integration support programme · integration support programme country: tunisia appraisal report...

TRANSCRIPT

Language : English Original : French

AFRICAN DEVELOPMENT BANK

INTEGRATION SUPPORT PROGRAMME COUNTRY: TUNISIA

APPRAISAL REPORT February 2009

Appraisal Team e E

Design Team: Team Members: Sector Director: Country Director: Division Manager:

H. Kouassi, Principal Macro-Economist, OSGE.2, N. Obayashi, Principal Country Economist, ORNA S.E. Mivedor, Chief Portfolio Officer OPSM.5/FTRY.4, and Consultants (Financial Economist and Trade Specialist). G. Negatu, Director, OSGE J. Kolster, Director, ORNA M. Kanga, Division Manager, OSGE.2

Peer Reviewers

C. Baumont: A. A. Ba : P. Yembiline:

Chief Country Economist, OREB Principal Country Economist, ORNB Senior Country Economist, ORCE

i

Table of Contents LIST OF TABLES-LIST OF BOXES-LIST OF FIGURES LIST OF ANNEXES - LIST OF TECHNICAL ANNEXES FISCAL YEAR – CURRENCY EQUIVALENTS i ACRONYMS AND ABBREVIATIONS i LOAN INFORMATION ii PROGRAMME EXECUTIVE SUMMARY iii PROGRAMME LOGICAL FRAMEWORK vii I . THE PROPOSAL 1 II . COUNTRY AND PROGRAMME CONTEXT 1

2.1 Government Development Strategies and Medium-Term Reform Priorities 1 2.2 Recent Economic Developments, Prospects and Constraints 3 2.3 Bank Portfolio Status 5

III – JUSTIFICATION, KEY DESIGN ELEMENTS AND SUSTAINABILITY 5

3.1 Link with CSP, Analytical Factors Underpinning Programme Preparation and Prerequisites 5 3.2 Collaboration and Coordination with other Donors 7 3.3 Outcomes and Lessons from Similar Past Operations 7 3.4 Relationship with other Bank Operations 8 3.5 Bank’s Comparative Advantages 8 3.6 Application of Good Practice Principles on Conditionality 8

IV – PROPOSED PROGRAMME 8

4.1 Programme Objectives 8 4.2 Programme Pillars and Expected Results 8 4.3 Financing Requirements and Arrangements 18 4.4 Programme Beneficiaries 18 4.5 Impact on Gender 18 4.6 Environmental Impact 19

V – IMPLEMENTATION, MONITORING AND EVALUATION 19

5.1 Implementation Arrangements 19 5.2 Monitoring and Evaluation Arrangements 19

VI – LEGAL DOCUMENTS AND AUTHORITY 20

6.1 Legal Documents 20 6.2 Conditions for Bank Group Intervention 20 6.3 Compliance with Bank Group Policies 21

VII – RISK MANAGEMENT 22 VIII – RECOMMENDATION 22 This report was written by Mr. H. Kouassi, Principal Macro-Economist, OSGE.2, Mrs. N. Obayashi, Principal Country Economist, ORNA, on the basis of the joint missions fielded with the World Bank and the European Union to Tunis in March, May and September 2008 as well as in February 2009, and supplemented by discussions with the Tunisian authorities. It also received the input of Mr. S. Mivedor, Chief Portfolio Officer, OPSM.5/FTRY.4, a Consultant Financial Economist, Consultant Trade Specialist, and also from discussions with Economists of the above-mentioned institutions. Questions on this report should be referred to Mr. G. Negatu, Director, OSGE (ext. 2077) and Mrs. M. Kanga, Division Manager, OSGE.2 (ext. 2251).

ii

List of Tables

List of Boxes

Box 1: Actions Prior to Presentation of PAI to the Boards to be implemented by end of February 2009

List of Figures

Figure 1: Most of growth in overall demand originates from non-EU markets

List of Annexes

List of Technical Annexes

Table 1 Trend of Competitiveness and Integration of Tunisian Economy, 2001-2006 Table 2 Medium-Term Macro-Economic Objectives, 2009-2011 Table 3 Key Analytic Works Used Table 4 Outcomes of Previous Operations and Linkage with PAI Table 5 PAI Financing Requirements and Arrangements, 2009-2010 Table 6 Risk Analysis

Annex 1 Development Policy Letter (see Technical Annex) 1 Annex 2 Matrix of Programme Measures 10 Annex 3 Note on Relations with IMF 2 Annex 4a Overall MTEF 3 Annex 4b Baseline Macro-Economic Indicators for Monitoring 1 Annex 5 Evaluation of Conditions Precedent to General Budget Support 1 Annex 6 Status of Application of Good Practice Principles on Conditionality 1

Annex 1 Letter of Intent on Development Policy Annex 2 Trend and Characteristics of FDIs Annex 3 Performance of Value-Added at Constant Prices in 2006 by end of the 10th Plan Annex 4 Impact of Financial Crisis in Tunisia Annex 5 Key 2009 Budget Measures and Presidential Measures for Export Companies Annex 6 IMF Recent Projections on World Economy Annex 7 Monitoring-Evaluation Arrangements Annex 8 Results Chain

iii

Fiscal Year January-December

Currency Equivalents (In February 2009)

UA 1 = DT 2.01760 (Tunisian Dinars) UA 1 = EUR 1.16411 (Euros) UA 1 = US$ 1.49192 (US Dollars)

Acronyms and Abbreviations ADB : African Development Bank API : Investment Promotion Agency BCT : Central Bank of Tunisia BTA : Long-Term Treasury Bonds (Bon du Trésor assimilable) BVMT : Tunis Stock Exchange CEPEX : Export Promotion Centre CFAA : Country Financial Accountability Assessment CGA : General Insurance Council CGC : General Compensation Fund (Caisse Générale de la Compensation) CNS : National Services Council CNSS : National Social Security Fund COTUNACE : Tunisian External Trade Insurance Company CPAR : Country Procurement Assessment Review CSP : Country Strategy Paper DGA : Department of Insurance DGP : Department of Forecasts EU : European Union FAMEX : Export Market Access Fund FCP : Mutual Fund FDI : Foreign Direct Investments FOPRODEX : Export Promotion Fund GAFTA : Greater Arab Free Trade Area GBO : Goal-oriented Budget Management GDP : Gross Domestic Product GFCF : Gross Fixed Asset Formation ILO : International Labour Organization IME : Mechanical and Electrical Industries IMF : International Monetary Fund INS : National Institute of Statistics ITC : International Trade Centre MDCI : Ministry of Development and International Cooperation MENA : Middle East and North Africa MFA : Multi-Fibre Arrangement MTEF : Medium-Term Expenditure Framework OPCVM : Undertaking for Collective Investments in Transferable Securities PAC : Competitiveness Support Programme PAI : Integration Support Programme PEFA : Public Expenditure and Financial Accountability SICAR : Venture Capital Investment Company SICAV : Open-ended Investment Company SVT : Treasury Bond Dealer UA : Unit of Account WEO : World Economic Outlook

iv

Loan Information

Client Information BORROWER : Republic of Tunisia EXECUTING AGENCY : Ministry of Development and International Cooperation Financing Plan

Source Amount (UA) Instrument ADB

US$ 250 million

ADB Loan

World Bank US$ 250 million IBRD Loan European Union EUR 50 million Grant

Information on ADB Financing

Loan/Grant Currency

US$

Interest Type Fixed base rate

Base Rate (Floating: Libor $6m) Rate setting arrangements, terms: at any time, at Borrower’s request

Interest Rate Margin 0.40% Funding Margin Variable, recomputed every six months

and passed on to clients Tenor 20 years, including a grace period of 5

years

Provisional Timeframe

Activities Date 1. Loan Agreement Negotiations March 2009 2. Board Presentation April 2009 3. Effectiveness May 2009 4. Disbursement of First Tranche May 2009 5. Supervision November 2009 6. Mid-term Review June 2010 7. Disbursement of Second Tranche July 2010 8. Supervision February 2011 9. Completion report August 2011

v

Programme Executive Summary Programme Overview 1. Programme Title : Integration Support Programme Geographical Scope : National Overall Timeframe : 18 months Programme Cost : US$ 250 million (ADB); US$ 250 million (World Bank) ;

EUR 50 million (European Union) Type of Programme : General budget support

2. The Bank’s financing will be disbursed from 2009 to 2010. The first tranche of US$ 125 million will be disbursed upon fulfilment of the conditions precedent to presentation of the Programme to the Boards and to loan effectiveness. The second tranche of US$ 125 million will be disbursed following satisfactory mid-term review of the Programme and fulfilment of the specific conditions. Expected Programme Outcomes 3. The aim of PAI is to boost growth and employment in keeping with the objectives of the 11th Plan (2007-2011), adopted in January 2007, and the Development Policy Letter. The specific objective of the Programme is to foster better integration into the global economy. 4. The overall expected outcomes (impacts) from 2009 to 2010 are: (i) reduced transaction costs and deepening of trade integration; (ii) improved business environment; and (iii) improved access to financing. The programme is underpinned by a stable and conducive macro-economic framework. 5. The final beneficiary of the Programme is the entire Tunisian population. It will benefit from the improved standard of living made possible by accelerated growth and increased job opportunities. The main intermediate beneficiaries are: (i) the public departments that will receive support from the Programme in the implementation of the 11th Plan, (ii) the private sector, which will have easier access to the financial sector and operate in an improved business environment, (iii) the unemployed, including women, who will have increased job opportunities, and (iv) consumers, who will have at their disposal less costly and better quality products and services. Needs Assessment and Relevance 6. The Programme is necessary for the following main reasons: (i) the country’s two-tier trade integration strategy with the co-existence of preferential (EU, GAFTA, etc.) and non-preferential partners has reached its limit, and (ii) strengthening of the overall integration of Tunisia into the global economy, backed by (a) reduced transaction costs and deepening of trade integration, (b) an improved business environment, and (c) improved access to financing is necessary to achieve the objectives of growth in per capita income and employment of the 11th Plan. The reforms adopted in this Programme will contribute to the achievement of these objectives and form part of the Plan’s priorities.

