processing shale feedstocks - digitalrefining · 3225 gallows road, fairfax, ... recent transaction...

TRANSCRIPT

processing shale feedstocks

2013

PTQ supplement

gas to petrochemicals special

gas cov copy 5.indd 1 28/02/2013 14:22

Imagine the

of forcing flames downward...

...against the natural buoyancy of the flue gases. Our steam methanereformer design fires upward, reducing fan power consumption by

40 - 50%, to save operating costs.

Choose the Foster Wheeler Terrace Wall™ Steam Reformer for your hydrogen plant.

ineff ciency

Learn more at www.fwc.com/terracewall

fw.indd 1 25/02/2013 15:00

©2013. The entire content of this publication is protected by copyright full details of which are available from the publishers. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means – electronic, mechanical, photocopying, recording or otherwise – without the prior permission of the copyright owner.The opinions and views expressed by the authors in this publication are not necessarily those of the editor or publisher and while every care has been taken in the preparation of all material included in Petroleum Technology Quarterly the publisher cannot be held responsible for any statements, opinions or views or for any inaccuracies.

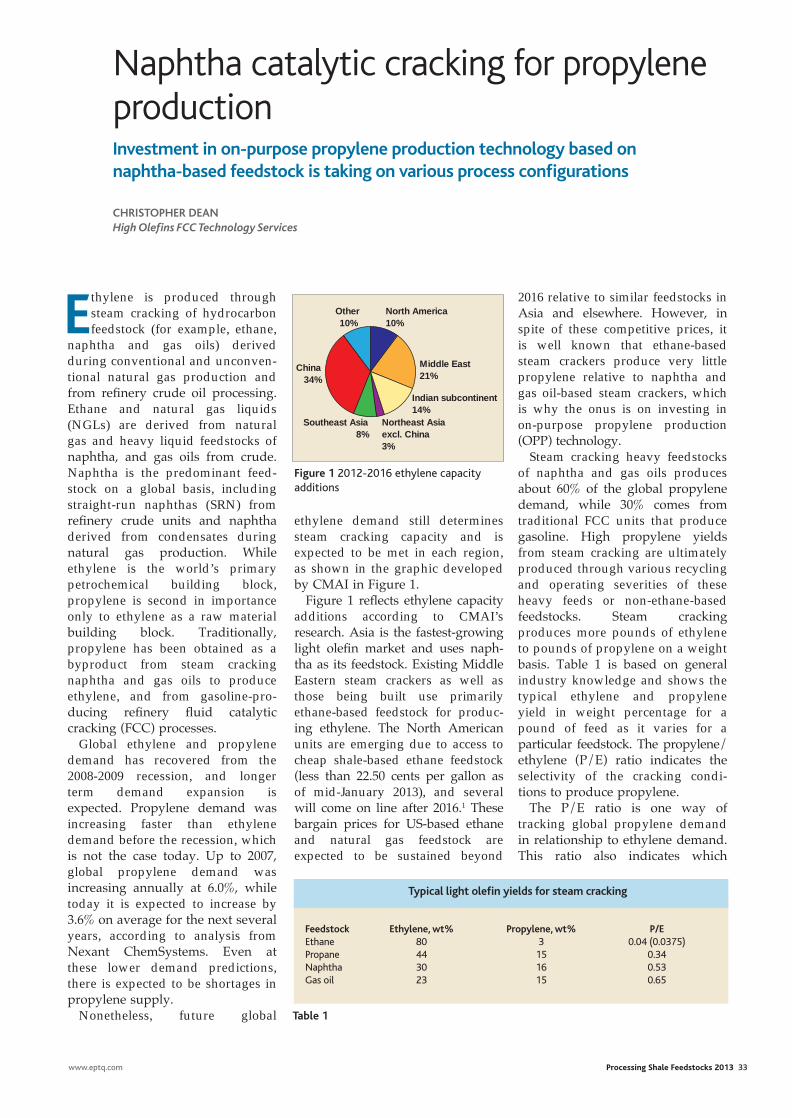

3 Weighing in on shale gas to petrochemicals RenéGonzalez 5 Roundtable ptq&a11 Processing Trends17 Shale gas feeds petrochemical expansion RenéGonzalez 17 Driving down costs in hydrogen production LuigiBressanandChrisDavis Foster Wheeler 29 Cracking hydrocarbon feedstock with a heavy tail JohanvanderEijk Technip

