impulse merchandising in drug stores - front-end focus merchandisin… · impulse merchandising in...

TRANSCRIPT

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

0

Impulse Merchandising At Drug Store

Checkouts

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

1

Agenda

Drug Store Merchandising Leadership

Drug Store Consumer Insights

Drug Store Merchandising Opportunities

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

2

The Leadership Challenge

“Leaders don’t force people to follow,

they invite them on a journey.”

Charles S. Lauer

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

3

Leadership In Drug Store Impulse Merchandising

Formation of a leadership council including the following manufacturers:

Masterfoods USA, a Division of Mars, Incorporated

The Wm. Wrigley Jr. Company

Time Warner Retail Sales & Marketing (TWRSM)

In partnership with Dechert-Hampe & Company, an independent research and consulting firm

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

4

Mission Of The Group

To work in partnership with retail customers and other stakeholders to improve store performance and enhance consumer satisfaction through:

New learning and consumer knowledgeDeveloping benchmarks and Best PracticesInnovative solutions for in-store merchandising

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

5

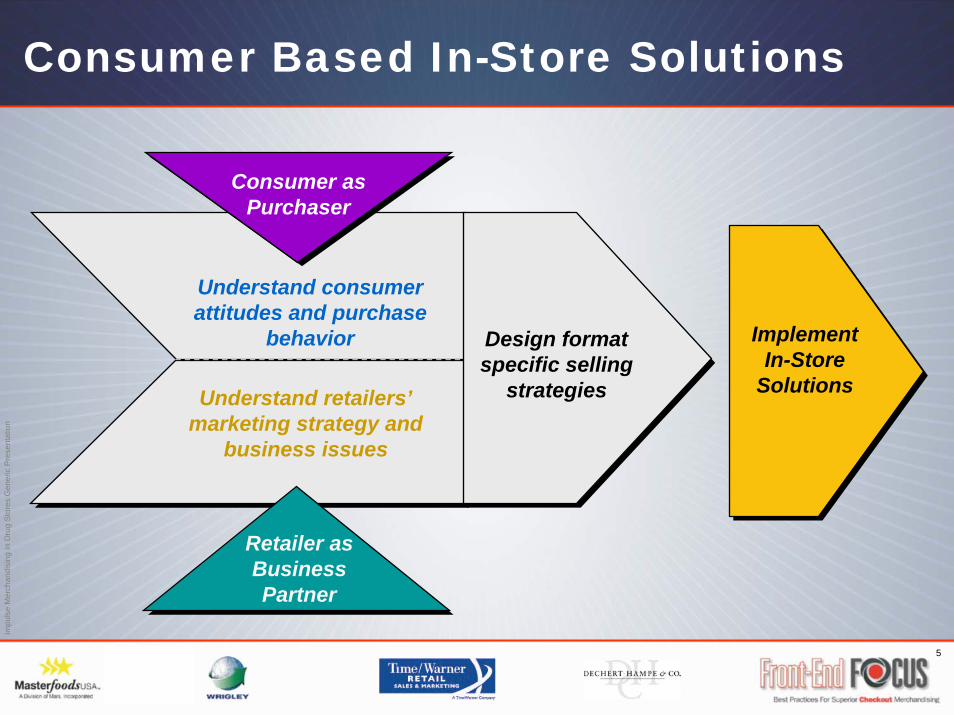

Consumer Based In-Store Solutions

Design format specific selling

strategiesUnderstand retailers’ marketing strategy and

business issues

Understand consumer attitudes and purchase

behavior

Consumer as Purchaser

Retailer as Business Partner

Implement In-Store

Solutions

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

6

Key Issues For The Drug Channel

Increasing Drug store count and industry consolidation have led to increased competition

Channel blurring has resulted in more cross-channel competition and increased importance of convenience

Two-thirds of Drug store sales are now from Pharmacy, but the majority of profit comes from front of store sales

Drug stores have lost shopper penetration and trip frequency to other outlets

Sources: MVI, A.C. Nielsen

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

7

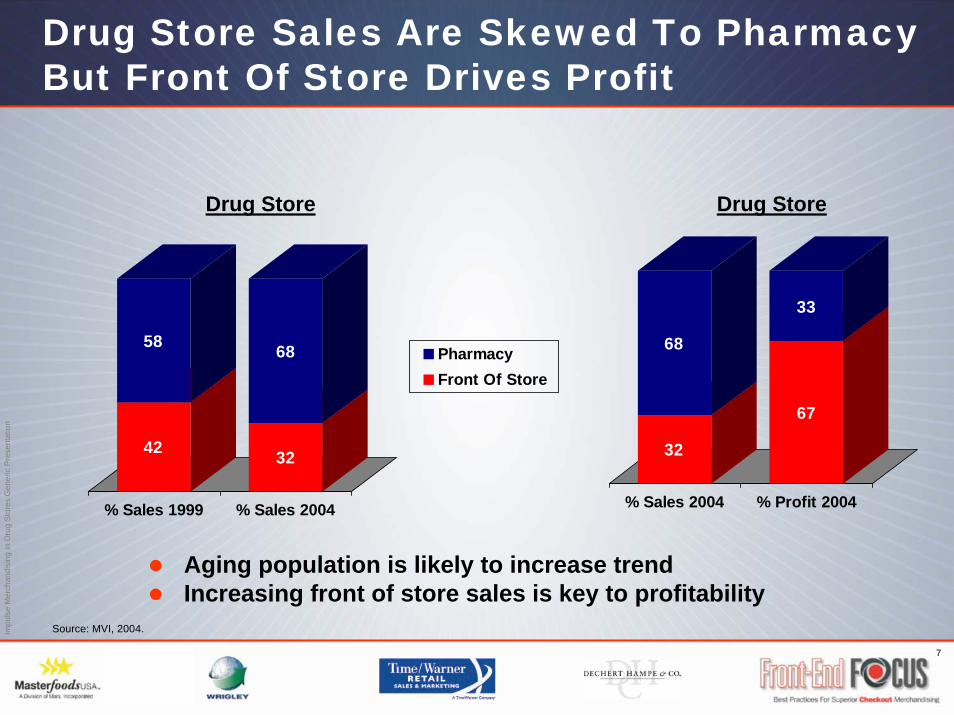

Drug Store Sales Are Skewed To Pharmacy But Front Of Store Drives Profit

42

58

32

68

% Sales 1999 % Sales 2004

PharmacyFront Of Store

32

68

67

33

% Sales 2004 % Profit 2004

Drug Store Drug Store

Aging population is likely to increase trendIncreasing front of store sales is key to profitability

Source: MVI, 2004.

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

8

Drug Stores Need To Increase Household Shopping Frequency

1011

1013

1415

1515

2521

1726

7870

WarehouseClubs

Dollar Stores

ConvenienceStores

Drug Stores

MassMerchandisers

Supercenters

Grocery

Mid-20042000

Household Shopping Frequency(# of Trips per Year)

Source: Nielsen Household Panel.

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

9

A Key Opportunity For Drug Stores Is To Increase Basket Ring

Source: Nielsen Household Panel. Basket does not include prescriptions or gas.

