indian unicorns will continue to strengthen through acquisitions in mobile, marketplaces & data...

TRANSCRIPT

India Technology Product M&A Industry Monitor

June 2015

2 Think Next Roundtable Report - India Technology Product M&A Industry Monitor

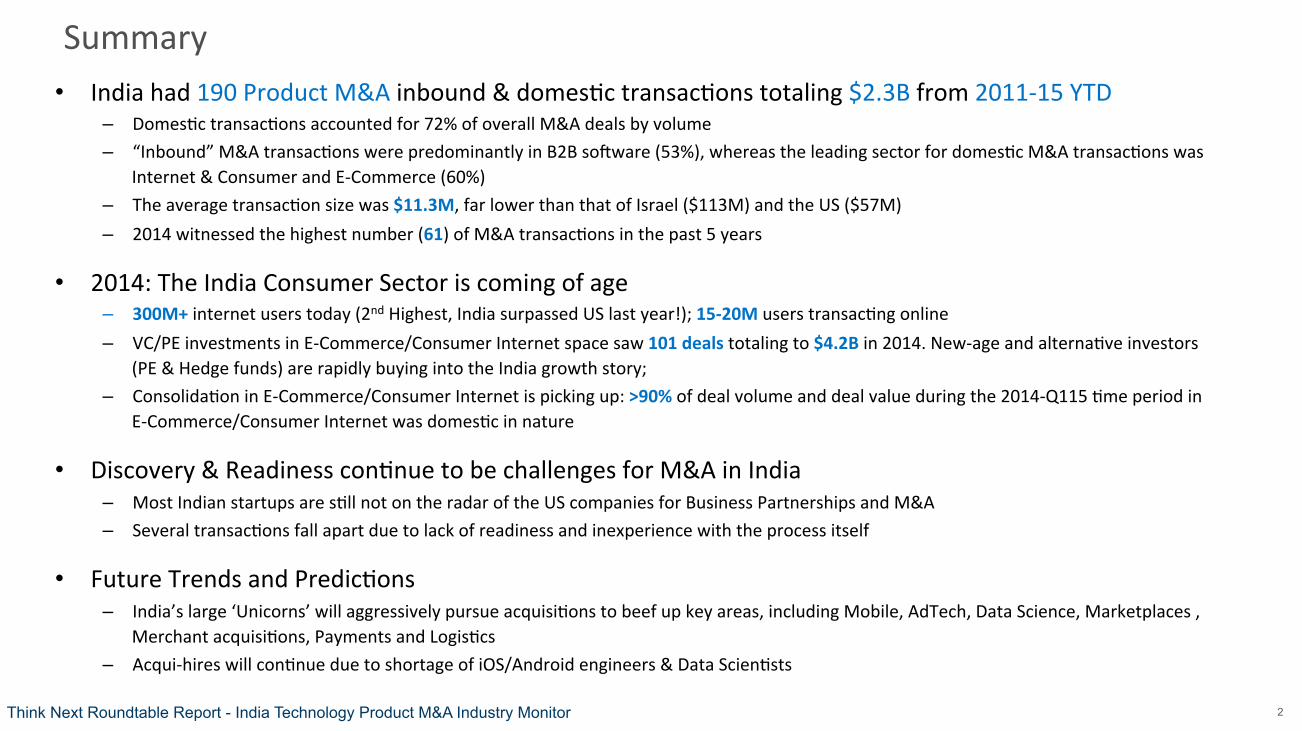

Summary • India had 190 Product M&A inbound & domes:c transac:ons totaling $2.3B from 2011-‐15 YTD

– Domes:c transac:ons accounted for 72% of overall M&A deals by volume – “Inbound” M&A transac:ons were predominantly in B2B soOware (53%), whereas the leading sector for domes:c M&A transac:ons was

Internet & Consumer and E-‐Commerce (60%) – The average transac:on size was $11.3M, far lower than that of Israel ($113M) and the US ($57M) – 2014 witnessed the highest number (61) of M&A transac:ons in the past 5 years

• 2014: The India Consumer Sector is coming of age – 300M+ internet users today (2nd Highest, India surpassed US last year!); 15-‐20M users transac:ng online – VC/PE investments in E-‐Commerce/Consumer Internet space saw 101 deals totaling to $4.2B in 2014. New-‐age and alterna:ve investors

(PE & Hedge funds) are rapidly buying into the India growth story; – Consolida:on in E-‐Commerce/Consumer Internet is picking up: >90% of deal volume and deal value during the 2014-‐Q115 :me period in

E-‐Commerce/Consumer Internet was domes:c in nature

• Discovery & Readiness con:nue to be challenges for M&A in India – Most Indian startups are s:ll not on the radar of the US companies for Business Partnerships and M&A – Several transac:ons fall apart due to lack of readiness and inexperience with the process itself

• Future Trends and Predic:ons – India’s large ‘Unicorns’ will aggressively pursue acquisi:ons to beef up key areas, including Mobile, AdTech, Data Science, Marketplaces ,

Merchant acquisi:ons, Payments and Logis:cs – Acqui-‐hires will con:nue due to shortage of iOS/Android engineers & Data Scien:sts

3 Think Next Roundtable Report - India Technology Product M&A Industry Monitor

VC/PE Funding is a strong source of Growth Capital for Indian Technology Product Companies

28 31 29 49

22

81 95

74

101

74

20 21

20

26

31

0

40

80

120

160

200

2011 2012 2013 2014 YTD 2015

# De

als

B2B SoOware Internet & Consumer / E-‐Commerce Mobility

99 143 171 377 248 555 603 808

4,209

1662 316 55

42

297

192

0

500

1000

1500

2000

2500

3000

3500

4000

4500

2011 2012 2013 2014 YTD 2015

USD

Mn

B2B SoOware Internet & Consumer / E-‐Commerce Mobility

India VC / PE Investments: Deal Value

India VC / PE Investments: Deal Volume § Investment in has grown by ~ between 2010-‐2014;.

