.0

-6.3

1950s

%

1.5

6.9

0.6

1950-2007

%

-10.6

-4.2

-5.1

1970s

%

4.6

10.6

0.9

1960s

%

10.28.67.9Real equity total returns

3.12.11.3Real bond returns

6.14.02.0Real equity capital gains

2000-2007

%

1980s

%

1900-2007

%

Source: ABN AMRO / London Business School :‘Global Investment Returns Yearbook 2008’Past performance is not a reliable indicator of future performance.

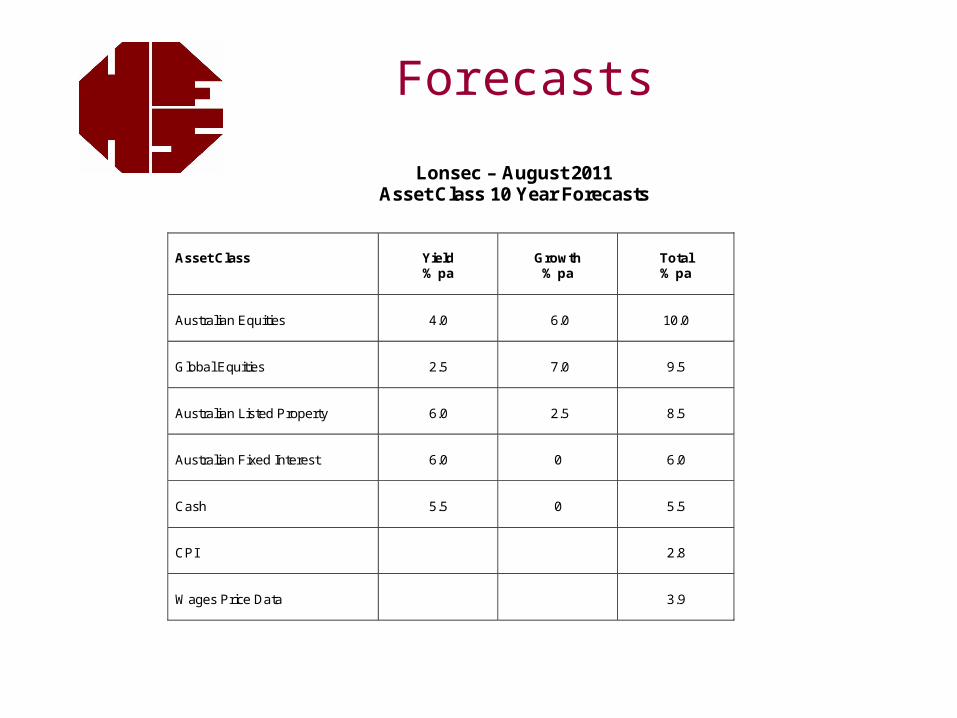

Forecasts

Lonsec – August 2011 Asset Class 10 Year Forecasts

Asset Class

Yield % pa

Growth

% pa

Total % pa

Australian Equities

4.0

6.0

10.0

Global Equities

2.5

7.0

9.5

Australian Listed Property

6.0

2.5

8.5

Australian Fixed Interest

6.0

0

6.0

Cash

5.5

0

5.5

CPI

2.8

Wages Price Data

3.9

farrelly’s17

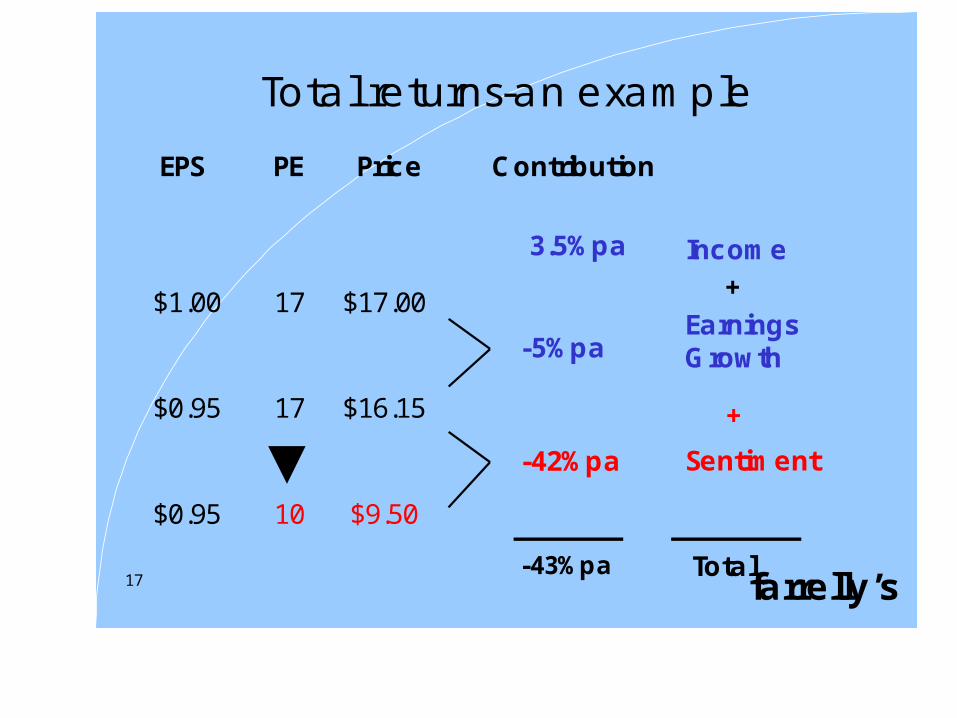

Total returns-an example

3.5%pa

EPS PE Price Contribution

$1.00 17 $17.00

$0.95 17 $16.15

$0.95 10 $9.50

-5%pa

-42%pa

Earnings Growth

Income

Sentiment

Total-43%pa

+

+

fa rre l ly ’ s4 1