$11$11

$10$12

$19$21

$32$33

$38$42

$49$56

$83$82

Dollar Stores

ConvenienceStores

Drug Stores

Grocery

MassMerchandiser

Supercenters

WarehouseClubs

Mid-2004

2000

Average $ Basket Ring

Basket size has increased, but still lags other outlets

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

10

Objectives Of The Drug Store Checkout Shopper Study

1. Understand current and emerging consumer attitudes and shopping behavior in the Drug class of trade

2. Develop new insight on the challenges and potential opportunities for impulse sales in Drug stores

3. Develop new concepts for in-store solutions to Drug store impulse merchandising

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

11

Drug Store Checkout Shopper Study

Scope

Participation by 4 major Drug store chainsResearch conducted in 72 stores in:

Atlanta Detroit No. New JerseyBoston Hartford PittsburghCharlotte Los Angeles San FranciscoChicago New Orleans

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

12

Drug Store Checkout Shopper Study

Methodology

Audits of 371 checkout locations in 72 storesObservations of 3,913 shoppers at point of saleIn-store interviews with 1541 consumersIndependent analysis by Dechert-Hampe & Co.

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

13

Impulse Merchandising Is A Key Element Of Drug Store Strategy

Drug stores need to recognize and adapt to changing consumer shopping occasions and patterns

Drug stores can generate incremental sales through more points of interruption with impulse items

Checkouts are the prime locations where all shoppers can be exposed to effective impulse merchandising

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

14

Key Drug Store Opportunities For Impulse Merchandising

Opportunity to refocus checkout merchandising on key impulse items that generate incremental sales and increase market basket

Opportunity to redesign Pharmacy and Photo checkouts around consumer buying behavior

Opportunity to utilize convenience strategy to drive shopping frequency with key consumables

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

15

Drug Store

Consumer Insights

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

16

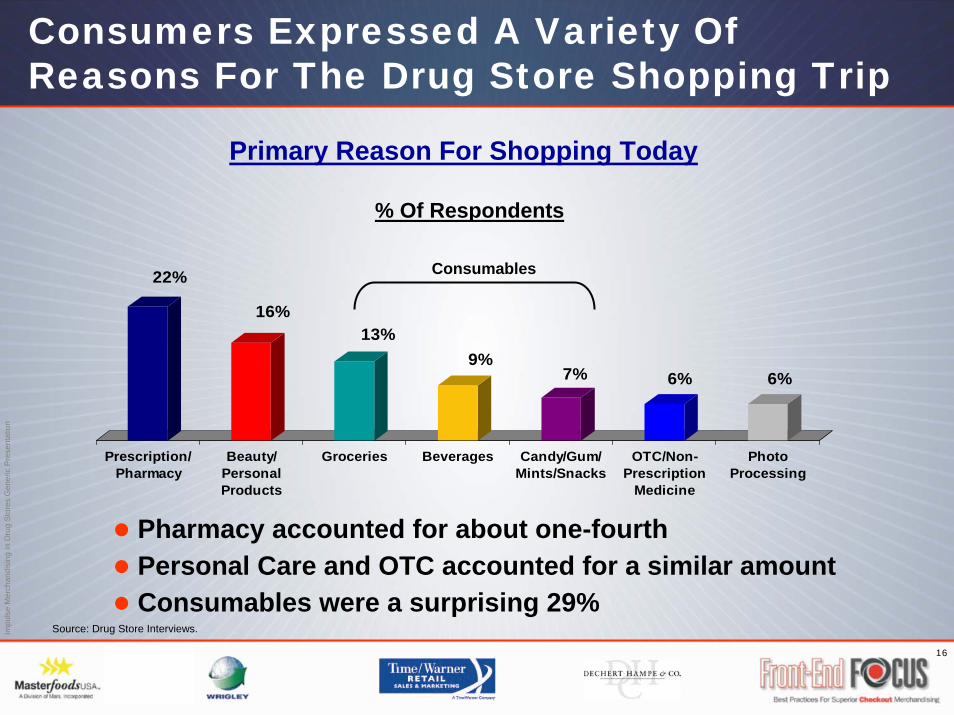

Consumers Expressed A Variety Of Reasons For The Drug Store Shopping Trip

Primary Reason For Shopping Today

22%

16%13%

9%7% 6% 6%

Prescription/Pharmacy

Beauty/PersonalProducts

Groceries Beverages Candy/Gum/Mints/Snacks

OTC/Non-Prescription

Medicine

PhotoProcessing

% Of Respondents

Pharmacy accounted for about one-fourth Personal Care and OTC accounted for a similar amountConsumables were a surprising 29%

Consumables

Source: Drug Store Interviews.

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

17

Most People Chose A Store Because It Was Near To Home Or Near Their Destination

10%

14%

15%

19%

21%

70%

Product Assortment

Sale/Coupon

Good ShoppingExperience

Good Values

Convenient - NearDestination

Convenient - NearHome

Why Did You Pick This Store?*% Of Respondents

Convenience of location leads to a case for consumables* Could provide multiple answers.Source: Drug Store Interviews.

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

18

Most Shoppers Had Something In Mind, But Not A Shopping List

17%21%

5%

57%Brought A Shopping List Had A Mental List Had No List Saw Something In Circular

Use of Shopping List% Of Respondents

The absence of a list suggests potential for impulse buyingSource: Drug Store Interviews.

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

19

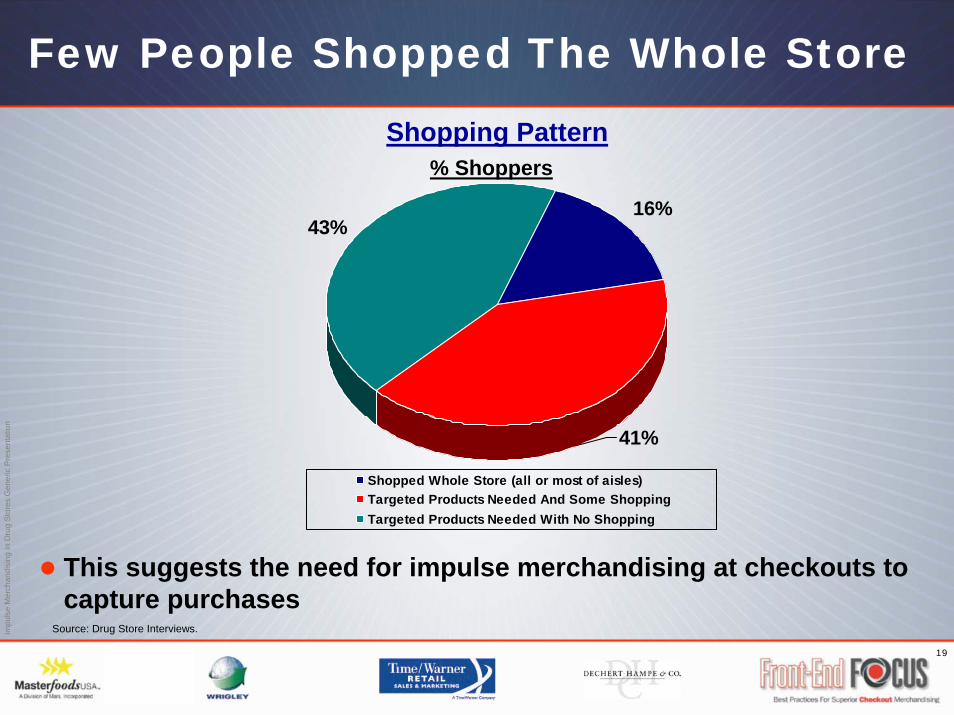

16%43%

41%

Shopped Whole Store (all or most of aisles)Targeted Products Needed And Some ShoppingTargeted Products Needed With No Shopping

Few People Shopped The Whole Store

% ShoppersShopping Pattern

This suggests the need for impulse merchandising at checkouts tocapture purchases

Source: Drug Store Interviews.

