intermarket perspective - hascol-...

TRANSCRIPT

Inter Market Perspective

To find our Research on Bloomberg, please type - IMKP <GO> www.jamapunji.pk

ANALYST CERTIFICATION AND REQUIRED DISCLOSURES BEGIN ON PAGE 17 & 18

Research Entity Number – REP-085

20 February 2017

Muneeb Naseem

+92-21-37131600 Ext. 305

..

• We reinstate coverage on HASCOL – the 3rd

largest OMC in Pakistan – with a Sell

stance and TP of PkR316/sh (downside: 12%). HASCOL enjoys unmatched ability to

sustain sales growth momentum and management track record is excellent;

however, changing industry dynamics will eventually decelerate growth, which itself

will become more expensive to sustain, in our view.

• Four main factors that will slow down growth are (i) other OMCs will replicate

HASCOL’s storage advantage, (ii) it will potentially be competing with 21 OMCs who

have recently obtained OMC license, (iii) chronically shrinking FO market, and (iv) a

less diversified sales mix than peers.

• HASCOL’s CY17F P/E of 23.6x appears stretched even as 3yr NPAT CAGR is projected

at 26% (PEG of 0.91x). We believe that the present pace of earnings growth is

difficult to sustain beyond the medium-term, particularly given the risks attached

with high leverage to finance the rapid expansion and the working capital

constraints of an imports based model.

Organic growth to slow down, reinstate coverage with Sell stance

We expect Hascol Petroleum (HASCOL) to continue gaining market share and reach an

overall level of 13% (from 7.5% currently) in the next three years after which resurgent

competition should moderate incremental growth. HASCOL’s sales have doubled since

CY13 led by aggressive retail and storage expansion amid low oil prices and complacent

competition. Its market share rapidly swelled from 2.5% to 7.5%, but incumbent

competition is now bringing its act together. Moreover, OGRA’s recent move to

encourage competition by granting licenses to 21 new players may also hurt growth

prospects, where new entrants will likely attempt to replicate HASCOL’s growth strategy

to gain market share.

Growth is not diversified…

Out of the three major products of HASCOL, one – furnace oil (FO) - is in a secular decline

due to GoP’s policy of rationalizing power fuel mix. While HASCOL has historically focused

on HSD/Mogas sales, it has not been able to penetrate Lubricants, Jet fuel and LPG

markets – which are difficult territories but also promise a second leg of growth for OMCs.

Failure to adequately substitute FO sales with other products will be a drag on growth.

…and will be expensive in future

HASCOL’s robust sales growth (last 3yr sales CAGR: 26%) has masked the high cost of

growth. Higher leverage is necessary to finance the aggressive expansion (capital leases

and issuance of Sukuks) complemented by working capital requirements (inventory and ST

borrowing), given predominantly import based business model (75% of purchases are

imported). Hence while sales growth will remain on a steep gradient, earnings growth will

not completely mimic the former going forward due to high operation and finance costs.

Valuations are pricing in a blue sky scenario

HASCOL trades at a CY17F P/E of 23.6x, which appears stretched notwithstanding

projected 3yr NPAT CAGR of 26% (PEG 0.91x) and synergies associated with partnering

with Vitol. In our view, the market has incorporated an implied market share of 15%+

along with phenomenal success of Lubricants business – which will be very difficult with

resurgent competition, in our view.

What can change our thesis?

(i) M&A activity where HASCOL potentially acquires a competitor, (ii) success in the

lubricants market exceed expectations and (iii) rentals from expanded storage.

Organic growth is already priced in; Sell

Hascol Petroleum Limited

Hascol Petroleum Limited

Price (PkR/sh) 357.96

TP (PkR/sh) 316.00

Stance Sell

Downside 11.7%

Fwd D/Y 2.5%

Total Return -9.2%

Bloomberg / Reuters HPL PA / HASC.KA

Mkt Cap (US$mn) 412.1

52wk Hi-Low (PkR/sh) 373.32-131.64

3m Avg. Daily Vol ('000 shrs) 890

3m Avg. Traded Val (US$mn) 3.127

Key Ratios CY15A CY16F CY17F CY18F

EPS (PkR) 9.41 12.12 15.15 18.62

EPS Gth (%) 28.9% 24.9% 22.9% 30.6%

P/E (x) 38.06 29.52 23.63 19.22

BVPS (PkR) 47.81 59.90 75.01 93.58

PBV (x) 7.49 5.98 4.77 3.83

DPS (PkR) 5.00 7.30 9.00 11.20

DY (%) 1.4% 2.0% 2.5% 3.1%

ROE (%) 19.6% 20.2% 20.1% 19.8%

ROA (%) 4.3% 4.5% 4.8% 4.7%

Debt/ EQT. (%) 39.8% 55.9% 46.4% 29.4%

EV/EBITDA (x) 23.25 12.68 11.82 10.30

Gross Margin 3.7% 4.5% 3.9% 3.6%

Source: IMS Research

HASCOL vs. KSE100 Index

-30%

0%

30%

60%

90%

120%

150%

180%

Feb

-16

Ap

r-1

6

Ma

y-1

6

Jul-

16

Au

g-1

6

Sep

-16

No

v-1

6

De

c-1

6

Feb

-17

KSE100 Index HASCOL

Source: IMS Research

2 | P a g e

Perspective

…which have lower margins

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

CY1

4

CY1

5

CY1

6

CY1

7F

CY1

8F

CY1

9F

CY2

0F

CY2

1F

Mogas Margins HSD Margins FO Margins

Source: IMS Research

Finance costs will rise on expansion

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

CY14 CY15 CY16 CY17F CY18F CY19F CY20F CY21F

Finance Cost/share (PkR/Shr)

Source: IMS Research

Rapid increase in market share for all products…

0%

2%

4%

6%

8%

10%

12%

14%

CY13 CY14 CY15 CY16

FO MOGAS HSD

Source: OCAC, IMS Research

..but sales growth expected to taper off after 2-3yrs

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

CY15 CY16 CY17F CY18F CY19F CY20F CY21F

Mogas Sales Growth HSD Sales Growth

Source: IMS Research

Higher reliance on Mogas and HSD sales…

12%

40%

48%

0.5%

FO MOGAS HSD Lubricants

Source: IMS Research, OCAC

Success in lubricants market will be crucial for profitability

0

5,000

10,000

15,000

20,000

25,000

30,000

CY14 CY15 CY16 CY17F CY18F CY19F CY20F CY21F

Lubricant Volumes (M.Tons)

Source: IMS Research, OCAC

3 | P a g e

Perspective

Company Profile

Hascol Petroleum Ltd. (HASCOL) is one of the fastest growing Oil Marketing Companies

(OMC) in Pakistan, currently ranked at No.3 in terms of overall sales of POL products.

