impact of the innovative pharma industry on the polish economy · within the medical community. in...

TRANSCRIPT

www.pwc.pl

Impact of the innovative pharma industry on the Polish economy

ReportSeptember 2011

2

Table of contents

Summary 5

Overview of the pharmaceuticals sector in Poland 11

The role in the economy 33

Current environment and future prospects 63

Appendices

Glossary 73

Acknowledgments

We would like to thank all the innovative pharmaceutical companies, that have devoted their time and effort to the project. Completion of the analysis would not have been possible without the quantitative and qualitative data provided by PwC survey participants.

We would like to thank IMS Health for preparing chapter two: “An overview of the pharmaceuticals market in Poland”, providing data on the pharmaceuticals market in Poland and the additional expert comments, which significantly improved the quality of this report.

We would like to express our gratitude to all respondents who shared their views on current and projected trends on the pharmaceuticals market in Poland and globally. These observations allowed us to show our analysis in a broader context, which has proved to be very valuable.

Development of this report was sponsored by the Pharmaceuticals Research and Manufacturers of America (PhRMA) and we would also like to thank PhRMA for its financial support during this project.

Methodology

In our quantitative analysis we have calculated the contribution of the pharmaceuticals industry to the Polish economy. We define the pharmaceuticals industry as manufacturing companies operating in the Polish market, both domestic and foreign, and local branches of international companies engaged in the resale of drugs on the Polish market.

In our analysis, we focused in particular on the innovative part of the industry.

Our macroeconomic analysis was based on an Input-Output model, which was then enhanced with extensive PwC experience in market modelling exercises.

We took into account both the direct and indirect influence of this contribution.

Direct impact:

• The value added to the economy generated directly by the pharmaceuticals industry, including employees compensation, direct taxes and company surpluses.

Indirect impact:

• Value added generated by the suppliers of goods and services for pharmaceuticals businesses.

• The induced effect evoked by increased consumer spending of households, due to employment in the pharmaceuticals sector or other related sectors.

Apart from the results of our empirical analysis, we believe that there are number of additional areas in which the pharmaceuticals industry influences the economy in a positive way. As those specific areas may require a greater level of commentary, we provide the latter in the qualitative part of this section.

Acknowledgments and methodology

We conducted our survey among nearly 30 innovative pharmaceutical companies operating in Poland

Jak już wspomniano, innowacja opracowana oraz wdrożona przez innowacyjne przedsiębiorstwa farmaceutyczne przynosi korzyści gospodarce oraz społeczeństwu. Z tego względu, oczywistym wydaje się, iż należy wspierać maksymalne wykorzystanie efektów procesu innowacyjnego

• Sektory farmaceutyczny i biotechnologiczny przodują w rankingu najbardziej innowacyjnych gałęzi w Europie (udział wydatków na B&R w przychodach 2009)

• Wiele badań jakościowych opartych na analizach, które zostały opublikowane w renomowanych czasopismach medycznych (np. Lichtenberg, 2001 czy Caliskan, 2009), potwierdza, że zaawansowane metody terapeutyczne mają pozytywny wpływ na długość życia, a stosowanie innowacyjnych leków przyczynia się w 40% do tego efektu

Tytuł wykresu

Nota: Źródło:

Tekst

SummarySection 1

In this report, we show that the pharmaceuticals sector in Poland, and in particular its innovative part, is important to the economy (1 of 4)

The purpose of this report was to determine the impact of innovative pharmaceutical companies on the development of the Polish economy in the form of:

• the revenues to the state budget, employment, the commission market for subcontractors, the raising competitiveness of the Polish economy through transfers of know-how, promotion of cooperation between industry and the world of science and stimulation of innovation;

• participation of companies in educational activities, corporate social responsibility (CSR) programmes, as well as charity activities in an effort to improve the condition of Polish society

and

defining the challenges facing the innovative pharmaceuticals industry.

The external environment and pharmaceuticals markets

Poland is the sixth largest pharmaceuticals market in Europe in terms of sales value, which reached PLN 20.1 billion in 2010.

Per capita expenditure on pharmaceuticals in Poland is among the lowest in Europe and amounts to EUR 114 annually, representing 52% of the average expenditure on drugs per capita in Europe. At the same time, pharmaceuticals in Poland are among the cheapest in Europe; their price being only 44% of the European average.

Expenditure on drugs accounts for more than 25% of total healthcare spending.

Co-payment for reimbursed drugs is 32%. As for the level of the patient’s co-payment for all drugs, the figure is 67%; in other European countries it ranges between 25% and 49%. This range of co-payment demonstrates the serious underfunding of Polish healthcare in the pharmaceuticals area.

In Poland, public and private healthcare expenditure amounts to 7% of gross domestic product (GDP), while in Western Europe (WE) this figure stands at 10% of GDP. Public spending on healthcare alone in Poland is 4.7% of GDP, while in WE it is estimated to be 7.5% of GDP.

Insufficient funding of the healthcare system in Poland is the main barrier limiting patients’ access not only to medicines but also to healthcare services.

Structure of the pharmaceuticals market in Poland

In Poland, there are nearly 450 pharmaceutical companies, of which 62 are innovative enterprises.

The 10 largest representatives of the pharmaceuticals market generate nearly 50% of its value. In the top 10 there are 8 innovative companies and among them there are three biggest pharma enterprises in Poland. The top three enterprises have manufacturing plants and generate 23% of the total pharmaceuticals’ market value.

6

Impact of the innovative pharma industry on the Polish economy • Report 7

Summary

In 2010, innovative pharmaceutical companies delivered products with a value of PLN 9.4 billion to the Polish market, which represents 58% of the prescription and hospital drugs market. They produce over 70% of drugs used in hospitals; in the case of the retail market, the share is 55%.

Over two-thirds of drugs in terms of value, used in Poland, are imported.

Impact on the budget and GDP

In 2010 alone, the pharmaceuticals industry contributed PLN 1 billion to the state budget in the form of taxes and other charges (according to the Central Statistical Office [GUS]), of which 60% was paid by innovative pharmaceutical companies.

Innovative companies are also accountable for 50% of the value of social security contributions paid by the Polish pharmaceuticals industry, with employment reaching one-third of this industry.

The pharmaceuticals industry contributes c.0.8% of GDP, a figure which has increased by nearly 20% over the four years since 2006. Almost 0.5% of GDP is generated by innovative pharmaceutical companies.

Commission market and cooperation with suppliers

The value of cooperation with suppliers of goods and services amounted to PLN 7.2 billion in 2010.

In 2010, 50 thousand contracts were signed, of which 95% were with national contractors.

Nearly 40% of the contracts’ value is associated with production activity of innovative pharma companies.

Employment

The pharmaceuticals industry employs 31 thousand people, of which 11 thousand work in innovative companies.

Another 80 thousand to 90 thousand jobs are in wholesalers and pharmacies entities which are inextricably linked with and dependent on sales of pharmaceuticals.

Nearly 20% employees of innovative pharmaceutical companies are employed in connection with R&D and manufacturing activities.

Most of the sales staff, constituting c. 50% of employees, are young, highly educated people, living across Poland. In this regard, pharmaceutical companies are becoming a major employer for groups threatened with unemployment, i.e. young university graduates and those living outside major urban agglomerations.

The average wage in the pharmaceuticals industry is 60% higher than the national average, reaching PLN 5.2 thousand.

In this report, we show that the pharmaceuticals sector in Poland, and in particular its innovative part, is important to the economy (2 of 4)

Investments

Seven out of sixteen pharmaceuticals factories in Poland belong to innovative pharma companies.

These factories include newly established production facilities, as well as those acquired from other entities and purchased during the privatisation of the Polish pharmaceuticals sector.

Privatisation of one of the pharmaceuticals factories by an innovative pharma company worth USD 400 million was one of the largest equity transactions during the transition period in Poland. This process has been reviewed by the Supreme Audit Office as one of the most effective sector privatisations.

In Poland, innovative companies manufacture c. 430 products at a volume of 200 million packages per year.

The value of exports in 2010 amounted to c. PLN 3.6 billion, which represents 34% of total sales of the innovative pharma industry in Poland.

About 1400 people work in the production facilities of innovative companies, which constitutes 13% of all employees in innovative pharma companies.

In 2010, these companies invested PLN 120 million to further develop and modernise their factories.

Seven functional hubs have been created. They provide services for more than 100 international markets in all areas of outsourcing services such as IT, clinical, financial and accounting services, distribution and logistics.

Thanks to clinical trials performed in Poland by innovative pharma companies, the state budget receives c. PLN 240 million annually from taxes and other charges.

Clinical trials also yield alternative cost savings to the budget of the National Health Fund (NHF), since their scope includes a large number of patients and they are financed by sponsors rather than public funds.

Innovative companies also conduct numerous activities in know-how transfer within the medical community.

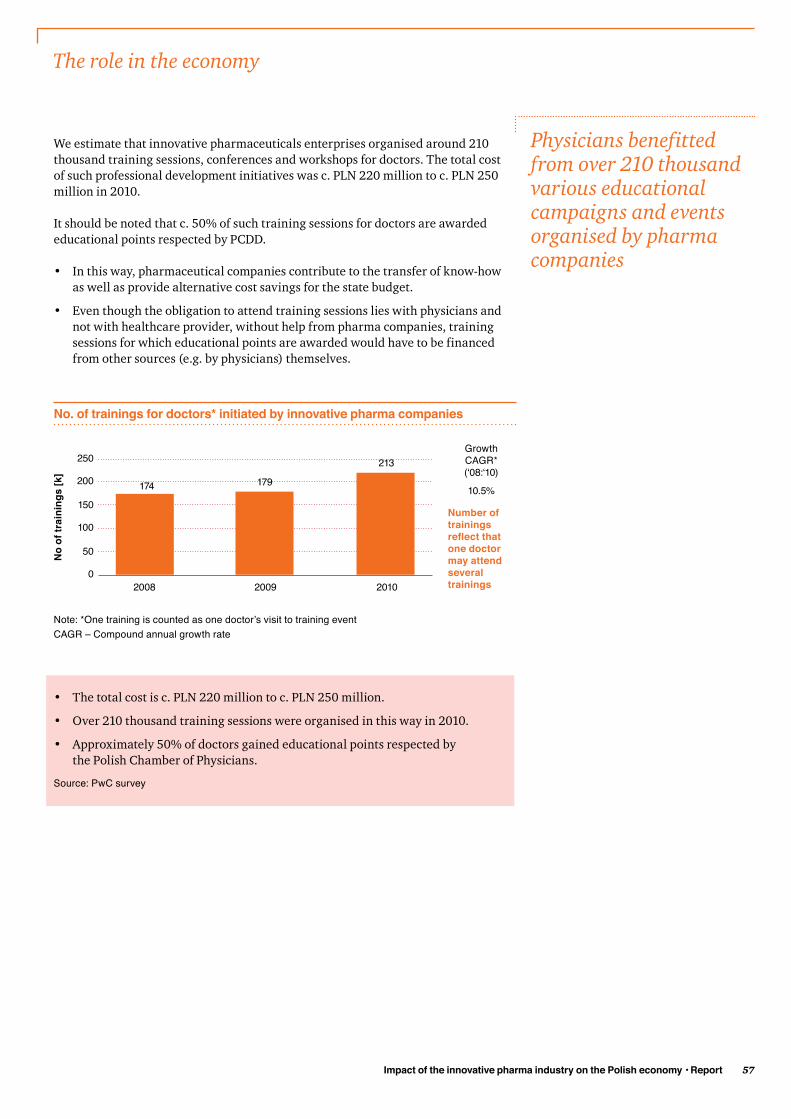

In 2010, innovative companies allocated more than PLN 220 million to organise 210 thousand training courses, conferences and workshops for physicians.

