ijmf market making in international capital marketsmariosp/mmindevelopingcountries.pdf · market...

TRANSCRIPT

Market making in internationalcapital markets

Challenges and benefits of its implementationin emerging markets

Andreas CharitouUniversity of Cyprus, Nicosia, Cyprus, and

Marios PanayidesUniversity of Utah, Salt Lake City, Utah, USA

Abstract

Purpose – The purpose of this paper is to critically evaluate the different market-making systemsfound in most developed capital markets and to provide guidance to emerging market regulators for apossible implementation of such a system.

Design/methodology/approach – The paper looks closely at the market design of seven developedcountries focusing on the obligations and privileges of market makers. Through a case study andempirical evidence the paper identifies advantage and disadvantage of a possible implementation of asimilar design to an emerging market.

Findings – The paper identifies three forms of market making applied today: the quote-driven, thecentralized and non-centralized systems. Four factors are proposed that regulatory authorities inemerging markets should consider when deciding whether, and which of, the three market-makingsystems they should implement. These are: current exchange design and the costs of restructuring,international and domestic investors’ sentiment towards the exchange, size of the emerging marketand the market designs in countries hosting the target foreign capital.

Research limitations/implications – The paper looks at the implementation of a market-makingsystem in an emerging market. Further research may investigate other ways of how emerging marketsauthorities can restructure their markets into more efficient, compatible and trustworthy financialvenues in order to attract both domestic and foreign investors.

Originality/value – The area of emerging markets’ microstructure design and market quality is stillrelatively under-studied. We provide evidence of the challenges and benefits of the implementation of amarket-making system in those markets.

Keywords Capital markets, Market system, Order systems

Paper type Research paper

The current issue and full text archive of this journal is available at

www.emeraldinsight.com/1743-9132.htm

This project was financially supported by the SEC Cyprus and the Cyprus Stock Exchange. Theauthors would like to thank seminar participants of the Cyprus Stock Exchange and Securitiesand Exchange Commission for their useful comments and suggestions (December 2003). Theywould also like to thank for their useful comments Amber Anand, Avi Wohl, Akis Kleanthous(Chair of the Cyprus Stock Exchange), Marios Clerides and Akis Hadjipieris (Chair and ViceChair, SEC-Cyprus, respectively), Stathis Thomadamis (Chairman of the SEC-Athens), EleniIoannidou (Athens Stock Exchange, Vice President). Michael Pagano (the Editor) and ananonymous referee provided valuable comments that significantly improved the manuscript.Remaining errors are the responsibility of the authors.

IJMF5,1

50

International Journal of ManagerialFinanceVol. 5 No. 1, 2009pp. 50-80q Emerald Group Publishing Limited1743-9132DOI 10.1108/17439130910932341

1. IntroductionIt is well documented that two of the main problems that emerging markets face arecapital supply shortage and low liquidity (Comerton-Forde and Rydge, 2006; O’Hara,2001; Kairys et al., 2000). Market regulators in these countries can consider a number ofrestructuring measures to alleviate these problems: introduction of marketsegmentation (i.e. segmenting trading hours, creating main and parallel markets),implementation of trading phases (i.e. offering both continuous and call auction tradingin a day), or provision of special incentives for the submission of limit orders (i.e.offering hidden orders and standing orders). In addition, the implementation of amarket making system can help boost liquidity, and, in combination with otherrestructuring measures, can provide important improvements in market quality. AsVenkataraman and Waisburd (2007), Nimalendran and Petrella (2003) and Majnoniand Massa (2001) show, the implementation of a market making system significantlypromotes liquidity, lowers transaction costs, reduces volatility and improves dailyturnover of listed securities. This study critically evaluates the types of market makingsystems found in developed capital markets and identifies the factors that stockmarket regulators in developing countries should consider when deciding which typeof system to implement[1].

In this study, we examine the market design of 30 stock exchanges in bothdeveloped and developing countries. Based on regulations (obligations and privilegesof market makers) and market design characteristics, we identify three types of marketmaking systems which are applied in modern stock markets:

(1) the quote-driven market making system;

(2) the centralized market making system in an order-driven market[2]; and

(3) the non-centralized market making system in an order-driven market[3].

We critically evaluate these three market making systems and discuss possibleadvantages and disadvantages of each system for emerging markets. We also identifypatterns in the geographic and temporal evolution of each market making system.

We propose four factors that regulatory authorities in emerging markets shouldconsider when deciding whether, and what kind, of market making system toimplement. These are:

(1) current exchange design and the costs of restructuring;

(2) international and domestic investors’ sentiment towards the exchange;

(3) size of the emerging market; and

(4) the market designs in those countries hosting the target foreign capital.

Empirically, using a dataset of mutual fund holdings invested in 46 countries, we testwhether familiarity with market design is a significant factor affecting foreigninvestors’ intention to invest. While similar to the approach of Chan et al. (2005), weextend their model by including the similarity of the market design between the foreignand domestic markets as a possible predictor. We find that similarity is indeed asignificant factor affecting foreign investors’ decisions to invest in a country.

In addition to providing guidance to capital market regulators in emerging markets,this study is relevant to academic researchers studying the determinants, costs andbenefits of the different market making systems. The paper identifies factors that

Internationalcapital markets

51

explain cross-national variation in market making systems. And it provides evidencethat market design is indeed a significant factor affecting the decisions of foreigninvestors. These findings have implications for theoretical models of optimal marketdesign.

The paper proceeds as follows. Section 2 reviews the market making literature as itapplies to international capital markets. We focus on empirical studies identifying theeffect of market making on the quality of financial markets. Section 3 describes themicrostructure design of seven developed markets with respect to:

. the role of market makers;

. the rights and obligations of market makers; and

. market makers’ fees.

Section 4 critically evaluates the major market making systems and identifies thebenefits and disadvantages of each system. Section 5 prescribes the major factors thatneed to be taken into consideration by emerging market authorities for the efficientimplementation of a market making system in their exchanges. Summary andconclusions are presented in Section 6.

2. Existing literatureNumerous theoretical and empirical studies investigate the role of market makers inthe trading process. Early theoretical work by Garman (1976), Amihud and Mendelson(1980), Kyle (1985), Glosten (1989) and Hasbrouck (1991) identifies the importance ofmarket makers and their effect in the quoted and transaction prices. Recent empiricalstudies have looked at the effect of market making using two distinct approaches. Thefirst approach is that of a natural experiment which investigates market qualitychanges within exchanges following the introduction of market makers. The secondgroup of studies is a cross-sectional comparison of market quality in exchanges withand without market making systems.

The first category of studies includes mainly a description of European exchangesthat have recently undergone a restructuring process. Nimalendran and Petrella (2003)look at the introduction of the market making system in the Italian Stock Exchangeequity trading process. Investigating different market quality measures before andafter the implementation of the system, the authors find that the market has becomemore efficient. In particular, looking at the volume, spread and liquidity (depth of themarket), they find that the introduction of market makers has substantially improvedliquidity, increased trading volume and lowered the bid-ask spread (cost of trading) ofeach individual instrument. Evidence shows that this improvement is greater for lowtrading (illiquid) stocks. Venkataraman and Waisburd (2007) reach similar conclusionsfor the Euronext Paris. However, they fail to identify a similar effect for highly liquidstocks. These stocks are shown to be unchanged for the daily market turnover beforeand after the restructuring of the system.

Moving beyond European exchanges, Anand and Weaver (2006) look at theintroduction of the specialist system for equity options on the Chicago Board ofOptions Exchange (CBOE)[4]. In 1999, the exchange superimposed the specialistsystem – with the introduction of the Designated Primary Market Makers – to theexisting dealer system that employed multiple market makers. Evidence shows thatthe specialist system improved the spread (both quoted and effective) and the depth of

IJMF5,1

52

the market. In addition, the CBOE gained market share from the other majorcompetitor, the AMEX option exchange.

