implications of u.s. shale gas and russian pipelines on european

TRANSCRIPT

Implications of U.S. Shale Gas and Russian Pipelines on European Gas Imports

Steven A. GabrielUniversity of Maryland

Co‐authors: Seksun Moryadee , Hakob AvetisyanUniversity of Maryland

Oslo, Norway28 August 2013

Prepared for the Links Project Final Meeting

Organization of Talk

2

• Overview of WGM• A Study of Pipelines, Part of LinkS Project (Funded by the Research Council of Norway)

• No Nord Stream pipeline (Base Case)• Nord Stream pipeline only• South Stream and Southern Corridor pipelines• Nord Stream, South Stream, Southern Corridor pipelines combined with U.S. exports and shale gas in China

• Results

C3

T3

K1,2,3

C1Producer

T1Trader

K1,2,3

SectorsM1

Marketer

L1

LNG Node

S3S1

Storage R3

RegasNode

Country 1 Country 3

Transit countries

Representation of Gas Market in WGM 2012

T1 T1

M3

T1

PipelineT1

Producer Problem (Example of Market Players’ Optimization Problems)

Revenue Cost

Production Capacity

Reserve Limitation

• Producers maximize their profit• WGM distinguishes three type of producers for North America (Conventional, Shale, Unconventional)• Cost function (Golombek Cost function) differs for each producer

Golombek Cost Functionα = 10, β =40, γ = 120

5

Market Clearing Conditions

INDUSTRIAL

City GATE STATION

COMMERCIAL

RESIDENTIAL

DISTRIBUTION SySTEM

UNDERGROUND STORAGE

TRANSMISSION SySTEM

Cleaner

Compressor Station

GAS PROCESSING PLANT

GAS PRODUCTION

Gas Well

Associated Gas and Oil Well

Impurities Gaseous Products

LiquidProducts

ELECTRIC POWER LNG VESSEL

World Gas Model (WGM)

• Production/Consumption Nodes: 41 (Groupsof countries, countries, regions)

• Covers over 95% of worldwide consumption • 10 periods: 2005‐2050, calibration year 2010• Typical decision variables

– Operating levels (e.g., production, storage injection)

– Investment levels (e.g., pipeline, liquefaction capacity)

• Other– Market power aspects (traders )– LNG contracts database– Seasonality of demand: low and high demand– Environmental policy consideration: Carbon

costs for supply chains• Computational aspects

– Large‐scale complementarity problem (optimization conditions for all players + market‐clearing conditions)

– ~66,000 vars. Solves in ~95 mins (2GB, 1.2 GHz)7

Study Overview and Objectives

Overview of current situation and new infrastructure– Europe's dependence on Russian natural gas– Russian future strategies – Nord Stream pipeline– South Stream pipeline– Southern Corridor project– U.S. liquefied natural gas exports

Main questions, gauge impact of likely new production and transportation infrastructures in northern and southern Europe, specifically:

– The flows from Russia to Europe given new pipeline capacity– The utilization factor (capacity) Nord Stream, South Stream, and

Southern Corridor pipelines– The investment decisions to increase capacities after 2020 8

Europe's Dependence on Russian Natural Gas

Source: BP Statistical Review 2012

• About a quarter of European gas supplies comes from Russia, nearly all of it passes through Ukraine

• 13 countries depend on Russian gas more than 50% of their consumption

18.12.55

2.89 5.33 6.8840.54

9.28 2.62 5.66 4.91 23.527.3 30.7

3.3

15.4 8.6 2.563.95 0.3

0%10%20%30%40%50%60%70%80%90%100%

Natural Gas Imports from Russia* (BCM) and Percentage of Total Consumption in 2011

% import from Russia

9

3.6

*Number on the bar

Current Russian Situation

• The EU aims to help diversify gas‐supply routes in order to reduce the dependence on Russia of some of its member states*1

• Increase in mineral extraction taxes cost $2.2 billion more in 2011 for Gazprom*2

• LNG increases flexibility of suppliers for Europe (e.g., Qatar and Australia)

• Recent cold weather forced Russia to keep natural gas for domestic consumption

*1http://www.ecfr.eu/scorecard/2012/russia/21*2http://www.euractiv.com/energy/russias‐natural‐gas‐dilemma‐analysis‐512092

Russian Future Strategies for Natural Gas Trade

10

Russian Future Strategies

• Russia is diversifying export gas markets, focus on Asia to offset potential decline in supply to Europe*

• Russia is expanding LNG export capacity and will export more LNG to Asian markets

• Russia needs to maintain long‐term contracts• Russia is increasing flows between Russia and Europe

bypassing Ukraine

Russian Future Strategies for Natural Gas Trade

11

*http://www.prnewswire.com/news‐releases/russia‐diversifies‐gas‐export‐markets‐‐‐increasing‐focus‐on‐asia‐to‐offset‐potential‐decline‐in‐supply‐to‐europe‐168408306.html

European Natural Gas Pipeline‐Competing Projects

Source: The economist

• Four pipeline projects compete against each other (TANAP‐TAP‐TIGI‐Nabucco) to bring gas from Central Asia to Europe

• Nabucco shareholders now believe that only a smaller version of the pipeline is realistic

• Russia aims to build second Baltic sea pipeline to increase supply to Europe as well as to bypass Ukraine

12

U.S. LNG Export Status As of August, 2013

Total of all applications Approved Pending

FTA application30.62 Bcf/d

( 316.51 Bcm/y )29.93 Bcf/d

(309.38 Bcm/y)0.69 Bcf/d

( 7.13 Bcm/y)

Non‐FTA application

29.21 Bcf/d (301.93 Bcm/y)

5.6 Bcf/d ( 57.88 Bcm/y)

23.61 Bcf/d (244.0 Bcm/y)

Source: U.S. Department of Energy

FTA with the U.S. requires national treatment for trade in natural gas, including Australia, Bahrain, Canada, Chile, Colombia, Dominican Republic, El Salvador, Guatemala, Honduras, Jordan, Mexico, Morocco, Nicaragua, Oman, Peru, Republic of Korea and Singapore

http://energy.gov/sites/prod/files/2013/08/f2/Summary_of_Export_Applications.pdf

Sabine Pass Liquefaction contracts

Freeport LNG Expansion contractsCurrently, DOE approved three non FTA Export Applications:

