india’s top residential investment opportunities · 19% rs 26 l rs 10 l ravet pune 20% rs 28 l rs...

TRANSCRIPT

India’s top residential

investment

opportunities Investment Advisory Report

November 2012

1

INVESTMENT DESTINATIONS - INDIA

Presented by:-

Gulam Zia

Executive Director, Advisory, Retail & Hospitality

2nd February 2013

2

20-YEARS PERFORMANCE OF VARIOUS

ASSET CLASSES

Current value of Rs.1 crore invested in 1992

* Prices exhibits South Mumbai property Real Estate

Silver

Gold

Sensex

USD

1.9 Cr

4 Cr

7 Cr

7.5 Cr

10 Cr

3

APPROACH FOR IDENTIFICATION OF THE TOP

RESIDENTIAL INVESTMENT DESTINATIONS

4

DESTINATION Connectivity to important locations

Proximity to office space Access to social infra Planned Development

Land availability Lifestyle shift

ZONE Employment: Occupied office space, industrial activity

Social & physical infrastructure: Analysis of development plan and extensive field survey

TOP 5 CITIES Business activities:

Banking penetration, hotel room demand, air passenger traffic Infrastructure development:

Current and proposed infrastructure spending

TOP 100 CITIES Top 100 cities based on population

INDIA Urban centres

MUMBAI

Ulwe

• Proximity to IT/ITeS hubs of Navi Mumbai

• Upcoming Trans Harbour Link & International airport

• Upcoming Seawood-Uran suburban rail network

• Prices to increase by 145% in the next five years from 4,000/sq.ft. to 9,800/sq.ft

Wadala

• Proximity to premium office markets

• Upcoming infrastructure projects like Monorail and Eastern Freeway

• Prices to increase by 133% in the next five years from 15,000/sq.ft. to 35,000/sq.ft

Chembur

• Proximity to premium office markets

• Upcoming infrastructure projects like Monorail, Eastern Freeway and Santacruz

Chembur link road

• Prices to increase by 125% in the next five years from 12,000/sq.ft. to 27,000/sq.ft

5

6

MUMBAI

DELHI-NCR

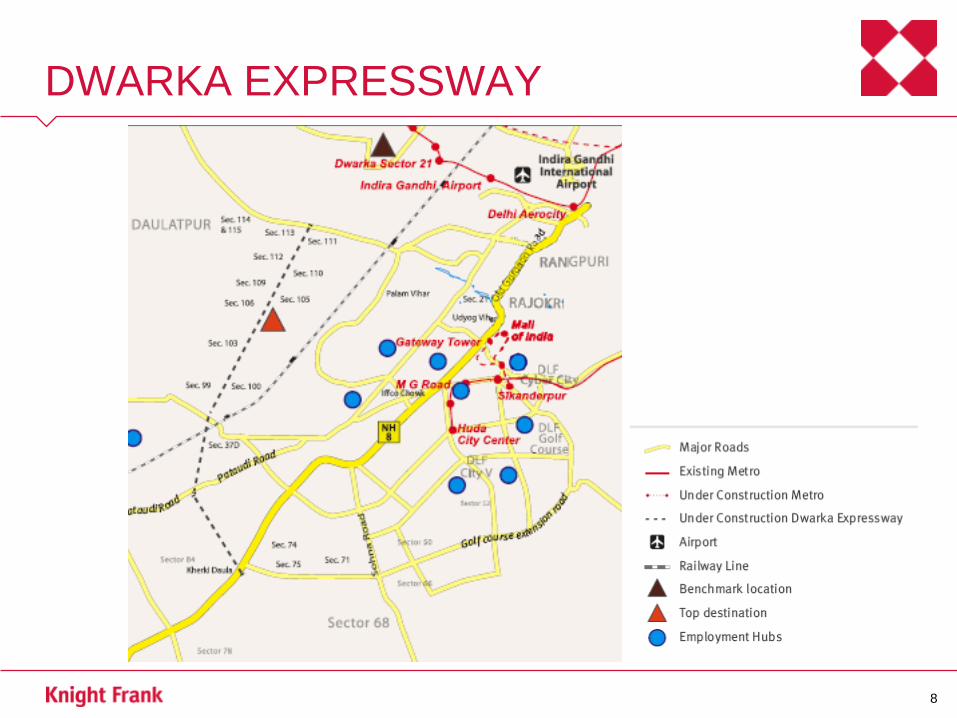

Dwarka Expressway

• Growth of IT/ITeS, BFSI & Consulting sectors

• Enhanced connectivity between Delhi & Gurgaon

• Upcoming diplomatic enclave

• Prices to increase by 108% in the next five years from 4,900/sq.ft. to 10,200/sq.ft