Incorporated in 2001 and converted into a public limited company in 2007, HASCOL has

achieved supernormal growth over the last 5yrs (tenfold increase in sales since CY10)

following a unique business model of relying on imports rather than local refineries and

expanding retail channels in suburbs and highways rather than city centers. HASCOL

currently has 424 fuel outlets with exclusive rights for M-2 motorway and has a

cumulative storage capacity of 136,600MT of fuel. HASCOL is currently the largest

importer of POL products in Pakistan after PSO, backed by Vitol Group which recently

acquired 25% stake in the company (intial 15% was followed by exercise of option for

another 10%).

HASCOL is spearheaded by Mr. Mumtaz Hasan Khan who has 50 years experience in the

Oil industry with start of his career in Burmah Shell Oil storage and Distribution

Company. He formed Hascombe Ltd. in 1980 as an oil trading company supplying crude

oil to major oil companies like Shell and Elf. Mr. Mumtaz also serves as the Director of

Pakistan Refinery Ltd (PRL). The current management has shown an unmatched ability

to identify opportunities and capitalize on competitor weaknesses.

Vitol Dubai Ltd., a global giant acquired a strategic 15% stake in HASCOL in February

2016 and it recently exercised the call option to acquire a further 10% stake in the

company. Vitol is one of the largest oil trading company in the world with terminals in

about 40 countries of the world trading 6mn bpd of POL products. Soon after the

acquisition, Vitol also signed a joint venture agreement with HASCOL to set up the

largest storage facility in the country at Port Qasim (200k MT).

HASCOL Journey: Supernormal growth HASCOL was granted the OMC license in 2005 and has been marketing POL products in

Pakistan ever since, with noticeable growth since its IPO in 2014. In a short span of

time, HASCOL has given intense competition to established OMCs like Pakistan State

Oil (PSO), Attock Petroleu m (APL) and Shell Pakistan (SHEL) by rapidly opening new fuel

stations - commissoning as many as 424 stations as of 2016. The company also has a

sizeable 136,600 MT of storage under operation enabling it to compete head on with

larger OMCs of Pakistan.

M

Hascol Revenue Breakup

12%

40%

48%

0.5%

FO MOGAS HSD Lubricants

Source: IMS Research, Company Accounts

Shareholding Pattern

General

Public

27%

Directors

27%

Marshal Gas

Pvt Ltd.

6%

Fossil Energy

Pvt Ltd.

7%

Vitol Dubai

Ltd.

25%

Others

8%

Source: IMS Research, Company Accounts

Market Share: HASCOL has disrupted the industry in the last 3 years

PSO,

63.1%

SHEL,

10.1%

APL,

8.9%

HASCOL,

2.5%

CY13

PSO,

56.5%

SHEL,

9.6%

APL,

7.2% HASCOL,

7.5%

CY16

Source: IMS Research, OCAC

4 | P a g e

Perspective

At the time of its IPO in 2014 (raised PkR1,406mn for storage and retail network),

HASCOL’s strategy was significantly different from what it is now. In a high oil price

scenario, the company was largely dependent on local refineries for supply of POL

products due to limited muscle to import fuel on its own. The company had only

imported 3 cargoes of fuel by then. It was also establishing a small 9,500 MT fuel

storage at Machike. Post IPO however, changes in both global and local dynamics (low

oil prices and lingering circular debt handicap for peers) led to an entirely different,

more aggressive strategy resulting in the shift to a more import based model and drive

towards large storage capacities.

Pre-IPO (2014) Now IPO Plan PkRmn

Retail Outlets 210 424 Machike Terminal 200

Storage Facilities (MT) 69,900 136,600 Retail Stations 100

Market Share 2.5% 7.5% Working Capital 200

Total Requirement 500

Source: IMS Research, Company Website, OCAC, OGRA

HASCOL has been able to achieve an overall market share of 7.5% in a short span of

time by following a unique supply chain strategy, penetrating deep in the market. On

the retail front, HASCOL targeted suburban areas and highways to generate higher

volumes per fuel station; it was also able to win the exclusive contract for M-2

motorway, which was earlier held by PSO. In order to maintain sustainable stream of

revenues, HASCOL targeted institutional customers and pushed sales with efficient

delivery and availability of products with storage terminals at strategic locations across

the country. Growth was conducive due to weaker competition at the time when larger

OMCs like PSO were in the midst of Circular Debt (a cash crisis in the power sector

which absorbs a large portion of overall OMC sales, majorly Furnace Oil) and

multinationals were looking to exit the market. HASCOL also followed an import based

model with lesser dependence on local refineries which was aided by a low oil price

scenario, to break the monopoly of larger OMCs.

HASCOL’s current revenue stream consists mainly of three major POL products: Mogas,

HSD and FO. It also plans to enter the LPG and Jet fuel market, where regulatory issues

and long-term contracts are barring penetration.The company also has a distribution

license of Germany based Fuchs lubricants, which it also plans to blend locally with a

new Lube blending facility.

HASCOL initially relied heavily on FO for its revenue due to (i) a low number of retail

outlets and (ii) PSO’s circular debt issue, which crippled its cash flows. HASCOL’s

revenue contribution from FO was c.39% in 2013, gradually shrinking to c.12% presently

with expansion in the retail network and PSO regaining strength through imports.

HASCOL plans to fuel ongoing growth trajectory by continuing to add 100 retail stations

every year, and gradually penetrating the urban centers. In order to maintain an

efficient supply chain given the import based model, it plans to build the largest storage

capacity of 456,900MT (total storage) at all strategic locations of Pakistan.

HASCOL raised PkR1.4bn in the IPO against the

initial target of PkR500mn due to

overwhelming interest from investors.

Three major products HSD, Mogas and FO

contribute 99.5% of revenue.

