international islamic university malaysia (iium), malaysia · 2020-01-15 · potential modes of...

TRANSCRIPT

1Journal of International Business and Management (JIBM)

https://rpajournals.com/jibm

JIBM Journal of International Business and Management

Journal Homepage: https://rpajournals.com/jibm

Role of Islamic Microfinance Institutions for Sustainable Development

Goals in Bangladesh

Md Nazim Uddin1* Hamdino Hamdan2

Salina Kassim3 Nor Azizan Che Embi4

Norma Bt Md Saad5 International Islamic University Malaysia (IIUM), Malaysia1, 2, 3, 4 & 5

Abstract

The goal of this paper is to explore the Islamic Microfinance Instruments (IMFs) in attaining sustainable development goals (SDGs) in Bangladesh. Propose a conceptual model along with exploring the efforts in attaining SDGs to fill the gap. The methodology of the study predicated on secondary data includes existing relevant literature, books and annual reports of easily sampled IMFs and Microcredit Regulatory Authority (MRA) in Bangladesh. The findings of the research show that microfinance organisations have a broader range to attain Sustainable Development Goals through their various investment modes. The analysis categorises the microfinance tools into large parts that are poverty decrease, end hunger for food, good health, equality education, clean drinking water, sanitation energy, gender equality, empowering women, and funding which have an optimistic effect to the real sector of the sustainable economic climate that will lead towards attaining SDGs. Microfinance organisations are carrying on their initiatives in attaining sustainable development goals through their various products. With growing the potentiality, microfinance has both direct and indirect effects on ensuring financial development, environmental sustainability, and social inclusion by creating work opportunity, distributing knowledge and skills, making self-dependent, protecting from undesirable effects. The paper also attempts to put suggestions to lessen the difficulties of microfinance performing as impediments to achieving the SDGs. Keywords: Sustainable Development Goals (SDGs), Microfinance Institutions (MFIs), Islamic Microfinance Institutions (IMFIs), Poverty, sustainability, Bangladesh

Introduction With the Millennium Development Goals (MDGs) expiring at the tip of 2015, the globe is making ready for the worldwide development agenda to succeed them post-2015. The proposed seventeen sustainable Development Goals (SDGs) are additional ambitious and holistic than their harbinger, and land would force commensurately challenging finance to implement them (Ahmed, 2015).

RPAJournals

Journal of International Business and Management 3(1): 01-12 (2020) Print ISSN: 2616-5163 Online ISSN: 2616-4655

*Corresponding author: Md Nazim Uddin; Email: [email protected]

DOI: https://doi.org/10.37227/jibm-2020-64

2Journal of International Business and Management (JIBM)

https://rpajournals.com/jibm

Sustainable Development as outlined because of the state of the globe which may be earned by combining native and international effort to fulfil the wants of an individual with the activities that may make sure the safety of the society and environment of future generation (Lindamood, 2017). For securing a world with sustainable development, the United Nations declared sustainable Development Goals (SDGs) in 2014. UN declared seventeen goals to be achieved in 2030 to ensure sustainable devolvement (Islam, Hunt, Jantan, Hashim & Chong, 2019). SDGs are the successor to the MDGs which were expected to be achieved among 2015. Microfinance institutions (MFIs) contributed a lot to achieve MDGs with achievement within the economy getting the presence of such structure.

Nevertheless, among these tools, financial debt primarily based tools encounter some issues in comparison to the equity-based financing structure. Microfinance tools are protected by principles getting the only motto to ensure the equity and justice in prosperity distribution to lead to hunger. It is established that economic structures having financial institution are much focused on social development. This research tries to explore the functions of Islamic microfinance in attaining SDGs in Bangladesh. This research mainly aims to investigate whether MFIs are adding to achieving SDGs in Bangladesh. Additional objectives one of the research is: (a) to recognise the microfinance instruments by which financial organisations are adding to attaining SDG; (b) showing the progressive situation and efficiency of Microfinance Institutions in Bangladesh; (d) showing the function of microfinance organisations in attaining SDGs.The rest of the paper organised as follows. Section 2 provides an overview of the existing literature on the sustainable development goals of IMFIs; Section 3 describes the research methodology; Section 4 contains the analysis of the impact of sustainable development goals on MFI performance, and finally, Section 5 provides some concluding remarks.

Literature Review

Though the People's Republic of Bangladesh has recently entered the list of developing country and created a perspective arrange termed as ‘Vision 2021' that aim is to reinforce the sustainability, it has troubled against poverty financial condition present poverty rate is 13.8% (World Bank, 2018). Despite conducting some researchers work concerning the importance of finance tools achieve SDGs and MDGs, it is still mentionable to explore the contributions of Islamic Microfinance Institutions (IMFIs) towards the event of Bangladeshi economy. MFIs are developing their service within the method that enhances the access of poor people that increase saving and economic gain. MFIs to lunch branches in a remote area and considers indigenous people regardless of gender, to become employed to serve and train poor people (Tunisan, 2015). Moreover, Implementation of MDG accomplished remarkable improvement towards dealing with essential problems of Bangladesh like high poverty line and infrastructural debt. However, some complications are exiting in severe magnitude, which could become reduced to the minimum due to the outcomes of achieving SDGs. The achievement of achieving SDGs may be maximised with the usage of economic instruments that provides some options that are terribly according to obtaining SDGs. The alternative of financial debt funding by equity financing (Buiter & Rahbari, 2015; Nabi et al., 2019). Usman et al., (2016) Incontestable the function of micro-finance in prospering poor people's features from the attitude of abilities and understanding to type them economically self-employed that result in additional authorisation. MFIs structure flourish the human capabilities and capital that eventually prospects to human successfulness (Mamun et al., 2011).

