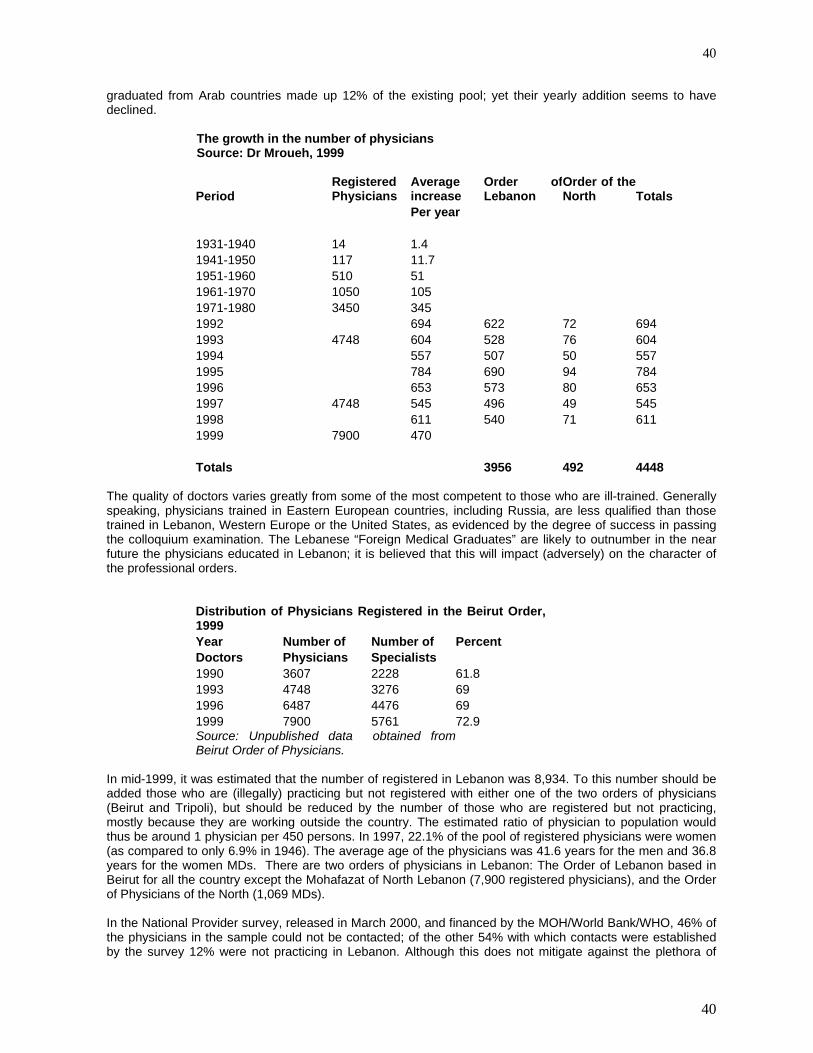

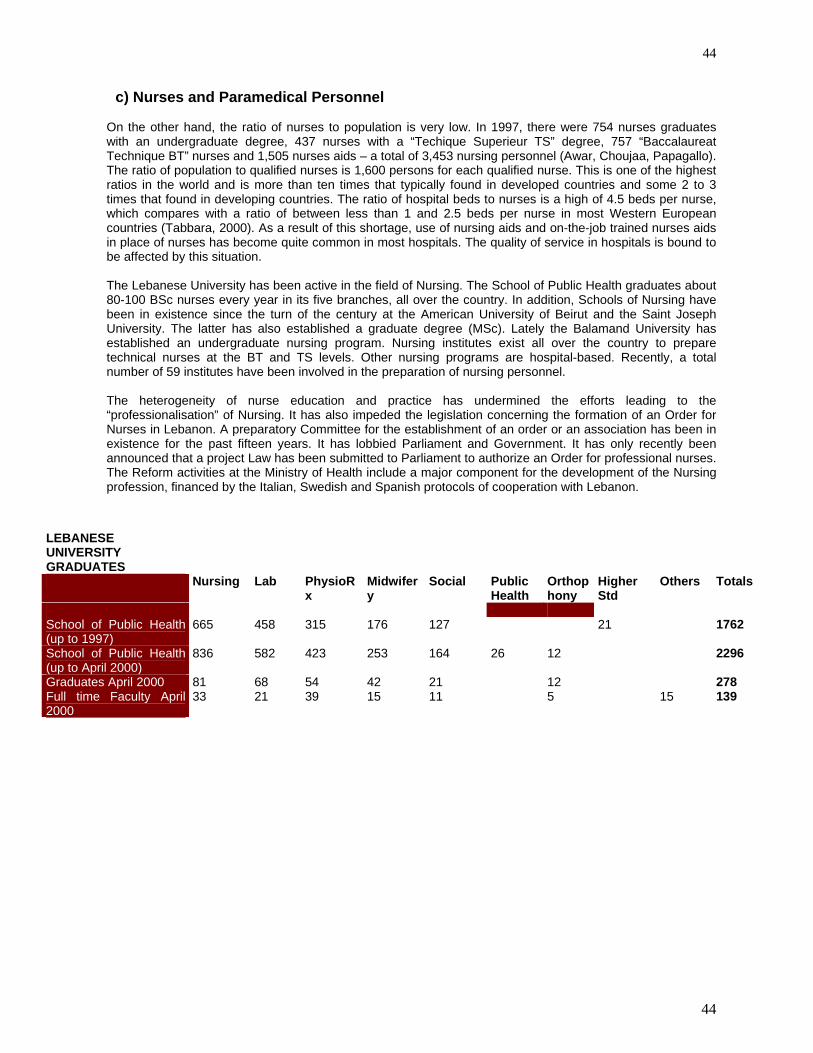

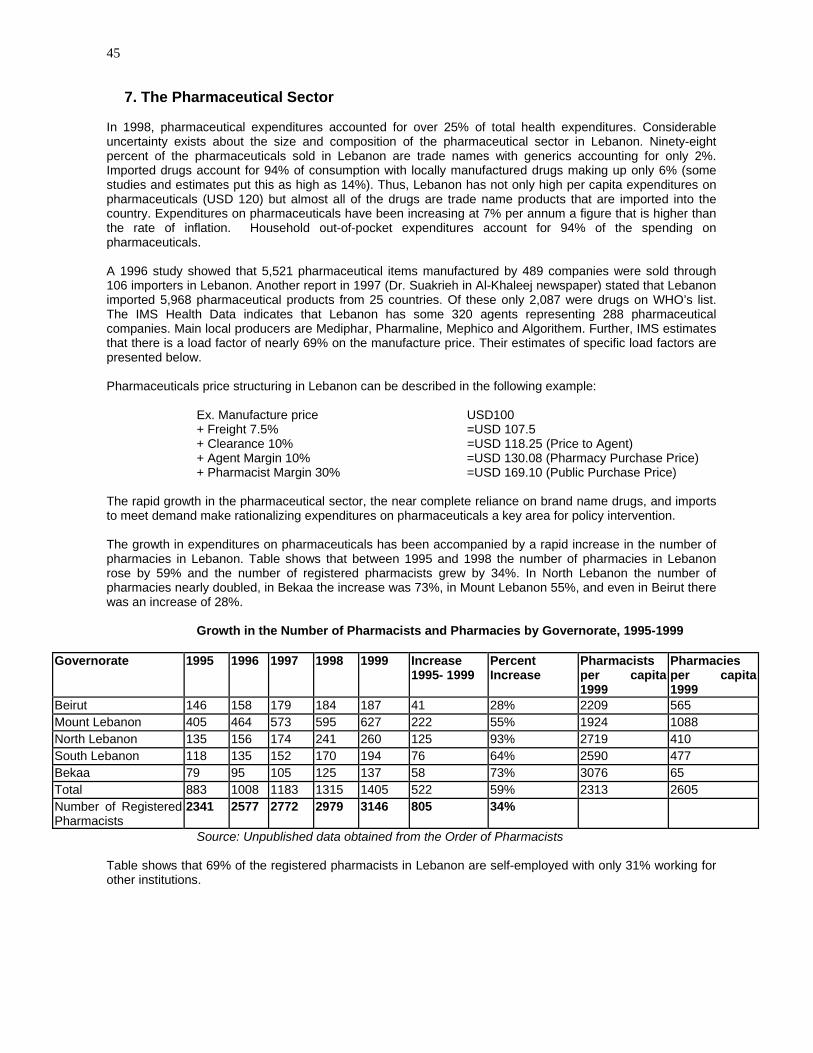

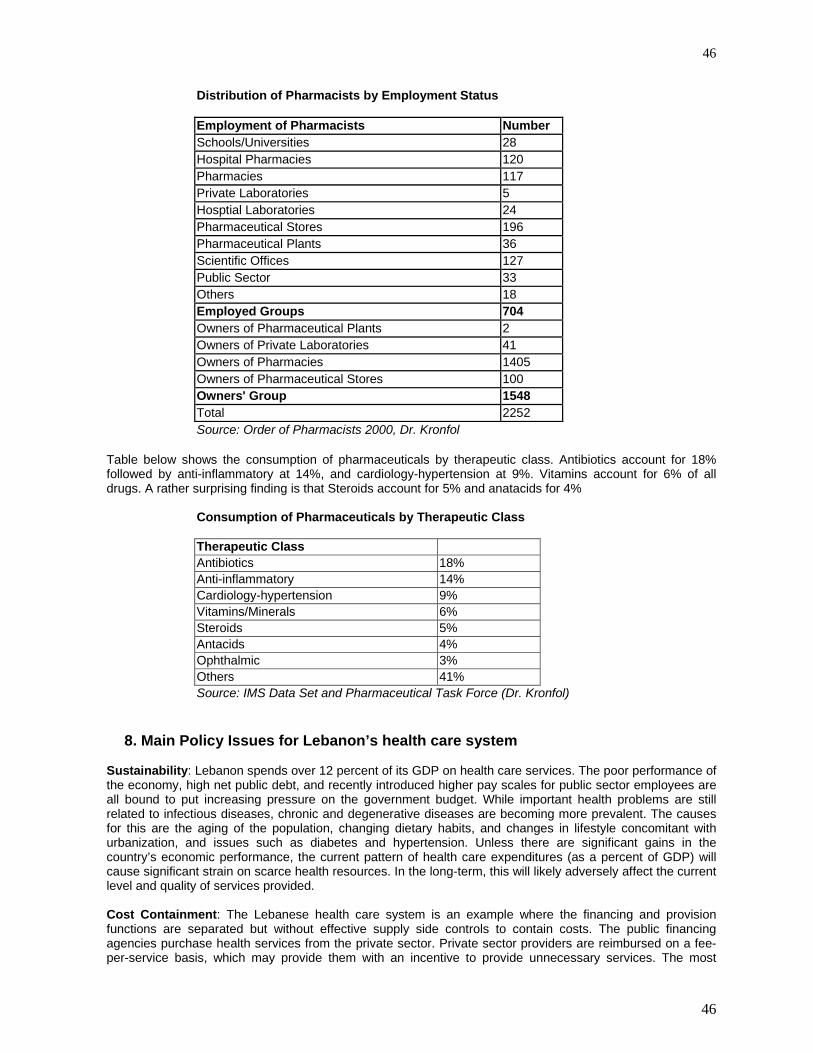

older population and health system: a profile of lebanon · 1 older population and health system: a...

TRANSCRIPT

1

Older Population and Health System: A profile of Lebanon

I. Introduction to Lebanon Lebanon is a middle income country with a population estimated at 4 million over 80% of whom live in urban areas (Central Administration of Census, 1997). Before the civil war, the Lebanese economy was robust, enterprise flourished, and it was the banking center of the Middle East. The civil war, which began in 1975, led to the relocation of many service sectors out of the country, much of the industrial and agricultural infrastructure was destroyed, the economy went into decline (E.I.U. Country Profile, 1992-93). Increased spending on security forces and the reduction in government revenues from taxes and other duties led to a steep increase in public debt. The purpose of this paper is to describe the health care system of Lebanon, analyze its components, highlighting issues that may require attention and that may need to be addressed. This paper has drawn from many studies that have been published or produced in the past few years. Annotation and recognition of the authors have been indicated all through II. Demographic Trends

1. Mortality and Fertility rates

The last population census was carried out in 1932. Recently two major surveys were conducted-- the PAPCHILD survey of 1996 covering 6,000 households and the UNFPA Population and Housing survey of 75,000 households. The latest estimates place the population at four million (Central Administration of Statistics, 1997). Of these, 93% are Lebanese citizens. Twenty-eight percent of the population is under the age of 15 and 10% over age 60. Population has been growing at 1.6 percent per year and Total Fertility Rate is 2.7. Tables below shows that with regard to key health and demographic indicators, Lebanon fares better than most other Middle Eastern countries.

Outcome indicators in selected Middle Eastern countries (1997-98)

Category Egypt Syria Jordan Lebanon 1998 Birth Rate, crude (per 1,000 people)

25 29 31 23.5

Death Rate, crude (per 1,000 people)

7 5 4 6.5

Life expectancy at birth, total (years)

66 69 71 70

Mortality rate, infant (per 1,000 live births)

51 31 29 28

Mortality rate, under-5 (per 1,000 live births)

66 38 35 32

However, there are still significant variations across the geographical regions of the country. A study conducted by UNICEF showed that even though infant and under-five mortality was low for the country as a whole, differences existed among regions. The Bekaa and Northern regions account for most of the under-five mortality. Similarly, in undeserved regions vaccination coverage tends to be lower. The Ministry of Health has initiated targeted campaigns to reduce these disparities. Table below provides some selected demographic and health indicators. It shows steady increases in life expectancy and a steady decline in morality rates. The demographic transition has been accompanied by an

2

2

epidemiological transition. While important health problems are still related to infectious diseases, chronic and degenerative diseases are becoming more prevalent. The causes for this are the aging of the population, changing dietary habits, and changes in lifestyle concomitant with urbanization. Prevalence rates for hypertension and diabetes are on the rise in Lebanon. In addition there are 4,000 – 5,000 new cases of cancer each year. Concerning AIDS, there were 3.1 cases per 100,000 people in 1997.

