information cascades among investors in equity …...1 information cascades among investors in...

TRANSCRIPT

1

Information Cascades among investors in Equity Crowdfunding

Silvio Vismara *

University of Bergamo

Abstract

A number of papers in finance study information cascades among investors, especially

in the IPO setting. These studies typically differentiate between informed and

uniformed investors by distinguishing two categories, namely institutional vs retail

investors, as this is the only information available in public equity offerings. Life

information available in equity crowdfunding platforms includes instead also the names

of individual investors, who may disclose further information about themselves (e.g.,

linking their profile to social networks). We investigate information cascades among

investors in 111 pitches posted in 2014 on Crowdcube, world’s leading investment

crowdfunding platform. We find that early investors influence late investors, increasing

the probability of success of an offer; public profile investors increase the appeal of the

campaign already among early investors, who mediate the positive effect of public

profile investors on the success of the campaign.

Keywords: Equity crowdfunding, Information cascades, Crowdcube, Entrepreneurial

finance.

* I would like to thank Massimo G. Colombo, Douglas Cumming, Sophie Manigart,

Gordon Murray, Darren Westlake (CEO & founder of Crowdcube), and seminar and

conference participants at the University of Augsburg, ZEW, 2014 AiIG conference in

Bologna, 2014 NSE conference in Mannheim, for helpful comments. Nicola Berera

provided superb research assistance.

Contact author: Silvio Vismara, Department of Economics and Technology

Management, University of Bergamo, Italy; viale Marconi 5, 24044 Dalmine (BG),

Italy. Ph. +39.035.2052352. Email: [email protected]

2

1. Introduction

New ventures face difficulties in attracting external sources of finance during

their initial stage. Recently, as a consequence of the financial crisis, even traditional

investors in start-ups, such as business angels and venture capitalists, have moved their

investment activity upstream and focus more frequently on later-stage investments

(Block and Sandner 2009). In this context, equity crowdfunding, legalized by recent

regulatory changes such as the CROWDFUND Act in the U.S.1, is becoming a valuable

alternative source of funding for entrepreneurs (Cumming and Johan, 2013). In the

Unites States, 534 private companies have already successfully hit their equity

crowdfunding target this year (January-September), collecting all together $217.7m

(CrowdValley, 2014). In the United Kingdom, equity crowdfunding has grown at a 201

per cent year–on–year growth rate and facilitated £84m in predicted total transaction

volume for 2014 (Nesta, 2014). The most successful platforms, Crowdcube, has so far

raised £42.3m from over 100,000 investors, with as much as £1.2m in just 16 seconds in

July 2014.

With such high numbers and growth rates, it is not surprising that an emerging

literature is focusing on the determinants of the success of crowdfunding campaigns (for

a review, see e.g. Schwienbacher and Larralde, 2013). Nevertheless, Ahlers et al. (2012)

is the only paper available so far that specifically studies equity crowdfunding. Using a

sample of 104 projects on the Australian platform ASSOB between October 2006 and

October 2011, they identify which characteristics of the top management team of the

firm (e.g. size or level of education) and of the offer (e.g. intention to seek an exit by

either IPO or a trade sale) affect the probability of success of a proposal. Our paper

contributes to this nascent literature by focusing on the signals that investors receive not

only from the characteristics of the project itself, which we control for, but more

notably from the behavior of other investors.

Crowdfunding projects are financed only if their target amount is reached.

Observing that a project has attracted many early contributions reassures potential

backers that the project has good chances of reaching its target capital and thus that the

time and resources invested to make a pledge will not be wasted. For this and other

1 The Capital Raising Online While Deterring Fraud and Unethical Non-Disclosures Act

(CROWDFUND Act) is one component of the broader Jumpstart our Business Startups (JOBS)

Act., enacted in 2012.

3

reasons (Colombo et al., 2014) the initial investments by early contributions are

therefore expected to pave the way for further contributions. Coherently, recent papers

show that a high number of contributions in the early days of pitch increases the

probability of success of crowdfunding campaigns in donation-based (Burtch et al.,

2013), reward-based (Agrawal et al., 2011; Colombo et al., 2014), and lending-based

platforms (Zhang and Liu, 2012), as it happens in other online marketplaces (e.g.

eBay.com (Simonsohn and Ariely, 2008) or Amazon.com (Chen et al., 2011)).

Empirical evidence on the role of early contributors on the success of equity

crowdfunding campaigns is instead missing. This is paradoxical for the prominent role

that information cascades among investors play in entrepreneurial finance, where

potential, external investors take decisions in conditions of high uncertainty. Our paper

fills this gap in the literature.

Informational cascades are crucial in entrepreneurial finance. In Initial Public

Offerings (IPOs), for instance, late investors alter their own valuations by observing the

behaviour of previous investors (Welch, 1992; Aggarwal et al., 2002; Amihud et al.

2003). IPOs with high levels of institutional demand in the early days of bookbuilding

also see high levels of bids from retail investors in the later days (Khurshed et al.,

2014). This explains why IPOs typically result in either over-subscription or under-

subscription, with very few cases in between. However, in IPOs, the information

available to the public about the nature of the bids is limited to the distinction between

institutional and retail investors. Equity crowdfunding platforms, instead, reveal online

the (nick)name of the investor for each bid. This availability of information at an

individual level is unique in the entrepreneurial finance and offers a privileged avenue

to investigate information cascades.

In crowdfunding platforms, ‘hot’ projects are typically displayed in the front of

the homepage, so visitors can see them immediately. Other projects are then listed

according to their popularity in terms of number of investors who have already backed

them. This easy access to information on the number of bids received through the

bidding process facilitates the rapidity and the size of informational cascades.

Furthermore, for each project, prospective investors can access with a single click to

other pages providing information of the project, on the entrepreneurial team behind it,

as well as to the list of crowdfunding investors (“crowdfunders”) who have backed the

4

project till then. For example, Figure 1 shows the screenshot of the investors page

available for each offer in Crowdcube, world’s leading investment crowdfunding

platform on which this paper is empirically based.

Investors can make their profile public and link it to social networks. This, in

turn, increases the appeal of the project. First, potential investors can evaluate the

information on the curriculum vitae of early backers as well as their track record of

previous investments in the platform. Second, by “tweeting” or linking in social

networks, early investors contribute to advertise the project that they pledged, enlarging

the pool of potential investors informed about the project. The investor’s motivations to

make her profile public are several and include, for instance, the desire to get in touch

with the founder. We argue that the investors who make their profile public, among

them business angels, can be assumed to be informed investors as, compared to the

average crowdfunder, they have a higher educational capital, higher project-specific

industry experience and higher track record of investments within the platform.

