india investment atlas · this information is confidential and was prepared by bain & company...

TRANSCRIPT

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent

DRAFT

India Investment Atlas

Jan 2018

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 2

The India investment atlas seeks to derive four sets of insights from FDI inflows

Key questions Key questions

Aggregate trends in FDI

• How have FDI inflows grown historically? How does this compare to peers?

• Which sectors benefit? What are sectoral trends vis-à-vis manufacturing and services?

• Who are the recipients of FDI? What is the degree of consolidation in flows?

Benefits of FDI

• What do recipients use the funds for? Capex/ Capital block creation vs. M&A vs. financial funding (opex)

• How do these trends of usage vary by sector?

• How does FDI impact employment generation?

Source of FDI

• From which countries do flows originate? (Given and “true” origin)

• How do these trends vary by sector?

• What are the dynamics by investor type? (Industry investors vs. Financial investors)

Regulations / Ease of FDI

• What type of flows require approval?

• What are the trends by sector?

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 3

Approach and methodology

Key questionsWhat we have done

Areas covered Specific analyses done

Aggregatetrends in FDI

• Historical trends in FDI

• Key sectors, recipients

• Degree of ‘consolidation’ in flows- #, size of txns.

• Peer benchmarking

• Analysis of two year (FY15-17) equity flows of $83B across 24K transactions to 9000+ recipients

• Analysis of H1 FY18

Benefits of FDI

(Impact in terms of financial performance,

employment, debt reduction, etc.)

• Financial performance of FDI recipients (vs. others)

• Analysis of 6433 companies that have received FDI (RBI Census)

• Impact on employment• Mapping of FDI to sector

employment intensity

• Split of inflows across capex, M&A, debt retirement, opex

• Bottom up build across 277 recipients ($52B, 63% of total) by sector

Source of FDI

(countries/ investors driving inflows)

• Origin country and “true” origin

• Flows through tax advantaged geos

• Dynamics (in terms of ‘true’ origin) by investor type

• Tracking back origin of ~730 investors accounting for $52B (63% of total)

Regulations / Ease of FDI

• % approvals by sector, transaction size, origin

• Analysis of two year (FY15-17) flows

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 4

Summary observations and implications

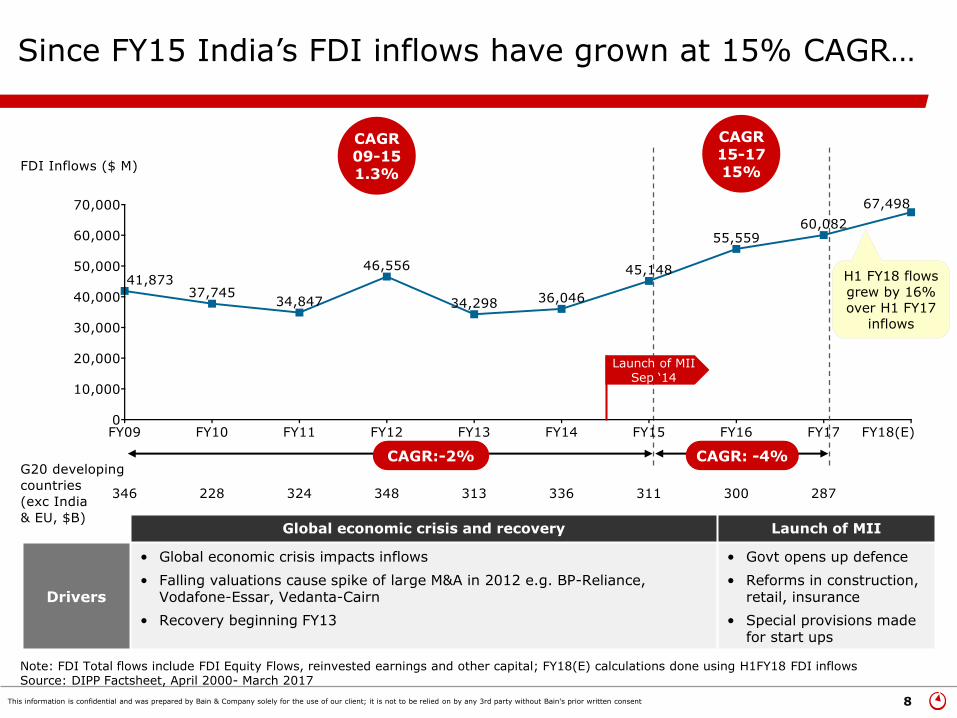

• India’s FDI inflows have accelerated since FY15, growing at 15% p.a. over the past 2 years, relative to historical growth of 1.3% p.a. over FY09-15

- Over the last two years, India has outperformed other developing countries in FDI inflows as well (inflows de-grew at 4% p.a. for the latter, over the past 2 years)

• FY15-17 saw 24K transactions to 9K+ recipients; Inflows are highly concentrated with top 150 recipients accounting for 60% of value; inflows continue to be broad-based in terms of sectors

- While the government can accelerate efforts to increase inflows to MSMEs, a set of concentrated recipients spread across 8-10 key sectors of the economy bodes well for India’s growth story going forward

• Service-oriented sectors have gained share of total inflows (59% in FY15-17 vs. 45% over FY13-15) vis-à-vis manufacturing

- Average transaction size for inflows into services sectors is smaller relative to manufacturing; however, the number of recipients is considerably higher than manufacturing

- New economy companies dominate computer related & trading sectors which account for 30% of incremental growth (FY15-17 vs. FY13-15), with an additional 35% from services sector dominated by insurance & financial services cos

- In addition to services, Electricals & electronics, Materials and Textiles saw high growth between FY14 and FY17; Energy, Auto, Pharma and Education also displayed significant uptick in H1FY18

- India has a significant share of global flows in services sectors (Information, Telecom, computer related and financial services), but continues to be underpenetrated in others

- Sectors such as pharma, energy, electronics, textiles and business services are under-penetrated but have shown strong recent growth

• Increased FDI inflows indicate better economy-wide performance: Historically, FDI receiving cos. have outperformed others on profitability (1.5X) and ROE (1.4X)

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 5

Summary observations and implications

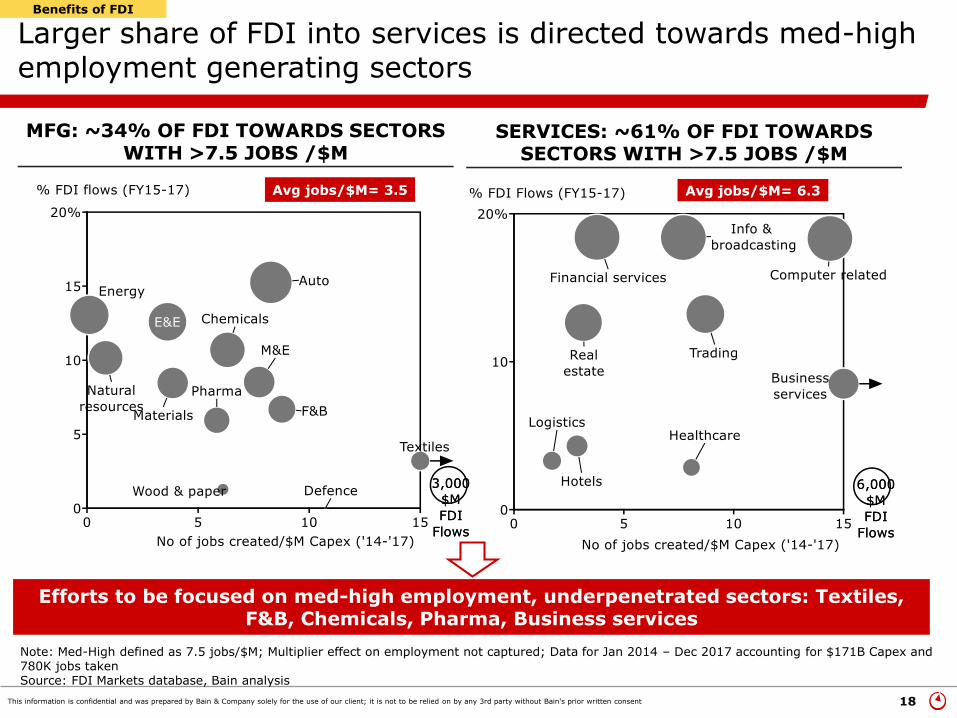

• Employment generation not likely to be impacted due to shift of inflows away from manufacturing-higher share of flows to services are directed towards med-high employment intensity sub-sectors

- Hence, even though % of FDI into manufacturing has declined, impact on job creation likely to be limited, given most inflows within manufacturing are to lower employment intensive sectors (Auto, Chemicals)

• FDI supports capital formation across both services & manufacturing sectors with 65% of total funds used towards gross capital assets (vs. debt reduction / opex)

- Service sector recipients of FDI focus on capital asset formation (typically branch building/ expansion) to the same extent as manufacturing sector recipients (~50% of recipients for both)

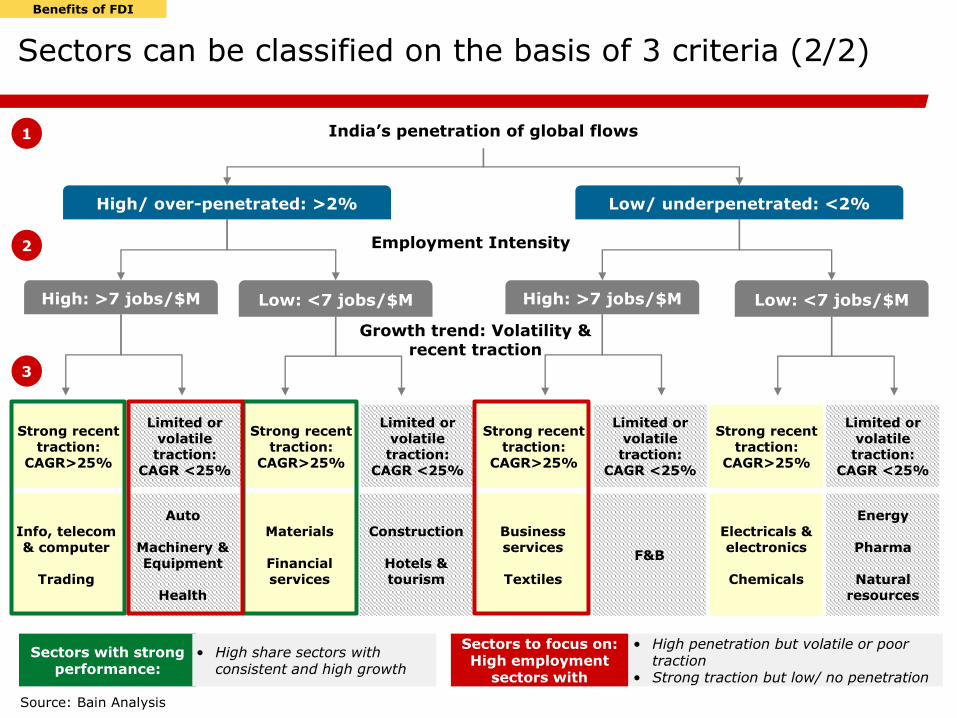

• Sectors can be classified based on India’s penetration of global flows, employment intensity and growth trends – high employment sectors with poor performance to be prioritized for focus

• Top 3 “true” countries of origin are USA, Japan and Singapore; India has significant headroom to improve its share of wallet with top investors despite significant growth in inflows

- Flows from 7 countries including key global investors USA, Canada and Japan have grown significantly since FY14; Increased flows from Switzerland, Netherlands and Singapore seen in H1FY18

- However, share of wallet of top investors is <5% for 7/12 investors; leading global investors like Spain, Sweden, Italy currently invest minimally in India