Talking about the issues regarding future sustainability of the actions of the local company and Worldwide NGOs World Health Organization are working designed for the reduction of impoverishment (Khanam et al., 2018). Sustainable development goals number nine is certainly social businesses to ensure long-lasting sustainability. MFIs services contribute to poverty reduction and determine bottlenecks in MFIs applications and functions between social, financial help and social organisation and criticised the present program of social business apply in Muslim nation controversy the usage of Zakah containing with the guidelines. In additional authorities’ participation to reinforce the social business to alleviate poverty Ahmed et al. (2015).

3Journal of International Business and Management (JIBM)

https://rpajournals.com/jibm

Assessment of Micro-finance Institutions They are briefly talked about as follows: In 1995, Islamic microfinance brands is the Rural Development Scheme (RDS) was founded for ensuring equity, proper rights and work opportunity for the rural people. The structure is designed in a method to fulfil the investment requirements of the rural people, especially in the agricultural sector. It helps them to eliminate poverty and to become self-reliant. Until now, the scheme is known as among the most significant Islamic Microfinance applications across the country (Akter at el., 2018). According to the World Bank report in 2018, only 7 % of 1 million borrowers have access to financial services in Bangladesh. This small group of debtors have a much better chance to receive Islamic Microfinance services from RDS, not only because of its flexible conditions and circumstances of the loan but also due to low charge for loan amount (Obaidullah, 2008). Profit and Loss Sharing Financing Profit & loss sharing financing predicated on equity and involvement have a stable relationship to the pure economics which business lead for an equitable distribution of income and prosperity and help out with allocating resources effectively (Hussain et al., 2016; Hossain et al., 2019). Mamun et al., (2017) identified two forms of profit and loss sharing financing, i.e., mudaraba and musharaka whereas Dhaoui (2015) added three more products Musuqat (Orchard financing), Muzar’ah (Share of harvest) and direct investment with mudaraba and musharaka in his model (Rashid et al., 2018; Khan & Hassan, 2019). The RDS maintains a mandatory savings provision where each member deposits BDT10 per week under Mudarabah savings account. In case of urgency, the members are allowed to withdraw their accumulated savings if they are not indebted to the RDS. In addition to this saving arrangement, each member is required to contribute a minimum of BDT 2.00 per week, which is deposited into Mudarabah savings account under the name of the respective centre. By this, a pool of savings is created, which is later used as Microinsurance to cover the unexpected loss of the borrowers due to their accidents or sudden natural disasters. Non-Profit and Loss Sharing Financing The non-PLS sharing finance is used to provide financing fund to the consumer and corporate credit. It includes the instrument smurâbaḥa, ijārah, salam, and istisna (Haneefet al., 2015; Hussain et al., 2016). The Bai-muajjal is the only mode of financing currently practised by RDS. Some other potential modes of financing, like Mudharabah, Ijarah, and Bai-salam, are yet to adopt (IBBL, 2018). The individual group member requests for the financing in around eight weeks of the membership and the initial loan that he or she can get ranged between BDT 8000-10,000 to until BDT 30,000. Upon successful repayment of this category of loan, the members are then eligible to apply for a higher loan which is ranged between BDT30,000 to BDT 200,000 under Microenterprise Investment Scheme (MEIS). Regardless of the type of loan, group members are required to pay off their total debts (principal amount with profit) in 44 equal instalments weekly (IBBL, 2018; Parvin et al., 2018). Islamic Social Enterprise Based Financing From the viewpoint of insufficient available funds, the long-term sustainability of Islamic microfinance institutions is an issue because of the insufficient diversification of financing modes as the majority of them are Murabaha-centric. Furthermore, to it, revenue and reduction sharing are seldom used, though it is regarded as ideal. Some zakah, Awqaf and card al-Hasana structured Islamic microfinance organisations are being regarded as potential (Uddin & Barai, 2016; Cho et al., 2019). The idea of Islamic social business provides been received from social-business concept promoted by Nobel Laureate, Muhammad Yunus. As the principal purpose of it is not profit maximisation, it has been simplified and centred on social justice providing health care, accommodation along with safeguarding environmental degradation (Begum et al., 2018).The