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

20

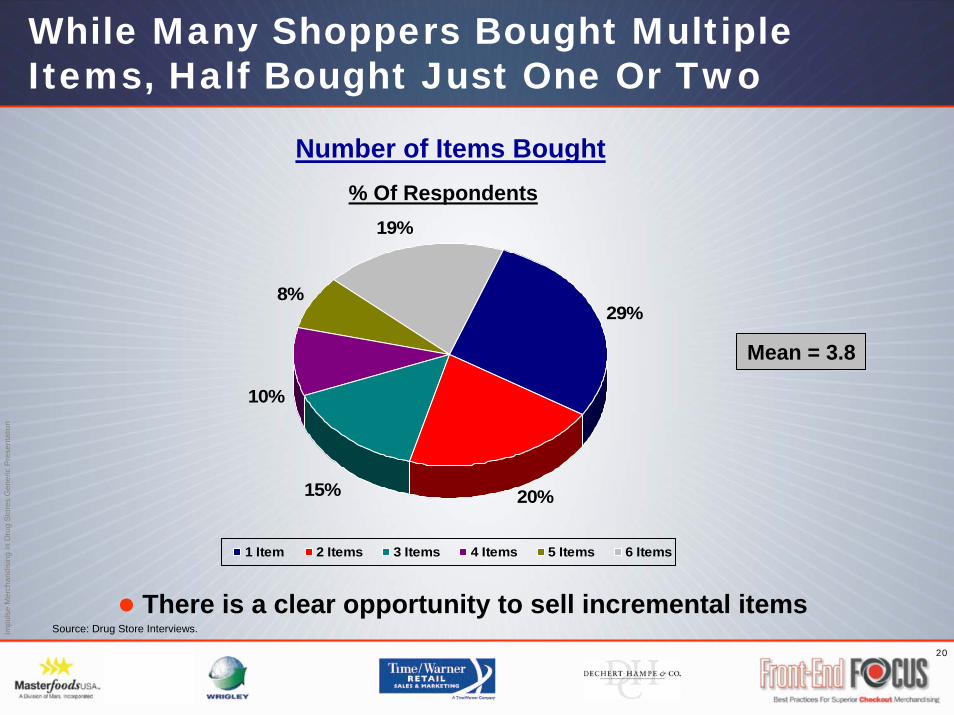

While Many Shoppers Bought Multiple Items, Half Bought Just One Or Two

29%

15%

10%

8%

19%

20%

1 Item 2 Items 3 Items 4 Items 5 Items 6 Items

Number of Items Bought% Of Respondents

Mean = 3.8

Source: Drug Store Interviews.

There is a clear opportunity to sell incremental items

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

21

Shoppers Spent An Average Of $16.00, But Almost Half Spent Less Than $ 10.00

8%

22%27%

14%

10% 4%

15%

Less Than $2.00 $2.00-$4.99 $5.00-$9.99$10.00-$19.99 $20.00-$29.99 $30.00-$49.99$50.00 Or More

Dollar Expenditure% Of Respondents

Mean = $15.97

Source: Drug Store Interviews.

There is a major opportunity to increase basket ring

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

22

16%

84%

Bought At Checkout Today Not Bought

Checkout Purchases Are A Key Source Of Incremental Volume

Bought Item at Checkout Today% Shoppers

One in six shoppers bought something at checkout today

Source: Drug Store Observations.

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

23

Drinks, Candy, Gum And Magazines Are Most Purchased Categories At Front-End Checkouts

1.0%1.0%

1.1%1.3%1.6%

1.6%2.0%2.3%2.6%

3.8%3.8%4.0%

5.2%

5.2%5.8%

Remedies-Headache

Remedies-Cold

Batteries

Mints

Salty Snacks

Oral Care

Candy-Novelty

Tobacco Access.

Candy-Bag

Magazines/Newspaper

Drink-Non Carb.

Gum

Cigarettes

Drinks-Carbonated

Candy-Bars

Source: Drug Store Observations.

Observed Purchase At Front-End Checkout% Shoppers

(2,636)

0.2%

0.3%

0.3%

0.3%

0.3%

0.4%

0.5%

0.5%

0.6%

0.7%

0.7%

0.8%

0.8%

1.0%

Razor Blades

Diet Products

Meat Snack

Video/DVD/CD

Cosmetics

Energy Bars

Phone Cards

Low Carb Snack

Film

Remedies-Cough

Camera

Nuts/Seeds

Cookies/Crackers

Lip Care

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

24

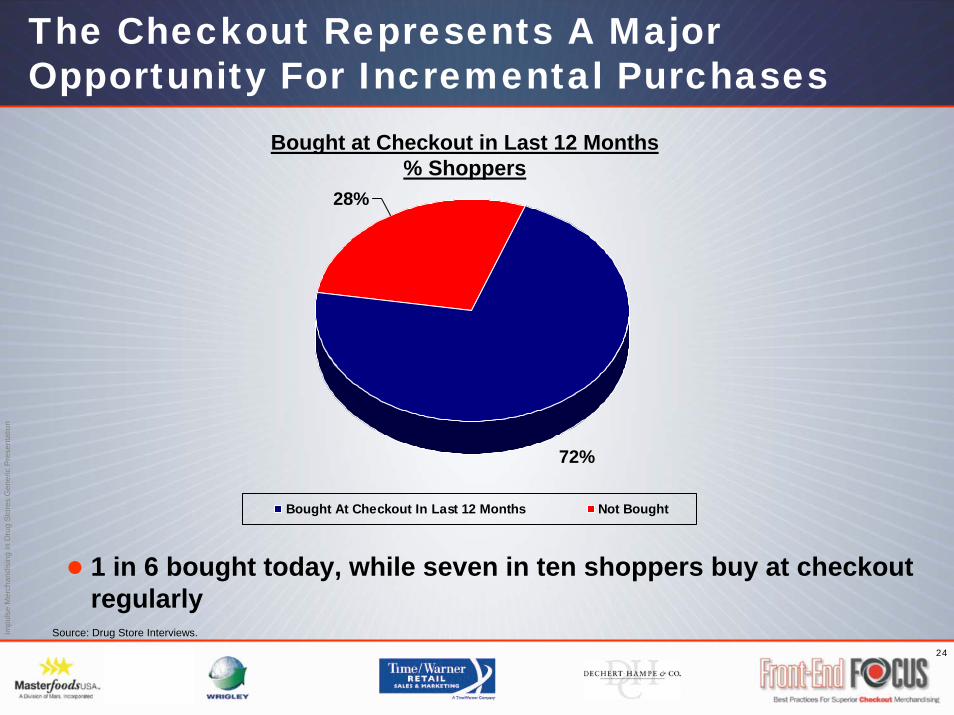

The Checkout Represents A Major Opportunity For Incremental Purchases

72%

28%

Bought At Checkout In Last 12 Months Not Bought

Bought at Checkout in Last 12 Months% Shoppers

1 in 6 bought today, while seven in ten shoppers buy at checkoutregularly

Source: Drug Store Interviews.

