investor presentationinvestor presentation - oceaneering · connections – grayloc connectors and...

TRANSCRIPT

Investor PresentationInvestor PresentationInvestor PresentationInvestor PresentationJune June 2016 2016

Forward-Looking StatementsStatements we make in this presentation that express a belief, expectation, or intention are forward looking. Forward-looking statements are generally accompanied by words such as “estimate,” “project,” “predict,” “believe,” “expect,” “anticipate,” “plan,” “forecast,” “budget ” “goal ” or other words that convey the uncertainly of future events or outcomesbudget, goal, or other words that convey the uncertainly of future events or outcomes. These forward-looking statements are based on our current information and expectations that involve a number of risks, uncertainties, and assumptions. Among the factors that could cause the actual results to differ materially from those indicated in the forward-looking statements are: industry conditions prices of crude oil and natural gas our abilitylooking statements are: industry conditions, prices of crude oil and natural gas, our ability to obtain and the timing of new projects, and changes in competitive factors. Should one or more of these risks or uncertainties materialize, or should the assumptions underlying the forward-looking statements prove incorrect, actual outcomes could vary materially from those indicatedfrom those indicated.

For additional information regarding these and other factors, see our periodic filings with the Securities and Exchange Commission, including our most recent Reports on Forms 10-K and 10-Q.

2

Why OII?

Global Provider of Diversified Services and Products in All Phases f h Off h Oilfi ld Lif C l

Global Provider of Diversified Services and Products in All Phases f h Off h Oilfi ld Lif C lof the Offshore Oilfield Life Cycle

Strong Balance Sheet and Cash Flow

of the Offshore Oilfield Life Cycle

Strong Balance Sheet and Cash Flow

Continue to Maintain or Grow Our Market Positions Continue to Maintain or Grow Our Market Positions

