investment proposal

TRANSCRIPT

Investment proposal

Wonderland – Theme park investment

2

Executive Summary

Global financial markets over the years have transformed and developed owing to the

integration of financial markets driven by the revolution brought about by globalisation and

internationalisation. Investors today are looking to capitalise on the first possible investment

opportunity, with the intention to grow and make financial gains. These developments have

however even transformed the role of corporate and project finance, surfacing their

importance as a significant investment analysis tool, looking into both the financial and non

financial feasibility of an investment project.

The undertaken report, for Wonderland Confectionaries would analyse and comment on the

financial and non-financial feasibility of the proposed venture into theme park investment,

the report would critically evaluate the project using the NPV project evaluation technique

and thus recommend that the project is financially sound would prove to a good investment

decision on the long run for Wonderland confectionaries.

3

Table of Contents

1. Introduction to corporate finance...............................4

1.1 Evolution and importance of Corporate finance....5

1.2 Overview of Wonderland project..........................8

2. NPV Calculation........................................................9

3. Project Appraisal.....................................................12

4. Conclusion and Recommendations.........................14

5. References................................................................15

4

1. Introduction to corporate finance

Today’s volatile market environment with changing economic and market conditions, have

surfaced and highlighted the growing significance of associated risk and the degree of failure

that could arise with any undertaken investment. Recently witnessed project failures have all

the more highlighted the growing concern about investment decisions, making it all the more

critical and crucial for business , as this may often can be the difference between the success

or the failure of the business. As reported in numerous literatures just as a good decision

could add financial and non financial value to a business, a wrong decision could lead the

organisation to financial disasters like bankruptcy or even liquidation.

Making the correct investment decision has always been an area of concern for finance

professionals, practitioners and investors themselves. It is believed that problems associated

with investment decisions is as old as the economy itself, further to this in order to ensure

success with optimal utilisation of limited investment resources, it is very vital all decisions

make in the course of action should be taken with due consideration and the influence it has

from the internal, external environment along with the influence decisions have on the

investors. As reflected in the work done by Van Groenendaal and Kleijnen, 2002; Biezma

and San Cristobal, 2006 the decisions made in corporate finance are primarily dominated by

calculus of Net present Value (NPV), internal rate of return (IRR) or the payback period.

Employing these financial calculations would enable the decision maker to assign values to

the adopted financial model, thus providing the best possible sensitive analysis of the most

likely outcome from the investment. These methods of investment evaluation are conducted

with the prime objective of reflecting the possible outcome from the intended investment,

adding to the knowledge, understanding of numerous elements involved, realistic timeframes

of expected returns etc thus positioning the investor in a strategically and financially sound

position so that they could capitalise on the opportunity the investment can possible offer.

Other than these methods the more traditional method as mentioned by Pike and Neale, 2000

is the consideration of bringing into account risk management principles, which would best

estimate the results from an investment.

The undertaken report aims to look into evaluation of the proposed investment venture that

Woodland confectionaries, would like to undertake as diversity from its principle operation.

Even with the element of entering into a whole new venture is financially sourced; there is a

need to ensure that the project that has been undertaken is both financially and non-

5

financially feasible, and achieving this investment analysis would be the prime objective of

this report. By the end of the analysis the report would be reflect and comment on the overall

feasibility of the investment project that Woodland confectionaries intends to undertake, the

report to conclude would on the basis of the report findings and analysis conclude with

recommendations and comments on whether or not the investment is in the best interest of

Woodland confectionaries, to best judge the case the report would make required

assumptions and analyse the financial and non financial performance of Alice Limited that

would possibly be the closest competitor for Woodland confectionaries in their theme park

venture.

