nols, tax credits and the loss limitation rules – post-tcja

TRANSCRIPT

NOLs, Tax Credits and the Loss Limitation Rules – Post-TCJA Moderator: John Orr Jr., Equinox Senior Director of Tax New York, NY [email protected] Ph. 646.572.4689 Panelists: Joseph Pari, Weil, Gotshal & Manges LLP Washington, D.C. [email protected] Ph. 202.682.7001 Paul Schockett, Skadden, Arps, Slate, Meagher & Flom LLP Washington, D.C. [email protected] Ph. 202.371.7815 Annette Ahlers, Pepper Hamilton LLP Los Angeles [email protected] Ph. 213.928.9825

April 1, 2019 l Tax Executives Institute Washington, D.C.

►Impact of TCJA on Losses ▸Section 172 ▸Section 382 ▸Section 163(j)

►Planning and M&A Considerations because of TCJA changes to NOLs and other tax attributes

Agenda 1

► Net operating losses (NOLs) arising in tax years ending after 12/31/2017 • Indefinite carryforward and no carrybacks • Old rules apply to NOLs from tax years ending on or before 12/31/2017 • NOLs for property and casualty insurance companies and farming losses

can still be carried back two years and offset 100% of the income • Mixed use companies?

▸ Use of NOLs for taxable years beginning after 12/31/2017 • Can only use these NOLs to offset up to 80% of taxable income for the

post 12/31/2017 tax year to which the NOL is carried

► No changes to capital loss carryforward and carryback rules • Carryback 3 years and carryforward 5 years • Only capital gains can offset capital losses • Permanent difference if carried back?

Impact of TCJA – Section 172 2

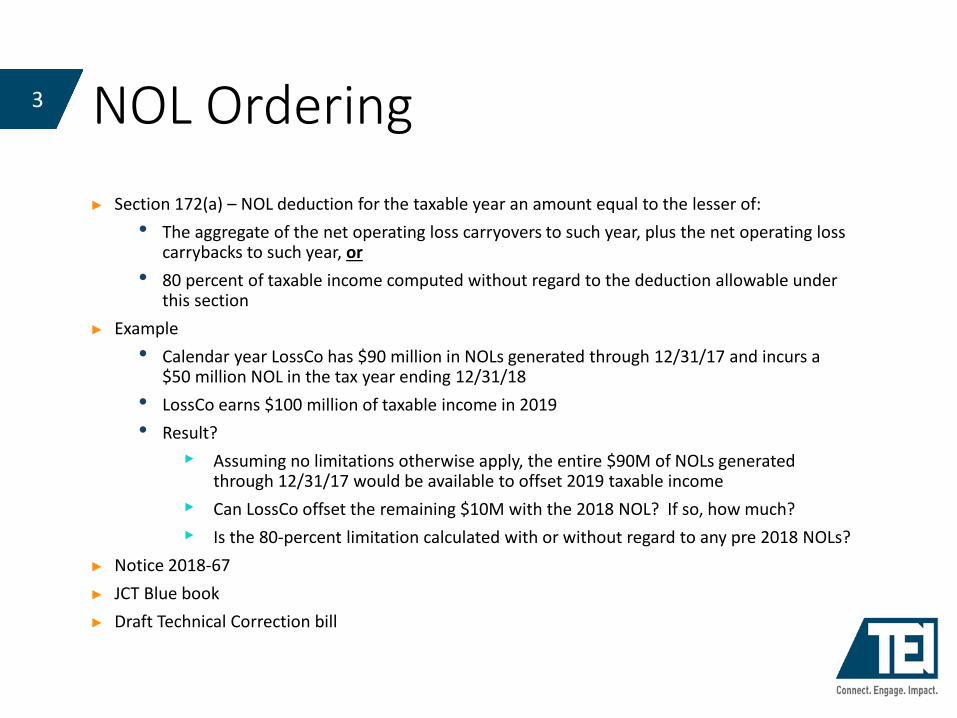

► Section 172(a) – NOL deduction for the taxable year an amount equal to the lesser of: • The aggregate of the net operating loss carryovers to such year, plus the net operating loss

carrybacks to such year, or • 80 percent of taxable income computed without regard to the deduction allowable under

this section ► Example

• Calendar year LossCo has $90 million in NOLs generated through 12/31/17 and incurs a $50 million NOL in the tax year ending 12/31/18

• LossCo earns $100 million of taxable income in 2019 • Result?

▸ Assuming no limitations otherwise apply, the entire $90M of NOLs generated through 12/31/17 would be available to offset 2019 taxable income

▸ Can LossCo offset the remaining $10M with the 2018 NOL? If so, how much? ▸ Is the 80-percent limitation calculated with or without regard to any pre 2018 NOLs?

