interests on transactions - for downloads -...

TRANSCRIPT

Interests on Transactions

Chapter 10 – 13

PV & FV of Annuities

PV & FV of Annuities

An annuity is a series of equal

regular payment amounts

made for a fixed number of

periods

2

Problem

• An engineer deposits P1,000 in a savings

account at the end of each year for 5 years.

How much money can he withdraw at the end

of 5 years if the bank pays interest at the rate

of 6% p.a., compounded annually?

An engineer deposits P1,000 in a savings account at the

end of each year for 5 years. How much money can he

withdraw at the end of 5 years if the bank pays interest

at the rate of 6% p.a. compounded annually?

FV = PV ( 1 + i ) ⁿ

FV = 1000(1.06)⁴ + 1000(1.06)³

+ 1000(1.06)² + 1000(1.06) + 1000

= P5,637.09

1 2 3 4 5

FV

An engineer deposits P1,000 in a savings account at the

end of each year for 5 years. How much money can he

withdraw at the end of 5 years if the bank pays interest

at the rate of 6% p.a. compounded annually?

FV = FV( rate, nper, pmt, pv, type)

FV = FV (.06,4,0,-1000,0) + FV (.06,3,0,-1000,0)

+ FV (.06,2,0,-1000,0) + FV(.06,1,0,-1000,0)

+ FV(.06,0,0,-1000,0)

= P5,637.09

1 2 3 4 5

FV

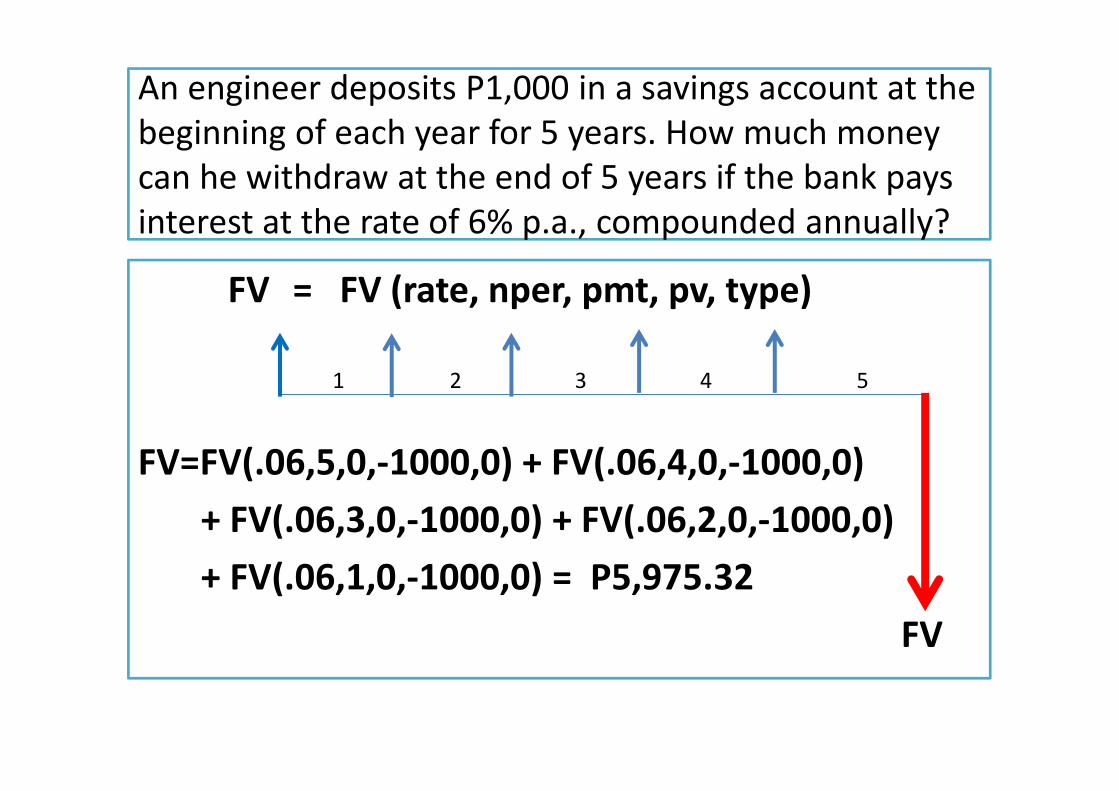

An engineer deposits P1,000 in a savings account at the

beginning of each year for 5 years. How much money

can he withdraw at the end of 5 years if the bank pays

interest at the rate of 6% p.a., compounded annually?