4Journal of International Business and Management (JIBM)

https://rpajournals.com/jibm

Islamic social enterprises could be formed predicated on zakah, and card al-Hasana into two categories, i.e., Awqaf structured trustees and zakah structured. The RDS emphasises on moral and spiritual areas of the group members. They are applied through various programs; for example, it includes offering lessons on the cultural, social and spiritual responsibility to business lead the lives in the Islamic way. Additionally, it inculcates many moral lessons among the people, a few of the ideals include leading life truthfully, executing good deeds, abiding by regulations and abstaining from unlawful work, becoming self-reliant, doing work for prosperity, increasing health awareness and seeking knowledge through education. (IBBL, 2018). Charity Based Financing Charity based financing may include masque based, and direct charity-based financing consist of the instruments of Sadaqa, cash waqf, and zakat. Rasid et al. (2018) two modes of financing profit-based and charity-based financing. The instruments of charity-based financing are Zakat, sadaqa, waqaf, and qard-al-hasana where profit-based financing includes saving products such as Wadia and Mudaraba and funds from commercial banks and other industrial sources (Gundogdu et al., 2018; Suzuki et al., 2018; Cho et al., 2019). The importance of the microfinance institutions is contributive to the financial development in Bangladesh. The large and integral part of the country remains unbanked which might be offered by microfinance because the bank supported concepts has been got quality there. The regular microfinance role is cost-effective in financial condition alleviation than MFIs. Because of this, they advised the use of microfinance tools, that are contributive to the people, to improve their earning capabilities that business lead to poverty alleviation. Though financial tools are used significantly throughout the Muslim world as well as Bangladesh, there is no theoretical platform of microfinance in attaining SDGs. The research proposes a conceptual model in conjunction with exploring the efforts achieve SDGs to fill the gap. Conceptual Model to achieve SDGs This study focuses on the role of Islamic microfinance institutions such as Profit and loss sharing financing, non-profit and loss sharing financing, Islamic social enterprise-based financing and charity-based financing to achieve sustainable development goals.

Source: Developed by authors.

Research Methodology In their research, explained how the study conceptualised, how data would be collected and analysed for a similar study. Hence, it does not only provide the philosophical basis for the study but also the practical roadmap. This study adopted a causal research design. The design was adopted because the study is conceptualised in such a way that one thing causes another; for instance, the role of Islamic microfinance institutions and achieve sustainable development goals. There is total of 655 members

Non-profit & loss sharing financing Islamic social enterprise-based financing

Profit & loss sharing financing

Charity based financing

Sustainable Development Goals

5Journal of International Business and Management (JIBM)

https://rpajournals.com/jibm

of MRA. However, some institutions did not have available data while others have adequate data at their microfinance divisions.

This study used secondary data and applied a different kind of techniques and approaches in data processing, analysis and presentation. The techniques and approaches were determined by the type of data collected. The analysis was based on case study of Islamic Micro-finance in Bangladesh.

Results and Analysis

Sustainable Development Goals The Sustainable Development Goals (SDGs), otherwise known as the 2030 Agenda for Sustainable Development, was adopted on 25 September 2015 as an intergovernmental set of aspirations. The Official Agenda for Sustainable Development comprises 17 Sustainable Development Goals, but the primary concern of this paper centres on the following SDGs.

Table 1. Microfinance sector of Bangladesh (Basic Activities)

Data Source: MRA-MIS, 2018.

End poverty in all its forms everywhere. Increase in spatial inequalities and higher incidence of rural poverty although overall financial growth is connected with some macro-level economic plans (Suri et al., 2011; Garcia-perez et al., 2018). For example, the advertising of export-oriented agriculture offers been associated with decreased food protection for rural populations. Also, the central-place theory for urban development is frequently at the trouble of rural areas that lack infrastructure, jobs, low-quality education, and limited usage of basic needs (Weber, 2017). In lots of rural societies, limited possibilities, low levels of education, poor health and nutrition perpetuates the condition of rural poverty (Farrigan & Parker, 2012; Zin, 2013). As a result, persistent inequity in the society with regards to the distribution of power, wealth and other resources force some to stay in poverty (Prabhakar et al., 2015). To close the severe inequality gap and also eradicate poverty, governments will need to have a leading role and modification plan priorities and spending allocations. This principle function may galvanise other inclusive initiatives from civil society, spiritual organisations, donor organisations etc.

Particulars 2013 2014 2015 2016 2017

No. of Licensed NGO- MFIs 649 742 753 758 655 Cancelled License 40 56 64 84 88 No of Branches 14,674 14,730 15,609 16,284 17,120 No. of Employees 110,734 109,628 110,781 127,820 139526 No. of Clients (Million) 24.60 25.11 26.00 27.79 29.9 Total borrowers (Million) 19.27 19.42 20.35 23.28 24.85 Loan Disbursement (Tk. Billion) 432.28 462.00 634.00 787.00 1045.78

Agri Loan Disbursement (Tk. Billion)

131.98 155.73 266.25 353.00 408.87

Amount of Loan Outstanding (Tk. Billion)

257.01 282.20 352.41 459.37 583.62

Agri Loan Outstanding (Tk. Billion)

89.05 115.77 147.60 285.00 354.00

Amount of Savings (Tk.Billion) 93.99 106.99 135.41 171.19 216.71 Loan Recovery (Tk. Billion) 375.07 447.89 522.47 773 876.85

Recovery Rate 97.69 95.64 96.02 95.50 97.90

6Journal of International Business and Management (JIBM)

https://rpajournals.com/jibm

End Hunger To get rid of food cravings, there usually is a requirement making better possibilities for farmers and concentrate on the desires of undernourished organisations. Sustainability means using fewer organic assets to make food and improve nutrition through improved education and gain access to and availability of quality foods (Dreier, 2015; Gundogdu et al., 2018). Patterson (2013) opined that there are different ways to end world hunger, some have been effective and others not, but emphasised that the following are top solutions. Despite the benefits made on the MDGs, Usage of enough, safe and healthy food to meet dietary needs has turned into a significant challenge for thousands of people. Forcadell & Aracil (2019) shows that, to achieve global food security, social security nets, international crisis grain reserves. The SDG 2 target is achievable with better opportunities for farmers and focuses on the needs of undernourished groups (Dreier, 2015; Jose & Chacko, 2017). However, this goal has been criticized by the International Food Policy Research Institute (IFPRI) based on not being ambitious enough.

