investor day 2012 - issuer directedg1.precisionir.com/.../na013184/pembinadec12investorday.pdf ·...

TRANSCRIPT

INVESTOR DAY 2012

TSX: PPL

NYSE: PBA December 4, 2012

FORWARD-LOOKING STATEMENTS & INFORMATION

This presentation is for information purposes only and is not intended to, and should not be construed to constitute, an offer to sell or the

solicitation of an offer to buy, securities of Pembina Pipeline Corporation. This presentation and its contents should not be construed, under

any circumstances, as investment, tax or legal advice. Any person accepting delivery of this presentation acknowledges the need to conduct

their own thorough investigation into Pembina and its activities before considering any investment in its securities.

In the interest of providing investors with information regarding Pembina, including management's assessment of Pembina's future plans and

operations, certain statements and information contained in this presentation constitute forward-looking statements or information within the

meaning of the "safe harbour" provisions of applicable securities legislation. Such forward-looking information and statements relate to

business strategy and plans, financial performance, the stability and sustainability of cash dividends, expansion and diversification

opportunities and other expectations, beliefs, goals, objectives, assumptions or statements about future events or performances. Undue

reliance should not be placed on these forward-looking statements and information as both known and unknown risks and uncertainties may

cause actual performance and financial results to differ materially from the results expressed or implied.

Forward-looking statements and information are based on Pembina Pipeline Corporation's expectations, estimates, projections and

assumptions in light of its experience and its perception of historical trends as well as current market conditions and perceived business

opportunities. These statements are not guarantees of future performance and are subject to a number of known and unknown risks and

uncertainties including but not limited to: the impact of competitive entities and pricing; reliance on key alliances and agreements; the strength

and operations of the oil and natural gas industry and related commodity prices; regulatory environment; fluctuations in operating results; the

availability and cost of labour and other materials; the ability to finance projects on advantageous terms; and tax laws and tax treatment.

Additional information on these factors as well as other factors that could impact Pembina's operational and financial results are contained in

Pembina's Annual Information Form and Management's Discussion and Analysis, and described in our public filings available in Canada at

www.sedar.com and in the United States at www.sec.gov. Readers are cautioned that this list of risk factors should not be construed as

exhaustive.

The forward-looking statements contained in this document speak only as of the date of this document. Except as expressly required by

applicable securities laws, Pembina and its subsidiaries assume no obligation to update forward-looking statements and information should

circumstances or management's expectations, estimates, projections or assumptions change. The forward-looking statements contained in

this document are expressly qualified by this cautionary statement.

In this presentation, we refer to certain financial measures such as total enterprise value and operating margin that are not determined in

accordance with International Financial Reporting Standards ("Canadian GAAP"). For more information about these non-GAAP measures, see

note 1 in the Appendix to this presentation. All financial information is expressed in Canadian dollars unless otherwise specified.

2

AGENDA

3

Introduction Scott Burrows

Midstream – NGL Bob Lock

Overview & Value Proposition Bob Michaleski

Midstream – Crude Oil Bob Jones

Strategy & Focus Mick Dilger

Dedicated to Pipeline & Facility Integrity Allan Charlesworth

Commodity Update Murray Buchanan

Dedicated to Stakeholders Bob Michaleski

Oil Sands & Heavy Oil Michael Hantzsch

Stable Financial Platform Peter Robertson

Gas Services Stuart Taylor

Conclusion Mick Dilger

Conventional Pipelines Paul Murphy

Lunch

Break

One-on-One Meetings

OVERVIEW & VALUE PROPOSITION

Bob Michaleski

PEMBINA ATTENDEES

5

Bob Michaleski

Chief Executive Officer

Paul Murphy

Vice President, Conventional Pipelines

Stuart Taylor

Vice President, Gas Services

Bob Jones

Vice President, Midstream

Scott Burrows Senior Manager, Corporate Development

& Planning

Mick Dilger

President & Chief Operating Officer

Peter Robertson Vice President, Finance & Chief Financial

Officer

Bob Lock

Vice President, Natural Gas Liquids

Allan Charlesworth Vice President, Integrity & Technical

Services

Michael Hantzsch

Vice President, Oil Sands & Heavy Oil

Murray Buchanan

Vice President, Strategy & New Ventures

CORPORATE PROFILE

6

Common Shares Outstanding (1) 292.3 million

Current Common Share Trading Price (1) $27.79

52-Week Trading Range $24.86 - $31.15

Market Capitalization (1) $8.1 billion

Total Enterprise Value (1) $10.8 billion

Annualized Dividend $1.62/share

Effective Yield (1) 5.8%

Corporate Credit Rating BBB

(1) As at November 27, 2012.

WHERE WE OPERATE

7

Map for illustrative purposes only.

Gas Processing Plant

Redwater Fractionator

Midstream Storage Facility

Truck Terminal

Rail Terminal

Other Pembina Pipelines

Third Party Pipelines

OBJECTIVE & STRATEGY

Objective:

To provide highly competitive and reliable

returns to investors through monthly

dividends while enhancing the long-term

value of its shares. Pembina's strategy is to:

Preserve value by providing safe, cost-

effective, reliable services

Diversify our asset base along the

hydrocarbon value chain to provide

integrated service offerings which enhance

profitability and customer service

Implement growth by pursuing projects or

assets that are expected to generate cash

flow per share accretion and capture long-

life, economic hydrocarbon reserves

Maintain a strong balance sheet with

prudent financial management to all

business decisions

8

9

VALUE PROPOSITION

Efficient and well-managed assets

One of Canada's largest and most diversified energy infrastructure companies

Industry Leader

Growing demand for NGL and crude oil midstream services

Resurgence of conventional plays

Strong Demand for our Services

Large integrated asset footprint with growth potential Substantial portfolio of diversified growth opportunities Assets ideally located for increased development

Well Positioned for Growth

Track record of solid performance Strong balance sheet Stable, low-risk asset base dominated by fee-for-service revenue

Solid Business Platform

10

STRONG MARKET PERFORMANCE

490

%

total

return(1)

17.8

% average

compound

annual return(1)

4 % CAGR

in dividends

per share(1)

$2.3

billion in

dividends paid

since inception

(1) 2002 – Q3 2012.

-

$100

$200

$300

$400

$500

-

$0.50

$1.00

$1.50

$2.00

2003 2004 2005 2006 2007 2008 2009 2010 2011

Op

era

tin

g M

arg

in (

$M

M)

Cas

h F

low

($ p

er

sh

are

)

CFPS Operating Margin

STRONG FINANCIAL PERFORMANCE

11

9

% CAGR in CFPS 2003 – 2011

13

% CAGR in operating margin 2003 – 2011

FOUR GROWTH PLATFORMS

12

Conventional Pipelines

Oil Sands & Heavy Oil

Gas Services

Midstream

Growth across the hydrocarbon value chain

DELIVERING ON OUR PROMISES

13

See "Forward-Looking Statements & Information.”

-

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

Investor Day 2010

Capital Budget Presentation

2012

2011 2012F 2013 Budget 2014F+

Cap

ital E

xp

en

dit

ure

s (

$M

M)

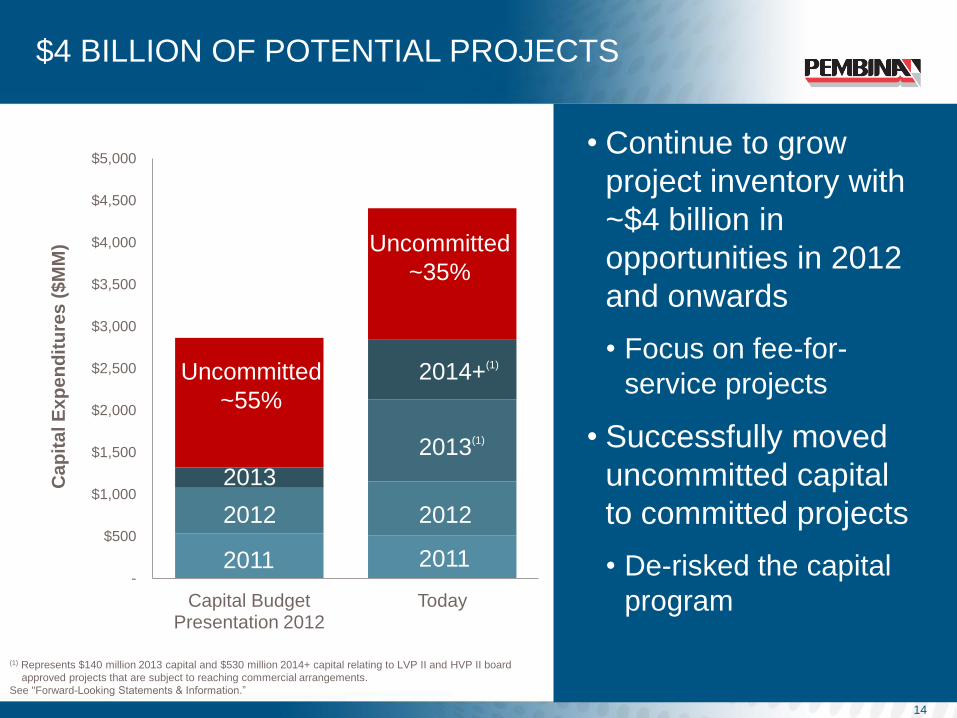

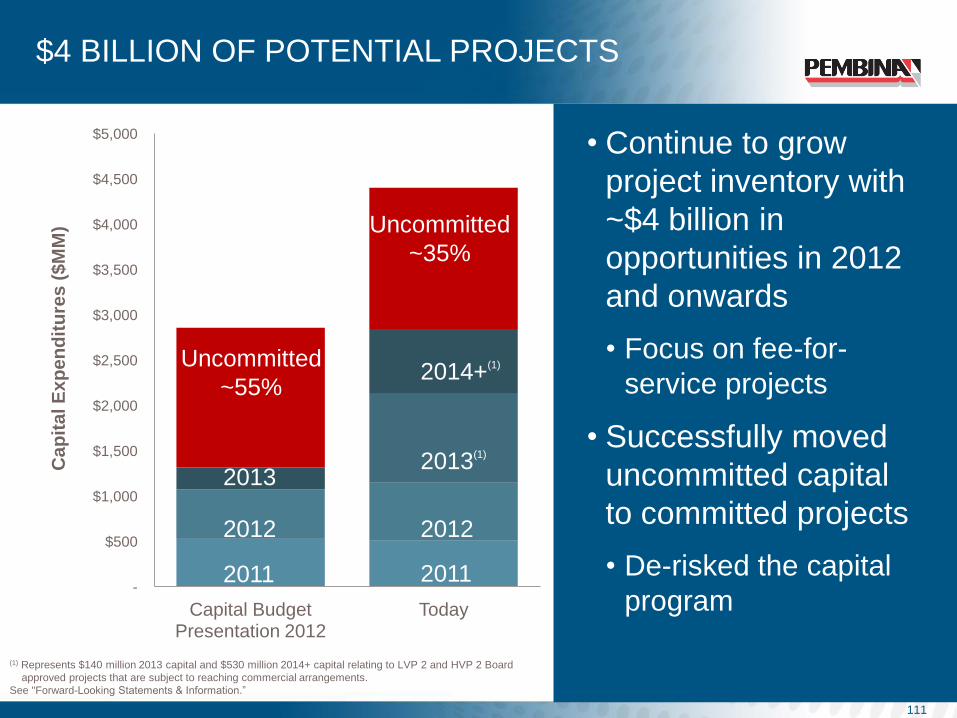

$4 BILLION OF POTENTIAL PROJECTS

• Continue to grow

project inventory with

~$4 billion in

opportunities in 2012

and onwards

• Focus on fee-for-

service projects

• Successfully moved

uncommitted capital

to committed projects

• De-risked the capital

program

14

-

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

$4,500

$5,000

Capital Budget Presentation 2012

Today

Ca

pit

al E

xp

en

dit

ure

s (

$M

M)

Uncommitted

~55%

Uncommitted

~35%

2011

2012

2013

2011

2012

2013(1)

2014+(1)

(1) Represents $140 million 2013 capital and $530 million 2014+ capital relating to LVP II and HVP II board

approved projects that are subject to reaching commercial arrangements.

