international financial reporting standards -...

TRANSCRIPT

© 2008 DeVry/Becker Educational Development Corp.

Unauthorized reproduction is prohibited.

International Financial Reporting

Standards

© 2008 DeVry/Becker Educational Development Corp. Unauthorized reproduction is prohibited.

IFRS

Overview

IFRS Impacts

Accounting Framework

Financial Statement Presentation

Revenue & Expense Recognition

90

© 2008 DeVry/Becker Educational Development Corp. Unauthorized reproduction is prohibited.

Overview

International Standards Adoption

A. The IASB (International Accounting Standards Board) is an

international standard-setting body. Until recently, few countries

permitted International Accounting Standards (IAS) to be used. Within

the last seven years, IAS have become required or a permitted

alternative in a number of countries around the world.

B. Although IAS had been permitted in many countries, only about 275

companies worldwide actually prepared financial statements using the

standards by 2002. However, IAS use is steadily increasing and is

likely to skyrocket as a result of recent milestone events.

C. Approximately 40% of the Fortune Global 500 companies are reporting

using IFRS. There are over 12,000 companies now using some

version of IFRS.

27

© 2008 DeVry/Becker Educational Development Corp. Unauthorized reproduction is prohibited.

Overview

Globalization of IFRSThe globalization of business and finance has driven almost 12,000

companies in over 100 countries to adopt IFRS.

28

Brazil

2010

Chile

2009

Europe

2005

Japan

(?)

Australia

2005

South

Africa

2005

India

2011

China

2007

Canada

2009/11

U.S.

(2011?)

Current or anticipated requirement or option to use IFRS (or equivalent)

© 2008 DeVry/Becker Educational Development Corp. Unauthorized reproduction is prohibited.

IFRS Timeline

2007

SEC Issues "Concept Release"

on allowing U.S. issuers a

choice between U.S. GAAP or

IFRS.2007

Final report on equivalence of

IFRS and national GAAPs.

2014

Large accelerated filers could be

required to make transition to IFRS

for FYE's on or after 12/15/2014.

2007 2009 2011 2013 2015

2008 2010 2012 2014

March 2008

SEC eliminates U.S. GAAP

reconciliation for IFRS filers. (For

“Private” Foreign Issuers). 2008

SEC publishes a Roadmap toward IFRS for

public comment.

2015

Accelerated filers may be required

to make transition to IFRS for

FYEs on or after 12/15/2015.

2011

SEC to decide whether to mandate use of IFRS for all

U.S. issuers based on progress on milestones.

2016

2016

Transition to IFRS for non-accelerated

filers w/ FYEs on or after 12/15/2016.

2009

Certain U.S. issuers may begin using

IFRSs for fiscal years ending on or

after December 15, 2009.

4

© 2008 DeVry/Becker Educational Development Corp. Unauthorized reproduction is prohibited.

Overview

• IFRS is said to be less rules based and

more principles based. As a result

there are less ―bright lines‖ around how

to account for transactions and allows

for greater judgment and flexability for

financial statement presentation and

recognition.

© 2008 DeVry/Becker Educational Development Corp. Unauthorized reproduction is prohibited.

Overview—SEC Roadmap

• SEC Roadmap• November 14, 2008 SEC published proposed road map preparing

financial statements in accordance with IFRS

• Comment Period Ended February 19, 2009.

• Roadmap identifies seven milestones to be achieved including

SEC consideration of required adoption of IFRS by all U.S.

Companies

• Achievement of milestones will be part of SEC eventual

consideration of whether to require adoption of IFRS by all U.S.

Issuers

• The proposed roadmap would not establish a date certain for

adoption of IFRS by U.S. Issuers

© 2008 DeVry/Becker Educational Development Corp. Unauthorized reproduction is prohibited.

Overview--Milestones

• 2009-2011

1. Improvement of IFRS

2. Accountability and Funding of IFRS

3. Improvement in the ability to use interactive data

4. Education and training on IFRS in the U.S.

• 2009-2016—Transition plan for the mandatory use of IFRS

5. Limited early use by eligible subset of entities (next slide)

6. SEC to determine mandatory use based on milestones 1-4

and experienced gained in milestone 5.

7. Implementation of mandatory use for large accelerated

filers (companies with common shares outstanding of $700

million or more) and non-accelerated filers.

© 2008 DeVry/Becker Educational Development Corp. Unauthorized reproduction is prohibited.