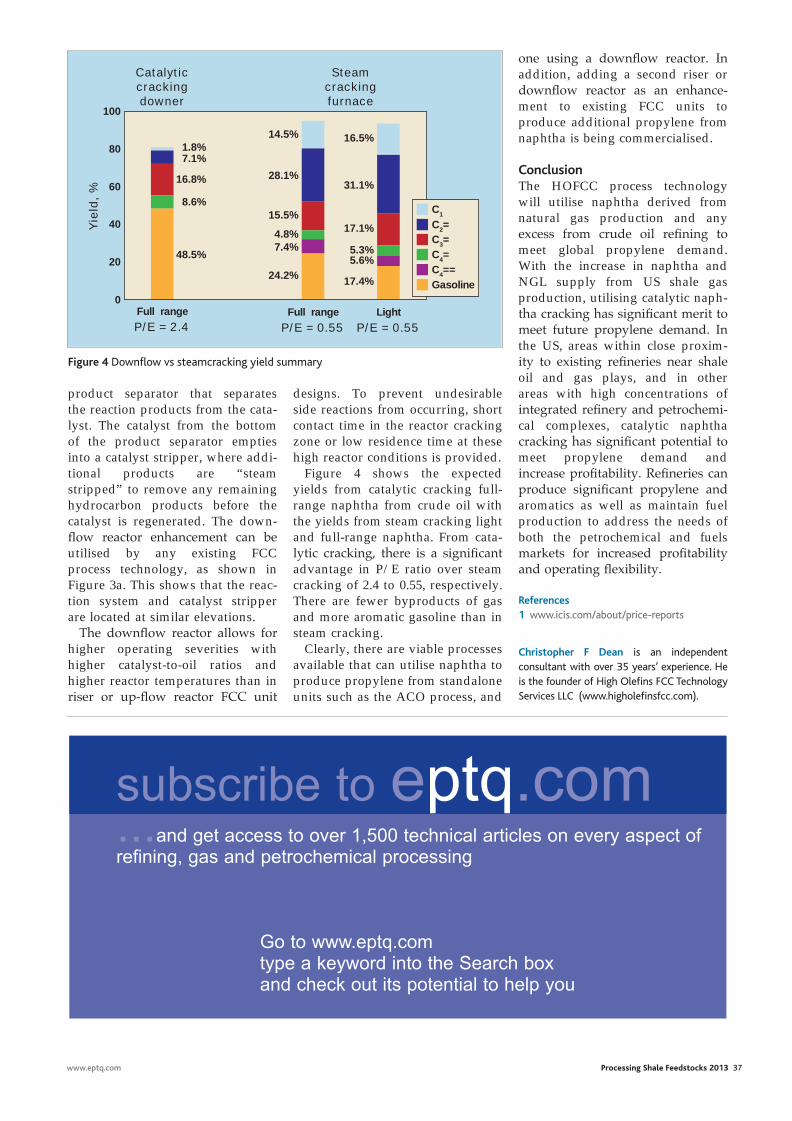

33 Naphtha catalytic cracking for propylene production ChristopherDean High Olefins FCC Technology Services

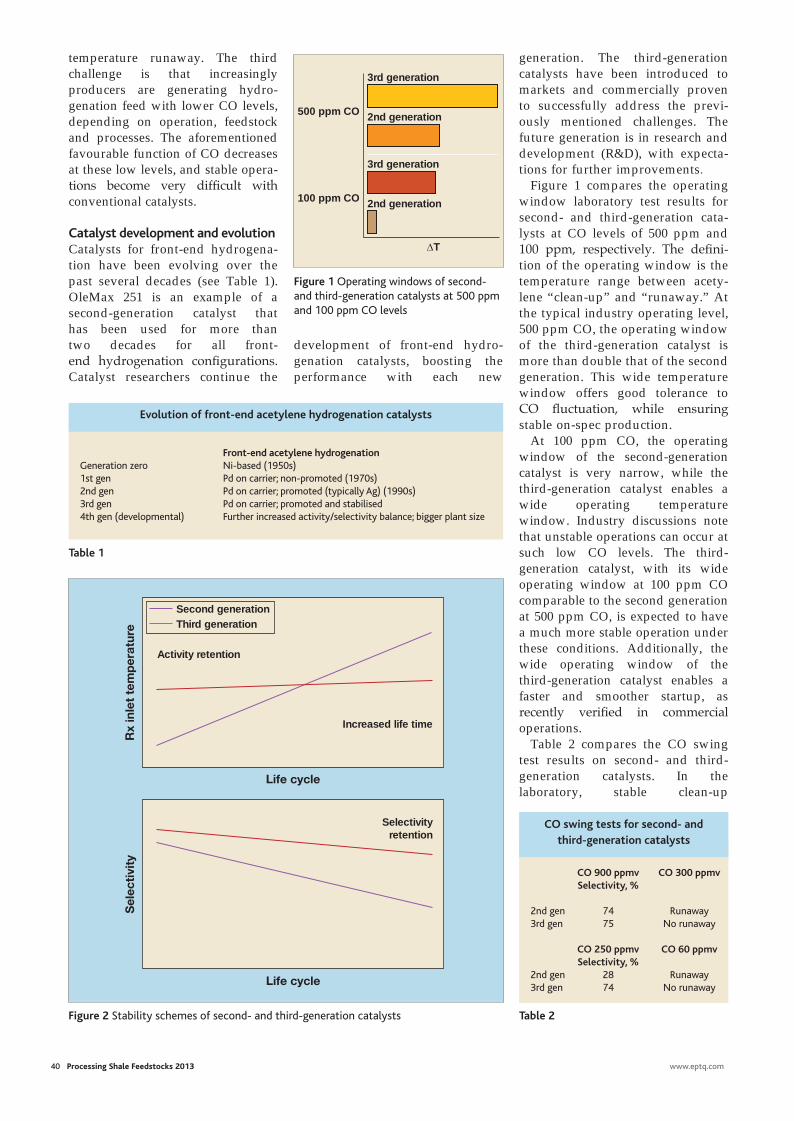

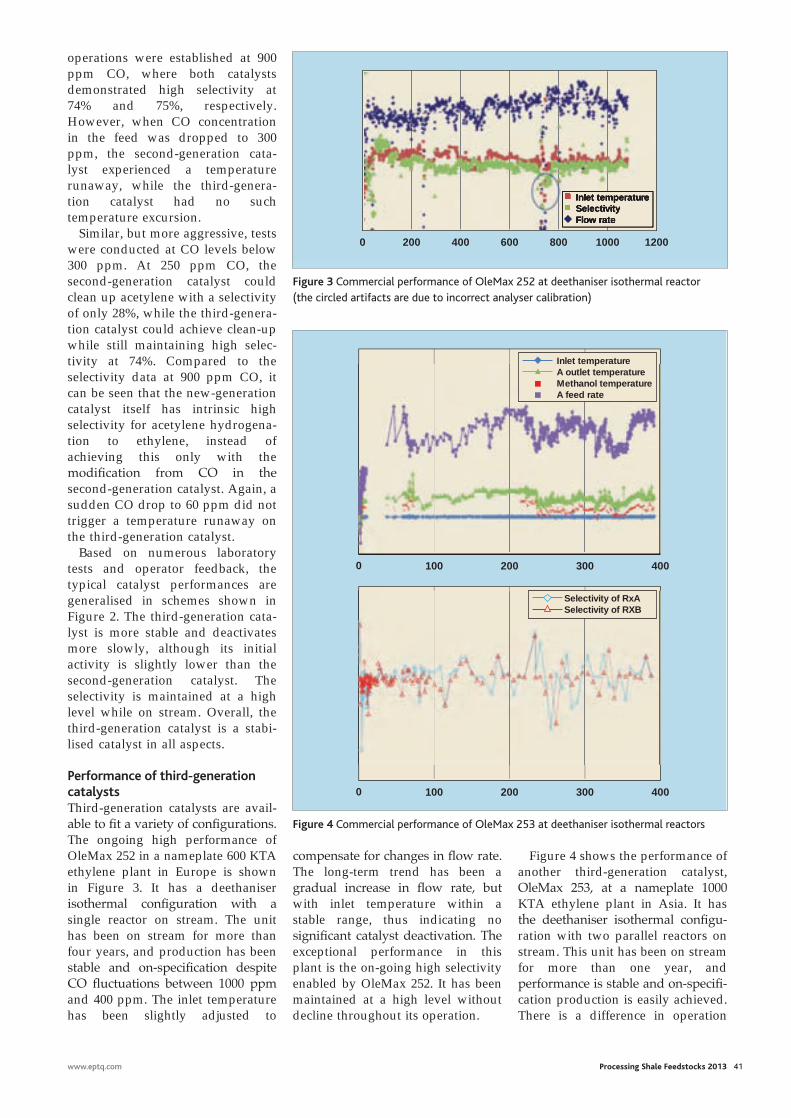

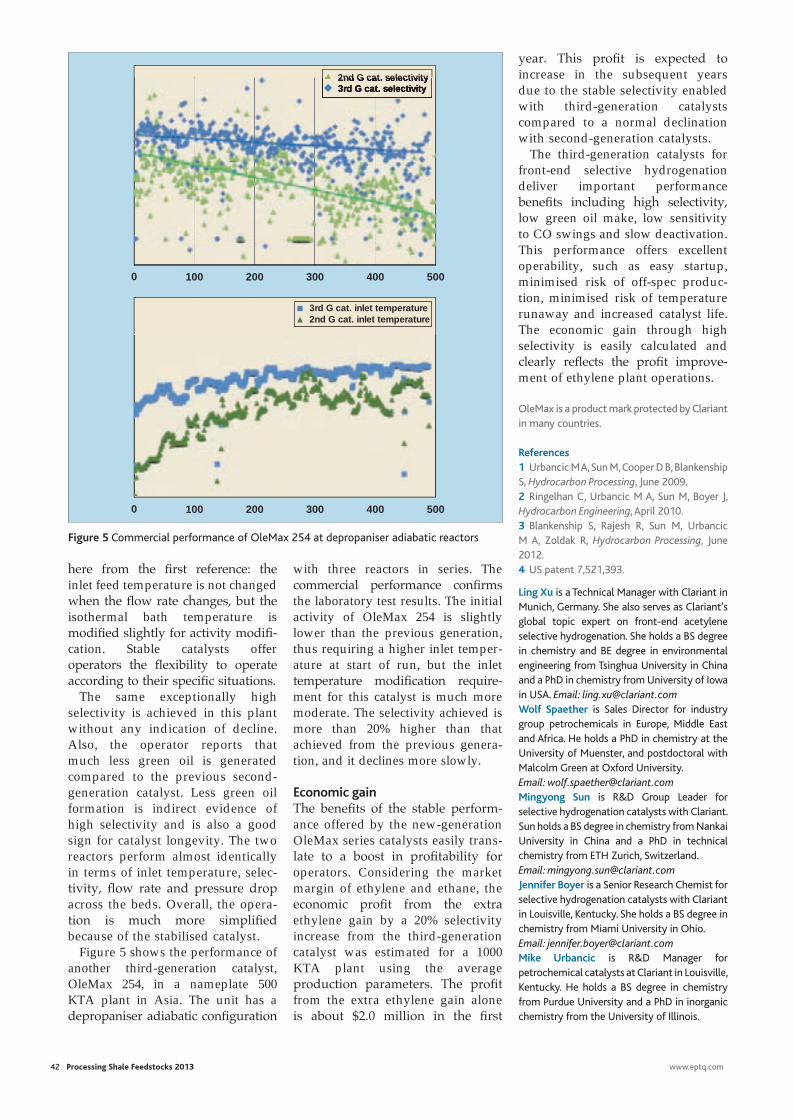

39 Maximise ethylene gain and acetylene selective hydrogenation efficiency LingXu,WolfSpaether,MingyongSun,JenniferBoyer andMichaelUrbancic Clariant

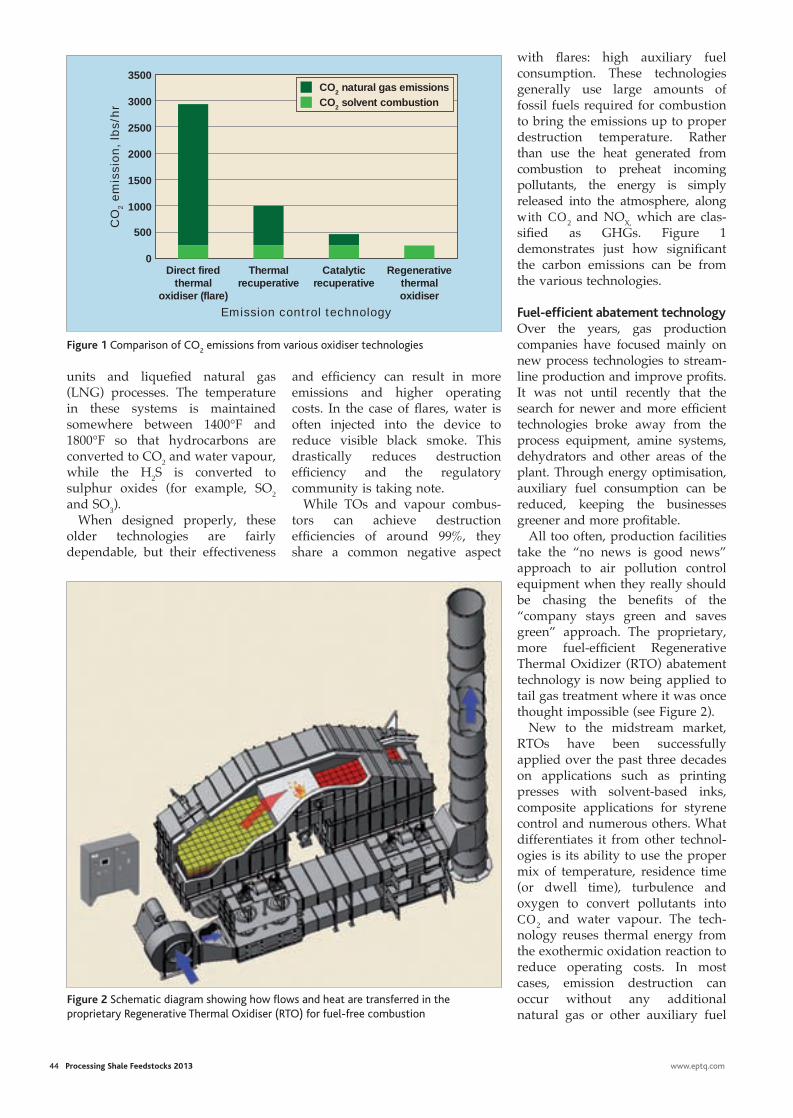

45 Reducing emission treatment costs for gas processors KevinSumm Anguil Environmental Systems

SasolFTWaxExpansionProject,Sasolburg,SouthAfrica:FosterWheeleristheengineering,procurementandconstructionmanagementcontractor,oneofthelargestSasolprojectsunderwayanywhereintheworld. Published by kind permission of Sasol. Image: Courtesy of Deryck Coetzer, Sasol

2013www.eptq.com

Processing shale feedstocks

gas to petrochemicalsspecial

ed com.indd 1 28/02/2013 14:25

ExxonMobil — Global Leader in Fuels and Lubes Process TechnologiesExxonMobil Technologies are applied across our corporation and by licensees worldwide in a growing list of process industry applications. Take advantage of our vast experience and ongoing commitment to continuously improve our industry leading technologies.

TECHNOLOGIES :

3225 Gallows Road, Fairfax, VA 22037-0001, USAwww.exxonmobil.com/tsl

+1-703-846-2568 fax [email protected]

Advanced Solutions for the World’s Toughest Energy Challenges

Leadership in Process Technology & Catalysis

developmentdeployment

discovery

2010

2000

1990

1980

1970

1960

1950

1940

SELECTIVE LUBE DEWAXING (MSDW)ExxonMobil’s new generation of MSDW technology continues to lead the industry.

Methanol to Gasoline (MTG)MTG converts methanol to sulfur free gasoline, including first commercial CTL application.

FLUID CATALYTIC CRACKINGFCC unit in 1942 would become the industry standard for production of gasoline.

BenzOUT Converts benzene contained in the refinery’s gasoline blend-stock into high octane alkyl-aromatics by reacting benzene with light olefins.

DISCOVERY OF ZSM-5 ZEOLITEThe discovery of ZSM-5 revolutionized many catalytic processes in refining and petrochemical industry.

pOWERFORMING

HydrofinishingCatalyst

MLDWDewaxing

Discovery of MCM-22

exxon.indd 1 28/02/2013 14:28

The European Union has arguably been the global leader in biodiesel production and use, with overall

biodiesel production increasing from 1.9 million tonnes in 2004 to nearly 10.3 million tonnes in 2007. Biodiesel production in the US has also increased dramatically in the past few years from 2 million gallons in 2000 to approximately 450 million gallons in 2007. According to the National Biodiesel Board, 171 companies own biodiesel manufacturing plants and are actively marketing biodiesel.1. The global biodiesel market is estimated to reach 37 billion gallons by 2016, with an average annual growth rate of 42%. Europe will continue to be the major biodiesel market for the next decade, followed closely by the US market.

Although high energy prices, increasing global demand, drought and other factors are the primary drivers for higher food prices, food competitive feedstocks have long been and will continue to be a major concern for the development of biofu-els. To compete, the industry has responded by developing methods to increase process efficiency, utilise or upgrade by-products and operate with lower quality lipids as feedstocks.

Feedstocks

Biodiesel refers to a diesel-equivalent fuel consisting of short-chain alkyl (methyl or ethyl) esters, made by the transesterification of triglycerides, commonly known as vegetable oils or animal fats. The most common form uses methanol, the cheapest alcohol available, to produce methyl esters. The molecules in biodiesel are pri-marily fatty acid methyl esters (FAME), usually created by trans-esterification between fats and metha-nol. Currently, biodiesel is produced from various vegetable and plant oils. First-generation food-based feedstocks are straight vegetable oils such as soybean oil and animal fats such as tallow, lard, yellow grease, chicken fat and the by-products of the production of Omega-3 fatty acids from fish oil. Soybean oil and rapeseeds oil are the common source for biodiesel produc-tion in the US and Europe in quanti-ties that can produce enough biodie-sel to be used in a commercial market with currently applicable

Processing Shale Feedstocks 2013 3

Project Editor René [email protected]

Production EditorRachel [email protected]

Graphics EditorRob Fris [email protected]

Editorial tel +44 844 5888 773fax +44 844 5888 667

Business Development DirectorPaul [email protected] Advertising SalesBob [email protected]

Advertising Sales Officetel +44 844 5888 771 fax +44 844 5888 662

PublisherNic [email protected]

CirculationJacki [email protected]

Crambeth Allen Publishing LtdHopesay, Craven Arms SY7 8HD, UKtel +44 844 5888 776fax +44 844 5888 667

ptq (petroleum technology quarterly) (ISSN No: 1632-363X, USPS No: 014-781) is published quarterly plus annual Catalysis edition by Crambeth Allen Publishing Ltd and is distributed in the US by SP/Asendia, 17B South Middlesex Avenue, Monroe NJ 08831. Periodicals postage paid at New Brunswick, NJ. Postmaster: send address changes to ptq (petroleum technology quarterly), 17B South Middlesex Avenue, Monroe NJ 08831.Back numbers available from the Publisher at $30 per copy inc postage.

Vol 18 No 3

2013

Weighing in on shale gas to petrochemicals

In rolling out this first issue of PTQ Processing Shale Feedstocks, we took into focus the rapid transformation undergone by the petrochemical industry with the advent of plentiful natural gas from North America’s unconventional

shale formations. Petrochemical industry planners are confident that expanding natural gas production will be available to supply steam crackers with cheap ethane feedstock for ethylene production. For propylene production, the economics of propane dehydrogenation (PDH) are now such that more than a dozen projects are on the books for 2013-2015 in China, US, Middle East, Brazil and other regions.

The following articles discuss these prospects for expanding petrochemical capacity in shale advantaged regions, weighed against the prospects for com-mitting shale gas resources to other industries, including power generation and LNG export.

Projected market demand for polymer-grade propylene (PGP) cannot be met by ethane-based steam crackers and refinery FCC units. On-purpose pro-pylene production (OPP), primarily in the form of PDH technology inte-grated with a petrochemical complex, is the most viable option. This option is spurred on by low-cost feedstock derived from shale gas.

A study released by Intratec Solutions in October 2012 on the PDH eco-nomics for PGP production noted that major petrochemical companies, including Dow Chemical and Enterprise Products, are building PDH units to take advantage of shale gas, which provides a high propane avail-ability leading to a feedstock advantage for US PDH units. The study esti-mated, for example, that Capex for PDH plants in the US are lower than China.

