integrated innovation | the key to sustainable growth ... · integrated innovation: the key to...

TRANSCRIPT

Integrated innovationThe key to sustainable growthGlobal ETF Survey 2016

C ontentsE x ec utive sum m ary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 04

S trategic them es . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 06

P roduct dev elopment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 07

H ot topic: F ocus on macro factors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

Mark et entry . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

ic c s fi a i i fici c a sca . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

D ig ital distrib ution. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

H ot topic: F ocus on mutual fund conv erg ence . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

R egional highlights . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

R eg ional summary : U S . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

R eg ional summary : Europe . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

i a s a Asia-Pacific . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

C onc lusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

K ey c ontac ts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

4 | Integrated innovation: the key to sustainable growth

Executive summary

I n J ul y- A ugust 2 0 1 6 , we interv iewed m ore than 7 0 l eading E T F prom oters, inv estors, m arket m akers and serv ice prov iders across the uro e and sia acific ur sam le includes res ondents at issuers mana in of lobal assets

5Integrated innovation: the key to sustainable growth |

T he ex chang e- traded fund ( ET F ) industry continues to ex tend i s s i ac c a si As A sindustry had enj oy ed a decade of g row th av erag ing 21. 5% per a a as s i ass s a a AU S $ 3. 4t. 1 T his achiev ement is ev en more impressiv e for hav ing b een made ag ainst a b ack drop of unprecedented economic

a a a fi a cia a a i i

c s i ass s c i a icthat industry AuM w ill reach U S $ 6t b y the end of 2020. W e also

c i s ic s a sassi a ac i sa i s ic i s a

underpinned b y the ET F industry ’ s commitment to innov ation. I nnov ation is crucial to ET F ’ s ab ility to meet an ev er g row ing rang e

s a a ac a i a i s s

s a s a s s s a i s sc a ac is ica i s c fi c a i a

i s a is i i c a c is is c a i i i s i s

c a s As i s s i is c i ssia fi s i c i a si i i is

g etting more intense as new prov iders enter the mark et. And the need to inv est in technolog y and compliance is mak ing the ab ility to achiev e scale more v ital than ev er.

is i s a ic s as iparticular importance:

• P c a a c c a i i aw ith prudence and transparency

• a c si a i s s a c ifor scale and ex pansion

• i i a is i i a a i s itechnolog y and inv estor demand

W e see these separate themes as b eing united b y an underly ing i i a i i s a ac ic i s a s i a

i a c i a i i i i s aw e b eliev e they point to a need for many ET F prov iders to dev elop a more integ rated approach to innov ation.

I nteg rated innov ation aims to achiev e b alance among different i a i s s c as a fi a i i a s c a sfi s i c a i i i a as c s i ac i i i s

i i a i a i s ia sto harness the disruptiv e pow er of ET F s across their full rang e of activ ities.

i s is fi i s c a i sc i i s c sfour strateg ic priorities that w ill enab le them to put integ rated innov ation into practice. W e conclude this report b y ex ploring these priorities in g reater detail. T hey are:

• a s s ai a c

• C reativ ity in the search for scale

• a s a c a c s a c a ici

• C ontrol of the dig ital ag enda

T he ET F industry ’ s track record of g row th is compelling . T he fact that so many mutual fund prov iders are entering the mark et is conclusiv e proof of ET F s’ g rav itational pull. B ut conv erg ence b etw een ET F s and other inv estment products also threatens the distinctiv eness that has serv ed the ET F industry so w ell. I f ET F prov iders w ant to not only continue g row ing b ut do so in a w ay that a s a i s s s ai a fi a i i i a ainteg rated approach to innov ation holds the k ey to success.

M att F orstenhausler G l obal and U S Weal th & A sset M anagem ent E T F L eader

L isa K ealy E M E I A Weal th & A sset M anagem ent E T F L eader

J ulie K err sia acific ealth sset ana ement

E T F L eader

1 D ata ex cludes ex chang e traded products ( ET P s) . U nless otherw ise i ica a a a s c

6 | Integrated innovation: The key to sustainable growth

Strategic themes

7Integrated innovation: the key to sustainable growth |

P roduct innov ation only seems to g row in importance as the ET F industry ex pands. P rov iders are arg uab ly more focused on product dev elopment than at any time in the sector’ s history . T he reasons are simple and compelling . P roduct dev elopment is essential for:

• ro th N ew products are v ital to sustaining g row th rates. a s s c s a a a ac ic s s i s a as fi a s

cc ss i a i is ss ia fi i s ic i s

• rofitability I nv estment capab ilities are seen as a k ey driv er of marg in improv ement. T he hig her fees that new and specializ ed products command help to offset pricing pressure on ex isting ET F s.

• ifferentiation a i c asi c fi i a i iss as a i s c i ia i i c aclimb ing fast into second place ( see F ig ure 1) . N ew entrants depend on ey e- catching products to stand out from the c i i c s c s sconv ersations w ith inv estors.

P roduct dev el opm ent

I nnov ation

16%15%

20%

15%

9%10%10%

13%

17%16%

18%

12%

7%8%

15%

12%13%

15%

12%12%

9%8%

15%

10%9%

12%

3%

10%

7% 7%

4%

8%

12%

8%

3%

7%

R ang e ofproducts

B rand/ reputationof promoter

S trateg iesemploy ed

b y products

P rice/ lev el ofmanag ement

fees

D istrib utionchannel access

Q uality ofproducts/ lowtrack ing error

Lev el ofspreads

S iz e ofa fund

2013 2014 2015 2016

What are prom oters f ocusing on in order to dif f erentiate them sel v es f rom others?

0%

5%

10%

15%

20%

25%

i ure hat are romoters focusin on to differentiate themsel es from others?

“ S ocially responsib le inv esting is certainly an area of increasing i a c s a a a ss i sassi s a a a c i iic a ca i ac a i a c

than standard plain v anilla b enchmark s. “

A ndrew W alsh E x e c u t i v e D i r e c t o r , E T F , U B S

8 | Integrated innovation: the key to sustainable growth

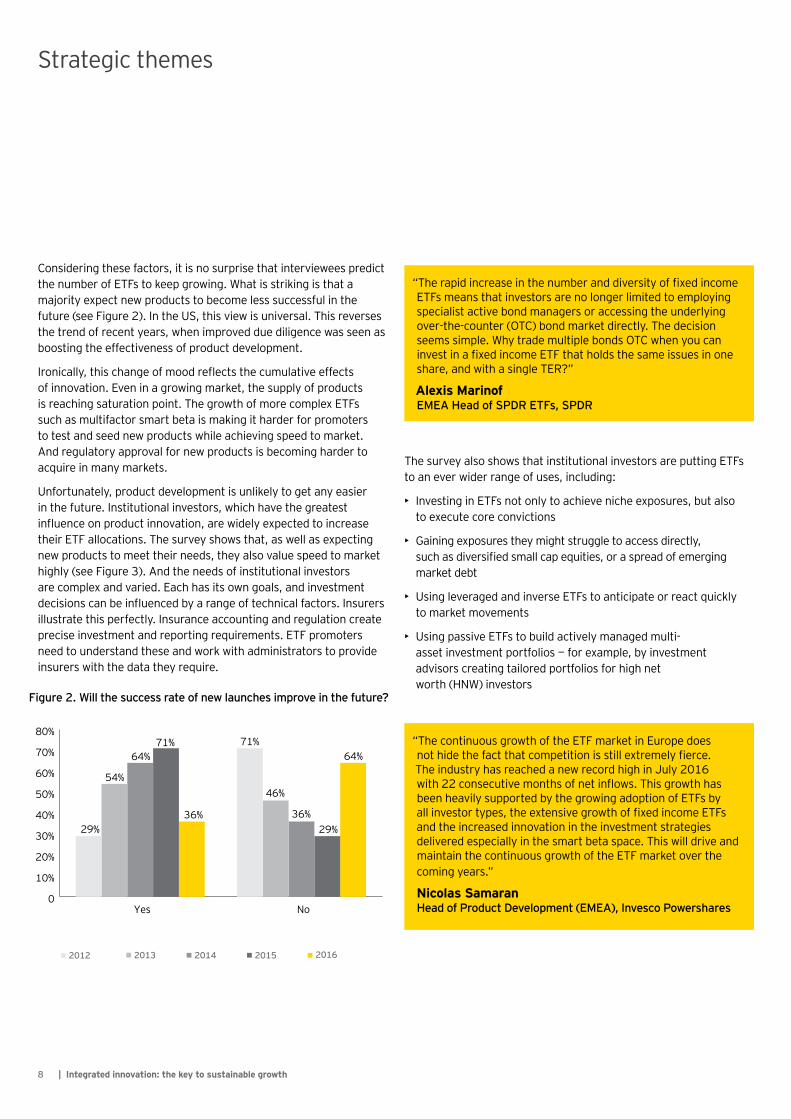

si i s ac s i is s is a i i s icthe numb er of ET F s to k eep g row ing . W hat is strik ing is that a maj ority ex pect new products to b ecome less successful in the

s i is i is i sa is s sc a s i i i c as s as

b oosting the effectiv eness of product dev elopment.

ica is c a c s c a i c si a i i a i a s c s

is reaching saturation point. T he g row th of more complex ET F s such as multifactor smart b eta is mak ing it harder for promoters to test and seed new products w hile achiev ing speed to mark et. And reg ulatory approv al for new products is b ecoming harder to acq uire in many mark ets.

a c is i a asii s i i a i s s ic a a si c c i a i a i c i c as

i a ca i s s s s a as as c ic s i s a s a s a

hig hly ( see F ig ure 3) . And the needs of institutional inv estors a c a a i ac as i s a s a i s

cisi s ca i c a a c ica ac s s sillustrate this perfectly . I nsurance accounting and reg ulation create precise inv estment and reporting req uirements. ET F promoters need to understand these and w ork w ith administrators to prov ide insurers w ith the data they req uire.

