infrastructure and australia ïs food industry: preliminary...

TRANSCRIPT

Infrastructure and Australia’s food industry: Preliminary economic assessment Nga Nguyen, Lindsay Hogan, Kenton Lawson, Peter Gooday, Richard Green, Keely Harris-Adams and Thilak Mallawaarachchi

Research by the Australian Bureau of Agricultural

and Resource Economics and Sciences

Research Report 13.13 November 2013

Infrastructure and Australia’s food industry: Preliminary economic assessment

ii

© Commonwealth of Australia Ownership of intellectual property rights Unless otherwise noted, copyright (and any other intellectual property rights, if any) in this publication is owned by the Commonwealth of Australia (referred to as the Commonwealth). Creative Commons licence All material in this publication is licensed under a Creative Commons Attribution 3.0 Australia Licence, save for content supplied by third parties, logos and the Commonwealth Coat of Arms.

Creative Commons Attribution 3.0 Australia Licence is a standard form licence agreement that allows you to copy, distribute, transmit and adapt this publication provided you attribute the work. A summary of the licence terms is available from creativecommons.org/licenses/by/3.0/au/deed.en. The full licence terms are available from creativecommons.org/licenses/by/3.0/au/legalcode. This publication (and any material sourced from it) should be attributed as: Nguyen, N, Hogan, L, Lawson, K, Gooday, P, Green, R, Harris-Adams, K and Mallawaarachchi, T 2013, Infrastructure and Australia’s food industry: Preliminary economic assessment, ABARES research report 13.13, Canberra, November. CC BY 3.0. Cataloguing data Nguyen, N, Hogan, L, Lawson, K, Gooday, P, Green, R, Harris-Adams, K and Mallawaarachchi, T 2013, Infrastructure and Australia’s food industry: Preliminary economic assessment, ABARES research report 13.13, Canberra, November. ISSN: 1447-8358 ISBN; 978-1-74323-156-2 ABARES project: 43408 Internet Infrastructure and Australia’s food industry: Preliminary economic assessment is available at: daff.gov.au/abares/publications. Australian Bureau of Agricultural and Resource Economics and Sciences (ABARES) Postal address GPO Box 1563 Canberra ACT 2601 Switchboard +61 2 6272 2010| Facsimile +61 2 6272 2001 Email [email protected] Web daff.gov.au/abares Inquiries regarding the licence and any use of this document should be sent to: [email protected]. The Australian Government acting through the Department of Agriculture represented by the Australian Bureau of Agricultural and Resource Economics and Sciences, has exercised due care and skill in the preparation and compilation of the information and data in this publication. Notwithstanding, the Department of Agriculture, ABARES, its employees and advisers disclaim all liability, including liability for negligence, for any loss, damage, injury, expense or cost incurred by any person as a result of accessing, using or relying upon any of the information or data in this publication to the maximum extent permitted by law. Acknowledgements This report was prepared for the Agricultural Policy Division in the Australian Government Department of Agriculture. The authors thank Trysh Stone and Ryan Wilson from Agricultural Policy Division, and Dale Ashton, Max Foster, Teresa Foster, Trish Gleeson, Michael Harris, Edwina Heyhoe, Kris Morey, Paul Morris, Daniel Pambudi and Alasebu Yainshet from ABARES for helpful comments and information. The authors appreciate useful input from Gary Dolman and David Mitchell and others from the Bureau of Infrastructure, Transport and Regional Economics (BITRE), as well as several people from the Department of Infrastructure and Transport and the Department of Regional Australia, Local Government, Arts and Sport. The authors also thank several industry representatives, particularly in Tasmania and Victoria, for information on the case studies presented in this report.

Infrastructure and Australia’s food industry: Preliminary economic assessment

iii

Foreword In 2011–12, Australia’s food exports were $30 billion or 12 per cent of total merchandise exports. Preliminary ABARES projections indicate that world agrifood consumption and imports are likely to increase markedly to 2050, with relatively strong growth in food demand in the Asian region. ABARES is undertaking more detailed assessments on the outlook in the What Asia Wants project.

This study is a preliminary assessment of infrastructure and Australia’s food industry with a focus on:

identifying issues that may affect the pattern of agricultural production in Australia and the implications for infrastructure requirements

examining impediments to private provision of infrastructure that would support growth in Australia’s agrifood industry.

The focus in this study is on the role of economic infrastructure—transport, water, energy and telecommunications facilities—in the future development of Australia’s food industry. This study identifies key possible research directions for future work that would assess impediments to infrastructure and identify policy response options that would support growth in Australia’s food production and processing industry. ABARES, in collaboration with the CSIRO, is also undertaking more detailed assessments of supply chains in northern Australia in the Northern Australia Food and Fibre Supply Chains study.

Kim Ritman Acting Executive Director November 2013

Infrastructure and Australia’s food industry: Preliminary economic assessment

iv

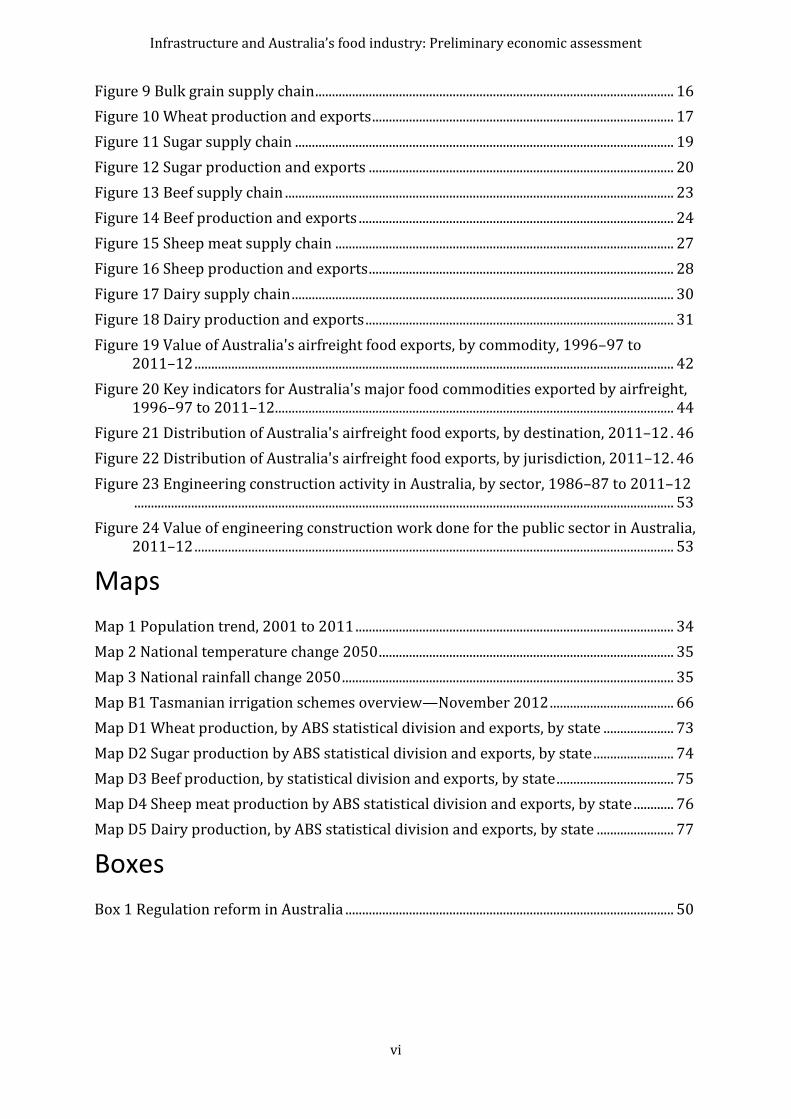

Contents

Summary ............................................................................................................................................................ 1

1 Introduction .......................................................................................................................................... 4

2 Background............................................................................................................................................ 5

Key economic linkages in Australia’s food market ................................................................ 5

Global food demand to 2050 ........................................................................................................... 5

Australia’s food production and trade ........................................................................................ 7

Australia’s key food and infrastructure industries ............................................................. 10

3 Regional distribution of Australia’s food production......................................................... 13

Methodology and data .................................................................................................................... 13

Wheat .................................................................................................................................................... 14

Sugar...................................................................................................................................................... 18

Beef ........................................................................................................................................................ 21

Sheep meat .......................................................................................................................................... 25

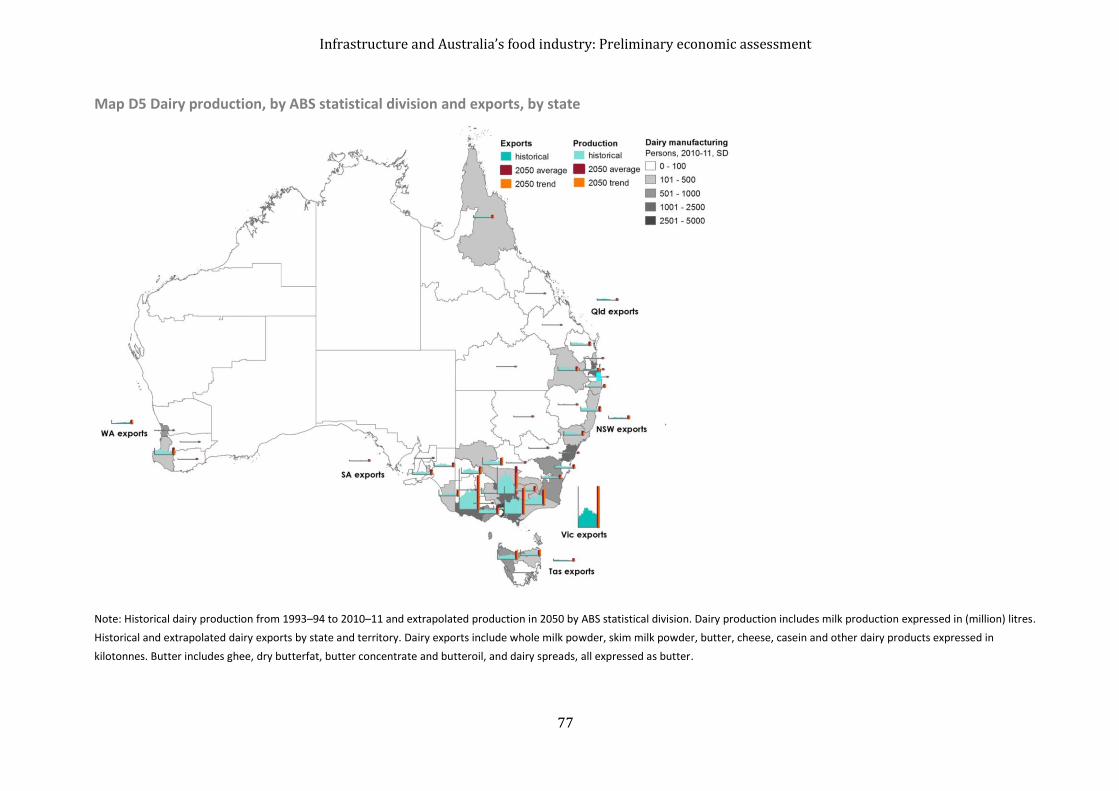

Dairy ...................................................................................................................................................... 28