Coherently, a novel hypothesis tested by this paper is that not only early backers matter

to the success of an equity crowdfunding campaign, but in particular the presence of

investors with public profile attract other investors.

These hypotheses are supported by the empirical evidence from a sample of 111

projects posted on Crowdcube between January to August 2014, for which we collected

day-by-day information on the bids at an individual investor level. Specifically, we find

that a higher number of investors backing the project in the early days of listing leads to

a higher number of late investors and, relatedly, a higher probability of success for the

project. Second, controlling for endogeneity, we find that investors with public profile

attract contributions of both early and late investors. Finally, arguably because a

“success-breeds-success” process is triggered once early contributions have been

attracted, we find that the role of investors with public profile on the success of the

campaign is fully mediated by early contributions.

The paper is organised as follows. Section 2 provides the research hypotheses.

Section 3 discusses data, variables and methodology used in the study. Section 4 reports

econometric results, and Section 5 concludes.

2. Hypotheses

5

2.1 Early investors

When decision makers face imperfect information about a product, they tend to

rely on the behaviours of the other individuals. There are two key requirements for

informational cascades to take place: uncertainty and sequentiality (Bikhchandani et al.,

1992). These conditions can occur in variety of situations, such as political voting,

fashion trends, technology adoption (Bikhchandani et al., 1998). The uncertainty about

the offer characterises equity crowdfunding platforms, like other entrepreneurial finance

settings. There is indeed a large degree of uncertainty about the quality of projects,

which are often proposed by first-time entrepreneurs. These information asymmetries

have been extensively highlighted by the entrepreneurial finance literature.

In equity crowdfunding marketplaces, however, the uncertainty problems are

less confined in supply-side issues. At least, on the demand side, investors are less

equipped to overcome these problems. Crowdfunding investors often lack the

experience and the capability (Ahlers et al., 2012) to evaluate different investment

opportunities. Due to fixed costs, they have limited opportunity to perform due

diligence (Agrawal et al., 2013). This leads to collective-action problems, where a large

number of investors each should be able to invest a small amount of money in a

company that is, they hope, early in its lifecycle (Ritter, 2013). Furthermore,

crowdfunding investors cannot even rely on the reputation of intermediaries such as

IPO underwriters.

Investors in equity crowdfunding cannot therefore count on much more than

themselves, the “crowd”. Observational learning theory predicts that when decision

makers have little information about the product, the importance of others’ decisions

increases (Bikhchandani et al., 1992). Similarly, late investors may learn by observing

the behaviour of previous backers and perceive accumulated capital as an indirect signal

of quality (Zhang and Liu, 2012). In crowdfunding platforms, the number of investors

who have already backed project are highly visible. Crowdcube, for instance, lists

projects according to their popularity, with ‘hot’ projects displayed in the front of the

homepage, so visitors can see them immediately. Early contributions can therefore

reassure backers when they face high uncertainty at the outset of crowdfunding

campaigns.

6

Early participation encourages additional participation not only for uncertainty

and for information-based motivations. Since many crowdfunding platforms operate on

an all-or-nothing base, late investors will be incentivised to fund campaigns that have

received many previous investments and are close to reach their target, in order not to

miss the opportunity of a successful pitch (Cumming et al., 2014). We therefore expect

that information of early investors’ bids matters to potential late investors, leading to

hypothesis H1.

H1: A higher number of early investors increases the probability of success of

equity crowdfunding campaigns.

2.2 Public profile investors

Since early contributions reduce investors’ uncertainty and generate informational

cascades, it is important to analyse what determines the attraction of investors in the

initial phase. Early backers in non-equity crowdfunding campaigns are typically people

with whom the proponent has social contacts, such as close friends and family members

(Mollick, 2013), often located in the same geographical area of the proponent (Agrawal

et al., 2011). Ordanini et al. (2011) label this phase “friend-funding phase”. Although

this could partly be the case also for equity crowdfunding, the possibility to attract

external investors is particularly important for entrepreneurial ventures seeking external

equity.

When the actions of individuals are sequential, highly-informed investors have less

incentive to wait to observe the actions of other individuals, and so they tend to move

first. Conversely, uninformed individuals tend to delay the decision and imitate the

actions of individuals who appear to have higher informational level or expertise

(Bikhchandani et al., 1992). In the IPO setting, Rock (1986) argues that high

uncertainty about the value of a firm increases the advantage for informed investors,

with the results of firms choosing to underprice their shares in order to attract

uninformed investors that would otherwise leave the market.

As individuals differ in the level of information they possess, it is often the case that

some investors enjoy an information advantage over others. Examples of informed

investors are institutionals or venture capitalist in IPOs, or majority shareholders in

M&A deals. This difference is likely to occur also in the equity crowdfunding context,

7

where, however, the information available is not limited to the category of investors but

specifically to individual investors. Investors can decide whether to make their profile

public, associating their legal name, social network presence and contact information, or

be anonymous, therefore choosing a nickname without disclosing further information.

We argue that investors with a public profile tend to be more informed than anonymous

investors. First, sophisticated investors, in particular business angels, that operate also

on equity crowdfunding platforms (Hornuf and Schwienbacher, 2014) are likely to

disclose their information and their investment decisions in the setting of

entrepreneurial finance. Second, in order to get informed, investors need to have a direct

contact with the proponent. This is actually necessary in order to request additional

information about the project before investing. The need of interaction with the

company’s founders encourages these investors to disclose their personal information.

We therefore argue that investors with a public profile attract other investors in

the initial days of equity crowdfunding campaigns for two main reasons. First,

uninformed investors receive a stronger signal from non-anonymous investors, because

of their expected higher level of information and experience. Second, investors with a

public profile will be likely to generate word-of-mouth effect around the project (Arndt,

1967), as demonstrated by Colombo et al. (2014) in a reward-based context.

Crowdcube, as other platforms, indeed enable investors to advertise the project on the

main social networks, increasing the possibility for other potential investors to become

informed about the pitch. These considerations lead to hypothesis H2.

H2: A higher percentage of investors with a public profile increases the number

of early investors in equity crowdfunding campaigns.

2.3 The mediating role of public profile investors

Once a high number of individuals has supported the project in the initial phase

of crowdfunding campaigns, we expect the positive effect of informed investors to

decrease. First, as argued by Colombo et al. (2014), once an adequate number of early

backers have been attracted, the aforementioned mechanisms of observational learning

begin to operate, thus driving the campaign towards either success or failure. Such

dynamics of informational cascades will take place based on what happened in the

8

initial phase. Second, in any case, late investors are incentivised to support campaigns

that are close to reach their target capital, in order to join a successful pitch.