Return Capital to Our Shareholders

Experienced Management Team

Return Capital to Our Shareholders

Experienced Management Team Experienced Management Team

Longer Term, Deepwater is Still Critical to Reserve Replenishment

Experienced Management Team

Longer Term, Deepwater is Still Critical to Reserve Replenishment

3

About Oceaneering – Five Operating Segments

ROVROV

Subsea ProductsSubsea Products

Subsea ProjectsSubsea Projects

Asset Integrity

Ad d T h l i

Asset Integrity

Ad d T h l iAdvanced Technologies Advanced Technologies

4

EXPLORATION DEVELOPMENT PRODUCTION DECOMMISSIONINGPHASE

About OII – In All Phases of Offshore Oilfield Life CycleEXPLORATION

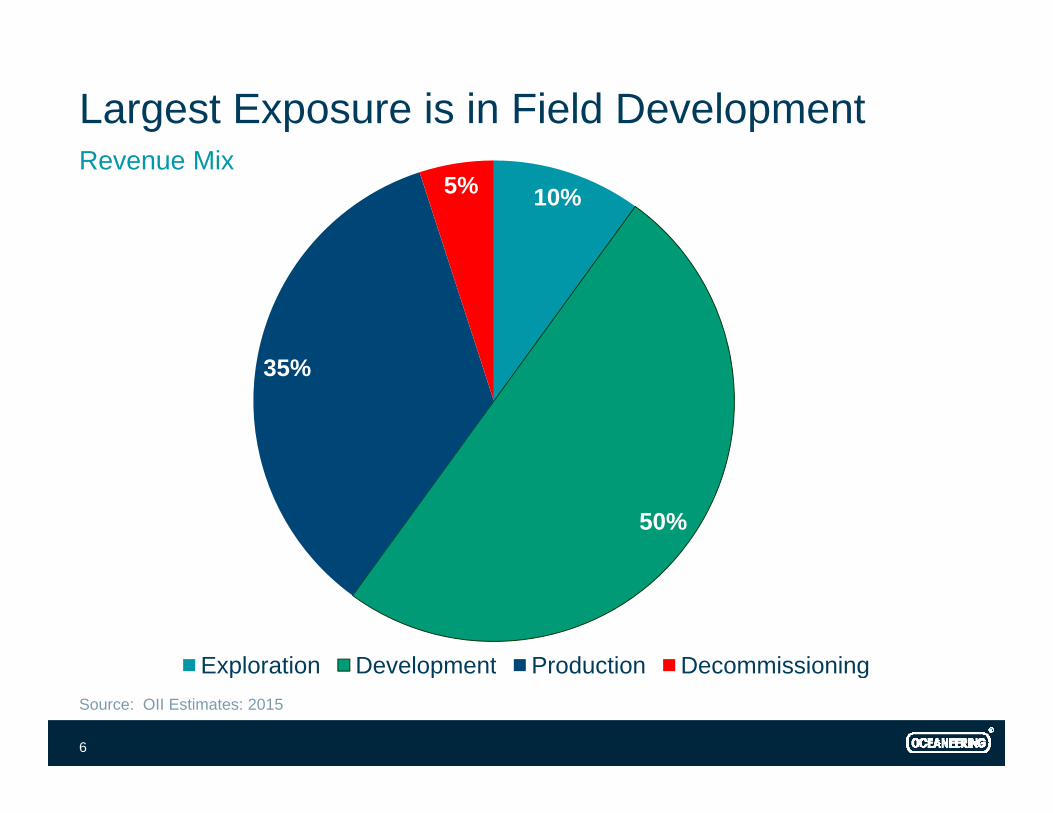

10%

DEVELOPMENT

50%

PRODUCTION

35%

DECOMMISSIONING

5%

# of OperatingFloating Drilling Rigs

# Subsea Tree Installations

# Subsea TreesIn Service

# of Field Abandonments

PHASE

% OII Revenue

#1 Market Driver g g ge

Business Segment P d t

•• ROVROV•• Survey (SP)Survey (SP)•• Tooling (SSP)Tooling (SSP)

Product and

Service Revenue Streams

• ROV• Survey (SP)• Tooling (SSP)

IWOCS I t ll ti &

• ROV• Tooling (SSP)• IWOCS (SSP)

S b H d (SSP)

• ROV • Tooling (SSP)• IWOCS (SSP)

• IWOCS – Installation & Workover Control Systems (SSP)

• Subsea Hardware (SSP)• Umbilicals (SSP)• Vessel-based Installation

Services (SP)Inspection Ser ices (AI)

• Subsea Hardware (SSP)• Vessel-based Inspection,

Maintenance & Repair Services (SP)

• Inspection Services (AI)

ROV = Remotely Operated Vehicles SSP = Subsea Products SP = Subsea Projects AI = Asset Integrity

• Inspection Services (AI)

5

Largest Exposure is in Field DevelopmentR Mi

10%5%Revenue Mix

35%

50%

Exploration Development Production DecommissioningExploration Development Production DecommissioningSource: OII Estimates: 2015