Overview –SEC Road Map

• Definition of limited early use by eligible subset of

entities are U.S. issuers that:

• Are among the 20 largest companies worldwide in its

industry measured by market capitalization

• IFRS are used as the basis for financial reporting more

often than any other basis by the 20 largest companies in

that industry.

• SEC estimates at present a minimum of 110 U.S. issuers

would be eligible for early use.

• These 110 issuers had, as of December 2007, a total

market capitalization of $2.5 trillion, which represented

approximately 12 percent of total U.S. market capitalization

© 2008 DeVry/Becker Educational Development Corp. Unauthorized reproduction is prohibited.

Overview

Convergence

A. Joint projects

Joint projects are the projects that both boards have agreed to conduct

simultaneously in a coordinated manner. Joint projects involve sharing

staff resources, and every effort is made to keep joint projects to a

similar time schedule. The IASB and the FASB conducted joint projects

to address revenue recognition and business combinations.

34

© 2008 DeVry/Becker Educational Development Corp. Unauthorized reproduction is prohibited.

Overview

B. The Short-term Convergence Project

The short-term convergence project is an active agenda project that is

being conducted jointly between the IASB and the FASB. The scope of

the short-term convergence project is limited to those differences

between IFRS and U.S. GAAP in which convergence around a high-

quality solution appears achievable in the short-term. Because of the

nature of the differences, it is expected that a high-quality solution can

usually be achieved by selection of either existing IFRS or U.S. GAAP.

35

© 2008 DeVry/Becker Educational Development Corp. Unauthorized reproduction is prohibited.

Overview

C. The Convergence Research Project

The FASB staff are currently working on a research project related to

convergence. The project seeks to identify all of the substantive

differences between U.S. GAAP and IFRS and to catalogue those

differences. The project scope includes:

1. Differences in standards addressing recognition;

2. Measurement, and

3. Presentation and disclosure.

36

© 2008 DeVry/Becker Educational Development Corp. Unauthorized reproduction is prohibited.

IFRS

Overview

IFRS Impacts

Accounting Framework

Financial Statement Presentation

Revenue & Expense Recognition

90

© 2008 DeVry/Becker Educational Development Corp. Unauthorized reproduction is prohibited.

IFRS Impacts

B. The greatest impact will be on functions close to accounting such as:

1. Audit

2. Tax

C. Impact will most likely also be felt by:

1. Legal (contractual arrangements)

2. Treasury

3. Information technology

4. Human resources

5. Corporate communications

40

© 2008 DeVry/Becker Educational Development Corp. Unauthorized reproduction is prohibited.

IFRS Impacts

D. Impact on the Audit function:

1. Audit committee–will have to adapt to auditing

the new financials as prepared under IFRS.

2. Audit department will need to audit the actual transition

process from U.S. GAAP to IFRS, including when the

systems are being used in parallel.

3. Auditors will need to learn a new set of accounting

principles and be able to identify the key differences

between U.S. GAAP and IFRS.

KEY POINTAuditors will now be forced to modify their professional judgment under IFRS accounting.

• IFRS being principles-based will have less bright line guidance than auditors were

accustomed to under U.S. GAAP.

• This is also likely to impact the Audit Committee as they need to be sure that they

concur with the interpretations made by corporate financial management.

Audit

Tax

Legal

Treasury

IT

HR

Corp.

Comm.

41

© 2008 DeVry/Becker Educational Development Corp. Unauthorized reproduction is prohibited.

IFRS

Overview

IFRS Impacts

Accounting Framework

Financial Statement Presentation

Revenue & Expense Recognition

90

© 2008 DeVry/Becker Educational Development Corp. Unauthorized reproduction is prohibited.

Accounting Framework

Terminology – How we say it!

OR

Do you speak IFRS? Translating the terminology.

U.S. GAAP IFRS

Accrual

Equity

Inventory

Investee

Plan

Presents fairly

Stock

Provision

Reserves

Stock

Associate

Scheme

True and Fair

Shares

37

© 2008 DeVry/Becker Educational Development Corp. Unauthorized reproduction is prohibited.

Accounting Framework

International vs. U.S.

Financial Information: Qualitative Characteristics

The IFRS framework requires that

financial information must be:

A. Understandable

B. Comparable

C. Relevant

D. Reliable

Similar characteristics to the IFRS, with greater emphasis

placed on the consistency of financial statements.