Selected Outcome Indicators for Lebanon

Series 1980 1990 1993 1994 1995 1996 1997 1999 Life expectancy at birth, female (years)

67 70 - - - - 72 73.9

Life expectancy at birth, male (years)

63 66 - - - - 68 71.7

Life expectancy at birth, total (years)

35 68 - - - - 70 73

Mortality rate, adult, female (per 1,000 female adults)

181 150 - - - - 134

Mortality rate, adult, male (per 1,000 male adults)

241 210 - - - - 177

Mortality rate, infant (per 1,000 live births)

48 36 - - - - 28 26

Mortality rate, under-5(per 1,000 live births)

- 40 - - - - 32

Mortality ratio, maternal(per 100,000 live births)

- 300 - - - - 104

2. Population Structure

a) The Population Pyramid

Source: Household survey 2000

Beirut Beirut suburbs

Rest of Mt Lebanon

North South Nabatieh Beqaa Lebanon

0-4 5.2 7.4 6.4 9.8 8.7 9.8 9 8 5-9 8.6 9.3 7.6 11.7 11.3 11.9 10.2 10 10-14 8.5 9.1 8.1 11.2 11.4 11.4 11.3 10 0-14 22.3 25.8 22.1 32.7 31.4 33.1 30.5 28 15-19 9.1 10.5 8.6 11.4 11.6 10.2 12.1 10.6 20-24 9.8 9.3 9.1 10 9 8.3 10.7 9.5 25-29 8.3 10 9.4 8.1 8.5 7.8 8.7 8.9 30-34 6.8 8.9 8.2 6.7 7.4 7.3 7 7.6 35-39 6.8 7.5 8.9 6.2 7.5 7.4 6.1 7.2

40-44 6.4 6.1 6.4 5 5.7 5.1 5.2 5.7 15-44 47.2 52.3 50.6 47.4 49.7 46.1 49.8 49.5 45-49 5.3 4.7 5.1 4 3.6 3.8 4.3 4.4 50-54 5.2 4.2 4.6 3.5 3.9 3.1 3.7 4 55-59 5 3.3 3.9 3 3.2 2.8 2.8 3.4 60-64 5.1 3.1 3.7 2.7 2.6 3.6 3.1 3.3 45-64 20.6 15.3 17.3 13.2 13.3 13.3 13.9 15.1 65-69 3.4 2.7 3.3 2.5 2.1 2.9 2.2 2.7 > 70 6.2 3.8 6.4 4.2 3.4 4.5 3.7 4.5 > 65 9.6 6.5 9.7 6.7 5.5 7.4 5.9 7.2 Unknown 0.1 0.1 0.2 0.1 0.1 Totals 99.7 99.9 99.7 100 99.9 99.9 100.1 99.8 Number individuals

3494 6350 4581 6420 3844 3592 4367 32648

3

3

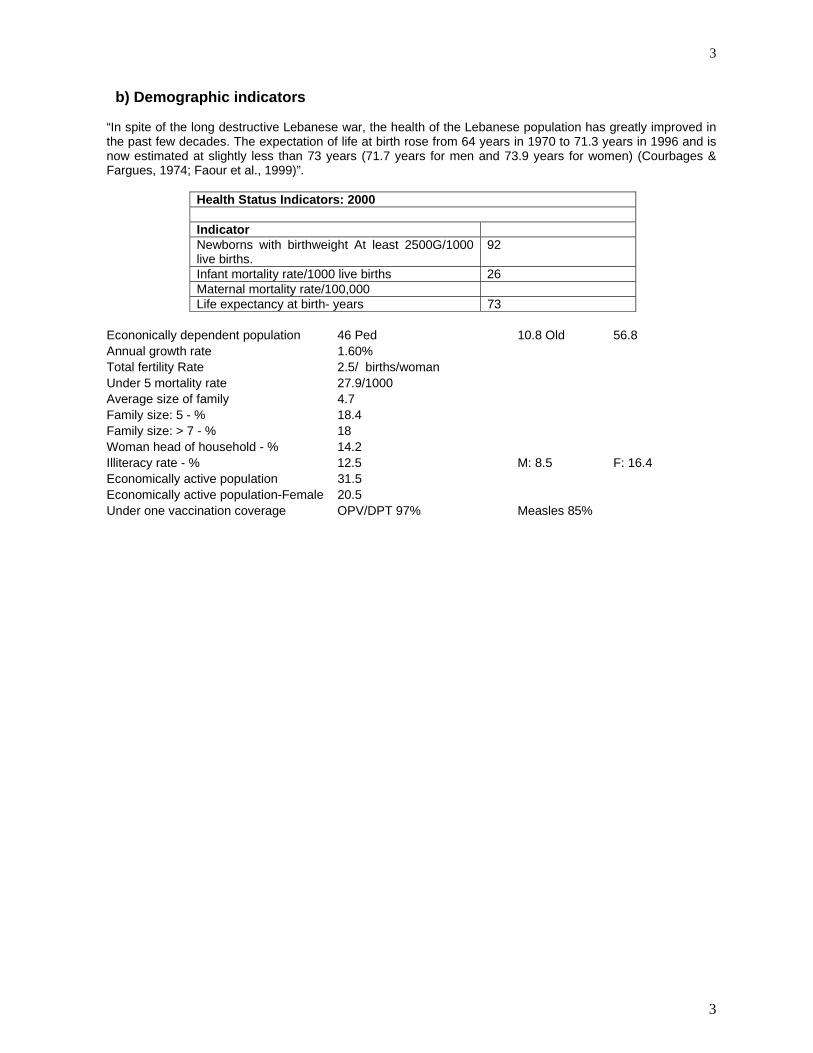

b) Demographic indicators “In spite of the long destructive Lebanese war, the health of the Lebanese population has greatly improved in the past few decades. The expectation of life at birth rose from 64 years in 1970 to 71.3 years in 1996 and is now estimated at slightly less than 73 years (71.7 years for men and 73.9 years for women) (Courbages & Fargues, 1974; Faour et al., 1999)”.

Health Status Indicators: 2000 Indicator Newborns with birthweight At least 2500G/1000 live births.

92

Infant mortality rate/1000 live births 26 Maternal mortality rate/100,000 Life expectancy at birth- years 73

Econonically dependent population 46 Ped 10.8 Old 56.8 Annual growth rate 1.60% Total fertility Rate 2.5/ births/woman Under 5 mortality rate 27.9/1000 Average size of family 4.7 Family size: 5 - % 18.4 Family size: > 7 - % 18 Woman head of household - % 14.2 Illiteracy rate - % 12.5 M: 8.5 F: 16.4 Economically active population 31.5 Economically active population-Female 20.5 Under one vaccination coverage OPV/DPT 97% Measles 85%

4

4

III. 50+ Population: General Assessments A major study, commissioned by the Ministry of Social Affairs, and undertaken by Dr Abla Sibai in September 1998, reviewed the published and unpublished reports concerning the older population. Further analysis was also undertaken of the Population and Housing Survey conducted by the Ministry in 1996. The sample survey of this study was a national probability sample covering the entire regions of Lebanon and consisted of some 70,000 households (10% of the estimated population). The current study abstracted the records of all individuals above the age of 60 years at the time of the survey. The following tables summarize the main findings, about this important section of the Lebanese population. It is worth noting that the very old (80 years and above) account for 10.6% of the old population among males and 12.1% among women. This is in accord with the literature whereby women are expected to live longer than men. The subgroup 60-64 years old Men in that age group were in their majority married (91.3%). More than two thirds were still working (68.3%): only 11.6% had retired. Almost half had completed only primary education, while 6% had finished university studies. Almost half were employees. More than 4/5th live in an apartment., that 70% of them actually own. Unlike men, less than 2/3rd of the women were still married in that age group: 28% had become widows. Almost 60% were illiterate and a little more than 1% had completed university. 90% of women were housewives at home. When employed, three quarters of women tended to be employees. Like men, most women lived in apartments that most of them actually owned. The subgroup 65-74 years old Men were still in their majority married. However only 43% were still working, while 20% had retired. When working, two thirds were self employed. Again most of men lived in apartments that thye entirely owned. Less than half of women were still married by the age of 75 years. 60% had become widows. The older age groups Even above 80 years, two thirds of men were still married, as compared to only 17% of women. Only 20% were still working, mainly in their own business.

5

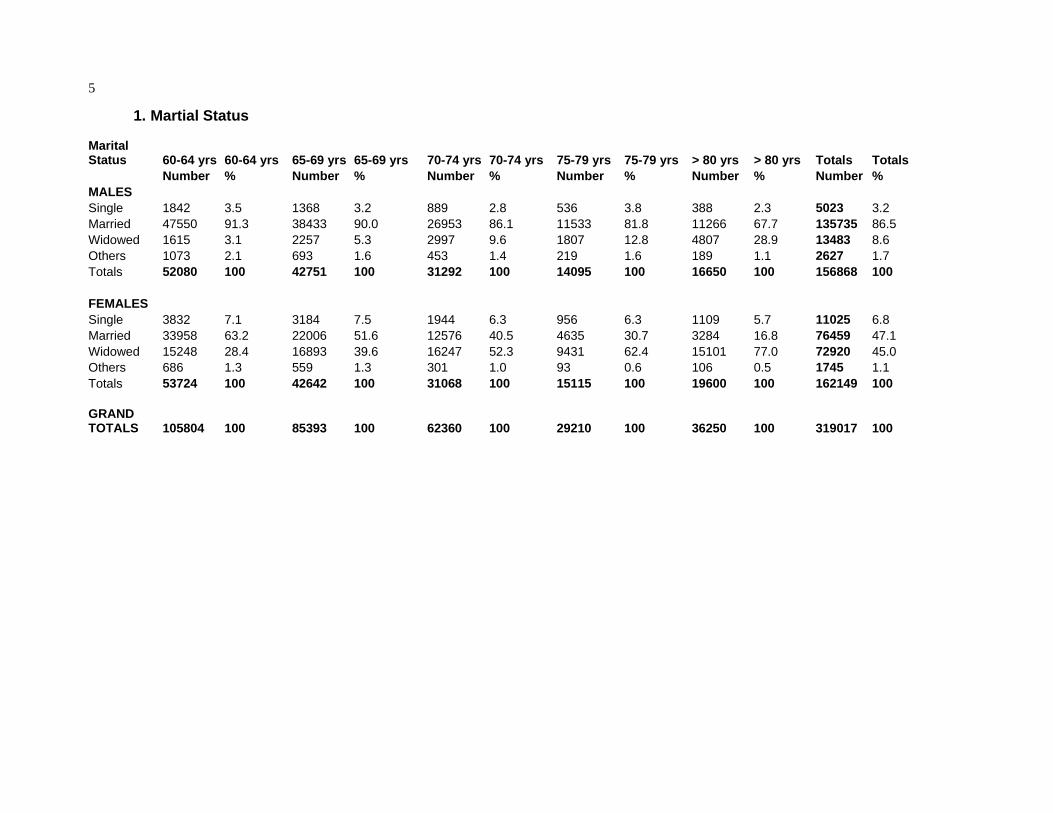

1. Martial Status

Marital Status 60-64 yrs 60-64 yrs 65-69 yrs 65-69 yrs 70-74 yrs 70-74 yrs 75-79 yrs 75-79 yrs > 80 yrs > 80 yrs Totals Totals Number % Number % Number % Number % Number % Number % MALES Single 1842 3.5 1368 3.2 889 2.8 536 3.8 388 2.3 5023 3.2 Married 47550 91.3 38433 90.0 26953 86.1 11533 81.8 11266 67.7 135735 86.5 Widowed 1615 3.1 2257 5.3 2997 9.6 1807 12.8 4807 28.9 13483 8.6 Others 1073 2.1 693 1.6 453 1.4 219 1.6 189 1.1 2627 1.7 Totals 52080 100 42751 100 31292 100 14095 100 16650 100 156868 100 FEMALES Single 3832 7.1 3184 7.5 1944 6.3 956 6.3 1109 5.7 11025 6.8 Married 33958 63.2 22006 51.6 12576 40.5 4635 30.7 3284 16.8 76459 47.1 Widowed 15248 28.4 16893 39.6 16247 52.3 9431 62.4 15101 77.0 72920 45.0 Others 686 1.3 559 1.3 301 1.0 93 0.6 106 0.5 1745 1.1 Totals 53724 100 42642 100 31068 100 15115 100 19600 100 162149 100 GRAND TOTALS 105804 100 85393 100 62360 100 29210 100 36250 100 319017 100

6

6

2. Working Status

Working status 60-64 60-64 65-74 65-74 > 75 yrs > 75 yrs Totals Totals Number % Number % Number % Number % MALES Working status 35567 68.3 32154 43.4 5952 19.4 73673 46.9 Home Based worker 293 0.6 346 0.5 160 0.5 799 0.5 Self-sufficient 3921 7.5 10500 14.2 7023 22.8 21444 13.7 Unemployed 1652 3.2 2791 3.8 906 2.9 5349 3.4 Retired 6037 11.6 15424 20.8 6603 21.5 28064 17.9 Others 4632 8.9 12848 17.3 10110 32.9 27590 17.6 Totals 52102 100 74063 100 30754 100 156919 100 FEMALES Working status 3603 6.7 2036 2.8 327 0.9 5966 3.7 Home Based worker 512 1.0 558 0.8 77 0.2 1147 0.7 Self-sufficient 566 1.1 1526 2.1 942 2.7 3034 1.9 Unemployed 85 0.2 85 0.1 58 0.2 228 0.1 Retired 298 0.6 591 0.8 311 0.9 1200 0.7 Housewife 48373 90.0 68087 92.3 31452 90.5 147912 91.2 Others 319 0.6 847 1.1 1570 4.5 2736 1.7 Totals 53756 100 73730 100 34737 100 162223 100 GRAND TOTALS 105858 100 147793 100 65491 100 319142 100

Employment status 60-64 60-64 65-74 65-74 > 75 yrs > 75 yrs Totals Totals Number % Number % Number % Number % MALES Self-employed 19174 52.1 22551 64.0 5153 73.6 46878 59.3 Employee 17613 47.9 12668 36.0 1845 26.4 32126 40.7 Totals 36787 100 35219 100 6998 100 79004 100 FEMALES Self-employed 1106 26.4 952 35.6 218 47.1 2276 31.1 Employee 3082 73.6 1725 64.4 245 52.9 5052 68.9 Totals 4188 100 2677 100 463 100 7328 100 GRAND TOTALS 40975 100 37896 100 7461 100 86332 100

7

7

After the pediatric age group (above 15 years), between 3-4.5 % of the older population was unemployed even at their advancing age. The overall unemployment was 9.4% for the population between 15-64 years. In the older brackets, only men were employed in the labor market.