Crosscutting issues .......................................................................................................................... 32

4 Case studies—infrastructure’s role in expanding production ....................................... 36

Tasmania ............................................................................................................................................. 36

Victorian greenhouse protected cropping.............................................................................. 38

Australia’s airfreight exports of food ........................................................................................ 42

5 Economic issues in infrastructure investment and Australia’s food industry ......... 48

Economic rationale for government intervention............................................................... 48

Broad policy reform processes in Australia........................................................................... 49

Commercialisation options in infrastructure industries .................................................. 50

Private participation in infrastructure investment in Australia .................................... 52

Economic issues and infrastructure policy—previous studies ...................................... 55

6 Conclusion ........................................................................................................................................... 59

Appendix A Infrastructure data sources ............................................................................................ 61

Appendix B Case study for Tasmania—consultations and irrigation projects.................... 63

Appendix C Infrastructure and key food industries: ABS input-output data ....................... 67

Appendix D Production and exports of key food commodities to 2050, by jurisdiction . 70

Appendix E Public-private partnership arrangements ................................................................ 78

References ...................................................................................................................................................... 80

Tables

Table 1 Australia's gross value of production in agriculture, fisheries and forestry, food and non-food, 2011–12 ..................................................................................................................... 7

Table 2 Australia's food trade, by commodity, 2011–12 ................................................................ 9

Table 3 Output and employment in food and infrastructure industries in Australia, 2011–12 ............................................................................................................................................... 10

Infrastructure and Australia’s food industry: Preliminary economic assessment

v

Table 4 Average annual beef input, output and productivity growth, by region, 1977–78 to 2010–11 .......................................................................................................................................... 22

Table 5 Average annual productivity growth in Australia’s dairy industry, by jurisdiction, 1978-79 to 2010-11 ........................................................................................................................ 29

Table 6 Key indicators for Australia's airfreight food exports, 1996–97 and 2011–12 .. 43

Table 7 Airfreight and Australia's food trade, by commodity, 2011–12 ............................... 45

Table 8 Ownership and management aspects of key commercialisation options ............. 52

Table 9 Value of engineering construction work done in Australia, by sector, 2011–12 ............................................................................................................................................... 54

Table A1 Infrastructure data sources from key agencies ............................................................ 61

Table B1 Recently completed, existing and planned irrigation projects in Tasmania ..... 65

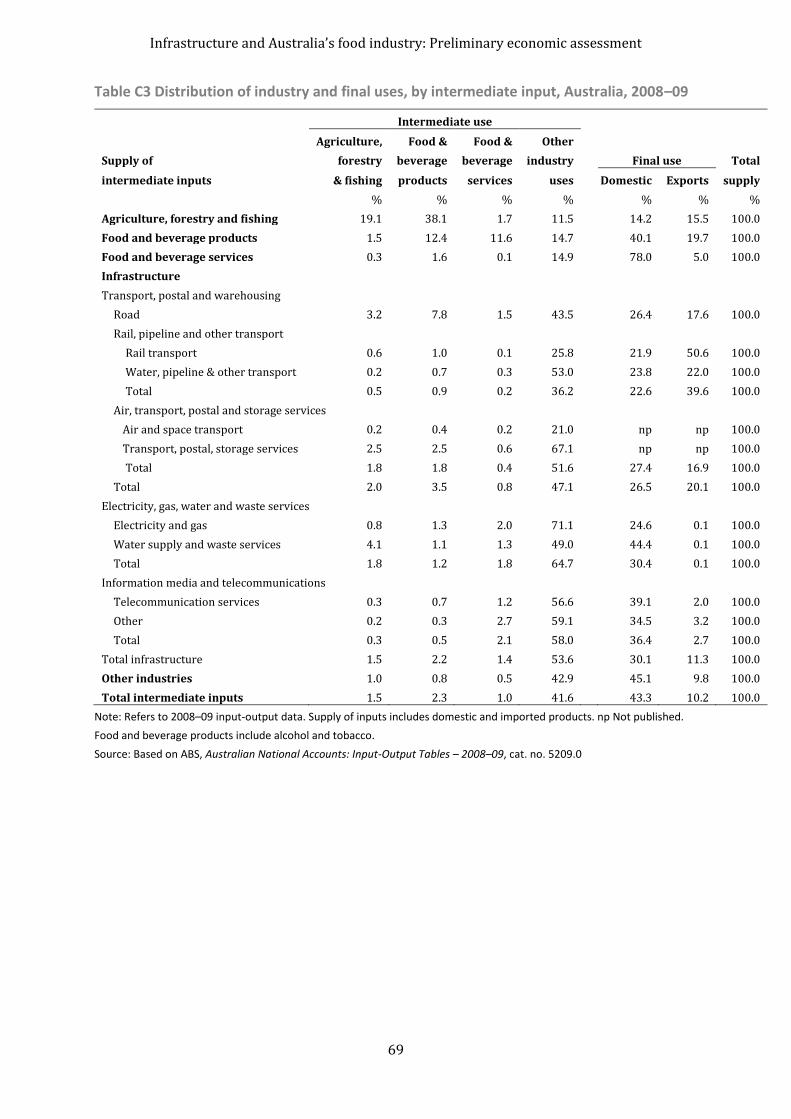

Table C1 Value of industry and final uses of intermediate inputs in Australia, 2008–09 ............................................................................................................................................... 67

Table C2 Distribution of intermediate inputs, by Industry and final use activity, Australia, 2008–09 .......................................................................................................................... 68

Table C3 Distribution of industry and final uses, by intermediate input, Australia, 2008–09 ............................................................................................................................................... 69

Table D1 Production and exports of wheat in 2050, average and trend approaches, by jurisdiction .......................................................................................................................................... 70

Table D2 Production and exports of sugar in 2050, average and trend approaches, by jurisdiction .......................................................................................................................................... 71

Table D3 Production and exports of beef and veal in 2050, average and trend approaches, by jurisdiction .......................................................................................................... 71

Table D4 Production and exports of sheep meat in 2050, average and trend approaches, by jurisdiction .................................................................................................................................... 72

Table D5 Production and exports of dairy in 2050, average and trend approaches, by jurisdiction .......................................................................................................................................... 72

Figures

Figure 1 Key economic linkages in Australia's food market .......................................................... 5

Figure 2 ABARES preliminary projections for world agrifood consumption and imports, 2007 and 2050 ..................................................................................................................................... 6

Figure 3 ABARES preliminary projections for Australia's major agricultural exports, by commodity, 2007 and 2050 ............................................................................................................ 6

Figure 4 Agriculture, fisheries and forestry—food and non-food commodities and uses. 7

Figure 5 Value of Australia's food exports, by commodity, 1996–97 to 2011–12 ................ 8

Figure 6 Leading countries in Australia's food trade, 2011–12 ................................................... 8

Figure 7 Distribution of uses of food products and services in Australia, 2008–09 ......... 11

Figure 8 Distribution of infrastructure input costs for key food industries in Australia, 2008–09 ............................................................................................................................................... 12

Infrastructure and Australia’s food industry: Preliminary economic assessment

vi

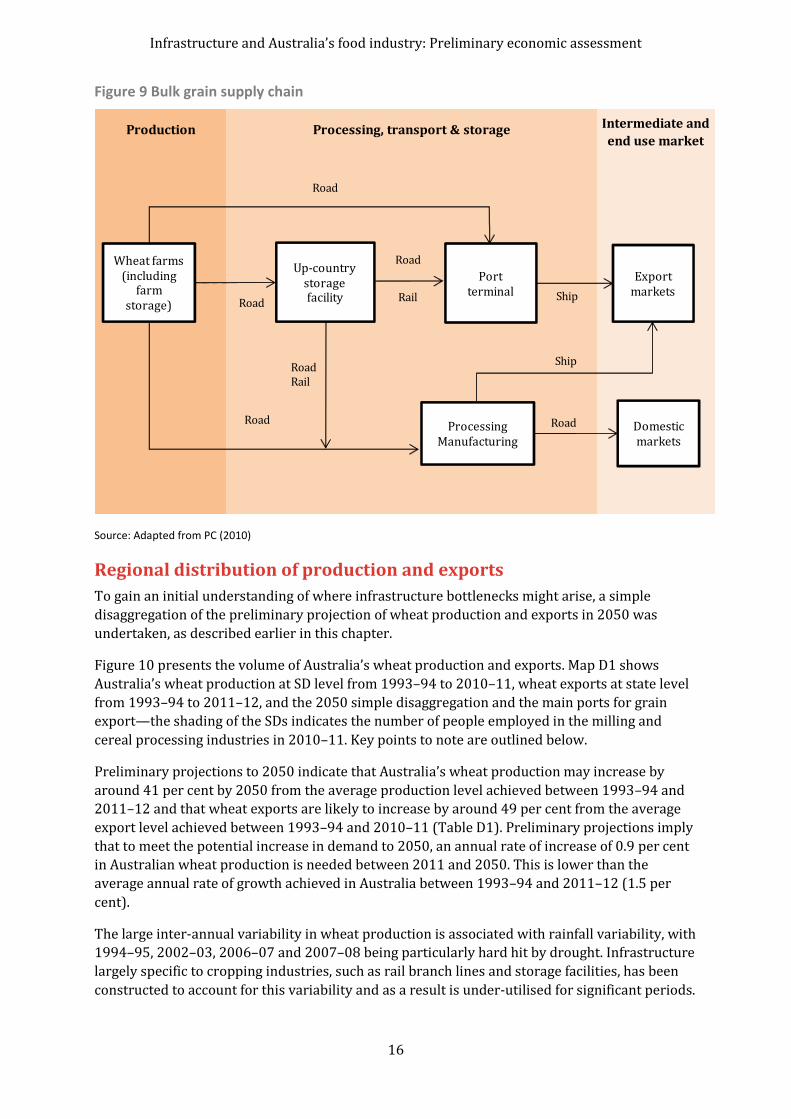

Figure 9 Bulk grain supply chain ........................................................................................................... 16

Figure 10 Wheat production and exports .......................................................................................... 17

Figure 11 Sugar supply chain ................................................................................................................. 19

Figure 12 Sugar production and exports ........................................................................................... 20

Figure 13 Beef supply chain .................................................................................................................... 23

Figure 14 Beef production and exports .............................................................................................. 24

Figure 15 Sheep meat supply chain ..................................................................................................... 27

Figure 16 Sheep production and exports ........................................................................................... 28

Figure 17 Dairy supply chain .................................................................................................................. 30