§ was invested in this sector in 2014 alone, with the two main companies (Flipkart & Snapdeal) accoun:ng for > 50% of the Indian internet investment dollars

§ Investments in showing an upward trend

~$1,910 M ~$1,111 M ~$652 M

~$300 M ~$123 M ~$113 M

Marquee PE/VC Investments Between 2014 And Q1 2015

Source: Signal Hill analysis and research, Venture Intelligence, YTD as on March 31, 2015

4 Think Next Roundtable Report - India Technology Product M&A Industry Monitor

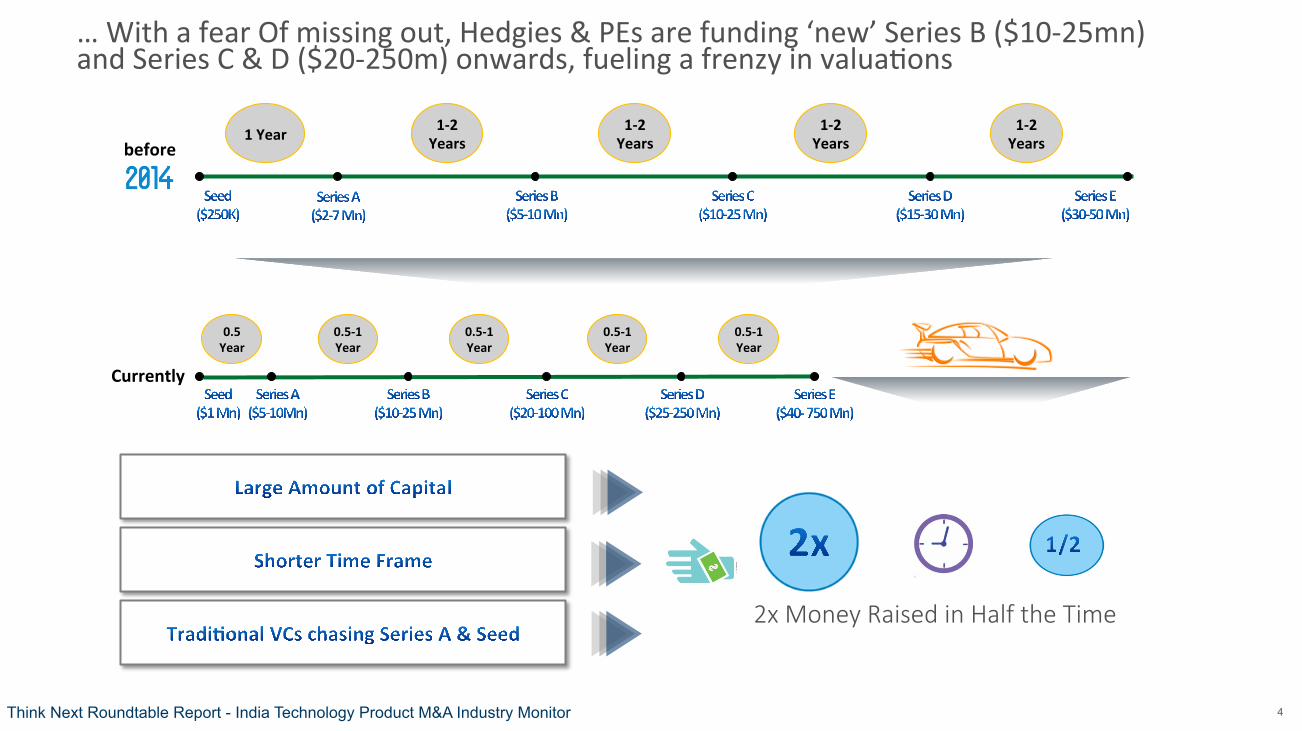

… With a fear Of missing out, Hedgies & PEs are funding ‘new’ Series B ($10-‐25mn) and Series C & D ($20-‐250m) onwards, fueling a frenzy in valua:ons

1 Year 1-‐2 Years

1-‐2 Years

1-‐2 Years

1-‐2 Years

0.5 Year

0.5-‐1 Year

0.5-‐1 Year

0.5-‐1 Year

0.5-‐1 Year

2x Money Raised in Half the Time

before

Currently

5 Think Next Roundtable Report - India Technology Product M&A Industry Monitor

New Age and Alterna:ve Investors are making a beeline to India…

The Early Risers With Long Term Commitment To Tech Inves]ng In India

Buoyant Market Condi]ons : Many Hedge Funds & Family Offices Buying Into India Internet & Sodware