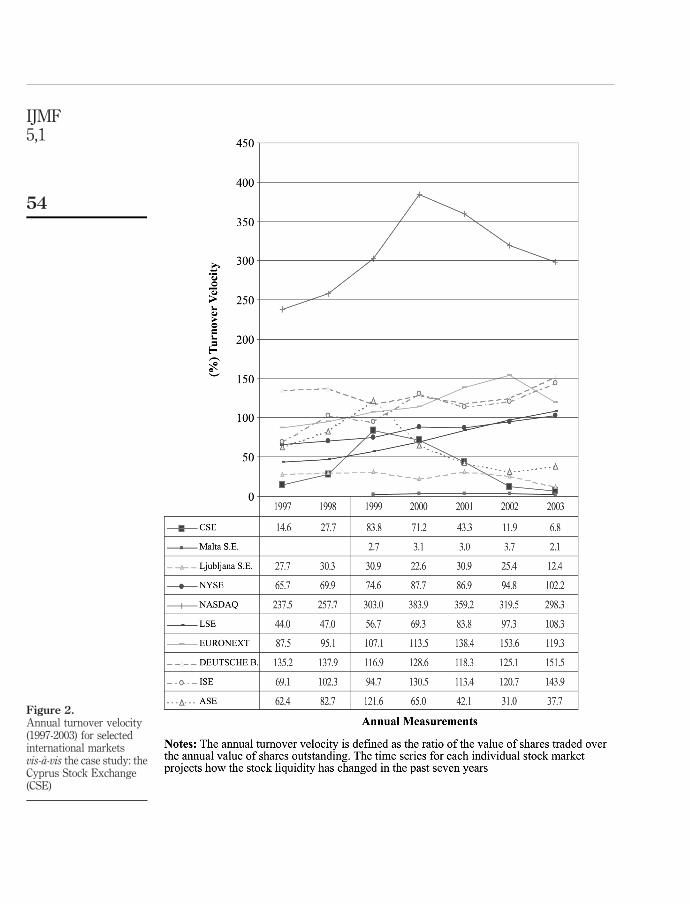

In sum, studies find substantial evidence that market makers serve as liquidityproviders in developed markets. Our study (Figures 1 and 2) shows that a majorproblem in emerging markets is low liquidity and low daily turnover. Thus, byinvestigating the implementation of market making in emerging markets, we provide aconnection between the particular needs of these markets and the advantages of themarket making system. To our knowledge, there is no other study to date thatexamines market making in developing countries, either empirically or theoretically[5].

There are, of course, numerous comparative studies of market design in differentexchanges. Westerholm et al. (2003) examine the three existing models of trading(continuous quote driven, order-driven, and periodic auctions that can either bequote-driven or order-driven) in 32 exchanges. Their results indicate that the existenceof a market making system can lead to lower price volatility and to lower transactioncosts than pure order driven systems. Furthermore, Jain (2003), who examined themarket structure of 51 stock exchanges, finds that market makers can significantlyimprove stock liquidity. Interestingly enough, he finds that this effect, and in particularthe reduction of transaction costs, is more pronounced in less liquid emerging marketscompared to that in more developed markets. Our study builds on this important resultand looks at the way emerging markets can restructure their design effectively in orderto benefit from the market quality that the market making system provides, whileavoiding the undesirable effects (i.e. higher transaction costs, collusion in dealermarkets) that might appear with the application of the new system.

There are also a number of studies that investigate the market quality of the twolargest capital stock exchanges, namely the NYSE (order driven system with a marketmaker) and NASDAQ (quote driven system). Bennett and Wei (2006) look at recentlisting switches of companies from NASDAQ to NYSE and find significant reductionsin return volatilities and price reversals, quoted spreads, and trading costs. In addition,Bessembinder (1999) looks at the transaction costs between the two markets and findsevidence that the market making system at the NASDAQ market is more costly[6].

Figure 1.Average monthly turnover

velocity (January-June2003) for selected

international stockmarkets

Internationalcapital markets

53

Figure 2.Annual turnover velocity(1997-2003) for selectedinternational marketsvis-a-vis the case study: theCyprus Stock Exchange(CSE)

IJMF5,1

54

Bessembinder and Kaufman (1997) and Huang and Stoll (1996b) also investigateexecution costs between the two large exchanges and find that NASDAQ is twice ascostly. Moreover, Christie and Schultz (1994) find collusion among market makers inthe NASDAQ market.

In summary, existing literature has identified several advantages of theimplementation of market making systems, namely improvements in liquidity,increases in trading volume and reductions in the bid-ask spreads. Interestingly,evidence suggests that these improvements are greater for low trading (illiquid)companies. Since stocks in emerging markets are mostly illiquid, the introduction of amarket making system may provide similar benefits to these markets. However, itshould be noted that possible disadvantages might also be related to theimplementation of market making systems[7]. Knowledge of such disadvantages isimportant, as it can determine which market making system should be implemented ina particular emerging market.

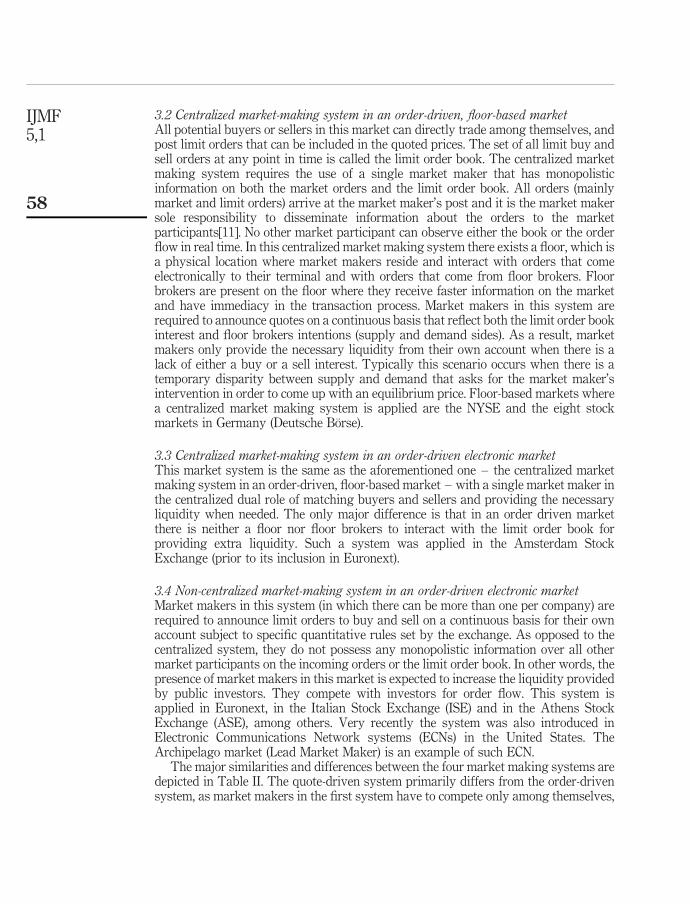

3. Market making in international marketsFinancial intermediaries have played a significant role in the stock market design inthe USA and Germany since the inception of stock markets in the nineteenth century.Even in today’s electronic era, market makers continue to be widely used in one form oranother as liquidity providers, stabilizers and order managers of the market.

Initial investigation regarding international capital markets showed that marketmaking is applied (or is considered for application) in the majority of the stock marketsthat we have examined. Table I depicts 30 stock markets in 29 countries (column 1). Itincludes 20 developed markets in North America, Europe and Asia, and ten emergingmarkets, most of which are European. This table also presents the marketcapitalization of each exchange (column 3), the trading system applied in that market(column 4) and whether market making is applied in their equities’ market (column 5).In addition column 5 shows the number of market makers per company. We observethat internationally the vast majority of developed countries implement marketmaking systems in their capital markets[8].

We proceed to classify market making systems into four categories based on marketmakers’ characteristics and trading design (Westerholm et al., 2003; Jain, 2003)[9].

3.1 Market making (dealer) system in a quote-driven, electronic marketIn this market, public investors generally cannot trade directly among themselves. Inorder for buyers (sellers) to execute an order they have to contact a market maker(dealer) who uses his/her own inventory in the transaction. In a quote-driven systemthere is more than one market maker per company who announces on a continuousbasis quotes to buy and sell a number of shares at a particular price[10]. In aquote-driven system, dealers (market makers) offer almost all the liquidity in themarket as they monopolize one side of the transaction with their quotes. At the sametime they compete among themselves for more competitive bid and/or ask prices thatwill attract the order flow from public investors. Stock markets that apply this systemare the NASDAQ and the London Stock Exchange (LSE).

Internationalcapital markets

55

Cou

ntr

ies

Sto

ckm

ark

et

Mar

ket

cap

ital

izat

ion

(mil

lion

sof

$as

ofJa

nu

ary

2003

)T

yp

eof

mar

ket

Nu

mb

erof

mar

ket

mak

ers

North

America

Un

ited

Sta

tes

New

Yor

kS

tock

Ex

chan

ge

8,77

9,48

5O

rder

dri

ven

floo

r-b

ased

mar

ket

On

e

Un

ited

Sta

tes

NA

SD

AQ

1,93

2,02

6Q

uot

ed

riv

enel

ectr

onic

mar

ket

At

leas

ton

e(m

inim

um

ofth

ree

for

new

issu

es)

Can

ada

Tor

onto

Sto

ckE

xch

ang

e59

2,58

0O

rder

dri

ven

elec

tron

icm

ark

etO

ne

Europe

Un

ited

Kin

gd

omL

ond

onS

tock

Ex

chan

ge

1,66

6,05

4Q

uot

ed

riv

enel

ectr

onic

mar

ket

(tra

dit

ion

al)

At

leas

ton

e

Ord

erd

riv

enel

ectr

onic

mar

ket

(SE

TS

)N

one

Ger

man

yD

euts

che

Bor

se67

7,93

4O

rder

dri

ven

floo

r-b

ased

mar

ket

(tra

dit

ion

al)