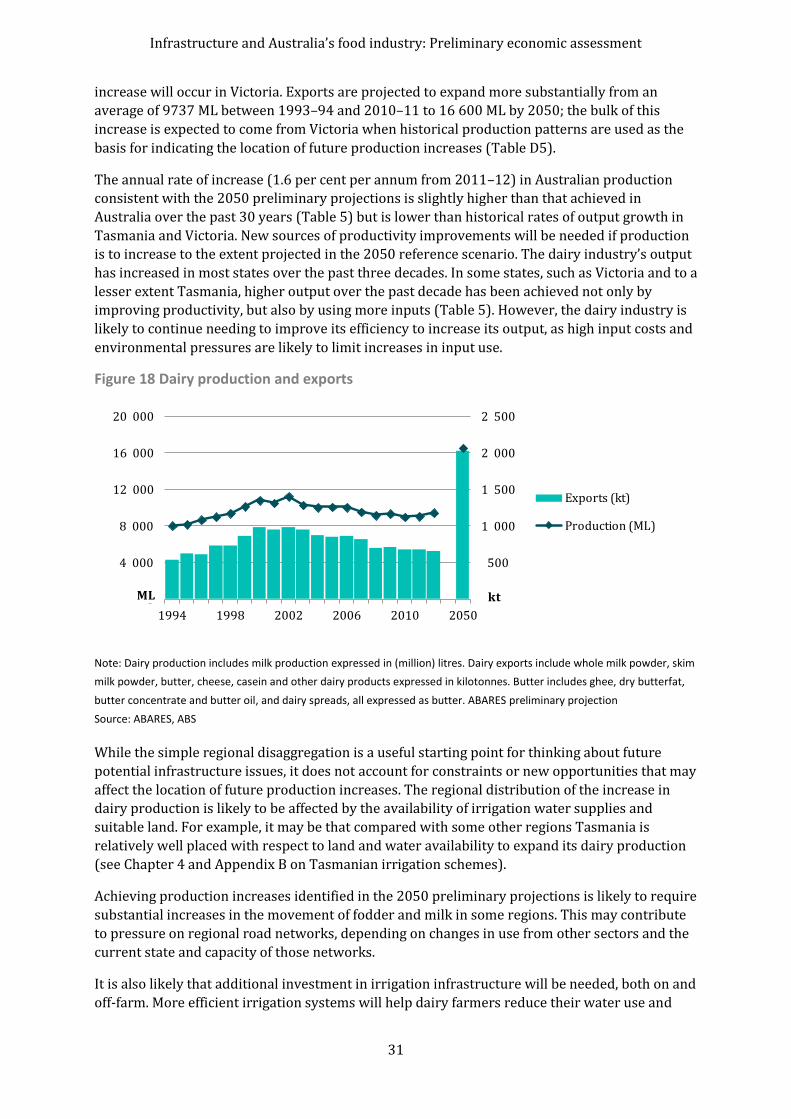

Figure 18 Dairy production and exports ............................................................................................ 31

Figure 19 Value of Australia's airfreight food exports, by commodity, 1996–97 to 2011–12 ............................................................................................................................................... 42

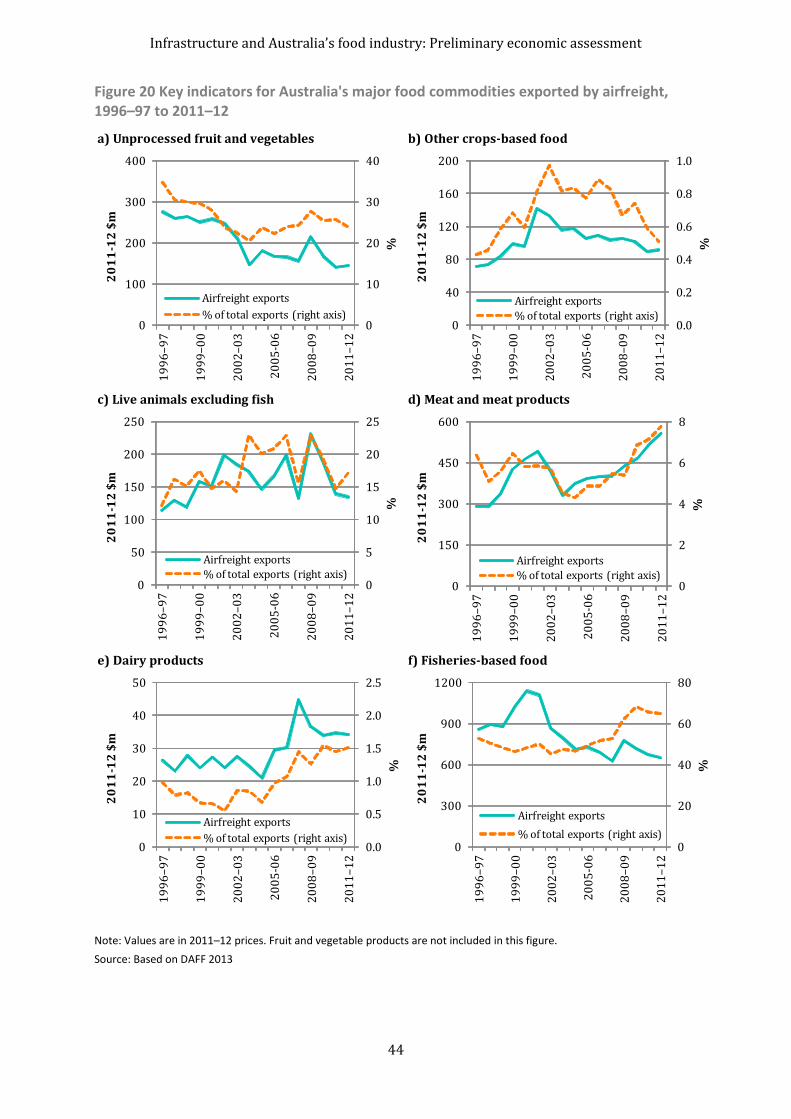

Figure 20 Key indicators for Australia's major food commodities exported by airfreight, 1996–97 to 2011–12....................................................................................................................... 44

Figure 21 Distribution of Australia's airfreight food exports, by destination, 2011–12 . 46

Figure 22 Distribution of Australia's airfreight food exports, by jurisdiction, 2011–12 . 46

Figure 23 Engineering construction activity in Australia, by sector, 1986–87 to 2011–12 ................................................................................................................................................................. 53

Figure 24 Value of engineering construction work done for the public sector in Australia, 2011–12 ............................................................................................................................................... 53

Maps

Map 1 Population trend, 2001 to 2011 ............................................................................................... 34

Map 2 National temperature change 2050 ........................................................................................ 35

Map 3 National rainfall change 2050 ................................................................................................... 35

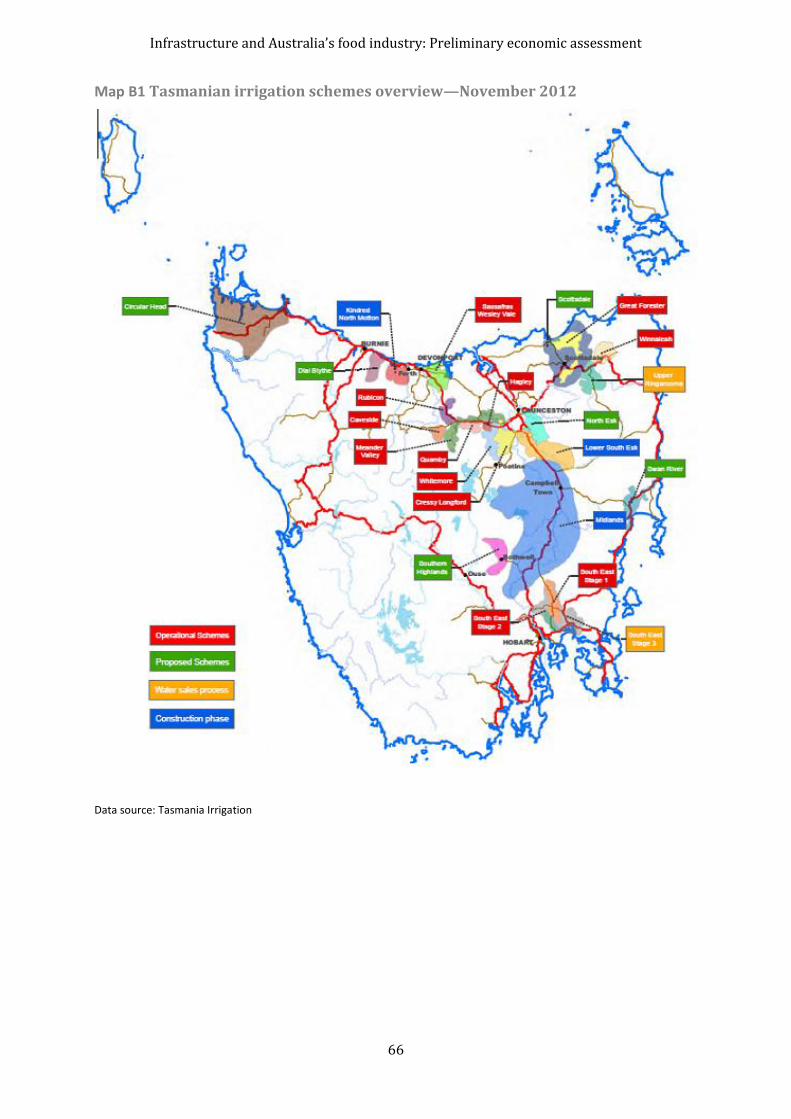

Map B1 Tasmanian irrigation schemes overview—November 2012 ..................................... 66

Map D1 Wheat production, by ABS statistical division and exports, by state ..................... 73

Map D2 Sugar production by ABS statistical division and exports, by state ........................ 74

Map D3 Beef production, by statistical division and exports, by state ................................... 75

Map D4 Sheep meat production by ABS statistical division and exports, by state ............ 76

Map D5 Dairy production, by ABS statistical division and exports, by state ....................... 77

Boxes

Box 1 Regulation reform in Australia .................................................................................................. 50

Infrastructure and Australia’s food industry: Preliminary economic assessment

1

Summary In 2011–12, Australia’s food exports were $30 billion or 12 per cent of total merchandise

exports. Preliminary ABARES projections indicate that world agrifood consumption and imports are likely to increase markedly to 2050, with relatively strong growth in food demand in the Asian region. Ongoing research in ABARES is examining the outlook for the world agrifood market to 2050 and assessing the implications for Australia’s food exports.

A key to realising potential growth opportunities is to ensure Australia’s infrastructure and biosecurity systems will support a growing food industry, moving food cost-effectively and efficiently to markets and supporting new export opportunities.

This study aims to identify key future research directions and provide a preliminary assessment of infrastructure and Australia’s food industry with a focus on:

- identifying issues that may affect the pattern of agricultural production in Australia and the implications for infrastructure requirements

- examining impediments to private provision of infrastructure that would support growth in Australia’s agrifood industry.