- Flows from tax advantage geographies have increased from 59% (FY08-12) to 67% (FY13-17) with Mauritius & Singapore leading, though these are expected to decline going forward, with DTAA agreements in place

- Investors can be classified based on existing relationship with India, size of outflows and growth trends – Large investors with low share of wallet or poor/volatile growth to be prioritized for focus

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 6

Summary observations and implications

• In terms of investor type, financial investors use tax advantaged geos more than industrial investors (~90% vs. 55% of total FDI respectively)

• Service sectors see higher % of flows through tax adv geos (78% vs. 58% for mfg) driven by higher share of FI’s and higher likelihood of industry investors to use tax adv geos for services

- FI’s likelier to invest in services accounting for 31% of flows to these sectors vs. 22% for manufacturing sectors

- Industry investors are 2X more likely to route service transactions through tax adv geos than for mfg sectors

• Ease of investing in India has improved over time; approvals are concentrated on larger size transactions & those that are routed through tax advantaged geographies

- Approvals account for <13% of all transactions in FY15-17, driven largely by telecom, services sector

- 22% of transactions of >$500M require approvals vs. <5% of those <$5M

- 17% of FDI inflows through tax advantage geographies are subject to approval vs. 8% of others

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 7

Summary: Sectors and investors prioritized for focus

Sectors with strong performance Investors with strong performance

… with whom India has high SoW but poor traction or

volatile relationship

… that have a negligible/

nascent relationship with

India but show strong traction

… that are under-penetrated but showing strong

traction

…where India has established

presence but with poor or volatile

growth

Sectors to focus on

High penetration of global flows

and high, consistent growth

High share of wallet and high,

consistent growth

Investors to focus on

High employment sectors… Large investors that…

• Information, telecom & computer related

• Trading

• Auto

• Machinery & Equipment

• Health

• Business services

• Textiles

• USA

• Japan

• UAE

• Switzerland

• Russia

• Germany

• Canada

• China

• South Korea

• Ireland

• France

• Materials

• Financial services

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 8

Global economic crisis and recovery Launch of MII

Drivers

• Global economic crisis impacts inflows

• Falling valuations cause spike of large M&A in 2012 e.g. BP-Reliance, Vodafone-Essar, Vedanta-Cairn

• Recovery beginning FY13

• Govt opens up defence

• Reforms in construction, retail, insurance

• Special provisions made for start ups

Since FY15 India’s FDI inflows have grown at 15% CAGR…

Launch of MII Sep ‘14

CAGR09-151.3%

CAGR15-1715%

Note: FDI Total flows include FDI Equity Flows, reinvested earnings and other capital; FY18(E) calculations done using H1FY18 FDI inflowsSource: DIPP Factsheet, April 2000- March 2017

CAGR:-2% CAGR: -4%

H1 FY18 flows grew by 16% over H1 FY17

inflows

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 9

… ahead of its developing country peers; Lower FDI Stock/GDP indicates further headroom for growth

Note: G20 developing countries include Argentina, Brazil, China, Indonesia, Russia, Mexico, Saudi Arabia, South Africa, Turkey; ASEAN include all 10 member countries; G33 includes all 48 member countries except Cuba & India; Next 11 includes all 11 member countriesSource: World Investment Report, 2017

India’s FDI inward stock/GDP is 14% vs 30% developing country avg

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 10

FDI flows are concentrated amongst recipients with only 150 companies (of ~9K) receiving 60% of total

TOP 150 RECIPIENTS DRIVE ~60% OF ALL FDI EQUITY INFLOWS

TOP 10 RECIPIENTS ACCOUNT FOR 20% OF FDI

Name Sector $M

Vodafone India Ltd Telecom 2501

Serene Senior LivingConstruction/Real estate

2252

Ambuja Cements Ltd.Materials manufacturing

1661

Triguna Hospitality Ventures (India) Pvt

Hotels & tourism* 1654

Jasper Infotech Pvt Ltd (Snapdeal)

Computer software/hardware

1585

Tata Teleservices Ltd Telecom 1574

Insitel Services Pvt Ltd (Sistema Jsfc Subsidiary)

Trading 1457

Amazon Seller Services Pvt. Ltd.

Trading 1442

Star India Pvt Ltd Info & Broadcasting 1158

Ani Technologies Pvt Ltd (Ola Cabs)

Computer software/hardware

1002

Benefits of FDI flows are limited to a few companies; MSMEs which have higher labour intensity receive limited fund flows

Source: DIPP Remittance Data FY15-17

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 11

This consolidation has increased over time with average FDI inflows/recipient increasing by 35% since FY14

Source: DIPP Remittance Data, 2000-2017

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 12

However, inflows continue to be broad based in terms of sectors, even with a concentrated set of recipients

Note: Sector classification based on DIPP definitions e.g. Triguna included in services though active in ‘hotels & tourism’; *Top 146 recipients with total investment of $100M+ from FY15-17 depicted Source: DIPP Remittance Data FY15-17

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 13

Services sectors gained share driven by large number of recipients; Manufacturing sectors more consolidated

Targeted support to potential manufacturing recipients in raising funds could increase flows in underpenetrated sectors

Note: Sector classification based on DIPP definitions; Services oriented includes services, computer, education, hospitals, tourism, information, telecom, trading; Manufacturing oriented includes Auto, Chemicals, Construction, Natural resources, Energy, F&B, Pharma, Textiles, Wood & paper, Machinery, Electronics, MaterialsSource: DIPP Remittance Data FY15-17, Bain Analysis

Top 3 recipients

ServicesComp. related

Trading Telecom Const. Auto Energy Electronics ChemicalsNatural

resources

TrigunaEmpowerIndusInd

Jasper Ani Tech.Accenture

InsitelAmazon

IKEA

VodafoneTata Tele

Viom Networks

SerenePRLDLF

SuzukiGeneral

Ford

AdaniMeenakshi EnergyPipavav Energy

EssarToshiba

Crompton Greaves

ShellUPL

Kansai Nerolac Paints

JSWEssel Mining

POSCO

SERVICE ORIENTED SECTORS GAINED SHARE

SERVICES SECTORS HAVE MORE RECIPIENTS BUT LOWER AVG. TNXVALUES THAN MFG RECIPIENTS

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 14

FY15-17 vsH1FY18

% Top 10 sectors

75% 77%

Note: Sector classification based on Bain sector definitions; M&E represents Machinery & EquipmentSource: Sector-wise DIPP Remittance Data FY’01-17, Bain Analysis

75%

FY13-15 vsFY15-17

Vodafone receiving $6B inflows

TELECOM AND COMPUTER SOFTWARE/HARDWARE GAINED SHARE IN FY15-17 &SHOW UPTICK IN H1FY18

Top 10 sectors account for ~80% of flows; Services, computer related and trading lead

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 15

7 sectors have grown significantly since 2014; Trading additionally shows uptick in H1FY18

Note: Total FDI Equity Inflows in India grew at 21% CAGR FY14-17; Uptick in FY18 for sectors with CAGR >40% FY17-FY18ESource: Sector-wise FDI Inflows, DIPP

2013-14 2016-17CAGR

(FY14-FY17)Uptick in H1FY18*

Electricals & electronics

480 2,602 76%

Materials 447 2,197 70%

Telecom 1,307 5,564 62%

Services 2,669 9,840 54%

Computer S/W H/W 1,126 3,652 48%

Textiles 205 621 45%

Info & broadcasting 542 1,570 43%

Natural resources 696 1,676 34%

Trading 1,355 2,789 27%

Hotel & Tourism 486 916 24%

Chemicals 807 1,404 20%

Energy 1,480 1,897 9%

Construction 1,711 1,966 5%

Health 685 747 3%

Auto 1,517 1,609 2%

Machinery & equipment 1,102 1,127 1%

Misc 757 542 -11%

Pharma 1,279 857 -12%

Education 262 160 -15%

F&B 4,828 964 -42%

>=40% 0-20% <=0%20-40%

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 16

Compared to global flows, India remains under penetrated on several fast growing sectors

Vietnam, China,

Malaysia

China, Mexico, Indonesia

China (EY, Deloitte, PWC), Egypt, Vietnam

China, Mexico, Indonesia

China, Vietnam, Mexico

China, Mexico, Malaysia

Efforts to be focused on med-high employment, underpenetrated sectors: Textiles, F&B, Machinery & Equipment, Business services

Note: Telecom included in Info & computer; CAGR unavailable for Logistics; Overall services CAGR used for business and financial servicesSource: UNCTAD, DIPP Database, FDI markets database, Bain Analysis

High growth sectors

Leading developing

country recipients

Under-penetrated

Over-penetrated

CAGR(FY14-17)>40% or CAGR FY17-FY18E

>40%

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 17

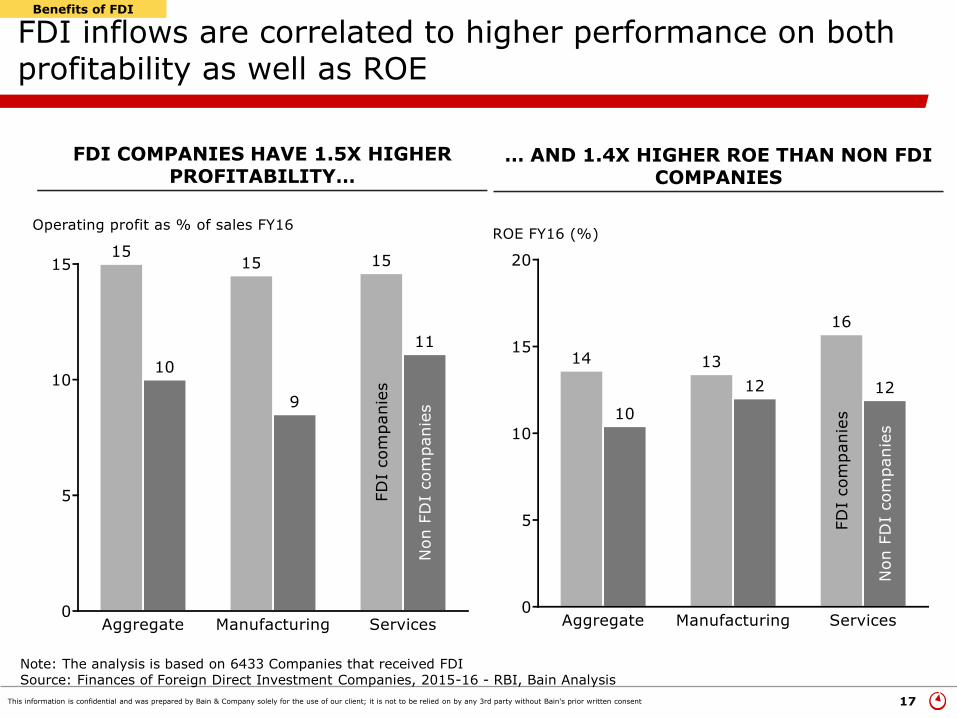

FDI inflows are correlated to higher performance on both profitability as well as ROE

… AND 1.4X HIGHER ROE THAN NON FDI COMPANIES

Note: The analysis is based on 6433 Companies that received FDISource: Finances of Foreign Direct Investment Companies, 2015-16 - RBI, Bain Analysis

FDI COMPANIES HAVE 1.5X HIGHER PROFITABILITY…

Benefits of FDI

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 18

Larger share of FDI into services is directed towards med-high employment generating sectors

Benefits of FDI

MFG: ~34% OF FDI TOWARDS SECTORS WITH >7.5 JOBS /$M

SERVICES: ~61% OF FDI TOWARDS SECTORS WITH >7.5 JOBS /$M

Note: Med-High defined as 7.5 jobs/$M; Multiplier effect on employment not captured; Data for Jan 2014 – Dec 2017 accounting for $171B Capex and 780K jobs taken Source: FDI Markets database, Bain analysis