• Sabine Pass Liquefaction (2.2 Bcf/d)• Freeport LNG Expansion (1.4 Bcf/d)• Lake Charles LLC (2 Bcf/d)

http://www.ogj.com/articles/2013/08/doe‐approves‐lake‐charles‐llc‐s‐lng‐exports‐to‐non‐fta‐countries.html

http://www.freeportlng.com/Liquefaction_Project.asp

http://phx.corporate‐ir.net/phoenix.zhtml?c=101667&p=irol‐presentations

15

U.S. Liquefied Natural Gas Exports: Market Estimation

Source: Cheniere Research estimates

U.S Exports Case (DOE Case): What If the U.S. Exports LNG 99 BCM/y to Asia and Europe?

16

West coast terminal

Gulf coast terminal

East coast terminal

2,900*

2,800*

5,100*

3,800*

5,600*

8,600*

24 BCM/y

24 BCM/y

27 BCM/y

24 BCM/y

*Distance in nautical miles

SOURCE: EIA 2011

UK

Spain

India

South Korea

WGM Cases and Assumptions

Cases and Descriptions (as part of Links Study funded by Research Council of Norway)

Cases Abbreviation Descriptions

Base BaseBase Case without Nord Stream, South Stream nor Southern Corridor pipelines

Nordstream Nord Only Nord Stream pipeline available

All pipelines available All

Nord Stream, South Stream, and Southern Corridor pipelines available

Russian pipelines vs.U.S. LNG export Low_Shale_DOE_Export_All

Low Chinese shale gas production along with exports from U.S. plus all

Russian pipelines18

Base Case

NordOnly

All

Low_Shale_DOE_All

Nord Stream Case and Model Assumptions

Nord Stream Pipeline

• Nord Stream is built in 2010• Capacity reaches 151 mcm/d or 55

BCM/y in 2015 • Pipeline connects N_RUW (Russia west

node) and N_GER (Germany)• 20% of initial capacity is considered for

pipeline expansion (investment decision) every five years if necessary

• Only Russian trader can access this pipeline

19

Source:http://www.energia.gr/article_en.asp?art_id=26120

South Stream and Southern Corridor Case and Model Assumptions

South Stream Pipeline

• Build South Stream in 2010 ( 15.75 BCM/y)• Connect N_RUW (Russian West) and N_ROM

(Romanian node)• Potentially start operating in 2015 with 15.75

BCM/y• Potentially add more capacity, (47.25 BCM/y) in

2015• Potentially operate at full capacity (63 BCM/y)

starting 2020• Consider maximum pipeline expansion (20 % of

initial capacity) if necessary

N_RUW

N_ROM

201515.75BCM/Y

202063.0 BCM/Y

20

Southern Corridor

• Build two new Pipelines: – 1. Trans‐Anatolian gas pipeline project (TANAP* ) connects

N_TRK (Turkish Node) and N_KZK (Kazakhstan ‐Azerbaijan aggregated in this node) with capacity 16 BCM/y in 2015

– 2. Nabucco West connects N_TRK (Turkish Node) and N_ROM (Romania ‐Bulgaria and Greece aggregated in this node) with capacity 10 BCM/y in 2015

• Potentially start operating at full capacity in 2020• Consider maximum pipeline expansion 20% of initial

capacity (3.2 BCM and 2.0 BCM every five years respectively)

South Stream and Southern Corridor Case and Model Assumptions (cont’d)

Source:http://www.neurope.eu/article/Turkish‐president‐ratifies‐tanap‐agreement

N_TRK N_KZKN_ROM

Southern Corridor Project

TANAP16 BCM/Y16 BCM/Y10 BCM/Y10 BCM/Y

Nabucco West

21

U.S. Gas Exports vs. Russian Pipelines

All pipelines combined with U.S. Exports

• Nord Stream, South Stream, and Southern Corridor Pipelines available

• U.S. LNG exports already approved and under contract + pending DOE approval to Asia and Europe(March,2012)

• 24 BCM/y to India• 24 BCM/y to South Korea• 27 BCM/y to UK• 24 BCM/y to Spain

• Low level of Chinese shale gas production• Shipping Cost = $8/KCM/1,000 nautical miles

22

Base 21 BCM

DOE 99 BCM

Observed Model Outcomes for Russian Flows

23

Only Nord Stream Available Flows at the maximum capacity of Nord Stream

All Pipelines Available Decreasing flow from Russia to Europe via Nord Stream

U.S. dominates in LNG markets

Russia loses in LNG market, so it increases flows in all

pipelines

Regional Prices

2,77

8,03

9,78

10,61

5,15

11,75

3,80

8,60 8,67

2,71

7,77

9,7210,19

5,10

11,44

3,74

9,23 8,98

0

2

4

6

8

10

12

14

16

18

AFRICA ASPACIF CHINA EUROPE FRSVTUN JAPAN MIDEAST NRTH_AM STH_AM

Prices for 2030 in $/MMBTU

Base

Nordonly

All

Low_Shale_Low_Export_allpipe

24

‐ North America increases significantly under export case ‐ European prices drop about 30‐50 cents/MMBTU