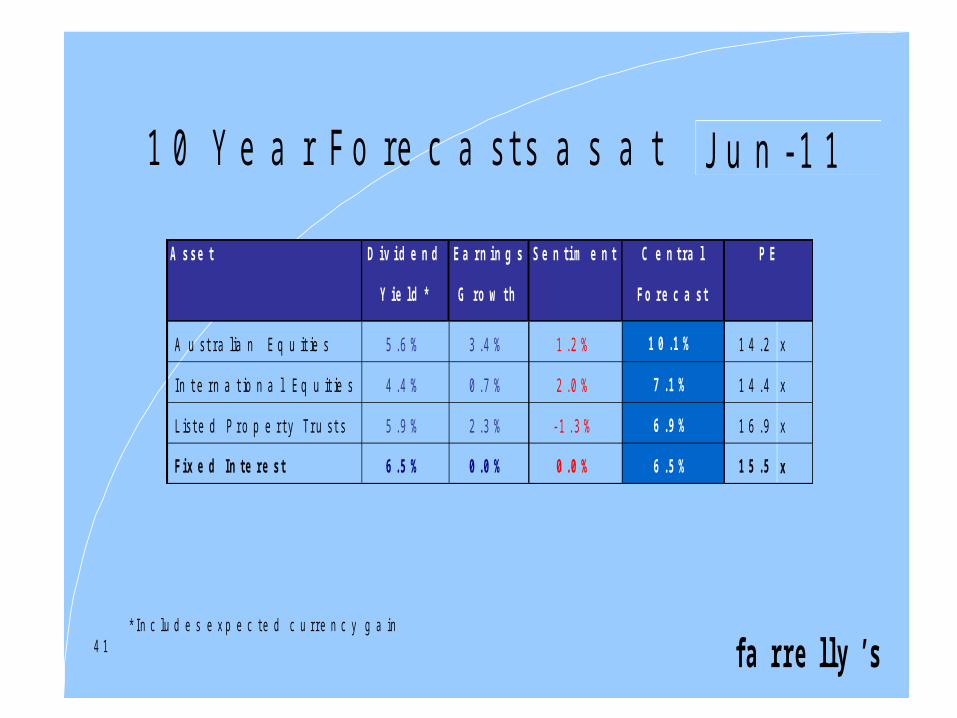

1 0 Y e a r F o r e c a s t s a s a t J u n - 1 1

* I n c lu d e s e x p e c t e d c u r r e n c y g a in

D iv i d e n d E a rn in g s C e n t ra l

Y ie ld * G ro w th Fo re c a s t

A u s t r a lia n E q u it ie s 5 . 6 % 3 . 4 % 1 . 2 % 1 0 .1 % 1 4 . 2 x

I n t e r n a t io n a l E q u it ie s 4 . 4 % 0 . 7 % 2 . 0 % 7 .1 % 1 4 . 4 x

L is t e d P r o p e r t y T r u s t s 5 . 9 % 2 . 3 % - 1 . 3 % 6 .9 % 1 6 . 9 x

F ix e d In te re s t 6 .5 % 0 .0 % 0 .0 % 6 .5 % 1 5 .5 x

A s s e t S e n ti m e n t P E

farrelly’s48

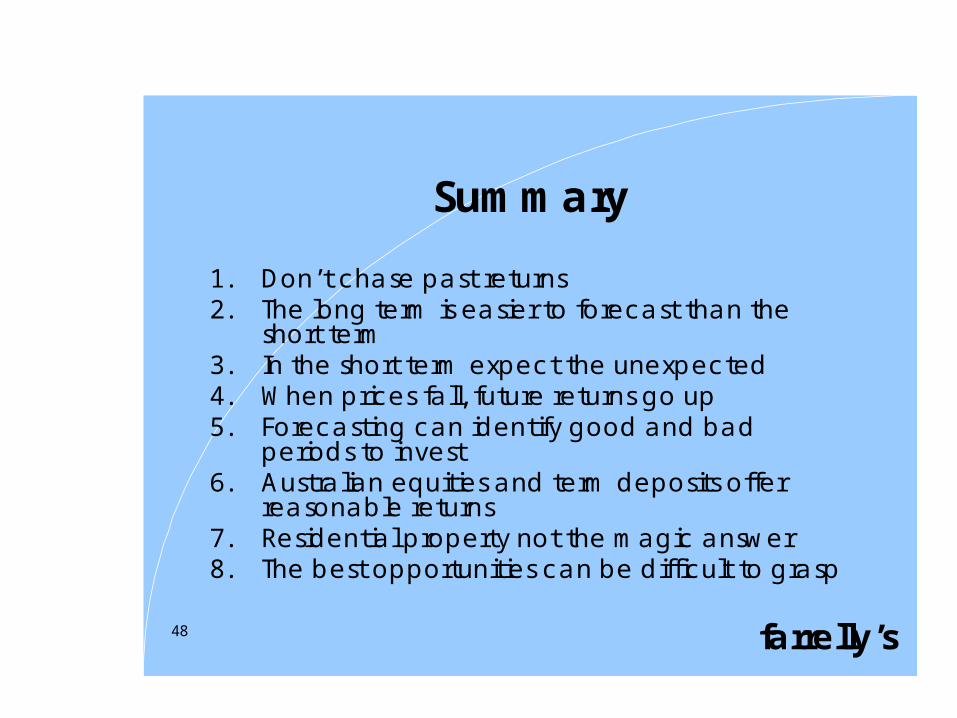

Summary

1. Don’t chase past returns2. The long term is easier to forecast than the

short term3. In the short term expect the unexpected4. When prices fall, future returns go up5. Forecasting can identify good and bad

periods to invest6. Australian equities and term deposits offer

reasonable returns7. Residential property not the magic answer8. The best opportunities can be difficult to grasp