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

25

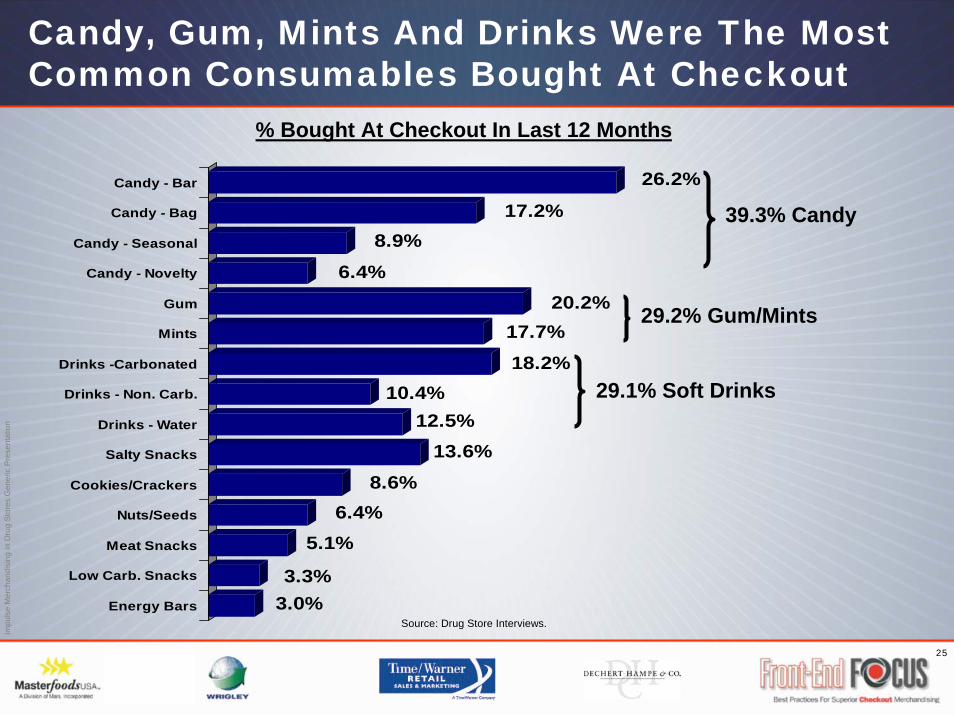

Candy, Gum, Mints And Drinks Were The Most Common Consumables Bought At Checkout

3.0%3.3%

5.1%6.4%

8.6%13.6%

12.5%10.4%

18.2%17.7%

20.2%6.4%

8.9%17.2%

26.2%

Energy Bars

Low Carb. Snacks

Meat Snacks

Nuts/Seeds

Cookies/Crackers

Salty Snacks

Drinks - Water

Drinks - Non. Carb.

Drinks -Carbonated

Mints

Gum

Candy - Novelty

Candy - Seasonal

Candy - Bag

Candy - Bar

% Bought At Checkout In Last 12 Months

Source: Drug Store Interviews.

39.3% Candy

29.2% Gum/Mints

29.1% Soft Drinks

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

26

Batteries, Cosmetics, Film And Magazines Are The Top Non-Consumables

11.8%

12.0%

12.3%

12.7%

12.9%

13.0%

13.0%

13.4%

15.0%

17.2%

22.8%

Remedies - Headache

Skin Care

Hair Care

Lip Care

Gift Cards

Remedies - Cough/Cold

Magazines

Cigarettes

Film

Cosmetics

Batteries

% Bought At Checkout In Last 12 Months

Source: Drug Store Interviews.

3.4%

3.5%

4.1%

5.5%

5.6%

6.5%

7.5%

7.5%

9.8%

10.6%

11.2%

Dieting Products

Phone Cards

Tobacco Accessories

Books

Video/DVD/CD

Cameras

Eye Care

Remedies - Stomach

Razor Blades

Vitamins

Oral Care

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

27

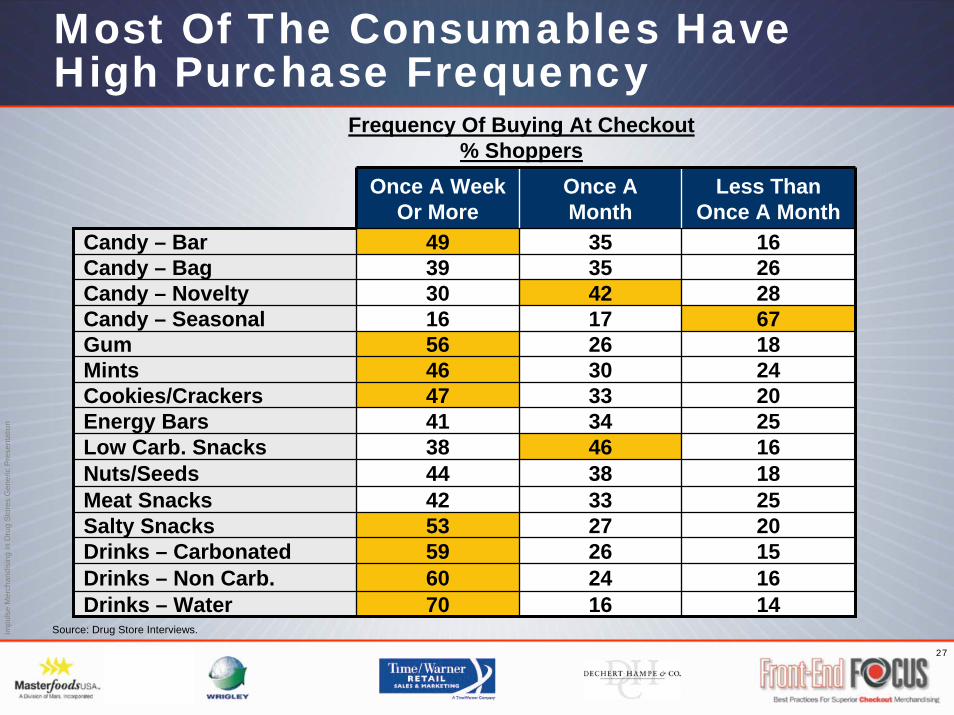

Most Of The Consumables Have High Purchase Frequency

Once A Week Or More

Once A Month

Less Than Once A Month

Candy – Bar 49 35 16Candy – Bag 39 35 26Candy – Novelty 30 42 28Candy – Seasonal 16 17 67Gum 56 26 18Mints 46 30 24Cookies/Crackers 47 33 20Energy Bars 41 34 25Low Carb. Snacks 38 46 16Nuts/Seeds 44 38 18Meat Snacks 42 33 25Salty Snacks 53 27 20Drinks – Carbonated 59 26 15Drinks – Non Carb. 60 24 16Drinks – Water 70 16 14

Frequency Of Buying At Checkout% Shoppers

Source: Drug Store Interviews.

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

28

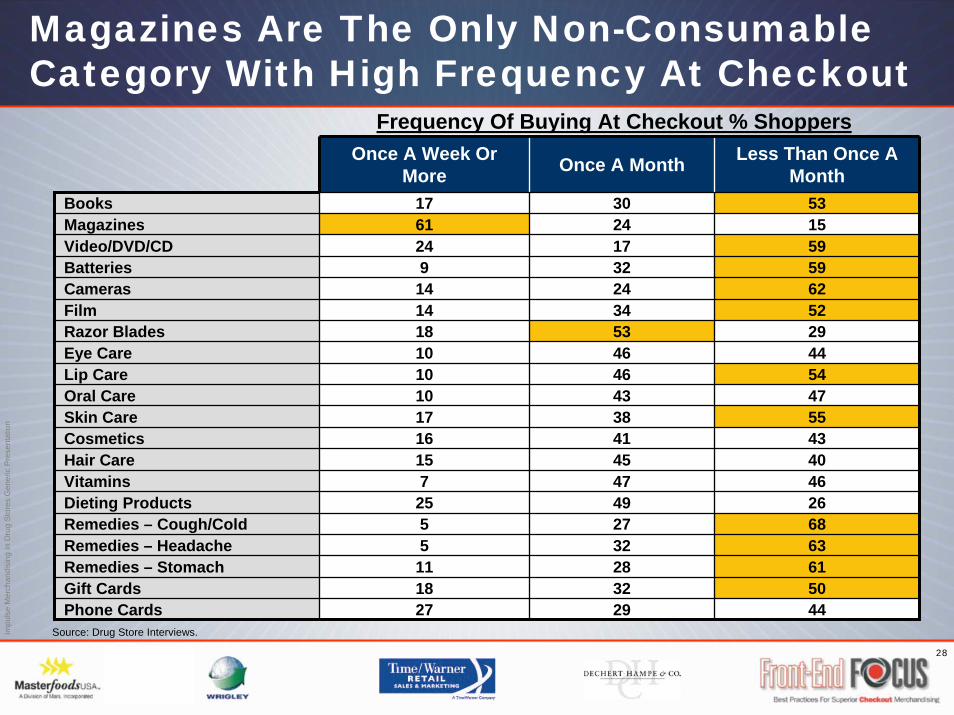

Magazines Are The Only Non-Consumable Category With High Frequency At Checkout

Source: Drug Store Interviews.