IFRS

52

U.S. GAAP

FAC No. 2

-

Materiality

N eutrality

ConsistencyComparability1

Threshold forRecognition

Secondary and Interactive Qualities

R epresentational

F aithfulness

Ingredients ofPrimary Qualities

Primary Decision-Specific Qualities

User-SpecificQualities

Pervasive Constraint

Users of AccountingInformation

Decision Makers and Their Characteristics

(for example, understanding or prior knowledge)

Benefits > Costs

Understandability

Decision Usefulness

ReliabilityRelevance

V erifiabilityT imeliness

P redictiveValue

F eedbackValue

© 2008 DeVry/Becker Educational Development Corp. Unauthorized reproduction is prohibited.

Accounting Framework

Reporting Element

I. Overview

The IFRS Framework presents five reporting

elements:

A. Assets

B. Liabilities

C. Equity

D. Income (includes revenues and gains)

E. Expenses (includes losses)

II. Balance Sheet

Assets are resources controlled from a past

event. Liabilities are present obligation arising

from a past event. Assets and liabilities are

recognized on the balance sheet when it is

"probable" that economic benefits will flow in to

or out from the entity, and those benefits must

be able to be measured reliably. Equity is the

residual interest in the assets after deducting

the entity's liabilities.

III. Income Statement

Income is increases in economic benefits that

result in increases in equity other than those

relating to contributions from equity participants.

Expenses are decreases in economic benefits

that result in decreases in equity other than

those relating to distributions to equity

participants.

Reporting elements and the definition and

recognition criteria are similar to IFRS; U.S. GAAP

concept statements provide guidance on the

following:

A. Assets

B. Liabilities

C. Equity

D. Income

E. Gains

F. Expenses

G. Losses

H. Investment by Owners

I. Distributions to Owners

J. Other Comprehensive Income

Other comprehensive income includes all changes

in equity during a period, except those resulting

from investments by and distributions to owners

IFRS (IAS 1) U.S. GAAP (FAC 6)

53

© 2008 DeVry/Becker Educational Development Corp. Unauthorized reproduction is prohibited.

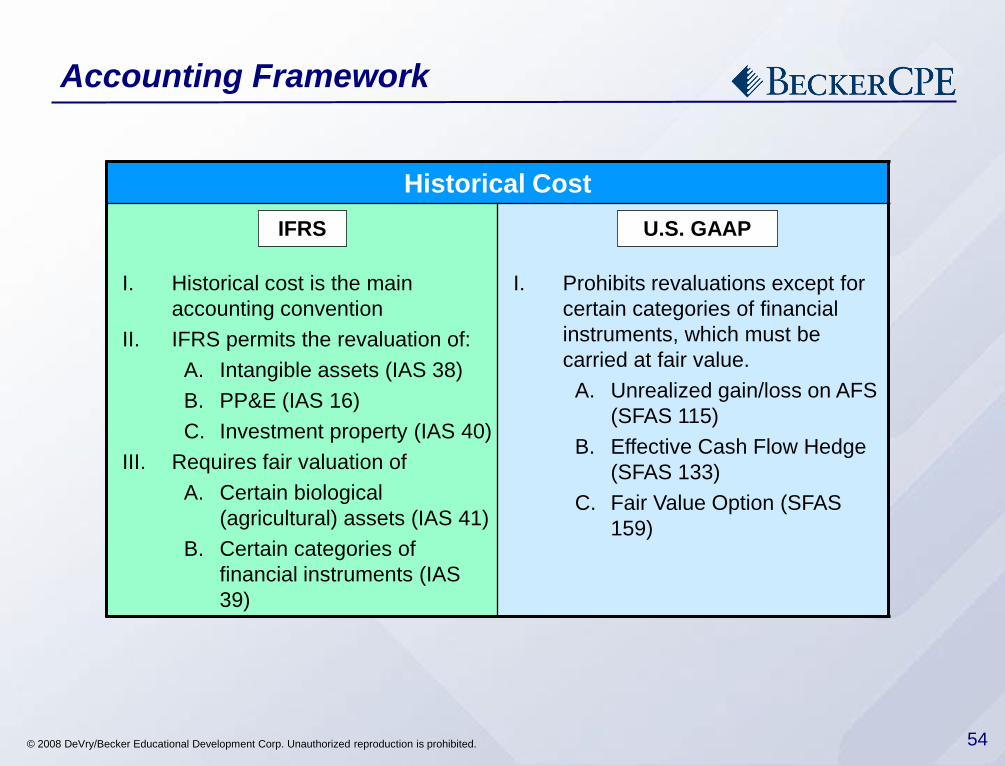

Accounting Framework

Historical Cost

I. Historical cost is the main

accounting convention

II. IFRS permits the revaluation of:

A. Intangible assets (IAS 38)

B. PP&E (IAS 16)

C. Investment property (IAS 40)

III. Requires fair valuation of

A. Certain biological

(agricultural) assets (IAS 41)

B. Certain categories of

financial instruments (IAS

39)

I. Prohibits revaluations except for

certain categories of financial

instruments, which must be

carried at fair value.