HASCOL has gained an overall market share of

7.5% from 2.5% in just 3 years

5 | P a g e

Perspective

Current Storage

Location / Terminal Petrol Diesel Fuel Oil Status Remarks

Al Abbas KMR 16,500 - - Leased

ZYCO Hsacol Terminal KMR 21,100 5,000 - Company Owned 3 Tanks Under Construction under OGRA Inspection

VTT Port qasim - - 56,000 Leased

Daulatpur 2,250 4,000 -

Shikarpure 2,750 6,000 - Company Owned

Machike 3,500 6,000 - Company Owned

Mehmoodkot 4,500 9,000 - Company Owned December 2016, Under OGRA Inspection

Sub Total (MT) 50,600 30,000 56,000

Under Construction Storages Location / Terminal Petrol Diesel Fuel Oil Status Expected Completion & Remarks

Port Qasim 50,000 69,600 87,000 Company Owned September 17 & September 18

Shikarpur Additional - 6,000 - Company Owned 18-March

Daulatpur Additional - 3,000 - Company Owned 18-March

Sahiwal 2,000 4,000 - Company Owned June 17

Kotla-Jam 4,000 4,000 - Company Owned December 17

Machike 'B' 50,000 10,000 - Company Owned December 17 Subject to NOC By LDA

Amangarh 500 2,200 - Company Owned December 16 Under OGRA Inspection

Thallian 16,000 12,000 - Company Owned December 17

Sub Total (MT) 122,500 110,800 87,000

Grand Total 173,100 140,800 143,000

Grand Total All Storages (MT)

456,900

Source: IMS Research

6 | P a g e

Perspective

Organic growth to slow down; reinstate coverage with Sell stance

We expect Hascol Petroleum (HASCOL) to continue gaining market share and reach an

overall level of 13% (from 7.5% currently) in the next three years after which

resurgent competition should moderate incremental growth. HASCOL’s sales have

doubled since CY13 led by aggressive retail and storage expansion amid low oil prices

and complacent competition. Its market share rapidly swelled from 2.5% to 7.5%, but

incumbent competition is now bringing its act together. Moreover, OGRA’s recent

move to encourage competition by granting licenses to 21 new players may also hurt

growth prospects, where new entrants will likely attempt to replicate HASCOL’s

growth strategy to gain market share.

Momentum to continue in the short term

HASCOL’s current sales growth momentum is likely to continue in the next couple of

years given the lagged competitive response from other OMCs, in our view. We believe

PSO, SHEL and APL will take some time to catch up with the storage advantage of

HASCOL and begin to recover their lost market share. The rapid growth of HASCOL was

partly supported by lackluster performance of bigger players where PSO was suffering

from severe cash flow issues due to circular debt, SHEL was widely understood to be

considering an exit from Pakistan and APL did not have enough storage to push growth

despite support from two group refineries (NRL and ATRL). We believe PSO and APL’s

new storage infrastructure will take time to come online; meanwhile, HASCOL can

continue to take advantage and grow. However, this window will eventually narrow

while excessive reliance on non-urban and non-retail channel sales (60% of total sales)

also calls into question the sustainability of growth as new competition seeps in and

uses similar strategy (targeting suburban areas).

Likely response from competitors in the medium term Competitor OMCs ha ve shown serious intent to counter the threat posed by HASCOL,

although we reiterate it will likely take some time for them to stop the bleeding. In a bid

to retain market share, the three major OMCs are likely to fill the gaps that they have

left for HASCOL to exploit in the last few years.

PSO: PSO is planning an investment of up to PkR8bn to double its Mogas storage

capacity to store inventory of up to 20 days (from 9-10 days presently) to ensure

availability of fuel at its 3,800 fuel stations spread across the country, which will shore

up its leadership position.

HASCOL sales growth is expected to moderate after next 2-3yrs

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

CY15 CY16 CY17F CY18F CY19F CY20F CY21F

(MT)

Mogas Volumes HSD Volumes Mogas Sales Growth (Rhs)

Source: IMS Research

Sales growth is expected to moderate after

medium-term

7 | P a g e

Perspective

SHEL: SHEL has already announced revamp of its fuel stations (neglected while it was

perhaps planning to exit Pakistan) to attract more customers. It has a very strong brand

name to leverage and a strong supply chain to bolster revival of its operations in little

time. To recall, SHEL historically had a market share of 13% where supportive GoP

policies (OMC margins linkage with CPI) and promising demand outlook may be

compelling them to stay in the market.

APL: APL has announced ramping up storage capacity by building terminals at strategic

locations of Port Qasim, Mehmood Kot, Gatti and Shikarpur. Note these are the same

locations where HASCOL’s storage facilities are located. It also continues to benefit

from presence of group refineries NRL and ATRL to back its supply chain.

Overall Market Share No. of Pumps Storage Capacity (MT)

PSO 57% 3,421 958,238

SHEL 10% 801 130,547

APL 7% 582 64,375

HASCOL 7% 424 136,600

Source: IMS Research, OCAC, OGRA

The completion of these plans will lead to a more level playing field and HASCOL will

have to resort to new competitive tactics to sustain market share growth.

Fragmented market expected in the long term

OGRA has recently granted OMC licenses to 21 new companies vs. only 12 currently

operating, in a bid to encourage competition, enhance customer service and shift to a

completely deregulated environment in the long run. The present business

environment with promising volumetric growth outlook, low oil prices and OMC

margins linked with inflation provide a lucrative opportunity for new players to enter

the industry. Key success factor will be big financial muscle because OGRA requires new

OMCs to enhance storage capacity for Pakistan, in order to avert shortage amid rapidly

growing demand.

We believe that the new players will imitate HASCOL’s growth strategy in order to

attain market share. A cost effective strategy used by HASCOL is to set up retail pumps

in outskirts of cities, small towns and highways, procure supplies from local refineries

and once cash flow is generated, move to the urban centers and start importing on its

own. They would also need significant capital for storage and supply chain

infrastructure, which is also easier to raise through both equity and debt market in the

present environment. Newer industry dynamics are suggestive of a fragmented market

resulting in shift to a more defensive approach for incumbents to defend their market

share rather than concentrating on gaining market share once competition becomes

fiercer.

HASCOL has audaciously challenged market share of competitors

0%

10%

20%

30%

40%

50%

60%

70%

80%

Overall FO Mogas HSD

PSO SHEL APL HASCOL

Source: IMS Research, OCAC

OGRA issued license to 21 new OMCs which is

unprecedented. GoP is likely planning a more

competitive deregulated market.

APL is building storage capacities in the same

localities as HASCOL.

8 | P a g e

Perspective

Thin margins on lack of diversified sales mix

FO is one of the highest selling POL products (with relatively higher margins)

constituting a major chunk of OMC sector sales. In this regard, GoP’s recent policy to

shift power generation mix away from FO is likely to dampen Industry sales where

HASCOL will also be impacted. While HASCOL has historically focused on HSD/Mogas

sales, it has not been able to penetrate Lubricants, Jet fuel and LPG market – which

are difficult territories but also promise a second leg of growth for OMCs. Failure to

adequately substitute FO sales with other products can also be a drag on growth.

Pakistan’s changing fuel mix

Pakistan is expected to add about 10,000MW of power generation capacity till 2018,

most of which is Coal based under the CPEC arrangement. Moreover, in a rising

international oil price scenario, FO based power generation would be 2x more

expensive than Natural Gas (above US$70/bbl) hence more substitution is likely to take

place. This would also be true for industrial consumers; with increased electricity

generation, reliance of industry on alternate power generators will also decrease.