Avg jobs/$M= 3.5 Avg jobs/$M= 6.3

Efforts to be focused on med-high employment, underpenetrated sectors: Textiles, F&B, Chemicals, Pharma, Business services

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 19

A study of a subset of projects further highlights that select service sectors create the most jobs/$

Services

Manufacturing

Benefits of FDI

Note: Multiplier effect on employment not captured; Data for Jan 2014 – Dec 2017 for top 10 sectors usedSource: FDI Markets Database, Bain Analysis

TOP 10 SECTORS: ACROSS $56B OF CAPEX INVESTMENT, A TOTAL OF 4,75,000 JOBS WERE CREATED I.E. 8.5 JOBS CREATED PER $1M

Top 10 sectors shown

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 20

Despite share gain by service oriented sectors, capital asset formation increased

GROSS CAPITAL ASSET CREATION HAS INCREASED IN MFG, SERVICES…

…DRIVEN BY EXTERNAL SOURCES BEYOND DEBT FUNDING

Benefits of FDI

Potential uses of funds: Capital asset creation, debt retirement, M&A and opex fundingIn case of acquisition of shares, fund flow is to existing shareholders, benefits of which are not

captured

Note: This analysis is based on 6,433 Companies that received FDISource: RBI report: ‘Finances of FDI Companies, 2015-16’, Bain Analysis

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 21

Sector Comments

Trading• Opening of new outlets/ warehouses e.g. IKEA

entry into India, Amazon warehouse expansion

FinancialServices

• Branch expansions e.g. IndusInd added 200 branches

Computer Related

• Expansion and acquisitions e.g. Snapdeal opened 6 logistics center, acquired 12 companies

Insurance• Branch expansions and investment in technology

e.g. HDFC Ergo GIC: investment in software

Bottom up study also shows that service recipients are equally likely to indulge in capital formation

Benefits of FDI

Avg.

Services 52%

Manufacturing 52%

Sector Comments

Chemicals

• Expansion of production capacity e.g. UPL plant in Gujarat, Sintex plant in Gujarat

Auto• Opening new manufacturing plants e.g. Suzuki

Motor Corp Guj started production in Feb 2017

Energy

• Launch of new plants, new entry e.g. ThemalPowertech Corporation recently entered; Azure power solar project in Punjab

Note: Data across 172 recipients shown; Only sectors with 5 or more recipients shown; Recipients whose gross blocks moved >20% were included to calculate change in BS; Excludes construction sector due to limited data availabilitySource: Bain Analysis

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 22

Moreover, services recipients were more likely to use funds for M&A…

Note: Data across 172 recipients shown; Only sectors with 5 or more recipients shown; M&As in the time frame of 2014-17 have been considered; Financial details for construction sector companies not available, hence has not been displayedSource: Bain Analysis

Benefits of FDI

Avg.

Services 28%

Manufacturing 13%

Sector Examples Sector Examples

TradingMyntra acquisition of 3 cos incl Xerio retail, Grid ant tech

ChemicalsUPL: Acquired Serra Bonita, Advanta

Comp Related

Snapdeal acquired 12 companies, Ola acquired 5 companies

EnergyAdani acquired 4 cos incl Korba west power, Power undertaking

Financial services

Kotak Mahindra: Acquired 5 cos including BSS Microfinance, Airtel Payments Bank, ING Vysya Bank Ltd

Natural Resources

JSW Steel acquired Welspun Maxsteel, Mahindra acquired Bill Forge

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 23

… while manufacturing recipients were more likely to use funds for debt retirement

Note: Data across 172 recipients shown; Only sectors with 5 or more recipients shown; Recipients whose liabilities moved >20%were included to calculate change in BS; Financial details for construction sector companies not available, hence has not been displayed; Source: Bain Analysis

Benefits of FDI

Sector Examples Sector Examples

LogisticsSterling Port: Liabilities reduced from INR 4.6B to INR 1.9B

ChemicalsLanxess India: Liabilities reduced from INR 7B to 2B

Business support

Avendus Capital Pvt Ltd: Liabilities reduced from INR 31M to 0 M

AutoGeneral Motors India: Liabilities reduced from INR 15B to INR 2B

Prof. services

Subex Limited: Liabilities reduced from INR 5 B to INR400 M

ElectronicsNovateur Electricals: Liabilities reduced from INR 13B to 8B

Avg.

Services 10%

Manufacturing 17%

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 24

Employment intensity (Jobs/$M capex)

India’s penetration of global flows

Growth trend: Volatility & recent traction

Sectors can be classified on the basis of 3 criteria (1/2)

1

2

3

Large: >$25B (Top 15) Low: <7/$MHigh: >7/$M

High impact sectors for focus Lower impact sectors

Low/ under-penetrated: <2%High/ over-penetrated: >2%

High share of global sector flows increases ability to win by providing

existing base

Under-penetration indicates high upside potential depending on India’s competitive

advantage

Strong recent traction implying momentum for future expansion

Efforts needed in order to ensure more consistent flows and higher growth

Limited or volatile traction: CAGR<25%Strong recent traction: CAGR >25%

Source: Bain Analysis

Benefits of FDI

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 25

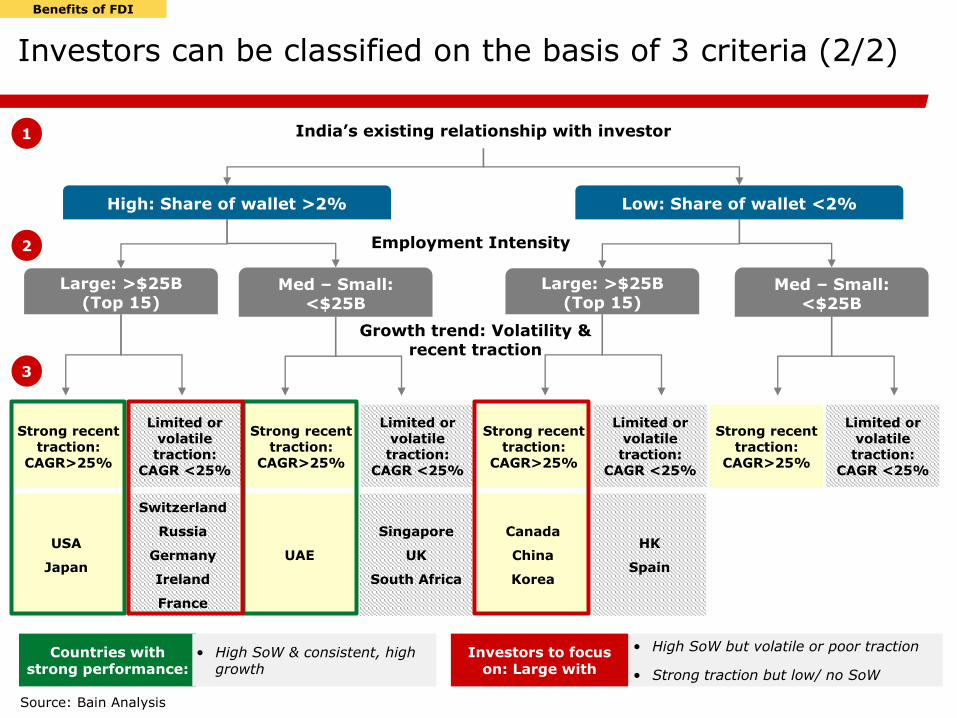

Sectors can be classified on the basis of 3 criteria (2/2)

India’s penetration of global flows

High/ over-penetrated: >2% Low/ underpenetrated: <2%

1

2 Employment Intensity

Growth trend: Volatility & recent traction

3

Sectors with strong performance:

Sectors to focus on:High employment

sectors with

• High share sectors with consistent and high growth

• High penetration but volatile or poor traction

• Strong traction but low/ no penetration

Benefits of FDI

High: >7 jobs/$M Low: <7 jobs/$M High: >7 jobs/$M Low: <7 jobs/$M

Source: Bain Analysis

Strong recent traction:

CAGR>25%

Limited or volatile traction:

CAGR <25%

Strong recent traction:

CAGR>25%

Limited or volatile traction:

CAGR <25%

Strong recent traction:

CAGR>25%

Limited or volatile traction:

CAGR <25%

Strong recent traction:

CAGR>25%

Limited or volatile traction:

CAGR <25%

Info, telecom & computer

Trading

Auto

Machinery & Equipment

Health

Materials

Financial services

Construction

Hotels & tourism

Business services

Textiles

F&B

Electricals & electronics

Chemicals

Energy

Pharma

Natural resources

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 26

Overall, FDI from tax advantage geos is increasing; Tax advantage geo flows are more consolidated

TAX ADVANTAGE GEOS ACCOUNT FOR ~67% OF FLOWS; SINGAPORE, NETHERLANDS GAIN

SHARE

%pt share gainFY13-17

vs.FY08-12

LARGER TRANSACTIONS ARE MORE LIKELY TO COME THROUGH TAX ADVANTAGE GEOS

Source of FDI

Note: Tax advantage geos classified based on report titled “Closing the Flood Gates”, Norwegian Ministry of Foreign Affairs (mid, premier category only); These countries represent ‘given origin’Source: DIPP Factsheet, April 2000 - June 2017; Bain analysis

Cyprus

UK

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 27

% GlobalFlows

(2016)

CAGR(FY14-FY17)

Uptick in H1FY18

Bermuda 0% 442%

Canada 5% 193%

Mauritius 0% 48%

U.S.A 21% 43%

Japan 10% 40%

South Korea 2% 39%

UAE 1% 38%

France 4% 26%

Italy 2% 23%

Switzerland 2% 15%

Netherlands 12% 14%

Singapore 2% 13%

Cyprus 0% 3%

Germany 2% 1%

United Kingdom -1% -23%

Note: Total FDI Equity Inflows in India grew at 21% CAGR FY14-17; -ve Global flows are recorded for UK since WIR accounts for intra-company loan movement resulting in –ve outflows; top 15 investors based on FY17 inflows have been represented; LHS represents ‘given origin’Source: Country-wise FDI Data, DIPP; World Investment Report , 2017

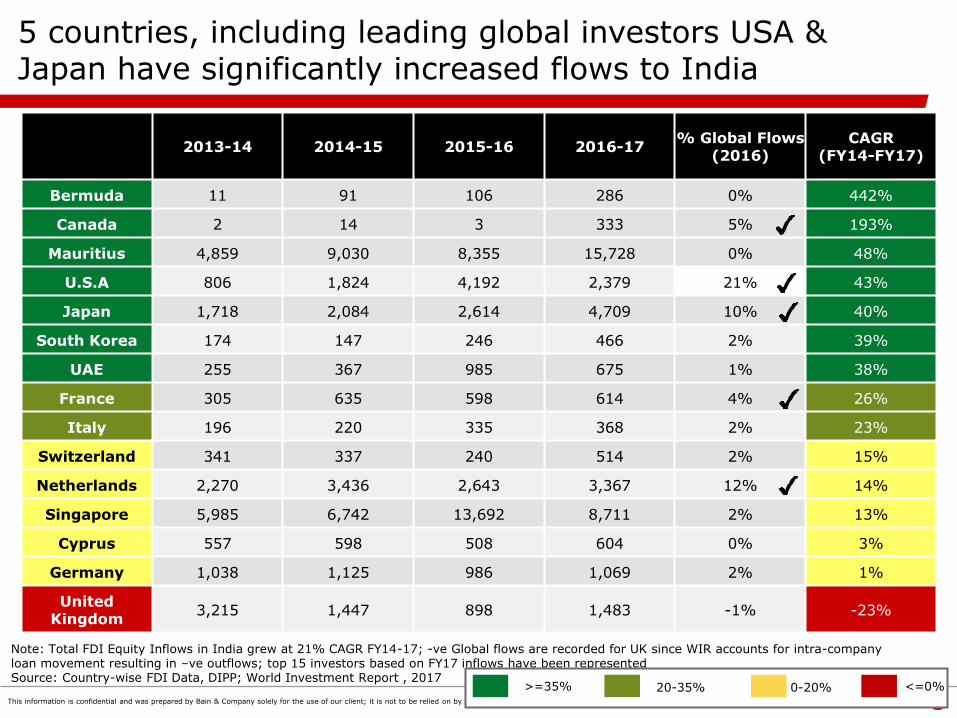

7 countries, including leading global investors USA & Canada have significantly increased flows to India

