impact of increasing production or marketing contract ... · impact of increasing production or...

TRANSCRIPT

1

Impact of Increasing Production or Marketing Contract Volume on Access to Competitive Markets

By:

Marvin L. Hayenga Professor of Economics

Neil E. Harl Charles F. Curtiss Distinguished

Professor in Agriculture and Professor of Economics

John D. Lawrence Associate Professor of Economics

Iowa State University

A report prepared for the Minnesota Department of Agriculture

January 21, 2000

2

Executive Summary

Impact of Increasing Production or Marketing Contract Volume on Access to Competitive Markets

Marvin L. Hayenga, Neil E. Harl and John D. Lawrence

The Minnesota legislature requested a study of the use of production contracts in agriculture and the impacts on access to markets by independent farmers. The study objectives were expanded to also consider marketing contracts and broader performance implications of expanding use of contract linkages between farmers, processors and merchandisers in a rapidly consolidating industry. This report describes the extent and type of production and marketing contracts used in agriculture; reviews the theory and available evidence on the firm and industry level effects of contracting in agriculture; provides estimates (from Minnesota industry members) of increased contract volumes in selected sectors of Minnesota agriculture; and analyzes likely impacts of increased contract volumes on independent producers' market access and other aspects of industry performance. Finally, the pros and cons of some possible legislative or regulatory changes related to contracting in agriculture are briefly considered. In the most recent large scale farmer surveys available, the USDA reported 32 percent of the total value of agricultural production was produced under contract arrangements, with nearly 37 percent of that under production contracts (1993 data). Farms of all sizes are involved in contracting, but the largest farms (gross sales of $500,000 or more) represented 1.1 percent of farms with contracts, and accounted for 58 percent of the value of production under contract. More than 185,000 farms had at least one marketing contract during 1993, but the largest farms reported almost half of total marketing contract volume. Marketing contracts for livestock commodities were much less common than production contracts; they accounted for 20 percent of farms and for 42 percent of the total value of production under marketing contracts. In contrast, about 80 percent of the farms with marketing contracts were for crop commodities and they accounted for about 58 percent of the value of production under marketing contracts. The different types of many production and marketing contracts are briefly described, along with their advantages and disadvantages. Processors may have greater control over the quality and timing of deliveries and the quality of inputs used in the production process. Many large farmers use production contracts to expand their operations without as much capital employed. Contracting usually shifts risk from farmers to contractors, and facilitates bringing more capital into agricultural production, but at the cost of reduced independence and rewards for the grower. The chief concern involves specialized producers with major investments who have very limited alternatives when contract renewal comes up, and processors have greater bargaining leverage. For other producers without contracts, the leading issue is

3

their access to markets. In many industries, the only access to markets has been through a contract for many years--e.g. processing vegetables, turkeys, broilers. In others, like hogs, the spot market is rapidly declining, and producers may have little alternative to becoming contractually or cooperatively linked; if not, they become a residual supplier with greater associated risks or rewards. The GMO issue in grains and oilseeds, and biotech value-added consumer traits likely in the near future, is likely to expand greatly the use of contracting to provide assurances to farmers and processors regarding what they are going to receive from each other. An increasing marketing contract share of an industry's volume reduces market alternatives for independent producers, especially when surplus production causes processors to bump up against capacity constraints, and reduces the number of effective competitors in the market. Obviously, the higher the share of an industry's volume that is vertically integrated or contractually linked, the more likely that independent producers will be unable to be in the business without a contract to assure a market outlet. Independent producers could be harmed by increased levels of contracting. There is little evidence of significant harm to date. But the industry structure is changing rapidly, increasing the chances of problems emerging. The primary policy issues and alternatives regarding the rapidly expanding "contract agriculture" relate to industry consolidation and market power concerns. In addition, there often are practical issues associated with contract complexity, information and grower education, and potential bargaining position inequities when contract renewals involve growers subject to great losses if a particular contractor chooses not to renew a contract. Minnesota already has more safeguards for farmers established in state law than most states. Some additional policy ideas that may warrant further study include: • providing an office to serve as a focal point in the Department of Agriculture or the

Attorney General's office to monitor concerns and collect complaints regarding contracting or market competition, and provide a vehicle to forward them more effectively to appropriate state and federal agencies to get their attention.

• prohibit packer feeding of hogs and cattle. • prohibit all marketing contracts. • allow closed producer cooperatives more flexibility in organizational form, and less

restrictive securities regulation and corporate farming laws. • establish a procedure in perishable product bargaining which results in an agreement,

perhaps binding arbitration in which a highly qualified arbitrator can choose one of the final offers, or some middle ground which is most consistent with the prevailing market situation and the equity interests of both parties.

• develop or adapt other states' checklists for use by farmers considering proposed production or marketing contracts -- dealing with the pros and cons, issues, implications, pitfalls of the proposed contracts or contracts similar to them.

• require that a standardized disclosure statement regarding the key financial risks and responsibilities in agricultural contracts should be provided to farmers by firms offering contracts.

4

• require a three-day cooling-off period after signing a contract in which a grower could cancel the contract with no repercussions.

• provide added funding for educational programs on agricultural contracts. Minnesota could provide funding for analysis of the pros and cons of new contract proposals in the state and publicize results to farmers and agribusiness firms in the state.

• enact laws requiring more transparency in contract markets by prohibiting confidentiality clauses in contracts, requiring registration of all (or new) agricultural production or marketing contracts, and require reporting of prices and terms established of all production and marketing contracts.

• do nothing; current state policy may be adequate. These policy alternatives have been enacted or proposed elsewhere, or have been developed by the authors of this study. Their comparative strengths and weaknesses are briefly outlined in the report. They are offered for consideration and debate, and are not necessarily advocated by the authors. The situation analysis, issues and policy suggestions emerging from our study hopefully will stimulate a more informed debate in relevant state agencies and the legislature as they consider future legislative proposals in a changing agricultural market and economic environment.

5

Impact of Increasing Production or Marketing Contract Volume on Access to Competitive Markets

Introduction

A number of issues have been raised at the national and state levels regarding the use of contracts in agriculture. A number of legislative proposals have been considered, and some enacted, which attempt to deal with the perceived problems. Yet there are a number of concerns remaining which may arise before legislators. This report is designed to provide agricultural department officials and legislators in Minnesota with: • A description of the extent and type of production and marketing contracts used in

agriculture; • The theory and available evidence on the firm and industry level effects of

contracting in agriculture; • Estimated likelihood of increased contract volumes in selected sectors of Minnesota

agriculture; • Analysis of likely impacts of increased contract volumes on independent producers'

market access and other aspects of industry performance; • Evaluation of the pros and cons of selected legislative or regulatory changes that

might be contemplated to deal with potential or current problems; These will assis t the Commissioner of Agriculture in making rule changes or recommendations for statutory proposals for consideration by the Minnesota legislature. This analysis is intended to provide a broad perspective on the role of contracting in the agricultural marketing arena in a rapidly consolidating industry, which is not unlike many other industries undergoing rapid structural change in the United States and abroad. We consider the underlying economic rationale for the increasing use of contracting in the food and agricultural sector, and some of the issues raised as the use of contracting has become more prevalent. Our review of the contracting literature draws heavily from Economic Research Service, U. S. Department of Agriculture (USDA) publications, supplemented by observations from numerous journal articles and our own analysis. In addition, the study team has interviewed selected Minnesota industry members regarding the Minnesota contract situation in their industries, and drawn upon the insights from the Minnesota Department of Agriculture staff and several university analysts in preparing this report. 1 This report is intended to stimulate more informed discussion in the legislative process. We try to offer the key points which would be raised on both sides of issues or policy

1 The input of the Minnesota Department of Agriculture staff in identifying key industries and legislative proposals potentially warranting consideration was very helpful, along with their review of our preliminary reports.