Good Health and Well-Being Ricard (2015) provides emphasised that to accomplish the SDGs; It wants to improve personal well-being, societal cohesion and better co-operation with our potential. It wants to move to the following level of co-operation to face the many issues of those situations. In cooperative communities, to address the problems of collective products and poverty during lots, it is required to provide about the voice of care, attention and altruism. The economic climate must be found to provide society, not to become offered by society. A healthy economy must abhor extraordinary inequality but motivate altruism, which can be having more factors for others. Mainly, government, recognised organisations and personal businesses should work in funding and offering critical public goods and protecting the interests of upcoming decades (Mia et al., 2018).

Quality Education According to Zahidi (2015), It has needed to move beyond initial study, then function to a model predicated on lifelong learning. Content and quality as well must modification with the focus on essential thinking. Business must play a critical role in the continuous skilling, up and reskilling-skilling of workers and broader communities (Wijesiri et al., 2015). Education is a required precondition of financial development (Coppock et al., 2012; Lam et al., 2019). It determines improvement in human well-being, not mainly the economy enhances health, increases society and the grade of organisations, strengthens resilience at all amounts and makes people happier (Lutz, 2015; Queralt & Romano, 2017). Economic growth follows education expansion because of the positive correlation between

economic growth and the educational level of the nation (Eichengreen et al., 2013; Ismail & Shaikh, 2018). To ensure higher productivity and economic growth, there is a need to have a critical mass of skilled and knowledge-based workers (Guan et al., 2011; Wamecke, 2015). There is the need to educate the economists and policymakers to make it a much higher priority in the development agenda. Hanushek and Woessmann (2015) argued that the most critical determinant of economic growth is knowledge capital of nations, which they define as the aggregate skills of the country’s population and which they measure by achievement scores on international mathematics and science examinations. This argument indicates that the importance of the education goal should be elevated because achieving it would provide the resources to reduce poverty, to improve health, and to provide for inclusive growth that lessens inequality within and between countries.

Gender equality SDG 5 seeks to halve extreme poverty in social groups based on age and gender. Females as a social group suffer devastation because they are burdened with manual function. Women in rural areas especially face an increased risk of poverty because of this of limited financial opportunities. There may be the have to translate these promotions into action by developing workplaces, governments, health care and education systems to supply an even playing field. To make sure that women are out from the extreme poverty trap and acquire equivalent decision-making power, it should take a social

7Journal of International Business and Management (JIBM)

https://rpajournals.com/jibm

protection ground for all. Similarly, ensuring social responsibility through the entire value chain, making suppliers follow equal pay and international labour requirements (Khalid & Kamaruddin, 2019). Decent Work and Economic Growth Well-functioning and transparent organisations are crucial in getting things correct and creating a well-balanced and predictable business environment essential to fuel expenditure, create jobs and facilitate the creation of higher value items and services within an economy (Drzeniek-Hanouz, 2015). It is reflective of a complete change in emphasis to even more meaningful and inclusive financial growth around the world not only about expanding national economies but by making sure the many vulnerable people in the culture are reached (Thakkar, 2015; Amesheva et al., 2019). For example, for businesses to show their function in sustainable advancement and be a robust force for social good, they need to be seen to improve the efficiency of economies through diversification, technological upgrading and development, encourage formalisation and development of micro, small and medium-sized enterprises. Thakkar (2015) recommended that to attain these targets at a macro level technology is among the main elements that may enable more inclusive financial growth in Bangladesh. The mobile ecosystem is a substantial driver of financial progress and welfare globally. However, the prospect of the mobile sector to transform Bangladesh societies will demand improved collaboration between all players in the community. On a micro level, we should factor in the function of small and medium enterprises to operate a vehicle job creation and financial growth, and also assisting entrepreneurship structural barriers for example access to markets, usage of finance and mentorship have to be resolved in a genuine and practical method (Schiano et al., 2017).