FV = PV ( 1 + i ) ⁿ

FV = 1000(1.06)⁵ + 1000(1.06)⁴ + 1000(1.06)³ + 1000(1.06)² + 1000(1.06)

= P5,637.09 (1.06) = P5,975.32

FV

1 2 3 4 5

An engineer deposits P1,000 in a savings account at the

beginning of each year for 5 years. How much money

can he withdraw at the end of 5 years if the bank pays

interest at the rate of 6% p.a., compounded annually?

FV = FV (rate, nper, pmt, pv, type)

FV=FV(.06,5,0,-1000,0) + FV(.06,4,0,-1000,0)

+ FV(.06,3,0,-1000,0) + FV(.06,2,0,-1000,0)

+ FV(.06,1,0,-1000,0) = P5,975.32

FV

1 2 3 4 5

FV = PV ( 1 + i ) ⁿ

FV = 1000 (1.06)⁵ + 1000(1.06)⁴ + 1000(1.06)³ + 1000(1.06)²+1000(1.06)

FV = Pmt (1 + i)ⁿ + Pmt ( 1+ i)ⁿ⁻ᶦ + Pmt (1 + i)ⁿ⁻² + Pmt(1 + i)ⁿ⁻³

+ Pmt (1 + i)ⁿ⁻⁴ + ….. + Pmt (1 + i)ⁿ⁻ⁿ

1000 = Pmt 0.06 = i

Geometric series: a + ax + ax² + + ax³ + ... + ax ⁿ⁻¹

Summation = Sn = a (1-xⁿ)

(1-x)

x = ratio of successive terms = [Pmt (1+i)ⁿ⁻ᶦ] / [Pmt (1+i)ⁿ⁻ᶦ] = 1 / (1+i)

a = first term = Pmt(1+i)ⁿ

FV = {Pmt(1+i)ⁿ} {1- [1/(1+i)]ⁿ} / {1 – [1/(1+i)]}

= Pmt (1+i)ⁿ [(1+i)ⁿ- 1)/(1+i)ⁿ] /[(1+ i – 1) / (1+i)]

FV = {Pmt (1+i) [(1+i)ⁿ- 1)]} / i annuity due formula

1 2 3 4 5

Basic Formula to UseBasic Formula to Use

B Loan Balance after n payments = FV Compounding – FV annuity

(5) B = PV (1 + i ) ⁿ - Pmt [ (1 + i)ⁿ - 1]

i

(1) FV compounding = PV ( 1 + i ) ⁿ

single transaction

(2) PV discounting = FV ( 1+ i )⁻ⁿsingle transaction

(3) FV annuity = Pmt [ (1 + i)ⁿ - 1]

ordinary annuity i

(4) PV annuity = Pmt [1 – (1 + i )⁻ⁿ]

ordinary annuity i 9

Basic Formula to UseBasic Formula to Use

B Loan Balance after n payments = FV Compounding – FV annuity

(5) B = PV (1 + i ) ⁿ - Pmt [ (1 + i)ⁿ - 1]

i

(1) FV compounding = PV ( 1 + i ) ⁿ

= FV (rate, nper, 0, pv, 0)

(2) PV discounting = FV ( 1+ i )⁻ⁿ= PV (rate, nper, 0, fv, 0)

(3) FV annuity = Pmt [ (1 + i)ⁿ - 1]

ordinary annuity i

= FV (rate, nper, pmt, pv, 0)