6

Revenue by Business Segment

7% 10% %

2014 2015 2016 Q1

29%14%

7%

27%12%

10%24%

12%

11%

16%20%

32%

21%

34% 31% 32%

$3.7 Billion $3.1 Billion $600 Million

ROV Subsea Products Subsea Projects Asset Integrity Advanced Technologies

2015

7

REMOTELY OPERATED VEHICLES 24%

Revenue Contribution Q1 2016

8

Oceaneering ROV Fleet Size318 ROV f M h 2016

336350

318 ROVs as of March 2016

315 318

300riod

End

300

Cou

nt a

t Per

250

Vehi

cle

2002008 2009 2010 2011 2012 2013 2014 2015 2016 Q1

9

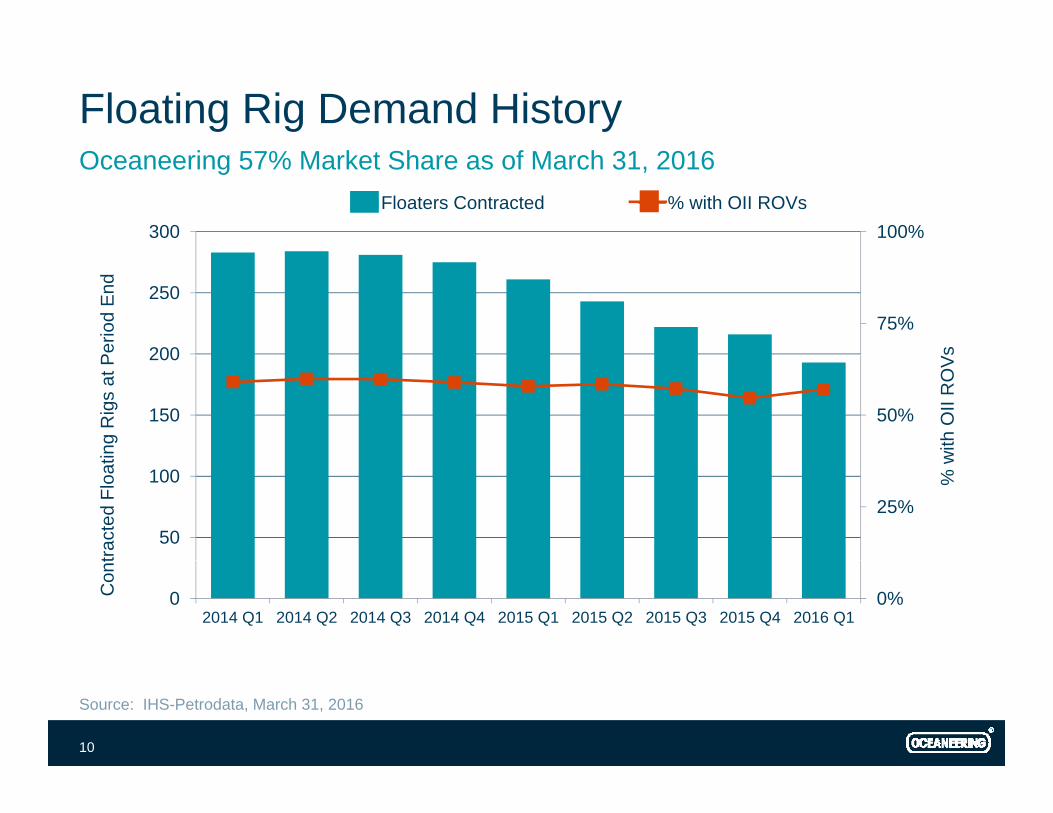

Floating Rig Demand HistoryO i % M k Sh f M h 31 2016

100%300Floaters Contracted % with OII ROVs

Oceaneering 57% Market Share as of March 31, 2016

75%200

250

sPerio

d E

nd

50%150

200

with

OII

RO

V

ing

Rig

s at

P

25%50

100 % w

tract

ed F

loat

0%02014 Q1 2014 Q2 2014 Q3 2014 Q4 2015 Q1 2015 Q2 2015 Q3 2015 Q4 2016 Q1

Con

t

Source: IHS-Petrodata, March 31, 2016

10

Oceaneering ROV Pricing and Fleet Utilization6% Fl U ili i f M h 2016

100%$11,000Revenue / Day on Hire Fleet Utilization

56% Fleet Utilization as of March 2016

70%

80%

90%

$8,000

$9,000

$10,000

nHire

50%

60%

70%

$5,000

$6,000

$7,000

eet U

tiliz

atio

ue /

Day

on

H

20%

30%

40%

$2 000

$3,000

$4,000

Fl

Rev

enu

0%

10%

$0

$1,000

$2,000

2008 2009 2010 2011 2012 2013 2014 2015 2016*

* YTD March 2016

11

SUBSEA PRODUCTS 32%

Revenue Contribution Q1 2016

Umbilicals

Tooling & Subsea Work Systems

I t ll ti dInstallation andWorkover Control

SystemsSubsea HardwareSubsea Hardware

12

Subsea Products

Required for Every Subsea Completion Required for Every Subsea Completion

Product Line Categories Service Technology and Rentals – IWOCS and Tooling

Product Line Categories Service Technology and Rentals – IWOCS and ToolingService Technology and Rentals IWOCS and Tooling Subsea Distribution – Umbilicals and