Reduced Inequalities There is a dependence on new policy frameworks and answers to drive growth that is inclusive and not limited by small elites. It is implied searching beyond redistribution to additional products that promote broad-based raises in living requirements for example entrepreneurship, well- functioning economic systems and the upholding of ethical ideals in business and public spheres (Blanke, 2015; Bui-Thanh et al., 2018). Pickett et al. (2015) have outlined five explanations of why the necessity to reduce global inequality. They described that health, social relationships, human capital development, economic progress and balance. Sustainable economies are not equally distributed in unequal societies and therefore, the necessity for equality. The wealthiest 0.7% of adults globally individuals holding over $1 million in wealth held about 44% of global net worth. Inequality emerged while a central concern today due to the developing body of proof that inequalities in income and prosperity cause economic instability, a variety of health and social complications, and detriment to pro-environment strategies and behaviour. Its repercussion impacts the social fabric hinders social cohesion and plays a part in environmental complications. They argued that life expectancy could be shorter and mortality prices are higher in more unequal societies. Levels of social cohesion, which includes trust and social capital, are reduced even more unequal societies. Indicators of women’s position and equality also tend to be worse. Even more equal countries generally have higher rates of innovation, probably due to greater social flexibility. Poverty reduction is compromised by income inequality. The International Monetary Fund (IMF) claims that reducing inequality and bolstering longer-term financial growth could be two sides of the same coin. Inequality drives position competition, which drives personal financial debt and consumerism. For actual improvements in worldwide population well-being, they need more equal societies. Achieving Sustainable Development The focus of SDGs towards financial advancement, environment sustainability and social inclusion has endured it to the developmental plans of nations (Sachs, 2012). This triple bottom level approach seeks to provide opportunities to the less privileged in the culture toward social,

8Journal of International Business and Management (JIBM)

https://rpajournals.com/jibm

environmental and financial performance. While the advantages of empowerment deals address their different vulnerabilities, besides, it assists in creating a sustainable environment and foster social cohesion. By concentrating on this great perspective, Microfinance is becoming a valuable tool to aid sustainable goals.

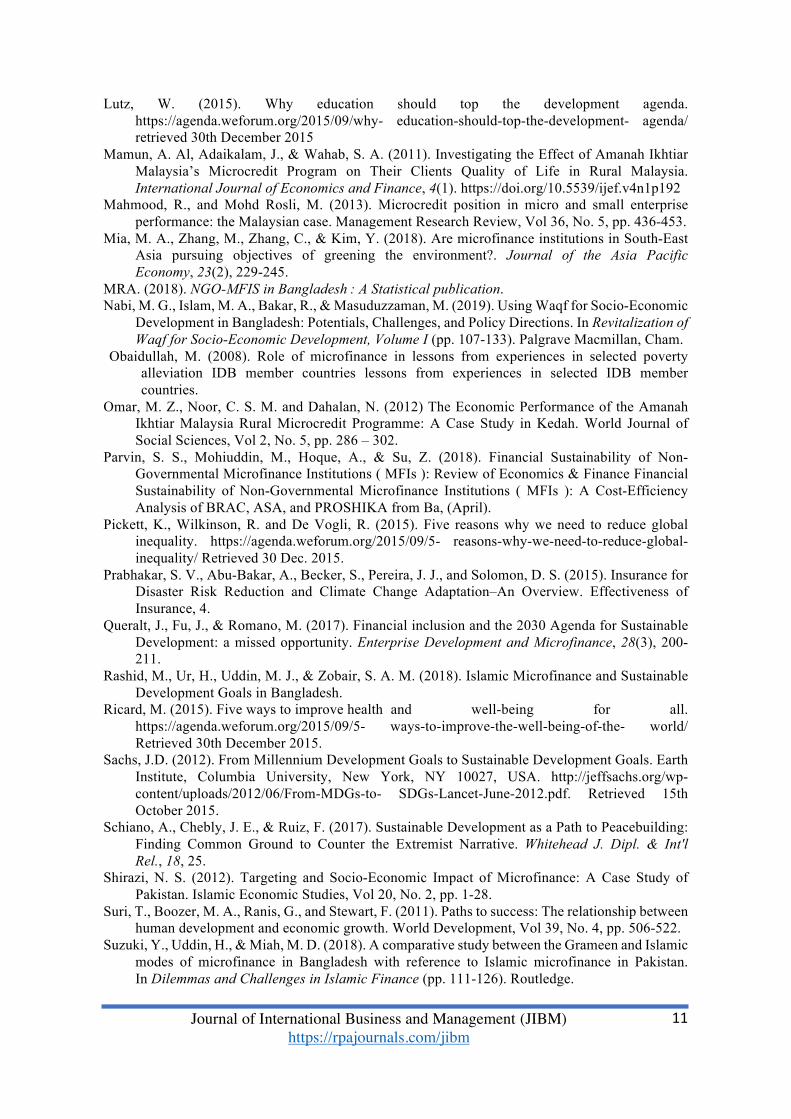

Table 2: Scenario of Islamic Microfinance in Bangladesh (2017)

Source: (i) Respective Islamic banks, (ii) Association of Muslim Welfare Associations

Bangladesh (AMWAB) and (iii) TMSS- Only conventional NGO with Islamic microfinance program. * Provisional data

There can be evidence to recommend that, this process of the SDGs is very much indeed included in the Micro-finance menu that provides Microcredit, Micro-saving and Micro-insurance (Table 2). The Micro-finance experiment has demonstrated the energy and success in achieving poor people, specifically in the rural areas and offers accelerated the development of their micro-enterprises (Mahmood and Mohd Rosli, 2013). Essentially, it is a prelude to entrepreneurial education and training, skills building, assets accumulation, self-reliance and communal services. This type of empowerment offers the possibility to have an effect on the client’s performance and enhance their micro and smaller businesses (Webster, 2015; Usman & Tasmin, 2016). The vulnerabilities of the indigent people have affected their self-reliance producing them with no self-confidence to contribute towards communal providers. The inclusive technique through Micro-finance empowerment gives them the capability to reinvent they are well worth and reap the benefits of increased national development, and the contribute meaningfully towards national development (Hatta and Ali, 2013). Assets will be the stock of prosperity that represents the long-term effects of income flows and expenditures, a necessary and more than enough condition for development and development (Table-

1.94

7

0.05

0.00

4

0.00

07

0.22

0.00

5 2.7

32.9

2

4.52

0.1

0.01

4.17

0.23

41.9

5

30.8

0.66

0.08

0.01 2.

