imf country report no. 15/190 lebanon country report no. 15/190 lebanon ... foreign-exchange and...

TRANSCRIPT

© 2015 International Monetary Fund

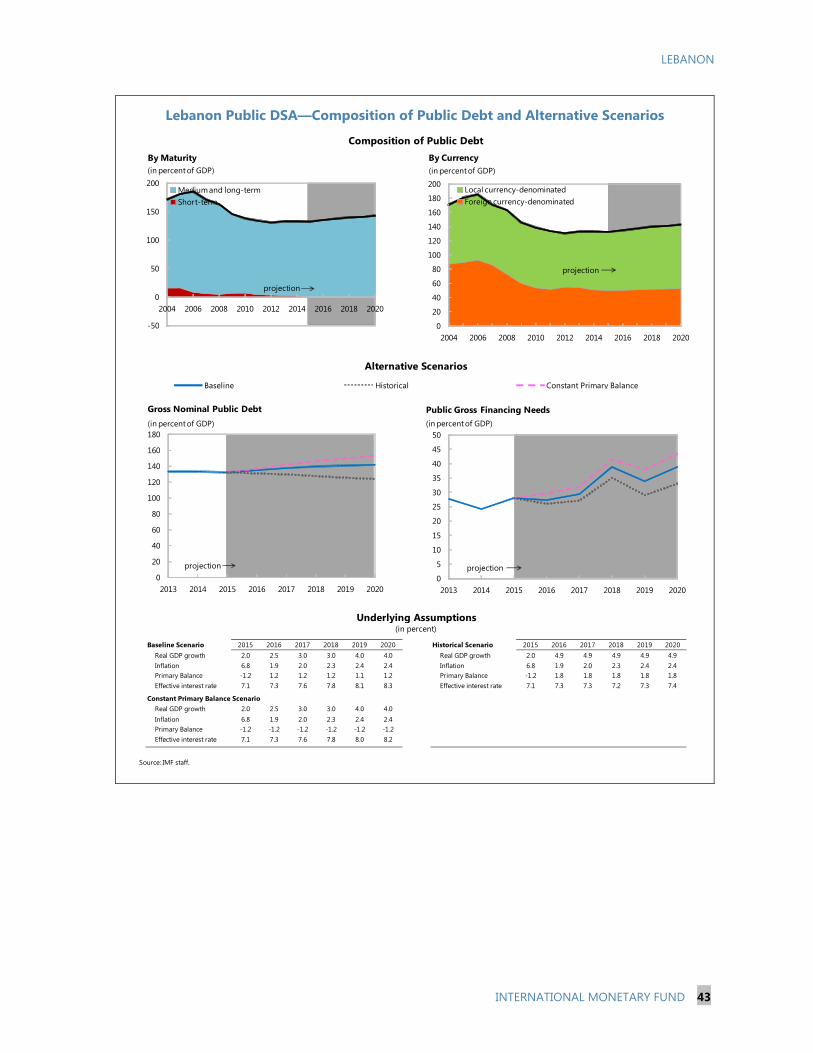

IMF Country Report No. 15/190

LEBANON 2015 ARTICLE IV CONSULTATION—PRESS RELEASE; STAFF REPORT; AND STATEMENT BY THE EXECUTIVE DIRECTOR FOR LEBANON

Under Article IV of the IMF’s Articles of Agreement, the IMF holds bilateral discussions with members, usually every year. In the context of the 2015 Article IV consultation with Lebanon, the following documents have been released and are included in this package: A Press Release summarizing the views of the Executive Board as expressed during its

June 26, 2015 consideration of the staff report that concluded the Article IV consultation with Lebanon.

The Staff Report prepared by a staff team of the IMF for the Executive Board’s consideration on June 26, 2015, following discussions that ended on May 12, 2015, with the officials of Lebanon on economic developments and policies. Based on information available at the time of these discussions, the staff report was completed on June 11, 2015.

An Informational Annex prepared by the IMF staff.

A Statement by the Executive Director for Lebanon.

The IMF’s transparency policy allows for the deletion of market-sensitive information and premature disclosure of the authorities’ policy intentions in published staff reports and other documents.

Copies of this report are available to the public from

International Monetary Fund Publication Services PO Box 92780 Washington, D.C. 20090

Telephone: (202) 623-7430 Fax: (202) 623-7201 E-mail: [email protected] Web: http://www.imf.org

Price: $18.00 per printed copy

International Monetary Fund Washington, D.C.

July 2015

Press Release No. 15/309 FOR IMMEDIATE RELEASE June 30, 2015

IMF Executive Board Concludes 2015 Article IV Consultation with Lebanon

On June 26, 2015, the Executive Board of the International Monetary Fund (IMF) concluded the Article IV consultation1 with Lebanon.

The conflict in Syria, now in its fifth year, dominates Lebanon’s outlook, with refugees now comprising over one-quarter of the population. The refugee crisis is straining local communities, adding to poverty and unemployment, and placing further pressure on the economy’s already-weak public finances and infrastructure. Moreover, Lebanon faces a difficult domestic political situation. The presidency has been vacant since May 2014 and a lack of consensus between the major parties is hindering passage of key legislation.

In the face of this uncertainty, growth remains subdued. Following a sharp drop in 2011, growth has crawled upward to about 2–3 percent but remains well short of potential. IMF staff estimate that GDP increased by only 2 percent in 2014 and project a similarly modest growth rate in 2015. Lebanon’s traditional growth drivers—tourism, real estate, and construction—have received a significant blow and a strong rebound is unlikely soon. Lebanon’s return to potential growth (4 percent) before 2019 is now doubtful. Inflation also declined sharply in 2014 on the back of lower oil prices and other one-off factors, but should return to about 3 percent by end-2015.

On the fiscal side, exceptional factors allowed for a primary surplus in 2014, but without decisive action fiscal deterioration will continue in 2015. The 2014 primary surplus of about 2.5 percent of GDP largely resulted from exceptional telecom transfers and, to some extent, from withheld and delayed payments. But the primary balance is expected to return to a deficit of almost 1.25 percent of GDP in 2015, with public debt remaining high at 132 percent of GDP. Foreign-exchange and financial markets continue to be resilient, despite Lebanon’s sizable external financial requirements. Inflows remain large, particularly from non-resident deposits; and in the context of Lebanon’s currency peg to the U.S. dollar, the Banque du Liban (BdL) has maintained an adequate level of gross foreign exchange reserves.

1 Under Article IV of the IMF's Articles of Agreement, the IMF holds bilateral discussions with members, usually every year. A staff team visits the country, collects economic and financial information, and discusses with officials the country's economic developments and policies. On return to headquarters, the staff prepares a report, which forms the basis for discussion by the Executive Board.

International Monetary Fund 700 19th Street, NW Washington, D. C. 20431 USA

2

Executive Board Assessment2

Executive Directors commended the authorities for preserving macroeconomic stability and market confidence despite the unprecedented humanitarian and economic spillovers from the conflict in Syria, including a daunting inflow of refugees which has taken a toll on public finances, infrastructures, and the social fabric. Against this background, they called on the international community to provide greater humanitarian and development assistance to Lebanon. While acknowledging that a very difficult economic and political context limits feasible policy choices, Directors encouraged the authorities to further strengthen confidence and secure more inclusive growth by implementing priority fiscal and structural reforms promptly.

Directors stressed that a sustained fiscal adjustment is essential. They welcomed the primary surplus in 2014, but noted that it mostly reflected one-off factors. They cautioned that, without further adjustment, the public debt ratio will continue to rise and add to existing vulnerabilities, crowding out essential public investment and social spending. As a first step, Directors encouraged the authorities to pass an appropriately ambitious budget for 2015. They also stressed the urgent need to reform the electricity sector to remove a large drain on the public finances.

More broadly, Directors underscored the need to place public indebtedness on a sustainable downward path. In this context, they advised caution in implementing a salary-scale adjustment for public-sector employees. They pointed to significant scope to increase revenue equitably, including by improving compliance and broadening the tax base, starting with fuel taxation. Further, Directors observed that changing the spending mix toward capital and social spending would help mitigate the procyclical impact of fiscal adjustment. They also considered that strengthening the safety nets and reforming the pension system could improve equity and fiscal sustainability.

Directors commended the central bank for supporting macroeconomic stability and maintaining adequate international reserves. They agreed that monetary policy should remain geared to supporting the U.S. dollar peg, which has served Lebanon well. Looking ahead, they underscored that fiscal adjustment would help reduce the financial and institutional burden on the central bank related to quasi-fiscal activities.

Directors noted the critical role played by Lebanon’s banking system in securing sustained, broad-based economic growth. They commended the authorities’ close oversight of the financial system, and stressed the need for continued vigilance and efforts to strengthen the regulatory framework. They highlighted the importance of increasing capital buffers, improving loan classification and restructuring rules, and further enhancing the framework to counter money

2 At the conclusion of the discussion, the Managing Director, as Chairman of the Board, summarizes the views of Executive Directors, and this summary is transmitted to the country's authorities. An explanation of any qualifiers used in summings up can be found here: http://www.imf.org/external/np/sec/misc/qualifiers.htm.

3

laundering and terrorism financing. Directors welcomed the authorities’ recent request for an update assessment under the Financial Sector Assessment Program.

Directors underscored the need to advance structural reforms to promote job creation and improve competitiveness. In addition to electricity reform, which is a critical priority, Directors highlighted the need for labor reforms, improvements in public service provision, and legislation to reinvigorate private investment, including in the oil and gas sector. Directors also encouraged the authorities to improve Lebanon’s statistical system, building on ongoing progress.

LEBANON STAFF REPORT FOR THE 2015 ARTICLE IV CONSULTATION

KEY ISSUES

Context. The Syrian crisis and the associated inflow of refugees continue to dominate Lebanon’s short-term outlook, compounding long-standing policy weaknesses and vulnerabilities. Political paralysis has set in, with virtually no progress on the structural front. Growth has remained modest and insufficient to make a dent in rising poverty and unemployment. A welcome improvement in the primary fiscal position in 2014 was largely due to temporary factors, and will not be sustained absent adjustment efforts—implying that, without additional effort, Lebanon’s already-sizable public debt burden will only worsen. Financial conditions have nonetheless remained stable, as deposit inflows continue to fund the economy and sizeable buffers support the credibility of the exchange rate peg.

Policy priorities. Policies should aim at restoring fiscal sustainability and securing inclusive growth, to help engineer a soft-landing to a stronger economy. While Lebanon’s macrofinancial structure has, historically, held up well in the face of past turmoil, certain features remain a source of considerable vulnerabilities. Continued oversight of the financial system will be instrumental in containing them.

Key recommendations. While difficult political conditions make major reforms difficult, action could be taken now in two important areas: (i) passing a budget for 2015—the first in a decade, as a signal that the fiscal situation is under control; and (ii) starting well-known reforms in the electricity sector, which remains a major impediment to improved productivity, competitiveness, growth, and equity.

Over the short term, the authorities should look beyond the temporary impact of lower oil prices and deliver a credible policy mix with sustained adjustment and a falling public debt ratio. Revenue measures should be broad-based, starting from increases in fuel taxation; while spending composition should move away from transfers to the electricity company toward capital projects and social programs. Fiscal adjustment would also reduce the financial and institutional burden on the Banque du Liban and ultimately promote interest rate flexibility.

Over the medium term, social stability requires job-rich and sustainable growth. Continued efforts to ensure a sound financial system will support this objective, along with structural reforms to improve competitiveness and equity, starting from Lebanon’s pension schemes.

June 11, 2015

LEBANON

2 INTERNATIONAL MONETARY FUND

Approved By Adnan Mazarei (MCD) and Ranil Salgado (SPR)

Discussions took place in Beirut during April 28–May 12, 2015. The staff team comprised Mses. Fedelino (head) and Nakhle (local economist), Messrs. Alshahrani and Tiffin (advance team’s head, all MCD), Mr. Jarmuzek (FAD), Mr. Lambert (MCM), and Mr. Takizawa (SPR). Mr. Mazarei (MCD) and Ms. Choueiri (OED) joined some of the policy discussions. The team met Prime Minister Salam, Parliament Speaker Berri, Minister of Finance Khalil, Governor of the Banque du Liban Salamé, members of parliament, and representatives of the private sector, civil society, and the international community. The team shared with the authorities its work on a range of analytical and policy issues. Ms. Panaligan and Ms. Pineda contributed to the preparation of this report.