vi

7. The Programme is necessary now because it will consolidate the gains of the three previous competitiveness support programmes (PAC I, PAC II and PAC III) implemented from 1999 to 2007, and supported by the Bank. The Bank and the other co-financiers are intervening, at the request of the Government, to support its efforts in the implementation of its Development Programme against the backdrop of an acute global economic crisis. 8. The approach adopted appears to be the most relevant. The arrangements under the Programme should enhance the chances of satisfactory implementation, including: risk-sharing, with the presence of the other donors, and coordinated support; fulfilment of the general and technical conditions for this type of programme; the substantial increase in the financial support to meet the Government’s needs amplified by the economic crisis; the results-based specific implementation and monitoring-evaluation arrangements; and conditionality consistent with relevant good practices, including conditions precedent to submission to the Boards. All these factors should allow for achievement of the Programme’s expected outcomes. The PAI’s areas of intervention are consistent with the 11th Plan reflected in Tunisia’s Development Policy Letter and CSP 2007-2011. Value Added for the Bank 9. The Bank’s value added in this operation lies mainly in the experience and lessons drawn from this type of support after the three previous competitiveness support programmes, which culminated in completion reports. These lessons and experiences, which were shared with the co-financiers, were judiciously used in this Programme. In addition, the Bank has mobilized expertise for the financial sector and trade reforms. Institutional Development and Knowledge Building 10. The PAI contributes to the development of Tunisia’s public administration and private sector (intermediate beneficiaries of the Programme). It also contributes to knowledge building through the analytical studies preceding it and through the conduct of studies, institutional, legislative and regulatory assessments to be used in formulating and implementing the Programme and other future operations. There will be further knowledge building with the preparation of the completion reports at the end of the Programme. Risk Management 11. The risks relating to outputs, or the satisfactory implementation of the Programme, are lessened owing to the fulfilment of the general and technical conditions for general budget support. The relevance of the programme formulation also reduces the risk involved in implementation. It is also quite unlikely that the private sector and consumers will not adhere to the reforms. External shocks (major variations in commodity prices and global economic activity) represent the only significant risks to the impacts. However, the low level of integration of the Tunisian financial sector, the counter-cyclical option of the medium-term 2009-2011 programme, reflected in the 2009 budget, and the substantial increase in financial support to meet the Government’s needs will help to mitigate this risk. Lastly, the economic rescue and revival plans in the major industrialized and emerging countries could also reduce the extent and duration of the effects of the global economic crisis on the Tunisian economy as from 2009.

vii

Results-Based Logical Framework

Country : Tunisia Programme Name : Integration Support Programme (PAI) 2009-2010 Team : H. Kouassi, OSGE/N. Obayashi, ORNA

HIERARCHY OF OBJECTIVES EXPECTED OUTCOMES SCOPE PERFORMANCE

INDICATORS

TARGETED OBJECTIVES AND

TIMEFRAME ASSUMPTIONS/RISKS

1.Goal: Boost growth and employment, in keeping with the objectives of the 11th Plan (2007-2011)

1.Impact: Growth is continuous and sustainable Unemployment is reduced

1. Beneficiaries: Tunisian population Active population

1. Indicators: Average growth rate of real GDP Sources: MDCI, PAI reports Data collection method: Supervision missions Overall investment rate Sources: MDCI, PAI reports Data collection method : Supervision missions Average unemployment rate Sources : MDCI, PAI reports Data collection method : Supervision missions

1. Expected long-term Trends-Timeframe Real growth rate rises from 4.5% in 2008 to average of 5.0% in 2009 and 2010 and to 6.0% in 2011 Overall investment rises from 25.5% in 2008 to an average of 26.4% in 2009 and 2010 and to 28.0% in 2011 Unemployment rate drops from 14.1 % in 2007 to an average of 13.1% in 2009 and 2010

Programme Goal Foster better integration into global economy

Impacts: Transaction costs are reduced and trade integration is deepened

Beneficiaries:

Government Departments Productive sector Consumers Job-seeking young graduates

Impact Indicators: Average ordinary rate Sources of data: MDCI, INS, PAI reports Data collection method: Supervision missions

Expected Long-term Trends-Timeframe: Average ordinary rate drops from 21.7% to 18% from 2007 to 2010

Assumptions Programme’s impacts are achieved

viii

HIERARCHY OF OBJECTIVES EXPECTED OUTCOMES SCOPE PERFORMANCE

INDICATORS

TARGETED OBJECTIVES AND

TIMEFRAME ASSUMPTIONS/RISKS

----------------------------------

Access to bank and non-bank financing is improved ------------------------------------ Business environment is improved

------------------------

Degree of openness measured by X+M/GDP in % Sources of data: MDCI, INS, PAI reports Data collection method : Supervision missions --------------------------------

Average growth rate of private sector loans Sources of data : MDCI, BCT, PAI reports Data collection method : Supervision missions Contribution of financial market to GFCF Sources of data : MDCI, Rapports BCT Data collection method : Supervision missions --------------------------------------- Doing Business ranking Sources of data: Rapports Doing Business 2010-2011; PAI supervision reports Data collection method: Supervision missions

Degree of openness increases from 114% in 2007 to 123% in 2010 -------------------------------

Growth rate of private sector loans higher in 2009-2010 than level of 11.2% in 2007 The average contribution of the financial market to the GFCF higher in 2009-2010 than level of 7.6% in 2007 ---------------------------------- Tunisia’s Doing Business ranking in 2009 and 2010 improved compared to that of 2008 (73rd)

Risks

Effects of external shocks stemming from global economic crises may disrupt achievement of expected impacts

Mitigation Measures -Adequate counter-cyclical policies contained in MTEF 2009-2011 and Budget 2009: - Relevant formulation of Programme - Low integration of Tunisian financial sector - Counter-cyclical policies in leading industrialized and emerging countries - Substantial financial support

ix

HIERARCHY OF OBJECTIVES EXPECTED OUTCOMES SCOPE PERFORMANCE

INDICATORS

TARGETED OBJECTIVES AND

TIMEFRAME ASSUMPTIONS/RISKS

3. Inputs: ADB: US$ 250 million European Commission: Euro 50 million World Bank: US$ 250 million

Outputs All measures (see Matrix of Measures) necessary to reduce transaction costs and deepen trade integration are implemented

------------------------------ All measures (see Matrix of Measures) necessary to improve access to bank and non-bank financing are implemented -------------------------------- All measures (see Matrix of Measures) necessary to improve business environment are implemented

Beneficiaries: Government Departments

Output Indicators See Matrix of Measures Sources of data: See Matrix of Measures Data collection method: Supervision missions ------------------------------------ See Matrix of Measures Sources of data: See Matrix of Measures Data collection method: Supervision missions ----------------------------- See Matrix of Measures Sources of data: See Matrix of Measures Data collection method : Supervision missions

Expected Long-term Trends See Matrix of Measures See Matrix of Measures See Matrix of Measures

Assumptions General and technical conditions for general budget support are fulfilled Financial support available and predictable Acceptance of Programme by private sector and consumers Risks Low risks. Mitigation Measures Not required

REPORT AND RECOMMENDATION BY THE BANK GROUP MANAGEMENT TO THE BOARDS OF DIRECTORS ON A PROPOSED LOAN TO TUNISIA FOR THE

INTEGRATION SUPPORT PROGRAMME

I. PROPOSAL 1.1 Management submits the following Report and Recommendation on a proposed loan of US$ 250 million (UA 167.57 million) to Tunisia to finance the Integration Support Programme (PAI). It is a programme of general budget support to the Government to be implemented over 18 months, as from May 2009. The appraisal, conducted in June 2008, was supplemented with other missions in September 2008, then January and February 2009. It follows a request formulated by the Government in January 2008 and is consistent with the Government’s 11th Plan (2007-2011) and the Country Strategy Paper (CSP) (2007-2011) adopted in January and July 2007. The 11th Plan and the ensuing Development Policy Letter were considered satisfactory by the Bank, the World Bank and the European Commission, which are involved in the financing of this Programme. The Programme design took into account the principles of the Paris Declaration on Aid Effectiveness, as well as good practice principles on conditionality. 1.2 This operation comes after the three structural reform programmes involving competitiveness support, implemented from 1999 to 20071. Its ultimate goal is to support the Government in achieving the growth and employment objectives stated in the Development Policy Letter. It is also intended to help the country address the difficulties arising from the global crisis context and prepare the Tunisian economy for the future. These goals will be achieved, in part, through creating enabling conditions for more effective integration of the country, a small economy with export-based growth, into the world economy. The expected outcomes (impacts) are: (i) reduced transaction costs and deepening of trade integration for both goods and services; (ii) improved business environment; and (iii) improved access to financing. The Programme is underpinned by a stable and conducive macro-economic framework. Given the context of the global economic crisis, it has been agreed that a prudent and gradual approach will be adopted. The PAI thus represents a stage in the implementation of more in-depth future structural reforms. II. COUNTRY AND PROGRAMME CONTEXT 2.1 Government Development Strategy and Medium-Term Priorities 2.1.1 Before detailing the Government’s current development strategy and medium-term priorities, it is necessary to briefly explain the context in which the strategy was defined and its justification. 2.1.2 Integration has played a crucial role in the economic success of Tunisia, a small economy endowed with few natural resources, which has experienced steady improvement in its per capita income for several decades. Indeed, the introduction of an offshore system in the early 1970s coupled with incentives to attract FDIs and increase manufacturing exports was

1 The Competitiveness Support Programme (PAC) was implemented through three operations: PAC I: 1999-2001; PAC II:

2002-2004; and PAC III: 2005-2007 and jointly financed with the World Bank and the European Union.