On

e

Ord

erd

riv

enel

ectr

onic

mar

ket

(Xet

ra)

Pos

sib

ilit

yof

one

orm

ore

Fra

nce

Eu

ron

ext

Par

is1,

508,

127

Ord

erd

riv

enel

ectr

onic

mar

ket

Pos

sib

ilit

yof

one

orm

ore

Th

eN

eth

erla

nd

sE

uro

nex

tA

mst

erd

am1,

508,

127

Ord

erd

riv

enel

ectr

onic

mar

ket

Pos

sib

ilit

yof

one

orm

ore

Bel

giu

mE

uro

nex

tB

russ

els

1,50

8,12

7O

rder

dri

ven

elec

tron

icm

ark

etP

ossi

bil

ity

ofon

eor

mor

eP

ortu

gal

Eu

ron

ext

Lis

bon

1,50

8,12

7O

rder

dri

ven

elec

tron

icm

ark

etP

ossi

bil

ity

ofon

eor

mor

eS

pai

nM

adri

dS

tock

Ex

chan

ge

474,

246

Ord

erd

riv

enel

ectr

onic

mar

ket

Pos

sib

ilit

yof

one

orm

ore

Ital

yIt

alia

nS

tock

Ex

chan

ge

471,

492

Ord

erd

riv

enel

ectr

onic

mar

ket

At

mos

ton

eG

reec

eA

then

sS

tock

Ex

chan

ge

65,7

92O

rder

dri

ven

elec

tron

icm

ark

etP

ossi

bil

ity

ofon

eor

mor

eD

enm

ark

Cop

enh

agen

Sto

ckE

xch

ang

e74

,956

Ord

erd

riv

enel

ectr

onic

mar

ket

Pos

sib

ilit

yof

one

orm

ore

Au

stri

aW

ien

erB

orse

26,3

74O

rder

dri

ven

elec

tron

icm

ark

etO

ne

Fin

lan

dH

elsi

nk

iSto

ckE

xch

ang

e12

9,00

0O

rder

dri

ven

elec

tron

icm

ark

etA

tm

ost

one

Nor

way

Osl

oS

tock

Ex

chan

ge

65,6

70O

rder

dri

ven

elec

tron

icm

ark

etP

ossi

bil

ity

ofon

eor

mor

eS

wit

zerl

and

Sw

iss

Sto

ckE

xch

ang

e52

2,31

1O

rder

dri

ven

elec

tron

icm

ark

etP

ossi

bil

ity

ofon

eor

mor

eIc

elan

dIc

elan

dS

tock

Ex

chan

ge

7,02

9O

rder

dri

ven

elec

tron

icm

ark

etN

one

Asia

Jap

anT

oky

oS

tock

Ex

chan

ge

2,01

6,27

7O

rder

dri

ven

elec

tron

icm

ark

etN

one

(continued

)

Table I.Market makinginvestigation ininternational equitymarkets

IJMF5,1

56

Cou

ntr

ies

Sto

ckm

ark

et

Mar

ket

cap

ital

izat

ion

(mil

lion

sof

$as

ofJa

nu

ary

2003

)T

yp

eof

mar

ket

Nu

mb

erof

mar

ket

mak

ers

Isra

elT

el-A

viv

Sto

ckE

xch

ang

e40

,667

Ord

erd

riv

enel

ectr

onic

mar

ket

Non

e

Hon

gK

ong

Hon

g-K

ong

Sto

ckE

xch

ang

e46

4,36

6O

rder

dri

ven

elec

tron

icm

ark

etN

one

Emergingmarkets(recentlyjoined

theEuropeanUnion)

Pol

and

War

saw

Sto

ckE

xch

ang

e26

,315

Ord

erd

riv

enel

ectr

onic

mar

ket

At

leas

ton

e

Cze

chR

epu

bli

cP

rag

ue

Sto

ckE

xch

ang

e11

,148

Ord

erd

riv

enel

ectr

onic

mar

ket

At

leas

ton

e

Slo

vak

iaL

jub

ljan

aS

tock

Ex

chan

ge

5,72

4O

rder

dri

ven

elec

tron

icm

ark

etN

one

Mal

taM

alta

Sto

ckE

xch

ang

e1,

413

Ord

erd

riv

enel

ectr

onic

mar

ket

Non

eE

ston

iaE

ston

ian

Sto

ckE

xch

ang

e2,

511

Ord

erd

riv

enel

ectr

onic

mar

ket

At

mos

ton

e

Cy

pru

sC

yp

rus

Sto

ckE

xch

ang

e4.

726

Ord

erd

riv

enel

ectr

onic

mar

ket

Non

e

Other

emergingmarkets

Eg

yp

tC

airo

Sto

ckE

xch

ang

e42

,822

Ord

erd

riv

enel

ectr

onic

mar

ket

Non

eT

urk

eyIn

stan

bu

lS

tock

Ex

chan

ge

36,6

05O

rder

dri

ven

elec

tron

icm

ark

etN

one

Ind

iaB

omb

ayS

tock

Ex

chan

ge

119,

714

Ord

erd

riv

enel

ectr

onic

mar

ket

Non

e

Notes:

Th

ista

ble

show

sth

em

ark

etd

esig

nof

30st

ock

mar

ket

sin

29co

un

trie

su

nd

erin

ves

tig

atio

nw

ith

resp

ect

toM

ark

etM

akin

g.

Inp

arti

cula

r,w

ep

rese

nt

info

rmat

ion

for

thre

em

ajor

stoc

km

ark

ets

inN

orth

Am

eric

a,12

Eu

rop

ean

Un

ion

(EU

)co

un

trie

san

dtw

om

ajor

stoc

km

ark

ets

inA

sia.

Ad

dit

ion

ally

,we

inv

esti

gat

eth

em

ark

etst

ruct

ure

ofte

nem

erg

ing

mar

ket

s,si

xof

wh

ich

hav

ere

cen

tly

join

edth

eE

U.E

ach

mar

ket

isch

arac

teri

zed

wit

hre

spec

tto

the

typ

eof

mar

ket

-mak

ing

syst

emu

sed

,i.e

.as

Flo

or-b

ased

mar

ket

,E

lect

ron

icm

ark

etor

Qu

ote-

dri

ven

mar

ket

(Col

um

n4)

.In

add

itio

nth

en

um

ber

ofm

ark

etm

aker

su

sed

inea

chco

un

try

(col

um

n5)

also

char

acte

rize

the

mar

ket

Table I.

Internationalcapital markets

57

3.2 Centralized market-making system in an order-driven, floor-based marketAll potential buyers or sellers in this market can directly trade among themselves, andpost limit orders that can be included in the quoted prices. The set of all limit buy andsell orders at any point in time is called the limit order book. The centralized marketmaking system requires the use of a single market maker that has monopolisticinformation on both the market orders and the limit order book. All orders (mainlymarket and limit orders) arrive at the market maker’s post and it is the market makersole responsibility to disseminate information about the orders to the marketparticipants[11]. No other market participant can observe either the book or the orderflow in real time. In this centralized market making system there exists a floor, which isa physical location where market makers reside and interact with orders that comeelectronically to their terminal and with orders that come from floor brokers. Floorbrokers are present on the floor where they receive faster information on the marketand have immediacy in the transaction process. Market makers in this system arerequired to announce quotes on a continuous basis that reflect both the limit order bookinterest and floor brokers intentions (supply and demand sides). As a result, marketmakers only provide the necessary liquidity from their own account when there is alack of either a buy or a sell interest. Typically this scenario occurs when there is atemporary disparity between supply and demand that asks for the market maker’sintervention in order to come up with an equilibrium price. Floor-based markets wherea centralized market making system is applied are the NYSE and the eight stockmarkets in Germany (Deutsche Borse).

3.3 Centralized market-making system in an order-driven electronic marketThis market system is the same as the aforementioned one – the centralized marketmaking system in an order-driven, floor-based market – with a single market maker inthe centralized dual role of matching buyers and sellers and providing the necessaryliquidity when needed. The only major difference is that in an order driven marketthere is neither a floor nor floor brokers to interact with the limit order book forproviding extra liquidity. Such a system was applied in the Amsterdam StockExchange (prior to its inclusion in Euronext).

3.4 Non-centralized market-making system in an order-driven electronic marketMarket makers in this system (in which there can be more than one per company) arerequired to announce limit orders to buy and sell on a continuous basis for their ownaccount subject to specific quantitative rules set by the exchange. As opposed to thecentralized system, they do not possess any monopolistic information over all othermarket participants on the incoming orders or the limit order book. In other words, thepresence of market makers in this market is expected to increase the liquidity providedby public investors. They compete with investors for order flow. This system isapplied in Euronext, in the Italian Stock Exchange (ISE) and in the Athens StockExchange (ASE), among others. Very recently the system was also introduced inElectronic Communications Network systems (ECNs) in the United States. TheArchipelago market (Lead Market Maker) is an example of such ECN.

