investor presentation - nutrien conference... · this presentation is prepared in accordance with...

TRANSCRIPT

Investor PresentationFebruary 2018

Legal Disclaimer

Certain statements and other information included in this presentation constitute "forward-looking information" or "forward-looking statements" (collectively, "forward-looking statements") under applicable securities laws. All statements in this presentation, other than those relating to historical information or current conditions, are forward-looking statements, including, but not limited to, statements relating to certain strategic benefits expected to result from the combination of Agrium and PotashCorp, the nature and timing of operating synergies and Nutrien's expected capital allocation strategy and dividend policy.

Forward-looking statements in this presentation are based on certain key expectations and assumptions made by Nutrien, including expectations and assumptions concerning: customer demand for Nutrien's products; commodity prices and interest and foreign exchange rates; operating synergies, capital efficiencies and cost-savings; applicable tax laws; future production rates; future debt ratings; the sufficiency of budgeted capital expenditures in carrying out planned activities; and the availability and cost of labour and services. Although Nutrien believes that the expectations and assumptions on which such forward-looking statements are based are reasonable, undue reliance should not be placed on the forward-looking statements because Nutrien can give no assurance that they will prove to be correct.

Forward-looking statements are subject to various risks and uncertainties which could cause actual results and experience to differ materially from the anticipated results or expectations expressed in this presentation. Key risks and uncertainties include, but are not limited to: general global economic, market and business conditions; weather conditions including impacts from regional flooding and/or drought conditions; crop plant area, yield and prices; supply and demand and price levels for major products of Nutrien may vary from what we currently anticipate; failure to realize anticipated synergies or cost savings in connection with the combination of Agrium and PotashCorp; risks regarding the integration of Agrium and PotashCorp; failure to realize governmental and regulatory requirements and actions by governmental authorities, including changes in government policy, government ownership requirements, changes in environmental, tax and other laws or regulations and the interpretation thereof; political risks, including civil unrest, actions by armed groups or conflict; regional natural gas supply restrictions; counterparty and sovereign risk; relationships with employees, customers, business partners and competitors and risk factors set forth in Nutrien’s business acquisition report dated February 20, 2018 and in Agrium’s and PotashCorp’s respective annual information forms, each dated February 20, 2018, all filed under respective corporate profiles on SEDAR and EDGAR.

For material assumptions and risks associated with our 2018 guidance, see “Forward-Looking Statements” in our press release dated February 5, 2018.

Nutrien disclaims any intention or obligation to update or revise any forward-looking statements in this presentation as a result of new information or future events, except as may be required under applicable U.S. federal securities laws or applicable Canadian securities legislation.

All reference to “$” and “USD$” are to U.S. dollars.

IFRS Advisory This presentation is prepared in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board (“IFRS”). IFRS financial information of Nutrien in 2018 reflects the operations of Nutrien. IFRS financial information for 2017 and prior reflects the operations of PotashCorp. For comparative purposes, certain historical financial information presented reflects the combined results of Agrium and PotashCorp.

Non-IFRS Financial Measures AdvisoryWe consider adjusted net earnings (loss) from continuing operations before finance costs, income tax (recovery) expense and depreciation and amortization ("EBITDA") , EBITDA margin, free cash flow, cash cost of goods sold and all adjusted combined financial information, all of which are non-IFRS financial measures, to provide useful information to both management and investors in measuring our financial performance and financial condition. Refer to the disclosure under the heading “Non-IFRS Financial Measures” and “Non-IFRS Financial Measures in MD&A included in Agrium and PotashCorp’s annual reports each as filed on SEDAR at www.sedar.com and EDGAR at www.sec.gov under our corporate profile on February 26, 2018, for a reconciliation of these non-IFRS measures to the most directly comparable measures calculated in accordance with IFRS and for a further discussion of how these measures are calculated and their usefulness to users including management. Non-IFRS financial measures are not recognized measures under IFRS and our method of calculation may not be comparable to that of other companies. These non-IFRS financial measures should not be considered as a substitute for, or superior to, measures of financial performance prepared in accordance with IFRS.