2

the first stage in this integration policy. It facilitated the integration of the offshore sector (area of choice of FDIs (Technical Annex II)) into the European production networks. Since the mid-1990’s, the Government has given a new direction to its integration policy by starting to open up the Tunisian industry to competition, particularly within the framework of the Partnership Agreement with the EU, the country’s leading economic partner. The dismantling of tariffs, creation of the free-trade zone for industrial products2 and its accompanying policies, as well as the rapid development of an offshore sector have contributed to the transformation of the Tunisian economy with the development of the manufacturing sector (Textile and Clothing (T-C) and Electrical and Mechanical Engineering (GME)) resulting in the structural transformation of industry and increased employment. These policies have boosted the competitiveness of the economy and facilitated integration (see Table 1 below). It can therefore be said that integration, which has been mainly preferential in recent years, contributed significantly to Tunisia’s economic successes.

Table 1 Trend of Competitiveness and Integration

of the Tunisian Economy (2001-2008)

2001 2005 2006 2007 2008 Current and Potential Competitiveness of the Country

Share of foreign market 0.64 - 0.70 0.71 0 .7 Share of domestic market - 50.6 56 56 Catch-up indicator of OECD countries 28 - 29.6 32.7 33.7 FDI in % of GDP 2.4 - 2.8 4.7 6.5 Management-staff ratio 10.0 - 13.8 - 14.9 Contribution of overall productivity of factors to growth 39.0 - 40.8 - 49.0 Inflation 3.5 3.3 3.5 3.1 5.0 Budget deficit (% GDP) 2.8 2.9 2.9 2.9 3.0 R&D costs in % of GDP 0.53 - 1.07 1.09 - Number of researchers 8515 - 14650 - - Life expectancy at birth 72.9 - 73.6 74.2 74.8 % o households connected to the internet 1.05 - 3.04 - -

Integration indicators (%) Protection rate - 31 22 16 - Degree of openness - 50.3 102.7 114 123 Export effort - 50 50.8 55.8 60.3 Share of exports to EU 80 80 77 79 72 Share of imports from EU 71 69 66 65 57 Sources: Tunisian authorities, World Bank, ADB

2.1.3 In spite of these successes, serious challenges remain. Despite the enviable growth of 4.5% recorded during the 10th Plan (2002-2006), it still falls below the historic level of 5% observed and is insufficient to reduce unemployment, which is presently around 14%. The assessment of the 10th Plan 2002-2006 reveals that apart from the Mechanical and Engineering Industries, there are some difficulties as regards value added in agriculture, textile and leather and tourism (Technical Annex 3).

2 The Free-Trade Zone for industrial products has been established since January 2008

3

23,9

76,1

0,05

17,3

82,7

0,031

0102030405060708090

EU Non EU MENA

Graph1: Most of growth in overall demand originates from non-EU markets

1995 2005

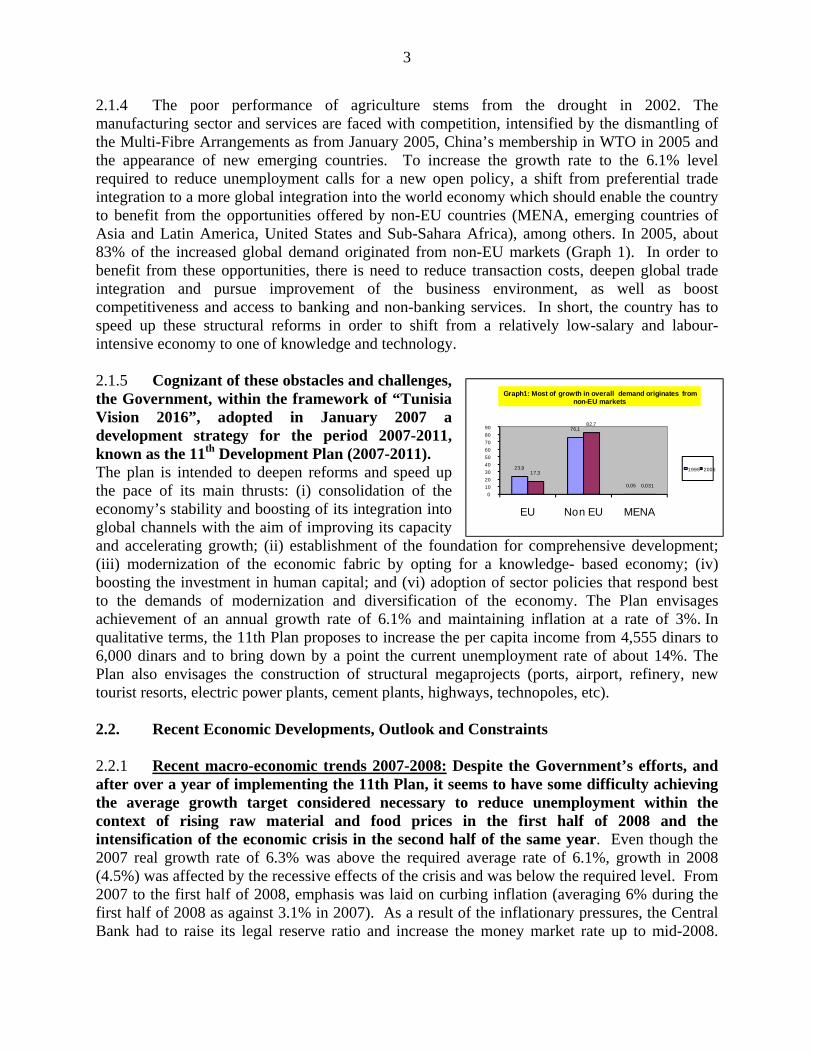

2.1.4 The poor performance of agriculture stems from the drought in 2002. The manufacturing sector and services are faced with competition, intensified by the dismantling of the Multi-Fibre Arrangements as from January 2005, China’s membership in WTO in 2005 and the appearance of new emerging countries. To increase the growth rate to the 6.1% level required to reduce unemployment calls for a new open policy, a shift from preferential trade integration to a more global integration into the world economy which should enable the country to benefit from the opportunities offered by non-EU countries (MENA, emerging countries of Asia and Latin America, United States and Sub-Sahara Africa), among others. In 2005, about 83% of the increased global demand originated from non-EU markets (Graph 1). In order to benefit from these opportunities, there is need to reduce transaction costs, deepen global trade integration and pursue improvement of the business environment, as well as boost competitiveness and access to banking and non-banking services. In short, the country has to speed up these structural reforms in order to shift from a relatively low-salary and labour-intensive economy to one of knowledge and technology. 2.1.5 Cognizant of these obstacles and challenges, the Government, within the framework of “Tunisia Vision 2016”, adopted in January 2007 a development strategy for the period 2007-2011, known as the 11th Development Plan (2007-2011). The plan is intended to deepen reforms and speed up the pace of its main thrusts: (i) consolidation of the economy’s stability and boosting of its integration into global channels with the aim of improving its capacity and accelerating growth; (ii) establishment of the foundation for comprehensive development; (iii) modernization of the economic fabric by opting for a knowledge- based economy; (iv) boosting the investment in human capital; and (vi) adoption of sector policies that respond best to the demands of modernization and diversification of the economy. The Plan envisages achievement of an annual growth rate of 6.1% and maintaining inflation at a rate of 3%. In qualitative terms, the 11th Plan proposes to increase the per capita income from 4,555 dinars to 6,000 dinars and to bring down by a point the current unemployment rate of about 14%. The Plan also envisages the construction of structural megaprojects (ports, airport, refinery, new tourist resorts, electric power plants, cement plants, highways, technopoles, etc). 2.2. Recent Economic Developments, Outlook and Constraints

2.2.1 Recent macro-economic trends 2007-2008: Despite the Government’s efforts, and after over a year of implementing the 11th Plan, it seems to have some difficulty achieving the average growth target considered necessary to reduce unemployment within the context of rising raw material and food prices in the first half of 2008 and the intensification of the economic crisis in the second half of the same year. Even though the 2007 real growth rate of 6.3% was above the required average rate of 6.1%, growth in 2008 (4.5%) was affected by the recessive effects of the crisis and was below the required level. From 2007 to the first half of 2008, emphasis was laid on curbing inflation (averaging 6% during the first half of 2008 as against 3.1% in 2007). As a result of the inflationary pressures, the Central Bank had to raise its legal reserve ratio and increase the money market rate up to mid-2008.

4

Table 2: Adjusted Medium-Term Macro-Economic Objectives, 2009-2011 2008 2009 2010 2011 Est. Obj. Obj. Obj. GDP (constant prices) % var.

4.5 4.5* 5.5* 6.0*

Deflator % var. 4.5 3.0* 3.0* 3.0* Investment(FBCF) % var.

6.5 3.0 7.9 6.1

Final consumption % var.

5.0 5.0 5.2 5.3

Export of goods & services % var.

14.1 1.5 0.1 7.9

Current ext. deficit (% GDP)

4.4 3.4 3.1 3.0

Budget deficit (% GDP)

3.0 3.0* 3.0* 3.0*

Outstanding public debt (% GDP)

51.7 51.8 51.0 49.6

Assumptions 2009-2011: Max. price/barrel of oil: $90; Growth rate. Euro zone: -2% (2009) and 1% (2010).*Adjusted objectives – Letter of Development Policy.