Investors’ SeminarSeptember 2011

Historical Data

Forecasts

Hayden Asset Allocation Model

Specific Investment Selection

Bad case scenarios

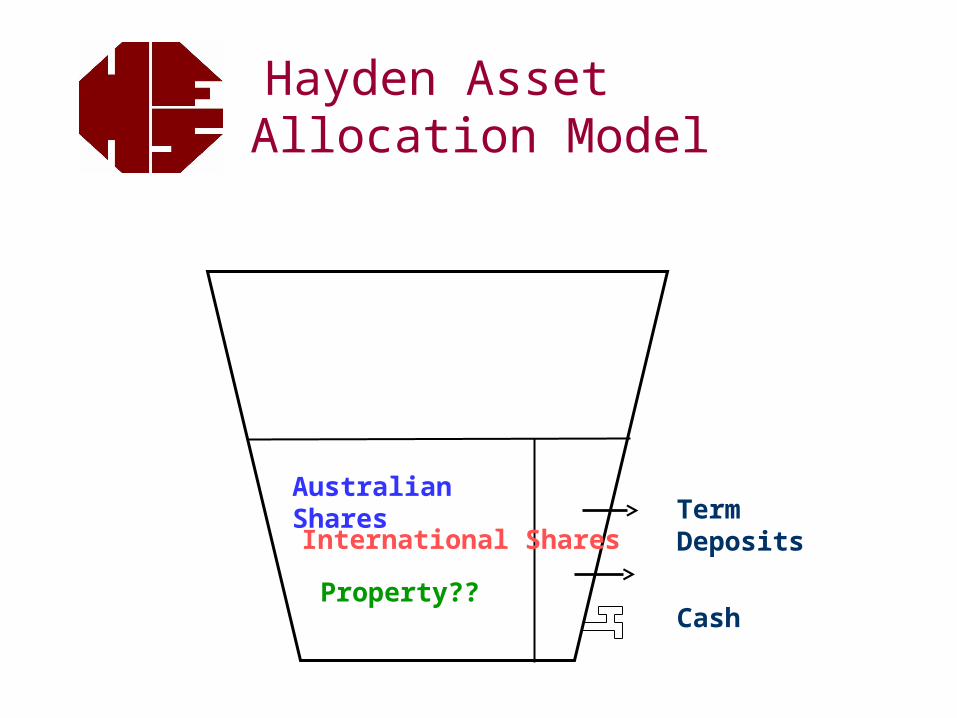

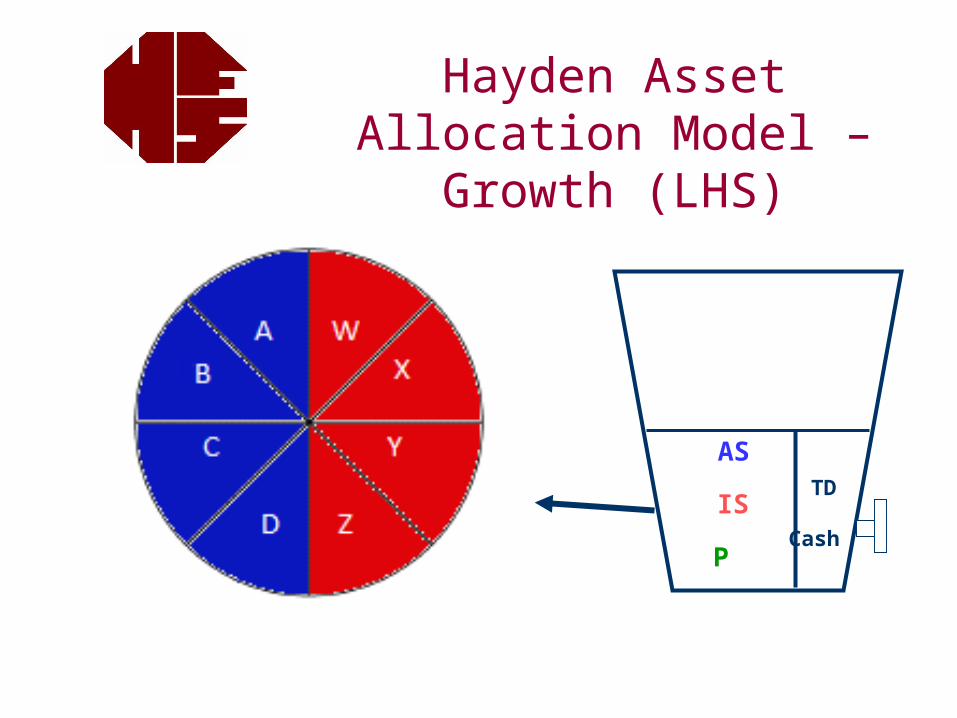

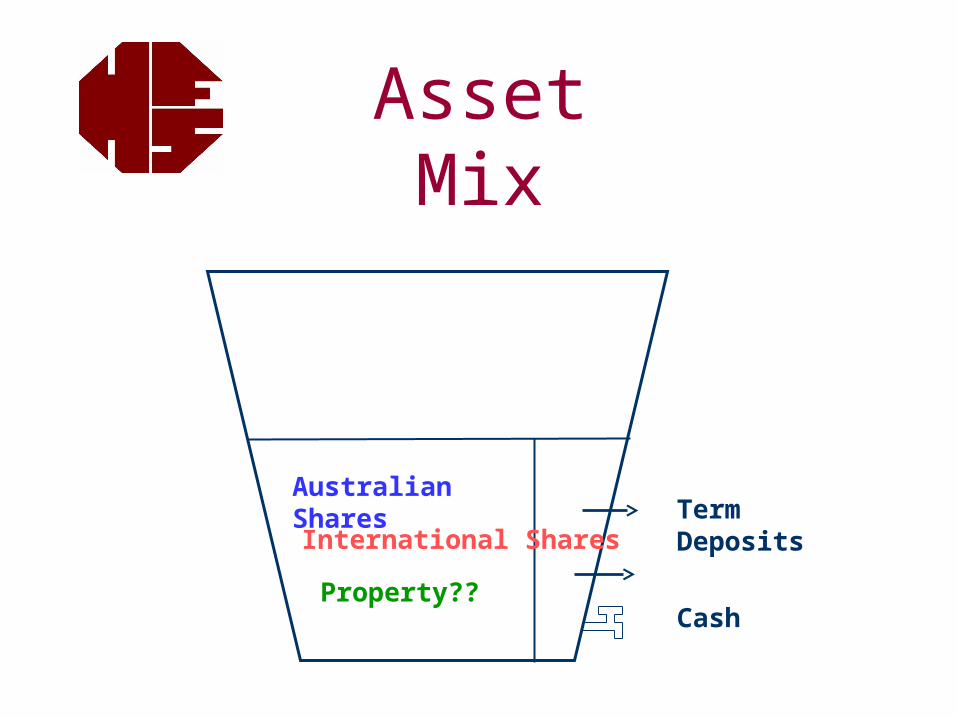

Hayden Asset Allocation Model

Australian SharesInternational Shares

Property??