T he surv ey also show s that institutional inv estors are putting ET F s a i a s s i c i

• s i i s ac i ic s s a sto ex ecute core conv ictions

• ai i s s i s acc ss i cs c as i sifi s a ca i i s a s a imark et deb t

• U sing lev erag ed and inv erse ET F s to anticipate or react q uick ly to mark et mov ements

• U sing passiv e ET F s to b uild activ ely manag ed multi-ass i s i s a i sadv isors creating tailored portfolios for hig h net w orth ( H N W ) inv estors

i ure ill the success rate of ne launches im ro e in the future?

29%

54%

64%71%

36%

71%

46%

36%29%

64%

Y es N o

2013 2014 20152012 2016

W ill the success rate of new launches improv e in future?

0

10%

20%

30%

40%

50%

60%

70%

80%“ T he continuous g row th of the ET F mark et in Europe does

i ac a c i i is s i fi cT he industry has reached a new record hig h in July 2016

i c s c i s i s is asb een heav ily supported b y the g row ing adoption of ET F s b y a i s s si fi i c sand the increased innov ation in the inv estment strateg ies deliv ered especially in the smart b eta space. T his w ill driv e and maintain the continuous g row th of the ET F mark et ov er the coming y ears. ”

N ic olas S am aran H e a d o f P r o d u c t D e v e l o p m e n t ( E M E A ) , I n v e s c o P o w e r s h a r e s

a i i c as i a i si fi i cET F s means that inv estors are no long er limited to employ ing specialist activ e b ond manag ers or accessing the underly ing ov er- the- counter ( OT C ) b ond mark et directly . T he decision seems simple. W hy trade multiple b onds OT C w hen y ou can i s i a fi i c a s sa iss s is a a i a si

A lex is M arinof E M E A H e a d o f S P D R E T F s , S P D R

S trateg ic themes

9Integrated innovation: the key to sustainable growth |

• s i i -c s s s as aliq uid alternativ e to credit default sw aps. Most respondents ( 75%) see ET F s as an ideal v ehicle to replace certain deriv ativ es.

a ici a s i s s scontinue to pursue new areas of product innov ation. C urrent and

i s a a a s s i a s a i sa c s a a s as s

• i ed income As ic i as s fi i ci a i s i fi s si s

All those surv ey ed in the U S and 85% g lob ally ex pect demand c i i s i a c i i s

i c s i i i fi i c s a

i ure hich factors are critical to the success of ne launches?

D emand forinv estment

strateg y

23%

21%

12%

17%

19%

13% 13% 13%

9%

12%

5%

10%11%

8%

6%5%

2%1% 1%

0%

F irst tomark et

I nnov ation Liq uidity Manag ementfees

S eeding D istrib utionchannel access

P roduct ty pe( sy nthetic

v s. phy sical)

D uedilig ence

Other

2015 2016

Which f actors are critical to the success of new l aunches?

0%

5%

10%

15%

20%

25%

“ W hen allocating to smart b eta strateg ies inv estors should fully understand the methodolog y of the underly ing index .

a a a c s a i ai i a i i a ia c a a

i i c s c i a i ia si ificadisparity in outcomes. ”

C hanc hal S am adder H e a d o f U K & I r e l a n d I n s t i t u t i o n a l E T F S a l e s a t L y x o r A s s e t M a n a g e m e n t , L y x o r

i i ass s ai a ic fi c aS ome respondents admit to concerns ab out the potential for

a i a a a s cia i c s icc s s c as ass - ac s c i a a - as s

( see F ocus on macro factors) .

• mart beta S mart b eta ET F s hav e g enerated the b ulk of new c a c s s a i a ac i s i s

i s s s i a c s a i sifica i a ac s a ac i a a s s a a ic a si i i s s a i i i - i c sP c s a i c asi i a a s a is is

ic sis sc s a a as a fi a s a

si i fi i c s a ia i a as s c as fii c s a a i i sshould outperform conv entional liab ility - w eig hted ones. B ut could

s a a i ca i is s i i sa c c s ac c i c ssi ia c ac

testing and the need to manag e inv estor ex pectations. I t remains to b e seen w hether smart b eta w ill meet the needs of inv estors in all mark et conditions.

• cti e s Activ e ET F s only represent 1% of g lob al ET F assets b ut are seen as a v ery important source of future g row th.

a a ic a a a a c s i a a a aAustralia and are a popular entry point for activ e asset manag ers a c i i fi s c as ac i s a i

a c as i a a a Asia-Pacifica s c a s a s a c i s ca

an ob stacle and promoters sometimes strug g le to meet mark et mak ers’ data needs. S o it is encourag ing that 62% of respondents b eliev e the industry w ill manag e to ov ercome transparency concerns. European promoters can look to other mark ets for c a i s i s s c as a a c i i s c a -traded mutual fund N ex tS hares structure in the U S .

“ ET P s continue to help democratiz e the g lob al inv estment industry . W hile inv estors and their intermediaries are

c i i ca i a is aa i i i s fi is i isi

ac c ic c ai i si i ss athreat of further reg ulation. S o althoug h the product ‘ land

a a a i a i i fi s ithe ones that are b est at distrib ution. ”

M ark W eeks Chief Executive Officer, ETF Securities (UK) Limited

S trateg ic themes

1 0 | Integrated innovation: the key to sustainable growth

• e era ed and in erse I H elped b y v olatile mark et c i i s s a i a s a i ia Asia-Pacific Asia i s s i a ic a s c s

c s - a i i as is a ai a ia a ai a a a ac a c s

reset daily means that they offer different ex posures to futures or short selling . P romoters need to ensure that inv estors

s a s i c s s cia si smulti- day periods. T he desire of the U . S . S ecurities and Ex chang e

issi i i s s a s s s s aa a s c a a i c s

in future.

• urrency hed in C urrency - hedg ed classes of ET F s continue to a ac si ifica i s a ic a i ig row th of cross- b order inv estment should also b oost demand for c c - s i Asia-Pacific P s a ic a a c a i s c c a s i i a a aeffect on the relativ e performance of these products.

• E nv ironm ental , social and gov ernance ( E S G ) / social l y res onsible in estin I themed s G row ing concerns ab out g lob al w arming and “ stranded assets” are g iv ing ES G /S R I themed ET F s a b oost. T here is increasing interest from

i ia ai i s s s cia i apromoters hav e issued ES G funds. F ollow ing the P aris Ag reement

c i s i i s s c as si s aconsidering ET F s as a low - cost alternativ e to activ ely manag ed ES G funds. As these products dev elop it w ill b e interesting to see w hich use q uasi- passiv e “ screening ” and w hich tak e a more activ e approach to portfolio selection.

T his list prov ides ample ev idence of the industry ’ s innov ativ e ca a i i i s i a s i i s a ia is s

sa i s i i i s c fi a s s aw orried ab out the potential side effects of innov ation. C ost b uildup a c ssi c i i a c c s s a a i ais s s c as ia is-s i a a

reg ulatory b ack lash.

i a s a c is s s a ai s a i ais s a s a c is a i i i s

some inv estors feel that there is still room for improv ement.

S tock lending is one ex ample of this conundrum. Most manag ers see stock lending as a positiv e function. T he maj ority of inv estors

c s i c i i c s a s c i as aia i c as i i i s i s s c

lending can reduce the transparency of returns and g iv e phy sical ET F s some of the features of sy nthetic ones. I f promoters w ant i s s c i s i s c i sica s

as a s a as ssi a i i i sa a i s s a i ici s a ai scollateral receiv ed b y funds.

C osts are another area w here transparency could b e improv ed. ET F promoters should mak e the total cost of ow nership as clear as ssi a i i a a s aex pense ratio ( T ER ) may sometimes b e outw eig hed b y transaction c s s s c as i s a s a a c a s is isespecially true w hen inv esting in the short term.

P c is a fi i i sit is b ecoming prog ressiv ely harder to achiev e. I nnov ation needs

ai a ic a s cificneeds w hile offering scalab ility . T he g ood new s is that industry play ers recog niz e the dang ers of ov ersupply and the importance of thoug htful innov ation that meets clear inv estor needs. As ET F s

c s s a i siinnov ation is b alanced b y a commitment to transparency and an aw areness of the need for sustainab ility .

“ As the trend tow ards passiv e inv esting continues to g ather ac s i a i i s i s a ic a

i s s a s a i s a a a acs cia fi i c i s i

E ric W iegand P r o d u c t S p e c i a l i s t — P a s s i v e I n v e s t m e n t s a t D e u t s c h e B a n k , D e u t s c h e B a n k A G , D e u t s c h e A s s e t M a n a g e m e n t

F ocus on m acro f actors

H ot topics

1 1Integrated innovation: the key to sustainable growth |

S o f ar, 2 0 1 6 has arguabl y seen m ore geopol itical unpredictabil ity than any year since the financial crisis es ondents think macro f actors — m ost notabl y a C hinese sl owdown, B rexit, U S pol itics and the threat of terrorism ose si nificant risks to market stability f course concerns ary amon re ions uro ean firms orry most about re it and a ossible breaku hile those in sia acific are more an ious about the health of the

hinese economy

n the u side macro shocks are creatin o ortunities for inno ation It is hi hly encoura in that the numbers of respondents who see m arket v ol atil ity as an opportunity outnumber those ho ie it as a threat by a ratio

his buoyant attitude re ects the fact that in estors are findin two key f eatures of E T F s particul arl y v al uabl e in current m arkets:

• A c c essibility. E T F s of f er inv estors access to strategies and assets they mi ht other ise stru le to obtain o yields ha e sent in estors ockin into s trackin di idend ei hted e uities hi h yield cor orate bonds and emer in market debt orei n e chan e uctuations continue to su ort demand

for currency hed ed s nd olatile e uity markets are boostin the o ularity of I s in uro e and sia acific

