internal revenue service balanced measurement...

TRANSCRIPT

Internal Revenue Service Balanced Measurement System

Roseanne Mobley, Acting ChiefOffice of Survey Management

Office of the Chief Financial OfficerInternal Revenue Service

Mandate of IRS

The mandate of the IRS is outlined in its Mission:

"Provide America's taxpayers top quality service by helping them understand and meet their tax responsibilities and by applying the tax law with integrity and fairness to all."

Vision of IRS

The Mission of the IRS is reflected in its Vision:

"The IRS in 2009 is a 21st Century agency with the human capital and technology capabilities to effectively and efficiently collect the taxes owed with the least disruption and burden to taxpayers."

IRS Values

The IRS Mission and Vision are achieved though its Values:• Integrity• Accountability• Accuracy• Respect• Professionalism• Partnering

Factors Affecting Achievement of the Vision

Achievement of the IRS Vision is affected by a number of external and internal factors:External Factors• Legislative changes• Internet and other electronic media• Abusive tax avoidance transactions• Increasingly diverse population• Globalization• TerrorismInternal Factors• Workforce renewal and development• Changes in the workforce

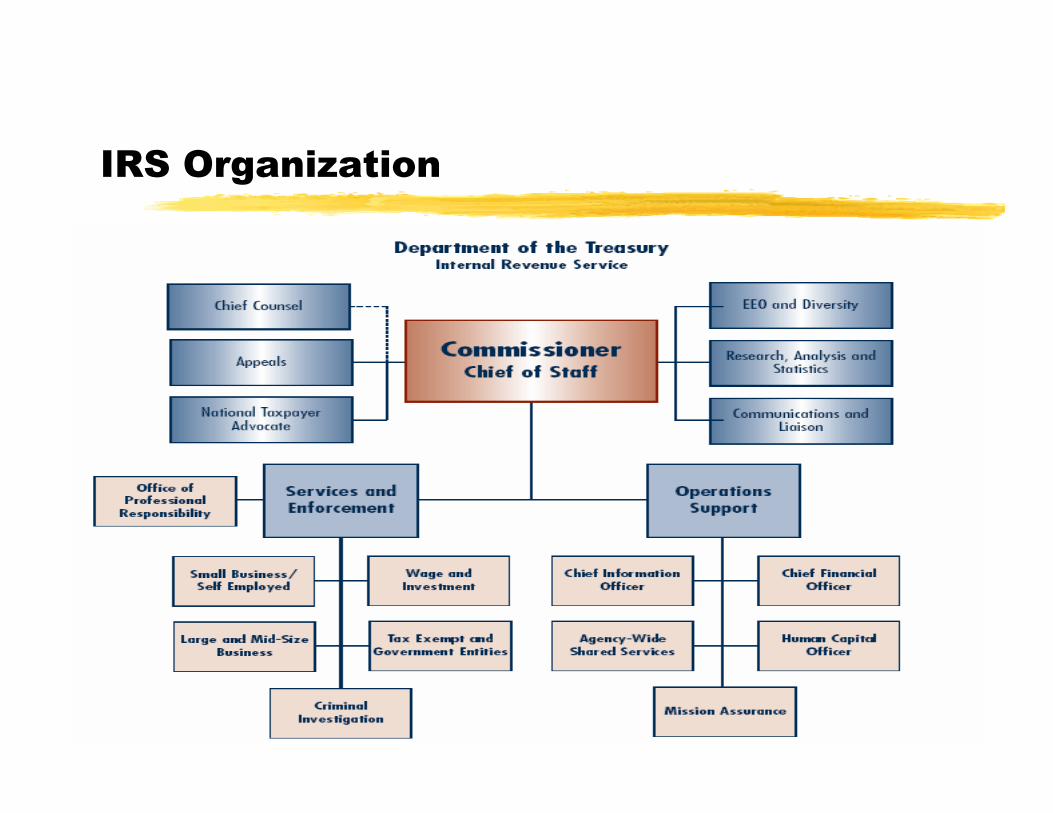

IRS Organization

IRS Market Segments

Legal Framework of U.S. Tax Administration

• Tax laws are passed by the U.S. Legislature (Senate and Congress), signed into law by the President, and then published within the Internal Revenue Code.

• U.S. tax laws are based on "Voluntary Compliance" which means each taxpayer is responsible for determining their correct tax, filing the appropriate return(s), and paying any tax balance due.

