indian power

TRANSCRIPT

THE INDIAN POWER SECTOR

Marching Towards a New Paradigm

DIVYA LIZ GEORGEDHARA B SHAHGEORGE JACOBMARY MONISHASHANKAR R

AGENDA

Indian Power Sector – A Glance

Major Players

Porters Five Force Analysis

Generation

Transmission & Distribution

Growth Drivers

Challenges & Quick Fixes

THE POWER SECTOR – AT A GLANCE

4th largest producer & consumer

of electricity

Expected CAGR – 7.5% over 2015-16

to 2020

Robust growth in

renewables

Favourable policy

environment

5th largest installed capacity[2,72,687

MW]

A

A

Installed Capacity

69%

15%

2% 13%

Thermal Hydro Nuclear RES

COAL 87%

GAS 12%

OIL 1%

FY 11 FY 12 FY 13 FY 14 FY 15 E

831 862937

9981072CAGR 5.2%

Demand for Power Growth Rate [In bn units]

FY 16 P FY 17 P FY 18 P FY 19 P FY 20 P

1,1421,223

1,3191,425

1,541CAGR 7.5%

Projected Demand Growth for Power for next 5 Years [bn units]

45%

22%

7%

26%

FY 2015Industrial Agricultural Commercial Domestic

Sector wise Demand Growth

41%

20%8%

31%

FY 2020E

Industrial AgriculturalCommercial Domestic

MAJOR PLAYERS

CENTRAL

PRIVATE

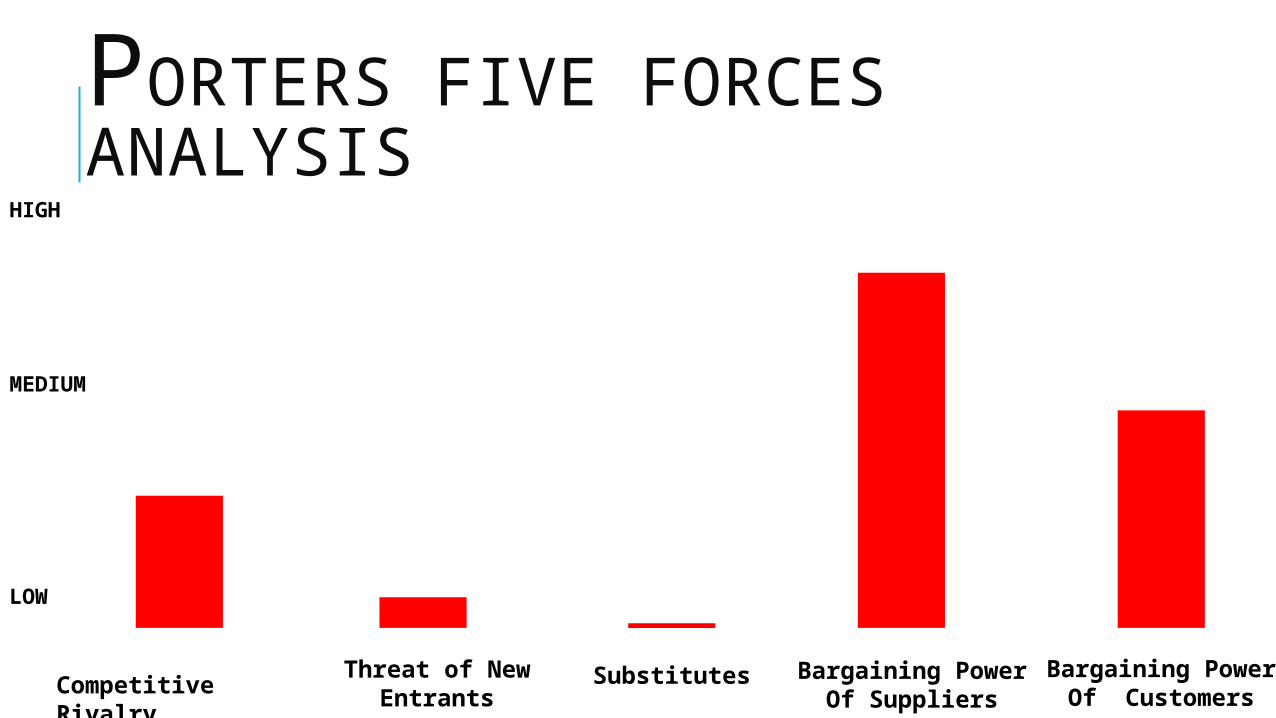

PORTERS FIVE FORCES ANALYSIS

Competitive Rivalry

Threat of New Entrants

Substitutes Bargaining PowerOf Suppliers

Bargaining PowerOf Customers

HIGH

MEDIUM

LOW

GENERATION

Power Demand-Supply

FY 11 FY 12 FY 13 FY 14 FY 15 0

200

400

600

800

1000

1200

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

De-mand

Supply

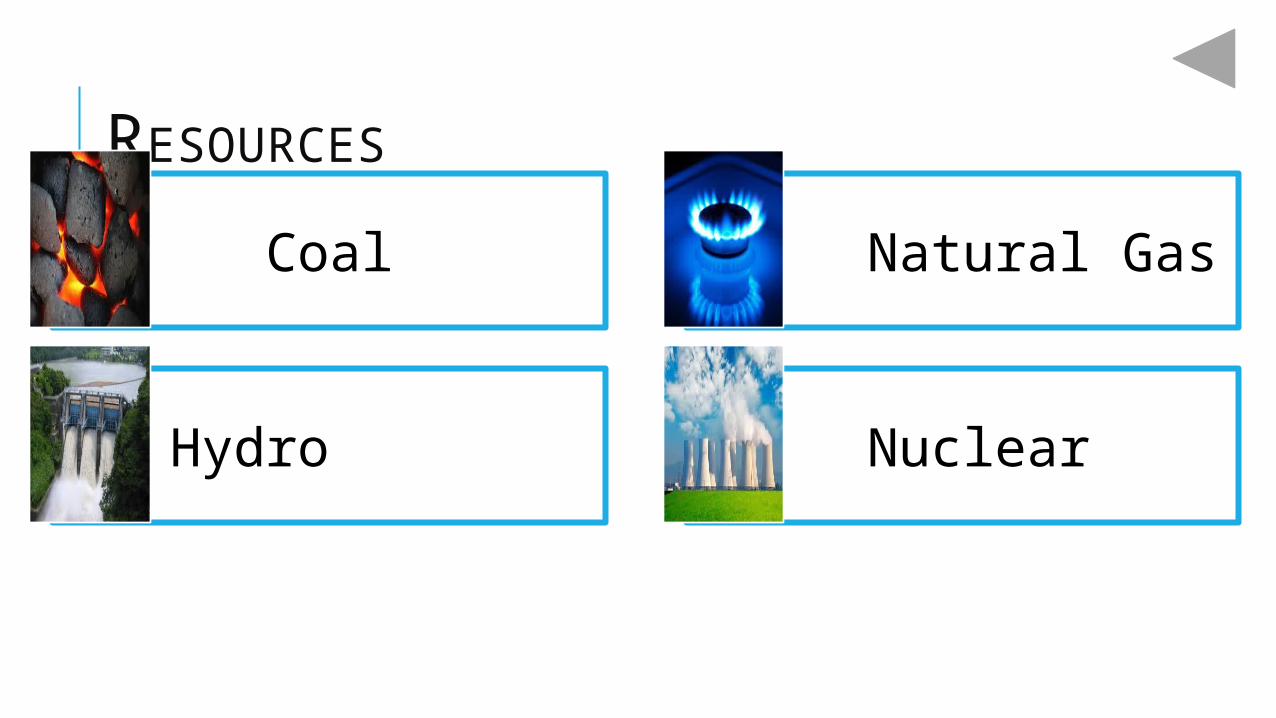

RESOURCES

Coal Natural Gas

Hydro Nuclear

transmission

distribution&

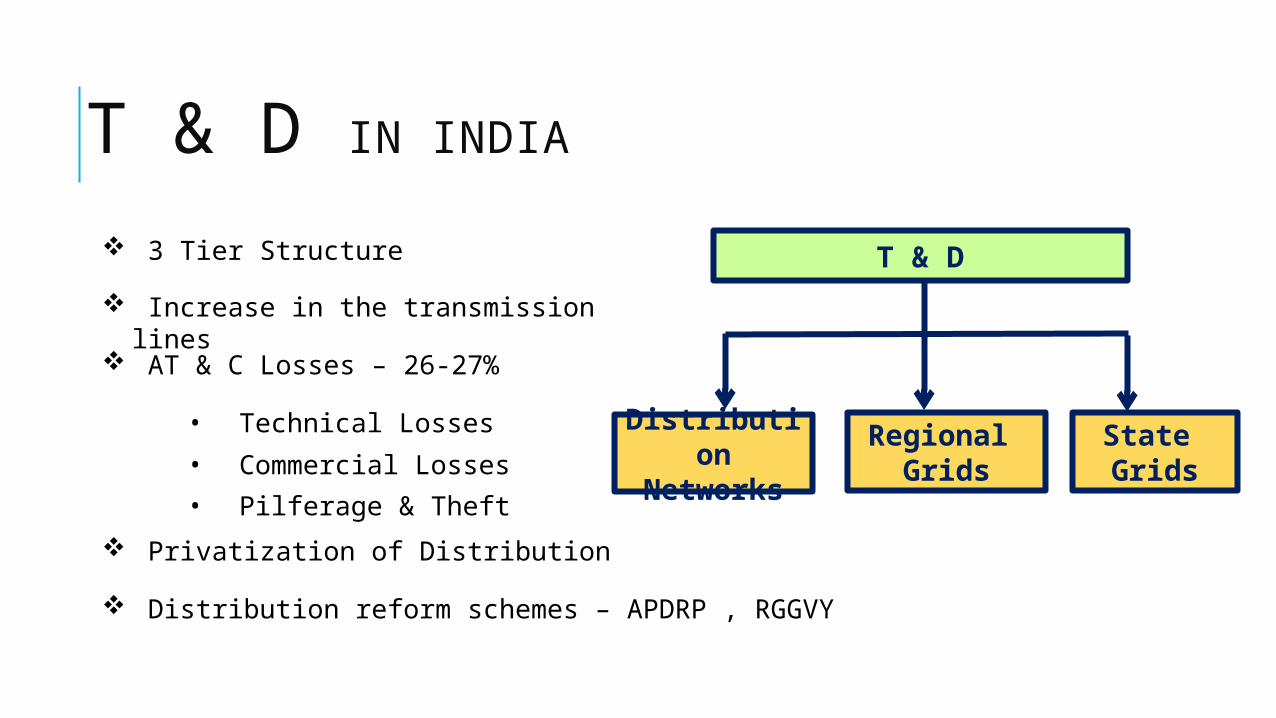

T & D IN INDIA

T & D

Distribution

Networks

State Grids

Regional Grids

3 Tier Structure

Increase in the transmission lines

AT & C Losses – 26-27%

• Technical Losses

• Commercial Losses

• Pilferage & Theft

Privatization of Distribution

Distribution reform schemes – APDRP , RGGVY

2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12 2012-13 -

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

9,000,000

10,000,000

Power : Transmission Lines

GROWTH DRIVERSGrowing Demand

Increase in industrial Activity

Increasing penetration, per-capita consumption

CHALLENGES IN POWER SECTOR Stretched financials and

developers Lack of long term PPA

Delay in clearances

Expansions through acquisitions

Limited gas availability

Constraints on financial flexibility of the players

QUICK FIXES

Land Acquisitions

Obtaining Forest & Environment clearances

Extent of fuel supply

Ordering BTC equipment

PPA

BUDGET IN ACTION Clean energy cess on coal

doubled Budget allocation to T&D up by

26% Setting up of NIIF, corpus of Rs 200B

Setting up of 5 UMPP’S

INR 5B towards proposed ultra mega solar power projects

SOURCE : CRISIL RESEARCH

THANK YOU