• L iq uidity. T he “ additional l ayer” of l iq uidity that E T F s can ro ide most notably in fi ed income markets is hi hly

attracti e to asset mana ers and hed e funds hey alue the ability to lace lar e trades ithin uoted s reads i uidity does not ust a eal to institutions etail in estors in H ong K ong and m ainl and C hina of ten take short- term positions and alue the ability to trade uickly

U nf ortunatel y, the sam e m arket conditions that m ake E T F s attracti e also ose challen es es ite the stron erformance of E T F s in the af term ath of recent ev ents such as the U K ’ s v ote to l eav e the E U , 3 7 % of prom oters f ear that E T F s m ay be

articularly susce tible to market instability

i en the industry s confidence in the mechanism these fears seem to be re utational in nature on ersations sho that some firms ha e articular concerns about fi ed income E T F s, which hav e generated negativ e publ icity in the past — albeit un ustifiably in the ie s of many i ed income s are of ten m ore l iq uid than underl ying assets, but this is not al ways the case stress e ent that makes it hard for authori ed participants to redeem units q uickl y coul d bring reputational risk, attract unwanted regul atory attention and set the whol e industry a ste back

T o be cl ear, no one in the industry expects E T F s to create or ev en contribute to a crisis ut a si nificant minority clearly belie es that E T F s m ay suf f er, perhaps unf airl y, f rom ev ents beyond the industry s control he industry needs to inno ate thou htfully and m anage inv estor expectations caref ul l y if it wishes to continue to benefit from market olatility

“ D espite the political and monetary policy uncertainty i ss i s a a a a P

mark ets hav e continued to g row healthfully . F ocusing on c is acc a a

c i a i fi i c s a ica i sET F s for institutional inv estors and a reshaping of the w ealth and retail adv isory space. “

U rsula M arc hioni E M E A C h i e f S t r a t e g i s t , i S h a r e s

S trateg ic themes

1 2 | Integrated innovation: the key to sustainable growth

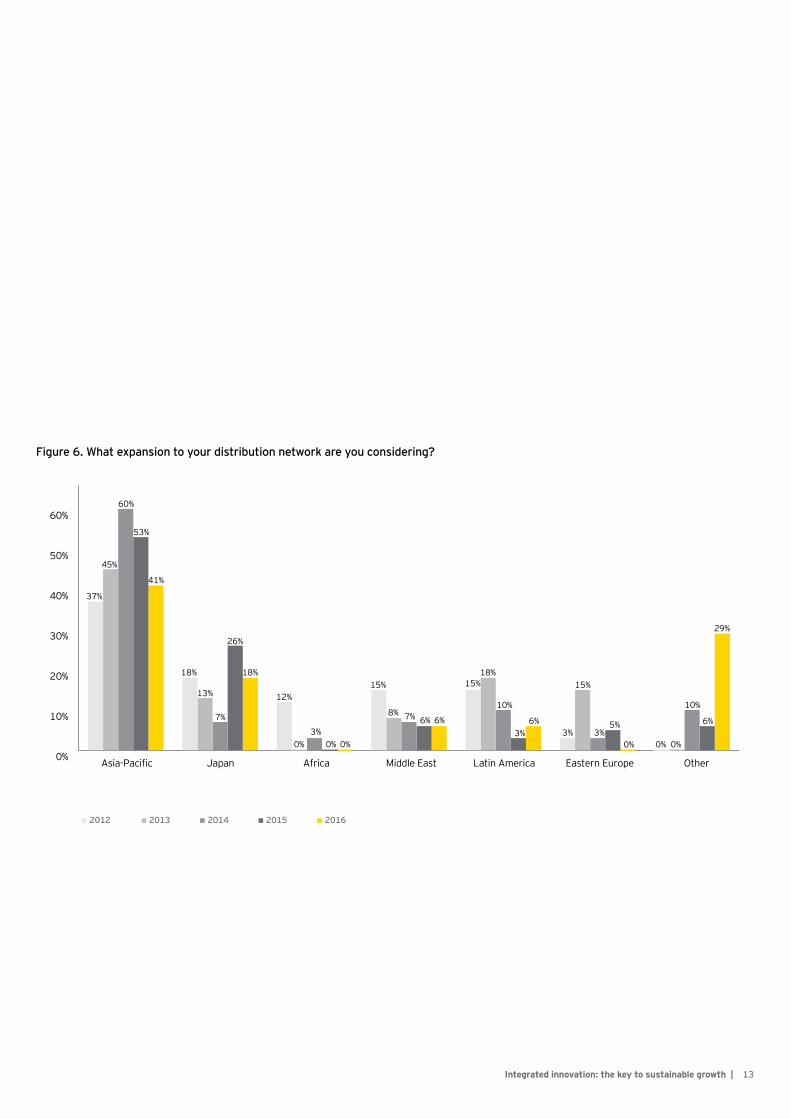

M arket entryT he rapid g row th of ET F assets continues to attract new entrants

i s i c asi i a c c a i s a ici i s s a ca s a a i fi is

( see F ig ure 4) . W afer- thin marg ins mean that ex isting prov iders i is i a A is sai

potential of ET F s is impossib le for new entrants to resist.

F irms entering the ET F mark et are chang ing as the industry g row s more sophisticated. T he surv ey show s that niche play ers and activ e manag ers are seen as much more lik ely entrants than i i a s a i c s s c s assmanag ement ( see F ig ure 5) . T hat is a notab le chang e and illustrates a strateg ic response b y activ e asset manag ers to the challeng e

s a a s ic a ac i a a s ac si s i a s a a Asia-Pacific

respondents ex pect to see a mix ture of U S - b ased promoters and traditional asset manag ers enter local ET F mark ets.

T he surv ey also show s that g eog raphic ex pansion remains a k ey g oal for estab lished ET F promoters k een to tap into fast- g row ing

a s Asia-Pacific ai s s a a s ciaa s s a s a a Asia-Pacific

s s i a a a s a A s a ia iss sare among those look ing to ex pand across the reg ion. S ome other

-ca c i fi i s a a

• a a ai s a a a i s s cias Asia-Pacific is c s si a a s

s ic a a i a s asfrom the B ank of Japan.

• A s a i Asia-Pacific i i s a a ii s ic a s ai a

C hinese issuers are among those launching 40 Act and U ndertak ing for the C ollectiv e I nv estment in T ransferab le S ecurities ( U C I T S ) funds for distrib ution in their home mark ets.

• a a c s i is a i i apromoters and is ex pected to attract the attention of U S play ers.

• A minority of European respondents ( 15%) are considering a si i a i A ica fi s i

i ure ill more romoters enter the market o er the ne t t o years?

i ure hat ty e of romoters do you see enterin the market o er the ne t t o years?

67%

23%

10%

83%

13%5%

86%

14%

0%

89%

11%

0%

90%

10%0%

2012 2013 2014 2015 2016

N o N o a n s w e rY e s

W ill more promoters enter the mark et ov er the nex t tw o y ears?

010%20%30%40%50%60%70%80%90%

100%

20162015

0

5%

10%

15%

20%

25%

30%

15%

22%

18%20%

28%

18%

10%

15%

19%

14%

10% 10%

Activ e manag ers/

others

Asset manag ers

w ith no current

ET F offering

U S - b ased ET F

prov iders

N iche play ers/ new

start- ups

Asia-b ased ET F

prov iders

Europe-b ased ET F prov iders

1 3Integrated innovation: the key to sustainable growth |

i ure hat e ansion to your distribution net ork are you considerin ?

Asia-Pacific

37%

45%

60%

53%

41%

18%

13%

7%

26%

18%

12%

0%3%

0% 0%

15%

8% 7% 6% 6%

15%18%

10%

3%6%

3%

15%

3%5%

0% 0% 0%

10%

6%

29%

Japan Africa Middle East Latin America Eastern Europe Other

2013 2014 20152012 2016

What expansion to your distribution network are you considering?

0%

10%

20%

30%

40%

50%

60%

70%

S trateg ic themes

1 4 | Integrated innovation: the key to sustainable growth

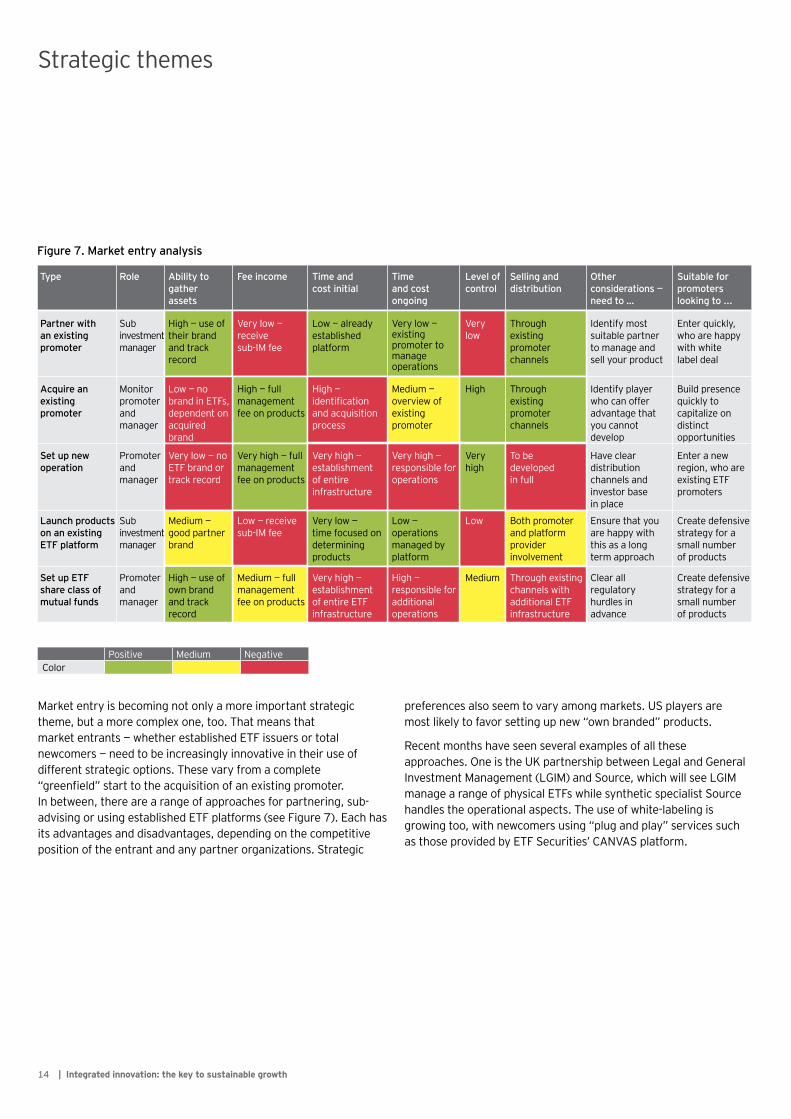

Mark et entry is b ecoming not only a more important strateg ic a c a a s a

a a s s a is iss s ac s i c asi i a i i i s

different strateg ic options. T hese v ary from a complete fi s a ac isi i a is i

a a a a ac s a i s -adv ising or using estab lished ET F platforms ( see F ig ure 7) . Each has i s a a a s a isa a a s i c i iposition of the entrant and any partner org aniz ations. S trateg ic