CONTENTS

CONTEXT: POLICY INERTIA _______________________________________________________________________ 4

AMID MOUNTING RISKS ________________________________________________________________________ 10

POLICY DISCUSSIONS ___________________________________________________________________________ 14

A. A More Balanced Policy Mix ___________________________________________________________________ 14

B. Aiming Higher: Stronger and More Inclusive Growth __________________________________________ 20

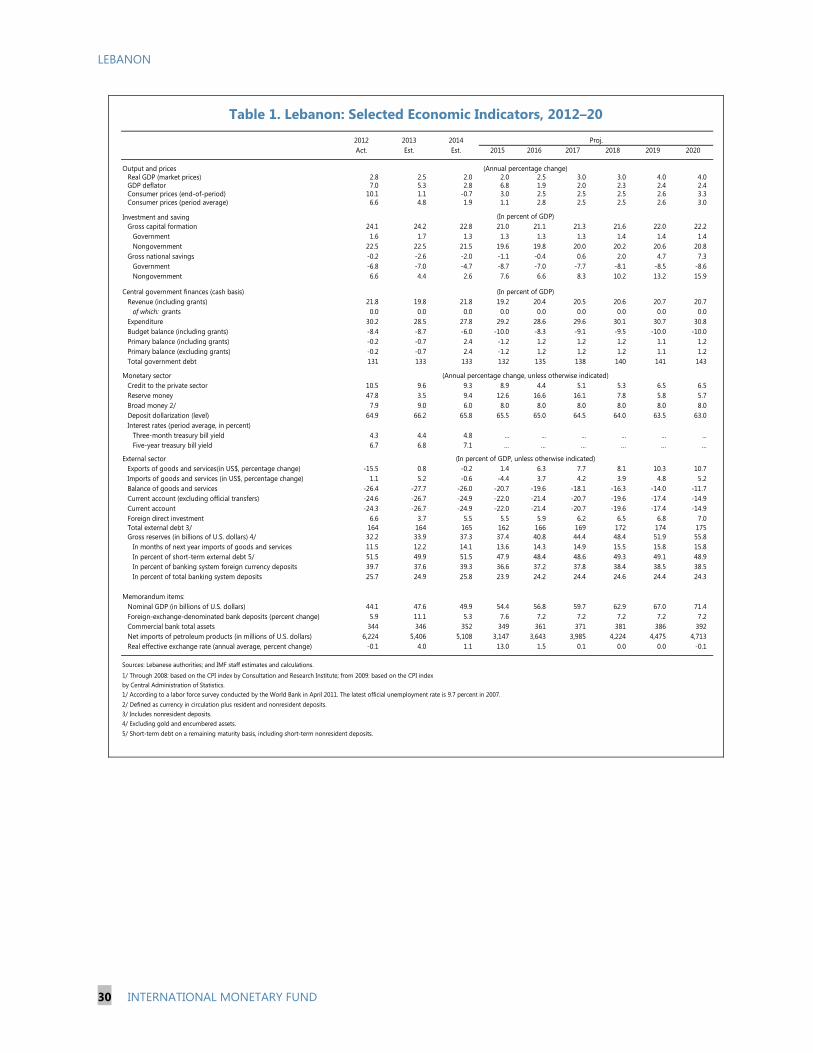

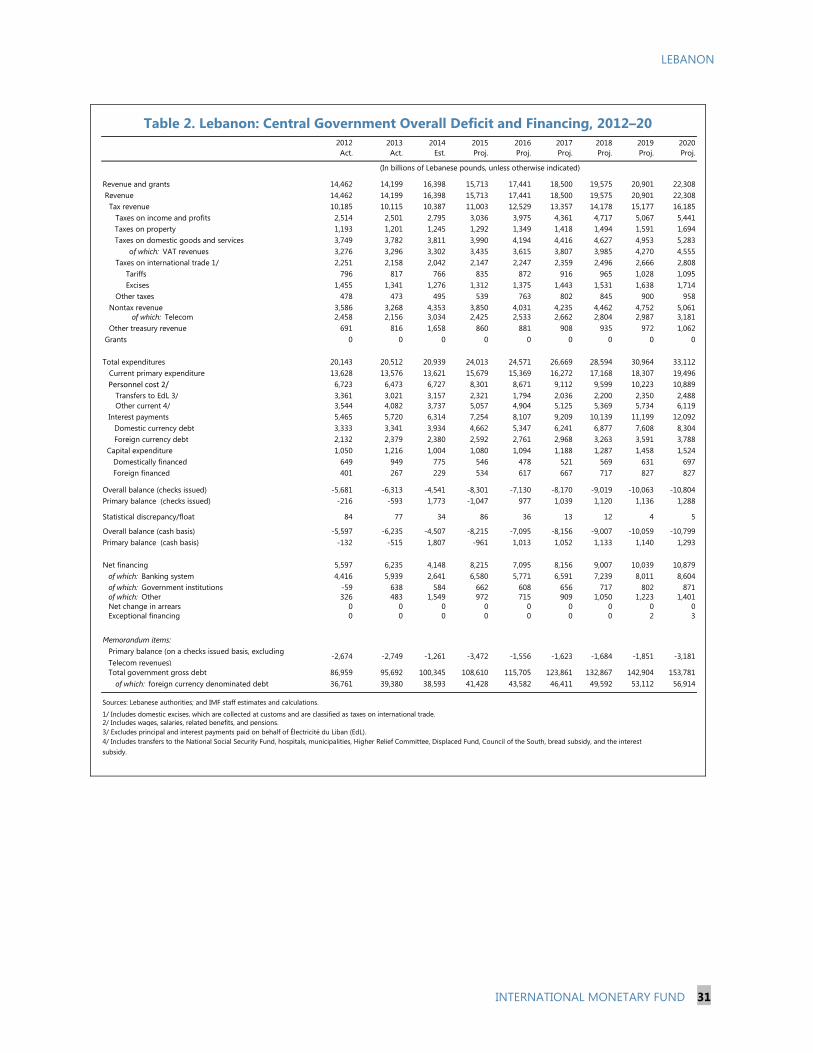

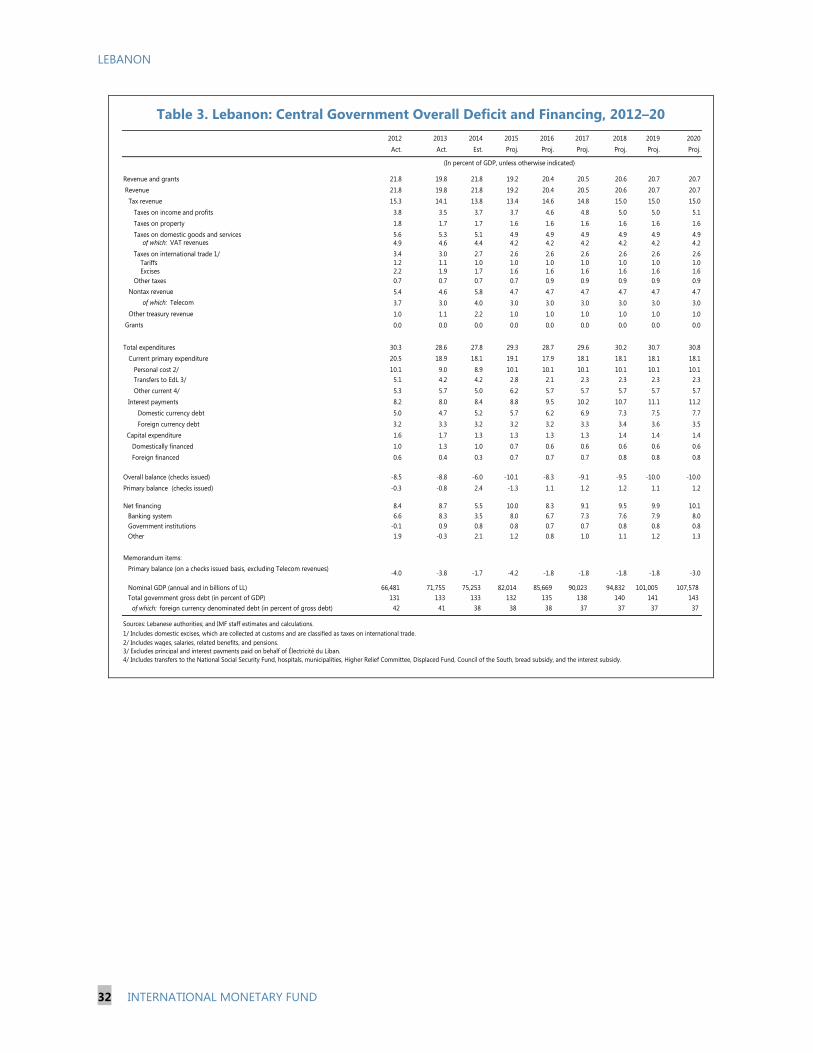

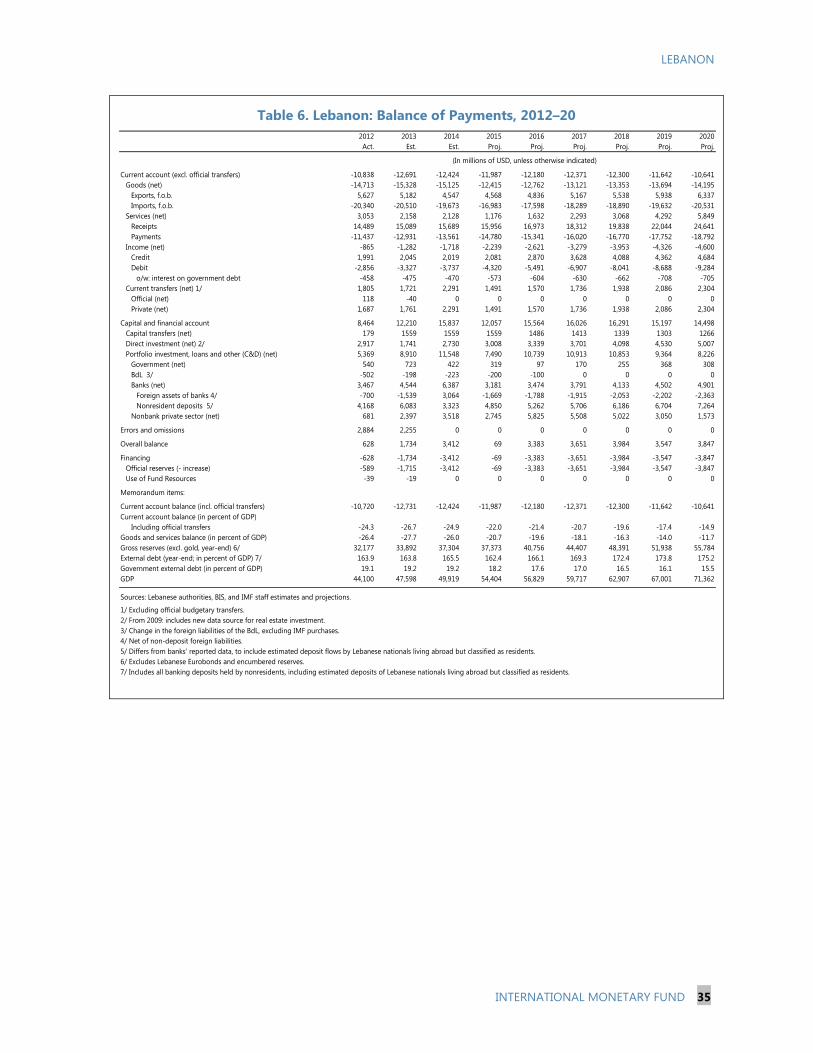

STAFF APPRAISAL _______________________________________________________________________________ 28 BOXES 1. The Prolonged Impact of the Syrian Refugee Crisis ______________________________________________ 6 2. Can Nominal GDP Increase with Falling Prices and Stagnant Growth? ___________________________ 8 3. Policies Since the 2014 Article IV Consultation __________________________________________________ 9 4. Why Increasing Fuel Taxation Makes Sense ____________________________________________________ 16 5. A Financial Conditions Index for Lebanon _____________________________________________________ 21 6. Data Issues in Lebanon—Capacity Constraints ________________________________________________ 27 TABLES 1. Selected Economic Indicators, 2012–20 ________________________________________________________ 30 2. Central Government Overall Deficit and Financing, 2012–20 (In billions of Lebanese pounds) ___ 31 3. Central Government Overall Deficit and Financing, 2012–20 (In percent of GDP) _______________ 32 4. Lebanon Government Debt, 2012–20 __________________________________________________________ 33 5. Monetary Survey, 2012–20 _____________________________________________________________________ 34 6. Balance of Payments, 2012–20 _________________________________________________________________ 35 7. Financial Soundness Indicators for the Banking Sector, 2010–14 ______________________________ 36

LEBANON

INTERNATIONAL MONETARY FUND 3

ANNEXES I. Public Debt Sustainability Analysis ________________________________________________________________37 II. External Sector Assessment _______________________________________________________________________45 III. External Debt Sustainability Analysis ______________________________________________________________48

LEBANON

4 INTERNATIONAL MONETARY FUND

CONTEXT: POLICY INERTIA… 1. Lebanon has a reputation of living close to the edge. In the past, it has weathered significant shocks, sustained macroeconomic imbalances even wider than those currently experienced, with political dynamics often preventing a more strategic approach to addressing underlying vulnerabilities.