Term Deposits

Cash

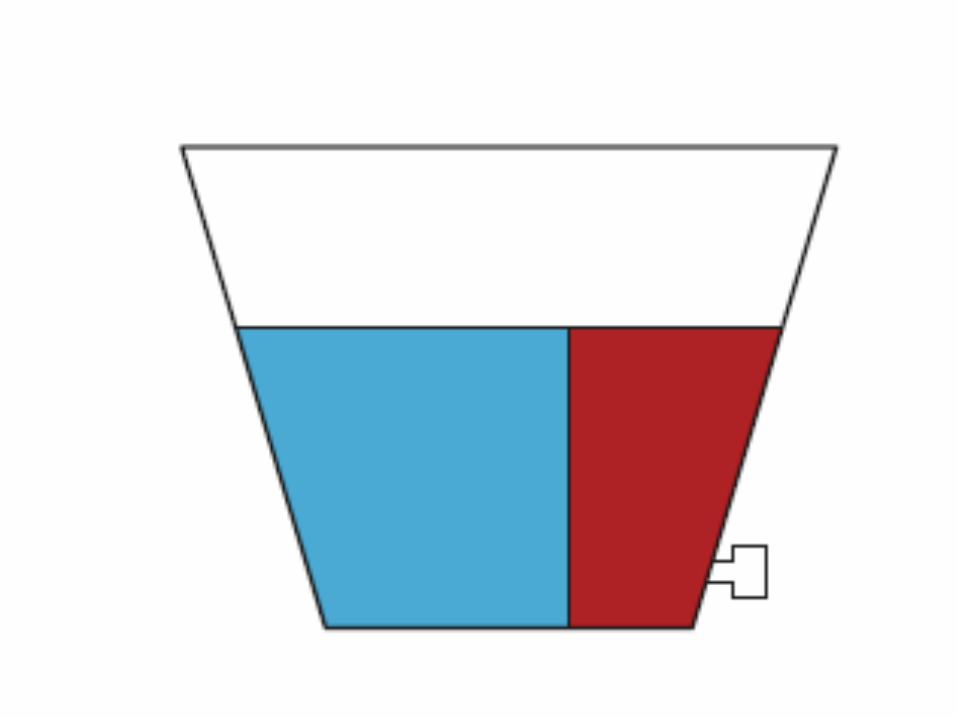

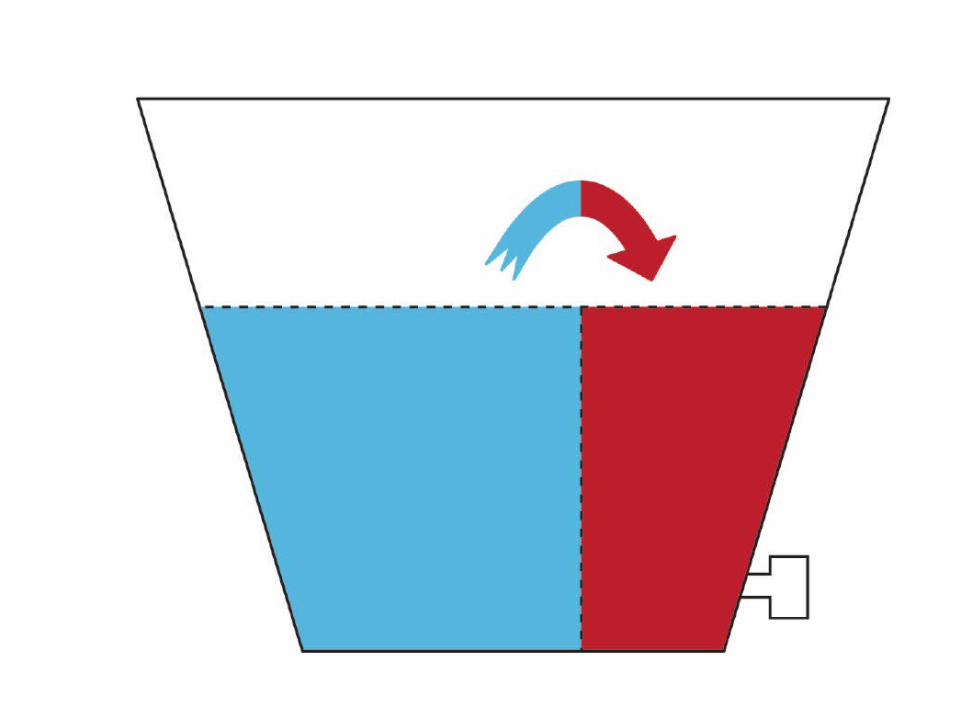

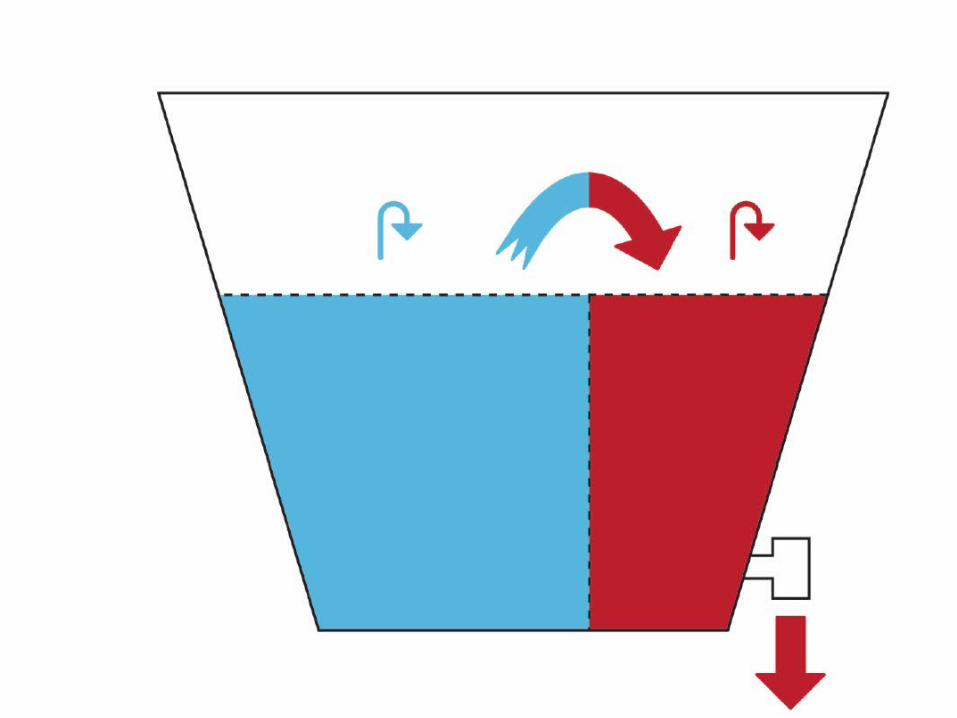

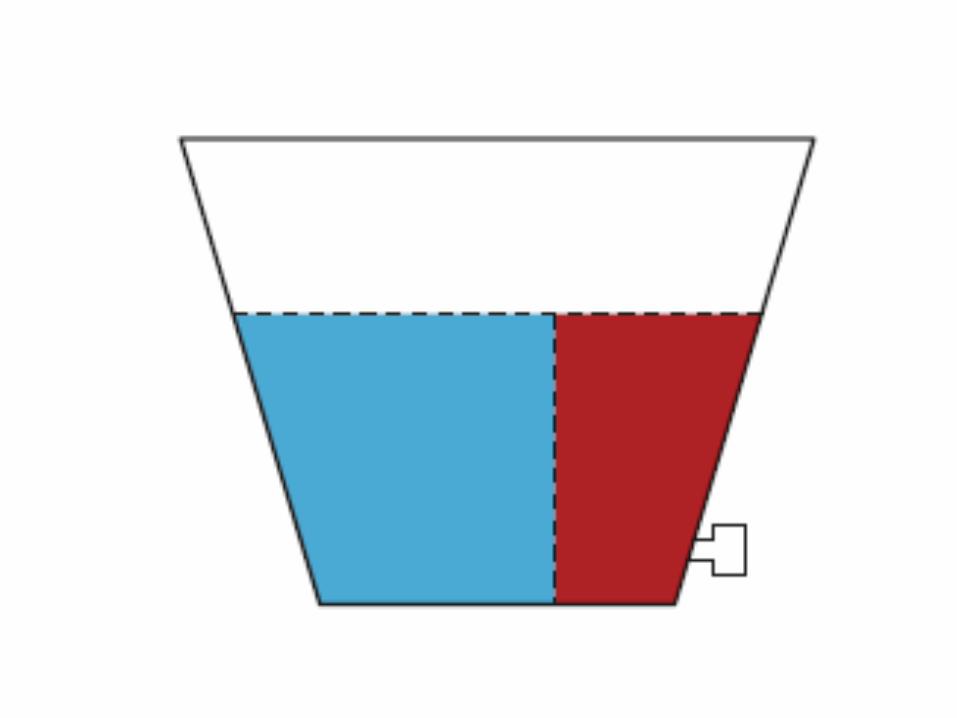

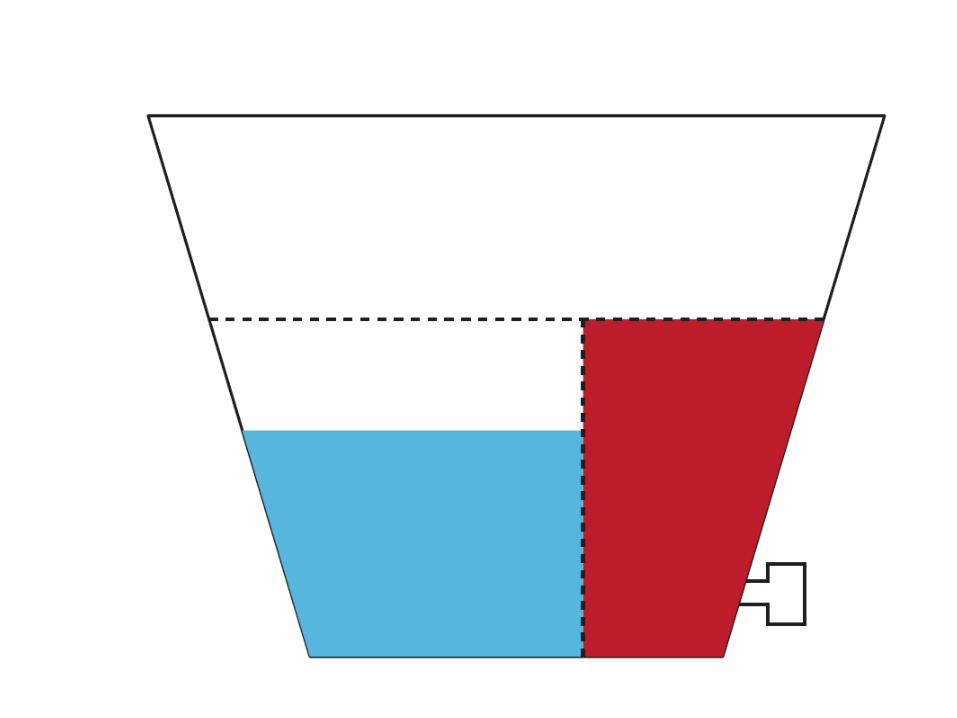

Segmentation Bar

RHS – Cash and Term Deposits

LHS – 10+ Year Focus

Never need to address the best investment for say 2 to 8 years.

Never need to predict the return of Growth assets over the short-term.

We do need dividends etc to replenish the RHS – but regularity is not relevant. It can be zero for 1 or 2 years (most unlikely because the businesses will not exist if they do not make profits).

The Hayden Asset Allocation Model

The Segmentation Bar – ie vertical bar that segregates the short-term RHS and the LHS

RHS - Return of the $ invested at the designated time; has a 0-2 year focus.

CashFlow Needs are the main determinator.

Cash and Term Deposits - this section is structured to be “Consumed”

Asset Mix - Decision 1

The LHS Side of the Bucket. The Goals are:

Main Goal - Long-Term Total Returns – 10 Year Targets

Sub Goal – replenish the Cash

Volatile Returns are not a concern

Income is not a focus – maximising returns is the goal. A business that reinvests is not any less attractive than one that pays out all profit as a dividend.