Once A Week Or More Once A Month Less Than Once A

MonthBooks 17 30 53Magazines 61 24 15Video/DVD/CD 24 17 59Batteries 9 32 59Cameras 14 24 62Film 14 34 52Razor Blades 18 53 29Eye Care 10 46 44Lip Care 10 46 54Oral Care 10 43 47Skin Care 17 38 55Cosmetics 16 41 43Hair Care 15 45 40Vitamins 7 47 46Dieting Products 25 49 26Remedies – Cough/Cold 5 27 68Remedies – Headache 5 32 63Remedies – Stomach 11 28 61Gift Cards 18 32 50Phone Cards 27 29 44

Frequency Of Buying At Checkout % Shoppers

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

29

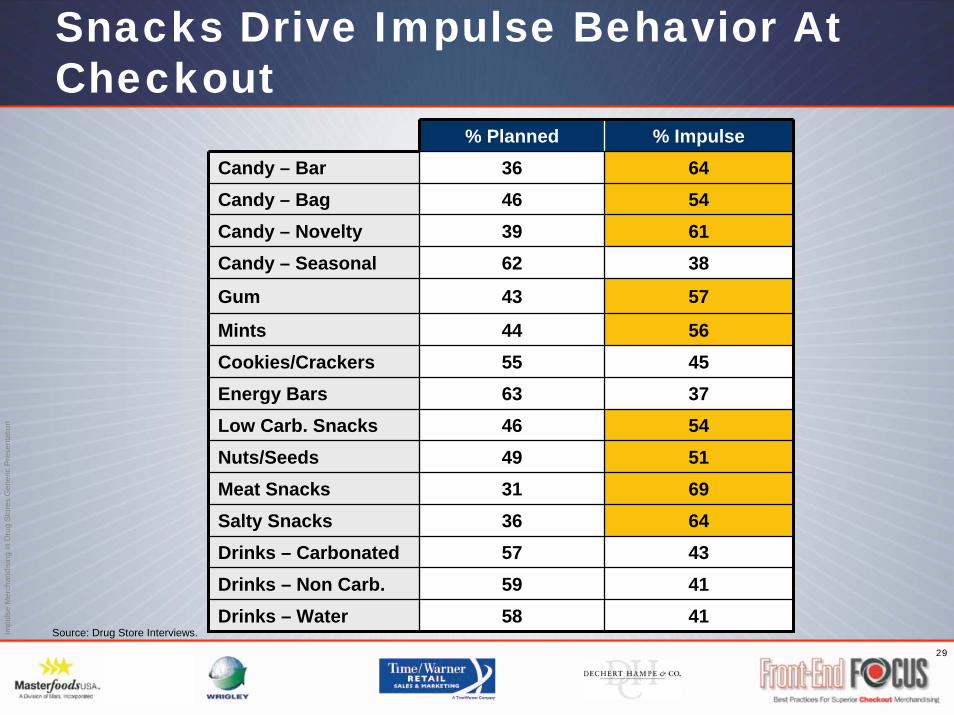

Snacks Drive Impulse Behavior At Checkout

% Planned % ImpulseCandy – Bar 36 64Candy – Bag 46 54Candy – Novelty 39 61Candy – Seasonal 62 38

Gum 43 57

Mints 44 56Cookies/Crackers 55 45Energy Bars 63 37Low Carb. Snacks 46 54Nuts/Seeds 49 51Meat Snacks 31 69Salty Snacks 36 64Drinks – Carbonated 57 43Drinks – Non Carb. 59 41Drinks – Water 58 41

Source: Drug Store Interviews.

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

30

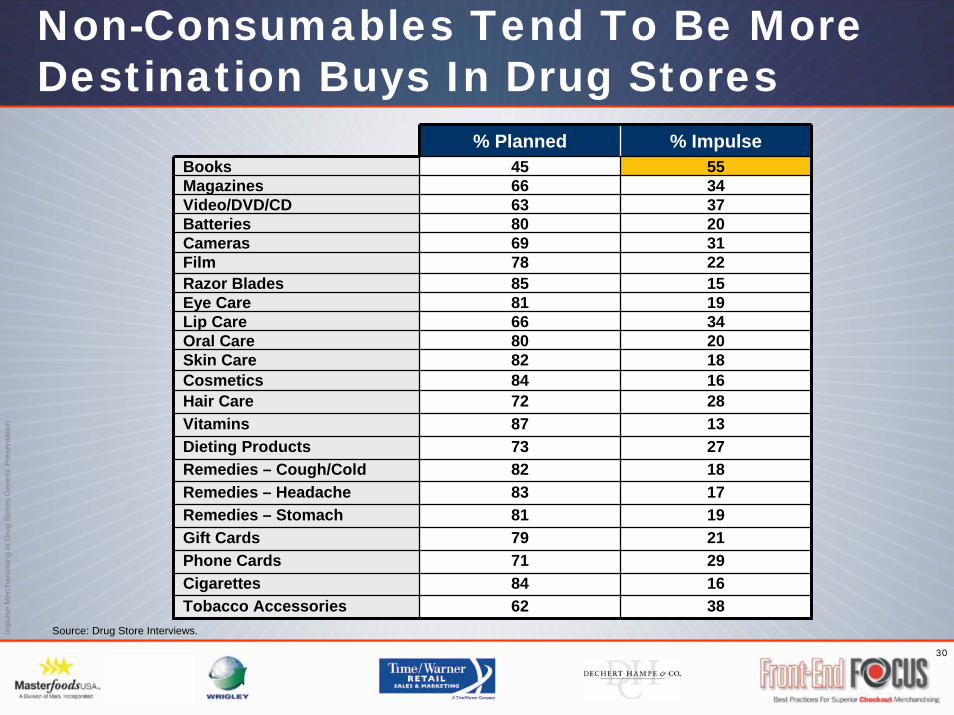

Non-Consumables Tend To Be More Destination Buys In Drug Stores

% Planned % ImpulseBooks 45 55Magazines 66 34Video/DVD/CD 63 37Batteries 80 20Cameras 69 31Film 78 22Razor Blades 85 15Eye Care 81 19Lip Care 66 34Oral Care 80 20Skin Care 82 18Cosmetics 84 16Hair Care 72 28Vitamins 87 13Dieting Products 73 27Remedies – Cough/Cold 82 18Remedies – Headache 83 17Remedies – Stomach 81 19Gift Cards 79 21Phone Cards 71 29Cigarettes 84 16Tobacco Accessories 62 38

Source: Drug Store Interviews.