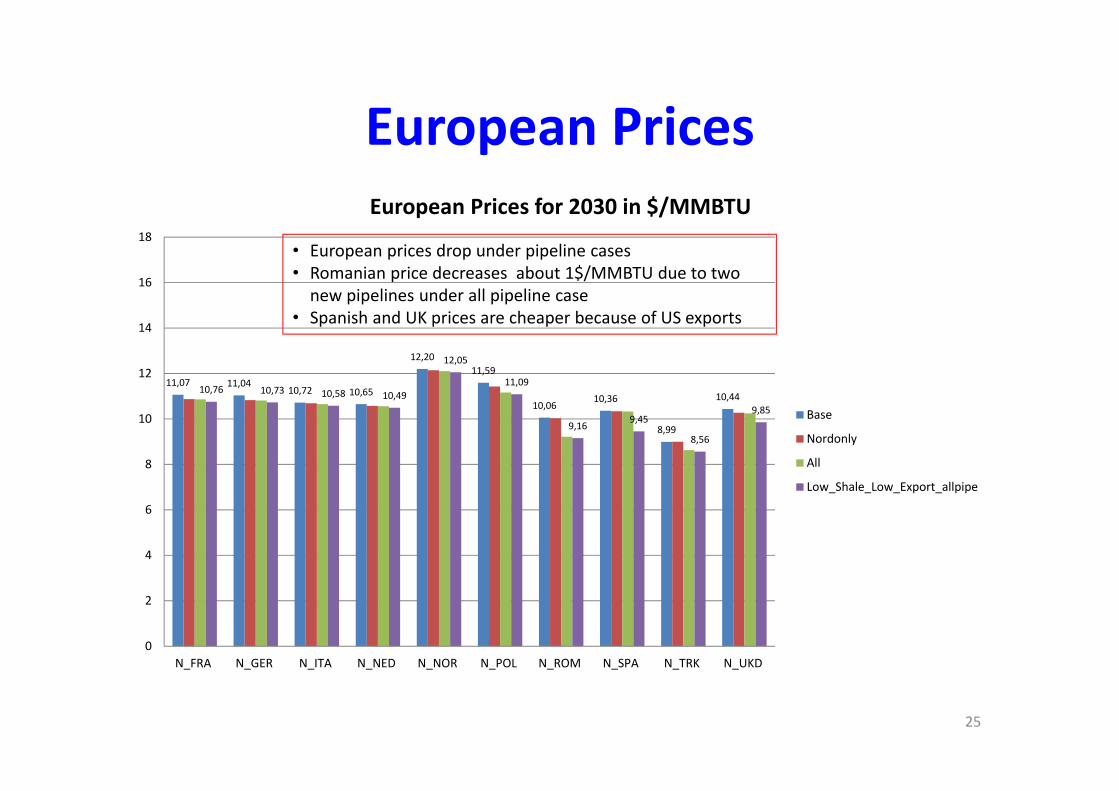

European Prices

11,07 11,0410,72 10,65

12,2011,59

10,0610,36

8,99

10,4410,76 10,73 10,58 10,49

12,05

11,09

9,169,45

8,56

9,85

0

2

4

6

8

10

12

14

16

18

N_FRA N_GER N_ITA N_NED N_NOR N_POL N_ROM N_SPA N_TRK N_UKD

European Prices for 2030 in $/MMBTU

Base

Nordonly

All

Low_Shale_Low_Export_allpipe

• European prices drop under pipeline cases• Romanian price decreases about 1$/MMBTU due to two new pipelines under all pipeline case

• Spanish and UK prices are cheaper because of US exports

25

Impact of Increased U.S. LNG Exports: UK

26

Total LNG transported to UK (BCM/Y) in 2030 ( BCM/y)Base NordOnly All Low_Shale_DOE_Export_allpipe

T_ALG 12.63 13.23 13.21 8.74T_NIG 7.11 7.80 7.76 3.13T_RUS 6.12 1.32 1.58 0.00T_USA 7.50 7.50 7.50 26.12Total 33.35 29.85 30.05 37.99

Natural Gas Transported by Pipeline to UK in 2030 (BCM/y)

Base Nordonly All Low_Shale_Low_Export_allpipeT_NED 9.39 9.38 9.46 6.89T_NOR 28.3 27.64 27.76 25.47T_RUS 3.32 8.11 8.27 7.24Total 41.01 45.13 45.49 39.6

Base All Nordonly Low_Shale_Low_Export_allpipeUK consumption 90.39 91.42 91.25 93.48Domestic production 16.74 16.74 16.74 16.72Total imported by pipeline 41.01 45.49 45.13 39.6Total imported by LNG 33.35 29.85 30.05 37.99Total Supply 91.10 92.08 91.92 94.31

• U.S. gas exports (26 BCM) replace existing LNG under US export case

• Under U.S. gas exports UK imports less by pipelines compared to other cases

Dynamic Change in Markets

27

RUW Flows by Pipeline in 2045 BCM/y

RUW Flows by LNG in 2045 BCM/y

Note:Production capacity for N_RUW is set to 1700 MCM/d from 2035‐2050

U.S. LNG reduces Russian LNG in Europe

Russia loses European market share in LNG market

Therefore, Russia increases flows~1BCM by pipelines under Export case

Base: U.S. export7.49 BCM to UK4.60 BCM to SpainExport Case:26.11 BCM to UK22 .89 BCM to Spain

Base Nordonly All Low_Shale_DOE_Export_allpipeR_CAE 0 0 0 1.88R_FRA 3.03 0 0 0R_NED 3.21 0 0 0R_SPA 4.91 5.29 5.31 2.81R_UKD 8.98 2.85 2.58 0.36Total 20.14 8.14 7.89 5.07

Base Nordonly All Low_Shale_DOE_Export_allpipe

N_GER 0 111.77 109.17 109.53

N_KZK 12.22 12.22 12.22 12.22

N_POL 67.21 28.62 26.48 26.42

N_ROM 0 0 24.26 24.41

N_RUE 0 0 0 0

N_TRK 31 30.2 28.88 28.59

N_UKR 138.87 102.29 82.39 83

Total Pipeline Export 249.31 285.12 283.41 284.2

Base CaseEuropean Flows in 2030 (BCM/y)Wholesale Nodal Prices

N_RUW

N_GER

N_UKR

N_POL

N_ROM

N_TRK

N_KZK

N_FRA

N_NOR

N_UKD

N_SPA

16857

88.46

62.6

21.87

16.3

N_ITA

31.14

3.32

2.8

20.88

42.3

7.8

28.2

6.1

4.44

0

24.4

$11.04

$11.07

$10.72

$12.20

$11.59

$10.06

$8.99

$10.44

$10.36$3.47

$9.16

$3.30

28Sabine Pass level

4.65

7.49

$7.05*

• The prices shown here are trader selling prices (wholesale price)• At Norway, price (producer trader) is $4.50 /MMBTU