Noida Extension

• Growth of IT/ITeS, BFSI & Consulting sectors

• Enhanced connectivity between Delhi & Noida

• Existing sound infrastructure & affordable pricing

• Prices to increase by 111% in the next five years from 3,200/sq.ft. to 6,760/sq.ft

7

DWARKA EXPRESSWAY

8

9

NOIDA EXTENSION

CHENNAI

Medavakkam and Pallikarnai

• Growth of the IT/ITeS & Auto sector

• Proximity to employment hubs on OMR and GST Road

• Occupied office space on OMR & GST Road to increase by 64% from 29 mn sq.ft. in

2012 to 47.9 mn sq.ft in 2017

• Upcoming Monorail corridor

• Prices in Medavakkam to increase by 103% in the next five years from 3,800/sq.ft. to

7,700/sq.ft

• Prices in Pallikarnai to increase by 93% in the next five years from 4,200/sq.ft. to

8,100/sq.ft

10

CHENNAI

11

PUNE

Hinjewadi, Tathawade, Ravet and Wakad

• Growth of the IT/ITeS sector

• Strategic location on the Mumbai-Pune Bypass Road

• Proximity to employment hubs of West Pune (Hinjewadi IT Park)

• Occupied office space in West Pune to increase by 81% from 22 mn sq.ft. in 2012 to

39.5 mn sq.ft in 2017

• Prices in Hinjewadi to increase by 100% in the next five years from 4,000/sq.ft. to

8,000/sq.ft

• Prices in Tathawade to increase by 98% in the next five years from 4,300/sq.ft. to

8,500/sq.ft

• Prices in Ravet to increase by 97% in the next five years from 3,950/sq.ft. to 7,800/sq.ft

• Prices in Wakad to increase by 91% in the next five years from 4,500/sq.ft. to 8,600/sq.ft

12

13

PUNE

BENGALURU

Hebbal

• Growth of the IT/ITeS & Bio-technology sector

• Benefits of IT investment Region in North Bengaluru

• Upcoming Monorail and widening of existing roads

• Occupied office space in North Bengaluru to increase by 80% from 7.5 mn sq.ft. in 2012

to 13.5 mn sq.ft in 2017

• Prices in Hebbal to increase by 94% in the next five years from 4,250/sq.ft. to 8,230/sq.ft