Other rapidly developing petrochemical opportunities involve the produc-tion of methanol (CH3OH) from the basic methane (CH4) molecule in shale gas. With methanol forming the basic building block for ammonia, fertilizer and olefins (ie, metathesis), it stands to reason that this value chain could emerge in parallel to shale gas advantaged ethylene plants.

Outside of petrochemicals, shale feedstock advantages being what they are is why refining industry planners anticipate having enough cheap shale gas available for hydrogen production and fuel gas consumption. Furthermore, the power industry sees a long-term transformation from coal to natural gas as the base-load power source. Further into the future, CNG as a substitute for diesel and other transportation fuels could increase significantly if major engine manufacturers such as Caterpillar continue promoting conversion of diesel powered machinery to CNG.

What are the long-term expectations for cheap natural gas feedstock? The energy industry is scrambling to accommodate this reversal of fortune from high gas prices (>$12/MMBtu to <3.50/MMBtu). In retrospect, feedstock costs for the LNG and petrochemical processing industries will remain com-petitive for many years to come.

RENé GONzALEz

Processing shale feedstocks

ed com.indd 2 25/02/2013 17:03

Q What opportunities are available for shale midstream processors going forward from 2013?

A Joshua Hallenbeck, Vice President, MarkWest Energy PartnersAs drillers (for example, Gulfport Energy) begin sell-ing methane, propane, butane, pentane and oil, such as from the 28.5 mcfd of natural gas now being produced from the Shugert 1 well in a section of the state of Ohio’s Utica Shale play known as Egypt Valley in Belmont County, Mark West Energy is now processing Gulfport gas from the first phase of its processing complex near Cadiz.

Gulfport’s success in the Utica Shale and the commencement of operations at our Cadiz Complex are significant accomplishments in the ongoing Utica Shale development in Eastern Ohio. Early results indi-cate this play is one of the most exciting new areas for natural gas and liquids production in the US — and given our leading position in the neighbouring Marcellus Shale, we are well positioned to support producers’ future development plans in the Utica.

In natural gas processing, the dry methane part of the gas stream is separated from the wet portions —ethane, butane, propane and pentane. During fractionation, the natural gas liquids and other substances are separated from each other. These sepa-rated gas products are then ready for use, with the ethane possibly going to a cracker plant somewhere in North America. MarkWest plans to send ethane from Cadiz to Gulf Coast markets for cracking there.

A Wouter van Kempen, President and CEO, DCP MidstreamThe DCP Midstream enterprise continues to execute on its slate of growth projects underpinned by solid contracts in liquids-rich areas. We process 6.3 trillion Btu of gas everyday and our NGL production is well over 400 000 bpd. Back in early December 2012, DCP Midstream and DCP Midstream Partners announced the construction of a new cryogenic plant that will serve the growing demand from producers in the liquids-rich Eagle Ford shale in Texas. The new Goliad plant (located near Goliad, Texas) will be constructed

and funded by the previously announced DCP Eagle Ford joint venture, which is owned two-thirds by DCP Midstream and one-third by DCP Midstream Partners.

The Goliad cryogenic plant will have a gas process-ing capacity of 200 million cfd and will become part of the DCP Eagle Ford system, providing Eagle Ford producers a one-stop service from the plant tailgate to Gulf Coast market centres. The Goliad plant is expected to be completed by Q1 2014. Through co- investment with DCP Midstream Partners and the recent transaction on the pipelines with Phillips 66 and Spectra Energy, we can continue to fund our proj-ects and create value for all our stakeholders. The Goliad plant is the seventh plant in South Texas owned by the DCP enterprise.

Q Based on your coverage of the US East Coast shale industry, can you comment on progress in the construction of ethane-based steam crackers for ethylene production?

A Julio Renteria, Business Development Manager, CatecA recent ICIS News report noted that the lack of infrastructure for Shell’s proposed western Pennsylvania cracker provides an opportunity for

www.eptq.com Processing Shale Feedstocks 2013 5

Roundtable ptq&a

Additional Q&A can be found at www.eptq.com/QandA

Modern ethylene processing plant Courtesy: Linde

Were it not for the evolving shale gas resources, separation and purification of gas for midstream processing would remain unchanged, but the multiple value-added routes emerging for petrochemicals, LNG and fuels requires new pipeline and product specifications for shale gas in particular, as discussed by the following respondents

Q&A copy 12.indd 1 25/02/2013 17:06

Nova Chemicals to expand its Corunna ethylene facil-ity and displace Shell’s ethane supply. According to Peter Voser, the Shell Chemicals CEO, Shell could have a cracker completed by 2017 if it began construc-tion in 2014. There are no ethane cracker plants in the Marcellus region at the present time, although Aither Chemicals, an upstart company touting an untried catalytic cracking approach, is promoting a plant near Charleston, West Virginia. Surplus ethane from the so-called “wet natural gas” of western Pennsylvania and northern West Virginia is too valuable to burn

because it can be cracked into ethylene for the manu-facture of polyethylene and other products.

According to some experts in the industry, Nova would have a more reliable destination for ethane if it expanded its Corunna cracker capacities near Sarnia, Ontario, Canada. The expansion would require less money and less time than Shell’s project. A major expansion at Corunna could be completed years before Shell completes construction of a world-scale facility.

The Sarnia region has salt caverns to store hydrocar-bons and liquefied petrochemical feedstock such as ethane. Nova’s Corunna cracker in Sarnia already plans to use ethane from the Marcellus shale basin. An exist-ing Sunoco pipeline from the western Pennsylvania to

Sarnia will transport 40 000 bpd of ethane to Nova’s cracker, and an additional 10 000 bpd to the region for other plants. In addition, Nova will upgrade the feed-stock capability at the cracker by the end of 2013 to 100% of NGL feeds, company CEO Randy Woelfel said. Also, Imperial Oil has a refinery and petrochemical complex in Sarnia. The complex produces a wide range of products, including polyethylene, solvents, olefins and aromatics, the company said.

Q What is an important technical challenge to consider for new steam crackers coming online before 2017?

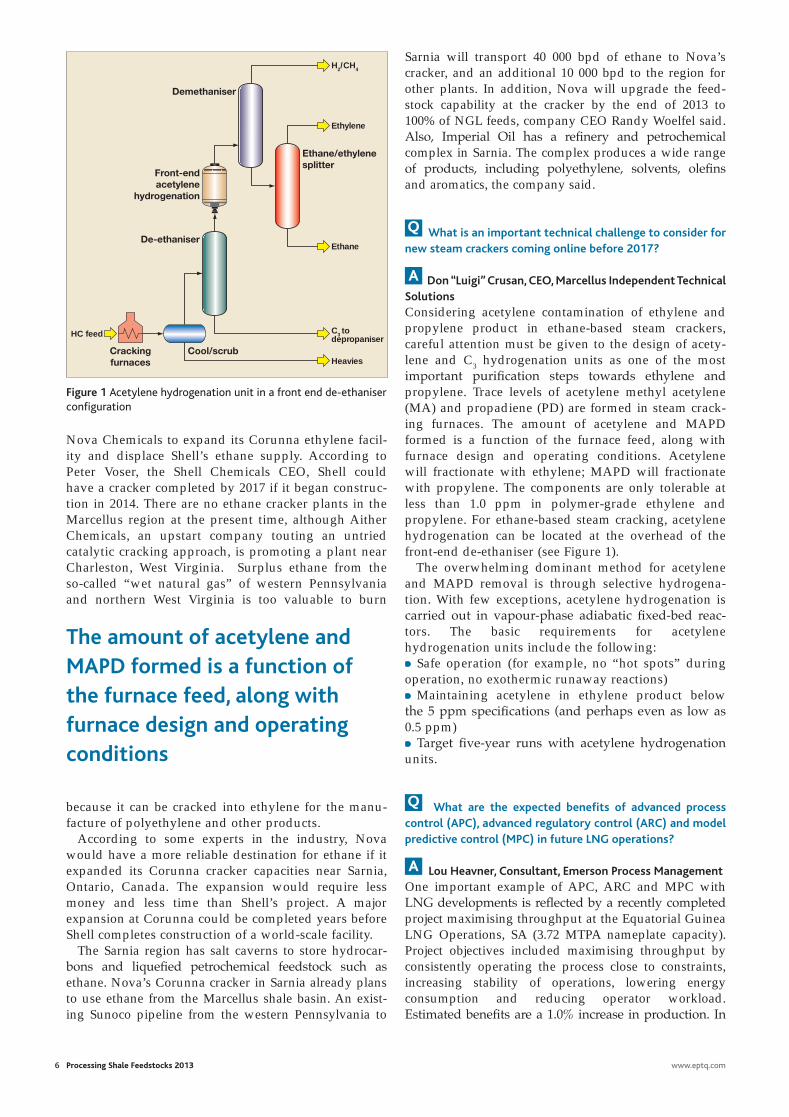

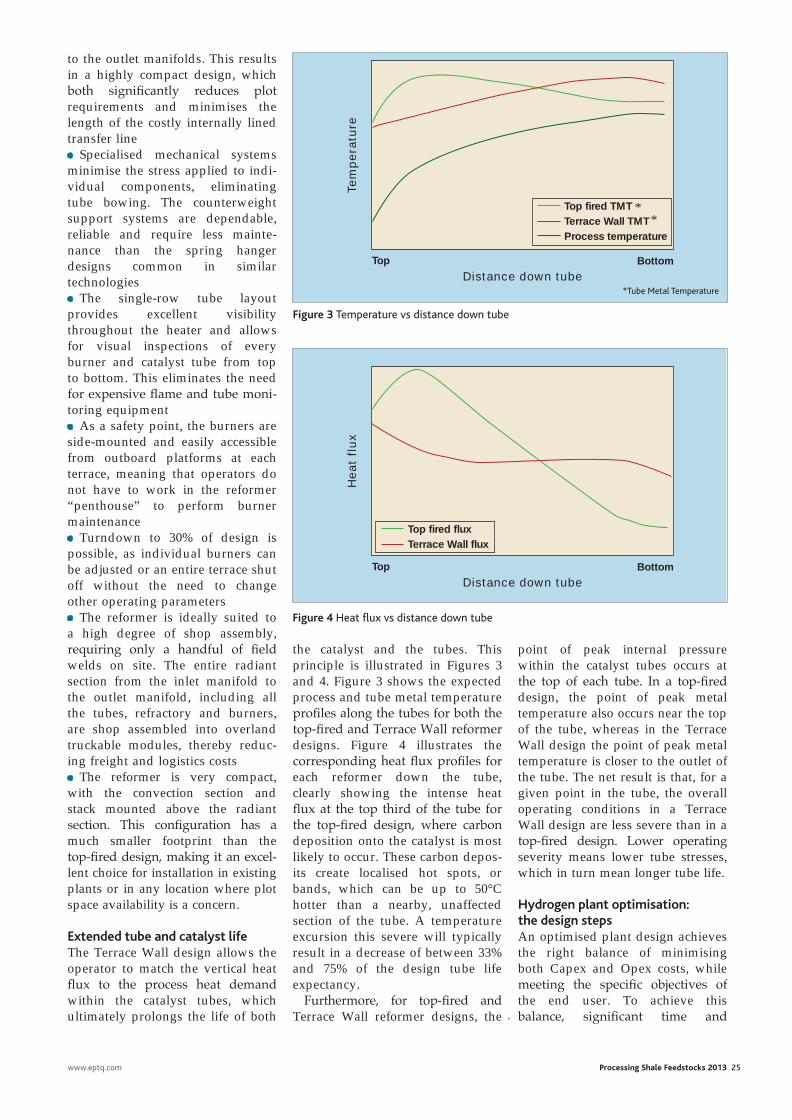

A Don “Luigi” Crusan, CEO, Marcellus Independent Technical SolutionsConsidering acetylene contamination of ethylene and propylene product in ethane-based steam crackers, careful attention must be given to the design of acety-lene and C3 hydrogenation units as one of the most important purification steps towards ethylene and propylene. Trace levels of acetylene methyl acetylene (MA) and propadiene (PD) are formed in steam crack-ing furnaces. The amount of acetylene and MAPD formed is a function of the furnace feed, along with furnace design and operating conditions. Acetylene will fractionate with ethylene; MAPD will fractionate with propylene. The components are only tolerable at less than 1.0 ppm in polymer-grade ethylene and propylene. For ethane-based steam cracking, acetylene hydrogenation can be located at the overhead of the front-end de-ethaniser (see Figure 1).

The overwhelming dominant method for acetylene and MAPD removal is through selective hydrogena-tion. With few exceptions, acetylene hydrogenation is carried out in vapour-phase adiabatic fixed-bed reac-tors. The basic requirements for acetylene hydrogenation units include the following:• Safe operation (for example, no “hot spots” during operation, no exothermic runaway reactions)• Maintaining acetylene in ethylene product below the 5 ppm specifications (and perhaps even as low as 0.5 ppm)• Target five-year runs with acetylene hydrogenation units.