Declining FO market will increase reliance on HSD and Mogas

HASCOL’s revenue concentration in three major products may also pose a risk to

revenue growth. Whereas HASCOL is partly immune to Pakistan’s changing power fuel

mix (shifting away from furnace oil to more coal/LNG/hydel based generation) due to

lower sales to power sector, increased availability of LNG and alternate fuels may also

reduce the reliance of industries on FO. Contribution from lubricants to revenue is

expected to increase with the installation of a lube blending plant; however, with major

players like SHEL, Caltex and PSO still present in the market, success of this product is

still questionable. Moreover, HASCOL has still not been able to penetrate the Jet fuel

and LPG market to broaden the product base to reduce dependence on Mogas and

HSD.

Dependence on Mogas and HSD is positive on a cash-flow basis due to possibility of

high turnover. However, on a profitability basis, both Mogas and HSD are thin margin

products while FO has relatively higher margins. Decline in FO sales going forward will

hurt the profitability of the company given high finance costs to import fuel and finance

capital expenditure. However, success of lubricants can be an offsetting factor.

FO Contribution to the revenue is decreasing

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

CY13 CY14 CY15 CY16

Source: IMS Research

FO Industry sales volume (MT)

5,500,000

7,000,000

8,500,000

10,000,000

CY

14

CY

15

CY

16

CY

17

F

CY

18

F

CY

19

F

CY

20

F

CY

21

F

CY

22

F

CY

23

F

CY

24

F

CY

25

F

FO Industry Sales

Source: IMS Research

GoP has decided to change the power fuel mix

due to expensive cost of electricity amid higher

oil prices.

9 | P a g e

Perspective

Sustaining growth will entail high costs

HASCOL’s robust sales growth (last 3yr sales CAGR: 26%) has masked the high cost of

growth. Higher leverage is necessary to finance the aggressive expansion (capital

leases and issuance of Sukuks) complemented by working capital requirements

(inventory and ST borrowing), given predominantly import based business model

(75% of purchases are imported). Hence, while sales growth will remain on a steep

gradient, earnings growth will not completely mimic the former going forward due to

high operational and finance costs.

Increasing leverage to finance expansion

HASCOL has followed an aggressive growth strategy in adding retail fuel outlets and

storages, where it plans to add a further 320,300MT of storage, continue expansion in

retail fuel outlets and install a new lube blending plant at a cost of PkR1.8bn. While all

this growth looks promising, HASCOL’s reliance on debt and capital leases has made it

more expensive (CY15 finance cost: PkR2.9/sh). With the current growth trajectory, we

forecast that this burden of finance costs is likely to increase further and will push

down on earnings where a hike in interest rates may slow down the expansion strategy.

Given the thin margins HASCOL earns on its sales, higher cost of financing is likely to

keep earnings growth in check. As it is, earnings growth outlook is not as promising as

sales outlook.

Import based model requires more working capital HASCOL’s massive dependence on imports will result in significant requirements for

working capital amidst large import costs, in our view. It currently imports 75% of its

total inventory, as per management guidance and hence has very low reliance on local

refineries for POL products. Whereas this strategy allows them to capitalize on the fluctuations in international oil prices, high import costs are an additional burden on

the profitability of the company, especially at a time when international oil prices will

be rising. Up till now, HASCOL could mitigate these costs through import differentials;

now however, the rapid increase in finance and imports cost will result in slower

earnings growth than revenue growth.

In a low oil price scenario, relying on imports might be feasible but as soon as oil prices

start to rise, HASCOL would need large working capital to import similar quantity of

inventory and thus costs would rise in tandem. In future, HASCOL would have built large

storages and reverting back to local refineries for supplies would mean wasting storage

and incurring maintenance costs too. Inventory gains due to price differentials will be

an offsetting factor in this regard; however, these would be possible if international

prices are rising.

Rising finance costs related to imports will trim margins

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

CY14 CY15 CY16 CY17F CY18F CY19F CY20F CY21F

Finance Cost/share (PkR/Shr)

Source: IMS Research

HASCOL recently issued PkR2bn Sukuks to

finance expansion.

10 | P a g e

Perspective

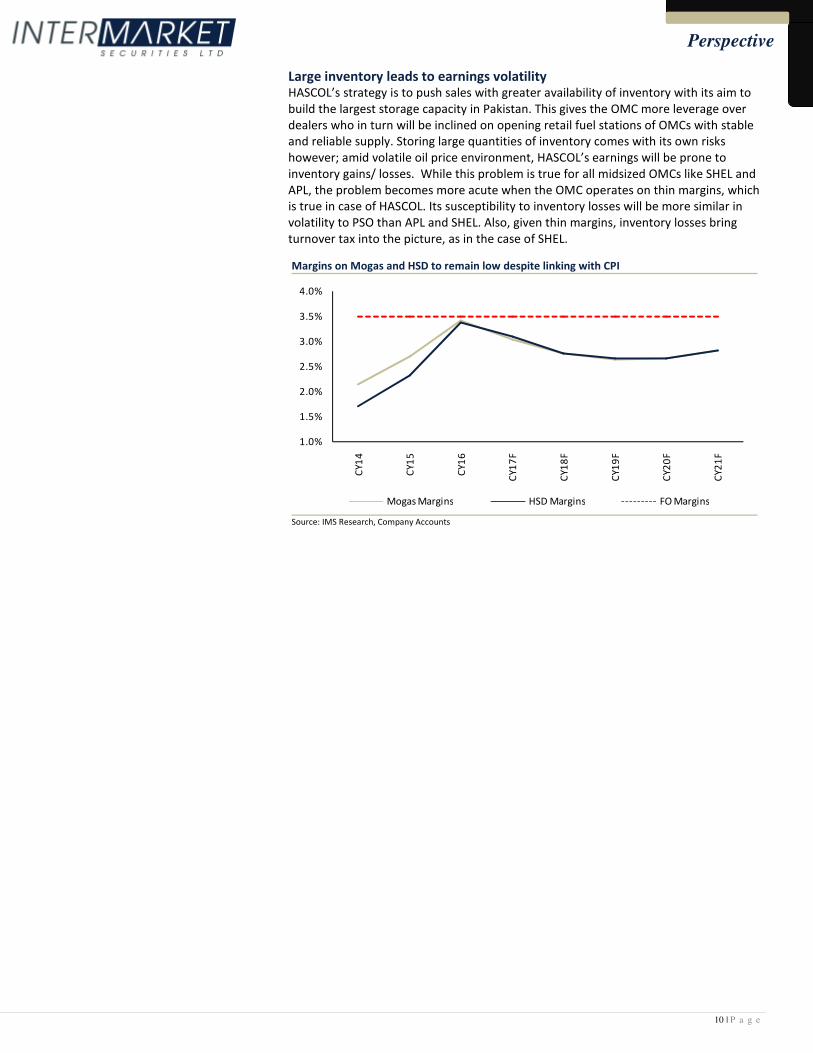

Large inventory leads to earnings volatility HASCOL’s strategy is to push sales with greater availability of inventory with its aim to

build the largest storage capacity in Pakistan. This gives the OMC more leverage over

dealers who in turn will be inclined on opening retail fuel stations of OMCs with stable

and reliable supply. Storing large quantities of inventory comes with its own risks

however; amid volatile oil price environment, HASCOL’s earnings will be prone to

inventory gains/ losses. While this problem is true for all midsized OMCs like SHEL and