Half of the training sessions were rewarded with educational points by the Polish Chamber of Doctors and Dentists (PCDD) under the compulsory, professional development of physicians.

Education and CSR

Pharmaceutical companies operating in the healthcare sector play a special role in activities aimed at improving the health of Poles.

The pharmaceuticals industry focuses on health education and shares its knowledge and experience in this area. Pharmaceutical companies have allocated PLN 20 million to conduct 60 educational campaigns, which have benefited around 620 thousand people.

Innovative pharma companies are involved in about 150 CSR initiatives.

8

In this report, we show that the pharmaceuticals sector in Poland, and in particular its innovative part, is important to the economy (3 of 4)

Impact of the innovative pharma industry on the Polish economy • Report 9

Summary

Conclusions

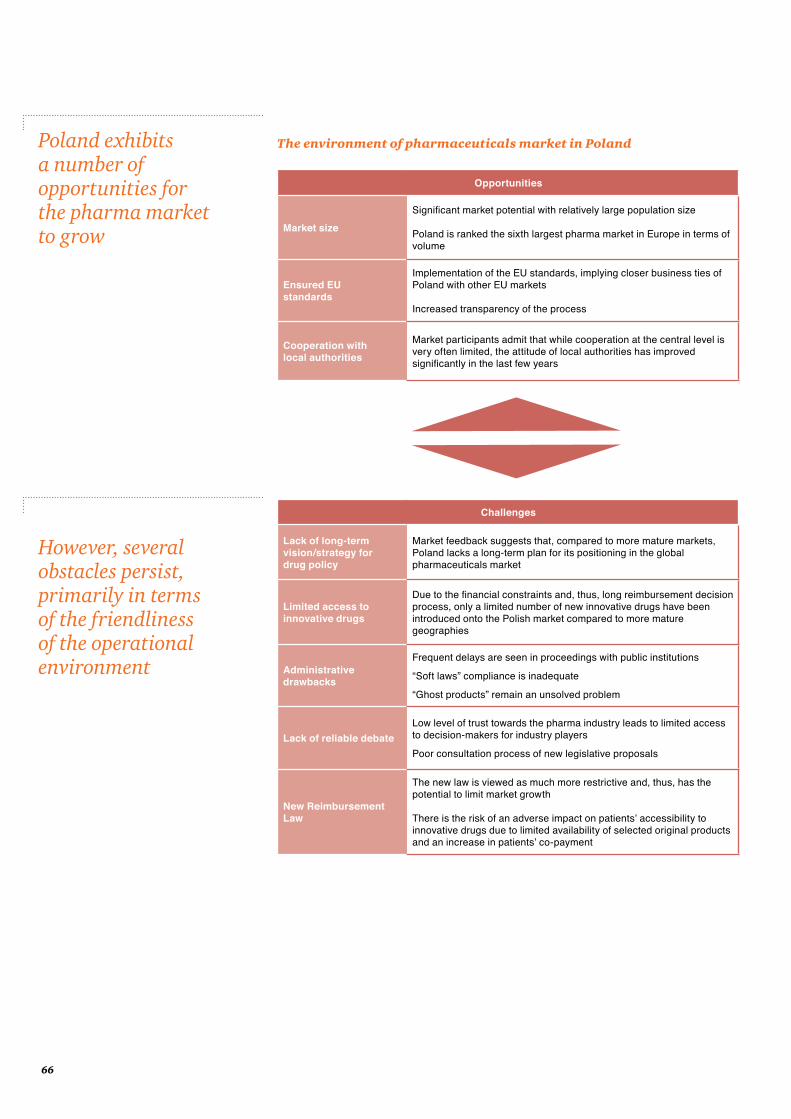

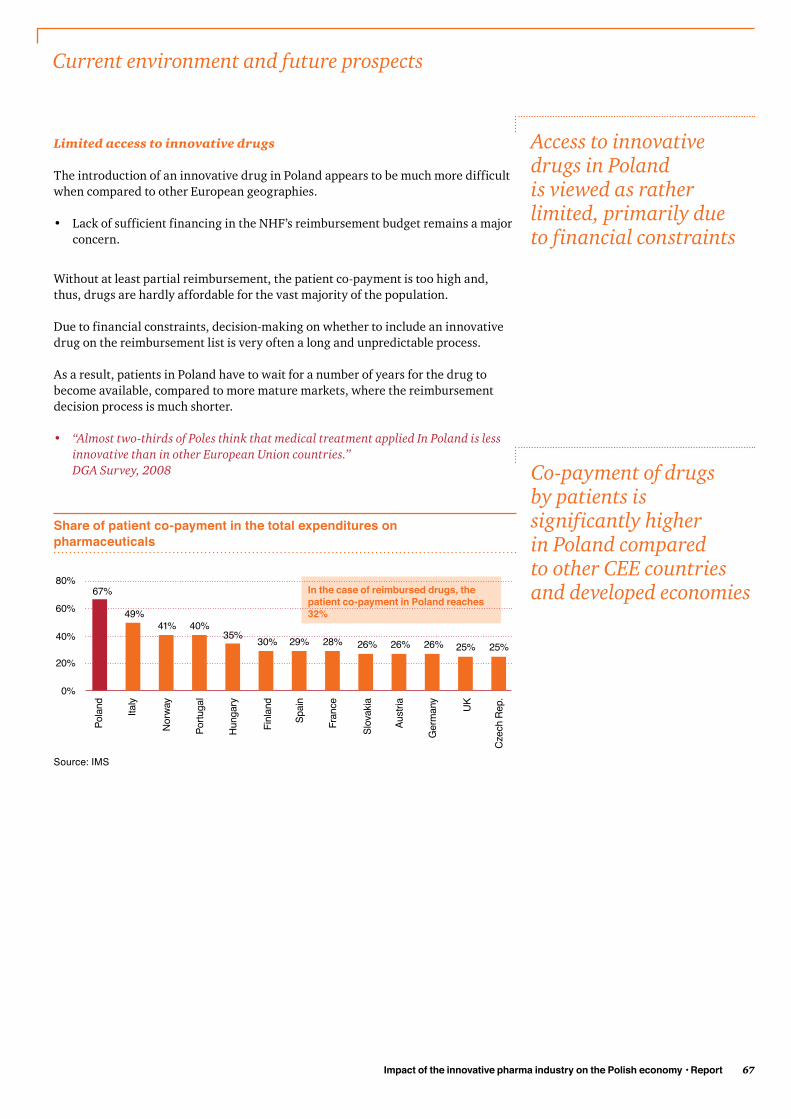

The unmet therapeutic needs of Polish patients, which require an increase in healthcare funding in order to reach a level of therapy availability comparable to other EU countries constitute an opportunity for increasing the engagement of innovative pharmaceutical companies in Poland.

In Poland, there is no long-term vision for an effective drug policy and its effective implementation.

Lack of consistent policy in this area, as well as insufficient public funding and delays in the processing of reimbursement decisions lead to the limited availability of innovative medicines for Polish society.

Poland is a country with some of the lowest prices for innovative medicines, as well as generic drugs. Significant price differences between countries lead to the export of Polish products to European markets.

Systematic implementation of EU regulations and the improved quality of Polish law will contribute to higher transparency of administration procedures. This is one of the key elements that determines decisions on locating of new investments.

The innovative pharma industry welcomes cooperation with local authorities. The quality of dialogue and debate with the central authorities is widely seen to be insufficient.

The recently adopted New Reimbursement Law could impact the stability of the pharmaceuticals market negatively:

• The profitability of wholesalers and pharmacies is expected to decline and consolidation at both these levels of distribution to widen.

• Due to the lack of rebate, patient co-payment may increase, and access to medicines may further deteriorate.

• The solutions implemented by the New Reimbursement Law may lead to the increase in parallel exports of medicines intended for the domestic market to other EU countries. This phenomenon may negatively impact the access of Polish patients to certain drugs.

A key factor that may significantly influence the development of commitment from innovative pharma companies in Poland is a partner dialogue with the central authorities.

The dialogue’s goal should be to clearly define the therapeutic needs of Polish society, the government’s expectations and possible responses to them by innovative pharma companies.

In this report, we show that the pharmaceuticals sector in Poland, and in particular its innovative part, is important to the economy (4 of 4)

z

Overview of the pharmaceuticals sector in Poland

Section 2

The following section was prepared by IMS Health and is based on market data and expertise of the company

12

Poland is the sixth largest European pharmaceuticals market in value terms

Per capita drug spend in Poland is one of the lowest in Europe

The Polish pharmaceuticals market versus other European countries

Market value in individual European countries

Poland is the sixth largest pharmaceuticals market in Europe and the leader in Central Eastern Europe (CEE) in terms of drug sales value.

Retail market – sales value, EUR bn – 2010 Sa

les

valu

e (E

UR b

n)

20

15

10

5

0

2521

.011

.810

.810

.34.

4

25.9

3.7

3.2

3.1

3.1

2.4

2.1

1.9

1.9

1.7 1.5

1.4

1.3

1.0

0.6

0.5

0.4

0.2

0.2

0.1

Ger

man

yFr

ance

Italy

Spai

nUK

Pola

ndG

reec

eSw

eden

*Be

lgiu

mNe

ther

land

sPo

rtuga

lAu

stria

Denm

ark*

Rom

ania

Hung

ary

Irela

ndFi

nlan

dCz

ech

Rep.

Slov

akia

Bulg

aria

Slov

enia

Lith

uani

aLa

tvia

Luxe

mbo

urg

Esto

nia

Source: IMS MIDAS, ExMan net prices (EUR), *pharmaceuticals market (drug market: retail Rx, retail OTC, and hospital markets)

Per capita market value in individual European countries

Despite being in sixth position, Poland has one of the lowest per capita drugspends in Europe, including the CEE countries (e.g. the Czech Republic,Hungary and Slovakia).