Q What are the expected benefits of advanced process control (APC), advanced regulatory control (ARC) and model predictive control (MPC) in future LNG operations?

A Lou Heavner, Consultant, Emerson Process ManagementOne important example of APC, ARC and MPC with LNG developments is reflected by a recently completed project maximising throughput at the Equatorial Guinea LNG Operations, SA (3.72 MTPA nameplate capacity). Project objectives included maximising throughput by consistently operating the process close to constraints, increasing stability of operations, lowering energy consumption and reducing operator workload. Estimated benefits are a 1.0% increase in production. In

6 Processing Shale Feedstocks 2013 www.eptq.com

HC feed

Demethaniser

Ethane/ethylene splitter

Front-end acetylene

hydrogenation

De-ethaniser

Cracking furnaces

Cool/scrub

H2/CH4

Ethylene

Ethane

C3 to depropaniser

Heavies

Figure 1 Acetylene hydrogenation unit in a front end de-ethaniser configuration

The amount of acetylene and MAPD formed is a function of the furnace feed, along with furnace design and operating conditions

Q&A copy 12.indd 2 25/02/2013 17:07

www.eptq.com Processing Shale Feedstocks 2013 7

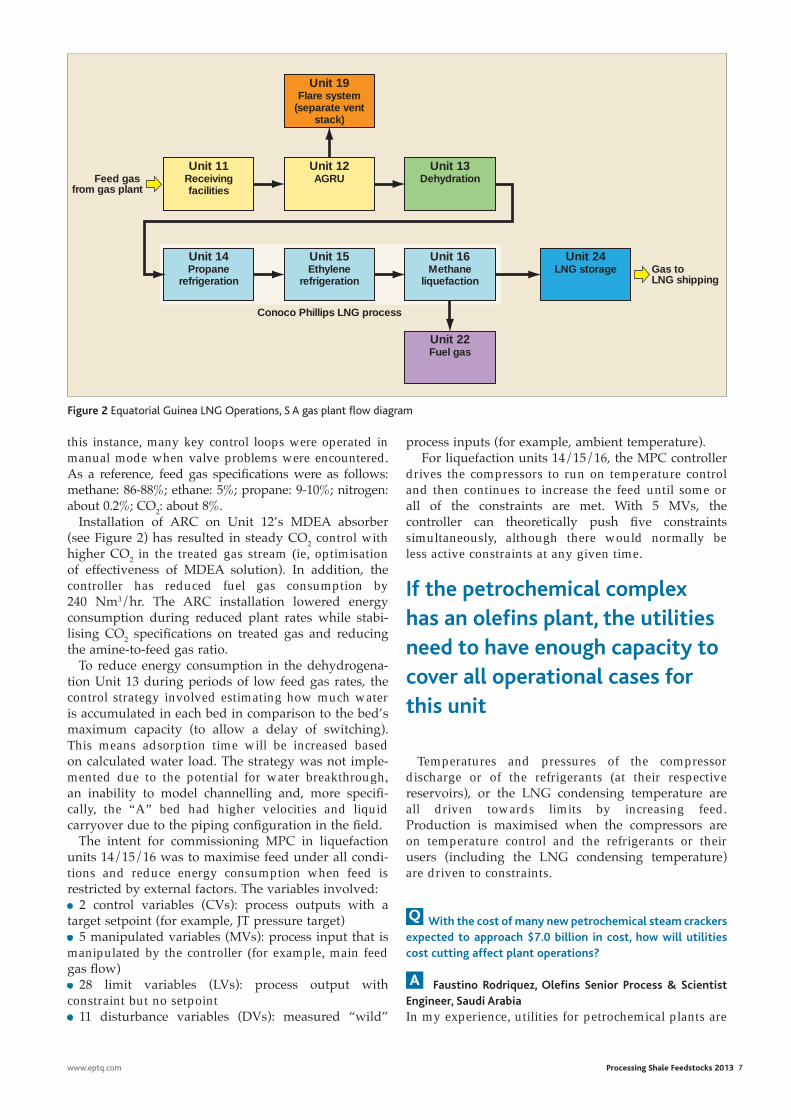

this instance, many key control loops were operated in manual mode when valve problems were encountered. As a reference, feed gas specifi cations were as follows: methane: 86-88%; ethane: 5%; propane: 9-10%; nitrogen: about 0.2%; CO2: about 8%.

Installation of ARC on Unit 12’s MDEA absorber (see Figure 2) has resulted in steady CO2 control with higher CO2 in the treated gas stream (ie, optimisation of effectiveness of MDEA solution). In addition, the controller has reduced fuel gas consumption by 240 Nm3/hr. The ARC installation lowered energy consumption during reduced plant rates while stabi-lising CO2 specifi cations on treated gas and reducing the amine-to-feed gas ratio.

To reduce energy consumption in the dehydrogena-tion Unit 13 during periods of low feed gas rates, the control strategy involved estimating how much water is accumulated in each bed in comparison to the bed’s maximum capacity (to allow a delay of switching). This means adsorption time will be increased based on calculated water load. The strategy was not imple-mented due to the potential for water breakthrough, an inability to model channelling and, more specifi -cally, the “A” bed had higher velocities and liquid carryover due to the piping confi guration in the fi eld.

The intent for commissioning MPC in liquefaction units 14/15/16 was to maximise feed under all condi-tions and reduce energy consumption when feed is restricted by external factors. The variables involved:• 2 control variables (CVs): process outputs with a target setpoint (for example, JT pressure target)• 5 manipulated variables (MVs): process input that is manipulated by the controller (for example, main feed gas fl ow)• 28 limit variables (LVs): process output with constraint but no setpoint• 11 disturbance variables (DVs): measured “wild”

process inputs (for example, ambient temperature). For liquefaction units 14/15/16, the MPC controller

drives the compressors to run on temperature control and then continues to increase the feed until some or all of the constraints are met. With 5 MVs, the controller can theoretically push fi ve constraints simultaneously, although there would normally be less active constraints at any given time.

Temperatures and pressures of the compressor discharge or of the refrigerants (at their respective reservoirs), or the LNG condensing temperature are all driven towards limits by increasing feed. Production is maximised when the compressors are on temperature control and the refrigerants or their users (including the LNG condensing temperature) are driven to constraints.

Q With the cost of many new petrochemical steam crackers expected to approach $7.0 billion in cost, how will utilities cost cutting affect plant operations?

A Faustino Rodriquez, Olefi ns Senior Process & Scientist Engineer, Saudi ArabiaIn my experience, utilities for petrochemical plants are

Unit 19Flare system

(separate vent stack)

Unit 11Receiving facilities

Unit 12AGRU

Unit 14Propane

refrigeration

Unit 15Ethylene

refrigeration

Unit 16Methane

liquefaction

Unit 24LNG storage

Unit 22Fuel gas

Unit 13Dehydration

Conoco Phillips LNG process

Gas to LNG shipping

Feed gas from gas plant

Figure 2 Equatorial Guinea LNG Operations, S A gas plant fl ow diagram

If the petrochemical complex has an olefi ns plant, the utilities need to have enough capacity to cover all operational cases for this unit

Q&A copy 12.indd 3 26/02/2013 11:21

plant are extremely small on a per-pound basis. Multiple, smaller US ethylene/polyethylene production facilities can support desired social objec-tives (more real jobs and a pool of experienced people).

In addition, there are four propane dehydrogena-tion (PDH) projects being seriously discussed, or moving forward, in North America. Interestingly, there are also new technologies ready for commercial-isation for the conversion of natural gas to propylene. One such new technology is bromine based and offered by GRT, Inc. The new technologies cite lower capital costs.

The current interest in PDH is based on the rapid switch to ethane as the feedstock of preference for ethylene production. For all practical purposes, no co-product propylene is produced when ethane is cracked (3% propylene yield for ethane, versus 18% for propane and 13% for naphtha). A factor that has to be considered when looking at new PDH facilities is what to do with the propylene. For some applications, polyethylene competes directly with polypropylene on a price basis. In the Pacific, if the price of propane is detached from crude prices, we will see propane replacing naphtha as a cracker feedstock. What I am suggesting is that the market leads, and a stampede to new PDH facilities could result in return on invest-ment (ROI) problems.

Q Can you elaborate why managing audits in the upstream drilling business has taken on such an urgency for the shale gas industry?

A Kevin Koser, President, ExaserveThere have been many changes with regards to company commitment and the vision of audits during and after projects. The urgency, I believe, has been driven because of the collision of two market shifts. First is the strict adherence to legal compliance and the focus on maintaining integrity throughout all company decisions and processes. This, of course, really ramped up when companies were introduced to heavier regulations (such as Sarbanes-Oxley) than they were used to in the past. Second is a series of very public projects that have either gone millions in excess over budget or failed outright, both of which have been highlighted by very public legal actions. Executives have made it a priority to have indepen-dent audit teams investigate a project’s governance to insure all legal agreements have been met and that both client and partner have delivered everything promised.

The solutions that Exaserv has implemented for drillers can be used by any and all companies that wish to streamline processes, insure both data integ-rity and consistency, and manage all aspects of their employee population for both current and future growth. This SAP solution, designed and built by Exaserv, is available to any small to mid-sized operator.

8 Processing Shale Feedstocks 2013 www.eptq.com

always short. The problem starts during the design basis. You must consider the start-up periods of the units and upset conditions. The requirements of utili-ties are totally different from normal operation to trip condition. If the petrochemical complex has an olefins plant, the utilities need to have enough capacity to cover all operational cases for this unit.

From a maintenance point of view, you should consider spare capacity for preventive maintenance and major turnarounds. Normally, utilities must be available 100% of the time. So, high reliability consid-erations are required. In my experience, reducing costs in the project phase never covers loss of production because utilities are short in the future during the operational phase.

It is very difficult to indicate a margin of design for utilities in a petrochemical complex. Every utility needs to be analysed separately, considering many cases of operation. But consider a least 25% over- capacity over the worst case requirement. The worst case is peak demand during upsets or unit start-up. Be very careful in defining capacities and over-design for flare systems, incinerator and wastewater treatment systems.

Q There has been a lot of focus on new world-scale ethane-based ethylene plants and propane dehydrogenation (PDH) units coming online in the US by 2017. Do you see other alternatives to these high capital projects?

A James Cutler, CEO, Appalachian ResinsAppalachian Resins has received some very favour-able response to its business model and development efforts. There certainly are situations in which “world-scale” ethane-based ethylene plants are the way to go. No question about it. Alternatively, smaller plants, sized to reflect local markets, also have a place.

Development economics can dictate that a plant less than world scale is desirable. These factors can reflect environmental considerations, ability to dispose of ethane during periods of ethylene plant downtime and a wide array of required supporting off-sites. Another recently observed factor is that restart-up time due to power failures can be significant for world-scale ethylene plants.

The bottom line, in today’s world — resiliency due to facility redundancy — is an important consider-ation. Labour savings due to having a larger ethylene

The current interest in propane dehydrogenation is based on the rapid switch to ethane as the feedstock of preference for ethylene production

Q&A copy 12.indd 4 25/02/2013 17:07

Reliable SwiSS Quality

API 618Rod load up to 1'500 kN/335'000 IbsPower up to 31'000 kW/42'100 HP

Full Range:

You get moRe than Just aPRocess gas comPRessoR

Lubricated up to 1'000 bar, non-lubricated up to 300 bar

For highest availability: We recom-mend our own designed, in-house engineered compressor valves and key compressor components

Designed for easy maintenance

We are the competent partner with the full range of services – worldwide

→ www.recip.com/api618

Reliable SwiSS Quality

API 618Rod load up to 1'500 kN/335'000 IbsPower up to 31'000 kW/42'100 HP

Full Range:

You get moRe than Just aPRocess gas comPRessoR

Lubricated up to 1'000 bar, non-

For highest availability: We recom-mend our own designed, in-house engineered compressor valves and key compressor components

Designed for easy maintenance

We are the competent partner with the full range of services – worldwide

YouR BeneFit:lowest liFe cYcle costs

burckhardt.indd 1 7/3/12 21:39:05

1207

_e

www.airliquide.com

Because our genes lead us to an irrepressible passion for new solutions.

The only thing longer than our company historyis the list of our innovations.

When it comes to providing innovative plant and system solutions, Air Liquide Global E&C Solutions is your partner of choice – worldwide. No surprise, since we innovate relentlessly in order to bring sustainable and cost-eff ective solutions

to society, levera ging partnerships with customers, suppliers, academics and communities. This is not only demonstrated by thousands of patents, but by pionee-ring reference projects around the globe as well. Yours could be the next one.