T ype

P artner withan existingprom oter

A cq uire anexistingprom oter

S et up newoperation

L aunch productson an existingE T F pl atf orm

S et up E T Fshare cl ass ofm utual f unds

S ub inv estmentmanag er

Monitorpromoterandmanag er

P romoterandmanag er

S ub inv estmentmanag er

P romoterandmanag er

H ig h — use oftheir b randand trackrecord

Low — nob rand in ET F s,dependent on acq uiredb rand

V ery low — noET F b rand ortrack record

Medium —g ood partnerb rand

H ig h — use ofow n b randand trackrecord

V ery low —receiv esub - I M fee

H ig h — fullmanag ementfee on products

V ery hig h — fullmanag ementfee on products

Low — receiv esub - I M fee

Medium — fullmanag ementfee on products

Low — alreadyestab lishedplatform

H ig h —i ifica iand acq uisitionprocess

V ery hig h —estab lishmentof entireinfrastructure

V ery low —time focused ondeterminingproducts

V ery hig h —estab lishmentof entire ET Finfrastructure

V erylow

H ig h

V eryhig h

Low

Medium

T hroug hex istingpromoterchannels

T hroug hex istingpromoterchannels

T o b edev elopedin full

B oth promoterand platformprov iderinv olv ement

T hroug h ex istingchannels w ithadditional ET Finfrastructure

I dentify mostsuitab le partnerto manag e andsell y our product

I dentify play erw ho can offeradv antag e thaty ou cannotdev elop

H av e cleardistrib utionchannels andinv estor b asein place

Ensure that y ouare happy w iththis as a longterm approach

C lear allreg ulatoryhurdles inadv ance

Enter q uick ly ,w ho are happyw ith w hitelab el deal

B uild presenceq uick ly tocapitaliz e ondistinctopportunities

Enter a newreg ion, w ho areex isting ET Fpromoters

C reate defensiv estrateg y for asmall numb erof products

C reate defensiv estrateg y for asmall numb erof products

V ery low —ex istingpromoter tomanag eoperations

Medium —ov erv iew ofex istingpromoter

V ery hig h —responsib le foroperations

Low —operationsmanag ed b yplatform

H ig h —responsib le foradditionaloperations

R ol e A bil ity togatherassets

F ee incom e T im e andcost initial

T im e and costongoing

L ev el ofcontrol

S el l ing anddistribution

O therconsiderations —need to …

S uitabl e f orprom otersl ooking to . . .

C olorP ositiv e Medium N eg ativ e

i ure arket entry analysis

preferences also seem to v ary among mark ets. U S play ers are most lik ely to fav or setting up new “ ow n b randed” products.

R ecent months hav e seen sev eral ex amples of all these a ac s is a s i a a a

s a a a c ic i smanag e a rang e of phy sical ET F s w hile sy nthetic specialist S ource handles the operational aspects. T he use of w hite- lab eling is

i i c s si a a s ic s s cas s i c i i s A A a

1 5Integrated innovation: the key to sustainable growth |

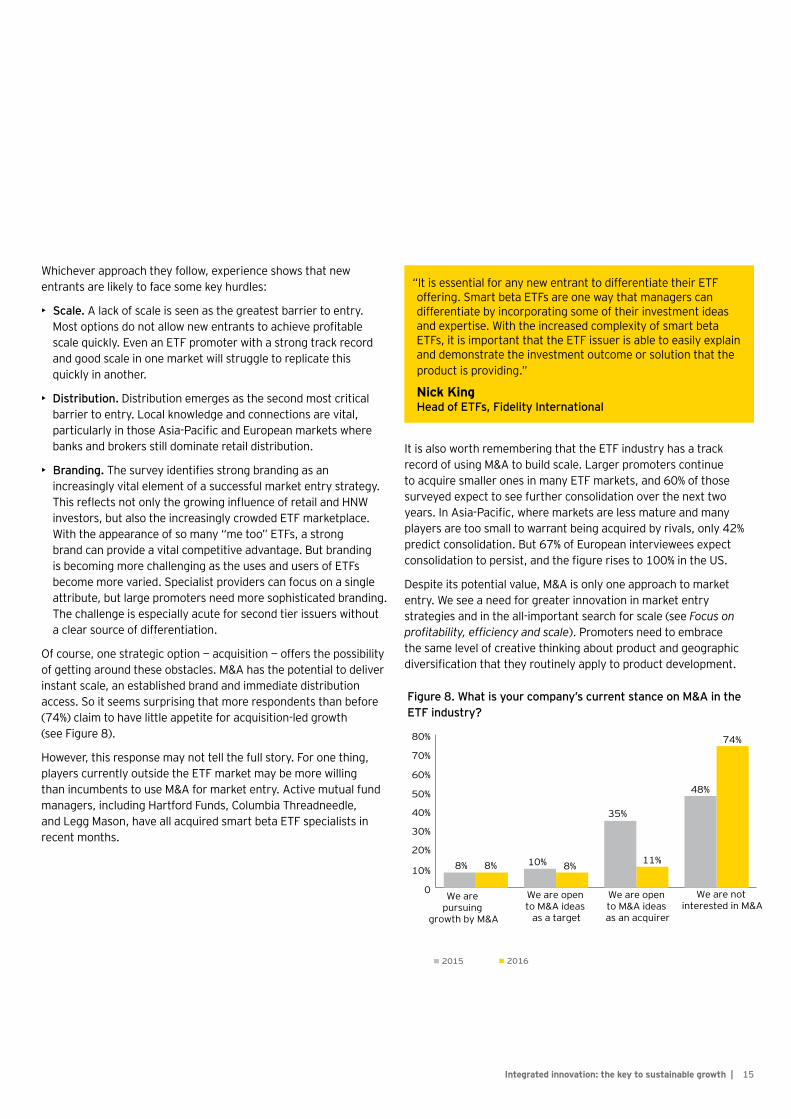

i ure hat is your com any s current stance on in the industry?

20162015

W hat is y our company ' s current stance on M& A in the ET F industry ?

0

10%

30%

20%

40%

50%

60%

70%

80%

8% 8%

35%

48%

74%

11%10% 8%

W e are pursuing

g row th b y M& A

W e are open to M& A ideas

as a targ et

W e are open to M& A ideas as an acq uirer

W e are not interested in M& A

ic a ac i c s s aentrants are lik ely to face some k ey hurdles:

• cale A lack of scale is seen as the g reatest b arrier to entry . s i s a a s ac i fi a

scale q uick ly . Ev en an ET F promoter w ith a strong track record and g ood scale in one mark et w ill strug g le to replicate this q uick ly in another.

• istribution D istrib ution emerg es as the second most critical a i ca a c c i s a i aa ic a i s Asia-Pacific a a a s

b ank s and b rok ers still dominate retail distrib ution.

• randin s i ifi s s a i as aincreasing ly v ital element of a successful mark et entry strateg y .

is c s i i c ai ai s s a s i c asi c a ac

i a a a c s a s a sb rand can prov ide a v ital competitiv e adv antag e. B ut b randing is b ecoming more challeng ing as the uses and users of ET F s b ecome more v aried. S pecialist prov iders can focus on a sing le a i a s s is ica a iT he challeng e is especially acute for second tier issuers w ithout a clear source of differentiation.

c s s a ic i ac isi i s ssi i ii a s s ac s A as ia i

i s a sca a s a is a a i ia is i iaccess. S o it seems surprising that more respondents than b efore ( 74%) claim to hav e little appetite for acq uisition- led g row th ( see F ig ure 8) .

is s s a s iplay ers currently outside the ET F mark et may b e more w illing

a i c s s A a Ac i aa a s i c i a s ia a

a as a a ac i s a a s cia is s irecent months.