6

alternatives for consideration, although we recognize (and the reader will undoubtedly notice) that the comparative strength of the arguments may not be equal.

Importance of market power Perhaps the greatest single problem in contracting is the matter of economic and strategic vulnerability of the weaker party in a contracting relationship when there are wide differences in market power and, hence, in bargaining power. One enduring example over the past 100 years has been laborers contracting with large firms for employment. A century ago, because of the great difference in bargaining power, laborers turned to unionization to achieve a level of countervailing power in negotiating with large industrial firms. As the age of contract agriculture progresses, producers of some agricultural products may experience similar consequences stemming from their lack of bargaining power in dealing with input suppliers and output processors and merchandisers. Contracting between parties of approximately equal market power or even between parties of somewhat unequal power can work satisfactorily. However, contracting between parties of vastly unequal power, with one party economically vulnerable, raises the specter of potentially serious problems if the more powerful party uses its market power to exact contract concessions from the weaker party to the contract. If the weaker party (e.g. a grower) can easily shift to other enterprises with little or no added costs or loss of income, then there is little economic vulnerability and potential problem. If the stronger party (e.g. a processor) has little or no good alternative to dealing with experienced growers for essential raw materials or market outlets (if an input supplier) for their products, there also may be potential economic vulnerability for the seemingly stronger party. If it is difficult for a grower already committed to major specialized investments for a single agricultural production enterprise to acquire a substitute for an important production input (like improved germ plasm) or market outlet, then the grower may be in a poor negotiating position and have to settle for whatever they are offered. For example, the contract relationship between a packer controlling the only slaughter facility in the region and growers with substantial fixed investment in production facilities may lead to a pattern of concessions by the grower when contracts are up for renewal. Producers without meaningful options as contracts terminate are vulnerable to pressure from integrators to accept terms that would not be acceptable were competition present. That is particularly true where substantial amounts of fixed costs in specialized building or equipment are involved (such as with livestock grow-out facilities, or specialized harvesters) and when producers are under financial pressure. The more powerful party to contracting typically dominates in contract drafting, and may be in a position to allocate risks and rewards in a manner favorable to that party, possibly even imposing a "take it or leave it" strategy when negotiating contract renewals unless meaningful competition is present. Thus, the levels of concentration and competition in industries in the food and agricultural sector (especially those developing contractual links with farmers) may be

7

especially important to monitor and evaluate. In the context of this study, federal and state governments need to evaluate the potential for abuse of power by contracting parties, and the effectiveness of current policies to protect against or deal with possible abuses. Safeguards for meaningful competition are important in the long-term contract linkages between farmers and other industry participants and, more generally, to reduce the potential abuse of market power in all types of buyer-seller relationships at all levels in the food production, processing and distribution systems. Disparity in bargaining power is an issue in agriculture that is likely to become increasingly important as the impetus toward industry consolidation in the agricultural input and processing industries and more contract linkages of those firms with farmers continues.

Contracting in agriculture

Types of contracts Contracts are an integral part of the production and marketing of selected livestock commodities, such as broilers, turkeys, eggs, and milk. There are two important types of contracts extensively used in agriculture--production contracts and marketing contracts. Such crops as fruit, vegetables, and sugar beets and cane are mostly produced under contracts. Today, production contractors receive a substantial share of farm receipts. These “contractors” typically provide much of the operating capital, bear a large share of production and price risk, and earn the majority of net income from the commodity’s production. “Growers” who provide the labor, the land or facilities, may benefit by being able to expand their operations more rapidly than otherwise possible, with less debt and fewer financial risks (and rewards). Almost one-third of the total value of production on U. S. farms is produced under contractual arrangements. Most of the value of production under contract was produced to fulfill marketing contracts. Just over one-third of the contracted value was produced in conjunction with a production contract, where the contractor (not the grower) retains ownership of the commodity. Farm operations often have both marketing and production contracts. (New USDA contract use estimates are expected in 2000; much of the data cited come from the most recent 1993 and 1997 USDA Economic Research Service studies, as noted in the text. We expect the new data will show higher production and marketing contract share of volume in many agricultural commodities.) Contractors have varying degrees of control over a farmer’s production decisions, depending on the type of contract. Marketing contracts refer to verbal or written agreements between a contractor and a grower that sets a price (or pricing mechanism) and an outlet for the commodity before harvest or before the commodity is ready to be marketed. Most management decisions remain with the growers since they retain ownership while the commodity is being produced. The farmer or grower typically assumes all production risks, but may share price risk with the contractor. Marketing contracts can take many forms, such as: • Forward sales of a growing crop, where the contract provides for later delivery and

establishes a price or contains provisions for setting a price later; • Price setting after delivery based on a formula that considers grade and yield; or

8

• Pre-harvest pooling arrangements among a group of farmers, where the amount received is determined by the net pool receipts for the quantity sold by all farmers in the pool.

Production contracts for livestock, poultry, or crop commodities are either oral or written agreements that require a grower to perform certain tasks involved in producing a commodity in return for a fee for services and inputs provided to a contractor. The contractor typically owns the commodity being produced under contract. These contracts usually specify the quality and quantity of a particular commodity that is to be produced, and who bears various costs and responsibilities. The contractual agreement spells out the production inputs to be provided by each party and the amount of payment to be received by the grower for services and inputs provided. The proportions in which costs and revenues are shared between growers, ranchers, and their contractors vary among commodities and generally depend on the amount of inputs and managerial oversight provided by the contractor. Production contracts typically give the contractor substantial control over the production process. More and more, a grower's funds are combined with capital from outside the immediate family. Growers get equity from a variety of arrangements, as farm businesses link with multiple suppliers of inputs and customers for their outputs. Contracts and contractors are both a source of capital or shifters of risk that often can facilitate acquisition of capital from other sources. The share of production under production or marketing contracts by commodity, 1993

Percent Corn 12.3 Soybeans 12.4 Wheat 6.8 Cotton 32.7 Peanuts 64.6 Rice 19.6 Vegetables/fruit/nursery 47.4 Cattle, hogs, sheep 18.5 Dairy 47.9 Poultry 89.4 All other commodities 18.6 All commodities 31.5____________________________________________ Source: USDA Farm Costs and Returns Survey, 1993, all versions. Contracting was more prevalent on farms specializing in certain commodities in 1993. Close to 90 percent of poultry production was produced under contract in 1993. In comparison, less than 2 percent of cattle producers used contracts, although the value of production under custom feeding or marketing contracts comprised about 23 percent of the total value of production on these farms or ranches.