It is intended that subsequent work will assess impediments to infrastructure and identify policy response options that would support growth in Australia’s food production and processing industries.

Economic infrastructure—transport, water, energy and telecommunications facilities—provides essential services to a wide range of economic activities, including Australia’s domestic and international food supply chains. In 2008–09, the latest year available, infrastructure services accounted for 11 per cent of total intermediate input costs in the agriculture, forestry and fishing sector, 10 per cent in the food processing industry and 14 per cent in the food services industry (includes storage facilities).

Regional distribution of Australia’s food production

The potentially significant expansion of Australian production and exports of key agricultural commodities—wheat, sugar, beef, sheep meat and dairy—will increase pressure on the infrastructure that currently supports these supply chains.

Wheat—while current distribution networks would appear to be adequate to process future wheat production in years with average seasonal conditions, additional capacity is likely to be needed in good years.

Sugar—to accommodate significant increases in production and exports of sugar, improvements in handling capacities may be needed along the supply chain.

Beef and sheep meat—as beef and sheep meat production increases it will be important to address issues in the livestock supply chain, including network connectivity with major supply chain points for high productivity vehicles, the condition of roads and the competition for access to ports.

Dairy—achieving substantial dairy production increases is likely to require substantial increases in the movement of fodder and milk in some regions which would contribute to pressure on regional road networks.

Infrastructure and Australia’s food industry: Preliminary economic assessment

2

Infrastructure that allows food to be moved cost-effectively and efficiently to markets will be important in making the most of opportunities presented by rapidly growing Asian markets.

The road network is of particular importance to food supply chains and as production and exports expand it will become increasingly important that issues affecting performance are addressed. These include connectivity across the road network and with other transport modes, road and rail pricing distortions, funding arrangements and the integration of planning and investment across modes.

- The potential expansion of production in areas currently without adequate infrastructure presents additional challenges. For example, a significant expansion of beef production in northern Australia would need to be supported by large infrastructure investments. Similarly, to achieve substantial increases in dairy production it is likely that additional investment in irrigation infrastructure will be needed, both on and off-farm.

Case studies

The case studies conducted in Tasmania and in the Victorian greenhouse protected cropping industry highlight the need to address issues related to multi-use infrastructure for production expansion. These issues include infrastructure access pricing and availability.

Further infrastructure investments in Tasmania are only viable if certain volume thresholds can be met and infrastructure use can be spread throughout the year. Even when viable infrastructure investments are available, making investments happen requires knowledge of production and consumption and the mechanisms to match this knowledge to funds.

The value of Australia’s airfreight food exports was $1.6 billion in 2011–12. International food supply chains based on air transport have increased in importance over the past several years for several food commodities. Australia’s airfreight exports of fruit and vegetables, livestock-based food and fisheries-based food accounted for 12.2 per cent of total food exports in 2011–12, compared with 9.4 per cent in 2004–05.

- Airfreight is a cost effective transport option for high value, low volume food products where food quality is dependent on timely delivery to the end-use market, and where the price premium received for the quality attributes of the food product is sufficient to justify the higher transport cost.

- Future growth in Australia’s airfreight food exports will be influenced by market access and biosecurity policy arrangements, investment in domestic high value food production and processing activities, and complementary infrastructure investment to support the further development of efficient international supply chains based on air transport.

Economic issues

The economic rationale for government intervention is mainly based on the natural monopoly characteristics of infrastructure industries (an important source of market failure). In a natural monopoly, industry costs tend to be lower if there is a single provider since this avoids costly duplication of infrastructure facilities (such as water storage, treatment and delivery infrastructure).

In recent decades, there has been a broad regulation reform process in Australia that emphasises the important role of reducing the regulatory burden on business and the community. For infrastructure industries, the main aim in policy reform has been to achieve efficient and sustainable pricing and provision of infrastructure services.

Infrastructure and Australia’s food industry: Preliminary economic assessment

3

Public provision of infrastructure services has been the traditional model used in Australia and other OECD countries, although there has been considerable interest in recent decades in reassessing the role of the private sector in infrastructure industries. Commercialisation options mainly represent alternative approaches to addressing the natural monopoly aspects of an infrastructure industry by increasing competitive pressures in the industry.

- Public-private partnerships (PPPs) are important commercialisation options that have the potential to increase competition. Such partnerships mainly refer to arrangements where the government enters into a contractual agreement with a private organisation to provide specified core functions. Public-private partnerships generally have an emphasis on private sector financing of infrastructure projects.

In Australia, private sector participation in infrastructure investment projects has increased in recent decades.

- The value of engineering construction work done for the public sector in all industries increased from $15 billion in 1986–87 to $32 billion in 2011–12 (in 2010–11 prices). Over this period, the private sector’s share of work done for the public sector increased from 34 per cent to 51 per cent.

- In 2011–12, the value of engineering construction work done in infrastructure industries (excluding gas) was $60 billion of which $28 billion (47 per cent) was private activity for the private sector, $16 billion (27 per cent) was private activity for the public sector, and $15 billion (26 per cent) was public activity for the public sector.

Future research directions

Key future research directions that may be considered include:

- Australia’s food production, processing and exports to 2050: implications for infrastructure—undertake a more comprehensive assessment of key supply-side factors influencing the pattern of food production, processing and exports to 2050 in regional and remote areas of Australia, and identify implications for infrastructure requirements. This research would be complementary to the ABARES research on What Asia Wants.

- Integrated modelling by BITRE and ABARES—in this collaborative research, ABARES would focus on integrating food production and processing activities into the BITRE model framework for infrastructure in Australia.

- Food supply chain analysis—a useful area for future research may be to undertake simulations of important aspects of Australia’s food supply chain with a focus on infrastructure requirements to support export growth of key food commodities to 2050. It is beyond the scope of subsequent work to examine specific infrastructure projects.

- Pricing and provision of key food infrastructure services in Australia—assess impediments to investment in infrastructure, including the private provision of infrastructure, and identify policy response options that would support growth in Australia’s domestic and international food supply chains.

There is likely to be an important role in future research to examine the experience in other OECD countries and assess the extent to which the overseas experience provides useful policy implications for Australia.

Infrastructure and Australia’s food industry: Preliminary economic assessment

4

1 Introduction After increasing strongly during the 1990s, the real value of Australia’s food exports fell overall

between 2001–02 and 2009–10 reflecting the impact of drought and increased domestic

demand (Hogan & Morris 2010). With the end of the drought and strong growth in world food

demand, Australia’s food exports have increased strongly over the past two years, from $24

billion in 2009–10 to $30 billion in 2011–12 (ABARES 2013; current prices). Food exports

accounted for 12 per cent of Australia’s total merchandise exports in 2011–12.

Ongoing research in ABARES is examining the outlook for the world agrifood market to 2050

and assessing the implications for Australia’s food exports. Preliminary ABARES projections

indicate that world agrifood consumption may increase by around 77 per cent between 2007

and 2050 (Linehan et al. 2012a, 2013). World food trade is also likely to become more important

in supplying people with their food requirements over this period. Given its geographic

proximity, Australia is well placed to supply additional food to the strongly growing Asian

market.

A key to realising potential growth opportunities is to ensure Australia’s infrastructure and

biosecurity systems will support a growing food industry, moving food cost-effectively and

efficiently to markets and supporting new export opportunities.

This study is a preliminary assessment of infrastructure and Australia’s food industry with a

focus on:

identifying issues that may affect the pattern of agricultural production in Australia and the implications for infrastructure requirements

examining impediments to private provision of infrastructure that would support growth in Australia’s agrifood industry.

It is intended that subsequent work will assess impediments to infrastructure and identify policy

response options that would support growth in Australia’s food production and processing

industry.

Infrastructure facilities provide basic services to industry and households. This study focuses on

key economic infrastructure including transport, water, energy and telecommunications

facilities (consistent with the coverage of Australian infrastructure statistics in BITRE 2012):

Economic infrastructure incorporates the physical structures from which goods and associated services are produced that enter as common inputs to many industries, and which play a large part in determining efficiency, industry costs and levels of production. (Chan et al. 2009, p. 3)

This report presents relevant information and examines key aspects relating to infrastructure in

Australia’s food supply chain including: background information (Chapter 2); the regional

pattern of Australia’s food production, processing and exports, including a comparison of

historical outcomes with 2050 preliminary projections (Chapter 3); case studies (Chapter 4);

economic issues relating to the pricing and provision of infrastructure in Australia’s food supply

chain (Chapter 5); and concluding comments, including identifying key future research

directions (Chapter 6). Major infrastructure data sources are listed in Appendix A and

background information on the case study for Tasmania is provided in Appendix B.

Infrastructure and Australia’s food industry: Preliminary economic assessment

5

2 Background This chapter provides background information on global food demand to 2050, Australia’s food

production and trade, and economic linkages between key food and infrastructure industries.

Key economic linkages in Australia’s food market

Australia’s food supply chain includes food producers, processors, distributors and service

providers (Figure 1). Australia is a net food exporter—between 2006–07 and 2008–09, around

60 per cent of Australia’s agricultural production was exported and around 54 per cent of food

production was exported (Penm et al. 2010). Consistent with other physical supply chains, the

food supply chain is highly dependent on a range of infrastructure for continuity of operation

(Bartos et al. 2011).

Figure 1 Key economic linkages in Australia's food market

Global food demand to 2050

The world’s long-term food requirements are likely to be substantial, particularly as the world

population is projected to increase from around 7 billion in 2011 to 9.3 billion in 2050 and

10.1 billion in 2100 (UN 2011; medium variant). By 2050, world agricultural production may

need to increase by 70 per cent to meet the food security demands of the growing world

population (HLPE 2011).

In ongoing research, ABARES is examining the outlook for the world agrifood market to 2050

and assessing the implications for Australia’s food exports. Preliminary ABARES projections

indicate that, between 2007 and 2050, world agrifood consumption may increase by 77 per cent

or 1.3 per cent a year on average (in 2007 US dollars) (Linehan et al. 2013, 2012,). Higher

demand in Asia accounts for over two-thirds of the projected increase in world food demand.

World consumption is projected to increase most strongly for fruit and vegetables (annual

average growth rate of 1.2 per cent), meat (1.7 per cent), dairy products (1.1 per cent), cereals

(1.8 per cent), fish (1.7 per cent) and vegetable oils (1.4 per cent) (Figure 2a).