See "Forward-Looking Statements & Information.”

GROWTH TRAJECTORY

• Anticipate growth

across all four

business units

largely underpinned

by customer

agreements

• Diverse asset base

and critical mass in

all businesses

allows for asset

optimization and

greater resource

capture

15

(1) A portion of which is subject to reaching commercial arrangements.

See "Forward-Looking Statements & Information.”

-

$200

$400

$600

2013 2014 2015 2016 Uncommitted 2013 - 2017

HVP/LVP Expansion Other CBU Growth

Saturn/Resthaven Nipisi/Mitsue Expansion

FST Strategy Nexus Terminal

Cavern and Other Uncommitted opportunities

Op

era

tin

g M

arg

in (

$M

M)

(1)

80%

11%

9%

Cost-of-Service & Fee-for-Service

Product Margin

Frac Spread

2016F(1,2)

SECURING OPERATING MARGIN

16

By 2016

of operating income

will be fee-for-service

or cost-of-service

Fee-for-service focused capital program

80%

(1) Represents committed capital. (2) Price deck based on the forward curve as at October 9, 2012.

See "Forward-Looking Statements & Information.”

Growing our fee-for-service and

cost-of-service business by 80% by 2016

STRATEGY & FOCUS

Mick Dilger

HIGHLY INTEGRATED BUSINESS

18

Gas/NGL

Conventional

Consumption Distribution Downstream

Upgrading

Mining/In-situ Field

Upgrading

Feeder

Pipelines Refining Collection,

Storage,

Distribution,

Marketing

Consumption Production Feeder

Pipelines

Field

Handling &

Treatment

Refining Distribution Collection,

Storage &

Distribution

Hub

Collection,

Storage,

Distribution,

Marketing

Oil Sands &

Heavy Oil

New Services

Traditional

NGL Focus

Mid

stre

am

& M

ark

etin

g C

ross C

om

mo

dity

Arb

itrag

e

Production Feeder

Pipelines Main-Line

Extraction

Collection,

Storage,

Marketing

Fractionation Logistics

& Distribution

Consumption Field

Handling &

Processing

New Services

MAJOR GEOLOGICAL PLAYS (WCSB)

19

Map for illustrative purposes only.

Gas Processing Plant

Redwater Fractionator

Midstream Storage Facility

Truck Terminal

Rail Terminal

Other Pembina Pipelines

Third Party Pipelines

MAJOR GEOLOGICAL PLAYS NATURAL GAS

20

Pembina operates within some of the most economical

natural gas resources plays in Canada

Source: Scotiabank.

Note: Red indicates fields that Pembina participates in.

-

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

Bre

ak

eve

n (

$/m

cf)

MAJOR GEOLOGICAL PLAYS CRUDE OIL

21

Fields that Pembina participates in:

-

$10

$20

$30

$40

$50

$60

$70

$80

$90

Bre

ak

eve

n (

$/b

bl)

Source: Scotiabank.

Note: Red indicates fields that Pembina participates in.

OPPORTUNITIES

22

ENVIRONMENT & TREND BUSINESSES

IMPACTED OPPORTUNITIES

Horizontal multi-frac technology

Resurgence of conventional plays

Conventional Pipelines

Gas Services

Midstream

System optimization & expansion

NGL developments

Full-service terminals

High oil-to-gas ratio

Focus on liquids-rich gas

Conventional Pipelines

Gas Services

Midstream

Expand gathering, processing and

transportation

Shallow/deep cut facilities

Fractionation

Greater heavy oil & diluent demand

Growing production

Oil Sands & Heavy Oil

Midstream

Nipisi & Mitsue expansion

New oil sands pipelines, expansions

& connections

Flexibility to capture market volatility

Energy market hubs Midstream

Hub development

Storage, rail & export terminals

Product arbitrage

See "Forward-Looking Statements & Information.“

COMMODITY UPDATE

Murray Buchanan

23

CRUDE OIL

Crude oil continues to be relatively strong

-

$20

$40

$60

$80

$100

$120

$140

$160

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

$U

S / B

BL

WTI Brent

Source: Bloomberg.

NATURAL GAS

25

Natural gas prices have started to rebound

-

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

$14.00

$16.00

$18.00

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

$U

S / M

MB

TU

Henry Hub AECO

Source: Bloomberg.

ALBERTA ETHANE SUPPLY/DEMAND

• Ethane production

mainly sold under

longer-term contract

• Demand expected to

increase in Alberta

• Petchems have

indicated plans to

expand facilities

provided sufficient

ethane supply

• Current facilities could

be debottlenecked

increasing capacity by

60,000 bpd

26

-

50

100

150

200

250

300

350

2005 2007 2009 2011 2013 2015 2017 2019 2021 2023 2025

Alberta/BC Supply Vantage Imports

Potential Cracking Capacity

Current Derivative Capacity

mb

pd

Ethane sold on a gas cost plus basis

See "Forward-Looking Statements & Information.” Source: IHS.

WTI, BRENT & MONT BELVIEU

PROPANE PRICES

27

Source: OPIS & forward strip.

Propane fundamentals have led to a divergence from historical crude relationship

-

$20

$40

$60

$80

$100

$120

$140

$160

2005 2006 2007 2008 2009 2010 2011 2012

$U

S / B

BL

WTI Mt. Belvieu Propane Differential

US PROPANE INVENTORIES

28

Source: EIA.

Inventories at levels similar to 2005, 2006 & 2009

65

66.8 67.4

69.9

71.8

61.6 59.0

69.6

64.2

60.3

73.7

50

55

60

65

70

75

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

MM

bb

ls (

En

d o

f O

cto

ber)

US PROPANE SUPPLY COMPARISON

29

Source: EIA (Historical), 2012 based on 8 months actual.

Increasing gas plant supply partially offset by lower imports

2006 Actual 2012 Forecast

40%

17%

43%

51%

8%

41% Refineries

Refineries Gas Plants Gas Plants

Imports Imports

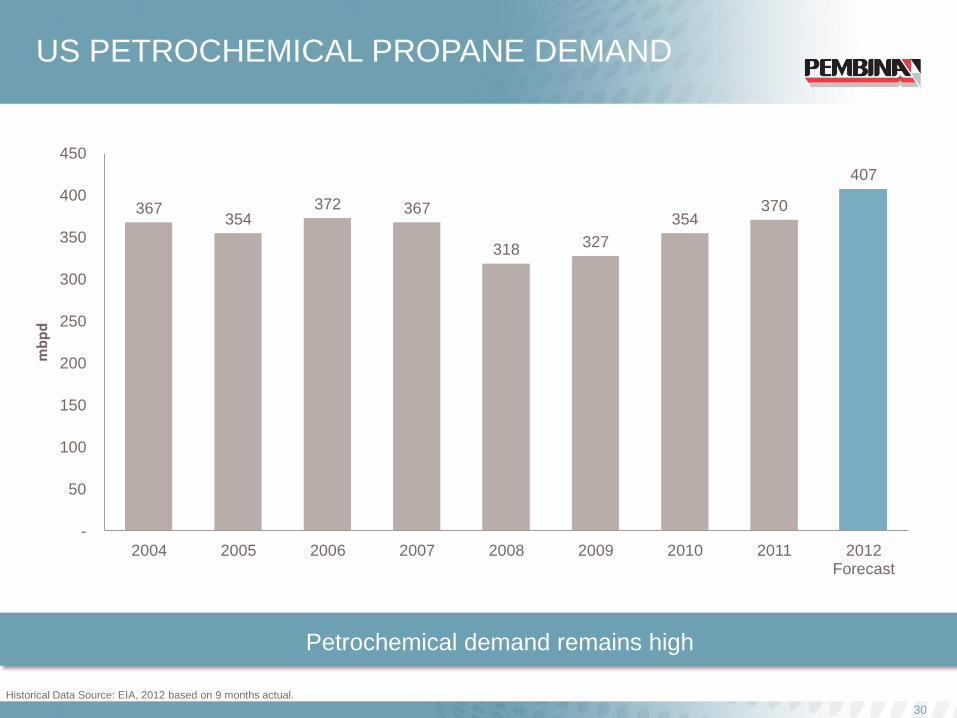

US PETROCHEMICAL PROPANE DEMAND

30

Historical Data Source: EIA, 2012 based on 9 months actual.

Petrochemical demand remains high

367 354

372 367

318 327

354 370

407

-

50

100

150

200

250

300

350

400

450

2004 2005 2006 2007 2008 2009 2010 2011 2012 Forecast

mb

pd

INTERNATIONAL SPOT PROPANE PRICES

31

Data Source: IHS.

Strong arbitrage supporting exports

$U

S/U

SG

$0.50

$0.75

$1.00

$1.25

$1.50

$1.75

$2.00

$2.25

Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12 Jul-12 Aug-12 Sep-12 Oct-12

Japan NW Europe Mont Belvieu

Spre

ad s

ignific

antly

exceeds tra

nspo

rtation

costs

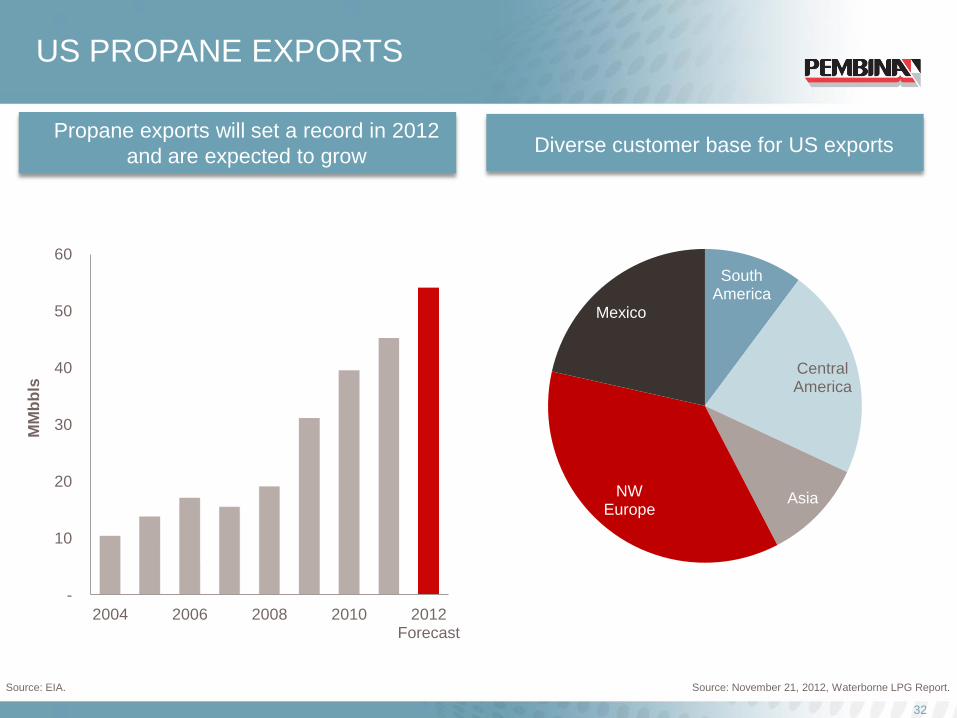

US PROPANE EXPORTS

32

MM

bb

ls

Source: EIA.