*This price does not include transportation cost

Base CaseSample Summarized Structure of Norwegian Natural Gas Market

29

20.88

42.3

7.8

28.2

N_GER$11.04

N_FRA$11.07

T_NORN_POL

$11.59

N_UKD$10.44

N_NOR

P_NOR

$12.20

$5.53*

• Decision to sell to domestic market or export made by the trader• Trader decides to export to other nodes when it is profitable• Existing traders at consuming node can insert market power and compete with other traders

*Producer selling price

Base Case

30

4.65 BCM

N_GER$10.36

T_USA

N_UKD$10.44

N_US7

P_US7

$7.05

$7.05*

*Producer selling price

7.49 BCM

• It is assumed that U.S. market is in perfect competition in WGM• U.S. exports to Europe from Gulf coast under contracts

Sample Summarized Structure of the U.S Natural Gas Export Market

European Flows in 2030 (BCM/y)Wholesale Nodal Prices

N_RUW

N_GER

N_UKR

N_POL

N_ROM

N_TRK

N_KZK

N_FRA

N_NOR

N_UKD

N_SPA

116

32

16.9

13.53

21.75

22.25

N_ITA

33.29

8.1

2.8

21.0242.3

7.6

27.6

6.1

84.79

NordOnly

4.6

0

24.4

$10.82

$10.87

$10.69

$12.14

$11.4

$10.03

$8.99

$10.27

$10.33$3.52

$9.15

$3.28

• Less Russian flows through N_UKR and N_POL (less than 30% of Base Case)• Prices in $/MMBTU, prices mostly decrease compared to the Base Case

(Turkey stays the same, Kazakhstan slightly increases)• U.S. gas stays only in UK or Spain (no flow out of UK and Spain)

31Sabine Pass level

4.65

7.49

$7.12*

*This price does not include transportation cost

European Flows in 2030 (BCM/y)Wholesale Nodal Prices

N_RUWN_RUW

N_GERN_GER

N_UKRN_UKR

N_POLN_POL

N_ROMN_ROM

N_TRKN_TRK

N_KZKN_KZK

N_FRAN_FRA

N_NORN_NOR

N_UKDN_UKD

N_SPAN_SPA

93.3

29.7

16.4

13.01

0

22.56

N_ITA

33.93

7.96

8.2

2.803

21.04

42

7

27.77

17.10

84.7

24.2

All

3.43

4

23.8

$10.81

$10.86

$10.65

$12.10

$11.16

$9.21

$8.62

$10.24

$10.33

$3.55

$9.16

$3.27

32

• Europe get more supply from central Asia• Flow between N_UKR to N_ROM equal to 0• N_ROM exports 4 BCM to N_POL • 5 additional BCM flow from N_FRA to N_UKDSabine Pass level

4.65

7.49

$7.23* *This price does not include transportation cost

European Flows in 2030 (BCM/y)Wholesale Nodal Prices

N_RUWN_RUW

N_GERN_GER

N_UKRN_UKR

N_POLN_POL

N_ROMN_ROM

N_TRKN_TRK

N_KZKN_KZK

N_FRAN_FRA

N_NORN_NOR

N_UKDN_UKD

N_SPAN_SPA

92.9

29.7

15.4

12.08

0

21.36

N_ITA

35.13

7.89

7.2

2.803

21.25

42.3

6.9

25.4

17.9

84.7

24.43.49

4

23.7

Low_Shale_DOE_All

$10.72

$10.75

$10.58

$12.05

$11.08

$9.15

$8.56

$9.85

$9.45$3.48

$9.09

$3.21

33

• Less supply from N_NOR and N_FRA sends to N_UKD due to U.S. LNG

DOE Level

$8.85 *This price does not include transportation cost

Conclusions and Findings:

• Nord Stream and South Stream pipelines reduce the flows through Poland and Ukraine (30% for NordStream case and 45% of All pipelines case)

• Nord Stream pipeline capacity is favorable and expanded almost all time periods for all cases, therefore the total capacity reaches more than 100 BCM/y in 2050

• South Stream pipeline capacity is not expanded as much due to Southern Corridor project and flow capacity

• Average European gas price drops 25 cents/MMBTU for NordStreamOnly Case and 40 cents/MMBTU for all pipelines case relative to Base Case

• U.S. gas exports do not significantly affect to Russia’s flows but reduce natural gas prices in importing countries (UK and Spain)

34

Conclusions and Findings:

• Southern Corridor project is preferable for pipeline operator more than South Stream due to lower investment cost (onshore vs. offshore)

• N_GER is considered to be a main hub which distributes gas to Europe when Nord Stream is available

35

Extra Slides

36

Interesting Game Theory Counterflow Effect: Test Results from WGM

37

Counterflow under Allpipe Case

Assumptions: • Market power causes counterflows among nodes • We focus on only cycle of flows among N_GER‐N_ROM‐N_POL

• Market power level of existing traders at Poland is considered in this test

Three tests on WGM• Base Case, we use for reference• Test 1, market power is set to be zero for all existing traders

• Test 2, market power is set to be 0.5 for all traders• Test 3, market power is set to be 0.75 for all traders

Level of market power

Trader Base Test Test 1 Test 2 Test 3T_ALG 0.75 0 0.5 0.75T_NIG 0.75 0 0.5 0.75T_AUS 0.75 0 0.5 0.75T_RUS 0.75 0 0.5 0.75T_KZK 0.5 0 0.5 0.75T_NED 0.5 0 0.5 0.75T_NOR 0.75 0 0.5 0.75T_QAT 0.75 0 0.5 0.75T_YAM 0.75 0 0.5 0.75T_TRI 0.75 0 0.5 0.75