February 26, 2018

2

Presentation Outline

February 26, 2018

3

1 Nutrien Overview and Vision

2 Fundamentals and Outlook

3

Capital Allocation4

1

Strategy and Opportunities

Our Vision is to be the Leading Global Agribusiness Company

February 26, 2018

4

$500 million in run rate synergies expected to be achieved by the end of 2019

Leading ag platform provides earnings stability & multiple avenues for growth

(geographic, product and technology)1

2

Significant free cash flow and strong balance sheet provides opportunity for

meaningful shareholder returns and growth3

Significant potential upside to a recovery in crop nutrient markets; $25/mt

increase in fertilizer prices expected to generate ~$650M in additional EBITDA4

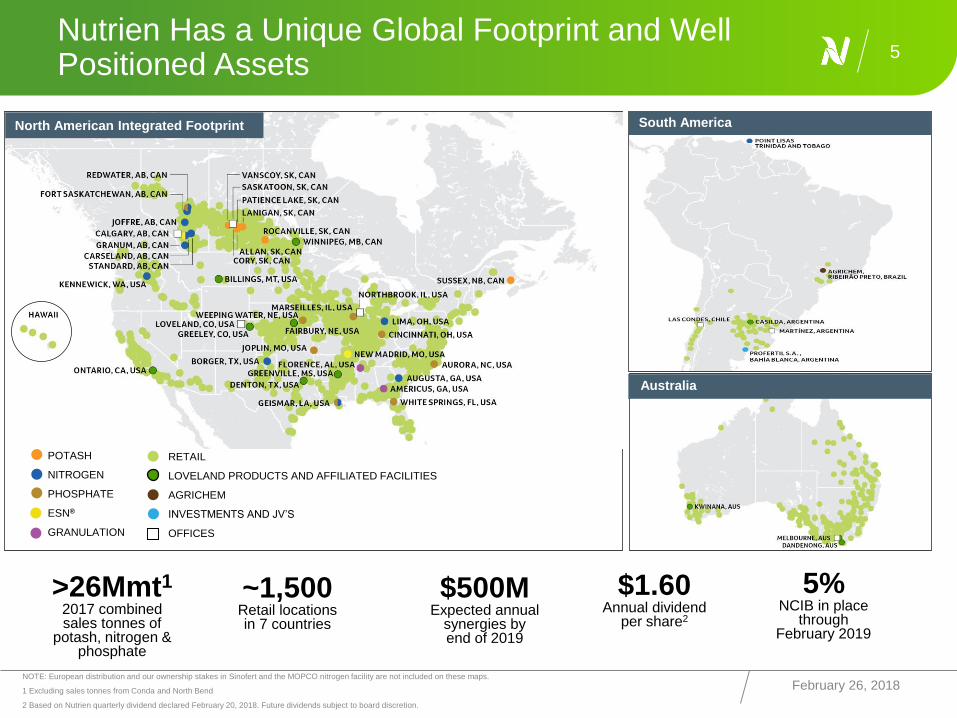

Nutrien Has a Unique Global Footprint and Well Positioned Assets

NOTE: European distribution and our ownership stakes in Sinofert and the MOPCO nitrogen facility are not included on these maps.

1 Excluding sales tonnes from Conda and North Bend

2 Based on Nutrien quarterly dividend declared February 20, 2018. Future dividends subject to board discretion.

5

>26Mmt1

2017 combined sales tonnes of

potash, nitrogen & phosphate

$500MExpected annual

synergies by end of 2019

$1.60Annual dividend

per share2

~1,500Retail locations in 7 countries

LEGEND:

POTASH

NITROGEN

PHOSPHATE

ESN®

GRANULATION

RETAIL

LOVELAND PRODUCTS AND AFFILIATED FACILITIES

AGRICHEM

INVESTMENTS AND JV’S

OFFICES

South America

Australia

5%NCIB in place

through February 2019

North American Integrated Footprint

February 26, 2018

~33%

~24%~7%

~36%

Diversified Portfolio Provides Stability and Multiple Avenues for Growth

February 26, 2018

6

Retail

Phosphate

and Sulfate Nitrogen

Potash

2017 Adjusted

Combined EBITDA Split1

1 Reflects adjusted combined EBITDA, which is derived from historical financial information of PotashCorp and Agrium and do not include the effects of a) intersegment eliminations, b) the equity earnings

and operating results of completed or anticipated divestitures in connection with the merger, c) allocation of certain corporate costs or d) the impairment charge related to Phosphate. Determination of

Adjusted Combined EBITDA required allocation of historical amounts on a basis consistent with how Nutrien will report financial information in the future. This information does not purport to project the

future operating results of Nutrien, and is not necessarily indicative of what Nutrien’s results of operations would have been had the merger been completed on January 1, 2017.

2 Cash provided by operating activities from continuing operations excluding the impact of net changes in non-cash working capital less sustaining capital expenditures.