► Notice 2018-67 ► JCT Blue book ► Draft Technical Correction bill

NOL Ordering 3

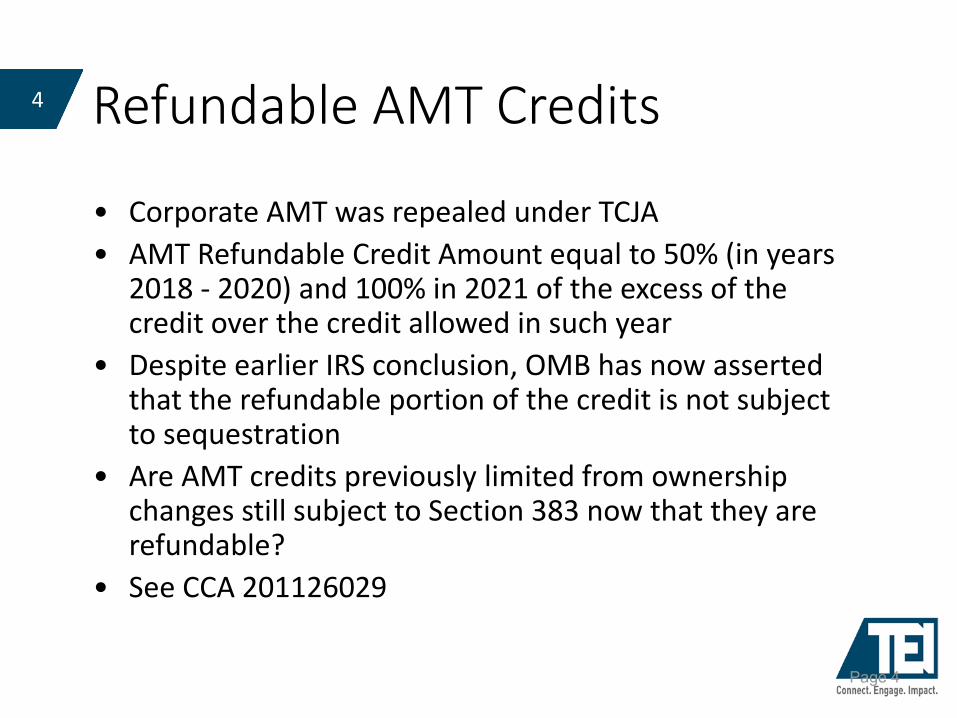

• Corporate AMT was repealed under TCJA • AMT Refundable Credit Amount equal to 50% (in years

2018 - 2020) and 100% in 2021 of the excess of the credit over the credit allowed in such year

• Despite earlier IRS conclusion, OMB has now asserted that the refundable portion of the credit is not subject to sequestration

• Are AMT credits previously limited from ownership changes still subject to Section 383 now that they are refundable?

• See CCA 201126029

Refundable AMT Credits

Page 4

4

Purpose of Section 382: • Limits ability of a corporation to offset future income using

NOLs generated prior to a “change in ownership” and certain built-in losses recognized post-change

Policy: • Enacted to prevent “trafficking” in NOLs • Is designed to prevent abuses involving the acquisition of loss

corporation stock followed by the contribution of income-producing assets or diversion of income-producing opportunities to the corporation.

• Other limitations on attributes may apply in addition to Section 382, including Section 269, SRLY, disallowance of the NOLs based upon a review of their origin, 1.1502-36, etc...

Overview of Section 382

Page 5

5

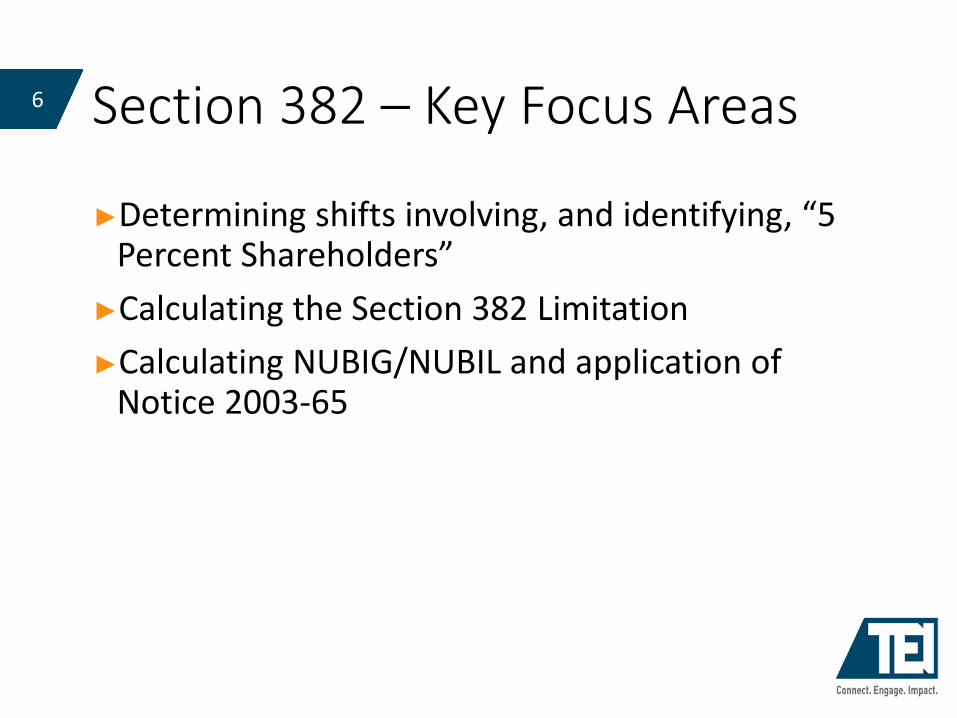

►Determining shifts involving, and identifying, “5 Percent Shareholders”

►Calculating the Section 382 Limitation ►Calculating NUBIG/NUBIL and application of

Notice 2003-65

Section 382 – Key Focus Areas 6

What or Who is a 5% Shareholder? 7

Any individual who owns directly or indirectly an amount of the loss corporation stock that aggregates to a 5% ownership interest by value

Include indirect 5% shareholders • Trying to get to “arms and legs”

A C

X

A is indirect 5% shareholder of LossCo

A sells 30% of X stock to C

24% shift in LossCo (30% multiplied by 80%) even though direct shareholder X still owns 80% B