>=35% 0-20% <=0%20-35%

TOP 10 COUNTRIES ACCOUNT FOR ~90% OF FLOWS IN 2016-17

BERMUDA & CANADA GREW OVER LAST 4 YEARS, SWITZERLAND GAINED IN H1FY18

Source of FDI

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 28

USA, UK use tax advantage geos the most; US, Japan & Singapore are top 3 “true” origin countries

COMPUTER SOFTWARE & HARDWARE SECTOR RECEIVES 94%* OF FLOWS THROUGH GEOS OFFERING TAX ADVANTAGE

Source of FDI

USA & JAPAN DRIVE HIGHEST FDI

INFLOWS

Note: Data shown for 662 investors; Analysis done for top recipients of each sector covering $9331M of services, $5778M of computer S/H, $4181M of trading, $5474M of Telecom, $1598M of Energy, $1168M of Electrical & Electronic, $2706M of Automobile, $4088M of construction, $1888M of Chemicals, $1808M of Natural Resources & $9759M of OthersSource: DIPP Remittance Data, 2000-2017

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 29

Scope to increase SoW with existing investors; add’lpotential with other top global investors not investing today

SIGNIFICANT HEADROOM FOR INDIA TO GAIN SOW WITH CURRENT INVESTORS – 8/13 INVESTORS HAVE <5% SOW

TARGET TOP GLOBAL INVESTORS CURRENTLY

NOT INVESTING IN INDIA

Spain:

$42B global outflows

$168M current India

Inflow (2016)

Sweden:

$23B global outflows

Current India Investment NA

Italy:

$23B global outflows

$123M current India Inflow (2016)

Finland:

$23B global outflows

Current India Investment NA

Note: All outflows represent flows in 2016; top investors based on FY17 inflows shown after mapping to ‘True Origin’; SOW for Tax Adv. Geos has been calculated using net outflows; SOW for Singapore & HongKong not shown as net outflows are negativeSource: World Investment Report, 2017; UK Global Outflows Data is from their govt website

Non-Tax Adv. Geos

Tax Adv. Geos

Legend:

Source of FDI

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 30

Size of investor outflows

India’s existing relationship with investor

Growth trend: Volatility & recent traction

Investors can be classified on the basis of 3 criteria (1/2)

1

2

3

Large: >$25B (Top 15) Med – Small: <$25BLarge: >$25B (Top 15)

Global investors of significance, with large potential upside from increasing

share of wallet

Smaller scale investors, limited upside from increasing share of wallet

Low share of wallet: <2%High share of wallet: >2%

Existing relationship increases ability to win by providing existing base

Lowered ability to win when relationship needs to be initiated

Strong recent traction implying momentum for future expansion

Limited or negative traction and/or volatile inflows to India indicates poor quality of

relationship

Limited or volatile traction: CAGR<25% or volatility >0.8

Strong recent traction: CAGR >25%

Source: Bain Analysis

Source of FDI

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 31

Investors can be classified on the basis of 3 criteria (2/2)

India’s existing relationship with investor

High: Share of wallet >2% Low: Share of wallet <2%

1

2 Employment Intensity

Growth trend: Volatility & recent traction

3

Countries with strong performance:

Investors to focus on: Large with

• High SoW & consistent, high growth

• High SoW but volatile or poor traction

• Strong traction but low/ no SoW

Benefits of FDI

Large: >$25B(Top 15)

Med – Small:<$25B

Large: >$25B(Top 15)

Med – Small:<$25B

Source: Bain Analysis

Strong recent traction:

CAGR>25%

Limited or volatile traction:

CAGR <25%

Strong recent traction:

CAGR>25%

Limited or volatile traction:

CAGR <25%

Strong recent traction:

CAGR>25%

Limited or volatile traction:

CAGR <25%

Strong recent traction:

CAGR>25%

Limited or volatile traction:

CAGR <25%

USA

Japan

Switzerland

Russia

Germany

Ireland

France

UAE

Singapore

UK

South Africa

Canada

China

Korea

HK

Spain

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 32

Financial investors account for 28% of total, investing higher in services; More likely to use tax advantage geos

Source of FDI

COMPUTER S/W & H/W HAS THE HIGHEST SHARE OF FLOWS FROMFINANCIAL INVESTORS

Note: Financial Investors includes PE, VC, Hedge Funds, Asset Mgmt.; Analysis done for top recipients of each sector covering$9331M of services, $5778M of computer S/H, $4181M of trading, $5474M of Telecom, $1598M of Energy, $1168M of Electrical & Electronic, $2706M of Automobile, $4088M of construction, $1888M of Chemicals, $1808M of Natural Resources & $9759M of Others; Source: DIPP Remittance Data, 2000-2017, Bain Analysis

Avg.

Services 32%

Manufacturing 24%

FINANCIAL INVESTORS USE TAX ADVANTAGE GEOS MORE

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 33

Additionally, industry investors prefer to route service related transactions through tax advantage geos

Source: DIPP Remittance Data, 2000-2017; Bain analysis

Source of FDI

Avg.

Services 65%

Manufacturing 30%

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 34

Hence, service related industries see higher use of tax advantage geos than manufacturing industries

~78% OF FDI INFLOWS FOR THE SERVICES SECTOR CAME THROUGH TAX ADVANTAGE GEOS COMPARED TO 58% FOR MANUFACTURING SECTOR

Services Manufacturing

(78%) (58%)

Note: Tax advantage geos classified based on report titled “Closing the Flood Gates”, Norwegian Ministry of Foreign Affairs (mid, premier category only); Sector classification as per DIPP Source: DIPP Remittance Data, 2000-2017

Source of FDI

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 35

Ease of investing improved over the last 15 years; However, high inflow sectors telecom, services require a high % of approvals

>65% CUMULATIVE FDI INFLOWS IN THE LAST 5 YEARS CAME THROUGH AUTOMATIC ROUTE

Note: Calendar year data has been used due to unavailability of financial year dataSource: Statement on Year-wise/Route-wise FDI Equity Inflows, SIA, Jan 2000 to March 2017

Increasingly easy for investors to invest, reflecting positively on reforms made

4 SECTORS DRIVE FLOWS THROUGH APPROVAL ROUTE; SERVICES, TELECOM SIGNIFICANT

Further analysis of telecom, services transactions required to determine need

for easing policy restrictions

Ease of regulations

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 36

Larger size transactions and flows sourced from tax advantage geos have higher approval %ges

Ease of regulations

~22% OF DEALS GREATER THAN $500M REQUIRED APPROVAL

~17% FDI INFLOWS FROM TAX ADVANTAGE GEOS NEEDED APPROVAL

Source: DIPP remittance Data, 2000-2017

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 37

Next Steps

Potential areas to explore further

Key aspects to cover

Aggregate• Handbook of

best practices

• International best practices in attracting FDI and impact of the same

• State-wise best practices applied

Benefits of FDI

• Engagement plan by sector

• Prioritize focus sectors based on

• Benefits: Employment, capex, GDP

• Ability to drive FDI flows: Size of global pool, India’s competitive advantage

• Identify potential recipients

• Align on areas of support

• State-wise assessment of FDI benefits

• Evaluate which states receive end flows, by sector

• Impact of FDI flows by state: capital assets created, employment generated

Source of FDI

• Mandate by country/ trade mission

• Prioritize focus countries based on

• Attractiveness: Full potential, sector overlap with priority sectors

• Ability to win: India’s competitive advantage vs. current top recipient countries

• Create playbook for each country including i) Key sectors ii) Top investor companies to target iii) Potential recipients

• Impact of new DTAA agreements

• Estimate potential impact on FDI flows of new DTAA agreements

Regulations• Impact of

liberalization• Understand historical impact of liberalization on FDI inflows - by sector and

investor

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 38

Backup

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 39

7 sectors have grown significantly since 2014

Note: Total FDI Equity Inflows in India grew at 21% CAGR FY14-17Source: Sector-wise FDI Inflows, DIPP

2013-14 2014-15 2015-16 2016-17CAGR

(FY14-FY17)H1FY18 FY17-FY18E

Electricals & electronics 480 902 812 2,602 76% 541 -58%

Materials 447 286 97 2,197 70% 84 -92%

Telecom 1,307 2,895 1,324 5,564 62% 6,084 119%

Services 2,669 5,371 8,282 9,840 54% 4,367 -11%

Computer S/W H/W 1,126 2,296 5,904 3,652 48% 3,045 67%

Textiles 205 232 247 621 45% 217 -30%

Info & broadcasting 542 328 1,132 1,570 43% 402 -49%

Natural resources 696 2,123 1,080 1,676 34% 118 -86%

Trading 1,355 2,897 4,108 2,789 27% 1,563 12%

Hotel & Tourism 486 777 1,333 916 24% 470 3%

Chemicals 807 1,043 1,494 1,404 20% 897 28%

Energy 1,480 1,323 1,645 1,897 9% 1,537 62%

Construction 1,711 1,639 4,623 1,966 5% 1,246 27%

Health 685 568 742 747 3% 497 33%

Auto 1,517 2,726 2,527 1,609 2% 1,235 54%

Machinery & equipment 1,102 1,187 1,184 1,127 1% 607 8%

Misc 757 953 943 542 -11% 280 3%

Pharma 1,279 1,498 754 857 -12% 864 102%

Education 262 79 231 160 -15% 223 179%

F&B 4,828 919 849 964 -42% 581 21%

>=40% 0-20% <=0%20-40%

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 40

Sectors can be classified on the basis of 3 criteria: India’s share of global sector flows, employment, growth trends

Auto 4,136 136,310 3.0% 8.28 2% 0.91

Health 1,490 21,340 7.0% 8.08 3% 0.36

Machinery & equipment

2,311 82,050 2.8% 7.75 1% 0.49

Legend>2% >7 >20 % <0.6

<2% <7 <20 % >0.6

SectorCurrent size($M)

Global pool($M)

Penetration(Share %)

Employment(Jobs/$M)

CAGR(FY13-17)

Volatility

Info, Telecom & computer

19,146 44,796 42.7% 14.38 48% 0.01

Trading 6,897 114,954 6.0% 8.71 27% 0.34

Materials 2,294 59,500 3.9% 3.86 70% 0.58

Financial services 9,598 243,661 3.9% 3.78 54% 0.30

Construction 6,589 224,009 2.9% 3.16 5% 0.81

Hotel & Tourism 2,247 46,833 4.8% 2.87 24% 0.70

Pharma 1,611 208,350 0.8% 5.84 -12% 0.7

Natural resources 2,756 328,212 0.8% 0.84 34% 0.99

Energy 3,542 346,555 1.0% 0.11 9% 0.75

Business services 4,438 325,841 1.4% 15.91 54% 0.30

Textiles 868 57,688 1.5% 15.58 45% 0.32

F&B 1,813 212,929 0.9% 8.77 -42% 0.91

Electricals & electronics

3,414 186,174 1.8% 3.62 76% 0.31

Chemicals 2,899 169,055 1.7% 6.32 20% 0.1

Note: Information & broadcasting, Telecom, Computer S/W H/W have been clubbed for comparison to global flows; Volatility has been calculated by 1-R2 (explained variance) value of sector flows over FY13-17Source: Bain Analysis