DST Global

6 Think Next Roundtable Report - India Technology Product M&A Industry Monitor

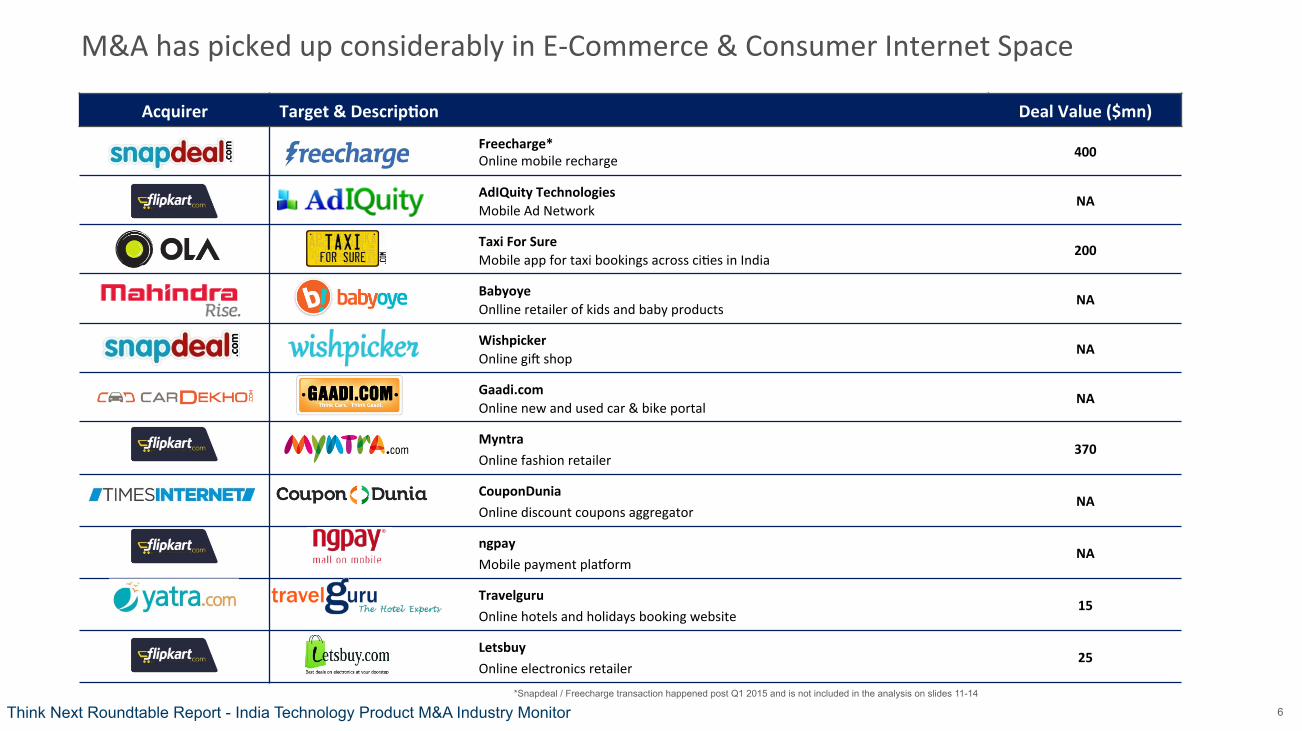

M&A has picked up considerably in E-‐Commerce & Consumer Internet Space

Acquirer Target & Descrip]on Deal Value ($mn)

Freecharge* Online mobile recharge 400

AdIQuity Technologies Mobile Ad Network

NA

Taxi For Sure Mobile app for taxi bookings across ci:es in India

200

Babyoye Onlline retailer of kids and baby products

NA

Wishpicker Online giO shop

NA

Gaadi.com Online new and used car & bike portal

NA

Myntra Online fashion retailer

370

CouponDunia Online discount coupons aggregator

NA

ngpay Mobile payment plaporm

NA

Travelguru Online hotels and holidays booking website

15

Letsbuy Online electronics retailer

25

*Snapdeal / Freecharge transaction happened post Q1 2015 and is not included in the analysis on slides 11-14

7 Think Next Roundtable Report - India Technology Product M&A Industry Monitor

Global Technology Majors have started looking at India, mostly for Technology and Talent acquisi:ons

Acquirer Target & Descrip]on

Zipdial Mobile marke:ng and engagement plaporm

BookPad Online document crea:on and collabora:on soOware

Limle Eye Labs Mobile app analysis tools for app developers and testers

Dexetra Mobile app with Contextual Recommenda:ons

Talent Neuron Market Intelligence Tech Tools based on data-‐analy:cs

Impermium Cyber Security

KDK Sodware SoOware solu:ons for payroll processing, personal finance, and tax prepara:on and filing in India