LossCo

30%

80% 20%

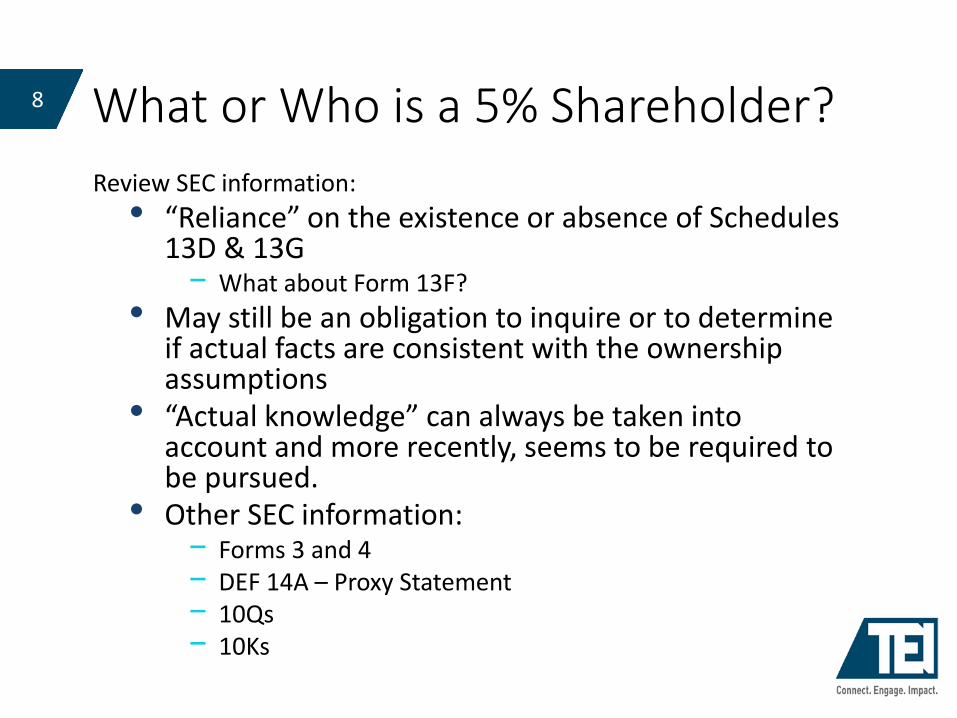

Review SEC information: • “Reliance” on the existence or absence of Schedules

13D & 13G − What about Form 13F?

• May still be an obligation to inquire or to determine if actual facts are consistent with the ownership assumptions

• “Actual knowledge” can always be taken into account and more recently, seems to be required to be pursued.

• Other SEC information: − Forms 3 and 4 − DEF 14A – Proxy Statement − 10Qs − 10Ks

What or Who is a 5% Shareholder? 8

Investment advisors might not count as 5% shareholders • PLRs distinguish between a person who has the right to the

dividends and proceeds from the sale of a loss corporation’s stock (the “economic owner”) and the investment advisor, who holds the power to vote and/or dispose of such stock (the “reporting owner”) − Right to dividends − Right to proceeds upon the sale of stock

• PLR 9533024, PLR 9725039, PLR 200806008, and PLR 200902007

• If not a separate 5% shareholder, the stock is treated as held by the public group

• Similar rule for “family of funds” filing as a 5% shareholder where no fund owns 5% or more

Section 382 – Investment Advisors 9

► 1.382-2T(k)(2) – IRS ruling policy allows/requires loss corporations to use “actual knowledge” to determine 5% owners, including indirect 5% owners.

► Actual Knowledge can include: ▸ Schedules 13D’s and 13G’s filed with SEC ▸ Stock Surveillance company engaged by loss corporation ▸Monitoring brokerage houses ▸ Direct Inquiries of certain persons filing Schedule 13Gs. See,

PLR 201403007 (September 19, 2013). ► In PLR 201403007, the taxpayer made the statement that, “Aside

from these methods, Company has no other actual knowledge regarding or relevant system of tracking the owners of its stock.”

Section 382 – Tracking 5% Shareholders—The Pursuit of “Actual Knowledge”

10

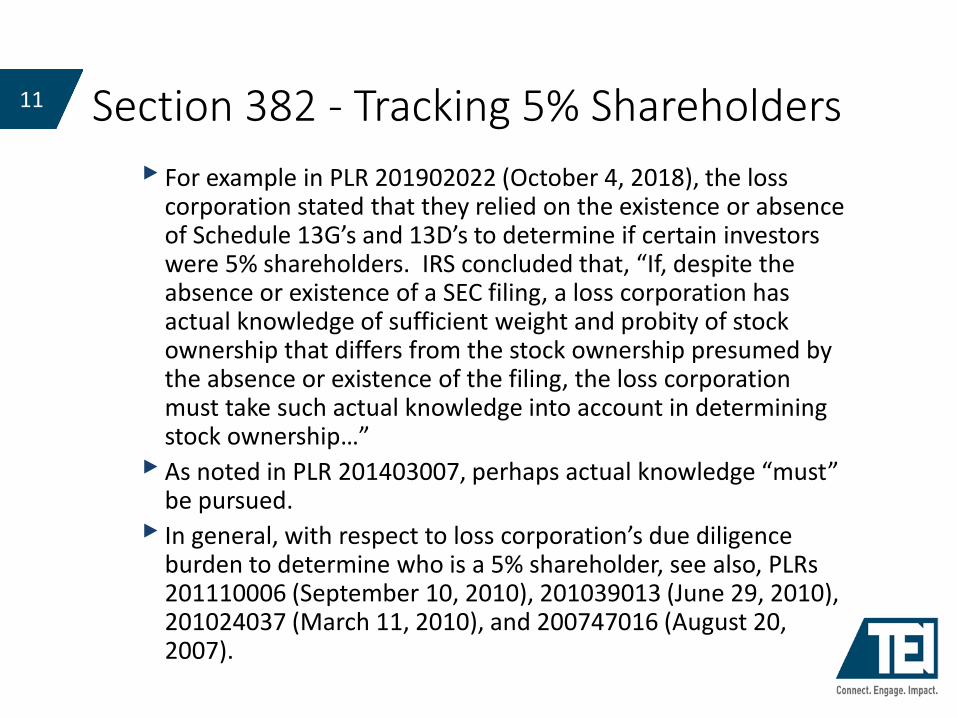

▸ For example in PLR 201902022 (October 4, 2018), the loss corporation stated that they relied on the existence or absence of Schedule 13G’s and 13D’s to determine if certain investors were 5% shareholders. IRS concluded that, “If, despite the absence or existence of a SEC filing, a loss corporation has actual knowledge of sufficient weight and probity of stock ownership that differs from the stock ownership presumed by the absence or existence of the filing, the loss corporation must take such actual knowledge into account in determining stock ownership…”

▸ As noted in PLR 201403007, perhaps actual knowledge “must” be pursued.