The major similarities and differences between the four market making systems aredepicted in Table II. The quote-driven system primarily differs from the order-drivensystem, as market makers in the first system have to compete only among themselves,

IJMF5,1

58

whereas in the order-driven systems public investors provide substantial competitionfor order flow. The role and the number of the market makers divide the centralizedand non-centralized systems. The monopoly of information and the continuousannouncement of quotes that represent a fair and orderly market are the characteristicsof the single market maker in the centralized system, whereas one or more marketmakers in the non-centralized system act as mere liquidity providers submitting limitorders continuously for their own account. The existence of floor brokers distinguishesthe last two systems: the centralized floor-based and the centralized electronic marketmaking systems.

Dealer system in aquote-driven electronicmarket

Non-centralized MMsystem in anorder-driven electronicmarket

Centralized MM systemin an order-drivenelectronic market

Centralized MM systemin an order- drivenfloor-based market

Market makers compete(mainly) among oneanother for the orderflow from investors.Investors cannot tradeamong themselves, as adealer is the principalbuyer or seller for eachtransaction (usinghis/her own inventory)

Market makers compete with public investors that act as liquidity providersalong with market makers when submitting limit orders. A transactionusually has public investors – as both buyers and sellers. These investorsact through brokers or through electronically submitted orders

One or more marketmakers submit theirquotes using their owninventory on acontinuous basis. Theonly regulations theyhave to follow arequantitative rules withrespect to the minimumamount of their quotedepth and theirmaximum spread

Only one market maker per company acts as amanager or auctioneer matching buyers andsellers. The quotes that she submits usuallyrepresent the best orders in the limit order book.She is only adding personal orders to buy and sellwhen the book does not provide enough liquidity.The regulations that the market maker followsdescribe the way in which she provides a fair andorderly market when announcing the quotes usingthe investors’ demand and supply

There is no floor andthere are no floorbrokers standing by themarket maker’s post.All the orders comeelectronically to themarket maker’s limitorder book. The marketmaker is the managermatching electronicbuyers and sellers

The floor of theexchange is the venuewhere floor brokers cannegotiate deals moreefficiently withoutdisplaying theirintentions to the public.The market maker isthe auctioneer for thefloor brokers’ incomingorders

Note: This summary table describes the major differences and similarities of the four market-makingsystems

Table II.Similarities and

differences of the MMsystems

Internationalcapital markets

59

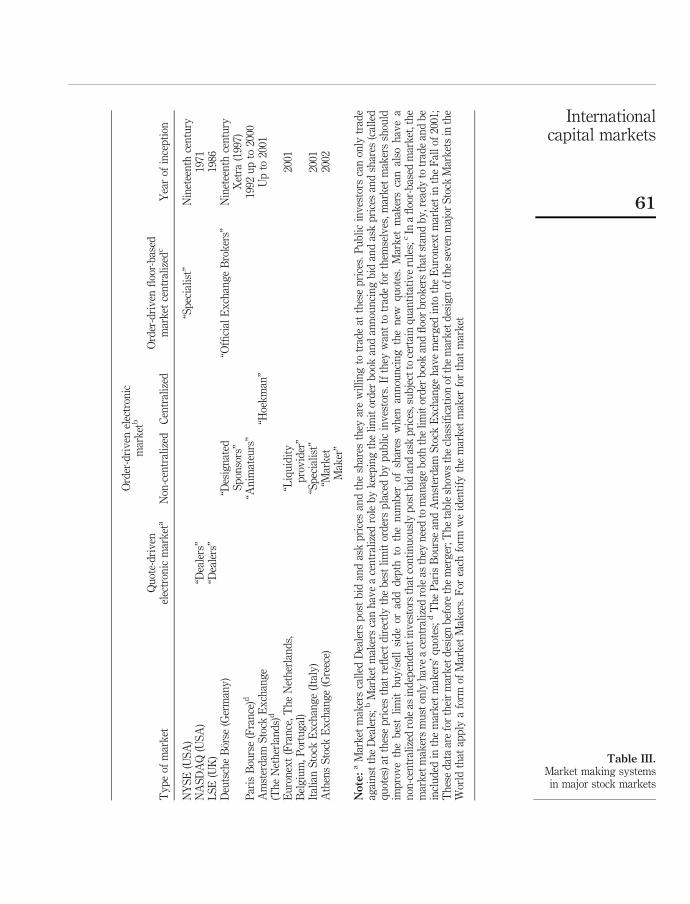

In order to provide guidance to regulators in emerging markets on the introductionof a market making system, we proceed by looking more closely at seven major stockmarkets in nine developed countries that use market-making systems. The choice ofthese markets was based mainly on their economic influence in the internationalmarket scene. By identifying in detail the parameters that characterize the marketmaking design in these stock markets we aim to provide guidance to emerging marketregulators who want to implement such a design. Table III shows these markets andthe particular market making system that is applied. We observe that the NYSEdesign, which is the oldest one, follows the centralized market making system with thespecialist acting as the manager of the limit order book and the provider of a “fair andorderly market”, (NYSE, 1999 Rule 104). This system goes back to the inception of theNYSE in the nineteenth century. Under this system, electronic communication has asecondary role in the functioning of the market[12]. In the USA, there exists also theNASDAQ market, introduced in 1971. Its trading system is based on the quote-drivenelectronic market. This market making system was also applied in the London StockExchange since the 1981 “big bang” reform.

Similar to the NYSE, the German Deutsche Borse has a long history of centralizedmarket making. All eight stock markets of the Deutsche Borse have a floor and acentralized market maker, the “Official Exchange Broker” (formerly “Kursmakler”).Germany is also host to a second market making system, the Xetra market. Thiselectronic market is a non-centralized system, with the Designated Sponsors (formerly“Betreuers”) acting as the market makers. The new system in Germany absorbs themajority of the electronic orders (as opposed to the orders that are handled by floorbrokers), as 90 per cent of the DAX index orders and 80 per cent of all orders flowthrough Xetra. This form of market making is also applied by Euronext (liquidityprovider), the Italian Stock Exchange (specialist) and the Athens Stock Exchange(market maker). Moreover, prior to 2001 the Amsterdam Stock Exchange was using thecentralized market making system in an order-driven electronic market with the“Hoekman” acting as the human intermediary responsible for all orders that werearriving to his/her terminal electronically[13].

Certain characteristics of different market making systems that should be takenseriously into consideration by regulatory bodies when redesigning their marketsrelate to:

. the obligations and privileges of market makers; and

. the market maker’s profits and the determination of those profits in eachsystem[14].

These characteristics are important elements to the functionality of the market makingsystem.

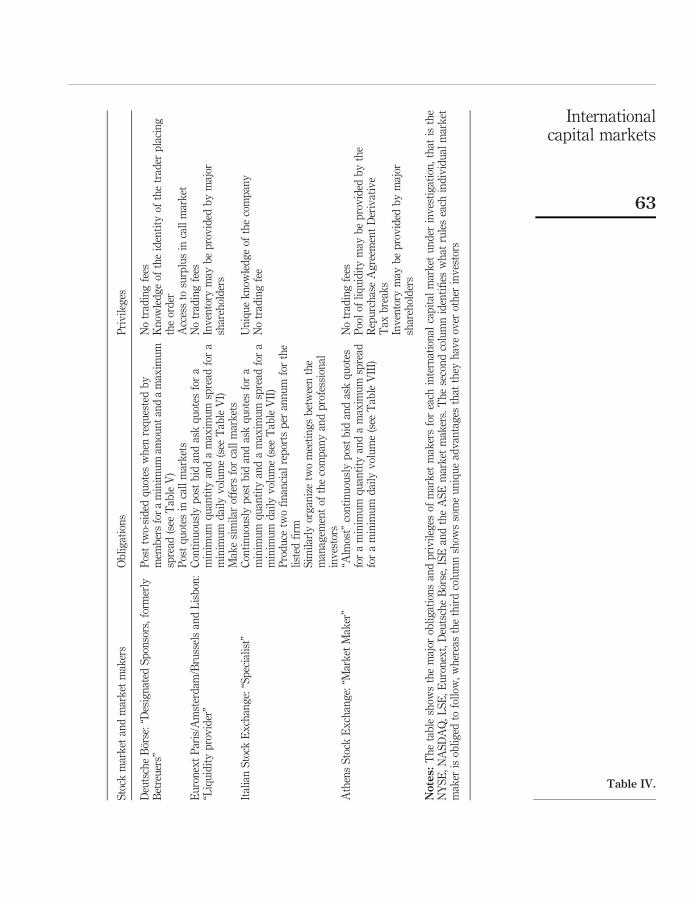

Table IV presents the major obligations and privileges of the market makers in theseven developed markets under investigation. In the quote-driven market (NASDAQ,LSE), market makers (dealers) are obliged to continuously post bid and ask forreasonable spread and trade with either other dealers or investors who post limit ormarket orders exclusively. Their bid (ask) prices can never be greater (less) than theask (bid) price of all the other dealers for that security. Dealers in quote-driven systemsdo not pay any trading fees. In addition, they have the privilege to set bid and askquotes to attract trades on only one side of the spread and thus limit their exposure to

