investor strategy day inputs industry includes 'non-crop' $5.4 billion chemistry global...

TRANSCRIPT

March 2009

Investor Strategy Day

2

Investor Strategy Day

Agenda

Strategic overview Brian Benson

Regional overview – Australia/New Zealand Lachie McKinnon

Regional overview – Europe Alain Chalandon

Hugo Schweers

Regional overview – North America Dale Mellody

Nufarm innovation & product development Mike Pointon

Seeds strategy Brent Zacharias

Plant tours David Pullan

Mick O'Donnell

Global growth strategy

Nufarm Investor Strategy Day

March, 2009

Brian Benson

Group General Manager Agriculture

Agricultural inputs industry

Includes 'non-

crop' $5.4 billion

CHEMISTRY

Global crop

protection 2007 $38.8

billion

Combined markets

$69 billion

Includes ag bio

$6.9 billion

Global seeds market

2007 - $30 billion

BIOLOGY

2008 strong growth in chemistry & biology

Key growth drivers remain in place

Eating more protein/meat

Using crops to produce energy

Growing population

Growing in wealth

De

man

d

Demand and supply imbalance

Source: USDA, FAO, Goldman Sachs Commodities Research

Strong demand will require a substantial increase

in acreage and Yield ImprovementsIndices

Key strategic elements

Consolidate

the base

Build the brand

Build the

organisationDrive for growth

Build strategic

relationships

& alliances

Strategic growth drivers

Build

geographic

platform

Mostly in place

Seeds &

seed

treatment

Emerging growth

platform

Broaden

product

portfolio

Activity is now

focused here

Australia 80%

Total sales

NZ$306m(crop protection)

1995

Australia

80%

ROW

20%

Total sales

$763m(crop protection)

2000

Australia

65%

ROW

35%

Strategic growth drivers

Globalising the business

Total sales

$2.49 billion

(crop protection)

2008

Australia

29%

ROW

71%

Products and pipeline

Expanding product portfolio

Product Category 2007 sales value (US$m)