In 2010, the per capita drug spend in Poland amounted to 52% of the averageper capita drug spend in Europe.

Retail market, per capita drug spend in 2010 (EUR)

EUR 200

150

100

50

0

250

300

337

336

331

331

32535

0

317

290

257

255

249

234

226

196

187

183

168

165

128

114

110

103

99 8779

Denm

ark*

Swed

en*

Luxe

mbu

rgG

reec

eIre

land

Fran

ceG

erm

any

Belg

ium

Finl

and

Slov

enia

Aust

riaSp

ain

Portu

gal

Italy

Neth

erla

nds

Slov

akia

Hung

ary

UKCz

ech

Rep.

Pola

ndLi

thua

nia

Esto

nia

Latv

iaRo

man

iaBu

lgar

ia

350

Average EUR 218

Source: IMS MIDAS, ExMan net prices (EUR), *pharmaceuticals market (drug market: retail Rx, retailOTC, and hospital markets), EUROSTAT.

Impact of the innovative pharma industry on the Polish economy • Report 13

Due to the low level of total healthcareexpenditure in Poland,the share of drug spending in totalhealthcare expenditure is high compared to the more developed markets

Public funds for drugs are insufficient, which leads to an excessiveincrease in patient drugspending

Public drug spend

The share of spending on drugs in total healthcare expenditure is relatively high,mainly due to the low level of healthcare expenditure in Poland.

Drug spending as a percentage of total healthcare expenditure in 2009

20%

15%

10%

5%

0%

25%

30%

10%

15%

19%

13%

21%

16%19%

28%

12%

31%

22%25%

29%

21%24%

Fran

ce

Switz

erla

nd

Ger

man

y

Slov

enia

Aust

ria

Spai

n

Italy

Slov

akia UK

Hung

ary

Czec

h Re

p.

Pola

nd

Lith

uani

a

Esto

nia

Latv

ia

35%

40% WECEE

Source: WHO, BMI

Share of the public drug spend in total drug expenditure in 2009

80%

65%

40%

20%

0%

100%

68%77%

59%67%

73%67%

47%

71%

85%

57%62%

38%43%

27%

Fran

ce

Switz

erla

nd

Ger

man

y

Slov

enia

Aust

ria

Spai

n

Italy

Slov

akia UK

Hung

ary

Czec

h Re

p.

Pola

nd

Lith

uani

a

Esto

nia

Latv

ia

WECEE

Source: WHO

Overview of the pharmaceuticals market in Poland

14

Market structure – share of generic drugs

The share of generic drugs in Poland is one of the highest in Europe. In 2010, itamounted to c. 66% in value, when calculated for the total retail market (Rx andOTC drugs).

Share of generic drug sales in 2010 (PLN)

40%

30%

20%

10%

0%

50%

60%

53%

53%

46%

45%

44%

66%

44%

43%

38%

38%

37%

36%

36%

35%

34%

32%

32%

31%

30%

28%

23%

Pola

ndBu

lgar

iaCz

ech

Rep.

Slov

akia

Ger

man

yHu

ngar

yPo

rtuga

lUK Ita

lySl

oven

iaFi

nlan

dSw

eden

*De

nmar

k*Fr

ance

Aust

riaG

reec

eBe

lgiu

mSp

ain

Neth

erla

nds

Irela

ndLu

xem

burg

Esto

nia

Latv

iaLi

thua

nia

Rom

ania

70%

N/A

Source: IMS MIDAS, ExMan net prices (EUR), *pharmaceuticals market (drug market: retail Rx,retail OTC, and hospital markets)

Average drug prices in Europe

The average drug price in Poland is one of the lowest in Europe at 44% of theEuropean average. Such a low price level results mainly from the high share ofgeneric drugs, the low availability of innovative drugs and the strong pricepressure in the area of reimbursed drugs.

Average drug price in 2010, ExMan net price (EUR)

20

15

10

5

0

25

19.7

17.1

14.6

13.5

13.3

23.0

12.9

11.2

10.0

9.2

9.1 9.0

8.3

7.1 6.5

4.5

4.2

3.6

3.0

Denm

ark*

Swed

en*

Ger

man

yFi

nlan

dIre

land

Belg

ium

Luxe

mbu

rgNe

ther

land

sAu

stria

Portu

gal

Slov

enia

Gre

ece

Spai

nFr

ance

Slov

akia

Italy UK

Hung

ary

Esto

nia

Czec

h Re

p.La

tvia

Lith

uani

aRo

man

iaPo

land

Bulg

aria

Average EUR 8.2

6.6

6.4

5.9

5.9

5.5

4.7

Source: IMS MIDAS, ExMan net prices (EUR), *pharmaceuticals market (drug market: retail Rx,retail OTC, and hospital markets), EUROSTAT

Poland is at the forefront of Europe with the highest sales of generic drugs

Poland has one of the lowest average drugprices in Europe

EUR

Impact of the innovative pharma industry on the Polish economy • Report 15

The average price of bothgeneric and innovativedrugs in Poland is one of the lowest in Europe

Average price of generic drugs in Europe

In Poland, the prices of both generic and innovative drugs are among the lowest in Europe. Generics are 40% lower and innovative drugs 56% lower than theEuropean average.

Generic drugs in 2010, average ExMan net price (EUR)

8

6

4

2

0

10

12

9.8

9.5

7.8 7.5 7.0

11.5

6.5

6.0

5.7

5.7

5.3

4.7

4.6

4.4

2.8

2.0

Den

mar

k*Sw

eden

*G

erm

any

Finl

and

Belg

ium

Prtu

gal

Irela

ndG

reec

eAu

stria

Luxe

mbu

rgSl

oven

iaIta

lyN

ethe

rland

sSp

ain

Hun

gary

Slov

akia

Cze

ch R

ep.

UK

Fran

cePo

land

Bulg

aria

Esto

nia

Latv

iaLi

thua

nia

Rom

ania

14

N/A

Average EUR 4.7

4.2

4.1 3.9

3.5

3.4

EUR

Source: IMS MIDAS, ExMan net prices (EUR), *pharmaceuticals market (drug market: retail Rx, retailOTC, and hospital markets)

Average price of innovative drugs in Europe

The average price of an innovative drug in Poland is EUR 7.4. The countries withthe highest drug prices, such as Denmark, Germany and Sweden, are the potentialdirections for parallel drug exports from Poland.

Innovative drugs in 2010, average net ExMan price (EUR)

40

30

20

10

0

50

60

50.5

47.3

29.9

29.7

23.2

52.3

20.8

20.5

18.0

16.9

16.3

16.2

7.4 6.4

Den

mar

k*G

erm

any

Swed

en*

Net

herla

nds

Finl

and

Irela

ndBe

lgiu

mLu

xem

burg UK

Fran

ceSl

oven

iaAu

stria

Spai

nSl

ovak

iaPr

tuga

lG

reec

eC

zech

Rep

.H

unga

ryIta

lyPo

land

Bulg

aria

Esto

nia

Latv

iaLi

thua

nia

Rom

ania

N/A

Average EUR 16.8

12.4

11.8

10.4

8.7

8.613

.713

.9

EUR

Source: IMS MIDAS, ExMan net prices (EUR), *pharmaceuticals market (drug market: retail Rx, retailIOTC, and hospital markets)

Overview of the pharmaceuticals market in Poland

16

Price differences between an innovative drug and its generic equivalent

Poland has some of the lowest prices in both innovative and generic drugs inEurope. The significant differences in drug prices across Europe lead to theexport of drugs from Poland to other European markets. In particular, thisconcerns expensive innovative drugs, most of which are reimbursed.

In the Netherlands, the average price of a generic drug is 6.5 times lower thanthe average price of an innovative drug. In Poland, the average price of a generic drug is only 2.6 times lower than the average price of an innovative drug.

Average prices of innovative drugs versus generic equivalents in 2010 (EUR)

5.35.2

5.04.8

4.5

6.5

3.83.63.6

3.33.2

NetherlandsGermany

UKFrance

Sweden*Denmark*

FinlandIreland

LuxembourgSlovakiaBulgaria

SpainSlovenia

AustriaBelgium

Czech Rep.Poland

HungaryGreece

ItalyPortugalEstonia

LithuaniaLatvia

Romania

N/A

0 1 2 3 4 5 6 7

3.23.1

2.82.8

2.72.6

2.12.0

1.81.8

Source: IMS MIDAS, ExMan net prices (EUR), *pharmaceuticals market (drug market: retail Rx, retailOTC, and hospital markets)

The average price ofan innovative drug in Poland is only 2.6 timeshigher than the averageprice of its genericequivalent whereas in the Netherlands the average price of an innovative drug is 6.5 times higher thanthe average price of its generic equivalent

Impact of the innovative pharma industry on the Polish economy • Report 17

Overview of the pharmaceuticals market in Poland

In Poland, drug spending for the European top 30 hospital drugs is five toeight times lower than that in other Europeancountries

Compared to the major European countries, the Polish hospital market has thelowest per capita spending (EUR 4.5) for the European top 30 hospital drugs.

Of the TOP 30 hospital drugs, 26 are available on the Polish hospital market.

Hospital market value for TOP 30 hospital products in 2010, ExMan net prices (million EUR)

Number of TOP 30 hospital drugs available on the Polish market in 2010T

Per capital spending on TOP 30 hospital drugs in 2010

Italy 1 825 30 30.2 Є

Spain 1 779 28 38.7 Є

France 1 637 26 25.3 Є

UK 1 624 30 26.2 Є

Germany 962 28 11.8 Є

Poland 173 26 4.5 Є

European TOP 30 hospital drugs:

ARANESP, ATRIPLA, AVASTIN, AVONEX, CLEXANE, CRESTOR, ENBREL, GLIVEC, HERCEPTIN, HUMIRA, INEGY, KEPPRA, LANTUS, LIPITOR, LUCENTIS, LYRICA, MABTHERA, NEULASTA,

NEXIUM, PLAVIX, REMICADE, REVLIMID, SERETIDE, SEROQUEL, SINGULAIR, SPIRIVA, SYMBICORT, TAXOTERE, TRUVADA, ZYPREXA

Source: IMS MIDAS, ExMan net prices (EUR) , Hospital market

18

The pharmaceuticals market in Poland

The structure of the pharmaceuticals market is broken down into retailand hospital markets

In 2010, the value of the pharmaceuticals market in Poland (retail and hospital)reached PLN 20.1 billion in ExMan net prices. The mean annual change (CAGR)in the value of the pharmaceuticals market between 2003 and 2010 was 6.4%.