• Taxes in the United States are Administered by the Internal Revenue Service a bureau of the United States Treasury Department.

Voluntary Compliance

While the Internal Revenue Service relies on voluntary compliance from the vast majority of taxpayers, historically theService was granted significant enforcement authority to deal with non-compliant taxpayers independent of court oversight:

• Authority to administratively assess tax, penalty and interest.• Authority was delegated to individual employees to seize assets.

Taxpayer Attitude

• Most U.S. taxpayers voluntarily comply and pay their taxes on time.

• But in a free society there are individuals and groups who either don't agree with the tax laws or with the way the government spends tax dollars. They seek to avoid their tax responsibilities.

• This is where compliance laws are used to enforce each taxpayer’s responsibility to pay the correct tax.

Measuring Performance

• Methods of measuring performance have evolved, as have the public’s attitude and acceptance of IRS activities in dealing with non-compliance.

• The delegated level of enforcement authority has evolved along with these other changes.

Evolution of Performance Measures

1970 – 1980

Measurement of performance for the most part focused on enforcement actions initiated to obtain compliance:• Number of seizures • Dollars collected per staff hour• Dollars assessed by the IRS Examination function

In 1973 the IRS responded with Policy Statement P-1-20, intended to reduce the emphasis on enforcement activity.

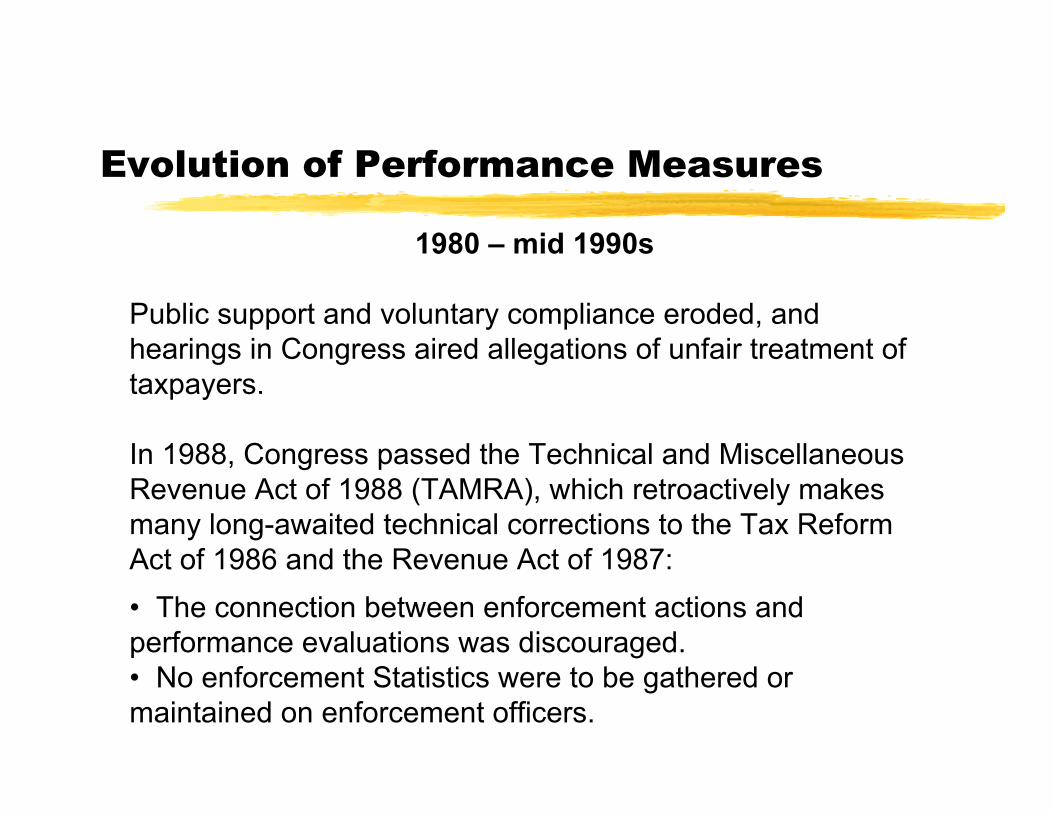

Evolution of Performance Measures

1980 – mid 1990s

Public support and voluntary compliance eroded, and hearings in Congress aired allegations of unfair treatment of taxpayers.