Redbus Online bus :cke:ng website

8 Think Next Roundtable Report - India Technology Product M&A Industry Monitor

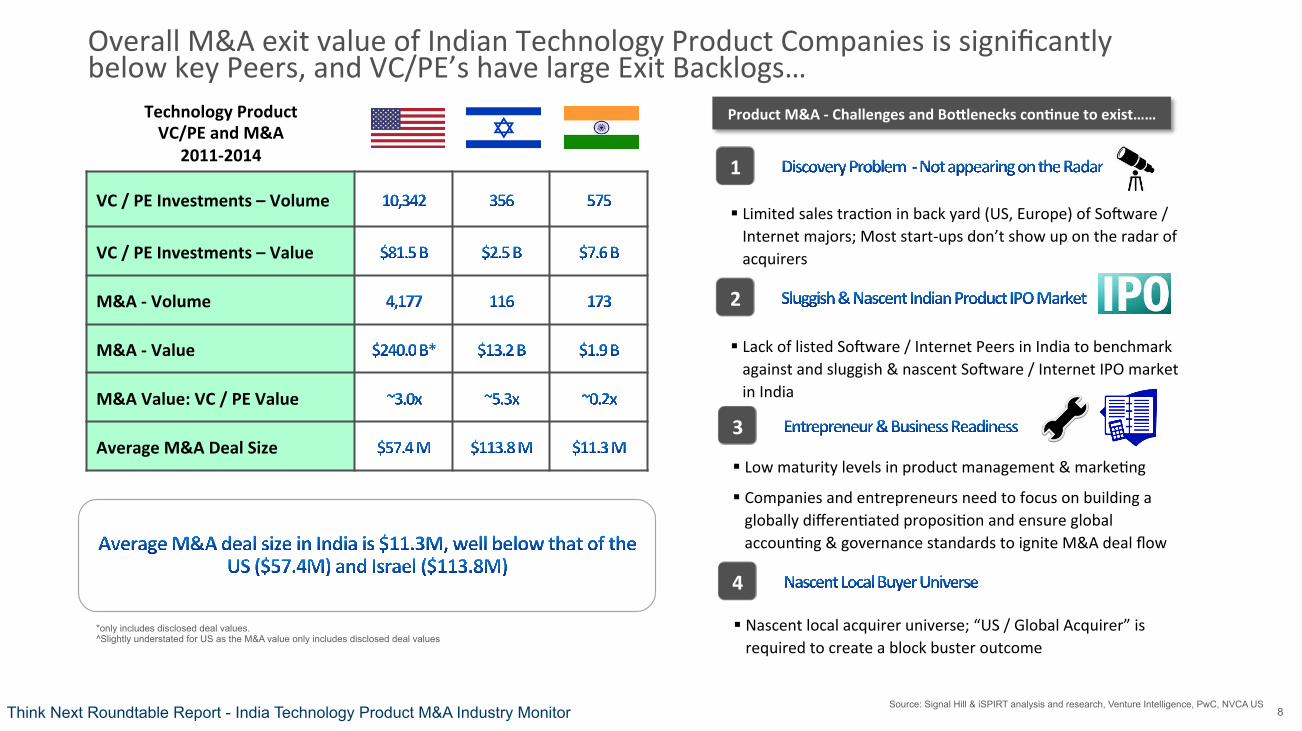

Overall M&A exit value of Indian Technology Product Companies is significantly below key Peers, and VC/PE’s have large Exit Backlogs…

Source: Signal Hill & iSPIRT analysis and research, Venture Intelligence, PwC, NVCA US

Technology Product VC/PE and M&A

2011-‐2014

VC / PE Investments – Volume

VC / PE Investments – Value

M&A -‐ Volume

M&A -‐ Value

M&A Value: VC / PE Value

Average M&A Deal Size

Product M&A -‐ Challenges and Bomlenecks con]nue to exist……

§ Limited sales trac:on in back yard (US, Europe) of SoOware / Internet majors; Most start-‐ups don’t show up on the radar of acquirers

1

§ Lack of listed SoOware / Internet Peers in India to benchmark against and sluggish & nascent SoOware / Internet IPO market in India

2

§ Low maturity levels in product management & marke:ng

§ Companies and entrepreneurs need to focus on building a globally differen:ated proposi:on and ensure global accoun:ng & governance standards to ignite M&A deal flow

3

4

§ Nascent local acquirer universe; “US / Global Acquirer” is required to create a block buster outcome

*only includes disclosed deal values. ^Slightly understated for US as the M&A value only includes disclosed deal values

9 Think Next Roundtable Report - India Technology Product M&A Industry Monitor

India Technology Product M&A : 2011 – YTD 2015

Product M&A Deal Volume (Cumula]ve) : 2011 – Q1 2015 Product M&A Deal Value (Cumula]ve) : 2011 – Q1 2015

29%

36%

14%

7%

14%

31%

31%

23%

5%

9%

-‐ Internet & Consumer accounted for 36% of deals in India and represented 31% of the overall deal value

-‐ Domes:c M&A transac:ons have been mostly in the Internet/Consumer and E-‐commerce space, whereas the inbound M&A deals have predominantly been in the B2B SoOware area

-‐ Volume of M&A in mobile has increased from 9% in 2010 -‐ Q1 2014 to 14% in 2011 -‐ Q1 2015 period

AdTech & Marke:ng Automa:on B2B SoOware Internet & Consumer E-‐Commerce Mobile

Source: Signal Hill & iSPIRT analysis and research, Venture Intelligence, YTD as on March 31, 2015

10 Think Next Roundtable Report - India Technology Product M&A Industry Monitor

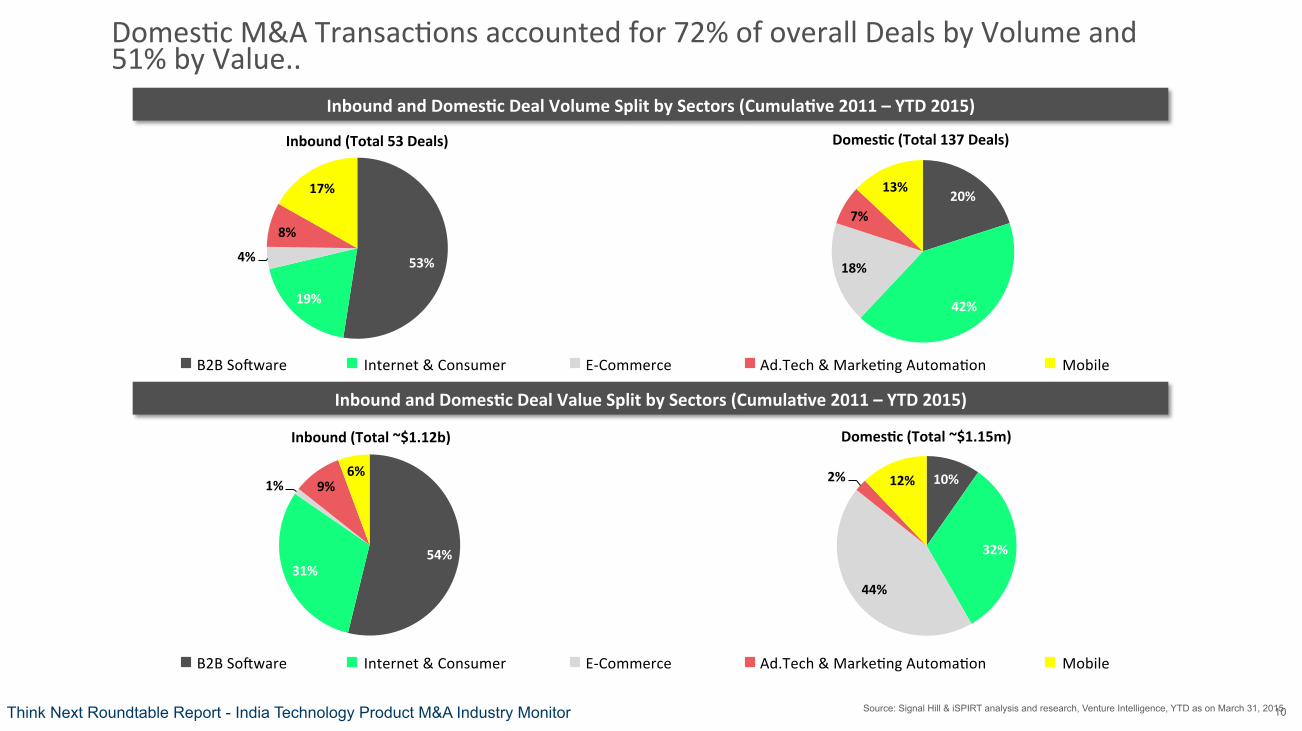

Inbound and Domes]c Deal Volume Split by Sectors (Cumula]ve 2011 – YTD 2015)

Domes:c M&A Transac:ons accounted for 72% of overall Deals by Volume and 51% by Value..