9

Dairy farmers have long had verbal or written contracts with their processors or cooperatives, and most milk is produced under marketing orders. Dairy farmers report that about 43 percent of their total receipts from milk and a limited amount of replacement heifers were marketed under contract, with 28 percent of farms reporting the use of contracts. Thirty six percent of farm and ranches specializing in the production of fruits or vegetables had contracts in 1993, over 30 percent of the total value of cotton production and 12 percent of the total value of corn production occurred under contract, mostly marketing contracts. Nearly 65 percent of all peanuts were produced under contract in 1993. Production contracting The use of production contracts on U.S. farms was measured by the 1988 Agricultural Economics & Land Ownership Survey conducted by the Census Bureau. The results were similar to the previous surveys. About 1.8 percent of all farms used production contracts. The value of commodities produced under production contracts totaled about $17.9 billion or about 13 percent of the total value of commodities sold in that year. The USDA 1993 Farm Cost and Returns Survey data indicate that about $47 billion (32 percent) of the total value of production was produced under contract arrangements, with nearly 37 percent of that under production contracts. Farms often report having both marketing and production contracts. Input suppliers (e.g. feed companies or cow-calf operations), farmers themselves (e.g. Iowa Select Farms), processors of farm commodities (e.g. Del Monte), or non-farm investors may offer contracts to farm operators. Farms of all sizes are involved in contracting. The gross sales value for the largest share of farms with contracts ranged between $50,000 and $249,999 in 1993. These farms represented 49 percent of farms with contracts and produced about 24 percent of the total value of all production under contract. The largest farms with gross sales of $500,000 or more represented 1.1 percent of farms with contracts, but accounted for 58 percent of the value of production under contract. Many contracts are written so that the contractor either directly pays for inputs, supplies the inputs, or reimburses the producer for expenses required to produce the commodity under contract. Survey data suggest that overall, 6 percent of total cash operating expenses were paid by contractors in 1993, but this varies by commodity and size of farm. Expenses paid by contractors were most common on poultry farms, where, on average, contractors paid 69 percent of operating expenses. Large farms received most of the contractor-paid expenses--60 percent went to farms with gross sales of $500,000 or more. Seed, fertilizer, and chemicals accounted for 72 percent of all expenses paid by those contractors.

10

To illustrate the diversity of production contract arrangements, several types of contracts are described below. Several are adapted from the USDA (1996) study of production and marketing contracts. Broiler contracts Production contracts are most extensive in the broiler industry, with virtually all birds raised in a processors’ own facilities or under production contract. Broiler contracts are the most widely publicized livestock production contracts, comprising approximately 40 percent of all livestock and poultry production contracts in 1993 (USDA). While the specific contract terms vary from company to company, most broiler contracts indicate the division of responsibility for providing inputs and method of compensating growers. The grower usually provides land and housing facilities, utilities, labor, and other operating expenses, such as repairs and maintenance, manure disposal, and chicken house cleaning. The contractor provides chicks, feed, veterinary supplies and services, management services or field personnel, and transportation. Expenses for fuel and litter can be shared or paid by either party, depending on the nature of the contract. Contractors usually own and operate hatcheries, feed mills, and/or processing facilities. In some cases, the contractor may pay some fixed costs, such as insurance, or provide financing for capital purchases like grow-out buildings. The contractor makes the most significant production decisions, such as the size and timing of bird placement and delivery, genetic characteristics of the birds, specific feed ingredients, and the capacity and other characteristics of the chicken house. Growers paid fixed expenses for interest, insurance, taxes, and lease payments that accounted for one-third of cash expenses on these farms. Expenses for production inputs provided by the contractor, including fees paid to the grower, averaged two-thirds of the costs. All farms with broiler contracts reported that the contractor provided chicks and feed. The contractor paid veterinary expenses for almost all farms reporting broiler contracts. Broiler contracts usually provide three types of compensation for grower services: (I) the base payment, (2) an incentive or performance payment, and (3) the disaster payment. The base payment represents a fixed fee per pound of live meat produced. Some contractors are shifting to payment per unit of space. Processed vegetable contracts In 1993, 11,700 farms reported at least one crop production contract (USDA, 1996). Nearly half of these farms had contracts that involved processed vegetables. There were several common components of production contracts for processed vegetables. The contract indicated which inputs will be provided by the contractor, limited in most cases to seed and custom services such as harvesting or hauling. The amount to be produced was specified, with detailed requirements regarding production practices, such as chemical and fertilizer applications. The contractor usually stipulated grading standards along with terms for compensating the grower. More commonly, particularly in California and Washington, the amount paid to the grower was negotiated through a bargaining association that represents a group of producers. In most cases, the association did not assume title to the vegetables.

11

The contractor provided seed to nearly 80 percent of the farms with a single processing vegetable production contract. Some operations were provided custom planting services, which included seed. Custom hauling and fertilizer and chemical applications were the other most commonly supplied inputs reported by 70 percent and 60 percent of contract producers, respectively. Hueth, et al., summarized the contract provisions in a large number of California fruit and vegetable operations. They found much variation in the contract provisions, even within a single commodity. Approximately 6 of the 15 commodities’ contracts involved providing or requiring particular seed or plant varieties, 2 provided pruning or thinning services, 4 provided or arranged for harvesting services. Tomato canners carefully choreographed variety selection, planting, harvesting and delivery schedules to make efficient use of their processing facilities. Field persons monitoring the process and providing logistical and communication services were almost universal. Quality measures were heavily used in processing crops to adjust grower payments, but seldom used for fresh market crops (USDA grades or sorting out inferior product before payment were more likely). Some contracts were acreage contracts, while some were tonnage contracts involving different risks for growers. Goodhue reports that fresh tomato packers controlled a larger share of the production decisions than processors, doing the harvesting themselves to control directly the quality of tomatoes shipped. In contrast, processors allowed growers to harvest the tomatoes and control the in-field sorting. Hog production contracts The practice of establishing a contract with another farm operation to raise livestock broadens the scope of managerial input and capital ownership associated with production. One of the most common situations is for a farm operation to establish a contract relationship to participate in only one of the production stages of raising livestock. A pork producer could offer a contract to another grower to "finish" his or her hogs, for example, by having the second operator feed weaner pigs raised by the contractor until time to sell them to a processor. This allows both farm operators to increase business volume with limited facilities, while specializing in one stage of livestock production. Under this type of arrangement the contractor delivers young animals to the grower’s operation. The grower provides a confinement facility, sometimes built to the contractor’s specifications, plus labor and utilities. The contractor supplies feed, veterinary services, management consulting and supervision. The contractor retains title to the animals until they are removed from the contractee's operation. The fee paid to the grower is usually a flat fee per head produced or per square foot of feedlot space provided. A national pork producer survey in 1998 found both contract farrowing (17 percent of all pigs produced) and contract finishing operations (30 percent of hogs produced) in 1997. Payments were still primarily per pig produced and marketed, with other bonuses for good feed efficiency and low death loss, but 32 percent of the volume produced had payments based primarily on the space (and proportional use of labor, equipment, etc,) used by the pigs (Lawrence, Grimes, and Hayenga). The primary benefits to medium-

12

size farmers offering contracts to other growers were greater access to capital, ability to expand, and reduced risk. Larger operators offering contracts cited financial leverage, dealing with environmental constraints and accessing labor as the principal advantages. Growers sometimes act as contractors to obtain inputs like feeder pigs for their separate finishing process. The "vertical coordination" between different farm operations may have benefits for each of the parties. This allows producers to specialize in farrowing, nursery or finishing operations. As with other contract arrangements, the allocation of capital and returns from investment vary, depending on the specific terms of the contract. In some cases, the fee paid takes the form of livestock retained by the contractee. There are many other examples where this practice may be attractive to livestock or poultry operations, which represent variations of the two previous examples. Egg producers may contract with other farms that raise layers. Turkey operations may contract to have poults raised by another farm business. Beef feeding contracts Feeding cattle in someone else’s feedlot (termed custom feeding) or pasture (termed backgrounding) is extensively practiced in the major cattle producing states. Schroeder and Blair surveyed cattle feeding operations in Kansas and found a variety of services offered by feedlot operators to investors. Feedlot operators provided labor, facilities, utilities, nutritional and veterinary services, financing of part or all of the cattle, feed and services provided (or would feed cattle on a partnership basis). Payments for feedlot services were built into yardage fees for use of pen space, or in feed cost surcharges, or both. Most custom feeding contracts have been developed by the feedlot operator, not the cattle investor. This is an interesting contrast to contractors typically developing the contracts in many other industries. Seed production contracts Seed production contracts have been extensively used for decades. Using seed corn production as an example, farmers produce seed using the seed company's parent seed on land separated from other corn. The farmer provides the land, fertilizer and chemicals, soil preparation and planting labor, and labor for pest control (sometimes). The company supplies seed, consultation on production management practices, crop spraying and chemicals (sometimes), and the specialized harvesting equipment, labor and hauling. The latter is to insure high quality of the harvested seed and control of the valuable germ plasm. The farmer is paid based on the volume harvested, with payments scaled up to reflect differences in inbred yields versus conventional corn which could have been grown instead. Pricing alternatives are structured to provide similar opportunities to conventional corn marketing, based upon cash markets, futures or options markets, and more recently marketing loan or loan deficiency payment alternatives. Ownership of the proprietary seed is maintained by the seed company. Production contract impacts For many of the reasons cited earlier, growers might choose to establish contracts where they provide capital and a fee to another farm operation for a specific crop or livestock