3 Calculated as (EBITDA less sustaining capital)/ EBITDA. 2018F based on mid-point of guidance as of Feb 5, 2018.

4 Based on Nutrien quarterly dividend declared February 20, 2018. Future dividends subject to board discretion.

USD billions (unless otherwise noted)

2017 Adjusted

Combined

Revenue $18.3

EBITDA1 $2.7

Free Cash Flow 2 $1.3

Sustaining Capital $1.0

Free Cash Flow

Conversion3

63% (2017)

~70% (2018F)

Annual Dividend per

Share4 $1.60

Summary Financial

Performance

~25% increase in estimated 2018 EBITDA

versus proforma 2017

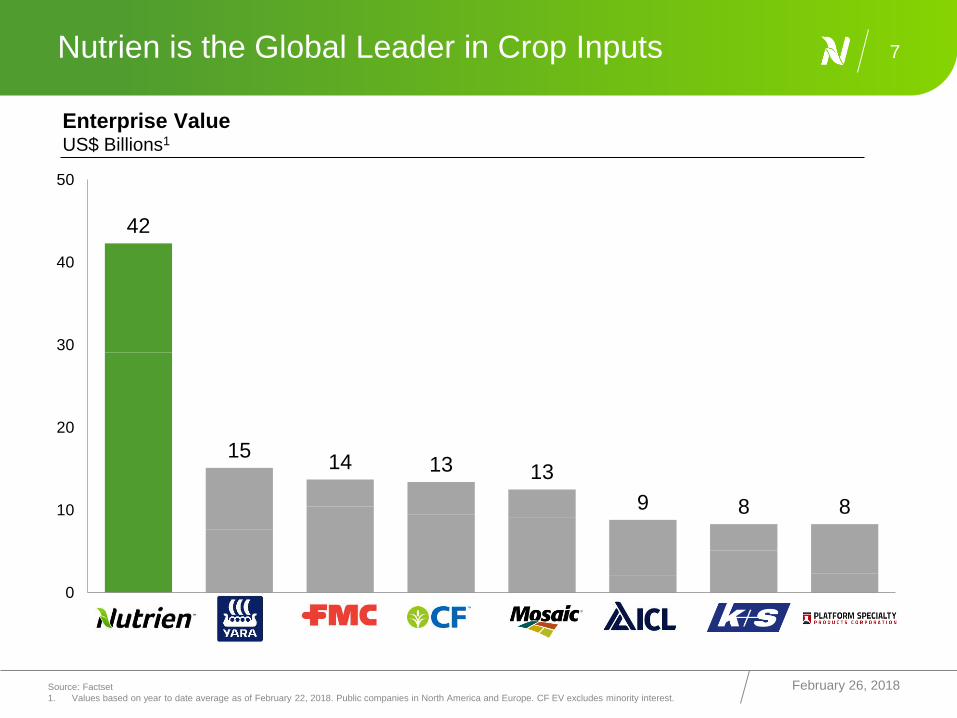

Nutrien is the Global Leader in Crop Inputs

42

15 14 13 13

9 8 8

0

10

20

30

40

50

Nutrien YAR FMC CF MOS ICL K+S PAH

February 26, 2018Source: Factset

1. Values based on year to date average as of February 22, 2018. Public companies in North America and Europe. CF EV excludes minority interest.