77

0.03

34.3

6I s l a m i B a n k B a n g l a d e s h

L i m i t e d

A l A r a f a h I s l a m i c B a n k

L i m i t e d

F i r s t S e c u r i t y

I s l a m i B a n k L i m i t e d

S o c i a l I s l a m i c B a n k

L i m i t e d

I s l a m i c N G O s / M F I s

( 2 0 ) *

C o n v e n t i o n a l N G O w i t h

I s l a m i c M i c r o f i n a n c e

( 1 ) *

T o t a l

Is lamic Microfinance in Bangladesh (2017)

Number of Clients (Million)

Yearly Loan Didbursement (BDT in Billion)

Outstanding of Loan (BDT in Billion)

9Journal of International Business and Management (JIBM)

https://rpajournals.com/jibm

1). They will be the foundation of upcoming consumption and prosperity and are considered an essential indicator of empowerment (Al-Mamun et al., 2012). Standard of living of a home depends on the possession and quality of household assets.

Ownership of asset is an essential achievement towards financial viability and self- reliance. The more any individual, community or corporation has of every one of the above components, the stronger it is more capability it has and more empowered it is (Bartle, 2012). There are many varied methods by which Micro-finance is felt to have relevance on the client’s wellbeing. Microfinance empowerment has been thought to be an essential tool for reducing poverty and enhancing the household’s standard of living in terms of better and bigger houses and normal circumstances (Al Mamun et al., 2012). In addition, it plays a vital function in the empowerment of poor people, especially females, towards developing their micro-enterprises (Omar et al., 2012). The vulnerability of the poor is decreased, and their socioeconomic position improved with a much better wellness condition and the training level of their children (Table-1). Similarly, it enhances career development with a significant increase in firm functionality uniquely entrepreneurial ideals and management procedures (Mahmood and Mohd Rosli, 2013; Shirazi, 2012). The empowerment allows the clients to control the business enterprise and make decisions individually and also to participate in the community with improved self-esteem. This status allows them to control their financial life effectively, reduce stress and increase security.

Conclusion and Recommendation The significant achievements on the MDGs targets worldwide have justified the massive budgets and the concerted efforts in the last one and a half-decade. However, the progress made has been uneven across regions and countries especially for the poorest and the most vulnerable. The SDGs pursues aspirations to end hunger, ensure healthy lives and promoting well- being and promote opportunities for all, among other goals. To facilitate a better relationship between the poor and the rich, there is the need to encourage wealth transfer, increase the money supply and reduce poverty. In Muslim countries, Micro-finance is regarded as an essential tool for addressing wider deprivations and vulnerabilities of the poor. To address multidimensional deprivations, a variety of products such as Micro-credit, Micro-savings and Micro-insurance are crucial to the social cohesion of small groups, communities, institutions or societies.

It promotes entrepreneurial education and training, skills building, assets accumulation, self-reliance and communal services. Microfinance Empowerment focuses on reducing poverty and improving the household’s quality of life of the poor people especially women towards developing their micro-enterprises, and their socioeconomic status improved with better health condition. There is an indication that a significant increase in firm performance and participation in community activities has been achieved. This drive is towards sustainable lives that reduce stress and increases the security of poor people.

References

Ahmed, H. (2015). On the Sustainable Development Goals and the Role of Islamic Finance. Policy Research Working Paper 7266, (May).

Ahmed, H., Mohieldin, M., Verbeek, J., & Aboulmagd, F. (2015). On the sustainable development goals and the role of Islamic finance. The World Bank.

Akter, A., Ahmad, N., Jaafar, W. M. W., Zawawi, D. B., Islam, M. M., & Islam, M. A. (2018). Empowerment of Women through Entrepreneurial Activities of Self-Help Groups in Bangladesh. Journal of International Business and Management, 1(1), 1-15.

Amesheva, I., Clark, A., & Payne, J. (2019). Financing for Youth Entrepreneurship in Sustainable Development. Sustainable Development Goals: Harnessing Business to Achieve the SDGs through Finance, Technology, and Law Reform, 253-273.

Bartle, P. (2012). Elements of Community Strength. Measuring Community Empowerment. Community Empowerment Collective. http://cec.vcn.bc.ca/cmp/modules/mea-int.htm

10Journal of International Business and Management (JIBM)

https://rpajournals.com/jibm

retrieved 4th December 2015. Begum, H., Alam, A. F., Mia, M. A., Bhuiyan, F., & Ghani, A. B. A. (2018). Development of Islamic

microfinance: a sustainable poverty reduction approach. Journal of Economic and Administrative Sciences.

Blanke, J. (2015). Reduce inequality within and among countries http://www.weforum.org/agenda/2015/09/how-achievable-are-the-sustainable-development- goals/. Retrieved on 30th December 2015.