IJMF5,1

60

Ord

er-d

riv

enel

ectr

onic

mar

ket

b

Ty

pe

ofm

ark

etQ

uot

e-d

riv

enel

ectr

onic

mar

ket

aN

on-c

entr

aliz

edC

entr

aliz

edO

rder

-dri

ven

floo

r-b

ased

mar

ket

cen

tral

ized

cY

ear

ofin

cep

tion

NY

SE

(US

A)

“Sp

ecia

list

”N

inet

een

thce

ntu

ryN

AS

DA

Q(U

SA

)“D

eale

rs”

1971

LS

E(U

K)

“Dea

lers

”19

86D

euts

che

Bor

se(G

erm

any

)“D

esig

nat

edS

pon

sors

”“O

ffici

alE

xch

ang

eB

rok

ers”

Nin

etee

nth

cen

tury

Xet

ra(1

997)

Par

isB

ours

e(F

ran

ce)d

“An

imat

eurs

”19

92u

pto

2000

Am

ster

dam

Sto

ckE

xch

ang

e(T

he

Net

her

lan

ds)

d“H

oek

man

”U

pto

2001

Eu

ron

ext

(Fra

nce

,T

he

Net

her

lan

ds,

Bel

giu

m,

Por

tug

al)

“Liq

uid

ity

pro

vid

er”

2001

Ital

ian

Sto

ckE

xch

ang

e(I

taly

)“S

pec

iali

st”

2001

Ath

ens

Sto

ckE

xch

ang

e(G

reec

e)“M

ark

etM

aker

”20

02

Note:

aM

ark

etm

aker

sca

lled

Dea

lers

pos

tb

idan

das

kp

rice

san

dth

esh

ares

they

are

wil

lin

gto

trad

eat

thes

ep

rice

s.P

ub

lic

inv

esto

rsca

non

lytr

ade

agai

nst

the

Dea

lers

;bM

ark

etm

aker

sca

nh

ave

ace

ntr

aliz

edro

leb

yk

eep

ing

the

lim

itor

der

boo

kan

dan

nou

nci

ng

bid

and

ask

pri

ces

and

shar

es(c

alle

dq

uot

es)

atth

ese

pri

ces

that

refl

ect

dir

ectl

yth

eb

est

lim

itor

der

sp

lace

db

yp

ub

lic

inv

esto

rs.

Ifth

eyw

ant

totr

ade

for

them

selv

es,

mar

ket

mak

ers

shou

ldim

pro

ve

the

bes

tli

mit

bu

y/s

ell

sid

eor

add

dep

thto

the

nu

mb

erof

shar

esw

hen

ann

oun

cin

gth

en

ewq

uot

es.

Mar

ket

mak

ers

can

also

hav

ea

non

-cen

tral

ized

role

asin

dep

end

ent

inv

esto

rsth

atco

nti

nu

ousl

yp

ost

bid

and

ask

pri

ces,

sub

ject

toce

rtai

nq

uan

tita

tiv

eru

les;

cIn

afl

oor-

bas

edm

ark

et,t

he

mar

ket

mak

ers

mu

ston

lyh

ave

ace

ntr

aliz

edro

leas

they

nee

dto

man

age

bot

hth

eli

mit

ord

erb

ook

and

floo

rb

rok

ers

that

stan

db

y,r

ead

yto

trad

ean

db

ein

clu

ded

inth

em

ark

etm

aker

s’q

uot

es;d

Th

eP

aris

Bou

rse

and

Am

ster

dam

Sto

ckE

xch

ang

eh

ave

mer

ged

into

the

Eu

ron

ext

mar

ket

inth

eF

all

of20

01;

Th

ese

dat

aar

efo

rth

eir

mar

ket

des

ign

bef

ore

the

mer

ger

;Th

eta

ble

show

sth

ecl

assi

fica

tion

ofth

em

ark

etd

esig

nof

the

sev

enm

ajor

Sto

ckM

ark

ets

inth

eW

orld

that

app

lya

form

ofM

ark

etM

aker

s.F

orea

chfo

rmw

eid

enti

fyth

em

ark

etm

aker

for

that

mar

ket

Table III.Market making systemsin major stock markets

Internationalcapital markets

61

Sto

ckm

ark

etan

dm

ark

etm

aker

sO

bli

gat

ion

sP

riv

ileg

es

NY

SE

:“S

pec

iali

sts”

Con

tin

uou

sly

pos

tb

idan

das

kq

uot

esth

atar

eeq

ual

toor

bet

ter

than

the

bes

tli

mit

ord

erb

ook

ord

ers

Ad

dto

the

boo

kq

uot

esp

rice

s,an

dtr

ade

wh

enth

ere

isin

suffi

cien

tor

der

flow

orw

hen

they

are

acti

ng

asan

agen

tto

floo

rtr

ader

sD

eter

min

eth

eop

enin

gp

rice

.M

ain

tain

afa

iran

dor

der

lym

ark

et

Un

iqu

ek

now

led

ge

ofth

eli

mit

ord

erb

ook

Per

cen

tag

efe

ew

hen

acti

ng

asan

agen

tfo

rfl

oor

bro

ker

sU

niq

ue

pos

itio

nN

otr

adin

gfe

es

NA

SD

AQ

:“D

eale

rs”

Con

tin

uou

sly

pos

tb

idan

das

kq

uot

esof

reas

onab

lesp

read

and

trad

ew

ith

eith

erot

her

dea

lers

orin

ves

tors

wh

op

ost

lim

itor

mar

ket

ord

ers

excl

usi

vel

yT

he

bid

(ask

)p

rice

sca

nn

ever

be

gre

ater

(les

s)th

anth

eas

k(b

id)

ofal

lth

eot

her

dea

lers

inth

ese

curi

ty

No

trad

ing

fees

;se

tb

idan

das

kq

uot

esto

attr

act

trad

eson

only

one

sid

eof

the

spre

ad;

thu

sli

mit

thei

rex

pos

ure

tou

nw

ante

din

ven

tory

pos

itio

ns.

Rel

ativ

ely

con

stan

tco

mp

etit

ion

for

ord

erfl

owfr

omm

ain

lyth

eot

her

dea

lers

.L

imit

ord

ers

are

not

asfr

equ

ent

orco

mp

etit

ive

LS

E:

“Dea

lers

”C

onti

nu

ousl

yp

ost

bid

and

ask

qu

otes

ofre

ason

able

spre

adan

dtr

ade

wit

hei

ther

oth

erd

eale

rsor

inv

esto

rsw

ho

pos

tli

mit

orm

ark

etor

der

sex

clu

siv

ely

No

trad

ing

fees

;se

tb

idan

das

kq

uot

esto

attr

act

trad

eson

only

one

sid

eof

the

spre

ad;

thu

sli

mit

thei

rex

pos

ure

tou

nw

ante

din

ven

tory

pos

itio

ns.

Rel

ativ

ely

con

stan

tco

mp

etit

ion

for

ord

erfl

owfr

omm

ain

lyth

eot

her

dea

lers

.L

imit

ord

ers

are

not

asfr

equ

ent

orco

mp

etit

ive.

Deu

tsch

eB

orse

:“O

ffici

alE

xch

ang

eB

rok

ers,

form

erly

Ku

rsm

akle

rs”

Con

tin

uou

sly

pos

tb

idan

das

kq

uot

esth

atar

eeq

ual

toor

bet

ter

than

the

bes

tli

mit

ord

erb

ook

ord

ers

Ad

dto

the

boo

kq

uot

esp

rice

san

dtr

ade

wh

enth

ere

isin

suffi

cien

tor

der

flow

orw

hen

they

are

acti

ng

asan

agen

tto

floo

rtr

ader

sD

eter

min

eth

eop

enin

gp

rice

Un

iqu

ek

now

led

ge

ofth

eli

mit

ord

erb

ook

Per

cen

tag

efe

ew

hen

acti

ng

asan

agen

tfo

rfl

oor

bro

ker

sU

niq

ue

pos

itio

nN

otr

adin

gfe

es

(continued

)