Field Development Hardware Connections – Grayloc Connectors and Pipeline Repair Systems

Service Technology and Rentals IWOCS and Tooling Subsea Distribution – Umbilicals and

Field Development Hardware Connections – Grayloc Connectors and Pipeline Repair Systemsy p p y Flow Control Solutions – BOP Control Spares and Rotator Valves

Highly Engineered

y p p y Flow Control Solutions – BOP Control Spares and Rotator Valves

Highly Engineered Highly Engineered

Worldwide Coverage

Highly Engineered

Worldwide Coverage

13

Subsea Installations Forecast

$1,500500

Tree Installations SSProducts Revenue

$1,200400

D in

Mill

ions

ns

$600

$900

200

300

Rev

enue

, US

D

e In

stal

latio

n

$300

$600

100

00

SSP

rodu

cts

R

Tre

$002011 2012 2013 2014 2015 2016F 2017F 2018F 2019F 2020F

S

Source: Quest Offshore, May 2016

14

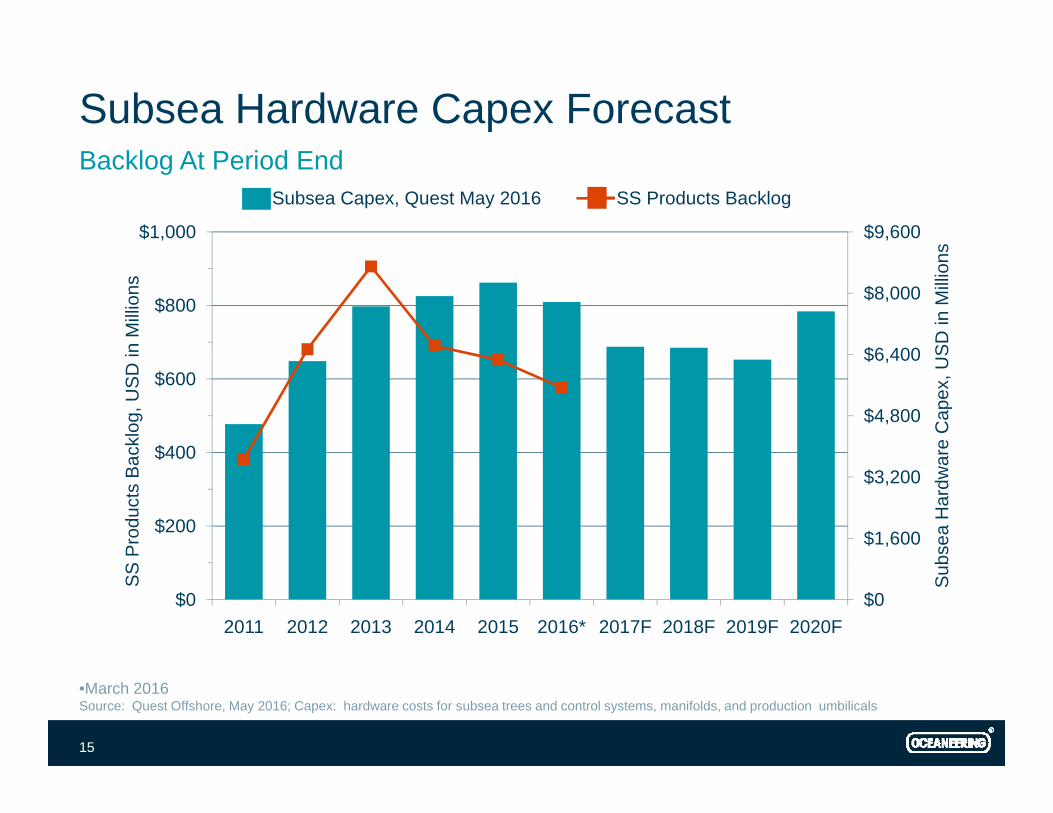

Subsea Hardware Capex ForecastB kl A P i d E d

$9,600$1,000

s

Subsea Capex, Quest May 2016 SS Products Backlog

Backlog At Period End

$6 400

$8,000$800

SD in

Mill

ion

in M

illio

ns

$4,800

$6,400

$400

$600

are

Cap

ex, U

S

ackl

og, U

SD

i

$1,600

$3,200

$200

$400

bsea

Har

dwa

Pro

duct

s B

a

$0$02011 2012 2013 2014 2015 2016* 2017F 2018F 2019F 2020F

Sub

SS

•March 2016Source: Quest Offshore, May 2016; Capex: hardware costs for subsea trees and control systems, manifolds, and production umbilicals

15

SUBSEA PROJECTS21%

Revenue Contribution Q1 2016

Diving

Deepwater

16

Subsea Projects Overview f

GOM Shallow Water Installation and IRM

Assets Available for this Market

4 Oceaneering Vessels, Diving Support 3 Saturation Diving Systems

Deepwater Installation and IRM 6 Chartered Vessels, DP 2 Oceaneering Vessels, DP

1 O i V l DP d li t th d f 2016 1 Oceaneering Vessel, DP, delivery at the end of 2016