Farmers & fishers

Key influences: prices, availability &

cost of inputs (e.g. land, water, labour,

energy), technologies, climate

& other risks

Agriculture & fishing

Food processors

Economies of scale by accessing farm

produce from different regions;

value adding (product branding, quality premium);

innovation

Manufacturing

Consumers

Key influences: food prices, population,

incomes, tastes and preferences

Food security: reliable access to affordable, safe &

nutritious food

Households

Key economic issues: global food security, trade and market access

Outlook to 2050: strong food demand growth in the Asian region

Exports

Food demand in Australia

Food supply in Australia

World food market

Imports

Distributors & service providers

Efficient & diversified distribution network

(e.g. transport & storage, wholesale &

retail trade); restaurants etc; food

tourism, R&D

Services

Infrastructure and Australia’s food industry: Preliminary economic assessment

6

International trade is likely to become more important in supplying people with food—

preliminary projections indicate the share of world consumption sourced from imports may

increase from around 10 per cent in 2007 to 15 per cent in 2050. World agrifood imports are

projected to increase by 2.4 per cent a year on average between 2007 and 2050 with significant

increases in world imports of fruit and vegetables (annual average growth rate of 1.5 per cent),

meat (4.2 per cent), dairy products (1.8 per cent), cereals (5.1 per cent), fish (2.1 per cent) and

vegetable oils (1.8 per cent) (Figure 2b).

Figure 2 ABARES preliminary projections for world agrifood consumption and imports, 2007 and 2050

Data source: Linehan et al. 2012a

Higher global agrifood demand is expected to provide significant export market opportunities

for the domestic food industry, particularly given Australia’s geographic proximity to the

strongly growing Asian market. ABARES preliminary projections indicate Australia’s agricultural

exports are likely to increase most strongly for beef, wheat, dairy products, sheep meat and

sugar (in 2007 US dollars) (Figure 3). Preliminary ABARES projections for the quantity of

Australia’s agrifood production and exports to 2050 are provided in Chapter 3.

Figure 3 ABARES preliminary projections for Australia's major agricultural exports, by commodity, 2007 and 2050

Data source: Linehan et al. 2012a

a) Consumption b) Imports

0 500 1000 1500 2000

Other food

Vegetable meal

Vegetable oils

Fish

Dairy products

Cereals

Meat

Fruit & vegetables

2007 US$b

2050

2007

0 100 200 300

Other food

Vegetable meal

Vegetable oils

Fish

Dairy products

Cereals

Meat

Fruit & vegetables

2007 US$b

2050

2007

0 5 10 15

Sheep meat

Sugar

Dairy products

Wheat

Beef

2007 US$b

2050

2007

Infrastructure and Australia’s food industry: Preliminary economic assessment

7

Australia’s food production and trade

Food production

The agricultural, fisheries and forestry sector produces both food and non-food commodities

(Figure 4). Food commodities may be produced for food use (human consumption, and animal

and fish feed) or non-food use (such as inputs to biofuel production).

Figure 4 Agriculture, fisheries and forestry—food and non-food commodities and uses

In 2011–12, the gross value of Australia’s agricultural, fisheries and forestry production was

$52 billion, comprising food commodity production of around $45 billion (86 per cent of the

total) and estimated non-food commodity production of around $7.5 billion (14 per cent) (Table

1). The gross value of food commodities produced, at least partly, for human consumption was

an estimated $43 billion or 82 per cent of total production in 2011–12 (DAFF 2013; see also

DAFF 2012b).

Table 1 Australia's gross value of production in agriculture, fisheries and forestry, food and non-food, 2011–12

Commodity Value Share of total

$b %

Food commodities

Crops a 24.0 46.1

Livestock and livestock products b 18.3 35.1

Fisheries products c 2.3 4.4

Total food commodity groups 44.5 85.6

Non-food commodity groups

Cotton lint and cottonseed 2.9 5.6

Wool 2.9 5.5

Pearls 0.1 0.2

Forestry products 1.6 3.2

Total non-food commodity groups 7.5 14.4

Agriculture, fisheries and forestry—total

Crops 26.9 51.6

Livestock and livestock products 21.1 40.6

Fisheries products 2.4 4.6

Forestry products 1.6 3.2

Total 52.0 100.0

Note: a Excludes cotton lint and cottonseed. b Excludes wool. c Excludes pearls.

Source: ABARES 2013

Agriculture, fisheries and

forestry

Food commodities

Food use

Human consumption

Animal and fish feed

Non-food use

e.g. biofuels

Non-food commodities

Non-food use

Infrastructure and Australia’s food industry: Preliminary economic assessment

8

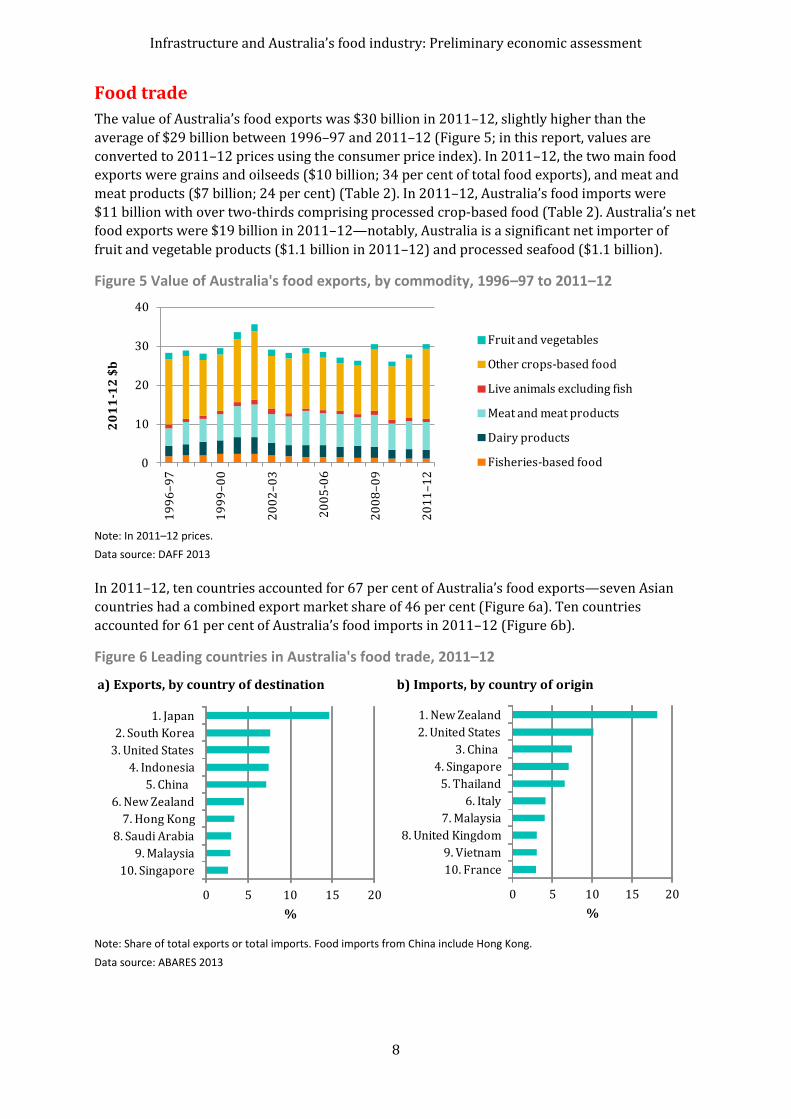

Food trade

The value of Australia’s food exports was $30 billion in 2011–12, slightly higher than the

average of $29 billion between 1996–97 and 2011–12 (Figure 5; in this report, values are

converted to 2011–12 prices using the consumer price index). In 2011–12, the two main food

exports were grains and oilseeds ($10 billion; 34 per cent of total food exports), and meat and

meat products ($7 billion; 24 per cent) (Table 2). In 2011–12, Australia’s food imports were

$11 billion with over two-thirds comprising processed crop-based food (Table 2). Australia’s net

food exports were $19 billion in 2011–12—notably, Australia is a significant net importer of

fruit and vegetable products ($1.1 billion in 2011–12) and processed seafood ($1.1 billion).

Figure 5 Value of Australia's food exports, by commodity, 1996–97 to 2011–12

Note: In 2011–12 prices.

Data source: DAFF 2013

In 2011–12, ten countries accounted for 67 per cent of Australia’s food exports—seven Asian

countries had a combined export market share of 46 per cent (Figure 6a). Ten countries

accounted for 61 per cent of Australia’s food imports in 2011–12 (Figure 6b).

Figure 6 Leading countries in Australia's food trade, 2011–12

Note: Share of total exports or total imports. Food imports from China include Hong Kong.