Table IV.Market makers’obligations and privileges

IJMF5,1

62

Sto

ckm

ark

etan

dm

ark

etm

aker

sO

bli

gat

ion

sP

riv

ileg

es

Deu

tsch

eB

orse

:“D

esig

nat

edS

pon

sors

,fo

rmer

lyB

etre

uer

s”P

ost

two-

sid

edq

uot

esw

hen

req

ues

ted

by

mem

ber

sfo

ra

min

imu

mam

oun

tan

da

max

imu

msp

read

(see

Tab

leV

)P

ost

qu

otes

inca

llm

ark

ets

No

trad

ing

fees

Kn

owle

dg

eof

the

iden

tity

ofth

etr

ader

pla

cin

gth

eor

der

Acc

ess

tosu

rplu

sin

call

mar

ket

Eu

ron

ext

Par

is/A

mst

erd

am/B

russ

els

and

Lis

bon

:“L

iqu

idit

yp

rov

ider

”C

onti

nu

ousl

yp

ost

bid

and

ask

qu

otes

for

am

inim

um

qu

anti

tyan

da

max

imu

msp

read

for

am

inim

um

dai

lyv

olu

me

(see

Tab

leV

I)M

ake

sim

ilar

offe

rsfo

rca

llm

ark

ets

No

trad

ing

fees

Inv

ento

rym

ayb

ep

rov

ided

by

maj

orsh

areh

old

ers

Ital

ian

Sto

ckE

xch

ang

e:“S

pec

iali

st”

Con

tin

uou

sly

pos

tb

idan

das

kq

uot

esfo

ra

min

imu

mq

uan

tity

and

am

axim

um

spre

adfo

ra

min

imu

md

aily

vol

um

e(s

eeT

able

VII

)P

rod

uce

two

fin

anci

alre

por

tsp

eran

nu

mfo

rth

eli

sted

firm

Sim

ilar

lyor

gan

ize

two

mee

tin

gs

bet

wee

nth

em

anag

emen

tof

the

com

pan

yan

dp

rofe

ssio

nal

inv

esto

rs

Un

iqu

ek

now

led

ge

ofth

eco

mp

any

No

trad

ing

fee

Ath

ens

Sto

ckE

xch

ang

e:“M

ark

etM

aker

”“A

lmos

t”co

nti

nu

ousl

yp

ost

bid

and

ask

qu

otes

for

am

inim

um

qu

anti

tyan

da

max

imu

msp

read

for

am

inim

um

dai

lyv

olu

me

(see

Tab

leV

III)

No

trad

ing

fees

Poo

lof

liq

uid

ity

may

be

pro

vid

edb

yth

eR

epu

rch

ase

Ag

reem

ent

Der

ivat

ive

Tax

bre

aks

Inv

ento

rym

ayb

ep

rov

ided

by

maj

orsh

areh

old

ers

Notes:

Th

eta

ble

show

sth

em

ajor

obli

gat

ion

san

dp

riv

ileg

esof

mar

ket

mak

ers

for

each

inte

rnat

ion

alca

pit

alm

ark

etu

nd

erin

ves

tig

atio

n,

that

isth

eN

YS

E,

NA

SD

AQ

,L

SE

,E

uro

nex

t,D

euts

che

Bor

se,

ISE

and

the

AS

Em

ark

etm

aker

s.T

he

seco

nd

colu

mn

iden

tifi

esw

hat

rule

sea

chin

div

idu

alm

ark

etm

aker

isob

lig

edto

foll

ow,

wh

erea

sth

eth

ird

colu

mn

show

sso

me

un

iqu

ead

van

tag

esth

atth

eyh

ave

over

oth

erin

ves

tors

Table IV.

Internationalcapital markets

63

unwanted inventory positions. Finally, only in a quote-driven system do marketmakers have the advantage of a relatively constant competition for order flow. Thus, incontrast to the order-driven system, limit orders are not the driving force of liquidityand therefore any competition from limit order traders with dealers is minimal and notcompetitive. This competition has direct positive implications for the dealers’ profitsand risks.

In the centralized market making system (NYSE, Deutsche Borse), market makersare obliged to announce on a continuous basis bid and ask quotes that arerepresentative of the best prices in the limit order book (electronic orders) and of theintentions of the floor brokers – reflecting the interest of the market. In addition,whenever there is a disparity of supply and demand, the market makers have to step inand provide the necessary liquidity by announcing bid/ask quotes for their ownaccount. Their role as defined by the NYSE (Rule 104) is to act as providers of a “fairand orderly” market. As such they are obliged to be either the buyer or the seller fororders that otherwise had been defused through the market would have created bigtemporal price fluctuations not representative of the true price of the stock.

Finally, centralized market makers are responsible for announcing the openingprice in any auction trading periods. This is in contrast to the pure order book systemin which the opening price is based on a simple algorithm that maximizes thetransaction volume. As far as privileges are concerned, centralized market makershave monopolistic knowledge of the limit order book. Their unique position on the floorof the exchange allows them to observe both all orders that are entered electronicallyinto the system and the intentions of the floor brokers. Moreover, they are waived ofany trading fees for their own transactions. Finally, they are free to set a fee for allorders that the floor brokers are leaving with them on the floor.

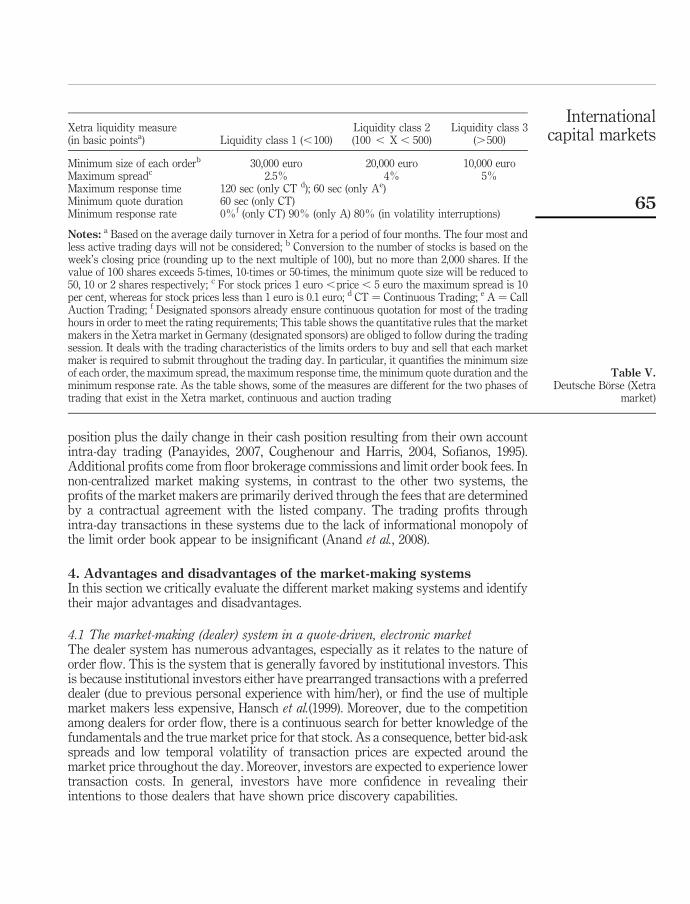

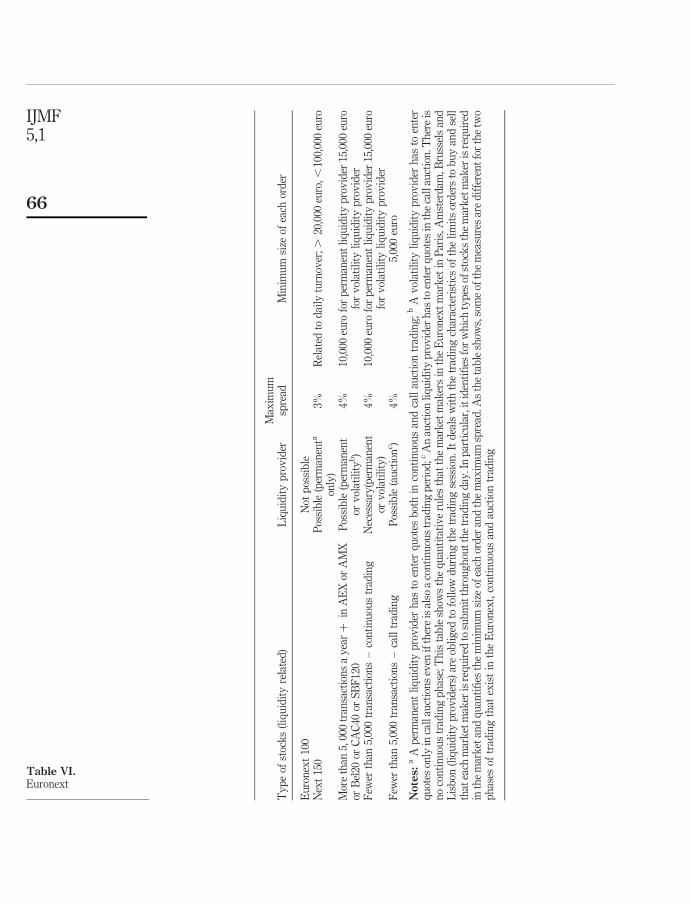

Lastly, in markets that employ the non-centralized market making system(Euronext, Germany’s Xetra market, the Italian Stock Exchange, the Athens StockExchange,) market makers are obliged to continuously enter the system orders to buyor sell for their own account (principal bid and ask quotes) following a clearlyformulated quantitative set of rules. Tables V-VIII present these detailed rules thatrelate to the minimum quantity announced at the quoted prices, the maximum spreadbetween bid and ask prices, the minimum number of transactions intra-daily, and themaximum time between new quote announcements by the market makers. In additionto these quantitative rules, market makers may also be obliged to inform investors ofthe current financial state of their listed company at regularly scheduled yearlyconferences and bi-annual reports (Italian Stock Exchange). Regarding tradingprivileges, in the non-centralized-market making system, market makers have notrading fees. They also enjoy the privileges of having their inventory rebalanced byeither major company shareholders or exchange mechanisms (as in Euronext, AthensStock Exchange), as well as possessing specific knowledge of their company (as in theISE)[15].