Propane exports will set a record in 2012

and are expected to grow

-

10

20

30

40

50

60

2004 2006 2008 2010 2012 Forecast

Source: November 21, 2012, Waterborne LPG Report.

Diverse customer base for US exports

South America

Central America

Asia NW Europe

Mexico

US GULF COAST LPG EXPORT CAPACITY

33

Source: Waterborne LPG Report, Company reports.

Significant export capacity is being built

MM

bb

ls p

er

Mo

nth

-

2

4

6

8

10

12

14

16

June 2012 January 2013 September 2013 December 2014

Current Capacity Enterprise Products Expansion Targa Resources Expansion - Phase 1 Targa Resources Expansion - Phase 2 Occidental Announced Terminal

WESTERN CANADIAN FIELD BUTANE

INVENTORY LEVELS

34

Source: NEB.

-

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

Apr. May Jun. Jul. Aug. Sept. Oct. Nov. Dec. Jan. Feb. Mar. Apr.

MM

bb

ls

2010/2011 2011/12 2012/13 5 YR AVERAGE

5 Year Inventory Range

Western butane inventories at low end of 5-year range

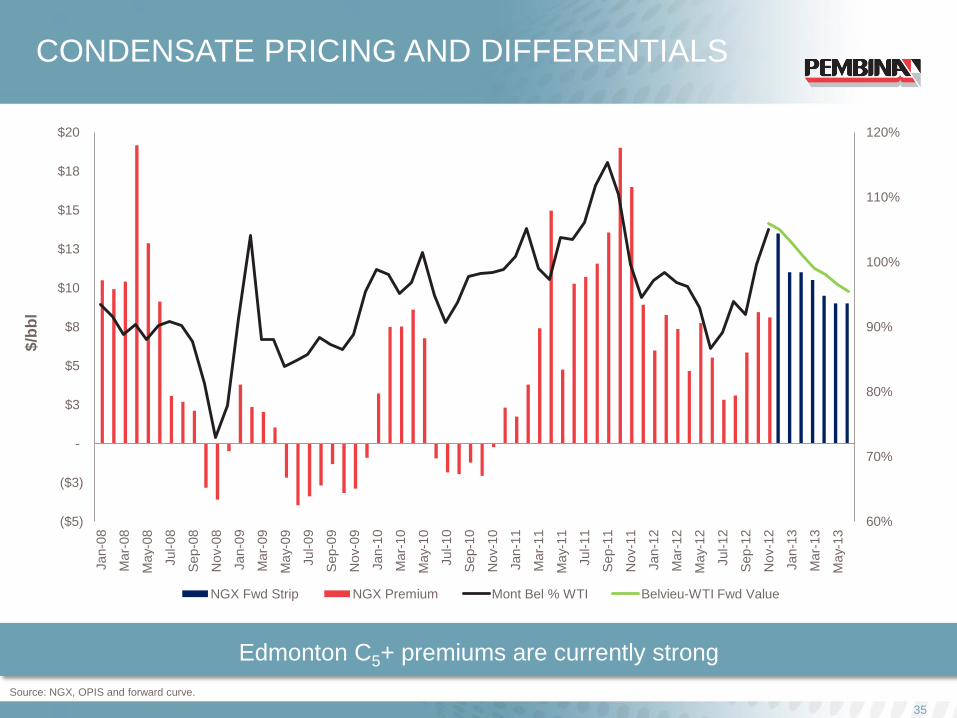

CONDENSATE PRICING AND DIFFERENTIALS

35

Edmonton C5+ premiums are currently strong

Source: NGX, OPIS and forward curve.

$/b

bl

60%

70%

80%

90%

100%

110%

120%

($5)

($3)

-

$3

$5

$8

$10

$13

$15

$18

$20

Jan-0

8

Mar-

08

May-0

8

Jul-08

Sep-0

8

Nov-0

8

Jan-0

9

Mar-

09

May-0

9

Jul-09

Sep-0

9

Nov-0

9

Jan-1

0

Mar-

10

May-1

0

Jul-10

Sep-1

0

Nov-1

0

Jan-1

1

Mar-

11

May-1

1

Jul-11

Sep-1

1

Nov-1

1

Jan-1

2

Mar-

12

May-1

2

Jul-12

Sep-1

2

Nov-1

2

Jan-1

3

Mar-

13

May-1

3

NGX Fwd Strip NGX Premium Mont Bel % WTI Belvieu-WTI Fwd Value

COMMODITY UPDATE – KEY TAKEAWAYS

• US propane export

capacity will more

than double in the

next year

• Current outlook for

butane in western

Canada is positive for

the near-term

• Demand for

condensate in

western Canada will

continue to grow with

increasing heavy oil

production

36

OIL SANDS & HEAVY OIL

Michael Hantzsch

37

38

OIL SANDS & HEAVY OIL

pipeline systems: oil sands, heavy oil, diluent 5

870 mbpd contracted capacity

10-25 year average

contract life

INDUSTRY LEADER

• Operational excellence

• 99% reliable

• Diverse connectivity to various industry hubs for crude oil and condensate

• Superior relationship with key stakeholders (aboriginal communities and producers)

• Proven track record of reliable and safe transportation services

39

Edmonton

Scotford Refinery

Cheecham Terminal

Fort McMurray

Syncrude

CNRL Horizon

Seal / Pelican Heavy Oil

Syncrude Pipeline

Horizon Pipeline

Cheecham Lateral

Nipisi Pipeline

Mitsue Pipeline

Peace Pipeline

Map for illustrative purposes only, using third-party info.

SOLID BUSINESS PLATFORM

• Contracts are long-life and provide flow through of operating expenses

• Embedded expansion opportunities on existing contracts

• Recent construction experience and assets in key locations support

future growth

40

PIPELINE SYSTEM SYNCRUDE HORIZON CHEECHAM NIPISI & MITSUE

Contracted

Capacity (bpd) 389,000 250,000(1) 136,000 127,000(2)

Contract Type Cost-of-Service Fixed Return Fixed Return Fixed Return

Initial Term 25+ years 25+ years 25+ years 10+ years

Shippers Syncrude Partnership:

Canadian Oil Sands 36.74%

Imperial Oil 25%

Suncor 12%

Sinopec 9.03%

Nexen 7.23%

Murphy 5%

Mocal 5%

CNRL Conoco

Total

Nexen

CNOOC

CNRL

Cenovus

PMLP

(1) Denotes ultimate capacity. (2) By mid-2013.

-

100

200

300

400

500

600

700

800

900

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012F 2013F

Nipisi & Mitsue Expansion

STRONG DEMAND FOR OUR SERVICES

41

See "Forward-Looking Statements & Information."

Nipisi & Mitsue

Syncrude

Syncrude expansion

Cheecham

Horizon

mb

pd

WELL POSITIONED FOR GROWTH

• Rapid growth in demand for

diluent and take-away capacity

for dilbit from heavy oil and oil

sands’ producers in Alberta

• Integrated marketing

opportunities for various

blends of dilbit

• Aggregating and terminalling

opportunities for smaller

producers

• Optimization and embedded

expansion opportunities of

existing footprint/infrastructure

42

WELL POSITIONED FOR GROWTH

DILUENT SUPPLY

43

Access to various sources of diluent supply to meet oil sands demand

Connected Condensate

Supply

Pembina’s

Access

Pembina conventional system

Redwater fractionator

Southern Lights pipeline

Rail import

Proposed Cochin pipeline

reversal (mid-2014)

Storage potential

Connected Butane Supply Pembina’s

Access

Redwater fractionator

Truck rack

Fort Saskatchewan pipeline

2013 CAPITAL PROJECTS

44

Capital Project 2013 Capital ($MM)

Nipisi & Mitsue pump stations and connectivity $25

Business development and other $20

Total $45

• Additional pump station for the Nipisi pipeline will increase system

capacity from 93,000 bpd to 105,000 bpd by the end of the second

quarter of 2013

• Additional pump station for the Mitsue pipeline will to increase system

capacity from 18,000 bpd to 22,000 bpd by the end of the third quarter

of 2013

• Adding additional terminal connection

Cap

ital E

xp

en

dit

ure

s (

$M

M)

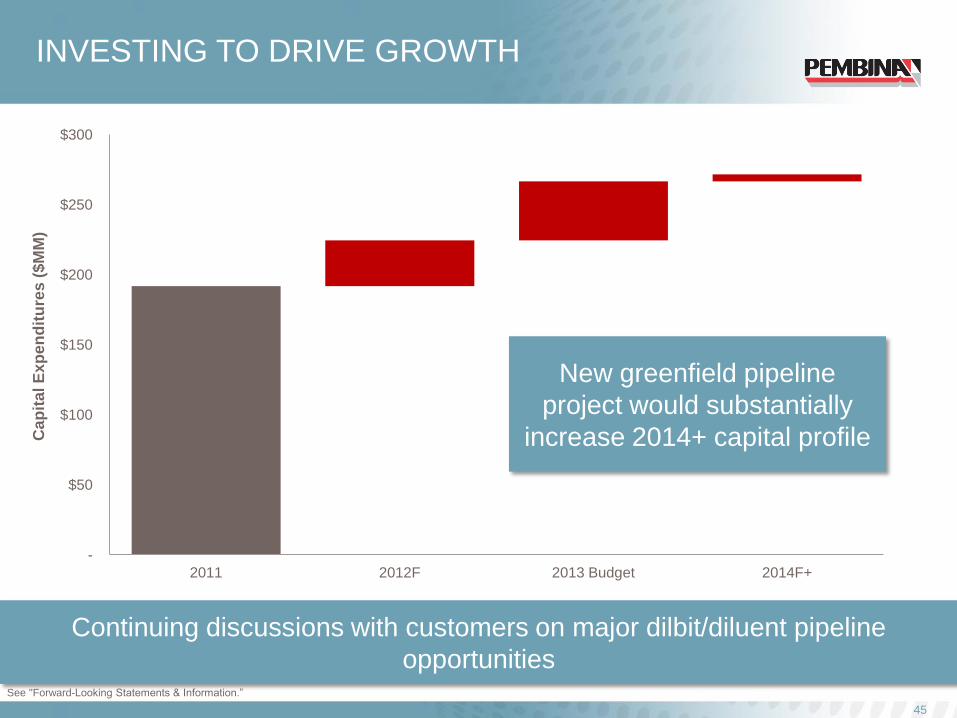

INVESTING TO DRIVE GROWTH

45

Continuing discussions with customers on major dilbit/diluent pipeline

opportunities See "Forward-Looking Statements & Information.”