Therefore, we argue that bids from investors that choose to make their profile

public attract investors early on. Conversely, their role fades once early contributions

have been attracted because of their uncertainty-reducing effect and because, as

motivated to support of our first hypothesis, early participation encourages additional

participation for not only uncertainty and information-based motivations. Hypothesis 3

follows.

H3: The number of early investors mediates the positive effect of informed

investors with a public profile on the success of equity crowdfunding.

3. Research design

3.1 Crowdcube

We test our research hypotheses using the projects posted on Crowdcube in the

period January to August 2014. Established in 2011 with head offices at the Innovation

Centre of the University of Exeter, Crowdcube is the first equity crowdfunding platform

in the UK and currently the world leader. Crowdcube vets the business plan of each

before listing, whereas there is no ongoing reporting from the company to its

shareholders. There is no listing fee, but a success fee of 5% of the target amount. The

platform, regulated by the UK Financial Conduct Authority, offers securities to

investors that do not invest more than 10% of their portfolio in unlisted shares or

unlisted debt securities. The minimum investment in a pitch is £ 10, while there is no

maximum. Individual commitments are aggregated via the platform until the funding

target is reached and the crowdfunding scheme works in the traditional “all-or-nothing”

fashion. This means that only if the target amount is reached, the campaign is

successful, and the pledges are transferred in six weeks from the escrow account to the

project proponent’s account. Investors will therefore become direct shareholders in that

company. If the target is not reached, all pledges are voided.

Investors in Crowdcube must be over 18 years old and legally entitled to invest.

This means that they must be in a country, such as EU member states, where they may

legally receive financial promotions. Instead, Crowdcube does not advertise investment

opportunities to people in the United States, Canada or Japan from where cannot

9

register or view pitches. Investors need to register as platform members, which require

them to certify to be informed of investment’s opportunities and risks, or to receive

independent advice. Once registered, investors can access to webpages on the

companies, which reports a description of the business of the company, of its

entrepreneurial team, of the offer, and of the bids received. In Crowdcube, investors can

remain anonymous or make their profile public, as shown in Figure 1. Besides

commenting on the platform’s forum, public profile investors can directly contact the

entrepreneur to ask for additional information, and they can advertise the pitch through

social networks (e.g. Linkedin, Facebook and Twitter) or on their website.

[FIGURE 1]

3.2 Sample and variables

Our sample is made of the 111 pitches listed in Crowdcube in the period from

January to August 2014.2 The number of observations is lower than in studies on

reward-based crowdfunding (see, e.g. Colombo et al., 2014), but it is higher the 104

ASSOB projects used in Ahlers et al. (2012). Information collection on the bids at an

individual investor level was day-by-day automatically carried out through the

progression of each crowdfunding campaign. The success of a campaign is measured

with three variables, namely the number of investors, the funding amount, both

measured at the end of the campaign, and a dummy variable equal to one for pitches

reaching or exceeding their target capital (Success). The Funding_Amount, measured as

a percentage of the target capital collected, is a more fine-tuned measure of success of

the campaign, and indicates how much capital has been raised (if the variable is equal or

higher than 1; how close the pitch was to reach the target, otherwise).

The number of investors is available for each project in each day of campaign.

We are in particular interested in the investments taking place in the early days of the

pitch. To identify early investors (Early_Investors), we use observation windows fixed

conventionally between the launch of the campaign and the fifth and tenth day.3. We

2 We excluded three pitches with duration lower than ten days because of their inadequacy to

investigate the role of early vs late investors, which is the aim of this paper. 3 For robustness, we re-run all the regression considering as early investors those bidding in the

first 7, 12, and 15 days. Results did not change substantially.

10

identify as Late_Investors those bidding the end of these observation windows (i.e. 5 or

10 days) to the end of the campaign. Differently from studies on other non-equity

crowdfunding platforms (e.g., Colombo et al., 2014), we use fixed observation windows

because the duration of pitches in Crowdcube is automatically set to 60 days. However,

successful pitches can be closed before the end and, in some cases, the duration can be

extended at discretion of the platform to reach the target. In regressions, we control for

these ex-post change in the duration of the campaign by introducing a control variable

(Duration). The (nick)name of investors in Crowdcube is publicly available. However,

it is upon the individual investor to decide whether to make her profile public, through

linking it to social network or websites. In our study, these investors are defined

Public_Profile_Invetors and are identified as a percentage over the observation

windows.

To investigate whether the information on previous investors matters in the

investment decisions of subsequent platform visitors, we control for a series of variables

concerning the project and its proponents.4 First, as in Colombo et al. (2014), we

measure the Social_Capital of the proponent in terms of number of Linkedin

connections. This proxies the professional social contacts that an individual proponent

has prior to start her campaign.5 We control for the size of the Top Management Team

(TMT_Size), by counting the number of members of the entrepreneurial ventures as

reported in the “Team” page of each pitch. As in Ahlers et al. (2012), we control for the

target amount (Target_Capital) and for the percentage of equity offered to investors

(Equity_Offered) in each pitch. Firms seeking financing on Crowdcube can choose to

offer investors different classes of shares, with or without voting rights. We measure the

percentage of investment threshold to achieve shares with voting rights, as a percentage

4 In unreported results, we increase the number of control variables by introducing a dummy for

the pitches offering investors a reward if the target capital is raised (73%) and a dummy variable

if the start-up location is London (45%). Besides the more generous Seed Enterprise Investment

Scheme as controlled for with the Tax_Incentives variables in the paper, we also run regressions

including identifying Tax_Incentives pitches as those that qualify for Enterprise Investment

Scheme tax relief (80%). Finally, the IPO is not the only exit option that can be planned. Other

exit options include trade sales (72%) and management buyouts or a share buy-backs (11%).

Again, we run regressions and find that results do not change substantially using these different

set of control variables. 5 In our sample, there are 6 projects with two proponents, and 2 projects with three. the

Social_Capital of these projects is measured as the average number of Linkedin connections of

the proponents.

11

of the target capital (Voting_Rights_Threshold). Project can qualify for tax incentives

according to the UK Seed Enterprise Investment Scheme, which is designed to help to

encourage seed investment in early stage companies for up to £150,000 capital raised

(Tax_Incentives).6 At listing, proponents declare their intentions with regard to exit and

pay-out policies. Similarly to Ahlers et al. (2012), we use a dummy variable equal to

one when an exit through IPO is planned (Exit_IPO), and a dummy variable equal to

one if the firm plans to distribute dividends (Dividends). Both these intentions are

disclosed on the webpages that describe each project. Finally, we control for industry

using Crowdcube classification.