Global Data Solutionsi l di AIRSIS i d i 2014 including AIRSIS, acquired in 2014

Survey/AUV Services - C&C Technologies i d i 2015 acquired in 2015

17

Leveraged to Deepwater

Projects Take Years to Develop Projects Take Years to Develop

Largely Oil Reservoirs with High Production Flow Rates

Largely Oil Reservoirs with High Production Flow Rateswith High Production Flow Rates

Well Capitalized Customer Base 50% Revenue from E&P Majors in Prior 3 Years

with High Production Flow Rates

Well Capitalized Customer Base 50% Revenue from E&P Majors in Prior 3 Years ~50% Revenue from E&P Majors in Prior 3 Years

Investment Based on Long-Term Commodity Price

~50% Revenue from E&P Majors in Prior 3 Years

Investment Based on Long-Term Commodity Price

18

Long Term: Offshore is EssentialD R i Si ifi

Source of90

Incremental Bbls Existing Fields Bbls

Deepwater Remains Significant

Source of Additional ~26Mm B/D

Crude Production80

e

32%

68%60

70

d C

onde

nsat

eM

B/D

68%

50

60

Cru

de a

nd MM

Offshore Onshore

40

Source: Morgan Stanley Research , Wood Mackenzie, Rystad Energy, and Company Data – March 2016

19

Expect Extended Declines from Producing Fields

4.0

New Production from New Fields Decline from Aging Fields

3.0

3.5

Day

1 5

2.0

2.5

Barr

els

Per

D

0.5

1.0

1.5

Mill

ion

B

0.02014 2015 2016 2017 2018

Inverting Balance presented by Bloomberg; Source data from Rystad

20

Strong Balance Sheet and LiquidityC i l S d All i

Liquidity (at end of First Quarter 2016)$371 Million of Cash

Capital Sources and Allocations

o $371 Million of Cash o $500 Million Undrawn Revolving Credit Facility, Expiring October 2020o Only $19 Million of Debt Maturities Until October 2018

Organic Capital Expenditureso Expect to Range From $125 Million to $175 Million in 2016