38

Counterflow Effect: Test Results from WGM

Counterflow Test 1 (market power for existing traders in Poland=0)

N_POL]

N_GER

N_ROM

14.2

3.09

0

$10.97

$5.91

$9.31

N_POL]

N_GER

N_ROM

20.28

3.63

2.21

$10.90

$10.75

$9.32

N_POL]

N_GER

N_ROM

22.5

3.63

5.73

$10.93

$12.2

$9.36

Counterflow Test 2 (market power for existing traders in Poland = 0.5)

Counterflow Test 3 (market power for existing traders in Poland = 0.75)

Trader Problem

Revenue

Transport Cost

Storage Cost

Natural Gas Cost

Contractual obligations

Storage Cycle Con

Loss

Trader• Buys gas from producer• Exerts market power• Controls usage of storage• Responsible for regulated and congestion fee

Storage Operator Problem

Revenue

Expansion cost

Injection Capacity

Extraction Capacity

Working Gas Capacity

Maximum ExpansionStorage Operator• Provides an economic mechanism to efficiently allocate storage capacity to traders• Maximizes the discounted profit resulting from selling injection capacity and extraction capacity to traders

Transmission System Operator Problem

Revenue Expansion Cost

Arc Capacity

Maximum Expansion

Transmission System Operator (TSO)• Provides an economic mechanism to efficiently allocate transport capacity to traders• Maximizes the discounted profit resulting from arc capacity to traders minus investment cost from expansion• Congestion fees “Tau” come from market clearing condition between TSO and traders

Net Imports and Exports

‐278,2

‐26,29

198,73

429,91

‐393,52

124,37

‐179,11

‐36,6

11,01

‐271,5

‐22,02

201,38

447,87

‐383,23

126,64

‐168,01

‐86,75

2,4

‐600

‐400

‐200

0

200

400

600

AFRICA ASPACIF CHINA EUROPE FRSVTUN JAPAN MIDEAST NRTH_AM STH_AM

Net Imports(+) and Exports(+) in 2030 BCM/y

Base

Nordonly

All

Low_Shale_Low_Export_allpipe

42

‐ North America displaces other natural gas exporters under export case ‐ European imports more gas for all cases compared to Base Case

Country Nodes for Europe In WGM

43

Node Country RegionGER Austria EuropeGER Czech Republic EuropeGER Denmark EuropeGER Germany EuropeGER Switzerland EuropePOL Baltic Region EuropePOL Finland EuropePOL Poland EuropePOL Sweden EuropePOL Slovak Republic Europe

FRABelgium and Luxembourg Europe

FRA France EuropeROM Bulgaria EuropeROM Greece EuropeROM Hungary EuropeROM Romania EuropeUKD Iceland EuropeUKD United Kingdom EuropeITA Italy EuropeITA Slovenia EuropeSPA Spain EuropeSPA Portugal EuropeNED Netherlands EuropeNOR Norway EuropeTRK Turkey Europe

PolandPolandNorwayNorway

TurkeyTurkey

FranceFrance

SpainSpain

UKUK

Germany

Germany

RomaniaRomania

ItalyItaly

NetherlandsNetherlands

WGM has 10 country nodes aggregated in Europe

Map source:http://www.yourchildlearns.com/online‐atlas/europe‐map.htm

44

Country Node for FRSVTUN In WGM

Node Country RegionKZK Armenia FRSVTUNKZK Azerbaijan FRSVTUNKZK Georgia FRSVTUNKZK Kazakhstan FRSVTUNKZK Turkmenistan FRSVTUNKZK Uzbekistan FRSVTUNUKR Belarus FRSVTUNUKR Ukraine FRSVTUNRUE Russia East FRSVTUNRUL Russia Sakhalin FRSVTUNRUW Russia West FRSVTUN

UkraineUkraine Russia WestRussia West

KazakhstanKazakhstan

Source:http://www.uga.edu/gm/602/FeatProtecting.html

Russia SakhalinRussia Sakhalin

South Stream Flows

15,79

21,16

23,0524,26 24,26 23,73 24,26 24,26

15,79

21,24

23,2224,42 24,42 23,90 24,42 24,42

0

5

10

15

20

25

30

2015 2020 2025 2030 2035 2040 2045 2050

Flows between N_RUWN_ROM BCM/y

All

Low_Shale_Low_Export_allpipe

45Flows through pipeline increase in small amount when the U.S. exports more gas to Europe

Nord Stream Utilization Factors in Term of Percentage

46

Nordonly All Low_Shale_Low_Export_allpipe

Year Capacity* Flows* %Utilization Capacity* Flows* %Utilization Capacity* Flows* %Utilization

2015 55.25 53.26 96.40% 55.25 53.26 96.40% 55.25 53.26 96.40%

2020 66.20 63.77 96.33% 66.20 63.77 96.33% 66.20 63.77 96.33%2025 77.15 74.28 96.28% 77.15 74.28 96.28% 77.15 74.28 96.28%

2030 88.10 84.80 96.25% 88.10 84.80 96.25% 88.10 84.80 96.25%

2035 99.05 95.31 96.22% 99.05 95.31 96.22% 99.05 95.31 96.22%

2040 110.00 105.82 96.20% 110.00 105.82 96.20% 110.00 105.82 96.20%

2045 116.21 111.78 96.19% 113.49 109.18 96.19% 113.86 109.53 96.19%

2050 116.07 111.78 96.30% 113.36 109.18 96.31% 113.73 109.53 96.30%

*BCM/y

European Net Imports and Exports

71,39

113,88

101,07

‐8,16

‐119,51

44,6934,99

43,62

74,25 73,6972,16

115,62

101,72

‐7,81

‐115,84

45,6237,05

45,69

76,84 76,82

‐150

‐100

‐50

0

50

100

150

N_FRA N_GER N_ITA N_NED N_NOR N_POL N_ROM N_SPA N_TRK N_UKD

European Imports(+) and Exports(‐) in 2030 BCM/y

Base

Nordonly

All

Low_Shale_Low_Export_allpipe

• New pipelines bring more supply from Russia to Europe but they affect other producers