7

Enterprise ValueUS$ Billions1

Fundamentals and Outlook

INVESTOR PRESENTATION February 26, 2018

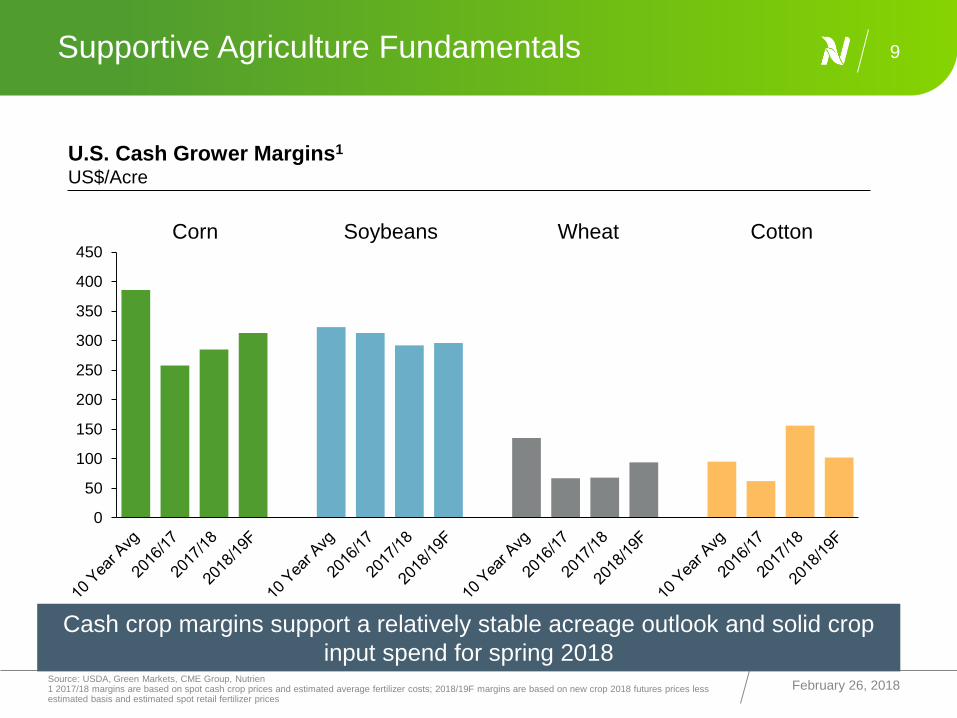

Supportive Agriculture Fundamentals

February 26, 2018

9

0

50

100

150

200

250

300

350

400

450Corn Soybeans Wheat Cotton

U.S. Cash Grower Margins1

US$/Acre

Cash crop margins support a relatively stable acreage outlook and solid crop

input spend for spring 2018Source: USDA, Green Markets, CME Group, Nutrien1 2017/18 margins are based on spot cash crop prices and estimated average fertilizer costs; 2018/19F margins are based on new crop 2018 futures prices less estimated basis and estimated spot retail fertilizer prices

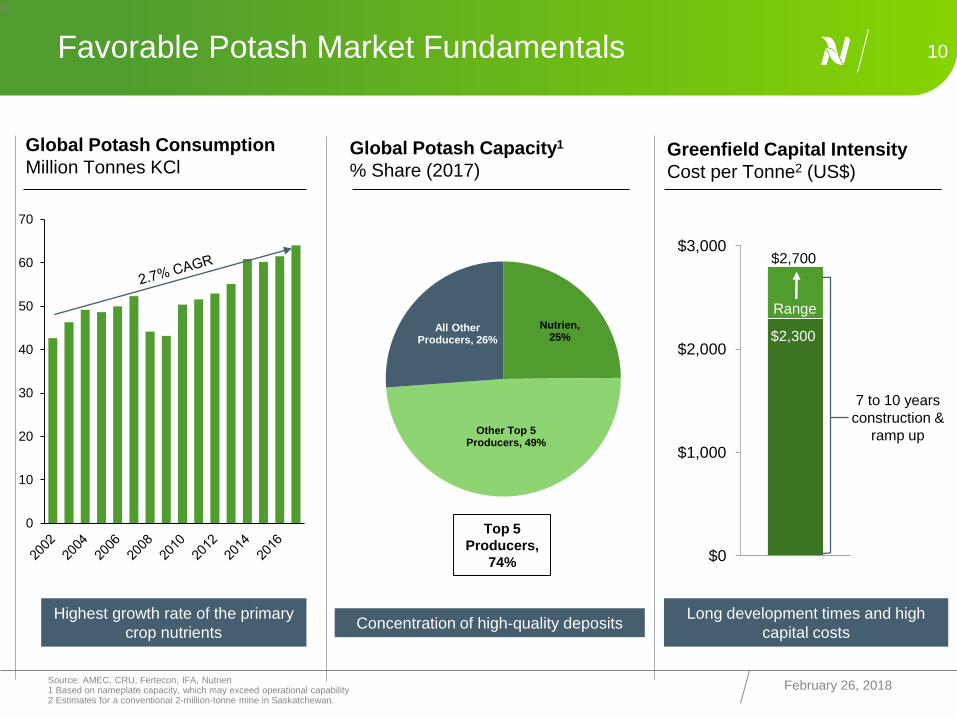

Favorable Potash Market Fundamentals

February 26, 2018

1

0

10

Highest growth rate of the primary

crop nutrients

Nutrien, 25%

Other Top 5 Producers, 49%

All Other Producers, 26%

Concentration of high-quality depositsLong development times and high

capital costs

$0

$1,000

$2,000

$3,000

0

10

20

30

40

50

60

70

Top 5

Producers,

74%

$2,700

$2,300

7 to 10 years

construction &

ramp up

Global Potash Consumption

Million Tonnes KClGlobal Potash Capacity1

% Share (2017)Greenfield Capital Intensity

Cost per Tonne2 (US$)

Source: AMEC, CRU, Fertecon, IFA, Nutrien1 Based on nameplate capacity, which may exceed operational capability 2 Estimates for a conventional 2-million-tonne mine in Saskatchewan.