AIR2185025_AZ_TechnoDNA_10/12_RZ.indd 1 16.10.12 14:18air liquide.indd 1 25/02/2013 17:05

New gas-to-petrochemical infrastructures require higher environmental compliance A growing percentage of ethane feedstock planned for new ethylene processing plants in North America are from unconventional gas resources. These unconven-tional gas resources are trapped in very tight or low permeability rock, and the effort required to extract them is greater than for conventional gas resources. This means higher intensity of drilling, entailing more industrial activity and disruption above ground. Producing gas from unconventional formations in many cases involves the use of hydraulic fracturing to boost the flow of gas from the well.

The potential environmental hazards and other features of unconventional gas development predicates higher investment in measuring, monitoring and controlling the potential environmental impact from the wellhead to the petrochemical processing facility. Starting at the wellhead, early and sustained engage-ment can reduce the above-ground impacts. This includes rigorous assessment, monitoring and handling of water resources for shale and tight gas.

Unconventional gas has higher production-related greenhouse gas emissions than conventional gas, but the difference can be reduced and the emissions of other pollutants lowered by eliminating venting and minimis-ing flaring during the well completion phase, similar in scope to reduced flaring seen in refinery and petrochem-ical process facilities. For example, releases of methane, wherever they occur in the gas supply chain serving the petrochemical end user, are particularly damaging, given methane’s potency as a greenhouse gas.

The main reason for the potentially larger environ-mental impact of unconventional gas operations is the nature of the resources themselves: unconventional resources are less concentrated than conventional deposits. They are more difficult to extract because they are trapped in very tight or low permeability rock that impedes flow. Since the resources are more diffuse and difficult to produce, the scale of the industrial operation required for a given volume of unconven-tional output is much larger than for conventional production. This means that drilling and production activities can be considerably more invasive, involving a generally larger environmental footprint.

Propylene production by dehydrogenation increases in importanceWith the ratio of propylene to ethylene expected to continue decreasing as a result of reduced naphtha-based steam cracking (while ethane-based

Reduce gasoline cutpoint

steam cracking from shale gas increases), propane dehydrogenation (PDH) to propylene will continue to expand in importance, as seen over the past two years in major petrochemical centres such as China. However, new PDH units are expected to be announced in North America and the Middle East too.

Of major importance to efficient PDH reactor design is the dehydrogenation catalyst. Recently, propane combined with selective hydrogen combustion over Pt-Sn bimetallic catalysts was discussed by Shinji Kaneko, et al, from the Department of Applied Chemistry, Saitama University in Saitama, Japan. Kaneko and colleagues noted that PDH has typically been carried out in the presence of inert gas, hydrogen or steam (normal dehydrogenation).

In the Kaneko study, dehydrogenation of propane combined with selective hydrogen combustion was studied over supported Pt-Sn bimetallic catalysts. A catalytic test for normal dehydrogenation was also carried out as part of the proposed process. Pt/Al2O3 modified with Sn and Zn was found to be suitable for both of these two reactions. In the normal dehydroge-nation, conversions equal to the calculated equilibrium conversion were achieved with almost complete selec-tivity for propylene. Optimisation of catalyst composition was done by the addition of various amounts of Sn to Pt/Al2O3 and Pt/Zn-Al-O. For dehy-drogenation combined with hydrogen combustion, selective hydrogen combustion was achieved over Pt-Sn bimetallic catalysts. Moreover, a stable conver-sion higher than that of equilibrium for normal dehydrogenation was obtained using Pt-Sn/Zn-Al-O under certain reaction conditions.

New technology makes small LNG facilities more competitive The Royal Dutch Shells Pearl gas-to-liquids (GTL) mega project at Ras Laffan in Qatar cost almost $20 billion. The facility delivered its first cargo of synthetic fuels in 2012 and, at full capacity, it will yield a quarter of Qatar’s entire oil output.

Halfway around the world, another mega project is taking shape. Shell has committed to building a float-ing liquefied natural gas (LNG) plant at its Prelude field off Western Australia. The plant, which will super-cool gas so it can be delivered worldwide by tanker, will be the largest floating structure ever built, six times as large as a Nimitz-class aircraft carrier. While this is a massive floating LNG plant, floating liquefaction plants may be scaled down and used to develop smaller or more remote fields where a land-

www.eptq.com Processing Shale Feedstocks 2013 11

Processing Trends

Changes in technology implementation have improved flexibility and lowered Capex and operational costs in the gas industry and downstream markets linked to LNG and ethylene

proc trends .indd 1 25/02/2013 19:22

diverge too widely between regions, and that buyers are not dependent on a single supplier.

To be sure, a key technical development in the LNG industry has been the evolution in the size of LNG trains over the past 25 years, resulting in significant unit cost reduction. Similar to liquefaction facilities, LNG ships have also been increasing in size to achieve reductions in the unit cost of LNG transported. Lessons learned in the design, execution and imple-mentation of large LNG trains and ships, as well as the overall changes in LNG liquefaction trains, has been key to the evolving design of the LNG value chain.

Nevertheless, the number of large discovered, unde-veloped gas resources needed to realise such economies of scale is decreasing. Continuous technol-ogy evolution will have to be maintained to enable economic utilisation of smaller, undeveloped, remote gas accumulations via concepts such as the previously noted floating liquefaction. The need to access markets in stricter permitting environments will drive innova-tion in terminals. In addition, an increasingly CO2-constrained regulatory environment will likely necessitate improved efficiencies and lower greenhouse gas emissions across the LNG value chain.

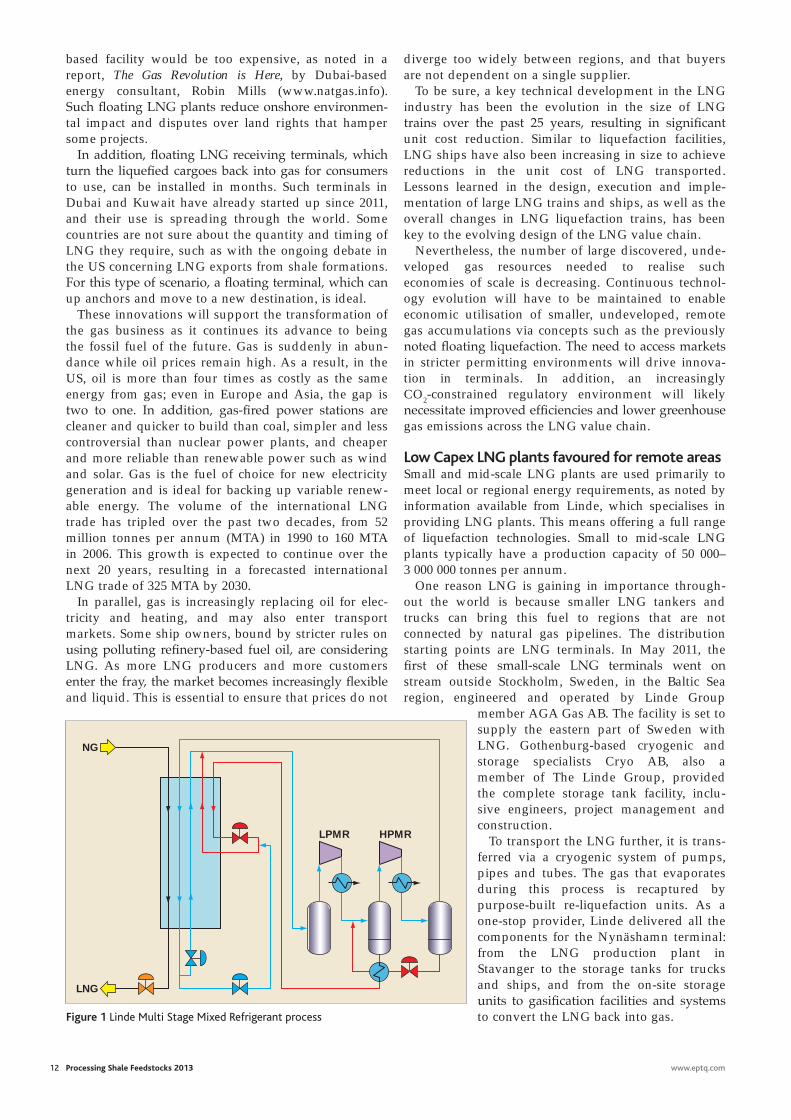

Low Capex LNG plants favoured for remote areasSmall and mid-scale LNG plants are used primarily to meet local or regional energy requirements, as noted by information available from Linde, which specialises in providing LNG plants. This means offering a full range of liquefaction technologies. Small to mid-scale LNG plants typically have a production capacity of 50 000– 3 000 000 tonnes per annum.

One reason LNG is gaining in importance through-out the world is because smaller LNG tankers and trucks can bring this fuel to regions that are not connected by natural gas pipelines. The distribution starting points are LNG terminals. In May 2011, the first of these small-scale LNG terminals went on stream outside Stockholm, Sweden, in the Baltic Sea region, engineered and operated by Linde Group

member AGA Gas AB. The facility is set to supply the eastern part of Sweden with LNG. Gothenburg-based cryogenic and storage specialists Cryo AB, also a member of The Linde Group, provided the complete storage tank facility, inclu-sive engineers, project management and construction.

To transport the LNG further, it is trans-ferred via a cryogenic system of pumps, pipes and tubes. The gas that evaporates during this process is recaptured by purpose-built re-liquefaction units. As a one-stop provider, Linde delivered all the components for the Nynäshamn terminal: from the LNG production plant in Stavanger to the storage tanks for trucks and ships, and from the on-site storage units to gasification facilities and systems to convert the LNG back into gas.

12 Processing Shale Feedstocks 2013 www.eptq.com

based facility would be too expensive, as noted in a report, The Gas Revolution is Here, by Dubai-based energy consultant, Robin Mills (www.natgas.info). Such floating LNG plants reduce onshore environmen-tal impact and disputes over land rights that hamper some projects.

In addition, floating LNG receiving terminals, which turn the liquefied cargoes back into gas for consumers to use, can be installed in months. Such terminals in Dubai and Kuwait have already started up since 2011, and their use is spreading through the world. Some countries are not sure about the quantity and timing of LNG they require, such as with the ongoing debate in the US concerning LNG exports from shale formations. For this type of scenario, a floating terminal, which can up anchors and move to a new destination, is ideal.

These innovations will support the transformation of the gas business as it continues its advance to being the fossil fuel of the future. Gas is suddenly in abun-dance while oil prices remain high. As a result, in the US, oil is more than four times as costly as the same energy from gas; even in Europe and Asia, the gap is two to one. In addition, gas-fired power stations are cleaner and quicker to build than coal, simpler and less controversial than nuclear power plants, and cheaper and more reliable than renewable power such as wind and solar. Gas is the fuel of choice for new electricity generation and is ideal for backing up variable renew-able energy. The volume of the international LNG trade has tripled over the past two decades, from 52 million tonnes per annum (MTA) in 1990 to 160 MTA in 2006. This growth is expected to continue over the next 20 years, resulting in a forecasted international LNG trade of 325 MTA by 2030.

In parallel, gas is increasingly replacing oil for elec-tricity and heating, and may also enter transport markets. Some ship owners, bound by stricter rules on using polluting refinery-based fuel oil, are considering LNG. As more LNG producers and more customers enter the fray, the market becomes increasingly flexible and liquid. This is essential to ensure that prices do not

NG

LNG

LPMR HPMR

Figure 1 Linde Multi Stage Mixed Refrigerant process

proc trends .indd 2 26/02/2013 11:16

www.aveva.com/futureofplantdesign

AVEVA E3D is thE corE DEsign ApplicAtion within thE AVEVA plAnt proDuct portfolio. it is fully intEropErAblE with All othEr AVEVA EnginEEr, DEsign AnD MAnAgE proDucts.

AVEVA Everything3D plant Design for lean construction

AVEVA’s vision for the future of plant Design allows project teams to move up to a new level of performance for plant design and drives a new era of plant Design for lean construction. AVEVA Everything3DtM (AVEVA E3DtM) is the new plant design product from AVEVA that exploits technology innovations in laser scanning, mobile and cloud computing to enable lean construction in plant project execution.

tM No 1 for Rapid Project Start-upprojects can be established in the shortest time, no matter where in the world project teams are based

No 1 for Design EfficiencyEnabling project teams to make savings of up to 20% compared to systems available today

No 1 for ComplianceEnsuring projects meet with corporate, client and legal standards

No 1 for Removing Rework in Constructionconnecting the plant design discipline to the fabricator and constructor to maximise project profits

scAn thE Qr coDE with your MobilE DEVicE to sEE thE futurE of plAnt DEsign or Visit tinyurl.com/avevae3d

aveva.indd 1 25/02/2013 14:59

14 Processing Shale Feedstocks 2013 www.eptq.com

At present, there are around 70 LNG terminals worldwide. Small-scale facilities such as the one in Nynäshamn are still the exception but offer a signifi-cant benefit, which is now boosting demand – their size makes them ideal for sites near industrial parks and cities, keeping them close to customers and the point of use. The Stockholm terminal, for example, also supplies LNG to the neighbouring crude oil refin-ery, run by the company Nynas. From this natural gas, the refinery generates the hydrogen it needs to process crude oil. In the past, it used naphtha, but the switch to natural gas will cut the refinery’s CO2 emissions by up to 58 000 tonnes per year.