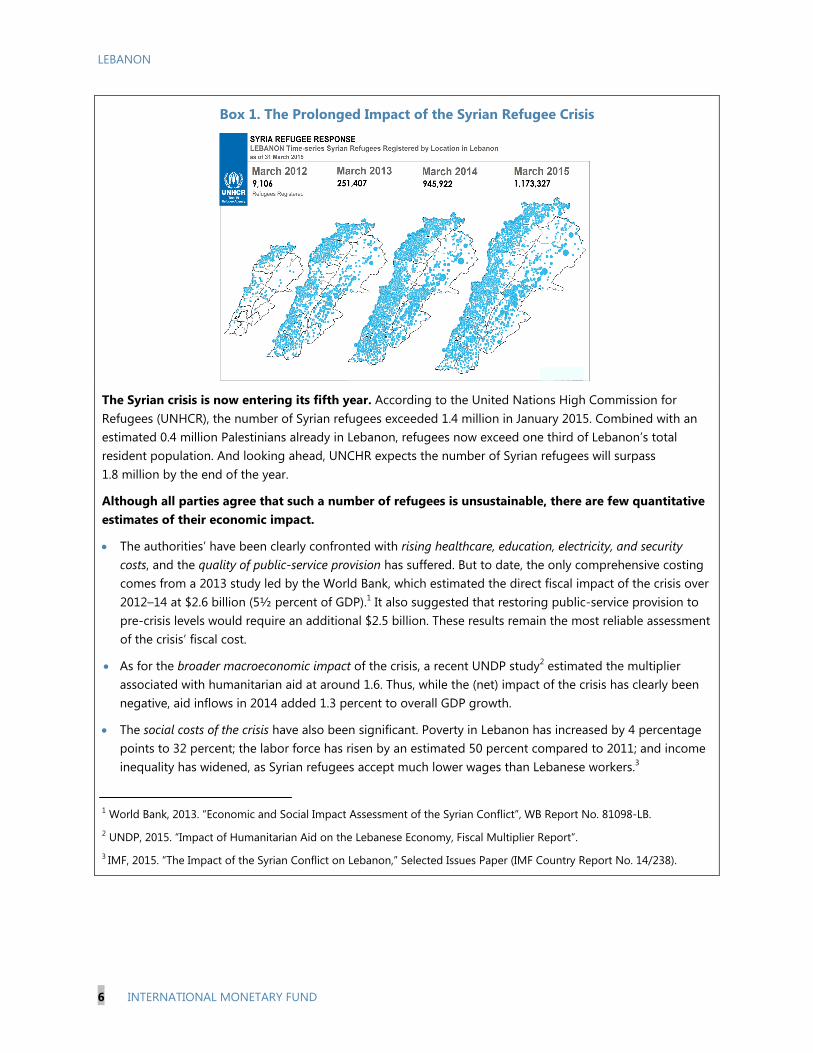

2. But this time may be different. The Syria crisis—now in its fifth year—represents one of the worst humanitarian crises since the Second World War, and is the key determinant of Lebanon’s short-term outlook and longer-term prospects (Box 1). The number of refugees has steadied, partly as a result of tighter border restrictions. But they nonetheless comprise over one-quarter of the population, straining local communities, adding to poverty and unemployment, and placing further pressure on Lebanon’s already-weak public finances and infrastructure. The authorities have stepped forward and should be commended for hosting the refugees, but they cannot shoulder this overwhelming burden alone. International support has helped, but remains insufficient given the sheer scale of Lebanon’s humanitarian and development needs.

3. The country is in the grip of a protracted political crisis. The presidency has been vacant since May 2014, and parliament lacks sufficient consensus to convene to discuss key legislation. Without a president, cabinet can still enact legislation, but only if agreed unanimously by all 24 ministers—which is very difficult given the current political fissures. Parliament’s term was recently extended (for a second time) to June 2017, adding to concerns as to its legitimacy. In this environment, a few targeted policy actions would send a strong signal about the country’s will and determination to move forward despite the many challenges ahead.

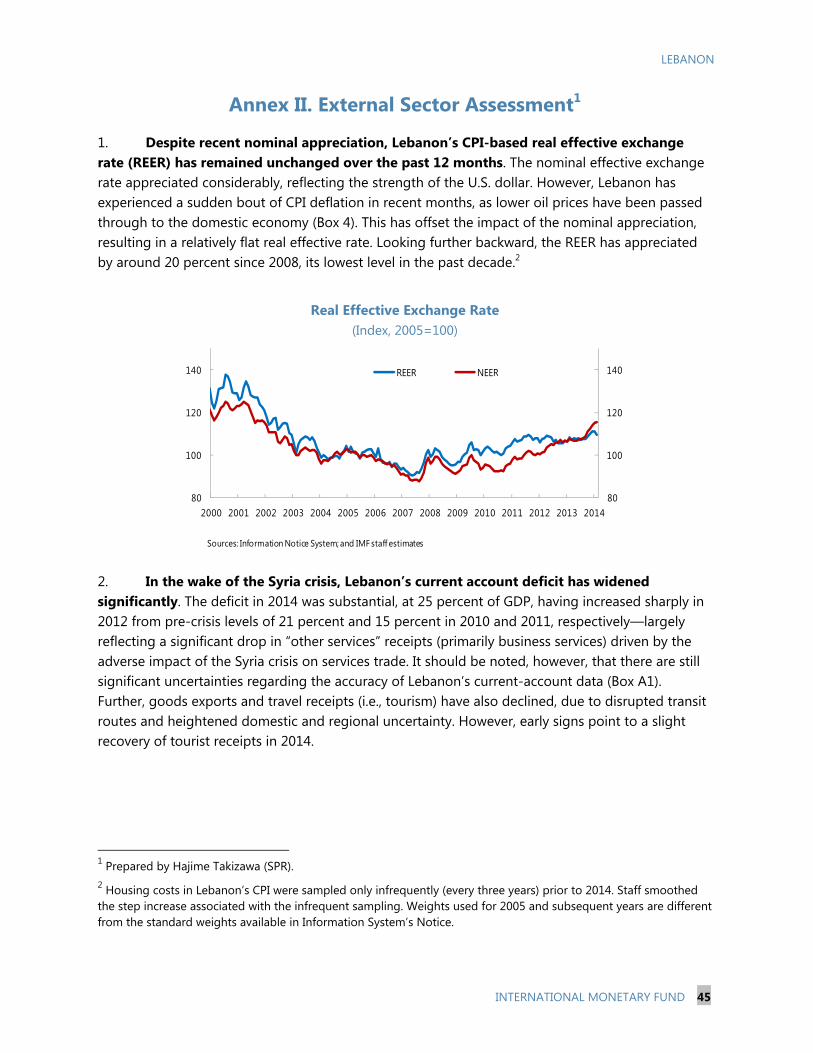

4. Growth has decelerated significantly. Following a crash from 8 percent in 2010 to less than 1 percent in 2011, growth has inched upward to around 2–3 percent, but remains well short of its potential. Inflation also declined sharply in 2014, owing to lower oil prices and a number of additional one-off developments, but is expected to return to a trend rate of about 3 percent in 2015. In this regard, lower CPI inflation has essentially offset the recent appreciation of the Lebanese pound (pegged to the U.S. dollar), leaving Lebanon’s real effective exchange rate broadly unchanged.

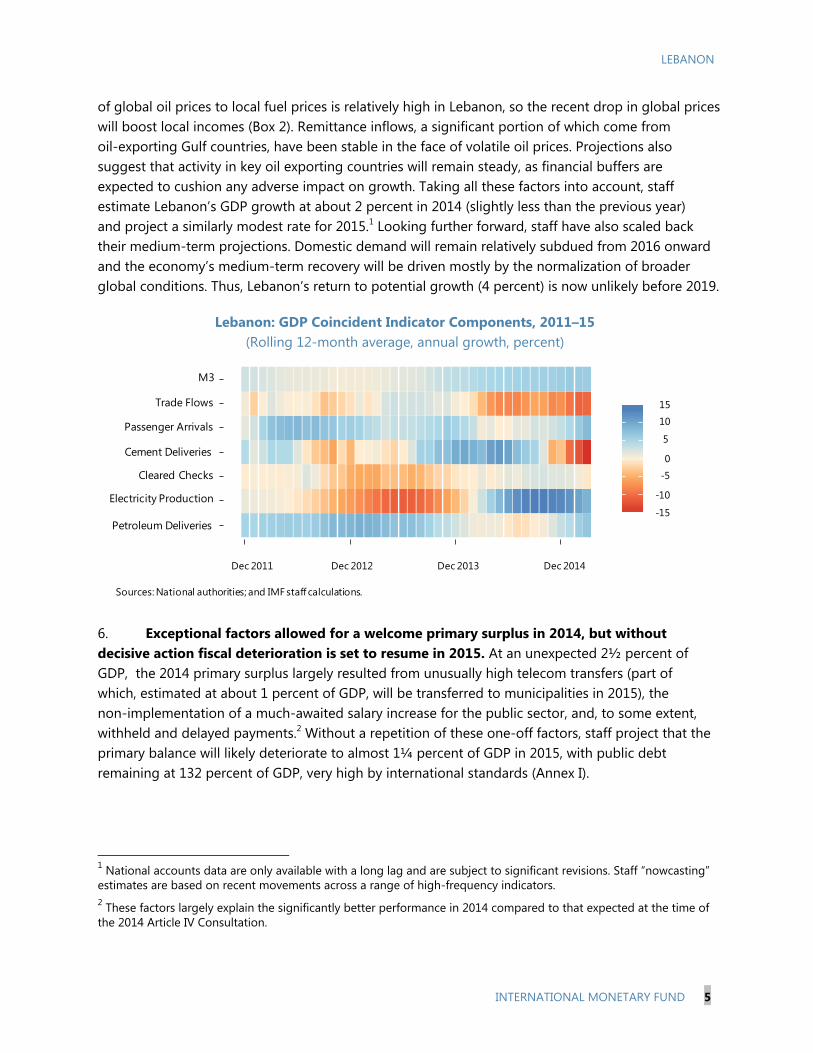

5. Rising uncertainty is taking a toll on the economy, but incomes and consumption are receiving a temporary boost from lower oil prices. Lebanon’s traditional growth sectors—tourism, real estate, and construction—have all taken a significant blow, and a strong rebound is unlikely in the immediate future. Indeed, early indications for 2015 point to a marked softening of the construction sector, particularly for high-end residential projects. However, the pass-through

0

5

10

15

0

5

10

15

2009 2012

GDP Indicators(Percent growth, annual)

BdL Indicator (12m ma)

IMF Staff Indicator

Official GDP

IMF Estimate

Sources: National authorities, and IMF staff calculations.

LEBANON

INTERNATIONAL MONETARY FUND 5

5

15

10

0

-5

-10

-15

Dec 2011 Dec 2012 Dec 2013 Dec 2014

M3

Trade Flows

Passenger Arrivals

Cement Deliveries

Cleared Checks

Electricity Production

Petroleum Deliveries

Sources: National authorities; and IMF staff calculations.

of global oil prices to local fuel prices is relatively high in Lebanon, so the recent drop in global prices will boost local incomes (Box 2). Remittance inflows, a significant portion of which come from oil-exporting Gulf countries, have been stable in the face of volatile oil prices. Projections also suggest that activity in key oil exporting countries will remain steady, as financial buffers are expected to cushion any adverse impact on growth. Taking all these factors into account, staff estimate Lebanon’s GDP growth at about 2 percent in 2014 (slightly less than the previous year) and project a similarly modest rate for 2015.1 Looking further forward, staff have also scaled back their medium-term projections. Domestic demand will remain relatively subdued from 2016 onward and the economy’s medium-term recovery will be driven mostly by the normalization of broader global conditions. Thus, Lebanon’s return to potential growth (4 percent) is now unlikely before 2019.

Lebanon: GDP Coincident Indicator Components, 2011–15 (Rolling 12-month average, annual growth, percent)

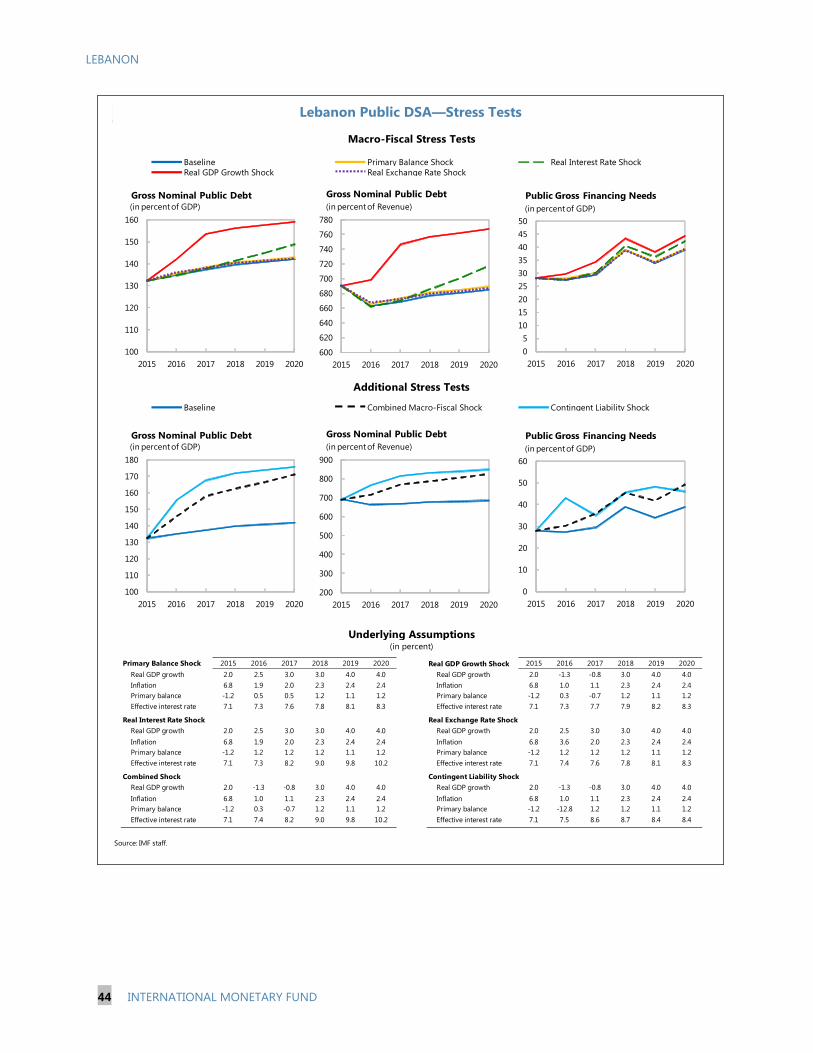

6. Exceptional factors allowed for a welcome primary surplus in 2014, but without decisive action fiscal deterioration is set to resume in 2015. At an unexpected 2½ percent of GDP, the 2014 primary surplus largely resulted from unusually high telecom transfers (part of which, estimated at about 1 percent of GDP, will be transferred to municipalities in 2015), the non-implementation of a much-awaited salary increase for the public sector, and, to some extent, withheld and delayed payments.2 Without a repetition of these one-off factors, staff project that the primary balance will likely deteriorate to almost 1¼ percent of GDP in 2015, with public debt remaining at 132 percent of GDP, very high by international standards (Annex I).