Sectors with high share and growth

Sectors with strong performance

High penetration/ employment with

poor growth

High growth/ employment with

low share

Sectors for focus

Low employment, under-penetrated

Under-penetrated, poor growth

Low employment with poor or volatile growth

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 41

While few mfg. sectors have higher % of exports, overall focus remains on Indian consumers

Note: Export to sales % obtained for FY16; % FDI equity inflows FY15-17 depicted; Transport Storage & communication comprises of Logistics Services & Information & BroadcastingSource: St 11: Select Financial Ratios of the select 6,433 FDI Companies - Industry Group Wise, RBI; DIPP remittance data FY15-17;

SELECT MFG. SECTORS HAVE HIGHER % OF EXPORT SALES

Services Manufacturing

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 42

Note: Total FDI Equity Inflows in India grew at 21% CAGR FY14-17; -ve Global flows are recorded for UK since WIR accounts for intra-company loan movement resulting in –ve outflows; top 15 investors based on FY17 inflows have been representedSource: Country-wise FDI Data, DIPP; World Investment Report , 2017

5 countries, including leading global investors USA & Japan have significantly increased flows to India

2013-14 2014-15 2015-16 2016-17% Global Flows

(2016)CAGR

(FY14-FY17)

Bermuda 11 91 106 286 0% 442%

Canada 2 14 3 333 5% 193%

Mauritius 4,859 9,030 8,355 15,728 0% 48%

U.S.A 806 1,824 4,192 2,379 21% 43%

Japan 1,718 2,084 2,614 4,709 10% 40%

South Korea 174 147 246 466 2% 39%

UAE 255 367 985 675 1% 38%

France 305 635 598 614 4% 26%

Italy 196 220 335 368 2% 23%

Switzerland 341 337 240 514 2% 15%

Netherlands 2,270 3,436 2,643 3,367 12% 14%

Singapore 5,985 6,742 13,692 8,711 2% 13%

Cyprus 557 598 508 604 0% 3%

Germany 1,038 1,125 986 1,069 2% 1%

United Kingdom

3,215 1,447 898 1,483 -1% -23%

>=35% 0-20% <=0%20-35%

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 43

Note: Total FDI Equity Inflows in India grew at 21% CAGR FY14-17; Only investors >$100M flows in FY17 have been shown; Volatility is the 1-R2 value for India inflows of a country from FY13-17Source: Country-wise FDI Data, DIPP; World Investment Report , 2017; *Office for National Statistics, UK

Investors can be classified on the basis of size, share of wallet and growth trends

Flows to India $M

$M Global flows

SOW (%)CAGR

(FY13-FY17)Volatility

USA 13,476 299,003 5 43% 0.42

Japan 5,724 145,242 4 40% 0.39

UAE 1,011 15,711 15 38% 0.34

Canada 861 66,403 1 193% 0.26

China 983 183,100 1 31% 0.71

South Korea 292 27,274 1 39% 0.52

Russia 1,603 27,272 6 -11% 0.99

Switzerland 2,075 30,648 7 15% 0.74

France 1,969 57,328 3 26% 0.94

Germany 875 34,558 3 1% 0.67

Ireland 741 44,548 3 -57% 0.89

Singapore 5,034 23,888 N/A 13% 0.40

UK 3,501 12,600 28 0% 0.93

South Africa 373 3,382 11 -23% 0.94

Hong Kong 635 62,460 0 -2% 0.73

Spain 168 41,789 0 -13% 0.24

Legend:>$1B >$25B >2 >25% <0.5

>0.5B-$1B <$25B 1-2 0-25% 0.5-0.8

<0.5B <1 < 0% >0.8

Investors with strong relationship and growth

Large investors with recent strong traction

Large investors with strong existing relationship but poor or volatile growth

Small investors with poor or volatile growth

Large investors with no relationship

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 44

Top investors covering 50% of FDI Equity Inflows spread across sectors

Note: The investors represented here are true investors ie. Parent companies of given investors & represents 304 investorsSource: Bain analysis

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 45

Share of Delhi, TN and KTK RBI offices growing in the last 4 years

Note: CY data has been used due to unavailability of FY dataSource: SIA Monthly bulletin

IN THE LAST 4 YEARS, DEL, TN AND KTK GAINED SHARE OVER MH

HOWEVER, IN FY17 THE TREND REVERSED DUE TO MH’S EFFORTS, SLOWING E-COMMERCE

• Slowing investments in e-commerce impacted flows to Delhi, KTK, TN

• Maharashtra's textile park and coastal economic zone led to gains

CY13-16 vs. CY00-12

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 46

Backup: Sector mapping

Bain sector tag (23 sectors)

DIPP sector maps (63 sectors*)

Services Services, Air transport, sea transport, Consultancy, Agri Services

Machinery & equipment Agricultural machinery, Boilers & Steam generating plants, Commercial & household equipment, Earth moving machinery, Industrial Instruments, Industrial Machinery, Machine Tools, Medical appliances, Railway components, Scientific Instruments

Natural resources Coal, Metallurgical industries, Mining, Petroleum & natural gas

Chemicals Chemicals, Dye stuffs, Fertilizers

Construction Construction activities, Construction development

Electricals & electronics Electrical equipment, Electronics, Prime movers

Energy Power, Non-conventional energy

F&B Food processing, fermentation industries, Sugar, Tea & coffee, Vegetable oils

Information Information & BroadcastingPrinting of books

Materials Cement & Gypsum, Ceramics, Glass

Wood & paper Paper & pulp, Timber

Textiles & leather Textiles, Leather

Trading Trading, Retail trading

Others Rubber, Glue & gelatin, Soaps & Cosmetics, Diamond & Gold, Misc mechanical & engineering

As-Is: Computer software & hardware, Auto, Telecom, Hospitals, Hotels & Tourism, Misc, Pharma, Defence, Education

N/A: Coir, Mathematical, surveying & drawing instruments, Photographic raw film & paper

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 47

Appendix

• Details of top 10 recipients by sector

• Top 5 recipients and investors using tax advantage geographies by sector

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 48

# RecipientTotal

Inflow($M)

YrInvestor

Use of Funds Details of use of fundsGiven True

1

Empower Research Knowledge Services Pvt Ltd

663FY16

• Headstrong Consulting (Singapore) Pte Ltd

• Genpact • Funding for hiring SMEs (up ~75%)

2IndusInd Bank Ltd

520FY17

• Various • IndusInd Group

• Added 200 branches in FY17

• Acquisition of The Royal Bank of Scotland NV Diamond & jewelry Financing Business & Loan Portfolio

3Kotak Mahindra Bank Ltd

397FY17

• Sumitomo Mitsui Banking Corporation

• Heliconia PTE Ltd

• ING Mauritius Investments

• Sumitomo Mitsui Banking Corporation

• Temasek Holdings

• ING Group

• Acquisition of BSS Microfinance Pvt Ltd, Institutional Investor Advisory Services India Ltd, Airtel Payments Bank Ltd, ING Vysya Bank Ltd, Multi-commodity Exchange of India Ltd

4Reliance Life Insurance Company Ltd

338FY16

• Nippon Life Insurance Company

• Nippon Life Insurance Company

• Flows through acquisition

5Serco BPO Pvt Ltd

325FY16

• Serco International SARL

• Serco Facilities Management BV

• Serco

• Reduction in debt from INR 20B to INR 6.5B FY15-16

Note: 20% share of recipients computed on total service equity FDI for FY15-17 of $18,113M; True Investors have been marked as parent companies of given investors; Only top investors have been shown for a recipient;Source: DIPP Remittance Data, 2000-2017; Bain Analysis

CapexDebt retirement

M&A OpexIndustry Financial Investors

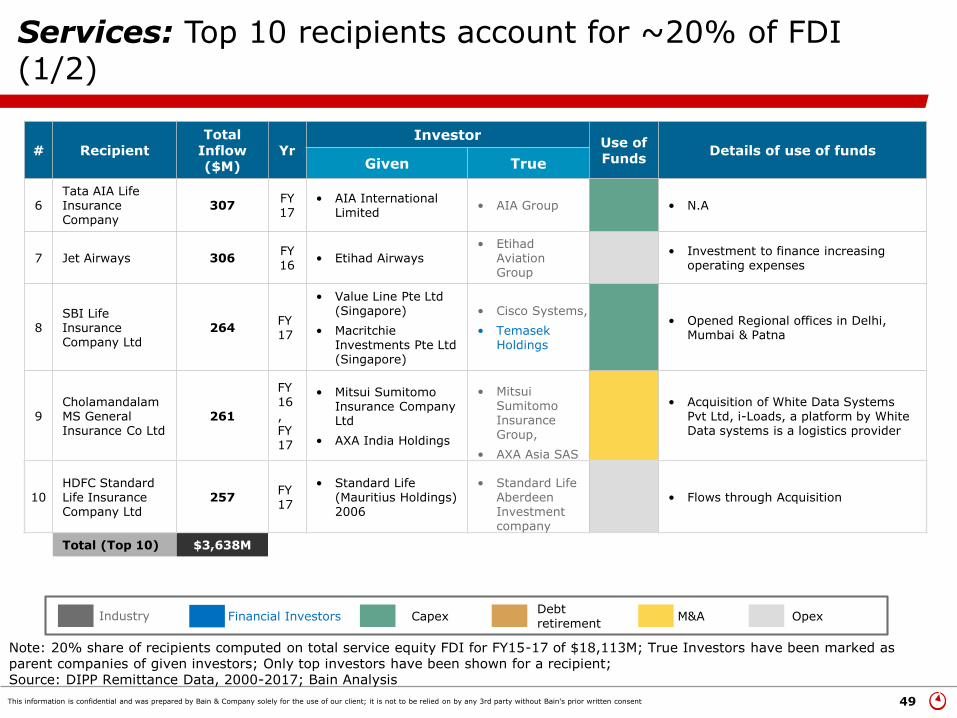

Services: Top 10 recipients account for ~20% of FDI (1/2)

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 49

# Recipient Total

Inflow($M)

YrInvestor

Use of Funds

Details of use of fundsGiven True

6Tata AIA Life Insurance Company

307FY17

• AIA International Limited

• AIA Group • N.A

7 Jet Airways 306FY16

• Etihad Airways• Etihad

Aviation Group

• Investment to finance increasing operating expenses

8SBI Life Insurance Company Ltd

264FY17

• Value Line Pte Ltd (Singapore)

• Macritchie Investments Pte Ltd (Singapore)

• Cisco Systems,

• Temasek Holdings

• Opened Regional offices in Delhi, Mumbai & Patna

9Cholamandalam MS General Insurance Co Ltd

261

FY16,FY17

• Mitsui Sumitomo Insurance Company Ltd

• AXA India Holdings

• Mitsui Sumitomo Insurance Group,

• AXA Asia SAS

• Acquisition of White Data Systems Pvt Ltd, i-Loads, a platform by White Data systems is a logistics provider

10HDFC Standard Life Insurance Company Ltd

257FY17

• Standard Life (Mauritius Holdings) 2006

• Standard Life Aberdeen Investment company

• Flows through Acquisition

Total (Top 10) $3,638M

Note: 20% share of recipients computed on total service equity FDI for FY15-17 of $18,113M; True Investors have been marked as parent companies of given investors; Only top investors have been shown for a recipient;Source: DIPP Remittance Data, 2000-2017; Bain Analysis

CapexDebt retirement

M&A OpexIndustry Financial Investors

Services: Top 10 recipients account for ~20% of FDI (1/2)

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 50

# RecipientTotal

Inflow($M)

Yr

Investor Use of

Funds

Details of use of funds

Given True

1

Jasper InfotechPvt. Ltd

(Snapdeal)