-

$50

$100

$150

$200

$250

$300

2011 2012F 2013 Budget 2014F+

New greenfield pipeline

project would substantially

increase 2014+ capital profile

FUTURE OPPORTUNITIES

Nipisi expansion:

• Phase 2 – 150,000 bpd

• Full – 200,000 bpd

Mitsue expansion:

• Phase 2 – 30,000 bpd

• Full – 45,000 bpd

Horizon expansions

embedded

Support growing in-situ

operators

Working on new greenfield

pipeline project

46

GAS SERVICES

Stuart Taylor

47

48

GAS SERVICES

903 MMcf/d of net

processing capacity

by 2014

350

kilometres of

gas gathering

pipeline

368 MMcf/d net capacity at

Cutbank Complex(1)

(1) The Cutbank Complex has gross capacity of 425 MMcf/d.

See "Forward-Looking Statements & Information."

INDUSTRY LEADER

• Operational excellence

• Shallow cut 98% reliable

• High plant utilization: >85%

• Regional wells contain total

NGL of 75 -100 bbls/MMcf

• Q3 2012 processing

volume: 275 MMcf/d

• Cutbank Complex: 425

MMcf/d of sweet gas,

shallow cut processing

capacity (368 MMcf/d net to

Pembina)

• 205 MMcf/d deep cut

processing capacity at

Musreau 49

Cutbank Gas Plant

Musreau Gas Plant

Kakwa Gas Plant

Resthaven Gas Project

Younger

Taylor

Cutbank Complex

Resthaven

Saturn

Redwater

Edmonton

Fort McMurray

Fox Creek Pump Station

Saturn Gas Plant

Empress

Calgary

Gas Processing Plant

Redwater Fractionator

Pembina Pipelines

Pembina Gas Services Pipelines

Proposed Gas Services Pipelines

Map for illustrative purposes only.

ALBERTA Peace Pipeline

Peace Pipeline

SOLID BUSINESS PLATFORM

• Strategically positioned

infrastructure in active and

emerging NGL rich plays

• Provide gas gathering,

compression and shallow/deep

cut processing services

• 100% fee-for-service revenue (no

direct commodity exposure)

• Underpinned by long-term contracts

• Expansion projects are 100%

contracted, minimum 75% take-or-

pay

• Aggregate supply for Pembina’s

integrated assets to provide

comprehensive services for

producers

STRONG DEMAND FOR OUR SERVICES

51

-

100

200

300

Q3 2009

Q4 2009

Q1 2010

Q2 2010

Q3 2010

Q4 2010

Q1 2011

Q2 2011

Q3 2011

Q4 2011

Q1 2012

Q2 2012

Q3 2012

Cutbank Complex: gas processing volume

(MM

cf/

d)

See "Forward-Looking Statements & Information.”

STRONG DEMAND FOR OUR SERVICES

Shallow cut:

• Separation and recovery of an NGL mixture of

higher density hydrocarbons from raw natural

gas streams

• Achieved by cooling gas under pressure to

condense the liquids, then separating out the

NGL in a distillation column

• Shallow cut process temperatures can be as

low as -40°C

52

Recoveries Ethane (C2) Propane (C3) Butane (C4) Condensate (C5+)

Shallow Cut (C5+) ~0% ~0% Less than 2% 92+%

Shallow Cut (C3+) Less than 2% 25-35% 45-55% 95+%

Deep Cut (C2+) Up to 80% 95+% 99+% 99+%

More NGL = more value for customers

Deep cut (enhanced extraction):

• Separation and recovery of a higher amount of

NGL present in the raw natural gas streams

• Captured by cooling the natural gas stream

sufficiently to change the phase of the

components from a gas to a liquid, then

separating those two streams using distillation

• Deep cut process temperatures can be as low

as -100°C

STRONG DEMAND FOR OUR SERVICES

Why? NGL extraction yields a higher

value to producers than

otherwise realized from selling

products as gas

53

Goal

Providing producers the

opportunity to realize the highest

value for their products on a

fee-for-service basis

Provide customers with

integrated services downstream

of our processing plants

See "Forward-Looking Statements & Information.”

318

205

200

130

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

-

100

200

300

400

500

600

700

800

900

1,000

Cutbank Musreau Shallow Expansion

Saturn Resthaven Total Processing Capacity

Total Liquids Extraction Capacity (bpd)

50

STRONG DEMAND FOR OUR SERVICES

54

40,000 bpd of NGL Conventional Pipelines Fractionation Market

MM

cf/

d

Under Construction 2013/14

bp

d

See "Forward-Looking Statements & Information.”

In-Service

903 MMcf/d

Contracted Growth

WELL POSITIONED FOR GROWTH

Map for illustrative purposes only.

• Assets strategically placed to support growth in Duvernay, Montney, Cardium and Deep Basin

• Multiple geological zones with material liquids content enhancing producer economics

• New developments require significant increase in gas processing infrastructure

• Significant land purchases and drilling activity in last two years in liquids rich areas serviced by Pembina’s gas plants

• Close proximity to and integrated with existing Pembina infrastructure

CALGARY

EDMONTON

FORT

MCMURRAY

Fort Saskatchewan

Ethylene Storage

Montney

Cardium

Duvernay

Deep Basin

Musreau

Kakwa Resthaven

Saturn

Cutbank

Source: Accumap; Map displays all gas

wells drilled and land purchases made since

January 2010.

55

2013 CAPITAL PROJECTS

56

• Two deep cut facilities with 400 MMcf/d (330 MMcf/d net to Pembina)

liquids extraction capacity

• Additional compression at the Cutbank Complex to increase throughput

See "Forward-Looking Statements & Information.”

Capital Project 2012 Capital

($MM)

2013 Capital ($MM)

2014+ Capital ($MM)

Saturn $75 $90

Resthaven $45 $95 $20

Cutbank Complex Upgrades,

Other $50 $30

Total $170 $215 $20

CONSTRUCTION MILESTONES:

SATURN & RESTHAVEN

57

Saturn

To Date

Next

Steps

• Ordered 96% of long-lead equipment

• Obtained ERCB and regulatory approval

• Completed stakeholder consultation

• Plant site construction 30% complete

• ~60 % of costs secured

• Complete gas plant construction by Q4 2013

• Commission pipelines by Q4 2013

• In-service: Q4 2013

Resthaven

To Date

Next

Steps

• Ordered 80% of long-lead equipment

• Obtained ERCB and regulatory approval

• Completed stakeholder consultation

• Plant site construction 5% complete

• ~55 % of costs secured

• Complete gas plant construction by Q1 2014

• Commission pipeline by Q1 2014

• In-service: Q1 2014

See "Forward-Looking Statements & Information.”

INVESTING TO DRIVE GROWTH

-

$100

$200

$300

$400

$500

$600

2011 2012F 2013 Budget 2014F+

Cap

ital E

xp

en

dit

ure

s (

$M

M)

58

Pembina is investing to support producer requirements

See "Forward-Looking Statements & Information.”

FUTURE OPPORTUNITIES

• High utilization of Pembina’s

existing facilities is driving

possible expansions

• Requests for nominations

outstanding for:

• Additional 200 MMcf/d

shallow cut expansion at

Musreau

• Additional 200 MMcf/d deep

cut expansion at Saturn (a

twin of the initial facility)

• Gas plants to support

producer development and

growth of the Duvernay

59

See "Forward-Looking Statements & Information.”

CONVENTIONAL PIPELINES

Paul Murphy

60

61

CONVENTIONAL PIPELINES

7,850

kilometres

of pipeline

50

% of Alberta's conventional

crude oil production transported

on Pembina's systems

30

% of NGL produced in

western Canada

transported on Pembina's

systems and growing

696

mbpd current

throughput

capacity(1)

(1) Includes Drayton Valley expansion completed in 2012.

INDUSTRY LEADER

62

Northern System

Swan Hills System

Bonnie Glen System (50% Operated)

Brazeau NGL System

NEBC/Western System

Peace System

Drayton Valley System

Liquids Gathering System (LGS)

Map for illustrative purposes only.

• Operational excellence

• 99% reliable

• Proximal to prolific geology

• Q3 2012 throughput: 444

mbpd

• Q4 2012 to-date

throughput: 464 mbpd(1)

• Connected to refineries and

export pipelines

• Over 300 receipt points

adding diversity to

producers and product type

Kamloops

Calgary

Caroline

Edmonton Drayton

Valley

Whitecourt

Grande Prairie

Fort St John

Swan Hills

Valleyview

Fort McMurray

Taylor

Dunvegan

Fort Saskatchewan

(1) Q4 to date ending Nov 27, 2012.

SOLID BUSINESS PLATFORM

• 100% of revenue is fee-for-service

• No direct commodity exposure

• Expansions underpinned by long-term

contracts

• Established infrastructure captures

incremental production from major

resources plays

• Diversification in geology and geography

• Tightening pipeline capacity has

customers requesting firm service

(take-or-pay) arrangements

• Continued construction of major

gathering laterals into existing and

new service areas

• Excellent customer relations

63

-

100

200

300

400

500

Q1 2009 Q2 2009 Q3 2009 Q4 2009 Q1 2010 Q2 2010 Q3 2010 Q4 2010 Q1 2011 Q2 2011 Q3 2011 Q4 2011 Q1 2012 Q2 2012 Q3 2012 Q4 to date

Crude & Condensate NGL

374 mbpd

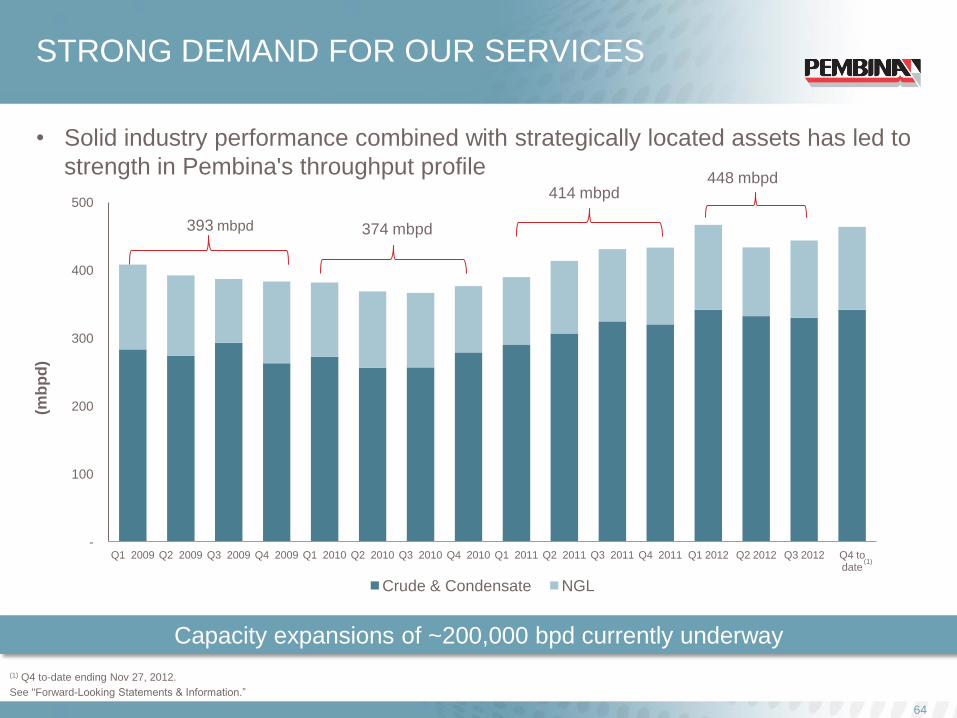

STRONG DEMAND FOR OUR SERVICES

64

• Solid industry performance combined with strategically located assets has led to

strength in Pembina's throughput profile 414 mbpd

448 mbpd

(mb

pd

)

393 mbpd

Capacity expansions of ~200,000 bpd currently underway

(1) Q4 to-date ending Nov 27, 2012.