Unemployment by age and sex - Per cent Source: Household survey 2000 Males Females Totals 15-19 31.5 41.7 33.5 20-24 19.4 19.3 19.3 25-29 8 13 9.6 30-34 5.4 9 6.4 35-39 3.3 9.5 5 40-44 3.4 5.4 3.9 45-49 3.4 2.1 3.1 50-54 4.5 1.7 4.1 55-59 5.1 1.3 4.5 60-64 4.5 4 65-69 3.9 3.5 > 70 3.3 3 15-64 years 8.6 11.6 9.4 Number individuals 7789 2717 10506

8

8

3. Educational levels by age group

Educational level 60-74 years 60-74 years Above 75 yrsAbove 75 yrs Total Total

Number % Number % Number % MALES Illiterate 36879 29.2 12471 40.5 49350 31.4 Informal/Primary 63015 49.9 13619 44.3 76634 48.8 Intermediate/Secondary 18681 14.8 3273 10.6 21954 14.0 University/Higher Studies 7591 6.0 1392 4.5 8983 5.7 Totals 126166 100 30755 100 156921 100 FEMALES Illiterate 72080 56.5 24657 71.0 96737 59.6 Informal/Primary 39276 30.8 7733 22.3 47009 29.0 Intermediate/Secondary 14531 11.4 2134 6.1 16665 10.3 University/Higher Studies 1598 1.3 213 0.6 1811 1.1 Totals 127485 100 34737 100 162222 100 GRAND TOTALS 253651 100 65492 100 319143 100

9

9

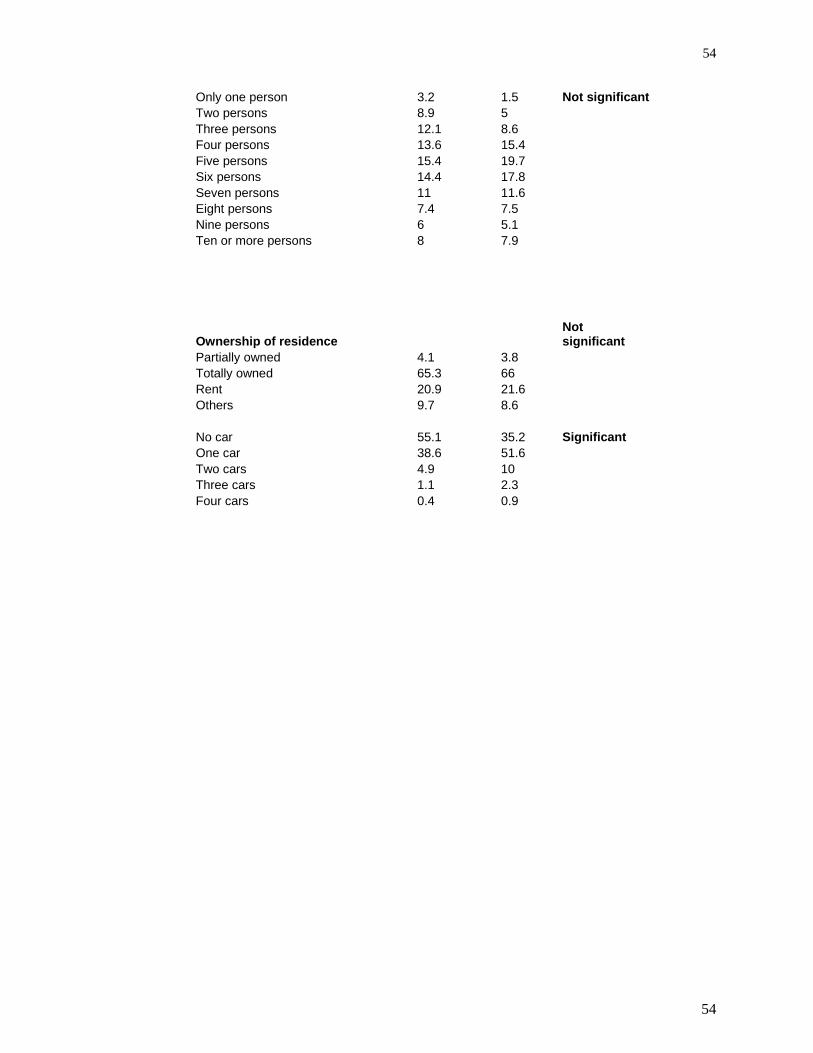

4. Housing and living arrangements

Type of residence 60-74 60-74 > 75 yrs > 75 yrs Totals Totals Number % Number % Number % MALES Independent residence 27185 21.5 8594 27.9 35779 22.8 Apartment in a building 98763 78.3 22130 72.0 120893 77.0 Shack 124 0.1 20 0.1 144 0.09 Others 93 0.1 10 0.03 103 0.07 Totals 126165 100 30754 100 156919 100 FEMALES Independent residence 27024 21.2 9617 27.7 36641 22.6 Apartment in a building 100193 78.5 25059 72.1 125252 77.2 Shack 144 0.1 61 0.2 205 0.1 Others 215 0.2 0 0 215 0.1 Totals 127576 100 34737 100 162313 100 GRAND TOTALS 253741 100 65491 100 319232 100

Ownership of residence 60-74 60-74 > 75 yrs > 75 yrs Totals Totals Number % Number % Number % MALES Entirely owned 87897 69.7 22481 73.1 110378 70.3 Partially owned 2205 1.7 668 2.2 2873 1.8 Rented 28779 22.8 5942 19.3 34721 22.1 Others 7285 5.8 1664 5.4 8949 5.7 Totals 126166 100 30755 100 156921 100 FEMALES Entirely owned 84427 66.2 23780 68.5 108207 66.7 Partially owned 3272 2.6 1220 3.5 4492 2.8 Rented 31692 24.9 7017 20.2 38709 23.9 Others 8095 6.3 2720 7.8 10815 6.7 Totals 127486 100 34737 100 162223 100 GRAND TOTALS 253652 100 65492 100 319144 100

10

IV. 50+ Population Health Indicators 1. Health Wellness and illness In the National household health survey, the percent of the older population in the representative sample of the entire Lebanese population was 10.5% for the population above 60 years of age. This survey was conducted in 1998 and released in December 2000. The proportion of the tranche above 65 years was 7.2%. Almost one third of the above 60 years old perceived their health status to be poor, as compared to 6.7% for the entire population. It should be cautioned however that the unknown responses in that age group was higher than 40.8%! Perception of health wellness Source: Household survey 2000 Poor Average Good Very Good Excellent Unknown Sample < 5 years 1.8 5.6 30.8 32.9 28.7 0.3 2635 5-14 1.8 6.2 30.5 33.4 27.8 0.3 6535 15-59 4.5 16.7 36.1 25.4 14.6 2.6 19959 > 60 32.5 38.7 21.6 4.2 1.6 1.5 3501 Not determined 11 22.8 25.4 40.8 18 Overall 6.7 16 33 25.4 17 1.9 32648 When asked whether they have suffered from an illness or injury, in the past month, close to two thirds of the older population responded that they were fine and healthy (as compared to 73% of the general public). This rate did not increase appreciably between the age of 60 and 70 years.

Suffered illness or injury in past month Source: Household survey 2000 Males Females Totals Sample Has had Has had Has had Anterior Unknown illness accident both illness 0-4 41.6 38.1 39.9 2635 39 0.8 0 0 0.2 5-9 29.5 31.1 30.3 3268 10-14 22.1 23.5 22.8 3267 25.2 1.1 0.1 0.2 0.2 15-19 19.5 23.9 21.7 3413 20-24 20.9 25.6 23.2 3108 25-29 22.3 28 25.2 2872 30-34 24.1 31.4 28.1 2466 35-39 27.3 31.7 29.7 2352 40-44 27.8 36 32.3 1861 45-49 27.9 38.3 33.5 1445 50-54 29.5 44.4 37.3 1320 55-59 31.5 44.3 37.9 1122 26.4 1.1 0.2 0.3 2.6 60-64 35.1 46.9 41.2 1104 65-69 36.2 48.9 42.7 897 70 above 41.1 47.9 44.4 1500 41.2 1.1 0.2 0.5 1.4 Unknown 16.6 11 18 Total 27.4 32.9 30.2 32648 28.7 1.1 0.1 0.2 1.8

11

11

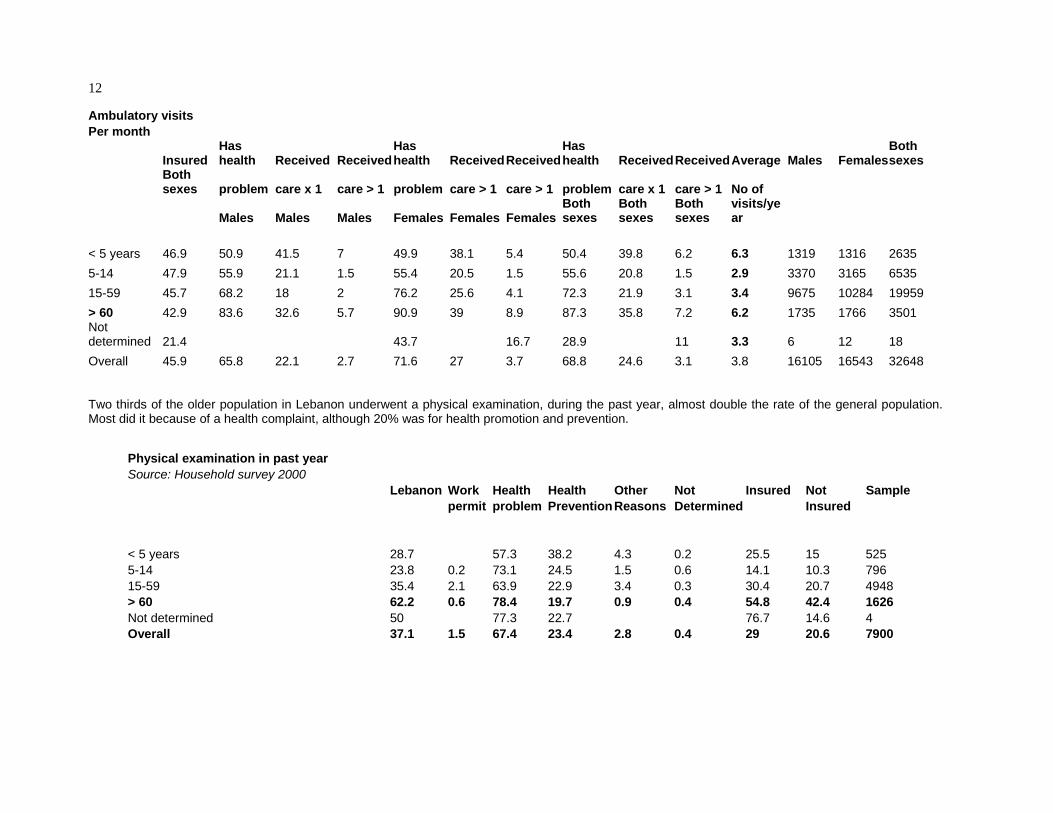

The information in the table below has been accumulated from several questions within the household survey. In the first place, 43% of the above 60 years old are insured in Lebanon. This is the average for the general population. It should not be surpising since most of the insurance coverage (public providers) cover individuals and dependents, including parents. Some may still be covered because of employment status, as noted earlier. Close to 84% of men and 91% of women (above 60 years) indicated that they have a health problem. However only 32.6% of men and 39% of women sought care for this health problem, i.e. only 30-40% of this age group seek attention to a health problem, at least once during the past month. A small proportion (5.7% of men) and 8.9% of women sought medical care more than once per month for these health problems. However it is important to retain that the population above the age of 60 years scores a visit rate of 6.2 visits per person per year to the ambulatory health facilities, almost double the national average. .

12

Ambulatory visits Per month

Insured Has health Received Received

Has health Received Received

Has health Received ReceivedAverage Males Females

Both sexes

Both sexes problem care x 1 care > 1 problem care > 1 care > 1 problem care x 1 care > 1 No of

Males Males Males Females Females FemalesBoth sexes

Both sexes

Both sexes

visits/year

< 5 years 46.9 50.9 41.5 7 49.9 38.1 5.4 50.4 39.8 6.2 6.3 1319 1316 2635 5-14 47.9 55.9 21.1 1.5 55.4 20.5 1.5 55.6 20.8 1.5 2.9 3370 3165 6535 15-59 45.7 68.2 18 2 76.2 25.6 4.1 72.3 21.9 3.1 3.4 9675 10284 19959 > 60 42.9 83.6 32.6 5.7 90.9 39 8.9 87.3 35.8 7.2 6.2 1735 1766 3501 Not determined 21.4 43.7 16.7 28.9 11 3.3 6 12 18 Overall 45.9 65.8 22.1 2.7 71.6 27 3.7 68.8 24.6 3.1 3.8 16105 16543 32648 Two thirds of the older population in Lebanon underwent a physical examination, during the past year, almost double the rate of the general population. Most did it because of a health complaint, although 20% was for health promotion and prevention.

Physical examination in past year Source: Household survey 2000 Lebanon Work Health Health Other Not Insured Not Sample permit problem Prevention Reasons Determined Insured < 5 years 28.7 57.3 38.2 4.3 0.2 25.5 15 525 5-14 23.8 0.2 73.1 24.5 1.5 0.6 14.1 10.3 796 15-59 35.4 2.1 63.9 22.9 3.4 0.3 30.4 20.7 4948 > 60 62.2 0.6 78.4 19.7 0.9 0.4 54.8 42.4 1626 Not determined 50 77.3 22.7 76.7 14.6 4 Overall 37.1 1.5 67.4 23.4 2.8 0.4 29 20.6 7900

13

2. Chronic illnesses This poor perception of wellness was confirmed when close to 75% of men of this age bracket (above 60 years) declared at least one chronic illness (men) and 84.2% of women. Chronic illnesses Source: Household survey 2000

Declared at Declared at Declared atSample size

Sample size Sample size

least 1 dis least 1 dis least 1 dis Males Females Both sexes Males Females Both sexes < 5 years 10.4 8 9.2 1319 1316 2635 5-14 14.8 12.8 13.8 3370 3165 6535 15-59 29.1 38.3 33.8 9675 10284 19959 > 60 73.4 84.2 78.9 1735 1766 3501 Not determined 16.6 11 6 12 18 Overall 29.3 35.8 32.6 16105 16543 32648 3. Risk factors for non-communicabe diseases The National health household survey attempted to seek information on lifestyles. Smoking was used as one indicator. It was found that 26% of the Lebanese population above the age of 15 years did smoke. The population above the age of 60 years tended to be on the higher side of smokers: 30% between the ages of 60-70 years and 16% at a more advanced age.