53%

19%

4%

8%

17%

Inbound (Total 53 Deals)

20%

42%

18%

7%

13%

Domes]c (Total 137 Deals)

54% 31%

1% 9% 6%

Inbound (Total ~$1.12b)

10%

32%

44%

2% 12%

Domes]c (Total ~$1.15m)

Inbound and Domes]c Deal Value Split by Sectors (Cumula]ve 2011 – YTD 2015)

Ad.Tech & Marke:ng Automa:on B2B SoOware Internet & Consumer E-‐Commerce Mobile

Ad.Tech & Marke:ng Automa:on B2B SoOware Internet & Consumer E-‐Commerce Mobile

Source: Signal Hill & iSPIRT analysis and research, Venture Intelligence, YTD as on March 31, 2015

11 Think Next Roundtable Report - India Technology Product M&A Industry Monitor

10 14 9 19

3

8 10 18

26

6

5

9 3

4

5

4

6 3

1

3

4 6

11

3

0

10

20

30

40

50

60

70

2011 2012 2013 2014 Q1 2015

# De

als

B2B SoOware Internet & Consumer E-‐Commerce Ad.Tech & Marke:ng Automa:on Mobile

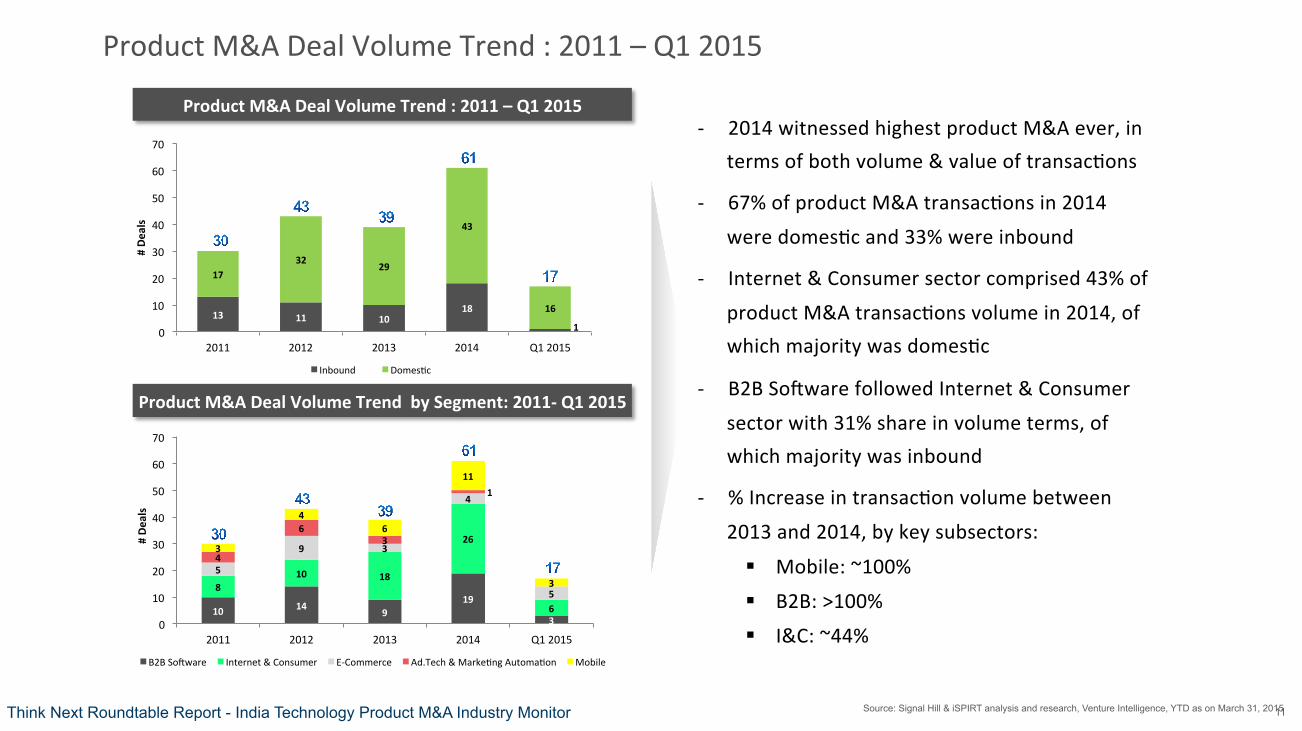

Product M&A Deal Volume Trend : 2011 – Q1 2015

13 11 10 18

1

17 32

29

43

16

0

10

20

30

40

50

60

70

2011 2012 2013 2014 Q1 2015

# De

als

Inbound Domes:c

Product M&A Deal Volume Trend : 2011 – Q1 2015

Product M&A Deal Volume Trend by Segment: 2011-‐ Q1 2015

-‐ 2014 witnessed highest product M&A ever, in terms of both volume & value of transac:ons

-‐ 67% of product M&A transac:ons in 2014

were domes:c and 33% were inbound

-‐ Internet & Consumer sector comprised 43% of

product M&A transac:ons volume in 2014, of which majority was domes:c

-‐ B2B SoOware followed Internet & Consumer

sector with 31% share in volume terms, of which majority was inbound

-‐ % Increase in transac:on volume between

2013 and 2014, by key subsectors:

§ Mobile: ~100%

§ B2B: >100%

§ I&C: ~44%

Source: Signal Hill & iSPIRT analysis and research, Venture Intelligence, YTD as on March 31, 2015

12 Think Next Roundtable Report - India Technology Product M&A Industry Monitor

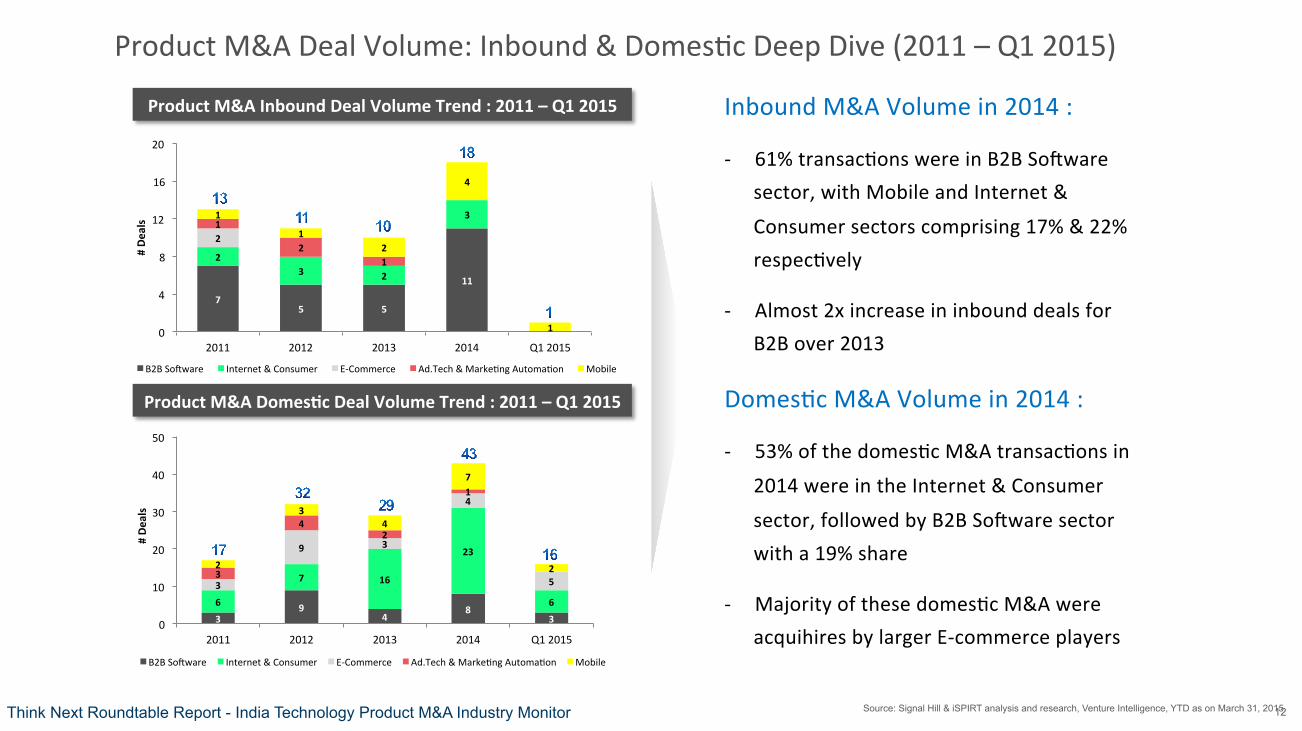

Product M&A Deal Volume: Inbound & Domes:c Deep Dive (2011 – Q1 2015)

Product M&A Inbound Deal Volume Trend : 2011 – Q1 2015

Product M&A Domes]c Deal Volume Trend : 2011 – Q1 2015

Inbound M&A Volume in 2014 :

-‐ 61% transac:ons were in B2B SoOware sector, with Mobile and Internet &

Consumer sectors comprising 17% & 22% respec:vely

-‐ Almost 2x increase in inbound deals for B2B over 2013

Domes:c M&A Volume in 2014 :

-‐ 53% of the domes:c M&A transac:ons in

2014 were in the Internet & Consumer

sector, followed by B2B SoOware sector with a 19% share

-‐ Majority of these domes:c M&A were acquihires by larger E-‐commerce players

3 9

4 8

3

6

7 16

23

6

3

9 3

4

5 3

4 2

1

2

3 4

7

2

0

10

20

30

40

50

2011 2012 2013 2014 Q1 2015

# De

als

B2B SoOware Internet & Consumer E-‐Commerce Ad.Tech & Marke:ng Automa:on Mobile

7 5 5

11

2 3 2

3

2 1

2 1

1

1 2

4

1 0

4

8

12

16

20

2011 2012 2013 2014 Q1 2015

# De

als

B2B SoOware Internet & Consumer E-‐Commerce Ad.Tech & Marke:ng Automa:on Mobile

Source: Signal Hill & iSPIRT analysis and research, Venture Intelligence, YTD as on March 31, 2015