13

service. The principal motivations for this practice include economic advantages of specialization in one or more production stages, facility limitations, or other types of capital constraints. Sometimes lenders may strongly encourage production contracts for beginning farmers without much capital, and for financially stressed farmers. These incentives are most relevant in the production of livestock commodities, which, unlike crops, are portable between farm operations and can have longer and more clearly delineated stages of production. Growers producing crops do contract for services, but this relationship had traditionally been captured as "custom machine-hire" or custom work. Processors are more likely to engage in production contracts to assure timing, quality and quantity of inputs into their specialized processing plants. Sometimes, capturing the profits from cattle feeding, hog or poultry production, or multiplying and protecting proprietary germ plasm in breeding or seed businesses can be the primary motivating force for other growers, processors or input supply companies entering into crop or livestock production contracts with growers. Because some crop processors or seed companies often need to control the amount and variety planted and the production practices used, they tend to direct the terms of the contracts, with the fees for services and quantity to be produced being the primary negotiation with individual growers. Exceptions also arise, such as cattle feeding, where the contracts are often standard practice and fee contracts prepared by the custom feedlots, not the cattle investor. One advantage of production contracts is that the grower and contractor share risks of both production and marketing of the commodity, though the extent of transferring risk varies from contract to contract. Another advantage is that financing is available either directly from the contractor or indirectly through other lenders who are more assured of loan repayment. Marketing contracts More than 185,000 farms had at least one marketing contract during 1993 (USDA, 1996). Eighty percent of these farms had gross sales of less than $250,000, and they accounted for 33 percent of the total value of production under marketing contracts. Even though all farm sizes used marketing contracts, the largest farms with gross sales reported almost half of total marketing contract volume more than $500,000 annually. Seventy percent of the farms using marketing contracts in 1993 were classified as crop farms (other crops—36 percent, fruit and vegetables—20 percent, corn—11 percent, cotton—3 percent). These farms accounted for 56 percent of the total value of commodities produced under marketing contracts. Even though dairy farmers usually have a verbal agreement with buyers, the USDA data show that dairy farms comprised 17 percent of farms using formal marketing contracts and accounted for 34 percent of the total value of commodities produced under marketing contracts. In 1993, 40 percent of marketing contracts were structured such that total compensation carried across calendar years, perhaps partly for tax deferral purposes.

14

Marketing contracts for livestock commodities were much less common than production contracts; they accounted for 20 percent of farms and for 42 percent of the total value of production under marketing contracts. In contrast, about 80 percent of the farms with Value of selected commodities produced under marketing contracts, 1997 ______________________________________________________________________ Value of production under Commodity marketing contracts ______________________________________________________________________ Percent Barley 19 Canola 46 Cattle 9 Corn 8 Cotton 33 Dry edible beans 3 Eggs 6 Fruits 59 Oats 3 Peanuts 41 Peas 9 Potatoes 43 Rice 31 Sorghum for grain 6 Soybeans 9 Sugar beets 82 Sunflowers 8 Vegetables 24 Total value of production under marketing contracts, all commodities 22 ______________________________________________________________________ Source: USDA, Economic Research Service, 1997 Agricultural Resource Management Study, special analysis. marketing contracts were for crop commodities and they accounted for about 58 percent of the value of production under marketing contracts.