Smoking Source: Household survey 2000 Smoker Smoker Smoker Sample

Males Females Both sexes

15-19 6.3 1.8 4.1 3413 20-24 20.1 6.3 13.4 3108 25-29 32.9 11.7 22.2 2871 30-34 43.5 22.8 32.2 2466 35-39 48.2 29.6 38.2 2352 40-44 51 32.4 41 1861 45-49 57 34.3 44.8 1445 50-54 46.8 31.9 39 1320 55-59 50.3 25.6 37.9 1122 60-64 42.4 19.2 30.4 1104 65-69 38.3 18.8 28.4 897 70 above 21.7 10.2 16 1500 Unknown 18 Total 33.7 18.3 25.8 Sample 11415 12062 23477 23477

14

14

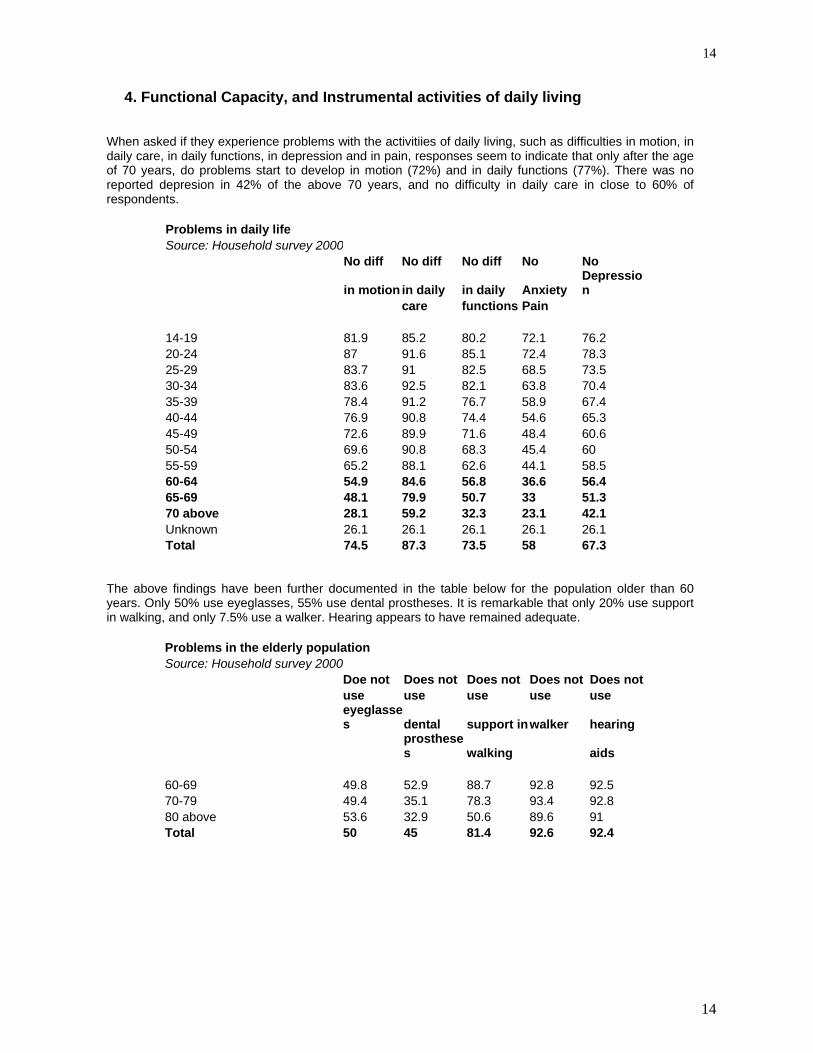

4. Functional Capacity, and Instrumental activities of daily living When asked if they experience problems with the activitiies of daily living, such as difficulties in motion, in daily care, in daily functions, in depression and in pain, responses seem to indicate that only after the age of 70 years, do problems start to develop in motion (72%) and in daily functions (77%). There was no reported depresion in 42% of the above 70 years, and no difficulty in daily care in close to 60% of respondents.

Problems in daily life Source: Household survey 2000 No diff No diff No diff No No

in motion in daily in daily Anxiety Depression

care functions Pain 14-19 81.9 85.2 80.2 72.1 76.2 20-24 87 91.6 85.1 72.4 78.3 25-29 83.7 91 82.5 68.5 73.5 30-34 83.6 92.5 82.1 63.8 70.4 35-39 78.4 91.2 76.7 58.9 67.4 40-44 76.9 90.8 74.4 54.6 65.3 45-49 72.6 89.9 71.6 48.4 60.6 50-54 69.6 90.8 68.3 45.4 60 55-59 65.2 88.1 62.6 44.1 58.5 60-64 54.9 84.6 56.8 36.6 56.4 65-69 48.1 79.9 50.7 33 51.3 70 above 28.1 59.2 32.3 23.1 42.1 Unknown 26.1 26.1 26.1 26.1 26.1 Total 74.5 87.3 73.5 58 67.3

The above findings have been further documented in the table below for the population older than 60 years. Only 50% use eyeglasses, 55% use dental prostheses. It is remarkable that only 20% use support in walking, and only 7.5% use a walker. Hearing appears to have remained adequate.

Problems in the elderly population Source: Household survey 2000 Doe not Does not Does not Does not Does not use use use use use

eyeglasses dental support inwalker hearing

prostheses walking aids

60-69 49.8 52.9 88.7 92.8 92.5 70-79 49.4 35.1 78.3 93.4 92.8 80 above 53.6 32.9 50.6 89.6 91 Total 50 45 81.4 92.6 92.4

15

15

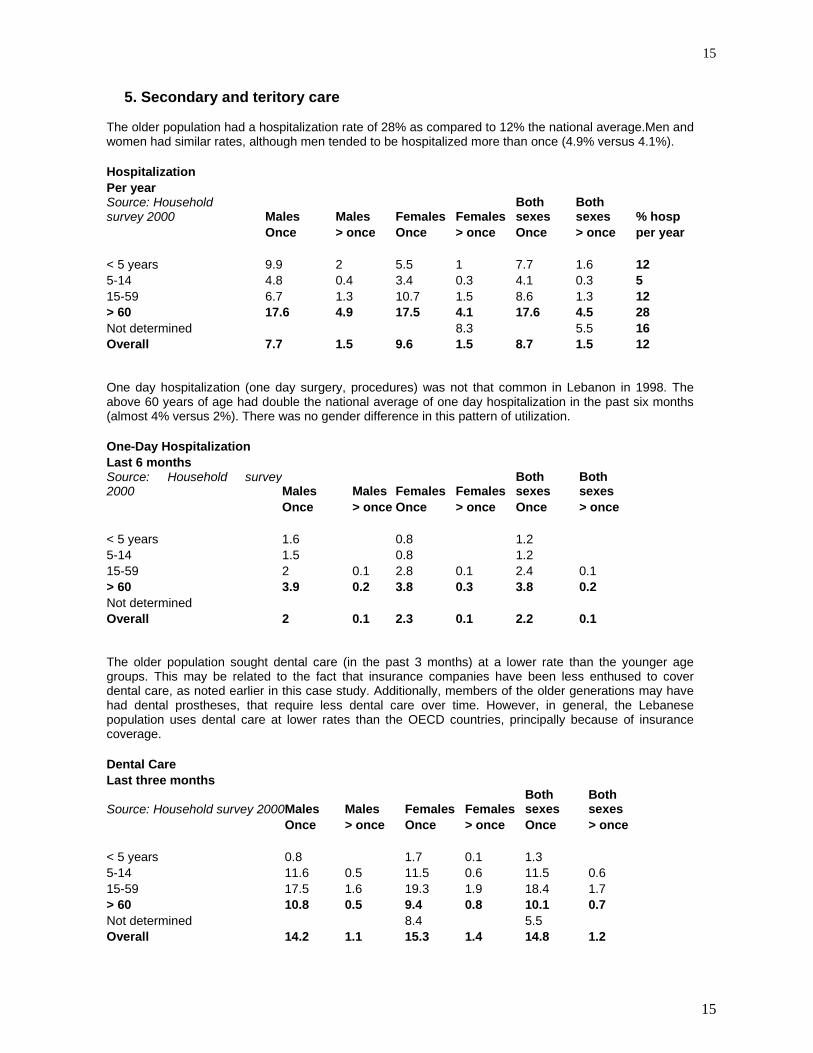

5. Secondary and teritory care The older population had a hospitalization rate of 28% as compared to 12% the national average.Men and women had similar rates, although men tended to be hospitalized more than once (4.9% versus 4.1%). Hospitalization Per year Source: Household survey 2000 Males Males Females Females

Both sexes

Both sexes % hosp

Once > once Once > once Once > once per year < 5 years 9.9 2 5.5 1 7.7 1.6 12 5-14 4.8 0.4 3.4 0.3 4.1 0.3 5 15-59 6.7 1.3 10.7 1.5 8.6 1.3 12 > 60 17.6 4.9 17.5 4.1 17.6 4.5 28 Not determined 8.3 5.5 16 Overall 7.7 1.5 9.6 1.5 8.7 1.5 12 One day hospitalization (one day surgery, procedures) was not that common in Lebanon in 1998. The above 60 years of age had double the national average of one day hospitalization in the past six months (almost 4% versus 2%). There was no gender difference in this pattern of utilization. One-Day Hospitalization Last 6 months Source: Household survey2000 Males Males Females Females

Both sexes

Both sexes

Once > once Once > once Once > once < 5 years 1.6 0.8 1.2 5-14 1.5 0.8 1.2 15-59 2 0.1 2.8 0.1 2.4 0.1 > 60 3.9 0.2 3.8 0.3 3.8 0.2 Not determined Overall 2 0.1 2.3 0.1 2.2 0.1 The older population sought dental care (in the past 3 months) at a lower rate than the younger age groups. This may be related to the fact that insurance companies have been less enthused to cover dental care, as noted earlier in this case study. Additionally, members of the older generations may have had dental prostheses, that require less dental care over time. However, in general, the Lebanese population uses dental care at lower rates than the OECD countries, principally because of insurance coverage. Dental Care Last three months

Source: Household survey 2000 Males Males Females Females Both sexes

Both sexes

Once > once Once > once Once > once < 5 years 0.8 1.7 0.1 1.3 5-14 11.6 0.5 11.5 0.6 11.5 0.6 15-59 17.5 1.6 19.3 1.9 18.4 1.7 > 60 10.8 0.5 9.4 0.8 10.1 0.7 Not determined 8.4 5.5 Overall 14.2 1.1 15.3 1.4 14.8 1.2

16

16

The utilization of ambulatory services (visits last month), dental visits (last 3 months), hospitalizations (last year), one day hospitalization (last six months) were compared to identify differences in utilization due to insurance status. Most of the parameters did not change appreciably except perhaps for hospitalization (19.4 versus 16.6% and 5.8% versus 3.6%). As we had noted earlier, the older population is insured to the same tune as the rest of the population (about 50%), while the other half accesses the medical faciliites of the Ministry of Health, the insurance of last resort for the uninsured.

Utilization of medical care and Insurance Status Ambulatory Ambulatory Ambulatory Ambulatory Dental care Dental care Dental care Dental care Visits x 1 Visits > 1 Visits x 1 Visits > 1 Once More than 1 Once More than 1 Insured Insured Not insured Not insured Insured Insured Not insuredNot insured < 5 years 40.1 7.7 39.7 4.9 1.5 1 0.1 5-14 years 22 1.5 19.8 1.4 12.7 0.9 10.5 0.3 15-59 years 23 3.6 22.1 2.8 19.9 1.8 18 1.8 > 60 years 37.3 7.7 35.6 7.3 10.2 0.7 10.2 0.7 Not determined 25.6 14.6 14.6 Overall 25.6 3.9 24.6 3.3 15.9 1.3 14.3 1.2 Hospital Hospital Hospital Hospital Hospital Hospital Hospital Hospital admit x 1 admit > 1 admit x 1 admit > 1 Day x 1 Day > 1 Day x 1 Day > 1 Insured Insured Not insured Not insured Insured Insured Not insuredNot insured < 5 years 9.8 2.1 5.8 1.1 0.9 1.4 5-14 years 4.3 0.5 4 0.3 1.2 1.1 15-59 years 10.1 1.8 8 1.1 2.7 0.1 2.3 0.1 > 60 years 19.4 5.8 16.6 3.6 4 0.3 3.8 0.2 Not determined 25.6 Overall 9.7 1.9 8 1.2 2.3 0.1 2.1 0.1

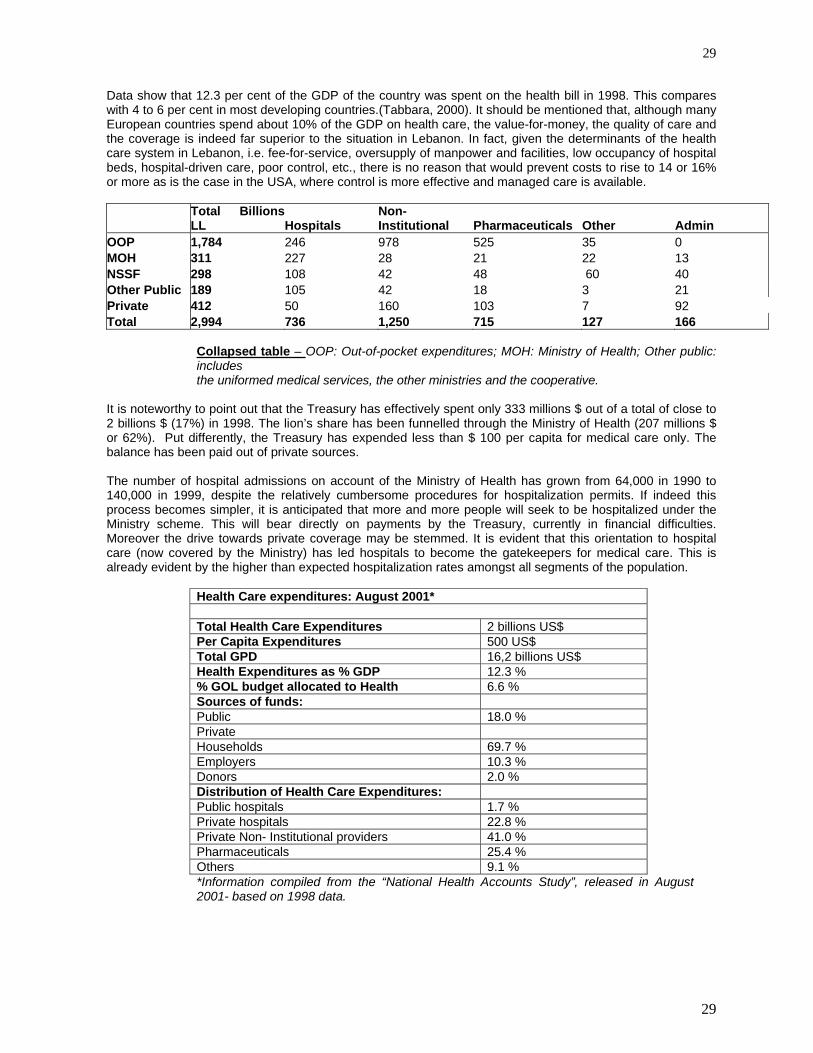

As indicated earlier in this case study for Lebanon, the overall health care bill amounted in 1998 to 2,994,000 billions LL or close to 2 billions $. Of this amount, 1,785 billions were spent out-of-pocket, 311 billions was expended by the Ministry of Health, 297 billions by the National Social Security Fund, all the other public funds spent 189 billions, while private insurance spent 412 billions. Each of these parties allocated these sums to hospital care, outpatient care, pharmaceuticals, other expenses and administration, as shown in the table below, that has been adapted from the National Health Accounts study for Lebanon 1998, released in December 2000.