Data source: ABARES 2013

0

10

20

30

40

19

96

–9

7

19

99

–0

0

20

02

–0

3

20

05

-06

20

08

–0

9

20

11

–1

2

20

11

-12

$b

Fruit and vegetables

Other crops-based food

Live animals excluding fish

Meat and meat products

Dairy products

Fisheries-based food

a) Exports, by country of destination b) Imports, by country of origin

0 5 10 15 20

10. Singapore

9. Malaysia

8. Saudi Arabia

7. Hong Kong

6. New Zealand

5. China

4. Indonesia

3. United States

2. South Korea

1. Japan

%

0 5 10 15 20

10. France

9. Vietnam

8. United Kingdom

7. Malaysia

6. Italy

5. Thailand

4. Singapore

3. China

2. United States

1. New Zealand

%

Infrastructure and Australia’s food industry: Preliminary economic assessment

9

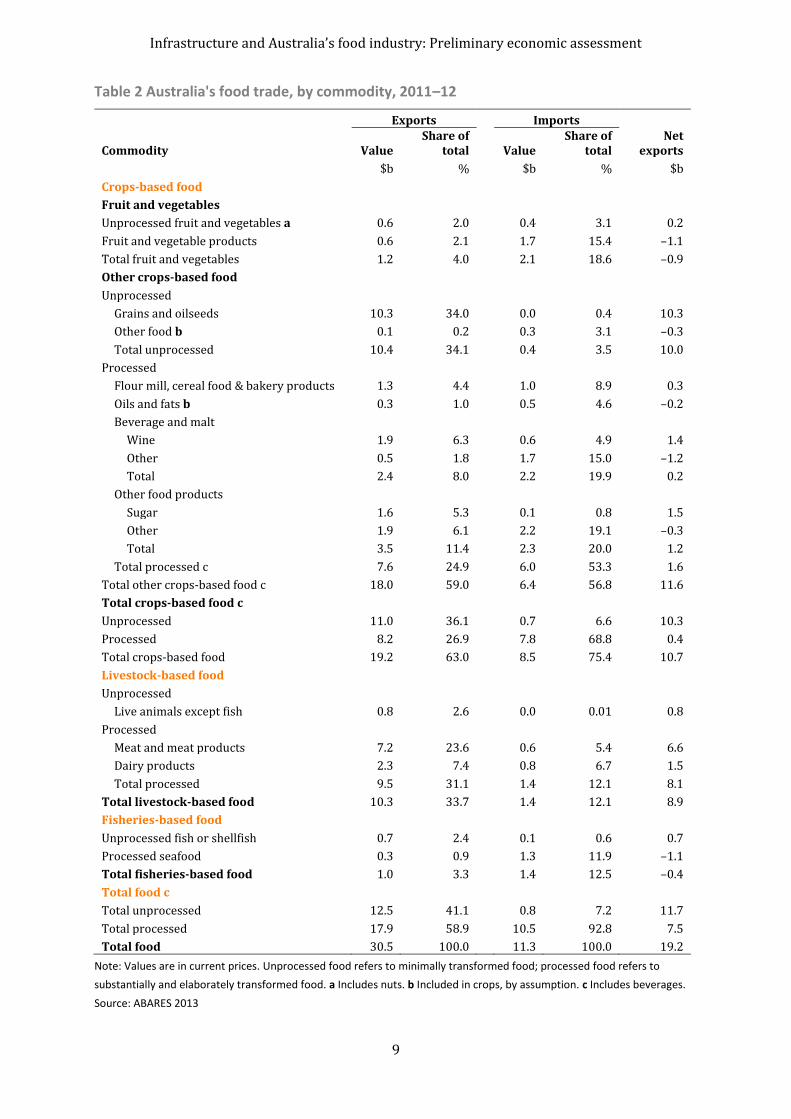

Table 2 Australia's food trade, by commodity, 2011–12

Exports

Imports

Commodity Value

Share of total Value

Share of total

Net exports

$b % $b % $b

Crops-based food

Fruit and vegetables

Unprocessed fruit and vegetables a 0.6 2.0 0.4 3.1 0.2

Fruit and vegetable products 0.6 2.1 1.7 15.4 –1.1

Total fruit and vegetables 1.2 4.0 2.1 18.6 –0.9

Other crops-based food

Unprocessed

Grains and oilseeds 10.3 34.0 0.0 0.4 10.3

Other food b 0.1 0.2 0.3 3.1 –0.3

Total unprocessed 10.4 34.1 0.4 3.5 10.0

Processed

Flour mill, cereal food & bakery products 1.3 4.4 1.0 8.9 0.3

Oils and fats b 0.3 1.0 0.5 4.6 –0.2

Beverage and malt Wine 1.9 6.3 0.6 4.9 1.4

Other 0.5 1.8 1.7 15.0 –1.2

Total 2.4 8.0 2.2 19.9 0.2

Other food products Sugar 1.6 5.3 0.1 0.8 1.5

Other 1.9 6.1 2.2 19.1 –0.3

Total 3.5 11.4 2.3 20.0 1.2

Total processed c 7.6 24.9 6.0 53.3 1.6

Total other crops-based food c 18.0 59.0 6.4 56.8 11.6

Total crops-based food c

Unprocessed 11.0 36.1 0.7 6.6 10.3

Processed 8.2 26.9 7.8 68.8 0.4

Total crops-based food 19.2 63.0 8.5 75.4 10.7

Livestock-based food

Unprocessed

Live animals except fish 0.8 2.6 0.0 0.01 0.8

Processed

Meat and meat products 7.2 23.6 0.6 5.4 6.6

Dairy products 2.3 7.4 0.8 6.7 1.5

Total processed 9.5 31.1 1.4 12.1 8.1

Total livestock-based food 10.3 33.7 1.4 12.1 8.9

Fisheries-based food

Unprocessed fish or shellfish 0.7 2.4 0.1 0.6 0.7

Processed seafood 0.3 0.9 1.3 11.9 –1.1

Total fisheries-based food 1.0 3.3 1.4 12.5 –0.4

Total food c

Total unprocessed 12.5 41.1 0.8 7.2 11.7

Total processed 17.9 58.9 10.5 92.8 7.5

Total food 30.5 100.0 11.3 100.0 19.2

Note: Values are in current prices. Unprocessed food refers to minimally transformed food; processed food refers to

substantially and elaborately transformed food. a Includes nuts. b Included in crops, by assumption. c Includes beverages.

Source: ABARES 2013

Infrastructure and Australia’s food industry: Preliminary economic assessment

10

Australia’s key food and infrastructure industries

In this section, the key food industries are given by the agriculture, forestry and fishing sector

(includes food production), the food and beverage products industry (food processing) and the

food and beverage services industry (food services).

Output and employment

Output (based on gross value added) and employment data for the key food and infrastructure

industries in 2011–12 are given in Table 3. Gross value added is the value of output in an

industry or sector minus the value of goods and services consumed as inputs in the production

process (excluding the consumption of fixed capital) (ABS 2012a).

In 2011–12, the agriculture, forestry and fishing sector and food and beverage products industry

together accounted for 4.0 per cent of Australia’s gross domestic product and 4.9 per cent of

total employment. In the same year, infrastructure industries accounted for 10.0 per cent of

gross domestic product and 8.2 per cent of total employment—the transport, postal and

warehousing industry was the largest infrastructure industry (4.9 per cent of gross domestic

product), followed by information media and telecommunications (2.8 per cent), electricity and

gas (1.4 per cent) and water supply and waste services (0.9 per cent).

Table 3 Output and employment in food and infrastructure industries in Australia, 2011–12

Output

Employment

Industry/Aggregate Value Share of total Level Share of total

$b % 000 %

Agriculture, forestry and fishing 35 2.4 334 2.9

Food and beverage products 23 1.6 227 2.0

Accommodation and food services 34 2.3 763 6.7

Infrastructure

Transport, postal and warehousing

Road 20 1.4 – –

Rail, pipeline and other transport 11 0.8 – –

Air and space transport 8 0.5 – –

Transport, postal and storage services 32 2.2 – –

Total 71 4.9 565 5.0

Electricity, gas, water and waste services

Electricity and gas 21 1.4 – –

Water supply and waste services 13 0.9 – –

Total 33 2.3 153 1.3

Information media and telecommunications 41 2.8 216 1.9

Total infrastructure 146 10.0 935 8.2

Other industries 1117 76.9 9153 80.2

Gross value added at basic prices 1353 93.2 – –

Taxes less subsidies on products 94 6.5 – –

Statistical discrepancy 5 0.3 – –

Gross domestic product/total persons 1452 100.0 11413 100.0

Note: Output is industry gross value added (chain volume measures); other industries include ownership of dwellings.

Employment is thousands of persons; average of four quarters (based on original data). Food and beverage products

include alcohol and tobacco.

Sources: ABS 5206.0 (Australian National Accounts: National Income, Expenditure and Product) and 6291.0 (Labour Force)

Infrastructure and Australia’s food industry: Preliminary economic assessment

11

Food supply chain—main uses of food products and services in Australia

ABS input-output data describe the production and subsequent use of all goods and services in

the Australian economy (ABS 2012a). Input-output data for Australia in 2008–09, the latest year

available, are given in Appendix C. Intermediate inputs are domestic and imported products that

are used by industry (intermediate use) and/or in final use categories (domestic use and

exports).

The main uses of food products and services in 2008–09 are given in Figure 7 (based on share of

total supply; see Table C3). The main use of agriculture, forestry and fishing products was in the

food and beverage products industry (38 per cent) (Figure 7a). The main use of food and

beverage products was in the domestic market, particularly household consumption (40 per

cent) (Figure 7b). Food and beverage services were mainly used in the domestic market,

particularly household consumption (78 per cent) (Figure 7c).

The food supply chains for five major export commodities in Australia are discussed further in

Chapter 3.

Figure 7 Distribution of uses of food products and services in Australia, 2008–09

Note: Based on share of total supply in 2008–09; total supply is given in each subheading. Figure includes intermediate and

final uses of food products and services.

Data source: ABS, Australian National Accounts: Input-Output Tables – 2008–09, cat. no. 5209.1

a) Agriculture, forestry and fishing products ($67 billion)

b) Food and beverage products ($99 billion)

c) Food and beverage services ($55 billion)

0 20 40 60 80

Final use - export market

Final use - domestic market

Other industry uses

Food and beverage services

Food and beverage products

Agriculture, forestry and fishing

%

0 20 40 60 80

Final use - export market

Final use - domestic market

Other industry uses

Food and beverage services

Food and beverage products

Agriculture, forestry and fishing

%

0 20 40 60 80

Final use - export market

Final use - domestic market

Other industry uses

Food and beverage services

Food and beverage products

Agriculture, forestry and fishing

%

Infrastructure and Australia’s food industry: Preliminary economic assessment

12

Infrastructure inputs to key food industries

In 2008–09, infrastructure inputs were valued at $4.2 billion in the agricultural, forestry and

fishing sector (10.6 per cent of total intermediate inputs), $6.3 billion in the food and beverage

products industry (10.1 per cent) and $3.9 billion in the food and beverage services industry (14

per cent) (Table C1 and Table C2). Road transport and transport, postal and storage services

were the two main infrastructure costs in the food production and processing industries, while

information media and telecommunications was the main infrastructure cost in the food

services industry (Figure 8).

Notably, these food production, processing and services industries used around 5.1 per cent of

the total value of infrastructure services supplied in 2008–09 (Table C3).

Figure 8 Distribution of infrastructure input costs for key food industries in Australia, 2008–09

Note: Total infrastructure costs in 2008–09 are given in each subheading.

Data source: Based on ABS, Australian National Accounts: Input-Output Tables – 2008–09, cat. no. 5209.1

a) Agriculture, forestry and fishing sector ($4.2 billion)

b) Food and beverage products industry ($6.3 billion)

c) Food and beverage services industry ($3.9 billion)

0 10 20 30 40 50 60

Information media & telecommunications

Water supply & waste services

Electricity & gas

Transport, postal & storage services

Air & space transport

Rail, pipeline & other transport

Road transport

%

0 10 20 30 40 50 60

Information media & telecommunications

Water supply & waste services

Electricity & gas

Transport, postal & storage services

Air & space transport

Rail, pipeline & other transport

Road transport

%

0 10 20 30 40 50 60

Information media & telecommunications

Water supply & waste services

Electricity & gas

Transport, postal & storage services

Air & space transport

Rail, pipeline & other transport

Road transport

%

Infrastructure and Australia’s food industry: Preliminary economic assessment

13

3 Regional distribution of Australia’s food production

By 2050 it is likely that strong growth in global food demand will drive higher world agrifood

prices and production and lead to increases in Australian agricultural production and exports

(Linehan et al. 2012a). It will be important to understand the potential regional distribution of

this increased production, particularly in relation to the future capacity of infrastructure

supporting commodity supply chains. In this chapter the supply chains of five selected

commodities—wheat, sugar, beef, sheep meat and dairy products—are discussed and a simple

methodology is used to disaggregate preliminary projections of increases in production and

exports to 2050 to specific regions in order to facilitate a discussion of potential infrastructure

challenges.

Methodology and data

A discussion of potential future infrastructure challenges facing the agriculture sector would

ideally be informed by a set of long-term regional production projections for key commodities.

However, long-term projections at a regional level are not currently available. To facilitate a

discussion of potential infrastructure challenges, preliminary results from the ABARES agrifood

model of global agricultural supply, demand and trade (see Linehan et al. 2012b) are used.