See "Forward-Looking Statements & Information.”

(1)

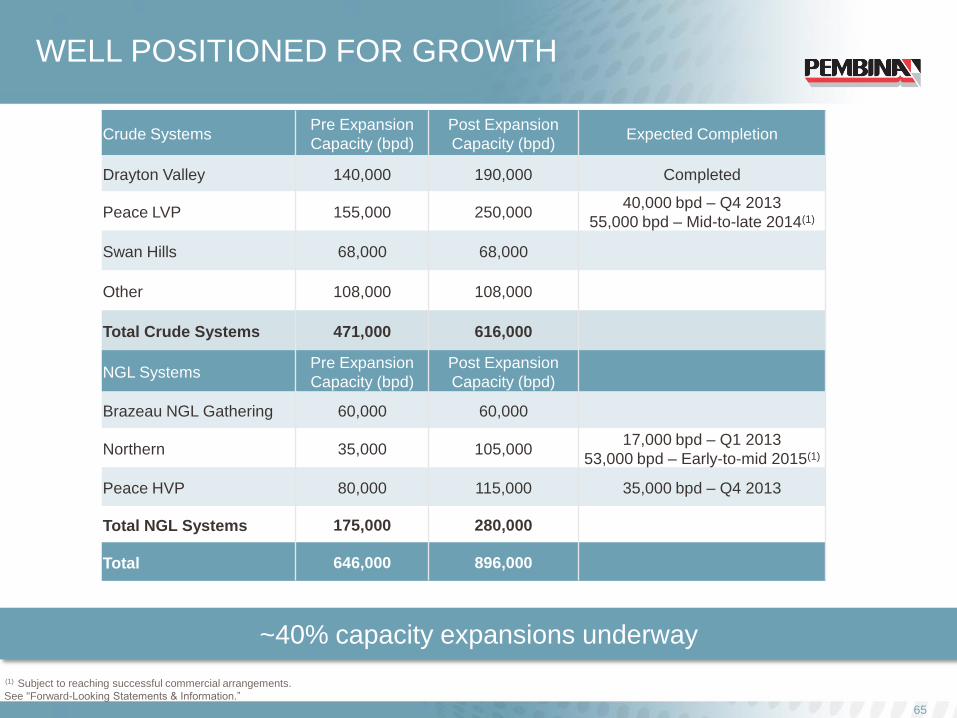

WELL POSITIONED FOR GROWTH

65

Crude Systems Pre Expansion

Capacity (bpd)

Post Expansion

Capacity (bpd) Expected Completion

Drayton Valley 140,000 190,000 Completed

Peace LVP 155,000 250,000 40,000 bpd – Q4 2013

55,000 bpd – Mid-to-late 2014(1)

Swan Hills 68,000 68,000

Other 108,000 108,000

Total Crude Systems 471,000 616,000

NGL Systems Pre Expansion

Capacity (bpd)

Post Expansion

Capacity (bpd)

Brazeau NGL Gathering 60,000 60,000

Northern 35,000 105,000 17,000 bpd – Q1 2013

53,000 bpd – Early-to-mid 2015(1)

Peace HVP 80,000 115,000 35,000 bpd – Q4 2013

Total NGL Systems 175,000 280,000

Total 646,000 896,000

(1) Subject to reaching successful commercial arrangements.

~40% capacity expansions underway

See "Forward-Looking Statements & Information.”

2013 CAPITAL PROJECTS

66

See "Forward-Looking Statements & Information.”

(1) Subject to reaching successful commercial arrangements.

Capital Projects 2012 Capital

($MM)

2013 Capital ($MM)

2014+ Capital ($MM)

Peace Crude & Condensate

Expansion Phase 1 $5 $20

Peace Crude & Condensate

Expansion Phase 2(1) $70 $145

NGL System Expansion Phase 1 $45 $50

NGL System Expansion Phase 2(1) $70 $260

Saturn and Resthaven Liquids

Pipelines $45 $55

Other Tie-Ins and Upgrades $110 $90 $125

Total $205 $355 $530

Whitecourt Ps

Valleyview Ps

Glenevis Ps

Mayerthorpe Whitecourt

Grande

Praire

Dawson Creek

Fox Creek Ps

Tony Creek Ps

Kakwa Ps

Lator Ps

Bald Mtn. Ps

La Glace Ps

Wapiti Ps

Gordondale Ps

Gilwood ps

Dunvegan

Belloy

Upgrade

Valleyview

Pump Station

New 50 mbbl C5+

Storage

New Smoky River

Pump Station

New LVP Pump Station

Pump Station Upgrades

New HVP Pump Station

HVP Storage

LVP Storage

New Pipeline

Gordondale to Valleyview:

2 upgrades & 2 new pump stations

Fox Creek to Edmonton:

3 upgrades & 3 new pump stations

Proposed New Operation:

1. Redirect LGS to Northern

System at Spirit River

2. Use LGS (south leg) for LVP

Gordondale to LaGlace

CURRENT EXPANSIONS: LVP PHASE 1 & 2

67

BC AB

LVP Phase 1 expansion to 195 mbpd;

Phase 2 expansion to 250 mbpd

Upgrade LaGlace

Pump Station

• Crude oil and condensate volumes on the Peace Pipeline system are

expected to increase. To support this growing production, Pembina plans

to increase capacity in two phases:

• Phase 1 LVP expansion: expand crude oil and condensate capacity by

an additional 40,000 bpd to reach 195,000 bpd by the end of 2013

• Phase 2(1) expansion: add an additional 55,000 bpd of capacity; can be

brought into service in mid to late-2014

• Once complete, the proposed expansions will increase capacity by 91

percent to 250,000 bpd

• Limited new pipeline build means low environmental risk

68

MAJOR EXPANSION – LVP

(1) Phase 2 subject to commercial arrangements.

WHITECOURT PS

VALLEYVIEW

PS

GLENEVIS PS

Mayerthorpe

Edson

Whitecourt

VALLEYVIEW Grande

Prairie

Dawson

Creek

Taylor

Ft. St. John

FOX CREEK

PS TONY

CREEK PS

KAKWA PS

LATOR

PS

BALD MTN. PS

LA GLACE PS

WAPITI PS

GORDONDALE PS

GILWOOD PS

BC AB

Dunvegan

Belloy

2 HVP pump station

upgrades & 3 new HVP

pump stations

Additional HVP storage at Spirit River &

HVP pipeline from Doe to Spirit River

New 24” HVP pipeline

Namao to Fort

Saskachewan/Redwater

Re- direct Swan Hills

crude to Peace

North HVP to 16”

pipeline

New HVP Pump Stations

Upgrade Existing HVP Pump Stations

Peace HVP Phase 1 Expansion

New LVP Pump Stations

New LVP Storage

New HVP Storage

Upgrade Wapiti pump station

reverse excess volumes from

Peace to Northern system

Install wc breakout

tanks for LVP

CURRENT EXPANSIONS: HVP PHASE 1 & 2

HVP Phase 1 expansion to 167 mbpd;

Phase 2 expansion to 220 mbpd

• Producer activity focused on NGL development continues to be strong in

the Deep Basin Cretaceous, Montney and Duvernay resource plays

served by the Peace and Northern Systems ("NGL System")

• Phase 1 NGL expansion: expand capacity on Pembina’s NGL Systems

by an additional 52,000 bpd to reach 167,000 bpd by the end of 2013

• Phase 2(1) expansion: add an additional 53,000 bpd of capacity; can be

brought into service in early to mid-2015

• Once complete, the proposed expansions will increase capacity by 61

percent to 220,000 bpd

• Limited new pipeline build means low environmental risk

70

MAJOR EXPANSION – HVP

(1) Phase 2 subject to commercial arrangements.

INVESTING TO DRIVE GROWTH

71

Resurging conventional plays continue to provide growth platform

-

$200

$400

$600

$800

$1,000

$1,200

$1,400

2011 2012F 2013 Budget 2014+ Est.

Ca

pit

al E

xp

en

dit

ure

s (

$M

M)

See "Forward-Looking Statements & Information.”

(1) Phase 2 subject to commercial arrangements.

(1) (1)

Kamloops

Calgary

Caroline

Edmonton

Grande Prairie

Fort St John

Swan Hills

Valleyview

Fort McMurray

Taylor

Dunvegan

Fort Saskatchewan

FUTURE OPPORTUNITY: DUVERNAY

72

Northern System

Swan Hills System

Bonnie Glen System (50% Operated)

Brazeau NGL System

NEBC/Western System

Peace System

Drayton Valley System

Liquids Gathering System (LGS)

Map for illustrative purposes only.

ALBERTA

• Well-positioned to capture

Duvernay growth

• Estimated reserves of 477 Tcf of

gas and 19 billion barrels of oil

• Since 2009 ~$4.5 billion has

been raised in land sales

-

$500

$1,000

$1,500

$2,000

$2,500

Kaybob Willesden Green Edson

To

tal L

an

d S

ale

P

roceed

s -

D

uv

ern

ay (

$M

M)

Source: TD Securities, geoScout.

-

20

40

60

80

100

120

Kaybob Willesden Green Edson

To

tal W

ell L

icen

ses -

D

uv

ern

ay

FUTURE OPPORTUNITIES

• Capacity expansions

can be implemented

incrementally and

efficiently as service

area production

grows

• Growth in alternate

delivery locations

• New service areas

• Exploit underutilized

assets

73

10 seconds each, =

MIDSTREAM – NGL

Bob Lock

75

76

NGL MIDSTREAM: REDWATER WEST

73

mbpd fractionation

capacity

6.8 MMbbls net specification

product storage 80

mbpd

condensate rail

terminal

355

MMcf/d net extraction

capacity(1)

(1) The Younger extraction facility has gross capacity of 750 MMcf/d.