1 National accounts data are only available with a long lag and are subject to significant revisions. Staff “nowcasting” estimates are based on recent movements across a range of high-frequency indicators. 2 These factors largely explain the significantly better performance in 2014 compared to that expected at the time of the 2014 Article IV Consultation.

LEBANON

6 INTERNATIONAL MONETARY FUND

Box 1. The Prolonged Impact of the Syrian Refugee Crisis

The Syrian crisis is now entering its fifth year. According to the United Nations High Commission for Refugees (UNHCR), the number of Syrian refugees exceeded 1.4 million in January 2015. Combined with an estimated 0.4 million Palestinians already in Lebanon, refugees now exceed one third of Lebanon’s total resident population. And looking ahead, UNCHR expects the number of Syrian refugees will surpass 1.8 million by the end of the year.

Although all parties agree that such a number of refugees is unsustainable, there are few quantitative estimates of their economic impact.

The authorities’ have been clearly confronted with rising healthcare, education, electricity, and security costs, and the quality of public-service provision has suffered. But to date, the only comprehensive costing comes from a 2013 study led by the World Bank, which estimated the direct fiscal impact of the crisis over 2012–14 at $2.6 billion (5½ percent of GDP).1 It also suggested that restoring public-service provision to pre-crisis levels would require an additional $2.5 billion. These results remain the most reliable assessment of the crisis’ fiscal cost.

As for the broader macroeconomic impact of the crisis, a recent UNDP study2 estimated the multiplier associated with humanitarian aid at around 1.6. Thus, while the (net) impact of the crisis has clearly been negative, aid inflows in 2014 added 1.3 percent to overall GDP growth.

The social costs of the crisis have also been significant. Poverty in Lebanon has increased by 4 percentage points to 32 percent; the labor force has risen by an estimated 50 percent compared to 2011; and income inequality has widened, as Syrian refugees accept much lower wages than Lebanese workers.3

1 World Bank, 2013. “Economic and Social Impact Assessment of the Syrian Conflict”, WB Report No. 81098-LB. 2 UNDP, 2015. “Impact of Humanitarian Aid on the Lebanese Economy, Fiscal Multiplier Report”. 3 IMF, 2015. “The Impact of the Syrian Conflict on Lebanon,” Selected Issues Paper (IMF Country Report No. 14/238).

LEBANON

INTERNATIONAL MONETARY FUND 7

Box 1. The Prolonged Impact of the Syrian Refugee Crisis (concluded)

A comprehensive strategy is yet to be put in place. As a matter of policy, Lebanon has long maintained that it is not a country of asylum, a final destination for refugees, or a country of resettlement. But there is no consensus on the best way to curb the inflows or deal with existing refugees—memories about Palestinian refugee camps have prevented the consideration of organized settlements or any measure that might allude to a permanent presence. After a long delay, the authorities adopted a policy paper in October 2014 focusing on three broad principles: (i) reducing the number of individuals registered in Lebanon as displaced; (ii) addressing local security concerns; and (iii) sharing the burden of the crisis by expanding the humanitarian response to include local communities and infrastructure. It also encouraged relocation to safe areas in Syria, or for third countries to offer more resettlement opportunities. As part of this policy, the authorities have tightened border-control requirements; and registrations of new refugees are now down to around 10,000 per month, compared to around 30,000 per month prior to October 2014.

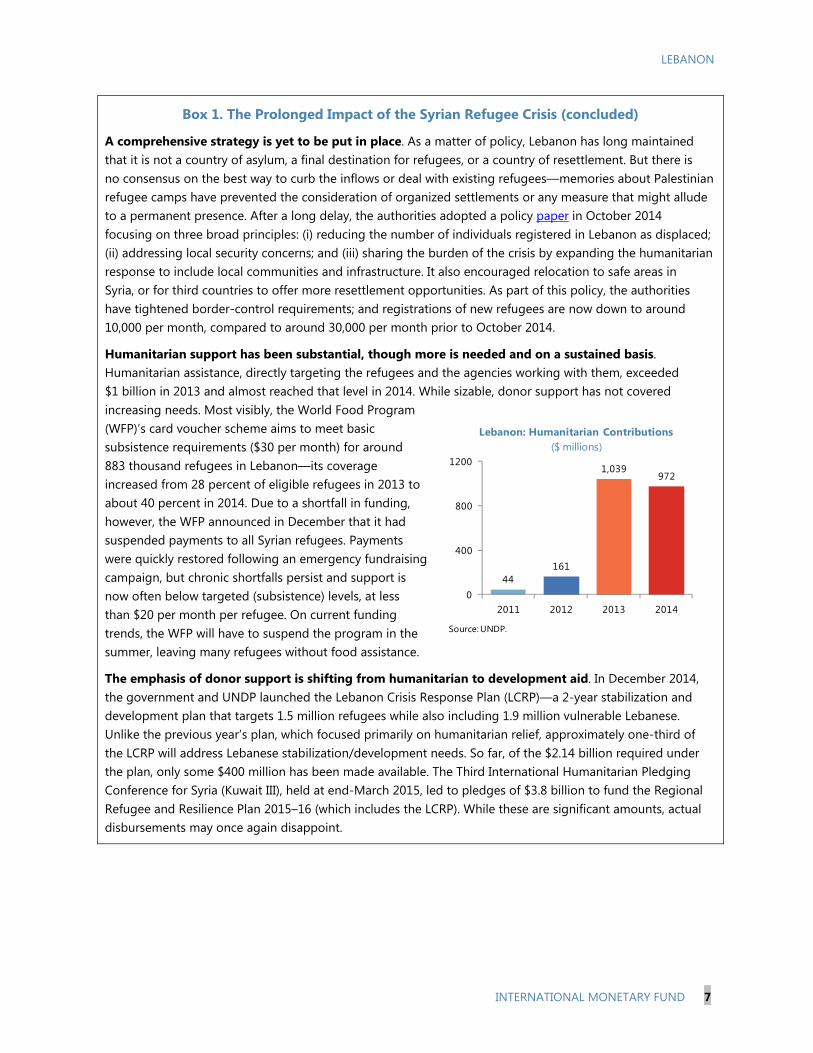

Humanitarian support has been substantial, though more is needed and on a sustained basis. Humanitarian assistance, directly targeting the refugees and the agencies working with them, exceeded $1 billion in 2013 and almost reached that level in 2014. While sizable, donor support has not covered increasing needs. Most visibly, the World Food Program (WFP)’s card voucher scheme aims to meet basic subsistence requirements ($30 per month) for around 883 thousand refugees in Lebanon—its coverage increased from 28 percent of eligible refugees in 2013 to about 40 percent in 2014. Due to a shortfall in funding, however, the WFP announced in December that it had suspended payments to all Syrian refugees. Payments were quickly restored following an emergency fundraising campaign, but chronic shortfalls persist and support is now often below targeted (subsistence) levels, at less than $20 per month per refugee. On current funding trends, the WFP will have to suspend the program in the summer, leaving many refugees without food assistance.

The emphasis of donor support is shifting from humanitarian to development aid. In December 2014, the government and UNDP launched the Lebanon Crisis Response Plan (LCRP)—a 2-year stabilization and development plan that targets 1.5 million refugees while also including 1.9 million vulnerable Lebanese. Unlike the previous year’s plan, which focused primarily on humanitarian relief, approximately one-third of the LCRP will address Lebanese stabilization/development needs. So far, of the $2.14 billion required under the plan, only some $400 million has been made available. The Third International Humanitarian Pledging Conference for Syria (Kuwait III), held at end-March 2015, led to pledges of $3.8 billion to fund the Regional Refugee and Resilience Plan 2015–16 (which includes the LCRP). While these are significant amounts, actual disbursements may once again disappoint.

44161

1,039972

0

400

800

1200

2011 2012 2013 2014

Lebanon: Humanitarian Contributions($ millions)

Source: UNDP.

LEBANON

8 INTERNATIONAL MONETARY FUND

Box 2. Can Nominal GDP Increase with Falling Prices and Stagnant Growth?

Despite weak growth and falling prices, Lebanon’s nominal GDP is rising. Staff have recently scaled back their real GDP growth estimates, amidst falling inflation (actually negative at end-2014). But nominal GDP projections have actually increased. So why is nominal GDP rising so rapidly? The answer stems from the relationship between two commonly used measures of inflation—the consumer price index (CPI) and the GDP deflator.

The CPI and deflator typically move together, but not always. Indeed, there may be occasions when they provide very different pictures of inflation. The discrepancy often stems from movements in a country’s terms of trade, i.e. the ratio of export prices to import prices. Essentially, the CPI basket includes imports, but not exports; whereas the GDP deflator includes exports, but not imports. So, if the prices of these two trade-related items move in different directions, the gap between the CPI and the deflator may be significant. To gauge the size of the gap, it is useful to note that:

GDP deflator = "Domestic prices" export prices import prices

where α and β are the relative importance of exports and imports, respectively, as a proportion of GDP. If Lebanon’s terms of trade improve—either through rising export prices or falling import prices—then the deflator will tend to rise faster than the CPI. And as a result, nominal GDP will grow relatively quickly; reflecting the fact that Lebanon is effectively wealthier.

Looking forward, nominal GDP is projected to grow rapidly in 2015. WEO projections imply a significant improvement in Lebanon’s terms of trade in 2015, owing in large part to the recent drop in oil (import) prices, but reflecting also the strengthening U.S. dollar. These factors will boost nominal GDP growth, despite subdued consumer prices and modest real growth.

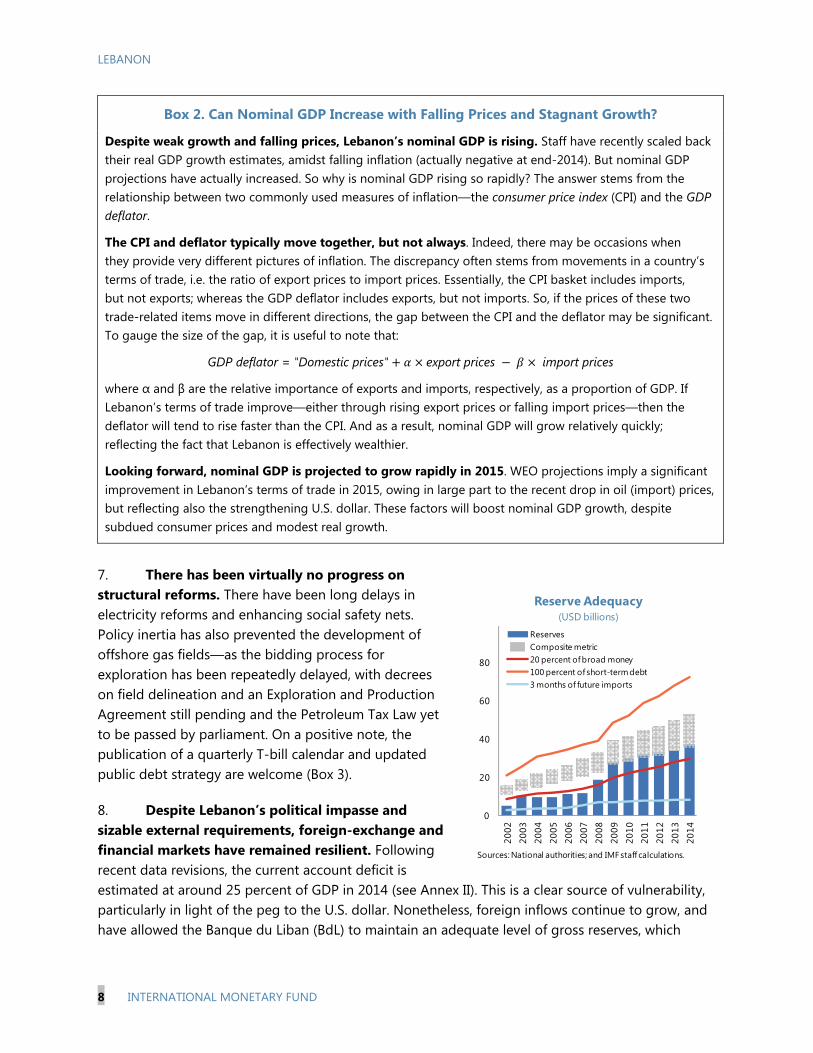

7. There has been virtually no progress on structural reforms. There have been long delays in electricity reforms and enhancing social safety nets. Policy inertia has also prevented the development of offshore gas fields—as the bidding process for exploration has been repeatedly delayed, with decrees on field delineation and an Exploration and Production Agreement still pending and the Petroleum Tax Law yet to be passed by parliament. On a positive note, the publication of a quarterly T-bill calendar and updated public debt strategy are welcome (Box 3).