▸ In general, with respect to loss corporation’s due diligence burden to determine who is a 5% shareholder, see also, PLRs 201110006 (September 10, 2010), 201039013 (June 29, 2010), 201024037 (March 11, 2010), and 200747016 (August 20, 2007).

Section 382 - Tracking 5% Shareholders 11

►Fair market value of old loss corporation multiplied by a published IRS rate (long-term tax-exempt rate) subject to certain adjustments, including certain capital contributions, excess nonbusiness assets (e.g., cash) and/or corporate contractions. ▸Final regulations issued on April 25, 2016 modified

the calculation of the long-term tax-exempt rate. These rules effectively lower the rate for any ownership changes occurring in November 2016 and thereafter.

▸The rate for March 2019 was 2.39%. ►Section 383 limits other attributes (e.g. credit

carryforwards)

Calculating the Section 382 Limitation 12

► Section 382(h) requires any loss corporation that undergoes an ownership change to determine whether it has a Net Unrealized Built-in Gain (“NUBIG”) or Net Unrealized Built-In Loss (“NUBIL”)

► If a corporation has a NUBIL, then built-losses recognized during the five-year recognition period are treated as pre-change losses and subject to the Section 382 annual limitation

► If a corporation has a NUBIG, then built-in gains recognized in any year during the five-year recognition period will increase the Section 382 limitation for that year

► A stand-alone loss corporation can have a NUBIG or NUBIL, but not both

► Threshold amount (if not met or exceeded, NUBIG or NUBIL is 0): ▸$10 million or ▸If less than $10 million, 15% of the value of the

assets

Determination of Built-in Gains and Losses

13

► Notice 2003-65 provides safe harbor guidelines regarding the determination of NUBIG/NUBIL and the identification of RBIG/RBIL ▸ Modified by Notice 2018-30 to take into account certain aspects of TCJA

(discussed on slide 15)

► 2018-2019 Priority guidance plan released/updated on November 8, 2018 calls for additional guidance under section 382(h)(6) in response to TCJA

► Practice Tip: All prior ownership changes, even in closed years, should be reviewed to determined if Section 382 limit may be increased even if closing agreement issued (See Vail Resorts)

Notice 2003-65

Page 14

14

►Two approaches for determining when items of income, gain, deduction, and loss are treated as RBIG and RBIL ▸ 1374 Approach ▸ 338 Approach

►Similar results under both approaches for dispositions ►Different results with respect to items of income and

deductions ▸ 1374 more narrow approach with fewer items as RBIG and RBIL

►Must pick one or the other ►Treasury has commented that they may issue guidance

that takes away the electivity

Notice 2003-65 (cont’d)

Page 15

15

► The TCJA provides that new and used qualified property acquired and placed in service after 9/27/17 may be eligible for immediate expensing. ▸ Qualified property generally includes tangible property (i.e., intangible assets and

goodwill are excluded)

▸ Immediate expensing automatically applies to qualified assets unless elect out

▸ Includes deemed asset purchases (Section 338(h)(10))

▸ Phased down of 100% allowance by 20% per year generally starting in 2023

► Notice 2018-30 – Requires that the calculations under Notice 2003-65 with respect to the Section 338 approach in calculating RBIG must use the prior law cost-recovery system and not the 100-percent expensing approach as stated in new Section 168(k). ▸ As a result, loss corporations must maintain detailed records supporting the RBIG

calculation, and not just refer to what the taxpayer would have done in an actual Section 338 transaction.

▸ Creates additional record keeping

Notice 2018-30 16

Replaces old “earnings stripping” rule under former Section 163(j) which limited interest deductions paid by corporations to related tax-exempt persons Applies to all businesses regardless of form, with exceptions for taxpayers with average annual

gross receipts of $25M or less for the prior three-year period. ▸ No grandfathering, and ▸ applies regardless of tax status of payee or payee’s relationship to taxpayer (related and 3rd party)

► Limits the deduction for “net business interest expense” to 30% of “adjusted taxable income” ► Adjusted taxable income is taxable income computed without regard to (similar to EBITDA):

▸ any item of interest, gain, deduction or loss that is not properly allocable to a trade or business ▸ any business interest or business interest income ▸ the amount of any net operating loss deduction ▸ the new 20% deduction for certain pass-through income (199A) ▸ in the case of tax years beginning prior to Jan. 1, 2022, any deduction allowable for depreciation,

amortization or depletion (after, the calculation becomes similar to EBIT)

► If an amount of business interest is not allowed as a deduction for a tax year due to the §163(j) limitation, the amount is carried forward and treated as business interest paid in the next tax year (i.e., a disallowed business interest expense carryforward).

► But there is no carryforward of an excess §163(j) limitation amount. ► Following general carryforward rules, current year business interest expense is deducted

before disallowed business interest expense carryforwards.