Following the drop in oil and food prices in the second half of 2008, the inflation rate dropped to 5% by the end of 2008. In terms of budget policy, the focus has been on more effective revenue mobilization (83% of public resources are generated from tax revenue) which has helped to offset the increased spending, resulting in a slightly higher budget deficit (3.0% in 2008 compared with 2.9 in 2007). This spending policy resulted in a 4% increase in salaries, 159% increase in compensation expenditure3 (General Compensation Fund, oil and transport subsidies) and a 6% rise in capital expenditure, driving domestic demand up by 6.5%. The budget deficit was mainly financed by BTAs. This dynamic and prudent public debt management enabled a quasi-stabilization of the public debt ratio (51.7% in 2008 compared with 51% in 2007). Externally, the current account deteriorated (4.4% in 2008 compared with 2.6% in 2007) due to rising import costs and declining export growth. Financing of the current account deficit was covered by FDI inflows (DT 3.1 million in 2008 compared to DT 2.0 million in 2007) and gross foreign exchange reserves fell from 4.2 months of imports (US$8.8 million) in 2008 compared with 4.5 months of imports in 2007. The banking sector was barely affected by the crisis given its limited capacity to borrow externally, as it is not authorized to invest in foreign stock markets and benefits from the foreign exchange controls in force. There is, however, a high level of non-performing loans (17.6% in 2008) and a low level of provisioning of such loans (53.4%) (See details of impact of crisis in Technical Annex 4). 2.2.2 Government’s response to the crisis during last half of 2008: MTEF 2009-2011, 2009 Budget and Presidential Measures: During the second half of 2008, the Government adopted an ambitious general MTEF (2009-2011) (Annex IVa), the 2009 Finance Law and Presidential measures to deal with the crisis. The authorities sought to make the objectives of the MTEF and budget forecasts relating to the global economic crisis dependent on the national economy. 2.2.3 Given the context of the worsening crisis, the medium-term growth targets were adjusted downwards. Consequently, the adjusted growth targets are 4.5 % instead of 5.0% in 2009 and 5.5% instead of 6.2% in 2010 (Table 2, Annex I and Annex IVb). The inflation is expected to level off to an average of 3% from 2009 to 2011. Given the slowdown in the pace of export growth, investments and consumption will continue to drive growth in 2009 and 2010. Consumption is sustained by the salary increase (average of 4.0%) and continued compensation measures and expenditure. The 2009 Finance Law has adopted a counter-cyclical budgetary policy. The budget has gone up by 12.6% compared to the 2008 Finance Law (DT 15.2 million). The objective of the economic budget is to strengthen economic development, improve the business environment, pursue job creation and mitigate the social effects of the crisis. Special importance is given in the budget and the presidential measures to 3 Compensation expenditure increased from DT 554 million in 2004 to DT 1281 million in 2007 and DT 2036 million in 2008.

5

creating enabling conditions for the growth of export companies and to enhanced protection of such companies from the effects of the crisis (Technical Annex 5). A number of structural measures are also envisaged. The Central Bank has relaxed its monetary policy, as well as that of foreign exchange for export companies. A Crisis Monitoring Committee has been set up. 2.2.4 Macro-economic stability seems far from being achieved given the global crisis context. In order to achieve the 6% growth target and reduce the unemployment rate in the medium-term, the economy’s resistance to external shocks must be consolidated and the Government needs sustained support to overcome the current difficulties and prepare the Tunisian economy for the future. This implies bolstering macro-economic stability and pursing the reforms, particularly by reducing transaction costs and deepening trade integration, improving the investment climate and facilitating access to financing. Lastly, it is worth indicating that Tunisia does not have a reform programme with the IMF. The mission conducted by the IMF staff team in June 2008, for the Article IV Consultation, confirmed the sound economic and social management of the country, but also underscored the need to pursue the structural reforms (See Annex III).

2.3 Status of Bank Portfolio 2.3.1 As at 16 January 2009, the Bank’s portfolio comprised 10 projects with net commitments of UA 669, including 24% from the OPSM window. Currently, it does not contain any reform programme. With an overall rating of 2.7 points out of 3 in 2008, compared to 2.53 in 2005, the portfolio’s performance is very satisfactory. It is among the Bank’s best, and does not have any project-at-risk. It is performing well due to the Bank’s increased monitoring of its operations, as well as better knowledge of project management.

III. JUSTIFICATION, KEY DESIGN ELEMENTS AND SUSTAINABILITY 3.1 Link with CSP, Country Readiness Assessment and Underlying Analytical Factors 3.1.1 Links with CSP: The PAI is in line with CSP 2007- 2011, which takes account of the priorities of the 11th Plan. It contributes to the CSP’s first pillar of “reinforcement of macro-economic policies and acceleration of structural reforms” and the second pillar, “modernization of infrastructure and consolidation of the productive sector”. The Programme was contained in the request submitted by the Government in January 2008. 3.1.2 Prerequisites for Implementation of General Budget Support: The general and technical prerequisites for the implementation of a general budget support programme have been met. In terms of the general prerequisites, the political situation in Tunisia is stable and the general elections slated for 2009 are not expected to disrupt this stability. Even though the macro-economic situation has been recently affected by external factors, it is still viable, and is expected to rally with the implementation of the MTEF. The Government’s commitment appears tangible and irrevocable. It considers the PAI to be an operation that will allow it to implement the 11th Plan. The PAI was formulated using a participatory approach, and there was consensus on it within Government. At the technical level, there is, through the 11th Plan, a development programme that is relatively well prepared and formulated using a satisfactory participatory approach. The country’s principal partners consider it credible and relevant, and have undertaken to support it in the medium-term. Furthermore, the country has quality institutional capacity. The Ministry of Development and International Cooperation (MDCI), responsible for

6

coordination of the PAI, and the Ministries involved in the implementation of the PAI have competent human resources to ensure implementation and monitoring of the Programme. In addition, the PAI benefits from excellent cooperation and collaboration among the partners (the Bank, the World Bank and European Commission) (see section 3.2.) as well as between the Government and the partners. Owing to the unavailability of a recent assessment of public finance management, CFAA 2004 served as a reference point (Annex V). It shows that even at that time, the Tunisian public expenditure system was assigned a low budgetary and financial risk factor4. Public finance management reforms have continued since 2004, and the country has adopted a goal-oriented budget approach. The audited budget is generally produced within 6 months each year. It is comprehensive and of good quality. The aim is to present it at the same time as the Finance Law. It could be considered that the institutional, legislative and legal framework of public finance is of good quality and, on the whole, provides highly satisfactory assurance of reliability and transparency. Given the quality of governance, measured by the Country Policy and Institutional Assessment (CPIA) 2007 (above 3 over the past five years), there is very little risk of reversibility of the reforms. A PEFA is planned for 2009. 3.1.3 Analytic Work: The programme design has a solid analytical underpinning due to the existence of several recent work covering intervention strategies and various targeted areas for support carried out by the Bank, other partners and the Government. This has contributed to good ownership and formulation of the Programme. Table 3 below gives an idea of the key analytic work.

Table 3 Key Analytic Work Used

Strategy/Areas of Reform Analytic Work Institutions Status Strategy CSP 2007-2011

11th Development Plan CAS 2004-2008

ADB Government WB

Completed Completed Completed

Macro-economic Framework Article IV 2007 and 2008 World Development Outlook Nov 2008-February 2009 CFAA 2004 MTEF 2009-2011-Budget 2009 Employment PSEW 2008

IMF IMF EC/WB Government WB

Completed Completed Completed Completed Completed

Trade Integration Global Integration Study 2008 Business Competitiveness Studies 2006 Africa Competitiveness Study 2006 11th Development Plan

WB FIAS/WB ADB/WB Government

Completed Completed Completed Completed

Business Environment Competitiveness Study 2007 Competitiveness Study 2006 Doing Business 2008 et 2009 Completion Reports PAC I, II and III Africa Competitiveness Study 2006

ADB IEQ-Tunisie WB ADB/WB/EC ADB/WB

Completed Completed Completed Completed Completed

Financial Sector Study on SICARs 2008 BTS Study on Micro-Projects 2006 Completion Reports PAC I, II and III