15

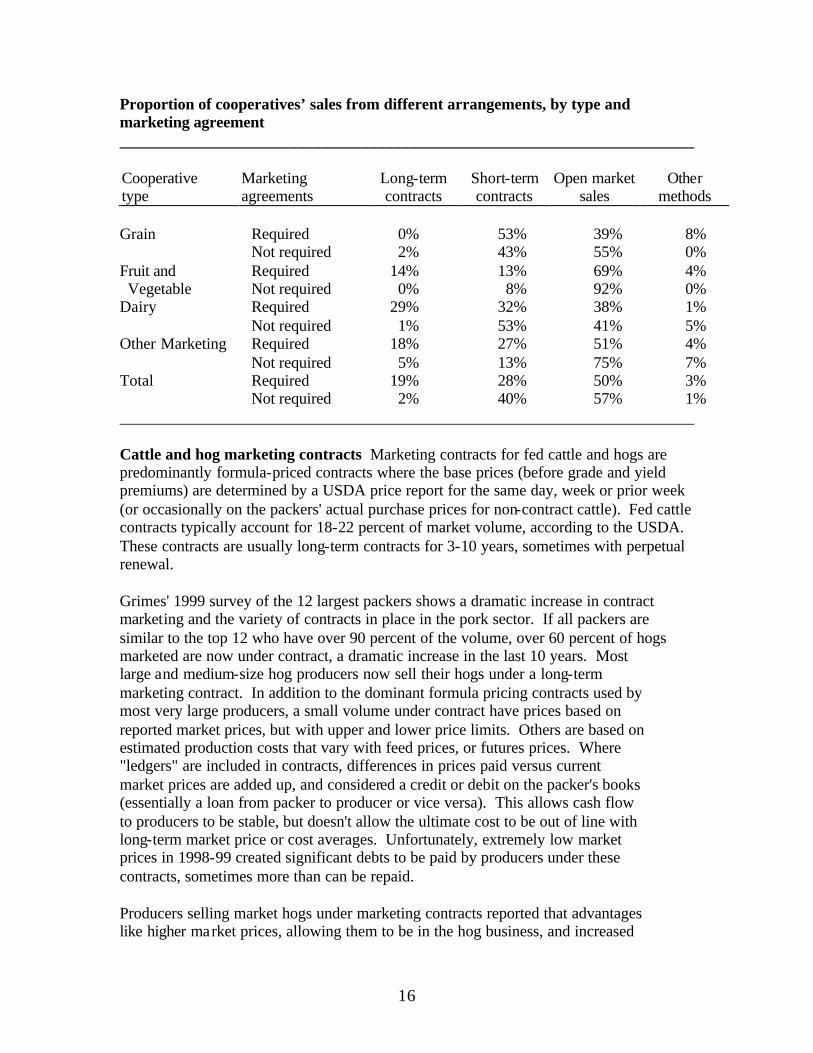

More recent 1997 USDA data for slightly different commodity classes show the overall percent of production under marketing contracts was 22 percent. The commodities for which marketing contracts played an important coordination role were sugar beets, fruit, canola, cotton, potatoes, peanuts, rice, and vegetables. Cooperative marketing agreements Cooperative marketing agreements involve farmers contracting with their own farmer cooperative. Under marketing agreements, members are required to market their output to their cooperative, which in turn provides marketing services. A 1997 USDA survey of marketing cooperatives (Wissman) with total sales of $15 million or more provides an indication of market agreement use. The USDA study included more than half of the total marketing sales of all U.S. agricultural cooperatives. Use of marketing agreements and cooperative characteristics ___________________________________________________________ Proportion with Cooperative Number of marketing type cooperatives agreements ___________________________________________________________ Grain 306 6 Fruit & Vegetable 56 88 Dairy 73 76 Other 87 60 ___________________________________________________________ 1. Marketing agreements included contracts and bylaw provisions that required member marketing through the cooperative. 2. Tobacco cooperatives were not included in average number of members. Considering all cooperatives, those with marketing agreements made 19 percent of their marketing sales with long-term marketing contracts. These were primarily in dairy, with lower percentages elsewhere, especially in grain marketing cooperatives. Grain coops used short term contracts heavily or spot market transactions. Some examples of marketing contracts are described below. We exclude from consideration farmers' direct use of futures or options markets for hedging, as this typically does not involve delivery of farm products, and it is regulated by the Commodity Futures Trading Commission.

16

Proportion of cooperatives’ sales from different arrangements, by type and marketing agreement ________________________________________________________________________ Cooperative type

Marketing agreements

Long-term contracts

Short-term contracts

Open market sales

Other methods

Grain Required 0% 53% 39% 8% Not required 2% 43% 55% 0% Fruit and Required 14% 13% 69% 4% Vegetable Not required 0% 8% 92% 0% Dairy Required 29% 32% 38% 1% Not required 1% 53% 41% 5% Other Marketing Required 18% 27% 51% 4% Not required 5% 13% 75% 7% Total Required 19% 28% 50% 3% Not required 2% 40% 57% 1% ________________________________________________________________________ Cattle and hog marketing contracts Marketing contracts for fed cattle and hogs are predominantly formula-priced contracts where the base prices (before grade and yield premiums) are determined by a USDA price report for the same day, week or prior week (or occasionally on the packers' actual purchase prices for non-contract cattle). Fed cattle contracts typically account for 18-22 percent of market volume, according to the USDA. These contracts are usually long-term contracts for 3-10 years, sometimes with perpetual renewal. Grimes' 1999 survey of the 12 largest packers shows a dramatic increase in contract marketing and the variety of contracts in place in the pork sector. If all packers are similar to the top 12 who have over 90 percent of the volume, over 60 percent of hogs marketed are now under contract, a dramatic increase in the last 10 years. Most large and medium-size hog producers now sell their hogs under a long-term marketing contract. In addition to the dominant formula pricing contracts used by most very large producers, a small volume under contract have prices based on reported market prices, but with upper and lower price limits. Others are based on estimated production costs that vary with feed prices, or futures prices. Where "ledgers" are included in contracts, differences in prices paid versus current market prices are added up, and considered a credit or debit on the packer's books (essentially a loan from packer to producer or vice versa). This allows cash flow to producers to be stable, but doesn't allow the ultimate cost to be out of line with long-term market price or cost averages. Unfortunately, extremely low market prices in 1998-99 created significant debts to be paid by producers under these contracts, sometimes more than can be repaid. Producers selling market hogs under marketing contracts reported that advantages like higher market prices, allowing them to be in the hog business, and increased

17

access to capital were more important than disadvantages (e.g. locked out of higher prices). In the Southeast, prior surveys had found access to shackle space in plants was most important for large hog producers there (Lawrence, Grimes and Hayenga). Feeder pigs are sometimes sold under marketing contracts, with the prices established using a variety of methods. Sometimes prices are based upon reported market prices, a pricing formula based on corn and market hog prices, or even profit-sharing arrangements on the finishing operations. __________________________________________________________________ Twelve largest U. S. pork packers' procurement methods, January, 1999 __________________________________________________________________

Pricing Method Percent Formula (a reported price plus some amount) 44.2 Fixed price tied to futures (i.e., a cash contract) 3.4 Fixed tied to feed prices, no ledger 2.9 Fixed tied to feed prices, 6.9 with ledger maintained Window risk sharing, no ledger 3.6 Window risk sharing, ledger maintained 1.0 Other (packer-owned) 2.3 Spot market purchases 35.8 Source: Glenn Grimes, University of Missouri Issues that occasionally arise are the failure of someone to deliver or acquire cattle or hogs as specified under a contract. These issues are usually settled by individual negotiation of buy-out provisions or by court decisions if lawsuits are necessary to resolve differences. In addition, the Packers and Stockyards Act prohibits packers from undue or unreasonable preference in purchasing livestock from producers. However, the only court case involved IBP's long term purchasing agreement with a group of Kansas cattle feeders; a USDA administrative law judge and a subsequent appeals court decision found that the contract (not offered to others) did not involve undue or unreasonable preferences

18

for those cattle feeders by IBP (In re IBP, Inc., P&S docket number D-95-49, Sept. 25, 1997; IBP, Inc. v. Dan Glickman, No.98-3104, U.S. Court of Appeals for the Eighth District, August 13, 1999). Grain marketing contracts Grain marketing contracts are heavily used in the Midwest, with a large volume of grain marketed being forward priced with an elevator, processor or feeder, based upon futures market prices. More complicated forward contract systems sometimes include deferred payment contracts, hedge-to-arrive contracts for single or multiple crop years, options-based minimum price contracts, and basis only contracts, among others (National Grain and Feed Association). Midwest farmer use of forward contracts in grain sales is substantial. While only limited data are available, a 1992 representative farmer survey in Kansas by Goodwin and Schroeder found 35 percent of corn producers used forward contracts for 37 percent of their crop, and 31 percent of soybean producers used forward contracts for 33 percent of their crop, on average. Patrick, Musser and Eckman found Purdue Top Producer Workshop participants, likely a more sophisticated group of managers, used cash forward contracts extensively. Typically over 60 percent of the producers used forward contracts, pricing over 20 percent of their crop. In addition, minimum price (3-4 percent of producers) and hedge-to-arrive (7-19 percent of producers) contracts were used. Multiple-year hedge-to arrive contracts have been the subject of much litigation, as their design flaws became evident when corn prices reached record levels in 1996 (Lence, Hayenga and Harl). In addition, some grain merchandisers offered option-based contracts without delivery required before they were permitted by the Commodity Futures Trading Commission. A 1999 U.S. Feed Grains Council survey found 12 percent of corn growers were growing specialty corn varieties. The most popular specialty grain contracts were high-oil corn marketing contracts which have premiums based on oil content over standard market prices. Other producers of specialty grains, usually under marketing contracts, grow waxy corn, white corn, popcorn, and food grade soybeans, among others. The European Union's failure to approve import of some GMO products, and the announced labeling requirements for GMO products by Japan and several other countries are fostering a major logistics crisis in grain and oilseed marketing in fall, 1999. The consequence is likely to include identification and separation of various types of GMO commodities from conventionally bred crops, with certification and testing at each stage of the marketing process to assure no mixing of types. This is very expensive, so expect contracts that provide incentives for particular genetics and the paper trail to assure its purity to become common in the grain market, with penalty provisions to make up for losses if noncompliance is traced back to a particular supplier. The emergence of genetically modified grains and oilseeds with added value traits like improved phosphorus absorption in animals, improved oil and protein is likely to lead to an increase in contracting in Midwest grain and oilseeds in the next few years if the current GMO policy issues are resolved. Identity preservation will be essential to capture