In those instances where LNG plant capacity is less than 200 000 tonnes per annum, and Capex and simplicity are important, the Linde Multi Stage Mixed Refrigerant (LIMUM) single mixed refrigerant process shown in Figure 1 can be considered. This process uses Linde’s own plate-fin heat exchangers and is paired with the company’s coil-wound heat exchangers. In either variation, the process is an energy-efficient alter-native to expander processes for peak shaving and small LNG plants.

Ethylene plant technology improvementsEfficiently pushing feed through an ethylene plant is one of the most important aspects of profitable ethylene plant operations. Modern compressor design has evolved rapidly over the past 10 years, as the typical world-scale ethylene steam cracker rating exceeds over 1.0 million metric tons per year (mtpy). Steam turbine-driven ethylene compressors generate high horsepower and are the largest compressors produced by industry manufacturers such as Mitsubishi Heavy Industries Compressor Corporation (see Figure 2). This type of single-shaft, multi-stage compressor forms the heart of a petrochemical plant. Compressors for ethylene plants are ordinarily a compressor train of one of three types: compressors for charge gas, for ethylene gas or for propylene gas.

Other critical areas of the ethylene plant that have seen significant improvements include water treatment technology for plant processes and the downstream

fractionation train. Water treatment technology drives profitability, reliability and sustainability for ethylene producers by reducing or preventing fouling and corro-sion. For example, Nalco’s proprietary Actrene technology improves the efficiency of ethylene plant de-ethanisers and depropanisers by extending the run length to eight years or more. This technology reliably mitigates and controls fouling in light ends fraction-ation units. Fouling and corrosion control is also important for maintaining continuous operation of an ethylene plant’s pyrolysis gas compressors.

In addition, compressor corrosion and fouling control technology enables up to 10 years of continuous opera-tion of pyrolysis gas compressors, setting new industry standards for compressor performance. Coke formation and resulting fouling in other areas of the ethylene plant can be seen in the pyrolysis furnaces. Coke formation will impede heat transfer and restrict process flow. Recent developments such as Nalco’s proprietary Coke-Less anti-coking programme suppress furnace coke formation, which increases capacity, improves ethylene yield, lowers TMT, reduces CO formation, extends run length, reduces fuel consumption, reduces steam-to-hy-drocarbon ratio and eliminates sulphiding agents. The anti-coking programme also leads to improved heat transfer and lower pressure drop, and a potential exten-sion of coil life.

Polyethylene technology trendsThe global polyethylene industry experienced strong growth over the last five years and is expected to continue advancing as it reaches approximately $148.1 billion in 2017, with a compounded annual growth rate of 3.5% over the next five years, according to a recently published study by Lucintel entitled Research & Markets: Global Polyethylene Industry 2012-2017: Trend, Profit and Forecast Analysis. According to the study, strategies such as new product innovation, processes and feedstock technologies are expected to help players capture market share. Lucintel has analysed the global polyethylene industry and presents its findings in the study. The following is a brief summary of the detailed study.

The Asia Pacific (APAC) region dominates the polyeth-ylene market and represents 41.8% of the global market. A combination of factors such as feedstock price (crude oil and naphtha), feedstock availability, lightweight properties, energy costs, environmental issues and government regulations are affecting the industry dynamics significantly. Polyethylene is a consolidated industry and consists of high-density polyethylene (HDPE), linear low-density polyethylene (LLDPE) and low-density polyethylene (LDPE) as the segments.

China and India are expected to drive the polyeth-ylene industry due to low-cost labour, downstream processing capacity additions and government- supported subsidy packages. The introduction of ultra-high molecular weight polyethylene and sugar cane-based polyethylene are emerging trends that are expected to affect the future growth in the industry.

In other areas of the world, companies are building new polyethylene capacity. The Braskem-Idesa

The execution of functional safety assessment and validation must take place on every safety project and must be carried out by functional safety experts

Figure 2 Steam turbine-driven ethylene compressors from Mitsubishi Heavy Industries Compressor Corporation

proc trends .indd 3 26/02/2013 11:16

polyethylene project in Mexico is a good example of new polyethylene production plant project scope and objectives. This project, named Ethylene XXI, will be the largest private petrochemical facility in Mexico. It is being built in the city of Nanchital in the municipal-ity of Veracruz, in southeast Mexico. It will produce 1.05 million tonnes of polyethylene a year from ethane feedstock. Braskem-Idesa is a joint venture between Brazilian petrochemical company Braskem and a Mexican petrochemical group, Grupo Idesa. Braskem and Idesa respectively hold 65% and 35% interest in the joint venture.

The purpose of the project is to reduce the gap between Mexico’s local polyethylene production and demands, which are currently being met by importing one million tonnes of polyethylene every year.

The joint venture will own and operate the polyeth-ylene production facility. The construction of the facility is estimated to cost approximately $2.5 to $3 billion, which will represent the biggest foreign direct investment (FDI) in Mexico by a private Brazilian company.

The integrated petrochemical complex will include an ethane cracker, two HDPE plants and an LDPE plant. The ethane cracker will have a nominal capacity of about 1.0 million tonnes per annum. The first HDPE plant will have a capacity of approximately 400 000 tonnes per annum, while the second HDPE plant will produce 350 000 tonnes of polyethylene per annum. The LDPE will have a nominal production capacity of 300 000 tonnes per annum.

The twin HDPE plants will be based on the propri-etary Innovene S slurry high-density PE technology developed by Ineos Technologies. According to avail-able information, the Innovene S slurry process requires low investment and operating costs. It features two-reactor bimodal technology and combines circulation, heat exchange and reaction volume all in one system.

The lone LDPE plant will be based on LyondellBasell’s proprietary Lupotech T process tech-nology, one of the world’s most widely used high-pressure LDPE processes. Technology for the upstream ethylene cracker plant will be supplied by Technip.

Ethane that will be used as raw material for the Veracruz polyethylene manufacturing facility will be supplied by Pemex Gas y Petroquímica Básica (Pemex Gas). As per an agreement signed between Braskem-Idesa and Pemex Gas, the latter will supply 66 000 barrels of ethane a day for a period of 20 years. The project is located in close proximity to the Pemex facili-ties, which provides easy access to ethane. The site also has easy access to highways, railroads and ports.

Mitsubishi Heavy Industries Compressor Corporation (MCO), a wholly owned subsidiary of Mitsubishi Heavy Industries (MHI), was involved in supplying five compressors and three steam turbines for the facility. GE was contracted in April 2012 to supply its hyper-compressor and booster compressor technologies for the LDPE plant.

www.eptq.com

SAMSON AG · MESS- UND REGELTECHNIK Weismüllerstraße 3 60314 Frankfurt am Main · GermanyPhone: +49 69 4009-0 · Fax: +49 69 4009-1507 E-mail: [email protected] Internet: www.samson.deSAMSON GROUP · www.samsongroup.net

A01

120E

N

Partner with the Best

With over 50 independent subsidiar-ies and more than 220 engineering and sales offi ces spread across the world, SAMSON ensures the safety and environmental compatibility of your plants on any continent.

To offer the full range of high-quality control equipment used in industrial processes, SAMSON has brought together highly specialized compa-nies to form the SAMSON GROUP.

proc trends .indd 4 27/02/2013 10:52

NATCO

Cameron

PETRECO

RAISING PERFORMANCE. TOGETHER™

AD00387P

F L O W E Q U I P M E N T L E A D E R S H I P

CAMERON®

CONSEPT ®

CYNARA®

HYDROMATION®

KCC™

METROL®

MOZLEY®

NATCO®

PETRECO®

PORTA-TEST®

TST-CFU™

UNICEL®

VORTOIL®

WEMCO®

As the industry’s most comprehensive solutions provider, Cameron’s Process Systems

division integrates the strengths of NATCO and PETRECO to deliver a wide range

of solutions for today’s refiners.

• Industry-leading engineering expertise

• Diverse portfolio of solutions and services

• Extensive aftermarket services network

• Project management capabilities

Discover a higher level of performance and value at www.c-a-m.com/ProcessSystems

Integrated Strengths and Refining Solutions.Cameron’s Process Systems division delivers advanced products and processes for your refining needs.

• Industry-leading product support

• Advanced laboratory and pilot testing

• Full-service project support

• Cameron commitment to quality

CAMER-1125_Refining_PTQ.indd 1 2/21/13 9:50 AMcameron.indd 1 25/02/2013 15:00

Shale gas feeds petrochemical expansion

Capital investment for petro-chemical projects now on the books will bring petrochemi-

cal project activity in North America to a level not seen since the 1960s. These process invest-ments are primarily related to ethane-based steam crackers and other olefins-producing assets. Other major investments include propane dehydrogenation (PDH) units, gas-to-liquids (GTL) plants, methanol and aromatics production facilities. In parallel, the 500 or so midstream gas processing, gas treating and fractionation facilities in the continental US will need to be upgraded or expanded to meet pipeline specifications (with refer-ence to corrosive CO2, H2S, nitrogen, water and so on) in the transport of shale-based natural gas (as well as conventional gas) to new steam crackers and planned LNG export facilities.

Since the 1970s, several genera-tions of high natural gas prices in North America have led to an over-seas exodus of the petrochemical industry. Actually, it was not only petrochemical processors that left North America — alumina, ferti-lizer, cement, steel mills and other energy-intensive manufacturing industries also found other coun-tries with lower fixed and variable costs. However, energy costs based on $3.50/MMBtu (or less) for natu-ral gas are bringing these industries back to the US. Natural gas prices in Europe and Asia are expected to remain relatively high (>$12 MMBtu) in the long term.

Since it costs, on average, $8.0 to $10.0 million to bring a new shale well into commercial production,

North American ethylene capacity is set to increase significantly with new crackers coming online after 2016, plus higher production of propylene and other derivatives

ReNé GoNzAlez

upstream drillers are challenged to turn a profit with natural gas prices at their current low levels. Shale liquids production (crude oil and condensate) is currently the profit driver for the upstream drilling business. But beyond 2016, the onus is on leveraging the plentiful and cheap suppliers of natural gas (“wet” and “dry” gas) in the US for LNG export and as feedstock (primarily ethane) for at least seven world-scale steam crackers

announced in the US. In addition, about 15 licences had been submit-ted to US authorities as of December 2012 for construction of LNG liquefaction facilities and export terminals. However, most experts doubt that all 15 LNG projects will come to fruition due to political factors, environmental opposition and shifting global market dynamics.

Variability complicates gas treatmentWhile there are close to 500 gas processing plants in North America, older low-volume processing plants are being replaced with new plants that are

more efficient. In addition, these plants are large-volume operations, increasing overall daily processing capacity, according to James Tobin, Natural Gas Industry Analyst for EIA. It also appears, he says, that more gas treatment plants are being built because many unconventional gas wells yield fewer natural gas liquids. This leads Tobin to conclude that the gas treating market is growing faster than the processing segment.

There is a lot of variability in shale gas quality relative to conven-tional gas, according to experts. For example, Keith Bullin, Senior Consulting Engineer for Bryan Research & Engineering (BR&E), recently noted that the Antrim Shale has a high nitrogen concen-tration, whereas New Albany shale wells show high CO2 concentra-tions. Economically treating and processing these gases requires the ability to handle a great deal of variability in the same field.

Treatment often begins at the well-head, offers Bob Dunn, President of the Gas Processors Association (GPA). Contaminants such as highly corrosive CO2 and H2S are removed at a treatment facility near the field or at a gas processing plant. “Removing the CO2 near the field is often done for pipeline protection,” he remarks.

Pipeline quality standards limit the amount of CO2, nitrogen, oxygen and water vapour in the gas stream, in addition to a heating value limit of about 1035 Btu per cubic foot. In some cases, when plants are not yet available, waivers are granted for a limited time, according to Dunn. This enables

www.eptq.com Processing Shale Feedstocks 2013 17

Shale liquids production (crude oil and condensate) is currently the profit driver for the upstream drilling business

rene.indd 1 25/02/2013 19:27

18 Processing Shale Feedstocks 2013 www.eptq.com

said the expansion plans were in response to new low-cost ethane and other light NGLs becoming available as a result of shale gas production. Expansion of Petro 1, originally set for year-end 2014, is scheduled for 2015. Before the projects were announced, cracker capacity was 567 000 tpy and 522 000 tpy, respectively.