In 1988, Congress passed the Technical and Miscellaneous Revenue Act of 1988 (TAMRA), which retroactively makes many long-awaited technical corrections to the Tax Reform Act of 1986 and the Revenue Act of 1987:• The connection between enforcement actions and performance evaluations was discouraged.• No enforcement Statistics were to be gathered or maintained on enforcement officers.

Evolution of Performance Measures

Mid 1990s to date

Allegations of unfair treatment continued in Congress. The Taxpayer Bill of Rights was passed, providing legislated protections for taxpayers.

The IRS Restructuring and Reform Act of 1998 provided very specific direction for the collection of taxes and the rights tobe provided taxpayers. Significant safeguards were implemented to protect taxpayer rights:• Wide range of appeal procedures for taxpayers• Establishment of the internal Taxpayer Advocate position• Personal penalties for employees who intentionally violated taxpayer rights

Mandates for Performance Measurement Change

• The Internal Revenue Service Restructuring and Reform Act of 1998 (RRA 98) required the IRS to change its measures to balance customer service with overall tax administration responsibilities

• Treasury Regulation Part 801-- Balanced System for Measuring Organizational and Employee Performance -- implements the IRS Balanced Measurement System

Previous Approaches

• Emphasis on Achieving Measures

• Dependent on Dollar Results• No Customer or Employee

Measures• Large Number of Measures• Process Measures Used

Balanced Approach

• Emphasis on Achieving Mission• Balanced Priorities• New Customer Satisfaction and

Employee Satisfaction Measures• Small Number of Measures• Outcome Measures Used

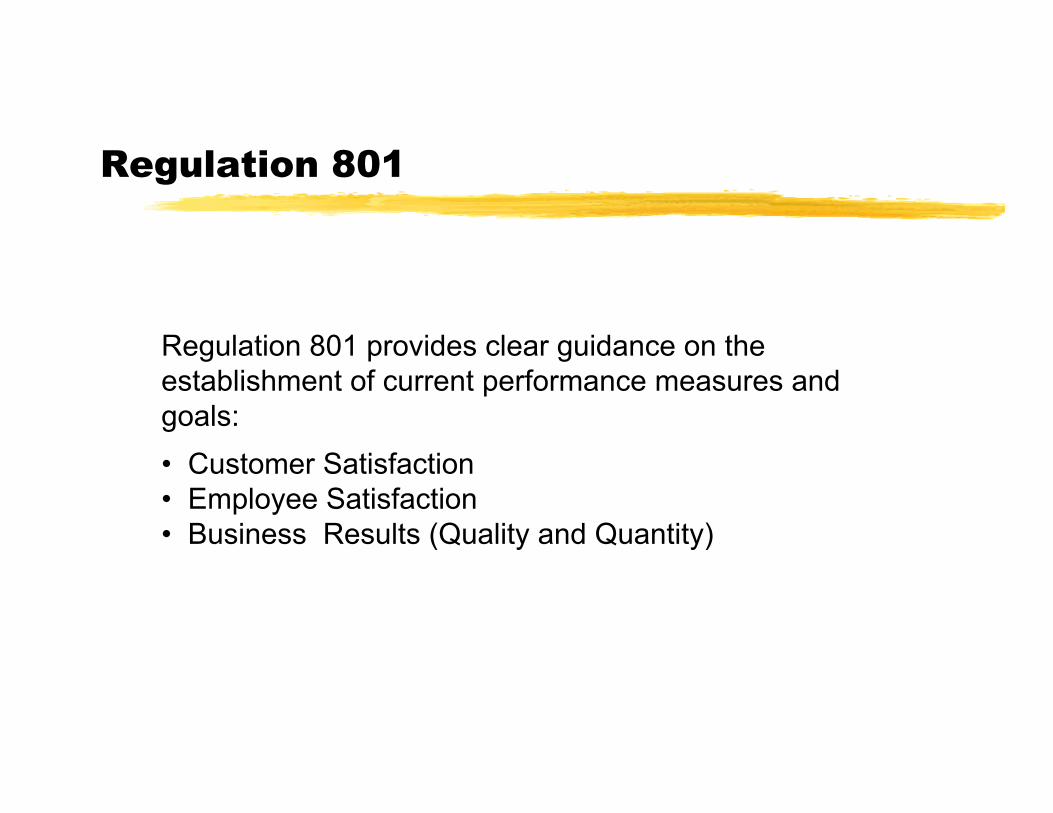

Regulation 801

Regulation 801 provides clear guidance on the establishment of current performance measures and goals:• Customer Satisfaction• Employee Satisfaction• Business Results (Quality and Quantity)