19

and insure the benefits of the new specialty traits tailored for particular feed or food uses. Contracts will be necessary to insure producers with a market outlet that will offer a premium for the value-added commodity, and provide customers with an assured supply of specialty products. Potato marketing contracts In the Midwest, most potato marketing contracts are with potato processors who specify the approved varieties, production practices (e.g. chemical use practices) that must be followed, and set the delivery time. The quantity to be produced and the base price are established via individual or group negotiation before planting. Some fresh market potatoes are marketed under contract with cooperative or independent packing houses, with quantity specified in the agreement, and prices based upon quality, shrink, and prevailing market prices at time of delivery. Fruits and nut marketing contracts Most marketing contracts for fruit and tree nuts are offered by cooperatives and processors. In addition to establishing the quantity to be delivered, the contract terms involve specifying a price or pricing formula for a specific commodity grade or quality and the timing of payments. In many instances the contractor provides for any marketing charges and transportation. In 1993, two out of three commercial-sized farms that specialized in the production of fruit and tree nuts had at least one marketing contract (USDA, 1996). Dairy marketing contracts Midwest dairy processors frequently have contracts for milk supply with dairy farmers to assure an outlet for a very perishable product. These typically are continuing relationships, but 30-day notice contracts are prevalent in Minnesota, with prices based upon prevailing market prices and cooperative returns. With the advent of futures contracts for dairy products a few years ago, some processors provide producers with fixed price contracts for selected months or a full year, at their request, based on the level of futures contract prices.

Advantages and disadvantages of contracts Processors may vertically integrate into farm production or employ production contracts to exercise greater control over the quality and timing of deliveries and the quality of inputs used in the production process. Again, reduced risk or greater profits may result. The shifts in risk and associated benefits associated with vertical integration or production contracts depend to a great extent on the nature of the contract and the industry structure. Typically, the benefits associated with integration or contractual control increase as production and marketing interrelationships become more complex and when breakdowns in marketplace competition are most likely (such as opportunistic behavior by contracting parties). For perfectly competitive industries, all firms are subject to price fluctuations caused by supply and demand shifts whether or not they are vertically integrated. Integration or contracting cannot provide protection from such risks, though they may shift the risks into other commodity markets (e.g. corn and soybean meal rather than market hog price risk). While vertical integration and contracting can reduce risks and/or enhance profits for some firms or growers, others may find such a strategy unattractive. Depending on the

20

size of the firm and the extent of the proposed integration, the benefits associated with specialization and scale economies can be greatly reduced or lost, particularly in perfectly competitive markets. For growers in such markets who choose to vertically integrate, the gain may be primarily through enterprise (or business) diversification. Lower risk can result if there are negative or weakly positive price, yield, or profit correlations between the different stages of the production process, different crop or livestock enterprises, and different locations when weather-related risks are important, as they often are in agricultural crops. Studies of contract arrangements or vertical integration have attempted to determine the factors motivating participation by farmers (Leckie; Harris and Massey; Lowenberg-DeBoer, Featherstone and Leatham; Sporleder; Royer and Bhuyan). Many of the circumstances leading to the adoption of contract arrangements are specific to a commodity. Nonetheless, some general reasons for farmers getting involved in contracts were summarized by the USDA (1996): Farmer contract rationale • Income stability. Because most contract arrangements reduce risks in comparison

with traditional production or marketing channels, a contracting farmer’s resulting income tends to be more stable over time;

• Improved efficiency. To the extent that management decisions are transferred to the contractor, producers without substantial expertise can benefit from technical advice, managerial expertise, market knowledge, and access to technological advances (such as high-quality animal breeds or seed stock) sometimes not otherwise available;

• Market security. Contracts typically convey signals to the producer regarding grades and standards that best meet consumer demands. By entering into these arrangements, the grower can guarantee that someone will buy the produce if the specifications are met. Also, by varying degrees, some amount of the market-oriented price risk is transferred from the producer to the contractor;

• Access to capital. Production contracts eliminate much of the need for growers to obtain production credit because the contractor provides most of the inputs. In most instances, the contractor maintains title to the product and such advances are not usually characterized as credit transactions. Contracts also provide a means for a farmer to increase the volume of business with relatively limited capital requirements. Income stability associated with contract arrangements may allow a more favorable credit rating for the borrower, thus enhancing access to credit.

Contractors' rationale Processors' and other contractors' rationale for contracts were also summarized by the USDA: • Controlling input supply Because many agricultural processing facilities involve

extensive investments in buildings, equipment, and labor, processors must establish an orderly flow of a large volume of uniform products to control operating costs;

21

• Improving response to consumer demand. By asserting more control over production processes, contractors can better respond to changing market conditions. There may be a faster response to changing consumer preferences, which may require producers to alter standards or product form.

• Expanding and diversifying operations . Processors and other businesses can strengthen their competitive position in the market through contract arrangements by virtue of increased coordination and efficiencies available with larger volumes of business. Even though the contractor accepts a greater share of the market (price) risk with production contracts, the benefits of having a regular supply of uniform goods probably outweigh the costs. Large, integrated firms may also capture returns in another phase of production.

Possible disadvantages of contracts According to the USDA, not all aspects of contract arrangements are viewed positively: • Loss of independence

The loss of entrepreneur ial independence is perhaps the largest disadvantage to the farmer (Hamilton). Under contracts, many of the production practices are specified in order to bring a uniform product to market. Practices specified may include schedules of chemical application or of feeding, and the types of inputs used.

• Inequitable risk and return sharing Farmers become providers of labor, land, utilities, and some management services for a fee, or are guaranteed market access for a product, which must meet certain specifications. Farmers (sometimes influenced by their lenders) judge whether the trade-off of income stability and/or a confirmed market is a fair exchange for the loss of independence. Contracts should specify who owns the product and holds the risk of loss in the crop or livestock, and when ownership passes from one party to another, if at all. Since contracts are legal documents, attorney fees are an additional cost to help insure equitable terms in the agreements.

In addition, the possibility of the contractor not providing livestock or poultry under the contract, providing low quality inputs, or non-renewal of a contract which requires specialized assets have been raised as potential disadvantages. The lack of adequate local market competition in the spot market or for new contract arrangements when contracts expire may put growers of specialty commodities at a significant bargaining disadvantage. Growers are also subject to the risk of the contractor’s financial failure, with payment for services or products at risk, especially if there is no enforceable security interest in the crops or livestock grown under contract. Some broader concerns expressed regarding marketing contracts focus on the incentive for market manipulation by processors having a high proportion of their purchases under contracts based upon reported spot market prices. If there are only few competitors in the spot market, the potential for spot market manipulation may exist, and spot market prices might be lower than "competitive" market prices for independent producers (and formula-priced contract suppliers too).

22

In addition, some concerns have been raised regarding the lack of transparency in markets dominated by contract supplies, with the corresponding decline in spot market volume and price information. Concerns about inequities among contract and non-contract producers, and inequities in the terms of marketing contracts offered to different producers have been raised. These have prompted calls for mandatory price reporting, including contract supply prices (recently passed in Congress for cattle and hogs). Some organizations have even called for the banning of all contracts for livestock procurement by packers, along with a ban on all packers feeding of livestock. Some states have enacted such laws. For example, Iowa has banned large packer ownership of livestock feedlots since 1975, and banned packer feeding of hogs since 1996. Additional societal issues Contract arrangements and the resulting organizational structure in agriculture may pose additional societal issues, such as: • Environmental concerns .

The trend toward large confined animal feeding facilities presents additional environmental concerns, such as animal waste management and use of chemicals for disease control. Because environmental controls may increase costs to the farmer, he or she may wait to implement environmental practices until the contract specifies and/or compensates for the additional costs. As growers or contractors become more sensitive to increasingly hot environmental issues in their area, contracts may have to contain language addressing these issues.