Herbicides 800

Insecticides 1,350

Fungicides 1,448

Other 50

TOTAL 3,648

Products coming off-patent 2009-2014

Source: Phillips McDougall

Nufarm will continue to target the substantial number of

products coming off patent over the next 5-10 years

25 global projects plus regional projects

Products and pipeline

Portfolio expansion driven by

Access to 'new' off-patent chemistry

New formulations and mixtures

Improved delivery systems

Co-marketing agreements with other companies

Targeted acquisition

Products and pipeline

12

An active, full pipeline …

New herbicide positions

Sulfonylureas

Pyridines

HBNs & mixtures

„Fops‟ and Dims graminicides

New fungicide positions

Fluazinam

Triazoles & mixtures

Strobilurins & mixtures

copper mixtures

New insecticide positions

Global roll-out of neonicotinoids

Pyrethroids

IGRs

Mixtures

New seed treatment positions

Neonicotinoid straights

Triazole straights

Neonicotinoid based mixtures

Triazole based mixtures

Nufarm growth strategy

Key pillars consistent

Growth drivers evolving

Global consistency with regional adaption

Delivering

strongly

March, 2009

Lachie McKinnon

General Manager

Australasia

Nufarm Investor Strategy Day

Australia

Nufarm Australia

The bigger picture …

Water

Crop efficiencies

Availability

Biotechnology / GM crops

The 'corporate' farmer

Seasonal swings

Carbon trading

Australia – major crops

Broadacre – 67% Horticulture – 14%

Pasture – 3%

Cotton – 3%

Sugarcane – 4%

Seed treatment – 3%

Other – 6%

Consumption of crop protection products

Australia – major crops

2001/02 2002/03 2003/04 2004/05 2005/06 2006/07 2007/08 est 2008/09

WHEAT 11,513,265 11,161,874 13,046,798 12,218,512 11,715,000 10,938,349 12,029,115 13,396,409

BARLEY 3,678,229 3,843,984 4,454,917 3,577,292 3,964,550 3,488,463 4,170,752 4,471,268

CANOLA 1,327,488 1,294,539 1,209,346 1,134,000 960,600 854,914 1,037,500 1,311,641

OATS 775,362 910,447 1,104,238 658,900 841,200 768,875 833,999 885,260

SORGHUM 809,672 654,876 722,632 765,850 729,800 541,566 766,500 800,000

TRITICALE 400,814 401,903 439,982 256,450 373,550 359,535 342,929 387,922

LUPINS 1,138,325 1,024,577 850,105 737,850 831,350 441,556 450,862 455,454

COTTON 350,000 350,000 350,000 350,000 150,000 150,000 63,000 120,000

FIELD PEAS 334,528 379,111 353,168 279,350 321,450 327,988 300,996 286,576

CHICK PEAS 243,241 200,372 199,611 135,200 155,680 247,635 305,141 318,211

FABA BEANS 180,549 174,688 146,309 209,800 183,850 162,225 133,039 172,124

LENTILS 201,245 179,950 122,950 129,800 131,600 139,210 139,000 128,678

RICE 105,000 105,000 80,000 105,000 80,000 20,000 6,000 10,000

21,057,718 20,681,321 23,080,056 20,558,004 20,438,630 18,440,317 20,578,833 22,743,543

Planted area (hectares)

Australian Crop Forecasters Feb 2009

Change in $500k to $2mill farms

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Grain andMixed

Farming

Sugar Cotton LivestockExtensive

LivestockIntensive

Fruit Grapes HorticultureOther

Vegetables

Industry

Farm

Nu

mb

ers

2001 $500k to $2mill 2006 $500k to $2mill

Australia – farm sizes

Change in $2million farms

-

50

100

150

200

250

300

350

400

450

Grain andMixed

Farming

Sugar Cotton LivestockExtensive

LivestockIntensive

Fruit Grapes HorticultureOther

Vegetables

Industry

Farm

Nu

mb

ers

2001 >$2mill 2006 >$2mill

Australia – farm sizes

Ag-Chem distribution channel

Importing Manufacturer Local Manufacturer

Local Formulation

Third Party

“Trader”

Distributors – eg Landmark, Elders, CRT, IHD etc.

End-user – farmers etc

Technical

sales

Branded Product

eg “Roundup®”

Distribution customers

Nufarm / Crop Care

Nufarm Limited(all back end functions)

R&D, Finance, Logistics, Manufacturing

Nufarm Australia Ltd

Lachlan McKinnonGeneral Manager

Melbourne

National Sales & MarketingRegional Sales teams

Crop Care

Simon AdamGeneral Manager

Brisbane

National Sales & MarketingRegional Sales teams

Nufarm / Crop Care

Separate TMsSeparate CSO

Separate TMsSeparate CSO

Separate Product Range

TriflurXRoundup

Amicide 625Avadex Extra

Separate Product Range

AchieveFusionSusconTalstar

Same logistics

Business overview

A full service model

Manufacturing

Synthesis

& formulation

Logistics

Regional

service

centers

Regulatory

Substantial

resources

Intellectual

property

Product

Development

New

formulations

Mixture

products

Innovative

packaging

Marketing

'Agricentres'

Loyalty

programs

Sales

Field force

After Sales

Service -

admin etc

Global

partners

Market position

Nufarm has a clear market leadership position

Ranked no. 1 in all major crop segments

Only fully integrated supplier based in Australia

2nd brand position with Crop Care

Maximise molecule share

Comprehensive and varied offering

Seeds (including GMO position)

Farm machinery / Croplands

Nufarm Australia

The challenge …

To retain leadership position … every market share

point of it!

To improve the 'quality' of the business

Move customers / end users up the value chain

Regularly 'renew' product offerings

Strengthen customer loyalty

Improve efficiencies: supply chain / logistics

To anticipate and adapt to changes in agriculture

Climate

Customer base

Nufarm Australia

Adding value

Product development

Regulatory / technical support

Innovative marketing

Loyalty programs

Spraywise decisions

Agricentres

After sales support

Strategy & Drivers – 2009 - 2013

Grow EBIT

Resource Allocation

Customer Focus

End User Development

Product Development

Personnel

Cost management

Improve Quality of

Sales

Focused R&D

Enhanced Supply Chain

Q & A

March, 2009

Alain Chalandon

General Manager

South West Europe

Nufarm Investor Strategy Day

South West Europe

Crop protection market by crop

1.7

4.5

4.7

5.8

8

9.5

9.5

10.7

13.3

32.3

0 5 10 15 20 25 30 35

Sunflower

Pome Fruit

Sugarbeet

Potato

Rape

Maize

Vine

Other Crop

Other F & V

Cereals

2008 European Ag Chem Market : 8191 M€

(% of total)