At a national level, exports of beef, wheat, dairy products, sheep meat and sugar are projected to

have the largest increase in real value (Linehan et al. 2012a) with the real export value of beef

and dairy products projected to more than double by 2050 (Figure 3). Due to their large

potential increases in real value, these five commodities are the focus of the current scoping

study but it is worth noting that future growth in production of other commodities might also be

affected by infrastructure constraints; this may be explored in future research.

As Linehan et al. (2012a) highlighted, these projections are conditional on a set of assumptions

about likely trends, particularly in the global macro-economic environment and agricultural

technological change, together with assumptions about the sensitivity of agricultural demand

and supply to changes in incomes and prices. As such, Linehan et al. (2012a) suggest this

‘conditional baseline’ may serve as a starting point for scenario analysis. The ABARES agrifood

model is being further developed, so the projections of Linehan et al. (2012a) and those used in

this report should be viewed as preliminary.

As output from the ABARES agrifood model is only available at a national level, it is necessary to

‘downscale’ the results to explore implications at a regional level.

Long annual time series of historical production are available at the ABS Statistical Division (SD)

level. The preliminary projections for 2050 from the ABARES agrifood model have been

disaggregated across the 60 SDs that partition Australia, using two simple approaches.

The ‘average’ approach assumes that an SD’s share of Australia’s production in 2050 is equal to its average share of production from the past 10 years (2000–01 to 2010–11).

The ‘trend’ approach extrapolates the linear trend in an SD’s share of Australia’s production from 1993–94 to 2010–11 to 2050, but constrains it to within 75 to 125 per cent of the 10-year average share of production.

Infrastructure and Australia’s food industry: Preliminary economic assessment

14

Where historic trends in the share of Australian production accounted for by each region are

expected to continue, the trend approach would usually be preferred. However, the continuation

of historic trends may not be appropriate in all cases and the average approach may be more

suitable. Substantial differences in the results produced using each approach indicate significant

trends in historic data. Development of modelling capacity that produces results at a regional

level and incorporates information on constraints to production (such as availability of suitable

land and water resources) is required to improve on the simple approaches employed here.

The preliminary projections for export quantities in 2050 were also disaggregated across the six

states and the Northern Territory using the same approaches.

The ‘simple disaggregation’ is presented with annual time series of historical production and

exports from 1993–94 to 2010–11 in each commodity regional distribution map in Appendix

D—employment in the corresponding food processing industry in 2010–11 is indicated by the

shading of the SDs. Summary information on production and exports under the average and

trend approaches is also provided in Appendix D.

The approaches taken here to disaggregate preliminary national projections will not capture

future major new development areas or major shifts in the pattern of production (for example,

as a result of climate change), but may be considered a first approximation to how potential

production increases may be distributed and provide a way to explore potential future

infrastructure challenges.

The discussion of potential infrastructure issues associated with an expansion in production of

each commodity, as presented later in this chapter, draws on previous studies where possible.

Further analysis is needed to identify areas where additional investment in infrastructure may

be required. However, the availability of data needed for such analysis is currently limited. In

particular, data on freight movements (detailed data on the products being transported and

origin and destination of the products) is not comprehensive and limits the understanding of

transport requirements for the agriculture sector and the broader freight task (Tulloh & Pearce

2011).

Further research could undertake a more detailed analysis of potential infrastructure

constraints in agrifood supply chains, including consideration of potential scenarios for the

regional pattern of future growth in agricultural production and exports (such as the potential

impacts of climate change on the location of agricultural production).

Wheat

The wheat industry, its supply chain and the infrastructure linking each stage are outlined

below. The simple disaggregation of the preliminary projections of national wheat production

and exports to 2050 is then presented, followed by a brief discussion of potential infrastructure

issues associated with an expansion in production.

Wheat production and exports

Wheat is the most significant grain crop grown in Australia in terms of area sown, volume of

grain produced and value of the crop. In 2011–12 the total area of wheat sown in Australia was

13.9 million hectares, with 29.9 million tonnes of production. The estimated value of wheat

production in 2011–12 was $6.78 billion, accounting for 14.1 per cent of the gross value of total

farm production (ABARES 2013).

Infrastructure and Australia’s food industry: Preliminary economic assessment

15

Australia exported 23 million tonnes of wheat in 2011–12, accounting for nearly 77 per cent of

wheat production. The total value of wheat exports was $6.4 billion, equivalent to 16 per cent of

the total value of rural exports (ABARES 2013). Although most wheat produced in Australia is

exported in bulk, the composition of total exports by mode varies across states. Over the five

years to 2008–09, non-bulk exports accounted for about 35 per cent of Victoria’s exports, 30 per

cent of Queensland’s and 20 per cent of New South Wales’ exports. In the same period, non-bulk

exports accounted for only 6–7 per cent of exports from Western Australia and South Australia

(PC 2010).

The wheat industry has undergone significant changes in technology adoption, management

practices, structure and marketing arrangements.

Long-term productivity gains have been achieved through the adoption of new technologies and

management practices in the cropping industry (Hughes et al. 2011). This includes increased use

of fertilisers, seed and crop chemicals, causing materials’ share of all cropping inputs to more

than double since 1977–78. Increased yields have also come from the introduction of low-till

and no-till farming and the introduction of new crop varieties (Dunlop et al. 2004). A shift in the

1980s and 1990s toward much larger and more efficient sowing and harvesting equipment has

been another key contributor to higher productivity (Nossal et al. 2009).

The number of grain farms in Australia declined by 40 per cent between 1977–78 and 2003–04

and the average area operated per farm increased by 50 per cent (Alexander & Kokic 2005).

Increases in average farm size have facilitated productivity growth. The average area cropped

per farm more than doubled over the past two decades, with the highest growth in area

occurring in Western Australia. Larger cropping farms tend to be more productive because of

their greater capacity to adopt new technologies (Sheng et al. 2011), particularly advanced

cropping technologies that are often only suitable for use on farms above a minimum size.

The marketing arrangements for wheat have also undergone significant change. Between 1999

and 2008 the single desk marketing arrangements were dismantled, which has provided

growers with more choices to market grain and manage production and price risk (PC 2010).

Wheat supply chain and infrastructure

Most of Australia’s wheat is supplied through the bulk grain handling system (PC 2010). Figure 9

provides an overview of the bulk grain supply chain.

The supply system starts with farm production and on-farm storage, followed by a network of up-country storage facilities connected by road and rail transport links to manufacturers, processors, port facilities and intermediate and end use markets.

A portion of Australia’s wheat production is stored on-farm or transported directly from the farm gate to processing and manufacturing facilities or a non-bulk grain handler for packing and sale or export in containers and bags.

Export of wheat and processed wheat is mainly by sea freight from port terminals or directly from processing and manufacturing facilities.

Processed wheat products are transported to domestic markets using the road network. The domestic market is now the dominant market segment in New South Wales and Queensland and potentially Victoria (NTC 2009b).

Infrastructure and Australia’s food industry: Preliminary economic assessment

16

Figure 9 Bulk grain supply chain

Source: Adapted from PC (2010)

Regional distribution of production and exports

To gain an initial understanding of where infrastructure bottlenecks might arise, a simple

disaggregation of the preliminary projection of wheat production and exports in 2050 was

undertaken, as described earlier in this chapter.

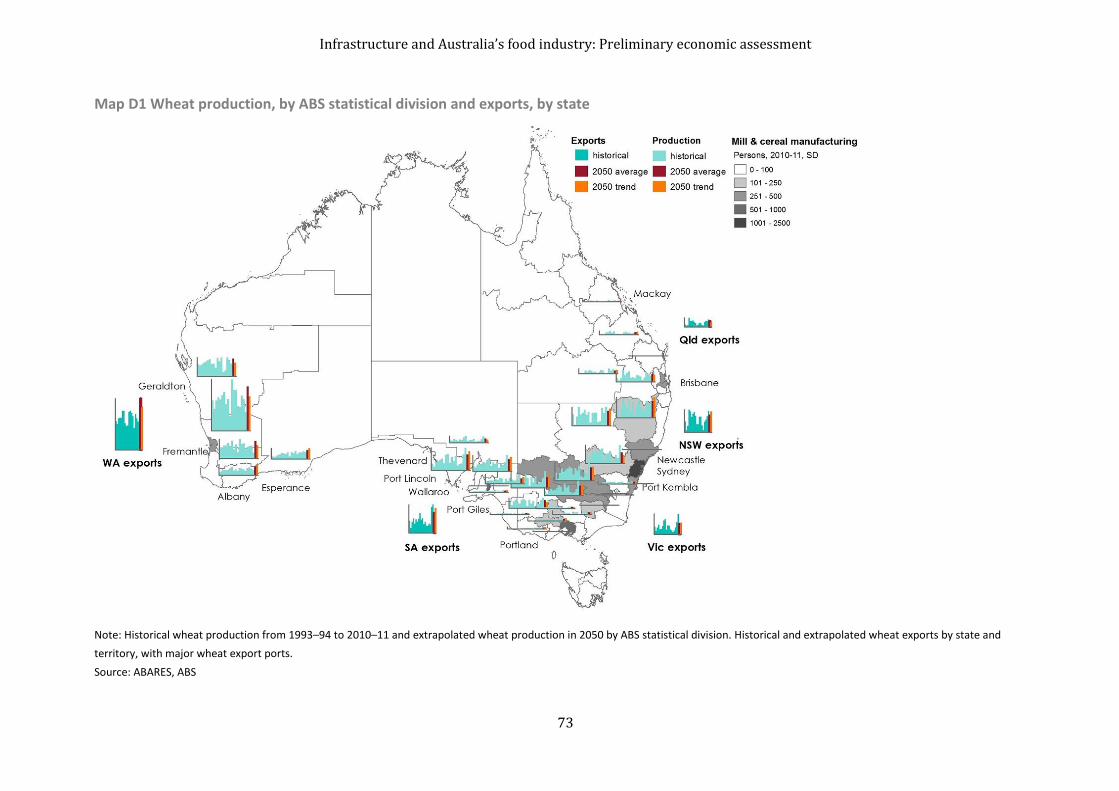

Figure 10 presents the volume of Australia’s wheat production and exports. Map D1 shows

Australia’s wheat production at SD level from 1993–94 to 2010–11, wheat exports at state level

from 1993–94 to 2011–12, and the 2050 simple disaggregation and the main ports for grain

export—the shading of the SDs indicates the number of people employed in the milling and

cereal processing industries in 2010–11. Key points to note are outlined below.

Preliminary projections to 2050 indicate that Australia’s wheat production may increase by

around 41 per cent by 2050 from the average production level achieved between 1993–94 and

2011–12 and that wheat exports are likely to increase by around 49 per cent from the average

export level achieved between 1993–94 and 2010–11 (Table D1). Preliminary projections imply

that to meet the potential increase in demand to 2050, an annual rate of increase of 0.9 per cent

in Australian wheat production is needed between 2011 and 2050. This is lower than the

average annual rate of growth achieved in Australia between 1993–94 and 2011–12 (1.5 per

cent).