APL, the problem becomes more acute when the OMC operates on thin margins, which

is true in case of HASCOL. Its susceptibility to inventory losses will be more similar in

volatility to PSO than APL and SHEL. Also, given thin margins, inventory losses bring

turnover tax into the picture, as in the case of SHEL.

Margins on Mogas and HSD to remain low despite linking with CPI

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

CY1

4

CY1

5

CY1

6

CY1

7F

CY1

8F

CY1

9F

CY2

0F

CY2

1F

Mogas Margins HSD Margins FO Margins

Source: IMS Research, Company Accounts

11 | P a g e

Perspective

Competitor Analysis

HASCOL has followed a unique business model to penetrate in the OMC market, and

has followed a thin margin/volume driven approach. Narrow margins in a high fixed

costs business model are not sustainable, in our view, as realized by other mature

OMCs who have moved in high margin businesses and created synergies.

Revenue Mix: HASCOL is largely dependent on 3 major products for its revenues out of

which FO is a declining market and other revenue streams like Jet Fuel, LPG and

Lubricants are either absent or not contributing materially to revenue. While HASCOL

may try to grow these lines, it faces inhibiting factors such as (i) PSO’s fuel supply

agreements for FO and Jet fuel, (ii) APL’s presence in non-energy products market like

Bitumen and (iii) SHEL’s brand equity in Lubricants and Jet fuel market. Moreover, GoP

has recently deregulated HOBC which is a high margin product; sales of this product

would be concentrated in urban centers where HASCOL has less presence.

Profitability: Gross profitability of all the companies looks higher than HASCOL due to a

diversified product mix, where all the other players have deregulated products in their

product portfolio unlike HASCOL. We argue that, like PSO, since the sales are leveraged,

HASCOL’s thin margins expose it to risks.

Fuel Supply Arrangements: PSO is the largest importer of POL products and has been

able to sustain the model based on the scale and GoP backing that it has. SHEL has

resorted to local refineries for fuel supply while APL has leveraged group refineries for

efficient availability of inventory. Comparison of the OMC space suggests import based

model is only sustainable with scale economies as high as PSO to bear high finance and

storage operations costs. Therefore, HASCOL can become a more profitable OMC with

more local procurement. Increasing stake in Pakistan Refinery (PRL) will have helped

circumvent this issue, but PSO has taken over the opportunity. Future refineries (in

Karak, KPK) or fully operational Byco Oil refinery will provide other ways out of this

problem.

Leverage: All the OMCs except PSO are deleveraged, which is still in the midst of a

circular debt crisis and is only able to sustain with GoP backing. It is worth noting that

both APL and SHEL can potentially undergo aggressive expansion to counter HASCOL

going forward where HASCOL is set to remain leveraged as it undergoes further

expansion given the policy of capital leases to acquire assets.

Payout: We believe that distribution of earnings for HASCOL will remain low in the

medium term as compared to competitors where APL already has a healthy payout

policy and PSO will start paying out as soon as circular debt issue eases out.

PSO APL SHEL HASCOL

Revenue Mix (major products) HSD, Mogas and FO HSD, Mogas, FO and Bitumen HSD, Mogas, Lubricants and Jet fuel HSD, MS and FO

Gross margins* 4.32% 4.37%. 5.58% 3.69%

Net margins* 2.43% 2.42% 2.54% 1.48%

ROE* 19.4% 25.5% 22.4% 20.3%

Fuel Supply Arrangements Majorly Imported Group Refineries Import + local refineries Majorly Imported

Retail Network (before Rev) 3,800 563 780 424

Debt to Equity 1.15 0 0.34 0.56

Exposure to circular debt High Low None None

Payout Low High Low Low

P/E 7.8x 11x 14.5x 23.6x

*Adjusted for inventory gains/losses

HASCOL may try to diversify its revenue mix but

it will face challenges.

12 | P a g e

Perspective

Valuations are pricing in a blue sky scenario

HASCOL trades at a CY17F P/E of 23.6x, which appears stretched notwithstanding

projected 3yr NPAT CAGR of 26% and synergies associated with partnering with Vitol.

In our view, the market has incorporated an implied market share of 15%+ along with

phenomenal success of Lubricants business. While these expectations are possible,

these would require weaker competition as has been the case in the last 3 years. A

lower payout (20%) despite cash sales also dampens the investment case.

Valuations stretched even in bull case scenario

HASCOL trades at a CY17F P/E of 23.6x, at a 195% premium to the OMC space and

116% premium to the KSE-100 Index. We believe valuations are stretched where the

market is ostensibly equating earnings growth with volumetric growth, ignoring higher

finance and inventory costs going forward. HASCOL’s valuations appear stretched even

by assuming a bull-case scenario of 15% market share in the next 3yrs.

We have valued HASCOL by assuming an overall market share of 13% in the next 3

years (vs. 7.5% at present) and adequate success in the lubricants business (market

share of 10% by CY20). We believe that low payout despite cash sales further calls into

question the premium assigned to the scrip.

We indicate that similar growth trajectory was also seen for APL in 2005-07 period

when the average 3-year earnings CAGR was 70%. During this time, APL followed a

similar strategy of building fuel stations in the outskirts concentrating in high demand

areas of Punjab. Interestingly APL traded at a P/E in the range of 14-16x at that time as

compared to HASCOL which is forecasted to grow at a 3-year CAGR of 26%; much below

APL’s peak growth rate. The historical comparison is suggestive of a massive premium

being assigned to HASCOL.

Comparison with embryonic APL is telling

We compare APL’s early growth period of 2005-2007 with HASCOL’s current growth in

order to gauge the valuations where its earnings grew by 4x from 2005-2007 while it

touched peak P/E valuations of 16x, at a 26% premium to the market as compared to

HASCOL trading at a P/E of 23.6x, at a 116% premium to the market.