Midstream services company Enterprise Products recently reported it will build a PDH unit in Texas. In order to meet global market requirements for polymer-grade and chemical-grade propylene, almost two dozen PDH units have been announced since 2010, primarily in China. Similar units are beginning to be announced in the US to meet the growing propylene deficit. Numerous refinery FCC units throughout the world have been reconfigured to increase propylene production. Propylene-producing FCC technology has scored numer-ous successes over the past 18 months, with new units announced in Thailand, Brazil and elsewhere. However, in the US, refinery-based propylene production is still not in sufficient volumes to compensate for the disproportionately lower propylene production from ethane-based steam crackers.

The Enterprise Products PDH unit will have a capacity of 750 000 tonnes/year of polymer-grade propylene (PGP) and will use 35 000 bpd of propane feedstock.

producers to begin marketing gas from new fields as the processing plant is built.

If the gas is not pipeline quality, it typically is processed at a refrig-eration or cryogenic plant. In refrigeration units, the gas is cooled and the NGLs precipitate out, explains Bullin, removing more than 90% of the propane and about 40% of the ethane. Other heavier components are almost entirely removed.

In cryogenic units, gas tempera-ture is reduced to -120 to -150°F, he explains. The temperature drop causes the ethane and other heavier hydrocarbons to condense, remov-ing more of the natural gas liquids and 90-95% of the ethane.

As previously noted, there were more than 500 gas processing plants in the US before 2005. Most of these were small, relative to the size of a typical crude oil refinery, and were in remote areas of the US Southwest and the Rocky Mountains. Since that time, addi-tional plants have been added at least in part to address demand in unconventional gas plays. This has resulted in the need to build modu-lar facilities in areas where gas processing and gas treating facili-ties previously did not exist, such as in North Dakota. Other shale plays, including Niobrara, Woodford, Eagle Ford, Marcellus and Barnett, are ramping up natu-ral gas plant capacity. When a horizontally drilled shale gas well

starts flowing, there is often a tremendous increase in volume, making it critical that the infra-structure is in place to process the gas and move it to market.

Prior to the 1990s, most process-ing operations were owned by the pipeline or gas production compa-nies. When a producer planned to develop new fields, the processors were fully informed and could build capacity to match production. There are now many independent midstream processors, which relieves pipelines and/or producers of the capital requirements for processing, but also raises coordi-nation issues that are a big challenge for emerging shale markets, making coordination between service providers and producers one of the biggest busi-ness challenges in the industry.

Ethane-based steam cracking Competitive economics that could not have been foreseen only three years ago now make ethane-based steam cracking projects in the US competitive against other ethane and naphtha/gas oil steam crackers in Asia and Europe. For example, Westlake Chemical in Houston will perform planned maintenance and an expansion of the Petro 2 ethyl-ene unit at the company’s complex in Lake Charles, Louisiana, in Q1 2013. This expansion will increase ethane-based ethylene capacity by about 104 000-109 000 tonnes/year (tpy). In 2011, Westlake Chemical

Panoramic view of Woodside’s Pluto LNG Plant in Western Australia with engineering, procurement and construction management by Foster Wheeler WorleyParsons JV. The plant is operated by Woodside in joint venture with Kansai Electric and Tokyo Gas CourtesyofWoodside.Source:FosterWheeler

rene.indd 2 25/02/2013 19:27

www.eptq.com Processing Shale Feedstocks 2013 19

The facility should be operational by 2015, Enterprise said. The company did not disclose the finan-cial details. “By 2015, with completion of expansions that have already been announced, Enterprise would have 708 000 bpd of [natural gas liquids] NGL fractionation capacity, which would provide up to 177 000 bpd of propane supply,” says the company. “Enterprise also has PGP storage facilities and a 102-mile [164 km] pipeline system, capable of delivering PGP to 18 downstream customers and to international markets through the partnership’s propylene export terminal in Seabrook, Texas,” adds the company.

In 2010, PetroLogistics brought on stream the world’s largest PDH unit on the Houston Ship Channel. “Some people may have that thought that was crazy at the time,” recalls Chuck Carr, Director of Propylene Studies at IHS Chemical. “But we now forecast about 150 000 bpd of propane demand is going to be added in North America by 2020. All of that is from the chemi-cal industry, with the North American fuel market for propane forecast for minimal growth.” The biggest and most recent move in propane is a plan by Dow Chemical to get into dehydrogenation. Dow announced in 2012 that it will produce propylene at its Freeport, Texas, complex using PDH technol-ogy. The Freeport complex is one of the largest chemical manufacturing sites in the world. The facility will produce 750 000 metric tons annu-ally of PGP and is scheduled to come on stream in 2015. The company says the facility will be the largest single-train PDH plant in North America.

Expanding infrastructureUse as a fuel directly and to gener-ate power remain by far the primary markets for natural gas, but the shale revolution has wrought fundamental change in the upstream market. Chemical compa-nies across North America are beginning to believe in the new reality of plentiful and reasonably priced natural gas. Petrochemical industries, including olefins

producers, PDH, polymer and aromatics producers all expect North American natural gas prices, currently at $3.45 per MMBtu at the end of January 2013, to remain competitive for the long term. Lawmakers in the US government, including 89 Republicans and 21 Democrats, petitioned US Department of Energy (DOE) Secretary Steven Chu on 31 January to move forward with allowing construction of liquefaction facili-ties and LNG terminals for exporting LNG to European and Asian markets, where gas sells three and four times as much as it does in the US market.

US manufacturers, power genera-tors and chemical processors are opposed to LNG exports for fear

that natural gas prices will skyrocket as a result of multiple LNG export outlets. However, many analysts believe shale gas production will continue to expand so that only slight increases in gas prices can be expected with a simultaneous LNG export market and a growing domestic consump-tion, primarily by the petrochemical processing industry.

According to a 25 January report by Jennifer A Diouhy in the Houston Chronicle concerning the new LNG export opportunities from the US: “Additional costs of liquefying [cryogenic liquefaction] natural gas, shipping it overseas and then converting it again at its destination could add $6.30 to $8.39 to the price per MMBtu,” as she

noted from a government commis-sioned study. She noted that the DOE is reviewing applications from more than a dozen companies (15 companies have submitted applica-tions for LNG export facilities at press time) to export at least 22.6 bcf of natural gas to countries that do not have free trade agreements with the US. Post-Fukushima Japan, for instance, is eager to find power sources to replace nuclear power after the 2011 earthquake and tsunami that nearly destroyed the Fukushima Dai-Ichi plant. To be sure, the growing demand for safe and clean power sources through-out the world puts natural gas at the forefront not only as a petro-chemical feedstock, but as a “base load” power source instead of coal.

Methane, the most basic hydro-carbon molecule with one carbon atom attached to four hydrogen atoms (CH4) is not simply for turn-ing generators and heating beans on the stove; it is also the primary feedstock for methanol and ammo-nia. While ethane is the primary natural gas molecule in shale gas, there is also a market for the meth-ane, propane and butane produced from most shale plays throughout the world. As previously noted, the main market in North America for ethane is as a feedstock for steam crackers to make ethylene. That, in turn, is made into polyethylene (used in plastics products) or other derivatives.

Propane and butane are mostly fuels, but the shift in steam cracker feed slates from naphtha and mixed natural gas liquids to primarily ethane means more ethylene out of the other end, and less of the important propylene and butadiene co-products. While it is clear that the PDH technology for propylene production has been gaining momentum since 2010, other petro-chemical manufacturers are also exploring methanol-to-olefins to increase propylene production. Needless to say, propylene is used primarily for polypropylene, another high-volume thermoplastic. Butadiene is an essential compo-nent in elastomers. Most tyres are styrene butadiene rubber; styrene is made from ethylene plus benzene

Competitive economics now make ethane-based steam cracking projects in the US competitive against other ethane and naphtha/gas oil steam crackers in Asia and Europe

rene.indd 3 25/02/2013 19:27

fundamental change in their busi-ness. “Shale gas and the associated NGLs are a game-changer for our members,” says Cooper. “We are reading on a weekly basis about expanded production and new chemistries based on this new supply of energy and feedstocks. The producers tell us that natural gas is affordable and plentiful, not just today, but on a structural and strategic-planning level. We expect it to be a dependable source for a long time,” Cooper continues.

Regardless as to how well capital-ised the upstream drilling and production business can expect to be over the next several years, adequate midstream infrastructure is required to efficiently transport natural gas feedstock to market. For example, two pipeline projects announced over the past year will transport ethane from Pennsylvania to major petrochemical centres. Last

year, Sunoco inked a deal to move ethane from the Marcellus shale region to Nova Chemical’s mega complex at Sarnia, Ontario. Then, in January, Enterprise Products Partners confirmed plans to build a 1230-mile line from Pennsylvania to the Gulf Coast, to begin commercial operations in Q1 2014.

Since post-World War II, pipeline projects completed from the Gulf Coast to the US East Coast have been too numerous to mention. In a radical turn of events, the Eastern Appalachia-to-Texas, or Atex line, will be built with an initial capacity of 190 000 bpd of ethane, and trans-port rates will start at $0.15 a gallon, according to Enterprise reports. Chesapeake Energy will be the anchor shipper, having commit-ted to 75 000 bpd over the first five years, the company says. To save time and money, other Gulf Coast

20 Processing Shale Feedstocks 2013 www.eptq.com

(ethyl benzene), with polystyrene constituting the third major thermoplastic.

As if to signal the dawn of a new era, the largest methanol producer in the world, Methanex Corporation, said early in January that it would relocate at least one of its idle trains from its complex in Cabo Negro, Chile, to an existing facility near Geismar, Louisiana. Site-specific engineering has begun, and the 1.0 million mtpy plant is expected to be operational in the second half of 2014. Early in February, Jacobs Engineering was awarded the contract to reconstruct the Geismar plant. At the time of the announcement, Bruce Aitken, President and Chief Executive Officer of Methanex, commented, “The outlook for low North American natural gas prices makes the State of Louisiana an attractive location in which to produce meth-anol. The timing of this project is excellent; there is strong demand growth for methanol globally and there is little new production capac-ity being added over the next several years.”

The Methanex plant is one of several that will increase North American methanol capacity by 158% to 3.48 million mtpy by 2014, according to Dewey Johnson, Senior Director of Chemical Market Research at IHS Chemical in Houston.

It takes 32 MMBtu of natural gas to make one metric ton of metha-nol, so 3.48 million metric tons of methanol requires 111.36 trillion Btu (111.36 bcf) of gas, says Johnson. By itself, increased metha-nol output is not enough to move the needle on US gas prices, but he notes that it is certainly a signifi-cant new source of demand. “Methanol and fertilizer from methane certainly are important end-use markets, but we look mostly at olefins, ethylene and co-products, and their derivatives,” says James Cooper, Vice President of Petrochemicals for the American Fuel & Petrochemical Manufacturers (AFPM) Association. For chemical producers, the shale gas boom has surpassed being merely a benefit to becoming a

to East Coast pipelines are being “reversed.”

Carlo Barrasa, Director of NGLs and Cracker Economics at IHS Chemical, estimates ethylene steam cracker feeds were about 40% ethane in the past generation. Barrasa says, “Today, feed slates are 70% ethane, and that will continue to creep higher every year.” Barrasa notes that at $0.44/gallon for ethane, the production cost for ethylene comes to $0.18/pound. “The market price for ethyl-ene is about $0.70/pound, so cracker operators are experiencing a tremendous profit margin right now,” he observed in early 2012. “They are taking any opportunity to optimise their trains to consume ethane,” he added.

Ethylene steam crackersIn June 2011, Shell announced that it was developing plans to build a large steam cracker with integrated derivative units in the Appalachian region. “Building an ethane-fed cracker in Appalachia will unlock significant gas production in the Marcellus by providing a local outlet for the ethane,” says Ben van Beurden, Shell’s Executive Vice President for Chemicals. “This fits well with our strategy to strengthen our chemicals feedstock advantage and would be another step in growing our chemicals business to meet increasing demand.” The company released a statement saying the complex included a steam cracker to turn ethane produced from the Marcellus into ethylene and other petrochemical building blocks. In addition to the cracker, Shell said in the release that it was “also considering poly-ethylene and monoethylene glycol units to help meet increasing demands in the North American market. Much of the polyethylene and monoethylene glycol produc-tion will be used by industries in the Northeast.”