I t is also w orth rememb ering that the ET F industry has a track c si A i sca a s c iac i s a s i a a s a s

surv ey ed ex pect to see further consolidation ov er the nex t tw o a s Asia-Pacific a s a ss a a aa s a s a a a i ac i i a s

predict consolidation. B ut 67% of European interv iew ees ex pect c s i a i sis a fi is s i

s i i s ia a A is a ac aentry . W e see a need for g reater innov ation in mark et entry strateg ies and in the all- important search for scale ( see Focus on profitability, efficiency and scale) . P romoters need to emb race the same lev el of creativ e think ing ab out product and g eog raphic i sifica i a i a c

“ I t is essential for any new entrant to differentiate their ET F offering . S mart b eta ET F s are one w ay that manag ers can differentiate b y incorporating some of their inv estment ideas and ex pertise. W ith the increased complex ity of smart b eta

s i is i a a iss is a asi aiand demonstrate the inv estment outcome or solution that the product is prov iding . ”

N ic k K ing H e a d o f E T F s , F i d e l i t y I n t e r n a t i o n a l

1 6 | Integrated innovation: T he key to sustainable growth

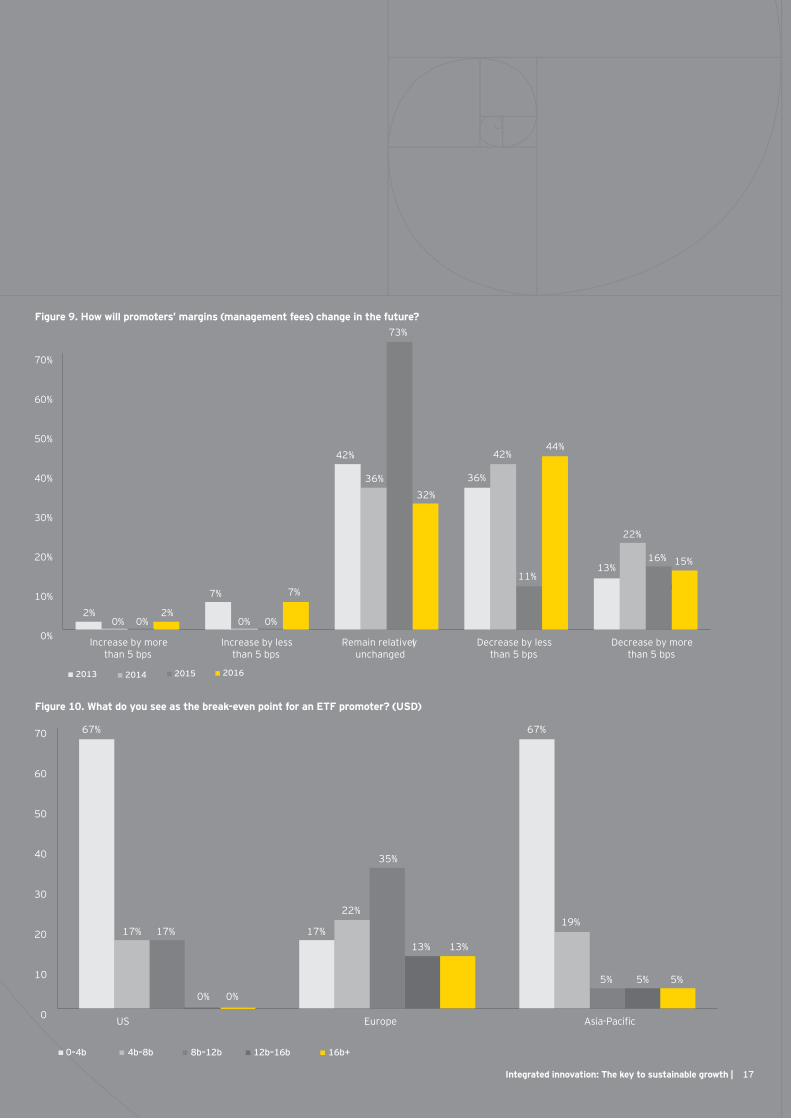

ocus on rofitability efficiency and scaleom etition kee s ushin fees lo er era e lobal

T E R s f el l f rom 3 3 to 2 8 basis points ( bps) in the two years to une he decline as reatest in core markets ith s

f al l ing f rom 3 1 bps to 2 7 bps in passiv e eq uity and f rom 2 4 bps to b s in fi ed income

It is hard to belie e that a era e fees can fall much lo er ut the U S — where T E R s are al ready at their l owest — continues to see intense com petition, and riv al ry in l arge E uropean m arkets is fierce too he sur ey sho s that the outlook for fees has shifted do n ard a ain in contrast to the last sur ey s stabili ation see i ure on ersations ith inter ie ees also su est

that ricin ressure is becomin reater in niche roduct areas his ill hurt smaller s eciali ed romoters and im lies that

innov ation m ay not support m argins f or as l ong as the industry had ho ed

romoters not only face fallin fees eratin costs are risin too e ulatory e enses are becomin more onerous es ecially in uro e nd firms face increasin ressure to in est in di ital technolo y middle and back office automation client re ortin and cybersecurity sia acific firms hich often operate on v ery tight budgets, l ook particul arl y v ul nerabl e to cost in ation

T he com bination of m argin pressure and cost growth m eans that scale is becomin e er more central to rofitability althou h the sur ey sho s si nificant re ional ariations or e am le nearly

of and sia acific res ondents say romoters can break e en ith less than b in u but that fi ure is ust in uro e see i ure here is a similar icture at product l ev el , where 6 9 % of al l E T F s ( those bel ow U S $ 1 0 0 m in si e account for ust of industry u ma ority of those surv eyed ( 6 0 % ) see U S $ 4 0 m or m ore as the m inim um break e en hurdle but anecdotal comments im ly that this fi ure can be m for anilla funds In uro e here re ulation and m ul tipl e l istings push up costs, 3 8 % set the bar at U S $ 8 0 m or hi her

S o how can E T F prom oters achiev e greater scal e – particul arl y in the fra mented markets of uro e and sia? side from

e see t o key ossibilities

he first is ia collaborati e inno ation by romoters brokers e chan es or clearin houses urrent e am les include a E uropean cross- border issuance and settl em ent pl atf orm m anaged by two cl earing houses and a l eading E T F prom oter; the hen hen on on tock onnect and the ondon tock

chan e s s u comin launch of an function

he second o tion is consolidation at the roduct le el In ractical term s this shoul d be the easiest option, though it has been un o ular to date ut ith numbers of s continuin to ro the surv ey suggests a growing wil l ingness to de- l ist or cl ose sub-scale funds his is articularly true in the o far has seen record l ev el s of U S f und cl osures, and 6 7 % of U S respondents expect to reduce their range by up to 2 5 products ov er the comin year i en the market s leadershi role this is a hi hly

ositi e si nal for the hole industry romoters may be reluctant to take the lead on roduct consolidation but should find safety in numbers If issuers can find the confidence to routinely re ie

roduct rofitability say e ery t o years the industry ould be all the stron er

s a a a i s i a i i c sof inv esting for millions of indiv iduals around the g lob e.

i si -c s a i i sifi s iultimately lead to b etter inv esting outcomes for these inv estors.

a ic a c s a si i s a asi ifica i ai i s i s

M ark F itz gerald H e a d o f P r o d u c t D e v e l o p m e n t , E u r o p e , V a n g u a r d

H ot topics

1 7Integrated innovation: T he key to sustainable growth |

F igure 9 . H ow will p rom oters’ m argins ( m anagem ent f ees) c hange in the f uture?

4%

0%

10%

20%

30%

40%

50%

60%

70%

I ncrease b y morethan 5 b ps

2% 2%0% 0% 0%0%

7% 7%

42%

36%

73%

32%

36%

42%

11%

44%

13%

22%

16% 15%

R emain relativ elyunchang ed

I ncrease b y lessthan 5 b ps

D ecrease b y morethan 5 b ps

D ecrease b y lessthan 5 b ps

2013 2014 2015 2016

F igure 1 0 . W hat do you see as the break- even p oint f or an E T F p rom oter? ( U S D )

0

10

20

30

40

50

60

70

U S

67%

17% 17%

0%0%

17%

22%

35%

13% 13%

67%

19%

5% 5% 5%

Europe

0 – 4 b 4 b– 8 b 8 b– 1 2 b 1 2 b– 1 6 b 1 6 b+

S trateg ic themes

1 8 | Integrated innovation: the key to sustainable growth

D igital distributioni s as a c i a ac c i a ii c c a s i s c s ic

isc a i a s i s asa a s ac i a i is i i c sET F promoters face the same distrib ution challeng es as all fund

i s i a i i ca i s s a ss i is s i i a s s s i i i

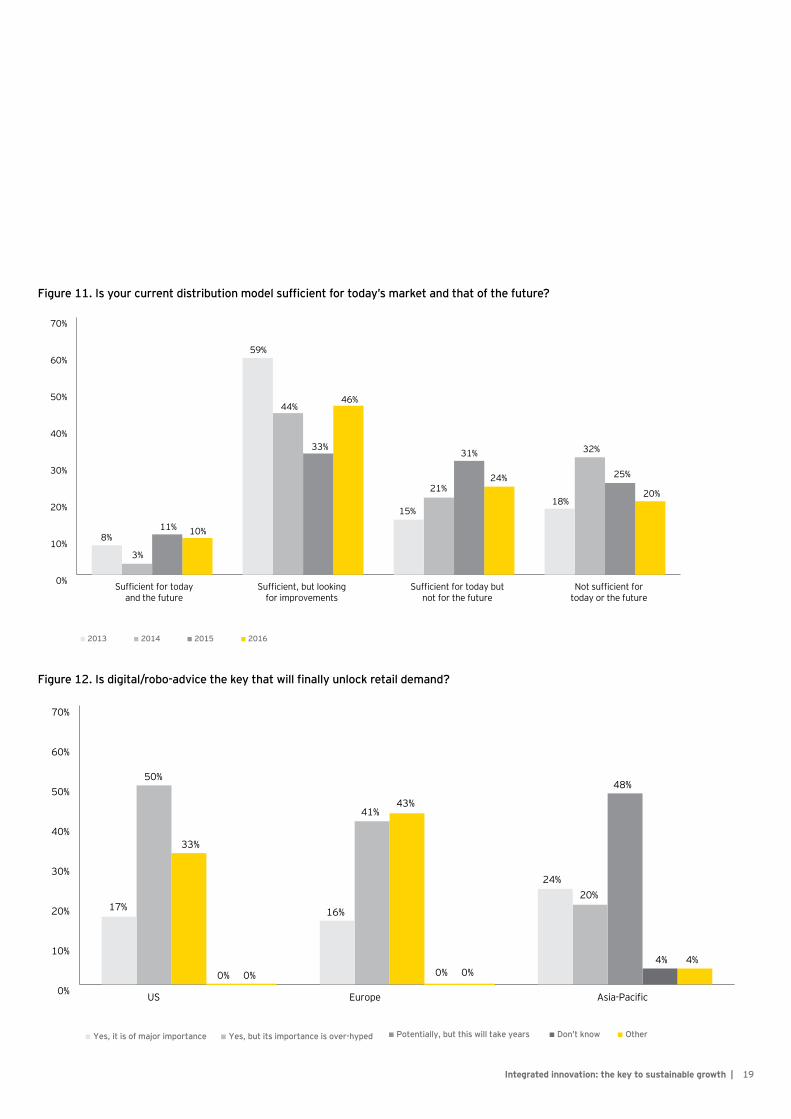

a ac is i i s c a s s i c aev idence that inv estors are increasing ly enthusiastic ab out dig ital distrib ution ( see F ig ure 11) . Only 10% of respondents b eliev e their is i i is s i a a a c ai i i as i s fici

T he emerg ence of rob o- adv isors as a scalab le retail channel could ov erturn this picture. T he surv ey show s real ex citement ab out

-a is s i s s c iaccelerate ET F g row th. N early half of interv iew ees ( 45%) think

-a is s i i i c ss a a i s i si i fi a s a is a ic a a a i i

a Asia-Pacific ai i s is s as a a i s c of g row th.