Market PER (x) vs. APL PER (x)

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

No

v-0

5

Ap

r-0

6

Sep

-06

Feb

-07

Jul-

07

De

c-0

7

May

-08

Oct

-08

Mar

-09

Au

g-0

9

Jan

-10

Jun

-10

No

v-1

0

Ap

r-1

1

Sep

-11

Feb

-12

Jul-

12

De

c-1

2

May

-13

Oct

-13

Mar

-14

Au

g-1

4

Jan

-15

Jun

-15

No

v-1

5

Ap

r-1

6

Sep

-16

Feb

-17

APL (PER-x) Market PE (x)

Source: Bloomberg, IMS Research

HASCOL’s valuations are at a significant

premium to when a young APL was undergoing

its own rapid growth phase

Valuation Table PkRmn CY17F CY18F CY19F … CY25F Beta 1.18

FCFF (1,388) (368) 411

6,796

Cost of Equity 15.10%

Discounted FCFF (1,388) (325) 316

2,402

Cost of Debt 8%

WACC Floating

Sum of PV 11,789

Target D/E 20%

Terminal Value 21,215

EV 33,004

Cash + Investments 9,329

Debt 4,051

Value of Equity 38,282

Target Price (PkR) 316.0

Source: IMS Research

13 | P a g e

Perspective

While there are similarities, between the young APL and today’s HASCOL, there are

marked operational advantages for the former that HASCOL does not have. APL grew at

a much faster growth rate than HASCOL during that time with rapid retail outlets

expansion (similar to HASCOL with 50-70 outlets every year). It also had the advantage

of two group refineries (NRL and ATRL) providing strong inventory support. With the

storage infrastructure of group refineries in place, APL used to store only 4-6 days of

inventory in its storage, thereby saving working capital and operational costs. Lesser

inventory storage also reduced APL’s correlation to oil market volatility. Comparing this

with an import based model of HASCOL, high working capital and import costs would

depress earnings and dampen the pace of growth trajectory followed by APL.

Moreover, APL had a more profitable revenue portfolio with significant contribution

from deregulated products while HASCOL is largely dependent on sales of Mogas and

HSD which have regulated margins. Additional support for APL came from export of POL

products to land-locked Afghanistan and significant commission for export of NAPTHA

on behalf of NRL and ATRL. This diverse product mix gave a unique advantage to APL

which HASCOL currently does not have. In our view, HASCOL trading at 116% premium

to the market (vs. 27% peak premium for APL), despite having relatively slower earnings

growth, reliance on imports and lower margins product mix, is unjustified.

14 | P a g e

Perspective

Upside Risks: What can change our thesis?

While we argue that HASCOL’s sales growth will slow down beyond the medium term

due to multiple reasons and that earnings growth will remain lower as compared to the

sales growth, there are some upside risks associated with our thesis which have been

taken into consideration.

Above expected success in the Lubricants market

We argue that HASCOL’s current business model will translate in slower earnings

growth as compared to sales growth due to high import, working capital and financing

costs. In order to accelerate earnings growth and improve margins, HASCOL needs to

achieve phenomenal success in the lubricants market. In this regard, HASCOL has a

technical service agreement with Fuchs Labs Germany for marketing “Fuchs” branded

lubricants in Pakistan and has announced a Lube blending plant at a cost of US$20mn.

This will enable HASCOL to aggressively market the products where it only sold c.

7,000MT in CY16 as per our estimates. Success in our view can take two forms: either

HASCOL replicates high double-digit growth as in petroleum products or becomes able

to charge high margins like the incumbents in this market.

Pakistan’s lubricants market is estimated to have a demand of 200,000MT/year which is

expected to grow at 5% CAGR. This demand is driven both by automobile and industries

where Motor Oil, Heavy duty engine oil and Industrial oil are consumed the most. The

industry is divided into organized and unorganized sector, where most of the sales

come through the retail fuel stations (organized sector).

Market for lubricants is concentrated with the largest three players dominating c. 60%

of the market. Brand equity and retail network play a major role in success in this

industry. The industry is dominated by SHEL, Caltex and PSO (constituting c.60% of the

market) backed by high brand equity and widespread retail network all over the

country. Lubricants are the highest margin products for OMCs where margins range

between 20-40% depending on the OMC. Our estimates suggest c.45% of Shell’s profits

for CY15 were contributed by Lubricant sales which contributed only 7% to revenues.

We have assumed a decent success of lubricants business in our model driven by

aggressive expansion in retail network, which will boost availability of the products.

However, taking SHEL and PSO as proxy, SHEL (800 outlets) has dominated the

lubricants market despite PSO’s larger retail network (3,800 retail outlets). This is

suggestive that brand equity plays a higher role in success in this market. Our channel

checks suggest higher brand equity for SHEL and Caltex branded lubricants where

consumers are willing to pay premium for their product. Given this context, success of a

relatively new brand would be limited in our view and sales would be pushed through

the HASCOL retail channel.

Lubricant Volumes

0

5,000

10,000

15,000

20,000

25,000

30,000

CY14 CY15 CY16 CY17F CY18F CY19F CY20F CY21F

Lubricant Volumes (M.Tons)

Source: IMS Research

Lubricants have the highest margin among POL

products, in the range of 25-40%.

Brand Equity is the most important factor in

Lubricants business while Lube blending plant

can improve supply chain.

15 | P a g e

Perspective

Storage Rental can generate substantial income

Historically, PSO and SHEL were the major importers of POL products in the country and

have had substantial storage capacities to store inventory. Other smaller OMCs relied

on local refineries for inventory and hence were able to avoid expenditure on storage.

More recently, HASCOL took the lead with its import based model and is investing

heavily in storage facilities. The new strategy is driven by the philosophy of pushing

sales with efficient and widespread of availability of products across the country which

is only possible with storage facilities at strategic locations.

HASCOL currently has 136,600MT of owned and leased storage for different products

across the country while it plans to add 320,300MT in the next 2 years. Availability of

such huge storage space will not only help HASCOL ensure availability of its inventory

throughout the country but may also open up additional revenue streams in the form of

storage rental, which is currently only contributing PkR50mn to the profits but may be

substantial in the future. Affordability of own storages is only possible for operations at

a certain scale and all the 21 new OMCs might not be able to achieve that scale

immediately, hence HASCOL might be able to lease out its storage facility potentially

generating substantial income in return.

Potential acquisition of a competitor

A potential upside trigger for HASCOL would be acquisition of a competitor like SHEL

which has been said to be mulling exit from the market since quite some time (it is

perhaps now considering to stay in the space given improved industry dynamics). This

move can give HASCOL an instant access to retail outlets at premium locations which

alternatively would take several years to replicate. However, this instant access would

come at a premium and financing such an acquisition might be a pertinent issue given

the already high leverage to finance expansions. We indicate that HASCOL has Vitol as a

strong sponsor which may play a role in financing such acquisition. This move would be

unchallenged since other competitors like APL or new entrants might also pursue such

lucrative quick entry in the premium market which would push the price further north.