Dividends Dividendso Expect to Continue the Quarterly Dividend of $0.27 Per Share –

Subject to Anticipated EPS Levels and Board Approval

A i iti Acquisitions o Continue to Consider Investments that Augment Our Service or Product

Offerings

Consider Share Repurchases

21

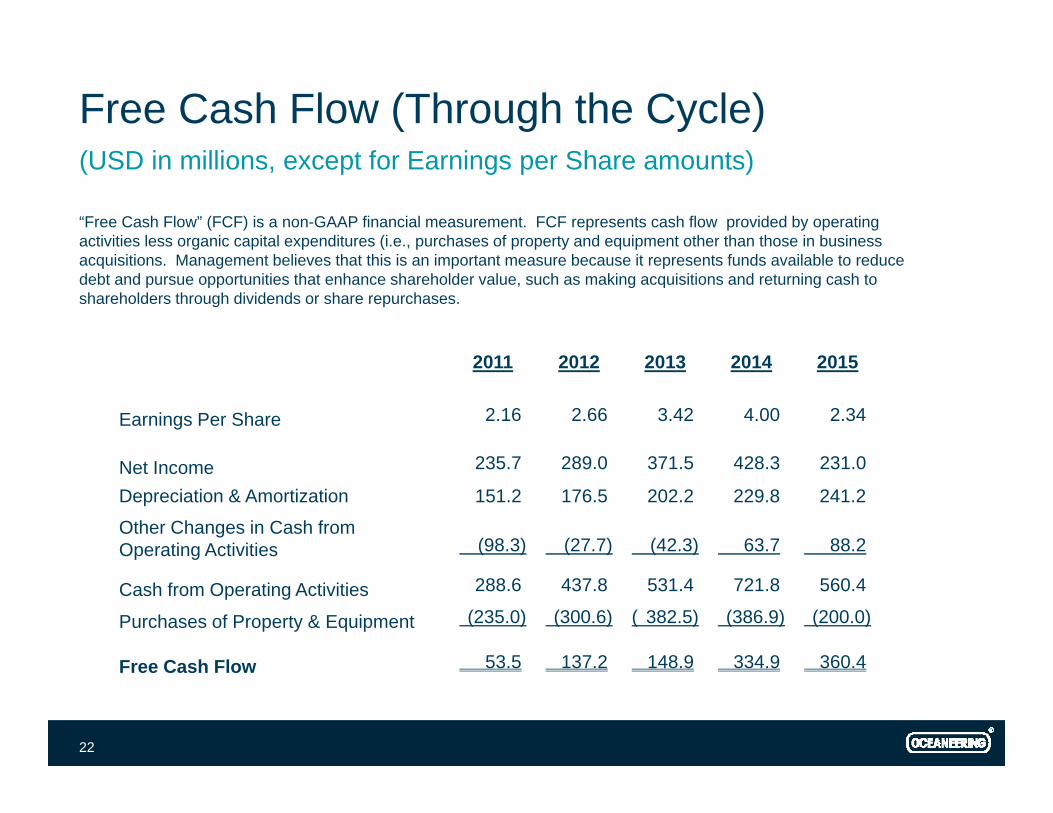

Free Cash Flow (Through the Cycle)(USD i illi f E i Sh )

“Free Cash Flow” (FCF) is a non-GAAP financial measurement. FCF represents cash flow provided by operating activities less organic capital expenditures (i.e., purchases of property and equipment other than those in business

(USD in millions, except for Earnings per Share amounts)

2011 2012 2013 2014 2015

acquisitions. Management believes that this is an important measure because it represents funds available to reduce debt and pursue opportunities that enhance shareholder value, such as making acquisitions and returning cash to shareholders through dividends or share repurchases.