Pharmaceuticals market – sales value, PLN bn

20

15

10

5

0

2512.9

TOTAL

Retail market - Rx drugs

Sale

s va

lue

(PLN

bn)

1.5

8.7

2.7

1.5

8.9

2.8

1.7

9.6

2.9

1.9

10.0

2.9

2.1

10.8

3.2

2.3

11.9

3.4

2.7

12.9

3.8

2.8

13.4

3.8

2.9

14.2

4.3

2003 2004 2005 2006 2007 2008 2009 2010 2011*

13.2 14.2 14.8 16.1 17.6 19.4 20.1 21.4

Retail market - OTC drugsHospital market

* 2011 forecastSource: IMS Health, National Data 05/2011, ExMan net prices (PLN). Pharmaceuticals market (retail Rx, retail OTC and hospital)

Individual segments of the pharmaceuticals market

In 2010, the market for Rx drugs available in retail pharmacies represented 67%of the total pharmaceuticals market and was worth PLN 13.4 billion.

The reimbursed drugs available in the retail market made up more than half ofthe total value of the pharmaceuticals market in Poland.

The hospital market and the retail over-the-counter (OTC) market represented13.9% and 19.2% respectively of the market share in value terms.

Percentage structure and value of the retail Rx market and the hospital market in Poland in 2010, ExMan net prices (PLN)

Retail market, reimbursed Rx drugs Hospital market

10.1 bn

17.8%20.2%62.0%

Retail market, non-reimbursed Rx drugs

3.3 bn 2.9 bn

100 % = retail Rx market and hospital marketSource: IMS Health, National Data 05/2011, ExMan net prices (PLN). Pharmaceuticals market(excluding OTC drugs)

In 2010 the value of the Polish pharmaceuticals market reached PLN 20.1 billion. The mean annual change in the value of the pharmaceuticals market was +6.4% between 2003 and 2010

Impact of the innovative pharma industry on the Polish economy • Report 19

Innovative and generic companies – volume structure

The volume market share of innovative companies amounted to 38% in 2010.

Pharmaceuticals market volume by company profile

100%

80%

60%

40%

20%

0%

67%

33%

2010

Generic companies

Innovative companies

100%

80%

60%

40%

20%

0%

62%

38%

2010

Volume as thenumber of packages

Total pharmaceuticals market Pharmaceuticals market excluding OTC drugs*

100 %= Retail Rx market, OTC retail market , and hospital market;* 100 %= Retail Rx market and hospital market Source: IMS Health, National Data 05/2011, ExMan net prices (PLN). Pharmaceuticals market (excluding OTC drugs) Definition of an innovative company: the sales value of innovative drugs in the pharmaceuticals market (drug market: retail and hospital) in 2010 represented 50% or more of the company’s portfolio value. In the case of multi-organisational corporations, the sales value of the “parent” company is used

Innovative and generic companies – value structure

Due to price differences, the market share of innovative companies is significantlyhigher, amounting to 58% in 2010.

Pharmaceuticals market value by company profile

Total pharmaceuticals market Pharmaceuticals market excluding OTC drugs*

100%

80%

60%

40%

20%

0%

47%

53%

2010

Generic companies

Innovative companies

100%

80%

60%

40%

20%

0%

42%

58%

2010

Sales value on thepharmaceuticalsmarket in 2010,ExMan net prices(PLN)

PLN 9,4 bn

PLN 10,7 bn

PLN6.8 bn

PLN9.4 bn

100 % = Retail Rx market, OTC retail market , and hospital market;* 100 % = Retail Rx market and hospital marketSource: IMS Health, National Data 05/2011, ExMan net prices (PLN). Pharmaceuticals market(excluding OTC drugs)

The volume share of innovative companiesamounted to 38% of the Polish pharmaceuticals market (excluding OTC drugs)

Sales value of innovative drugs amounted to PLN 9.4 billion in 2010, whichrepresented 58% of the total market value (excluding OTC drugs)

Overview of the pharmaceuticals market in Poland

20

Innovative and generic companies in the hospital market

In 2010 innovative companies represented over 71% of the hospital market value.

Hospital market value share broken down by generic and innovative companies

80%

60%

40%

20%

0%

100%

Innovative companies

41%

71% 71%

2003 2004 2005 2006 2007 2008 2009 2010

Generic companies

59% 61% 65% 66% 69% 70%

29%29%30%31%34%35%39%

Source: IMS Health, National Data 05/2011, ExMan net prices (PLN). Hospital market Definition of an innovative company: the sales value of innovative drugs in the pharmaceuticals market (drug market: retail and hospital) in 2010 represented 50% or more of the company’s portfolio value. In the case of multi-organisational corporations, the sales value of the “parent” company is used

Innovative and generic companies in the retail Rx market

In 2010 innovative companies represented 55% of the retail Rx market value.

Retail Rx market value share broken down by generic and innovative companies

80%

60%

40%

20%

0%

100%

Innovative companies

35%

56% 55%

2003 2004 2005 2006 2007 2008 2009 2010

Generic companies

65% 60% 60% 59% 58% 57%

45%44%43%42%41%40%40%

Source: IMS Health, National Data 05/2011, ExMan net prices (PLN). Hospital marketDefinition of an innovative company: the sales value of innovative drugs in the pharmaceuticals market(drug market: retail and hospital) in 2010 represented 50% or more of the company’s portfolio value. In the case of multi-organisational corporations, the sales value of the “parent” company is used

In 2010 innovativecompanies representedover 71% of hospital market value

Innovative companiesgenerate more than half of the retail marketvalue

Impact of the innovative pharma industry on the Polish economy • Report 21

Generic drugs make up c. 60% of the retail Rxmarket in value and 76% in volume

Retail Rx market – volume share of products by registration type

The Polish pharmaceuticals market is predominantly a market of generic drugs,mainly branded generic drugs.

The access to innovative drugs is perceived as quite limited, which mainly resultsfrom the high level of patients’ co-payments connected with the limited financingof drugs by the NHF.

Product shares in the retail Rx market by registration type – volume

80%

60%

40%

20%

0%

100%

Rx generic drugs

22.7%

2003 2004 2005 2006 2007 2008 2009 2010

Rx original drugs

22.3% 22.6% 22.7% 23.4% 23.7% 23.7% 23.5%

77.3% 77.7% 77.4% 77.3% 76.6% 76.3% 76.3% 76.5%

Source: IMS Health, National Data 05/2011, ExMan net prices (PLN). retail Rx market.Original drugs: According to the IMS definition - ORIGINAL BRANDS, LICENSED BRANDSGeneric drugs: According to the IMS definition - OTHER BRANDS, PATENT N/A, UNBRANDED

Retail Rx market – Value share of products by registration type

Over the last eight years, the share of generic Rx drugs has increased from 53.8% to 59.8% in value terms. In volume terms, it fell from 77.3% to 76.5%.

Product shares in the retail Rx market by registration type – value

80%

60%

40%

20%

0%

100%

Rx generic drugs

46.2%

2003 2004 2005 2006 2007 2008 2009 2010

Rx original drugs

42.3% 40.7% 39.5% 38.9% 39.7% 39.5% 40.2%

53.8% 67.7% 59.3% 60.5% 61.1% 60.3% 60.5% 59.8%

Source: IMS Health, National Data 05/2011, ExMan net prices (PLN). retail Rx market.Original drugs: According to the IMS definition - ORIGINAL BRANDS, LICENSED BRANDSGeneric drugs: According to the IMS definition - OTHER BRANDS, PATENT N/A, UNBRANDED

Overview of the pharmaceuticals market in Poland

22

Imported drugs and locally produced drugs – sales value

In 2010, imported drug sales amounted to PLN 12.3 billion.In the same period, the value of locally produced drugs was PLN 3.9 billion.The mean annual change (CAGR) in the market value between 2003 and2010 was +7.6% for imported drugs and +4.5% for locally produced drugs.

Imported and locally produced drugs – Sales value (PLN bn)

Imported drugs

7.4

3.9

2003 2004 2005 2006 2007 2008 2009 2010

Locally produced drugs

2.9 3.4 3.6 3.8

12.311.610.4

9.38.58.0

7.38

6

4

2

0

10

12

14

3.1 3.33.9

mld

PLN

Source: IMS Health, National Data 05/2011, ExMan net prices (PLN). Pharmaceuticals market(excluding OTC drugs)

Imported and locally produced drugs – structure of sales

In 2010, the share of imported drug products in the pharmaceuticals market(excluding OTC drugs) represented 75.7%. Between 2003 and 2010, theincreased by 4 percentage points. The share of imported drugs was even largerin the hospital market – in 2010, it amounted to c. 85%. Between 2003 and2010, it increased by 18.5 percentage points.

Imported and locally produced drugs – Sales volume share

80%

60%

40%

20%

0%

100%

Imported drugs - volume

38.9%

2003 2004 2005 2006 2007 2008 2009 2010

Local drugs - volume

40.5% 43.0% 45.3% 48.2% 49.9% 51.4% 52.9%

61.1% 59.3% 57.0% 54.7% 51.8% 50.1% 48.6% 47.1%

Source: IMS Health, National Data 05/2011, ExMan net prices (PLN). Pharmaceuticals market(excluding OTC drugs)

The Polish pharmaceuticals market(excluding OTC drugs)is dominated by imported products

Domestic drug production accounts fornearly one quarter ofthe total market value. However, in recent yearsthe growth of this marketsegment has clearly slowed down

Impact of the innovative pharma industry on the Polish economy • Report 23

Imported and locally produced drugs – sales value share

80%

60%

40%

20%

0%

100%

Imported drugs - value

28.3%

2003 2004 2005 2006 2007 2008 2009 2010

Local drugs - value

30.0% 29.1% 28.7% 27.6% 26.5% 25.3% 24.3%

71.7% 70.0% 70.9% 71.3% 72.4% 73.5% 74.7% 75.7%

Source: IMS Health, National Data 05/2011, ExMan net prices (PLN). Pharmaceuticals market(excluding OTC drugs)

Average price

The change in the average price is influenced not only by changes in the pricesof drugs but also by changes in the drug consumption structure. It is particularlypronounced in the hospital market where the share of oncology drugs, which arerelatively more expensive than other drugs, has been systematically increasingover the years, thus causing an increase in the average drug price for the totalmarket.