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

31

Drug StoreImpulse Merchandising

Opportunities

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

32

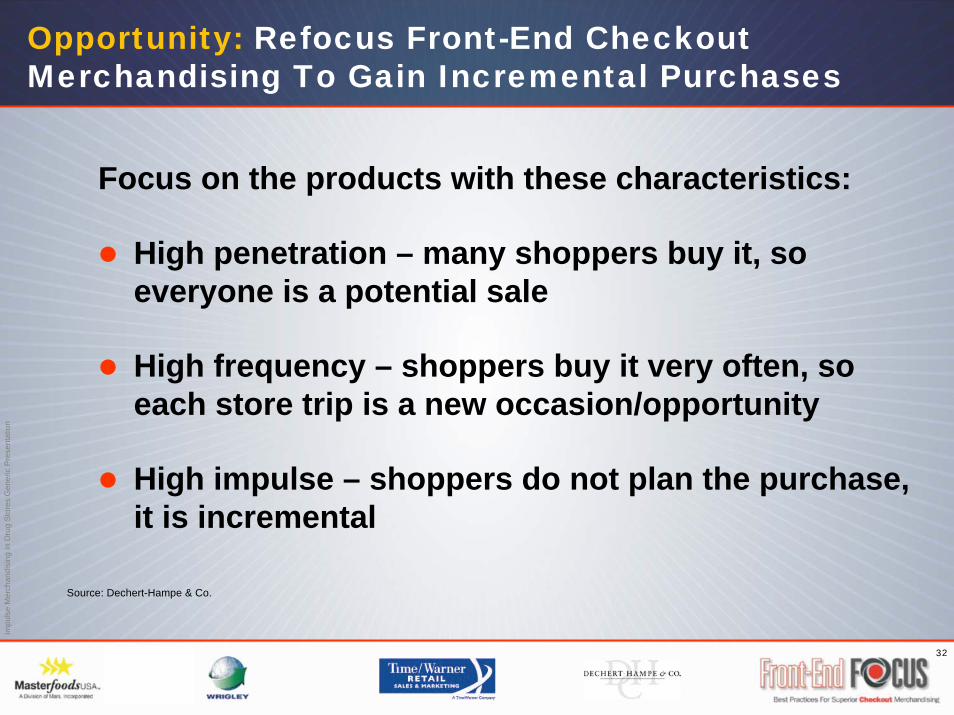

Opportunity: Refocus Front-End Checkout Merchandising To Gain Incremental Purchases

Focus on the products with these characteristics:

High penetration – many shoppers buy it, so everyone is a potential sale

High frequency – shoppers buy it very often, so each store trip is a new occasion/opportunity

High impulse – shoppers do not plan the purchase, it is incremental

Source: Dechert-Hampe & Co.

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

33

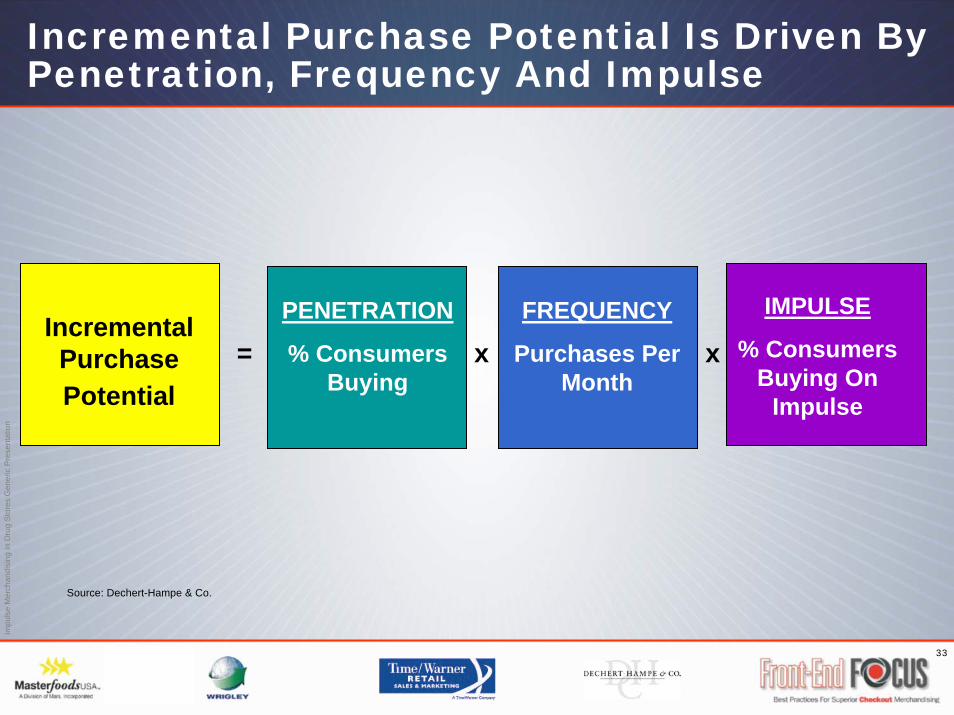

Incremental Purchase Potential Is Driven By Penetration, Frequency And Impulse

= x xIncremental Purchase Potential

PENETRATION

% Consumers Buying

FREQUENCY

Purchases Per Month

IMPULSE

% Consumers Buying On

Impulse

Source: Dechert-Hampe & Co.

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

34

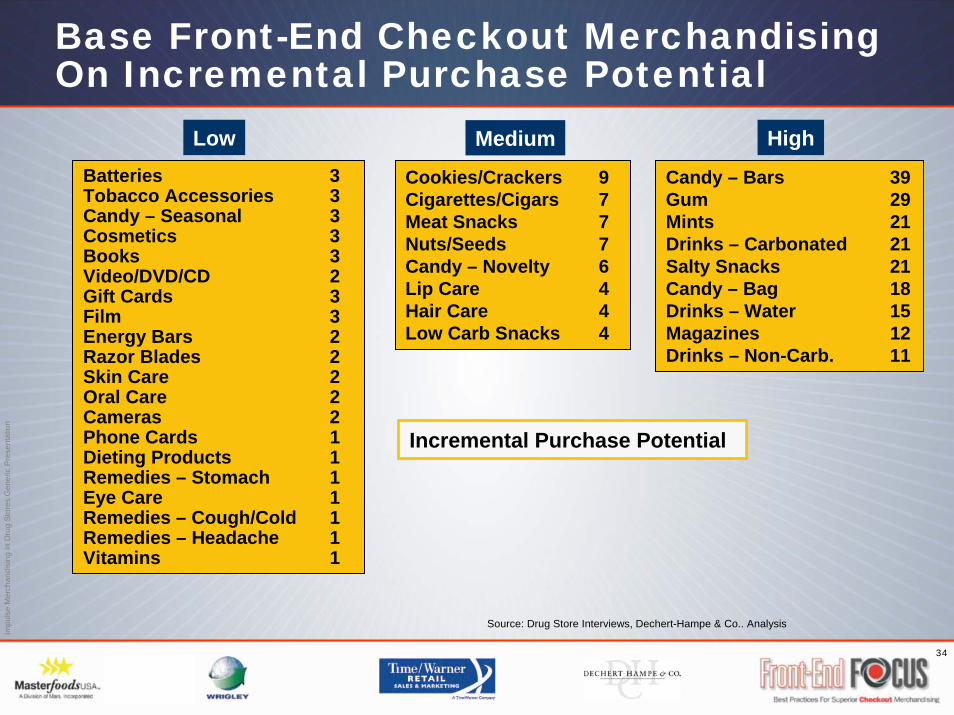

Base Front-End Checkout Merchandising On Incremental Purchase Potential

Batteries 3Tobacco Accessories 3Candy – Seasonal 3Cosmetics 3Books 3Video/DVD/CD 2Gift Cards 3Film 3Energy Bars 2Razor Blades 2Skin Care 2Oral Care 2Cameras 2Phone Cards 1Dieting Products 1Remedies – Stomach 1Eye Care 1Remedies – Cough/Cold 1Remedies – Headache 1Vitamins 1