Range

70%

75%

80%

85%

90%

95%

100%

Relatively Tight Potash Supply & Demand 11

February 26, 2018

0

10

20

30

40

50

60

70

80

Demand Growth @ 3.0%/yr

Demand Growth @ 2.7%/yr

Operational Capability

Global Potash S&DMillion Tonnes KCl

Global Utilization Rate1

Percent

Expect demand growth and capacity closures to offset capacity additions;

operating rates expected to be at or above historical average

Demand Growth @ 2.7%/yr*

Demand Growth @ 3.0%/yr*

Source: CRU, Fertecon, IFA, Nutrien1 Based on estimated operational capability * Demand growth based on 20 year CAGR 2002 to 2022

Tightening Global Nitrogen Supply & Demand 12

February 26, 2018

Global Nitrogen S&DMillion Tonnes Nitrogen

70%

75%

80%

85%

90%

95%

100%

0

20

40

60

80

100

120

140

160

180 Demand Operational Capability

Forecast improvement in nitrogen capacity utilization expected over the medium-term

Global Utilization Rate1

Percent

Source: CRU, Nutrien1 Based on estimated operational capability. Adjusted for idled capacity in China and Eastern Europe. * Demand growth based on 20 year CAGR 2002 to 2022

Demand Growth @ 2.0%/yr*

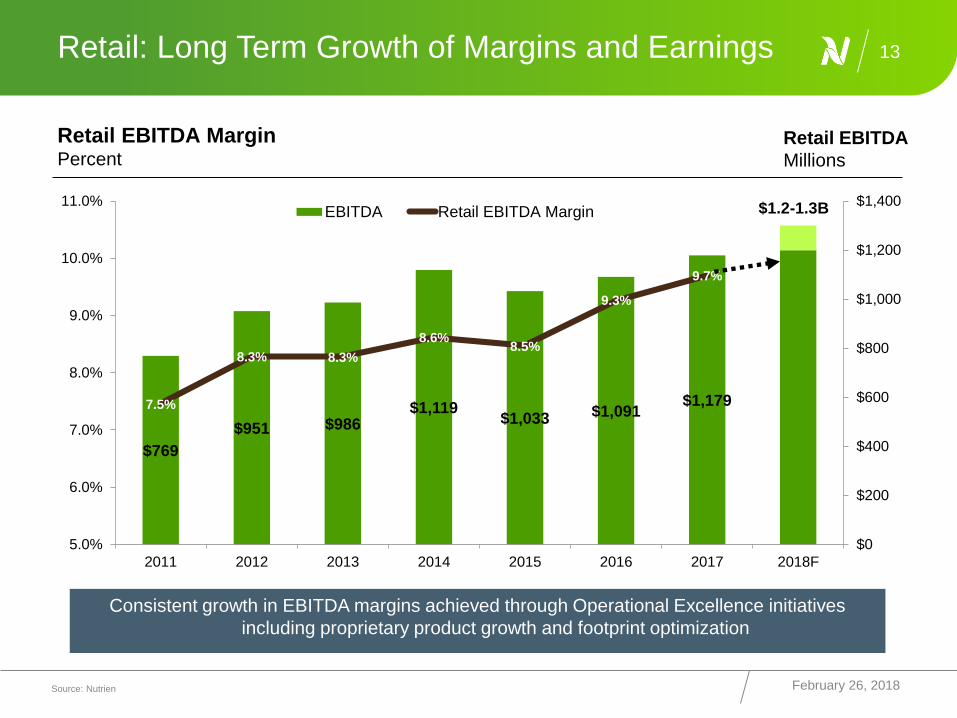

Consistent growth in EBITDA margins achieved through Operational Excellence initiatives

including proprietary product growth and footprint optimization

Retail: Long Term Growth of Margins and Earnings

February 26, 2018

13

$769

$951 $986$1,119

$1,033 $1,091$1,1797.5%

8.3% 8.3%

8.6%8.5%

9.3%

9.7%

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

11.0%

2011 2012 2013 2014 2015 2016 2017 2018F

EBITDA Retail EBITDA Margin $1.2-1.3B

Retail EBITDA MarginPercent

Retail EBITDA

Millions

Source: Nutrien

Strategy and Opportunities

INVESTOR PRESENTATION February 26, 2018

1. Complete Integration

• Bring people, systems, assets and operations together

• Complete required sales of equity investments

2. Deliver Synergies

• $500M annual run-rate expected by the end of 2019

• Costs to achieve below benchmark standards

3. Business Unit Strategy

• Complete portfolio review of combined company

• Determine key priorities for each business unit

Nutrien Strategic Priorities

February 26, 2018

15

Capital Priorities

• Continue to invest in growth opportunities – focus on Retail

• Enhance shareholder returns – dividend and share buybacks

• Strong balance sheet – maintain investment grade credit ratings

Highly confident in full synergy realization by the end of 2019. Achieved ~$60 million in run-rate

synergies year-to-date.