Total Hospitals Non-Institutional Pharmaceuticals Other Admin

OOP 1,785 246 978 525 35 0 MOH 311 227 28 21 22 13 NSSF 297 108 42 48 60 40 Other Public 189 105 42 18 3 21 Private Ins. 412 50 160 103 7 92 Total 2,994 735 1,250 715 128 166

The population over the age of 65 years had a health care bill of 426 billions LL (284 millions $), of which 251 (167 millions $) were out-of-pocket expenditures.

17

17

Age 65 and Over Subset

Total Hospitals Non-InstitutionalPharmaceuticals Other Admin OOP 251 49 127 71 5 0 MOH 56 44 4 3 3 2 NSSF 41 19 5 5 7 5 Other Public 28 18 5 2 0 3 Private Ins. 50 9 18 12 1 11 Total 426 138 158 93 16 22

Insured 65+

Total Hospitals Non-Institutional Pharmaceuticals Other Admin

OOP 65 8 44 12 1 0 MOH 15 14 0 0 0 1 NSSF 41 19 5 5 7 5 Other Public 28 18 5 2 0 3 Private Ins. 50 9 18 12 1 11 Total 199 67 71 31 9 20 Uninsured 65+

Total Hospitals Non-Institutional Pharmaceuticals Other Admin

OOP 186 40 83 59 4 0 MOH 42 30 4 3 3 2 NSSF 0 0 0 0 0 0 Other Public 0 0 0 0 0 0 Private Ins. 0 0 0 0 0 0 Total 228 71 87 62 7 2

This sum (426 billions LL), was spent as follows: 199 billions LL by the insured above the age of 65 years, and 228 by the uninsured in that same age group, as detailed in the two tables above.

Future Law Profile Matrix for Total NSSF coverage of Population

Total Hospitals Non-Institutional Pharmaceuticals Other Admin

OOP 1,491 169 855 430 37 0 MOH 218 160 19 16 14 9 NSSF 297 108 42 48 60 40 Other Public 189 105 42 18 3 21 Private Ins. 247 30 96 62 4 55 New Plan 875 155 323 266 13 118 Total 3,317 726 1,377 840 131 242

If the National Social Security were to become universal and cover all the Lebanese population, actuarial studies indicated that the overall health care bill would increase to 3,317 billions LL or 2.211 billions $, an increase of 10.6%. The population over the age of 65 years, that would now become insured in its totality, was expected to consume 632 billions LL or 421 millions $, i.e. about 1,460 $ per person above the age of 65 years per year, for all medical expenditures..

18

18

V. Health Care System of Lebanon 1. Historical review of Health Care system The issues and difficulties facing the health care system (HCS) are not new, and they precede the civil disturbances of the last two decades. They emanate from an attitude of “laissez-faire” that had characterized most sectors since the country achieved its independence in 1943. Lebanon’s health sector until 1958 had followed the international trends that had prevailed in the first half of the twentieth century. Initially, at the turn of that century, the State had focused primarily on promulgating legislation to protect Society against health ills, that were then predominantly infectious diseases. Thus, the quarantine system was established, laws governing water supply and sewage disposal were promulgated, and dispensaries for the poor and facilities to house the contagious patients and the mental patients were built and managed by the State. Medical care, that was not as sophisticated then, was entrusted to the charitable, religious and community groups, often with support from the Government. Private practice and facilities started in the twenties, patterned on the French model since Lebanon was then under the mandate of France. Physicians who had trained and specialized primarily in Europe returned and opened small facilities to treat their inpatients, within their specialty. Medical education, and indeed the preparation of health manpower, was confined to the two prestigious foreign universities: the American University of Beirut (since 1866) and the Saint Joseph University (since 1877). Both were and continue to be centers for excellence in health profession education. One should note nevertheless that the two universities were educating then for the entire region (including Palestine) since few educational facilities existed in the Region (except for Egypt, Syria and Iraq). Thus the output of its Lebanese graduates was small, elitist and selective. In the first fifteen years of independence (1943-1958), the State built a network of regional, district and rural hospitals, all within a referral system, to provide care, for essentially the under-privileged. Patients were then required to attest to their financial need to be admitted for care. This regulation (that had continued from the earlier days, impacted negatively on the Government facilities, since it stigmatized the users within their community, as being in need. Although this regulation was discontinued in 1970, the perception remained and languished. The ethos of care by the Government was “paternalistic”, a favor to the less privileged. After a relatively benign civil disturbance in 1958 (if compared to the latter one in 1975), the Government attempted major reforms in all sectors. In a sense, Lebanon adapted the trends that prevailed in the world after the end of the second world war. In the health sector, these reforms were quite advanced even when compared with more developed countries. Social development with community participation, primary health care principles, were actively encouraged and institutionalized. The National Social Security Fund was established in 1964, to insure social programs in Maternity, Medical Care (1971), Occupational accidents, end-of-service indemnities, family allowances, for its enrollees and their dependents. The Cooperative of the Civil Servants was also established four months later, as a temporary institution, to cover the civil servants (until the NSSF had time to extend its programs). The Government was moving into the vision of health care as a human right, provided in a spirit of solidarity amongst the different strata of the population. The civil disturbances that had started in 1975 had a major negative impact on the public health care system. The state facilities were often at dangerous sites of the country, and were in their majority destroyed, looted or deserted. The staff found difficulty in reaching their work station. The centralization of the Ministry of Health had prevented the smooth flow of supplies, pharmaceuticals, systems, manpower and regulations. To provide care for the traumatized population, the Government relied on the private sector. Before the war, in 1970, only 10% of the Ministry budget used to be expended on the care of its patients in private facilities, principally for advanced care that was not available in the public hospitals. This budget line provided the ready opportunity for the treatment of patients during the war. Of all sectors in the economy, none flourished as much as the private health sector during the past two decades. However, no one denies the extent that the private hospital sector assisted in the provision of care, under duress, during that long period of strife. It is to be noted that these incentives expanded the private sector to areas of the country that were until then under-served. Just before the civil strife and all through that crisis, the preparation of physicians was accelerated in Lebanon as well as in the Region. This is attributed to the social and economic preeminence of physicians in Society (and also as a sure way to climb the social and political ladder). The Lebanese University had been established in 1954 ; in addition, scores of Lebanese left for medical education abroad, on grants and fellowships provided by friendly governments, often from the former Soviet Union and Arab countries. The numbers, quality, preparation, background, homogeneity of the medical corps began to change drastically.

19

19

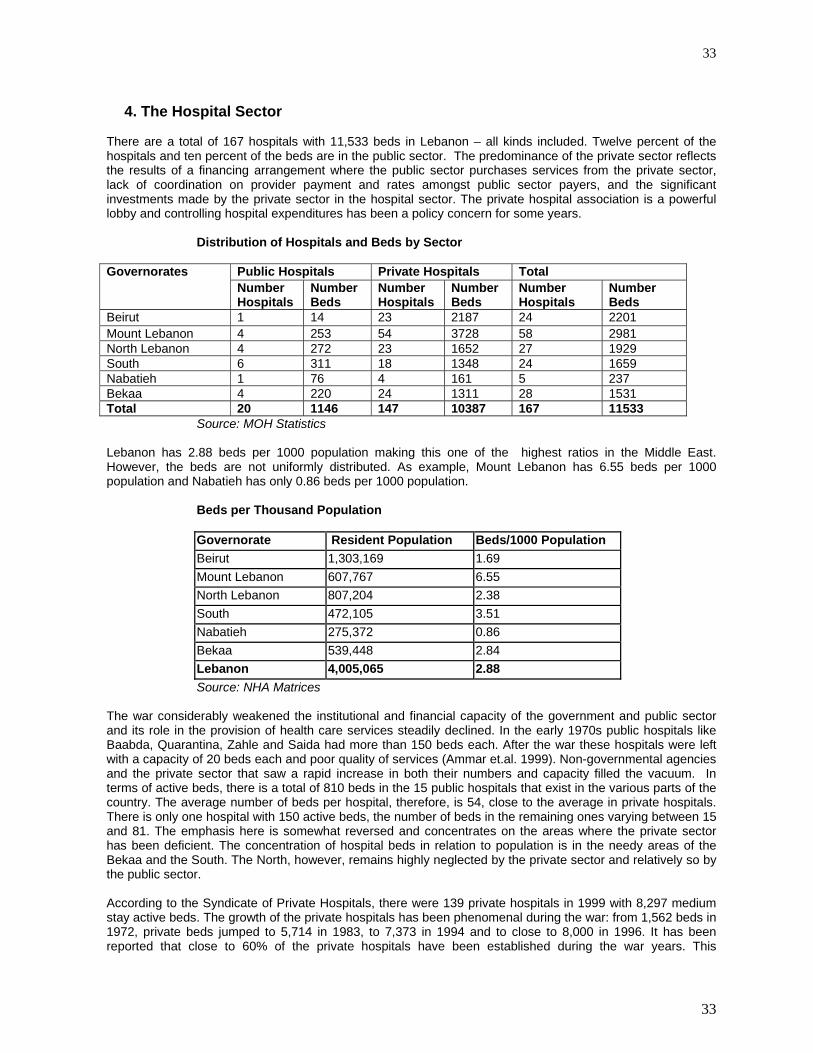

After the war ended in 1990, the Government started to refurbish its hospitals and to build new ones. In 1992, the Ministry decided to cover the treatment of patients undergoing complex surgeries and medical care such as cardiac surgery, cancer treatment, renal dialysis. These developments however have failed to delineate the role of the Ministry of Health, in a clear and sustainable manner. As is stands today, the Ministry is essentially yet another financing public agency, since close to 80% of its budget (as will be detailed further down) is spent on the hospitalization of patients on its account in private hospitals. The Ministry of Health has not been prepared for this role, in its legislation. The existing legislation, promulgated in 1961, stills defines the role of the Ministry, as a “public health” entity, i.e. the provision of non-personal health services, to the communities and the country in addition to is regulatory responsibilities (licensure, inspection and control). Moreover, from its original role to provide care for the poor, the Ministry has evolved to be the safety net, to cover, in principle, the medical care of all the non-insured, and to promote access and equity. Initially, the Ministry of Health provided hospital care to the medically indigent, in a paternalistic manner. Hospital care was seen as a “financial duress” for the medically indigent, and progressively for other segments of the population. In 1992, coverage was extended to the complex procedures and treatments, basically the “catastrophic illnesses” that would tax any household financially. This has oriented care towards the hospitals, to insure coverage and facilitate access, to the satisfaction of all users and providers, and to the detriment of Primary Health Care and its role as gatekeeper of care. In summary, Lebanon has a highly fragmented health care system. The war considerably weakened the institutional and financial capacity of the government and public sector and its role in the provision of health care services steadily declined. Non-governmental agencies and the private sector that saw a rapid increase in both their numbers and capacity filled the vacuum. Health care services have become increasingly oriented towards curative care with a rapid growth in the number of hospitals and centers for high technology services. Today ninety percent of hospital beds are in the private sector. The Primary Health Care system has remained weak.

2. Financing health care According to the National Household Health Expenditures and Utilization Survey ( NHHEUS), 46.8% of the population reported having some form of insurance (either social or private). If one excludes the non-Lebanese population that is estimated at 7.6% the government is responsible for the remaining 45.6% of the population. There also is a fair amount of geographic variation in the profile of the insured by Mohafazat or governorate. The highest proportion of the population covered is in Beirut and Mount of Lebanon with the lowest coverage in Bekaa and Nabatyeh. Information was obtained on the proportion of the population covered by various financing agencies from these agencies. Expenditures on hospital care by public financing agents are very high. Overall, 66.4 percent of the recurrent public health expenditures is spent on hospital based care, 14% on ambulatory care, 7.8% on pharmaceuticals, other goods accounts for 5%, 6.8% on administration. In the case of the Ministry of Health 71% of its budget is used to pay for hospital based care. Expenditures on primary health care services are a sub-set of that on non-institutional health care providers and accounts for less than 5% of public expenditures. The Ministry of Health has not been able to disburse all amounts allotted to primary health care and in some cases these resources have been diverted to curative care services. There are three sources of governmental health insurance providers in Lebanon, in addition to the payments made by the Ministry of Public Health to private hospitals for the hospitalization of the uninsured applicants. a) The National Social Security Fund (NSSF) The NSSF was established in 1964, within the programs of reforms that had been legislated after the 1958 civil disturbances. The Public Law mandated the creation of independent funds to cover Workmen’s compensation, end-of-service indemnities and Maternity and Sickness. The latter was implemented in 1971. The NSSF is quite similar to the French model of Social Security. It is financed by the employer, the employee and the Government. The high social costs of the NSSF has led employers to underestimate the salaries of their employees, and/or employ non-Lebanese in preference to the nationals.