77

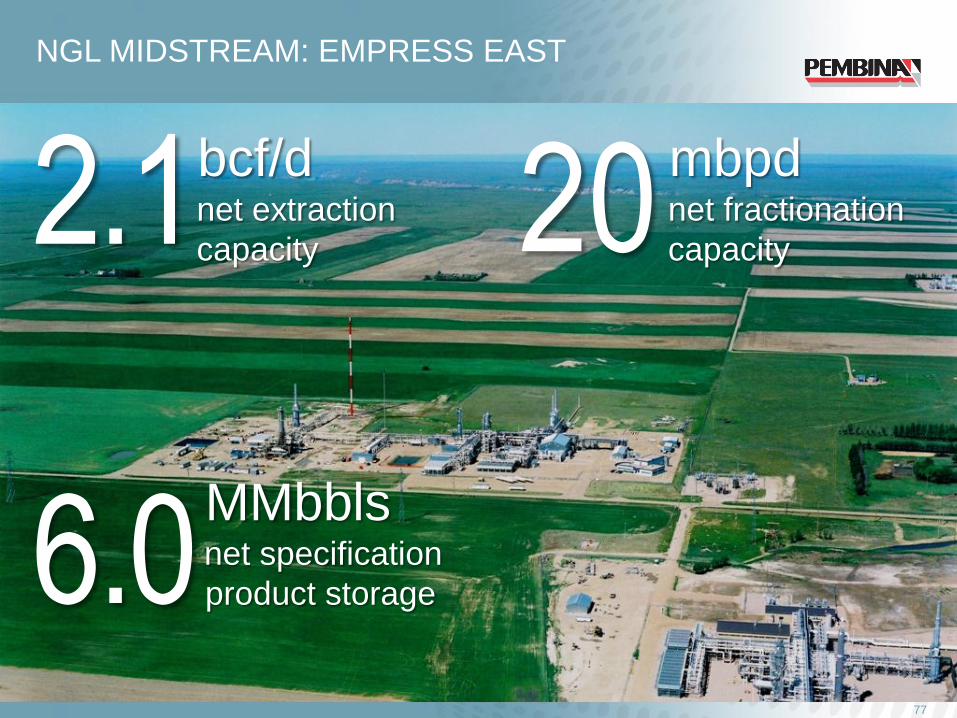

NGL MIDSTREAM: EMPRESS EAST

2.1

bcf/d

net extraction

capacity 20

mbpd

net fractionation

capacity

6.0 MMbbls net specification

product storage

INDUSTRY LEADER

Redwater West:

• Operational excellence: >87% reliability

• Positioned to capture emerging liquids growth

opportunities

• Large-scale, sulphur capable ethane-plus

fractionation

• Largest NGL rail yard in Canada

Empress East:

• Operational excellence: >98% reliability

• Most efficient plants

• Full condensate recovery at Empress

• Enbridge pipeline access to east/central North

American propane and butane markets

78

Empress Cromer

Sarnia

Coruna

Lynchburg

12.8 MMbbl (net) commercial cavern storage

Redwater

Taylor

Gas Processing Plant

Redwater Fractionator

Midstream Storage Facility

Truck Terminal

Rail Terminal

Pembina Pipelines

Third Party Pipelines

Map for illustrative

purposes only.

INDUSTRY LEADER

• Large, competitive

Alberta NGL supply

footprint

• Integrated facilities and

operations across the

continent

• Large scale, versatile

NGL rail fleet and

storage facilities

• Established and

effective marketing

team

79

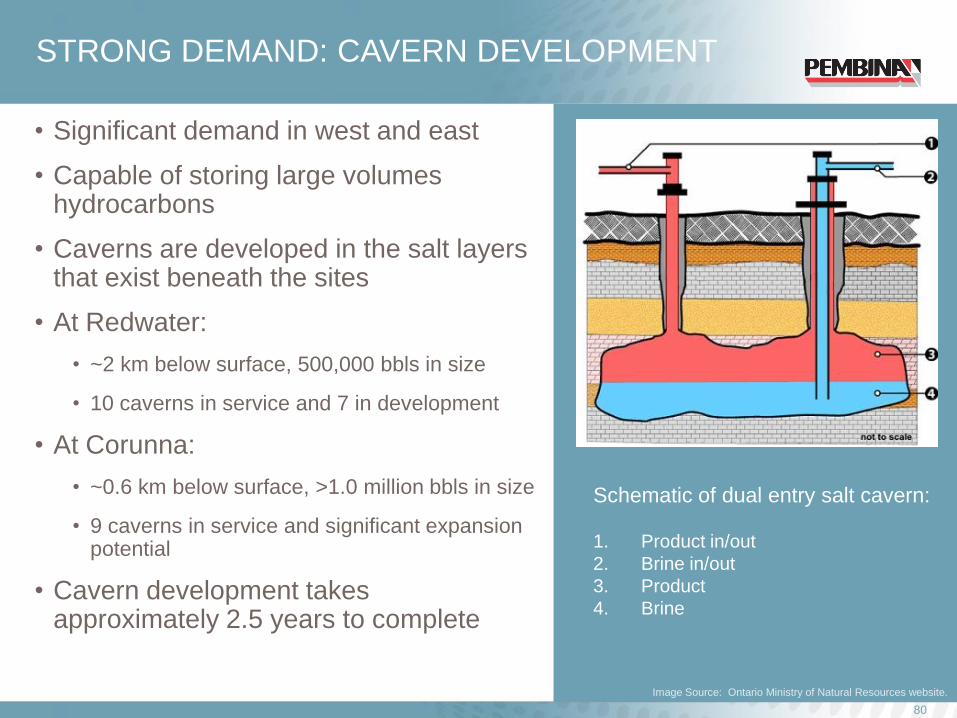

STRONG DEMAND: CAVERN DEVELOPMENT

• Significant demand in west and east

• Capable of storing large volumes hydrocarbons

• Caverns are developed in the salt layers that exist beneath the sites

• At Redwater:

• ~2 km below surface, 500,000 bbls in size

• 10 caverns in service and 7 in development

• At Corunna:

• ~0.6 km below surface, >1.0 million bbls in size

• 9 caverns in service and significant expansion potential

• Cavern development takes approximately 2.5 years to complete

80

Image Source: Ontario Ministry of Natural Resources website.

Schematic of dual entry salt cavern:

1. Product in/out

2. Brine in/out

3. Product

4. Brine

2013 CAPITAL PROJECTS

81

See "Forward-Looking Statements & Information."

(1) Subject to reaching commercial arrangements. (2) Includes 9 months of capital.

Capital Project 2012 Capital(2)

($MM)

2013 Capital ($MM)

2014+ Capital ($MM)

Redwater West:

Cavern & Storage Development $100 $90 $40

Terminalling & Connectivity $35 $45

Other $45 $30

Empress East:

Cavern & Storage Development $10 $15 $5

Terminalling & Connectivity $10

Other $10 $20

Total $165 $200 $90

Redwater Fractionator II(1) $15 $410

WELL POSITIONED FOR GROWTH

FORT SASKATCHEWAN FRACTIONATION FULL

Development of RFS II:

• Current WCSB C2+ supply

exceeds existing Alberta C2+

fractionation capacity

• Near-term forecast for

incremental WCSB C2+

production is strong

• Advancing plans to double the

size of Redwater

• Incremental 73,000 bpd of C2+

fractionation capacity and full

NGL service offering

• Anticipated on-stream Q4 2015

82

See "Forward-Looking Statements & Information.”

INVESTING TO DRIVE GROWTH

83

Liquids-rich gas development driving demand for downstream infrastructure

Note: Chart includes capital spent by Provident Energy Ltd.

-

$100

$200

$300

$400

$500

$600

$700

2011 2012F 2013 Budget 2014F+

Cap

ital E

xp

en

dit

ure

s (

$M

M)

See "Forward-Looking Statements & Information.”

84

v

LPG

Terminal

Fractionation Rail

Transport

VLGC

Export

Demand

Petchem

Plants

Autogas

Propane

Cylinders

Pipelines

Potential

Partner

FUTURE OPPORTUNITIES

PROPANE EXPORT

• Propane production surplus in North America, including WCSB

• World markets responding to low North American prices

• Asian interest in North American supply, including west coast options

• Supports additional fractionation capacity in Alberta

MIDSTREAM – CRUDE OIL

Bob Jones

85

86

MIDSTREAM – CRUDE OIL

21

inbound

pipeline

connections

21

truck terminals

located across

pipeline network 3 hub locations in the

Edmonton / Fort

Saskatchewan area form

PNT

13

outbound

pipeline

connections

1,150

mbpd of volume

transported through

connected pipelines

INDUSTRY LEADER

• Develop and provide terminal, hub & storage services to support the energy industry

• 630,000 barrels of above ground crude oil and condensate storage capacity

• Potential to expand up to 3,000,000 barrels

87

Gas Processing Plant

Redwater Fractionator

Midstream Storage Facility

Truck Terminal

Rail Terminal

Midstream Operations

Other Pembina Pipelines

Third Party Pipelines

PRINCE GEORGE

TAYLOR

KAMLOOPS CALGARY

EDMONTON

FORT

MCMURRAY

VANCOUVER

PEMBINA

NEXUS

TERMINAL

Map for illustrative purposes only.

SOLID BUSINESS PLATFORM

• Integrated revenue stream

• Liquids capture and

terminaling supports

growth for other Pembina

business units

• Interconnectivity increases

options for customers

• Increasing fee-for-service

revenue through

development of FST,

storage and other services

• Upside opportunities in

various market conditions

88

STRONG DEMAND FOR OUR SERVICES

Customer support for truck terminals:

• Bringing ~60,000 bpd on to Pembina's

conventional pipelines(1)

Increasing connectivity at PNT:

• 5 diluent streams

• Fully connected – increased access of

Pembina's pipelines to terminal

• Growth platform – dilbit

• Restored export capability for terminal

to Enbridge; working on TMPL –

Kinder Morgan

89

(1) 2012 YTD Average.

2013 CAPITAL PROJECTS

90

• Converting two existing truck terminals to FSTs and constructing three

new greenfield locations

• Develop 300,000 bbls of above ground storage at ENT

• Crude oil rail on-loading potential of 40,000 bpd

• Pipeline development connecting ENT to Redwater

See "Forward-Looking Statements & Information.”

Capital Project 2012 Capital ($MM)

2013 Capital ($MM)

2014+ Capital ($MM)

PNT terminal and

interconnection growth $10 $75 $20

Full-service truck

terminals $25 $40 $40

Other $20 $15

Total $55 $130 $60

WELL POSITIONED FOR GROWTH

91

Namao Hub

Peace Pipeline

Northern Pipeline

Swan Hills Pipeline

Nipisi Pipeline

Brazeau Pipeline

Cloverbar Hub

Pembina Redwater

Fractionator

ENT

Parcel A

Bonnie Glen Pipeline

Drayton Valley Pipeline

Imperial Refinery

TMLP Kinder Morgan

Export Pipeline

Suncor Refinery

Enbridge Export Pipeline

Other Fracs/Storage:

Dow, Keyera, Plains

Shell Scotford Refinery

Horizon Pipeline

Syncrude Pipeline

Enbridge

Southern Lights Pipeline

Pembina Nexus Terminal

Edmonton Area

Pembina Pipelines

Pipelines by others

Future Pembina Pipelines

Plains Rainbow Pipeline

CN & CP Rail Opportunities

Truck and Rail

Opportunities

Edmonton Pipeline Alley

WELL POSITIONED FOR GROWTH: FST

92

MONTNEY

DEEP BASIN

SWAN HILLS

CARDIUM

SLAVE POINT

SEAL

PELICAN LAKE

Map for illustrative purposes only.

PRINCE GEORGE

TAYLOR

KAMLOOPS CALGARY

EDMONTON

FORT MCMURRAY

Fort Saskatchewan Ethylene

Storage

DUVERNAY

Pembina Pipelines

Existing terminals

FST Prospects

2012/2013 FST Developments

Five FST locations to be developed in 2013 See "Forward-Looking Statements & Information.”

-

$50

$100

$150

$200

$250

$300

$350

$400

2011 2012F 2013 Budget 2014F+

Cap

ital E

xp

en

dit

ure

s (

$M

M)

INVESTING TO DRIVE GROWTH

93

Significant growth opportunities in terminal and hub services

See "Forward-Looking Statements & Information.”

FUTURE OPPORTUNITIES

PNT expansion

• Terminal integration complete

• Redwater and PNT connected

• Redwater and Heartland

connected

• Proprietary rail fleet for crude oil

and condensate service

Redwater oil development

• CN connection

• Salt cavern storage

Heartland development

• Surface and salt cavern storage

• East-west connector to oil sand

and diluent pipelines

PNT development

• High capacity export line to

Enbridge

• Surface storage development

• CP/CN rail connection

Hardisty development

• Terminalling and storage

94

See "Forward-Looking Statements & Information.”