C onv ersations w ith interv iew ees reinforce the impression that -a is s c a a i i s s

b y b oosting direct sales b ut also b y supporting inv estment adv isors. is a a s i sa i a s a a is a c fi

rob o- adv isors. Many respondents feel that the rob o- adv isor promise -c s i sifi ai i s a a ca

b e deliv ered using ET F s.

a -a is s a s a a c a i aN ot necessarily . T he surv ey show s that ex citement ab out rob o- adv isors is tempered w ith increasing realism. T w o- thirds

s s i i i a fi a s-a is s i acc a a a a a

i i i a a fi a s sias a s a i samong mark ets. R ob o- adv isors are g athering b illions of assets in the U S b ut they are at a much earlier stag e in Europe and Asia-Pacific a i i s s as a aa a a Asia-Pacific s s i -a is s

w ill tak e y ears to b oost retail demand ( see F ig ure 12) .

“ W e see ex ponential g row th in ET F sav ing s plans for retail inv estors in G ermany . T hese are mainly offered b y online a s a s i c asi i s a s as

a a sa i s a is as s - a i sifi i ic s

A rne S c heehl H e a d o f E T F s a l e s , C o m S t a g e E T F

“ Online distrib ution has b ecome dominant for b oth ET F s as w ell as eq uities in Japan. W e may need to approach the retail mark et b y utiliz ing the latest technolog y such as F inT ech. ”

K atsum asa M atsum ura S e n i o r M a n a g e r , N o m u r a A s s e t M a n a g e m e n t

1 9Integrated innovation: the key to sustainable growth |

i ure Is your current distribution model sufficient for today s market and that of the future?

i ure Is di ital robo ad ice the key that ill finally unlock retail demand?

U S

17%

50%

33%

16%

0% 0% 0% 0%

41%43%

24%20%

48%

4% 4%

Europe Asia-Pacific

Y e s , i t i s o f m a j o r i m p o r t a n c e Y e s , b u t i t s i m p o r t a n c e i s o v e r - h y p e d P o t e n t i a l l y , b u t t h i s w i l l t a k e y e a r s D o n ’ t k n o w O t h e r

Is di ital robo ad ice the key that ill finally unlock retail demand?

0%

10%

20%

30%

40%

50%

60%

70%

fici aa

8%

3%

11% 10%

59%

44%

33%

46%

15%

21%

31%

24%

18%

32%

25%

20%

fici ii s

fici a s ficia

2013 2014 2015 2016

Is your current distribution model sufficient for today's market and that of the future?

0%

10%

20%

30%

40%

50%

60%

70%

S trateg ic themes

2 0 | Integrated innovation: the key to sustainable growth

a i is as s a ia i s Asia-Pacific i sa sias ic a s i i s

a s i s a Asia-Pacific a s s s ica as a -a -a is s si a i i i i a fi s isa ac a ic a a s a ica

si a i a is i i c a s aca i a i s ca a s a s a a acto neg otiate w ith partners.

s s s s s a s i i s s ii i ss ac i i a is i i s i

patience to realiz e long - term rob o- adv isor g row th. I t also implies that a j oined- up dig ital strateg y that recog niz es the need to b uild emotional eng ag ement throug h direct and social media w ill b e v ital.

i s c a s a c si ac ac s i c i

• ider atterns of di ital distribution R ob o- adv isor tactics fi i a is i i s a i s s i s

a ica i is i c ai sa s -a is s ca sadv ised sales and H N W channels too. W ill they complement other c a s ca i a i P s c s icroutes to prioritiz e.

• han in in estor references Millennial inv estors may seem i a a -a is s a

less inv estib le income than older g enerations and face other ssi fi a cia i i i s fi s s a i a i i

a i a a i s s i a fi a ciaassets may not b e as resistant to dig ital distrib ution as w idely ass i s s a s a i c sw ith recent EY research show ing that H N W clients may b e more

-a is s a ass a i s s 2

• e ional differences Ex pectations for rob o- adv isors v ary a i s a a a s cmost dig ital distrib ution to retain elements of traditional adv ice. s a is i i a a s a s a i a a s

i c i i s i s a s i a A s a ia i sa i s acc s i a a

Alib ab a in C hina.

• he human element si -a is s s i a along w ay to g o to w in the trust of inv estors. ET F prov iders need to do all they can to encourag e inv estors to use this channel. W hile s i s s a a a a a -a is sothers may prefer hy b rid models that comb ine automation w ith a deg ree of human g uidance.

• nershi s artnershi P romoters can tak e a numb er of approaches to rob o- adv isor distrib ution. T hose that can afford it could b uy estab lished rob o- adv isors. B uilding a proprietary platform is another option. F irms could also partner w ith s a is -a is s i i i a s i

i s s c - a i a s sonline inv estment accounts.

• Inte ration ith social media Althoug h 35% of respondents c si s cia ia i a s sa i i s cia ia s a i s ahav e y et to appoint a head of social media. A successful dig ital s a i s s cia ia i a i s i sj ust to “ push” mark eting information.

As a is i c i i s i i s semb race the w ay that inv estors’ g row ing appetite for dig ital technolog y is reshaping retail and H N W distrib ution. R ob o- adv isors a a i a s a s ctak e y ears to reach their potential in many mark ets. P romoters

s a i a i i i a s a i s a ac a s i c a s i i s c s a

industry practices ( see Focus on mutual fund convergence) . T hat i s a - i a s a fi sai i - i i i

2 The experience factor: The new growth engine in wealth management,

“ W e b eliev e that b ring ing more transparency to the European a i fi a si ifica i c asi

ass s a a as as a i

G uy S im p kin H e a d o f B u s i n e s s D e v e l o p m e n t E u r o p e , B a t s E u r o p e

F ocus on m utual f und conv ergenceF ocus on m utual f und conv ergence

2 1Integrated innovation: the key to sustainable growth |

ne of the most interestin ualitati e findin s to emer e from the surv ey is the im pression that conv ergence between E T F s and mutual funds may be acceleratin

his sounds counterintuiti e s ha e a uni ue structure and ha e traditionally been defined by their differences from mutual funds ut o er the ast fi e years these distinctions ha e becom e bl urred in som e areas, incl uding:

• C ost. C om bined with the ref orm of retail distribution in m any m arkets, the strategic threat f rom l ow- cost E T F s has f orced the m utual f und industry to reduce m anagem ent f ees and other char es

• C ontent. T he range of options that E T F s prov ide has l ed m any in estors to re e aluate the e ibility of inde in includin ia mutual funds

• S truc ture he structural boundaries bet een s and mutual funds ha e been eroded by the emer ence of hybrid ehicles E xchange- traded m anaged f unds hav e dom inated headl ines, but exchanges in I tal y and the N etherl ands now al l ow m utual funds to be traded classes of mutual funds ha e also been launched in a number of markets

M ore recentl y, the gl obal shif t toward passiv e inv estm ent has ser ed to stimulate con er ence he first fi e months of sa lobal acti e out o s of b and assi e in o s of

b 3 he stren th of these o s is encoura in asset m anagers to reduce costs by integrating both sets of products into a sin le inde based offerin fter all it makes sense for E T F s and m utual f und ranges to be com pl em entary, not com etiti e third of romoters say they do not dif f erentiate between E T F s and other products, but are l ed by in estor references

S o, does conv ergence with m utual f unds represent a threat to the industry?

e sus ect the ans er is robably not If many in estors are becom ing “ v ehicl e agnostic, ” that is because m utual f und prov iders are increasingl y f ocused on prov iding the f eatures that hav e m ade E T F s m ore successf ul than other index funds includin lo costs and e ibility hat can only be ood f or inv estors — and f or those institutions abl e to com pete in the

market nd to be clear the sur ey does not su est that s and mutual funds ill e er fully con er e

N onethel ess, we do expect conv ergence to present existing E T F prom oters and new entrants with a twof ol d chal l enge: to ensure that they are strategical l y pl aced to take adv antage of conv ergence and to ensure that they del iv er optim al outcom es to in estors hiche er in estment ehicle they choose

“ I b eliev e that ET F s w ill continue to b e a maj or disruptiv e force in the fund industry and asset g row th is most lik ely to focus on innov ativ e smart b eta strateg ies. ”

N iz am H am id E T F S t r a t e g y , W i s d o m T r e e

s a a ac i i s s ac ss i si c i s a si i i i a

fici c a a i i s cific s

J ü rgen B lum berg H e a d o f C a p i t a l M a r k e t s E u r o p e , S o u r c e

Ass a a Ac i ai i Financial Times

H ot topics

22 | Integrated innovation: the key to sustainable growth

Regional highlights

2 3Integrated innovation: the key to sustainable growth |

R egional sum m ary: U Sis s a s a s s a

ai a i s i i a i s s a c i s caa a s ic a i s s a fi s s ici s s a c c a a i s c a s

s i s ac i i s fici c ctotal AuM in the U S mark et to g row from U S $ 2. 3t at the end of A s a a a a ag row th rate of around 15%. W e identify the follow ing k ey themes:

• ro in ado tion T he U S ET F industry continues to increase its rang e of inv estors. S elf- directed retail inv estment is g row ing .