8. Despite Lebanon’s political impasse and sizable external requirements, foreign-exchange and financial markets have remained resilient. Following recent data revisions, the current account deficit is estimated at around 25 percent of GDP in 2014 (see Annex II). This is a clear source of vulnerability, particularly in light of the peg to the U.S. dollar. Nonetheless, foreign inflows continue to grow, and have allowed the Banque du Liban (BdL) to maintain an adequate level of gross reserves, which

0

20

40

60

80

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Reserve Adequacy (USD billions)

ReservesComposite metric20 percent of broad money100 percent of short-term debt3 months of future imports

Sources: National authorities; and IMF staff calculations.

LEBANON

INTERNATIONAL MONETARY FUND 9

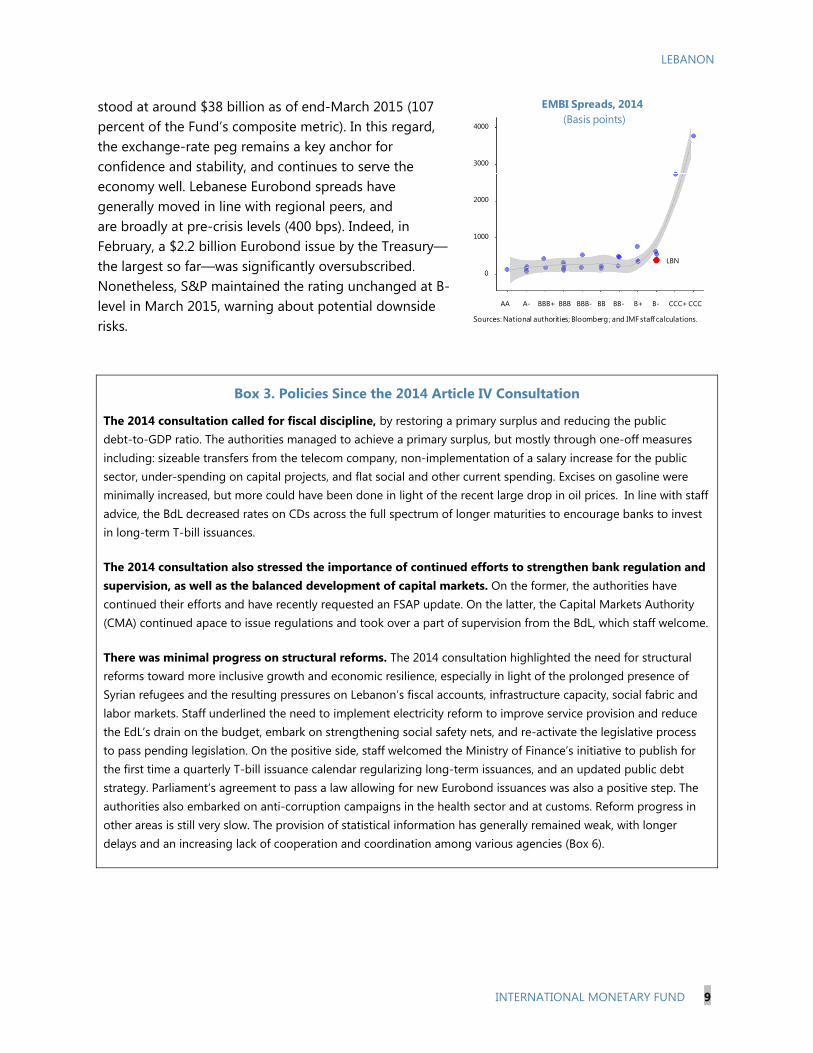

AA A- BBB+ BBB BBB- BB BB- B+ B- CCC+ CCC

4000

3000

2000

1000

0

LBN

EMBI Spreads, 2014 (Basis points)

Sources: National authorities; Bloomberg ; and IMF staff calculations.

stood at around $38 billion as of end-March 2015 (107 percent of the Fund’s composite metric). In this regard, the exchange-rate peg remains a key anchor for confidence and stability, and continues to serve the economy well. Lebanese Eurobond spreads have generally moved in line with regional peers, and are broadly at pre-crisis levels (400 bps). Indeed, in February, a $2.2 billion Eurobond issue by the Treasury—the largest so far—was significantly oversubscribed. Nonetheless, S&P maintained the rating unchanged at B- level in March 2015, warning about potential downside risks.

Box 3. Policies Since the 2014 Article IV Consultation

The 2014 consultation called for fiscal discipline, by restoring a primary surplus and reducing the public debt-to-GDP ratio. The authorities managed to achieve a primary surplus, but mostly through one-off measures including: sizeable transfers from the telecom company, non-implementation of a salary increase for the public sector, under-spending on capital projects, and flat social and other current spending. Excises on gasoline were minimally increased, but more could have been done in light of the recent large drop in oil prices. In line with staff advice, the BdL decreased rates on CDs across the full spectrum of longer maturities to encourage banks to invest in long-term T-bill issuances.

The 2014 consultation also stressed the importance of continued efforts to strengthen bank regulation and supervision, as well as the balanced development of capital markets. On the former, the authorities have continued their efforts and have recently requested an FSAP update. On the latter, the Capital Markets Authority (CMA) continued apace to issue regulations and took over a part of supervision from the BdL, which staff welcome.

There was minimal progress on structural reforms. The 2014 consultation highlighted the need for structural reforms toward more inclusive growth and economic resilience, especially in light of the prolonged presence of Syrian refugees and the resulting pressures on Lebanon’s fiscal accounts, infrastructure capacity, social fabric and labor markets. Staff underlined the need to implement electricity reform to improve service provision and reduce the EdL’s drain on the budget, embark on strengthening social safety nets, and re-activate the legislative process to pass pending legislation. On the positive side, staff welcomed the Ministry of Finance’s initiative to publish for the first time a quarterly T-bill issuance calendar regularizing long-term issuances, and an updated public debt strategy. Parliament’s agreement to pass a law allowing for new Eurobond issuances was also a positive step. The authorities also embarked on anti-corruption campaigns in the health sector and at customs. Reform progress in other areas is still very slow. The provision of statistical information has generally remained weak, with longer delays and an increasing lack of cooperation and coordination among various agencies (Box 6).

LEBANON

10 INTERNATIONAL MONETARY FUND

…AMID MOUNTING RISKS 9. Lebanon’s unique macro-financial structure is a source of resilience, but also of key risks. With aggregate assets exceeding 350 percent of GDP, the Lebanese banking sector is one of the largest in the world and the largest in the MENA region as a share of GDP. Banks attract substantial deposits from both residents and nonresidents, including from Lebanon’s large overseas diaspora. And they play a crucial role in channeling these funds to both the private and public sectors, helping fund large budget and current account deficits. In itself, the banking system has a relatively conservative business model, is well-supervised, and enjoys a relatively stable funding base with significant buffers. While the nexus between the banks and the sovereign has been at the core of Lebanon’s resilience, it also means that broader macroeconomic stability depends in large part on the banks’ continued ability to attract foreign deposits.

10. Based on traditional financial-soundness indicators, there is little evidence of a build-up of risks to financial stability.

Credit to the nonfinancial private sector has grown by about 9 percent per year over 2013–14, faster than nominal output. As a result, the private sector credit-to-GDP ratio increased from 86 to 91 percent over the same period, in part driven by three BdL stimulus packages totaling $3.4 billion. While this might otherwise be a cause for concern, standard metrics such as the “credit gap” (the deviation of credit-to-GDP from its long-run trend) suggest that, based on Lebanon’s past experience, risks to financial stability are not currently out of line.

At the same time, the BdL has introduced new macroprudential measures to contain the build-up of risk, tightening provisioning rules for retail loans and imposing new restrictions on lending to households, in the form of lower loan-to-value ratios and debt-service-to-income ratios.

60

70

80

90

100

0

5

10

15

20

25

30

2007 2008 2009 2010 2011 2012 2013 2014

Credit to the Private Sector(y/y growth, percent)

Credit/GDP (RHS)

Credit Growth

Sources: Banque du Liban ; and IMF staff calculations.

Lebanon's Macro-Financial System

Note: The width of the arrows is proportional to the size of the exposures.

BANQUE DU LIBAN

RE

ST O

F T

HE

WO

RLD

BANKS

GOVERNMENT OF LEBANON

RESIDENT PRIVATE SECTOR

LEBANON

INTERNATIONAL MONETARY FUND 11

0

10

20

30

40

2008 2009 2010 2011 2012 2013 2014

Non-Resident Deposits 1/ (y/y growth)

1/ Includes deposits of non-resident banks.Sources: National authorities; IMF staff calculations.

Private sector leverage appears contained. Leverage is not a pressing worry for Lebanese banks, as the system’s leverage ratio (at 6.5 percent) is well above Basel III’s minimum requirement of 3 percent. Similarly, household indebtedness is reasonable, at around 44 percent of household income. However, there is little available data on non-financial corporate leverage.

Risks could arise following a sharper downturn of the real estate market. A sizable fraction of bank loans to the private sector have been directed at the real estate sector, where activity is softening. But, in the absence of a price index, the number and value of property sales can serve as a proxy for the housing cycle. Both indicators grew by close to 3 percent in 2014. This is slightly more than the 2009–14 average for the number of transactions, but well below the past average for the value of sold properties (around 11 percent).

11. Nonetheless, the structure of Lebanon’s financial system, and the tight nexus between banks and the sovereign, make the economy dependent on the confidence of non-resident depositors. As noted above, deposit inflows are the key source of funding for the economy. These inflows have been resilient, including in the face of financial- and commodity-market volatility. Deposit growth has decelerated over recent years—but at 7–8 percent, it has remained sufficient to cover Lebanon’s (public and external) financing needs and to maintain the current international reserve buffer. However, risks from a further escalation of regional conflict (or other external events) are exceptionally high, and could lead to a negative and potentially protracted investor response.

12. Spillovers from the Syria crisis pose the most serious threat to the economy. Under the baseline, staff assume that the conflict in Syria will begin to ease toward the end of 2016; at which point confidence will come back and growth will gradually return to potential—a modest 4 percent. Thus, in contrast to the recent past, when high GDP growth helped contain Lebanon’s imbalances, subdued growth over the

Housing Other

Hotels & Rest.

Other Real Estate

Construction

Trade and Services

Individuals IndustryFin.

Interm.

Other Agric.

Bank Loans by Sector, June 2014

Sources: Banque du Liban; and IMF staff calculations.

0

2

4

6

8

10

12

14

16

18

2015 2016 2017 2018 2019 2020

Public Debt Repayment Profile(USD billion)

Foreign principal

Foreign interest

Domestic principal

Domestic interest

Sources: National authorities; and IMF staff calculations.

LEBANON

12 INTERNATIONAL MONETARY FUND

foreseeable future will likely remain too low to stabilize debt, create jobs, or address the country’s deepening social tensions. On the (so far unlikely) upside, however, if the crisis in Syria were to be resolved, Lebanon would be in a unique position to assist in its reconstruction, with significant and positive implications for local incomes and growth.

13. Downside risks associated with the Syrian crisis are exceptionally high. In addition, two key risks also loom large (see Risk Assessment Matrix):

Continued fiscal deterioration due to political stalemate and entrenched social tensions. In the face of social pressures and refugee needs, the authorities may postpone fiscal adjustment as politically too difficult. Any such course would further increase public debt, possibly leading to financing pressures and lower investor confidence. This could, in turn, quickly spread into the macro-financial sphere—triggering lower deposits, higher financing costs, deteriorating bank finances, mounting exchange-rate pressures, and falling reserves.

Stalled structural reforms. Continued erosion of already weak infrastructure, and further disappointments, especially on the electricity front—compounded by the pressures from the refugee presence—could further weaken growth and competitiveness. This would have a direct impact on Lebanon’s already-adverse debt dynamics and social stability (with a longer-term feedback loop on domestic security).

Authorities’ views

14. The authorities broadly agreed with staff’s assessment of risks. They viewed developments in the region, most notably the crisis in Syria, as the main risk to security and relatedly, macroeconomic stability. They continued to believe that, although the international community had helped, it had done too little to allow Lebanon to deal adequately with the tragedy of the refugees, and that much more was needed to stem a crisis that transcended national and regional borders.

15. They were less concerned about spillovers from global financial market volatility and increased interest rates. They noted that, in the past, the pass-through from dollar to domestic interest rates had been gradual and incomplete, and that Lebanon would manage as long as a sufficiently large differential vis-à-vis dollar rates was maintained.

16. They shared staff’s assessment on the key role of continued deposit inflows. However, they underscored that, as the stock of deposits grows larger, less emphasis should be put on the growth rate per se rather than on the absolute size of the inflows, which continued to be sufficient to fund the economy. A slowdown in itself was not a pressing concern and was to be expected, given the domestic and regional outlook.