1.1 Evolution and importance of Corporate finance

Corporate finance over the last few decades has gained a very significant position in today’s

modern economies, as reported by numerous researchers and academicians there have been

great developments in both practice and principles, revolutionising the way business

approach and apply corporate and project finance. As mentioned by Liber, 2001 when the

history of corporate finance is reviewed, signs of major developments came to surface in the

1970s, and the primary driver for these developments have been sophisticated financial

market practice, that starting evolving in a much more risk oriented environment owing to

numerous corporate failures and disasters. In the present financial and economical

environment one of key players that have surfaced are the stock markets, and with the influx

of globalisation and internationalisation, financial markets have got more integrated giving

way to numerous investment opportunities all across the globe.

With such growing opportunities, investors today are always on a lookout to capitalise on all

possible chances to venture into new investments; however they need to ensure that the

project undertaken is both financially and non-financially feasible, as an incorrect investment

decisions could, not only lead to project failure, but could damage the present health of the

business, leading to severe blows to its financial standing and future market position. With

the growing significance of the risk analysis and project feasibility leading to successful

investment outcomes, project finance has really emerged and developed as an important

investment tool, reflecting on critical success and failure factors associated with a project

undertaking.

As Liber, 2001 further contributes to the literature by mentioning that there are numerous

definitions associated and addressing project finance; however the best representation of

6

project finance is the one given by Leslie. E. Sherman Infrastructure and Finance Practice

Group, Thelen. Reid and Priest LLP and is as discussed below:

“Project finance – non-recourse financing of the development and construction of a

particular project in which participants looks principally to the revenues expected to be

generated by the project for the repayment of some loans and the assets of the projects and in

many cases as collateral for loans rather than to the general credit of the project sponsor.”

(By Leslie E. Sherman Infrastructure and Finance Practice Group, Thelen. Reid and Priest

LLP http://www.constructionweblinks.com)

According to current statistics global project finance “recorded the highest half year volume

since 2000 with $98.5billion and 210 deals and 1H 2006, compared to $72.3 billion and 248

deals in 1H 2005. This represents a 36% increase from the same period last year and a 41%

increase from 1H 2004”. (Project Finance Journal September, 2006. pg. 41)

PARTIES TO PROJECT FINANSING

Source: Chew 2001

As reflected in most corporate and project management journals, most project management

projects today are privately funded and can be best characterised by the following three

features:

7

The host government local or central provides concessions to private companies that aid

and establish a project as a separate company.

As most of the finance is managed by the project manager or the sponsor of the

investment project, therefore a major portion of the equity would be of the project

company.

The project company operates on a very high debt to equity ratio, with limited resources

from the government or the equity holders in event of a default, the company also enters

into a comprehensive contractual agreement drawn between the suppliers and the

customers.

(Chew 2001)

Project finance a relative new concept in the field of corporate finance and can be very

distinctly differentiated from traditional corporate finance as briefly discussed below:

Project finance can be distinguished from traditional corporate finance functions in terms

of the credit evaluation and assessment process when it comes to loans, the present

practice now doesn’t only consider the capabilities of the company to repay but also look

at more technical details like profit scenarios of the undertaken project, steady cash flow

projections these elements act like collaterals to the undertaken debt.

Project Finance has a more technical outlook over the traditional approach of financing

which considered financing a specific project by either the means of debt and/or equity;

this modernized approach uses various technical financial tools and models, which

analyses the future and current value of the investment. It evaluates the projects’ outcome

on the bases of the future returns in the form of profit and cash flows.

In the case of traditional corporate finance the guarantee of the debt taken on the entire

property of the company responsible for the project, while in the case of project finance

the main guarantee for the project are the assets that are related to the project that is being

financed.

The other significant difference is that in the case of project finance the loan is intended

to be repaid by the cash flow generated from the investment itself and also the profit

8

generated from the project, this however is not the case of traditional corporate finance,

the project finance has over the years emerged as an alternative to the conventional

methods used and is applied on a large scale projects globally.