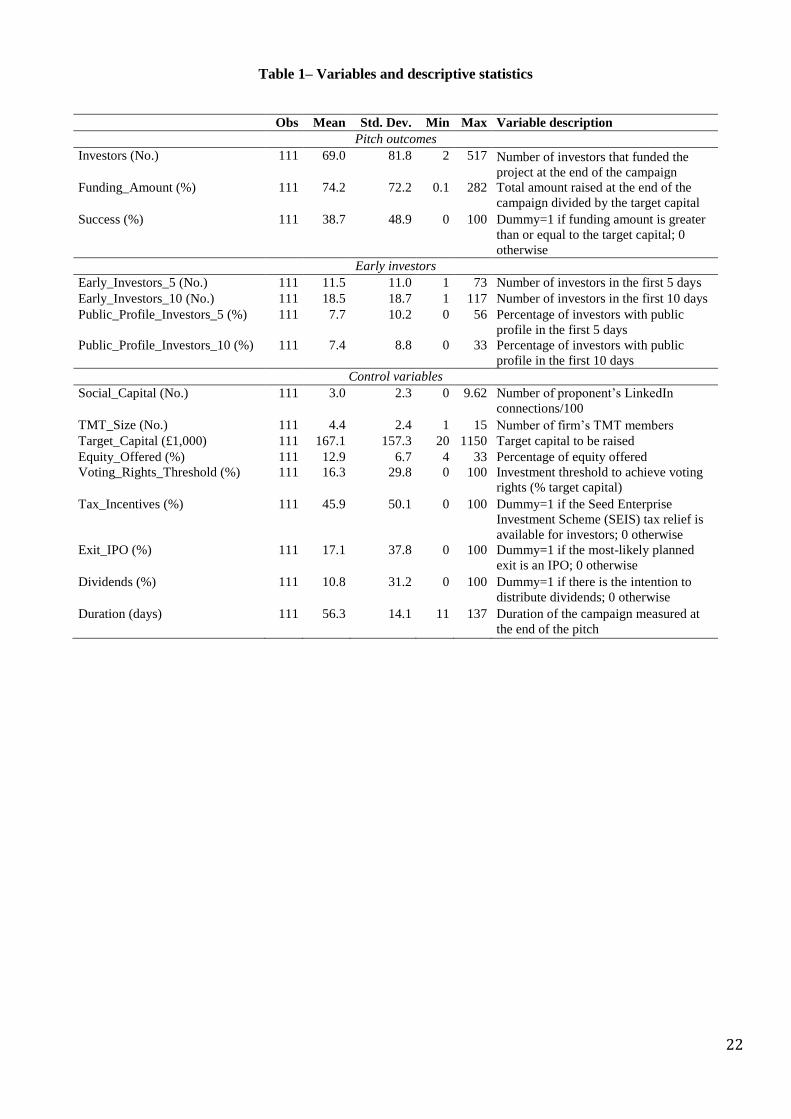

The definitions of the variables and descriptive statistics are reported in Table 1,

while the correlation matrix is in the Appendix.

[TABLE 1]

3.3 Descriptive statistics

The percentage of successful pitches (Success) in our dataset is 38.7% and the

average percentage of target amount raised is 74.2%. Successful pitches (i.e. those that

at least reached the target) are in black in Figure 2. The Figure shows the frequency of

outcome for funding amount at the end of the pitch, relative to the initial target amount.

About one third of the projects did not collect bids for up to 20% of the target amount.

Consistent with the incentives in the all-or-nothing framework, no project reached

between 80% and the total target amount. As reported in Table 1, the average number of

investors per pitch in our sample is equal to 69, much higher than the average reported

by Ahlers et al. (2012) for ASSOB (8 investors). On average, 11.5 investors back a

pitch in the first five days and 18.5 in the first ten days (Early_Investors). This is similar

to the findings of Colombo et al. (2014) who find an average of 11 investors at one sixth

of the campaign (usually 5 days) in Kickstarter.

[FIGURE 2]

6 The Seed Enterprise Investment Scheme was introduced in April 2012 as a derivative of the

Enterprise Investment Scheme. Investors receive initial tax relief of 50% on investments up to

£100,000 and Capital Gains Tax exemption for any gains on the SEIS shares.

12

Figure 3 shows the number of investors over the time window, distinguishing

between successful and unsuccessful projects (43 and 68 projects, respectively).

Predictably, the number of investors is higher in successful offers (on average, 140 vs

24 investors in unsuccessful offers). More importantly, the ratio in the number of

investors between successful and successful increases over time. For instance, the

average number of investors after five days in a pitch that will be successful is 18,

versus 7.2 in unsuccessful ones (2.5 times). At ten day from the opening of the pitch,

the number of investors in successful projects is 30, versus 11 (2.74 times). At the end

of the pitch, the average number of investors in successful pitches is six time larger than

that in successful pitches (140/24).7 This evidence points to “success-breeds-success”

dynamics, where projects able to collect bids already in the first days are deemed

successful. On the contrary, in unsuccessful pitches, the weak number of investors in

the first few days leads to even weaker demands later.

[FIGURE 3]

Most of early investors choose not to make their profile public, and the mean

value of Public_Profile_Investors is equal to 7.7% and 7.4% at 5 and ten 10 from the

launch of the campaign, respectively. However, successful pitches are characterized by

a higher fraction of public profile investors, in particular within the first 5 days of pitch

(9.1% vs 6.9%). The levels and the difference between successful and unsuccessful

decreases over time (e.g. 8.7% vs 6.6 after ten days). It is difficult to prove that public

profile investors are better informed than other investors, as the latter are not

identifiable. However, by analysing a random sample of 200 public profile investors in

Crowdcube, we find two interesting characteristics. First, they invest more often than

the average investor. Indeed, their average portfolio is of 4.8 investments, versus 2.7

declared by Crowdcube as average for active investors in the platform. Second, we find

that public profile investors have typically a higher level of entrepreneurial and project-

specific expertise. 88% of the investors in the sample has skills in entrepreneurship and

7 Figure 3 is standardized to an event window of 60 days, which is the Duration of pitches in

Crowdcube. T-tests on the difference in means reveal that the number of investors in successful

projects is higher than in unsuccessful pitches from the 5th day onwards (statistical significance

at 1%).

13

start-ups, and 44% has experience in the specific industry of the funded project. This is

presumably higher than the “amateur” crowdfunder, typically described as having

limited experience in evaluating investment opportunities (Agrawal et al., 2013;

Belleflamme et al., 2013). In the UK, in particular, the majority of equity crowdfunding

investors are “retail Investor with no previous experience of early stage/venture capital

investment” (NESTA, 2014).