Support from Vitol in sustaining the import based model

Vitol Dubai Ltd. which recently acquired a 25% stake in HASCOL is a huge oil giant

involved in trading of POL products all over the globe. We recognize that support from

Vitol in order to sustain an import based model in the medium term can be an upside

trigger. This support can come in the form of financing new expansions such as its role

in Port Qasim installation. It may also play a stronger role as an import arm for HASCOL,

where Vitol may import POL products on HASCOL’s behalf and they may not have to

invest in working capital. Lastly, HASCOL can benefit from Vitol’s expertise in global oil

trade in order to capitalize on the volatility in the international oil market.

16 | P a g e

Perspective

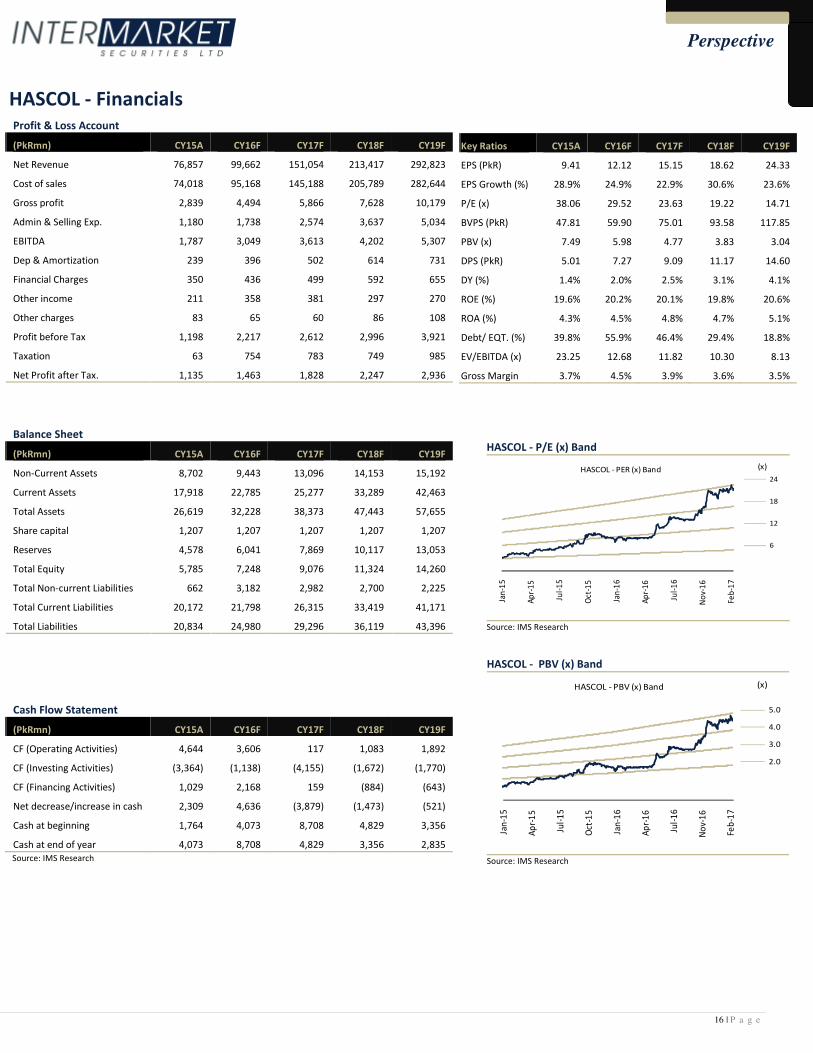

Profit & Loss Account

(PkRmn) CY15A CY16F CY17F CY18F CY19F

Net Revenue 76,857 99,662 151,054 213,417 292,823

Cost of sales 74,018 95,168 145,188 205,789 282,644

Gross profit 2,839 4,494 5,866 7,628 10,179

Admin & Selling Exp. 1,180 1,738 2,574 3,637 5,034

EBITDA 1,787 3,049 3,613 4,202 5,307

Dep & Amortization 239 396 502 614 731

Financial Charges 350 436 499 592 655

Other income 211 358 381 297 270

Other charges 83 65 60 86 108

Profit before Tax 1,198 2,217 2,612 2,996 3,921

Taxation 63 754 783 749 985

Net Profit after Tax. 1,135 1,463 1,828 2,247 2,936

Balance Sheet

(PkRmn) CY15A CY16F CY17F CY18F CY19F

Non-Current Assets 8,702 9,443 13,096 14,153 15,192

Current Assets 17,918 22,785 25,277 33,289 42,463

Total Assets 26,619 32,228 38,373 47,443 57,655

Share capital 1,207 1,207 1,207 1,207 1,207

Reserves 4,578 6,041 7,869 10,117 13,053

Total Equity 5,785 7,248 9,076 11,324 14,260

Total Non-current Liabilities 662 3,182 2,982 2,700 2,225

Total Current Liabilities 20,172 21,798 26,315 33,419 41,171

Total Liabilities 20,834 24,980 29,296 36,119 43,396

Cash Flow Statement

(PkRmn) CY15A CY16F CY17F CY18F CY19F

CF (Operating Activities) 4,644 3,606 117 1,083 1,892

CF (Investing Activities) (3,364) (1,138) (4,155) (1,672) (1,770)

CF (Financing Activities) 1,029 2,168 159 (884) (643)

Net decrease/increase in cash 2,309 4,636 (3,879) (1,473) (521)

Cash at beginning 1,764 4,073 8,708 4,829 3,356

Cash at end of year 4,073 8,708 4,829 3,356 2,835

Source: IMS Research

Key Ratios CY15A CY16F CY17F CY18F CY19F

EPS (PkR) 9.41 12.12 15.15 18.62 24.33

EPS Growth (%) 28.9% 24.9% 22.9% 30.6% 23.6%

P/E (x) 38.06 29.52 23.63 19.22 14.71

BVPS (PkR) 47.81 59.90 75.01 93.58 117.85

PBV (x) 7.49 5.98 4.77 3.83 3.04

DPS (PkR) 5.01 7.27 9.09 11.17 14.60

DY (%) 1.4% 2.0% 2.5% 3.1% 4.1%

ROE (%) 19.6% 20.2% 20.1% 19.8% 20.6%

ROA (%) 4.3% 4.5% 4.8% 4.7% 5.1%

Debt/ EQT. (%) 39.8% 55.9% 46.4% 29.4% 18.8%

EV/EBITDA (x) 23.25 12.68 11.82 10.30 8.13

Gross Margin 3.7% 4.5% 3.9% 3.6% 3.5%

HASCOL - Financials

HASCOL - P/E (x) Band

Jan

-15

Ap

r-1

5

Jul-

15

Oct

-15

Jan

-16

Ap

r-1

6

Jul-

16

No

v-1

6

Feb

-17

(x)HASCOL - PER (x) Band 24

18

12

6

Source: IMS Research

HASCOL - PBV (x) Band

Jan

-15

Ap

r-1

5

Jul-

15

Oct

-15

Jan

-16

Ap

r-1

6

Jul-

16

No

v-1

6

Feb

-17

(x)HASCOL - PBV (x) Band

5.0

4.0

3.0

2.0

Source: IMS Research

17 | P a g e

Perspective

I, Muneeb Naseem, certify that the views expressed in the report reflect my personal views about the subject securities. I also