DEDICATED TO PIPELINE & FACILITY INTEGRITY

Allan Charlesworth

96

INTEGRITY MANAGEMENT PROGRAM

• In-Line Inspection

• Metal loss

• Crack detection

• Geometry

• Internal Corrosion Program

• Monitor product quality at pipeline inlet

• Chemical inhibition

• Cathodic Protection

• Controlling external (soil side) corrosion

• Facility Integrity

• Governs operation, inspection, monitoring and

mitigation (if required) for all pressure vessels

and tanks

• Geotechnical Program

• Water crossing depth-of-cover

• Slope stability

• Geospatial Information System (GIS)

• Captures, stores, analyzes, manages and

presents pipeline integrity data

INTEGRITY EXPENDITURES

97

An

nu

al

Ex

pe

nd

itu

res

($

MM

)

See "Forward-Looking Statements & Information.”

-

50

100

150

200

250

300

350

400

450

500

-

$10

$20

$30

$40

$50

$60

$70

$80

2005 2006 2007 2008 2009 2010 2011 2012F 2013F

In-Line Inspection Repairs Geotechnical Cathodic Protection Conventional Throughput

mb

pd

Integrity, 32%

Power, 24%

Other, 44%

2013 Operating Expenses

IN-LINE INSPECTIONS (ILI)

• Pembina has over 450 ILI

capable pipeline segments

• Pembina completes an average

of 50 – 60 inspections/year

• Inspections typically result in

300 – 500 digs annually

• Main tool technologies

• Magnetic flux leakage (MFL)

• Geometry (deformations)

• Combo tools (MFL and

geometry)

• Ultrasonic crack detection

98

99

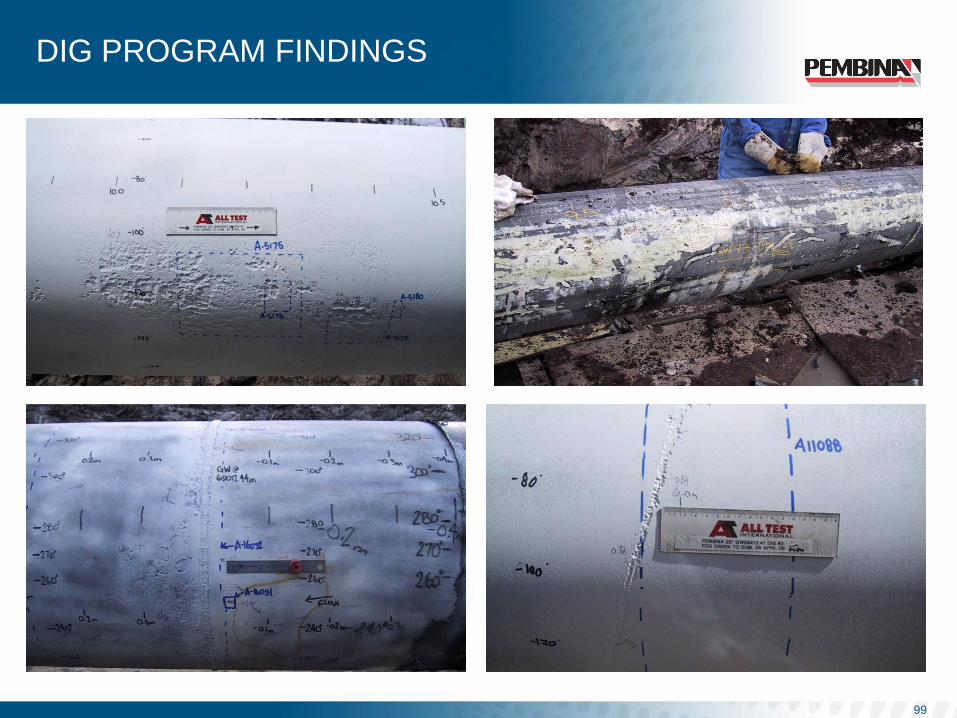

DIG PROGRAM FINDINGS

ULTRASONIC CRACK DETECTION TOOL

100

Transmitter

Battery Packs

Sensor Carrier Electronic &

Data Recorder Packs

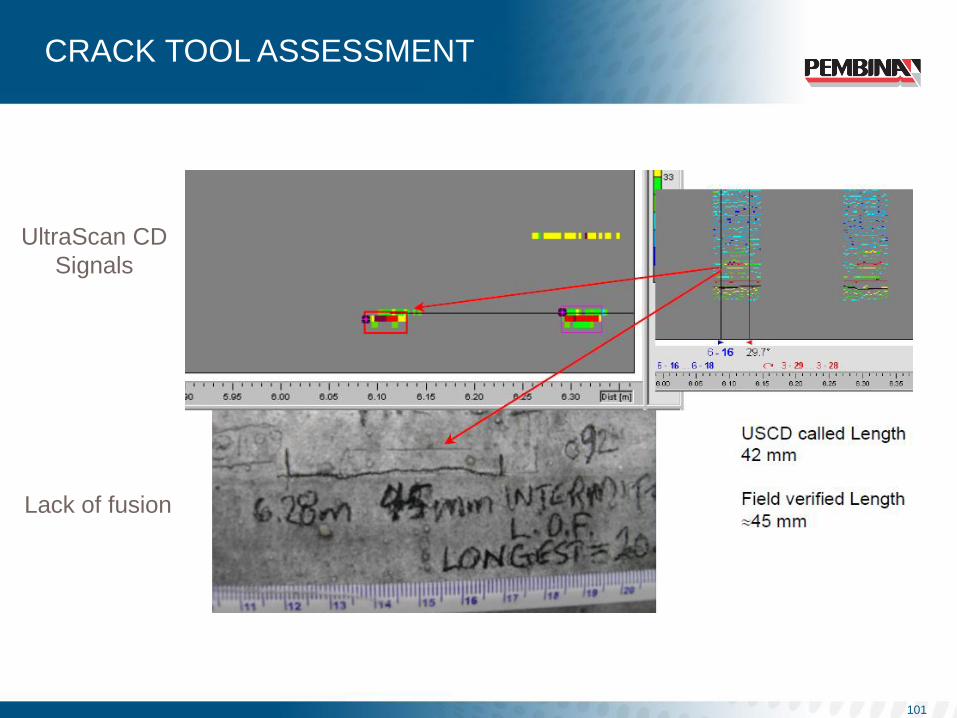

CRACK TOOL ASSESSMENT

101

UltraScan CD

Signals

Lack of fusion

REPAIR METHODS

102

B-Sleeve

Compressive Sleeve (Petrosleeve)

SUMMARY

• Program has transitioned from primarily metal loss threat evaluation to

include geohazards, crack and geometry threats

• Exploring new technologies to enhance detection and analysis of threats

• Development of Pembina’s GIS has provided for a more comprehensive

analysis of threats and mitigation options

• 2013 Focus

• Completion of integrity programs for expansion projects

• Continue to leverage the GIS system to advance risk assessment and will include Class

location studies and outflow analysis

• Complete the integration of Provident assets into Pembina’s integrity management

programs

103

DEDICATED TO STAKEHOLDERS

Bob Michaleski

INVESTING IN OUR COMMUNITIES

• Being a good neighbour where

we live, work and play helps

Pembina build relationships and

maintain our social license to

operate

• Committed to the communities in

which we operate by giving back

• Our decisions are based on the

unique characteristics of each

community

Preserve & protect the environment

Advance education

Foster wellness & build community

105

Pembina supports

organizations that:

INVESTING IN OUR COMMUNITIES

United Way

2012 Campaign raised $1 million

including employee contributions and

Company match for the United Way of

Calgary & Area

106

Employee Matching Gift Program

We encourage our employees to give

back to their communities by matching

their donations

STAKEHOLDER ENGAGEMENT

• Anticipate and manage the

social impacts of our

operations

• Pembina has a reputation

for honesty, transparency

and respecting our

stakeholders

• Long history of forging

productive working

relationships with

communities, landowners,

regulators, customers and

elected officials

107

• 800 employees

• 12 field offices

• Average of 8.3

years of service

Reputation for

attracting and

retaining

employees

EMPLOYER OF CHOICE

108

SAFETY

Our Safety, Environment & Security management system is cornerstone of

Pembina’s success and is deeply embedded in our corporate culture:

Working towards zero accidents, injuries and environmental incidents

• All accidents, injuries and incidents are preventable

• Loss management policies, programs and procedures (which include our emergency

response plans) and an incident reporting and tracking system

Arming ourselves with the knowledge to improve

• Tracking health, safety and environmental statistics is just as important as measuring

operating and financial performance

Driving our way to zero

• Any Pembina employee expected to drive on company-time is required to participate in

Collision Avoidance training every three years

109

STABLE FINANCIAL PLATFORM

Peter Robertson

$4 BILLION OF POTENTIAL PROJECTS

111

2011

2012

2013

2011

2012

2013

2014+

-

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

$4,500

$5,000

Capital Budget Presentation 2012

Today

Ca

pit

al E

xp

en

dit

ure

s (

$M

M)

Uncommitted

~55%

Uncommitted

~35%

2011

2012

2013

2011

2012

2013(1)

2014+(1)

(1) Represents $140 million 2013 capital and $530 million 2014+ capital relating to LVP 2 and HVP 2 Board

approved projects that are subject to reaching commercial arrangements.

See "Forward-Looking Statements & Information.”

• Continue to grow

project inventory with

~$4 billion in

opportunities in 2012

and onwards

• Focus on fee-for-

service projects

• Successfully moved

uncommitted capital

to committed projects

• De-risked the capital

program

GROWING CAPITAL OPPORTUNITIES

• Pembina continues

to see growing

opportunities

across all of its

businesses

• Emphasis on fee-

for-service based,

accretive projects

112

See "Forward-Looking Statements & Information.“

1

billion 2013

capital program

~$

-

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

$1,100

2012F 2013F

Cap

ital E

xp

en

dit

ure

s (

$M

M)

Conventional Pipelines Oil Sands & Heavy Oil

Midstream Gas Services

Other Capital

(1) Phase 2 HVP/LVP expansion subject to commercial arrangements.

(1)

POTENTIAL SOURCES & USES 2013-2016

Sufficient

liquidity and

access to capital

to prudently

finance growth

113

5.5 billion

(2013-2016)

Cash Flow

Debt Financing

DRIP

Public Equity

Dividends

Capital Expenditures

-

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

Potential Sources Potential Uses

$M

M

See "Forward-Looking Statements & Information.“

~$

LIQUIDITY & ACCESS TO CAPITAL

• Access capital at attractive rates

• Sufficient funding for near-term projects

• DRIP(1) currently raising ~$22 million

per month

• $1.5 billion credit facility

• Current undrawn capacity of ~$1 billion

• Excellent relationships with capital

providers

• Prudent and flexible capital

structure

• Senior debt to total capital ~30%(2)

• Dedicated to our BBB credit ratings

Well-

positioned

to execute our

business plan

114

(1) DRIP is the Premium Dividend™ and Dividend Reinvestment Plan. (2) YE 2012 estimate.

Committed to

maintaining our

investment grade

rating

• Fixed rate debt

• Commodity and power hedging

• Credit risk management

Committed to

mitigating risk

PRUDENT FINANCIAL MANAGEMENT

115

LONG-TERM DEBT MATURITY & STRUCTURE

116

86%

14%

Fixed Rate (average rate of 4.90%)

Variable Rate (average rate of 2.85%) (1)

(1) As of September 30, 2012.