Overview of the IRS Balanced Measurement System

Business Results

Customer Satisfaction

Employee Satisfaction

• Provide accurate and professional services to internal and external customersin a courteous, timely manner

• Create an enabling environment for employees by providing quality leadership, adequate training, and effective support services

• Generate a productive quantity of work in a quality manner and provide meaningful outreach to all customers

Objectives of the IRS Balanced Measurement System

• Translate the IRS mission, vision, and strategic goals into a tool to:– Communicate organizational priorities– Guide and motivate performance– Obtain feedback

• Establish Employee Satisfaction and Customer Satisfaction as organizational objectives equal in importance to Business Results

• Support managers in taking actions to foster employee and customer satisfaction

• Provide a clearer picture to customers of how IRS values improving customer and employee satisfaction

Balanced Measures and the Management Hierarchy

Strategic

Strategic

Operational

Diagnostic toolGoals/Targets

Employee Critical Job ElementsIndividual/Managerial

Performance Appraisals

IRS Level

Business Unit

Individual Level

A Framework to Link Measures with Strategic Goals -- 2001

STRATEGIC GOALS AND OBJECTIVES

Service to Each Taxpayer

Make filing easier• Provide first quality service to each

taxpayer needing help with his or her return or account

• Providing prompt, professional, helpful treatment to taxpayer in cases where additional taxes may be due

Service to All Taxpayers

• Increase fairness of compliance• Increase overall compliance

Productivity through a Quality Work Environment

• Increase employee job satisfaction• Hold agency employment stable while

economy grows and service improves

• Overall Customer Satisfaction• Burden

• Payment Compliance• Filing Compliance• Reporting Compliance

• Overall Employee Satisfaction• Workload Resource Index

SERVICE-WIDE AND MAJOR CUSTOMER SEGMENT STRATEGIC MEASURES

• Customer Satisfaction with specific products and services

• Quantity of work products and services produced

• Quality, accuracy and timeliness of products and services provided

• Organizational Unit and Work Group Employee Satisfaction

OPERATING UNIT OPERATIONAL MEASURES

• Diagnostic data that is helpful in understanding what influences and impacts operational and strategic measures.• Workload data used to project expected levels of activity for an organizational unit or program.

DIAGNOSTIC AND WORKLOAD INDICATORS

• Performance plans or agreements for executives, managers and management officials aligned with strategic goals and balanced measures of customer satisfaction, employee satisfaction, and business results.

• Critical job elements for front-line employees aligned with the the goals of balanced measures.

INDIVIDUAL MEASURES

IRS

Bal

ance

d M

easu

rem

ent S

yste

mO

r ganiz ation al Per formance

A Framework to Link Measures with Strategic Goals -- 2005

STRATEGIC GOALSImprove Taxpayer Service

• Improve Service Options for the Tax Paying Public

• Facilitate Participation in the Tax System by All Sectors of the Public

• Simplify the Tax Process

Enhance Enforcement of the Tax Law

• Discourage and Deter Non-Compliance

• Ensure that Tax Practitioners Adhere to Professional Standards and Follow the Law

• Detect and Deter Domestic and Offshore-Based Tax and Financial Criminal Activity

• Deter Abuse within Tax-Exempt and Governmental Entities and Misuse of such Entities by Third Parties for Tax Avoidance or Other Unintended Purposes

Modernize the IRS through Its People, Processes, and

Technology

• Increase Organizational Capacity to Enable Full Engagement and Maximum Productivity of Employees

• Modernize Information Systems to Improve Service and Enforcement

• Ensure the Safety and Security of People Facilities, and Equipment

• Modernize Business Processes and Align the Infrastructure Support to Maximize Resources Devoted to Front-line Operations

• Customer Satisfaction Data• Rate of Accuracy• Burden Reduction• Level of Service• Rate of Electronic Interactions• Timeliness of Responding to

Customer Inquiries

• Rate of Reporting Compliance• Rate of Filing Compliance• Rate of Payment Compliance• Percent of Priority Guidance List

Items Published• Percent of Americans Who Think It

Is OK to Cheat on Taxes• Average Cycle Time

• Level of Employee Engagement• Index of Employee Perceptions of

Performance Management System• President’s Management Agenda

Scorecard• Ratio of Mission Critical

Occupations (MCO) Employees to Non-MCO Employees

• Benchmark IT Services and Development to Private Industry standards for Cost, and Scheduled, and Functionality