• For those countries new pipelines go through, imports increase

47

Regional Level Results

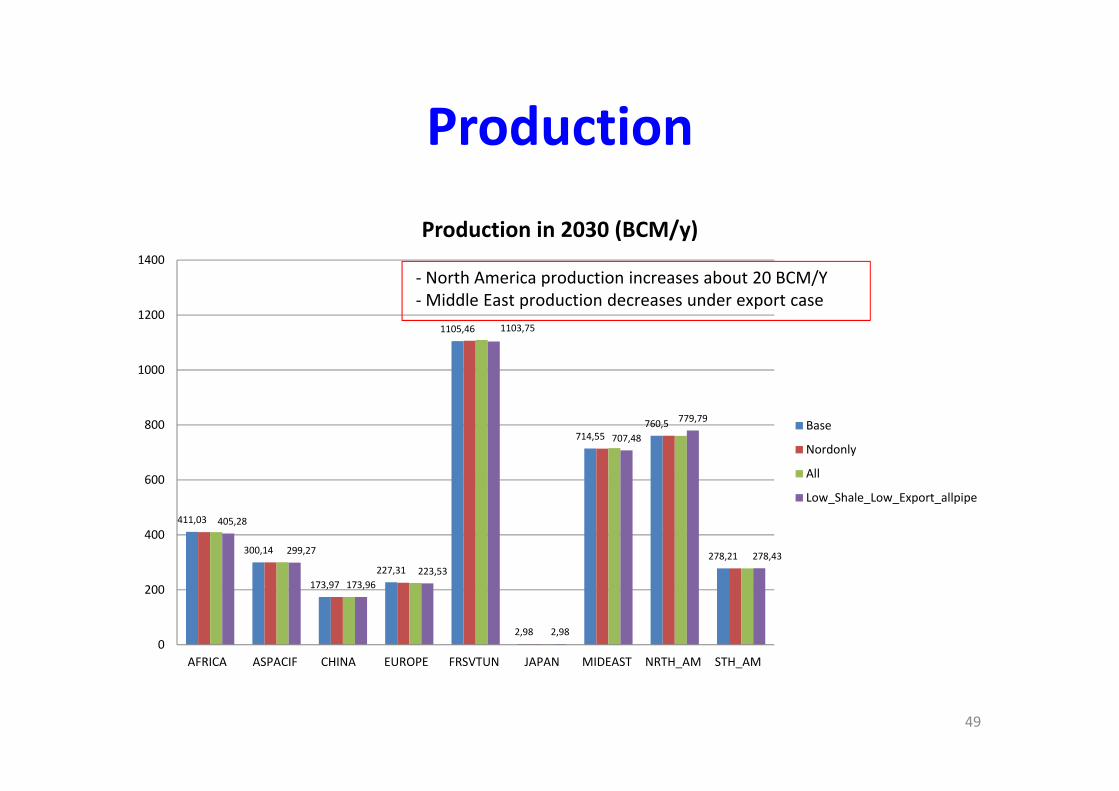

Production

411,03

300,14

173,97227,31

1105,46

2,98

714,55760,5

278,21

405,28

299,27

173,96223,53

1103,75

2,98

707,48

779,79

278,43

0

200

400

600

800

1000

1200

1400

AFRICA ASPACIF CHINA EUROPE FRSVTUN JAPAN MIDEAST NRTH_AM STH_AM

Production in 2030 (BCM/y)

Base

Nordonly

All

Low_Shale_Low_Export_allpipe

‐ North America production increases about 20 BCM/Y‐Middle East production decreases under export case

49

Consumption

132,83

273,85

372,7

656,59

701,39

127,3

535,45

723,47

289,22

133,78

277,25

375,34

670,6712

129,56

539,48

692,58

280,84

0

100

200

300

400

500

600

700

800

AFRICA ASPACIF CHINA EUROPE FRSVTUN JAPAN MIDEAST NRTH_AM STH_AM

Consumption in 2030 BCM/Y

Base

Nordonly

All

Low_Shale_Low_Export_allpipe

50

‐ North America consumption decreases 70 BCM/y under export case ‐ European consumption increases about 3‐5 BCM

Pipeline Capacity Expansion

0 2 4 6 8 10 12

All

Low_Shale_Low_Export_allpipe

7,39

7,78

1,50

1,43

2,17

2,76

TANAP Capacity in BCM/y

2020

2025

2030

51• Total capacity expansion of this pipeline (decision variable in the

model ) is about 10 BCM/y compared to actual capacity (16 BCM/y)

Southern Corridor Flows

6,18 6,18 6,18 6,18 6,18 6,18 6,18 6,186,37

13,92

15,31

17,98 17,98 17,98 17,98 17,98

0

2

4

6

8

10

12

14

16

18

20

2015 2020 2025 2030 2035 2040 2045 2050

Flows between N_KZKN_TRK BCM/y

Base

Nordonly

All

Low_Shale_Low_Export_allpipe

52• Flows reach maximum capacity after 2030• This implies that more natural gas flows from central Asia to Europe

Pipeline Capacity Expansion

0 2 4 6 8 10 12

All

Low_Shale_Low_Export_allpipe

5,3436

5,21585

1,971

1,971

0,97455

1,13515

1,971

1,971

N_TRK and N_ROM Pipeline Capacity Expansion BCM/y

2020

2025

2030

2035

2040

2045

53

•This pipeline competes with South Stream•It is expanded for almost all time period due to cheaper costs (onshore pipeline)