In addition to the aforementioned obligations and possible penalties of the marketmakers, evidence shows that profits differ between the non-centralized and thecentralized and quote-driven market making systems. Specifically, for both thecentralized and quote-driven market making systems, the market makers’ profits relateprimarily to intra-day transactions. In particular, empirical studies have shown thatthe main profits come primarily from the daily change in the market makers’ inventory

IJMF5,1

64

position plus the daily change in their cash position resulting from their own accountintra-day trading (Panayides, 2007, Coughenour and Harris, 2004, Sofianos, 1995).Additional profits come from floor brokerage commissions and limit order book fees. Innon-centralized market making systems, in contrast to the other two systems, theprofits of the market makers are primarily derived through the fees that are determinedby a contractual agreement with the listed company. The trading profits throughintra-day transactions in these systems due to the lack of informational monopoly ofthe limit order book appear to be insignificant (Anand et al., 2008).

4. Advantages and disadvantages of the market-making systemsIn this section we critically evaluate the different market making systems and identifytheir major advantages and disadvantages.

4.1 The market-making (dealer) system in a quote-driven, electronic marketThe dealer system has numerous advantages, especially as it relates to the nature oforder flow. This is the system that is generally favored by institutional investors. Thisis because institutional investors either have prearranged transactions with a preferreddealer (due to previous personal experience with him/her), or find the use of multiplemarket makers less expensive, Hansch et al.(1999). Moreover, due to the competitionamong dealers for order flow, there is a continuous search for better knowledge of thefundamentals and the true market price for that stock. As a consequence, better bid-askspreads and low temporal volatility of transaction prices are expected around themarket price throughout the day. Moreover, investors are expected to experience lowertransaction costs. In general, investors have more confidence in revealing theirintentions to those dealers that have shown price discovery capabilities.

Xetra liquidity measure(in basic pointsa) Liquidity class 1 (,100)

Liquidity class 2(100 , X , 500)

Liquidity class 3(.500)

Minimum size of each orderb 30,000 euro 20,000 euro 10,000 euroMaximum spreadc 2.5% 4% 5%Maximum response time 120 sec (only CT d); 60 sec (only Ae)Minimum quote duration 60 sec (only CT)Minimum response rate 0%f (only CT) 90% (only A) 80% (in volatility interruptions)

Notes: a Based on the average daily turnover in Xetra for a period of four months. The four most andless active trading days will not be considered; b Conversion to the number of stocks is based on theweek’s closing price (rounding up to the next multiple of 100), but no more than 2,000 shares. If thevalue of 100 shares exceeds 5-times, 10-times or 50-times, the minimum quote size will be reduced to50, 10 or 2 shares respectively; c For stock prices 1 euro ,price , 5 euro the maximum spread is 10per cent, whereas for stock prices less than 1 euro is 0.1 euro; d CT ¼ Continuous Trading; e A ¼ CallAuction Trading; f Designated sponsors already ensure continuous quotation for most of the tradinghours in order to meet the rating requirements; This table shows the quantitative rules that the marketmakers in the Xetra market in Germany (designated sponsors) are obliged to follow during the tradingsession. It deals with the trading characteristics of the limits orders to buy and sell that each marketmaker is required to submit throughout the trading day. In particular, it quantifies the minimum sizeof each order, the maximum spread, the maximum response time, the minimum quote duration and theminimum response rate. As the table shows, some of the measures are different for the two phases oftrading that exist in the Xetra market, continuous and auction trading

Table V.Deutsche Borse (Xetra

market)

Internationalcapital markets

65

Ty

pe

ofst

ock

s(l

iqu

idit

yre

late

d)

Liq

uid

ity

pro

vid

erM

axim

um

spre

adM

inim

um

size

ofea

chor

der

Eu

ron

ext

100

Not

pos

sib

leN

ext

150

Pos

sib

le(p

erm

anen

ta

only

)3%

Rel

ated

tod

aily

turn

over

;.20

,000

euro

,,10

0,00

0eu

ro

Mor

eth

an5,

000

tran

sact

ion

sa

yea

rþ

inA

EX

orA

MX

orB

el20

orC

AC

40or

SB

F12

0P

ossi

ble

(per

man

ent

orv

olat

ilit

yb)

4%10

,000

euro

for

per

man

ent

liq

uid

ity

pro

vid

er15

,000

euro

for

vol

atil

ity

liq

uid

ity

pro

vid

erF

ewer

than

5,00

0tr

ansa

ctio

ns

–co

nti

nu

ous

trad

ing

Nec

essa

ry(p

erm

anen

tor

vol

atil

ity

)4%

10,0

00eu

rofo

rp

erm

anen

tli

qu

idit

yp

rov

ider

15,0

00eu

rofo

rv

olat

ilit

yli

qu

idit

yp

rov

ider

Few

erth

an5,

000

tran

sact

ion

s–

call

trad

ing

Pos

sib

le(a

uct

ion

c )4%

5,00

0eu

ro

Notes:

aA

per

man

ent

liq

uid

ity

pro

vid

erh

asto

ente

rq

uot

esb

oth

inco

nti

nu

ous

and

call

auct

ion

trad

ing

;b

Av

olat

ilit

yli

qu

idit

yp

rov

ider

has

toen

ter

qu

otes

only

inca

llau

ctio

ns

even

ifth

ere

isal

soa

con

tin

uou

str

adin

gp

erio

d;c

An

auct

ion

liq

uid

ity

pro

vid

erh

asto

ente

rq

uot

esin

the

call

auct

ion

.Th

ere

isn

oco

nti

nu

ous

trad

ing

ph

ase;

Th

ista

ble

show

sth

eq

uan

tita

tiv

eru

les

that

the

mar

ket

mak

ers

inth

eE

uro

nex

tm

ark

etin

Par

is,A

mst

erd

am,B

russ

els

and

Lis

bon

(liq

uid

ity

pro

vid

ers)

are

obli

ged

tofo

llow

du

rin

gth

etr

adin

gse

ssio

n.I

td

eals

wit

hth

etr

adin

gch

arac

teri

stic

sof

the

lim

its

ord

ers

tob

uy

and

sell

that

each

mar

ket

mak

eris

req

uir

edto

sub

mit

thro

ug

hou

tth

etr

adin

gd

ay.I

np

arti

cula

r,it

iden

tifi

esfo

rw

hic

hty

pes

ofst

ock

sth

em

ark

etm

aker

isre

qu

ired

inth

em

ark

etan

dq

uan

tifi

esth

em

inim

um

size

ofea

chor

der

and

the

max

imu

msp

read

.As

the

tab

lesh

ows,

som

eof

the

mea

sure

sar

ed

iffe

ren

tfo

rth

etw

op

has

esof

trad

ing

that

exis

tin

the

Eu

ron

ext,

con

tin

uou

san

dau

ctio

ntr

adin

g

Table VI.Euronext

IJMF5,1

66

In contrast, one of the major disadvantages of this system is the dealers’ monopolisticcontrol of the prices of the financial instruments they trade. Since the majority of ordersare traded through the dealers (they are either the buyers or sellers in a transaction),there is evidence that the dealers set quoted prices that are more profitable to them.Studies by Christie and Huang (1994) and Christie and Schultz (1994) led investors totake unprecedented legal actions against dealers and be penalized by the SEC. Theseinstitutional and individual investors were responding to the fact that dealers were notquoting prices in odd ticks of a dollar but rather they preferred to trade in even ticksonly. Bessembinder and Kaufman (1997) also reveal the effects of the even-odd ticksmisconduct when they compare measures of market quality between NASDAQ and

NEHA Main and parallel market

Maximum spread 5 per cent 3 per centMinimum daily quantity 0.5 per cent times shares

outstandingShares outstanding times

one-fifth of the daily averageturnover in the six preceding

monthsMinimum size of eachorder

One-fifth of the minimumdaily quantity

1/30 of the minimum dailyquantity

Maximum time for a neworder to be announced

Five minutes Ten minutes

Notes: This table shows the quantitative rules that the market makers in the Athens Stock Market areobliged to follow during the trading session. It deals with the trading characteristics of the limitsorders to buy and sell that each market maker is required to submit throughout the trading day. Inparticular, in the ASE, the rules are differentiated between two markets, the NEHA market and themain and parallel market. The rules are further quantified with respect to four measures: Themaximum spread of the market maker’s orders, the minimum daily quantity, the minimum size of eachorder and the maximum time for a new order to be announced