Europe

Crop protection market

Product split

Global sales* European sales*

Fungicides

36.3%

Others

4.2%

Herbicides

46.3%

Insecticides

13.2%

Fungicides

24%

Others

3.2%

Herbicides

47.7%

Insecticides

25.1%

* Phillips McDougall 2007

Market share positions

28.6%

21.3%16.7%

5.5%

4.8%

2.8%

2.7%

15.3%2.3% BCS

Syngenta

BASF

Dupont

Dow

Monsanto

MAI

Nufarm

Others

Europe

Growth by region 2008

0%

5%

10%

15%

20%

25%

NAFTA Latin America Europe Asia

5%

22%

15.10%

10.90%

Phillips McDougall November 2008

South West Europe - Snapshot

Regional markets covered

Direct presence:

France

Spain

Portugal

Italy

Greece

Egypt

Sales into:

North Africa & Africa

Middle East

Turkey & South Balkans

Major crop focus

Cereals

Corn

Vineyards

Horticulture

Major product positions

Current: Coming:

Glyphosate Imidacloprid

Bromoxynil Nicosulfuron

Amitrole Fluazinam

Phenoxies Lambda Cyhalothrin

DFF Tebuconazole

Copper fungicides

Market evolution 2002-2008 (M€)

Key South European markets

33

%3

%

65

%

PRIVATESWHOLESALER

SCOOPS

FARMERS

AGCHEM COMPANIES

64 %

35 %

1 % 2 %

Distribution structure

South West Europe

Success factors

Building the organisation

Recruitment of good people

Improved reporting systems

Better supply chain management

Small acquisitions

Italy, Portugal, Greece

Developing the product portfolio

Internally developed products

3rd party products

New formulations and mixtures

Last five years

Regional sales have grown

by 73%

South West Europe

The opportunity

Market access potential for Nufarm in SWE is

roughly 50% of the overall SWE market

We need to:

1. Expand our distribution network in implementing new

country sales forces (Morocco, Bulgaria, Turkey)