STRATEGIC MEASURES

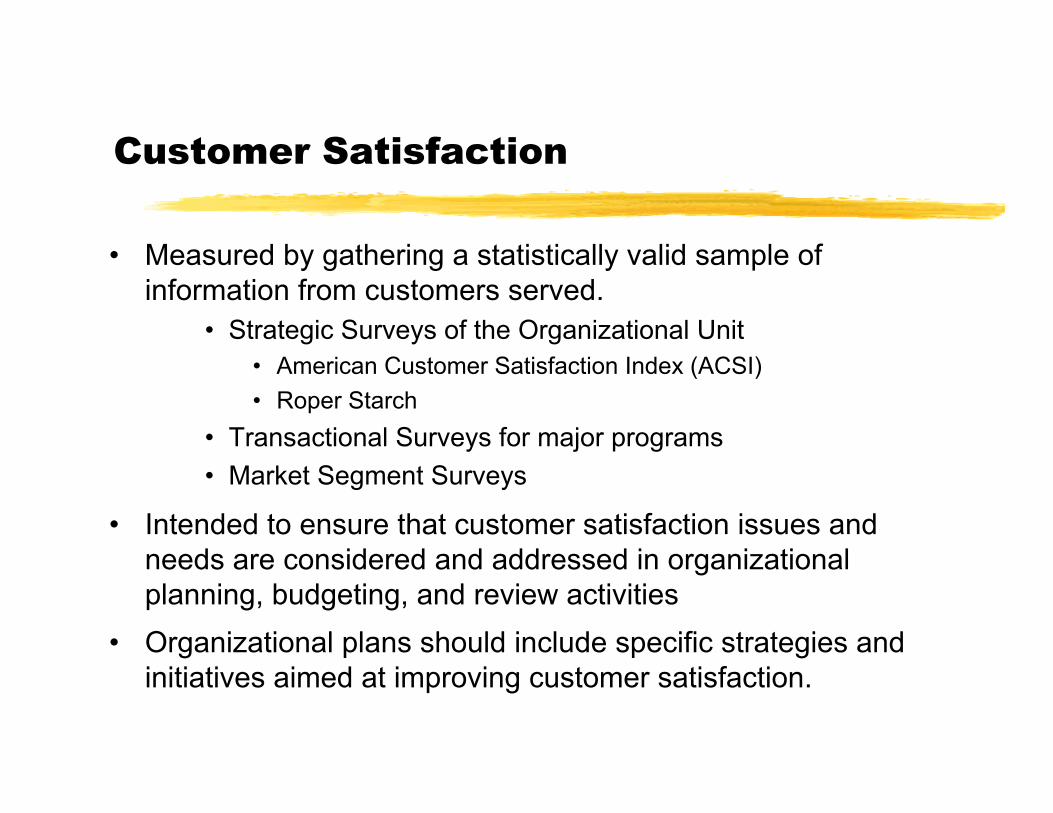

Customer Satisfaction

• Measured by gathering a statistically valid sample of information from customers served.

• Strategic Surveys of the Organizational Unit• American Customer Satisfaction Index (ACSI)• Roper Starch

• Transactional Surveys for major programs• Market Segment Surveys

• Intended to ensure that customer satisfaction issues and needs are considered and addressed in organizational planning, budgeting, and review activities

• Organizational plans should include specific strategies and initiatives aimed at improving customer satisfaction.

Employee Satisfaction

• Census Survey -- measures organizational units, sub-units, and work groups by all-employee annual survey

• Intended to ensure that employee satisfaction issues and needs are considered and addressed in organizational planning, budgeting, and review activities.

• Organizational plans should include specific strategies and initiatives aimed at improving employee satisfaction.

Business Results

• Quantity is measured through outcome-neutral production and resource data:• Number of cases closed• Hours expended

• Quality is measured through review systems which compile data such as:• Accuracy• Timeliness

• Intended to ensure that a productive quantity of work is generated in a quality manner.

• Organizational plans should include specific targets for business results.

(A regulatory limitation on the use of quantity measures requires that goals or targets not be set for measures except in conjunction with goals for customer satisfaction, employee satisfaction, and quality measures.)

Measures and the IRS Management Model

Plan

Review

DoRevise

PLAN: Balanced Measures are included in the plan as indicators of where IRS wants to go and answers the question: “How will we know if we’ve achieved the strategy?”

DO: Ongoing analysis of Balanced Measures data including diagnostic indicators and trends.