20

20

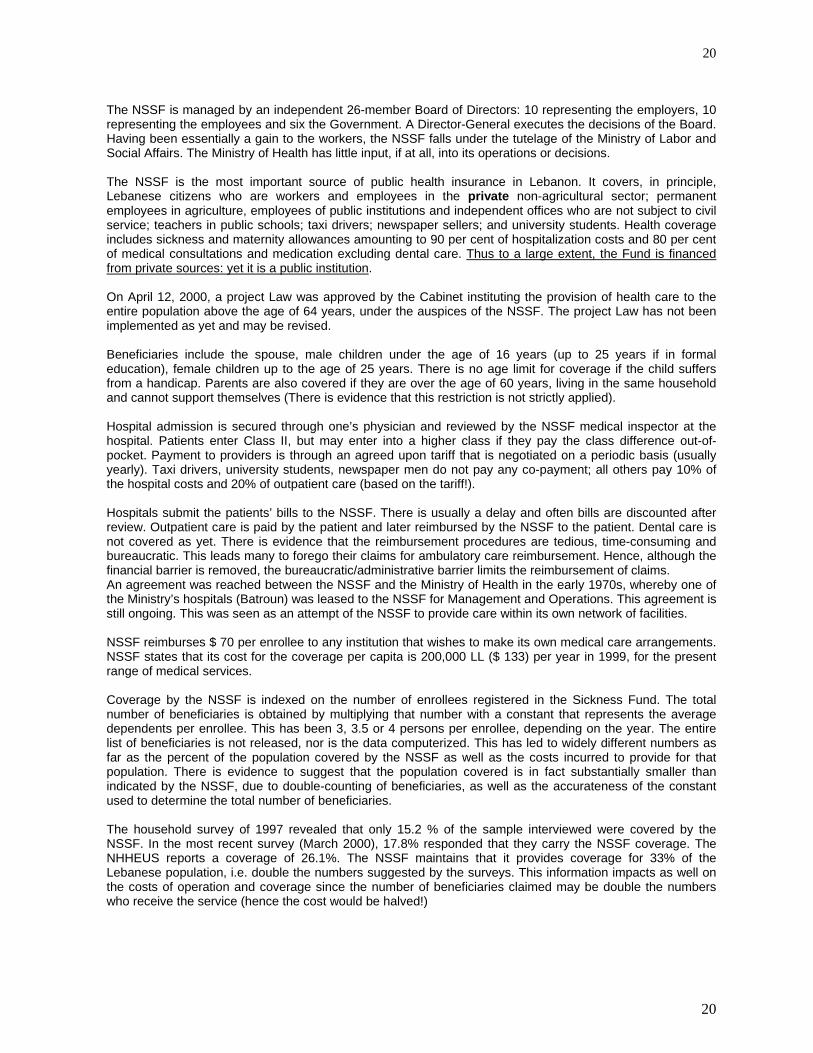

The NSSF is managed by an independent 26-member Board of Directors: 10 representing the employers, 10 representing the employees and six the Government. A Director-General executes the decisions of the Board. Having been essentially a gain to the workers, the NSSF falls under the tutelage of the Ministry of Labor and Social Affairs. The Ministry of Health has little input, if at all, into its operations or decisions. The NSSF is the most important source of public health insurance in Lebanon. It covers, in principle, Lebanese citizens who are workers and employees in the private non-agricultural sector; permanent employees in agriculture, employees of public institutions and independent offices who are not subject to civil service; teachers in public schools; taxi drivers; newspaper sellers; and university students. Health coverage includes sickness and maternity allowances amounting to 90 per cent of hospitalization costs and 80 per cent of medical consultations and medication excluding dental care. Thus to a large extent, the Fund is financed from private sources: yet it is a public institution. On April 12, 2000, a project Law was approved by the Cabinet instituting the provision of health care to the entire population above the age of 64 years, under the auspices of the NSSF. The project Law has not been implemented as yet and may be revised. Beneficiaries include the spouse, male children under the age of 16 years (up to 25 years if in formal education), female children up to the age of 25 years. There is no age limit for coverage if the child suffers from a handicap. Parents are also covered if they are over the age of 60 years, living in the same household and cannot support themselves (There is evidence that this restriction is not strictly applied). Hospital admission is secured through one’s physician and reviewed by the NSSF medical inspector at the hospital. Patients enter Class II, but may enter into a higher class if they pay the class difference out-of-pocket. Payment to providers is through an agreed upon tariff that is negotiated on a periodic basis (usually yearly). Taxi drivers, university students, newspaper men do not pay any co-payment; all others pay 10% of the hospital costs and 20% of outpatient care (based on the tariff!). Hospitals submit the patients’ bills to the NSSF. There is usually a delay and often bills are discounted after review. Outpatient care is paid by the patient and later reimbursed by the NSSF to the patient. Dental care is not covered as yet. There is evidence that the reimbursement procedures are tedious, time-consuming and bureaucratic. This leads many to forego their claims for ambulatory care reimbursement. Hence, although the financial barrier is removed, the bureaucratic/administrative barrier limits the reimbursement of claims. An agreement was reached between the NSSF and the Ministry of Health in the early 1970s, whereby one of the Ministry’s hospitals (Batroun) was leased to the NSSF for Management and Operations. This agreement is still ongoing. This was seen as an attempt of the NSSF to provide care within its own network of facilities. NSSF reimburses $ 70 per enrollee to any institution that wishes to make its own medical care arrangements. NSSF states that its cost for the coverage per capita is 200,000 LL ($ 133) per year in 1999, for the present range of medical services. Coverage by the NSSF is indexed on the number of enrollees registered in the Sickness Fund. The total number of beneficiaries is obtained by multiplying that number with a constant that represents the average dependents per enrollee. This has been 3, 3.5 or 4 persons per enrollee, depending on the year. The entire list of beneficiaries is not released, nor is the data computerized. This has led to widely different numbers as far as the percent of the population covered by the NSSF as well as the costs incurred to provide for that population. There is evidence to suggest that the population covered is in fact substantially smaller than indicated by the NSSF, due to double-counting of beneficiaries, as well as the accurateness of the constant used to determine the total number of beneficiaries. The household survey of 1997 revealed that only 15.2 % of the sample interviewed were covered by the NSSF. In the most recent survey (March 2000), 17.8% responded that they carry the NSSF coverage. The NHHEUS reports a coverage of 26.1%. The NSSF maintains that it provides coverage for 33% of the Lebanese population, i.e. double the numbers suggested by the surveys. This information impacts as well on the costs of operation and coverage since the number of beneficiaries claimed may be double the numbers who receive the service (hence the cost would be halved!)

21

21

NSSF COVERAGE Source: Director-General 1999 Employees in Public and Private sectorsand teachers in private schools 328843 University students 21077 Taxi drivers 34635 Newspapers men 100 Totals 384655

b) The Cooperative of the Civil Servants (Coop) The third most important source of public health insurance is the Cooperative of the Civil Servants. The Law instituting the Coop was issued in 1964, four months after the Law of the NSSF by the same Cabinet. An article in the Law stipulates that the Coop is to be merged with the NSSF once the latter has been developed. The Coop insures all employees of the public sector who are subject to the laws of the Civil Service. Health insurance here covers 90 per cent of hospitalization costs and 75 per cent of consultations, medication and dental treatment for the employee (up to a ceiling, beyond which the Coop covers all). In addition, it covers 75 per cent of hospitalization costs for the family members of the employee and 50 per cent of their medical consultations and pharmaceuticals The Coop is operated by the Office of the Prime Minister. It covers the permanent civil servants. The staff on contracts are covered by the NSSF (as above). The Coop also covers educational and other family benefits. After a service of 20 years, the civil servant (and his dependents) is covered also after retirement. The Coop uses the multiplier of 6 to estimate the dependents (and hence the beneficiaries)! Coverage includes hospital care, ambulatory services, dental care and optometric services as well. Coverage is in First, Second or Third class depending on the employment grade of the enrollee. Dental care is covered, as well as 90% of treatment abroad up to $ 10,000. The Coop is financed from a 1% deduction of the payroll: the balance is covered by the Government. The Coop enters into a tariff agreement with the providers, independently of the other public funds. The tariff of the Coop is usually more advantageous than the other funds; its hospitalization rate was only 7% in 1995. C)The Security Forces The coverage of the security forces is achieved through several funds: The Military are covered by the Ministry of Defense, through the Military Medical Services. The Internal Security forces (ISF) have their own plan, under the Ministry of Interior. The staff of the Public Security, the Customs employees and those of the State Security are covered through two different funds, under the Office of the Prime Minister. All uniformed staff members are covered with their dependents and their parents. The dependency ratio is 3.5 persons per enrollee. The following benefited from the security forces’ schemes, as per the Official Gazette:

1998

Army- Enrollees 85,000 Army- Beneficiaries 325,000 ISF – Enrollees 23,100 ISF- Beneficiaries 78,100 General Security- Enrollees 3,800 General Security- Beneficiaries 13,000 State Security- Enrollees 1,463 State Security- Beneficiaries 3,877 Totals 533,340

22

22

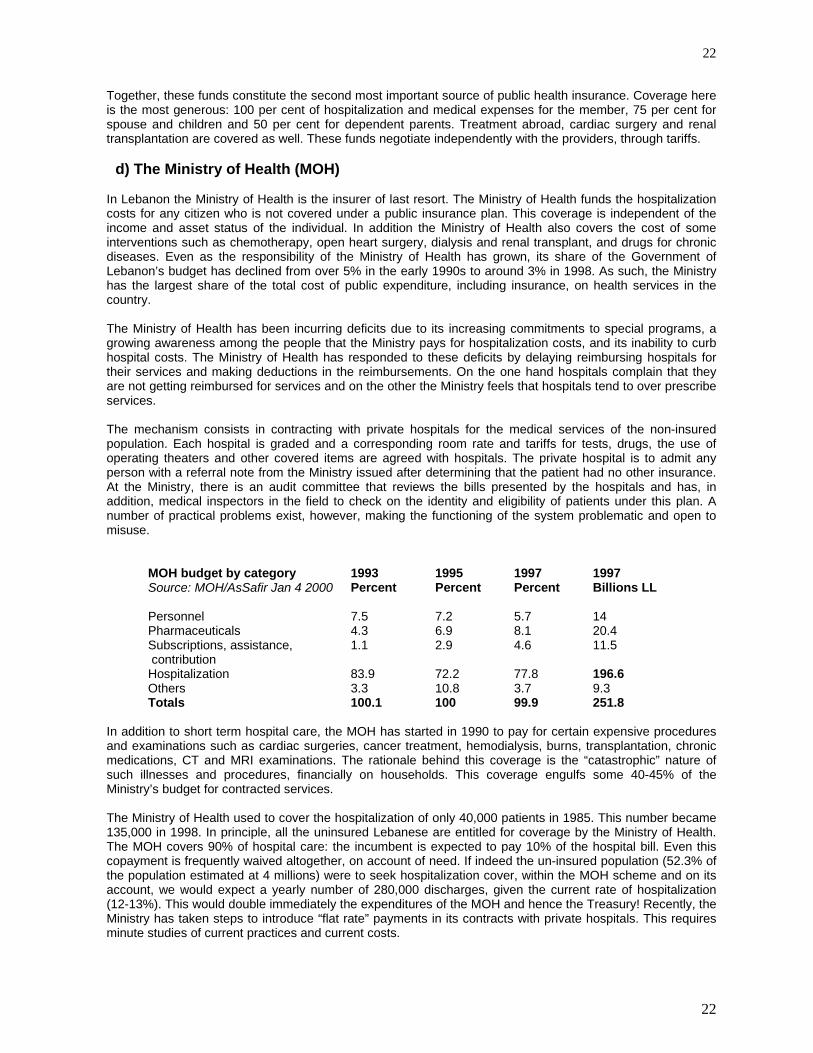

Together, these funds constitute the second most important source of public health insurance. Coverage here is the most generous: 100 per cent of hospitalization and medical expenses for the member, 75 per cent for spouse and children and 50 per cent for dependent parents. Treatment abroad, cardiac surgery and renal transplantation are covered as well. These funds negotiate independently with the providers, through tariffs. d) The Ministry of Health (MOH) In Lebanon the Ministry of Health is the insurer of last resort. The Ministry of Health funds the hospitalization costs for any citizen who is not covered under a public insurance plan. This coverage is independent of the income and asset status of the individual. In addition the Ministry of Health also covers the cost of some interventions such as chemotherapy, open heart surgery, dialysis and renal transplant, and drugs for chronic diseases. Even as the responsibility of the Ministry of Health has grown, its share of the Government of Lebanon’s budget has declined from over 5% in the early 1990s to around 3% in 1998. As such, the Ministry has the largest share of the total cost of public expenditure, including insurance, on health services in the country. The Ministry of Health has been incurring deficits due to its increasing commitments to special programs, a growing awareness among the people that the Ministry pays for hospitalization costs, and its inability to curb hospital costs. The Ministry of Health has responded to these deficits by delaying reimbursing hospitals for their services and making deductions in the reimbursements. On the one hand hospitals complain that they are not getting reimbursed for services and on the other the Ministry feels that hospitals tend to over prescribe services. The mechanism consists in contracting with private hospitals for the medical services of the non-insured population. Each hospital is graded and a corresponding room rate and tariffs for tests, drugs, the use of operating theaters and other covered items are agreed with hospitals. The private hospital is to admit any person with a referral note from the Ministry issued after determining that the patient had no other insurance. At the Ministry, there is an audit committee that reviews the bills presented by the hospitals and has, in addition, medical inspectors in the field to check on the identity and eligibility of patients under this plan. A number of practical problems exist, however, making the functioning of the system problematic and open to misuse.

MOH budget by category 1993 1995 1997 1997 Source: MOH/AsSafir Jan 4 2000 Percent Percent Percent Billions LL Personnel 7.5 7.2 5.7 14 Pharmaceuticals 4.3 6.9 8.1 20.4 Subscriptions, assistance, contribution

1.1 2.9 4.6 11.5

Hospitalization 83.9 72.2 77.8 196.6 Others 3.3 10.8 3.7 9.3 Totals 100.1 100 99.9 251.8

In addition to short term hospital care, the MOH has started in 1990 to pay for certain expensive procedures and examinations such as cardiac surgeries, cancer treatment, hemodialysis, burns, transplantation, chronic medications, CT and MRI examinations. The rationale behind this coverage is the “catastrophic” nature of such illnesses and procedures, financially on households. This coverage engulfs some 40-45% of the Ministry’s budget for contracted services. The Ministry of Health used to cover the hospitalization of only 40,000 patients in 1985. This number became 135,000 in 1998. In principle, all the uninsured Lebanese are entitled for coverage by the Ministry of Health. The MOH covers 90% of hospital care: the incumbent is expected to pay 10% of the hospital bill. Even this copayment is frequently waived altogether, on account of need. If indeed the un-insured population (52.3% of the population estimated at 4 millions) were to seek hospitalization cover, within the MOH scheme and on its account, we would expect a yearly number of 280,000 discharges, given the current rate of hospitalization (12-13%). This would double immediately the expenditures of the MOH and hence the Treasury! Recently, the Ministry has taken steps to introduce “flat rate” payments in its contracts with private hospitals. This requires minute studies of current practices and current costs.