(4) PV annuity = Pmt [1 – (1 + i )⁻ⁿ]

ordinary annuity i

= PV (rate, nper, pmt, fv, 0) 10

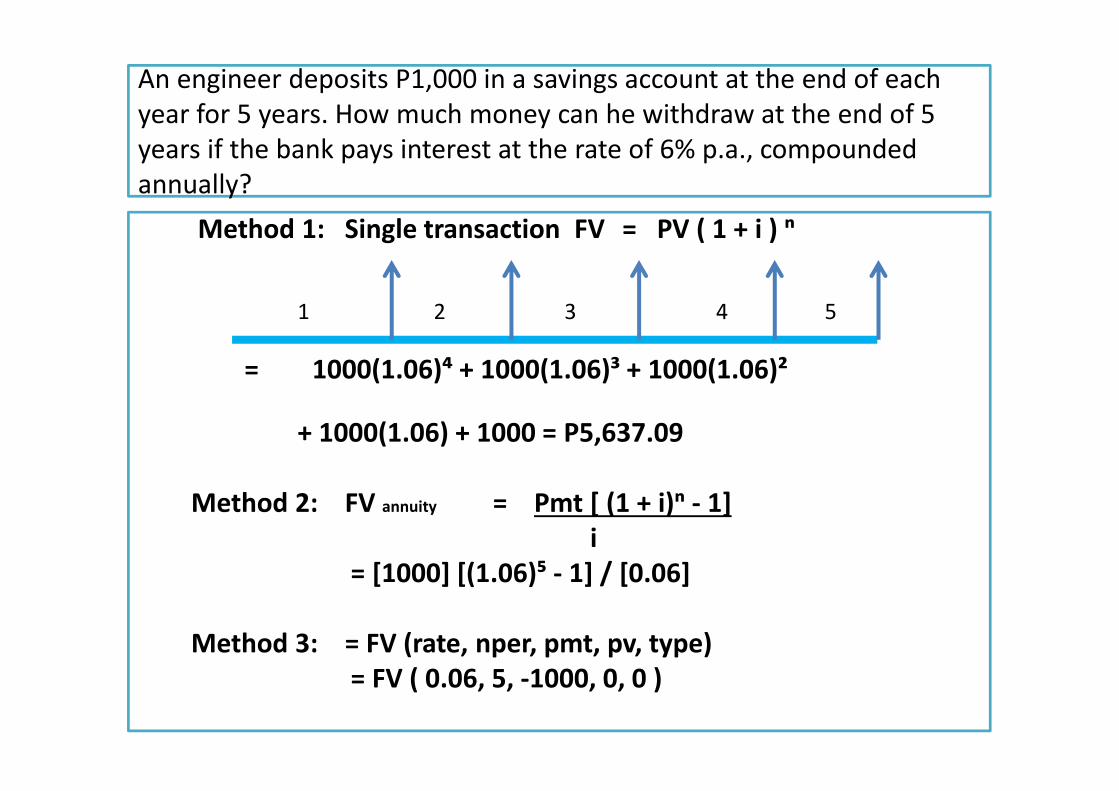

An engineer deposits P1,000 in a savings account at the end of each

year for 5 years. How much money can he withdraw at the end of 5

years if the bank pays interest at the rate of 6% p.a., compounded

annually?

Method 1: Single transaction FV = PV ( 1 + i ) ⁿ

= 1000(1.06)⁴ + 1000(1.06)³ + 1000(1.06)²

+ 1000(1.06) + 1000 = P5,637.09

Method 2: FV annuity = Pmt [ (1 + i)ⁿ - 1]

i

= [1000] [(1.06)⁵ - 1] / [0.06]

Method 3: = FV (rate, nper, pmt, pv, type)

= FV ( 0.06, 5, -1000, 0, 0 )

1 2 3 4 5

B. Annuities:

A series of equal payments

A. Ordinary Annuity: Regular

deposits are made at the end of

the period.