Considering the entrepreneurs’ Social_Capital, the average number of LinkedIn

connections of the company’s founders is equal to 300. Colombo et al. (2014) report a

much lower number of average LinkedIn connection (49), because they do not consider

external social capital when the pitch proponent is a company. This situation cannot

occur on Crowdcube. The number of TMT members (TMT_Size) varies from 1 to 15,

with an average of 4.4. Startups on ASSOB have instead a higher number of people,

with an average of 3.6 board members and 7.2 staff employed (Ahlers et al., 2012). The

average target capital of our sample pitches is £ 167,000, with a minimum of £ 20,000

and a maximum of £ 1.15M.8 This is lower than the average target mount reported by

Ahlers et al. (2012) in Australian ASSOB (AUD 1,78m) but higher than in UK

competing platforms (e.g., in the same period January-September 2014, we find that the

average successful pitch in Seedrs raised £123,106). These figures suggest that the

Australian platform is suitable for more mature firms and larger individual investors

than Crowdcube. On the contrary, the figures for other types of crowdfunding are

smaller, with reward-based pitches typically smaller than US$ 100,000.

The average percentage of Equity_Offered at the pitch is equal to 13%, while the

average threshold to achieve voting rights is equal to 16% of the target capital

(Voting_Rights_Threshold). Investors are often eligible for the Seed Enterprise

Investment Scheme of Tax_Incentives (46%). A minority of the projects is meant to be

exited via IPO (17% IPO_Exit) or to pay Dividends (11%) in the near future. The

average Duration of the campaigns in our sample is 56 days; the minimum is 11 and the

maximum 137.

3.4 Methodology

8 The average successful pitch in the period January-September 2014 raised £240,234, as

compared to an average £35,274 amount of bids collected by unsuccessful pitches.

14

To test Hypothesis 1, we use as dependent variable our three measures of

success of a pitch (i.e. Investors, Funding_Amount, and Success). We run a negative

binomial regression on the number of late investors, with respect to the definition of

Early_Investors (e.g. investors by the fifth or the tenth day of the pitch). A standard

OLS regression is used for the percentage of amount raised at the end of the campaign

and a probit regression on the binary variable of success. To investigate the

determinants of early investments (Hypothesis 2) as well as the mediation model

between public profile investors and early investors, we use negative binomial

regression models. The percentage of public profile investors is therefore used as an

independent variable in the estimate of the determinants of early investment decisions.

Given that these two variables are measured over the same time window (e.g. 0-5 days,

or 0-10 days of pitch), there could be an endogeneity problem due to simultaneity. To

ensures sequentiality, we also run regressions where the number of early investors

(dependent variable) is measured after the percentage of public profile investors. For

instance, we will report in Model 3 of Table 3 the results of a regression where the

dependent variable is the number of investors from the sixth to the 10th day of pitch,

while the independent variable is the percentage of public profile investors from the

opening to the 5th day of pitch.

4. Results

Table 2 reports the regression results where the dependent variables are

measures of the success of crowdfunding campaigns. Results support our Hypothesis 1.

A higher number of early investors increases the probability of success of equity

crowdfunding campaigns. Results, that are robust across observation windows, are

significant for each dependent variable. These findings are similar to those of Colombo

et al. (2014), who provide evidence on the relationship between early investments and

success of reward-based crowdfunding campaigns.

The number of TMT members (TMT_Size) is positively related with the

outcome of the campaigns, and is therefore perceived by outside investors as a positive

signal of the firm’s ability to cope with the uncertainty of the market. Interestingly, the

amount of target capital (Target_Capital) does not impact the probability of success of

the campaigns. These findings on TMT size and target capital confirm are in line with

15

Ahlers et al. (2012) results in equity crowdfunding in Australia. A higher percentage of

equity offered at the offer (Equity_Offered) is associated with a lower number of

investors. Similarly to what happens in other public equity offerings, entrepreneurs who

retain a high proportion of equity convey a positive signal to investors (Leland and

Pyle, 1977). Finally, contrary to Ahlers et al. (2012), the intention to have an IPO exit,

as declared by the proponents, does not significantly impact on the outcome of

campaigns on Crowdcube.

[TABLE 2]

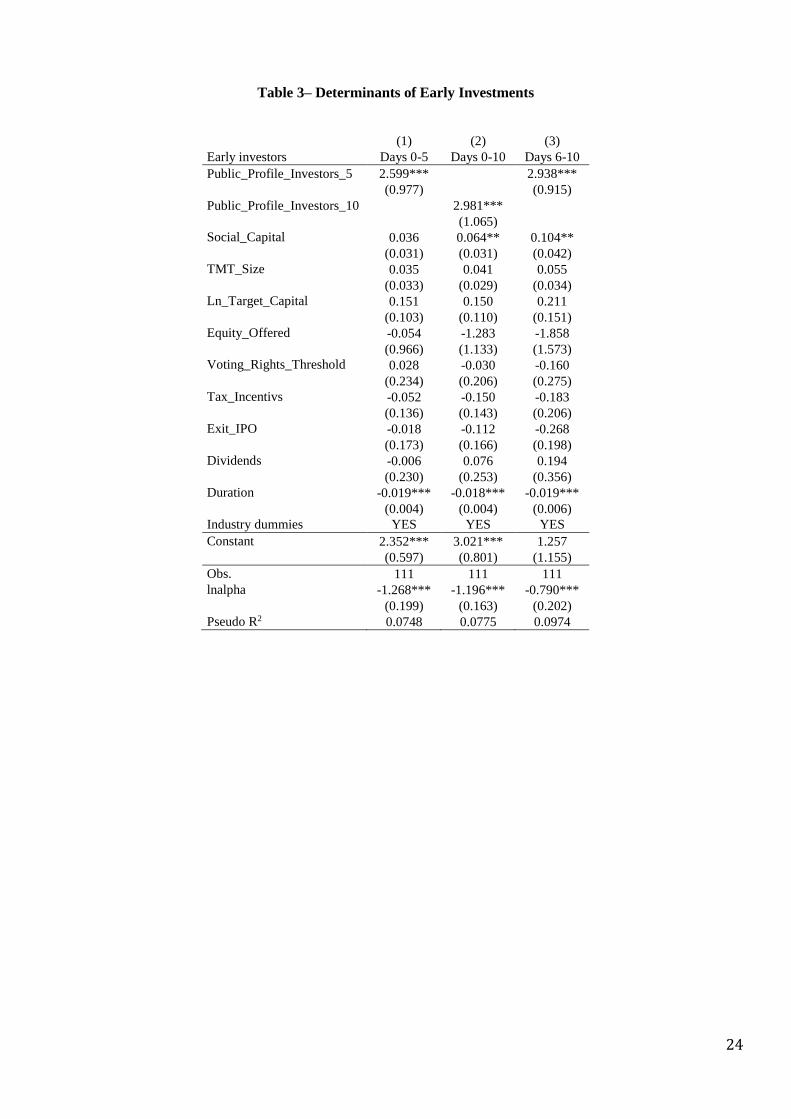

In Table 3, the dependent variable is the number of early investors. Results

support our Hypothesis 2. A higher percentage of investors with a public profile

increases the number of early investors in equity crowdfunding campaigns. Model 3

shows that a higher percentage of public profile investors in the first five days of pitch

attracts more investors in the following five days. Results are therefore robust for

endogeneity due to simultaneity.