Section 163(j) -The New Net Interest Limitation

17

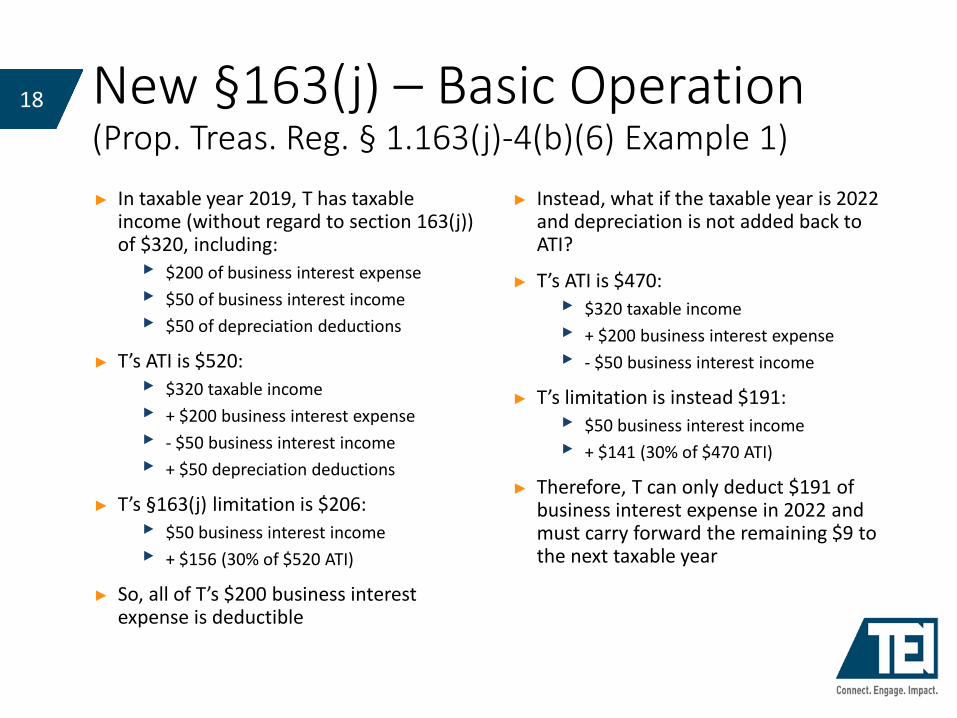

► In taxable year 2019, T has taxable income (without regard to section 163(j)) of $320, including: ▸ $200 of business interest expense ▸ $50 of business interest income ▸ $50 of depreciation deductions

► T’s ATI is $520: ▸ $320 taxable income ▸ + $200 business interest expense ▸ - $50 business interest income ▸ + $50 depreciation deductions

► T’s §163(j) limitation is $206: ▸ $50 business interest income ▸ + $156 (30% of $520 ATI)

► So, all of T’s $200 business interest expense is deductible

► Instead, what if the taxable year is 2022 and depreciation is not added back to ATI?

► T’s ATI is $470: ▸ $320 taxable income ▸ + $200 business interest expense ▸ - $50 business interest income

► T’s limitation is instead $191: ▸ $50 business interest income ▸ + $141 (30% of $470 ATI)

► Therefore, T can only deduct $191 of business interest expense in 2022 and must carry forward the remaining $9 to the next taxable year

New §163(j) – Basic Operation (Prop. Treas. Reg. § 1.163(j)-4(b)(6) Example 1)

18

New §163(j) Statute – In General (cont’d) ► Excepted Trades or Businesses ▸ Interest expense allocable to a trade or business described in

§163(j)(7) (i.e., an “excepted” trade or business) is not subject to limitation under §163(j).

▸ The term “trade or business” does not include – ▸ Employee services ▸ Certain regulated utilities ▸ An electing real property business ▸ An electing farming business

▸ An election by an electing real property or farming business is irrevocable.

▸ Property used in a trade or business that is exempt from the §163(j) limitation generally is excluded from the definition of “qualified property” for 100% bonus depreciation eligibility under §168(k).

19

New §163(j) Proposed Regulations – In General ► Treasury released proposed regulations on November 26, 2018 that address new §163(j) (the

“Proposed Regulations”). ► The Proposed Regulations are organized into 11 sections – Prop. Reg. §§ 1.163(j)-1 through

1.163(j)-11. 1: Definitions 2: Computation of limitation 3: Relationship of limitation to other provisions affecting interest 4: C corporations and consolidated group members 5: Disallowed business interest expense carryforwards of C corporations 6: Partnerships and S corporations 7: Foreign corporations 8: Foreign persons with effectively connected income 9: Excepted trades or businesses 10: Allocation of income and expense to non-excepted and excepted trades or businesses 11: Transition rules

► Effective Date – prospective but taxpayers may elect to adopt the Proposed Regulations on retroactive basis ▸ Final regulations will be effective for tax years ending after the date on which they are

published in the Federal Register. ▸ Taxpayers and related parties (within the meaning of §§267(b) and 707(b)(1)) may elect to

adopt the Proposed Regulations for tax years beginning after December 31, 2017, so long as all rules are applied on a consistent basis.

20

New §163(j) Interest ►The Proposed Regulations provide a broad definition of interest.

Items described as interest generally can be divided into 2 categories – amounts traditionally considered interest and then interest equivalents.

► Interest includes amounts paid, received or accrued for the use or forbearance of money and amounts treated as interest under other Code provisions, such as OID, qualified stated interest, acquisition discount, market discount, repurchase premium and amounts treated as interest under §§467 and 7872.

► Interest equivalents include guaranteed payments for the use of capital, loan commitment fees, substitute interest payments and debt issuance costs.

►The Proposed Regulations also include an “anti-avoidance rule” to the effect that amounts “predominantly incurred in consideration of the time value of money” that would otherwise be deductible are treated as interest. The rule likely would cover, for example, guarantee fees and forbearance fees.

21

New §163(j) – Interest anti-avoidance example

22

A B

A C

$1000

Gold

Gold (in 6 months)

$1013

Prop. Treas. Reg. § 1.163(j)-1(b)(20)(v) Example 3:

► A borrows gold (from a 3rd party) and sells it to B for $1000.

► A enters into a futures contract to purchase gold from C in 6 months for $1013.

► Under the proposed regulations, A’s loss of $13 is considered “predominantly associated with the time value of money” and is treated as an interest expense.

New §163(j) ATI ► Certain Adjustments to ATI ▸ The Proposed Regulations include as adjustments to taxable income the items set

forth in the statute. However, the Proposed Regulations include additional adjustments and certain clarifications.

▸ An adjustment is taken into account only once for purposes of determining ATI. ▸ For example, a deduction for the depreciation of nonbusiness property under §167 cannot be

taken into account as both a deduction for depreciation and an item of deduction that is not allocable to a trade or business.

▸ Only the adjustments to taxable income in the Proposed Regulations may be made. ▸ For example, a deduction under §243 for dividends received by a C corporation (that is not a RIC

or REIT) reduces the taxable income of the C corporation; the C corporation cannot add back the amount of the deduction in computing ATI.