B. Annuities Due: Regular deposits

are made at the beginning of the

period

12

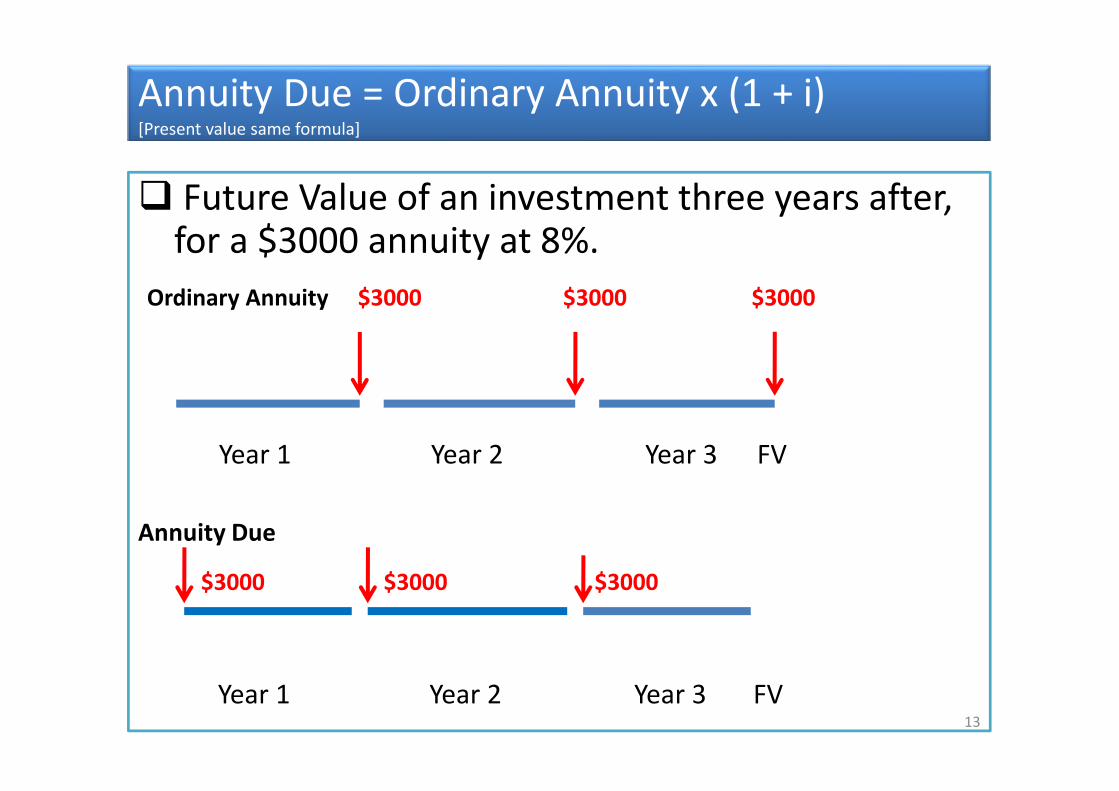

Annuity Due = Ordinary Annuity x (1 + i) [Present value same formula]

� Future Value of an investment three years after, for a $3000 annuity at 8%.