Buiter, W. H., & Rahbari, E. (2015). Why economists (and Economies) should love Islamic finance. Journal of King Abdulaziz University: Islamic Economics, 28(1).

Bui-Thanh, L., Morales, L., & Andreosso-O’Callaghan, B. (2018). Microfinance in Southeast Asia: The Case of Vietnam Over the Period 2005–2015. In Asian Nations and Multinationals (pp. 159-173). Palgrave Pivot, Cham.

Cho, S., Sultana, R., & Kwon, S. (2019). Social enterprise and sustainable development in Bangladesh and Korea: Opportunities and challenges. Asian Social Work and Policy Review, 13(2), 189-198.

Dhaoui, E. (2015). The role of Islamic Microfinance in Poverty Alleviation: Lessons from Bangladesh Experience.

Dreier, L. (2015). End hunger, achieve food security and improved nutrition and promote sustainable agriculture.http://www.weforum.org/agenda/2015/09/how-achievable-are-the-sustainable-development- goals/. Retrieved 30th December 2015.

Drzeniek-Hanouz, M. (2015). Promote sustained, inclusive and sustainable economic growth, full and productive employment and decent work for all. http://www.weforum.org/agenda/2015/09/how-achievable-are-the-sustainable- development-goals/. Retrieved 30th December 2015.

Farrigan, T., and Parker, T. (2012). The concentration of poverty is a growing rural problem. Amber Waves, 10 (4). USDA ERS. http://www.ers.usda.gov/amber- waves/2012-december/concentration-of- poverty.aspx#.VtJnxhjKo9K. Retrieved on 28 February 2016.

Forcadell, F. J., & Aracil, E. (2019). Can multinational companies foster institutional change and sustainable development in emerging countries? A case study. Business Strategy & Development, 2(2), 91-105.

Hanushek, E. and Woessmann, L. (2015). Why Universal Basic Skills Should Be the Primary Development Goal. http://www.weforum.org/agenda/2015/05/why-universal-basic-skills-should-be-the- primary-development-goal. Retrieved 20th January 2016.

Haneef, M. A., Pramanik, A. H., Mohammed, M. O., Bin Amin, M. F., & Muhammad, A. D. (2015). Integration of waqf-Islamic microfinance model for poverty reduction: The case of Bangladesh. International Journal of Islamic and Middle Eastern Finance and Management, 8(2), 246-270.

Hossain, I., Muhammad, A. D., Jibril, B. T., & Kaitibie, S. (2019). Support for smallholder farmers through Islamic instruments: The case of Bangladesh and lessons for Nigeria. International Journal of Islamic and Middle Eastern Finance and Management, 12(2), 154-168.

Islam, M. A., Hunt, A., Jantan, A. H., Hashim, H., & Chong, C. W. (2019) Exploring challenges and solutions in applying green human resource management practices for the sustainable workplace in the ready-made garment industry in Bangladesh. Business Strategy & Development. 1–12. https://doi.org/10. 1002/bsd2.99

Ismail, A. G., & Shaikh, S. A. (2018). Role of Islamic Economics and Finance in Sustainable Development Goals. Islamic Economic Studies and Thoughts Centre (IESTC), 1(1).

Khan, F., & Hassan, M. K. (2019). Financing the Sustainable Development Goals (SDGs): The Socio-Economic Role of Awqaf (Endowments) in Bangladesh. In Revitalization of Waqf for Socio-Economic Development, Volume II (pp. 35-65). Palgrave Macmillan, Cham.

Lam, S. S., Zhang, W., Ang, A. X., & Jacob, G. H. (2019). Reciprocity Between Financial and Social Performance in Microfinance Institutions. Public Performance & Management Review, 1-26.

Lindamood, D. (2017). Towards a more sustainable water future : water governance and Sustainable Development Goal 6 achievability in India by.

11Journal of International Business and Management (JIBM)

https://rpajournals.com/jibm

Lutz, W. (2015). Why education should top the development agenda. https://agenda.weforum.org/2015/09/why- education-should-top-the-development- agenda/ retrieved 30th December 2015

Mamun, A. Al, Adaikalam, J., & Wahab, S. A. (2011). Investigating the Effect of Amanah Ikhtiar Malaysia’s Microcredit Program on Their Clients Quality of Life in Rural Malaysia. International Journal of Economics and Finance, 4(1). https://doi.org/10.5539/ijef.v4n1p192

Mahmood, R., and Mohd Rosli, M. (2013). Microcredit position in micro and small enterprise performance: the Malaysian case. Management Research Review, Vol 36, No. 5, pp. 436-453.

Mia, M. A., Zhang, M., Zhang, C., & Kim, Y. (2018). Are microfinance institutions in South-East Asia pursuing objectives of greening the environment?. Journal of the Asia Pacific Economy, 23(2), 229-245.

MRA. (2018). NGO-MFIS in Bangladesh : A Statistical publication. Nabi, M. G., Islam, M. A., Bakar, R., & Masuduzzaman, M. (2019). Using Waqf for Socio-Economic

Development in Bangladesh: Potentials, Challenges, and Policy Directions. In Revitalization of Waqf for Socio-Economic Development, Volume I (pp. 107-133). Palgrave Macmillan, Cham.