Southern Corridor Flows

5,01

6,90

7,998,27

8,55

10,44 10,66

0

2

4

6

8

10

12

2020 2025 2030 2035 2040 2045 2050

Flows between N_TRK and T_ROM in BCM/y

Base

Nordonly

All

Low_Shale_Low_Export_allpipe

54

• This pipeline competes with South Stream by sending gas to N_ROM• U.S. exports do not affect the flows to N_ROM because there is no connection

from N_UKD and N_SPA to N_ROM

Pipeline Capacity Expansion

0 5 10 15 20 25

All

Low_Shale_Low_Export_allpipe

15,75

15,75

5,48

5,56

1,93

2,01

1,23

1,22

0,08

0,18

South Stream Capacity in BCM/y

2015

2020

2025

2030

2035

55

South Stream is not expanded as much due to the following reasons:1. this pipeline competes with southern corridor project 2. In our model there is only one pipeline flow out from N_ROM and small capacity 3. South Stream has higher investment cost (offshore pipeline) compared to Southern Corridor project

South Stream Utilization Factors in Term of Percentage

56

All Low_Shale_Low_Export_allpipe

Year Capacity* Flows* %Utilization Capacity* Flows* %Utilization

2015 16.15 15.79 97.78% 16.15 15.79 97.78%

2020 21.63 21.16 97.84% 21.71 21.24 97.83%

2025 23.56 23.05 97.85% 23.73 23.22 97.85%

2030 24.79 24.26 97.87% 24.95 24.42 97.86%

2035 24.87 24.26 97.54% 25.13 24.42 97.18%

2040 24.83 23.73 95.56% 25.09 23.90 95.27%

2045 24.83 24.26 97.69% 25.09 24.42 97.34%

2050 24.83 24.26 97.69% 25.09 24.42 97.34%

*BCM/y

57

Nordonly All Low_Shale_Low_Export_allpipe

Year Capacity* Flows* %Utilization Capacity* Flows* %Utilization Capacity* Flows* %Utilization2015 6.5758 6.18 93.91% 6.57 6.37 97.00% 6.57 6.37 97.00%2020 6.5758 6.18 93.91% 13.96 13.54 97.01% 14.35 13.92 96.99%2025 6.5758 6.18 93.91% 15.46 15.00 97.02% 15.78 15.31 96.99%2030 6.5758 6.18 93.91% 17.63 17.10 97.01% 18.54 17.98 97.00%2035 6.5758 6.18 93.91% 17.63 17.10 97.01% 18.54 17.98 97.00%2040 6.5758 6.18 93.91% 17.63 17.10 97.01% 18.54 17.98 97.00%2045 6.5758 6.18 93.91% 17.63 17.10 97.01% 18.54 17.98 97.00%

2050 6.5758 6.18 93.91% 17.63 17.10 97.01% 18.54 17.98 97.00%

Southern Corridor Utilization Factors in Term of Percentage

*BCM/y

Southern Corridor Utilization Factors in Term of Percentage (N_TRK‐N_ROM)

58

All Low_Shale_Low_Export_allpipe

Year Capacity* Flows* %Utilization Capacity* Flows* %Utilization

2020 5.34 5.14 96.10% 5.22 5.01 96.08%

2025 7.31 7.03 96.05% 7.19 6.90 96.03%

2030 8.29 7.96 96.08% 8.32 7.99 96.00%

2035 8.60 8.26 96.09% 8.61 8.27 96.01%

2040 8.92 8.57 96.07% 8.90 8.55 96.02%

2045 10.90 10.46 96.04% 10.87 10.44 96.00%

2050 11.07 10.63 96.04% 11.10 10.66 96.02%

*BCM/y

European Production

59

Production in Norway declines due to new pipelines and US exports

14,898,94

49,47

120,48

2,98

12,25

1,48

16,7414,898,94

49,4

116,83

2,98

12,22

1,47

16,72

0

20

40

60

80

100

120

140

N_GER N_ITA N_NED N_NOR N_POL N_ROM N_TRK N_UKD

European Production in 2030 BCM/y

Base

Nordonly

All

Low_Shale_Low_Export_allpipe

European Consumption

71,42

128,58

109,89

41,29

0,98

47,61 47,1443,61

75,68

90,39

72,18

130,27

110,52

41,56

0,98

48,5249,14

45,7

78,25

93,48

0

20

40

60

80

100

120

140

160

N_FRA N_GER N_ITA N_NED N_NOR N_POL N_ROM N_SPA N_TRK N_UKD

European Consumption in 2030 BCM/y

Base

Nordonly

All

Low_Shale_Low_Export_allpipe

Most European countries increase their consumption (cases left to right)

60

Production Cost Function

61

Producers

Production cost parameters Maximum production mcm/d 2030 Producer prices ($/MMBTU)

2030 Wholesale prices

($/MMBTU)lin mmQ mmG 2010 2015 2020

Norway 35 50 80 278 343 403 5.53 12.20

Germany 50 60 80 69 57 48 10.89 11.04

UK 50 60 80 182 87 69 10.13 10.44

Poland 50 60 80 9 9 8 11.18 11.59

• At Norway, price (producer trader) is $5.53 /MMBTU

Production Cost Parameters, Maximum Production (MCM/d), and Prices ($/MMBTU)

62

Findings:

• In the perfect competition case (market power =0), flow from N_ROM to N_POL reduces to 0 and no counterflow• In the imperfect competition case (test 2 and 3), the flow from Romania to Poland increases corresponding to level of market power• The greater the level of market power the trader has, the greater the flow

Counterflow Effect: Test Results from WGM

Case Flow from Romania to Poland (BCM/y)Base test 4Test 1 0Test 2 2.21Test 3 5.37

Nord Stream Pipeline

Technical Information• 1,224 km long• 2 pipeline string (27.5 BCM each)