EC WB ADB/WB/EC

Completed Completed Completed

WB: World Bank; EC: European Commission; IEQ: Institute of Quantitative Studies

4 On a risk assessment scale of 4 levels: low (4), average (3), significant (2) very high (1).

7

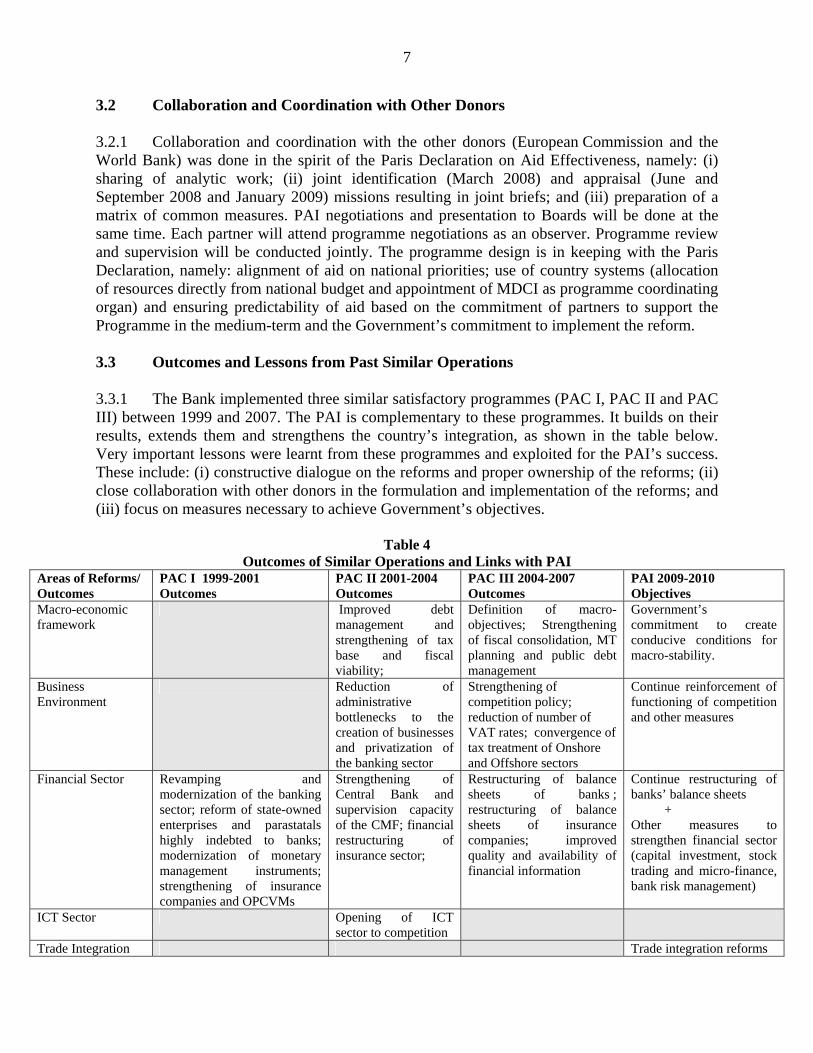

3.2 Collaboration and Coordination with Other Donors 3.2.1 Collaboration and coordination with the other donors (European Commission and the World Bank) was done in the spirit of the Paris Declaration on Aid Effectiveness, namely: (i) sharing of analytic work; (ii) joint identification (March 2008) and appraisal (June and September 2008 and January 2009) missions resulting in joint briefs; and (iii) preparation of a matrix of common measures. PAI negotiations and presentation to Boards will be done at the same time. Each partner will attend programme negotiations as an observer. Programme review and supervision will be conducted jointly. The programme design is in keeping with the Paris Declaration, namely: alignment of aid on national priorities; use of country systems (allocation of resources directly from national budget and appointment of MDCI as programme coordinating organ) and ensuring predictability of aid based on the commitment of partners to support the Programme in the medium-term and the Government’s commitment to implement the reform. 3.3 Outcomes and Lessons from Past Similar Operations 3.3.1 The Bank implemented three similar satisfactory programmes (PAC I, PAC II and PAC III) between 1999 and 2007. The PAI is complementary to these programmes. It builds on their results, extends them and strengthens the country’s integration, as shown in the table below. Very important lessons were learnt from these programmes and exploited for the PAI’s success. These include: (i) constructive dialogue on the reforms and proper ownership of the reforms; (ii) close collaboration with other donors in the formulation and implementation of the reforms; and (iii) focus on measures necessary to achieve Government’s objectives.

Table 4 Outcomes of Similar Operations and Links with PAI

Areas of Reforms/ Outcomes

PAC I 1999-2001 Outcomes

PAC II 2001-2004 Outcomes

PAC III 2004-2007 Outcomes

PAI 2009-2010 Objectives

Macro-economic framework

Improved debt management and strengthening of tax base and fiscal viability;

Definition of macro-objectives; Strengthening of fiscal consolidation, MT planning and public debt management

Government’s commitment to create conducive conditions for macro-stability.

Business Environment

Reduction of administrative bottlenecks to the creation of businesses and privatization of the banking sector

Strengthening of competition policy; reduction of number of VAT rates; convergence of tax treatment of Onshore and Offshore sectors

Continue reinforcement of functioning of competition and other measures

Financial Sector Revamping and modernization of the banking sector; reform of state-owned enterprises and parastatals highly indebted to banks; modernization of monetary management instruments; strengthening of insurance companies and OPCVMs

Strengthening of Central Bank and supervision capacity of the CMF; financial restructuring of insurance sector;

Restructuring of balance sheets of banks ; restructuring of balance sheets of insurance companies; improved quality and availability of financial information

Continue restructuring of banks’ balance sheets + Other measures to strengthen financial sector (capital investment, stock trading and micro-finance, bank risk management)

ICT Sector Opening of ICT sector to competition

Trade Integration Trade integration reforms

8

3.4 Relationship with other Bank Operations 3.4.1 The objective, through the PAI, which aims at macro-economic stability, trade integration and improvement of the financial sector and business environment, is to build a platform of structural reforms that will contribute to the success of the other operations of the Government’s programme. To support the PAI, a number of studies proposed by the co-financiers is being discussed with the Government. Concerning services, a study on the strategic positioning of the chartered accountancy profession is being conducted by the Bank from FAPA resources. This study is intended to carry out a diagnosis of this sector and the formulation of a strategy to promote the sector, and forms part of the service component of the PAI. A PEFA is scheduled for 2009. The Bank is also participating in the financing of the Enfidha airport. 3.5 Bank’s Comparative Advantages 3.5.1 The Bank’s value added in this operation lies mainly in the experience and lessons drawn from this type of support after the three previous programmes of support to competitiveness, for which completion reports were prepared. These lessons and experiences, which were shared with the co-financiers, were judiciously used in this Programme. In addition, the Bank has mobilized expertise for the financial sector and trade reforms. 3.6 Application of Good Practice Principles on Conditionality 3.6.1 Good practice principles on conditionality, particularly those relating to ownership, coordinated accountability framework and the adaptation of this framework to the context, choice of disbursement conditions necessary for achieving results, and the predictability of the financial support were taken into account in the formulation of the PAI. The details are given in Annex VI. IV. PROPOSED PROGRAMME 4.1 Programme Goal and Objective 4.1.1 The goal of the Integration Support Project (PAI) is to boost growth and employment in line with the objectives of the 11th Plan (2007-2011). The programme’s specific objective is to foster better integration into the global economy. 4.2 Programme Pillars, Operational Objectives and Expected Outcomes 4.2.1 In the light of the country’s developmental challenges, the Government’s programme priorities and CSP 2007-2011, the Programme, which is based on the assumption of a stable macro-economic environment, has the following objectives: (i) reduce transaction costs and deepen trade integration, (ii) improve access to bank and non-bank financing, and (iii) improve the business environment. The Programme measures are presented in the Matrix of Measures in Annex II.

9

Programme Underpinnings: A Stable and Conducive Macro-economic Framework 4.2.2 Maintaining a stable and conducive macro-economic environment is key to the programme implementation. A series of key indicators, showing the macro-economic trends in 2009-2010 and updated in line with the MTEF objectives, was agreed in early 2009 and will be monitored regularly (see Annex IVb). Interpretation of possible gaps between the outputs and reference indicators will take into account the influence of factors beyond the control of the authorities. OBJECTIVE 1: REDUCE TRANSACTION COSTS AND DEEPEN TRADE INTEGRATION 4.2.3 The Integration Support Programme (PAI) reforms aim at deepening integration in the goods trade, enhancing facilitation of the service trade and the efficiency of trade logistic services, and promoting service exports. The trade reforms proposed are the unilateral type. 4.2.4 Objective 1a: Deepen integration in the goods trade. Context and Challenges: Customs duties levied on industrial goods from the EU are 0%, and that for non-preferred partners (“most favoured nation” tariffs) is around 24.7%. This tariff gap artificially favours goods from the preferred countries to the detriment of cheaper goods from third countries; it further limits the goods trade with non-EU countries, which offers stronger growth potential than in the Euro zone. Moreover, institutional and regulatory discrepancies in the norms and standards of the quality of goods between Tunisia, on one hand, and between Europe and other trading partners, on the other, were identified as major obstacles to the goods trade. There is, therefore, need to continue to simplify tariffs and reinforce the convergence of standards and norms for goods. 4.2.5 Recent Actions: The Government recently reduced the number of tariff bands from 54 to 9, leading to a 10-point drop in average tariff and also a reduction in the average common customs tariff, from 31% to 21.7% from 2006 to 2008. Several other external trade facilitation and normative and regulatory convergence measures were taken, including the introduction of the electronic administration of trade procedures (Tunisie Trade Net), simplification of customs procedures, and technical control and access to information on international norms and standards. 4.2.6 Programme Measures: The Government intends to adopt a two-pronged approach to deepening integration of the goods trade. First, it will pursue simplification of the tariff structure by: (i) implementing before the end of February 2009, the 2009 Audited Budget Law amending the customs tariff regime, by reducing the number of customs tariff rates from 9 to 6, including the “zero” tariff rate; and (ii) implementing the Finance Law for 2010, to amend the customs tariff system by reducing the number of customs tariff rates from 6 to 5, including the “zero” tariff rate. Secondly, the Government will ensure regulatory and normative convergence between Tunisia, the EU and other trade partners. To this end, by the end of February 2009, the Inter-Ministerial Council (CI) will adopt: (iii) a bill on standards and norms applicable to all goods imported into or used in Tunisia, in compliance with best international practices; and two other bills on: (iv) food security, and (v) security of industrial goods. In 2010, the Government

10

will: (vi) set up a quality control and food security agency, and (vii) transform half the existing compulsory norms into voluntary ones. Measures (i) and (iii) will be conditions precedent to submission of the Programme to the Boards. Measure (ii) will be a condition for disbursement of the second tranche of the loan. 4.2.7 Expected Outcomes: (i) The tariff structure is simplified and the average common customs tariff is reduced in 2009 and 2010; (ii) quality norms and standards for food items and industrial goods are improved and converge with those of Europe and other trading partners in 2009 and 2010. Details of the output indicators are given in the Matrix of Measures in Annex I and the Logical Framework Matrix on page vii. 4.2.8 Objective 1b: Enhance trade facilitation and efficiency of trade logistic services. Context and Challenges: Despite efforts by Government, trade procedures (documents and information needed for imports, non-tariff measures, rules governing the technical control of imports) are not well-known. While the country has made giant strides in terms of logistics, it still faces constraints that increase time and logistics costs. These include the absence of logistics centres and modern warehouses and the poor service quality of certain operators as well as the lack of a deep-sea port. It is therefore necessary to facilitate trade procedures, reduce port passage costs and time and facilitate international logistics procedures. 4.2.9 Recent Actions: The Government has prepared a new Customs Code which came into force this year, and set up a one-stop shop at Rades for import controls, although this is not yet functional. Rades is Tunisia’s largest port, with container traffic accounting for 90% of its operations, and maritime traffic, 22%. The Presidential measures taken in December 2008 include making this one-stop shop operational. The authorities have also stepped up measures to reduce the stay in port for goods by easing customs procedures. There are plans to build a deep-sea port and an airport at Enfidha, which is at an advanced stage. 4.2.10 Programme Measures: The Government intends to enhance the efficiency of trade logistics services by intervening in three areas. It has been agreed that, first, trade procedures should be facilitated through the following measures in 2009: (i) draw up and publish a list of non-tariff measures in accordance with ITC classification (including technical control measures); (ii) post on the Customs website, customs tariffs and all information and documents required for imports; (iii) adopt a decree to complement the provisions of decree 94-1744 of 29 August 1994 on technical control, with a view to (a) spelling out the modalities and factors justifying sampling and analysis for list A, B, and C products and (b) introducing an effective mechanism for recourse, in the event of non-compliance, to give the option to submit said products for testing by another laboratory that meets international standards (including private laboratories). In 2010, (iv) complete the inter-connection of all technical control services at Tunisie Trade Net; (v) set up a selective import control management system that allows for prioritizing checks on risky products and operators and conducting faster controls for non-risky products and operators; and (vi) update the list of non-tariff measures. Following this, port passage costs and times should be reduced in 2010 by (vii) making the Rades one-stop shop operational and establishing the “liasse de transport” (transport bundling) system, which integrates and electronically connects all operators on the transport chain and (viii) revising the port dues and charges scale. Lastly, the authorities intend to facilitate international logistics operations for exporters and service