• The shrinking numbers of farms and concentration of production. Contracting may not necessarily lead to fewer farms, since farms of all sizes use contracts. But it does lead to concentration of decision-making and to less diversity in products and production practices. Agricultural communities are more vulnerable to decisions made outside the community. The number of farms will continue to decline, with or without contracting, and land will be absorbed by other farms. Fewer and larger farms have implications for rural communities in employment, local tax policy, and infrastructure planning.

The benefits and costs of contracting Farmers contract with other growers to leverage their capital, capture economies of scale and efficiency gains from specialization (Rhodes). Processors use contracts because they desire uniformity and predictability to suit consumers, but they also benefit from lower costs in processing, packing, and grading. The consumer may be able to buy chicken or vegetables at a few cents per pound less. Farmers benefit by having a guaranteed market outlet, sometimes a guaranteed price, and access to a wider range of production inputs, and they can concentrate their management efforts on a particular part of the production process. How other benefits and costs are distributed to the industry and the rural community has not been quantified well; these include the impacts of consolidation, inputs supplied by contractors rather than local retailers, and marketing channel control distributed away from spot markets.

23

One point deserves emphasis. Though there are few surveys available, most farmers with contracts have expressed general satisfaction with contract terms, with advantages greater than the disadvantages (Lawrence, Grimes, and Hayenga). The majority of growers with contracts typically plan to continue contract usage. Some forms of contract production might actually be viewed as granting farmers some degree of market power, if one defines "market power" as the ability to influence price or other contract terms, or walk away from the contract if terms are not acceptable. Contract agriculture sometimes provides opportunities for alternative production enterprises which otherwise would not be feasible for producers. As biotechnology becomes more accepted worldwide and innovative new products are developed, the contracts which likely will be involved will offer expanded opportunities for producers for more enterprise diversification. However, after the first adopters of the new technology capture some improved returns in early contracts (with higher risk), subsequent growers under marketing or production contracts are likely to be paid only competitive market returns to produce the higher-value commodities (Hayenga and Kalaitzandonakes). Effects of contracting on farm-level risk Studies have examined the linkage between vertical integration and farm-level risk. Whitson, Barry, and Lacewell eva luated the risk-return effects of selling fed calves or holding them through subsequent stages in the production process. The authors found that, at low-income levels, the preferred sequence involved production of weaned calves with subsequent placement in a feedlot, a result consistent with negative profit correlations between the different stages of the production process. Knoeber summarized several studies of hog and poultry production contracts. They document that contract production does in fact shift risk from the grower to the contractor, but growers pay for this with reduced expected income. He argues that these studies suggest that risk shifting is the fundamental reason for contract production. But other studies in timber and farmland use conclude otherwise. He explores whether contracts offer superior incentives to invest in specialized assets like building and equipment, or genetics, superior incentives for better effort by growers, superior incentives for contractors to provide higher quality inputs or do more research into better production methods. He reports that Frank and Henderson found that risk shifting and providing incentives for innovation are reasons for vertical coordination and contract production. Effects of contracting on spot market prices Ward, Schroeder, Barkley and Koontz examined the impact of captive supplies of fed cattle on spot market prices. After summarizing prior studies that found small or inconclusive impacts on prices, their analysis of major beef packer purchases for one year found a relatively weak relationship between captive supply deliveries and spot market prices. Prices for cattle purchased by marketing agreements were slightly higher ($.07-.10 per cwt.) than spot market cattle prices. Cattle purchased using a fixed price contract had lower prices than spot market cattle, perhaps because they had been purchased earlier in an upward trending market.

24

Effects of contracting on market supply If a production or marketing contracting system shifts risk and facilitates bringing more capital into production of any commodity, there should be a shift in the industry supply curve that can lead to lower market prices and producer margins, at least temporarily. While no studies have documented that impact, lower market prices (and incomes) in response to lower risk for producers should not be a surprising result. Further, long-term contracts with assured volumes and prices may reduce the responsiveness of growers to cyclical prices. More volume stability can have positive effects on industry efficiency and consumer acceptance, but it could aggravate the extent and magnitude of cyclical price fluctuations, increasing the volatility of industry prices and producer incomes. Effects of contracting on producer access to markets For some growers, the issue associated with increased contracting is reduced access to markets. For many years, the only access to markets in many industries has been through a contract -- e.g. processing vegetables, turkeys, and broilers. In others, like hogs, the spot market is rapidly declining, and producers may have little alternative than to become contractually or cooperatively linked to processors, or become a residual supplier (which bears potentially big risks or rewards). The GMO issue in grains and oilseeds, and biotech value-added consumer traits likely in the near future, is likely to expand greatly the use of contracting to provide assurances to farmers and processors regarding what they are going to receive from each other. To the best of our knowledge, the current economic literature has not addressed the issue of reduced market access by noncontracting producers. However, it is obvious that as a higher percent of an industry's volume is vertically integrated or contractually linked, more independent producers are unable to be in the business without a contract, with more restricted market outlets and potentially greater risk with specialty crops, or less competition, especially when production levels approach processing capacity. Certainly, there is a possibility that independent producers could be harmed by increased levels of contracting, but there is little evidence of significant harm to date. At the same time, the increasing demand for "production services" by other farmers and processors and the increased demand for the contractual quantity and quality assurance from marketing contracts by processors and merchandisers could offer new market opportunities for Minnesota growers.

Minnesota industry survey results Several Minnesota agricultural industries were selected for analysis in consultation with the Minnesota Department of Agriculture staff. The primary industries where contracting was expected to be extensive were processing vegetables, potatoes, market hogs, dairy, and turkeys. A small group of 2-4 knowledgeable producers and processors per industry were selected for telephone interviews. Telephone interviews were conducted primarily during September 1999, asking their views on the: • Percent of volume produced involved in production and marketing contracts in

Minnesota in their industry in 1999; • Rationale for contractors and growers engaging in each type of contract;

25

• Estimated growth in production and marketing contracts in 5 years; • Rationale for estimated growth; • Perceived issues, concerns, or problems related to contracts in their industry. Since only a small nonrandom sample was selected for interview, the estimates or projections reported should not be considered statistically precise. However, the views of very knowledgeable industry members regarding likely direction of change and rationale for contracting use can be instructive. (A more detailed summary of the interview results is in the Appendix.) There are a large volume of Minnesota vegetables, potatoes, hogs, turkeys and milk produced or marketed under some type of contract, though the knowledgeable industry members sometimes have widely varying estimates of the contract market share in some industries. These contracts are entered into voluntarily, and have advantages that conceivably outweigh the disadvantages for both parties, or both parties would not sign the contract. Processing vegetables have been produced exclusively under contract with processors for many years, generally with few problems. Production contracts are essential for very perishable products and highly specialized plants. Hog production contracting is relatively new, but increasing, with most contracts between producers or producers with cooperatives, not with packers. Marketing contracts have been in place in the dairy industry for years, but new futures contracts are allowing more fixed-price contracts than were possible before. Turkey, hog and potato marketing contracts with processors are important and growing, especially in hog marketing. The recent financial distress due to low hog prices is likely to force many more hog farmers into marketing or production contracts if they need outside capital to stay in business or expand. Most persons interviewed saw no major problems or issues. Exceptions were in the processing vegetable and potato industry where organizations have formed to offset with the perceived weak bargaining position of growers against processors. Some "ledger" contracts in the pork industry have drawn public attention as debts built up under extended periods of low pork prices, but producers with those contracts also received much higher prices in 1998. One packer has offered new contract proposals that would work off or eliminate those producer debts in question. General issues brought up in several industries in this survey and elsewhere include the complexity of contracts and the difficulty of anticipating their implications, especially the potential problems. Yet, the likelihood is strong that contract linkages among producers and their customers will likely increase. Sources of capital for agriculture generally prefer to lend where contracts reduce the perceived risk, and the turkey and hog industries are perceived as risky industries. Many hog producers' financial positions have severely eroded in the last two years, and more production and marketing contracts to limit that risk are likely. The dairy industry used to have significant price protection from