13

605

69

233 184

30

22

136

76

637

283

0

100

200

300

400

500

600

700

800

900

2011 2012 2013 2014 Q1 2015

USD

Mn

Inbound Domes:c

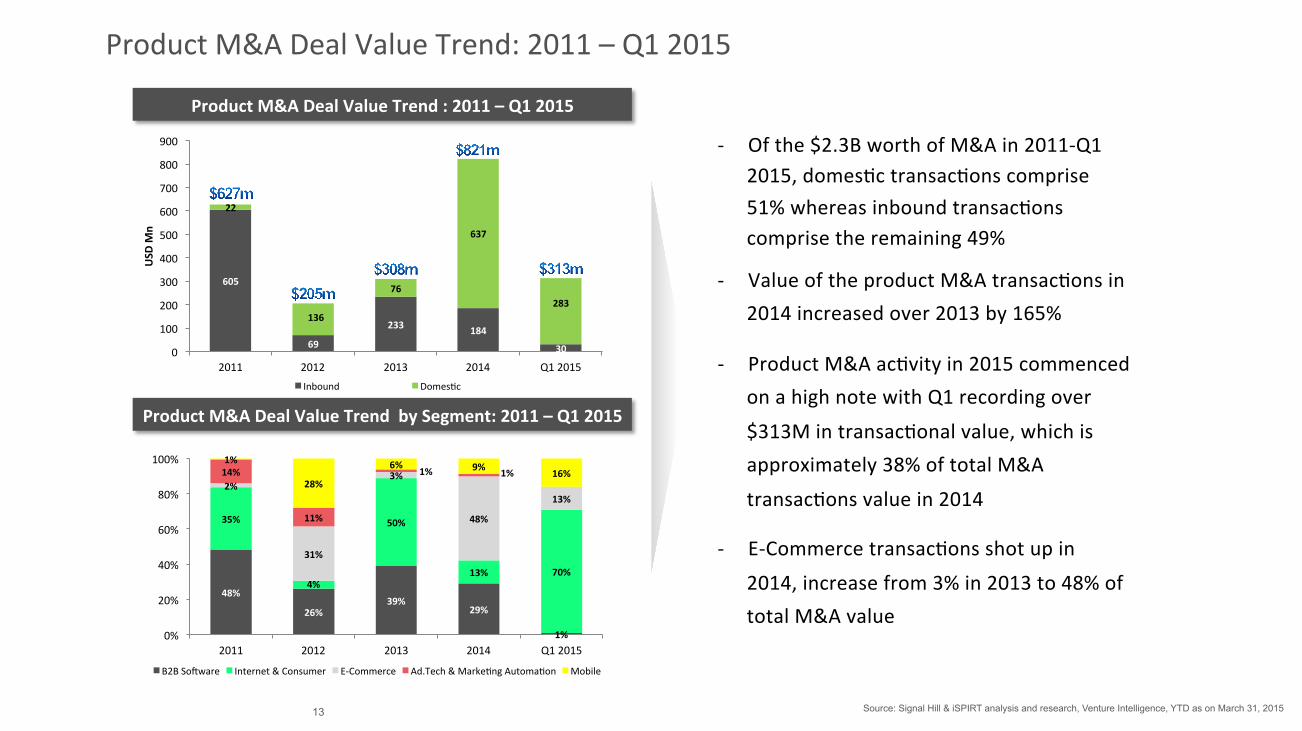

-‐ Of the $2.3B worth of M&A in 2011-‐Q1 2015, domes:c transac:ons comprise 51% whereas inbound transac:ons comprise the remaining 49%

-‐ Value of the product M&A transac:ons in 2014 increased over 2013 by 165%

-‐ Product M&A ac:vity in 2015 commenced on a high note with Q1 recording over

$313M in transac:onal value, which is approximately 38% of total M&A

transac:ons value in 2014

-‐ E-‐Commerce transac:ons shot up in

2014, increase from 3% in 2013 to 48% of total M&A value

Product M&A Deal Value Trend: 2011 – Q1 2015

Product M&A Deal Value Trend : 2011 – Q1 2015

Product M&A Deal Value Trend by Segment: 2011 – Q1 2015

48%

26% 39%

29%

1%

35%

4%

50%

13% 70%

2%

31%

3%

48%

13%

14%

11%

1% 1% 1%

28%

6% 9% 16%

0%

20%

40%

60%

80%

100%

2011 2012 2013 2014 Q1 2015

B2B SoOware Internet & Consumer E-‐Commerce Ad.Tech & Marke:ng Automa:on Mobile

Source: Signal Hill & iSPIRT analysis and research, Venture Intelligence, YTD as on March 31, 2015

14 Think Next Roundtable Report - India Technology Product M&A Industry Monitor

Product M&A Deal Value: Inbound & Domes:c Deep Dive (2011 – Q1 2015)

49% 64%

49%

81%

38% 4% 43%

14% 13%

32%

7% 5%

100%

0%

20%

40%

60%

80%

100%

2011 2012 2013 2014 Q1 2015 B2B SoOware Interenet & Consumer / E-‐Commerce Others

Es]mated Product M&A Inbound Deal Value Trend : 2011 – Q1 2015

Es]mated Product M&A Domes]c Deal Value Trend : 2011 – Q1 2015

Inbound M&A Value in 2014 : -‐ Out of $179M inbound M&A in 2014,

soOware was >80% which is a substan:al increase from 49% in 2014

-‐ Internet & Commerce / Ecommerce share dropped from 43% in 2013 to 14% in 2014

Domes:c M&A Value in 2014 : -‐ Domes:c M&A was dominated by Mobile

as a result of several small acquihires

-‐ Internet & consumer con:nued to dominate the value, a trend started in 2013

25% 7% 7% 14%

1%

41%

51%

84% 75% 92%

34% 42%

9% 11% 7%

0%

20%

40%

60%

80%

100%

2011 2012 2013 2014 Q1 2015

B2B SoOware Interenet & Consumer / E-‐Commerce Others

Source: Signal Hill & iSPIRT analysis and research, Venture Intelligence, YTD as on March 31, 2015

15

Key Insights from MicrosoO Ventures’ Think Next Roundtable

1. The India Consumer Sector has come of age a) India has 300M+ internet users today, with 15-‐20M users transac:ng online. India surpassed US (~279M) in

Dec2014 in terms of number of internet users and is only second to China (~600M)

b) Amazon has said that India was fastest to a $1B GMV for them;

c) New investors such as Tiger, DST Global, SoObank are wri:ng large cheques

2. Discovery: con:nues to be challenge #1 for India product companies for M&A a) Most startups are s:ll not on the radar the big US acquirers for BD and eventual M&A

b) Most of the M&A transac:ons are very small and are domes:c (India for India transac:ons)