▸ The §250 deduction is calculated without regard to adjustments required by the taxable income limitation under §250(a)(2), with the result that a taxpayer has 2 §250 calculations – 1 for §163(j) purposes and 1 for §250 purposes.

▸ An amount incurred as depreciation, amortization or depletion, but capitalized to inventory under §263A and included in cost of goods sold, is not a deduction for depreciation, amortization or depletion for purposes of §163(j).

▸ Special rules apply for purposes of computing ATI – ▸ For partnerships and CFCs ▸ Involving dispositions of depreciable property

23

New §163(j) Certain Operating Rules ►Ordering and operating rules govern the interaction between

§163(j) and other provisions of the Code affecting interest – ▸ Provisions that defer, capitalize or disallow interest expense (e.g.,

§§163(e)(5)(A)(i), (f), (l) or (m) or 264(a), 265, 267A, 279, 1277 or 1282) apply before §163(j).

▸ §§263A and 263(g) apply before §163(j). ▸ §246A applies before §163(j). ▸ §163(j) applies before §§461(l), 465 and 469.

►Character of a C corporation’s interest income and interest expense – ▸ A C corporation can only have business interest income and expense for

purposes of §163(j) (unless allocable to an excepted trade or business). ▸ A corporation’s items of income, gain, deduction or loss are properly

allocable to a trade or business for purposes of §163(j) and therefore taken into account in determining ATI (unless allocable to an excepted trade or business).

▸ Above treatment generally applies to items allocated from a partnership to a corporate partner, with a special rule for certain §951(a) and §951A(a) inclusions by a domestic partnership.

24

New §163(j) Additional Rules (cont’d) ►§381(c)(20) treats a disallowed business interest expense

carryforward as a §381 attribute, meaning an acquiring corporation succeeds to the disallowed business interest expense carryforwards of a target in a §381(a) transaction. The Proposed Regulations – ▸ Clarify that the carryover item includes disallowed business interest

expense from the tax year ending on the date of the transfer; and ▸ Limit the acquiring corporation’s ability to use the carryforward in its 1st

taxable year ending after the acquisition, consistent with treatment of NOL carryforwards under Treas. Reg. §§ 1.381(c)(1)-1 and -2.

►Disallowed business interest expense carryforwards are potentially subject to limitation under §382 and SRLY.

►A C corporation’s E&P is determined without regard to business interest expense disallowance (i.e., a C corporation generally reduces its E&P by disallowed business interest expense).

►The §163(j) limitation applies at the consolidated group level, with the consolidated group having a single limitation that is applied to a member’s business interest expense.

25

► P and S are members of the same consolidated group

► G (unrelated) lends P $100 at 10% interest

► Then, P lends S $100 at 12% interest

► Under the proposed regulations, the intercompany obligation between P and S is disregarded in determining the group’s ATI and P and S’s business interest expense and business interest income

► For purposes of §163(j), P has $10 of business interest expense

New §163(j) Consolidated Groups (Prop. Treas. Reg. § 1.163(j)-4(d)(5) Example 2)

26

G P

S

Loan

Loan

New §163(j) Depreciation ► The Proposed Regulations contain a number of provisions modifying ATI to account for

§163(j)(8)(A)’s requirement that ATI be computed without regard to any deduction allowable for depreciation. ▸ For taxable years beginning before January 1, 2022, any deduction for depreciation under

§167 or 168 is added to taxable income to determine ATI. Prop. Treas. Reg. § 1.163(j)-1(b)(1)(i)(D).

▸ With respect to the sale or other disposition of property, ATI is reduced by the lesser of (1) any gain recognized on the sale or other disposition of such property, and (2) any depreciation, amortization, or depletion deductions for the tax years beginning after December 31, 2017, and before January 1, 2022, with respect to such property. Prop. Treas. Reg. § 1.163(j)-1(b)(1)(ii)(C). This rule sometimes is referred to as the “Anti-Double Counting Subtraction” rule.

▸ Depreciation, amortization, and depletion capitalized to inventory under section 263A are not treated as deductions, and are not adjustments, in computing ATI. In some industries, most depreciation is converted to cost of goods sold, and the Proposed Regulations prohibit any benefit for depreciation—even pre-2022.

▸ With respect to the sale or other disposition of stock of a member of a consolidated group that includes the selling member, ATI is reduced by the investment adjustments with respect to such stock that are attributable to deductions taken for depreciation. Prop. Treas. Reg. § 1.163(j)-1(b)(1)(ii)(D).

27

New §163(j) Depreciation (cont’d)

Facts 1. On Date 1, X transfers $100 to Y in

exchange for Asset A, a depreciable asset. 2. Between Date 1 and Date 2, X depreciates

Asset A’s adjusted basis to $0. 3. On Date 2, X transfers Asset A to Z in

exchange for $40.

U.S. Federal Income Tax Considerations For taxable years beginning before January 1, 2022, as Asset A is depreciated, the depreciation reduces X’s taxable income but does not impact X’s ATI for purposes of §163(j). On the disposition of Asset A, the Proposed Regulations would reduce ATI for the $40 of gain recognized on the sale of Asset A.

X

Date 1:

A

Y $100

Asset A

A Asset A FMV: $100 AB: $100

X

Date 2:

A

Z $40

Asset A

A Asset A FMV: $40 AB: $0

Example 1

28

New §163(j) §382 Aspects ► §382(d)(3) treats a disallowed business interest expense carryforward as a “pre-change

loss” subject to §382.

► The Proposed Regulations clarify the term “§382 disallowed business interest carryforward” of a loss corporation consists of – ▸ The loss corporation’s disallowed business interest expense carryforwards, including

disallowed disqualified interest, as of the ownership change, and ▸ The carryforward of the loss corporation’s disallowed business interest expense paid or

accrued in the pre-change period is determined by using a daily proration method, regardless of whether the loss corporation has made a closing-of-the-books election under Treas. Reg. § 1.382-6(b)(2).