[TABLE 3]

In Table 4, we test for the mediation effect of early investors, similarly to

Colombo et al. (2014), and find support for our Hypothesis 3. The number of early

investors mediates the positive effect of investors with a public profile on the success of

equity crowdfunding.

[TABLE 4]

5. Conclusions

Existing papers on information cascades among investors in entrepreneurial setting

differentiate between informed and uniformed investors by distinguishing two

categories, institutionals vs retails investors. This is indeed the only information

available in equity offerings in public markets, as the name of the investors in not made

available to the public. Recently, a new method to raise money from individuals has

16

emerged for entrepreneurial ventures. Equity crowdfunding campaigns are an ideal

setting to test information cascade among investors as the name (or nickname) of the

individual investors is made public. In this setting, investors are typically uninformed

about the underlying quality of the projects and their proponents, but they can use the

information on previous investment decisions as a signal of the unobservable attributes

of new ventures. We take advantage of this information to test the relevance of

information cascade between investors in 111 pitches posted on Crowdcube in 2014.

We first demonstrate that contributions in the early days of the pitch are fundamental in

attracting other investors and thus increase the probability of success of the campaigns.

Given the importance of early contributions to the success of equity crowdfunding

campaigns, we then investigate the determinants of early investors, which can only

partially rely on the accumulated capital and the number of early contributions to assess

the quality of the project. We find that public profile investors play a crucial role in

attracting other investors in the initial days of the pitch, conveying to uninformed

investors a strong signal of quality of the venture. We also demonstrate that

entrepreneur’s social capital increases the probability of receiving outside financing in

the initial stages. Finally, we provide empirical evidence that the number of early

investors mediates the positive effect of the percentage of public profile investors on the

success of equity crowdfunding campaigns.

This paper makes several contributions. First, it advances knowledge to the empirical

research on the determinants of success of equity crowdfunding campaigns, which is

still limited because there are few large platforms with a significant number of projects

to investigate. To the best of our knowledge, only Ahlers et al. (2012) have empirical

addressed the topic, using a sample of 104 projects posted on the Australian platform

ASSOB to analyse signalling mechanisms from start-ups to investors. We extend their

research by including the dynamics between investors (information cascades and word-

of-mouth) that can lead to the success of the campaigns.

Second, we contribute to the literature of signalling theory in entrepreneurship,

explaining how investors make choices characterised by information asymmetry issues.

In particular, we focus on the signalling dynamics between investors in equity

crowdfunding platforms.

17

Third, we contribute to the research on informational cascades in financial markets.

Similar to what has been demonstrated in an IPO context (Amihud et al., 2003; Pollock

et al., 2008), where investors alter their own evaluations of the stocks upon observing

the behaviour of previous investors, we show that observational learning is likely also to

play a crucial role in an equity crowdfunding. Uninformed investors are indeed likely to

imitate the previous investment decisions, and in particular those of public profile

investors. This also confirms the emergent literature on observational learning in a non-

equity crowdfunding context (Colombo et al., 2014).

Finally, we extend knowledge on the role of social capital in entrepreneurial finance.

Entrepreneurs’ social connections help investors to reduce information asymmetries and

have been demonstrated to influence venture finance decisions (e.g. Shane and Cable,

2002). Our study provides empirical evidence about their importance in equity

crowdfunding in increasing the pitch popularity and thus in attracting a large number of

investors in the first stages, similar to what demonstrated for reward-based

crowdfunding (Colombo et al., 2014).

The limitations of this study offer avenues for further research. First, the limited number

of observations calls for future investigation. In particular, studies on larger samples

would benefit from information about individual investors other than their public profile

and could shed light on the possible role of the reputation of investors, besides

proponents. In this paper, this level of information is used to prove that public profile

investors are (more) informed investors (than the typical amateur crowdfunder). At the

moment, information relative to which projects each investor previously bid is relevant

only for the projects at the end of the sampling period, as in the first projects this is null

by definition. Arguably, it would need more time and projects to effectively test for

reputation effects from individual investors. Relatedly, as business angels operate on

equity crowdfunding platforms (Hornuf and Schwienbacher, 2014), it would of interest

to investigate their behaviour in this context. This will offer insights on the

complementarity or substitute role of angel investors and crowdfunding. Finally, the

signal provided by the proponent and TMT members is in this study only used as

control variable. These aspects, clearly, could be investigated more deeply and reveal a

more important role. For instance, we measured entrepreneurs’ social capital by the

absolute number of LinkedIn connections, but we did not qualify the socioeconomic

18

importance of each contact. TMTs could be investigated with reference to their value-

protection vs value-creation roles.

Last, our study has interesting implications for both entrepreneurs and managers of

crowdfunding platforms. Projects’ proponents should rely on their personal connections

in the initial stages of the campaigns, in order to attract a higher number of early

contributions and stimulate informational cascades dynamics. They should also

advertise their campaigns on social networks in order to create a word-of-mouth effect.

Accordingly, managers of the platforms should facilitate the connections with social

networks in order to increase the popularity of the pitches and attract more investors.

19

References

Aggarwal, R., Prabhala, N. R., and Puri, M. (2002). Institutional allocation in initial

public offerings: Empirical evidence. Journal of Finance, 57(3), 1421-1442.

Agrawal, A. K., Catalini, C., and Goldfarb, A. (2011). The geography of crowdfunding.

National Bureau of Economic Research.

Agrawal, A. K., Catalini, C., and Goldfarb, A. (2013). Some simple economics of

crowdfunding. National Bureau of Economic Research.

Ahlers, G. K., Cumming, D., Günther, C., and Schweizer, D. (2012). Signaling in equity

crowdfunding. Available at SSRN, 2161587.

Amihud, Y., Hauser, S., and Kirsh, A. (2003). Allocations, adverse selection, and

cascades in IPOs: Evidence from the Tel Aviv Stock Exchange. Journal of

Financial Economics, 68(1), 137-158.

Arndt, J. (1967). Role of product-related conversations in the diffusion of a new

product. Journal of marketing Research, 291-295.