1.2 Overview of Wonderland project

“Wonderland Confectionaries Inc successfully owns a chain of restaurants, and currently is

looking to diversify is course of business and venture into a new business stream, it intends

and proposes to venture into investing in a theme park, which would be an initial investment

of £500 million, although the business does not have any prior experience or expertise in this

area of business, a thorough research spending an amount of £400,00 was undertaken on

theme parks and the management on the basis of this found the investment very attractive, a

team of finance professionals within the business were asked to the associated risk and the

appropriate financial structure of the closest theme park and on the basis various sources of

finance were considered and the possible fiancé structure was proposed. However the overall

feasibility of the project still remains under question, an in-depth analysis of various financial

and non financial issues is now being carried out to comment and recommend on the overall

success of the project.”

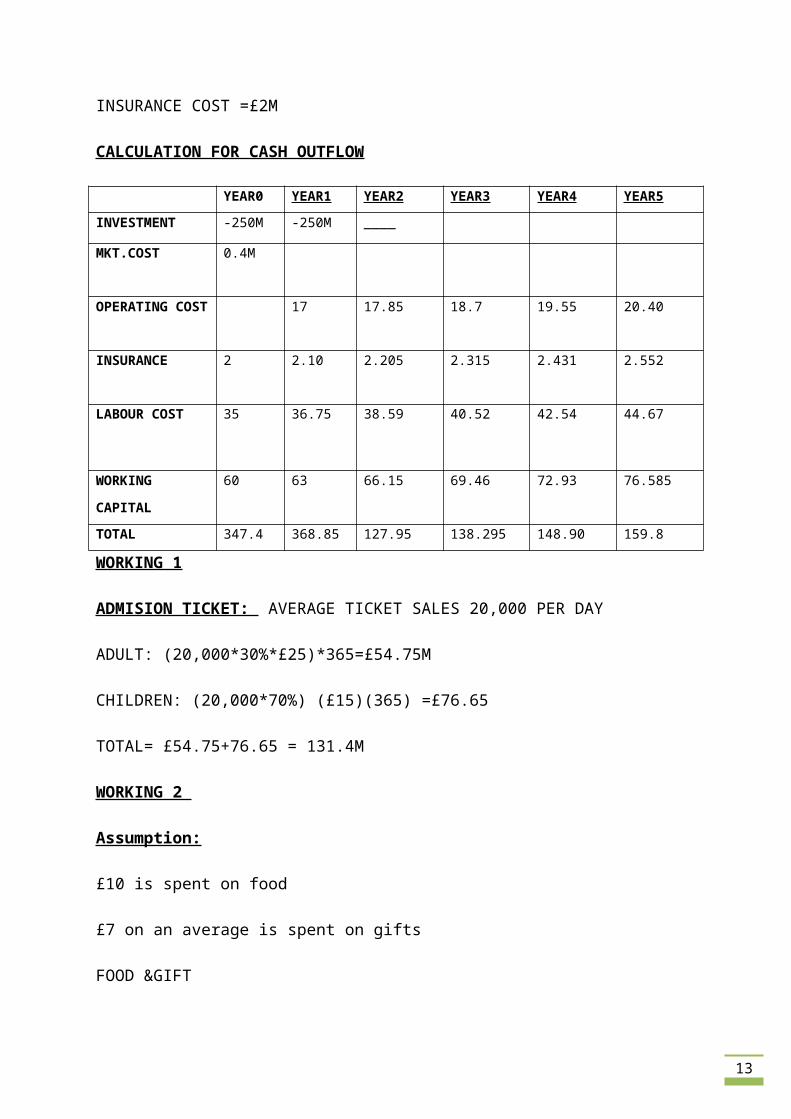

2. NPV Calculation

WONDERLAND

CASH OUT FLOW

INITIAL INVESTMENT =£500M

9

YEAR 0 = -£250

YEAR1= -£250M

RESEARCH MARKETING COST = YEAR 0 -£400,000

OPERATION COST = £17M

IT WILL INCREASE £0.85M EVERY YEAR

WORKING CAPITAL REQUIRED = £60M

LABOUR COST =£35M

INSURANCE COST =£2M

CALCULATION FOR CASH OUTFLOW

YEAR0 YEAR1 YEAR2 YEAR3 YEAR4 YEAR5

INVESTMENT -250M -250M ____

MKT.COST 0.4M

OPERATING

COST

17 17.85 18.7 19.55 20.40

INSURANCE 2 2.10 2.205 2.315 2.431 2.552

LABOUR COST 35 36.75 38.59 40.52 42.54 44.67

WORKING

CAPITAL

60 63 66.15 69.46 72.93 76.585

TOTAL 347.4 368.85 127.95 138.295 148.90 159.8

WORKING 1

ADMISION TICKET: AVERAGE TICKET SALES 20,000 PER DAY

ADULT: (20,000*30%*£25)*365=£54.75M

CHILDREN: (20,000*70%) (£15)(365) =£76.65

TOTAL= £54.75+76.65 = 131.4M

10

WORKING 2

Assumption:

£10 is spent on food

£7 on an average is spent on gifts

FOOD &GIFT

FOOD: 20,000*(10*40%)*365 =£29.2M

GIFT = 20,000(7*45%)*365 =22.995M

TOTAL = 52.195M

CASH INFLOW:

0 1 2 3 4 5 6

TICKET

REVENUE(W1)

131.4 137.97 144.87 152.11

FOOD

&GIFT(W2)