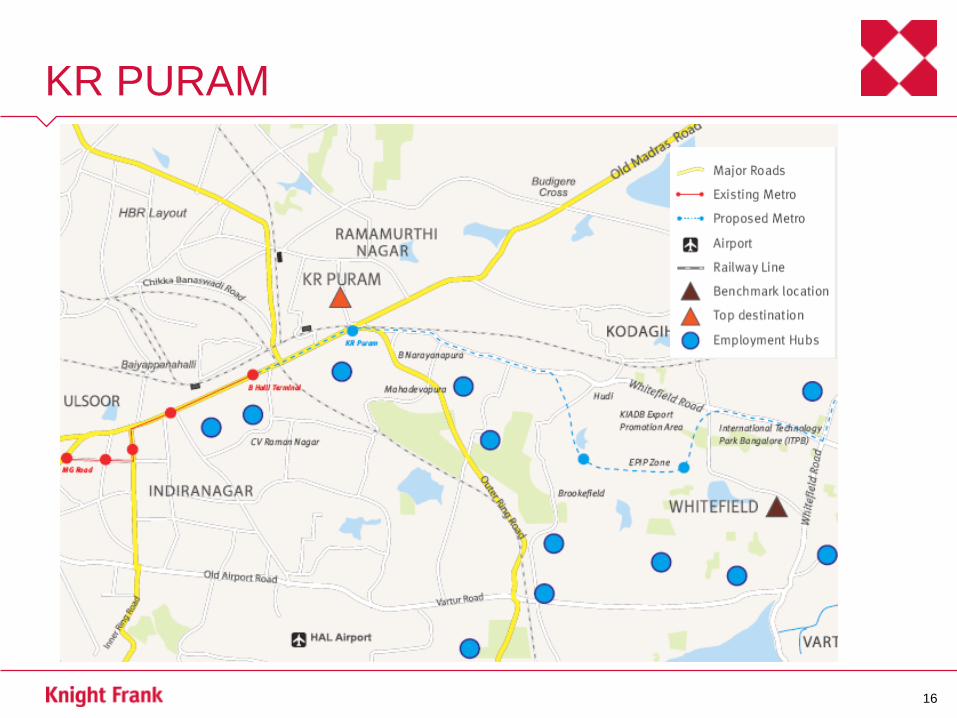

KR Puram

• Growth of the IT/ITeS & Bio-technology sector

• Lifestyle shift

• Upcoming metro connectivity

• Prices in KR Puram to increase by 91% in the next five years from 3,245/sq.ft to

6,200/sq.ft

14

15

HEBBAL

KR PURAM

16

INVESTMENT OPTIONS:

BUDGET OF UP TO RS 25 LAKH

17

Noida Extension Delhi - NCR

Destination City Min. ticket

size Investor

contribution Investor returns

23% Rs15 L Rs 6 L

Ulwe Mumbai 29% Rs15 L Rs 6L

Meddvakam Chennai 21% Rs 21 L Rs 8L

Hinjewadi Pune 21% Rs 23 L Rs 9L

Pallikarni Chennai 19% Rs 24L Rs 10L

Tathawade Pune 20% Rs 25 L Rs 10L

* Investor Returns based on Loan to Value ratio of 60%, mortgage rate of 10.5% and loan tenure of 20 yrs.

INVESTMENT OPTIONS:

BUDGET BETWEEN RS 25 TO 50 LAKH

18

Wakad Pune

Destination City Min. ticket

size Investor

contribution Investor returns

19% Rs 26 L Rs 10 L

Ravet Pune 20% Rs 28 L Rs 11L

K R Puram Bengaluru 19% Rs 31 L Rs 12L

Hebbal Bengaluru 19% Rs 36L Rs 14L

Dwarka Exp. Delhi-NCR 22% Rs 47L Rs 19L

* Investor Returns based on Loan to Value ratio of 60%, mortgage rate of 10.5% and loan tenure of 20 yrs.

INVESTMENT OPTIONS:

BUDGET OF RS 50 LAKH AND ABOVE

19

Chembur Mumbai

Destination City Min. ticket

size Investor

contribution Investor returns

26% Rs 54L Rs 22L

Wadala Mumbai 27% Rs 183 L Rs 73L

* Investor Returns based on Loan to Value ratio of 60%, mortgage rate of 10.5% and loan tenure of 20 yrs.

20

Rank Destination City2012 Average

Price (Rs./sq.ft.)

2017 Forecasted

Price (Rs./sq.ft.)

Price

Appreciation

Prices to double

In (Years)

1 Ulwe Mumbai 4,000 9,800 145% 3.4

2 Wadala Mumbai 15,000 35,000 133% 3.8

3 Chembur Mumbai 12,000 27,000 125% 4.0

4 Noida Extension Delhi-NCR 3,200 6,760 111% 4.5

5 Dwarka Expressway Delhi-NCR 4,900 10,200 108% 4.6

6 Medavakkam Chennai 3,800 7,700 103% 4.9

7 Hinjewadi Pune 4,000 8,000 100% 5.0

8 Tathawade Pune 4,300 8,500 98% 5.1

9 Ravet Pune 3,950 7,800 97% 5.1

10 Hebbal Bengaluru 4,250 8,230 94% 5.3

11 Pallikarnai Chennai 4,200 8,100 93% 5.4

12 Wakad Pune 4,500 8,600 91% 5.5

13 KR Puram Bengaluru 3,245 6,200 91% 5.5

TOP DESTINATIONS

Thank You