LEBANON

INTERNATIONAL MONETARY FUND 13

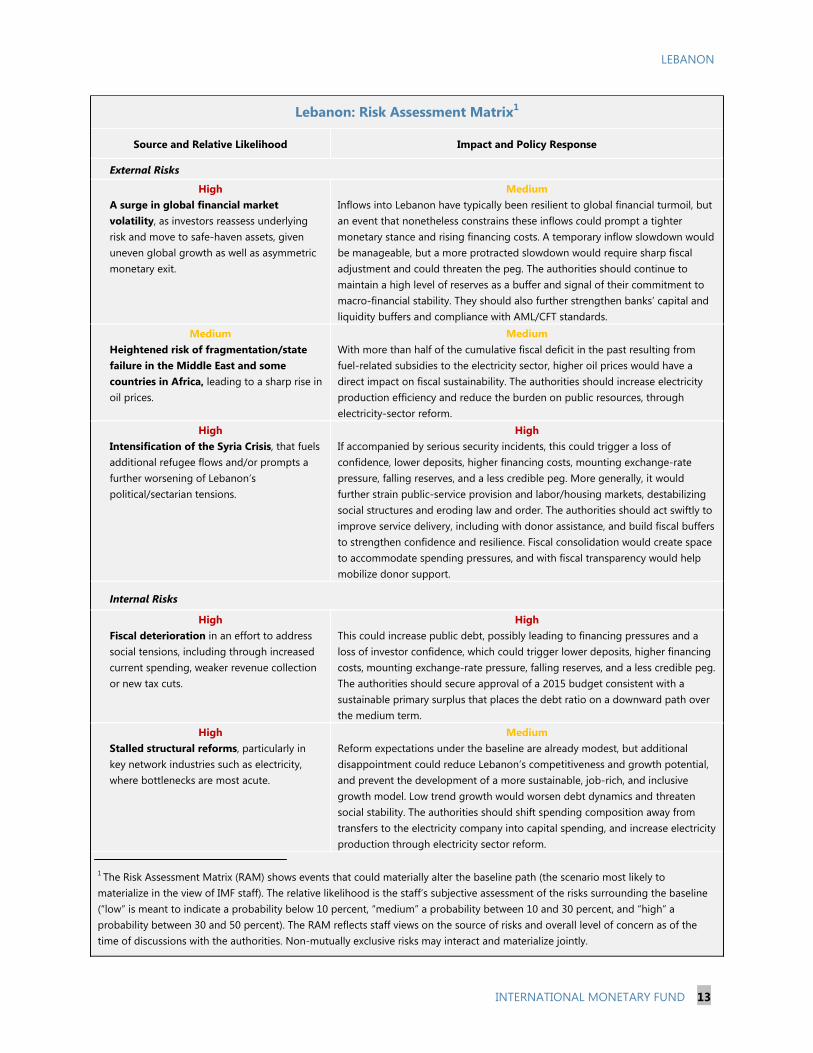

Lebanon: Risk Assessment Matrix1

Source and Relative Likelihood Impact and Policy Response

External Risks

High A surge in global financial market volatility, as investors reassess underlying risk and move to safe-haven assets, given uneven global growth as well as asymmetric monetary exit.

Medium Inflows into Lebanon have typically been resilient to global financial turmoil, but an event that nonetheless constrains these inflows could prompt a tighter monetary stance and rising financing costs. A temporary inflow slowdown would be manageable, but a more protracted slowdown would require sharp fiscal adjustment and could threaten the peg. The authorities should continue to maintain a high level of reserves as a buffer and signal of their commitment to macro-financial stability. They should also further strengthen banks’ capital and liquidity buffers and compliance with AML/CFT standards.

Medium Heightened risk of fragmentation/state failure in the Middle East and some countries in Africa, leading to a sharp rise in oil prices.

Medium With more than half of the cumulative fiscal deficit in the past resulting from fuel-related subsidies to the electricity sector, higher oil prices would have a direct impact on fiscal sustainability. The authorities should increase electricity production efficiency and reduce the burden on public resources, through electricity-sector reform.

High Intensification of the Syria Crisis, that fuels additional refugee flows and/or prompts a further worsening of Lebanon’s political/sectarian tensions.

High If accompanied by serious security incidents, this could trigger a loss of confidence, lower deposits, higher financing costs, mounting exchange-rate pressure, falling reserves, and a less credible peg. More generally, it would further strain public-service provision and labor/housing markets, destabilizing social structures and eroding law and order. The authorities should act swiftly to improve service delivery, including with donor assistance, and build fiscal buffers to strengthen confidence and resilience. Fiscal consolidation would create space to accommodate spending pressures, and with fiscal transparency would help mobilize donor support.

Internal Risks

High Fiscal deterioration in an effort to address social tensions, including through increased current spending, weaker revenue collection or new tax cuts.

High This could increase public debt, possibly leading to financing pressures and a loss of investor confidence, which could trigger lower deposits, higher financing costs, mounting exchange-rate pressure, falling reserves, and a less credible peg. The authorities should secure approval of a 2015 budget consistent with a sustainable primary surplus that places the debt ratio on a downward path over the medium term.

High Stalled structural reforms, particularly in key network industries such as electricity, where bottlenecks are most acute.

Medium Reform expectations under the baseline are already modest, but additional disappointment could reduce Lebanon’s competitiveness and growth potential, and prevent the development of a more sustainable, job-rich, and inclusive growth model. Low trend growth would worsen debt dynamics and threaten social stability. The authorities should shift spending composition away from transfers to the electricity company into capital spending, and increase electricity production through electricity sector reform.

1 The Risk Assessment Matrix (RAM) shows events that could materially alter the baseline path (the scenario most likely to materialize in the view of IMF staff). The relative likelihood is the staff’s subjective assessment of the risks surrounding the baseline (“low” is meant to indicate a probability below 10 percent, “medium” a probability between 10 and 30 percent, and “high” a probability between 30 and 50 percent). The RAM reflects staff views on the source of risks and overall level of concern as of the time of discussions with the authorities. Non-mutually exclusive risks may interact and materialize jointly.

LEBANON

14 INTERNATIONAL MONETARY FUND

POLICY DISCUSSIONS 17. Lebanon needs to take action. Over the short term, the key challenge will be to articulate a coherent policy mix, starting immediately with credible adjustment to restore fiscal sustainability. Over the longer term, social stability requires job-rich, sustainable growth that benefits all, which cannot happen without a more inclusive macroeconomic environment and structural reform. These two themes—ushering in a more balanced policy mix and laying the ground for higher and more inclusive growth—featured prominently in the 2015 Consultation.

A. A More Balanced Policy Mix

18. The need for fiscal adjustment is inescapable. Without it, and in the context of Lebanon’s slowing growth and rising global interest rates, public debt will increase. Similarly, without adjustment, government financing needs will continue to rise; the underlying codependence between banks and the sovereign will intensify; and Lebanon’s reliance on deposit inflows will grow larger, exposing the economy even more to sudden swings in depositors’ confidence. On all these counts, delayed adjustment will simply exacerbate Lebanon’s underlying vulnerabilities.

19. The case for fiscal adjustment is also grounded in fairness. Without it and with ever more debt, interest payments will soar to some 12 percent of GDP, or about 40 percent of total spending, crowding out essential social programs and infrastructure projects and largely benefitting public debt holders at the expense of the less-privileged. Thus lack of fiscal adjustment is also costly and inequitable.

20. Yet, on current policies fiscal sustainability will remain elusive. Under the baseline scenario, staff assume that the salary scale adjustment for the public sector will be implemented as part of a package including the following revenue measures:3 an increase in the corporate income tax rate (from 15 to 17 percent); the introduction of a capital gains tax on real estate; an increase in the tax rate on interest income (from 5 to 7 percent); and new stamp duties and fees. However, while the proposed package generates moderate primary surpluses, it would not be sufficient to tackle Lebanon’s deteriorating debt dynamics. As a result, debt is projected to reach 143 percent of GDP by 2020, with its trajectory subject to significant downside risks (Annex I).

3 While the salary increase is subject to uncertainty, in the ongoing political debate it is clearly linked to the adoption of (partially) compensating revenue measures. Staff projections assume that the salary increase will be implemented as of January 1, 2015, while the revenue measures will become effective as of January 1, 2016.

Lebanon: Government Spending, 2014

Wages InterestEDL

TransfersCurrent

SpendingPublic

Investment

2 squares = 1 percent of GDPSources: National authorities; and IMF staff calculations.

LEBANON

INTERNATIONAL MONETARY FUND 15

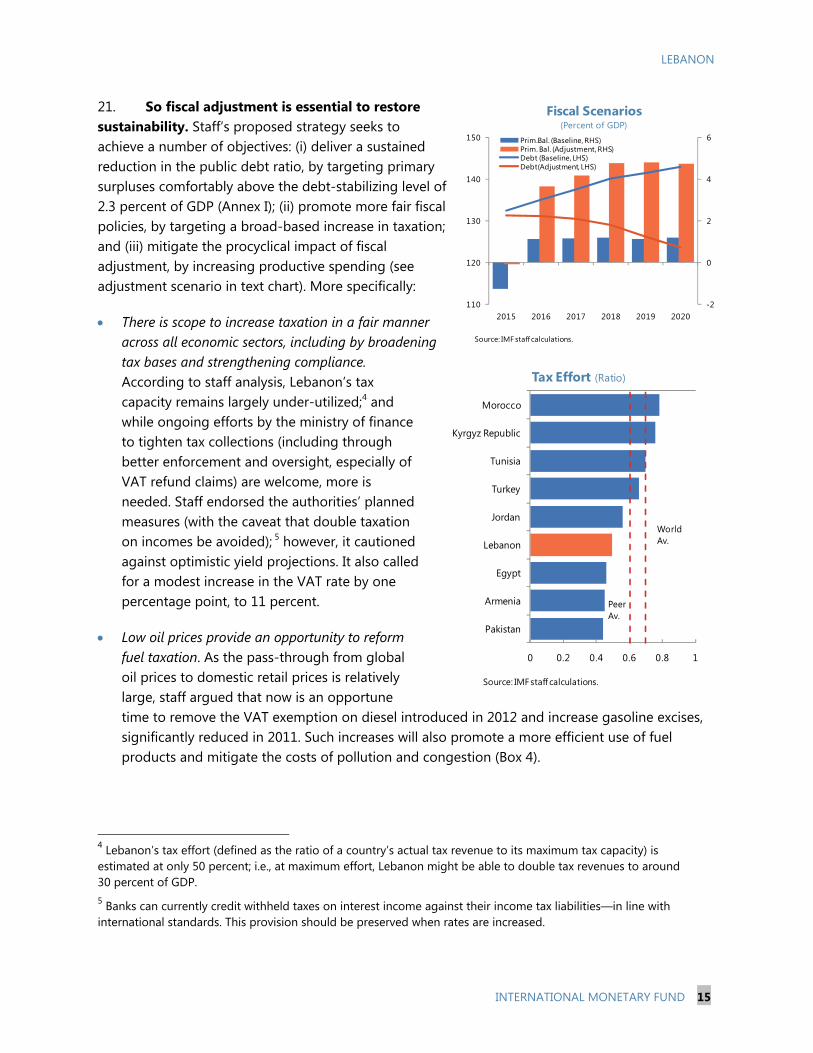

21. So fiscal adjustment is essential to restore sustainability. Staff’s proposed strategy seeks to achieve a number of objectives: (i) deliver a sustained reduction in the public debt ratio, by targeting primary surpluses comfortably above the debt-stabilizing level of 2.3 percent of GDP (Annex I); (ii) promote more fair fiscal policies, by targeting a broad-based increase in taxation; and (iii) mitigate the procyclical impact of fiscal adjustment, by increasing productive spending (see adjustment scenario in text chart). More specifically:

There is scope to increase taxation in a fair manner across all economic sectors, including by broadening tax bases and strengthening compliance. According to staff analysis, Lebanon’s tax capacity remains largely under-utilized;4 and while ongoing efforts by the ministry of finance to tighten tax collections (including through better enforcement and oversight, especially of VAT refund claims) are welcome, more is needed. Staff endorsed the authorities’ planned measures (with the caveat that double taxation on incomes be avoided); 5 however, it cautioned against optimistic yield projections. It also called for a modest increase in the VAT rate by one percentage point, to 11 percent.

Low oil prices provide an opportunity to reform fuel taxation. As the pass-through from global oil prices to domestic retail prices is relatively large, staff argued that now is an opportune time to remove the VAT exemption on diesel introduced in 2012 and increase gasoline excises, significantly reduced in 2011. Such increases will also promote a more efficient use of fuel products and mitigate the costs of pollution and congestion (Box 4).

4 Lebanon’s tax effort (defined as the ratio of a country’s actual tax revenue to its maximum tax capacity) is estimated at only 50 percent; i.e., at maximum effort, Lebanon might be able to double tax revenues to around 30 percent of GDP. 5 Banks can currently credit withheld taxes on interest income against their income tax liabilities—in line with international standards. This provision should be preserved when rates are increased.

-2

0

2

4

6

110

120

130

140

150

2015 2016 2017 2018 2019 2020

Fiscal Scenarios (Percent of GDP)

Prim.Bal. (Baseline, RHS)Prim. Bal. (Adjustment, RHS)Debt (Baseline, LHS)Debt(Adjustment, LHS)

Source: IMF staff calculations.

0 0.2 0.4 0.6 0.8 1

Pakistan

Armenia

Egypt

Lebanon

Jordan

Turkey

Tunisia

Kyrgyz Republic

Morocco

Tax Effort (Ratio)

WorldAv.

PeerAv.

Source: IMF staff calculations.