2. Feed our portfolio and address gaps in our product

range

3. Expand our distribution base

4. Develop our team and competencies

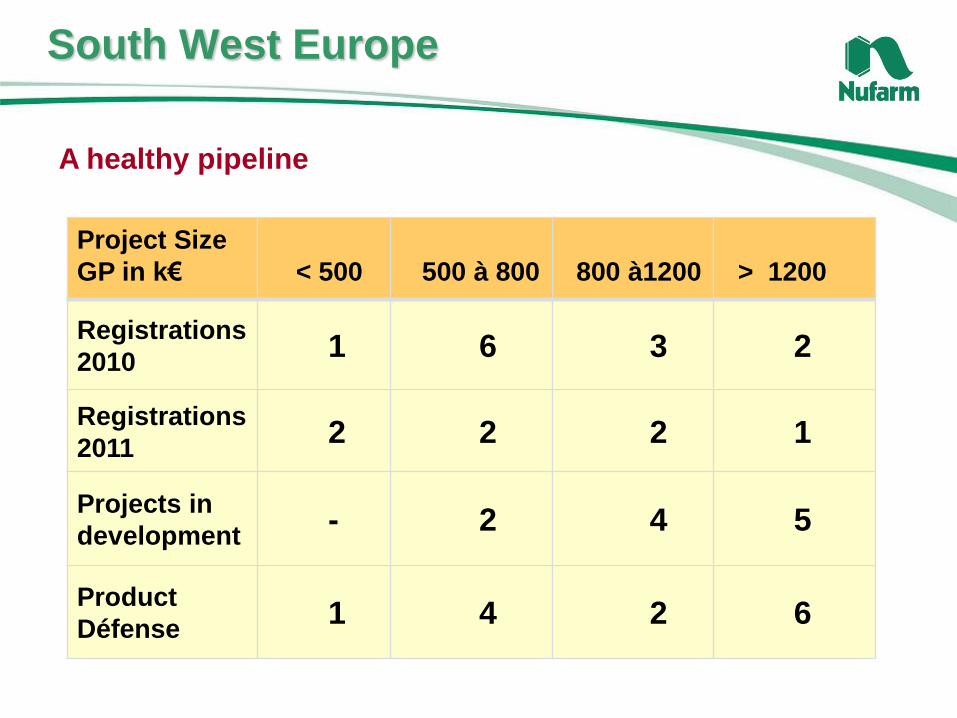

Project Size

GP in k€ < 500 500 à 800 800 à1200 > 1200

Registrations

20101 6 3 2

Registrations

20112 2 2 1

Projects in

development- 2 4 5

Product

Défense1 4 2 6

South West Europe

A healthy pipeline

South West Europe

Conclusion

Nufarm is an active player now in South West

Europe

Our potential is to double our turnover in the

next 4-5 years

Team and customer focus

Q & A

March, 2009

Hugo Schweers

General Manager

North East Europe

Nufarm Investor Strategy Day

North East Europe

North East Europe - Snapshot

Regional markets covered

Direct presence:

Germany

UK / Ireland

Benelux

Nordics

Baltics

Austria

Poland

Czech

Slovakia

Hungary

Romania

Sales into:

Ukraine

Russia

Belarus

Kazakhstan and other 'Stans'

Poland

Czech

Slovakia}F&N

Joint venture

Major crop focus

Cereals

Corn

Oil seed rape (OSR)

Potatoes

Major product positions

Current: Coming:

Phenoxy herbicides Cereal fungicides

Glyphosate Potato fungicides

Fenoxaprop & insecticides

Copper fungicides OSR fungicides &

MSM insecticides

Chlortoluron Seed treatment

Fluquinconazole

Germany/ AU/CH 54

BeNeLux/Nordics/ Baltics 132

UK/Ire 178

Poland/CZ/SK 53

Hungary 28

Rumania 20

CIS 83

NEE Total 548

Nufarm owned registrations (labels)

NEE - Product registrations

North East Europe - Snapshot

Distribution structure

Western Europe

Wholesalers: Co-ops & privates

Retailers: Decreasing; consolidation

Farmers: Farm size increasing

Officials: Local recommendations

Central & Eastern Europe

Distributors: Co-ops and independents

Farmers: Large farming enterprises

North East Europe

Nufarm's strong growth driven by …

New product introductions

Expansion into new markets

Broader distribution base

Strengthening of commercial

capabilities

Last three years

Industry growth → 15%

Nufarm growth → 40%

Eastern Europe portfolio – key launches

Market

segment

Est.

Value

2013 - $m

2008-09 2010-11 2012-13 Impact

Cereal

fungicides

790 Tebuconazole Tebuconazole -

mix

Strobilurin-

mix

Growth

Cereal

herbicides

860 U 46 D

U 46 M

Duplosan

Alliance

Carmina

Phenoxies

Bio enhancers

Strong growth

Corn

herbicides

650 Zeagran

Ultimate

Emblem flo Nicosulfuron-

Bromoxynil

Strong growth

Seed

treatments

860 Gizmo Nuprid-max Tebuconazole-

mix

Growth

NEE - targeting strong share growth in key segments

Cereal

herbicides

Corn

herbicides

18

22

IPU/ CTU/ Phenoxies/ DFF/ HBN/ MSM

BEE - / Sobie - / Bio-enhancer - Technologies

Bromoxynil / Terbutylazin / Nicosulfuron

Mixed Ester - Technology

North-Western European market shares

North East Europe

Competitive strengths

Development - New product launches delivering 40% of

growth

Distribution - Building commercial capabilities

Shaping the future - New businesses

Operations - From sustainability to out performance

People - Strong team; development potential

Risk management in Eastern Europe

Supply to distributors

Payment terms follow crop pattern (90-240 days)

Under-developed banking systems; Austrian Bank

assurance

Challenges

Risk management in Eastern Europe

Instruments

Professional credit management team in Linz

Commercial terms include:

Rebates paid after debt collection

Cash discounts for early payment

Customer financing scheme with pre-payment included

Customer classification to support credit limit setting

North East Europe

Opportunities

20 new major product launches in the next five years

Move into seeds in Eastern Europe

Build a strong seeds and seed treatment portfolio

Expand operating base

Q & A

North America

& Central America

Dale Mellody

General Manager, North America

Group General Manager, Marketing

March, 2009

Nufarm Investor Strategy Day

The Region – North & Central America

57

Herbicide = 65%, Insecticide = 18%, Fungicide = 12% , Other = 5%

Raleigh

CalgaryChicago

Cali

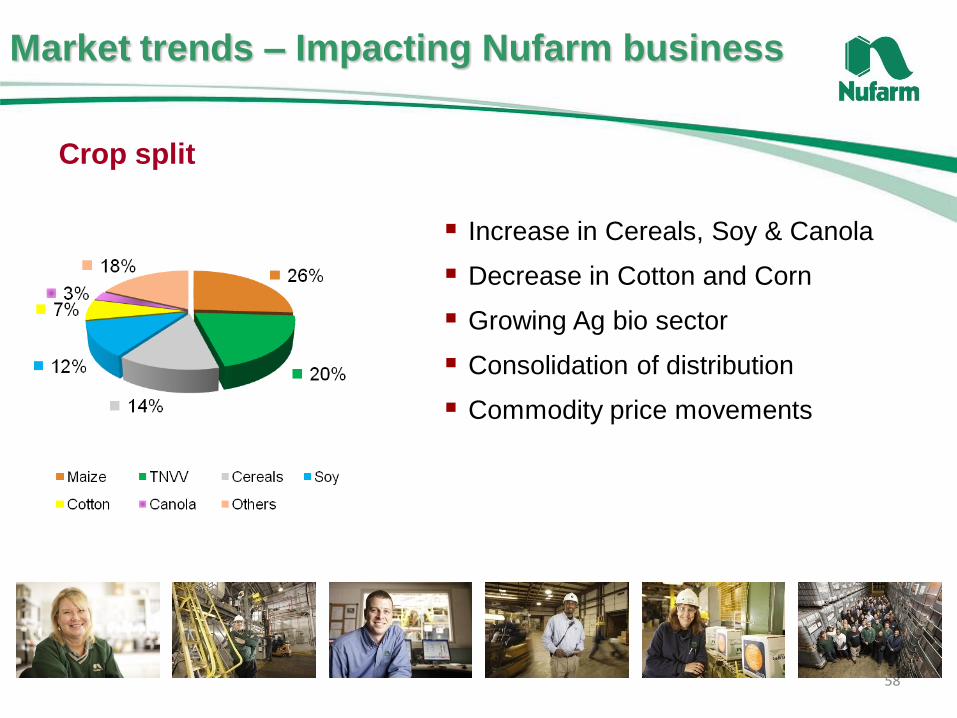

Market trends – Impacting Nufarm business

58

Increase in Cereals, Soy & Canola

Decrease in Cotton and Corn

Growing Ag bio sector

Consolidation of distribution

Commodity price movements

Crop split

Nufarm presence

Regional HQ – Chicago

Manufacturing bases in Chicago, Calgary & Colombia

Development center in Research Triangle Park, North Carolina

US Segments:

- Crop protection - Turf & ornamental

- Seed treatment - Vegetation management & forestry

Key Product Positions - Glyphosate

- Phenoxy Herbicides

- Imidacloprid

National field force in Canada & Colombia

400+ employees

In excess of 800 registrations

59

60

Less than 4% market share

Branded & Private Label business

Targeted Crop + portfolio approach

- Cereals - TNVV

- Pasture - US turf

- Cotton

Low cost business model

Support key distribution

Growth by acquisition – product & company

Focus on Nufarm Brand

AUD$NAFTA & Central America Sales

$334M

$386M$464M

$496M

$619M

High quality, flexible supplier of

value-added generic chemistry

Nufarm business

Nufarm People – part of branding campaign

We recognize that you have a

choice in suppliers

Our entire team is empowered,

enabled and dedicated to providing

better choices to help our customers

build better businesses

Why this matters: we will work with

you to deliver the value you need to

make the best business decision for

the customer

Growth & opportunity

Low market share – organic growth

Recognize benefits of recent

acquisitions

New products – 26 product launches in

2008 & 2009

New markets

New segments

Diversification – 12 herbicides, 9

insecticides & 5 fungicides

3rd Party Relationships & bolt-on

acquisition opportunities

62

A new high load

GLYPHOSATE

with superior

performance in

tankmixes, and

LESS product

to HANDLE

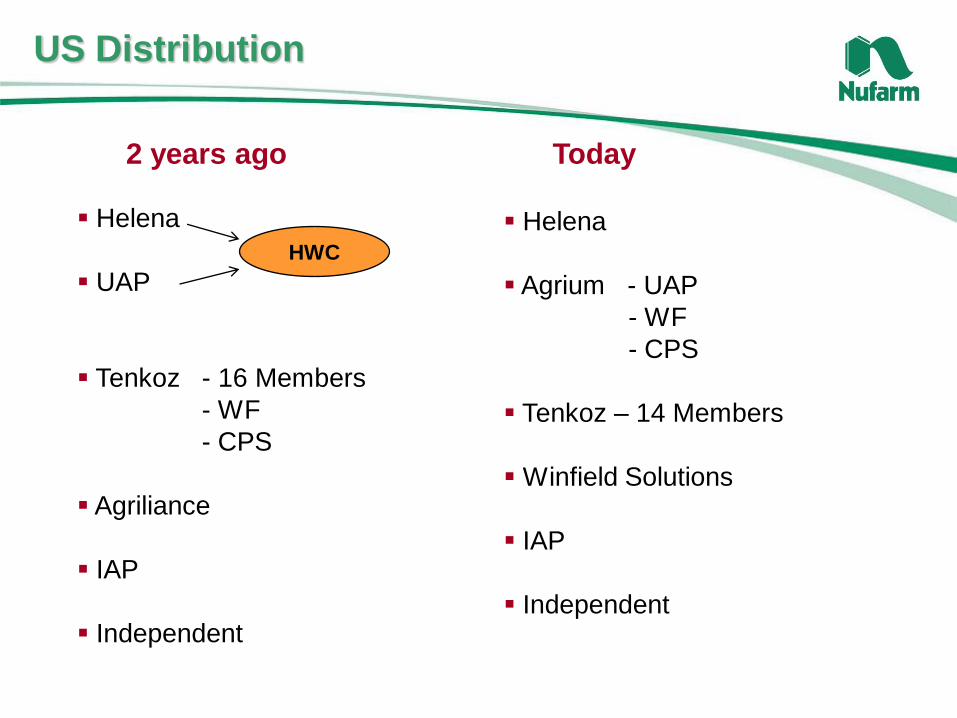

US Distribution

Helena

UAP

Tenkoz - 16 Members

- WF

- CPS

Agriliance

IAP

Independent

HWC

Helena

Agrium - UAP

- WF

- CPS

Tenkoz – 14 Members

Winfield Solutions

IAP

Independent

2 years ago Today

Canada Distribution

Agricore

SAS Wheat Pool

Federated Co-op

Cargill

James Richardson Int

Univar

UAP

IPCO

Viterra

Federated Co-op

Cargill

James Richardson Int

Univar

UAP/Agrium

2 years ago Today

Short term challenges & opportunities

Operational excellence

New product introductions

Development & people

Product stewardship &

maintenance

Events „out of our control‟

65

March, 2009

Mike Pointon

Group General Manager

Innovation & Development

Nufarm Investor Strategy Day

Product development

and innovation

Strategic growth drivers

Build

geographic

platform

Broaden

product

portfolio

Innovation and

product

development focus

… in the largest – and fastest growing – segment of

the industry

28.3%

patented

32.1%

Proprietary off patent

39.6%

generic

Patented Off patent

28.3% 71.7%

Total 2007 industry sales

Source - Phillips McDougall

Nufarm competes …

US$33.4bn

Industry segments

focused here

68

Global innovation and development

Chicago

BrisbanePerth

Melbourne

São PauloSantiago

19

4

1

5

2

Europe (31)

6

8

14

4

Australia (32)

3

1

2

NZ (6)

11

Indonesia (2)

21

Malaysia (3)

1

Japan (1)

2

Canada (2)Calgary

8

7

2

USA (17)

1

Chile (1)

Regulatory Affairs 51

Formulation Development 23

Field Trial 24

GLP Laboratory 5

Process Technology 8

Total Group: 111

Paris

Belvedere

Barcelona

Linz

Tokyo

Kuala Lumpur

Jakarta

Columbia (2)2

Brazil (13)

Fortaleza

5

3

3

2

Wyke

Cologne

Fortaleza

Costa Rica (2)2

Product development

Product development in Nufarm …

Defends and maintains existing registrations ('license to

sell')