Average drug price, ExMan net price (PLN), in the Rx retail and hospital market

35

30

25

20

0

Drug’s average price - retail Rx market

2003 2004 2005 2006 2007 2008 2009 2010

15

10

5

16.519.5

22.0

14.1 15.5 16.0 16.3 16.6 17.6

32.2

19.3

40

15.3

34.9

18.6

25.528.7

Drug’s average price - hospital market

Source: IMS Health, National Data 05/2011, ExMan net prices (PLN). Pharmaceuticals market(excluding OTC drugs)

Overview of the pharmaceuticals market in Poland

Changes in the average drug price for the whole market is influenced not only by changes in the prices of drugs, but also by changes in the drug consumption structure. The entry of new and more expensive drugs results in an increase in the average drug price

PLN

24

Elements of market value increase between 2003 and 2010

Between 2003 and 2010, the value of the retail Rx market increased by 53.5%.The vast majority of this increase resulted from the market launches of newdrugs, which accounted for 63% of this increase. The change in the drugconsumption structure, such as switching to more expensive therapies, accountedfor 17% of the increase. The change in the prices of drugs was a negative growthelement (-26%), meaning that drug prices were steadily falling. On the hospitalmarket, the prices of the products available in the market since 2003 fell by 31%.The value of the hospital market increased by over 83% in this period, with newlaunches being the major element of the increase.

Elements of market value increase in the period 2003-2010

100%

80%

60%

40%

20%

0%

New entries

Changes in the drugconsumption structure

140%

120%

-20%

-40%

63%

17%

-26%

87%

27%

-31%

+54% +83%

Changes in drug price

Rx retail Hospital

Source: IMS Health, National Data 05/2011, ExMan net prices (PLN). Pharmaceuticals market(excluding OTC drugs)

Over the last few years, the unit drug price hasbeen steadily decreasing.The markets have been growing, mainly dueto the launch of new drugs and changes inthe drug consumptionstructure, such as switching to moreexpensive therapies

Impact of the innovative pharma industry on the Polish economy • Report 25

Rx drugs account for 86% of the value ofparallel drug imports to Poland

In 2010 the value ofparallel export of drugsamounted to over PLN 810 million. As a result of the new reimbursementlaw, a further significantincrease in the scale ofparallel exports is expected

Parallel imports

Over the last few years, Poland has been systematically increasing its share of theparallel drug trade in Europe. Both directions of parallel trade, import and export,have been developing very strongly.

Retail market, sales value, and the number of drugs from parallel imports in the market

Sales value of products from parallel import

2003 2004 2005 2006 2007 2008 2009 2010

Number of available products from parallel import

160

120

80

40

0

200

PLN

bn

Number of products from

parallel im

port

96 1740 0 8 13 663619

90176

299

430

200

100

0

300

400

500

Source: IMS Health, National Data 5/2011, ExMan net prices (PLN). Retail market.Data shows parallel imports via the wholesale channel.

Parallel exports – trade balance (compared to parallel imports)

In 2010 parallel drug exports from Poland amounted to PLN 810 million.

The proposed amendments to the reimbursement law and the continuous pricing pressure on reimbursed drugs have resulted in increasing price differences across countries. This results in an increase in the value of parallel drug exports from Poland. In the near future the value of this market may reach PLN 1,5-2 billion.

In 2010, the trade balance of parallel imports and exports of Rx drugs was PLN635 million in favour of parallel drug exports out of Poland.

Value of parallel exports from and imports to Poland

100%

80%

60%

40%

20%

0%

Value of parallel exports

Value of parallel imports

-20%

291

66

534

96

810

174

201020092008

Source: IMS Poland, Sales Shot, National data 05/2011, ExMan net prices (PLN).Data shows parallel exports via the wholesale and retail channel.

Overview of the pharmaceuticals market in Poland

26

Main players on the Polish pharmaceuticals market

The top 10 players on the Polish pharmaceuticals market are responsible for 50%of total market value, while the top 30 represent more than 82.7% The remaining17.3% of the market value is divided among around 415 companies.

In volume terms, the top 10 players account for 54% of Polish drug sales. All thesecompanies have production facilities in Poland.

Of the top 30 companies, 16 have production facilities in Poland, which are mainlylocated close to the major cities such as Warsaw, Łódź and Poznań.

Market share of top 10 corporations in Poland – 2010

Sanofi-group

Novartis

Glaxosmithkline

Polpharma

Roche

Servier

Merck & Co

Pfizer

Teva

Astrazeneca

Other

0% 20% 40% 60%

Polpharma

Sanofi-group

Novartis

Glaxosmithkline

Teva

Servier

Valeant Pharma

Adamed Poland

KRKA

Gedeon Richter

Other

0% 20% 40% 60%

8.5%

8.2%

6.1%

5.2%

4.6%

3.9%

3.8%

3.4%

3.1%

3.1%

50.1%

10.8%

7.6%

7.3%

5.1%

5.1%

4.6%

3.9%

3.5%

3.2%

2.9%

46.0%

Value Volume

Source: IMS Health, National Data 05/2011, ExMan net prices (PLN). Pharmaceuticals market(excluding OTC drugs)

445 active playersoperated in the Polishpharmaceuticalsmarket (excludingOTC drugs) in 2010.The top 10 companiesgenerated 50% ofmarket value

Impact of the innovative pharma industry on the Polish economy • Report 27

Two of the TOP 10corporations on the Polish retail Rx market are Polish companies

Eight of the TOP 10corporations on the Polish hospital market are innovative companies

The definite majority of the TOP 10 corporations operating on the Polish retail Rxmarket and hospital market are innovative companies.

TOP 10 corporations on the retail Rx market in 2010 (value)

Ranking Corporationtype

Corporation name Sales value (PLN m) in 2010

Number of products(brands) on themarket in 2010

1 Original SANOFI‐GROUP 1 140 131

2 Original NOVARTIS 1 004 232

3 Original GLAXOSMITHKLINE 834 121

4 Generic POLPHARMA 716 104

5 Original SERVIER 627 69

6 Generic KRKA 489 62

7 Original MERCK & CO 478 73

8 Generic TEVA 463 167

9 Generic ADAMED POLAND 456 60

10 Original ASTRAZENECA 436 30

TOP 10 corporations on the hospital market in 2010 (value)

Ranking Corporationtype

Corporation name Sales value (PLN m) in 2010

Number of products(brands) on themarket in 2010

1 Original NOVARTIS 330 263

2 Original ROCHE 311 44

3 Original SANOFI‐GROUP 237 157

4 Original PFIZER 208 104

5 Original GLAXOSMITHKLINE 151 159

6 Original MERCK & CO 138 71

7 Generic POLPHARMA 121 130

8 Original BAYER 118 77

9 Generic WARSZAWA ZF POLFA 88 84

10 Original BRISTOL‐MYERS SQB. 84 31

Source: IMS Health, National Data 05/2011, ExMan net prices (PLN). Pharmaceuticals market(excluding OTC drugs)Definition of an innovative company: the sales value of innovative drugs in the pharmaceuticalsmarket (drug market: retail and hospital) in 2010 represented 50% or more of the company’s portfoliovalue.In the case of multi-organisational corporations, the sales value of the “parent” company is used.

Overview of the pharmaceuticals market in Poland

28

The largest players inPoland are innovativecompanies engaged inthe production of innovative and genericdrugs

In 2010 the TOP 30 corporations accounted for c. 83% of the Polish pharmaceuticalsmarket. Of the TOP 30, 16 are innovative companies responsible for 54.4% of market value

TOP 30 corporations in 2010 – pharmaceuticals market (excluding OTC drugs)

Top 30corporations

MSV* Rx-INN

Rx-Gx

OTC Production in Poland

Functional hubs(range of operations)

Sanofi-Group(incl. Zentiva)

8.5% ✔ ✔ ✔ Rzeszów, Chociw

Novartis (incl. Sandoz)

8.2% ✔ ✔ ✔ Stryków

GSK 6.1% ✔ ✔ ✔ Poznań IT Centre (global); Logistics and Distribution Centre (global)

Polpharma 5.2% ✔ ✔ ✔ Starogard Gd., Duchnie, Sieradz

Roche 4.6% ✔ ✔ ✔ IT Centre (global),Clinical Research Centre (CEE)

Servier 3.9% ✔ ✔ ✔ Warszawa

Merck (MSD) 3.8% ✔ ✔ ✔ Clinical Research Centre (EU)

Pfizer 3.4% ✔ ✔ ✔

Teva Group 3,1% ✔ ✔ ✔ Kraków, Kutno

AstraZeneca 3.1% ✔ ✔ ✔ Clinical Research Centre(CEE)

KRKA 3.0% ✔ ✔ ✔ Warszawa

Adamed (incl.Polfa Pabianice)

2.8% ✔ ✔ Pieńków, Pabianice

Bayer 2.7% ✔ ✔ ✔

Novo Nordisk 2.5% ✔ ✔ ✔

Abbott 2.5% ✔ ✔

Gedeon Richter 1.9% ✔ ✔ ✔ Grodzisk Maz.

Astellas Pharma 1.7% ✔ ✔ ✔

Valeant Pharma 1.7% ✔ ✔ Rzeszów

J&J 1.6% ✔ ✔ ✔

Eli Lilly 1.4% ✔ ✔ ✔

Biofarm 1.3% ✔ ✔ ✔ Poznań

Boehringer Ing. 1.2% ✔ ✔ ✔

UCB 1.2% ✔ ✔ ✔

Merck KGAA 1.2% ✔ ✔ ✔

Polfa Warszawa 1.1% ✔ ✔ Warszawa

Polfa Tarchomin 1.1% ✔ ✔ ✔ Tarchomin

Nycomed 1.1% ✔ ✔ ✔ Łyszkowice SSC (EU)

BMS 1.0% ✔ ✔ ✔

Lek-Am 0.8% ✔ ✔ ✔ Zakroczym

Menarini 0.8% ✔ ✔ ✔

* MSV – Sales value share in the pharmaceuticals market (excluding OTC drugs)Source: IMS Health, National Data 05/2011, ExMan net prices (PLN). Pharmaceuticals market(excluding OTC drugs)

Impact of the innovative pharma industry on the Polish economy • Report 29

Over half of the TOP 30 pharma companiesoperating on the Polish market have productionfacilities in Poland

The three largestcompanies in Poland areinnovative pharma players with productionfacilities (Novartis, Sanofi-Aventis and GSK)

Locations of the major investments (production facilities and functional hubs) of the TOP 30 pharma companies in Poland

x3

Legend

Production

Functional hub

Note: The Teva Group owns Pliva Krakow and Teva KutnoPolpharma owns three production facilities near Gdansk (one is in Medana and one waspurchased from Bioton). Polfa Pabianice is a subsidiary of Adamed.Source: Company information, PwC analysis

Undoubtedly, the range of interactions within the domestic economy increasesalongside rising investments. Some pharma companies have their productionfacilities in different regions of Poland.

Moreover, some innovative pharma companies have also established theirfunctional hubs in Poland (e.g. IT, Clinical Research and Shared Service Centres).

Market feedback indicates the absence of incentives supporting the developmentof investments at the central government level. However, overall cooperation with local authorities is very highly rated.