2011 2012 2013 2014 2015

Earnings Per Share 2.16 2.66 3.42 4.00 2.34

235 7 289 0 371 5 428 3 231 0Net Income 235.7 289.0 371.5 428.3 231.0

Depreciation & Amortization 151.2 176.5 202.2 229.8 241.2

Other Changes in Cash from Operating Activities (98.3) (27.7) (42.3) 63.7 88.2

Cash from Operating Activities 288.6 437.8 531.4 721.8 560.4

Purchases of Property & Equipment (235.0) (300.6) ( 382.5) (386.9) (200.0)

Free Cash Flo 53 5 137 2 148 9 334 9 360 4Free Cash Flow 53.5 137.2 148.9 334.9 360.4

22

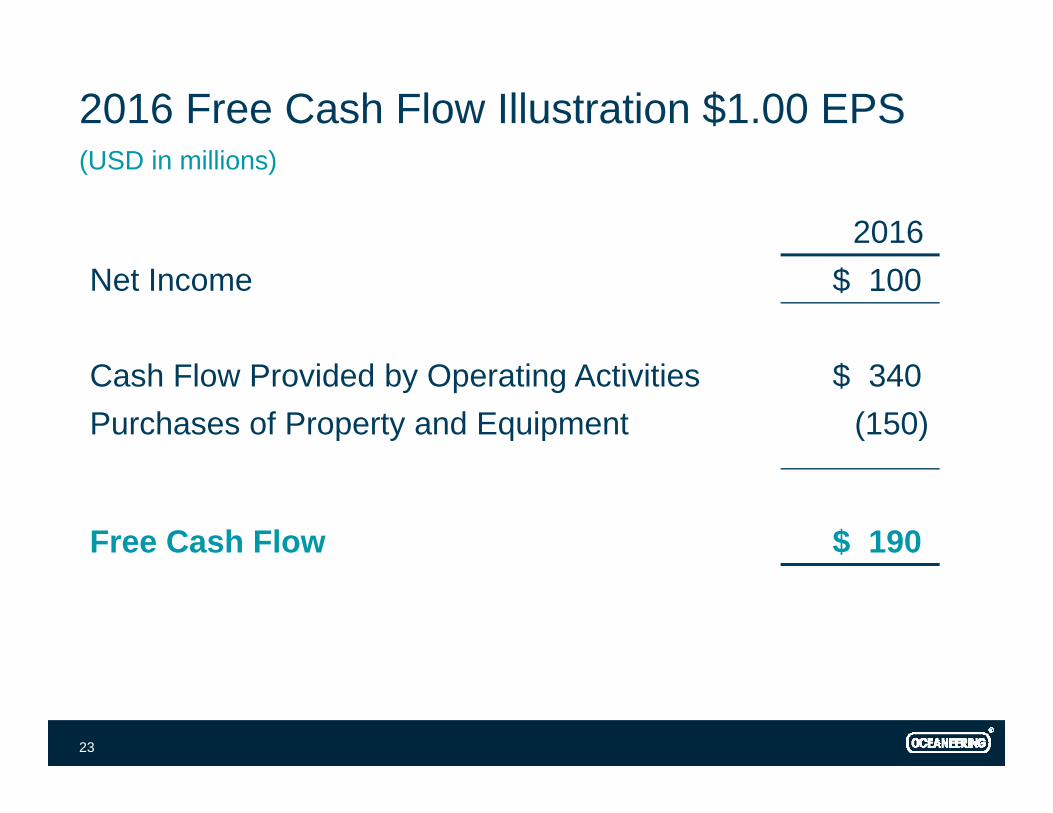

2016 Free Cash Flow Illustration $1.00 EPS(USD i illi )

2016

(USD in millions)

Net Income $ 100

Cash Flow Provided by Operating Activities $ 340Purchases of Property and Equipment (150)

Free Cash Flow $ 190

23

2016 Outlook

Shaping Up to be a Challenging Year

Aligning our Operations with Current Activity

Forecasting Declines in Each Oilfield Segment, Most Notably:

o ROV, Outlook Remains Cloudyo Subsea Products, Margins to Weaken Throughout the Year