Asset Mix - Decision 2

Projections

What are the key timeframes:

0-2 years – no projections needed. Cash and Term Deposits cover all goals in this time frame

2-8 years – not necessary to invest in this timeframe if we can have a 10 year focus which incorporates better returns

10+ years – the key goals. Again we use the Tim Farrelly Projections

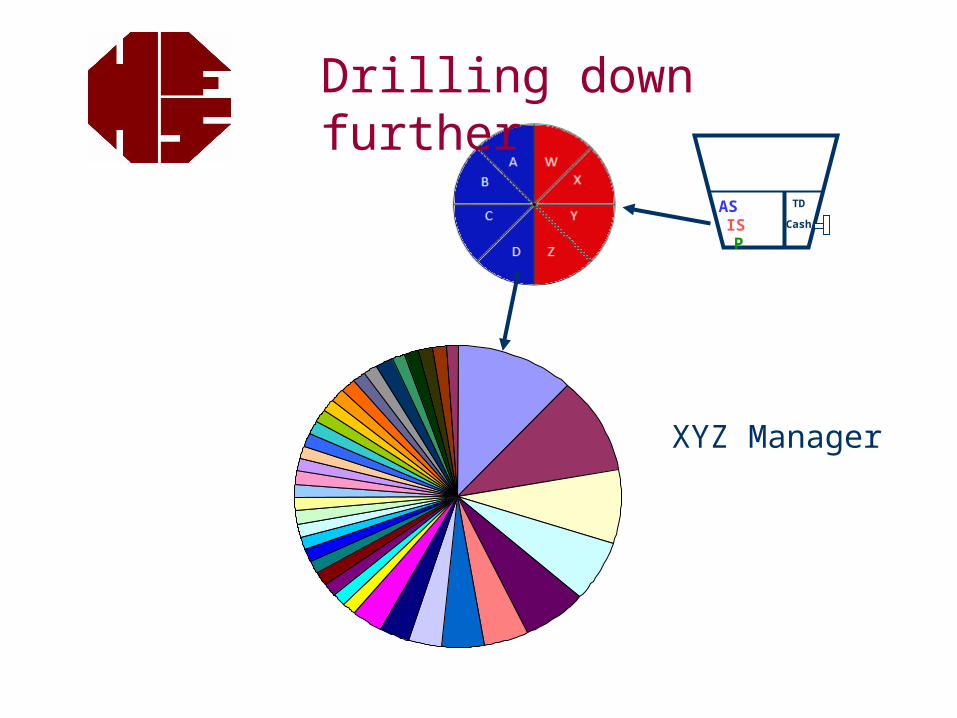

AS

IS

P

TD

Cash

Hayden Asset Allocation Model – Growth (LHS)

Specific Investments for the LHS

Australian/International Shares

We have a 10 year plus time frame so we are sharing in the profits generated by the business – ie either dividends and/or capital growth generated by higher profits

We want a good portfolio and we want it monitored and changed when needed

Best way - contract Specialist Stock-pickers

ASISP

TD

Cash

Drilling down further

XYZ Manager

The three choices:

1. Index Funds …*

2. Choose Your Own Stocks …#

3. Contract a High-Quality Stock-Picker

* 3 is preferred because some businesses better than others- ie either in a better Industry and/or better Management.

# 3 is preferred because some people have specialised skills and resources in finding and then analysing businesses? It is worthwhile contracting these skills.

Is a Stock-Picker Needed?

A quality stock-picker is contracted for

Their selected portfolio of shares and

Their skills in monitoring and changing that portfolio

For each underlying investments we can ask them why they part-own that business and what are the key factors that would lead them to sell that business

The investee businesses must either have High Profit Margins or High Turnover and Reasonable Profit Margins. And this advantage must be sustainable.

Choosing a Stock-Picker

Specific Investments

We, via the Specialist Stock-pickers, want :

** the best performing businesses over a 10+ year time frame

We want to buy these on the stock-market

Most stock-market participants are looking for the best 1 year performers. Their time frame may be shorter, eg 3 months,or……even intra-day!

This can be to our advantage. Avoid the noise.

How Many Managers -ie stock-pickers?

Obtain diversification – ie different processes and different people/perspectives

Not too many that we dilute the best performers

Around 3-5 in both Australian and International Shares

The businesses that we part-own (via our specialist Fund Managers) should, or must, meet these criteria:

We want to select Good Businesses – ie those with a Durable Competitive Advantage

We want to avoid Poor Businesses - ie those where price is the major motivating factor in the consumer’s decision to buy their product or service.

The Buffett Overlay

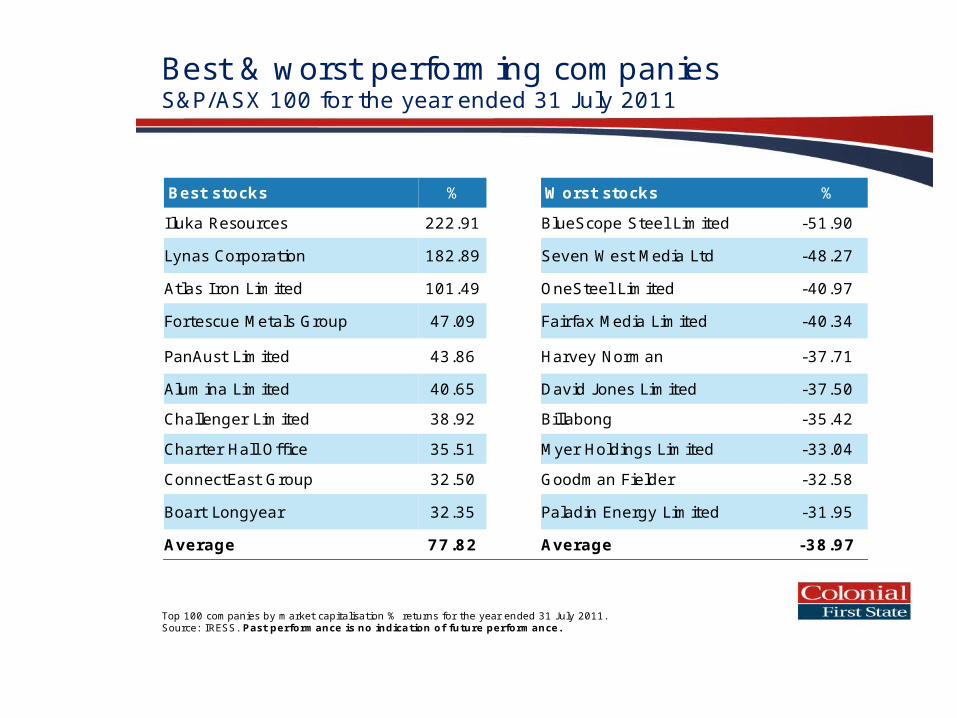

Top 100 companies by market capitalisation % returns for the year ended 31 July 2011. Source: IRESS. Past performance is no indication of future performance.