23

23

e) The Private insurance companies The private insurance market is growing rapidly in Lebanon. According to the Ministry of Economy sources approximately 70 private insurance companies provide health insurance. They provide both complementary and comprehensive health insurance policies. The former is to complement and fill gaps in the benefits provided by NSSF, CSC, and health insurance arrangements for the Army and Police. The latter refer to stand alone health insurance policies that can cover a range of benefits including inpatient and outpatient care, and coverage for pharmaceutical expenses. It is estimated that 8% of the population has comprehensive coverage and 4.6% gap insurance. According to the ACAL (Association of Lebanese Insurance Companies), health insurance continues to dominate the sector, representing some 48% of total premiums written. The top 20 firms control about 70% of the market. In May of 1999, Parliament passed an insurance reform law that is expected to pave the way for the consolidation of the sector.

Insurance Premiums 1997-1998

Type of Coverage Total Premium 1998 ($ million)

Total Premium 1997 ($ million) Increase %

Hospitalization 215 198 8.58 Life 75 80 6.26 Motor 25 64 11.15 General Accidents 41 27 51.24 Fire 34 19 85.86 Workmen’s Compensation

16 18 13.88

Marine 12 15 17.14 TOTAL 450 421 7.05

Source: NHA Matrices Compared to other countries in the region, Lebanon has a fairly well developed private insurance sector. Private insurance is licensed by the Ministry of Economy. Insurance companies are required by law to set aside 40% of premiums as reserves. Ten of the companies are foreign owned and preliminary reports indicate that another ten are non-operational. The two global reinsurance companies with offices in Lebanon are MunichRe and SwissRe. Nearly 85% of the policies are purchased by employers as an employee benefit or to fill gaps in NSSF coverage. Insurance policies in Lebanon typically cover in-patient care. Outpatient services are covered for an additional premiums with co-payments of around 20%. Estimates of the breakdown of expenditures by private insurance companies by type of service shows that physician fees account for 30% of expenses, pharmaceuticals for 31%, hospitalization costs for 15%, and administrative expenses for 24%. Many insurance companies still consider health to be a loss leader. The private insurance market is inadequately regulated. Consequently, insurers indulge in “cream skimming”, selecting only good risks and either denying coverage or setting very high premiums for individuals with pre-existing conditions. The administrative costs of private insurance are high: up to 50% of the premium. A large proportion of that is disbursed to middlemen. Insurance companies pay 11% of the premium as a tax to the Ministry of Economy. The private insurance company must also lodge 40% of its premium as guarantee.

Distribution of Private Insurance Expenditures Item Percentage Physician Fees 30% Pharmaceuticals 31% Hospitalization Costs 15% Administrative Expenses 24% Total 100% Source: NHA matrices

24

24

The number of Lebanese enrolled in private insurance had risen between 1992 and 1995, only to stabilize or even decrease lately. In 1998, the Central Statistics Agency estimated that 464,000 (116,000 of which is co-insurance) persons had taken up a private insurance; Mednet’s estimates are 473,000 (173,000 of which are for co-insurance). The hospitalization rate for this population varied between 11-15% over the period 1995-1999. Insurance policies in Lebanon typically cover in-patient care. Outpatient services are covered for an additional premiums with co-payments of around 20%. f) The Mutual Funds There is also a growing number of mutual funds being established, covering health expenses in the context of syndicates, associations and other groups. The mutual funds started in 1991. This movement is under the tutelage of the Ministry of Housing and Cooperatives. The Law governing the mutual funds permit any group of 50 persons (or above) to form a mutual fund. The linkage could be professional, religious or community-based. Tax laws that provide tax-breaks to non-profit groups have lead to a proliferation of mutual funds that offer health insurance coverage to their enrollees. Recent estimates would indicate that about 65,000 individuals were covered for health benefits by mutuelles. However, the number of enrollees ranges from as low as sixty-six to twelve thousand. Private insurance companies feel the differential tax treatment distorts the playing field and the growth of mutual funds hampers the competitiveness of the insurance market. Mutual funds do not pay taxes on the premium, unlike the private insurance companies.

Insurance Status of the Lebanese Population Source: Household Survey 2000

Beirut Beirut Rest of North South Nabatieh Beqaa Lebanon suburbs Mt

Lebanon

NSSF - Alone 18 17 19.6 11.5 12.1 9.3 11.2 14.5 NSSF - With other insurance 5.8 6.3 4.1 1.5 1.2 0.9 0.9 3.2 Total NSSF 23.8 23.3 23.7 13 13.3 10.2 12.1 17.7 Coop - Alone 3 3 3.5 4.5 5.6 7.1 5.1 4.2 Coop - with other insurance 0.2 0.4 0.1 0.2 0 1.4 0.1 0.3 Total Coop 3.2 3.4 3.6 4.7 5.6 8.5 5.2 4.5 Uniformed - alone 3.8 6.4 7 12 4.4 7.5 12.5 8 Uniformed - with other insurance

0 0.1 0 0.2 0 0.1 0.2 0.1

Total Uniformed 3.8 6.5 7 12.2 4.4 7.6 12.7 8.1 Private insurance - alone 15.3 10.4 13.6 3.6 4 1.3 2.9 7.6 Private insurance - with other insurance

1.7 0.8 0.8 0.9 1.1 0.2 0.2 0.8

Total - Private insurance 17 11.2 14.4 4.5 5.1 1.5 3.1 8.4 Complementary insurance 4 5.2 3.3 0.7 1.2 0.5 0.7 2.5 Municipality coverage 1.2 0.3 0 0.6 0.3 0 0.1 0.4 Insurance/in school or at work-alone

0.1 1 0.5 1.7 0.2 0.2 0.6 0.8

Insurance/in school or at work-others

0.1 0.3 0.1 1 0.1 0 0.2 0.3

Insurance/in school or at work 0.2 1.3 0.6 2.7 0.3 0.2 0.8 1.1 Insurance - Syndicates - alone

2.5 1.9 2.6 0.7 1.7 1.9 1.4 1.7

Insurance - Syndicates - with other

0.5 0.1 0.2 0 0.3 0.1 0 0.1

Insurance - Syndicates - Total 3 2 2.8 0.7 2 2 1.4 1.8 Other type of insurance - alone

3 2.4 0.5 3.7 20.4 7.8 1.4 4.8

Other type of insurance - with other

0 0.1 0 0.5 1.4 1.1 0 0.4

Other type of insurance - 3 2.5 0.5 4.2 21.8 8.9 1.4 5.2

25

25

Total Non-insured 45.3 48.8 46.5 57.2 46 61.2 63 52.3 Unknown 1.5 2.2 1.9 1.9 2.6 1.5 0.6 1.8 All insured 59.2 55.7 55.9 43.3 54 39.4 37.5 49.7 All groups 106 106.7 104.3 102.4 102.6 102.1 101.1 103.8 Other type of insurance includes UNRWA. Hizbollah, etc.

g) The Non-Governmental Organizations (NGOs) There is a relatively small proportion of the total health bill that represents coverage of beneficiaries of health assistance from local and foreign not-for-profit and non-governmental organizations (NFP/NGOs) operating generally at the local level in poorer urban districts and underprivileged rural areas. The importance of this coverage is rather in the fact that it relates to needy individuals who would have great difficulty obtaining health services from other sources. Medical care, offered through NGOs witnessed major extension during the war years. It became evident that health care is a magnet to attract the sympathies and allegiance of the population then under duress. This has waned somewhat since 1990. However, it should be noted that the involvement of the Community in the provision of medical care, did offer some innovative models for the financing, governance and management of health services. Some of this experience has assisted in the push for the autonomy of public hospitals. h) Donor Assistance In 1998, donor assistance amounted to 1.96% of total health care financing. The sharpest decline in donor assistance has been to immunization and control of diseases and there has been a significant increase in support for family planning activities. Outlays for capital investment account for the majority of donor assistance. The Ministry of Health and other government agencies are the primary beneficiary of donor assistance.

Summary of External Assistance Disbursements to Health Sector (000s LL)

Area 1995 1996 1997 1998 Sector Policy and Planning 1,116,000 1,636,500 1,828,500 828,000 Primary Health Care 11,775,000 11,112,000 6,688,500 4,701,000 Immunization and control of diseases 820,500 5,191,500 589,500 111,000 Family Planning 985,500 1,057,500 619,500 1,137,000 Hospitals and Health Centers 19,632,000 53,755,500 41,491,500 46,867,500 Total 34,330,995 72,754,996 51,219,497 53,646,498 Percentage Change in External Assistance

Area 1995 1996 1997 1998 Sector Policy and Planning 46.6% 11.7% -54.7% Primary Health Care -5.6% -39.8% -29.7% Immunization and control of diseases 532.7% -88.6% -81.2% Family Planning 7.3% -41.4% 83.5% Hospitals and Clinics 173.8% -22.8% 13.0% Total 111.9% -29.6% 4.7%

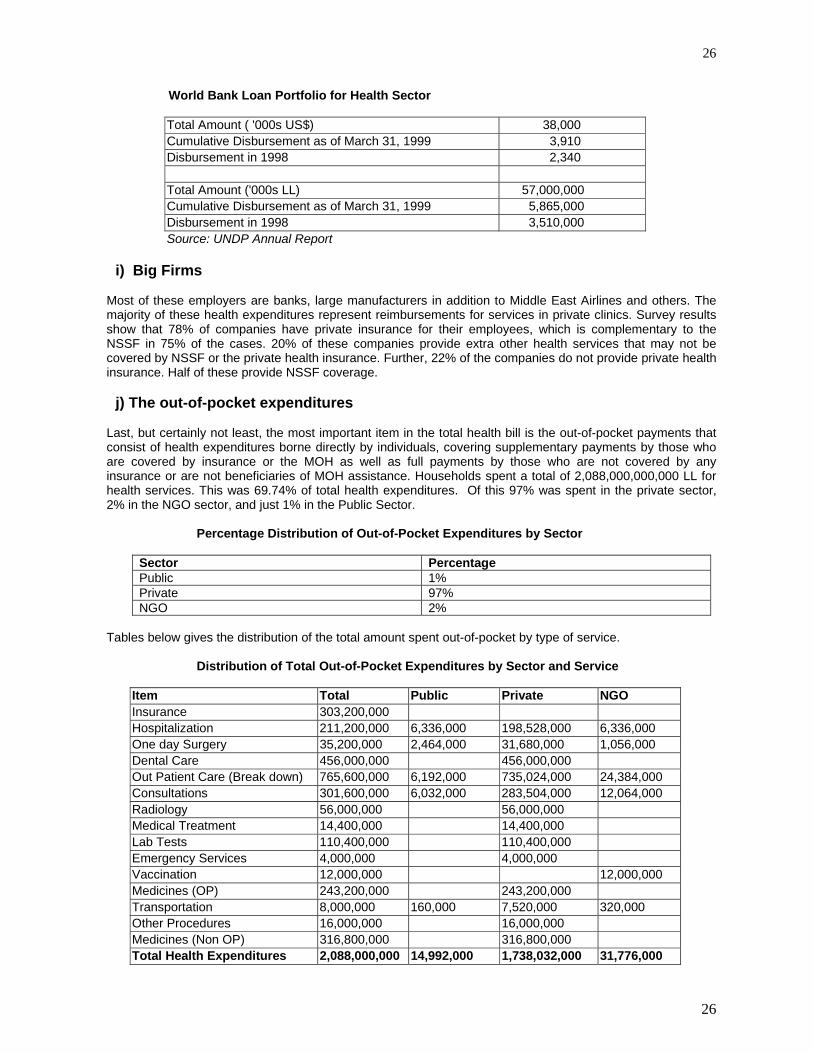

Source: UNDP Annual Report and Information from CDR The World Bank has been supporting health sector reform as well as capital investment activities in Lebanon. The World Bank’s loan portfolio was USD 38 million. Of this disbursements in 1998 amounted to USD 2.34 million and cumulative disbursements until the end of March 31, 1999 was USD 3.91 million.

26

26

World Bank Loan Portfolio for Health Sector

Total Amount ( '000s US$) 38,000 Cumulative Disbursement as of March 31, 1999 3,910 Disbursement in 1998 2,340 Total Amount ('000s LL) 57,000,000 Cumulative Disbursement as of March 31, 1999 5,865,000 Disbursement in 1998 3,510,000 Source: UNDP Annual Report

i) Big Firms Most of these employers are banks, large manufacturers in addition to Middle East Airlines and others. The majority of these health expenditures represent reimbursements for services in private clinics. Survey results show that 78% of companies have private insurance for their employees, which is complementary to the NSSF in 75% of the cases. 20% of these companies provide extra other health services that may not be covered by NSSF or the private health insurance. Further, 22% of the companies do not provide private health insurance. Half of these provide NSSF coverage. j) The out-of-pocket expenditures Last, but certainly not least, the most important item in the total health bill is the out-of-pocket payments that consist of health expenditures borne directly by individuals, covering supplementary payments by those who are covered by insurance or the MOH as well as full payments by those who are not covered by any insurance or are not beneficiaries of MOH assistance. Households spent a total of 2,088,000,000,000 LL for health services. This was 69.74% of total health expenditures. Of this 97% was spent in the private sector, 2% in the NGO sector, and just 1% in the Public Sector.

Percentage Distribution of Out-of-Pocket Expenditures by Sector

Sector Percentage Public 1% Private 97% NGO 2%

Tables below gives the distribution of the total amount spent out-of-pocket by type of service.

Distribution of Total Out-of-Pocket Expenditures by Sector and Service

Item Total Public Private NGO Insurance 303,200,000 Hospitalization 211,200,000 6,336,000 198,528,000 6,336,000 One day Surgery 35,200,000 2,464,000 31,680,000 1,056,000 Dental Care 456,000,000 456,000,000 Out Patient Care (Break down) 765,600,000 6,192,000 735,024,000 24,384,000 Consultations 301,600,000 6,032,000 283,504,000 12,064,000 Radiology 56,000,000 56,000,000 Medical Treatment 14,400,000 14,400,000 Lab Tests 110,400,000 110,400,000 Emergency Services 4,000,000 4,000,000 Vaccination 12,000,000 12,000,000 Medicines (OP) 243,200,000 243,200,000 Transportation 8,000,000 160,000 7,520,000 320,000 Other Procedures 16,000,000 16,000,000 Medicines (Non OP) 316,800,000 316,800,000 Total Health Expenditures 2,088,000,000 14,992,000 1,738,032,000 31,776,000

27

27

The household survey only reinforces the fact that the private sector dominates the market in Lebanon. Seventy-eight percent of outpatient visits took place in the private sector, followed by the NGO sector at 12%, with the Public sector accounting for only 9% of all visits. With regard to hospitalizations the private sector once again accounts for nearly 86% of all admissions with the Public sector accounting for 9%. The Public Sector fares a little better when it comes to one day surgery probably because it both pays for this as well provides these services at its facilities. Dental care is almost exclusively the domain of the private sector. This predominance of the private sector in Lebanon makes it clear that any attempt at containing costs and improving efficiency will require the participation and buy-in of the private sector. At the same time unless this sector is better managed, meaningful changes to the health system cannot be achieved.