Significant Value Creation from Merger Synergies 16

$150

$500

$125

$100

$125

$0

$100

$200

$300

$400

$500

$600 Distribution /

Optimization• Rail Fleet

Optimization

• Distribution

and

Warehouse

Optimization

• Logistics

Savings

• Portfolio

Integration

Production

Optimization• Phosphate

Integration

• Potash

network

efficiencies

• Nitrogen

optimization

Procurement• Procurement

optimization

SG&A• SG&A

Efficiencies

Target

++

+

Expected Run-Rate SynergiesUS$ Millions

February 26, 2018Source: Nutrien

$250

End of

2019

End of

2018

~$60 YTD

2018

Nutrien to Supply Western Canada MAP Market from Increased Production at White Springs & Aurora

February 26, 2018

17

Source: Nutrien1 White Springs rock costs are lower, partly offset by higher transport cost and higher sulfur & NH3 costs, variable cost advantage varies depending on MAP price. Assumptions include: Variable cost savings ranges represent $30/mt higher and lower than 2019 MAP price forecast for Western Canada.

~15 ~15

~15 ~15

5

24

30

40

Lower P price Higher P price

0

20

40

60

80

100 ~$95M

~$65M

Phosphate and sulfate synergy potential of

~$80M made possible by the merger

Additional Potential Benefits

• Improved N.A. phosphate S/D balance

• Capital cost to convert Redwater MAP to AS

lower than other options

Lower Net

sustaining

Lower Fixed cost

Variable cost

Savings

AS expansion

Phosphate and Sulfate Synergy PotentialUS$ Millions

• Ammonium Sulphate conversion at Redwater

delivers $30-40M gross margin

• Variable cost savings = White Springs rock

costs are $140-180/mt lower than Redwater’s

delivered rock costs1

• Repurposing Redwater phosphate = lower

expected sustaining/fixed costs & running

White Springs/Aurora @ higher utilization

which lowers per tonne costs

Direct Synergy Potential

Business Unit Priorities

February 26, 2018

18

• Growth (acquisitions and proprietary products), Optimize network, Advance digital capabilitiesRetail