Low

Candy – Bars 39Gum 29Mints 21Drinks – Carbonated 21Salty Snacks 21Candy – Bag 18Drinks – Water 15Magazines 12Drinks – Non-Carb. 11

High

Cookies/Crackers 9Cigarettes/Cigars 7Meat Snacks 7Nuts/Seeds 7Candy – Novelty 6Lip Care 4Hair Care 4Low Carb Snacks 4

Medium

Incremental Purchase Potential

Source: Drug Store Interviews, Dechert-Hampe & Co.. Analysis

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

35

Opportunity: Design Pharmacy Checkout Merchandising Around The Consumer

Merchandise health-related products to provide solution sales at Pharmacy checkouts

Display Magazines and Books to provide information and entertainment for consumers while waiting for prescriptions

Display Consumables (Candy, Gum, Mints, etc.) to generate impulse purchases

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

36

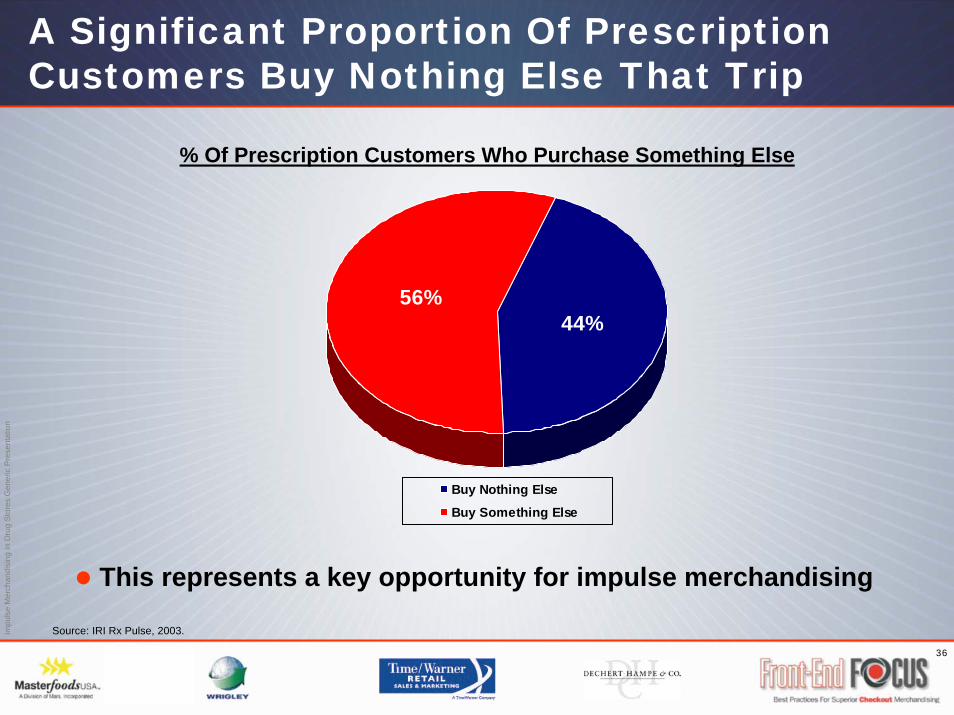

A Significant Proportion Of Prescription Customers Buy Nothing Else That Trip

44%56%

Buy Nothing ElseBuy Something Else

% Of Prescription Customers Who Purchase Something Else

This represents a key opportunity for impulse merchandising

Source: IRI Rx Pulse, 2003.

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

37

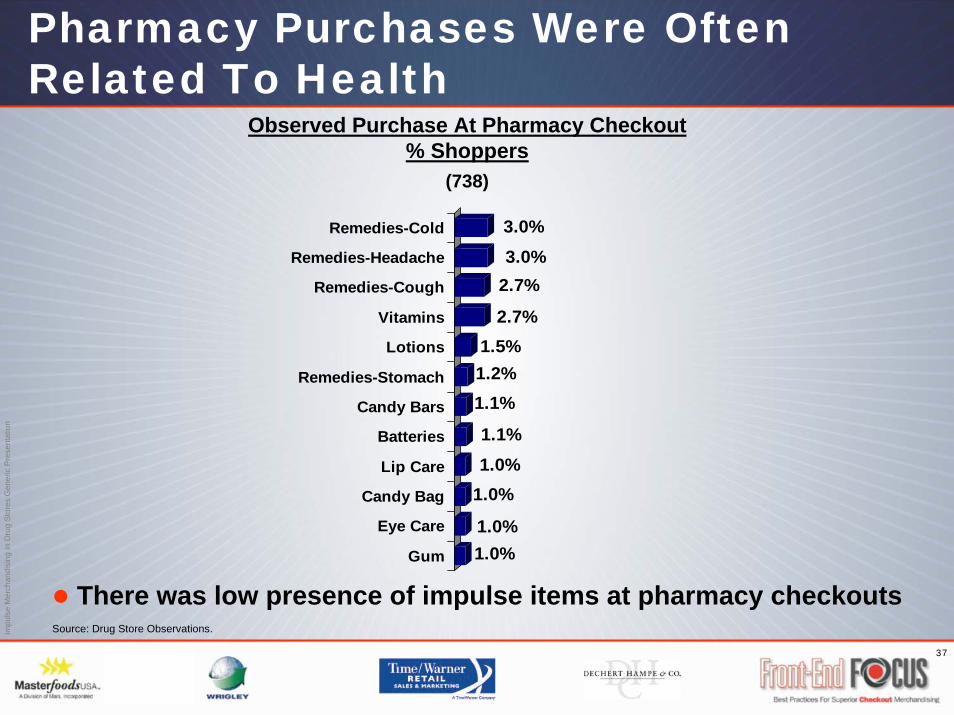

Pharmacy Purchases Were Often Related To Health

1.0%1.0%

1.0%1.0%1.1%

1.1%1.2%1.5%

2.7%

2.7%3.0%3.0%

Gum

Eye Care

Candy Bag

Lip Care

Batteries

Candy Bars

Remedies-Stomach

Lotions

Vitamins

Remedies-Cough

Remedies-Headache

Remedies-Cold

Observed Purchase At Pharmacy Checkout% Shoppers

(738)

There was low presence of impulse items at pharmacy checkoutsSource: Drug Store Observations.

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

38

Design Pharmacy Checkout Merchandising Around Consumer Buying Patterns

DisplayMagazinesTo ProvideInformation

AndEntertainment

OfferRelated

Remedies and

WellnessProducts

Display Candy,Gum, Mints And Snacks

for Impulse Sales

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

39

Opportunity: Design Photo Checkout Merchandising Around The Consumer

Merchandise Photo related products such as Film and Cameras

Display a variety of Batteries including photo and specialty batteries

Provide an assortment of photography and other special interest Magazines

Display Consumables (Candy, Gum, Mints, etc.) to capture impulse sales

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

40

Purchases At Photo Counters Are Limited To Related Products

1.2%

2.4%

2.9%

4.3%

14.3%

Candy Bar

Batteries

Cameras

Video/DVD/CD

Film

Observed Purchase At Photo Checkout% Shoppers

(421)

There was low presence of impulse items at Photo checkoutsSource: Drug Store Observations.