Subsea Projects Impacted by Angola althougho Subsea Projects, Impacted by Angola, although expecting some Seasonal Uptick

2Q16 vs 1Q16 Operational Results Flat to Down

24

Conclusion

Longer Term, Deepwater is Still Critical to Reserve Replenishment

Global Provider in All Phases of Offshore Oilfield Life Cycle, with a Deepwater Focusp

Further Differentiate with Integrated Solutions

Strong Liquidity and Cash Flow

Maintain or Grow Our Market Positions Maintain or Grow Our Market Positions

Emerge from the Current Cycle Ready for the Upturn

25

Earnings Per Share2016 Q1 $0 26 201 $2 34

$5.00

2016 Q1 - $0.26; 2015 - $2.34

$4.00

hare

$2.00

$3.00

arni

ngs

per S

$1.00

$

Ea

$0.002008 2009 2010 2011 2012 2013 2014 2015 2016*

* First Quarter 2016

27

EBITDA

$1,000

$750

s

$500

SD in

Mill

ions

$250

US

$02008 2009 2010 2011 2012 2013 2014 2015 2016*

* First Quarter 2016

28

EBITDA Reconciliation to Net Income(USD i illi )Earnings before interest, taxes, depreciation and amortization (EBITDA) is a non-GAAP financial measurement. Oceaneering’s management uses EBITDA because we believe that this measurement is a widely accepted financial indicator used by investors and analysts to analyze and compare companies on the basis of operating performance, and that this measurement may be used by some investors and others to make informed investment decisions. You should not consider EBITDA in isolation from or as a substitute for net

(USD in millions)

Q1 Q1

investors and others to make informed investment decisions. You should not consider EBITDA in isolation from or as a substitute for net income or cash flow measures prepared in accordance with generally accepted accounting principles or as a measure of profitability or liquidity. EBITDA calculations by one company may not be comparable to EBITDA calculations made by another company. The following table provides a reconciliation between net income (a GAAP financial measure) and EBITDA (a non-GAAP financial measure) for Oceaneering’s historical and projected results on a consolidated basis for the periods indicated:

Period Ended 2011 2012 2013 2014 2015Q1

2015Q1

2016

Net Income 235 7 289 0 371 5 428 3 231 0 69 5 25 1Net Income 235.7 289.0 371.5 428.3 231.0 69.5 25.1

Depreciation & Amortization 151.2 176.5 202.2 229.8 241.2 58.0 59.8

Subtotal 386.9 465.5 573.7 658.1 472.2 127.5 84.9

Interest Expense/Income, Net .2 2.3 1.7 4.4 23.4 5.6 5.8

Income Tax Expense 102.2 132.9 170.8 195.2 105.3 31.7 11.4

EBITDA 489.3 600.7 746.2 857.7 600.9 164.8 102.1

29

Oceaneering ROV Leading Market PositionR l O d V hi l

Ownership Drill Support Market Share

Remotely Operated Vehicles

31531%

OIISubsea 7

11057%

FugroDOF SubseaC-InnovationsHelixSaipemTMTTMTTechnipHarkandIKM GroupOtherWorldwide Fleet

1027 Vehicles*193 Floating Rigs Contracted**

1027 Vehicles

Source: *OII Estimates - December 2015; **IHS Petrodata and OII Estimates – March 31, 2016

31

Oceaneering ROV FleetG hi P fil M h 2016

36

Geographic Profile – March 2016

10330

25

52

72

GOM Africa Norway Brazil Asia/Pac Other

318 Vehicles

32

Oceaneering ROVs on Vessels M h 2016March 2016

Locations Customers

24

12

18 4537

2828

GOM Africa Norway Other Operators Contractors

82 Vehicles

33

Investor Relations Contact

Suzanne SperaDirector Investor RelationsDirector, Investor [email protected]

34