Best & worst performing companiesS&P/ASX 100 for the year ended 31 J uly 2011

Best stocks % Worst stocks %

Iluka Resources 222.91 BlueScope Steel Limited -51.90

Lynas Corporation 182.89 Seven West Media Ltd -48.27

Atlas I ron Limited 101.49 OneSteel Limited -40.97

Fortescue Metals Group 47.09 Fairfax Media Limited -40.34

PanAust Limited 43.86 Harvey Norman -37.71

Alumina Limited 40.65 David J ones Limited -37.50

Challenger Limited 38.92 Billabong -35.42

Charter Hall Office 35.51 Myer Holdings Limited -33.04

ConnectEast Group 32.50 Goodman Fielder -32.58

Boart Longyear 32.35 Paladin Energy Limited -31.95

Average 77.82 Average -38.97

[8]

Source: Bloomberg

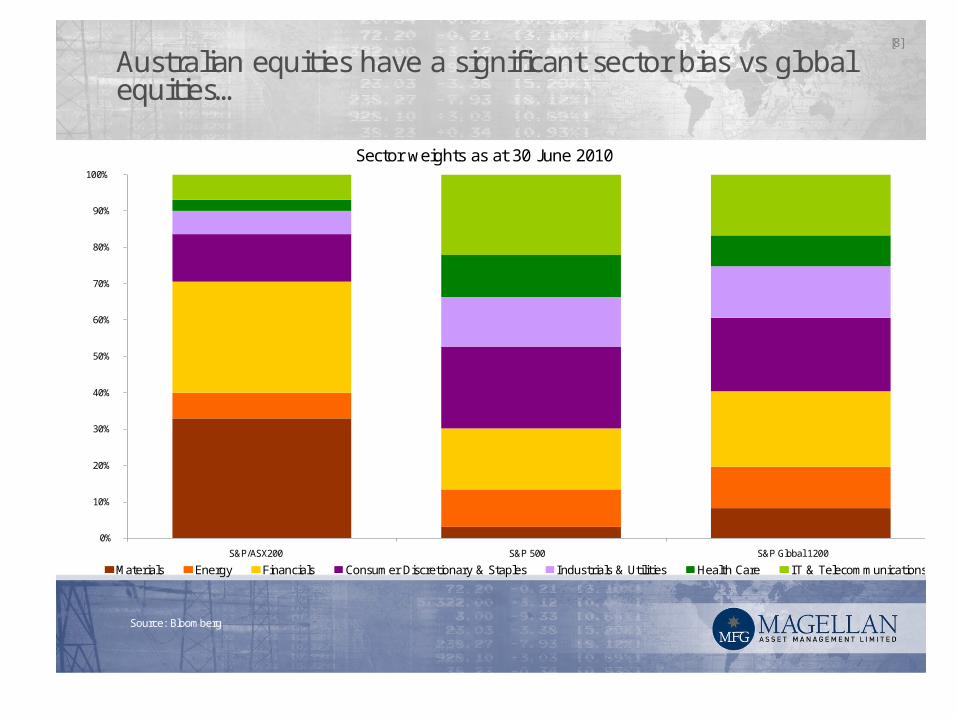

Australian equities have a significant sector bias vs global equities…

Sector weights as at 30 June 2010

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

S&P/ASX200 S&P 500 S&P Global 1200

Materials Energy Financials Consumer Discretionary & Staples Industrials & Utilities Health Care IT & Telecommunications

[40]

Portfolio strategyAlways focus on quality and minimising the risk of permanent capital loss

• Invest into extremely high quality “cash cows” with low risk exposure to consumer growth in the developing world

• The age of the Internet and the rise of e-commerce

• The move to a cashless society

Investors’ SeminarSeptember 2011

Historical Data

Forecasts

Hayden Asset Allocation Model

Specific Investment Selection

Bad case scenarios

Investors’ SeminarSeptember 2011

What is our greatest fear?

“running out of money”

“not achieving lifestyle goals”

“losing money”…..readily addressed; we need patient capital; there is no value-add by counting it daily…..need the faith to leave it; let it grow; leave it in a Bank, a Property, a Business etc

Investors’ SeminarSeptember 2011

The Fear:

Not achieving our goals (including running out of money)

What’s needed:

The “tap” turned on at a reasonable rate

Reasonable long-term returns

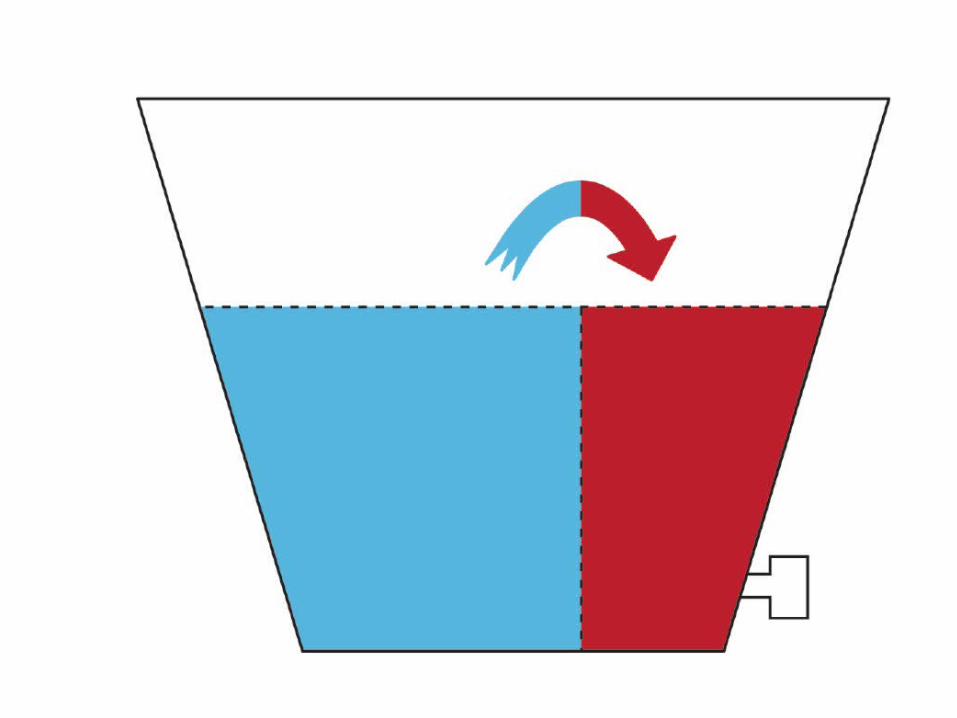

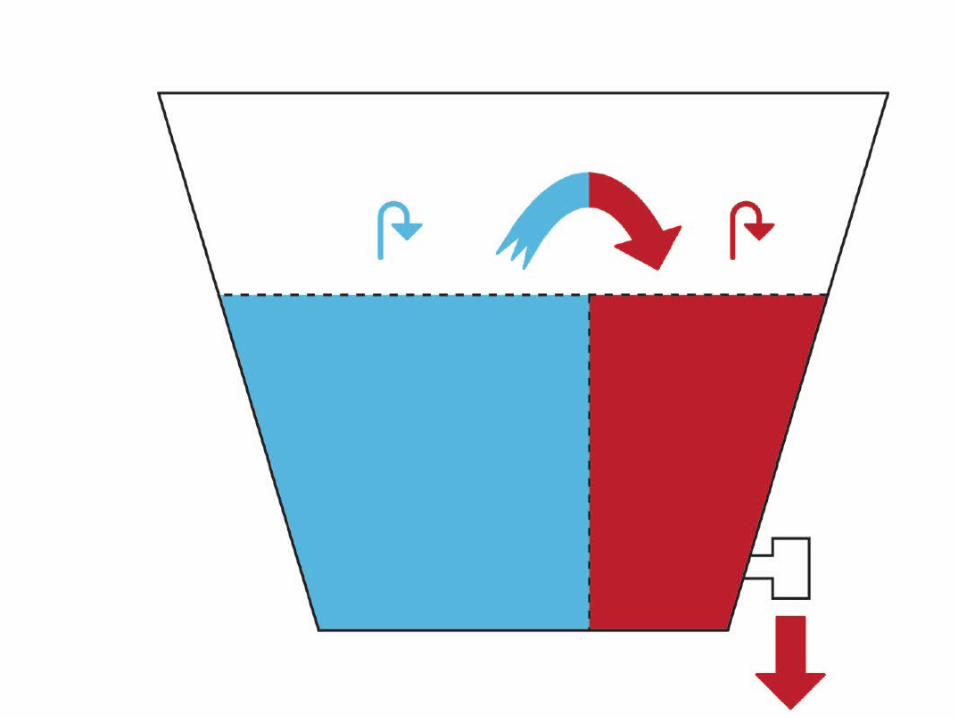

Bad case scenarios:

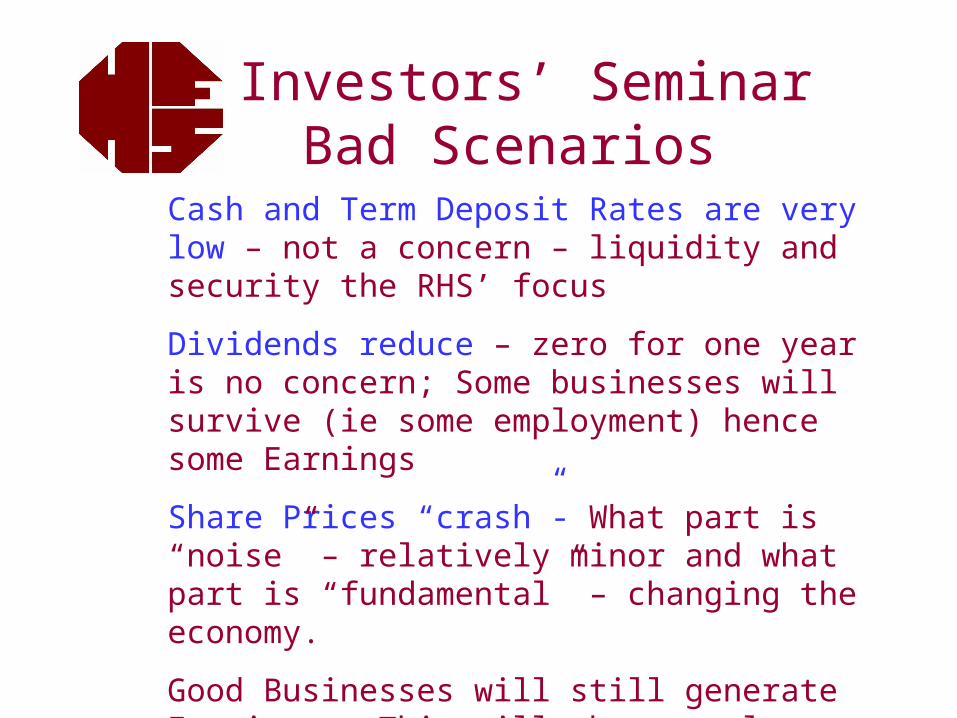

Share Prices “crash”; Dividends reduce; Cash and Term Deposit Rates are very low

Investors’ SeminarBad Scenarios

Cash and Term Deposit Rates are very low – not a concern – liquidity and security the RHS’ focus

Dividends reduce – zero for one year is no concern; Some businesses will survive (ie some employment) hence some Earnings

Share Prices “crash”- What part is “noise” – relatively minor and what part is “fundamental” – changing the economy.

Good Businesses will still generate Earnings. This will show partly as Dividends; partly in increased future Dividends; and partly an increased intrinsic value of the Business.

Illustrating theBad Case Scenarios

Cash and Term Deposit Rates - zero

Dividends reduce – NB Still will be some dividends (ie any surviving business will pay dividends most years)

Share Prices “crash”- The LHS will never be zero – there will always be some businesses

AssetMix

Australian SharesInternational Shares

Property??

Term Deposits

Cash

ASISP

TD

Cash

Specialist Stock-picker

XYZ Manager

Changes to Lifestyle or Financial Goals

Asset Sector Changes – eg if the 10 year return differential is significant;

Switching of Fund Managers – may be needed at any time if a change to skill level or portfolio integrity. In switching Managers we retain the same asset sector exposure –eg to shares.

Switching

Realistic Goals

Structure/Strategy (Tax etc)

Super Fund Admin

Asset Mix 1 -Cash/TermDs needed

Asset Mix 2–Growth Section (LHS)

Stock-Picker Selection

The Boxes to Tick

Peace-of-mind for Investors

1. Part-own a lot of great businesses. We have a portfolio of businesses that is well diversified across locations, industries and size.

2. Employing (contracting) some very wise people to monitor and change our portfolio of investee businesses when necessary.