REVISE: As a result of review discussions, Balanced Measures and actions may be adjusted or goals revised.

REVIEW: Balanced Measures are used in periodic assessments of how well IRS achieved plan goals with an emphasis on “getting behind the numbers.”

OngoingDay- to- Day

Management

Corporate Performance Tracking

• Balanced Measure Goals are aligned with Operating and Functional corporate Business Results (quality/quantity), Employee Satisfaction, and Customer Satisfaction measures, which are gathered for each function.

• 74 critical measures are tracked as performance indicators.

• Results of data gathered are compiled and reported on monthly, quarterly, semiannual, or annual time periods depending on the statistic.

Theory in Practice: Modernization and Information Technology Services

MITS Balanced Measures:• Business Results

• Percent Systems Response Time• Percent Systems Availability• Percent of Production Priority 1 Software ITAMS Tickets

Resolved Timely by BSD• Employee Satisfaction

• Annual Employee Survey• Overall Customers Satisfaction and Dissatisfaction

• Enterprise Service Desk Transaction Survey• RIS Customer Survey• Master Service Level Agreement (MSLA) Customer Survey• End User Surveys

Theory in Practice: Modernization and Information Technology Services

MITS Balanced Measures Reporting:• MITS Strategy and Program Plans (S&PPs) (Annual)• MITS Business Performance Reviews (BPRs) (Quarterly)• MITS Presentation to IRS Oversight Board - Performance Subcommittee (Quarterly)• Monthly Business Performance Summary (MBPS) (Monthly) • Business Performance Management System (BPMS) (Monthly)

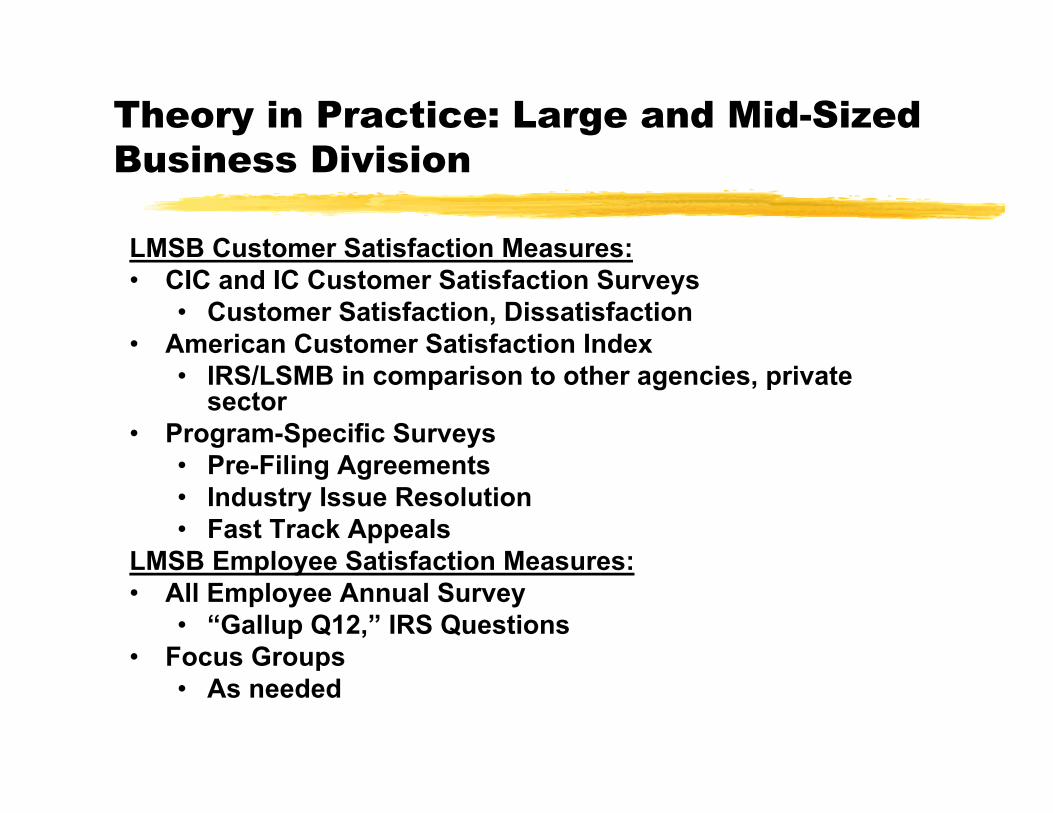

Theory in Practice: Large and Mid-Sized Business Division

LMSB Customer Satisfaction Measures:• CIC and IC Customer Satisfaction Surveys

• Customer Satisfaction, Dissatisfaction• American Customer Satisfaction Index

• IRS/LSMB in comparison to other agencies, private sector

• Program-Specific Surveys• Pre-Filing Agreements• Industry Issue Resolution• Fast Track Appeals