The large inter-annual variability in wheat production is associated with rainfall variability, with

1994–95, 2002–03, 2006–07 and 2007–08 being particularly hard hit by drought. Infrastructure

largely specific to cropping industries, such as rail branch lines and storage facilities, has been

constructed to account for this variability and as a result is under-utilised for significant periods.

Production Processing, transport & storage Intermediate and

end use market

Road

Ship

Up-country storagefacility

Port terminal

Export markets

Road Rail

Road

Road

Ship

Road

Domestic markets

Wheat farms (including

farm storage)

Rail

RoadProcessing

Manufacturing

Infrastructure and Australia’s food industry: Preliminary economic assessment

17

The simple disaggregation of the preliminary projections for wheat production and exports in

2050 is of a similar order of magnitude to the recent peak seasons. For example, in Western

Australia, it is projected that by 2050, average wheat production will be 10.8 million tonnes,

slightly lower than the highest production level of the past 10 years (11.4 million tonnes in

2004). However, as the 2050 volumes are an average level with significant inter-annual

variability, they do imply substantial increases in years with good seasonal conditions.

Figure 10 Wheat production and exports

Note: Exports include the grain equivalent of wheat flour. ABARES preliminary projection

Source: ABARES, ABS

Maintaining current distribution networks would appear to be adequate for processing future

production levels in years with average seasonal conditions. However, increased capacity may

be needed in years with good seasonal conditions. In addition, increased international

competition is likely to continue to drive efforts to increase the efficiency of grain handling.

The National Transport Commission identified a number of impediments to supply chain

performance in its Supply Chain Pilots Draft Position Paper (NTC 2009a) which are outlined

below. Wheat/grain production expansion to 2050 is likely to increase the importance of

addressing these issues.

Road and rail pricing distortion is a primary impediment to efficient modal decisions and appropriate capital investment by government and industry. Under current road and rail pricing structures, much of the rural transport network is provided on a subsidised basis. The provision of subsidies makes it difficult for governments to prioritise capital investment and major maintenance needs between individual regional routes, and between rural and urban routes. In addition, for grain transport, governments have to weigh up the need for rail track provision, particularly in lightly populated areas which are already serviced by roads.

Limited integration planning and investment exists across modes in the grain supply chain despite the interdependencies between road and rail investment and between land transport and port investments. For example, the closure of branch lines in the grain networks is not normally considered together with increased road maintenance costs.

Vertical separation between low-volume rail networks and above-rail services provides few benefits and incurs high costs. The rationale for vertical separation of below-rail infrastructure provision from above-rail operations is to promote above-rail competition.

0

5 000

10 000

15 000

20 000

25 000

30 000

1994 1998 2002 2006 2010 2050kt

Exports

Production

Infrastructure and Australia’s food industry: Preliminary economic assessment

18

However, for the grain industry, as there is limited scope for more than one above-rail operator due to low volumes, the costs of vertical separation might outweigh the benefits. The National Transport Commission (NTC 2009a) suggested that an investigation of vertical reintegration of grain networks be undertaken.

Around 90 per cent of wheat exports is handled in bulk and around 10 per cent are in bags and

containers (PC 2010). The use of containers for exports expanded significantly after the

marketing of Australian wheat was deregulated and reached more than one-quarter in 2007–08.

Using containers can provide some flexibility in peak years. However, in more recent times, the

use of containers has been consistently declining and it is not clear to what extent they will

continue to be used.

Sugar

The sugar industry, its supply chain and the infrastructure linking each stage are outlined below.

The simple disaggregation of the preliminary projections of national sugar production and

exports to 2050 are then presented, followed by a brief discussion of potential infrastructure

issues associated with an expansion in production.

Sugar production and exports

The Australian sugar industry produces raw and refined sugar from sugar cane. In 2011–12 the

gross value of sugar cane production was approximately $1.2 billion and total sugar production

was 3.7 million tonnes, roughly 2 per cent of world sugar production (ABARES 2013).

Queensland accounts for 95 per cent of Australian sugar production and the remainder is

produced in New South Wales.

Around 75 to 80 per cent of sugar produced in Australia is exported, making Australia one the

world’s largest exporters of raw sugar. In 2011–12, Australia exported 2.6 million tonnes of

sugar, which was about 5 per cent of world sugar exports and valued at nearly $1.6 billion

(ABARES 2013).

The previous decade has seen rationalisation of the number of cane growing farms. The

Australian sugar industry has 3765 cane farm businesses (ABS 2012b) and 24 sugar mills

(Australian Sugar Milling Council 2012). From 2005 to 2008 there was downward pressure on

the profitability of some canegrowers as world sugar supply increased (Hooper 2008). There

has been a trend toward fewer, larger cane growing farms as smaller growers have left the

industry. However, production has remained relatively stable and it is likely that some

economies of scale exist in sugar production (Hooper 2008). Higher prices, foreign investment

and a desire by processors to reduce spare capacity have also provided incentives to maintain

cane production area or return land to cane production (Rabobank 2013).

Sugar cane production is particularly important for some regional Queensland economies. In the

Townsville region, sugar cane production was 54 per cent ($344 million) of the region’s total

gross value of agricultural production and accounted for 58 per cent of the region’s farms

(Trestrail et al. 2013a). Sugar cane production was also important in the Mackay and Cairns

regions, contributing 27 per cent to the total gross value of agricultural production in both

regions or $240 million and $185 million, respectively (Trestrail et al. 2013b, c). The importance

of sugar cane to regional economies was less pronounced in New South Wales. Sugar cane

production contributed 11 per cent ($22 million) of the Coffs Harbour – Grafton region’s gross

value of agricultural production, the third most important agricultural output after fruit and beef

for the region (Binks et al. 2013).

Infrastructure and Australia’s food industry: Preliminary economic assessment

19

Sugar supply chain and infrastructure

Figure 11 provides an overview of Australia’s sugar supply chain.

Harvested sugar cane is transported to a miller, usually within 16 hours of harvest to avoid crop deterioration. To achieve this, most sugar production is organised around sugar mills.

In Queensland, transport from the farm to the miller is primarily by miller-owned cane railway, but also by road.

In New South Wales, transport from the farm to the miller is by road.

At the mill, the harvested sugar cane is milled into raw sugar and stored short-term in bulk bins at the mill.

Figure 11 Sugar supply chain

Source: Adapted from Woodhead et al 2006.

In Queensland, bulk raw sugar is transported by road or rail to bulk sugar terminals, where it is stored before being exported or sent to refineries. Queensland accounts for all Australian sugar exports.

Bulk raw sugar either from bulk terminals or container terminals is sea freighted to overseas markets.

In New South Wales, bulk raw sugar is primarily transported by road to refineries for refining and processing for domestic consumption.

Refined sugar and other manufactured sugar products are transported to the domestic markets through the road network and sea freight.

Apart from raw and refined sugar, the industry produces molasses, ethanol (using molasses as a feedstock); electricity for export to the grid, mulch, mull mud (fertiliser) and furfural.

Production Processing, transport & storage End use market

RoadRoad

RailRoad

Sugar farms Miller

Export markets

Domestic markets

Manufacturing(Refinery)

Bulkterminal

Ship

RailRoad

Containerterminal

Road

Ship

Road

Rail

Road

Infrastructure and Australia’s food industry: Preliminary economic assessment

20

Regional distribution of production and exports

To examine the potential regional distribution of sugar production and exports to 2050 the

approach described at the beginning of this chapter was used. Figure 12 presents Australia’s

sugar production and exports. Map D2 shows SD level historical sugar production from 1993–94

to 2010–11 and projected sugar production in 2050—the shading of the SDs in the map

indicates the number of people employed in sugar and confectionery manufacturing industries

in 2010–11. Key points to note are outlined below.

Figure 12 Sugar production and exports

Note: ABARES preliminary projection

Source: ABARES, ABS

Preliminary projections to 2050 indicate the potential for Australian sugar production and

exports to be significantly larger in 2050 than historical production and exports:

production is projected to increase by 58 per cent by 2050 from the average production achieved between 1993–94 and 2010–11 of 4.8 million tonnes (Table D2)

exports are projected to expand substantially, to 6.3 million tonnes by 2050 from the average achieved between 1993–94 and 2011–12 of more than 3.7 million tonnes (Table D2).

Preliminary projections of substantial increases in production and exports reflect, to a large

degree, expectations of increases in global demand. While Australian production would have to

increase by less than 1.2 per cent a year from 2011 to reach the 2050 projection, this would be a

considerable change from the average annual decline of 0.7 per cent realised between 1993–94

and 2011–12. The opportunities and constraints to increased sugar production in Australia

require further investigation.

Using the simple disaggregation methods described earlier, the largest projected increase in

sugar production is in northern and far northern Queensland, near the Cairns, Mourilyan,

Lucinda, Townsville and Mackay ports. Projected production in these regions in 2050 is greater

than the historical production average or trend. However, the existing sugar industry is largely

landlocked and the scope for expanding cane areas does not appear to be large so most of any

increase from these areas would need to come from improvements in yield.

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

1994 1998 2002 2006 2010 2050

kt

Exports

Production

Infrastructure and Australia’s food industry: Preliminary economic assessment

21

If significant increases from existing areas are realised, significant improvements in sugar

handling capacities may also be needed along the supply chain to move sugarcane from farms to

mills and ports, and onto ship for exports. Sugar specific infrastructure, including cane railways

and bulk sugar terminals, as well as supporting road infrastructure, will be important.

The simple disaggregation of projected increases does not consider potential production in new

regions, such as the Ord River irrigation area which produced sugar cane until the mill closure in

2007–08. Expansion of sugar cane production into new regions may be more likely than

significant expansion from existing regions but will require investment in sugar specific

infrastructure to move sugar cane to mills and then to refineries or to a port with bulk sugar

handling capacity.

Beef

The beef industry, its supply chain and the infrastructure linking each stage are described below.

The simple disaggregation of the preliminary projections of national beef production and

exports to 2050 is then presented, along with a discussion on potential infrastructure issues

associated with an expansion in production.

Beef and veal production and exports

The industry accounts for more than half of Australia’s total meat production in volume terms.

In 2011–12, the industry produced 2.1 million tonnes of beef and veal. The gross value of

Australian cattle and calf production (including live cattle exports) was around $7.5 billion in

2011–12, accounting for 16 per cent of the gross value of farm production (ABARES 2013).

Australia is one of the world’s largest exporters of commercial livestock and red meat. The value

of beef and veal exports in 2011–12 was $4.5 billion and the value of live cattle exports was

$412 million (ABARES 2013).

The Australian beef industry in northern Australia is markedly different to that in southern

Australia. Differences in climatic and pasture conditions have resulted in significant differences

in stocking rates, average herd size and the main cattle breeds (Thompson & Martin 2012).