In a news release, Shell says it has “an array of long-term options to monetize natural gas. Extracting ethane and other natural gas liquids (to produce) petrochemicals is one of these options, which also include developing shipping

“Shale gas represents a once-in-a-century change in the competitive balance worldwide”

rene.indd 4 25/02/2013 19:27

www.eptq.com Processing Shale Feedstocks 2013 21

hard pressed to change the new dynamics in the North American gas market.” For example, by several estimates, two-thirds of the plastics converters in North America are within 500 miles of the Marcellus Shale play, making the economics for world-scale ethane-fed steam crackers, the basic petrochemical to plastics building block, a viable option in what was previously thought of as an isolated market with limited opportunity for down-stream expansion, in spite of low ethane feedstock costs.

The American Chemistry Council recently completed a study entitled Shale Gas and New Petrochemicals Investment: Benefits for the Economy, Jobs and U.S. Manufacturing. It antic-ipates a $16.2 billion private investment over several years in new plant and equipment for manufacturing petrochemicals. That investment would lead to a 25% increase in US petrochemicals capacity and $32.9 billion in addi-tional chemical industry output, the study estimates.

from Haldor Topsøe and Fischer-Tropsch (FT) technology from Velocys. Haldor Topsøe’s ATR is a proprietary technology for reform-ing natural gas into synthesis gas, a mixture of hydrogen and carbon monoxide (CO). In the GTL plant, said the Calumet announcement, this synthesis gas will move through Velocys’s FT process, converting it into long-chain hydrocarbons, typi-cally paraffins, naphthenes and aromatic compounds.

Game changer“Shale gas represents a once-in-a-century change in the competitive balance worldwide,” according to Garrett Gee, Director of Chemical Advisory Services at Price-waterhouseCoopers. He added, “This is a major capital opportunity to play a global game very differ-ently.” He stresses that “Even if the estimates of shale gas supply are off by half, it still represents a huge volume of light hydrocarbons. Even if LNG exports of US-produced gas go ahead full out, all that would be

solutions for LNG; proprietary GTL technology to produce fuels, lubri-cants and chemicals; and gas-for-transport in markets focus-ing on heavy-duty vehicles, marine and rail transportation.” The situa-tion in the Marcellus is “a classic trapped ethane problem,” observes Mark Eramo, Vice President of Chemical Research and Analysis at IHS Chemical. “It is the same thing we saw in Saudi Arabia in the past two decades. You can either build a cracker on site and ship the deriva-tives, or you can build a pipeline to transport the ethane. Both are viable.”

Calumet Specialty Products Partners recently announced that it is considering adding a 1000 bpd GTL plant to its Karns City, Pennsylvania, speciality products plant. Production could begin in second-half 2014. Calumet has commissioned Pasadena, Texas-based Ventech Engineers International to design and deliver the GTL plant that will use a propri-etary autothermal reformer (ATR)

Air Pollution Control Technologiesfor Off-Gas Treatment at Glycol Regeneration Processes, Amine Treaters, Nitrogen Rejection Units and More!

• High Destruction Efficiency (99%+) and Low Operating Costs

• Small Carbon Footprint for Green House Gas Compliance

• Special Materials of Construction & Design Considerations for Acid Gases

+1 414-365-6400www.anguil.com

rene.indd 5 25/02/2013 19:28

propylene passion

Yet another sign that the world is aching for more

propylene. Profit from the global propylene gap with

a proven, innovative solution from UOP.

No matter what your feedstock and production realities,

UOP can bring you the on-purpose propylene solution that’s

just right for you: UOP OleflexTM (propane dehydrogenation)

process; UOP Advanced MTO Process; PetroFCCTM process; RxProTM process and

the Total Petrochemicals/UOP Olefin Cracking process. For nearly 100 years, UOP

has been developing the cutting-edge technologies our clients rely upon to drive their

growth, profitability and operational flexibility. Our broad propylene solution portfolio

is yet another example of our unwavering commitment to innovation.

Process Technology • Catalysts • Adsorbents • Performance Equipment • Profitability ConsultingUOP LLC, 25 East Algonquin Road, Des Plaines, IL 60017-5017, USA phone: +1-847-391-2000 fax: +1-847-391-2253 www.uop.com

© 2013 UOP LLC. All rights reserved.

UOP_Propylene_Passion_Ad_A5_Ad A5 148mmx210mm UOP6010 2/27/13 11:34 AM Page 1

uop.indd 1 28/02/2013 09:26

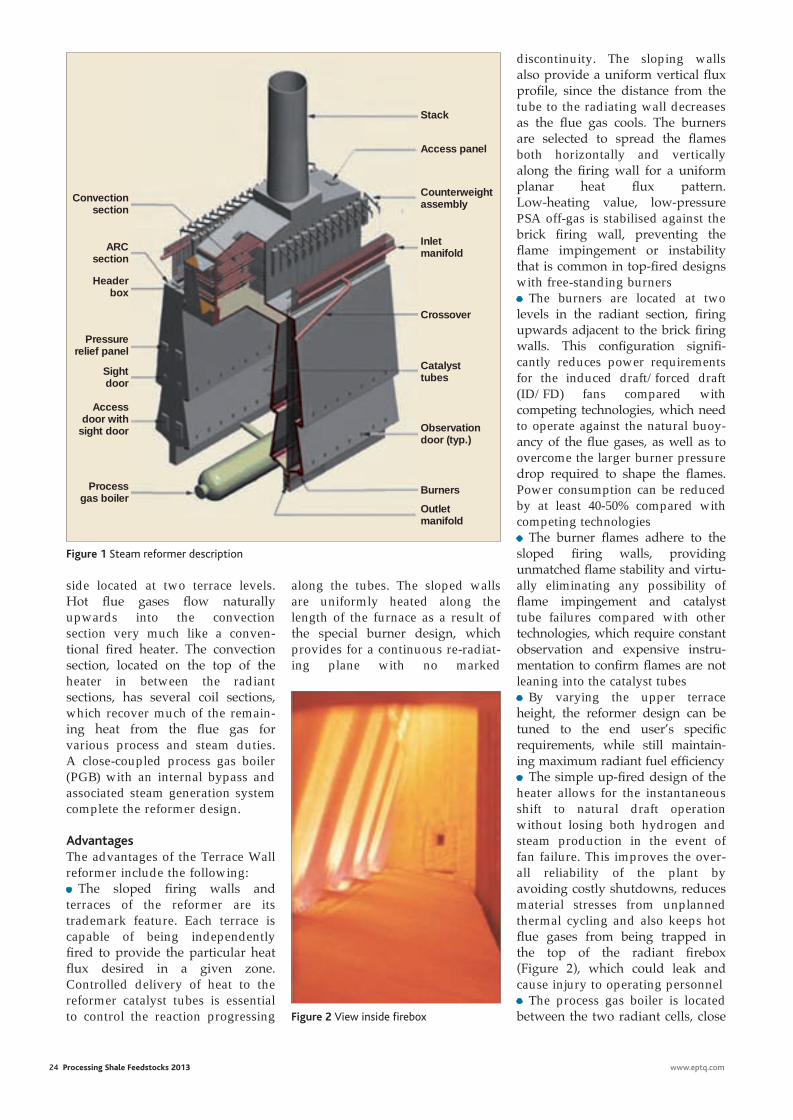

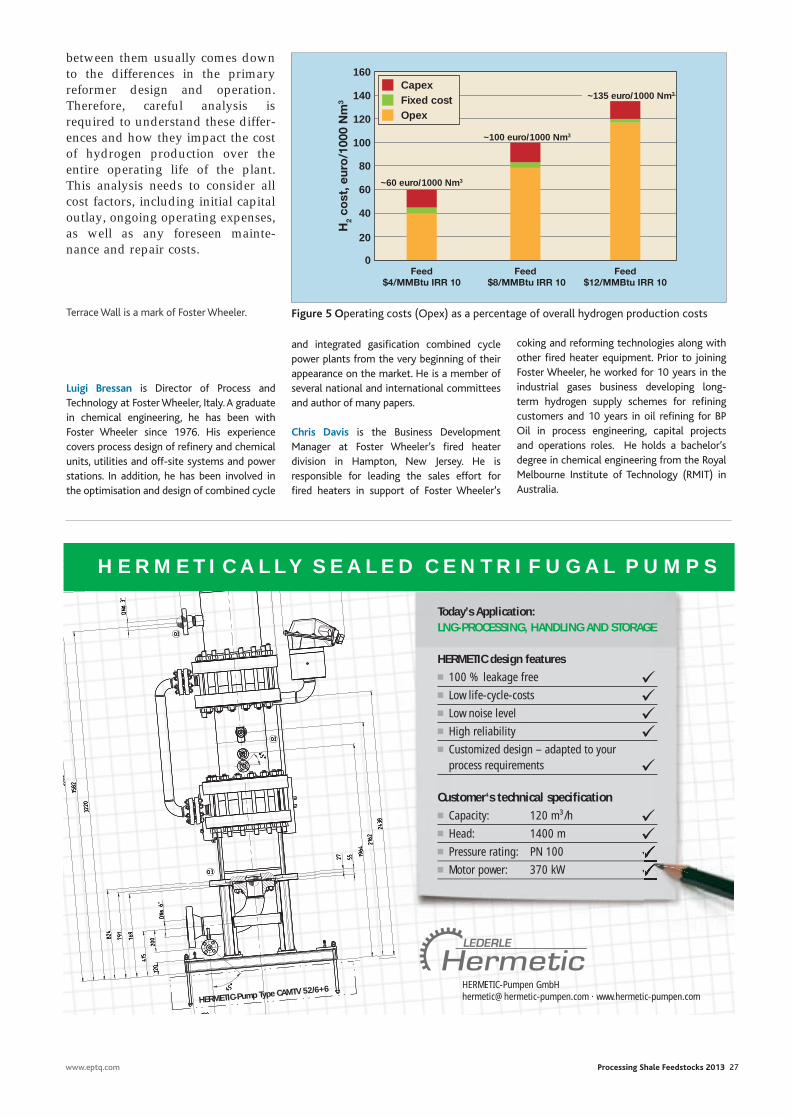

Driving down costs in hydrogen production

The global demand for refinery hydrogen has increased significantly over the past

decade due to changes in available crude feedstocks and tighter envi-ronmental regulations, which have forced the refining industry to reduce sulphur, olefins and aromat-ics content in transportation fuels. This, coupled with the continued growth in diesel demand, means that refiners are investing heavily in both hydrotreating and hydroc-racking facilities, and are constantly looking for access to low-cost, reliable sources of high-purity hydrogen.

Foster Wheeler pioneered steam methane reforming (SMR) technol-ogy and has delivered more than 100 hydrogen and synthesis gas plants around the world, with a total installed capacity of more than 3.5 million Nm3/h of hydrogen. The company’s patented and proprietary Terrace Wall reformer furnace was developed in conjunc-tion with SMR technology in the early 1960s. Updates and improve-ments to plant efficiency, lower maintenance costs, simplified oper-ations and enhanced plant safety have been documented in previ-ously published articles.

These hydrogen-producing SMR plants process a wide range of feedstocks from natural gas to naphtha and range in size from 5000 to 200 000 Nm3/h. The range of hydrogen solutions provided include:• Optimised plant design and oper-ating parameters tailored to the operator’s requirements, integrating overall plant and reformer furnace design to reduce total lifecycle costs

An optimised hydrogen plant design achieves the right balance of minimising both Capex and Opex costs, while meeting the specific objectives of the end user

Luigi BressAn and Chris DAvisFoster Wheeler

• Full understanding of constructa-bility issues and impact on total installed cost, with the ability to incorporate a high degree of modu-larisation of the Terrace Wall reformer, reducing construction costs• One-stop shop, providing consist-ency through all design phases, ensuring single-point accountability for process and operational guarantees• Safety in design that incorporates the latest state-of-the-art design principles as well as end user feed-back, to enable safe and reliable plant operations.

steam reformer-based technologySMR continues to be the leading technology for hydrogen produc-tion and, although it is a mature technology, incremental economic improvements are being continu-ously developed, which improve overall plant efficiency, reduce the cost of hydrogen production and minimise the impact on the envi-ronment by reducing CO2 emissions.

The hydrogen production plant consists of five main sections:• Treatment section Feedstock is hydrotreated and the resulting H2S is captured in a zinc oxide bed. Different schemes are available, with the most commonly used being a lead-lag reactor arrange-ment. Reaction temperatures are obtained by thermal exchange in the reformer’s heater convection section• Pre-reforming section A pre- reforming section is generally installed to eliminate the long-chain hydrocarbons in heavier feedstocks