Ordinary Annuity $3000 $3000 $3000

Year 1 Year 2 Year 3 FV

Annuity Due

$3000 $3000 $3000

Year 1 Year 2 Year 3 FV13

I. Ordinary Annuity:

Future Value

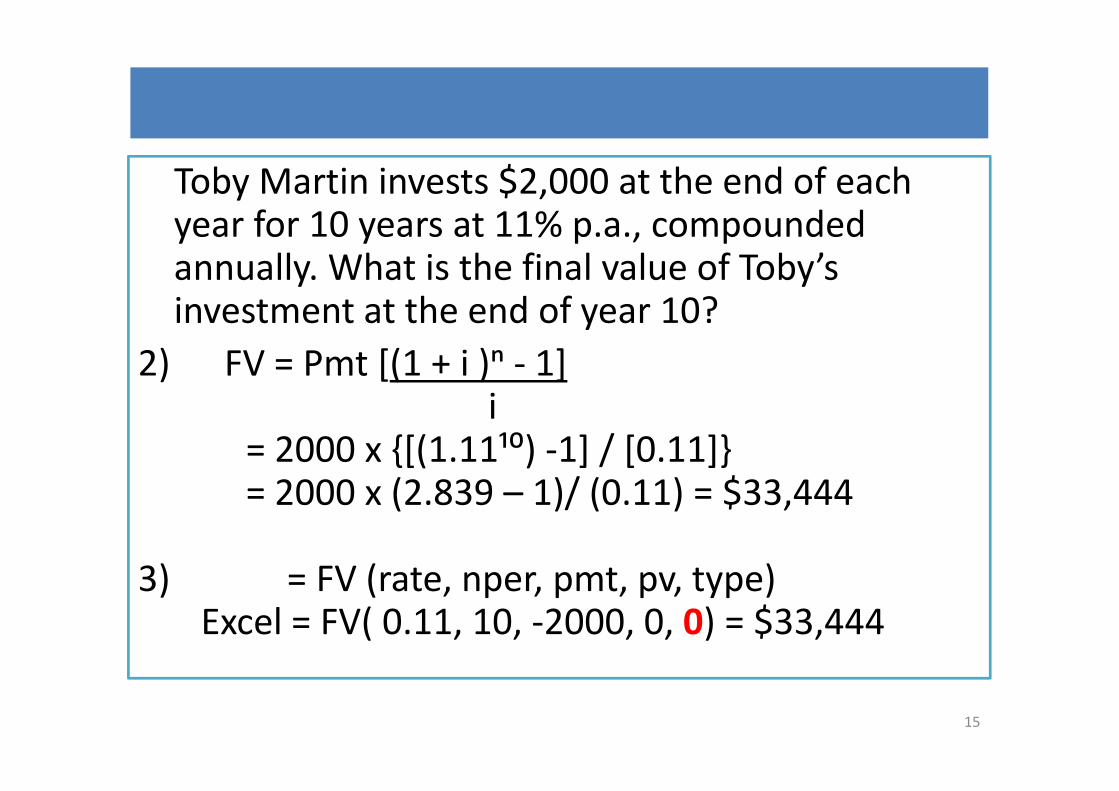

Toby Martin invests $2,000 at the end of each year for 10 years at 11% p.a., compounded annually. What is the final value of Toby’s investment at the end of year 10?

1) By Table:Periods = 10 x 1 = 10 ; Rate = 11 % / 1 = 11%

Table 13-1 Table Factor = 16.7220

Future Value = $2,000 X 16.7220 = $ 33,444

14

Toby Martin invests $2,000 at the end of each year for 10 years at 11% p.a., compounded annually. What is the final value of Toby’s investment at the end of year 10?