26

the government, but the new riskier market environment is likely to lead to much more use of futures and options-based short or intermediate-length contracts to reduce price risk, and longer-term contractual arrangements may follow. Industries like grains and oilseeds have few long-term contracts. Yet, GMO issues or value-added traits built into the seed will require identity preservation and many more contractual relationships throughout the entire production and marketing system. Food safety concerns are also likely to spawn contractually linked production and marketing systems (food chains) which can assure customers of best practices, no improper chemicals or additives, and offer trace-back to the source of any problem that does arise. The current level of financial stress could also induce farmers to accept terms in new or renewed contracts that would not have been accepted in more prosperous times Consequently, the reader should expect changes in the amount and types of contracts to continue to occur. While no pressing issues are identified in our small Minnesota survey, there are some policy alternatives below which we developed, or have been proposed or are used elsewhere. These policy options may warrant examination by the Minnesota Department of Agriculture as the Commissioner develops recommended policies regarding contracting in agriculture for consideration by the legislature.

Policy alternatives

The primary policy issues and alternatives relate to industry consolidation and market power concerns, and more practical issues associated with contract complexity, information or bargaining position inequities when contract renewals involve growers subject to great losses if a particular contractor chooses not to renew. We emphasize policy alternatives best suited to the state, since many broader issues (e.g., antitrust) probably are dealt with more effectively at the federal level. For example, the U.S. Department of Justice could be funded specifically to maintain a substantially higher level of oversight over structural shifts in food and agriculture. This could involve more staff enforcing Clayton Act limits on food and agricultural sector mergers expected to diminish competition substantially, or dealing with potentially illegal contracts (tying arrangements) requiring use of a company's other products or services in order to do business with them on other products in which they have a dominant market position. Recent mergers and acquisitions in the food and agricultural sector have attracted attention, as the consolidation of the sector continues. These have been in the seed and chemical industries (e.g. Monsanto and several seed companies, DuPont and Pioneer), the grain merchandising industry (e.g. Cargill and Continental Grain), in the farm equipment business (e.g. Case and New Holland), and the pork sector (e.g. Smithfield acquiring Carroll's and Murphy's pork production operations). Some industries in Minnesota have limited number of market outlets for farmers, where one or a few processors dominate the local market. There are some potential policy options at the state level to deal with increasing concentration and reduced competition concerns, or potentially illegal tying or packaging

27

product sales or purchases by powerful firms dealing with farmers. One possibility would be to provide an office to serve as a focal point in the MDA or the Attorney General's office to monitor concerns and collect complaints, and provide a vehicle to forward those more effectively to appropriate state and federal agencies to get their attention. Go beyond the fairly common corporate farming laws to prohibit packer feeding of hogs. Iowa passed such a law in 1996. This was intended to protect the independent family producer from what some might view as unfair corporate competition. However, processor feeding of the pork industry's competitors --poultry and beef-- was not prohibited, so a competitive tool was made unavailable to the pork industry. In addition, production activities could be shifted into other states, or new contractual agreements that do not involve ownership could be used, so the effectiveness of such laws at the state level is questionable. It is difficult to determine whether such laws have slowed the decline in the number of small and medium-sized hog production operations. If there are economic advantages to contract arrangements, and competing industries, states and countries use those contract systems, that may make it difficult for your state’s industry members to compete. Prohibit all marketing contracts with farmers, especially in the beef industry. Proponents of restrictions on contracting argue that fewer buyers are available for independent producers, and contractors use those supplies to push down prices in the spot market. If there are advantages to both parties voluntarily involved in marketing contracts, as discussed above, there needs to be significant evidence of social benefits coming from such a radical restriction of business relationships extensively used elsewhere in agriculture here and abroad before that could be reasonably contemplated. Since contract linkages limiting risks are often necessities before lenders will consider financing beginning farmers or expansions by present farmers, significant limitations on contracting could have significant adverse effects on many farmers. Where market outlets are limited, policies facilitating farmer organizations or government intervention to counter perceived market power or abuses in contracting are worth considering. In other situations, policies facilitating greater transparency in the contract markets, producer education regarding contract complexities and evaluation of potential impacts may be worth considering. Several possibilities are presented below. Collective action by farmers Cooperatives Since 1922, the Capper-Volstead Act has allowed farmers to forge alliances among themselves to achieve countervailing market power so long as it does not "unduly enhance" price.2 Section 1 of the Capper-Volstead Act of 19223 provides protection from antitrust challenge for producers who seek to bargain collectively with and contract with processors and input suppliers. To come within the protection of the Capper-Volstead Act, an organization must— 2 Capper-Volstead Act, 7 U.S.C. §§ 291, 292. See generally 14 Harl, Agricultural Law § 137.04 (1999). 3 7 U.S.C. §§ 291, 292.

28

(1) be operated for the mutual benefit of its members; (2) either limit each member to one vote regardless of the amount of stock or membership capital the member owns or, if dividends are paid on the basis of members' stock or membership capital, the dividends must be limited to a maximum of eight per cent per annum; (3) not handle a greater amount of products from nonmembers than from members; and (4) not be operated for profit.

Closed cooperatives The models most often used to design new-generation cooperatives come from American Crystal Sugar Company and Minnesota Corn Processors; both used a California model of cooperatives that required grower or producer agreements as well as an up-front equity investment. The characteristics of new-generation cooperatives have emerged over time and distinguish them from the traditional open cooperatives. Several attributes of these new-generation cooperatives are (Patrie):

• Equity investment is required prior to establishing delivery rights.

• Producer agreements between the cooperative and the producer link delivery of products to equity units purchased.

• Total delivery rights make equal processing capacity available for sale.

• Purchase of commodities is authorized by the cooperative for undelivered contracts.

• The transferability of equity feature means that shares can be sold to other eligible producers at prices agreed to by the buyers and sellers. Equity shares appreciate or depreciate in value based on the earnings potential they represent. Although the cooperative's board of directors doesn't set prices, they must approve all stock transfers so shares do not get into the hands of ineligible persons.

• High levels of cash patronage refunds are issued annually to the producer. Since equity is achieved in advance of business startup, a majority of the net can be returned annua lly to producers in cash.

These farmer cooperatives allow different capital and voting structures and limited rather than open membership. They have been permitted legislatively in some states. Many of the new processing cooperatives are "closed cooperatives". Membership is limited to the farmers who founded them and, in some instances, had the means to invest large amounts of capital.

Lawless, et al., suggest these new generation cooperatives typically take the raw products of their members' farms and process them in cooperatively-owned facilities. It differs from most traditional marketing cooperatives in the following ways: It is market-driven, in that market demand for the processed end-product determines the appropriate scale of the business-- and that, in turn, limits the size

29

of the membership, so that these become "closed" cooperatives. Furthermore, tradable membership shares not only allocate rights to deliver units of the farms' raw products, but these shares also spread "up-front" capitalization responsibilities equitably among members. In situations where a processing plant closes, specialized producers may use a closed cooperative to purchase the plant.