• 55 BCM/y full capacity• Pipeline connects Vyborg,

Russia and Lubmin, Germany through the Baltic Sea

• Gas source: the Yuzhno‐Russkoye field

Month /Year Description April, 2010 Project started June, 2011 Line 1 completed (27.5 BCM/Y) November, 2011 Started transporting gas for line 1 May, 2011 Started construction line 2 (27.5 BCM/Y) April, 2012 Line 2 completed, total capacity is (55BCM/Y) October, 2012 Implement full capacity of pipeline (55 BCM/Y)

Project TimelineSource: http://www.gazprom.com/f/posts/34/784591/nord‐stream_1_eng.jpg

Vyborg

Lubmin

63

South Stream Pipeline

Technical Information• 900 km long• 4 parallel pipelines (15.75 BCM/each)• 63 BCM/y –full capacity• Pipeline connects Anapa, Russia and Varna, Bulgaria through the Black Sea

Project Timeline

Source: http://www.naturalgaseurope.com/the‐south‐stream‐offshore‐pipeline

Year Descriptions2015 Start of Commercial Operation2016 15.57 BCM2017 31.50 BCM2018 47.25 BCM2019 63.00 BCM

Anapa

Varna

64

Southern Corridor Project

Technical Information

• This project will bring 16 BCM/y of natural gas from Shah Deniz 2 in Azerbaijan to Turkey

• 10 BCM/y will pass through Europe from Turkey to Bulgaria or Romania, and Turkey will retain 6 additional BCM/y

• Southern Corridor is expected to operate in 2018

• The Southern Gas Corridor is an initiative of the European Commission for gas supply from Caspian and Middle East to Europe

• Trans‐Anatolian gas pipeline project (TANAP) and Nabucco West were announced to bring gas to Europe on June 28,2012

Source:http://www.naturalgaseurope.com/bp‐socar‐duo‐coup‐de‐grace‐to‐nabucco

65

Applications

67

U.S. Liquefied Natural Gas Exports: Opportunity to Export

Project Timeline Implemented in WGM

2010 Nord stream capacity = 0Start building pipeline =55 BCM/y

2015Nord stream capacity available = 55 BCM/y

2015‐2050 Investment decisions considered, additional capacity 11BCM/y every five years

2010 Nord stream capacity = 0Start building pipeline =55 BCM/y

2015Nord stream capacity available = 55 BCM/y

2015‐2050 Investment decisions considered, additional capacity 11BCM/y every five years

2010South stream capacity = 0Start building pipeline =15.75 BCM/y)

2015South stream capacity available = 15.75BCM/yAdditional 47.25 BCM is started

2020South Stream =63 BCM/y

2020‐2050Consider 11 BCM/y for maximum expansion every five years

2010Southern Corridor capacity = 0

2015Start building 2 pipelines

Line1 N_KZK‐N_TRK = 16 BCM/yLine2 N_TRK‐N_ROM =6 BCM/y

2020Line1 N_KZK‐N_TRK = 16 BCM/yLine2 N_TRK‐N_ROM =10BCM/y

2020‐2050Consider investment decisions, max pipeline expansion 20% of initial capacity for each line every 5 years

Nord Stream Pipeline Case Legend:

South Stream and Southern Corridor Pipelines Case

Start Project Available Capacity Investment decisions

68

WGM Preliminary Resultshttp://www.smi‐online.co.uk/energy/uk/supply‐chain‐management‐in‐oil‐gas

Source:http://logisticszone.blogspot.com/2010_08_01_archive.html

Pipeline Capacity Expansion

0 20 40 60 80 100 120

Nordonly

All

Low_Shale_Low_Export_allpipe

55,12

55,12

55,12

10,95

10,95

10,95

10,95

10,95

10,95

10,95

10,95

10,95

10,95

10,95

10,95

10,95

10,95

10,95

6,21

3,49

3,87

Nord Stream Capacity in BCM/y

2015

2020

2025

2030

2035

2040

2045

70

• Nord Stream is expanded at maximum capacity expansion from 2020 to 2040• N_GER is treated as new hub of gas for Russia

Nord Stream Capacity Flows

53,26

63,77

74,28

84,80

95,31

105,82

111,78 111,78

53,26

63,77

74,28

84,80

95,31

105,82109,53 109,53

0

20

40

60

80

100

120

2015 2020 2025 2030 2035 2040 2045 2050

Flows between N_RUW N_GER in BCM/y

Nordonly

All

Low_Shale_Low_Export_allpipe

71

• Flows through Nord Stream drops after 2040 under All case due to Southern Corridor project + South stream pipeline, and production level reach maximum production

Selected Russian Flows in 2030 (BCM/Y)

0

167 116 93.392.9NordStream

SouthStream

24.2 24.4

84.784.7

84.7

325729.729.7

0

N_GER

N_ROM

N_UKR

N_POL

N_RUW

72

• New pipelines provide flexibility to Russian delivery gas to Europe

• Russian production level does not significantly increase but flow patterns change greatly

Selected Russian Flows in 2050 (BCM/Y)

0

132 102 82 83.7Nord Stream

South Stream

24.222.4

109112

109.5

28702625.8

0

N_GER

N_ROM

N_UKR

N_POL

N_RUW

73

• The impact of new pipelines is becoming more pronounced in terms of flow bypassing Ukraine and Poland

U.S. LNG Export Status As of April, 2013

Total of all applications Approved Pending

FTA application29.9 Bcf/d

(309.3 Bcm/y )26.1 Bcf/d

(269.7 Bcm/y)3.7 Bcf/d

(38.2 Bcm/y)

Non‐FTA application

28.5 Bcf/d (294.5 Bcm/y)

2.2 Bcf/d (23.44 Bcm/y)

26.2 Bcf/d (270.8 Bcm/y)

Source: U.S. Department of Energyhttp://www.fossil.energy.gov/programs/gasregulation/reports/summary_lng_applications.pdf

FTA with the U.S. requires national treatment for trade in natural gas, including Australia, Bahrain, Canada, Chile, Colombia, Dominican Republic, El Salvador, Guatemala, Honduras, Jordan, Mexico, Morocco, Nicaragua, Oman, Peru, Republic of Korea and Singapore