1519FY16, FY17

• Starfish I PTE Ltd

• Wonderful Stars PT Ltd

• Alibaba.com Singapore E-commerce Pvt Ltd

• SoftBank

• Hon Hai Precision Industry Co Ltd

• Alibaba Group

• Opened 6 logistics centres

• Acquired 12 companies including Smartprix, Acelyst, Unicommerce

2ANI Technologies

Pvt Ltd (Ola Cabs)954 FY16

• DST Asia IV, DST Investments XII Ltd, Apoletto Asia Ltd

• Internet Fund III PTE Ltd

• SIMI Pacific Pte Ltd

• DST Global

• Tiger Global Management LLC

• SoftBank

• Acquired 5 companies including Zipcash, Qarth Technologies

3Accenture Solutions Pvt Ltd

787 FY17• Accenture Services Mauritius Ltd

• Accenture Minority I BV• Accenture PLC

4One 97 CommunicationsLtd (PayTM)

625FY16,

FY17

• Alipay Singapore E-Commerce PTE Ltd

• Alibaba Group• Secured 3 new office

premises in Noida

5Optum Global Solutions Private Ltd

430 FY17• Optum Global Solutions

International BV• UnitedHealth

Group• Increased operating

expenses

CapexDebt retirement

M&A OpexIndustry Financial Investors

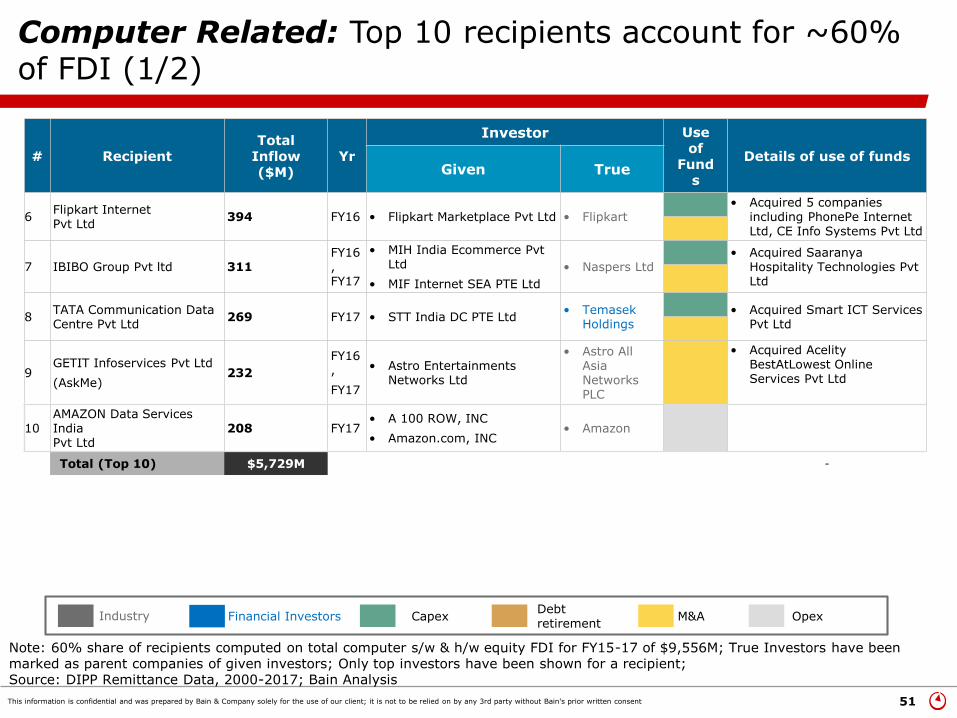

Computer Related: Top 10 recipients account for ~60% of FDI (1/2)

Note: 60% share of recipients computed on total computer s/w & h/w equity FDI for FY15-17 of $9,556M; True Investors have been marked as parent companies of given investors; Only top investors have been shown for a recipient;Source: DIPP Remittance Data, 2000-2017; Bain Analysis

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 51

# Recipient Total

Inflow($M)

Yr

Investor Use of

Funds

Details of use of fundsGiven True

6Flipkart InternetPvt Ltd

394 FY16 • Flipkart Marketplace Pvt Ltd • Flipkart• Acquired 5 companies

including PhonePe Internet Ltd, CE Info Systems Pvt Ltd

7 IBIBO Group Pvt ltd 311FY16, FY17

• MIH India Ecommerce Pvt Ltd

• MIF Internet SEA PTE Ltd

• Naspers Ltd• Acquired Saaranya

Hospitality Technologies Pvt Ltd

8TATA Communication Data Centre Pvt Ltd

269 FY17 • STT India DC PTE Ltd• Temasek

Holdings• Acquired Smart ICT Services

Pvt Ltd

9GETIT Infoservices Pvt Ltd

(AskMe)232

FY16,

FY17

• Astro Entertainments Networks Ltd

• Astro All Asia Networks PLC

• Acquired Acelity BestAtLowest Online Services Pvt Ltd

10AMAZON Data Services IndiaPvt Ltd

208 FY17• A 100 ROW, INC

• Amazon.com, INC• Amazon

Total (Top 10) $5,729M -

Note: 60% share of recipients computed on total computer s/w & h/w equity FDI for FY15-17 of $9,556M; True Investors have been marked as parent companies of given investors; Only top investors have been shown for a recipient;Source: DIPP Remittance Data, 2000-2017; Bain Analysis

CapexDebt retirement

M&A OpexIndustry Financial Investors

Computer Related: Top 10 recipients account for ~60% of FDI (1/2)

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 52

Note: 62% share of recipients computed on total trading equity FDI for FY15-17 of $6,894M; True Investors have been marked as parent companies of given investors; Only top investors for each recipient shownSource: DIPP Remittance Data, 2000-2017; Bain Analysis

# Recipient

Total Inflo

w($M)

Yr

Investor Use of

Funds

Details of use of funds

Given True

1Insitel Services Pvt Ltd

1457FY16,FY17

• SSA Fund (Singapore) PTE Ltd

• Sistema • Opened 10 new MTS Mitra stores across Mumbai, India

2Amazon Seller Services Pvt Ltd

1442FY16, FY17

• Amazon Asia Pacific Resources Pvt Ltd

• Amazon Eurasia Holdings S. A. R. L

• Amazon

• New warehouses in Tumkur, Hoskote, and a fulfilment centre in BLR

• Acquisition of EMVANTAGE PaymentsPvt Ltd

3 IKEA India Pvt Ltd 387FY16, FY17

• Ingka HoldingOverseas B.V.

• Ingka Pro Holding B. V.

• Stichting Ingka Foundation

• Entering Indian market for first time

• Opening stores in Hyderabad, Mumbai, Delhi, Bengaluru

• First manufacturing shop in UP

4FCA India Automobiles Pvt Ltd

178FY16,FY17

• FCA Italy SPA• Fiat Chrysler

Automobiles• Loss Funding

5 Ricoh India Ltd 165 FY17

• NRG Group Limited • Ricoh • Increase in Inventory

• Expansion of Data centre in Kolkata, hence increase in remuneration costs

CapexDebt retirement

M&A OpexIndustry Financial Investors

Trading: Top 10 recipients account for ~62% of FDI (1/2)

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 53

# Recipient Total

Inflow($M)

YrInvestor

Use of Funds

Details of use of fundsGiven True

6Myntra Designs Pvt Ltd

165FY16,FY1

7

• FK Myntra Holdings Pvt Ltd

• Flipkart Ltd• Flipkart

• Acquisition of 3 companies including Xerio Retail Pvt Ltd,Grid Ant technologies Pvt Ltd

7Adani Enterprises Ltd

154 FY16

• Gudami International PTE Ltd

• Deutsche Bank AG London

• Valiant Mauritius Partners Ltd

• PMC ProjectsIndia

• Deutsche Bank

• Valiant Capital Partners

• Reduction in debt from INR 719 B to INR 194B

8Decathlon Sports India Pvt Ltd

134FY16,FY17

• Decathlon SA • Decathlon• Opening new outlets-

plans of expanding to 50-60 outlets by 2019

9

Supermarket GrocerySupplies Pvt Ltd

104FY16,FY17

• Abraaj basket I Pvt Ltd

• Bessemer India Capital Holdings II Ltd

• Abraaj Group

• Bessemer Venture Partners

• Expansion of services in new cities, and new products & brands

• Acquired Delyver RetailNetwrok Pvt Ltd

10Arvind Fashions Ltd

101 FY17• Plenty Private Equity Fund

• Plenty CI Fund I LTd• Multiple Alternate

Asset• N.A.

Total (Top 10)

$4289M

Note: 62% share of recipients computed on total trading equity FDI for FY15-17 of $6,894M; True Investors have been marked as parent companies of given investors; Only top investors for each recipient shownSource: DIPP Remittance Data, 2000-2017; Bain Analysis

CapexDebt retirement

M&A OpexIndustry Financial Investors

Trading: Top 10 recipients account for ~62% of FDI (2/2)

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 54

Note: 51% share of recipients computed on total Construction equity FDI for FY15-17 of $6,596M; True Investors have been marked as parent companies of given investors; Only top investors for each recipient shownSource: DIPP Remittance Data, 2000-2017; Bain Analysis

# RecipientTotal

Inflow($M)

Yr

InvestorUse of Funds

Details of use of funds

Given True

1Serene Senior Living (Covai Sr Care )

2252 FY16 • Signature India LLC• Sterling-

Signature Senior Care Pvt Ltd

• Upcomingprojects near Chennai

2 PRL Developers 227 FY16

• Foglight Investment Ltd

• Broad Street Investments (Singapore) Pte

• Warburg Princus Group

• Goldman Sachs

• NA

3 DLF Midtown Pvt Ltd 223 FY16, FY17 • Reco Moti Pte Ltd • GIC, Singapore • NA

4M/S Soma Tollways Pvt Ltd

123 FY17• AIRRO (Mauritius) Holdings

VI• JP Morgan • NA

5Fedex Express Transportation & Supply

106 FY17

• Federal Express Europe Inc • FedEx

• NA

CapexDebt retirement

M&A OpexIndustry Financial Investors

Construction: Top 10 recipients account for ~51% of FDI (1/2)

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 55

# Recipient Total

Inflow($M)

Yr

InvestorUse of Funds

Details of use of funds

Given True

6Instakart Services Pvt Ltd

98 FY16• Klick2Shop Logistics

Services International• Flipkart • NA

7Experion Developers Pvt Ltd

79FY16,FY17

• Experion holdings Pte Ltd

• AT CapitalGroup

• NA

8SSN Logistics Pvt Ltd

78 FY16• Internet Fund III Pte Ltd

• Nexus Ventures III Ltd

• Tiger Global Management LLC

• Nexus Venture Partners

• Capital deployed to build infrastructure and designservices for e-commerce, hyper-local commerce, C2C commerce

9Unitech Developers & Projects Ltd

75 FY16

• BSREP india Office Holdings III Pte Ltd

• BSREP Moon C5 LP

• Brookfield Asset Management

• NA

10IOT Infrastructure& Energy Services Ltd

69FY16, FY17

• Oil Tanking India GMBH• Marquard &

bahls

• Liabilities reduced from INR 7.6 B to INR 5 B

Total (Top 10) $ 3331 M

Note: 51% share of recipients computed on total Construction equity FDI for FY15-17 of $6,596M; True Investors have been marked as parent companies of given investors; Only top investors for each recipient shownSource: DIPP Remittance Data, 2000-2017; Bain Analysis

Construction: Top 10 recipients account for ~51% of FDI (2/2)