Table VIII.Athens Stock Exchange

Daily average turnoveraMinimum daily quantityb

(euro)Maximum spread

(%)Minimum size of each order

(euro)

Up to 150,000 euro 50,000 3.5 2,500 euro150,000-500,000 75,000 3.0 2,500Over 500,000 100,000 2.5 2,500

Notes: a The obligations of the specialist on the market are determined on daily average turnover inthe six preceding months (March-August or September-February) for shares subject to the obligation.For newly-listed companies, the liquidity of shares with equal capitalization is considered; b For eachtrading session, the specialist undertakes to sustain the liquidity of the instrument until the executionof trades, operating as a specialist, for a value at least equal to the minimum daily quantity.Afterwards, the specialist may continue to operate as a specialist on a voluntary basis; This tableshows the quantitative rules that the market makers in the Italian Stock Market (specialists) areobliged to follow during the trading session. It deals with the trading characteristics of the limitsorders to buy and sell that each market maker is required to submit throughout the trading day. InItaly, only companies in the Star market are allowed to use a market maker. For the companies, marketmakers are obliged to follow quantitative rules that are related to the daily trading turnover of thecompany, the minimum daily quantity, the maximum spread and the minimum size of each order

Table VII.Italian Stock Exchange

Internationalcapital markets

67

NYSE. They conclude that the higher transaction costs shown in the NASDAQ marketare partly due to the monopolistic control of quotes by the dealers.

Another disadvantage of this system is the collusion that appears in dealer markets.This collusion may result in severe cost manipulation and lack of competitiveness onone side of the quote. In particular, Hansch et al. (1998) provide evidence that thedealers focus intra-daily only on one side of the quote (either the bid price or ask price)due to either the dealers’ information signals and/or their inventory rebalancing. Thus,they tend to announce misleading quotes that may affect negatively the price discoveryprocess (Barclay, 1997).

4.2 The centralized market-making system in an order-driven, floor-based marketThe centralized system has a number of major advantages that makes it preferable tocertain groups of investors. In particular, this system is attractive to institutionalinvestors that have the ability to transact large orders using the skills of floor brokers.Floor brokers can decide to “work through” an order. They have the knowledge andmeans to get competitive prices for institutional customers without revealing theirintentions to the public and thus avoid creating large price disturbances (Heidle andHuang, 2002). Published reports on floor trading at the NYSE reveal that even if thenumber of trades that are carried over by floor brokers is small compared to electronicorders, the size of these orders represents more than 60 per cent of the daily tradingvolume (Sofianos and Werner, 2000).

Another advantage of this system is that its transaction costs are relatively low.The fact that market makers are expected to step in and add liquidity when there is alarge bid-ask spread from other liquidity investors, results in trading costs that aresignificantly lower than in a pure limit order market. In addition, the market makers’daily interaction with floor brokers, lowers the market makers’ risks in keeping a fairand orderly market. Price-relevant information is disseminated on the floor of theexchange more effectively and that makes market makers less worried of tradingagainst privately informed traders[16].

Numerous studies have compared the NYSE market to other market designs.Bennett and Wei (2006), Bessembinder (1999), Barclay et al. (1998) and Huang and Stoll(1996a, b), among others, showed that the NYSE centralized market making structurehas lower transaction costs than its counterpart, the NASDAQ quote-driven market.Venkataraman (2001) compares the centralized market making system with thepure-order driven system by looking at the CAC40 stocks of the Paris Stock Exchange(before its ascension to Euronext) and compares transaction costs with matching pairsof NYSE stocks. He finds that the NYSE costs are substantially lower and attributesthat to the structural design of the exchanges. In addition, Kehr et al. (2001) look at thecentralized market making system in Germany (Deutsche Borse). They find that theexistence of the market makers minimizes the costs of trading in an auction phase.They also find that market makers smooth prices when the transaction phase changesbetween an auction and continuous phase. Garfinkel and Nimalendran (2003) showthat the degree of anonymity – that is, the extent to which a trader is recognized asinformed or not – is less in the NYSE than in NASDAQ. As we have already discussed,the centralized market making system’s structure creates a unique relationshipbetween the market maker (specialist) and the floor brokers. Battalio et al. (2007)identify empirically the networking behavior that exists on the floor. Such a structure

IJMF5,1

68

leads to a faster dissemination of information on the market participants and to a lowerdegree of anonymity. Heidle and Huang (2002) also find such an effect. They attributethe higher transaction costs (bid-ask spreads) of the NASDAQ market to the higherrisk of transacting with informed traders, a problem that is greatly mitigated by themarket structure of the NYSE.

In contrast with the aforementioned advantages, there are a number of disadvantagesthat are shown empirically in the literature. One of the major disadvantages of thissystem is that it is less transparent to the market participants than either the quotedriven system or the non-centralized system. The centralized position of the specialists(market makers) allows them to have unique knowledge of the market and thus be ableto observe on a continuous basis the supply and demand parity. This may lead to unfairpractices by market makers, practices that lead only to personal gains. For example,recent articles in the financial press have criticized specialists for “front running”[17].The allegations claim that when specialists observe a disparity between supply anddemand in their limit order book, they step ahead on the side of the book that has theprevalence in the disparity and place their own order knowing that once their order isexecuted either the instrument’s price will move in a favorable direction – their order tobuy (sell) is executed and the prices move up (down) – or if not, they have several otherorders waiting so that they can discharge their transaction. This free option, thatespecially the specialists can spot quite easily, has become much cheaper after thedecimalization of the NYSE[18]. The specialists can now “front run” – step ahead of theother orders to buy or sell depending on the disparity – with only a cent cost. Thispractice is also called “penny jumping.” Thus, the problem has been intensified and thepublic and institutional outcry for reform has greatly escalated in recent years[19].

Another disadvantage of this system arises from the fact that market makers in acentralized system have to maintain a fair and orderly market. They are obliged tosmooth transaction price changes when large price fluctuations are pending. This pricecontinuity rule leads to large inventory risks for market makers. In order to adjust forthese risks, market makers move the quoted prices in a direction favorable tothemselves in order to rebalance their position (Panayides, 2007). This practice addssignificant “noise” to the price discovery process and it temporarily masks the truemarket price. Theissen (2002) results are evident of such an effect. He comparesempirically the contribution to price discovery between the centralized system ofDeutsche Borse and its non-centralized Xetra market and finds support that the Xetramarket has a larger share.

4.3 The non-centralized market-making system in an order-driven electronic marketOne of the major advantages of this system is the transparency of the limit order bookto all market participants. In non-centralized markets the limit order book is eitheralmost as visible or equally visible (i.e. transparent) among investors and marketmakers. Thus, there is no monopolistic information of the order flow by either side.Such transparency can lead to lower transaction costs, especially among uninformedinvestors (Pagano and Roell, 1996). At the same time, since market makers have tocontinuously enter the system with limit orders to buy and sell, they provide thenecessary liquidity on a continuous basis and provide the necessary competition onequal terms between themselves and other investors (Nimalendran and Petrella, 2003).This system stands in contrast to both the centralized market making system and the

Internationalcapital markets

69

quote-driven system, where limit orders from the public cannot directly compete withmarket makers’ orders. This is so because market makers have immediacy and moreknowledge of the general market on their side.

Another advantage of this system relates to market making surveillance, as it is lesscostly to regulate. This is because the duties of the market maker in a non-centralizedsystem are predefined in a set of quantified rules (Tables V-VIII) that can beformulated and controlled electronically. In addition, as market makers’ access to themarket in a non-centralized system is only through a terminal similar to any otherinvestor (broker), there is no need for extra technical and human resources to monitortheir trading role.

On the other hand, major disadvantages of this system have been shownempirically in previous research. In particular, the application of this system does notnecessarily provide extra liquidity in the market. The market maker can practicallyavoid trading by providing orders to buy or sell that are non-competitive. Of course,this can only occur when the minimum liquidity available for the stock is alreadysufficient. Venkataraman and Waisburd (2007) show that the application of thenon-centralized market making system in Euronext Paris improved only the liquidityof the low turnover stocks and had no effect on the liquidity of highly traded stocks.

Another disadvantage of this system is that institutional investors do not find thenon-centralized market making system an attractive venue for investing. This isbecause they cannot hide their trading intentions and have to reveal their orders to thewhole market. Any effort to transact large volumes brings unwanted temporary pricefluctuation and “front-runners” that take advantage of the signal that the institutionalinvestors provide.

5. Implementing the market-making systems in emerging marketsIn this section we investigate the major factors that need to be taken into considerationby stock market regulators in developing countries when they consider implementingone of the aforementioned market making systems.