▸ Treas. Reg. § 1.382-6(d) provides that, if Treas. Reg. § 1.1502-76 applies (relating to the tax year of members of a consolidated group), an allocation of items is determined after applying Treas. Reg. § 1.1502-76.

▸ Thus, if a short year under Treas. Reg. § 1.1502-76 is a change year for which an allocation under this section is to be made, the allocation under this section applies only to the items allocated to that short taxable year under Treas. Reg. § 1.1502-76.

▸ Regulations modified to require pre-change losses for disallowed business interest expense to be absorbed before NOLs, and losses subject to a §382 limitation are absorbed before non-limited losses of the same type from the same tax year.

29

Example – Allocation of Business Interest Expense for Purposes of §382 (Prop. Treas. Reg. § 1.382-6(b)(4)(ii), Ex.)

Facts

• In 2019, X was a calendar year corporation that was not a member of a consolidated group.

• On May 26, 2019, X was acquired by Z (an unrelated third party), in a transaction that qualified as an ownership change under §382(g).

‒ In 2019, X had $100 of business interest expense and an $81 §163(j) limitation.

Bank X 1.1.2019

Z

X

5.26.2019

Bank 2019 interest = $100

X's 163(j) Limitation = $81

Creditor Debtor

New §163(j) §382 Aspects (cont’d)

30

Bank X 1.1.2019

Z

X

5.26.2019

Bank 2019 interest = $100

X's 163(j) Limitation = $81

US Federal Income Tax Considerations

• X's business interest expense deduction is ratably allocated between the pre-change and post-change periods.

‒ X may deduct $81 of its business interest expense of which $32.4 ($81 x (146 days/365 days) = $32.4) is allocable to the pre-change period.

‒ The remaining $19 of interest is disallowed business interest expense, of which $7.6 ($19 x (146 days/365 days) = $7.6) is allocable to the pre-change period.

‒ The $7.6 of disallowed business interest expense is treated as a §382 disallowed business interest carryforward, and thus is a pre-change loss within the meaning of Treas. Reg. § 1.382-2(a)(2).

• What if X joined Z's consolidated group for the remainder of 2019?

‒ This allocation applies only to the items allocated to the short taxable year under Treas. Reg. § 1.1502-76.

Example (cont’d)

Creditor Debtor

New §163(j) §382 Aspects (cont’d)

31

New §163(j) Allocation of Interest ►Prop. Treas. Reg. § 1.163(j)-10 sets forth rules for determining the

amount of interest expense, interest income, and other tax items of a taxpayer that is properly allocable to excepted and non-excepted trades or businesses for purposes of §163(j).

►A taxpayer’s interest expense and interest income is generally allocated to a taxpayer’s excepted and non-excepted trades or businesses under the Proposed Regulations based on the relative amounts of the taxpayer’s adjusted basis in the assets.

►A shareholder must look through to the assets of a non-consolidated domestic C corporation for purposes of allocating the shareholder's basis in its stock in the corporation between excepted and non-excepted trades or businesses if the shareholder's direct and indirect interest in the corporation satisfies the ownership requirements of §1504(a)(2).

►For purposes of Prop. Treas. Reg. § 1.163(j)-10, a consolidated group is treated as a single corporation. Consequently, the consolidated group, as opposed to a single member, is treated as engaged in excepted or non-excepted trades or businesses.

32

New §163(j) Allocation of Interest (cont’d)

Facts

P is a pure holding company that wholly owns both X and Y, but does not file a consolidated return with X or Y.

Assets A and C are used in excepted businesses by X and Y, respectively. Assets B and D are used in non-excepted businesses, by X and Y, respectively.

P has $100 of interest expense in Year 1.

U.S. Federal Income Tax Considerations

25% ($25 basis in Asset A/$100 total asset basis) of the X stock owned by P is allocated to excepted businesses and 100% ($100 basis in Asset C/$100 total asset basis) of the Y stock owned by P is allocated to excepted businesses. The remaining 75% ($75 basis in Asset B/$100 total asset basis) of P’s X stock is allocated to non-excepted businesses.

62.5% ($125 excepted stock basis/$200 total stock basis) of P’s interest expense is therefore allocated to excepted businesses and 37.5% ($75 non-excepted stock basis/$200 total stock basis) of P’s interest expense is allocated to non-excepted businesses.

The result here is the same as it would be in consolidation, but it would be different if the stock basis in X or Y did not conform to inside asset basis or if there were liabilities at X or Y, such that one had higher stock basis than the other, even if there were conformity.

X

A Asset A FMV: $75 AB: $25

P

Y

C Asset B FMV: $25 AB: $75

X Stock FMV: $100 AB: $100

Y Stock FMV: $100 AB: $100

B D Asset C FMV: $20 AB: $100

Asset D FMV: $80 AB: $0

Example

33

►Tax attributes can be a critical consideration in the valuation and structuring of M&A transactions

►They also can be valuable assets of an ongoing corporate enterprise

►Discussion topics: ▸Effect of TCJA changes on M&A valuation ▸Purchase price allocations in basis step-up

transactions ▸Alternatives to debt financing ▸Implicit expansion of section 382

Post-TCJA M&A & Planning Considerations

34

► TCJA’s reduction in tax rates: ▸ directly impacted the value of tax attributes that reduce taxable

income, such as NOLs (i.e., each dollar of NOL is now worth, at most, 21 cents and not 35 cents); and

▸ may have also indirectly impacted the value of tax attributes that reduce tax liability, such as credit carryovers (i.e., the time value of a tax credit carryover is reduced if there is less annual tax liability that the credit can offset)

► TCJA’s limits on NOL utilization and interest deductibility can negatively impact valuation of a target company where: ▸ the post-acquisition after-tax cash flows will be reduced due to the

inability to fully utilize NOLs and/or interest expense to offset taxable income; or

▸ the seller is seeking value for transaction tax deductions the net loss from which can no longer be carried back for a refund of a prior year tax liability