Belleflamme, P., Lambert, T., and Schwienbacher, A. (2013). Crowdfunding: Tapping

the right crowd. Journal of Business Venturing, 29(5), 585-609.

Bikhchandani, S., Hirshleifer, D., and Welch, I. (1992). A theory of fads, fashion,

custom, and cultural change as informational cascades. Journal of political

Economy, 992-1026.

Bikhchandani, S., Hirshleifer, D. and Welch, I. (1998). Learning from the behavior of

others: Conformity, fads, and informational cascades. The Journal of Economic

Perspectives, 151-170.

Block, J., Sandner, P. (2009). What is the effect of the financial crisis on venture capital

financing? Emperical evidence from US internet start-ups. Venture Capital - An

International Journal of Entrepreneurial Finance, 11, 295-309.

Burtch, G., Ghose, A., and Wattal, S. (2013). An empirical examination of the

antecedents and consequences of contribution patterns in crowd-funded markets.

Information Systems Research, 24(3), 499-519.

Chen, Y., Wang, Q., Xie, J. (2011). Online social interactions: A natural experiment on

word of mouth versus observational learning. Journal of Marketing Research,

48(2), 238-254.

20

Colombo, M. G., Franzoni, C., Rossi Lamastra, C. (2014). Internal Social Capital and

the Attraction of Early Contributions in Crowdfunding. Entrepreneurship

Theory and Practice.

Cumming, D.J., Leboeuf, G., Schwienbacher, A. (2014). Crowdfunding Models: Keep-

it-All vs. All-or-Nothing. SSRN working paper.

CrowdValley (2014), Equity Crowdfunding in the US One Year After Title II.

Hornuf, L. and Schwienbacher, A. (2014). Crowdinvesting – Angel investing for the

masses. Handbook of Research on Venture Capital: Volume 3. Business Angels.

Khurshed, A., Paleari, S., Pandè, A., and Vismara, S. (2014). Transparent bookbuilding,

certification, and initial public offerings. Journal of Financial Markets, 19, 154-

169.

Leland, H.E. and Pyle, D. (1977). Informational asymmetries, financial structure and

financial intermediation, Journal of Finance, 32, 371-387.

Mollick, E. (2013). The dynamics of crowdfunding: An exploratory study. Journal of

Business Venturing, 29(1), 1-16.

Nesta (2014). Understanding Alternative Finance: The UK Alternative Finance Industry

Report 2014.

Ordanini, A., Miceli, L., Pizzetti, M., and Parasuraman, A. (2011). Crowd-funding:

transforming customers into investors through innovative service platforms.

Journal of Service Management, 22(4), 443-470.

Ritter, J.R., (2013). Re-energizing the IPO Market, in Restructuring to Speed Economic

Recovery, edited by Martin Neil Bailey, Richard J. Herring, and Yuta Seki,

Brookings Press.

Rock, K. (1986). Why new issues are underpriced. Journal of financial economics,

15(1), 187-212.

Schwienbacher, A., and Larralde, B. 2013. Crowdfunding for small entrepreneurial

ventures (Vol. Handbook of entrepreneurial finance). (D. Cumming) New York:

Oxford University Press.

Shane, S., and Cable, D. (2002). Network ties, reputation, and the financing of new

ventures. Management Science, 48(3), 364-381.

Simonsohn, U., and Ariely, D. (2008). When rational sellers face nonrational buyers:

evidence from herding on eBay. Management Science, 54(9), 1624-1637.

21

Welch, I. (1992). Sequential Sales, Learning, and Cascades. Journal of Finance, 47,

695-732.

Zhang, J., and Liu, P. (2012): Rational Herding in Microloan Markets. Management

Science, 58(5), 892-912.

22

Table 1– Variables and descriptive statistics

Obs Mean Std. Dev. Min Max Variable description

Pitch outcomes

Investors (No.) 111 69.0 81.8 2 517 Number of investors that funded the

project at the end of the campaign

Funding_Amount (%) 111 74.2 72.2 0.1 282 Total amount raised at the end of the

campaign divided by the target capital

Success (%) 111 38.7 48.9 0 100 Dummy=1 if funding amount is greater

than or equal to the target capital; 0

otherwise

Early investors

Early_Investors_5 (No.) 111 11.5 11.0 1 73 Number of investors in the first 5 days

Early_Investors_10 (No.) 111 18.5 18.7 1 117 Number of investors in the first 10 days

Public_Profile_Investors_5 (%) 111 7.7 10.2 0 56 Percentage of investors with public

profile in the first 5 days

Public_Profile_Investors_10 (%) 111 7.4 8.8 0 33 Percentage of investors with public

profile in the first 10 days

Control variables

Social_Capital (No.) 111 3.0 2.3 0 9.62 Number of proponent’s LinkedIn

connections/100

TMT_Size (No.) 111 4.4 2.4 1 15 Number of firm’s TMT members

Target_Capital (£1,000) 111 167.1 157.3 20 1150 Target capital to be raised

Equity_Offered (%) 111 12.9 6.7 4 33 Percentage of equity offered

Voting_Rights_Threshold (%) 111 16.3 29.8 0 100 Investment threshold to achieve voting

rights (% target capital)

Tax_Incentives (%) 111 45.9 50.1 0 100 Dummy=1 if the Seed Enterprise

Investment Scheme (SEIS) tax relief is

available for investors; 0 otherwise

Exit_IPO (%) 111 17.1 37.8 0 100 Dummy=1 if the most-likely planned

exit is an IPO; 0 otherwise

Dividends (%) 111 10.8 31.2 0 100 Dummy=1 if there is the intention to

distribute dividends; 0 otherwise

Duration (days) 111 56.3 14.1 11 137 Duration of the campaign measured at

the end of the pitch

23

Table 2– Determinants of the success of a campaign

Late_Investors Funding_Amount Success

(1) (2) (3) (4) (5) (6)

Early vs late investors Days 0-5 Days 0-10 Days 0-5 Days 0-10 Days 0-5 Days 0-10

Early_Investors 0.061*** 0.046*** 0.033*** 0.023*** 0.152*** 0.101***

(0.014) (0.010) (0.006) (0.005) (0.033) (0.019)

Social_Capital 0.034 0.034 0.004 0.001 -0.001 -0.008

(0.030) (0.029) (0.032) (0.022) (0.021) (0.025)

TMT_Size 0.096*** 0.094*** 0.066** 0.077*** 0.175** 0.168**

(0.028) (0.031) (0.030) (0.026) (0.070) (0.074)

Ln_Target_Capital 0.066 -0.052 -0.062 -0.064 -0.018 0.009

(0.150) (0.146) (0.101) (0.093) (0.309) (0.322)