-a is s i s a ai is i sincreasing ly use ET F s to b uild standardiz ed portfolios and customiz ed solutions. I nstitutions are sub stituting ET F s for

s a c i i a i s a c a irang e of lev erag ed ET F s. T he surv ey show s that U S respondents are also upb eat ab out demand from H N W adv isors.

• om etition mar ins and ne entrants C ompetition is more i s a s a a a i i i a athis w ill only increase as more issuers enter the mark et. Activ e asset manag ers are seen as the most lik ely entrants. T he effects

c i i a s a s s a fi i i amak e new products successful and tak e the most dow nb eat v iew

fi a i i c s s a c acc a

• urther consolidation All U S respondents ex pect further c s i a i a s s s s s a

i a i ss a c i i a a fi s ireal adv antag es in scale or performance w ill face increasing

ss s c a i - i a scan also ex pect to attract the attention of larg er ET F prov iders.

• roduct inno ation I nnov ation is the leading source of c i i a a a a s a s a isi c asi i a i i c ass s ic a17% of U S ET F s compared w ith 24% of European ET F s and 23%

a s a s as a a a as sa s -s cific a i c c a

headaches b y increasing cash holding s and limiting less liq uid inv estments. Activ e ET F s are a k ey area of focus and w ill receiv e a b oost as more activ e specialists enter the mark et. T he approv al of periodically disclosed ET F s could b e a g ame chang er.

• randin in estment As competition increases and products i a a i is c i a a i i

A strong b rand is v ital to mak e products stand out w hen mark eting to adv ised and self- directed retail inv estors.

• i iti ation s s s s a fi s aready than others to seek operational improv ements throug h i i i a i i i a is i i is a a i

rob o- adv isors w idely seen as the future of retail adv ice. S ome U S -a is s a a a a ac i i s a s a ac a ass a a c s s a a

from human adv isors in the future.

• on er ence ith mutual funds T he g radual conv erg ence of ET F s and mutual funds is a g lob al theme b ut is most notab le in the U S . T he g row th of ex chang e- traded manag ed funds ( ET MF s) is i i s as is a s cia is sinto the ET F mark et. S ome promoters mak e little b randing distinction b etw een ET F s and other index funds ( see Focus on mutual fund convergence) .

• e ulation head ind or tail ind? I nterv iew ees feel that a sc i is i c asi as i s s as i fi i c a s a i as a

supportiv e. T he S EC ’ s focus on “ distrib ution fees in g uise” and a new suitab ility standard for adv isors are b oth ex pected

c a ai a a a sF iduciary S tandard R ule could also g iv e ET F adoption b y 401k inv estors a b oost.

24 | Integrated innovation: the key to sustainable growth

2 5Integrated innovation: the key to sustainable growth |

R egional sum m ary: E uropes a s a i a i i s

institutional tak e- up. F rag mentation is the b ig g est operational a ac i s a ca i c s c i a

themselv es felt. W e ex pect total AuM in Europe to g row from i A s a

av erag e annual g row th rate of ab out 16%. S ome of the k ey themes of European ET F mark ets are:

• Institutional o ortunity Asset manag ers are the leading s s s a i si s a i s s i s s

most v aluab le targ ets. T he sub stitution of ET F s for fully funded s c i s a a a s i a assi

s a i s is a i i a s s a ia i s ireg ulation and demand mean that promoters need to tailor their approach to each mark et.

• etail otential s retail reality S trong er retail adoption of ET F s remains a k ey long - term amb ition. T here is hug e interest in i i a is i i s i as a a ic s i s

s cc ss i a s i a ca i a ia -a icremains in its infancy and is ex pected to complement traditional channels for the foreseeab le future. D ifferent mark ets also call for different approaches. Online sav ing s b ank s are increasing ly s cc ss i a a s s a shav e y et to list ET F s along side other inv estment funds.

• ar ins and ne entrants European ET F mark ets are seeing si ifica ic si i ca iss s c i ss

a a s A sa i a i c s s a is c s ica i a a a i As a s

b reak - ev en lev els are hig her than in any other reg ion. N ew a s a c i A ica sc i s i a Asia-Pacific fi s

launching U C I T S products for distrib ution in home mark ets. a i i a a ass a a s assi a ac i

are also ex pected to enter in g reater numb ers. T raditional asset a a s assi a ac i a a s c

in g reater numb ers.

• he dri e for efficiency a i fici c is as a ic i i a fi s a s c i s - ic a i i i i a i s i i s a a i a sifor cross- b order trading is illustrated b y the success of pan- European stock ex chang e B ats. I ssuers are also ex ploring the capab ilities of the international settlement platform estab lished b y a larg e promoter and tw o clearing houses. At the product

c s s is a a a i s a sin Europe.

• roduct inno ation F ix ed income ET F s are ex pected to b e a i i s is a c i

s a a ic a s s as c cia sinstitutional adoption. D iv idend w eig hted eq uity funds are

a i ac s a ai i a as a a c i s c s s i i a

S ocial and G ov ernance themed ET F s and property ET F s is i c as a s a c c c s a a i s

i ac i s is i i a a a s aseek ing to b uild a track record in these products.

• he threat of re it More than 80% of interv iew ees see B rex it as a threat to the U K and European ET F mark ets. Most European respondents ( 80%) hav e set up w ork ing g roups to consider its i ac i s i s a a acc ss aa a s s a s s a s asEurope’ s larg est and most promising mark et w ill b e undermined.

i a s a s sc c a a sc s a s

i a c as a a i a a sc is i s is c c a a i i

a a c c i a is ca is i a a i fi s i a a

c a i a a i s

• om le effects of re ulation a a i a ac a c s as ia c sT he European S ecurities and Mark ets Authority ’ s ( ES MA)c s a i i a i is c a i c ai a

is a s s a sc i s is i c asi ssome initiativ es are seen as more helpful. Mark ets in F inancial I nstruments D irectiv e I I ( MiF I D I I ) should help to throw a lig ht on

- c a a i ic ca as i as i aA i c as c c s i s a fiincome ET F s that g iv e insurers “ look throug h” transparency . is i i s a a s i a i fi i s a

retail mark ets.

26 | Integrated innovation: the key to sustainable growth

2 7Integrated innovation: the key to sustainable growth |

e ional summary sia acificAsia-Pacific i c s s a s a s a a a a as s i As a i isa i i a a a a i a ia i s

in concentration and sophistication. W e ex pect ET F AuM in Asia-Pacific si a a i

a a a a a22%. W e ex pect Japanese AuM to g row from U S $ 182b to U S $ 380b

sa i a a a a a i sthemes include:

• aried roduct inno ation ET F innov ation continues to ev olv e in different w ay s across the reg ion. I nstitutions are b eing draw n

acc ssi i i a i i i a s i acounterparty risk is encourag ing them to sub stitute ET F s for OT C deriv ativ es. S mart b eta funds are b eing launched in many

a s i ac i s a a i i A s a ia aK orea they are v irtually ab sent in other mark ets. T he approv al of

s is s i i a i i

• e ulation sha in the industry Opinions ab out reg ulation are i a i s cas s a ca i is s as a a

on product innov ation. P romoters in sev eral mark ets w ould also lik e reg ulators to help ET F s compete more effectiv ely w ith mutual funds. R espondents in H ong K ong are among those w ho w ould lik e to see Australian- sty le reg ulation of retail commissions.

• he o ortunity T he surv ey show s increasing optimism ab out the potential for H N W inv estment. A numb er of interv iew ees say priv ate b ank s are eng ag ing activ ely w ith ET F

s fi s i i a i i a a sand w ealth adv isors w ould b e hig hly v aluab le g iv en the siz e and

fi a i i is s a i ia ic -c ass a a s

• e entrants and com etition s c i i a a iss a ac ss Asia-Pacific A a s c i

i s c i a ic a s a a ais less pressure on other asset classes. B reak - ev en lev els for

s a c s a a i asa c a i s c s i a i a s cshak e up this picture. Many of those surv ey ed ex pect more U S a a s Asia-Pacific a s a sAsia-Pacific iss s a c s i a a si

• Im ortance of structural reforms a Asia-Pacific sa s i a s i c i i a

i i Asia-Pacific A A Pass Asia iF unds P assport and Mutual R ecog nition are encourag ing promoters from mark ets such as Japan and K orea to consider reg ional ex pansion. F ollow ing approv al of the S henz hen- H ong K ong S tock C onnect it has b een announced that approv al for ET F

c s i a a is cto b oost cross- b order ET F trading b etw een mainland C hina and H ong K ong .

• anks s robo ad isors? R etail inv estors are seen as a strong a - s c i a Asia-Pacific a s

Asia-Pacific s s a ic a i ai a i a aA s a ia a sias ic a i i a is i i P sin mark ets lik e Japan and H ong K ong w ould b e delig hted to dev elop these channels and reduce their dependence on b ank s a a s s a ca i careg ulators sug g ests that stand- alone rob o- adv isors could need i a i Asia-Pacific

• eed for o erational in estment a Asia-Pacific sare ab le to operate at a smaller scale than their counterparts in Europe or the U S . B ut this is a doub le- edg ed sw ord. Many s a ac a a s a fi s ca fi s s

i i s a i a ca a i i i s ai s i c s c i c ai Asia-Pacific

promoters are b y far the most lik ely to hav e b een successfully hack ed.