“We have a generally positive experience with local authorities. Their attitude hassignificantly improved in recent years. They are currently more open to welcomenew investments in their regions.”Pharma company, Poland

Overview of the pharmaceuticals market in Poland

30

In recent years total NHF spending on drugreimbursement has significantly increased.However, the NHFis expected to limit further increases inreimbursement spending and will freeze it atthe current level

In 2010 patients’ co-payment for drugs amounted to 32.3%

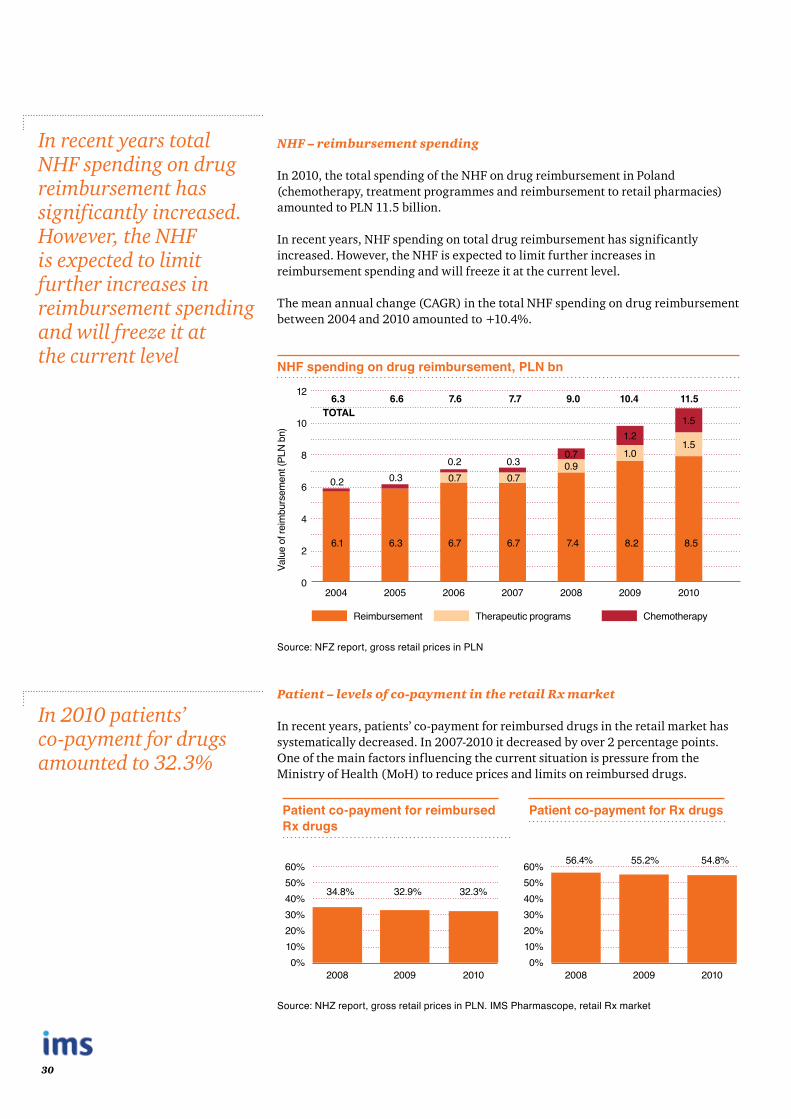

NHF – reimbursement spending

In 2010, the total spending of the NHF on drug reimbursement in Poland (chemotherapy, treatment programmes and reimbursement to retail pharmacies) amounted to PLN 11.5 billion.

In recent years, NHF spending on total drug reimbursement has significantly increased. However, the NHF is expected to limit further increases in reimbursement spending and will freeze it at the current level.

The mean annual change (CAGR) in the total NHF spending on drug reimbursement between 2004 and 2010 amounted to +10.4%.

NHF spending on drug reimbursement, PLN bn

8

6

4

2

0

10

12

Reimbursement

Valu

e of

reim

burs

emen

t (PL

N bn

)

0.2

6.1

2004

0.2

6.7

0.7

2006

0.3

6.7

0.7

2007

0.70.9

7.4

2008

1.21.0

8.2

2009

1.5

8.5

1.5

2010

Therapeutic programs Chemotherapy

2005

0.3

6.3

6.3 6.6 7.6 7.7 9.0 10.4 11.5TOTAL

Source: NFZ report, gross retail prices in PLN

Patient – levels of co-payment in the retail Rx market

In recent years, patients’ co-payment for reimbursed drugs in the retail market has systematically decreased. In 2007-2010 it decreased by over 2 percentage points. One of the main factors influencing the current situation is pressure from the Ministry of Health (MoH) to reduce prices and limits on reimbursed drugs.

Patient co-payment for reimbursed Rx drugs

Patient co-payment for Rx drugs

2008 2008

34.8% 32.9% 32.3% 40%30%20%10%0%

50%40%30%20%10%0%

50%60% 60% 56.4% 55.2% 54.8%

2009 20092010 2010

Source: NHZ report, gross retail prices in PLN. IMS Pharmascope, retail Rx market

Impact of the innovative pharma industry on the Polish economy • Report 31

Key market trends

Increasing competitionfrom generic drugs

The decline in R&D productivity and the upcoming expiry of blockbusters’ patent protection imply increased competition from generic drugs.

Strong pressure for price reductions very often leads to price negotiations with the payer.

Product portfoliodiversification

Those companies that were initially solely involved in the production of innovative drugs, increasingly engage in generics either by setting up their own production or through mergers and acquisitions.

Pricing pressures onreimbursed drugs

Since 2002 each subsequent revision of the reimbursement lists has involved significant reductions in drug prices and in limits on reimbursed drugs. Under the new law and due to the freeze on the drug reimbursement budget - this trend will continue.

Parallel tradeLow drug prices in Poland result in the increasing phenomenon of parallel exports. Parallel exports mainly concern expensive reimbursed Rx drugs. This situation may lead to reduced availability of these products on the local market.

Overview of the pharmaceuticals market in Poland

Impact of the innovative pharma industry on the Polish economy • Report 33

The role in the economy

Jak już wspomniano, innowacja opracowana oraz wdrożona przez innowacyjne przedsiębiorstwa farmaceutyczne przynosi korzyści gospodarce oraz społeczeństwu. Z tego względu, oczywistym wydaje się, iż należy wspierać maksymalne wykorzystanie efektów procesu innowacyjnego

• Sektory farmaceutyczny i biotechnologiczny przodują w rankingu najbardziej innowacyjnych gałęzi w Europie (udział wydatków na B&R w przychodach 2009)

• Wiele badań jakościowych opartych na analizach, które zostały opublikowane w renomowanych czasopismach medycznych (np. Lichtenberg, 2001 czy Caliskan, 2009), potwierdza, że zaawansowane metody terapeutyczne mają pozytywny wpływ na długość życia, a stosowanie innowacyjnych leków przyczynia się w 40% do tego efektu

Tytuł wykresu

Nota: Źródło:

Tekst

The role in the economySection 3

34

Innovation providesnumerous benefits for the economy and society…

…however, it also requires significantcapital investments

Innovation in the economy

Innovation is one of the key prerequisites of economic development. It assures itssustainability and enhances the living conditions of society.

“Innovation is most frequently defined as scientific discovery or invention, which is then commonly used in everyday life by society. It assures the sustainabledevelopment of the economy.”Report by Working Group for Innovation in Healthcare 2010

In particular, innovation in healthcare appears to be very important from the socialpoint of view. In the light of current and forecast epidemiologic trends, only thedevelopment and introduction of advanced therapies appears to have the potentialto take the technological progress in medicine forward.

• It appears that only innovative drugs can contribute to breakthroughs in therapy for some diseases, such as oncology, which still remains one of the leading causes of death; diabetes, which exhibits an increasing epidemiologic trend as well as musculoskeletal ailments, which are expected to be growing in volumes due to the ageing of the population.

• The total cost of a drug’s successful route to market exceeds EUR 1 059 million and the process itself can last up to 13 years. Thus, it requires significant business effort and innovative companies undertake such investments.

Average cost of the molecule route to market (EUR m)

0 200 400 600 800 1 000 1 200

Pre-human/Pre-clinical Phase II Approval Uncategorised

Phase I Phase III Pharmacovigilance (Phase IV)

Clinical trials

286 87 137 344 50 152 3 EUR 1 059 mlnEUR mln

Source: EFPIA, PwC analysis

Impact of the innovative pharma industry on the Polish economy • Report 35

The role in the economy

The pharmaceuticalssector is ranked as the most innovative industry in Europe

• The pharmaceuticals and biotechnology sector tops the ranking of the most innovative industries (R&D to sales ratio, 2009).

• A number of qualitative analysis-based studies, published in respected medical journals (e.g. Lichtenberg, 2001 or Caliskan, 2009), confirm that the introduction of advanced therapeutic methods has a positive impact on life expectancy, and the application of innovative drugs accounts for c. 40% of the life span.

Ranking of industrial sectors by R&D/Sales ratio, 2009

Pharma & biotech

Software & computer services

Technology hardware & equipment

Leisure goods

Healthcare equipment & services

Automobiles & parts

Electronic & electrical equipment

Aerospace & defence

All sectors

Chemicals

Industrial engineering

General industrials

Household goods

Fixed line telecom

Food producers

Oil & gas producers

0% 5% 10% 15% 20%

15.9%

9.9%

8.7%

6.5%

6.2%

4.7%

4.4%

3.9%

3.5%

3.4%

3.1%

2.6%

1.8%

1.7%

1.2%

0.4%

R&D/Sales ratio (%)

Note: Data relate to the top 1 400 companies with registered offices in the EU, Japan and the Rest of World,ranked by total worldwide R&D investmentSource: The 2010 EU Industrial R&D Investment Scoreboard, European Commission, JRC/DG Research

36

Access to this innovation appears rather limited in Poland, as confirmed by cross-European studies, which aim to index innovation development.

• Attention should be paid to the fact that Poland ranks significantly below the EU27 average.

• Even though innovation enhancement is included in the Ministry of Health’s (MoH) Green Books 2008 as one of the goals, not much progress appears to have been made. The historical growth in innovation is still very low in Poland, unlike in other emerging European markets where growth rates for the past years have been several times greater.

It appears that to be able to catch up with the more mature economies, moreemphasis should be placed on Poland’s strategic support for promoting innovation.