11

providers by (ix) laying down criteria for access to intermediary professions, such as freight-forwarders in 2009; in 2010 (x) setting up a regulatory framework for the creation and operation of logistical activity zones; and (xi) enhancing transparency and cutting back on time by abolishing manual cargo monitoring and setting up a GPS tracking system. Measures (v) and (vii) will be conditions for disbursement of the second tranche of the loan. 4.2.11 Expected Outcomes (Impacts): (i) Trade procedures are facilitated in 2009 and 2010; (ii) port passage costs and times are reduced in 2009 and 2010; (iii) international logistics operations for exporters and service providers are facilitated in 2009 and 2010. Details of the output indicators are shown in the Matrix of Measures in Annex I and the Logical Framework Matrix (page vii). 4.2.12 Objective 1c: Promote Service Trade. Context and Challenges: Most of the gains to be made in productivity and economic expansion in the coming years will be in the service sector, which is currently under-tapped. In terms of the institutional framework, the service sector is fraught with dispersed responsibilities between ministries and technical agencies, and lacks coordination. The absence of statistics on the service trade makes it impossible to draw up a relevant overall strategy that will help bolster the service sector. It is therefore necessary to put in a place a national framework for the formulation of a sector strategy, coordination of activities and implementation for the revitalization of the service sector. 4.2.13 Recent Action: Liberalization of the sector (transport, telecommunications, legal services, etc.) is ongoing. Several international fairs on service promotion have been organized. 4.2.14 Programme Measures: The Government intends to adopt a two-pronged approach to promoting the export of services. First, it will set up an institutional framework and coordinate services-related operations countrywide. To this end, (i) before the end of February 2009, Decree No. 2006-1826 of 26 June 2006 on the National Services Council (CNS) will be signed so as to: (a) authorize CNS to prepare a services development strategy; (b) formalize the creation of thematic commissions within CNS and (c) strengthen the role of the CNS Permanent Secretariat by setting up a goal-oriented management unit; and (ii) adopt the services development strategy proposed by CNS. Following this, the services development strategy will be implemented. In this respect, the following measures will be taken: (iii) prepare a diagnosis of the regulatory framework in 2009, in the form of sector briefs for sectors with high trade potential (health, services to businesses and professionals, transport, tourism and ICT); and in 2010, (iv) ensure that the CI adopts an action plan, prepared by CNS on the basis of a statutory assessment, to reform and promote the service sector, (v) prepare guidelines for services upgrade; (vi) prepare a common nomenclature of services and (vii) consolidate and publish on the Internet, for service sectors with strong potential for trade, (a) statistics on trade and FDIs and (b) legislation and regulations applicable to investment and trade. Measure (i) will be a condition precedent to submission of the Programme to the Boards. Measure (iv) will be a condition for disbursement of the second tranche of the loan.

12

4.2.15 Expected Outcomes: (i) CNS is set up and services-related operations are coordinated countrywide in 2009 and 2010; (ii) an action plan for the development of services is proposed by CNS, adopted and implemented in 2010. Details of the output indicators are shown in the Matrix of Measures in Annex I and the Logical Framework Matrix on page vii. OBJECTIVE 2: IMPROVED BUSINESS ENVIRONMENT 4.2.16 Tunisia’s investment climate has witnessed significant improvement in recent years, with very positive FDI trends (See Technical Annex I). For instance, the country moved up eight points in the “Doing Business 2009” ranking from 81st in 2007 to 73rd position in 2008. These efforts should be sustained. The PAI will focus on improving the administrative mechanisms governing the establishment and activities of businesses, and enhancing market competition and transparency. 4.2.17 Objective 2a – Improve administrative mechanisms governing the establishment and activities of businesses. Context and Challenges: Under the previous programmes (PAC II and III), Tunisia had embarked on improving the administrative mechanisms governing the establishment and activities of businesses under a reform process. These include, simplifying procedures for establishing a company. Despite the 31-point improvement in the Doing Business 2009 ranking for business registration in 2008, administrative authorizations are still required for permits to be granted; this increases delay. The companies have several identifiers. The Companies Register needs updating. Lastly, there are long delays in the appropriation of industrial land. There is thus the need to continue improving the administrative mechanisms governing the establishment and activities of businesses. 4.2.18 Recent Actions: The Government has also made efforts to reduce administrative authorizations. Indeed, 222 authorizations have been cancelled and 221 replaced by 185 specifications, some of which have been revised. There are currently only 96 authorizations, some of which will be changed into specifications. 4.2.19 Programme Measures: A two-pronged approach will be used to improve the mechanisms governing administrative activities. The authorities hope to simplify the modalities for establishing businesses by: (i) conducting an impact assessment in 2009 on the abolition of administrative authorizations and revision of the specifications on business registration and employment in the sectors concerned; (ii) adoption by the CI, before the end of February 2009, of a bill amending the Regional Planning and Urban Development Code, so as to reduce the time required by businesses to purchase industrial land; (iii) signing in 2010, a decree that reduces by half the number of activities for which operators are required to obtain prior authorization before commencement of activities; and (iv) obtaining in 2010, the opinion of the Competition Council on the specifications drawn up before 2005. With a view to improving the system of information on companies, three measures will be taken: (v) the CI’s adoption, before end February 2009, of a bill amending Law 95-44 of May 1995 on the Trade Register, to update the information contained therein; in 2010 (vi) putting online the Trade Register listing a significant number of businesses, with updated data and (vii) adopting a plan to introduce a single identifier for economic operators at the INS, CNSS, Customs and the Tax office, based on the recommendations of a study to be conducted by the World Bank. Measures (ii) and (v) will be conditions precedent to the presentation of the Programme to the Boards. Measures (iii) and (vii) will be conditions for the disbursement of the second loan tranche.

13

4.2.20 Expected Outcomes (Impacts): (i) The modalities for the registration and running of companies are improved in 2009 and 2010; (ii) time for granting industrial land is reduced in 2009 and 2010. The details of the output indicators can be found in the Matrix of Measures in Annex I and the Logical Framework Matrix on Page vii. 4.2.21 Objective 2b – Improve competition and market transparency. Context and Challenges: Poor application of statutory texts on competition appears to be the main constraint. The Competition Council (CC), an autonomous judicial institution and the Competition Directorate (DGC), has complained about the inadequate staffing and the poor knowledge of legislation by the business community and the general public. The Company Code needs to be amended to enable minority shareholders to have access to information, and sue in a court of law while risky operations also need to be controlled. Combating counterfeiting also constitutes a weak link in the competition chain. There is need to enhance the roles of the CC and the DGC, and intensify counterfeit control and market transparency. 4.2.22 Recent Actions: In 2006, the legislative and regulatory framework of competition in Tunisia underwent reform under PAC III with the strengthening of the role of the Competition Council, followed by its administrative and financial autonomy and the obligation to request its opinion on texts other than laws. These actions must be pursued. Revisions of the Company Code and the Trade Register are on the agenda. 4.2.23 Programme Measures: The authorities intend to improve the practice of competition in two ways. Initially, they will strengthen the role of the CC and the DGC through: (i) referral to the CC, by the authorities, for analysis the regulations and conduct of stakeholders in two economically significant service sectors in 2009; (ii) referral to the CC in 2010 by sector ministries concerned for a statutory assessment of competition between companies in at least two additional sectors; and (iii) increase in the CC and DGC staff and increased resources to step up activities to promote the culture of competition in 2009 and 2010. Lastly, counterfeiting controls will be tightened. To this end, in 2009, the authorities will: (iv) set up the National Anti-Counterfeiting Committee (CNAC), comprising all personnel responsible for the control and finding of offences, as provided by Law 2007-50 of 23 July 2007; and (v) adopt and implement in 2010, CNAC’s anti-counterfeiting programme for all services concerned; it will include an information system on referrals and follow-up actions. Lastly, investor protection and transparency of companies will be enhanced through (vi) adoption by Cabinet of the draft amendment of the Company Code and (vii) adoption of the CMF regulation on access to the title register. Measure (ii) will be a condition for disbursement of the second tranche of the loan. 4.2.24 Expected Outcomes (impacts): (i) Application of the laws on competition, and (ii) counterfeiting control are reinforced in 2009 and 2010; (iii) investor protection is enhanced and transparency of companies improved. Details of the performance indicators are shown in the Matrix of Measures in Annex I and the Logical Framework Matrix (page vii). 4.2.25 Objective 2c – Improve information on the regulatory framework for better convergence of supply and demand of labour. Context and Challenges: The ultimate objective of the integration policies is to reduce unemployment. The unemployment rate in