2) FV = Pmt [(1 + i )ⁿ - 1]i

= 2000 x {[(1.11¹⁰) -1] / [0.11]}= 2000 x (2.839 – 1)/ (0.11) = $33,444

3) = FV (rate, nper, pmt, pv, type) Excel = FV( 0.11, 10, -2000, 0, 0) = $33,444

15

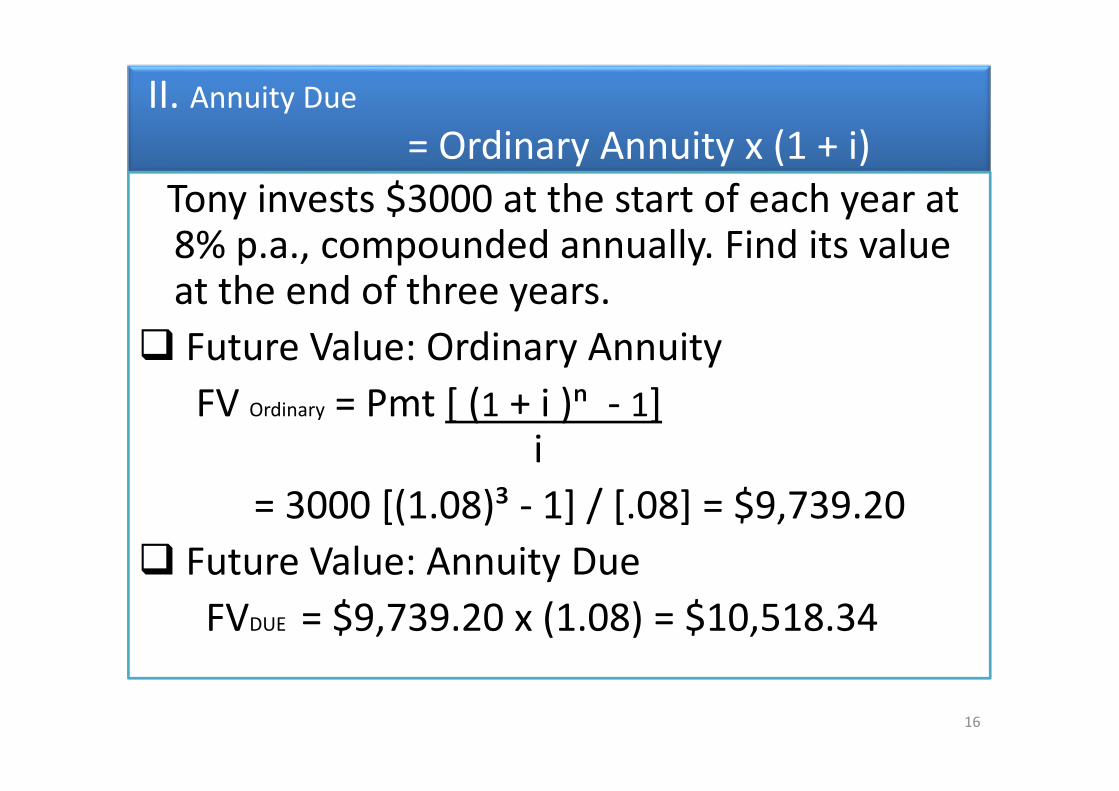

II. Annuity Due

= Ordinary Annuity x (1 + i)

Tony invests $3000 at the start of each year at 8% p.a., compounded annually. Find its value at the end of three years.

� Future Value: Ordinary Annuity

FV Ordinary = Pmt [ (1 + i )ⁿ - 1]i

= 3000 [(1.08)³ - 1] / [.08] = $9,739.20

� Future Value: Annuity Due

FVDUE = $9,739.20 x (1.08) = $10,518.34

16

Annuity Due

By Table 13-1 of textbook:

� Future Value: Ordinary Annuity

n = 3, i = 8% , table factor = 3.2464

FV = 3000 x 3.2464 = $9,739.20

� Future Value: Annuity Due

Add one period & subtract one payment

n = 4, i = 8% , table factor = 4.5061

FV = [3000 x 4.5061] – 3000 = $10,518.30

17

Annuity Due

� Future Value: Ordinary Annuity

n = 3, i = 8%

Excel: = FV (0.08,3,-3000,0,0) = $9,739.20

� Future Value: Annuity Due

n = 3, i = 8%

Excel: =FV (0.08,3,-3000,0,1) = $10,518.34

18

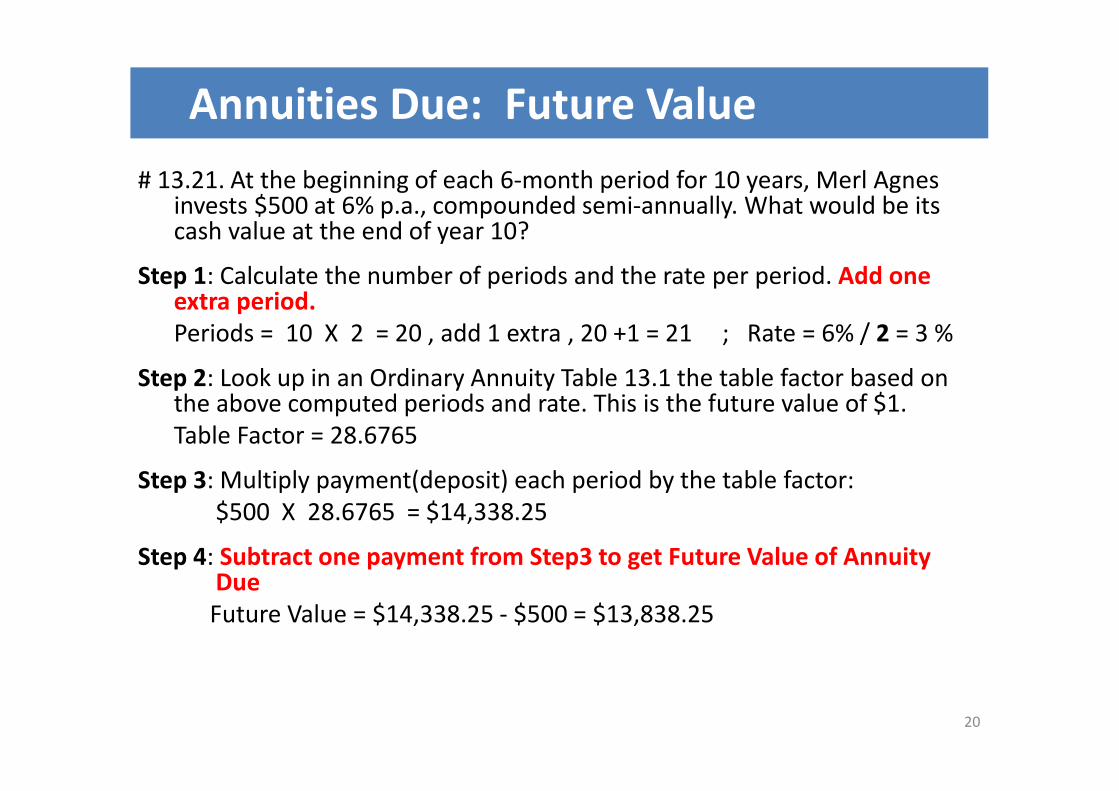

# 9

• # 13.21. At the beginning of each 6-month

period for 10 years, Merl Agnes invests $500

at 6% p.a., compounded semi-annually. What

would be its cash value at the end of year 10?

1) Formula: FV = 500 [(1.03)²⁰ - 1] (1.03)

0.03

= [500 [0.806111/ 0.03] (1.03)

= $13,838.24

2) = FV ( 0.03, 20, -500, 0, 1 ) = $13,838.24

19

Annuities Due: Future Value

# 13.21. At the beginning of each 6-month period for 10 years, Merl Agnes invests $500 at 6% p.a., compounded semi-annually. What would be its cash value at the end of year 10?

Step 1: Calculate the number of periods and the rate per period. Add one extra period.

Periods = 10 X 2 = 20 , add 1 extra , 20 +1 = 21 ; Rate = 6% / 2 = 3 %

Step 2: Look up in an Ordinary Annuity Table 13.1 the table factor based on the above computed periods and rate. This is the future value of $1.

Table Factor = 28.6765

Step 3: Multiply payment(deposit) each period by the table factor:

$500 X 28.6765 = $14,338.25

Step 4: Subtract one payment from Step3 to get Future Value of Annuity Due

Future Value = $14,338.25 - $500 = $13,838.25

20

II. Ordinary Annuity: Present value

On Joe’s graduation from college, his uncle promised him a gift of $12,000 in cash, or $900 every quarter for the next 4 years after graduation. If money could be invested at 8% p.a., compounded quarterly, which offer is better for Joe?

1) By Table:

Periods = 4 X 4 = 16 Rate = 8% / 4 = 2 %

Table 13 – 2 Factor = 13.5777

PV = $ 900 X 13.5777 = $ 12,219.93

Annuity is better than $ 12,000 cash

21

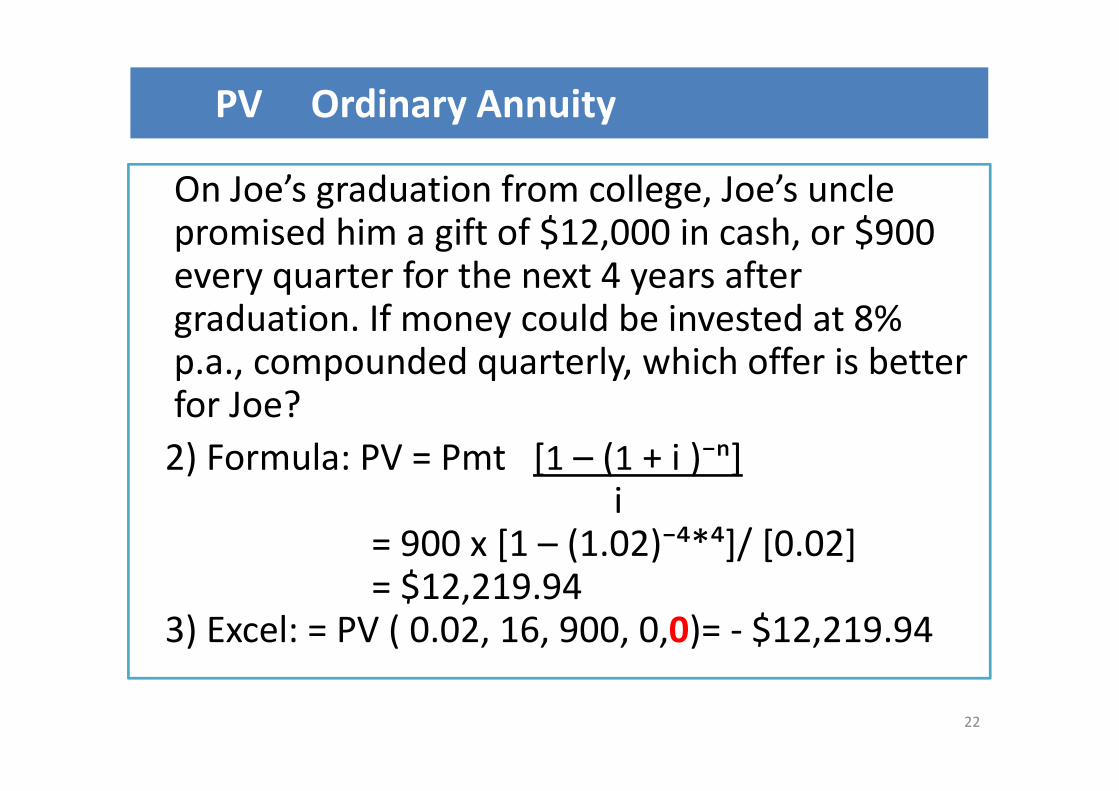

PV Ordinary Annuity

On Joe’s graduation from college, Joe’s uncle promised him a gift of $12,000 in cash, or $900 every quarter for the next 4 years after graduation. If money could be invested at 8% p.a., compounded quarterly, which offer is better for Joe?

2) Formula: PV = Pmt [1 – (1 + i )⁻ⁿ]i

= 900 x [1 – (1.02)⁻⁴*⁴]/ [0.02]= $12,219.94

3) Excel: = PV ( 0.02, 16, 900, 0,0)= - $12,219.94

22

Sinking Fund – annuity where the equal

periodic payments are determined

Jeff Associates plans to setup a sinking fund to repay $30,000 at the end of 8 years. Assume an interest rate of 12% p.a., compounded semi-annually.

1) By Table 13-3:

n = 8 x 2 = 16; rate = 12% / 2 = 6%

Table 13 – 3 factor = 0.0390

Sinking Fund = $ 30,000 X .0390

= $1,170

23

Sinking Fund

Jeff Associates plans to setup a sinking fund to repay $30,000 at the end of 8 years. Assume an interest rate of 12% p.a., compounded semi-annually.

� Formula: Pmt = FV [ i ]

[ (1 + i)ⁿ - 1 ]

= 30000 * {.06/[(1.06)⁸*² - 1]}

= $1,168.56

� Excel: = PMT(rate, nper, pv, fv, type)

Excel: = PMT (0.06, 16, 0, 30000,0) = - $1,168.56

24

Monthly payment & Payoff amountMonthly payment & Payoff amount

• Mr. Joson buys a car for P1M. A down payment of

20% of the car price is paid in cash, with the

balance to be paid in 36 months. The interest rate

is 14.25% p.a., compounded monthly. After 24

months of paying, Mr. Joson would like to know

his payoff amount.

i = 14.25% / 12 = 0.011875 per month

PV = P1M – P200K = P800,000

n = 36 months

• First step: Find monthly payment amount

Monthly Payment

• PV = [Pmt/i ] [ 1 – (1 + i )⁻ⁿ]

Pmt = [i PV ] / [1 – (1 + i)⁻ⁿ]

= [(0.011875)(800,000) = P27,439.34

[ 1 – (1.011875)⁻³⁶ ]

Using Excel: pmt(rate, nper, pv, fv, type)

= pmt (0.011875, 36, -800000, 0, 0)

= P27,439.34

• Second Step: Find the payoff amount

Payoff AmountB Loan Balance after n payments = FV Compounding – FV annuity

B = PV (1 + i ) ⁿ - Pmt [ (1 + i)ⁿ - 1]

i

= 800,000 ( 1.011875)²⁴

- 27,439.34 [ (1.011875)²⁴ - 1]

0.011875

= 1,062,025.08 – 756,820.62

= P305,204.46

Excel: = FV ( rate, nper, pmt, pv, type)

Method 1: = FV(0.011875, 24, 0, -800000, 0)

- FV(0.011875, 24, -27439.34, 0, 0)

Method 2: = FV(0.011875, 24, 27439.34, -800000, 0)

= P305,204.46 amount still to be paid

Add Timeline Drawing

END