Upgrading registration packages to new standards

Develops new registration packages for approved new

projects

New data for toxicology, product chemistry, field

efficacy and crop selectivity

Developed to global standards for different regulatory

requirements

Projects are both global and regional

Nufarm global registrations

2002 Total : 1,377 product

registrations

2008 Total : 2,787 product

registrations

Source – NUF registrations database adjusted to include Agripec

Innovation

Innovation in Nufarm…

Focused on delivery systems for existing active ingredients

Resources are not directed to discovery of new active

ingredients

Must be driven to provide better products for farmers

New ideas from the field

Improved value proposition through differentiation

Sustainable differentiation where possible through

Intellectual Property

Global and regional project

Global projects …

Funded / managed globally

Involved detailed analysis of 'radar' molecules'

Includes strategic and economic return

analysis

No shortage of opportunities …

25 currently approved global

development projects

Global and regional projects

Regional projects …

Selected / proposed by regional management

Address ' local' opportunities

Specific crops

Specific competitive dynamics

Specific pests and diseases

Examples of regional projects:

- Europe: Fluazinam, Tebuconazole / Prochloraz

- USA: Introduction of SU‟s

- Brazil: Replacement of OP‟s Acephate, Neonicotinoids & SPs

Resourcing and prioritising

Global Projects Regional Projects

Correct Prioritisation

Regional Human Resource

Innovation projects in Nufarm

Sorbie

Some active ingredients can only be

delivered as an EC liquid

Sorbie technology allows these

products to be delivered as a

granule

A.I. is dissolved in solvent

Solvent is applied to Sorbie™ granule

Granule is delivered to the spray tank

where it disintegrates and releases ai

Value add:

Significant reduction in operator exposure

Elimination of contaminated packaging

Innovation projects in Nufarm

Suscon®

Soil applied granules providing controlled release of A.I.

Established and proven technology in Australia sugar cane

Suscon Blue and Suscon Maxi now developed for

Different active ingredients

Several global markets

Value add:

Provides very flexible product delivery

system

Allows extension of residual activity

Adapts a.i.‟s to new use applications

Sugarcane efficacy

Untreated

Strips

Pilot plant

Innovation projects in Nufarm

Micro carrier system

Technology being applied to developing a new system for

phenoxy and other herbicides

Targeted uptake in solventless system

Objective is to establish a product with the following benefits:

Reduced dose while maintaining efficacy

Reduced cost

Increased adherence to leaf surface = improved rainfastness

Reduced crop effect: no surfactant, reduced dose, no damaging

solvent

Technology partner identified; contracts established

Has significant potential to be extended to other products

Early development stage

High throughput screening

Time to develop agricultural products is limited

by seasons. A number of projects are now being fast

tracked using high throughput screen with indicator species

A partnership has been developed with RMIT Melbourne and

Deakin

Provides earlier confirmation and rapid feedback of

formulations / technologies

Benefits of system

Increase testing capacity / throughput (improved volume and time)

Rapid response time 7-10 days turnaround versus 3+ months in glasshouse

Less materials required for testing

Greater capacity and reduced cost for patent exemplification

Can be used for herbicides and fungicides

Control

0.001 mM 2,4-D

0.01 mM 2,4-D 0.1 mM 2,4-D 1.0 mM 2,4-D

Maintaining registrations for our core products is

key

Consolidate the base

In summary

Innovation and development in Nufarm

Building new products to balance and expand our

portfolio

Drives internal growth

Q & A

March, 2009

Brent Zacharias

General Manager, Seeds

Nufarm Investor Strategy Day

The Seeds Strategy

Strategic objectives

Lead genetic and value improvements via R&D investment

Global branded player: select core crops, target geographies

Downstream influence and

value capture (beyond

seed)

Synergy with Nufarm base

(chemistry, formulations,

treatments)