LMSB Employee Satisfaction Measures:• All Employee Annual Survey

• “Gallup Q12,” IRS Questions• Focus Groups

• As needed

Theory in Practice: Large and Mid-Sized Business Division

LMSB Business Results Measures – Quality:• LQMS CIC and IC

• Quality Standards• Elements• Process Measures

• Timeliness• Cycle Time• Currency

LMSB Business Results Measures – Quantity:• Cases Closed -- CIC• Returns Closed -- IC• Direct Staff Years -- CIC, IC, Tax Shelters

Theory in Practice: Large and Mid-Sized Business Division

L M S B O rg a n iza tio n a l P e rfo rm a n c e M a n a g e m e n t F ra m ew o rk

E s ta b lis h m e n t o fB a la n c e d M e a s u re sG o a ls

U s e o f M e a s u re s InD riv in g a n dA s s e s s in gO rg a n iza tio n a lP e rfo rm a n c e

O rg a n iz a tio n a lL e v e l

C IC IC

U s e o f D ia g n o s ticIn d ic a to rs toU n d e rs ta n d a n dM o n ito r B a la n c e dM e a s u re sP e rfo rm a n c e a n dW o rk p la n .

C IC IC

U s e o f M e a s u re s a n dD ia g n o s tic s InA s s e s s in g In d iv id u a lP e rfo rm a n c e

N o te s

L M S B D iv is io n -L e v e l

M e a s u re s re su lts in fo rmb u t d o n o t d ire c tlyd e te rm in e m a n a g e r ia le va lu a tio n

E m p h a s is is o na p p ro p ria te n e s s o fa c tio n s ta k e n toe s ta b lish a n d m e e tL M S B g o a ls .

In d u s tryD ire c to r L e v e l

M e a s u re s re su lts in fo rmb u t d o n o t d ire c tlyd e te rm in e m a n a g e r ia le va lu a tio n

E m p h a s is is o na p p ro p ria te n e s s o fa c tio n s ta k e n toe s ta b lish a n d m e e tIn d u s try a n d L M S Bg o a ls .

D ire c to r o fF ie ldO p e ra tio n s

M e a s u re s re su lts in fo rmb u t d o n o t d ire c tlyd e te rm in e m a n a g e r ia le va lu a tio n

E m p h a s is is o na p p ro p ria te n e s s o fa c tio n s ta k e n inm e e tin g D F O a n dIn d u s try g o a ls .

T e rrito ryM a n a g e r

E ffe c tive n e ss o f u s in gd ia g n o s tic d a ta to in fo rmd a y-to -d a y b u s in e s sd e c is io n s a n d th e im p a c to n m e a s u re s g o a ls isco n s id e re d .

T e rr ito ry M a n a g e re x p e c te d to ta k ea c tio n s to s u p p o rth ig h e r le ve l g o a ls .

T e a m M a n a g e r E ffe c tive n e ss o f u s in gm e a s u re s a n d d ia g n o s ticd a ta to in fo rm d a y-to -d a yb u s in e s s d e c is io n s isco n s id e re d .

T e am M a n a g e re x p e c te d to ta k ea c tio n s to s u p p o rth ig h e r le ve l g o a ls .

R e v e n u e A g e n t C ritic a l J o b E le m e n tslin k w itho rg a n iza tio n a l g o a ls .

F ra m e w o rk is C o ns is ten t w ith T re a s u ry R e g u la tio n 8 0 1 a n d IR M 1 .5

Theory in Practice: Large and Mid-Sized Business Division

Organizational Level Quantity Measures(cases closed, timeapplied)

Quality Measures(LQMS)

Quality Measures(Timeliness – cycletime, currency)

CustomerSatisfaction

EmployeeSatisfaction

Data available at alllevels, but theestablishment ofquantity goals is limitedby Regulation 801 andIRM 1.5 to those levelsfor which all balancedmeasures data isavailable.