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

41

Design Photo Checkout Merchandising Around Consumer Buying Patterns

DisplaySpecialty Batteries

DisplayFilm/Cameras

Display Special Interest

Magazines

Shelves Of Candy,Gum, Mints And Snacks

for Impulse Sales

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

42

Opportunity: Drive Shopping Frequency With Key Consumables

Current frequency of store visits is dictated by prescriptions and infrequently purchased personal care

Frequency can be influenced by focus on convenience and effective in-store merchandising

Merchandising of frequently purchased items at checkout will be key to success

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

43

Key Checkout Categories Can Drive Shopping Frequency

7

21

25

27

32

Gum/Mints

Candy

Snacks

Magazines

CarbonatedBeverages

Source: A.C. Nielsen Household Panel; DHC Analysis

# Annual Purchases/Household

These are also high impulse categories that can generate incremental sales

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

44

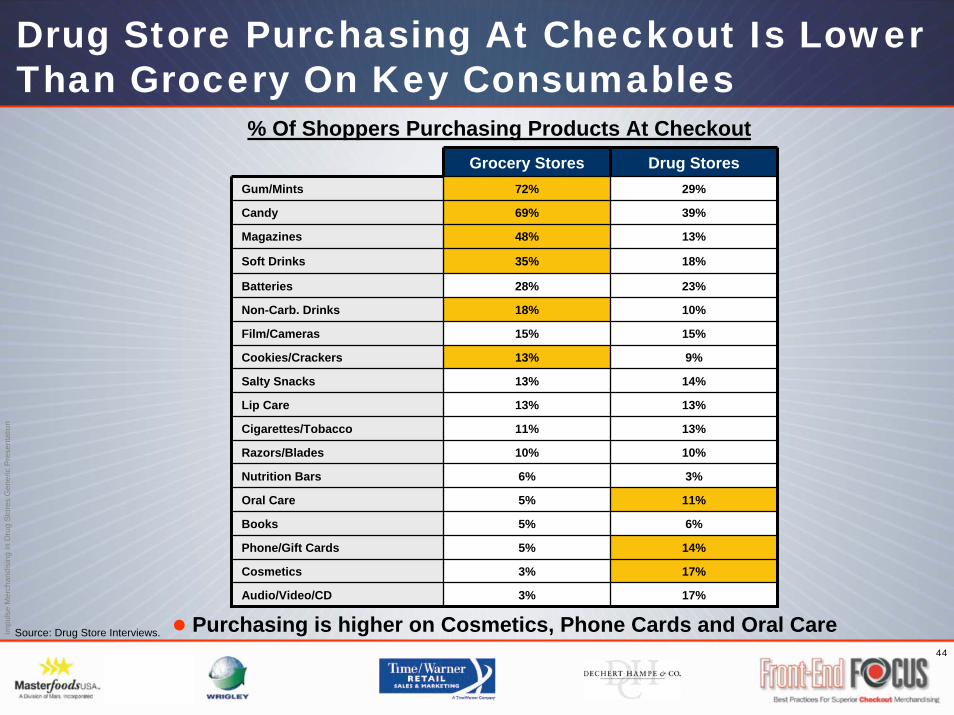

Drug Store Purchasing At Checkout Is Lower Than Grocery On Key Consumables

Source: Drug Store Interviews.

Grocery Stores Drug StoresGum/Mints 72%

69%

48%

35%

28%

18%

15%

13%

13%

13%

11%

10%

6%

5%

5%

5%

3%

3%

29%

Candy 39%

Magazines 13%

Soft Drinks 18%

Batteries 23%

Non-Carb. Drinks 10%

Film/Cameras 15%

Cookies/Crackers 9%

Salty Snacks 14%

Lip Care 13%

Cigarettes/Tobacco 13%

Razors/Blades 10%

Nutrition Bars 3%

Oral Care 11%

Books 6%

Phone/Gift Cards 14%

Cosmetics 17%

Audio/Video/CD 17%

% Of Shoppers Purchasing Products At Checkout

Purchasing is higher on Cosmetics, Phone Cards and Oral Care

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

45

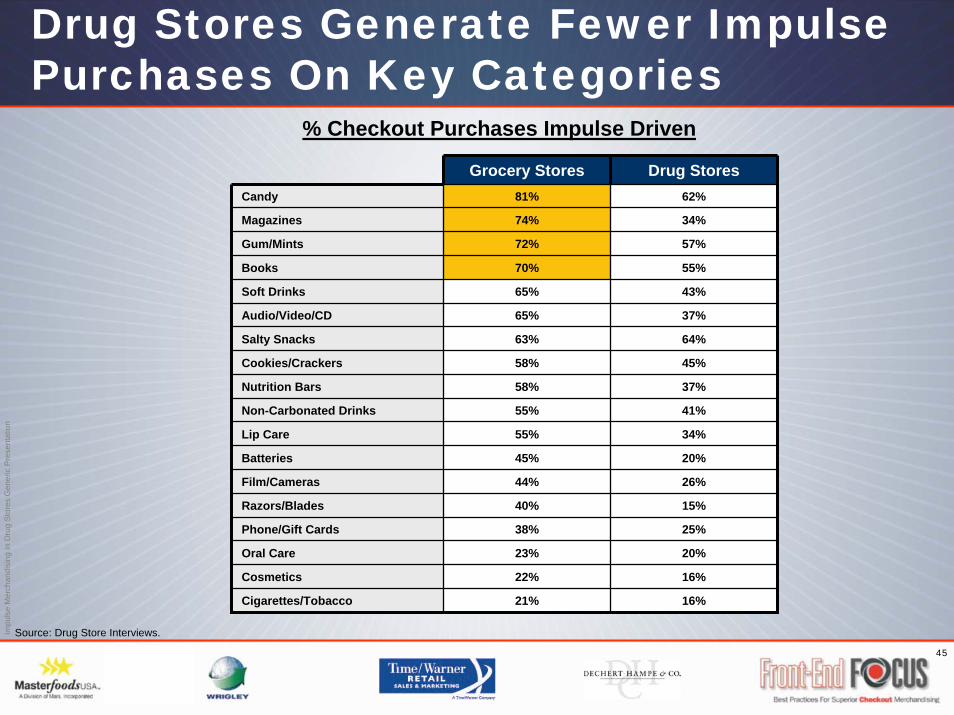

Drug Stores Generate Fewer Impulse Purchases On Key Categories

% Checkout Purchases Impulse Driven

Grocery Stores Drug StoresCandy 81%

74%

72%

70%

65%

65%

63%

58%

58%

55%

55%

45%

44%

40%

38%

23%

22%

21%

62%

Magazines 34%

Gum/Mints 57%

Books 55%

Soft Drinks 43%

Audio/Video/CD 37%

Salty Snacks 64%

Cookies/Crackers 45%

Nutrition Bars 37%

Non-Carbonated Drinks 41%

Lip Care 34%

Batteries 20%

Film/Cameras 26%

Razors/Blades 15%

Phone/Gift Cards 25%

Oral Care 20%

Cosmetics 16%

Cigarettes/Tobacco 16%

Source: Drug Store Interviews.

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

46

Summary Of Recommendations

Checkouts are the prime locations where all shoppers can be exposed to effective impulse merchandising

Incremental checkout sales are driven by a focus on items purchased broadly, frequently and on impulse

Drug stores should refocus Front-End checkout merchandising on impulse items and expand impulse merchandising at Pharmacy and Photo checkouts

Impu

lse

Mer

chan

disi

ng In

Dru

g St

ores

Gen

eric

Pre

sent

atio

n

47

Contact a representative of Masterfoods USA,

For Enhanced Impulse Merchandising

Wm. Wrigley Jr. Co., or Time/Warner Retail Sales & Marketing

Visit our Website at Front-EndFocus.com

Contact Bill Dusek or Ray Jones from Dechert-Hampe and Company at (847) 559-0490