A. Unrealized gain/loss on AFS

(SFAS 115)

B. Effective Cash Flow Hedge

(SFAS 133)

C. Fair Value Option (SFAS

159)

IFRS U.S. GAAP

54

© 2008 DeVry/Becker Educational Development Corp. Unauthorized reproduction is prohibited.

IFRS

Overview

IFRS Impacts

Accounting Framework

Financial Statement Presentation

Revenue & Expense Recognition

90

© 2008 DeVry/Becker Educational Development Corp. Unauthorized reproduction is prohibited.

Financial Statement Presentation--IFRS

vs. GAAP -- Examples

I. Differences Between IFRS and GAAP

II. More than 200 differences exist between IFRS and GAAP

accounting. For example:

III. IFRS does not allow extraordinary items, in contrast to

GAAP.

IV. R&D development is capitalized under IFRS and expensed

under GAAP.

V. IFRS does not allow LIFO inventory costing, whereas

GAAP does.

© 2008 DeVry/Becker Educational Development Corp. Unauthorized reproduction is prohibited.

Statement of Cash Flows Presentation – General (continued)

I. Format

The Cash Flow Statement is a required

statement under IAS 7, not IAS 1. The

requirements of IAS 7 are similar to the

requirements of SFAS 95 in the U.S. with a few

exceptions.

II. Special Items

Finally, IAS requires that the cash flow effects of

extraordinary items and discontinued operations

be disclosed separately as arising from

operating, investing, of financing activities.

I. Format

SFAS 95 requires:

A. Operating

B. Investing

C. Financing

II. Special Items

U.S. GAAP permits a similar presentation

for extraordinary items, but does not require

such treatment.

Financial Statement Presentation

IFRS (IAS 7) U.S. GAAP (SFAS 95)

80

Operating or Financing

Operating or Investing

Operating or Financing

Operating or Investing

Operating – unlessSpecific identification with financing or investing

Classification Item

Interest Paid

Interest Received

Dividends Paid

Dividends Received

Taxes Paid

Operating

Operating

Financing

Operating

Operating

© 2008 DeVry/Becker Educational Development Corp. Unauthorized reproduction is prohibited.

IFRS

Overview

IFRS Impacts

Accounting Framework

Financial Statement Presentation

Revenue & Expense Recognition

90

© 2008 DeVry/Becker Educational Development Corp. Unauthorized reproduction is prohibited.

Revenue & Expense Recognition

Revenue Recognition

I. The entity has transferred to the buyer

the significant risks and rewards of

ownership of the goods.

II. The entity retains neither continuing

managerial involvement nor effective

control over the goods.

III. It is probable that economic benefits will

flow to the entity.

IV. The stage of completion of the

transaction can be measured reliably.

V. The amount of revenue can be

measured reliably.

VI. The costs incurred or to be incurred in

respect of the transaction can be

measured reliably.

I. Revenue recognition criteria (SAB 104)

A. Persuasive evidence of an

arrangement exists.

B. Delivery has occurred or services

have been rendered.

C. Vendor's price to the buyer is fixed or

determinable.

D. Collectability is reasonably assured.

II. Multiple-element arrangements (EITF 00-

21): Issued to address revenue

arrangements with multiple deliverables

III. Software Revenue Recognition (SOP 97-

2)

IV. More than 200 pronouncements for

guidance

IFRS (IAS 18 & IAS 11) U.S. GAAP

91

© 2008 DeVry/Becker Educational Development Corp. Unauthorized reproduction is prohibited.

Overview of General Principles

Criteria per

U.S. GAAP

IAS 18

Goods Services

Evidence of

ArrangementImplicit Implicit

DeliveryTransfer of Risks

& Rewards

As performed

(Percent

Completed)

Fixed or

Determinable

Price

Reliable

Measurement

Reliable

Measurement

Collectability

Probable

economic

benefits will flow

to the entity

Probable

economic

benefits will flow

to the entity

92