R eg ional hig hlig hts

2 8 | Integrated innovation: the key to sustainable growth

s i Asia-Pacific s s i amark ets include the follow ing :

• on on R ecent months hav e seen a numb er of ex citing s i c i a c s a i s a

c i i s a s issi s a ac s s a s a is i ai a a a

b ut international institutions ty pically prefer to trade in H ong i c i i a a s i

c c a i a is i iand administrators are dev eloping their capab ilities in this area. P romoters and mark et mak ers ex pect the S henz hen- H ong K ong S tock C onnect to g iv e liq uidity an ev en b ig g er b oost than the S hang hai- H ong K ong link up.

• ustralia R etail inv estment continues to dominate the Australian mark et. P romoters b eliev e that the reg ulatory reform of commissions w ill continue to g iv e them further traction among

a ass a i s s c as A s a iainstitutions remain slow to adopt ET F s and ty pically use them for short- term inv estment. T he approv al of ET MF s b y the Australian S ecurities Ex chang e is helping activ e prov iders to ex pand. T he recent partnership b etw een ET F specialist B etaS hares and prominent activ e manag er AMP C apital illustrates the potential for new play ers to enter the activ e ET F mark et.

• a an a a s a is s a i ca a a ic s s i s s as a a

ic s a a s ic ass sw ith the b ulk track ing the N ik k ei 225 or T opix index es. I n a mov e i s i a i a i as a sex pressed a desire to inv est in capex - w eig hted ET F s. D omestic and i a i a iss s a a c i s a a s a ismore ES G - themed activ ity than elsew here in Asia. P romoters are i s i ia -a ic a ss sias ic

a i i a s a a a s fi s ac si i a si i as i Asia-Pacific a s

perhaps using passporting as a spring b oard.

29Integrated innovation: the key to sustainable growth |

30 | Integrated innovation: the key to sustainable growth

Conclusion

3 1Integrated innovation: the key to sustainable growth |

i s s a a i a s is icaa a c is c i s i s

s a i i i a i is s i i fi iex pansion. G row th w ill b ecome harder to achiev e as ET F s g row i si a i c a is a ic a a s amutual fund prov iders are activ ely seek ing to enter ET F mark ets.

ca i s i c i is i i c s aa s i i i s a ic si i i i a

i a a ac i a i ic a i i s i s sis i i ai ai i a a a c a

fi a i i a s s ai a i i s

W e see four k ey areas w here indiv idual promoters can capitaliz e on this insig ht and put integ rated innov ation into practice.

1. mart sustainable roduct de elo ment ET F s are meeting a a s i s s s i i i s i i

liq uid access to ex posures they mig ht otherw ise strug g le to ai s c as i a iss s

s a c i a i s i afi a i i a i ia i is s i a a s s ai a

T he risk s of hasty innov ation are g row ing as more ex otic ET F s are created and speed to mark et b ecomes an increasing priority . A a ic c i a i s a ss s cificconcerns ov er issues such as the transparency of activ e ET F s a i i i i is s fi i c c s A a i

fi s s a i a i is i ithe ev olv ing needs and priorities of inv estors as v aried as g lob al insurers and millennial sav ers.

2. reati ity in the search for scale ET F prov iders need to b e c a i i s a c sca ic is ss ia

ac i i s s ai a fi a i i is is s ia Asia-Pacific a s i a-c i i aP s a a s a s achain need to v iew scale throug h as many lenses as possib le.

s a s c a s a c a i s sca i sca i - a c ss- A P cc s i a i as a i a a s i sthe common features of ET F s and other index ing products could also offer economies of scale. And there is hug e untapped

ia i sca c a i a a s iespecially in the frag mented mark ets of Europe and Asia.

a is a i a fi s ion the dev elopment of international settlement b y creating a

a s c i i i s as a a is s i

F irms should tak e inspiration from ex amples of collab oration in a s i a as as i s as a is i i

trading and settlement.

3. rans arency related to roducts erformance and ricin T he ET F industry sees transparency as one of its k ey selling

i s s sc a a - c assicommitment in this area. T ransparency should not b e limited to disclosure ov er index es and product structures. P romoters need to ensure that they are informing inv estors ab out the

ssi a c s i a a c i i sb oth the long and short term. T his includes setting out how the performance of ET F s may differ from sub stitutab le products and instruments. A commitment to complete transparency ov er

ici i c i a c s s s i as as sa s s a s a c fi i a atheir products create.

4. ontrol of the di ital a enda i s s s i i atechnolog y is renow ned for its disruptiv e capab ilities. T he ET F industry should emb race these similarities and use dig itiz ation to b uild strong er inv estor eng ag ement. T his is not j ust ab out

i sa s -a ic a s a i a aidistrib ution opportunities. I t is ab out connecting w ith institutional and retail clients to streng then their b elief in ET F inv esting . F irms need to pay more activ e attention to areas such as social

ia a c s c i ic a i as i aw hich can suffer from underinv estment. T his req uires more than tactical initiativ es such as w ork ing w ith platforms to dev elop

i s i a i i s a a is a a a aET F promoters need to dev elop holistic dig ital strateg ies that a ss ics as a i as a i a fici c c s c ii i a is i i a c i i i s s

learn from other sectors of asset manag ement w hile tak ing an approach suited to the uniq ue features of ET F s.

s a fi i c a i sa s s ai i a i ac s s c as acc ssi i i ai i i a a i i s cc ss a i

s a si s a s i fi s i ainteg rated approach to innov ation. P romoters that achiev e an enterprise- w ide culture of innov ation w ill b e ab le to not only sustain i a s a s c i fi i a s

create v alue for inv estors.

32 | Integrated innovation: The key to sustainable growth

Key contacts

3 3Integrated innovation: the key to sustainable growth |

A m eric asU S

M att F orstenhausler E Y G l obal and U S Weal th & A sset M anagem ent E T F L eader

+ 1 212 773 1781 matt. forstenhausler@ ey . com

M ark M ic hel P artner + 1 617 585 1948 mark . michel@ ey . com

Carolyn Brayfield S enior M anager

+ 1 617 585 3405 ca a fi c

P eter J . B ush S enior M anager

+ 1 312 879 5472 peter. b ush@ ey . com

Asia-PacificA ustralia

R ita D a S ilva P artner + 61 2 8295 6142 R ita. D a. S ilv a@ au. ey . com

C hina ( m ainland)

A J L im E Y C hina Weal th & A sset M anagem ent L eader

+ 86 21 2228 2929 aj . lim@ cn. ey . com

H ong K ong

J ulie K err sia acific ealth sset ana ement eader

+ 852 2846 9888 j ulie. k err@ hk . ey . com

M att F orstenhausler E Y G l obal and U S Weal th & A sset M anagem ent E T F L eader

+ 1 212 773 1781 matt. forstenhausler@ ey . com

L isa K ealy EY E M E I A Weal th & A sset M anagem ent E T F L eader

+ 353 1 2212 848 lisa. k ealy @ ie. ey . com

J ulie K err sia acific ealth sset

M anagem ent E T F L eader

+ 852 2846 9888 j ulie. k err@ hk . ey . com

K ey contacts

3 4 | Integrated innovation: the key to sustainable growth

J ap an

S hintaro M iz unaga S enior M anager

+ 81 3 3503 1100 miz unag a- shntr@ shinnihon. or. j p

K orea

J eong H un- Y ou E Y K orea Weal th & A sset M anagem ent L eader

+ 82 2377 00972 j eong . hun. y ou@ k r. ey . com

M alaysia

B eng Y ean Y eo E Y M al aysia Weal th & A sset M anagem ent L eader

+ 60 3749 58771 b eng - y ean. y eo@ my . ey . com

P hilip p ines

V ic ky B L ee- S alas E Y P hil ippines Weal th & A sset M anagem ent L eader

+ 63 2894 8397 v ick y . b . lee- salas@ ph. ey . com

S ingap ore

S wee Y en Y eoh P artner

+ 65 6309 8915 S w ee- Y en. Y eoh@ sg . ey . com

T aiwan

A ndrew F uh E Y T aiwan Weal th & A sset M anagem ent L eader

+ 886 2275 78888 andrew . fuh@ tw . ey . com

T hailand

R ac hada Y ongsawadvanic h E Y T hail and Weal th & A sset M anagem ent L eader

+ 66 2264 9090 rachada. y ong saw adv anich@ th. ey . com

E urop eF ranc e

B ernard C harrue E xecutiv e D irector

+ 33 1 46 93 72 33 b ernard. charrue@ fr. ey . com

G erm any

M ic hael E isenhuth P artner

+ 49 89 14331 27519 michael. eisenhuth@ de. ey . com

Ireland

L isa K ealy E Y E M E I A Weal th & A sset M anagem ent E T F L eader

+ 353 1 2212 848 lisa. k ealy @ ie. ey . com

3 5Integrated innovation: the key to sustainable growth |

G erard C rossan M anager

+ 353 1 2212 147 g erard. crossan@ ie. ey . com

K ieran D aly S enior M anager

+ 353 1 2212 236 k ieran. daly @ ie. ey . com

L ux em bourg

B ernard L hoest P artner

+ 352 42 124 8341 b ernard. lhoest@ lu. ey . com

P ierre K em p eneer S enior M anager

+ 352 42 124 8644 pierre. k empeneer@ lu. ey . com

S witz erland

C hristian S oguel P artner

+ 41 58 289 41 04 christian. sog uel@ ch. ey . com

U K

G ary L ogan S enior M anager

+ 44 131 777 2298 g log an@ uk . ey . com

EY | Assurance | Tax | Transactions | AdvisoryAbout EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

© 2016 EYGM Limited. All Rights Reserved.

EYG no. 03357-164Gbl 1609-2053279 NE

ED None

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax or other professional advice. Please refer to your advisors for specific advice.

The views of third parties set out in this publication are not necessarily the views of the global EY organization or its member firms. Moreover, they should be seen in the context of the time they were made.

ey.com