52.195 52.80 57.54 60.42

ADVER.SAVING 3 3 3 3 3 3

W.CAPITAL 60 63 66.15 69.46 72.93 76.58

TOTAL 3 63 0249.595 261.92 274.87 288.46 76.58

WORKING 3

CAPITAL ALLOWANCE

ASSUMPTION = CAPITAL ALLOWANCE WOULD BE CALCULATED FROM FIRST

YEAR AFTER INVESTMENT AND WOULD BE CALCULATED ON FULL AMOUNT

OF £300M

BOOK VALUE BOOK VALUE

11

YEAR1= 300*25% =75M 300M-75=225

YEAR2= 225*25% = 56.25M 225-56.25=168.75

YEAR3=168.75*25%=42.187M 168.75-42.185=126.562

YEAR4=126.5625*25%=31.64 126.562-31.61=94.921

YEAR5=94.9218*25%=23.73 94.921-23.73=71.19

TAX SAVING ON CAPITAL ALLOWANCE

Y1= 75@35% = 26.25

Y2=56.25@35%=19.69

Y3=42.1875@35%=14.765

Y4 = 31.64@35% =11.07

Y5 =23.73.@35% =8.31

Y0 1 2 3 4 5 6

TOTAL INFLOW 3 63 249.595 261.92 274.87 288.46 76.58

TOTAL OUTFLOW -347.4 -368.85 -127.95 -138.295 -148.90 -159.8

TAXABLE

REVENUE

-344.4 -305.85 121.695 123.625 125.97 128.66 76.58

TAXATION@35% 120.54 107.05 -42.58 -43.27 -44.09 -45.03 -26.8

-223.86 -198.8 79.065 80.355 81.88 83.63 49.78

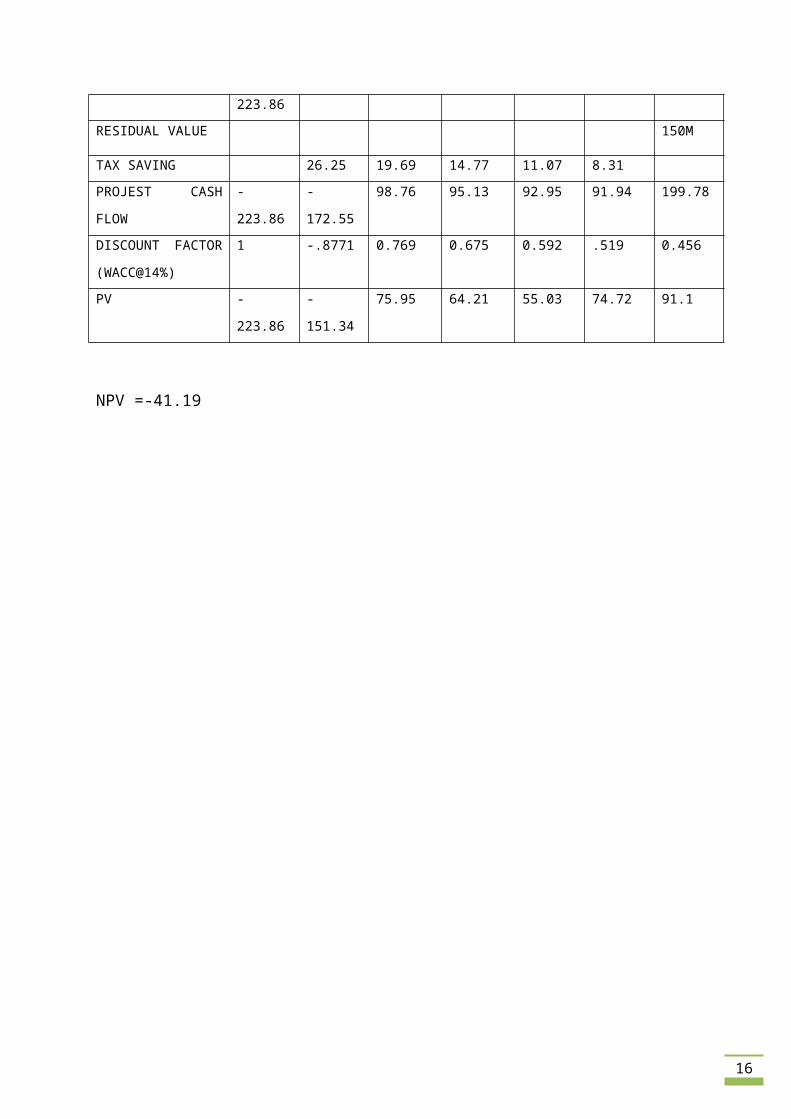

RESIDUAL VALUE 150M

TAX SAVING 26.25 19.69 14.77 11.07 8.31

PROJEST CASH

FLOW

-223.86 -172.55 98.76 95.13 92.95 91.94 199.78

DISCOUNT FACTOR

(WACC@14%)

1 -.8771 0.769 0.675 0.592 .519 0.456

PV -223.86 -151.34 75.95 64.21 55.03 74.72 91.1

NPV =-41.19

12

3. Project Appraisal

“Project appraisal can be considered as the analysis of an investment or a project in order to

determine its gained merits or advantages along with its acceptability in accordance with the

previously established criteria. In project finance project appraisal is one of the final steps

before project finance is finalized, this process not only validates the financial feasibility in

terms of costs being reasonable and sustainable but also looks at aspects like ground/

13

technical situation and also considers the objectives of the projects, its possibility of

achievement and most importantly it being realistic.”

The various techniques that are used for project appraisal are as follows:

Technical Appraisal:

Are all the pre-requirements that would and are vital for the success for the project

considered?

Selection of appropriate location, process and other needs are made and addressed to

satisfactorily.

Economic Appraisal:

A critical cost-benefit analysis

Elements of shadow prices and economic benefits and cost discussed

Impact of investment on society and locality

Impact and influence of savings on social and economical environment

Impact on fulfilment of national goals:-

(1) Self sufficiency

(2) Employment and

(3) Social order

Ecological Appraisal:

Impact of project on quality of :- Air, Water, Noise, Vegetation, Human life

Major projects ,such as these, cause environmental damage

Power plants

Industries like bulk drugs, chemicals and leather processing.

Likely damage & the cost of restoration

Financial Appraisal:

Whether the project is financially viable?