certify that no part of my compensation was, is, or will be, directly or indirectly, related to the specific recommendations made in

this report. I further certify that I do not have any beneficial holding of the specific securities that I have recommendations on in

this report.

Ratings Guide* Total Return

Buy More than 15%

Neutral Between 0% - 15%

Sell Below 0%

*Based on 12 month horizon unless stated otherwise in the report. Total Return is sum of any Upside/Downside

(percentage difference between the Target Price and Market Price) and Dividend Yield.

Valuation Methodology: We use multiple valuation methodologies in arriving at a Target Price including, but not limited to,

Discounted Cash Flow (DCF), Dividend Discount Model (DDM) and relative multiples based valuations.

Risks: Please refer to page 14.

Disclaimer: Intermarket Securities Limited has produced this report for private circulation only. The information, opinions and

estimates herein are not direct at, or intended for distribution to or use by, any person or entity in any jurisdiction where doing so

would be contrary to law or regulation or which would subject Intermarket Securities Limited to any additional registration or

licensing requirement within such jurisdiction. The information and statistical data herein have been obtained from sources we

believe to be reliable where such information has not been independently verified and we make no representation or warranty as to

its accuracy, completeness and correctness. This report makes use of forward looking statements that are based on assumptions

made and information currently available to us and those are subject to certain risks and uncertainties that could cause the actual

results to differ materially. No part of the compensation of the author(s) of this report is related to the specific recommendations or

views contained in this report.

This report is not a solicitation or any offer to buy or sell any of the securities mentioned herein. It is meant for information purposes

only and does not take into account the particular investment objectives, financial situation or needs of individual recipients. Before

acting on any information in this report, you should consider whether it is suitable for your particular circumstances and, if

appropriate, seek professional advice. Neither Intermarket Securities Limited nor any of its affiliates or any other person associated

with the company directly or indirectly accepts any liability whatsoever for any direct or consequential loss arising from any use of this

report or the information contained herein.

Subject to any applicable law and regulations, Intermarket Securities Limited, its affiliates or group companies or individuals

connected with Intermarket Securities Limited directly or indirectly may have used the information contained herein before

publication and may have positions in, or may from time to time purchase or sell or have a material interest in any of the securities

mentioned or may currently or in future have or have had a relationship with, or may provide investment banking, capital markets

and/or other services to, the entities mentioned herein, their advisors and/or any other connected parties.

18 | P a g e

Perspective

NOTICE TO US INVESTORS

This report was prepared, approved, published and distributed by Intermarket Securities Limited (IMS) located outside of

the United States (a “non-US Group Company”). This report is distributed in the U.S. by LXM LLP USA, a U.S. registered

broker dealer, on behalf of IMS only to major U.S. institutional investors (as defined in Rule 15a-6 under the U.S.

Securities Exchange Act of 1934 (the “Exchange Act”)) pursuant to the exemption in Rule 15a-6 and any transaction

effected by a U.S. customer in the securities described in this report must be effected through LXM LLP USA.

Neither the report nor any analyst who prepared or approved the report is subject to U.S. legal requirements or the

Financial Industry Regulatory Authority, Inc. (“FINRA”) or other regulatory requirements pertaining to research reports or

research analysts. No non-US Group Company is registered as a broker-dealer under the Exchange Act or is a member of

the Financial Industry Regulatory Authority, Inc. or any other U.S. self-regulatory organization.

Analyst Certification. Each of the analysts identified in this report certifies, with respect to the companies or securities

that the individual analyses, that (1) the views expressed in this report reflect his or her personal views about all of the

subject companies and securities and (2) no part of his or her compensation was, is or will be directly or indirectly

dependent on the specific recommendations or views expressed in this report. Please bear in mind that (i) IMS is the

employer of the research analyst(s) responsible for the content of this report and (ii) research analysts preparing this

report are resident outside the United States and are not associated persons of any US regulated broker-dealer and that

therefore the analyst(s) is/are not subject to supervision by a US broker-dealer, and are not required to satisfy the

regulatory licensing requirements of FINRA or required to otherwise comply with US rules or regulations regarding,

among other things, communications with a subject company, public appearances and trading securities held by a

research analyst account.

Important US Regulatory Disclosures on Subject Companies. This material was produced by Analysis of IMS solely for

information purposes and for the use of the recipient. It is not to be reproduced under any circumstances and is not to

be copied or made available to any person other than the recipient. It is distributed in the United States of America by

LXM LLP USA and elsewhere in the world by IMS or an authorized affiliate of IMS. This document does not constitute an

offer of, or an invitation by or on behalf of IMS or its affiliates or any other company to any person, to buy or sell any

security. The information contained herein has been obtained from published information and other sources, which IMS

or its Affiliates consider to be reliable. None of IMS accepts any liability or responsibility whatsoever for the accuracy or

completeness of any such information. All estimates, expressions of opinion and other subjective judgments contained

herein are made as of the date of this document. Emerging securities markets may be subject to risks significantly higher

than more established markets. In particular, the political and economic environment, company practices and market

prices and volumes may be subject to significant variations. The ability to assess such risks may also be limited due to

significantly lower information quantity and quality. By accepting this document, you agree to be bound by all the

foregoing provisions.

LXM LLP USA assumes responsibility for the research reports content in regards to research distributed in the U.S. LXM

LLP USA or its affiliates has not managed or co-managed a public offering of securities for the subject company in the

past 12 months, has not received compensation for investment banking services from the subject company in the past 12

months, does not expect to receive and does not intend to seek compensation for investment banking services from the

subject company in the next 3 months. LXM LLP USA has never owned any class of equity securities of the subject

company. There are not any other actual, material conflicts of interest of LXM LLP USA at the time of the publication of

this research report. As of the publication of this report LXM LLP USA, does not make a market in the subject securities.