Equity_Offered -2.876** -2.839* -1.648* -1.093 -3.525 -2.248

(1.355) (1.484) (0.910) (0.892) (2.786) (2.898)

Voting_Rights_Threshold 0.499 0.336 0.028 -0.021 0.232 0.101

(0.362) (0.364) (0.286) (0.274) (0.669) (0.618)

Tax_Incentives -0.308* -0.321* -0.112 -0.025 0.307 0.372

(0.185) (0.184) (0.144) (0.143) (0.414) (0.427)

Exit_IPO -0.028 0.070 0.025 0.055 0.551 0.597

(0.233) (0.248) (0.181) (0.177) (0.405) (0.422)

Dividends 0.269 0.095 0.257 0.256 1.196* 1.128*

(0.369) (0.369) (0.239) (0.239) (0.655) (0.586)

Duration 0.015** 0.021*** -0.001 0.006 0.025* 0.027

(0.006) (0.006) (0.006) (0.004) (0.014) (0.017)

Industry dummies YES YES YES YES YES YES

Constant 2.942*** 3.513*** 1.367 0.881 -4.422** -4.429**

(1.128) (1.069) (0.871) (0.699) (1.835) (1.859)

Obs. 111 108 111 108 111 108

lnalpha -0.463*** -0.319**

(0.109) (0.130)

Pseudo R2 0.0820 0.0878

0.403 0.415

R2 0.445 0.482

Robust St. Err. in parentheses. *** p<0.01, ** p<0.05, * p<0.10.

24

Table 3– Determinants of Early Investments

(1) (2) (3)

Early investors Days 0-5 Days 0-10 Days 6-10

Public_Profile_Investors_5 2.599***

2.938***

(0.977)

(0.915)

Public_Profile_Investors_10

2.981***

(1.065)

Social_Capital 0.036 0.064** 0.104**

(0.031) (0.031) (0.042)

TMT_Size 0.035 0.041 0.055

(0.033) (0.029) (0.034)

Ln_Target_Capital 0.151 0.150 0.211

(0.103) (0.110) (0.151)

Equity_Offered -0.054 -1.283 -1.858

(0.966) (1.133) (1.573)

Voting_Rights_Threshold 0.028 -0.030 -0.160

(0.234) (0.206) (0.275)

Tax_Incentivs -0.052 -0.150 -0.183

(0.136) (0.143) (0.206)

Exit_IPO -0.018 -0.112 -0.268

(0.173) (0.166) (0.198)

Dividends -0.006 0.076 0.194

(0.230) (0.253) (0.356)

Duration -0.019*** -0.018*** -0.019***

(0.004) (0.004) (0.006)

Industry dummies YES YES YES

Constant 2.352*** 3.021*** 1.257

(0.597) (0.801) (1.155)

Obs. 111 111 111

lnalpha -1.268*** -1.196*** -0.790***

(0.199) (0.163) (0.202)

Pseudo R2 0.0748 0.0775 0.0974

25

Table 4– Mediation model

(1) (2) (3) (4)

Early vs Late investors Days 0-5 Days 0-5 Days 0-10 Days 0-10

Public_Profile_Investors_5 2.572** 1.338

(1.014) (1.002)

Public_Profile_Investors_10 3.985** 0.717

(1.657) (1.426)

Early_Investors

0.057***

0.043***

(0.014)

(0.011)

Social_Capital 0.106** 0.092* 0.107** 0.053

(0.054) (0.052) (0.055) (0.054)

TMT_Size 0.129*** 0.100*** 0.136*** 0.094***

(0.033) (0.029) (0.033) (0.031)

Ln_Target_Capital 0.130 -0.054 0.088 -0.102

(0.159) (0.153) (0.169) (0.152)

Equity_Offered -0.568 -2.321 -1.028 -2.708*

(1.758) (1.420) (1.847) (1.470)

Voting_Rights_Threshold -0.080 0.192 -0.028 0.239

(0.350) (0.371) (0.377) (0.372)

SEIS -0.319 -0.208 -0.324 -0.296

(0.237) (0.194) (0.236) (0.192)

Exit_IPO -0.137 -0.085 -0.134 0.022

(0.246) (0.246) (0.259) (0.263)

Dividends 0.007 0.153 -0.022 0.058

(0.401) (0.390) (0.412) (0.361)

Duration 0.008 0.019*** 0.013* 0.021***

(0.007) (0.006) (0.007) (0.006)

Industry dummies YES YES YES YES

Constant 2.949** 2.754** 2.826** 3.481***

(1.296) (1.165) (1.286) (1.074)

Obs. 108 108 108 108

lnalpha -0.238** -0.510*** -0.067 -0.330**

(0.106) (0.112) (0.112) (0.130)

Pseudo R2 0.0597 0.0894 0.0592 0.0889

Robust St. Err. in parentheses. *** p<0.01, ** p<0.05, * p<0.10.

26

Appendix– Correlation matrix

1 2 3 4 5 6 6 8 9 10 11

1 Early_Investors_5 1.0000

2 Public_Investors_5 0.0948 1.0000

3 Social_Capital 0.4603* 0.0606 1.0000

4 TMT_Size 0.1112 0.0981 0.1044 1.0000

5 Ln_Target_Capital 0.2347* 0.1618 0.2870* 0.1959* 1.0000

6 Equity_Offered -0.0419 -0.0713 -0.1835 -0.2707* 0.0866 1.0000

7 Voting_Rights_Threshold -0.0240 0.0180 0.2571* -0.0824 0.0588 -0.1710 1.0000

8 Tax_Incentives 0.0598 -0.1724 -0.0742 -0.2481* -0.2908* 0.1076 0.0570 1.0000

9 Exit_IPO -0.0067 0.0082 0.0203 -0.0199 0.1234 0.0548 -0.0287 0.0551 1.0000

10 Dividends -0.0303 -0.0094 0.0256 -0.2159* -0.2004* 0.2045* 0.2245* -0.0024 -0.0123 1.0000

11 Duration -0.4100* -0.0436 -0.1499 -0.0766 0.0745 -0.0372 0.0140 -0.0662 0.0289 -0.1139 1.0000

27

Figure 1 – Screenshot of the “Investors” page for a Crowdcube pitch.

28

Figure 2 – Distribution of the percentage of amount raised at the end of the pitch, relative to target.

0

5

10

15

20

25

30

35

40

0-20 20-40 40-60 60-80 80-100 100-120 120-150 >150

Funding amount, as % of target

29

Figure 3 – Number of bidding investors during the pitch, distinguishing between successful and successful projects.

0

20

40

60

80

100

120

140

160

0 3 6 9 12 15 18 21 24 27 30 33 36 39 42 45 48 51 54 57 60

Number of investors over time

Successful

Unsuccessful