• Optimize network, Respond to market conditionsPotash

• Optimize network, Grow opportunisticallyNitrogen

• Deliver synergies, Optimize networkPhosphate and Sulfate

Integrated business to drive stable and growing free cash flow

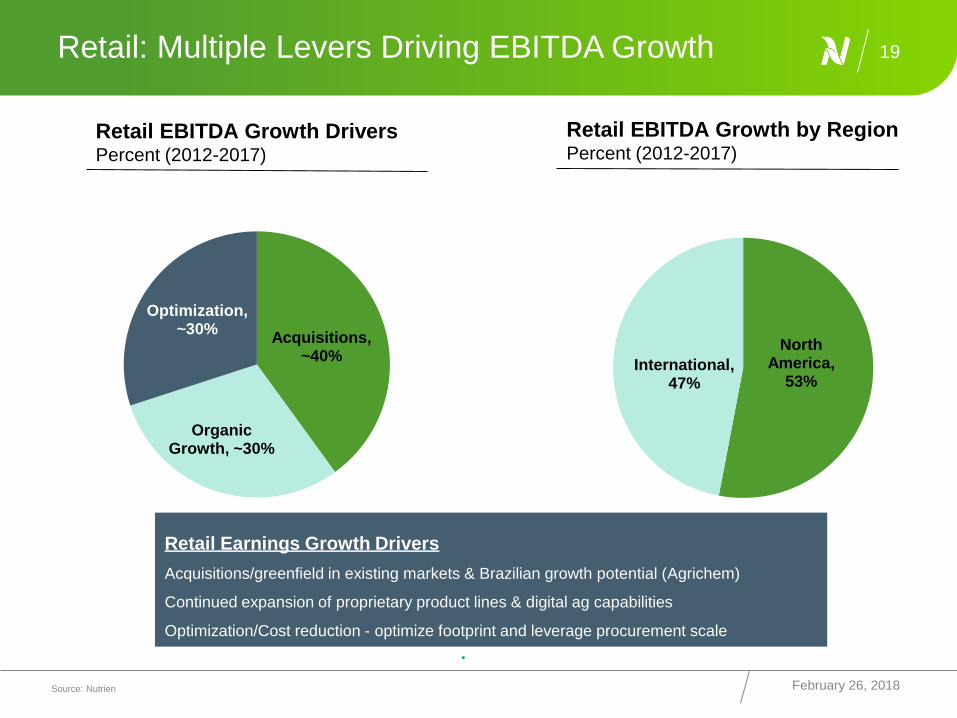

Retail: Multiple Levers Driving EBITDA Growth

Retail Earnings Growth Drivers

Acquisitions/greenfield in existing markets & Brazilian growth potential (Agrichem)

Continued expansion of proprietary product lines & digital ag capabilities

Optimization/Cost reduction - optimize footprint and leverage procurement scale

•

February 26, 2018

19

$75

$75

$75

North America,

53%International,

47%

Retail EBITDA Growth DriversPercent (2012-2017)

Source: Nutrien

Retail EBITDA Growth by RegionPercent (2012-2017)

Acquisitions, ~40%

Organic Growth, ~30%

Optimization, ~30%

Capital Allocation

INVESTOR PRESENTATION February 26, 2018

Multiple Levers to Generate Strong Free Cash Flow

February 26, 2018

21

Capture

Identified

Synergies

Stable and

Growing

Retail Base

Equity

Investment

Sales

$500M/year 1 Expect

$50-$140M of

EBITDA / Yr

~$4.5B estimated

net of tax

Fertilizer prices are more than

$100/mt lower than mid-cycle

(8 year avg prices)

Within

Nutrien’s

Control

External

Factors:

Leverage

to Upside

If fertilizer prices rise $25/mt = ~$650M EBITDA

If fertilizer prices rise $100/mt = ~$2.6B EBITDA

Capital

Priorities

Value Adding Growth

• Increase share in existing

markets (N.A & Australia)

• Focus on growing in Brazil

• Expand proprietary

business; digital ag

Enhance Shareholder

Returns

• Announced 5% NCIB

• Potential to further

increase dividend

(40-60% of FCF)

Enhance Balance Sheet

• Maintain investment grade

credit rating

1 Full $500M per year expected to be achieved by the end of 2019.

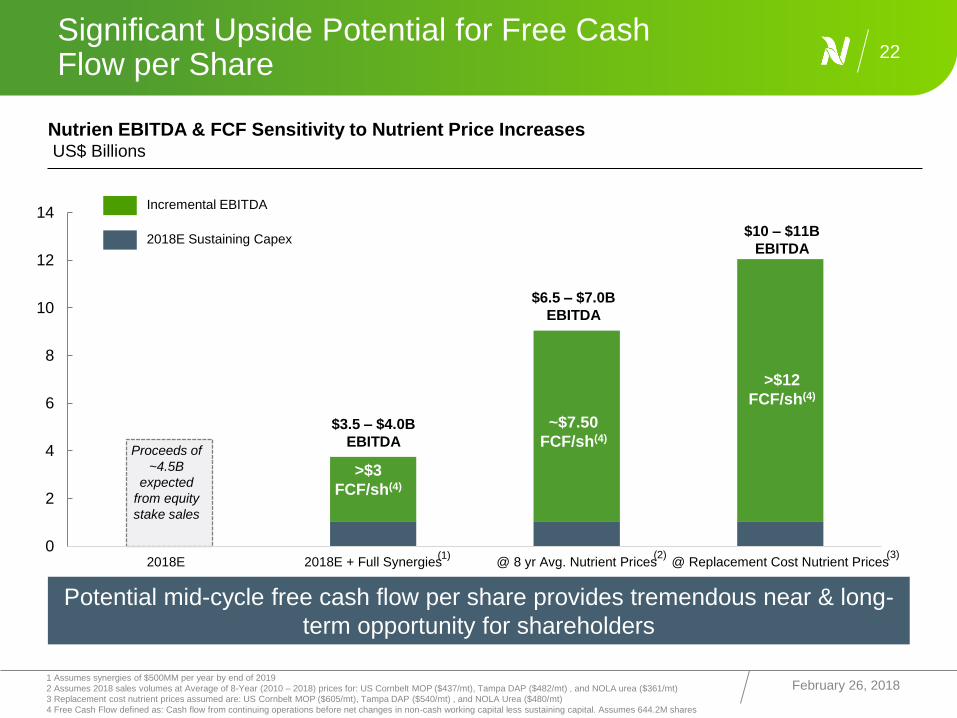

0

2

4

6

8

10

12

14

2018E 2018E + Full Synergies @ 8 yr Avg. Nutrient Prices @ Replacement Cost Nutrient Prices