CapexDebt retirement

M&A OpexIndustry Financial Investors

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 56

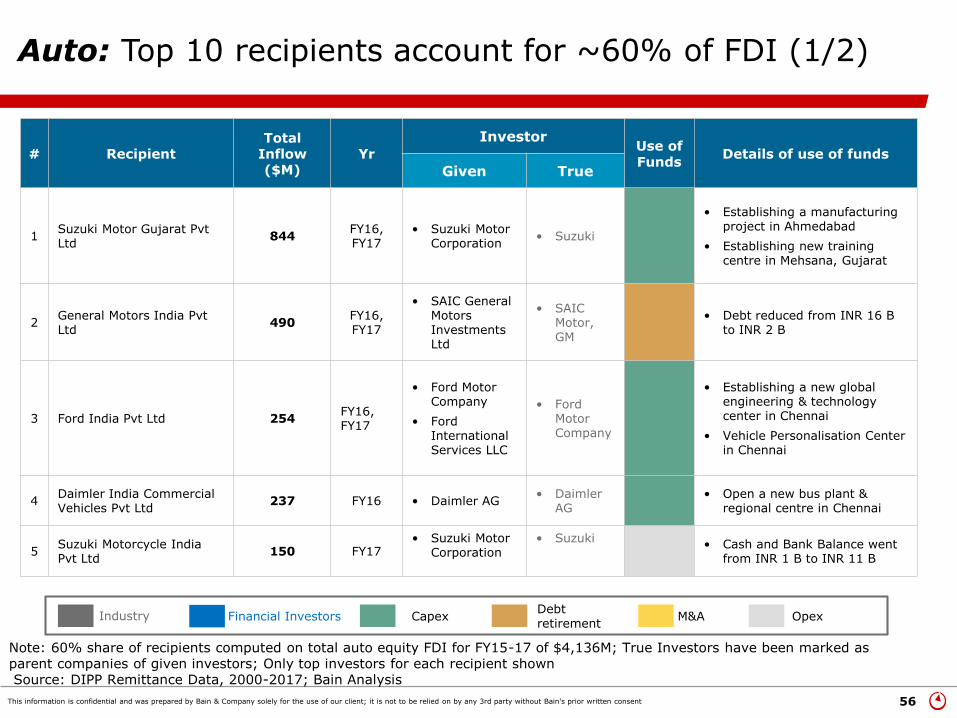

Note: 60% share of recipients computed on total auto equity FDI for FY15-17 of $4,136M; True Investors have been marked as parent companies of given investors; Only top investors for each recipient shownSource: DIPP Remittance Data, 2000-2017; Bain Analysis

# RecipientTotal

Inflow($M)

Yr

InvestorUse of Funds

Details of use of funds

Given True

1Suzuki Motor Gujarat Pvt Ltd

844FY16, FY17

• Suzuki Motor Corporation

• Suzuki

• Establishing a manufacturing project in Ahmedabad

• Establishing new training centre in Mehsana, Gujarat

2General Motors India Pvt Ltd

490FY16,FY17

• SAIC General Motors Investments Ltd

• SAIC Motor,GM

• Debt reduced from INR 16 B to INR 2 B

3 Ford India Pvt Ltd 254FY16, FY17

• Ford Motor Company

• Ford InternationalServices LLC

• FordMotor Company

• Establishing a new global engineering & technology center in Chennai

• Vehicle Personalisation Center in Chennai

4Daimler India Commercial Vehicles Pvt Ltd

237 FY16 • Daimler AG• Daimler

AG• Open a new bus plant &

regional centre in Chennai

5Suzuki Motorcycle India Pvt Ltd

150 FY17• Suzuki Motor

Corporation• Suzuki

• Cash and Bank Balance went from INR 1 B to INR 11 B

CapexDebt retirement

M&A OpexIndustry Financial Investors

Auto: Top 10 recipients account for ~60% of FDI (1/2)

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 57

# Recipient Total

Inflow($M)

Yr

InvestorUse of Funds

Details of use of fundsGiven True

6Isuzu Motors India Pvt Ltd

120 FY17• Isuzu Motors Asia Ltd

• Mitsubishi Corporation

• Isuzu Motors Ltd

• Mitsubishi Corporation

• Operating expenses increased

7Caparo Engineering India Pvt Ltd

115 FY16

• Caparo India Ltd

• Blue Elephant FinanceLtd

• Caparo

• Blue Elephant Capital Management

• New automotive componentsplant in southern India

• Debt reduced from INR 3.4 B to INR 2.3 B

8Komatsu India Pvt Ltd

98 FY17

• Komatsu Limited

• Komatsu Asia & Pacific PTE Ltd

• Komatsu Limited• Established a new hydraulic

excavator plant in Chennai

9Cosma International India Pvt Ltd

83FY16, FY17

• Magna Financing Luxembourg SARL

• Magna Cyprus Holding Ltd

• Magna International

• Opened a new manufacturing plant in Pune

10Rivigo ServicesPvt Ltd

74 FY17• Spring Canter

Investment Ltd• Warburg Princus

• Expansion of service offeringsacross India

Total (Top 10) $2467

Note: 60% share of recipients computed on total auto equity FDI for FY15-17 of $4,136M; True Investors have been marked as parent companies of given investors; Only top investors for each recipient shownSource: DIPP Remittance Data, 2000-2017; Bain Analysis

CapexDebt retirement

M&A OpexIndustry Financial Investors

Auto: Top 10 recipients account for ~60% of FDI (2/2)

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 58

Note: 89% share of recipients computed on total telecom equity FDI for FY15-17 of $6,887M; True Investors have been marked as parent companies of given investors; Only top investors for each recipient shownSource: DIPP Remittance Data, 2000-2017; Bain Analysis

# RecipientTotal

Inflow($M)

Yr

InvestorUse of Funds

Details of use of funds

Given True

1Vodafone India Ltd

2501 FY17

• Euro Pacific Securities Ltd

• Prime Metals Ltd

• Mobilvest

• Euro Pacific Capital

• Vodafone Group

• Expansion into other states

• Opened 2 global design stores in Pune

• New data center being set up

2Tata Teleservices Ltd

1574 FY17 • NTT Docomo Inc• Nippon Telegraph

& Telephone Corporation

• Loss Funding

3Viom Networks Ltd

893FY16, FY17

• ATC Asia Pacific PTE Ltd • ATC Asia Pacific Pte Ltd

• Debt of INR 58 B before being acquired by ATC

4

Videocon International Electronics Ltd

460FY16, FY17

• Videocon Mauritiu Energy Ltd

• VideoconIndustries Ltd

• NA

5Bharti Infratel

273 FY16

• QIB Class(total 33 investors)

• Anchor Investors(total 6 investors)

• Individual Investors

• Cash & Bank balance went up from INR 1.6 B to INR 31 B

CapexDebt retirement

M&A OpexIndustry Financial Investors

Telecom: Top 10 recipients account for ~91% of FDI (1/2)

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 59

# Recipient Total

Inflow($M)

YrInvestor

Use of Funds

Details of use of fundsGiven True

6 Tata Sky Ltd 182FY16, FY17

• Omega FII Investments Pte Ltd

• Network Digital Distribution Services

• Baytree Investments

• Tata Capital

• News Corporation

• Temasek Holdings

• Upgradation of Technology and Expansion

7 Hike Limited 124 FY17 • Hike Global ltd • Hike Ltd

• Funds raised for expansion

• Acquisition of Thought Mechanics Inc

8Unitech Wireless Tamil Nadu Pvt Ltd

104FY16, FY17

• Hike Global Pte Ltd

• Telenor Asia Pte Ltd• Hike Ltd

• Telenor• N. A.

Total (Top 8) $6111 M

Note: 89% share of recipients computed on total telecom equity FDI for FY15-17 of $6,887M; True Investors have been marked as parent companies of given investors; Only top investors for each recipient shownSource: DIPP Remittance Data, 2000-2017; Bain Analysis

CapexDebt retirement

M&A OpexIndustry Financial Investors

Telecom: Top 10 recipients account for ~91% of FDI (2/2)

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 60

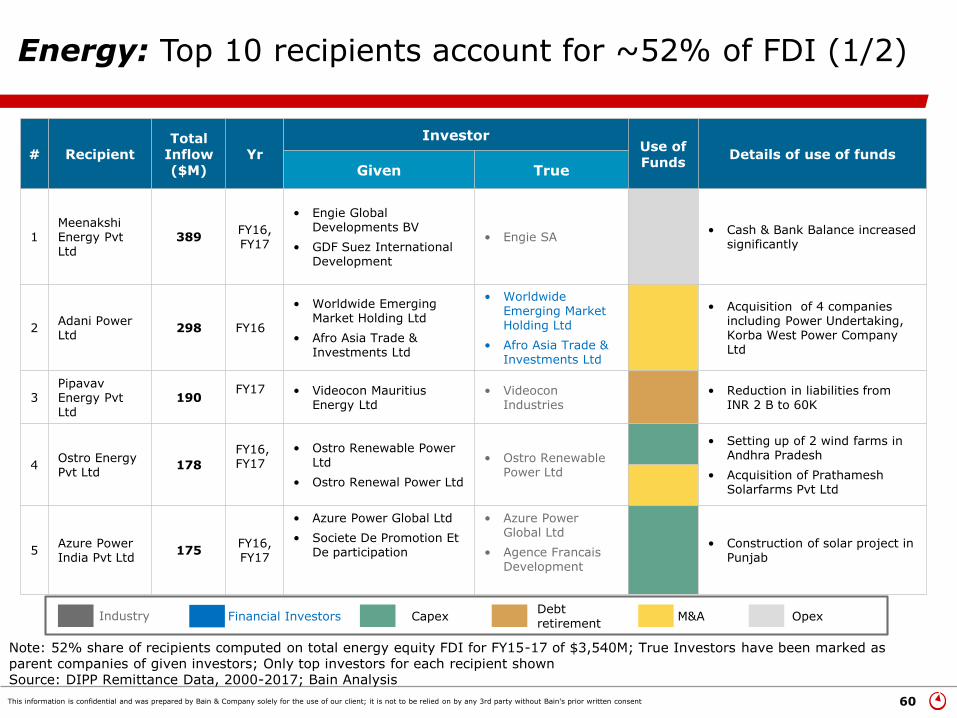

Note: 52% share of recipients computed on total energy equity FDI for FY15-17 of $3,540M; True Investors have been marked as parent companies of given investors; Only top investors for each recipient shownSource: DIPP Remittance Data, 2000-2017; Bain Analysis

# RecipientTotal

Inflow($M)

Yr

InvestorUse of Funds

Details of use of funds

Given True

1Meenakshi Energy Pvt Ltd

389FY16, FY17

• Engie Global Developments BV

• GDF Suez International Development

• Engie SA• Cash & Bank Balance increased

significantly

2Adani PowerLtd

298 FY16

• Worldwide Emerging Market Holding Ltd

• Afro Asia Trade & Investments Ltd

• WorldwideEmerging Market Holding Ltd

• Afro Asia Trade & Investments Ltd

• Acquisition of 4 companies including Power Undertaking, Korba West Power Company Ltd

3PipavavEnergy Pvt Ltd

190FY17 • Videocon Mauritius

Energy Ltd• Videocon

Industries• Reduction in liabilities from

INR 2 B to 60K

4Ostro Energy Pvt Ltd

178

FY16, FY17

• Ostro Renewable Power Ltd

• Ostro Renewal Power Ltd

• Ostro Renewable Power Ltd

• Setting up of 2 wind farms in Andhra Pradesh

• Acquisition of Prathamesh Solarfarms Pvt Ltd

5Azure Power India Pvt Ltd

175FY16, FY17

• Azure Power Global Ltd

• Societe De Promotion Et De participation

• Azure Power Global Ltd

• Agence Francais Development

• Construction of solar project in Punjab

CapexDebt retirement

M&A OpexIndustry Financial Investors

Energy: Top 10 recipients account for ~52% of FDI (1/2)