$250 $266

$450 $450

$173 $173

$300

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Notes Convertible Debentures

COMMODITY AND POWER HEDGING

• Frac spread exposure expected to

be below 10% in 2016 through

increased fee-for-service revenue

• Mitigate frac spread risk by locking in

cash flows required to cover a

minimum of 50% of the gas supply

cost

• Lock foreign exchange rates at time

of forward sales transactions

• Fix 100% of conventional pipelines

and NGL power required for current

year and tapered hedges for forward

years

117

118

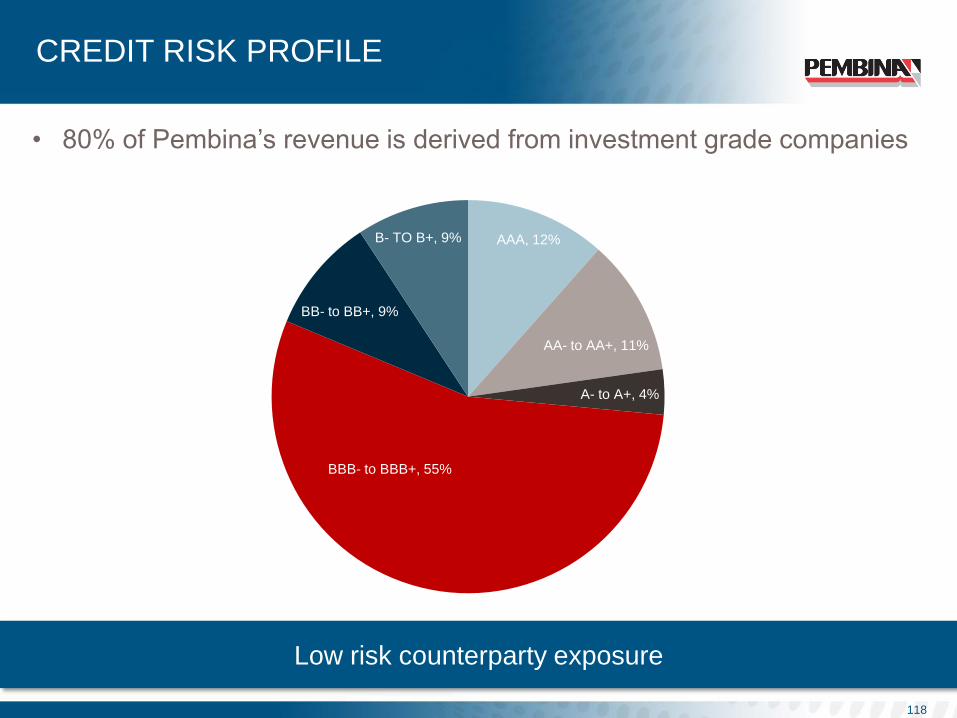

CREDIT RISK PROFILE

Low risk counterparty exposure

• 80% of Pembina’s revenue is derived from investment grade companies

AAA, 12%

AA- to AA+, 11%

A- to A+, 4%

BBB- to BBB+, 55%

BB- to BB+, 9%

B- TO B+, 9%

TAXATION

• Pembina expects to

be moderately cash

taxable in 2013

• Average annual CCA

deduction is 15% of

pool

119

Data as of September 30, 2012.

See "Forward-Looking Statements & Information.”

Estimated CCA pools

& non-capital losses 2012

CCA Pools Non-Capital

Losses

$2.4 billion $160 million

SUMMARY

Mick Dilger

2012 CORPORATE SUCCESSES

• Closed acquisition of Provident

Energy Ltd. on April 2, 2012 and

began trading on the NYSE

• Integration nearing completion with

only systems integration remaining

• Increased credit facility to $1.5

billion

• Increased dividend by 3.9% to

$0.135/month

• $450 million senior unsecured

medium-term notes issued at 3.77%

per annum on October 22, 2012

121

Saturn Gas Services /

Conventional Pipelines

• Received required regulatory approvals in Q3 2012

• Awarded construction contracts for pipelines

• Majority of major equipment for both facilities ordered

• Major equipment received at each site Resthaven

Gas Services /

Conventional Pipelines

NGL Expansion Conventional Pipelines

• Reached contractual threshold to proceed

• Received regulatory approval

• Began construction on two of the three pump stations in Q3 2012

Truck Terminals Midstream • Construction started in Q4 2012 on Judy Creek FST

Crude Expansion Conventional Pipelines • Added 50 mbpd capacity on the Drayton Valley system

Musreau

Expansion Gas Services • Deep cut and shallow cut in service Q3 2012

Storage & Other Midstream

• Commissioned 8,000 bpd expansion of Redwater fractionator on time

and under budget

• Brought fee-for-service cavern on stream at Redwater in Q3 2012

• Corunna brine pond expansion

2012 PROJECT ACCOMPLISHMENTS

122

Executing on capital commitments

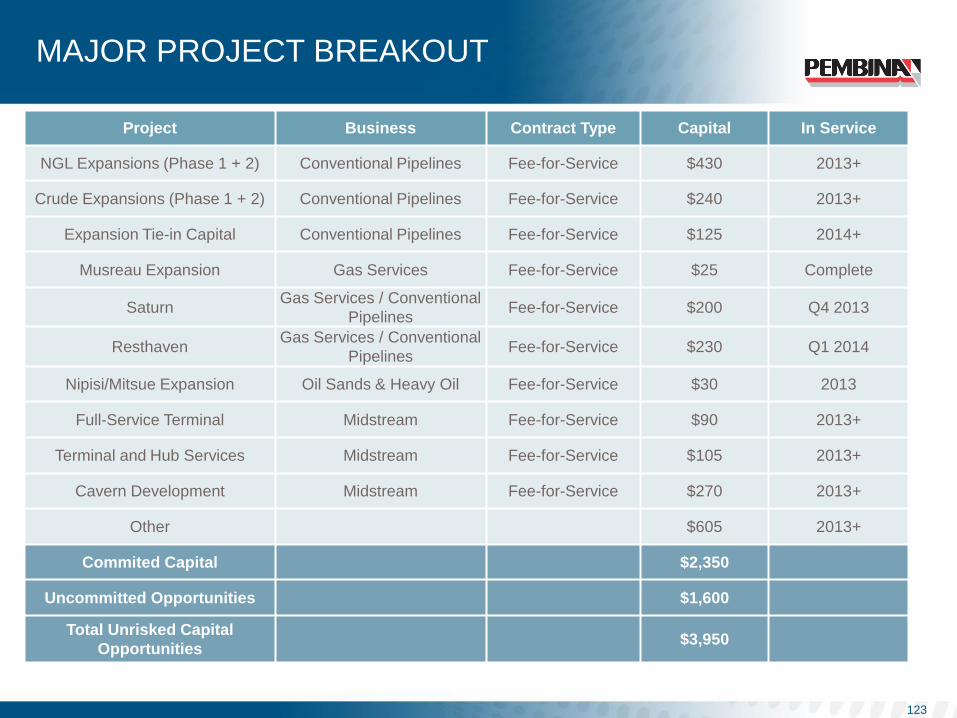

MAJOR PROJECT BREAKOUT

123

Project Business Contract Type Capital In Service

NGL Expansions (Phase 1 + 2) Conventional Pipelines Fee-for-Service $430 2013+

Crude Expansions (Phase 1 + 2) Conventional Pipelines Fee-for-Service $240 2013+

Expansion Tie-in Capital Conventional Pipelines Fee-for-Service $125 2014+

Musreau Expansion Gas Services Fee-for-Service $25 Complete

Saturn Gas Services / Conventional

Pipelines Fee-for-Service $200 Q4 2013

Resthaven Gas Services / Conventional

Pipelines Fee-for-Service $230 Q1 2014

Nipisi/Mitsue Expansion Oil Sands & Heavy Oil Fee-for-Service $30 2013

Full-Service Terminal Midstream Fee-for-Service $90 2013+

Terminal and Hub Services Midstream Fee-for-Service $105 2013+

Cavern Development Midstream Fee-for-Service $270 2013+

Other $605 2013+

Commited Capital $2,350

Uncommitted Opportunities $1,600

Total Unrisked Capital

Opportunities $3,950

GROWTH TRAJECTORY

• Anticipate growth

across all four

business units largely

underpinned by

customer agreements

• Diverse asset base

and critical mass in all

businesses allows for

asset optimization and

greater resource

capture

124

$0

$200

$400

$600

2013 2014 2015 2016 Uncommitted 2013 - 2017

HVP/LVP Expansion Other CBU Growth

Saturn/Resthaven Nipisi/Mitsue Expansion

FST Strategy Nexus Terminal

Cavern and Other Uncommitted opportunities

Op

era

tin

g M

arg

in (

$M

M)

(1)

(1) A portion of which is subject to reaching commercial arrangements.

See "Forward-Looking Statements & Information.”

SUMMARY

• Proven track record and management team

• Solid historical financial and operational performance under experienced leaders

• Demonstrated ability to execute on business plan and generate returns for shareholders

• Strategically located and well-established infrastructure

• Extensive asset footprint and high barriers to entry near long-life resource plays

• Highly contracted and stable cash flow

• Fee-for-service focused capital program

• Strong growth portfolio

• ~$4 billion of unrisked projects

• Strong balance sheet

• Investment-grade credit rating with proven access to debt/equity markets and financial flexibility

• History of stable and growing dividends

125

GOING THE DISTANCE

BOB MICHALESKI Chief Executive Officer

MICK DILGER President & Chief Operating Officer

PETER ROBERTSON Vice President, Finance & Chief Financial Officer

SCOTT BURROWS Senior Manager, Corporate Development &

Planning

Pembina Pipeline Corporation

www.pembina.com

Suite 3800, 525 – 8th Avenue S.W.

Calgary, AB T2P 1G1

Phone 403-231-3156

Fax 403-237-0254

Toll Free 1-855-880-7404

Email [email protected]

Trustee, Registrar & Transfer Agent

Computershare Trust Company of Canada

Suite 600, 530 – 8th Avenue S.W.

Calgary, Alberta T2P 3S8

1-800-564-6253

126

BOB MICHALESKI Chief Executive Officer

MICK DILGER President & Chief Operating Officer

PETER ROBERTSON Vice President, Finance & Chief Financial Officer

SCOTT BURROWS Senior Manager, Corporate Development & Planning

Pembina Pipeline Corporation

www.pembina.com

Suite 3800, 525 – 8th Avenue S.W.

Calgary, AB T2P 1G1

Phone 403-231-3156

Fax 403-237-0254

Toll Free 1-855-880-7404

Email [email protected]

Trustee, Registrar & Transfer Agent

Computershare Trust Company of Canada

Suite 600, 530 – 8th Avenue S.W.

Calgary, Alberta T2P 3S8

1-800-564-6253

APPENDIX

This presentation uses the terms "total enterprise value" (Pembina's market capitalization

plus long-term debt and convertible debentures) and "operating margin" (revenue less

operating expenses and product purchases), which are not recognized under Canadian

generally accepted accounting principles (GAAP). Management believes these non-GAAP

measures provide an indication of the results generated by Pembina's business activities and

the value those businesses generate. Investors should be cautioned that these non-GAAP

measures should not be construed as an alternative to net earnings, cash flow from operating

activities or other measures of financial performance determined in accordance with GAAP as

an indicator of Pembina's performance. Furthermore, these measures may not be

comparable to similar measures presented by others.

127