14

Tunisia has dropped in the last five years to 14% - still considered high by the authorities. Unemployment among young graduates is an important issue which is tied to the lack of convergence between the supply and demand of employment. Available studies, including those by Doing Business 2009 spell out the rigidity of the job market as an obstacle to job creation and investment. Temporary employment is not regulated. Besides, business and workers alike have very little knowledge of the Labour Code. It is necessary to improve information on work regulation and enhance convergence between supply and demand. 4.2.26 Recent Actions: In 2007, the Government embarked on reform of the labour policy geared toward the categories that encounter special difficulties in integrating professional life. There is, for instance, the programme aimed at improving the quality of services of employment offices to bring them up to par with international standards and thereby building their capacities to facilitate the integration of job seekers into professional life. 4.2.27 Programme Measures: The authorities intend to improve information on the regulatory framework to enhance the convergence of employment supply and demand by: (i) preparing a guide on labour laws in 2009 for businesses to improve their knowledge of the laws; (ii) conducting a study in 2010 on the application of dismissal procedures and rigidity in dismissals; this study will include an international comparative assessment; and (iii) in 2010, revising Articles 28, 29 and 30 of the Labour Code and adding articles 31 and 32 on the regulation of temporary employment agencies and submitting them to social partners. 4.2.28 Expected Outcomes (effects): (i) A guide on labour regulations is available in 2009; (ii) the Labour Code is revised to better reflect the convergence of employment supply and demand, and regulation on temporary employment. The details of performance indicators are shown in the Matrix of Measures in Annex I and the Logical Framework Matrix on page vii. OBJECTIVE 3: IMPROVE ACCESS TO FINANCING 4.2.29 Better integration calls for better access to financing5, including a competitive financial sector. To this end, it was agreed, under the programme, to improve performance and risk management in the banking sector to encourage the development of investment capital, strengthen the depth and liquidity of the Tunis Stock Exchange, and develop the micro-finance sector. 4.2.30 Objective 3a. Improve performance and risk management in the banking sector. Context and Challenges : The efficiency and competitiveness of the banking system necessarily depends on the quality of the portfolio, namely, reduction in the burden of non-performing loans in total commitments (17.6% in 2007) and better provisioning of non-performing loans (53.2% in 2007). The classified debt burden remains high and well beyond the level of that of emerging countries with similar incomes. Moreover, a good guarantee system facilitates access to credit. The compensation and pricing system of SOTUGAR, a surety company, is complex and inappropriate. It is important to pursue bank consolidation, tighten the rules of prudential management and address SOTUGAR’s shortcomings.

5 For the record, Tunisia’s ranking for obtaining a loan is 84 out of 181 countries (Doing Business 2009), which is below the

average performance of 73 out of 181 countries.

15

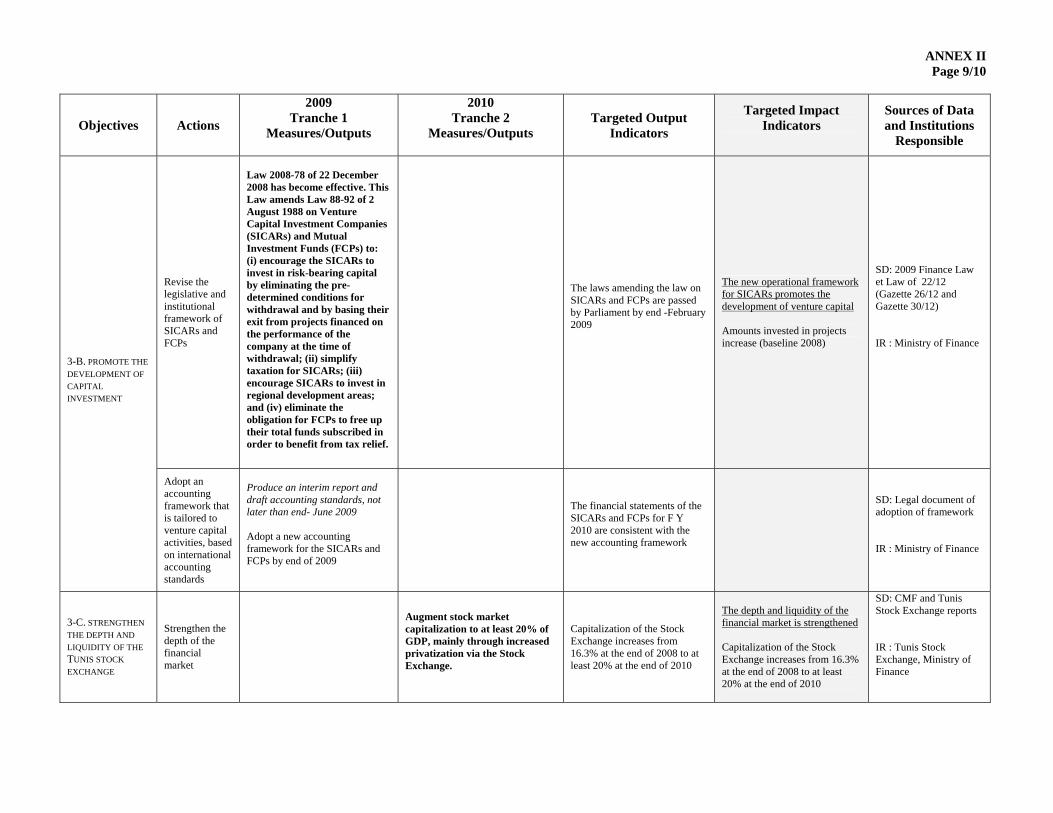

4.2.31 Recent Actions: It should be noted that the 2007 aggregates stated above are the outcome of efforts made by the Banks, which were encouraged by the Central Bank of Tunisia (BCT) since 2005 to reduce the rate of non-performing loans and increase the provisioning rate, which stood at 20.9% and 46.6% respectively during the period. These actions were sustained under PAC III. 4.2.32 Programme Measures: This entails adopting a two-pronged approach to improving performance and risk management in the banking sector. BCT will continue consolidating the portfolio of banks by (i) reducing the non-performing loan rates and the provisioning rates of such loans, showing a 15% drop for the former and a 70% rise for the latter. It will also tighten the rules of prudential management by banks by (ii) assessing the impact of circular 2006/19 on bank internal audits in 2010. Lastly, the measures entail modifying the compensation system and the rate-setting policy of SOTUGAR by (iii) carrying out an assessment of SOTUGAR’s compensation system and rate-setting policy in 2009 and (iv) in 2010, adopting an action plan for implementing the conclusions of the assessment, with a view to improving SOTUGAR’s operations. Measure (i) will be a condition for disbursement of the second tranche of the loan. 4.2.33 Expected Outcomes (Impacts): (i) Portfolio of banks is reorganized in 2010; (ii) prudential management rules of banks are tightened in 2010; (iii) SOTUGAR’s compensation system and rate-setting policy are improved in 2010. Details of performance indicators are shown in the Matrix of Measures in Annex I and the Logical Framework Matrix on page vii). 4.2.34 Objective 3b. Promote development of capital investment. Context and Challenges: Capital investment does not play a major role in investment financing in Tunisia. Nearly all operations take place in the form of on-lending contracts of equity capital to the project promoter and in the form of nominee contracts, which could be likened to credit operations. Mutual investment funds, dominated by compulsory mutual investment funds, are currently unattractive. Flaws in the institutional and legislative framework and even the accounting framework are perceived as barriers to stimulating this financial instrument. Capital investment is worth promoting. 4.2.35 Recent Actions: In a bid to improve capital investment operations in Tunisia, the Government of Tunisia recently undertook some measures, which include making it possible for SICAR to resort to SOTUGAR guarantee and the creation of legal structures that are consistent with international practices such as the seed fund and the Mutual Investment Fund (FCP). 4.2.36 Programme Measures: The Government plans to take a two-pronged approach to promoting capital investment development. First, the legislative and institutional framework of the SICARs (venture capital investment companies) and the FCPs (mutual investment funds) will be revised by (i) adopting, before end February 2009, law 2008-78 amending law 88-92 of 2 August 1988 on the SICARs and FCPs to (a) encourage the SICARs to invest in risk-bearing capital by basing their conditions for withdrawal from the equity of enterprises on the latter’s performance; (b) simplify taxation for investment companies; (c) encourage the SICARs to invest in regional development areas, and (d) eliminate the obligation on FCPs to free up their total funds subscribed in order to benefit from tax relief. Furthermore, the authorities will adopt

16

an accounting framework that is tailored to venture capital activities, on the basis of international accounting standards. To this end, (ii) they will produce an interim report and draft accounting standards in 2009; and (iii) adopt the new accounting framework for the SICARs and FCPs in 2009. Measure (i) will be a condition precedent to submission of the programme to the Boards. 4.2.37 Expected Outcomes (Impacts): (i) The legislative and institutional framework of the SICARs is revised in 2009; (ii) a new accounting framework tailored to the SICARs and FCPs is adopted in 2009. Details of the output indicators are found in the Matrix of Measures in Annex I and the Logical Framework Matrix on page vii. 4.2.38 Objective 3c. Beef up and increase liquidity of the Tunis Stock Exchange. Context and Challenges: Despite numerous incentive measures, the financial market is too narrow and not dynamic enough to play a significant role in private investment financing. Market capitalization was 15% in 2007 for 51 listed companies, compared to 86% in Morocco. Moreover, the equity market has very little liquidity. International institutions cannot issue bonds. It is important to beef up the financial market and increase liquidity on the bond market. 4.2.39 Recent Actions: The foremost event on the Stock Exchange in 2007 was the start of the alternative market6, which listed companies, particularly SMEs, under softer admission terms, guaranteeing transparency and liquidity, through the intervention of specialized bodies. The other major events of the year were the creation of the first FCP index and diversification of the financing sources of companies through the issue of the first subordinated loans on the bond market. 4.2.40 Programme Measures: This entails increasing the liquidity of the Tunis Stock Exchange. The activities planned are two-fold. First, the depth of the financial market will be strengthened by (i) augmenting stock market capitalization to at least 20% of GDP, through increased privatization via the Stock Exchange. Secondly, the Government hopes to boost the liquidity of the bond market in 2009 by increasing the authorized percentage of Long-term Treasury Bonds (BTA) purchased by foreigners from (ii) 20 to 25% in 2009 and from (iii) 25 to 30% in 2010; (iv) by authorizing international institutions, in 2010, to issue bonds on the Tunisian financial market under the same conditions as for local operators and (v) by producing, in 2010, a mid-term review report of law 2005/96 on financial security. Measure (i) will be a condition for disbursement of the second tranche of the loan. 4.2.41 Expected Outcomes (Impacts): (i) The depth of the financial market is reinforced in 2010 through an increase in stock capital; (ii) liquidity of the bond market is boosted in 2009 and 2010 through increased BTA holdings by foreigners and bond issues by international organizations. Details of the performance indicators are shown in the Matrix of Measures in Annex I and the Logical Framework Matrix on Page vii. 4.2.42 Objective 3d. Develop micro-finance activities. Context and Challenges: In Tunisia, micro-finance is currently confined to a micro-credit dimension, with two operators operating in