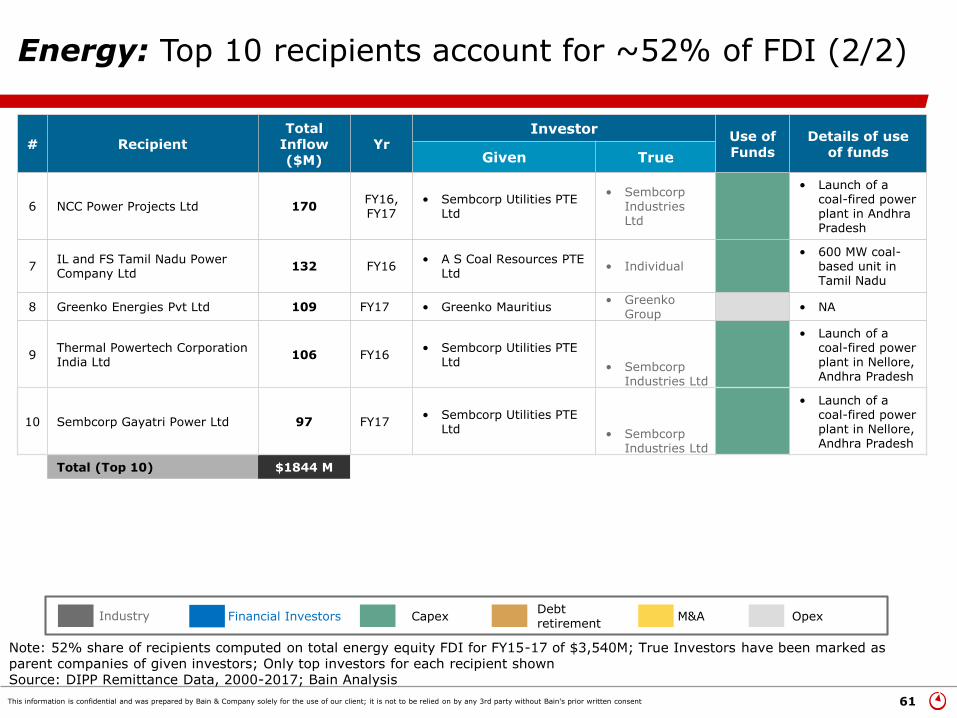

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 61

# Recipient Total

Inflow($M)

YrInvestor

Use of Funds

Details of use of fundsGiven True

6 NCC Power Projects Ltd 170FY16, FY17

• Sembcorp Utilities PTE Ltd

• Sembcorp Industries Ltd

• Launch of a coal-fired power plant in Andhra Pradesh

7IL and FS Tamil Nadu Power Company Ltd

132 FY16• A S Coal Resources PTE

Ltd• Individual

• 600 MW coal-based unit in Tamil Nadu

8 Greenko Energies Pvt Ltd 109 FY17 • Greenko Mauritius• Greenko

Group• NA

9Thermal Powertech Corporation India Ltd

106 FY16• Sembcorp Utilities PTE

Ltd • Sembcorp Industries Ltd

• Launch of a coal-fired power plant in Nellore, Andhra Pradesh

10 Sembcorp Gayatri Power Ltd 97 FY17• Sembcorp Utilities PTE

Ltd • Sembcorp Industries Ltd

• Launch of a coal-fired power plant in Nellore, Andhra Pradesh

Total (Top 10) $1844 M

Note: 52% share of recipients computed on total energy equity FDI for FY15-17 of $3,540M; True Investors have been marked as parent companies of given investors; Only top investors for each recipient shownSource: DIPP Remittance Data, 2000-2017; Bain Analysis

CapexDebt retirement

M&A OpexIndustry Financial Investors

Energy: Top 10 recipients account for ~52% of FDI (2/2)

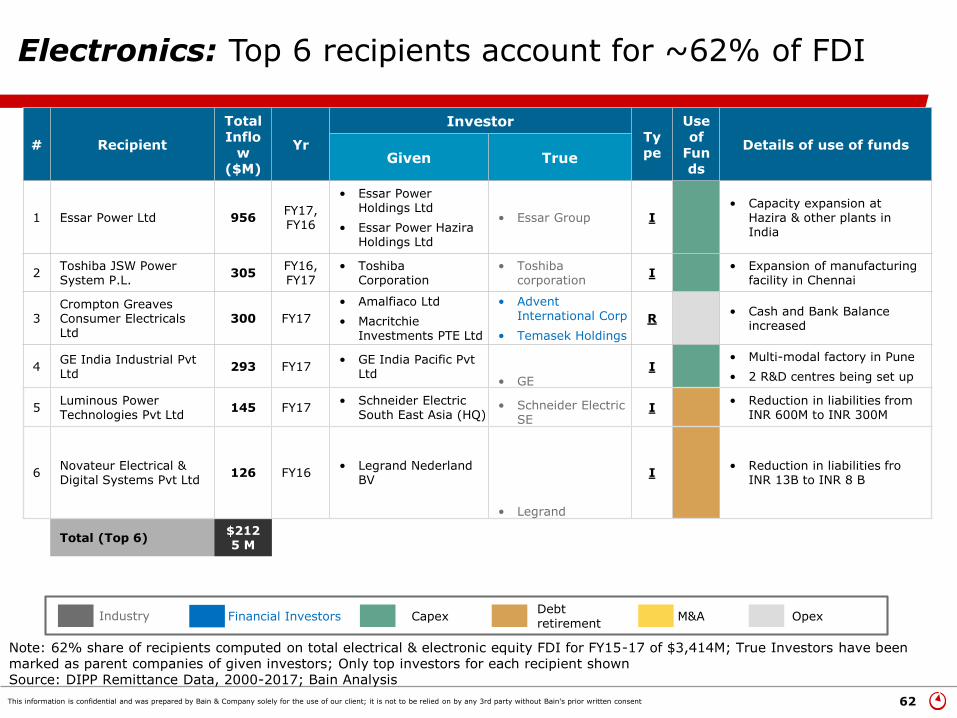

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 62

# Recipient

Total Inflo

w($M)

Yr

InvestorType

Use of

Funds

Details of use of fundsGiven True

1 Essar Power Ltd 956FY17, FY16

• Essar Power Holdings Ltd

• Essar Power Hazira Holdings Ltd

• Essar Group I• Capacity expansion at

Hazira & other plants in India

2Toshiba JSW Power System P.L.

305FY16, FY17

• Toshiba Corporation

• Toshiba corporation

I• Expansion of manufacturing

facility in Chennai

3Crompton Greaves Consumer Electricals Ltd

300 FY17

• Amalfiaco Ltd

• Macritchie Investments PTE Ltd

• Advent International Corp

• Temasek Holdings

R• Cash and Bank Balance

increased

4GE India Industrial Pvt Ltd

293 FY17• GE India Pacific Pvt

Ltd• GE

I• Multi-modal factory in Pune

• 2 R&D centres being set up

5Luminous Power Technologies Pvt Ltd

145 FY17• Schneider Electric

South East Asia (HQ)• Schneider Electric

SEI

• Reduction in liabilities from INR 600M to INR 300M

6Novateur Electrical & Digital Systems Pvt Ltd

126 FY16• Legrand Nederland

BV

• Legrand

I• Reduction in liabilities fro

INR 13B to INR 8 B

Total (Top 6)$2125 M

Note: 62% share of recipients computed on total electrical & electronic equity FDI for FY15-17 of $3,414M; True Investors have been marked as parent companies of given investors; Only top investors for each recipient shownSource: DIPP Remittance Data, 2000-2017; Bain Analysis

CapexDebt retirement

M&A OpexIndustry Financial Investors

Electronics: Top 6 recipients account for ~62% of FDI

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 63

Note: 65% share of recipients computed on total Chemicals equity FDI for FY15-17 of $2,900M; True Investors have been marked as parent companies of given investors; Only top investors for each recipient shownSource: DIPP Remittance Data, 2000-2017; Bain Analysis

# RecipientTotal

Inflow($M)

Yr

InvestorUse of Funds

Details of use of funds

Given True

1Shell India Markets Pvt Ltd

834FY16, FY17

• Shell Gas BV

• Shell India Ventures PTE Ltd

• Royal Dutch Shell• Scaling up number of retail

stations

2 UPL td 492 FY17 • As per list• Individual

Investors

• Expansion of production capacity of Nitrogen plant in Jhagadia

• Acquisition of Serra Bonita Sements SA, Advanta Ltd

3Kansai NerolacPaints Ltd

157 FY17 • Kansai Paint Co Ltd• Kansai Paint Co

Ltd• Reduction in liabilities from

INR 571 M to NR 294 M

4Sintex Industries Ltd

115 FY16• As per Annexure

• ICICI Bank UK PLC

• IndividualInvestors

• ICICI Bank

• Expansion of yarn plant in Gujarat

5Lanxess India Pvt Ltd

87FY16, FY17

• Lanxess Deutschland GMBH

• Lanxess Deutsche GMBH

• Lanxess AG

• Reduction of liabilities from INR 7 B to INR 2 B

CapexDebt retirement

M&A OpexIndustry Financial Investors

Chemicals: Top 9 recipients account for ~65% of FDI (1/2)

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 64

# Recipient Total

Inflow($M)

YrInvestor

Use of Funds

Details of use of fundsGiven True

6 Hyderabad Chemical Ltd 57 FY16• Nihon Nohyaku Co Ltd

• Nichino Service Co Ltd

• Nihon Nohyaku Co Ltd

• NA

7 Chiripal Poly Films Ltd 53FY16, FY17

• Amber Finance Ltd

• Waldorf Investments Ltd

• Amber Financial Investments Ltd

• Waldorf Investments Ltd

• Expansion at textile park in Bidaj, Gujarat

8 Excel Crop Care Ltd 50 FY17• Sumitomo Chemical Co

Ltd, Japan

• Sumitomo Mitsui Trust Group

• Setting up of pesticide plant in Gujarat

• Liabilities reduced from INR 86 M to INR 29M

9 Renewsys India Ltd 49FY16, FY17

• Far East Holdings Ltd

• Far East Holdings International Ltd

• Acquisition of Solar Semiconductor Pvt Ltd

Total (Top 9) $1894 M

Note: 65% share of recipients computed on total Chemicals equity FDI for FY15-17 of $2,900M; True Investors have been marked as parent companies of given investors; Only top investors for each recipient shownSource: DIPP Remittance Data, 2000-2017; Bain Analysis

CapexDebt retirement

M&A OpexIndustry Financial Investors

Chemicals: Top 9 recipients account for ~65% of FDI (2/2)

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 65

# Recipient Total

Inflow($M)

Yr

InvestorUse of Funds

Details of use of fundsGiven True

1 JSW Steel Ltd 719 FY17• JFE Steel

Corporation, Japan• JFE Steel Corporation

• Acquisition of JSW Industrial Gases Pvt Ltd, Welspun Maxsteel Ltd

2Essel Mining & Industries Ltd

483 FY16• Surya Abha

Investment Pte Ltd• Surya Abha

Investments Pte Ltd• NA

3POSCO Maharashtra Steels Pvt Ltd

318FY16, FY17

• POSCO • POSCO• Setting up new steel

plant in Maharashtra

4Mahindra CIE Automotive Ltd

122FY16, FY17

• Participaciones Internacionales Autometa

• Ainos Holdings Ltd

• CIE Automotive

• Kedaara Capital Investment Managers Ltd

• Acquisition of Bill Forge Pvt Ltd

5Castex Technologies Ltd

108FY16, FY17

• Standard Chartered Bank

• Deutsche Bank

• Swiss Finance Corp Mauritius Ltd

• Standard Chartered

• Deutsche Bank AG

• UBS AG

• Losses at INR 613.52cr in FY16

6Haldia Petrochemicals Ltd

99 FY17• Essex Development

Investments (Mauritius) • The Chatterjee Group

• Cash and Bank Balance increased

Total (Top 6) $1849 M