Effect of TCJA Changes on M&A Valuation

35

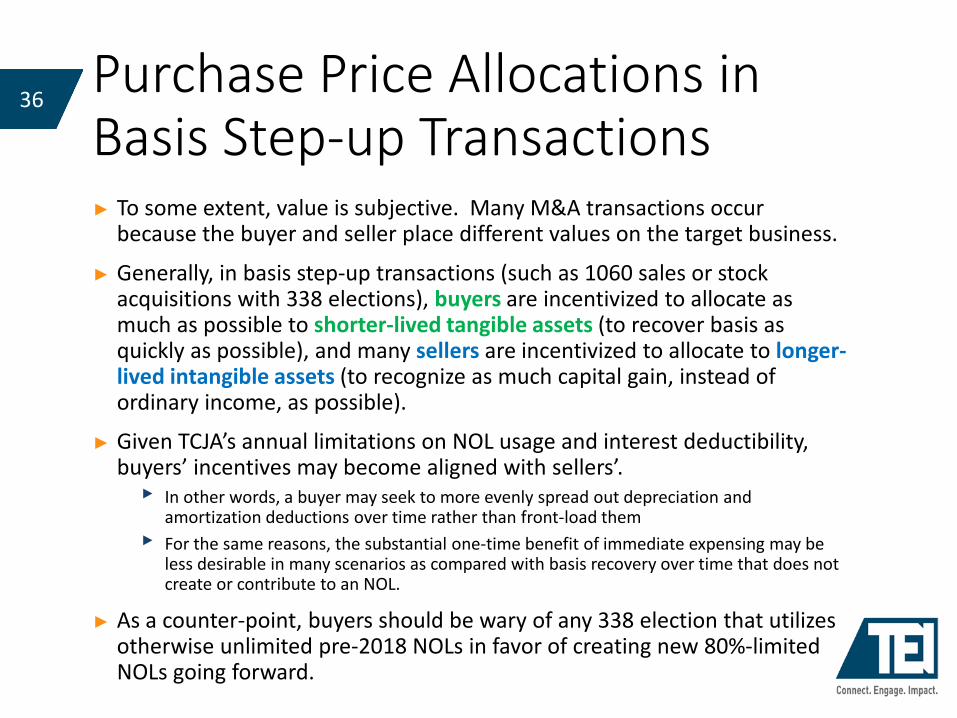

► To some extent, value is subjective. Many M&A transactions occur because the buyer and seller place different values on the target business.

► Generally, in basis step-up transactions (such as 1060 sales or stock acquisitions with 338 elections), buyers are incentivized to allocate as much as possible to shorter-lived tangible assets (to recover basis as quickly as possible), and many sellers are incentivized to allocate to longer-lived intangible assets (to recognize as much capital gain, instead of ordinary income, as possible).

► Given TCJA’s annual limitations on NOL usage and interest deductibility, buyers’ incentives may become aligned with sellers’. ▸ In other words, a buyer may seek to more evenly spread out depreciation and

amortization deductions over time rather than front-load them ▸ For the same reasons, the substantial one-time benefit of immediate expensing may be

less desirable in many scenarios as compared with basis recovery over time that does not create or contribute to an NOL.

► As a counter-point, buyers should be wary of any 338 election that utilizes otherwise unlimited pre-2018 NOLs in favor of creating new 80%-limited NOLs going forward.

Purchase Price Allocations in Basis Step-up Transactions

36

►The 163(j) limitation on interest deductibility could create an incentive in high leverage situations to seek out alternative financing transactions

►Although the proposed regulations set forth an expansive definition of “interest” for these purposes, other economic arrangements might be possible in certain scenarios ▸ For example, 163(j) does not generally apply to rental

payments or accruals ▸ Also, 163(j) does not generally apply to preferred returns on

partnership equity

Alternatives to Debt Financing? 37

► In TY2019, Corporation (T) borrows $10,000 at 8.0% interest ▸ T has business earnings of $1,000 and interest expense of $800, resulting in pre-tax

cash of $200. ▸ T’s § 163(j) limit is $300. ▸ T’s taxable income is $1,000 - $300 = $700. ▸ T’s TY2019 federal tax liability is $700 x 21% = $147. ▸ T’s after-tax cash flow is $200 - $147= $53.

► If, instead of issuing debt, T had offered $10,000 of preferred interests in a partnership that held T's business, with a preferred return equal to 9.0% of net profits: ▸ T’s share of the pre-tax cash flow is $100. ▸ T’s allocable taxable income also is $100.

▸ The preferred holder is allocated $900 of the partnership’s income under the terms of the partnership agreement.

▸ T’s TY2019 federal tax liability is $100 x 21% = $21. ▸ T’s after-tax cash flow is $100 - $21 = $79.

► Considerations: debt/equity; guaranteed payment rules; 163(j) anti-avoidance rule; ECI implications

Alternatives to Debt Financing? - Example

38

► The loss and expense limitations imposed by the TCJA may put an increased focus on section 382 protections

► There are likely to be more “loss corporations” now ▸ The limitations imposed by new sections 163(j) and 172 may cause more NOLs to be

carried forward and cause many corporations to have disallowed business interest expense carryforwards

► For any loss corporation that undergoes an ownership change, a greater amount of attributes may be subjected to a section 382 limitation that is determined under the essentially unchanged (pre-TCJA) rules for calculating the limitation ▸ Moreover, the section 382 limitation runs concurrently with other loss limitations

► It has been fairly common for a corporation with valuable NOLs to adopt measures to protect those assets ▸ For example, several public corporations have adopted poison pills to deter accretions of

stock ownership that may implicate a section 382 ownership change or charter restrictions that cause stock transfers to be null and void under law if they would otherwise contribute to a section 382 ownership shift

▸ See Selectica; PLR 200837027

► Query whether protections against section 382 ownership changes will become even more common given the potentially expanded ambit of section 382

Implicit Expansion of Section 382

39