$3.5 – $4.0B

EBITDA

$6.5 – $7.0B

EBITDA

$10 – $11B

EBITDA

Proceeds of

~4.5B

expected

from equity

stake sales

Significant Upside Potential for Free Cash Flow per Share

22

February 26, 2018

(1) (2)

2018E Sustaining Capex

Incremental EBITDA

1 Assumes synergies of $500MM per year by end of 2019

2 Assumes 2018 sales volumes at Average of 8-Year (2010 – 2018) prices for: US Cornbelt MOP ($437/mt), Tampa DAP ($482/mt) , and NOLA urea ($361/mt)

3 Replacement cost nutrient prices assumed are: US Cornbelt MOP ($605/mt), Tampa DAP ($540/mt) , and NOLA Urea ($480/mt)

4 Free Cash Flow defined as: Cash flow from continuing operations before net changes in non-cash working capital less sustaining capital. Assumes 644.2M shares

Potential mid-cycle free cash flow per share provides tremendous near & long-

term opportunity for shareholders

Nutrien EBITDA & FCF Sensitivity to Nutrient Price IncreasesUS$ Billions

>$3

FCF/sh(4)

~$7.50

FCF/sh(4)

(3)

>$12

FCF/sh(4)

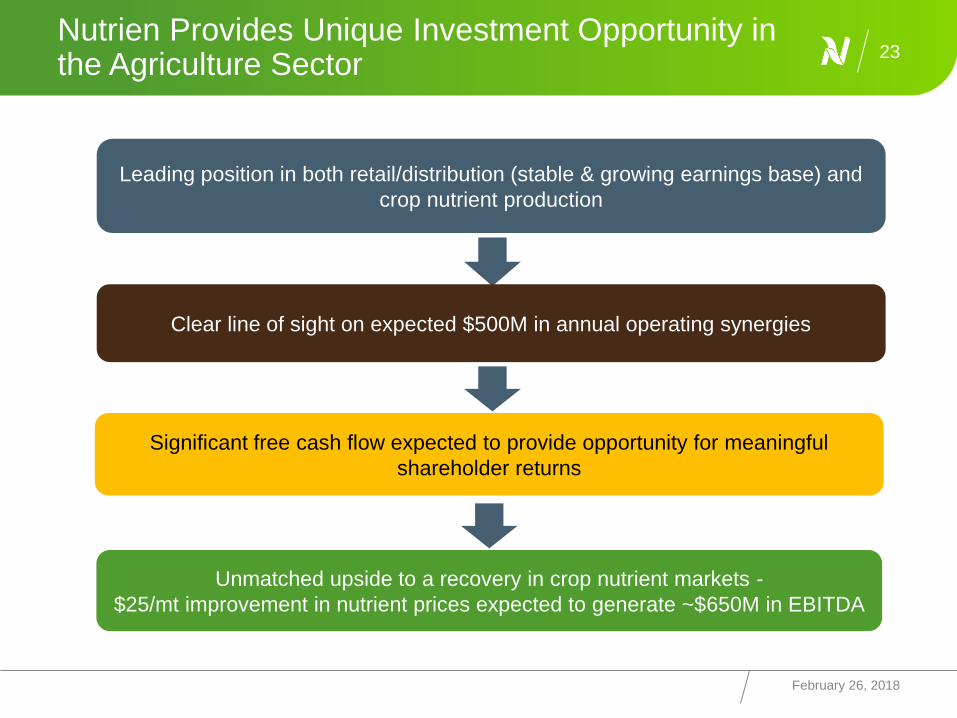

Nutrien Provides Unique Investment Opportunity in the Agriculture Sector

February 26, 2018

23

Leading position in both retail/distribution (stable & growing earnings base) and

crop nutrient production

Unmatched upside to a recovery in crop nutrient markets -

$25/mt improvement in nutrient prices expected to generate ~$650M in EBITDA

Clear line of sight on expected $500M in annual operating synergies

Significant free cash flow expected to provide opportunity for meaningful

shareholder returns

Thank you!

INVESTOR PRESENTATION February 26, 2018

For further information please visit Nutrien’s website at: www.nutrien.com

Follow Nutrien on:

twitter.com/nutrienltd

facebook.com/nutrienltd

linkedin.com/company/nutrien