14

(1) Servicing debt

(2) Meeting return expectations

In the case of Wonderland, the following project appraisal is done on the basis of the

following real options:

Expansion and flexibility to bring changes:

If the business decides to undertake a process of expansion during the due course of life of

the project, there are possibilities to undertake this expansion; this can be justified in

following project appraisal terms:

Technical Appraisal: The tem by the time of making expansion decision would have a well

equipped technical team, with complete technical and operational expertise. Processes,

machines and other requirements like location are already available

Economic appraisal:

In terms of economic appraisal the project in the next six years would start showing gains,

making the capital available for reinvestment, moreover as per the cash flow; the cash inflow

forecasted for the business is healthy and is growth with the age of the project.

Ecological appraisal:

The project is insured for an amount of £3 million and would be able to sustain any repairs,

replacements etc. The project does not have environmental hazards and would comply by the

required code of conduct.

Financial appraisal: The project is financial sound and would be able to meet all its liabilities

without any problems, working capital from year one shows an upward movement.

4. Conclusion and Recommendations

The above calculations and analysis are reflective of the financial feasibility of the

investment, as per the value reflected by the NPV and the inflow and outflow of cash from

15

the investment, it is evident that although the returns would be slow but the overall project is

self sustainable and is recommended as an investment.

£150 Million in the 6th year as residual income is very promising for the project, which is

backed by a health cash flow which matures with the age of the investment, a good flow of

inflow and outflow of capital is reflective of good working capital management practices.

Thus to conclude, the report strong recommends the investment on the basis of the fact that

the overall feasibility of the investment looks healthy the project is recommended to be

undertaken, after considering other non financial issues in regards to gaining trained and

expert experienced staff during project initiation and other environmental and social issues

that would need to be addressed.

5. References

Chew D the New Corporate Finance: Where Theory Meets Practice. 3rd Edition

2001.Pg. 367

16

Biezma, M.V. and San Cristobal, J.R. (2006) ‘Investment criteria for the selection of

cogeneration plants – a state of the art review’, Applied Thermal Engineering, Vol.

26, No. 5–6, pp.583–588

Van Groenendaal, W. and Kleijnen, J. (2002) ‘Deterministic versus stochastic

sensitivity analysis in investment problems: an environmental case study’, European

Journal of Operational Research, Vol. 141, No. 1, pp.8–20

Pike, R. (1986) Investment Decisions and Financial Strategy, Humanities Press,

Oxford, USA

Pike, R. and Neale, B. (1993) Corporate Finance and Investment – Decisions and

Strategies, Prentice-Hall, London, UK

Ponis, S., Tatsiopoulos, I., Vagenas, G. and Koronis, E. (2006) ‘A proposed ontology

to support knowledge logistics in virtual organisations: a case study from the

pharmaceutical industry’, Proceedings of EUROMA 2006, Moving up the Value

Chain, Glasgow, UK, pp.50–58

Donald H. Chew, The New Corporate Finance: Where Theory Meets Practice,

2001Hamberg, M. Strategic Financial Decisions. Malmo, Liber, 2001

Leslie. E. Sherman Infrastructure and Finance Practice Group, Thelen. Reid and Priest

LLP

Stephen A Ross, Randolph W Westerfield, Jeffery F. Jaffe, and Bradford D. Jordan

International Student Edition (2007) Core Principles & Applications of Corporate

Finance McGraw-Hill Irwin, New York, NY

Aaker J and Shumaker J (1994).... Looking back and looking Forward....., a

participatory approach to evaluation, Little Rock, Arkansas: Heifer Project

International

Barrow C J (1997) Environmental and Social Impact Assessment, An introduction,

London: Arnold Beck T and Stelcner M (1997) Guide to Gender-Sensitive Indicators,

Quebec: Canadian International Development Agency

Blackburn J and Holland J (Eds) (1998) Who Changes? Institutionalizing

participation in development, London: Intermediate Technology Publications

Davies. A (1997) Managing for Change, How to run community development

projects, London: Intermediate Technology Publications in association with

Voluntary Service Overseas

17

Davis J, Garvey G with Wood M (1993) Developing and Managing Community

Water Supplies, Oxfam Development Guidelines No 8, Oxford: Oxfam (UK and

Ireland)