Choice of Provider Type of Care Public Private NGOs Outpatient Visits 9.4% 78.4% 12.2% Hospitalizations 8.7% 85.7% 5.6% One day Surgery 19.8% 74.3% 5.9% Dental Care 0.6% 86.2% 13.2% Note: The distribution of dental care might underestimate use of Public facilities

Table below shows the percentage of household expenditures that went to pay for health services. On average, households spent a little over 14% of their household expenditures on health services. However, the burden of out-of-pocket expenditures, measured as a proportion of household expenditures, is not equitably distributed. It is seen that nearly a fifth of expenditures in households in the lowest income category went to heatlh. The proportion spent on health goes down with income and households in the highest income group spend only 8% on health care. Even though there might not be inequities in access as measured by per capita use rates the burden of out-of-pocket expenditures is inequitably distributed. While the Ministry of Health pays for hospitalization costs of the uninsured (including the poor) there is probably a need to develop a targeted financing scheme that assures financial access to health services for low income families.

Proportion of Household Expenditures Spent on Health Income Category (‘000 LL) Percent Less than 300 19.86% 300-500 17.96% 500-800 16.07% 800-1200 14.78% 1200-1600 14.02% 1600-2400 14.14% 2400-3200 11.36% 3200-5000 10.68% 5000 and over 8.05% All households 14.06%

Unlike use rate where one did not observe inequities in access the examination of expenditures does raise some equity concerns. On average Lebanese households spend 2,609,000 LL per year on health care. However, households in the Mount of Lebanon spend nearly twice as much on health as households in the North of Lebanon. Similary, one observes a clear correlation between household income and health expenditures. Households with lower incomes spend far less on health care than those with higher incomes. This inspite of the fact that they tend to use more health services on a per capita basis than higher income households. Per capita expenditures amounted to 522,000 LL per year. Of these 15% was spent on insurance, 10% on hospitalization, 2% on one day surgery, 22% for dental care, 36% for outpatient care (exlcuding drugs), and 15% on drugs. Once again the expenditures on pharmaceuticals only reinforces the need to better manage and control this sector. Similarly, the high share of dental expenditures coupled with the access issues observed earlier point probably point to the need to find ways of increasing insurance coverage for dental care.

28

28

Annual Per Capita Expenditures by Type of Service (‘000 LL)

Item Per Capita Per Cent Insurance 75.80 15 Hospitalization 52.80 10 One day Surgery 8.80 2 Dental Care 114.00 22 Out Patient Care (Break down) 191.40 36 Consultations 75.40 Radiology 14.00 Medical Treatment 3.60 Lab Tests 27.60 Emergency Services 1.00 Vaccination 3.00 Medicines (OP) 60.80 Transportation 2.00 Other Procedures 4.00 Medicines (Non OP) 79.20 15 Total Health Expenditures 522.00 100.00

k) Overall expenditures The table below list all the above sources and their respective financial contributions to the total national health bill.

Total LL Hospitals

Non-Institutional Health Care Providers Pharmaceuticals

Retail Sales, capital investment, profit

General Health Administration & Ins.

MOH 310,919,302 226,577,948 27,794,622 21,151,000 22,154,979 13,240,753 Army 86,620,910 50,769,000 3,874,410 13,200,000 2,082,500 16,695,000 ISF 39,708,970 24,371,000 7,853,471 5,236,499 350,000 1,898,000 GS 6,000,000 3,500,000 2,500,000 0 SS 2,400,000 1,450,000 950,000 0 MOSA 1,213,500 0 1,213,500 0 M DISP 230,000 115,000 115,000 0 CSC 45,128,944 24,337,128 18,762,550 0 94,953 1,934,313 NSSF 296,126,000 107,708,000 42,159,000 47,541,000 98,718,000 MUTUAL 33,850,231 0 25,387,673 8,462,558 EMPLOYERS 44,202,642 40,074,140 4,128,502 NGO's 6,774,000 0 6,774,000 0 0 0 Private Insurance Schemes 333,878,035 50,081,705 100,163,411 103,502,191 80,130,728 Household 1,784,800,000 246,400,000 978,400,000 560,000,000 Donors 966,000 0 0 0 966,000 0 Custom duties 1,300,000 Total 2,994,118,534 735,309,781 1,256,021,777 759,093,248 25,648,432 218,045,296

MOH= Ministry of Health; ISF= Internal Security Forces; GS: General Security forces; SS: State Security Forces; MOSA: Ministry of Social Affairs; M Disp: Ministry of the Displaced; CSC: Cooperative of civil servants; NSSF: National Social Security Fund; Mutual: Mutual Funds;

29

29

Data show that 12.3 per cent of the GDP of the country was spent on the health bill in 1998. This compares with 4 to 6 per cent in most developing countries.(Tabbara, 2000). It should be mentioned that, although many European countries spend about 10% of the GDP on health care, the value-for-money, the quality of care and the coverage is indeed far superior to the situation in Lebanon. In fact, given the determinants of the health care system in Lebanon, i.e. fee-for-service, oversupply of manpower and facilities, low occupancy of hospital beds, hospital-driven care, poor control, etc., there is no reason that would prevent costs to rise to 14 or 16% or more as is the case in the USA, where control is more effective and managed care is available.

Total BillionsLL Hospitals

Non-Institutional Pharmaceuticals Other Admin

OOP 1,784 246 978 525 35 0 MOH 311 227 28 21 22 13 NSSF 298 108 42 48 60 40 Other Public 189 105 42 18 3 21 Private 412 50 160 103 7 92 Total 2,994 736 1,250 715 127 166

Collapsed table – OOP: Out-of-pocket expenditures; MOH: Ministry of Health; Other public: includes the uniformed medical services, the other ministries and the cooperative.

It is noteworthy to point out that the Treasury has effectively spent only 333 millions $ out of a total of close to 2 billions $ (17%) in 1998. The lion’s share has been funnelled through the Ministry of Health (207 millions $ or 62%). Put differently, the Treasury has expended less than $ 100 per capita for medical care only. The balance has been paid out of private sources. The number of hospital admissions on account of the Ministry of Health has grown from 64,000 in 1990 to 140,000 in 1999, despite the relatively cumbersome procedures for hospitalization permits. If indeed this process becomes simpler, it is anticipated that more and more people will seek to be hospitalized under the Ministry scheme. This will bear directly on payments by the Treasury, currently in financial difficulties. Moreover the drive towards private coverage may be stemmed. It is evident that this orientation to hospital care (now covered by the Ministry) has led hospitals to become the gatekeepers for medical care. This is already evident by the higher than expected hospitalization rates amongst all segments of the population.

Health Care expenditures: August 2001* Total Health Care Expenditures 2 billions US$ Per Capita Expenditures 500 US$ Total GPD 16,2 billions US$ Health Expenditures as % GDP 12.3 % % GOL budget allocated to Health 6.6 % Sources of funds: Public 18.0 % Private Households 69.7 % Employers 10.3 % Donors 2.0 % Distribution of Health Care Expenditures: Public hospitals 1.7 % Private hospitals 22.8 % Private Non- Institutional providers 41.0 % Pharmaceuticals 25.4 % Others 9.1 % *Information compiled from the “National Health Accounts Study”, released in August 2001- based on 1998 data.

30

30

In summary, Lebanon has several different government, not-for-profit, and private for-profit financing schemes. These include:

Two employment based social insurance schemes Four different schemes to cover the security forces The Ministry of Health financing that covers any citizen who is not covered under any other scheme. MOH payments are not dependent on the income of the beneficiary A private insurance market that is largely employment based Mutual funds Out-of-pocket expenditures

l) Insurance Profile of the Population

Governorate Insured Non-Insured Missing Beirut 53% 45% 2% Beirut Suburbs 49% 49% 2% Mount of Lebanon 52% 47% 2% North of Lebanon 41% 57% 2% South of Lebanon 51% 46% 3% Nabatyeh 37% 61% 2% Bekaa 36% 63% 1% Total 46% 52% 2% Source: NHHEUS

Table One below shows the proportion of population covered by various financing agents as reported by these agencies and earlier estimates. Table II (next) provides the information as reported by the household survey. The most striking difference is observed in the coverage rates under NSSF. According to their estimates roughly 26.1% of the population is covered under the NSSF scheme. However, the household survey numbers show a lower coverage rate at 17.8%. The household survey results for other categories (Army and Private Insurance) closely match known figures.

Percentage of Population Covered by Various Financing Agencies- NHA Financing Agency Percent of Population

Covered NSSF 26.1%

CSC 4.4 Army 8.8 IS 1.9 GS+SS 0.4 Private Insurance 8.00 (complete coverage)

4.60 (gap insurance) Mutual Funds 1.6 MOH 42.70 Source: NSSF, CSC, Army, IS, GS, and SS figures obtained from agency or DOS. Private Insurance figures obtained from article by Ammar et.al.

Percent of Population Covered by Various Financing Agencies (Based on Household Survey) Type of Insurance Alone With

another insurance

Total

NSSF 14.6% 3.2% 17.8% Army 8.1% 0.0% 8.1% Private Insurance 7.6% 0.7% 8.3% CSC 4.3% 0.3% 4.6%

31

31

Complementary Insurance 2.5% 2.5% Group Insurance 1.8% 0.1% 1.9% Provided by Municipalities 0.4% 0.4% Insurance at Work 0.8% 0.8% Other Types of Insurance 4.8% 0.3% 5.1% Total 44.9% 4.6% 49.5% Source: NHHEUS Note: This will add up to more than 46% because people have multiple coverage

2. Benefits under Various Public Financing Schemes

Type of Services MOH NSSF CSC Armed Forces Hospitalization 85% 90% 90% 100% Physician No Up to 20000 LL 75% up to 12000LL Up to 20000LL Specialist No Up to 30000 LL 75% up to 12000LL Up to 30000LL Ambulatory No Yes 90% 100% Drugs No Yes Yes Yes Emergency Clinics No as physician and

specialist as physician and specialist as physician and

specialist Emergency Hospitals Hospital as Hospitalization as Hospitalization as

Hospitalization Dental Coverage No No 75% of tariff 100% Ophthalmology No No 75% up to 35000LL 100/80/6000 Immunization Yes at HC No No No Treatment Abroad No No 90% pre admission $10000 pre

admission Open Heart 8,000,000LL 90% As MOH 100% Kidney Transplant 19,000,000LL 90% As MOH 100% Dialysis 135000LL/session 100% 100% 100%

Source: NHA The health care system of Lebanon is experiencing a strong tilt towards curative care, fueled by an oversupply of physicians, hospital beds, abundance of high-tech expensive equipment, poor regulation and third party payment, as well as through the incentives inherent in third party coverage and provider payments. The rise in health expenditures can also be attributed to the high expectations of the population. These expectations are closer to those in developed economies Therefore unless the health care delivery system undergoes re-structuring, under any one of the reform options, the overall cost of medical care cannot but go on rising. 3. Health Care Utilization A National Household Health Expenditure and Utilization Survey (NHHEUS) has recently been completed. This represents the first time a health specific survey has been conducted in Lebanon. A nationally representative sample of roughly 6,500 households was used. The survey addressed the following main questions:

Health Care Use and its determinants Choice of Provider by type of service and its determinants Out-of-pocket expenditures by type of provider and service Insurance Status of population including multiple coverage Gender Equity in health care use The health status and health care use of the elderly

On average Lebanese used 3.6 outpatient visits per year, with males using 3.1 visits per capita per year and females 4.1 visists per year. While regional disparities exist in use rates, these do not appear to be significant.

32

32

This probably reflects the presence of a well-developed market for health services (in the private, NGO, and public sectors). An interesting finding is that unlike many other counties lower income individuals have higher use rates than those in higher income groups. Jordan is the other country in the region where similar results have been observed. This indicates that there does not appear to be inequities in access to health services if these are measured by use rates. Looking at use rates by age group it is seen that those over the age of sixty and those less than the age of five have the highest use rates. Other than those below the age of five use rates for females tends to be higher than males. Those who have insurance have higher use rates than the uninsured. Hospitalization rates hovered around 7 % amongst the population in 1984 (Beirut 1984-AUB). It is currently in the range of 12-13% as the table below indicates:

Ministry of Health discharges in Private hospitals 135,000 NSSF discharges 110,400 Cooperative discharges 18,300 Army Military discharges 44,300 Police discharges 23,000 Security forces discharges 2,800 Private insurance discharges 64,400 Self-Payers 96,000 Total discharges (1998) 494,200 ALOS 4 days Occupancy rate 55% Population 4 millions Private hospital beds 8,300 Public sector beds 810 Total hospital beds- acute 9,110 Hospitalization rate 12.5%

The household survey completed in March 2000 documented that the overall hospitalization rate is 12% per year (1.5% of the population had more than one hospitalization per year). As expected, in the age group (above 60 years), it was 28%, with 4.5% having more than one episode per year! Hospitalization episodes did not vary significantly amongst the regions. Hospitalization (once per year and more than once per year) was more frequent amongst lower income groups: 10.5% and 3.1% for households earning less than 300,000 LL per month, versus 7.8% and 2.2% for households earning more than 5 millions LL per month. Evidently hospitalization rates varied between the insured and the non-insured 10% versus 8 % for one admission per year; 1.6 % versus 1.2% for those admitted more than once per year. Hospitalization for one day (Day surgery, etc.) had similar frequencies across regions, income groups, age and insurance status. When examining hospitalization rates, one does not see inequities in use rates though those with insurance do tend to have a higher use of hospital services than those that are unisured. The age differences persist as in the case of outpatient care. The fact that lower income households have higher use rates than those with higher incomes quite likely reflects the fact that the government as the insurer of the last resort pays for hospital care for all uninsured in Lebanon. Thus those needing hospital care can either use insurance (social or private) or approach the Ministry of Health for finances. With regard to the use of Day Surgery, while the elderly have higher use rates than other age groups one does not observe the differences by insurance status as was seen in the case of outpatient care and hospitalization. This is likely because most insurance policies do not cover day surgery. With dental treatment an interesting observation is that the highest use rates are to be found in the Mount of Lebanon. As dental care is not covered under most insurance policies this probably reflects the fact that the largest number of dentists are to be found in the Mount of Lebanon area. Contrary to the trend with regard to other services, the elderly use far less dental care than those in the age group fifteen to fifty-nine. Similary, those in the lower income groups use less dental care than those in the higher income groups. While some of this might be a function of greater awareness the findings for income and age likely indicate a lack of access (due to the inability to pay).

33

33