6 Ministry of Finance Decree of 24 September 2007, on the amendment to the general regulations on the Tunis Stock Exchange

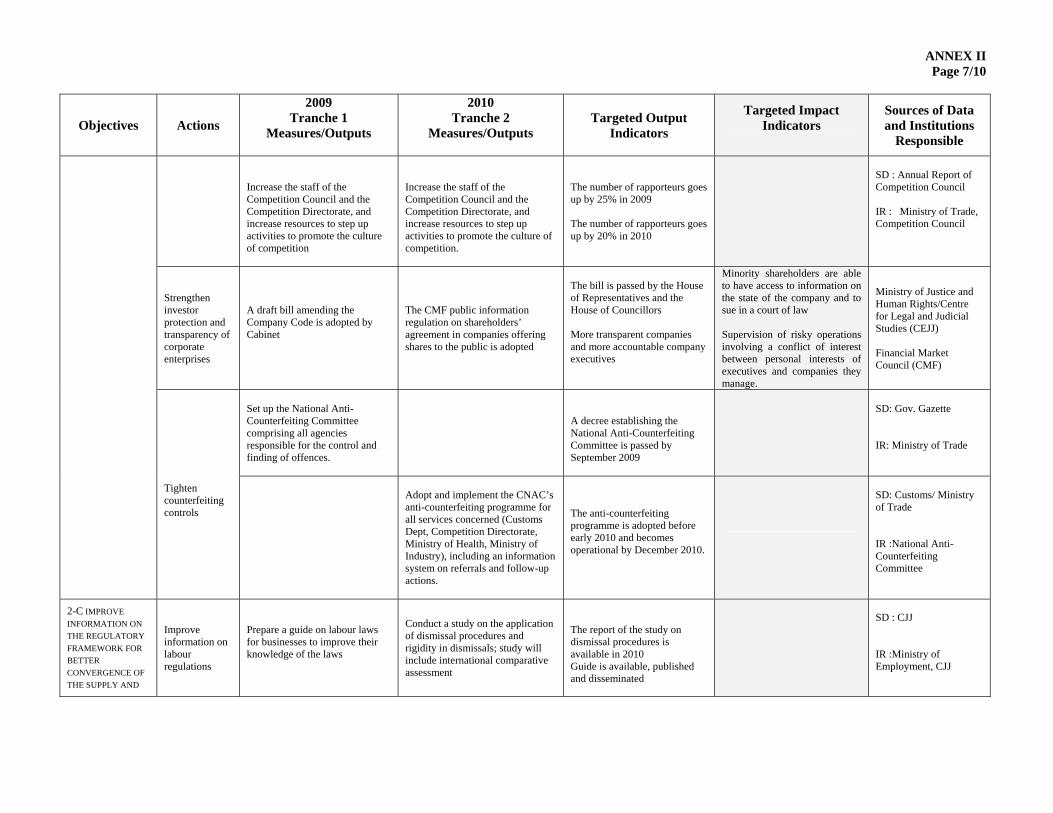

(BCT Annual Report, 2007)

17

the sector, the Banque Tunisienne de Solidarite (BTS) – a public institution – and Enda Inter-Arabes (international NGO). The current regulatory arrangements subject micro-credit activities to restrictions, including putting a ceiling on the credits granted, which today stands at DT 4,000, and an interest rate not exceeding 5% (this does not apply to Enda, which has special exemption). Banking institutions are systematically excluded from engaging in micro-credit activities. Strengthening integration of the financial sector implies streamlining the arrangements organizing micro-finance operations and removing some of the barriers to entering the sector. 4.2.43 Recent Actions: No significant decision has recently been taken to enhance micro-finance in Tunisia. 4.2.44 Programme Measures: The authorities therefore hope to develop micro-finance activities in two areas. First, embark on reform of the micro-finance system by (i) conducting a study in 2009, of the micro-finance market, with a view to identifying conditions for developing the sector, including those pertaining to reform of the legal and regulatory framework and (ii) in 2010, taking institutional and regulatory measures based on the conclusions of the study on micro-finance to boost the market. Secondly, improve the performance of BTS by (iii) launching a study on the performance and impact of the BTS with the Programme partners in 2009 ; (iv) and publishing, in 2010, a progress report on the implementation of the BTS reform action plan drawn up on the basis of the study’s findings. Measure (ii) will be a condition for disbursement of the second loan tranche. 4.2.45 Expected Outcomes (Impacts): (i) A study on the micro-finance sector is published in 2009 and measures taken to revamp the sector; (ii) a report on the performance of the BTS is published in 2009. Details of the performance indicators are shown in the Matrix of Measures in Annex I and the Logical Framework Matrix on page vii. 4.2.46 The Government agreed to implement the following actions prior to presentation of the Programme to the Boards of the Bank Group:

Box 1 Actions Prior to Presentation of PAI to Boards to be Implemented by the end of February 2009

Prior Action 1 : The 2009 Finance Law amending the customs tariff regime by reducing the number of customs

tariff rates from 9 to 6, including the « zero » tariff rate, has become effective (§4.2.6) Prior Action 2 : The CI has adopted the bill on standards and norms applicable to all goods imported into or used

Tunisia, in compliance with best international practices (§ 4.2.6) Prior Action 3 : Decree 2006-1826 of 26 June 2006 on the National Services Council (CNS) to: (a) authorize CNS

to prepare a services development strategy; (b) formalize the creation of thematic commissions within CNS; (c) strengthen the role of the CNS Permanent Secretariat (setting up a goal-oriented management unit) (§ 4.2.14), has been signed.

Prior Action 4 : The CI has adopted the bill amending the Regional Planning and Urban Development Code, in order to reduce the time required by businesses to purchase industrial land (§ 4.2.19)

Prior Action 5 : The CI has adopted a bill amending Law 95-44 of 2 May 1995 on the Trade Register, to update the information contained therein (§ 4.2.19)

Prior Action 6 : Law 2008-78 amending Law 88-92 of 2 August 1988 on the SICARs and FCPs to (a) encourage the SICARs to invest in risk-bearing capital by basing their conditions for withdrawal from the equity of enterprises on the latter’s performance, (b) simplify taxation for investment companies; (c) encourage the SICARS to invest in regional development areas, and (d) eliminate the obligation on FCPs to free up their total funds subscribed in order to benefit from tax relief has been enacted (§ 4.2.36).

18

4.2.47 These prior actions have also been adopted by the World Bank, which will present the programme to its Board in March 2009. The Government will submit to the Bank and the World evidence of the fulfilment these conditions precedent. 4.3. Financing Requirements and Arrangements 4.3.1 As a result of the financial crisis, which has led an increase in the margin applied to loans raised by emerging countries, including Tunisia, and the deterioration of investor confidence, the Government has decided on the prudent management of foreign exchange reserves and did not programme any borrowing on the international financial markets in 2009 as was the case in 2008. As shown in the table below, derived from CDMT 2009-2011, the 2009-2010 financing gap is zero after the financial assistance from the Bank and other partners. The Bank’s financing covers 14.2% of external borrowing in 2009 and 2010. The initial amount was US$ 50 million; it was increased to US$ 250 million, at the Government’s request, in the face of the crisis. The World Bank’s assistance consists of the same amount.

2007 2008 2009 2010 2011 2009-2010Own budget resources 5459,5 6162,3 6468,1 6859,6 7210,5 13327,7Financing requirements and expenditure 6121,1 6914,7 7288,9 7756,7 8182,5 15045,6Balance -661,7 -752,4 -820,8 -897,1 -971,9 -1717,9Net domestic financing 661,7 503,1 868,4 1014,6 1257,4 1882,9Net external financing -212,6 82,3 -146,7 -158,6 -312,3 -305,3 Loans 503,1 520,4 430,7 743,5 817,8 1174,2 Including ADB 84,3 83,3 167,6 World Bank 84,3 83,3 167,6 European Commission grant 22,0 21,0 43,0Repayment 715,7 438,1 577,4 902,1 1130,1 1479,5Privatization and other grants 212,6 167,0 99,1 41,1 26,8 140,3Financing gap 0,0 0,0 0,0 0,0 0,0 0,0 Source of data: Tunisian authorities, ADB, World Bank and European Commission

Exchange rates 02/09/09: UA 1 = DTN 2.0176 UA 1 = $1.49192 UA 1 = EUR 1.16411

Table 5: Financing Requirements and Sources - PAI 2009-2010 (In UA Million)

4.4 Programme Beneficiaries 4.4.1 The final beneficiary of the Programme is the entire Tunisian population. It will benefit from the improved standard of living made possible by the accelerated growth and increased job opportunities. The main intermediate beneficiaries are: (i) the public departments that will receive support from the Programme in the implementation of the 11th Plan, (ii) the private sector, which will have easier access to financial sector and operate in an improved business environment, (iii) the unemployed, who will have increased job opportunities, and (iv) consumers, who will have at their disposal less costly and better quality products and services. 4.5 Impact on Gender 4.5.1 Women account for more than one quarter of the active population and contribute to Tunisia’s rapid development. They form a sizeable labour force in industry and services. They