Innovation Union Scoreboard - Summary Innovation Index*, 2010

Growth in Summary Innovation Index*, CAGR ‘06:’10

SwitzerlandSweden

DenmarkFinland

GermanyUSA

JapanUK

BelgiumAustria

NetherlandsIreland

LuxembourgFrance

EU27CyprusIceland

SloveniaEstoniaNorway

PortugalItaly

Czech Rep.Spain

GreeceMalta

HungaryCroatiaPoland

SlovakiaSerbia

RomaniaLithuaniaBulgaria

Latvia

BulgariaPortugal

MaltaLatvia

RomaniaSlovenia

CyprusEstoniaCroatiaGreece

SwitzerlandItaly

FranceHungary

Czech Rep.Finland

GermanySerbia

NorwayNetherlands

BelgiumAustriaSpainJapan

IrelandUK

EU27USA

PolandSlovakiaIceland

DenmarkSweden

LuxembourgLithuania

0.0 0.5 1.0 0.0% 5.0% 5.0%

Summary Innovation Index* 2010 Summary Innovation Index* - GrowthCAGR ‘06:’10

Note: * Average Innovation Index is measured using a composite indicator building on data for 24 indicators related to R&D, investments, human resources, intellectual assets, etc. CAGR – Compound annual growth rateSource: Innovation Union Scoreboard 2010

The average level ofinnovation in Poland is much lower comparedto the more matureEuropean economies…

…and it has historicallygrown at a much lower pace than in most of CEEregion geographies aswell

Impact of the innovative pharma industry on the Polish economy • Report 37

The role in the economy

Areas of contribution

Patient access to drugs, which are continuously becoming more therapeuticallyadvanced, appears by far to be the very first and the most major contribution of theindustry to the welfare of society. From the economic point of view, the range ofareas of contribution is broader.

Among the pharmaceutical companies operating in our country the largestinfluence on the economy have been had by those businesses with productionfacilities in Poland. But those importing drugs from abroad also have a significantimpact on the economy and society. This consists of: business operations and jobcreation, education of physicians and patients, transfer of know-how, the generalraising of the level of medical knowledge in the country, etc.

Area of the mostsignificant contributionR&D

Education/Know-how

SSC/Functional

hubs

CSRState

budget

Labourmarket

Businessoperations

/Trade

Production /Investments

Inno

vativ

eG

ener

ic

Pure trade (Resale) Manufacture

Level of market engagement

Leve

l of i

nnov

ativ

enes

s

Source: PwC analysis

The pharma industrycontributes to economy and society in a number of ways. Firstly, it provides more advancedmethods of patienttreatment

Innovative companies with manufacturingactivity appear to have the most significantinfluence on the economy

38

Economic impact

In 2010, the total impact of pharmaceutical companies on value creation in thePolish economy, including both direct and indirect effects, was 0.80% of GDP.

• The direct contribution of the pharmaceuticals sector to the Polish economy was 0.32% of GDP.

• The indirect contribution (inter alia stimulating business for various types of companies) of the pharmaceuticals sector was 0.48% of GDP.

More than half of the effect came from indirect impact connected with costsincurred during production of pharmaceuticals in Poland (material costs, services,etc.) and generated 0.44% of GDP.

Approximately 60% of the contribution to GDP is generated by innovative pharmacompanies (0.47% of GDP).

Contribution to GDP in 2010

Total marketInnovative (% of total market)

Comment

Direct effect

Domesticmanufacture* 0.28%

0.19%(59%)

Value addition directlygenerated by pharmacompanies (both manufacture and resale)

Distribution and trade (Reselling)**

0.04%

Indirect effect

Domesticmanufacture* 0.44%

0.28%(58%)

Value addition generated by pharma companies’ suppliers of goods and services

Induced effect of anincreased consumer spend driven by employment andbusiness ties with thepharma industry (induced effect)

Distribution and trade (Reselling)**

0.04%

TOTAL EFFECT % of GDP 0.80% 0.47%(59%)

Note:*Includes contribution generated by companies with manufacturing activity in Poland;**Includes other pharma companies operating in Poland, excluding pure wholesalersTo calculate the revenue to the state budget, we used the value of taxes and fees paid by innovative firms, covering all their activities (including those related to innovative medicines, generic and OTC)Source: GUS, PwC analysis

In 2010, innovativepharma companiescontributed to c. 0.47% of Poland’s GDP, which is c. 60% of the total sector contribution

Impact of the innovative pharma industry on the Polish economy • Report 39

The role in the economy

Contribution to the labour market

In 2010, pharmaceutical companies directly employed 31 thousand people inPoland, which is c. 0.23% of the total number of people employed in Poland in2010.

Besides direct employment, pharmaceutical companies create around 80 thousand to 90 thousand jobs indirectly:

• Polish pharmacies as retail distributors of pharmaceuticals provide around 60 thousand jobs, which can all be ascribed to the activity of pharmaceutical companies.

• Pharmaceuticals wholesalers employ around 20 thousand to 30 thousand people.

• Job creation of suppliers of products and services to the pharma industry such as chemical components, machinery, marketing services, etc. is an additional contribution by the industry to the labour market.

Innovative companies employed around 11 thousand people (full-time equivalentsor FTEs), which is c. 35% of the total number of people employed in the pharmaindustry in Poland.

Contribution to labour market in 2010

Total market(% of employedpersons overall)

Innovative(% of employedpersons overall)

Comment

Direct employment

31.1 thousandjobs (0.23%)

11 thousandjobs (0.10%)

Includes direct employment inboth manufacturing and resellingcompanies

Employment inwholesale andpharamacies

c. 80-90 thousand jobs (0.64%)

Includes indirect employmentstimulated by the broader pharma sector, i.e. jobs in wholesale companies and pharmacies

Other indirectemployment (e.g.subcontractors)

Owing to pharma activity, additionaljobs are created across industries;however, the exact effect is notquantifiable

Includes jobs created insubcontracting companies providing goods and service to the pharma industry

Innovative companies, throughtheir R&D activity, also stimulatethe local CRO market and itsemployment

TOTAL EFFECT c. 110-120 thousand jobs (0.87%)

Source: GUS, ISI securities, PwC analysis

Directly, the innovativepharma industrygenerates around 11thousand jobs. However, the total effect on the labour market is much stronger

40

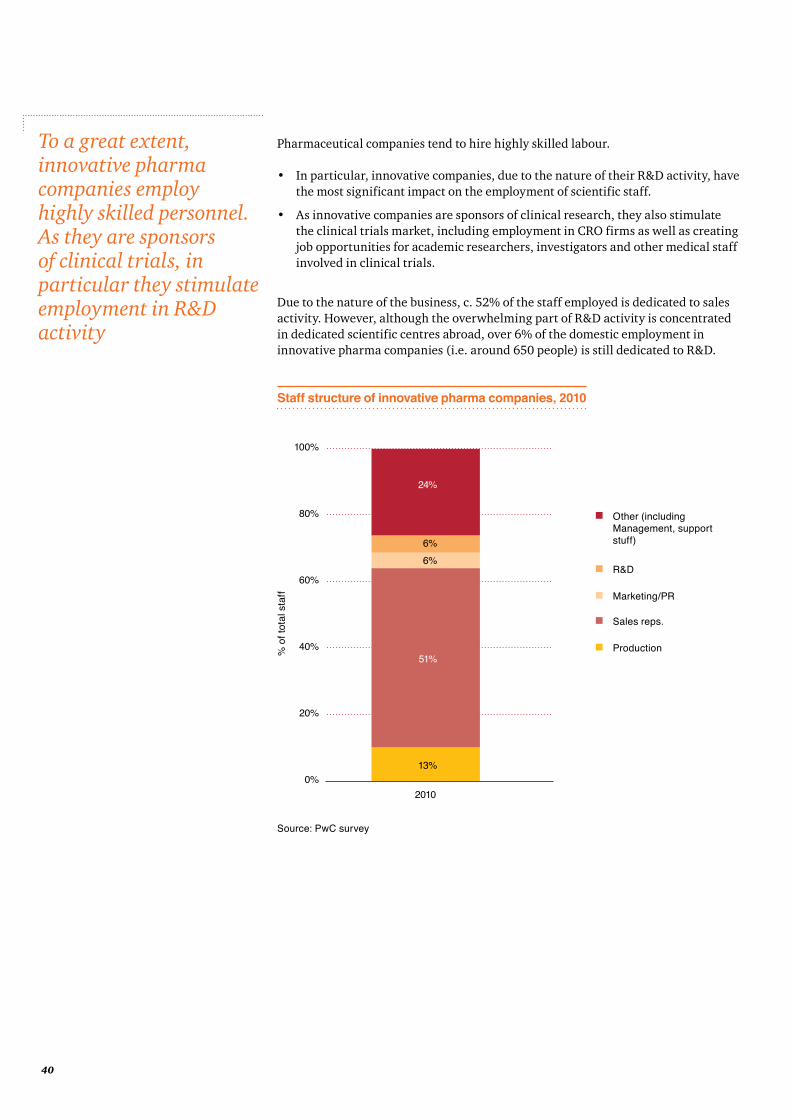

Pharmaceutical companies tend to hire highly skilled labour.

• In particular, innovative companies, due to the nature of their R&D activity, have the most significant impact on the employment of scientific staff.

• As innovative companies are sponsors of clinical research, they also stimulate the clinical trials market, including employment in CRO firms as well as creating job opportunities for academic researchers, investigators and other medical staff involved in clinical trials.

Due to the nature of the business, c. 52% of the staff employed is dedicated to sales activity. However, although the overwhelming part of R&D activity is concentrated in dedicated scientific centres abroad, over 6% of the domestic employment in innovative pharma companies (i.e. around 650 people) is still dedicated to R&D.

Staff structure of innovative pharma companies, 2010

100%

80%

60%

40%

20%

0%

24%

6%6%

51%

13%

2010

Other (includingManagement, supportstuff)

R&D

Marketing/PR

Sales reps.

Production% o

f tot

al s

taff

Source: PwC survey

To a great extent,innovative pharmacompanies employ highly skilled personnel. As they are sponsors of clinical trials, in particular they stimulate employment in R&D activity

Impact of the innovative pharma industry on the Polish economy • Report 41

The role in the economy

Employing mostly highly qualified staff corresponds to the fact that salaries in thepharmaceuticals sector are significantly higher than in other manufacturing sectorsin Poland.

• According to GUS, the average salary in the pharmaceuticals manufacturing industry in Poland is c. PLN 5.2 thousand, while Poland’s average remuneration is PLN 3.2 thousand.

• Wages in the pharma industry are c. 60% higher than Poland’s average wages.This fact also impacts the larger purchasing power of pharma industry employees, thus, leading to higher consumer spending and higher taxes paid.

GUS data shows that in 2010, all pharmaceutical companies spent, on average, c. PLN 1.5 thousand per head on the career development of their employees (i.e. both internal and external training sessions).

• PwC Survey results suggest that the average spend per employee in innovative companies is around three times higher than the overall industry average.

• Innovative companies allocated c. PLN 60 million to training internal staff in 2010.