Data available only toDFO level for IC /Industry Director levelfor CIC

Data available at alllevels, but expectationthat goals set only atlevel for which allbalanced measures areavailable

Data available only toDFO level for IC /Industry Director levelfor CIC

Data available at alllevels.

LMSB Division-Level Quantitative Goal Quantitative Goal Quantitative Goal Quantitative Goal Quantitative Goal

Industry DirectorLevel

Quantitative Goal Quantitative Goal Quantitative Goal Quantitative Goal Quantitative Goal

Director of FieldOperations

Quantitative Goal – ICQualitative Action – CIC

Quantitative Goal – ICQualitative Action – CIC

Quantitative Goal – ICQualitative Action – CIC

Quantitative Goal – ICQualitative Action – CIC

Quantitative Goal

Territory Manager Qualitative Action Qualitative Action Qualitative Action Qualitative Action Qualitative Action

Team Manager Qualitative Action Qualitative Action Qualitative Action Qualitative Action Qualitative Action

Revenue Agent Qualitative Action Qualitative Action Qualitative Action Qualitative Action Qualitative Action

Quantitative – Numeric goal, such as “increase by 5%” or “obtain 85% CIC quality rate.”Qualitative – Stated improvement, but not associated with a specific numeric increase/target. “Take actions to improve timeliness, quality over our currentbaselines.”

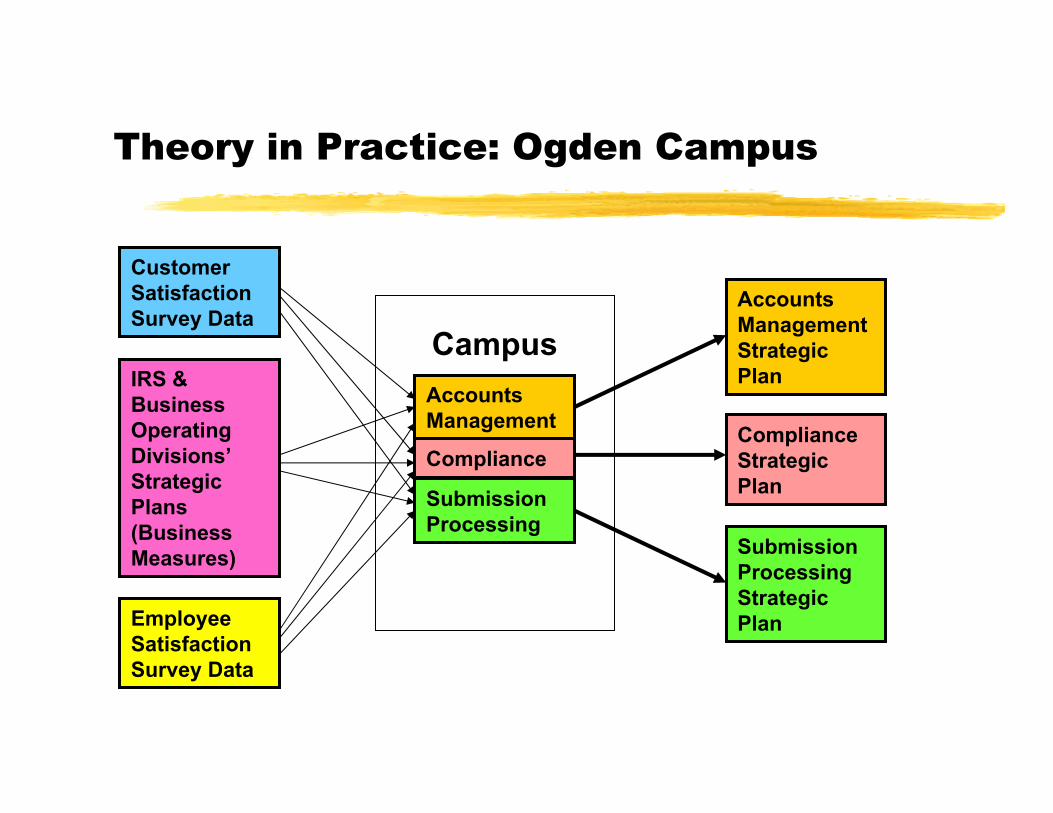

Theory in Practice: Ogden Campus

Accounts Management

Compliance

Submission Processing

Accounts Management Strategic Plan

Employee Satisfaction Survey Data

IRS & Business Operating Divisions’ Strategic Plans (Business Measures)

Customer Satisfaction Survey Data

Compliance Strategic Plan

Submission Processing Strategic Plan

Campus