LEBANON

16 INTERNATIONAL MONETARY FUND

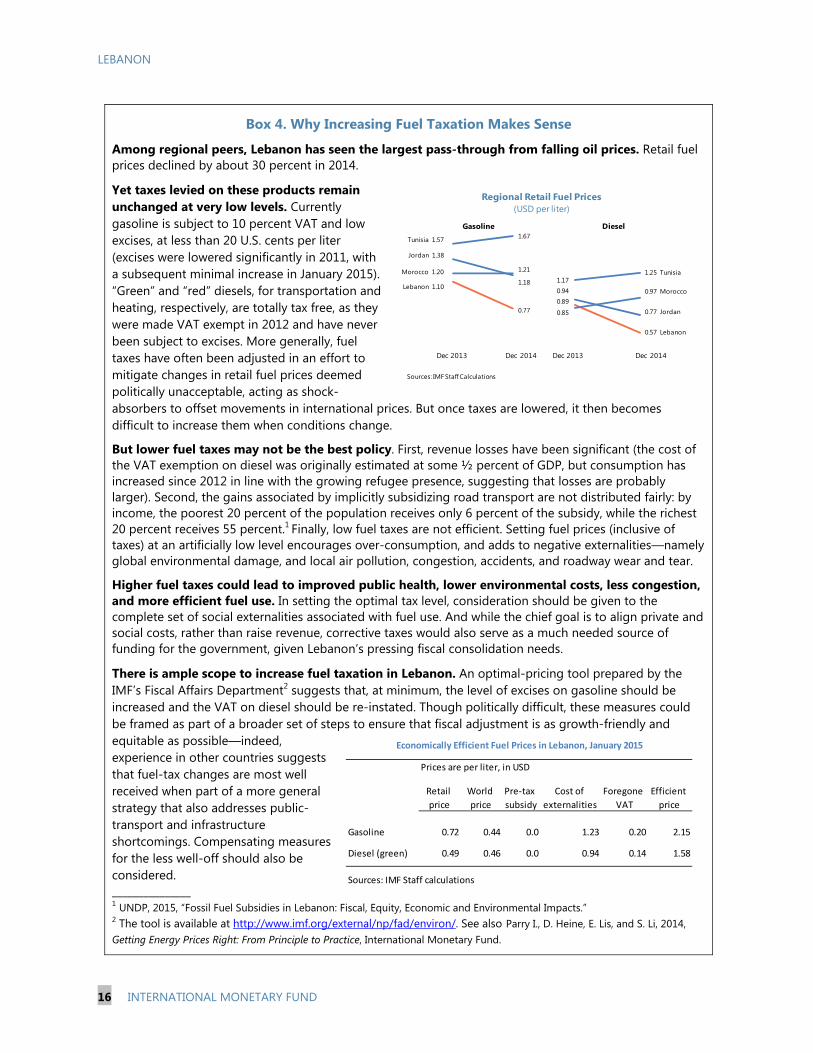

Box 4. Why Increasing Fuel Taxation Makes Sense

Among regional peers, Lebanon has seen the largest pass-through from falling oil prices. Retail fuel prices declined by about 30 percent in 2014.

Yet taxes levied on these products remain unchanged at very low levels. Currently gasoline is subject to 10 percent VAT and low excises, at less than 20 U.S. cents per liter (excises were lowered significantly in 2011, with a subsequent minimal increase in January 2015). “Green” and “red” diesels, for transportation and heating, respectively, are totally tax free, as they were made VAT exempt in 2012 and have never been subject to excises. More generally, fuel taxes have often been adjusted in an effort to mitigate changes in retail fuel prices deemed politically unacceptable, acting as shock-absorbers to offset movements in international prices. But once taxes are lowered, it then becomes difficult to increase them when conditions change.

But lower fuel taxes may not be the best policy. First, revenue losses have been significant (the cost of the VAT exemption on diesel was originally estimated at some ½ percent of GDP, but consumption has increased since 2012 in line with the growing refugee presence, suggesting that losses are probably larger). Second, the gains associated by implicitly subsidizing road transport are not distributed fairly: by income, the poorest 20 percent of the population receives only 6 percent of the subsidy, while the richest 20 percent receives 55 percent.1 Finally, low fuel taxes are not efficient. Setting fuel prices (inclusive of taxes) at an artificially low level encourages over-consumption, and adds to negative externalities—namely global environmental damage, and local air pollution, congestion, accidents, and roadway wear and tear.

Higher fuel taxes could lead to improved public health, lower environmental costs, less congestion, and more efficient fuel use. In setting the optimal tax level, consideration should be given to the complete set of social externalities associated with fuel use. And while the chief goal is to align private and social costs, rather than raise revenue, corrective taxes would also serve as a much needed source of funding for the government, given Lebanon’s pressing fiscal consolidation needs.

There is ample scope to increase fuel taxation in Lebanon. An optimal-pricing tool prepared by the IMF’s Fiscal Affairs Department2 suggests that, at minimum, the level of excises on gasoline should be increased and the VAT on diesel should be re-instated. Though politically difficult, these measures could be framed as part of a broader set of steps to ensure that fiscal adjustment is as growth-friendly and equitable as possible—indeed, experience in other countries suggests that fuel-tax changes are most well received when part of a more general strategy that also addresses public-transport and infrastructure shortcomings. Compensating measures for the less well-off should also be considered. _______________ 1 UNDP, 2015, “Fossil Fuel Subsidies in Lebanon: Fiscal, Equity, Economic and Environmental Impacts.” 2 The tool is available at http://www.imf.org/external/np/fad/environ/. See also Parry I., D. Heine, E. Lis, and S. Li, 2014, Getting Energy Prices Right: From Principle to Practice, International Monetary Fund.

Gasoline

0.57 Lebanon

0.97 Morocco

0.77 Jordan

1.25 Tunisia

Diesel

0.85

0.940.89

1.17Lebanon 1.10

Morocco 1.20

Jordan 1.38

Tunisia 1.57

Dec 2013 Dec 2014 Dec 2013 Dec 2014

Sources: IMF Staff Calculations

0.77

1.18

1.21

1.67

Regional Retail Fuel Prices(USD per liter)

Prices are per liter, in USD

Retail

price

World

price

Pre-tax

subsidy

Cost of

externalities

Foregone

VAT

Efficient

price

Gasoline 0.72 0.44 0.0 1.23 0.20 2.15

Diesel (green) 0.49 0.46 0.0 0.94 0.14 1.58

Sources: IMF Staff calculations

Economically Efficient Fuel Prices in Lebanon, January 2015

LEBANON

INTERNATIONAL MONETARY FUND 17

Lebanon: Fiscal Scenarios, 2016–18 (Percent of GDP)

Telecom transfers should be managed transparently. Staff noted that their ad-hoc nature

hampered proper cash management and called for a system of regular transfers.

The state-owned Electricité du Liban (EdL) should urgently be placed on a sound financial footing to reduce the need for government transfers. Staff noted that low oil prices have created some fiscal space, but that they cannot be relied upon to contain future transfers. Ideally, transfers should be eliminated. Staff therefore renewed calls for a comprehensive reform of the electricity sector (see next section). Ultimately, as service provision is improved, tariffs (unchanged since 1993) should be increased toward cost recovery levels while protecting lower-income consumers.

The salary scale adjustment should be implemented only if funded by credible revenue measures, phased in gradually and without retroactive payments. Staff underscored that it should be accompanied by steps toward comprehensive public-sector reform, such as lengthening working hours from 32 to 35 a week and capping overtime and benefits, to ensure that public servants are adequately remunerated based on their productivity.6 However, staff also noted that the salary debate had drawn attention away from the more pressing need for fiscal adjustment, and that fully funding the salary increases—the primary focus of ongoing political discussions—would do nothing to reduce the budget deficit, but would instead add pressures to already unsustainable public pension schemes (see below).

6 These measures were part of the original salary-scale proposal but later abandoned.

CIT

Capital Gains on Real Estate

Interest Income

Excises

Stamps and Fees

VAT

EDL Transfers

Personnel Costs

Interest payments

Capital Spending

5 percent of GDP

2016 2017 2018

BaselineAdjustment

RevenueBaselineAdjustmentSpending

Source: IMF staff estimates.

2016 2017 2018

LEBANON

18 INTERNATIONAL MONETARY FUND

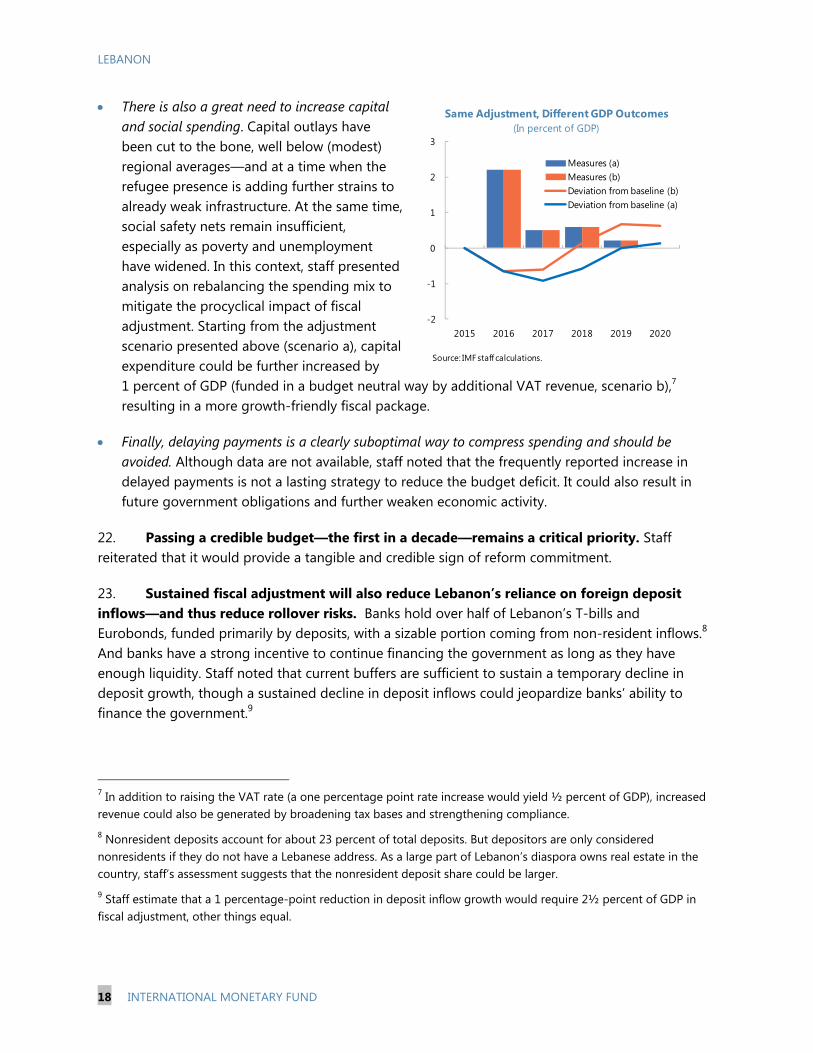

There is also a great need to increase capital and social spending. Capital outlays have been cut to the bone, well below (modest) regional averages—and at a time when the refugee presence is adding further strains to already weak infrastructure. At the same time, social safety nets remain insufficient, especially as poverty and unemployment have widened. In this context, staff presented analysis on rebalancing the spending mix to mitigate the procyclical impact of fiscal adjustment. Starting from the adjustment scenario presented above (scenario a), capital expenditure could be further increased by 1 percent of GDP (funded in a budget neutral way by additional VAT revenue, scenario b),7 resulting in a more growth-friendly fiscal package.

Finally, delaying payments is a clearly suboptimal way to compress spending and should be avoided. Although data are not available, staff noted that the frequently reported increase in delayed payments is not a lasting strategy to reduce the budget deficit. It could also result in future government obligations and further weaken economic activity.

22. Passing a credible budget—the first in a decade—remains a critical priority. Staff reiterated that it would provide a tangible and credible sign of reform commitment.

23. Sustained fiscal adjustment will also reduce Lebanon’s reliance on foreign deposit inflows—and thus reduce rollover risks. Banks hold over half of Lebanon’s T-bills and Eurobonds, funded primarily by deposits, with a sizable portion coming from non-resident inflows.8 And banks have a strong incentive to continue financing the government as long as they have enough liquidity. Staff noted that current buffers are sufficient to sustain a temporary decline in deposit growth, though a sustained decline in deposit inflows could jeopardize banks’ ability to finance the government.9

7 In addition to raising the VAT rate (a one percentage point rate increase would yield ½ percent of GDP), increased revenue could also be generated by broadening tax bases and strengthening compliance. 8 Nonresident deposits account for about 23 percent of total deposits. But depositors are only considered nonresidents if they do not have a Lebanese address. As a large part of Lebanon’s diaspora owns real estate in the country, staff’s assessment suggests that the nonresident deposit share could be larger. 9 Staff estimate that a 1 percentage-point reduction in deposit inflow growth would require 2½ percent of GDP in fiscal adjustment, other things equal.

-2

-1

0

1

2

3

2015 2016 2017 2018 2019 2020

Measures (a)Measures (b)Deviation from baseline (b)Deviation from baseline (a)

Same Adjustment, Different GDP Outcomes(In percent of GDP)

Source: IMF staff calculations.

LEBANON

INTERNATIONAL MONETARY FUND 19

24. Fiscal adjustment would reduce the financial—and institutional—burden on the BdL. The key priority of the BdL has, appropriately, been to build up Lebanon’s foreign exchange (FX) reserve buffers, given the central role of the peg as a nominal anchor. To this effect, the BdL has been channeling FX resources from the banking system into international reserves. Over the past couple of years, however, some of these funds have also been used to meet the FX needs of the government. At the same time, the BdL has also played a growing role in the allocation of credit to the private sector, by introducing subsidized schemes—accounting for about 20 percent of total outstanding loans and close to 75 percent of housing loans in 2014. Staff called for a gradual withdrawal from such quasi-fiscal schemes, allowing old subsidized credit schemes to expire. All these operations have taken a toll on the BdL’s income position. Looking forward, there is a need to gradually strengthen the BdL’s balance sheet.10

25. Finally, fiscal adjustment would allow for more market-determined interest rates. Staff noted that the BdL, at times, has helped finance the government by offering well-remunerated term deposits to banks in local currency, and channeling the proceeds to cover shortfalls in the T-bill market. As a result, the BdL has been effectively managing short- and medium-term T-Bill yields (unchanged since 2012) by using rates on its own CDs as a key signal. While financial conditions do not appear excessively loose or tight (Box 5), staff underscored that unchanging interest rates tend to dampen market signals, potentially distorting resource allocation and hindering market development. It therefore recommended that, as fiscal adjustment takes hold, the BdL should scale back its role as intermediary between banks and the sovereign, paving the way for more market-based benchmark T-bill yields.