Obaidullah, M. (2008). Role of microfinance in lessons from experiences in selected poverty alleviation IDB member countries lessons from experiences in selected IDB member countries.

Omar, M. Z., Noor, C. S. M. and Dahalan, N. (2012) The Economic Performance of the Amanah Ikhtiar Malaysia Rural Microcredit Programme: A Case Study in Kedah. World Journal of Social Sciences, Vol 2, No. 5, pp. 286 – 302.

Parvin, S. S., Mohiuddin, M., Hoque, A., & Su, Z. (2018). Financial Sustainability of Non-Governmental Microfinance Institutions ( MFIs ): Review of Economics & Finance Financial Sustainability of Non-Governmental Microfinance Institutions ( MFIs ): A Cost-Efficiency Analysis of BRAC, ASA, and PROSHIKA from Ba, (April).

Pickett, K., Wilkinson, R. and De Vogli, R. (2015). Five reasons why we need to reduce global inequality. https://agenda.weforum.org/2015/09/5- reasons-why-we-need-to-reduce-global- inequality/ Retrieved 30 Dec. 2015.

Prabhakar, S. V., Abu-Bakar, A., Becker, S., Pereira, J. J., and Solomon, D. S. (2015). Insurance for Disaster Risk Reduction and Climate Change Adaptation–An Overview. Effectiveness of Insurance, 4.

Queralt, J., Fu, J., & Romano, M. (2017). Financial inclusion and the 2030 Agenda for Sustainable Development: a missed opportunity. Enterprise Development and Microfinance, 28(3), 200-211.

Rashid, M., Ur, H., Uddin, M. J., & Zobair, S. A. M. (2018). Islamic Microfinance and Sustainable Development Goals in Bangladesh.

Ricard, M. (2015). Five ways to improve health and well-being for all. https://agenda.weforum.org/2015/09/5- ways-to-improve-the-well-being-of-the- world/ Retrieved 30th December 2015.

Sachs, J.D. (2012). From Millennium Development Goals to Sustainable Development Goals. Earth Institute, Columbia University, New York, NY 10027, USA. http://jeffsachs.org/wp- content/uploads/2012/06/From-MDGs-to- SDGs-Lancet-June-2012.pdf. Retrieved 15th October 2015.

Schiano, A., Chebly, J. E., & Ruiz, F. (2017). Sustainable Development as a Path to Peacebuilding: Finding Common Ground to Counter the Extremist Narrative. Whitehead J. Dipl. & Int'l Rel., 18, 25.

Shirazi, N. S. (2012). Targeting and Socio-Economic Impact of Microfinance: A Case Study of Pakistan. Islamic Economic Studies, Vol 20, No. 2, pp. 1-28.

Suri, T., Boozer, M. A., Ranis, G., and Stewart, F. (2011). Paths to success: The relationship between human development and economic growth. World Development, Vol 39, No. 4, pp. 506-522.

Suzuki, Y., Uddin, H., & Miah, M. D. (2018). A comparative study between the Grameen and Islamic modes of microfinance in Bangladesh with reference to Islamic microfinance in Pakistan. In Dilemmas and Challenges in Islamic Finance (pp. 111-126). Routledge.

12Journal of International Business and Management (JIBM)

https://rpajournals.com/jibm

Thakkar, A. (2015). How can Africa achieve growth for all its people? https://agenda.weforum.org/2015/09/how- can-Africa-achieve-growth-for-all-its-people/ retrieved 30 Dec. 2015.

Tunisan, E. D. (2015). The role of Islamic Microfinance in Poverty Alleviation: Lessons from Bangladesh Experience. Humanomics, 31(67323), 1–18. https://doi.org/10.1108/17538391111144515

Usman, S., Tasmin, R., Tun, U., & Onn, H. (2016). The Relevance of Islamic Micro-finance in achieving the Sustainable Development Goals. International Journal of Latest Trends in Finance & Economic Sciences IJLTFES, 6(August).

Uddin, H., & Barai, M. K. (2016). Islamic Microcredit: The Case of Bangladesh. Journal of Accounting, 6(1), 49-64.

Webster (2015). Elements of empowerment. Webster University 470 East Lockwood Avenue St. Louis, Missouri 63119 United States of America (800)981- 9801 http://www.webster.edu/public- safety/rad/elements-empowerment.html Retrieved 4th December 2015.

Weber, H. (2017). Politics of ‘leaving no one behind’: contesting the 2030 Sustainable Development Goals agenda. Globalizations, 14(3), 399-414.

Wijesiri, M., Viganò, L., & Meoli, M. (2015). The efficiency of microfinance institutions in Sri Lanka: a two-stage double bootstrap DEA approach. Economic Modelling, 47, 74-83.

Zahidi, S. (2015). Ensure inclusive and equitable quality education and promote lifelong learning opportunities for all. http://www.weforum.org/agenda/2015/09/how-achievable-are-the-sustainable- development-goals/. Retrieved 30th December 2015.

Zin, R. H. M. (2013). Malaysian Development Experience: Lessons for Developing Countries. Institutions and Economies (formerly known as International Journal of Institutions and Economies), Vol 6, No. 1, pp. 17-56.