85

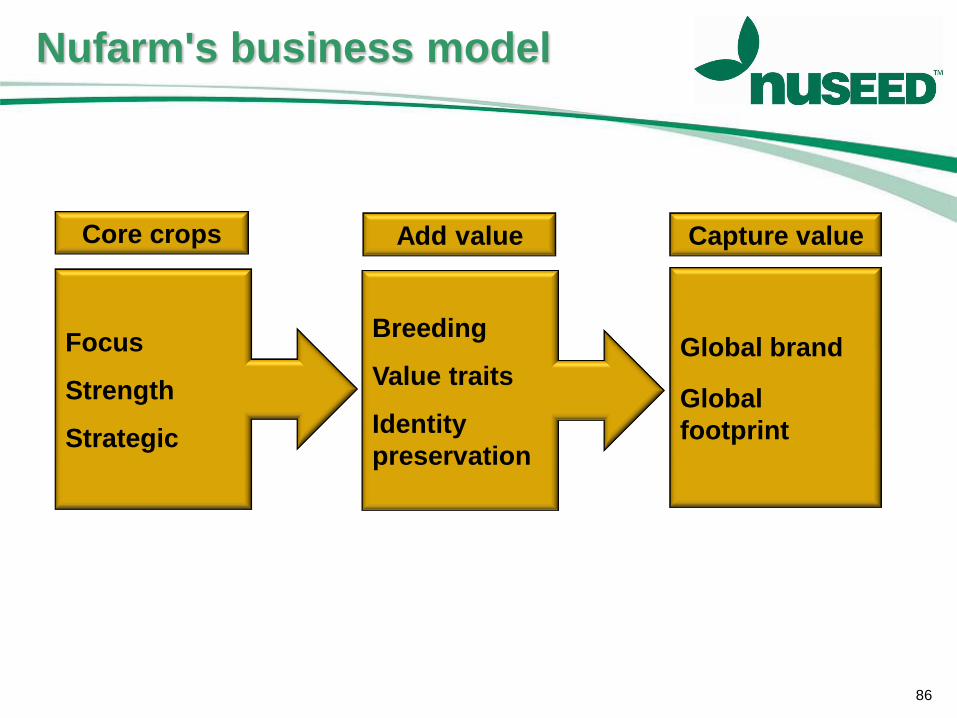

Nufarm's business model

Focus

Strength

Strategic

Core crops

Breeding

Value traits

Identity

preservation

Add value

Global brand

Global

footprint

Capture value

86

Core Crops

87Focus – Strength – Strategic

Canola

Position – leading Australia position

R&D projects – Triazine, Roundup Ready, Monola, hybrid

Sunflower

Elite genetics adapted in multiple countries

R&D projects – high oleic, herbicide & disease

resistance

Sorghum

Grain and forage hybrid development

R&D projects – improved yield and feed utilisation

(BMR)

Roundup Ready Canola

88

Australia

Commercialisation status

2008 release: 10,000 ha NSW, VIC

“22% yield over TT”; 100% “grow again”

2009 expect >100,000 ha

Nufarm position

Dominant canola share

One of three players in RR

Projected adoption of technology

75% conversion in 5 years

5 products on every hectare

GT61 (seed)

Roundup Ready (trait)

Senator + Jockey (treatment)

Roundup Ready (herbicide)

Core Crops

89Focus – Strength – Strategic

Canola

Position – leading Australia position

R&D projects – Triazine, Roundup Ready, Monola, hybrid

Sunflower

Elite genetics adapted in multiple countries

R&D projects – high oleic, herbicide & disease

resistance

Sorghum

Grain and forage hybrid development

R&D projects – improved yield and feed utilisation

(BMR)

Three primary canola nursery locations

Five primary sunflower / sorghum

nursery locations

Two generation cycles / year

65,000 nursery rows per annum

Trait enhanced

glasshouse

research

Breeding effort

90Breeding

Output Value Creation

End Users

Trait enhanced

seed

Retail partners &

crop protection

Grower Marketing and

Contracting

Processing

Partners

91Value traits / Identity preservation

Managing a value ladder

Canola

SorghumSunflower

92

5 Year Plan

Significant organic sales & value growth

2-3 strategic global acquisitions

20-25% EBIT return on revenue

Nuseed current footprint

Current markets

Partner breeding

Proprietary breeding

94Global platform

95

Summary

Strengthen global position in select

core crops

Drive technologies that enhance value

Extend global branded sales positions

(via Nufarm footprint)

Q & A

Nufarm Limited

Head office: 103-105 Pipe Road, Laverton North, Vic. Australia.

Tel: 61 3 9282 1000 Fax: 61 3 9282 1111 www.nufarm.com

A great time to be

in the business of

agriculture