3. Entrepreneur Readiness emerging as a new focus area during the M&A process a) Most entrepreneurs haven’t been through an M&A before, and are unsure about how to handle the process

b) For every deal that goes through, there are 4-‐5 others that fail because of readiness/prepara:on issues

c) iSPIRT offers an “M&A hotline” to entrepreneurs to provide support and advice in the event of inbound M&A interest

16

Key Insights from MicrosoO Ventures’ Think Next Roundtable (Cont’d)

4. India and China are different in the evolu:on of startups a) Due to protec:ve regula:ons by the Chinese government, several US companies (e.g.: YouTube and Facebook) cant

operate in China, so local companies like Baidu and Tencent can create mul:-‐Billion $ companies

b) Chinese companies historically have cultural and language barriers to expand interna:onally & hence usually focus on the domes:c market. On the other hand, India has 2 types of startups: India-‐for-‐India and India for global

c) Indian companies inherently have a big advantage over Chinese firms in addressing the global market

5. Acqui-‐hires (acquisi:ons with the sole intent of acquiring engineering talent) are extremely hot today a) Huge shortage of big data, analy:cs & android/iOS engineers in the valley;

b) Obviously, VC investors are less excited about acquihires & view them as a “last op:on”. On the other hand, founders view acquihires as a ‘badge of pedigree’

c) Bar is very high for startups – the en:re team will go through interviews during the process, and several startups fail this stage. An interna:onal team can expect to move to the US aOer the deal

17

6. A new genera:on of entrepreneurs coming up in India a) Looking to build deep-‐tech companies based out of India, serving the global market

b) Very much vision-‐driven: want to change the world rather than “sell-‐out” early

c) These entrepreneurs are also likely to be angel investors and help other startups succeed, in parallel to running their own firm

7. Venture economics works differently for entrepreneurs, VCs and angel investors

a) First-‐:me entrepreneurs have a higher incen:ve to ‘cash out’ earlier, since they have invested a large part of their :me with limited salary

b) The VC has the opposite perspec:ve: sta:s:cs say that only 10% of VC investments are “home runs” and return the fund, and so the VC wants to stay longer in the companies that are poten:al winners

c) Angel investors should not expect to exit during series-‐A, and should plan to stay long term. Usually a larger investor comes in during series-‐C and will buy-‐out the angels shares in order to obtain a larger shareholding %

Key Insights from MicrosoO Ventures’ Think Next Roundtable (Cont’d)

18

Future Trends & Predic:ons for 2015

1. The large Indian “Unicorns” will aggressively make strategic acquisi:ons to beef up key areas: focus areas include Mobile, Big Data / Analy:cs, Payments, AdTech, etc.

2. Technology Product M&A volumes and values will con:nue to increase rapidly. In B2B SoOware cross-‐border M&A

will con:nue to dominate transac:on volumes & values whereas in E-‐Commerce and Internet & Consumer domes:c M&A transac:ons will con:nue to dominate

3. Significant VC/PE funds will con:nue to flow into E-‐Commerce and Consumer Internet sectors, as new alterna:ve investors con:nue to enter the market. Key sectors will include the “unbundling and sharing” economy, as well as disrup:ve fintech

players (payments, crowdsourced financing etc)

4. Internet of Things [IOT] will receive significant interest from VCs and large acquirers: startups looking to take advantage of the ‘sensorifica:on’ of various sectors, including healthcare, enterprise, wearables and industries

5. Acqui-‐Hires will con:nue to be a cri:cal component for US and India companies: cri:cal areas include iOS, Android engineers and Machine Learning/Data Science experts

Signal Hill is a leading independent advisory bou:que serving the M&A and private capital raising needs of growth companies. Signal Hill’s experienced bankers provide deep domain exper:se and an unyielding commitment to clients in our sectors: Internet & Digital Media, Internet Infrastructure, Services and SoOware. With over 600 completed transac:ons and offices in Bal:more, Bangalore, Boston, Nashville, New York, Reston and San Francisco, Signal Hill leverages deep strategic industry and financial sponsor rela:onships to help our clients achieve Greater Outcomes®.

19

iSPIRT Founda:on is an industry think-‐tank founded by key par:cipants and proponents of the Indian soOware product industry. iSPIRT enables a strong ecosystem, connects and guides soOware product entrepreneurs and helps catalyse business growth. It encourages buyers to improve performance by leveraging soOware products effec:vely. iSPIRT advises policy makers on interven:ons that can set the industry on a higher growth trajectory

For ques]ons, please contact:

Sanat Rao, Partner (M&A), iSPIRT [email protected]

Klaas Oskam Managing Director, Signal Hill India [email protected]

This document has been prepared by Signal Hill Capital Advisory India Private Limited (“SHI”) & iSPIRT for discussion purposes only. The informa:on and opinions contained in this document are derived from public and private sources which we believe to be reliable and accurate but which, without further inves:ga:on cannot be warranted as to their accuracy, completeness or correctness. This informa:on is supplied on the condi:on that SHI and any partner, employee or affiliate of SHI are not liable for any error or inaccuracy contained herein, whether negligently caused or otherwise, or for loss or damage suffered by any person due to such error, omission or inaccuracy as a result of such a supply. SHI and its affiliates are also not liable for any loss or damage howsoever caused by relying on the informa:on provided in this document. In par:cular any numbers, ini:al valua:ons and schedules contained in this document are preliminary and are for discussion purposes only and does not cons:tute an opinion.

MicrosoO Ventures, a global ini:a:ve by MicrosoO, is a strategic partner for promising startups around the world focused on business growth and development, industrial strength technology and beau:ful usable products. Build locally, scale globally. We help smart companies take flight.

Gayathri Sharma Head – Ecosystem Alliances, MicrosoO Ventures