Authorities’ views

26. The authorities agreed that reducing the debt ratio is the main priority. They noted however that the political environment is extremely difficult, as shown by the protracted debate on the 2015 budget. While there was general consensus around the need to tackle well-known issues—such as reforms of electricity and civil service—concrete steps were unlikely. At the same time, they acknowledged that even small steps could have high impact as a signal of political action. Views remained split on the salary adjustment package, with some underscoring the need to bring hiring under control and adopting differentiated salary scale increases for different categories of public sector. At the same time, some noted that higher salaries were needed to secure a more decent living for public servants, and to mitigate corruption; while others were of the view that such increases cannot be afforded now.

27. The authorities also welcomed the emphasis on growth and fairness. They appreciated that, in contrast with past advice, staff was no longer recommending a VAT rate increase up to 15 percent, which they had viewed as regressive and politically unacceptable. They welcomed the

10 Lebanon is not a Special Data Dissemination Standards subscriber, and does not report data according to the International Reserves and Foreign Currency Liquidity Template. Details of the country’s net reserve position are therefore not published.

LEBANON

20 INTERNATIONAL MONETARY FUND

Fund’s ongoing technical assistance on boosting tax capacity through broadening tax bases and strengthening compliance, which would help spread the burden of adjustment.

28. There was broad agreement on the need to rebalance the policy mix to lighten the burden placed on the BdL. The authorities generally recognized that the BdL has been doing much to preserve the credibility of the peg while providing support to the government and the economy. They noted that recent steps to lower CD rates to align them fully with T-bill rates had been well-received, and could pave the way over time to a less active role in the management of government debt. But they disagreed with the claim that the BdL was actively intermediating the flow of funds between the banks and the government. Instead, they stressed that the issue of longer-term CDs was, in part, motivated by the BdL’s capital-market development goals—long-term BdL CDs were viewed as a key first step in extending the yield curve, and would ultimately help promote the issuance of longer-term T-bills by the Treasury. In this connection, they also explained that T-bills are more desirable than CDs to banks because they are more liquid—in fact when the government followed the central bank with the issuance of longer maturity bonds, banks showed appetite for these instruments. More broadly, they remained confident that the balance sheet of the BdL would be strengthened over time, though conditions were not yet favorable for pursuing alternative policy actions in the short term.

B. Aiming Higher: Stronger and More Inclusive Growth

29. Higher growth, better growth. Current low growth rates are insufficient to address social inequities and create jobs; and even in the past, higher growth has often only benefitted a few. In discussing Lebanon’s longer-term prospects, staff stressed three key areas: strengthening the financial system; structural reform, especially in electricity; and more and better data.

Financial stability

30. Sustained, broad-based growth requires a sound financial system. The banking system is one of the economy’s most critical pillars, and has contributed to growth and prosperity. Access of households and firms to banking services is high compared to the region or with other countries of similar income level.

LEBANON

INTERNATIONAL MONETARY FUND 21

Box 5. A Financial Conditions Index for Lebanon

A Financial Condition Index (FCI) combines several financial variables that influence GDP growth. It provides a summary measure of domestic financial conditions and can be used to assess macro-financial linkages. In particular, it points to the financial factors that are supporting or slowing real activity at any point in time.

Financial conditions appear to have tightened over the past year in Lebanon. Staff computed an FCI, showing that key drivers have been lower deposit growth and an appreciating real exchange rate, offset in part by low global interest rates.

The computation involves three steps.1

First, a vector-autoregressive model including financial variables and real GDP growth was estimated using quarterly data. The financial variables in the model include the 6-month LIBOR rate, deposit growth, the spread between lending and deposit rates (both in USD and local currency), and the real effective exchange rate (REER). The sample period covers 1995–2014.

Second, impulse responses are computed to assess the cumulative impact of a one-unit shock to the financial variables on GDP growth after 6 quarters. Structural shocks are identified through a Cholesky decomposition.2

Third, the estimated responses are used as weights for each variable in the FCI. All financial variables are expressed as deviations from their sample means.

LIBOR, deposit growth, and the REER are key drivers, with a more limited role for bank interest rate spreads.

Financial conditions eased significantly after 2008, supporting growth. The loosening reflected higher deposit inflows, lower global interest rates, a real depreciation and falling bank spreads.

But since 2014, financial conditions have tightened, in step with slowing economic activity. Deposit growth in particular has decelerated, and is below its 20-year average. Looking forward, rising global interest rates are expected to further tighten local conditions.

_____________________________________________________

1 See IMF’s Asia and Pacific Department Spring 2009 Regional Economic Outlook (Box 1.4), and Swiston (2008),“A U.S. Financial Conditions Index: Putting Credit Where Credit is Due,” IMF Working Paper 08/161. 2 The ordering assumes that domestic financial variables do not have a contemporaneous effect on GDP growth and that GDP growth and domestic financial variables do not contemporaneously affect the LIBOR rate.

-2

0

2

4

6

8

10

12

-30

-20

-10

0

10

20

30

1995 1997 1998 2000 2001 2003 2004 2006 2007 2009 2010 2012 2013

Financial Conditions Index

6-month LIBOR Deposit growthUSD loan-deposit spread LBP loan-deposit spreadReal effective exchange rate Financial Conditions IndexReal GDP growth (q-o-q, in percent, right scale)

Loos

erTi

ghte

r

Source: IMF staff estimates.

LEBANON

22 INTERNATIONAL MONETARY FUND

Indicators of Financial Inclusion

31. But the current environment is particularly challenging. Banks’ capital buffers are modest, considering their significant exposure to zero-weighted local-currency sovereign debt. And despite the implicit subsidy associated with the BdL’s credit support schemes, net interest margins have been contracting (though from large levels) and profit growth is down. Although as noted above there is little evidence that credit growth in Lebanon is excessive, the unfavorable outlook, combined with limited private-sector lending opportunities and already-large exposures to the government, would affect banks’ medium-term profitability.

32. Continued efforts to strengthen banking regulation and supervision are crucial. Nonperforming loans (NPLs) have increased slightly, from a low base, while provisioning has decreased and the use of overdraft facilities is widespread. Staff noted that the low level of NPLs, in particular, is potentially at odds with Lebanon’s slowing economy, and will likely increase in the short-to-medium term. In this regard, loan-classification rules do not provide an explicit test of whether the renegotiation or rescheduling of a loan could be concealing debt service problems. And there is no written rule regarding the classification of high-balance overdrafts that are permanently rolled over. Staff reiterated that the risk weights applicable to foreign currency claims on the BdL and holdings of Eurobonds should be set in accordance with the Basel capital adequacy framework. It welcomed the Banking Control Commission’s efforts to strengthen its supervision of banking groups with cross-border operations, and encouraged pursuing the establishment of supervisory colleges for Lebanese banking groups with significant operations abroad.

33. Macroprudential policies can be helpful to limit systemic risk. Staff welcomed the creation of a Financial Stability Unit within the BdL to monitor financial risks. New macroprudential measures were introduced in 2014—though it is too early to assess their effectiveness.

LebanonMiddle East and

North AfricaUpper Middle Income

Countries

Percentage of adults with a banking account (2011) 37 18 57

Percentage of adult women with a banking account (2011) 26 13 53

Percentage of adults having borrowed from a financial institution (2014) 15.6 n.a. 10.4

Percentage of firms with a line of credit (2013) 57.3 27.3 37.8

Percentage of small firms with a line of credit (2013) 49.1 21.8 32.6

Sources: National authorities; and World Bank FinStats Database.

02468

10

Capital adequacy

Profitability

Asset quality

FX exposure

Exposure to the sovereign

Liquidity

Bank Risk Indicators2013Q4

2014Q4

Note: Away from center signifies higher risks.Sources: BCC; and IMF staff calculations.

LEBANON

INTERNATIONAL MONETARY FUND 23

34. Risks related to Anti-Money Laundering and Combating the Financing of Terrorism (AML/CFT) issues remain. The existing legislation is not in line with revised international standards, as a new AML/CFT Law has been pending in parliament since 2010. Staff therefore called for its adoption and for the allocation of sufficient resources for its effective implementation. The BdL has also recently strengthened monitoring requirements at the level of each banking branch. Efforts should also focus on the regulation of cross-border cash transactions and the risk-based supervision of banks, and money remitters in particular, along with developing a better understanding of the origin of non-resident deposits and their beneficial owners.

35. The authorities’ request for an FSAP update is most welcome. The update is scheduled for 2016, and should also tackle the development of capital markets to help promote a more diversified flow of resources to the economy.

36. Reform of capital markets should continue. Building on ongoing progress (Box 3), staff recommended a rapid move to transforming the Beirut Stock Exchange into a joint-stock company—already foreseen in the law that established the Capital Markets Authority—to pave the way for its privatization.

Authorities’ views

37. The authorities agreed that a sound banking system is critical to Lebanon’s future growth and prosperity. In this regard, both the banks and their supervisors were keenly aware of the economic and reputational risks associated with Lebanon’s challenging environment, and all agreed on the need for a continued culture of prudence and caution. They underscored the BdL’s efforts to address Basel requirements ahead of the implementation deadlines and to require additional capital buffers on top of the Basel III minimum and conservation buffers. They noted that the decline in the ratio of specific provisions to NPLs over the past year was due to a composition effect—NPLs include "substandard" loans, which had increased in importance, but do not require specific provisions. The Banking Control Commission is progressively moving toward the adoption of International Financial Reporting Standards (IFRS) 9 norms that would require provisioning based on expected losses. But in the interim, it was stressed that total provisioning, including both specific and general provisions, had increased as a share of total NPLs. The authorities agreed that NPLs would likely grow in the immediate future, but considered that banks had sufficient buffers to comfortably absorb any increase.

38. The authorities expressed confidence in the effectiveness of Lebanon’s AML/CFT regime. They noted that, although the current framework is not formally compliant with international standards, there are three draft laws pending parliamentary approval. In the interim, the BdL requires that Lebanese banks abide by the regulations in place in the countries of their correspondent banks whenever these are stricter. They mentioned the reluctance and even refusal of Lebanese banks to deal with small money remitters as evidence of bank awareness of AML/CFT issues and stricter controls. Hence there is no concern about derisking by international correspondent banks vis-à-vis their Lebanese counterparts.

LEBANON

24 INTERNATIONAL MONETARY FUND

80

90

100

110

1202011 2012 2013 2014

Lebanon: Competitiveness Rank, 2011–14(Rank out of 144)

Source: World Economic Forum.

39. The authorities also underscored the importance of continuing the reform of capital markets. They highlighted the significance of market consultations on the capital markets regulations, with assistance from the World Bank, to marshal support and ownership of the reforms. As to the transformation of the Beirut Stock Exchange into a joint-stock company, they regretted that progress had been slow.

Structural reform

40. There cannot be enduring and inclusive growth without structural reform. The traditional drivers of growth in Lebanon are also those most vulnerable to region-wide uncertainty and security concerns. These sectors, in addition, have failed to provide the high-quality, job-rich growth needed to secure social stability. Indeed, Lebanon’s employment-growth elasticity (0.2) is one of the lowest in the region, and job creation has not kept up with the economy’s rapidly expanding labor force—now increased by the refugee influx.11 The reform agenda is well known, but little has been done. 41. Lebanon’s current account deficit suggests an underlying competitiveness problem, even factoring in the Syria crisis. The sharp increase in the deficit is attributable, in part, to the disruption of traditional trade relationships and elevated regional uncertainty—though the deficit is expected to improve (slowly) over the medium term. Nonetheless, even abstracting from the impact of Syria, the external balance is weaker than suggested by fundamentals, pointing to an underlying problem with productivity and competitiveness (see Annex II). If Lebanon is to transition to a stronger, more sustainable growth model, action is needed to boost

productivity, fight corruption, and address the cost of doing business.

42. Electricity reform is an urgent priority. Lebanon’s inefficient electricity supply is a major impediment to growth: losses from EdL weigh heavily on public finances, and poor service delivery has prompted the extensive use of costly private generators. Implementation of longstanding plans to strengthen generation capacity, switch to less-expensive natural gas, and improve transmission and distribution would go a long way

11 Officially, unemployment is estimated at 11 percent (though more than 20 percent including the refugees).

0 5 10 15 20

Jordan

Morocco

Mauritania

Algeria

Lebanon

Pakistan

Yemen, Rep.

Percent of Annual Sales

Losses Due to Electricity Outages

Source: World Bank Enterprise Survey, 2013.

LEBANON

INTERNATIONAL MONETARY FUND 25

toward reducing business and consumption costs. It would also ensure more equitable access to essential services. In parallel, the authorities should start to bring electricity tariffs more in line with cost recovery to reduce the burden on public finances—though in a way that protects more vulnerable consumers.