We note that the transfer of knowledge (such as business know-how) carried out by experienced staff takes place also when they are employed outside the industry. In this way, the experience gained has a bearing on work effects in other sectors ofthe economy.

Avarage monthly wages in the pharma industry vs. the market

2006 2007 2008 2009 2010

2.4 2.5 2.7 2.72.9 2.9

4.7

5.2

3.0 3.1

5.2

3.1 3.2

Inde

x (P

L av

erag

e ’10

= 1

00)

180

140

100

60

20

160

120

80

40

0

PLN

k

6

5

4

3

2

1

0

GrowthCAGR*(‘08:‘10)

Pharma

Manufacturing

PL average

4.7%

4.6%

4.7%

Note: CAGR – Compound annual growth rateSource: GUS

Wages and career developmentopportunities in the pharma sector appear to be significantly above national averages

Innovative companies tend to invest morein human capitalthan the other pharmacompanies

42

According to independent employee satisfaction surveys (e.g. “Great place to work”), innovative pharmaceutical companies are perceived as desirable places to work.

In the most recent edition of the survey, 4 out of the 10 highest-ranked businessesare innovative pharma companies.

Such results should be appreciated even more, as the survey takes a broader range of criteria into account, apart from a purely economic aspect (i.e. abovemarket salary).

The top 10 places to work in Poland (“Great place to work” employee satisfaction survey)

2009 edition 2010 edition 2011 edition

Rank Company Rank Company Rank Company

1 Google 1 IKEA 1 Microsoft

2 Novo Nordisk 2 Alior Bank 2 EMC ComputerSystems

3 Alior Bank 3 Leroy Merlin 3 SC Johnson

4 Sabre Polska 4 BMS 4 Novartis PolandPharma

5 Eli Lilly Polska 5 Instytut Nafty i Gazu 5 Hitachi Data

Systems

6 SKOKUbezpieczenia 6 Microsoft 6 Hilti

7 Hestia 7 SC Johnson 7 Eli Lilly Polska

8 GSK 8 Medtronic Poland 8 Amgen

9 Oriflame 9 LK Dr Irena Eris 9 Ochnik

10 Instytut Nafty i Gazu 10 Novartis Poland

Pharma (Sandoz) 10 Baxter

Source: Great Place To Work ® Institute

Results of independentemployee satisfactionsurveys show that innovative pharmacompanies are appreciated for their good work environment

Impact of the innovative pharma industry on the Polish economy • Report 43

The role in the economy

Investments

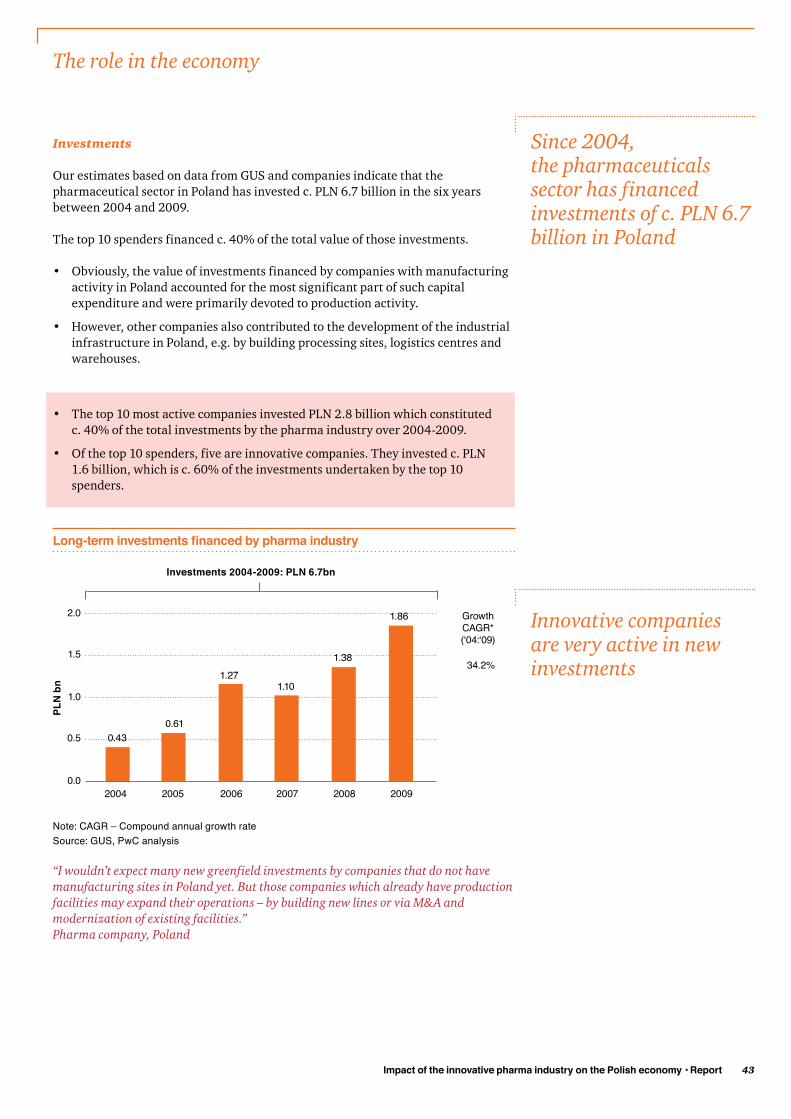

Our estimates based on data from GUS and companies indicate that the pharmaceutical sector in Poland has invested c. PLN 6.7 billion in the six years between 2004 and 2009.

The top 10 spenders financed c. 40% of the total value of those investments.

• Obviously, the value of investments financed by companies with manufacturing activity in Poland accounted for the most significant part of such capital expenditure and were primarily devoted to production activity.

• However, other companies also contributed to the development of the industrial infrastructure in Poland, e.g. by building processing sites, logistics centres and warehouses.

• The top 10 most active companies invested PLN 2.8 billion which constituted c. 40% of the total investments by the pharma industry over 2004-2009.

• Of the top 10 spenders, five are innovative companies. They invested c. PLN 1.6 billion, which is c. 60% of the investments undertaken by the top 10 spenders.

Long-term investments financed by pharma industry

2004 2005 2006 2007 2008

0.430.61

1.271.10

1.38

GrowthCAGR*(‘04:‘09)

PLN

bn

2.0

1.5

1.0

0.5

0.0

1.86

2009

Investments 2004-2009: PLN 6.7bn

34.2%

Note: CAGR – Compound annual growth rateSource: GUS, PwC analysis

“I wouldn’t expect many new greenfield investments by companies that do not havemanufacturing sites in Poland yet. But those companies which already have productionfacilities may expand their operations – by building new lines or via M&A andmodernization of existing facilities.”Pharma company, Poland

Since 2004, the pharmaceuticals sector has financed investments of c. PLN 6.7 billion in Poland

Innovative companies are very active in newinvestments

44

Production activities

Innovative pharma companies are consistently growing their business in Poland,also moving production activities to our country.

• Currently, they have seven manufacturing facilities in Poland. Of these, two are in the Łódz area, while the others are in the Wielkopolska, Mazovia and Podkarpackie regions.

• These include both newly established production facilities, as well as those acquired from other companies, and bought during the privatisation of the Polish pharmaceutical industry.

• The first production plant in Poland was purchased in 1998 and the last in 2010.

• The privatisation of a pharmaceutical factory by an innovative pharma company worth USD 400 million was one of the largest equity transactions during the transition period. This process has been reviewed by the Supreme Audit Office as one of the most effective sector privatisations.

In Poland, innovative companies manufacture around 430 products and produceannually around 200 million packages. The main character of this activity isproduction of solid forms, ointments, creams and capsules.

The development of production depends to a large extent on the transfer of drugs manufacturing from other countries to Poland, and is related to subsequent investments. In 2010 alone, innovative pharma companies invested c. PLN 120 million in the development and modernisation of their production facilities.

The structure of target markets to which pharmaceuticals produced in Poland are delivered differs depending on the portfolio of manufactured drugs. Drugs derived from global corporate portfolios are in the vast majority exported.

The value of exports was c. PLN 3.6 billion in 2010, which represents 34% of thetotal sales of the innovative pharmaceuticals industry in Poland. Polish drugs aredelivered to more than 80 markets worldwide.

• It is the pharmaceutical site of the Novartis Group that allocates the largest portion of production to exports.

• The largest exporter is the factory of GlaxoSmithKline in Poznan. The value of drugs sold abroad in 2010 was PLN 3.4 billion.

• The manufacturing site of Sanofi Group in Rzeszow provides 37% of its production to foreign markets.

As mentioned earlier, through the production of pharmaceuticals in Poland,innovative companies create new jobs and become a major employer in the regionswhere factories are located. In the drug factories of innovative companies, currently around 1,400 people are employed, representing c. 13% of the staff employed in the innovative pharma companies.

Innovative companies have seven drug factories in Poland, employing c.13% of all staff. Polishpharmaceuticals are delivered to 80 marketsworldwide and the value of their exports in 2010was c. PLN 3.6 billion

Impact of the innovative pharma industry on the Polish economy • Report 45

The role in the economy

Market feedback suggests that more incentives should be launched to attractfurther investments in Poland, especially at the central government level.

• “We need to remember that nothing can be just taken for granted! The currently active players entered the market in 1990s, attracted by low labour cost and great market potential at that time. But those advantages are expiring over time as Poland develops, therefore we need to implement some incentives to make us an attractive market.”Pharma company, Poland

• “It appears no central plan or strategy exists to attract and – perhaps even more importantly – to retain investments in Poland. On the other hand, local authorities are typically quite supportive. Access to local decision makers is well organized.”Pharma company, Poland

Professional service hubs and Shared Services Centres

Apart from production activities, a number of enterprises have selected Poland asthe location for outsourcing and/or shared services centres. Frequently, such units deal with providing services to other branches located worldwide.

• Apart from additional investment in facilities and contributions to the labour market, this phenomenon underpins a technology and know-how spillover.

• “The fact that our IT hub with the coverage of the whole of the CEE region is located in Poland creates a number of opportunities for the staff working here, e.g. increase technical skills, becoming familiar with international standards of system implementations, etc.”Pharma company, Poland

(See page [28] for examples of hubs located in Poland, which are centres responsible for IT services, R&D data processing and other business services).

Another wave of investments could beexpected provided greater incentives areintroduced

46

Contribution to the state budget

The pharmaceuticals industry significantly fuels the state budget with taxes andfees, both directly incurred by pharma companies as well as indirectly paid by theiremployees and cooperating companies.

PwC Survey results show that the overall pharmaceuticals industry fuels the statebudget to the tune of c. PLN 1.0 billion and innovative pharma companies pay c.60% of this amount.

The innovative companies stimulate flows to the budget through R&D activity andthe overall clinical trials market.